international certificate in enterprise risk management · pdf fileoverview of module 1:...

TRANSCRIPT

International Certificate in Enterprise Risk Management

ii | © 2016 Institute of Risk Management

Published by:

Institute of Risk Management

2nd Floor, Sackville House, 143–149 Fenchurch Street, London EC3M 6BN

Tel: +44 (0) 20 7709 9808

Fax: +44 (0) 20 7709 0716

Email: [email protected]

www.theirm.org

© 2016, 2015, 2014 Institute of Risk Management

First published 2014. This revised edition published September 2016.

All rights reserved. No part of this publication may be reproduced, stored in a

retrieval system, or transmitted, in any form or by any means, electronic,

mechanical, photocopying, recording or otherwise, without permission of the

copyright owner.

While every effort has been made to ensure that references to websites are

correct at time of going to press, the World Wide Web is a constantly changing

environment and Institute of Risk Management cannot accept any responsibility

for any changes to addresses.

Institute of Risk Management acknowledges product, service and company

names referred to in this publication, many of which are trade names, service

marks, trademarks or registered trademarks.

Instructional design, and editorial and production project management by

Wordhouse Ltd, Reading, UK.

© 2016 Institute of Risk Management | iii

Acknowledgements

Institute of Risk Management (IRM) wishes to thank and acknowledge the efforts

of Steve Shackleford, lead developer of this study guide, and reviewers Dorothy

Abade-Maseke, Niall Butler and Norman Sinclair.

IRM also thanks its global Education Advisory Board and current and past

examiners for their invaluable contribution and advice concerning the

redevelopment of the syllabus content.

Finally, we are grateful to Stephen Wellings and his team at Wordhouse Ltd for

their advisory and editorial services. Also to John Meed and Roger Merritt

Associates for their contributions to this revision.

iv | © 2016 Institute of Risk Management

Contents

Introduction ...................................................................................................... vii

Overview of Module 1: Principles of Risk and Risk Management.................. x

Unit 1 Concepts and definitions of risk and risk management ...................... 1

Introduction ....................................................................................................... 2

1.1 Approaches to defining risk ..................................................................... 2

1.2 Impact of risk on organisations ................................................................ 4

1.3 Types of risk ............................................................................................ 6

1.4 Development of risk management ........................................................... 6

1.5 Principles and aims of risk management ................................................. 9

Self-assessment questions ............................................................................. 10

Further reading ............................................................................................... 11

Feedback to activities ..................................................................................... 12

Answers to self-assessment questions ........................................................... 13

Unit 2 Risk management standards................................................................ 14

Introduction ..................................................................................................... 15

2.1 General risk management standards .................................................... 15

2.2 Alternative risk management approaches ............................................. 22

Self-assessment questions ............................................................................. 24

Further reading ............................................................................................... 25

Feedback to activities ..................................................................................... 26

Answers to self-assessment questions ........................................................... 27

Unit 3 Enterprise risk management ................................................................ 28

Introduction ..................................................................................................... 29

3.1 Defining Enterprise risk management ................................................... 29

3.2 Enterprise risk management overview .................................................. 31

© 2016 Institute of Risk Management | v

3.3 Implementing ERM ................................................................................ 33

3.4 Establishing the context for risk management ....................................... 34

3.5 Objective setting ................................................................................... 37

Self-assessment questions ............................................................................. 42

Further reading ............................................................................................... 42

Feedback to activities ..................................................................................... 44

Answers to self-assessment questions ........................................................... 47

Unit 4 Risk assessment 1: introduction and identification ........................... 48

Introduction ..................................................................................................... 48

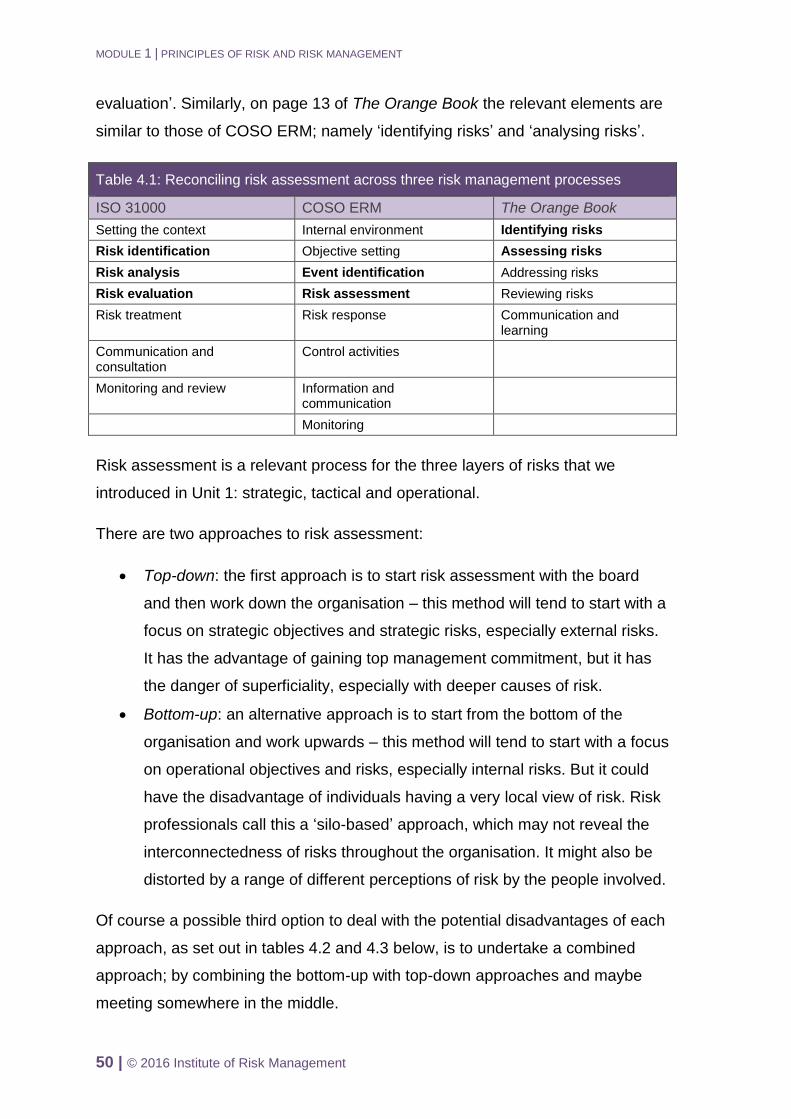

4.1 Risk assessment considerations ........................................................... 49

4.2 Risk causes (sources) and consequences ............................................ 55

4.3 Risk classification systems .................................................................... 60

Self-assessment questions ............................................................................. 70

Further reading ............................................................................................... 70

Feedback to activities ..................................................................................... 71

Answers to self-assessment questions ........................................................... 73

Unit 5 Risk assessment 2: risk analysis and evaluation ............................... 74

Introduction ..................................................................................................... 75

