internal audit quality and financial reporting quality ... · internal audit quality and financial...

TRANSCRIPT

DOI: 10.1111/1475-679X.12099Journal of Accounting Research

Vol. 54 No. 1 March 2016Printed in U.S.A.

Internal Audit Quality and FinancialReporting Quality: The JointImportance of Independence

and Competence

L A W R E N C E J . A B B O T T ,∗ B R I A N D A U G H E R T Y ,∗S U S A N P A R K E R ,† A N D G A R Y F . P E T E R S‡

Received 5 November 2013; accepted 24 September 2015

ABSTRACT

In light of the growing importance of internal audit functions (IAF) and thelimited archival evidence on internal audit quality, we examine an interactivemodel of IAF quality (comprised of competence and independence) to bet-ter understand the determinants of IAF effectiveness as a financial reportingmonitor. Our tests support the hypothesis that the joint presence of compe-tence and independence is a necessary antecedent to effective IAF financialreporting monitoring. In sum, our results show that, the answer to “what is theeffect of internal audit competence (independence) on financial reportingquality?” is “it depends on the independence (competence) of the internalauditor.” Our study extends the understanding of IAF quality determinantsin the realm of financial reporting as it relates to ongoing discussions by re-searchers, standard setters, regulators, and practitioners.

∗University of Wisconsin–Milwaukee; †Santa Clara University; ‡University of Arkansas.Accepted by Philip Berger. We are grateful for assistance from Tim Seidel and helpful

comments from Cory Cassell, Dana Hermanson, Chris Hines, Adi Masli, Bill Messier, MarcyShepardson, David Wood, and workshop participants at Santa Clara University, University ofArkansas, Texas Tech University, the 2013 AAA Annual Meeting, and the 2012 Auditing Sec-tion Midyear Conference.

3

Copyright C©, University of Chicago on behalf of the Accounting Research Center, 2015

4 L. J. ABBOTT, B. DAUGHERTY, S. PARKER, AND G. F. PETERS

JEL codes: D83; G39; M12; M41; M42

Keywords: internal audit; financial reporting quality; auditor indepen-dence; auditor competence

1. Introduction

In 2013, the NASDAQ Stock Market LLC (NASDAQ) proposed a rulechange that would require all NASDAQ registrants to maintain an internalaudit function (IAF) (NASDAQ [2013]).1 The New York Stock Exchange(NYSE) has required registrants to maintain an IAF since 2006. The ra-tionale for these requirements is that an effective IAF provides the au-dit committee and other financial reporting stakeholders with critical in-formation pertaining to a company’s risks (including financial reportingrisks) and internal controls (i.e., Harrington [2004], NASDAQ [2013]).Similarly, corporate governance proponents consistently emphasize theIAF’s role in enhancing financial reporting quality (Coram, Ferguson, andMoroney [2008], Prawitt, Smith, and Wood [2009], Cohen, Krishnamoor-thy, and Wright [2010]). Nonetheless, the IAF’s role in the financial report-ing process is not yet fully understood and empirical evidence concerningthe impact of IAF quality is minimal.

We investigate the potential impact of IAF quality as a joint functionof the IAF’s competence and independence. We base this view upon thetheoretical work of DeAngelo [1981], who notes that external audit qualityis a function of the external auditor’s ability (i.e., competence) to detectaccounting misstatements and willingness (i.e., independence) to obligeproper accounting treatments. Similar to DeAngelo [1981], we assumethat, within the internal audit function, competence and independenceare important and distinct constructs that must interact to result in qualityoutcomes.

Despite the intuitive appeal of IAF quality positively impacting financialreporting quality, prior empirical evidence is not as strong as the intuitionwould suggest. For example, Prawitt, Smith, and Wood [2009], using datafrom 2000 to 2005, document mixed evidence between an overall com-posite measure of IAF quality and financial reporting quality. Their singlecomposite IAF quality measure adds several, equally weighted individualIAF characteristics of competence and independence. One potential ex-planation for prior mixed results revolves around how these IAF character-istics interact with each other in creating IAF quality. Rather than an addi-tive relation between competence and independence whereby an increasein competence can compensate for decreased independence, IAF quality

1 The NASDAQ subsequently tabled the proposal as registrants expressed concerns overthe costs and benefits of the proposal. An objective of the current study is to provide evidenceconcerning one aspect of the benefits.

INTERNAL AUDIT QUALITY AND FINANCIAL REPORTING QUALITY 5

may be more appropriately described as an interactive, two-factor functionof both competence and independence. Thus, IAF competence (indepen-dence) may be unlikely to impact financial reporting quality unless it is inthe presence of IAF independence (competence).

In this paper, we develop and test a two-factor model of IAF quality asa function of the IAF’s ability to prevent/detect financial misstatements(i.e., competence) and its inclination to report the misstatements to theaudit committee and/or external auditor (i.e., independence). Our studyuses survey evidence from 189 Chief Internal Auditors (CIAs) from For-tune 1000 companies during fiscal 2009.2 From this uniquely detailed andrich set of IAF data, we are able to create separate measures of IAF com-petence and independence. Our measure of IAF competence is based onthe average hourly rate of budgeted IAF resources (Abbott, Parker, andPeters [2012]). We also identify three potential factors related to IAF inde-pendence. First, consistent with Abbott, Parker, and Peters [2010, 2012],we measure the audit committee’s IAF influence vis-a-vis management’sIAF influence across multiple oversight dimensions.3 If upper management(rather than the audit committee) wields greater IAF influence, this maycause the IAF to fear reprisal should the IAF question management’s finan-cial reporting decisions, and thus diminish the IAF’s objectivity or indepen-dence (e.g., Cohen, Krishnamoorthy, and Wright [2010], Norman, Rose,and Rose [2010]).

In addition to audit committee IAF influence, a review of the IAF litera-ture reveals two other potential threats to IAF independence: whether theIAF serves as a management training ground (MTG) and the sizeable pres-ence of an IAF outside service provider (OSP). In particular, when the IAFis used as an MTG, internal auditors may be more reluctant to report finan-cial reporting issues in an effort to ingratiate themselves to upper manage-ment (Messier et al. [2011], Christ et al. [2015]). The presence of an OSPmay create job security concerns for the in-house IAF, as registrants mayfind the variable cost nature of OSPs attractive as a means of achieving costsavings and/or financial reporting flexibility (Abbott et al. [2007]).

We regress our IAF-related variables and a set of control variablesagainst common measures of financial reporting quality, abnormal accruals

2 As compared to other extant IAF research, our sample follows the implementation of thePublic Company Accounting Oversight Board’s (PCAOB) Auditing Standard No. 5 on theeffectiveness of internal control over financial reporting (ICFR), a period when substantialIAF resources were diverted to ICFR testing.

