international finance lecture 4. overview common methods to conduct international business....

TRANSCRIPT

INTERNATIONAL FINANCE

Lecture 4

Overview

• Common methods to conduct international business.

• International trade Licensing, Franchising, Joint ventures, Acquisitions of existing operations, Establishing new foreign subsidiaries

Investment opportunities Financing opportunities Marginal Returns and Marginal Costs

• International opportunities in Europe

International Flow of Funds

Lecture 4

Lecture Objectives

Opportunities in Latin America, Europe and Asia

Provide a model for the valuation of MNC.

To explain the key components of the balance of

payments

To explain how the international flow of funds is

influenced by economic factors and other factors.

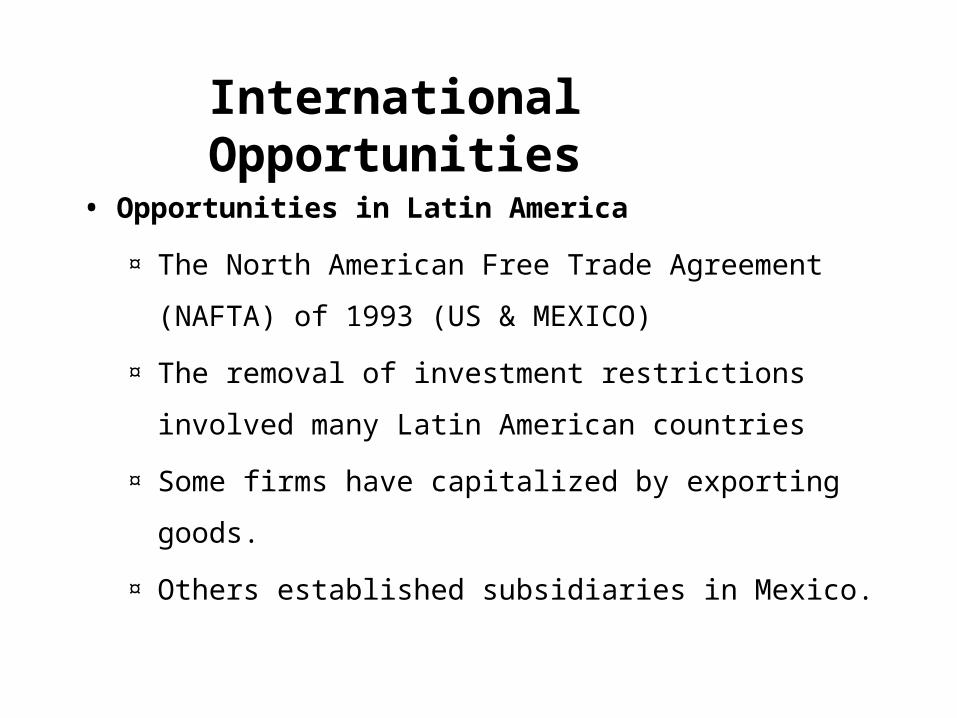

International Opportunities

• Opportunities in Latin America

¤ The North American Free Trade Agreement

(NAFTA) of 1993 (US & MEXICO)

¤ The removal of investment restrictions involved

many Latin American countries

¤ Some firms have capitalized by exporting goods.

¤ Others established subsidiaries in Mexico.

International Opportunities

• Opportunities in Asia

¤ The removal of investment restrictions in

1990s e.g. Pepsi, Coke, Apple , General

Motors, Proctor & Gamble etc.

¤ The impact of the Asian crisis in 1997-1998

(Indonesia, Malaysia & Thailand)

¤ Many companies went bankrupt and faced

capital outflows.

Exposure to International Risk

• International business usually increases an MNC’s exposure to:

exchange rate movements

foreign economies

political risk

Exchange Rate Movements

• Exchange of one currency in another to make payments

• Exchange rates fluctuate over time

• When a currency strengthens/ appreciates; products denominated in that currency becomes expensive to foreign customers

• Cause a decline in demand

• Decline in cash flows

• If the currency of parent company is strong so the remitted funds will convert into small amounts

Overview of an MNC’s Cash Flows

Profile A: MNCs Focused on International Trade

U.S.-based MNC

U.S. CustomersPayments for products

U.S. BusinessesPayments for supplies

Foreign ImportersPayments for exports

Foreign ExportersPayments for imports

Overview of an MNC’s Cash Flows

Profile B: MNCs Focused on International Trade and Licensing, Joint Ventures and Franchising

U.S.-based MNC

U.S. CustomersPayments for products

U.S. BusinessesPayments for supplies

Foreign ImportersPayments for exports

Foreign ExportersPayments for imports

Foreign FirmsFees for services provided

Fees for services received Foreign Firms

Overview of an MNC’s Cash Flows Profile C: MNCs Focused on International Trade, International