5.1 Introduction to risk analysis ................................................................... 75

5.2 Risk likelihood and impact ..................................................................... 77

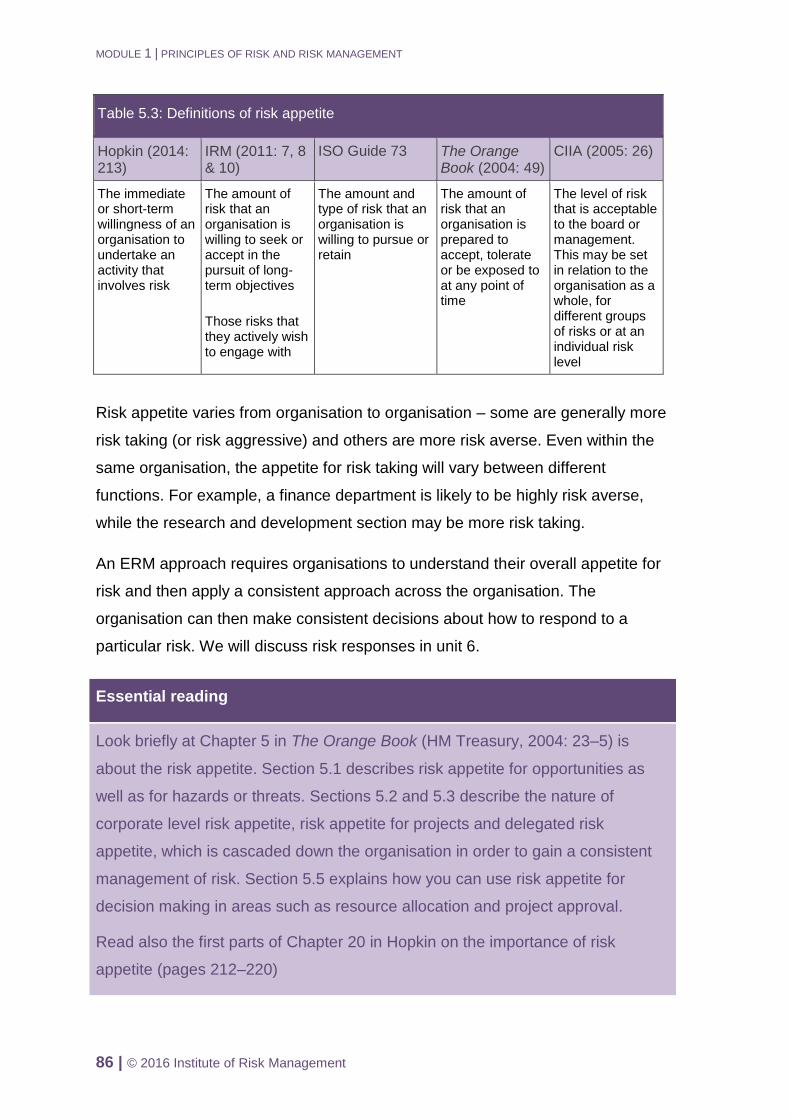

5.3 Risk evaluation and risk appetite ........................................................... 84

5.4 Loss control ........................................................................................... 89

5.5 Defining the upside of risk ..................................................................... 90

Self-assessment questions ............................................................................. 96

Further reading ............................................................................................... 96

Feedback to activities ..................................................................................... 97

Answers to self-assessment questions ........................................................... 98

vi | © 2016 Institute of Risk Management

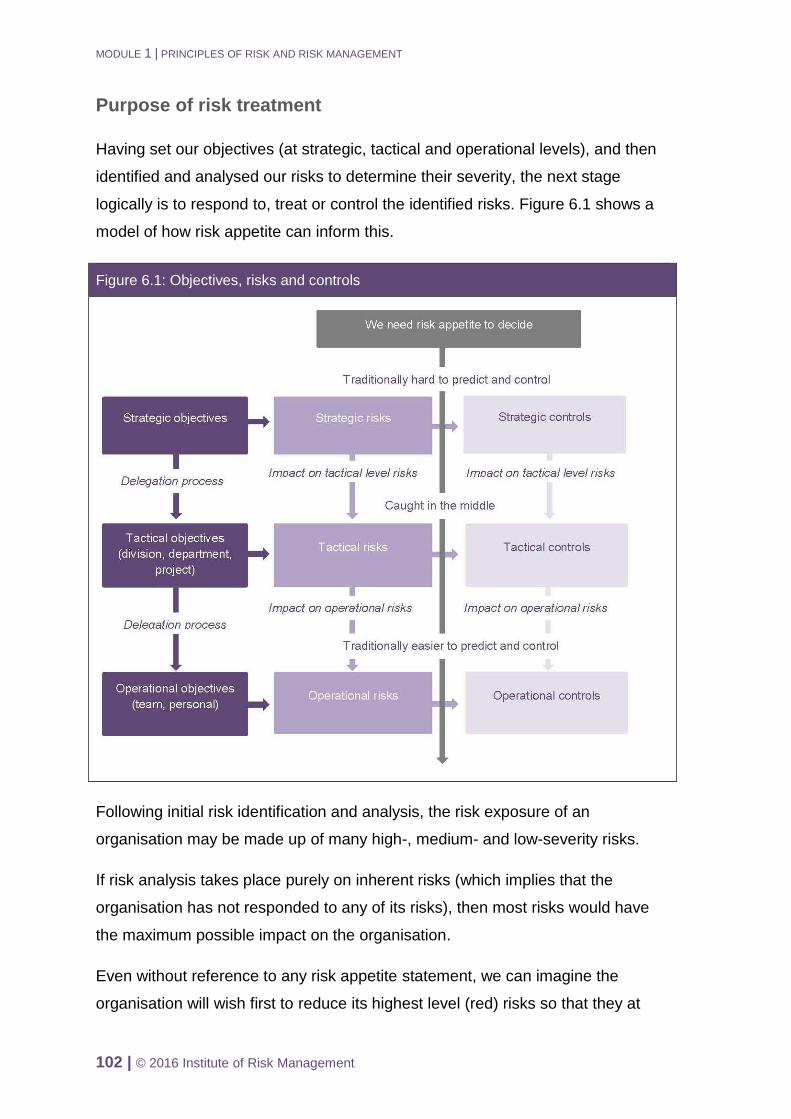

Unit 6 Risk response and risk treatment ...................................................... 100

Introduction ................................................................................................... 101

6.1 Introduction to risk treatment and risk response.................................. 101

6.2 The 4Ts ............................................................................................... 104

6.3 Risk control techniques (PCDD) .......................................................... 107

6.4 Control of selected hazard risks .......................................................... 110

6.5 Introduction to monitoring and review ................................................. 110

6.6 Insurance and risk transfer .................................................................. 117

6.7 Business continuity planning ............................................................... 118

Self-assessment questions ........................................................................... 123

Further reading ............................................................................................. 124

Feedback to activities ................................................................................... 125

Answers to self-assessment questions ......................................................... 130

References ...................................................................................................... 131

© 2016 Institute of Risk Management | vii

Introduction

This module provides an introduction to the fundamental principles and concepts

relating to risk and risk management. It asks you to consider the following

questions:

What do we mean by risk?

How did risk management develop into the profession that it is today?

What is enterprise risk management?

Which standards and frameworks exist to guide us through the process of

managing risk?

Module 1 underpins the remaining five modules of the International Diploma in

Enterprise Risk Management. Successful completion of modules 1 and 2 leads

to the award of International Certificate in Enterprise Risk Management.

About this study guide

This study guide will lead you step by step through the module in a series of

carefully planned units, and provide you with learning activities and self-

assessment questions to help you master the subject matter. The guide should

help you organise and carry out your studies in a methodical, logical and

effective way, but if you have your own study preferences you will find it a flexible

resource too.

Before you begin using this study guide, make sure you are familiar with the

advice, guidance and rules provided by IRM on such things as study and revision

skills, support and formal assessments in the Student Handbook which can be

found in The Study section of the IRM website.

If you are on a taught course, your tutor will explain how to use the guide in

conjunction with a programme of face-to-face workshops and seminars – when

to read the units, when to tackle the activities and questions, and so on.

If you are studying independently, you can use the study guide in the following

way:

viii | © 2016 Institute of Risk Management

The overview that follows will give you a feel for the nature and content of

the subject matter.

Plan your overall study schedule so that you allow enough time to

complete all units well before your examinations – in other words, leaving

plenty of time for revision. You can use the study and revision plan

template provided in the Student Handbook..

For each unit, set aside enough time for reading the text and other

essential readings, tackling all the learning activities and self-assessment

questions and the suggested further reading. And don’t forget the

opportunities to network with other students provided in the student

support area of the IRM website.

The study guide breaks the module content down into six units, which vary from

approximately 20 to 30 hours’ duration each. However, we are not advising you

to study for this sort of time without a break! The units are simply a convenient

way of breaking the syllabus into manageable chunks. Most people would try to

study one unit every two or three weeks, taking plenty of breaks within each unit.

You will quickly find out what suits you best.

Now let’s take a look at the structure and content of the individual units.

Each unit begins with an introductory page which sets out the overall learning

outcome for the unit, the main sections into which it is divided and the subsidiary

learning outcomes for each of those sections. The outcomes are designed to

help you understand exactly what you should be able to do after you’ve studied

the unit. You might find it helpful to tick them off as you progress through the unit.

You will also find them useful during revision. Following this, the resources

section will let you know which books, articles and web sources you will need to

access as ‘essential readings’ during the unit.

Then the main part of the unit begins, with the first of the numbered main

sections. Each unit contains essential readings which refer you to the relevant

textbooks, articles, and so on. It is essential that you do this reading, since it is

not possible to put everything you need to know in a single study guide. At this

level of study, wider reading is the key to developing deeper subject learning

through a contemporary, contextual and critical perspective.

© 2016 Institute of Risk Management | ix

At regular intervals in each unit, we have provided you with activities, which are

designed to get you actively involved in the learning process. You should always

try to complete the activities before reading on. You will learn much more

effectively if you are actively involved in doing something as you study, rather

than just passively reading the text in front of you. You will find the feedback on

the activities at the end of the unit.

Also featuring throughout each unit are Risk in the real world items, which are

brief case studies and examples showing how the key points relate to real world

organisations or events.