3 In contrast, prior research commonly utilizes a dichotomous influence variable basedupon whether the IAF’s formal reporting line is to the audit committee (e.g., Prawitt, Smith,and Wood [2009]). However, Abbott, Parker, and Peters [2010] note that 96% of Chief Inter-nal Auditors agreed with the statement “the Internal Auditor reports to the audit committee.”As such, the utilization of the formal reporting arrangement as the sole IAF independencecharacteristic leads to the possibility that the dichotomous identification of the reporting linecould simply capture a ceremonial structure and may not be indicative of a significant degreeof IAF independence.

6 L. J. ABBOTT, B. DAUGHERTY, S. PARKER, AND G. F. PETERS

(Kothari, Leone, and Wasley [2005], Prawitt, Smith, and Wood [2009]),and whether the firm just meets or beats analyst forecasts (Koh, Mat-sumoto, and Rajgopal [2008], Prawitt, Smith, and Wood [2009], Mandeand Son [2012]). Our abnormal accruals are further segregated intoincome-increasing and income-decreasing abnormal accruals. Consistentwith IAF quality being a two-factor, interactive function of independenceand competence, we document several statistically significant relations be-tween financial reporting quality and our interacted competence and in-dependence variables. We find that interactions between the IAF compe-tence and (1) the relative degree of audit committee IAF oversight and (2)the lack of a substantial OSP presence curtail both income-increasing andincome-decreasing abnormal accruals. We obtain similar results when weexamine the firm’s proclivity to just meet/beat analysts’ forecasts.

In contrast, when independence is proxied by whether the IAF is notused as an MTG, the interaction between the IAF independence factor andcompetence exhibits a statistically significant, mitigating impact on income-decreasing abnormal accruals. This finding is consistent with lower likeli-hoods of IAF reporting of inappropriate income-decreasing opportunisticreserve behaviors when the IAF is used as an MTG. In this manner, internalauditors hoping to move into a non-IAF position may endeavor to ingrati-ate themselves to management, or demonstrate their ability to be a teamplayer when they perceive a lower downside of doing so.4

Our paper contributes to the IAF literature in several ways. Our study isthe first to establish IAF characteristics as separate, distinct constructs thatact jointly in creating IAF quality. In doing so, this study contributes to ourunderstanding of IAF quality and the determinants of the IAF as an effec-tive internally based financial reporting monitor. Second, our results sug-gest that there are at least three factors that can impact IAF independenceand that these factors have differential interactive effects with IAF compe-tence in influencing financial reporting quality. In contrast, prior IAF liter-ature generally uses a dichotomous, single-variable independence measureand implicitly ignores other potential independence determinants (e.g.,Ahlawat and Lowe [2004]). Moreover, we find that our IAF independencecharacteristics are either not correlated or only weakly related to each otheror to our IAF competence measure. This is consistent with (1) IAF indepen-dence being characterized as a multifaceted attribute with at least three de-terminants and (2) IAF independence and competence being separate anddistinct constructs. While there is a very rich literature on threats to externalauditor independence, there is a paucity of archival evidence on the poten-tial determinants of internal auditor independence. With respect to internal

4 In terms of income-increasing abnormal accruals, internal auditors whose IAF serves asa management training ground may simply defer auditing more contentious, higher profileincome-increasing abnormal accruals to the external auditor. Internal auditors may do so withthe knowledge that external auditors are likely to expend greater audit effort on income-increasing accruals (Abbott, Parker, and Peters [2006]).

INTERNAL AUDIT QUALITY AND FINANCIAL REPORTING QUALITY 7

auditor competence, we also provide descriptive evidence of the qualifica-tions of the IAF staff and Chief Audit Executives (CAEs) in large firms, andthe types of functions those staff carry out. A more detailed understandingof the factors that influence IAF independence and competence should beof interest to researchers, standard setters, regulators, and practitioners intheir efforts to hone the IAF’s role as a financial reporting monitor.

Our study also provides archival evidence on the impact of third-partyIAF outsourcing on in-house IAF independence. Prior research has treatedoutsourcing as a threat to in-house IAF independence when the providerof such services was the external auditor (prior to the Sarbanes-Oxley Actof 2002 (SOX) when such service were allowed) (e.g., Ahlawat and Lowe[2004], Abbott et al. [2007], Prawitt, Sharp, and Wood [2012]). The evi-dence provided herein indicates that job security concerns can also be cre-ated by a large outsourcing presence unrelated to the external auditor. Fur-thermore, we find that over 65% of our sample IAFs have an outsourcingagreement in place and that close to 33% of our sample IAFs have a sizeableportion (i.e., in excess of 20%) of their budget allocated to OSPs. Giventhe pervasiveness of OSP-provided IAF services, we believe that future re-searchers should consider the nature and magnitude of OSPs in analyzingIAF independence.

Finally, we provide evidence that our IAF competence proxy, the hourlyin-house IAF rate, effectively summarizes several key IAF traits used in priorliterature that individually or collectively represent IAF quality, such astenure and certification (e.g., Prawitt, Smith, and Wood [2009], Lin et al.[2011]). Our competence variable has several attractive features for use infuture research as it (1) is continuous, (2) allows for comparison betweenIAFs of varying size, (3) does not require researcher judgment regardingthe weighting of IAF traits, and (4) does not require subjective judgmentby IAF respondents when collected via survey instrument.

Our study has several potential limitations. We draw survey data from asingle year, and 2009 was a year of significant economic events that mayhave affected the generalizability of our study in unknown ways.5 In addi-tion, discretionary accruals as a measure of management financial report-ing discretion, though widely used, are likely to measure the underlyingconstruct with error. Our test variables, similarly, are likely to contain mea-surement error. We have conducted a number of validity tests that are de-tailed in the sensitivity discussion, and support our IAF variables and results.Last, common to examinations involving internal attributes of an organiza-tion’s financial reporting environments, it is often difficult to disentanglethe potential endogeneity of the roles that reside within an organization(such as the IAF, Audit Committee, and Executive Suite). Nonetheless, webelieve our study offers insights into the operations of an increasingly im-portant component of the internal control systems of large companies.

5 We address this issue by conducting our analysis over the years 2010–2011, assuming thatour test variables would remain consistent over a short horizon. We find that our results con-tinue to be significant over that time frame.

8 L. J. ABBOTT, B. DAUGHERTY, S. PARKER, AND G. F. PETERS

2. Background and Prior Literature

Prior IAF research investigating audit outcomes generally focuses on theexternal auditor’s reliance on the IAF for financial statement audit assis-tance (e.g., Messier et al. [2011], Prawitt, Sharp, and Wood [2011], Abbott,Parker, and Peters [2012], Bame-Aldred et al. [2012]). This stream of re-search focuses on the two most prevalent IAF characteristics that extantaudit standards guide external auditors to consider: competence and inde-pendence.6 Competence generally refers to the auditor’s ability to performtasks diligently and in accordance with professional standards (e.g., IAASB[2013]). The Institute of Internal Auditors (IIA) defines competence as“the ability of an individual to perform a job or task properly, being a setof defined knowledge, skills and behavior” (IIA [2013, p. 2]). Within anIAF setting, independence is defined as “the freedom from conditions thatthreaten the ability of the internal audit activity to carry out internal auditresponsibilities in an unbiased manner” (IAASB [2013]). In other words,independence is often framed as objectivity or as the means to protectagainst bias, conflict of interest, or undue influence of others that wouldoverride professional judgments.