Arrangements, and Direct Foreign Investment

U.S.-based MNC

U.S. CustomersPayments for products

U.S. BusinessesPayments for supplies

Foreign ImportersPayments for exports

Foreign ExportersPayments for imports

Foreign SubsidiariesFunds remitted back

Foreign FirmsFees for services provided

Fees for services received Foreign Firms

Investment funds Foreign Subsidiaries

n

ttt

k1=

$,

1

CF E = Value

E (CF$,t ) = expected cash flows to be received at the end of period tn = the number of periods into the future in which cash flows are receivedk = the required rate of return by investors

Valuation Model for an MNC

• Domestic Model

n

tt

m

jtjtj

k1=

1 , ,

1

ER ECF E

= Value

E (CFj,t ) = expected cash flows denominated in currency j to be received by the U.S. parent at the end of period tE (ERj,t ) = expected exchange rate at which currency j can be converted to dollars at the end of period tk = the weighted average cost of capital of the MNC

Valuation Model for an MNC

• Valuing International Cash Flows

Impact of Financial Management and International Conditions on Value• An MNC will decide how much business to conduct in

each country and how much financing to obtain in each

currency.

• The MNC’s financial decisions determine its exposure to

the international environment.

An MNC can control its degree of exposure

to exchange rate effects, economic conditions, and

political conditions with its financial management.

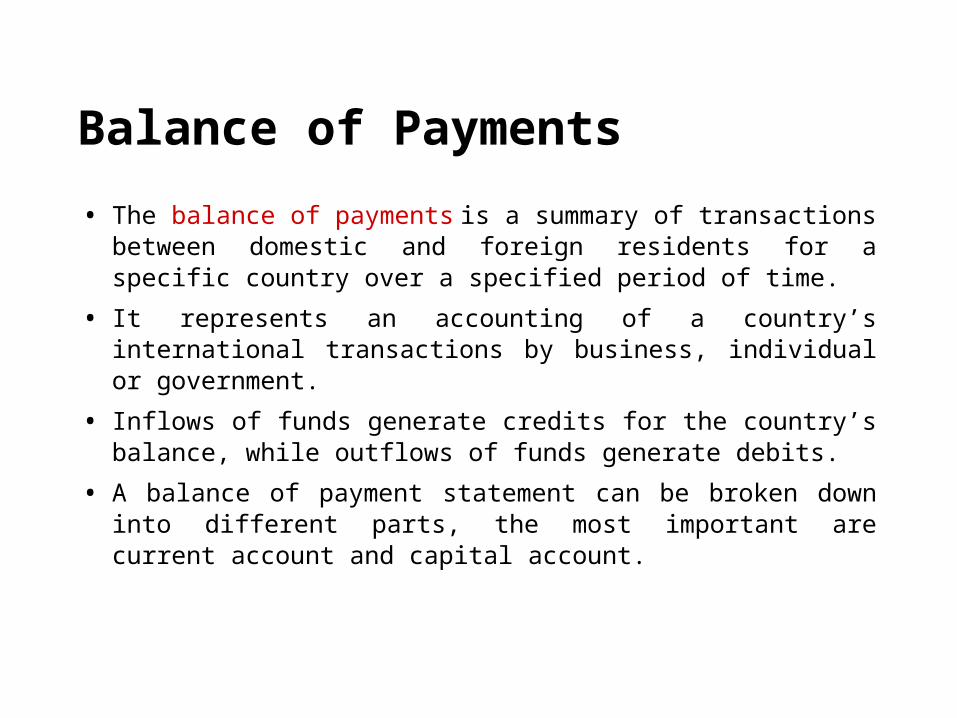

Balance of Payments

Balance of Payments

• The balance of payments is a summary of transactions between domestic and foreign residents for a specific country over a specified period of time.

• It represents an accounting of a country’s international transactions by business, individual or government.

• Inflows of funds generate credits for the country’s balance, while outflows of funds generate debits.

• A balance of payment statement can be broken down into different parts, the most important are current account and capital account.

Balance of Payments

• A balance of payment statement can be broken down into different parts, the most important are current account and capital account.

Current Account

• The current account summarizes the flow of funds

between one specified country and all other

countries due to purchases of goods or services,

or the provision of income on financial assets.

• Key components of the current account include

the balance of trade, factor income, and transfer

payments.

• The capital account summarizes the

flow of funds resulting from the sale of

assets between one specified country

and all other countries.

Capital Account

• The key components of the capital account are

• Direct Foreign Investment,

• Portfolio Investment,

• Other Capital Investment.

Capital Account

Overview

Opportunities in Latin America, Europe and Asia

Provide a model for the valuation of MNC.

MNC’s Cash flows with different aspects

• Balance of Payment (Accounting of

transactions)

¤ Current Account

¤ Capital Account

• Current Account (Purchase Summary)

¤ Balance of Trade

¤ Factor Income

¤ Transfer Payments

Overview

• Capital Account (Flow of funds; one country to

other)

¤ Direct Foreign Investment

¤ Portfolio Investment

¤ Capital Investment

• Trade volume is different

• Over all the World is developing

• Source: Adopted from South-Western/Thomson Learning.

2006

Overview

Source: Adopted from South-Western/Thomson Learning. 2006