The further reading section at the end of each unit will enable you to find more

detailed information, or suggest where you might explore a particular topic in

more depth. A full list of all sources referred to, both here and in the essential

readings, is given in a separate references section at the end of the study guide.

We provide a number of self-assessment questions at the end of each unit.

These are to help you to decide for yourself whether you have achieved the

learning outcomes set out at the beginning of the unit. Once again, there are

answers at the end of the unit. If you still do not understand a topic, having

attempted the self-assessment question, always try to reread the relevant

passages in the unit itself and the essential readings, or follow the advice on

further reading.

Good luck in your studies!

x | © 2016 Institute of Risk Management

Overview of Module 1: Principles of

Risk and Risk Management

Module aims

This module introduces the principles and concepts of risk and risk management.

The history of risk management is explored as a means of understanding the

current drivers of enterprise risk management, and the development and impact

of international standards. This leads to an examination of the ways in which

risks are classified and the models or frameworks that are utilised to identify,

assess and treat them.

Module learning outcomes

By the end of the module you should be able to:

Recognise the origins and key concepts relating to risk management.

Compare and contrast the main risk management standards.

Apply the concepts of enterprise risk management.

Examine the main approaches to risk identification.

Use the main approaches to the analysis and evaluation of risk.

Distinguish the main features of risk control techniques.

Main learning units and topics

Unit 1: Concepts and definitions of risk and risk management

Definitions of risk, impact of risk on organisations, introduction to types of risk,

definitions and development of risk management, principles and aims of risk

management.

Unit 2: Risk management standards

General risk management standards, alternative risk management approaches.

© 2016 Institute of Risk Management | xi

Unit 3: Enterprise risk management

COSO 2004, enterprise risk management, implementing ERM, establishing the

context for risk management.

Unit 4: Risk assessment 1: introduction and identification

Risk assessment considerations, risk classification systems (risk identification),

risk causes (sources) and consequences.

Unit 5: Risk assessment 2: risk analysis and evaluation

Introduction to risk analysis, risk likelihood and impact, loss control, defining the

upside of risk, the importance of risk appetite (risk evaluation).

Unit 6: Risk response and risk treatment

Introduction to risk treatment and risk response, the 4Ts, risk control techniques

(PCDD), control of selected hazard risks, introduction to monitoring and review,

insurance and risk transfer, business continuity planning (BCP).

Essential reading list

These are the texts we refer to in the essential reading sections. Hopkin (2014) is

the core text; you should be able to download the others on-line from the links

below.

Adams, J (2007) ‘Risk Management: It’s Not Rocket Science – It’s Much More

Complicated’, Public Risk Forum, May 2007. Valby, Denmark: European

Institute for Risk Management in collaboration with PRIMO (Public Risk

Management Organisation) Europe. Available at:

http://www.eirm.dk/en/Who%20We%20Are/~/media/Business%20Card/Articles

%20-%20EIRM/Publications%20by%20EIRM/PRF%20May%202007.ashx

Airmic/Alarm/IRM (2010) A structured approach to Enterprise Risk Management

(ERM) and the requirements of ISO 31000. London: Association of Risk

Managers/Public Risk Management Association/Institute of Risk

Management. Available at:

http://www.theirm.org/media/886062/ISO3100_doc.pdf

xii | © 2016 Institute of Risk Management

COSO (2004) Enterprise Risk Management: Integrated Framework, Executive

Summary. Committee of Sponsoring Organizations of the Treadway

Commission. Available at:

http://www.coso.org/documents/coso_erm_executivesummary.pdf

COSO (2014) Improving organizational governance and performance: How the

COSO frameworks can help. Committee of Sponsoring Organizations of

the Treadway Commission. Available at:

http://www.coso.org/documents/2014-2-10-COSO%20Thought%20Paper.pdf

HM Treasury (2004) The Orange Book: Management of Risk – Principles and

Concepts. London: HM Treasury. Available at:

http://hm-treasury.gov.uk/orange_book.htm

Hopkin, P (2014) Fundamentals of Risk Management, London: Kogan Page

RIMS (2011) An overview of widely used risk management standards and

guidelines. Risk and Insurance Management Society, Inc. Available at:

http://www.rims.org/resources/ERM/Documents/RIMS%20Executive%20Report

%20on%20Widely%20Used%20Standards%20and%20Guidelines%20March%2

02010.pdf

StrategicRISK (2012) ‘StrategicRISK 2012 Risk Report: The top concerns of

European risk managers’. Sponsored by Marsh Risk Consulting. London:

Newsquest Specialist Media. Available at:

http://www.strategic-risk-global.com/risk-report-2012-update/1397747.article

Unit 1 Concepts and definitions of

risk and risk management

Unit learning outcome

After studying this unit, you should be able to:

Recognise the origins and key concepts relating to risk management

Unit contents Section learning outcomes

1.1 Approaches to defining risk…2 Provide a range of definitions of risk and risk management

1.2 Impact of risk on organisations…4 Analyse how risks impact on organisations, for example by way of the attachment of risks theory

1.3 Types of risk…6 Describe options for classifying risks according to the nature, source and timescale of impact

1.4 Development of risk management…6 Outline the history of risk management, including the various specialist areas and approaches

1.5 Principles and aims of risk management…9

Consider the principles and aims of risk management and risk management’s importance to operations, projects and strategy

Resources

You will also need to consult the following resources:

Hopkin (2014), chapters 1–5

The Orange Book (HM Treasury, 2004), chapter 1

MODULE 1 | PRINCIPLES OF RISK AND RISK MANAGEMENT

2 | © 2016 Institute of Risk Management

Introduction

This unit provides a general introduction to some basic risk management

concepts. It will take you through some common definitions of risk and will look at

the positive and negative impact that risk has on organisations. It will introduce

key features of risk and risk management and introduce methods of classifying

risks. It moves on to discuss the history of risk management, and the principles

and benefits to organisations of good risk management.

1.1 Approaches to defining risk

There have been many attempts over the years to define risk. Frank Knight

(Knight, 1921), one of the fathers of modern risk management, said:

Risk can be applied to a situation where there are several possible

outcomes and, on the basis of past relevant experience, probabilities can

be assigned to the various outcomes that could prevail.

Uncertainty can be applied to a situation where there are several possible

outcomes but there is little past relevant experience to enable the

probability of the possible outcomes to be predicted.

This suggests that risk management covers the management of both quantifiable

risk and unquantifiable uncertainty.

As most if not all of the decisions made by an organisation will be ones with an

uncertainty of outcome (in other words, risky decisions), Douglas Barlow, another

very early writer on risk aptly stated in 1962, ‘all management is risk

management’ (Sedgwick Law, 2006).

A widely used definition of risk comes from the International Organization for

Standardization (ISO, 2009) which states that risk is

‘The effect of uncertainty on objectives’.

So the overriding purpose of risk management is to help organisations to identify,

understand and manage their risks and opportunities, and thereby increase the

likelihood of achieving their objectives by reducing uncertainty.

UNIT 1 | CONCEPTS AND DEFINITIONS OF RISK AND RISK MANAGEMENT

© 2016 Institute of Risk Management | 3

For examination purposes, it is vital to have in your mind one general definition

each of risk and risk management, such as the ISO one. IRM has stated that:

‘Organisations of all types face a variety of factors and influences that

make it uncertain whether and when they will achieve their objectives. The

effect of this uncertainty is termed ‘risk’. Effective risk management helps

organisations to identify, understand and manage the risks, thereby

maximising the likelihood of achieving their objectives. And this is the first

and overriding purpose of risk management.

‘Risk management is a core management discipline. Like general

management or project/change management, risk management is a

discipline that supports all organisational activities. The risks that

organisations face change all the time, so the art of good risk

management is to combine planning for what we already know has

happened and might occur, with preparation for unknown situations.

‘With the general public, however, risk management often has a poor

perception. Stories in the media of risk management getting in the way of

common sense are not infrequent. The failure of some health and safety

practitioners to properly communicate the immense benefits of their work

and the perceived failure of risk management in the world’s banks have all

added to these perceptions.’

Every organisation that wants to practise risk management should produce its

own clear, shared definition of what it means by the terms ‘risk’ and ‘risk

management’. There are specific tools we can use to describe risks, the most

common being the risk register. In module 2, we shall see the range of means of

storing such information from manual records, to spreadsheets, to fully blown

dedicated risk information management systems (RIMS).

Organisations have to first quantify (analyse) the relative severity of the risk

before any actions have been taken to manage it. This is called the inherent (or

gross) risk. We then again measure the same risk after risk management actions

have been taken. This we call the residual (or net, or current) risk.