Prawitt, Smith, and Wood [2009] is the first archival study to link IAFquality to financial reporting quality. The IAF quality measure used inPrawitt, Smith, and Wood [2009] is a single, additive composite, comprisedof equally weighted metrics representing experience, certification, train-ing, IAF reporting structure, time spent on financial activities, and rela-tive IAF size. Using data from 2000 to 2005, the authors find that theircomposite measure of IAF quality is associated with mitigation of income-decreasing accruals, but not income-increasing accruals. When they disag-gregate their IAF characteristics, they find positive relationships betweenfinancial reporting quality and the IAF’s professional certifications(income-decreasing accruals) and IAF size relative to industry (income-increasing accruals).7 Prawitt, Smith, and Wood [2009] do not find signif-icant associations between the IAF independence characteristic (whetherthe IAF reports to the audit committee) and financial reporting quality.8

While their composite measure of IAF quality includes facets of compe-tence and independence, it is unclear when both of these characteristicsare present for a given firm and whether their relationship is interactive oradditive.

6 The AICPA’s Statement of Auditing Standards 65 (SAS 65) discusses indicators of IAFcompetence and independence; however, very little overlap exists among the factors that SAS65 describes as competence-related versus independence-related (AICPA [1991]).

7 They explain the unexpected result on IAF size as the possibility that IAF size proxies forthe difficulty of monitoring the firm, and, when monitoring is more difficult, managers maybe able to find avenues to exercise more discretion to increase income.

8 During the sample period involved (2000–2005), Prawitt, Smith, and Wood [2009] findsignificant variation in this measure: 69% of sample IAFs reported to the audit committee and,as such, this was likely to be an appropriate and parsimonious proxy for IAF independence.

INTERNAL AUDIT QUALITY AND FINANCIAL REPORTING QUALITY 9

Recent research points to other potential determinants of IAF indepen-dence and measures of how audit committees influence IAF independence,such as outsourcing presence, MTG usage, and perceived audit committeeinfluence. (Quarles [1994], Abbott et al. [2007], Messier et al. [2011], Ab-bott, Parker, and Peters [2012]). In sum, prior research has provided onlylimited evidence on the impact of IAF quality. Furthermore, a number ofIAF competence and independence measures have yet to be linked on astand-alone (or interactive) basis to financial reporting quality. Finally, theIAF profession has also identified other mechanisms that can influence IAFindependence that have yet to be investigated.

3. Hypothesis Development

3.1 IAF MECHANISMS FOR IMPACTING FINANCIAL REPORTING QUALITY

The focus of this paper is on the association between IAF quality andfinancial reporting quality. Therefore, an important antecedent to our re-search question is a description of the specific mechanisms by which anIAF can influence financial reporting quality. We posit that these opportu-nities arise within at least four activities: assisting with the financial state-ment audit, financial statement audit of subsidiaries, compliance auditing,and special consulting projects.9 Within the areas of financial statementaudit assistance and audits of subsidiaries, the IAF performs specific auditprocedures that allow it to potentially influence accrual decisions. These in-clude review of the financial closing process, reviewing procedures for non-standard journal entries and postclosing adjustments, and specific reviewsof critical accruals such as accounts receivable valuation and inventory re-serves (IIA [2005]). Compliance auditing can involve testing transactionsor journal entries for compliance with the company’s financial reportingpolicy. Special consulting projects may also involve the IAF delving into ac-counting matters that require greater judgment on the part of the preparer,such as asset impairments, warranty reserves, collectability reserves, and/orinventory write-downs (PwC [2009]).

It should be noted that, in any of the prior tasks, the IAF may encounterhigh-level accruals choices. More specifically, the IIA advises that, as a partof the quarterly financial reporting process, the IAF should engage the IAFshould review the policies, procedures, and process for reporting and re-lated disclosures. In particular, the IIA advises that, as a part of the quarterlyfinancial reporting process, the IAF should engage “special or specificallytargeted reviews of high-risk, complex, and problem areas; including ma-terial accounting estimates, reserve valuations, off-balance sheet activities,major subsidiaries, joint ventures, and special purpose entities” (IIA [2005,p. 236]).

9 We developed this list from a review of the prior literature, examination of IAF profes-sional guidance, and discussion with CIAs. As discussed in our results section, respondentsindicate a nontrivial budget allocation to these four activities.

10 L. J. ABBOTT, B. DAUGHERTY, S. PARKER, AND G. F. PETERS

3.2 AUDIT COMMITTEE IAF OVERSIGHT IN THE INTERACTIVE IAF QUALITYMODEL

This study’s examination of IAF quality—and its potential impact on fi-nancial reporting quality—asserts that competence and independence arenecessary, but not individually sufficient determinants of IAF quality. Weinvestigate the potential impact of IAF quality as a joint function of theIAF’s competence and independence. While it is expected that a compe-tent auditor is more likely to discover a financial reporting misstatement,the reporting of the discovered misstatement is contingent upon the audi-tor’s independence or objectivity. Similar to DeAngelo [1981], we assumethat competence and independence are distinct constructs that must inter-act to ultimately impact financial reporting quality.

Our first hypothesis pertains to the interaction of IAF competence andIAF independence, measured by audit committee or C-Suite influence.Both external and internal auditing standards assert that internal auditorindependence is a direct function of the reporting relationship between theaudit committee and the IAF (IIA [2002], AICPA [2013]). However, eventhough official reporting by the IAF to the audit committee is common,the extent and effects of active oversight by the audit committee and unof-ficial oversight by management varies greatly (e.g., Ernst & Young [2008],Mabry and Schwartz [2008], Hoffelder [2012]). Moreover, prior academi-cians highlight the inherent conflicts of IAFs serving both managementand the audit committee (Hermanson [2002], Anderson [2003], Herman-son and Rittenberg [2003]).

Prior research supports an association between greater audit committeeoversight and greater independence for the IAF. For example, greater auditcommittee oversight of the IAF is associated with the greater shielding frompossible management pressure (Quarles [1994], Carcello, Hermanson, andRaghunandan [2005]).10 If the IAF is not sufficiently shielded from possiblemanagement pressure, the CEO or CFO can reduce the likelihood that theissue will be reported to the proper channel. When the departure fromreporting policy originates at the C-Suite level, the IAF’s independence isparticularly important. A lack of independence of the IAF from the C-Suitemay preclude the IAF from initiating a review of financial reporting choicesmade at the CFO/CEO level. This may prevent the discovery and reportingof financial reporting policy departures.11

10 For example, the internal auditors may be charged with reviewing the proper applicationof the firm’s policy for recording an inventory reserve. Divisions within the firm with sepa-rate profit targets may have incentives to either under- or overstate the reserve in order tomaximize internal rewards.

11 This mechanism may operate in two ways. First, the CEO/CFO may effectively pressurethe IAF to “filter” any IAF-generated reports that are forwarded to either the audit committeeor external auditor. Second, to the extent that the CEO/CFO can influence IAF budgets oractivities, the CEO/CFO may direct the IAF toward other activities that have an immediate,beneficial impact on current earnings such as the examination of vendor rebates or other

INTERNAL AUDIT QUALITY AND FINANCIAL REPORTING QUALITY 11

Following our expectations, we posit that, as audit committee IAF influ-ence (IAF independence) increases, the likelihood that a misstatement discov-ered by a competent IAF is either (1) properly reported to the audit commit-tee and external auditor or (2) corrected by the party responsible for theoriginal misstatement also increases. Both scenarios lead to greater finan-cial reporting quality. This leads to our first hypothesis (stated in alternativeform):

H1: The interaction between IAF competence and audit commit-tee IAF influence is positively associated with financial reportingquality.

3.3 THE IAF AS AN MTG IN THE INTERACTIVE IAF QUALITY MODEL

The second IAF independence determinant interacted with IAF compe-tence is the organization’s use of the IAF as an MTG. Prior research suggeststhat the use of IAF as an MTG is prevalent among corporate entities (Stew-art and Subramaniam [2010], Messier et al. [2011], Christ et al. [2015]).Many organizations see this as a means to attract and develop corporate tal-ent by instituting both formal and informal rotations within the IAF (Ernst& Young [2008]). Despite these intended benefits, other IAF constituentssee this as a potential threat to the independence of the IAF (Good-win and Yeo [2001], Ahlawat and Lowe [2004], Christopher, Sarens, andLeung [2009]). Although concerns about both the costs and benefits ofthis practice remain, the use of the IAF as an MTG is common (Prawitt,Smith, and Wood [2009]).

To date, few studies directly investigate the impact of MTGs on IAF inde-pendence (Stewart and Subramaniam [2010]). Messier et al. [2011] docu-ment a negative association between the use of the IAF as an MTG and theexternal auditor’s assessment of IAF independence. Despite the negative ef-fect on perceived independence, MTGs were not associated with perceiveddifferences in internal audit competence. This provides further evidencesuggesting that independence and competence are separate and distinctconstructs.

When the IAF is an MTG, the IAF may be less likely to report the finan-cial misstatement to the appropriate channel. If the misstatement reflectsnegatively on the division’s management, those managers may be less likelyto offer that particular internal auditor a position within that division. Pos-itive internal references may be less likely for an internal auditor seekinga position at a different division within the same company. In order for amisstatement to be corrected prior to the consolidation of results at theparent level, both IAF competence and independence must be present.As with our prior hypothesis, we consider the financial reporting quality

operational concerns, etc. (Abbott, Parker, and Peters [2010]). In doing so, the IAF is ef-fectively precluded from collecting evidence that might serve to repudiate other compliancedeviations involving financial reporting decisions.

12 L. J. ABBOTT, B. DAUGHERTY, S. PARKER, AND G. F. PETERS

consequences of the joint importance of IAF independence and compe-tency when independence is potentially conditioned by the explicit use ofIAF as an MTG. This leads to our second hypothesis (stated in alternativeform):

H2: The interaction between IAF competence and an IAF that is notused as an MTG is positively associated with financial reportingquality.

3.4 OUTSOURCED INTERNAL AUDIT ACTIVITIES IN THE INTERACTIVE IAFQUALITY MODEL

The final IAF independence factor interacted with IAF competence isthe presence of a substantial OSP. Outsourced IAF activities represent on-going sourcing strategies for many internal audit departments (Stewart andSubramaniam [2010]). Outsourcing all or a portion of the IAF providesmanagement with the flexibility of adjusting IAF costs during the courseof the year because outsourced IAF hours are essentially variable in na-ture. In contrast, in-house IAF hours are fixed in nature due to salary struc-tures. Moreover, outsourced IAF activities can allow management to deferexpense recognition into subsequent accounting periods by simply schedul-ing outsourced IAF activities into following years. This contracting flexibil-ity may be especially attractive to management when the firm is faced withrevenue shortfalls.

Despite potential benefits of IAF outsourcing, there may be a cost in theform of decreased, in-house IAF independence. In particular, Abbott et al.[2007] and Quarles [1994] note that a substantial IAF outsourcing pres-ence may undercut the in-house IAF’s willingness to confront managementon issues due to concerns over job status. If an internal auditor feels “re-placeable” as a consequence of outsourcing, he may be less willing to reporta misstatement to the appropriate outlet for fear of losing his job withinthe firm (Quarles [1994], Abbott et al. [2007]). As before, increased inde-pendence, in this case the lack of a substantial IAF outsourcing presence,increases the likelihood that a misstatement discovered by a competent IAFis properly reported or corrected by the party responsible for the misstate-ment.12 As already stated, we consider the financial reporting quality con-sequences of the joint importance of independence and competency whenin-house IAF independence is potentially influenced by the presence ofoutsourced IAF services. This leads to our third hypothesis (stated in thealternative):

H3: The interaction between IAF competence and the lack of asubstantial IAF outsourcing presence (increased IAF indepen-dence) is positively associated with financial reporting quality.

12 Though we feel the preponderance of evidence points to a positive association betweenreporting quality and the lack of an OSP, we acknowledge that it is possible that the use of anOSP might instead serve to spur the IIA to greater effort and independence in order to provetheir worth to the organization.

INTERNAL AUDIT QUALITY AND FINANCIAL REPORTING QUALITY 13

4. Research Design

4.1 SAMPLE SELECTION

Our study utilizes a survey questionnaire (see appendix) sent to 909 non-bank members of the FORTUNE 1000 (in terms of total sales).13 Consistentwith most prior internal audit research (e.g., Pelfrey and Peacock [1995],Scarbrough, Rama, and Raghunandan [1998], Raghunandan, Read, andRama [2001], Carcello, Hermanson, and Raghunandan [2005], Abbott,Parker, and Peters [2010, 2012]), the survey targets Chief Internal Audi-tors (CIAs) or Chief Audit Executives (CAEs). The survey includes ques-tions about the types of IAF services provided (whether in-house or out-sourced), assistance to the external auditors, presence and activities of anyOSPs, the reporting relationship between the IAF and the audit commit-tee, and whether the IAF serves as an MTG. We asked recipients to provideresponses based upon fiscal year 2009.