MODULE 1 | PRINCIPLES OF RISK AND RISK MANAGEMENT

4 | © 2016 Institute of Risk Management

Essential reading

Read the first three sections of chapter 1 of Hopkin, which cover ‘definitions of

risk’, ‘types of risk’ and ‘risk description’.

Have a quick look over the rest of the chapter – however, we will discuss these

issues in much more detail in later units of this module.

Activity 1.1

1 From your reading of this unit so far, and Chapter 1 of Hopkin, which definition

of risk seems most appropriate to you?

2 What is the difference between ‘hazard’, ‘control’ and ‘opportunity’ risks?

3 Does your organisation have a formal definition of risk? If so, how many people

are aware of it? If not, what do you think are the reasons for its absence?

Check your answers with those at the end of this unit.

Essential reading

Read The Orange Book, chapter 1. This provides a succinct, two-page

introduction to risk and risk management. Note carefully section 1.6, which also

uses Hopkin’s three dimensions, but adds that different skills and competencies

are required to manage risks at each of these levels.

1.2 Impact of risk on organisations

We have seen how one of the most well used definitions of risk relates to the

effect of uncertainty on objectives. Risks do indeed impact on corporate

objectives, but, as your next reading will show, they can also impact on key

dependencies, core processes and stakeholder expectations. We call this the

‘attachment of risk’ and organisations should map out how risks are attached to

each of these elements in order to fully analyse their impact.

UNIT 1 | CONCEPTS AND DEFINITIONS OF RISK AND RISK MANAGEMENT

© 2016 Institute of Risk Management | 5

Let’s consider the meaning of these three additional points of impact now,:

Key dependencies are the key things that the organisation needs to be

successful; they might be internal or external things but in short, they are

what the business depends upon for its future success.

Core processes are fundamental to organisational success because they

are the means of delivery of strategy and continuity of operations. A core

process can be defined as “the collection of activities that deliver a specific

stakeholder expectation”.

Stakeholders are the groups of individuals who have a stake in the

business, or are affected by what the organisation does – such as

investors, suppliers, customers, the wider society and government.

The rationale for the attachment of risk is that organisations should map out the

consequences of risk in order to fully analyse their impact.

Essential reading

Read Chapter 2 of Hopkin – pay particular attention to the third subject on the

attachment of risks, because this is a recurring theme throughout the module.

See also the boxes on page 26, which examines the difficulties in balancing risk

and reward in Formula 1 racing, and page 28, which looks at propensity for

taking risks.

Activity 1.2

1 Note down what Hopkin means by key dependencies, core processes and

stakeholder expectations.

2 With your colleagues, try to identify a key dependency and a core process

within your organisation. Then try to identify what types of risk your

dependency and your process might be vulnerable to.

MODULE 1 | PRINCIPLES OF RISK AND RISK MANAGEMENT

6 | © 2016 Institute of Risk Management

A report issued by the International Integrated Reporting Council in December

2013 (IIRC, 2013) shows how risk can impact on an organisation’s capital value

– see the further reading section at the end of unit 1.

RISK IN THE

REAL WORLD

Hopkin (on page 24) provides an example of an external key

dependency when talking about Northern Rock. Look also at

further context to the Northern Rock events in the table on

page 30.

1.3 Types of risk

You will now look more closely at classifying risks as hazard risks, control risks

and opportunity risks.

Essential reading

Read chapter 3 of Hopkin which looks at the timescale of risk impacts and then

explores hazard risks, control risks and opportunity risks further.

Activity 1.3

The box on page 36 of Hopkin gives an alternative typology of risk factors –

controllable and uncontrollable risks. Using heart disease as an example, give an

example of both controllable and uncontrollable risks.

1.4 Development of risk management

Understanding of the history of risk management can be useful: for several

reasons

The scope of risk management has changed to such a degree in recent

years that conventional views of risk have had to be altered – see for

example Bernstein (1996) in the further reading for unit 1.

UNIT 1 | CONCEPTS AND DEFINITIONS OF RISK AND RISK MANAGEMENT

© 2016 Institute of Risk Management | 7

Historically, risk management has focused on the mathematics of hazard-

based or financial risks. It tended to focus on specific risks and neglected

an enterprise-wide approach.

You need to understand the history to explain where we are now in risk

management and where this may lead in the future.

You will see that our changing world has produced new risks that do not

easily fit into historical frames of reference, and history tells us that new

risks come and old risks disappear – we can learn lessons on how people

reacted to new, emerging risks.

Risk management frameworks have developed only since 1995.

A historical timeline in risk management history might include the following:

1500: Religious belief, fate and superstition – evolutionary theory.

1500–1900: A decline of the above by educational enlightenment in risk.

1900–70: Development of specialist risk professions.

1970–95: Risk management specialism moves towards generalism.

1995–date: The maturing risk profession.

1995–date: The age of risk management standards.

But in the last few hundred years there was another significant trend towards:

More knowledge of causes and effects (as people experienced and better

understood their environment – initially from the passing down of stories

and then from first written records).

Turning mystery and superstition into unknown uncertainty and then into

known uncertainty (the time of the Enlightenment), which moved on into

people being able to measure risk for the first time through the

development of statistics.

There is great value in looking at the past. Not only can it provide insight into the

developmental dynamic of the field, it provides important guidance in

understanding why the modern world appears as it does, particularly with some

of the inherited superstitions and irrationalities.

MODULE 1 | PRINCIPLES OF RISK AND RISK MANAGEMENT

8 | © 2016 Institute of Risk Management

‘A brief history of risk management’ (Kloman, 2010), gives a history of risk

management from 1914 until 2008 and it includes something on the development

of risk specialisms, such as insurance, actuarial science, and health and safety.

Though the material skims the surface of a very detailed subject, it serves a

useful role in orienting you towards key events in the history of the field. See the

further reading section at the end of unit 1

Essential reading

Read chapter 4 of Hopkin which looks at the origins of risk management and the

development of risk management specialisms.

Activity 1.4

1 As a modern risk manager, why is it useful to understand something of the

history of risk management?

2 By talking to some of the longer serving members of your organisation, try to

discover something of the history of risk management in your organisation.

Since 2009 we have experienced a number of major risk events such as the

Arab Spring, major natural disasters, the range of sovereign debt crises in many

Eurozone countries and the slow signs of recovery in Western economies. All

these things impact our role in the risk profession.

Indeed, most of the exciting and worthwhile achievements humanity would like to

make are complex and not without their potential pitfalls. Risk management can

help organisations achieve what otherwise might be too risky or uncertain. Good

risk management is about being able to take risk. Good risk management is

about ‘reaching for the stars’.

UNIT 1 | CONCEPTS AND DEFINITIONS OF RISK AND RISK MANAGEMENT

© 2016 Institute of Risk Management | 9

At the same time, risk management is also about safeguarding organisations and

making them more resilient. While being ambitious, it is also important to protect

the value of the organisation. Managing so-called ‘downside risk’ – events whose

potential outcome is negative or undesirable – can help the organisation apply

controls and achieve its objectives.

Increasingly organisations are required by law, regulation or stakeholder

expectations to build risk management competencies and provide reports that

show that those competencies are effective. In the future, these reports might

well be audited in ways similar to the way financial reports are audited today.

1.5 Principles and aims of risk management

This final section looks at the five principles of risk management and the main

benefits or objectives of risk management.

Essential reading

Read chapter 5 of Hopkin on the principles and aims of risk management. Pay

particular attention to the acronyms PACED and MADE2, as these will be

recurring themes throughout module 1. On page 53, Hopkin demonstrates the

failed strategy of a real grocery retail chain from several years ago while on 56

he uses a car’s brakes, clutch and accelerator as a synonym to explain the

benefits of these three levels or types of risk.

Activity 1.5

1 List five benefits of good risk management.

2 Outline the five principles of risk management.

MODULE 1 | PRINCIPLES OF RISK AND RISK MANAGEMENT

10 | © 2016 Institute of Risk Management

RISK IN THE

REAL WORLD

PricewaterhouseCoopers (2010: 8) published a composite of a

range of research reports that took place prior to the global

financial crisis in 2009, which showed that strategic risk was by

far the greatest determinant of how shareholder value is

destroyed in business. PwC estimated that strategic risks

explained up to 60% of shareholder value decreases, followed

by 20% for operational risk losses, 15% for financial risk effects

and 5% for compliance risk effects. This study used the COSO

ERM classification of objectives/risks, which we will consider in

unit 3.

Self-assessment questions

These questions will help you to check your knowledge of Unit 1. They use a

multiple choice format similar to that you will meet in the exam. Choose the

option you think is right and then check with the answers at the end of this unit.