The first survey mailing (sent October 2009) resulted in a total of 118usable responses. A follow-up mailing (December 2009) produced an ad-ditional 99 usable responses, for a total of 227.14 However, we were unableto obtain complete Compustat data for 38 of these firms, bringing our to-tal sample to 189. Table 1 provides a distribution of observations by two-digit focus industry membership (Hogan and Jeter [1999]). To test for po-tential nonresponse bias, we compare the characteristics of the early andlate responders with each other and test for significant differences in size,leverage, return on assets, presence of a loss, and cash flow from opera-tions. None of the differences are significant.15 We also compare our re-spondents to the industry makeup of the original population of nonbankFortune 1000 firms. We conduct a test of differences of proportions com-paring the industry sample representation to the population and find onlythe underrepresentation of the energy and manufacturing sectors to besignificant.

4.2 CHARACTERISTICS OF THE IAF

Our survey responses provide information about the current nature ofthe IAF function in terms of qualification and activities. We document thatthe overwhelming majority (over 80%) of CAEs have a CPA certification

13 Banks are excluded since they do not possess inventory and have unique regulatory envi-ronments. We identified 909 nonbank firms within the Fortune 1000.

14 Our effective response rate of 20.7% (or 189 responses/909 total companies) comparesfavorably with the 12.7% rate obtained by Felix, Gramling, and Maletta [2001] in their internalaudit study. However, the Felix et al. rate may have been depressed by the need for surveyresponses from both the internal and external auditors to constitute a complete sample pair.Our response rate is higher than that reported in previous studies of senior managers. Forexample, Graham and Harvey [2001] report a 9% response rate.

15 As with all surveys, there is a possibility of unknown response bias and of incorrect re-sponses. While we tested our early and late respondents for differences on a number of di-mensions, as previously discussed, it is possible that undetected bias is present.

14 L. J. ABBOTT, B. DAUGHERTY, S. PARKER, AND G. F. PETERS

T A B L E 1Sample Selection Results

Related Two- No. of % of No. of Fortune % of FortuneFocus Industry Digit SIC Codes Firms Sample 1000 Firms∗ 1000 Firms∗

Construction 15–17 9 4.8 17 1.9Consumer product &

food20–33 43 22.8 180 19.8

Energy 10–14, 46, 49 32 16.9 172 18.9Financial services 60–64, 67 11 5.8 62 6.8Information &

Communication48, 73, 78, 79, 84 20 10.6 126 13.9

Manufacturing 34–39 31 16.4 140 15.4Personal services &

health care72, 80, 83 2 1.1 28 3.1

Professional,commercial services,education

75, 76, 82, 87, 89 1 0.5 11 1.2

Real estate 65, 70 1 0.5 6 0.7Retail & wholesale 50–59 35 18.5 149 16.4Transportation 40–42, 44, 45, 47 3 1.6 11 1.2All other 1, 2,7, 8, 99 1 0.5 6 0.7Totals 189 100 908 100

∗Banks are excluded from both the population and the sample as these firms face additional regula-tion unique to their industry and do not have significant inventory accounts (making the model unfit forregression purposes). The remaining Fortune 1000 firms (in terms of total assets) serve as our samplingpopulation.

while, perhaps surprisingly, only 39% have a Certified Internal Auditor(CIA) certification. Responses also indicate that the CISA certification isrelatively rare among CAEs (at approximately 10%). As a reflection of thechanging and increasing importance of systems-based auditing, we find thatthe CISA certification is much more prevalent (16%) among staff. At thestaff level, the CPA certification dominates, though less than half of staff(40%) have a CPA certification, while over a quarter of staff have a CIAcertification (28%). The CPA-CIA certification “gap” is lower for staff (40%vs. 28%) than it is for CAEs (82% vs. 39%). The CPA-CIA certification gapindicates that the current generation of CAEs was most likely hired fromexternal audit firms. Experience in financial statement auditing is stronglycorrelated (0.88) with the possession of a CPA. We believe this provides in-formation about the composition of the IAF at both the staff and executivelevel.

We also provide descriptive statistics about what activities IAFs are per-forming. We note that 100% of survey respondents allocated a portion oftheir annual IAF budget to Section 404–related work. Second, the meanpercentage of in-house IAF budgets allocated to Section 404 assistancewas 27.5%—the highest budget allocation percentage among IAF activities.Sample results indicate that over 65% of our sample IAFs have an outsourc-ing agreement in place and that, on average, close to 31.8% of outsourcedIAF budgets are dedicated to Section 404 assistance. Thus, if an outsourced

INTERNAL AUDIT QUALITY AND FINANCIAL REPORTING QUALITY 15

IAF is utilized, it is utilized heavily to provide Section 404 assistance. This re-sult is consistent with our contention that a significant OSP presence couldrepresent a threat to internal IAF independence since there is a large over-lap in the services that are provided by in-house IAFs vis-a-vis OSPs.

4.3 REGRESSION MODEL

To test the relationship between financial reporting quality and the inter-active nature of IAF competence and independence, we adapt the followingregression model from prior research:

ABNACC = b0 + b1IACOMP + b2ACIAFINF + b3NONMTG

+ b4NONOSP20 + b5IACOMP ∗ ACIAFINF

+ b6IACOMP ∗ NONMTG + b7 IACOMP ∗ NONOSP20

+ b8ASSETS + b9 AGE + b10LEVERAGE + b11SEGNUM

+ b12CFO + b13SALESGROW + b14MTB + b15CFOVOL

+ b16ROA + b17 LOSS + b18MATWEAK

+ b19−28INDUSTRY + ε. (1)

The variables used in the empirical models are summarized in table 2 anddiscussed below.

4.4 DEPENDENT VARIABLE

Following prior audit literature, we utilize abnormal accruals (ABNACC)as a proxy for financial reporting quality (Francis [2011]). To measure ab-normal accruals, we use the performance-adjusted cross-sectional variationof the modified Jones model (Dechow, Sloan, and Sweeney [1996]) as re-ported by Kothari, Leone, and Wasley [2005].16 The Kothari et al. modelincludes both an intercept term and a measure of performance. Consistentwith prior research, we first estimate the model for firms with informationavailable on Compustat for 2009 (excluding financial institutions), and ap-ply the results by two-digit SIC code to the calculation of abnormal accrualsfor the firms in our sample.17 Our estimate of abnormal accruals is theresidual from the following regression:

[TAit/Ait−1] = β0 + β1[1/Ait−1] + β2[(�REVit − DARit)/Ait−1]

+β3[PPEit/Ait−1] + β4[NIit/Ait−1] + εi t .

16 Our sample size, though small compared to many discretionary accruals studies, is similarto other survey-based work in the area (Prawitt, Smith, and Wood [2009], Prawitt, Sharp, andWood [2012]).

17 In separate untabulated tests, we also limited data for the estimation model to only For-tune 1000 firms. However, there were a total of 47 firms (almost a quarter of our sample)for which we could not estimate a reliable accrual estimation model. Thus, our tabulated AB-NACC variable based upon the Compustat population represents a tradeoff between capturingadditional business norms that drive transactional accruals within a given industry (popula-tion based) versus transaction accruals that might be limited to only a large-firm environment(large-firm subsample).