1 Which of these is best describes ‘residual’ (or net, or current) risks.

a) A risk before any actions have been taken to manage it

b) A risk associated with speculative opportunities

c) A risk after risk management actions have been taken

2 Which of these is best describes ‘hazard’ risks.

a) Risks associated with the benefits of speculative opportunities

b) Risks associated with ‘pure’ risks or perils

c) Risks associated with the management of uncertainty

3 What are core processes?

a) The means of delivery of strategy and continuity of operations

b) The key things that the organisation needs to be successful

c) Groups of individuals who have a stake in the business, or are affected

by what the organisation does

UNIT 1 | CONCEPTS AND DEFINITIONS OF RISK AND RISK MANAGEMENT

© 2016 Institute of Risk Management | 11

4 What of these best describes the term ‘mandatory’ in relation to risk

management objectives as set out in MADE2?

a) To ensure that risk management complies with the five principles of

PACED

b) To ensure that appropriate risk-management information is available

c) To ensure conformity with rules, regulations and obligations

Further reading

IRM’s Online Resource Centre (ORC) has a list of publications on the

introduction to risk and risk management in the section ‘Principles of risk’. Look

in particular at the subsections called ‘History of risk management’ and ‘Nature of

risk and uncertainty’.

Holton (2004) provides a good summary of how risk has been defined since

Frank Knight tried to distinguish risk from uncertainty and it discusses the

ensuing debate throughout the twentieth century.

Entsgo (undated) provides an easy to read two-page distinction between pure

and speculative risks.

Bernstein (1996) introduces the debate over the actual meaning of ‘risk’.

Historically, the risk management field has tended to define risk solely through its

statistical or mathematical nature, which is appropriate in many settings.

Kloman (2010) offers an introductory historical perspective on key developments

in the history of risk management, especially from 1914 to the start of the 2008

financial crisis.

In December 2013 a new organisation, the International Integrated Reporting

Council (IIRC) produced a major report, which has something to say on the

impact of risk in organisations as part of a much wider agenda to reform

corporate reporting to stakeholders. The IIRC measures value creation in the

form of six different types of capital owned by any organisation (IIRC, 2013: 11).

MODULE 1 | PRINCIPLES OF RISK AND RISK MANAGEMENT

12 | © 2016 Institute of Risk Management

If you are interested in finding out how businesses around the world justify their

investment in risk management (or rather enterprise risk management) you could

briefly review Accenture (2011).

Feedback to activities

Activity 1.1

1 The simplest definition is the one you can get from ISO 31000. You can find

this and several others from Hopkin’s table 1.1 (page 14).

2 The source for your answer to this question can be found in Hopkin chapter 1

‘Types of Risk’ (page 15). As you work through the book look for other

characteristics and differences for these three levels of risks, which he

describes from time to time.

3 If your organisation has a formal definition of risk (perhaps from a policy

document or a risk manual), compare it to some of the more official

definitions.

Activity 1.2

1 Key dependencies are the key things that the organisation needs to be

successful; they might be internal or external things but in short, they are

what the business depends upon for its future success.

2 Core processes are fundamental to organisational success because they are

the means of delivery of strategy and continuity of operations. A core process

can be defined as ‘the collection of activities that deliver a specific

stakeholder expectation’.

3 Stakeholders are the groups of individuals who have a stake in the business,

or are affected by what the organisation does – such as investors, suppliers,

customers, the wider society and government.

Activity 1.3

Controllable risks for heart disease include high blood pressure or cholesterol.

Uncontrollable risks include age or gender.

UNIT 1 | CONCEPTS AND DEFINITIONS OF RISK AND RISK MANAGEMENT

© 2016 Institute of Risk Management | 13

Activity 1.4

1 The scope of risk management has changed to such a degree in recent years

that conventional views of risk have had to be altered. Historically, risk

management has focused on the mathematics of hazard-based risks or on

financial risks. It tended to focus on specific risks. You need to understand

the history of risk and risk management to explain where we are now and

where things may go in the future. You will see that our changing world has

produced new risks that do not easily fit into historical frames of reference. So

in summary, the history helps to explain where we are today and might give

us some guide of the directions to where risk management is going in the

years to come.

2 They may be able to talk about some of the major crises or major periods of

change that the business faced and how the organisation got through those

changes intact.

Activity 1.5

1 Your solution can be found in Hopkin chapter 5. The MADE2 acronym – see

Hopkin’s table 5.2 (page 51) can help you to remember. You can also help

yourself by remembering the definition of risk, which implies that good risk

management will help achieve your organisation’s objectives.

2 Again an acronym from Hopkin chapter 5 is the source of your answer. This

time the acronym is PACED – see table 5.1 (page 50).

Answers to self-assessment questions

1-c

2-b

3-b

4-c

Unit 2 Risk management standards

Unit learning outcome

After studying this unit, you should be able to:

Compare and contrast the main risk management standards

Unit contents Section learning outcomes

2.1 General risk management standards…15

Describe the key stages in the risk management process, the main components of a risk management framework and the key features of the best known risk management standards and frameworks currently in use

2.2 Alternative risk management approaches…22

Compare and contrast a number of risk management standards

Resources

You should make sure you have access to the following resources before starting this unit:

Hopkin (2014), chapter 6

The Orange Book (HM Treasury, 2004), chapter 2

Airmic/Alarm/IRM (2010), part 1

RIMS (2011)

UNIT 2 | RISK MANAGEMENT STANDARDS

© 2016 Institute of Risk Management | 15

Introduction

This unit begins by looking at the main features of key general risk management

standards, including the most generally accepted ISO 31000 standard (ISO,

2009), as well as considering the importance of a range of risk related guidance.

It then looks briefly at some specialist risk management standards.

All risk management standards are recent; indeed, the first ever risk

management standard, the AS/NZS4360 was only released in 1995 (Standards

New Zealand, 2013). If anything, that fact demonstrates the still youthful state of

our profession and why even now risk managers still argue over such

fundamental issues such as the definition of risk.

Your organisation may use the characteristics of one of these standards to

implement a risk management process to manage its risks; it may combine them

and use elements from each; or it may even have its own bespoke standard.

As your career in risk management develops you will need to know well at least

one such risk management standard and how to apply it in your organisation.

2.1 General risk management standards

Risk management has developed over time and across many regions of the

world and many industry sectors, as well as within discrete professions, to meet

diverse needs. Risk management standards, within a clear framework, can

support a more consistent risk management process and this can help to ensure

that risk is managed effectively, efficiently and coherently across an organisation.

The following terminology is generally accepted and applies to ISO 31000:

Risk management

standard =

The risk management

framework +

The risk management

process

MODULE 1 | PRINCIPLES OF RISK AND RISK MANAGEMENT

16 | © 2016 Institute of Risk Management

IRM states that a simple risk management process is all about being able to:

identify risks (and opportunities)

evaluate and prioritise the significant risks (and opportunities)

manage the significant risks

In order to provide an explanation for the content of the risk management

framework, the acronym RASP or ‘Risk Architecture, risk Strategy and risk

Protocols’ has been developed. RASP is a supportive structure of the risk

management process – it is what helps to determine how the process works.

RASP is in fact an introduction to a substantial area of study which you will

undertake in module 2.

This unit looks at some general risk management standards. You have already

looked at the 8Rs and 4Ts model in Chapter 4 of Hopkin on page 40. The 8Rs

and 4Ts of (hazard) risk management does not form part of any wider, present

day risk management standard or framework, However it is surprisingly well

known and you might well find such an approach suitable for your organisation.

We shall now look at three other general risk management standards in the order

in which Hopkin discusses them in Chapter 6:

IRM (2002) model (page 59).

COSO ERM (page 63).

ISO 31000 model (page 65).

The IRM (2002) model

IRM (2002) describes a slightly different framework of the structure,

responsibilities, administration, reporting and communication in relation to risk.

Although slightly different to RASP, it is another acceptable approach to

describing the risk management framework.

UNIT 2 | RISK MANAGEMENT STANDARDS

© 2016 Institute of Risk Management | 17

The risk management framework can be likened to the risk management context.

In other words, it is the context in which the risk management process must

operate. Later, we shall see that the next two standards (COSO ERM and the

ISO 31000) also have something to say on the subject of the risk management

context. Two additional elements of the risk management context are:

External context – typically the organisation’s industry, products, markets,

logistics, supply chain, competitors and countries of operation.

Internal context – typically the organisation’s internal workings – its

divisions, departments, structures, cultures, leadership, strengths and

weaknesses, and so on.

As well as having a primary role of providing the context of risk management, the

framework also has a secondary role of ensuring that the outputs of the process

are communicated, and that the benefits anticipated (MADE2) from the

investment in risk management are delivered.

Essential reading

Read the first part of chapter 6 in Hopkin, ‘Scope of risk management standards’

which introduces the IRM (2002) risk management process – figure 6.1 (page

59). Look briefly as well at the short sections on ‘Risk management [process’ and

‘Risk management framework’.

Activity 2.1

1 In the light of your reading, write a one-sentence definition of each of these key

terms:

a) Risk management standard b) Risk management framework c) Risk

management process

2 Draw a flowchart which describes your organisation’s risk management

process

MODULE 1 | PRINCIPLES OF RISK AND RISK MANAGEMENT

18 | © 2016 Institute of Risk Management

The COSO ERM cube

The concept of enterprise risk management (ERM), which was first developed

around 2000, received a real boost in world-wide popularity during the autumn of

2004 when the Committee of Sponsoring Organisations of the Treadway

Commission (COSO) launched COSO ERM (COSO, 2004).

Essential reading

Look at the fourth part of Hopkin chapter 6 (page 62), ‘COSO ERM cube’, taking

note of figure 6.3 on page 63.

The COSO ERM framework is displayed as a cube, as in Hopkin Figure 6.3:

The front face is the risk management process, and you should be able to

summarise the content of each of the eight items.

The top face of the cube describes the four categories of organisational

objectives. Again you should be able to summarise the meaning of each

of these four items.

Finally, the side face of the cube shows the implementation process of the

standard. It indicates that ERM begins at entity level and then is cascaded

downwards and across the organisation. In that sense, the fully

implemented version of ERM has to be embedded in all roles, operations

and activities of the enterprise.

COSO ERM is an important standard and we will look at it in greater detail in Unit

3.

Activity 2.2

Write a one-sentence definition of each of these key terms:

a) risk architecture b) risk context c) risk protocols d) risk strategy

UNIT 2 | RISK MANAGEMENT STANDARDS

© 2016 Institute of Risk Management | 19

ISO 31000

The ISO 31000 standard, released in 2009, is probably the most straightforward

and certainly the most internationally accepted risk management standard. For

this reason, you should feel comfortable about its content and purpose and

especially be aware of its process.

Essential reading

Read the fifth part in Hopkin chapter 6 ‘Features of RM standards’, for an

introduction to ISO 31000. See in particular Figure 6.4 (page 65).

There are five clauses (or key elements) in ISO 31000, the most internationally

accepted risk management standard. We will briefly describe them here:

Clause 1

This clause defines the scope of the standard as being generic risk

management; in other words the standard is designed to be applicable to

organisations in a general sense and is not focused on any particular type or

form of organisation, nor for any international setting. Anyone can use this

standard irrespective of their particular risk context.

Clause 2

This clause provides definitions of 29 terms used in the standard; these are, in

fact, derived from another ISO document called ISO Guide 73:2009, which is a

glossary of risk management terms. The guide is available (at a cost) from ISO

(see references for a link to the ISO website). You do not need to learn the full

glossary contained in this guide because this study guide will provide you with all

the terms you need to know.

The next three key clauses cover:

the principles of risk management

the framework for risk management

the process of risk management

MODULE 1 | PRINCIPLES OF RISK AND RISK MANAGEMENT

20 | © 2016 Institute of Risk Management

Clause 3

Clause 3 is based on the principles of risk management. In Unit 1, we referenced

PACED as a tool to evaluate the principles of risk management. Clause 3 sets

out eleven principles, which we summarise below:

1 Risk management creates and protects value – the risk management

process should contribute to the achievement of objectives and

improvements in performance.

2 Risk management is an integral part of organisational processes – it is not

a stand-alone process and risk management activities, roles and

responsibilities should be incorporated into normal planning and

operational processes.

3 Risk management is part of decision making – decision making should be

better informed by considering what is known about potential uncertain

outcomes.

4 Risk management explicitly addresses uncertainty – it reinforces the need

to recognise uncertainty around the achievement of objectives and

determine an appropriate course of action.

5 Risk management is systematic, structured and timely – systems and

structures give the risk management process rigour and make its

outcomes more reliable.

6 Risk management is based on the best available information – different

perspectives need to be considered as inputs to the risk management

process, looking both inside and outside the organisation for areas of risk,

and considering the reliability of different information sources.

7 Risk management is tailored – systems should be designed for the

particular organisation, taking account of their context, size and

complexity.

8 Risk management takes human and cultural factors into account – the

systems need to fit the culture(s) of the organisation. They should

recognise the human factors within processes, and recognise human

factors as risks themselves.

UNIT 2 | RISK MANAGEMENT STANDARDS

© 2016 Institute of Risk Management | 21

9 Risk management is transparent and inclusive – a good risk management

system helps stakeholders understand the organisation’s context and

risks, and considers their views on risks and controls.

10 Risk management is dynamic, iterative and responsive to change – to

allow organisations to respond effectively to the continually changing

business environment, the risk management system itself should be

dynamic and always reflect the latest risk environment.

11 Risk management facilitates continual improvement of the organisation –

at the same time as being able to respond to change, the risk

management system needs to continually develop to help organisations

improve their risk management maturity.

Clause 4

The next clause in the ISO 31000 standard is the risk management framework.

This clause includes the essential steps in the implementation and ongoing

support of the risk management process. The initial component of the ISO 31000

framework is ‘mandate and commitment’ by the board and this is followed by:

design of framework

implement risk management

monitor and review framework

improve framework

The Airmic, Alarm, IRM (2010) guide (page 7) states that:

‘ISO 31000 describes a framework for implementing risk management,

rather than a framework for supporting the risk management process.

Information on designing the framework that supports the risk

management process is not set out in detail in ISO 31000. An organisation

will describe its framework for supporting risk management by way of the

risk architecture, strategy and protocols for the organisation.’

Clause 5

The final clause in the ISO 31000 standard, is the risk management process.

Three components of this process are also briefly described in the Airmic, Alarm,

MODULE 1 | PRINCIPLES OF RISK AND RISK MANAGEMENT

22 | © 2016 Institute of Risk Management

IRM (2010) guide on pages 8 and 9. For the moment, you should be able to

sufficiently understand the order so you can yourself draw the process diagram.

Essential reading

Read through part 1 of Airmic/Alarm/IRM (2010). This will provide you with

further information about the standard.

Activity 2.3

Briefly summarise the content of the five clauses of the ISO 31000 risk

management standard (one sentence for each clause)/.

2.2 Alternative risk management approaches

We conclude unit 2 with a brief review of some other approaches to risk

management.

Essential reading

Read the final part in Hopkin chapter 6 ‘Alternative approaches’.

RISK IN THE

REAL WORLD

Hopkin refers to one specialist standard called COBIT, which

provides guidance regarding information technology risk

management, in the box on page 68.

The CoCo framework can be seen as fitting around the internal environment of

COSO ERM. There is a relationship between governance, risk and compliance

(or GRC, which is a theme in module 2) – the board should focus on governance,

with separate risk functions overseeing the risk element, and a separate internal

audit function to monitor compliance.

Most countries of the world have their own corporate governance codes and

indeed there are some international codes. The rationale for a corporate

UNIT 2 | RISK MANAGEMENT STANDARDS

© 2016 Institute of Risk Management | 23

governance approach to risk management is that good risk management has to

start at the top of the organisation. The UK-based Cadbury Committee (1992), in

section 2.5 of its report on corporate governance, described this as the place

where ‘companies are directed and controlled’. In Module 2 you will study

corporate governance as a special topic.

In recent years there has been a trend to complement generic risk management

standards of the sort we have reviewed in this reading with industry-specific

ones. Before we complete this unit, we shall introduce one of them.

The Orange Book (HM Treasury, 2004) was designed in 2004 as a risk

management standard for the UK government sector and so is an example of a

sector-specific risk management standard. However, The Orange Book standard

is so succinct that it has generic value in its own right.

Essential reading

Read chapter 2 of The Orange Book which summarises The Orange Book’s risk

management model and gives a process diagram.

Note that the remaining chapters of The Orange Book describe each element of

the risk management model in detail.

Another sector-specific standard exists for the UK charity sector and we include

a reference to it as a further reading item at the end of the unit, if you are

interested to find out more.

As risk management systems develop in terms of maturity, advisory firms have

also designed their own risk management frameworks and toolkits. While each

promotes the unique selling points of that firm, the broad principles remain the

same: link to strategy objectives and core processes, risk identification,

assessment (or analysis), evaluation and action (treatment).