16 L. J. ABBOTT, B. DAUGHERTY, S. PARKER, AND G. F. PETERS

T A B L E 2Variable Definitions

Variable Description

ABNACC The Kothari, Leone, and Wasley (2005) version of the modified Jonesmodel measure of abnormal accruals. Abnormal accruals is the errorterm of the equation below:[TAit/Ait−1] = β0 + β1[1/Ait−1] + β2[(DR E Vit − DARit )/Ait−1] +β3[PP Eit/Ait−1] + β4[N Iit/Ait−1] + εi t ,where total accruals for estimation portfolio firm i for year t. TA, or totalaccruals, are defined as income before extraordinary items (CompustatData Item #18) minus operating cash flows (Data Item #308). Ait−1 istotal assets (Data Item #6) at t−1 for firm i. �REVit is the change in netrevenues (Data Item #12) for estimation portfolio firm i for year t. �ARit

is the change in accounts receivable (Data Item #2) for estimationportfolio firm i for year t. PPEit is gross property, plant, and equipment(Data Item #7) for estimation portfolio firm i for year t. NIit is netincome (Data Item #172) for estimation portfolio firm i for year t.

JM/BEAT∗ Dichotomous dependent variable coded “1” in instances where firm metthe forecast or exceeded it by the consensus, annual EPS forecast scaledby price at the beginning of the year by more than 0.0005; “0” else.

JM/BEATaccr∗ Dichotomous variable calculated using a two-step process. First, we

calculate unmanaged earnings by backing out discretionary abnormalaccruals from reported earnings. We then identify firms that would havemissed analysts’ forecasts, without management’s exercise of theaccounting discretion. For these firms, JM/BEATaccr equals “1” and for allother firms JM/BEATaccr equals “0.”

IACOMP Average IAF resource expenditure per hour. Calculated by dividing totalin-house IAF budget per survey question #4 by total in-house IA hoursper question #1.

ACIAFINF Relative audit committee IAF influence vis-a-vis management (CEO andCFO). Measured as the ratio of the total agreement points for the auditcommittee in the numerator divided by the total agreement points forthe CFO and CEO in the denominator. The numerator is the sum ofagreement points (per the 1–5 Likert-scale responses) on surveyquestions #12a, 12d, and 12g. The denominator is the sum of agreementpoints (per the 1–5 Likert-scale responses) on survey questions #12a–12i. The 1–5 Likert-scale response values are recalibrated to 0–4 forpurposes of computing this variable.

NONMTG Indicator variable coded “1” when the IAF does not serve as amanagement training ground per survey question #13 and “0”otherwise.

NONOSP20 Coded “1” (“0”) when the following ratio constructed from surveyquestion #4 is less than (greater than) 0.20: (Budgeted OSP $)/(BudgetedOSP $ + Budgeted in-house IAF $).

ASSETS Total assets in millions (Compustat Data Item #6).AGE Number of years the firm was listed on Compustat, truncated at 25 yearsLEVERAGE The sum of long-term debt (Compustat Data Item #9) and current

liabilities (Data Item #5) of a company divided by total assets (Data Item#6).

SEGNUM Number of disclosed segments in which the company operates.CFO Cash flows from operations (Compustat Data Item #308).

(Continued)

INTERNAL AUDIT QUALITY AND FINANCIAL REPORTING QUALITY 17

T A B L E 2—Continued

Variable Description

SALESGROW One year sales growth (Compustat Data Item #12FY2009 – Item #12 FY2008/Item #12 FY2008).

MTB A company’s market-to-book ratio (Compustat Data Item #24 ∗ Item #25/ Item #216).

CFOVOL Standard deviation of operating cash flows for 2005–2009.ROA Return on assets (Compustat Data Item #172 / Data Item # 6).LOSS Coded “1” if the firm experienced a loss in fiscal year 2008, “0” else.MATWEAK Indicator variable coded “1” for client firm disclosing a material

weakness in internal controls over financial reporting during the priortwo years and “0” otherwise.

INDUSTRY Coded “1” if firm’s two-digit SIC code is included in specific focusindustry per table 1, “0” otherwise. Focus industry groupings per Hoganand Jeter (1999).

∗Variable used only in additional analysis section.

We then segregate our abnormal accruals as positive (income-increasing)and negative (income-decreasing) abnormal accruals. Our predicted rela-tions are symmetrical for negative and positive accruals. We argue that, ifthe information used for internal decision-making is incorrectly biased ineither direction, there may be career penalties for the internal auditor.

4.5 TEST VARIABLES

Our test variables are IACOMP, ACIAFINF, NONMTG, and NONOSP20,and their respective interaction terms. Consistent with Abbott, Parker, andPeters [2012], IACOMP is a proxy for IAF’s competence. IACOMP is definedas the average in-house IAF resource expenditure per budget hour. We di-vided total in-house IAF budget per survey question #4 by total in-houseIA hours per question #1. On average, the resource commitment per hourof budgeted audit staff should capture and summarize several disparate di-mensions of IAF competence such as educational level, professional expe-rience, and certification of the IAF staff. When we compare IACOMP to thePrawitt, Smith, and Wood [2009] IAF quality measure, we find that most ofthe elements of the Prawitt, Smith, and Wood [2009] measure are relatedto competence (experience, certifications, training, IAF size (a measure ofunexpected spending on the IAF)). We suggest these individual IAF traitsare captured by an hourly, in-house IAF compensation rate.18

18 We believe our composite IACOMP measure offers other certain advantages, as it incor-porates many different IAF elements (i.e., experience, certification, training) into one sum-mary measure, is continuous in nature (allowing for easier comparison between different-sizedIAFs), and does not require an implicit equal weighting of inputs. Due in part to the underly-ing relationship between budgets and hours, we include additional subsequent tests to ascer-tain whether our proxy is correlated with various dimensions of competence. See additionalanalysis discussions. Utilizing per hour amounts strengthens our ability to capture individualauditor traits that might otherwise be lost when utilizing a measure of competence based upon

18 L. J. ABBOTT, B. DAUGHERTY, S. PARKER, AND G. F. PETERS

Following Abbott, Parker, and Peters [2012], we incorporate a separatecontinuous measure of audit committee influence into our tests of IAF in-dependence. Prior internal audit research suggests that oversight roles orinfluence, though potentially prescribed by a charter, do not necessarilymanifest themselves in practice as dichotomous characteristics (Kaplan andSchultz [2006], Ernst and Young [2008], Rose and Norman [2008]).19