The article published by RIMS (2011) compares and contrasts a number of

different standards, including familiar ones, such as ISO 31000, COSO ERM,

IRM (2002) – which it calls the FERMA: 2002 standard – and some which are

MODULE 1 | PRINCIPLES OF RISK AND RISK MANAGEMENT

24 | © 2016 Institute of Risk Management

less popular, such as the Open Compliance and Ethics Group standard: 2009

(OCEG), BS 31100: 2011 and Solvency II: 2012.

Essential reading

Turn to RIMS (2011). Briefly look at the first thirteen pages, which are all about

comparing these standards. Pay most attention to the three standards we

covered in this unit. There is a set of comparison tables for the remaining eleven

pages.

Activity 2.4

1 From your work on this unit, do you think opportunity (the flip side of risk) is

adequately addressed by the risk management processes outlined in this unit?

2 Which of the standards and models that we introduced in this unit best fits

the way your organisation manages risks?

Self-assessment questions

These questions will help you to check your knowledge of Unit 2. You can check

with the answers at the end of this unit.

1 Which one of the following risk standards contains ‘control activities’ as a

feature in the risk process?

a) COSO ERM

b) ISO 31000

c) IRM (2002) standard

2 Which one of the following definitions is the same as the definition of the

risk management context?

a) The risk management strategy

b) The risk management process

c) The risk management framework

UNIT 2 | RISK MANAGEMENT STANDARDS

© 2016 Institute of Risk Management | 25

3 Which part of the risk framework focuses on answering the question ‘Who

does what?’ in the organisation in relation to risk management?

a) Risk architecture

b) Risk context

c) Risk protocols

Further reading

IRM’s ORC (2014) has a segment with a range of publications from many places

on the range of risk management standards. It even has the IRM standard of

2002 translated into many different languages.

IRM (2002) has a range of content which is very useful in several of the following

units of this module as well as module 2. It runs through the whole of the process

(relevant for module 1), as well as providing some information around risk

management framework roles, responsibilities, structures and administration

(relevant for module 2).

Praxiom (2013) is a very useful and easy to read article. It forms a plain English

guide to ISO 31000.

SA/SNZ HB 436:2013 Risk management guidelines - Companion to AS/NZS ISO

31000:2009 is a handbook which provides guidance on the implementation of

AS/NZS ISO 31000:2009 (this is ‘identical to and reproduced from ISO

31000:2009’). The handbook expands on and explains the elements within the

standard and provides advice about applying it, including using it to evaluate and

improve existing risk management practice. The guidelines can be obtained from

the web link given in the references section (Standards New Zealand, 2013), but

you should be aware that there is a cost to access the content.

In 2012 the Treasury Board of Canada Secretariat issued a substantial

guidebook similar to The Orange Book for the management of risk in the

Canadian government sector. If you are interested you can read it on Treasury

Board of Canada Secretariat (2012).

MODULE 1 | PRINCIPLES OF RISK AND RISK MANAGEMENT

26 | © 2016 Institute of Risk Management

Finally, in 2010 the UK Charity Commission issued guidelines for risk

management specific to the charity sector (Charity Commission, 2010).

Feedback to activities

Activity 2.1

1 Your definitions should be along the following lines

a) Risk standard – A published guide for managing risk, usually

comprising a risk framework and (especially) a risk process.

b) Risk framework – Also known as the risk management context. This

comprises the risk strategy, risk architecture and risk protocols and

forms the risk context which helps to drive the risk process.

c) Risk process – The stages in the process of managing risk, which is

driven mainly by how you set up the framework (but also affected by the

internal and external environment).

2 You might actually find some documentation in your department that already

does this. If not, it is a most useful exercise because it could help you to

consider whether there are any gaps in what you do.

Activity 2.2

1 Your definitions should be along the following lines

a) Risk architecture – Part of the risk framework, which focuses on

answering the question ‘Who does what?’ in the organisation in relation

to risk management. This is displayed in Hopkin’s figure 6.2 (page 61).

b) Risk context – This covers three layers of organisation which together

drive the risk process; they are the external environment, the internal

environment and the risk management context (also known as the risk

framework).

c) Risk protocols – The set of tools, procedures and instructions that an

organisation has for managing risk.

UNIT 2 | RISK MANAGEMENT STANDARDS

© 2016 Institute of Risk Management | 27

d) Risk strategy – The agreed overriding purpose and aims of risk

management in the organisation, which involves the publication of a risk

policy document and the setting of the risk appetite.

Activity 2.3

Clause 1: Scope or purpose of ISO 31000.

Clause 2: A set of definitions used in the standard.

Clause 3: The principles and purposes of risk management.

Clause 4: The stages involved in setting up a risk management framework.

Clause 5: The risk management process

Activity 2.4

1 From the range of processes that we have looked at, we can see from the

underlying definitions of risk that most are meant for dealing with both

opportunities and risks (with perhaps the exception of the 8Rs and 4Ts

approach – you should see why when we reach unit 6). But perhaps they

could be criticised in assuming that the process for managing opportunities

does not appear to be distinguished in any way from managing downside risk.

Perhaps you could answer this question by considering your own

organisation: Does your organisation manage opportunities in the same way

that it manages downside risk? If the answer to the question is yes, why

make the distinction between opportunities and risk in the first place?

2 This activity should help you to compare and contrast your process of risk

management with the established standards to find out which of them it most

closely mirrors. Look at the terminology that people use to see which

standard you most closely resemble. In the last three units of the module we

will look at each of the stages of the process in much more detail.

Answers to self-assessment questions

1-a

2-c

3-a

Unit 3 Enterprise risk management

Unit learning outcome

After studying this unit, you should be able to:

Apply the concepts of enterprise risk management (ERM)

Unit contents Section learning outcomes

3.1 Defining Enterprise risk management overview…29

Outline the key characteristics of the COSO ERM framework

3.2 Enterprise risk management overview…31 Explain the key features of an enterprise-wide approach to managing risk

3.3 Implementing ERM …33 Identify the four stages of the ERM implementation process

3.4 Establishing the context for risk management…35

Discuss the various approaches to establishing the context for ERM

3.5 Objective setting…37 Discuss approaches to setting objectives

Resources

You should make sure you have access to the following resources before starting this unit:

Hopkin (2014), chapter 19

The Orange Book (HM Treasury, 2004), chapter 10

COSO (2004)

Airmic/Alarm/IRM (2010), part 2

COSO (2014)

UNIT 3 | ENTERPRISE RISK MANAGEMENT

© 2016 Institute of Risk Management | 29

Introduction

Enterprise risk management (ERM) is probably the most important development

of risk management since the year 2000 because it offers a holistic approach to

risk management. Most of the risk management standards we introduced in unit

2 provide holistic guidance to risk management and so are really enterprise risk

management standards.

From the point of view of the International Certificate and Diploma, risk

management and ERM are synonymous, so this module takes an ERM approach

to risk management. Shortreed (2010: 118) sees ERM as a fundamental part of

general management:

‘The integration of ERM is made possible since risk relates to uncertainty

of achieving objectives and the goal of the general management of an

organisation is to achieve objectives.’

In this unit we will define and provide an overview of ERM. We will describe how

it can be implemented, the context within which it is implemented and the role of

objective setting. We will focus much of our attention on the COSO ERM

framework, but we will also consider ERM’s relevance to ISO 31000.

RISK IN THE

REAL WORLD

To give you an early flavour of an ERM approach to risk

management, take a look at the hotel sector case study in

Hopkin (page 200), which explains the TSOGO SUN risk

management process.

3.1 Defining Enterprise risk management

James Lam (2003), chief risk officer at GE Capital, described ERM as ‘the

integrated management of business risk, financial risk, operational risk and risk

transfer to maximise a firm's shareholder value’. His meaning was that ERM

makes a company more successful by creating a single view of all risks and

managing those risks in a consistent way up, down and across the enterprise.

MODULE 1 | PRINCIPLES OF RISK AND RISK MANAGEMENT

30 | © 2016 Institute of Risk Management

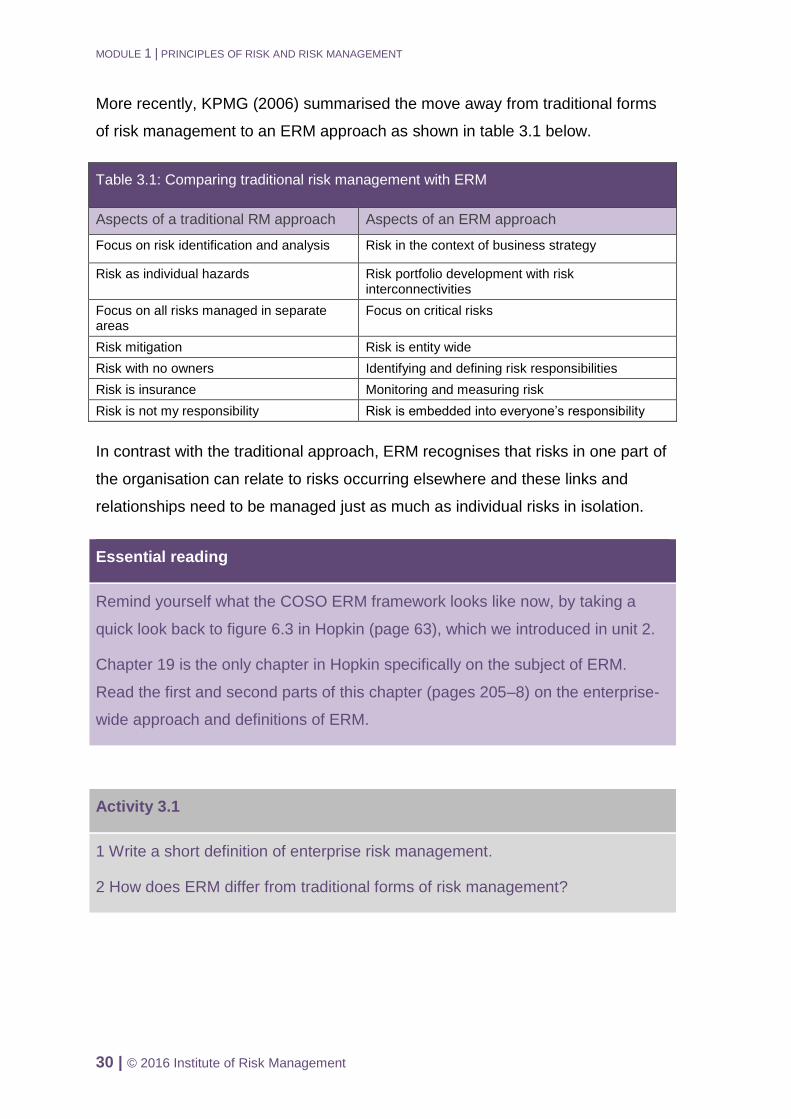

More recently, KPMG (2006) summarised the move away from traditional forms

of risk management to an ERM approach as shown in table 3.1 below.

Table 3.1: Comparing traditional risk management with ERM

Aspects of a traditional RM approach Aspects of an ERM approach

Focus on risk identification and analysis Risk in the context of business strategy

Risk as individual hazards Risk portfolio development with risk interconnectivities

Focus on all risks managed in separate areas

Focus on critical risks

Risk mitigation Risk is entity wide

Risk with no owners Identifying and defining risk responsibilities

Risk is insurance Monitoring and measuring risk

Risk is not my responsibility Risk is embedded into everyone’s responsibility

In contrast with the traditional approach, ERM recognises that risks in one part of

the organisation can relate to risks occurring elsewhere and these links and

relationships need to be managed just as much as individual risks in isolation.

Essential reading

Remind yourself what the COSO ERM framework looks like now, by taking a

quick look back to figure 6.3 in Hopkin (page 63), which we introduced in unit 2.

Chapter 19 is the only chapter in Hopkin specifically on the subject of ERM.

Read the first and second parts of this chapter (pages 205–8) on the enterprise-

wide approach and definitions of ERM.

Activity 3.1

1 Write a short definition of enterprise risk management.

2 How does ERM differ from traditional forms of risk management?

UNIT 3 | ENTERPRISE RISK MANAGEMENT

© 2016 Institute of Risk Management | 31

3.2 Enterprise risk management overview

ERM considers risks against the need to meet an organisation’s strategic,

operational, compliance and financial reporting objectives – the four elements of

the top face of the COSO ERM cube.

ERM ultimately implies that risk management should be ‘embedded’ from the top

of the organisation (entity level) downwards through the business. For ERM to

work effectively, it requires a high investment in risk management across the

enterprise, a high level of risk maturity and a strong framework for risk

assurance, because the board needs to know that the framework it has invested

in works effectively and consistently across the enterprise.

ERM stresses the need to consider the interdependency between risks. By

taking account of risk interrelationships and the interdependency of risks across

the enterprise, ERM will enable organisations to more accurately assess the

severity of their risks both individually and in total (this total assessment is

sometimes called the ‘risk exposure’).

RISK IN THE

REAL WORLD

For example, the outbreak of a major flu epidemic could

increase the likelihood of an IT risk event. If employees are

absent from work with flu, there are likely to be fewer people

around to monitor and enforce the organisation’s controls,

including IT controls. As a result, the controls are more likely to

fail. If the IT controls fail, we could then envisage the increased

likelihood of a financial risk arising, such as the inability to

place orders or invoice clients using the financial system.

Essential reading

Read the executive summary Enterprise Risk Management: Integrated

Framework, Executive Summary (COSO, 2004) which gives a good overview.

Page 1 summarises six characteristics of ERM, page 3 discusses the four

categories of organisational objectives and pages 3 and 4 describe the eight

MODULE 1 | PRINCIPLES OF RISK AND RISK MANAGEMENT

32 | © 2016 Institute of Risk Management

Essential reading

elements of the risk management process.

Activity 3.2

1 Explain why the first element on the side face of the COSO ERM cube is

described as ‘entity-level’.

2 Consider how one risk from a single source might impact on many departments

within your organisation.

RISK IN THE

REAL WORLD

Take a brief look at the case study on page 201 in Hopkin on

BG Group, a large energy company with widely dispersed

operations, which operates a group approach to managing

their ERM activities.

The companion research paper Improving organizational governance and

performance: how the COSO frameworks can help (COSO, 2014) explains how

the ERM process from the COSO cube can be used in a four-stage strategy

setting process. It argues that the starting point both to risk management and

strategy setting is a concept called ‘corporate governance’.

Essential reading

Have a brief look now at the research paper (COSO, 2014).

In addition to COSO ERM, there is also an internal control version. The COSO

Internal Control – Integrated Framework (COSO 1992, revised 2013) places the

emphasis on achieving internal control over financial reporting within the

organisation and for that reason it was later used as the framework of choice for

a very important piece of US law, the Sarbanes Oxley Act of 2002 – which you

will review in Module 2.

UNIT 3 | ENTERPRISE RISK MANAGEMENT

© 2016 Institute of Risk Management | 33

Learning activity 3.3

What are the driving forces in the development of ERM in your sector or country?

What are the main restraining factors?

3.3 Implementing ERM

This section considers techniques for implementing ERM. Bear in mind that:

Firstly, organisations will often employ a risk manager or a risk

management function to oversee the implementation and running of the

ERM framework. In some business sectors, such as banking and finance,

and in some countries of the world, the employment of a chief risk officer

is becoming a regulatory requirement.

Secondly, the PACED principles of risk management are essential factors

to take into account as part of the implementation of the ERM framework

in order to achieve the maximum benefits.

Thirdly, an organisation can assess the benefits of a fully implemented

and effective ERM framework by way of a process called FIRM (financial,

infrastructural, reputational and marketplace benefits). You could also

assess ERM benefits by the use of the MADE2 model.

In many ways, ERM implementation in an organisation is not really a type of risk

management but is more about a measure of the maturity of risk management

within the organisation. All things being equal, if you have ERM you are more

mature in risk management than if you do not have it.

Essential reading

Read the third part of Hopkin chapter 19 (pages 208–9) on ERM in practice.

Then skim read the fourth and fifth parts of Hopkin chapter 19 (pages 209–12) on

ERM and business continuity, ERM in energy and finance, and future

developments of ERM as we will consider these ideas later.

MODULE 1 | PRINCIPLES OF RISK AND RISK MANAGEMENT

34 | © 2016 Institute of Risk Management

The Airmic, Alarm, IRM guide (2010) identifies four stages to the implementation

process, using the acronym PIML:

planning and designing

implementing and benchmarking

measuring and monitoring

learning and reporting

Activity 3.4

Compare this process to the risk management ‘framework’ (or clause 4) of ISO

31000, which we looked at in reading 2. Can you see similarities between

clauses 4 and the Airmic, Alarm, IRM (2010) approach?

There are many guides and readings providing advice about the implementation

of ERM. In most cases, an overriding conclusion of these guides is that the

method of implementation will be contingent upon the risk characteristics of the

organisation concerned, along with its internal and external environment. In other

words, it is contingent on the ‘organisational context’ – a term we introduced in

unit 2 and will explore more next.

Essential reading

Skim read part 2 (pages 10–18) of the ‘Structured Approach to ERM’ guide

(Airmic/Alarm/IRM, 2010).

3.4 Establishing the context for risk management

Establishing the context for risk management is regarded in most risk