Therefore, ACIAFINF is defined as the relative level of influence exertedover the IAF by the audit committee vis-a-vis management. To measure ACI-AFINF, we asked (survey question #12) CIAs to state their level of agree-ment concerning the amount of influence exhibited by the audit commit-tee versus management (CEO and CFO) on reporting lines, terminationrights, and budget determination.20 The level of agreement can range fromstrongly disagree (“1”) to strongly agree (“5”). We then construct a ratioof the total agreement points for the audit committee in the numerator(i.e., the sum of agreement points for survey questions #12a, 12d, and 12g)divided by the total agreement points for the audit committee, CFO, andCEO in the denominator (i.e., the sum of agreement points for survey ques-tions #12a–12i).21

To further illustrate ACIAFINF, if the CIA answers “5” (i.e., stronglyagrees) to all survey questions #12a–12i, then the audit committee is seenas an equal IAF oversight partner with management. Our ACIAFINF vari-able would receive a value of 0.33, denoting 33% relative oversight of theIAF, vis-a-vis management. If, however, the CIA strongly disagrees with anyCEO/CFO relationship, while strongly agreeing with all audit committeerelationships, our ACIAFINF variable equals 1, denoting full IAF control bythe audit committee.22

IAF budgets deflated by firm size. Defining IACOMP as Budgets / Firm size yields inconclusiveresults, likely due in part to its lack of correlation with individual auditor competence traitsthat drive per hour costs. We thank the anonymous reviewer for bringing this to our attention.

19 Ernst and Young [2008] notes that audit committees take different approaches to thelevel of active oversight of the internal audit department, in which the internal auditor mayperceive different levels of actual influence or authority exhibited by the corresponding over-seer.

20 Similar to Abbott, Parker, and Peters [2010], we do not utilize answers to survey question#12j–12l (reviewing/approving the IAF’s annual risk assessment plan) when calculating theACIAFINF variable.

21 Within upper management, the IAF can report to either or both the CEO and CFO. Wecombine the CEO and CFO responses since both share common risk preferences (comparedto the Audit Committee) and are required by SOX Section 302 to certify the financial state-ments (SOX [2002]).

22 Survey responses to questions #12a–12i can range from 1 to 5, but are recalibratedto a scale of 0–4. By doing so, our ACIAFINF variable captures the intuition behind therelative IAF influence. For example, assume that the CIA respondent strongly agrees withthe audit committee’s influence over IAF reporting, termination, and budgeting (i.e., re-sponds with a “5” for survey questions 12a, 12d, and 12g). Also assume the CIA respon-dent also strongly disagrees with the CEO and CFO’s influence over IAF reporting, termi-nation, and budgeting (i.e., responds with a “1” for survey questions 12b/12c, 12e/12f, and

INTERNAL AUDIT QUALITY AND FINANCIAL REPORTING QUALITY 19

NONMTG represents our second facet of the IAF’s independence,namely, whether IAF is formally used as an MTG. NONMTG is coded “1”when the IAF is not part of a management training rotation, but instead isconsidered a separate career position within the company (survey question#13). The results of viewing the IAF as a distinct career position potentiallyinduces greater attachment by the staff to the role of professional inter-nal auditor, and thus a greater commitment to independence. In addition,those professionally attached to the IAF are less likely to feel pressure fromaudited managers in order to protect future placement opportunities.

NONOSP20 represents the extent of the threat to the in-house IAF pre-sented by the extent of outsourcing. Limited outsourcing may be related tothe need for specialized expertise not possessed by the IAF, but larger levelsof outsourcing may indicate a willingness on the part of a company to con-sider outsourcing core IAF functions. We identify outsourcing of more than20% of the total budget as an appropriate level to indicate a possible threatto the IAF. The initial 20% threshold is based upon informal conversationswith internal auditors concerning the level at which outsourcing would ap-pear to threaten job security. We expect that, as the level of outsourcingincreases, the in-house IAF may view itself as vulnerable to replacement,thus reducing the internal IAF’s independence. NONOSP20 is coded “1” ifthe level of outsourcing does not reach 20%, reflecting little or no threat toIAF independence. The extent of outsourcing is constructed from surveyquestion #4:

(Budgeted OSP $

)/(Budgeted OSP $ + Budgeted in-house IAF $

).

Each of our stated hypotheses addresses the interactive nature of IAFcompetence and separate measures of independence. We test H1 by inter-acting IACOMP and ACIAFINF. We test H2 by the interacting IACOMP andNONMTG. We test H3 by interacting IACOMP and NONOSP20. In all threeinteractions, we expect a negative (positive) association with abnormal ac-cruals (financial reporting quality).

4.6 CONTROL VARIABLES

We include control variables that may impact the level of abnormal ac-cruals. We expect that ASSETS (log of company size) will magnify the size

12h/12i). Without recalibration to a 0–4 scale, the ACIAFINF value would equal 0.833 (e.g.,(5+5+5)/(5+1+1+5+1+1+5+1+1)). With recalibration, the ACIAFINF value becomes 1 or((4+4+4)/(4+0+0+4+0+0+4+0+0)). A second example further illustrates. In this case,assume that the CIA strongly disagrees with the audit committee’s IAF reporting, termina-tion, and budgeting influence (i.e., responds with a “1” for survey questions 12a, 12d, and12g) and also strongly agrees with the CFO’s reporting, termination, and budgeting influence(i.e., responds with a “5” for survey questions 12b, 12e, and 12h). Also assume that the CIAstrongly disagreed with the CEO’s IAF reporting, termination, and budgeting influence (i.e.,responds with a “1” for survey questions 12c, 12f, and 12i). In this case, ACIAFINF equals 0(e.g., (0+0+0)/(0+4+0+0+4+0+0+4+0)).

20 L. J. ABBOTT, B. DAUGHERTY, S. PARKER, AND G. F. PETERS

of accruals (Dechow and Dichev [2002]). For this reason, we predict a pos-itive association between company size and positive accruals and a negativeassociation between company size and negative accruals. AGE (number ofyears the company has been listed on Compustat, truncated at 25 years) isincluded because firms may experience different accrual patterns as theyage (Prawitt, Smith, and Wood [2009]). We expect that LEVERAGE (to-tal debt/total assets) will be associated with more income-increasing ac-cruals to allow for nonviolation of debt covenants (Press and Weintrop[1990]) and income-decreasing accruals (DeAngelo, DeAngelo, and Skin-ner [1994]) to reduce earnings for contractual renegotiations. We includea variable that proxies for firm complexity using the number of operatingsegments a firm discloses in its 10K (SEGNUM). Firms with greater complex-ity may have greater financial reporting latitude due to the inherent com-plexity of their operations. We therefore expect that SEGNUM will be pos-itively (negatively) associated with income-increasing (income-decreasing)abnormal accruals. CFO (operating cash flows), SALESGROW (sales growthfrom the prior year), and MTB (market to book) are included to control forgrowth, and CFOVOL (operating cash flow volatility) is included because itmay impact the accrual calculation (Dechow, Sloan, and Sweeney [1996],Matsumoto [2002], Menon and Williams [2004]).

Low performance provides an incentive for accruals management, so weinclude ROA (net income/assets) and LOSS (coded “1” if the firm experi-enced a loss in the preceding year, “0” else). In terms of income-increasingabnormal accruals, increases in ROA may impact the calculation of ab-normal accruals and we expect a positive relation. In terms of income-decreasing accruals, positive ROA provides incentives to “smooth” earningsand we expect a negative association between ROA and income-decreasingabnormal accruals. Firms with a net loss may have an incentive to magnifyincome-increasing abnormal accruals to avoid debt covenant violations andmagnify income-decreasing abnormal accruals to “take a bath.” We there-fore expect a positive (negative) association between LOSS and income-increasing (decreasing) abnormal accruals. We also include an indicatorvariable for the presence of material internal control weaknesses. Mate-rial weaknesses have been shown to be associated with an increase in ab-normal accruals (Doyle, Ge, and McVay [2007]). Finally, consistent withprior accruals-based research, we include dummy variables for focus indus-try membership.

5. Results

5.1 DESCRIPTIVE STATISTICS

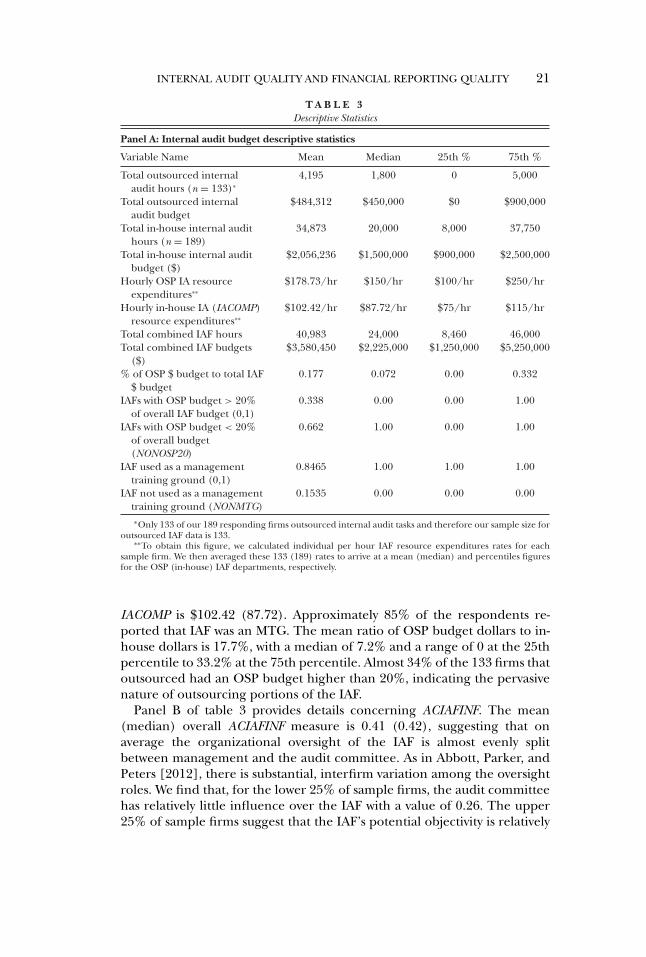

Table 3 presents descriptive statistics for the 189 respondents. PanelA provides information related to the IAF budget. The mean numberof in-house (outsourced) IAF hours is 34,873 (4,195) and the mean in-house (outsourced) budget is $2,056,236 ($484,312). The mean (median)

INTERNAL AUDIT QUALITY AND FINANCIAL REPORTING QUALITY 21

T A B L E 3Descriptive Statistics

Panel A: Internal audit budget descriptive statistics

Variable Name Mean Median 25th % 75th %

Total outsourced internalaudit hours (n = 133)∗

4,195 1,800 0 5,000

Total outsourced internalaudit budget

$484,312 $450,000 $0 $900,000

Total in-house internal audithours (n = 189)

34,873 20,000 8,000 37,750

Total in-house internal auditbudget ($)

$2,056,236 $1,500,000 $900,000 $2,500,000

Hourly OSP IA resourceexpenditures∗∗

$178.73/hr $150/hr $100/hr $250/hr

Hourly in-house IA (IACOMP)resource expenditures∗∗

$102.42/hr $87.72/hr $75/hr $115/hr

Total combined IAF hours 40,983 24,000 8,460 46,000Total combined IAF budgets

($)$3,580,450 $2,225,000 $1,250,000 $5,250,000

% of OSP $ budget to total IAF$ budget

0.177 0.072 0.00 0.332

IAFs with OSP budget > 20%of overall IAF budget (0,1)

0.338 0.00 0.00 1.00

IAFs with OSP budget < 20%of overall budget(NONOSP20)

0.662 1.00 0.00 1.00

IAF used as a managementtraining ground (0,1)

0.8465 1.00 1.00 1.00

IAF not used as a managementtraining ground (NONMTG)

0.1535 0.00 0.00 0.00

∗Only 133 of our 189 responding firms outsourced internal audit tasks and therefore our sample size foroutsourced IAF data is 133.

∗∗To obtain this figure, we calculated individual per hour IAF resource expenditures rates for eachsample firm. We then averaged these 133 (189) rates to arrive at a mean (median) and percentiles figuresfor the OSP (in-house) IAF departments, respectively.

IACOMP is $102.42 (87.72). Approximately 85% of the respondents re-ported that IAF was an MTG. The mean ratio of OSP budget dollars to in-house dollars is 17.7%, with a median of 7.2% and a range of 0 at the 25thpercentile to 33.2% at the 75th percentile. Almost 34% of the 133 firms thatoutsourced had an OSP budget higher than 20%, indicating the pervasivenature of outsourcing portions of the IAF.

Panel B of table 3 provides details concerning ACIAFINF. The mean(median) overall ACIAFINF measure is 0.41 (0.42), suggesting that onaverage the organizational oversight of the IAF is almost evenly splitbetween management and the audit committee. As in Abbott, Parker, andPeters [2012], there is substantial, interfirm variation among the oversightroles. We find that, for the lower 25% of sample firms, the audit committeehas relatively little influence over the IAF with a value of 0.26. The upper25% of sample firms suggest that the IAF’s potential objectivity is relatively

22 L. J. ABBOTT, B. DAUGHERTY, S. PARKER, AND G. F. PETERS

T A B L E 3—Continued

Panel B: Audit committee and management oversight of internal audit function

Degree of Agreement withsurvey statements #12a–12i Mean Median 25th % 75th %

IAF reports to the auditcommittee

4.73 5.00 4.00 5.00

IAF reports to the CFO 3.65 4.00 3.00 4.00IAF reports to the CEO 2.50 2.00 2.00 3.00Audit committee authorized to

terminate Chief InternalAuditor

4.52 5.00 3.00 5.00

The CFO authorized toterminate Chief InternalAuditor

3.65 4.00 3.00 4.00

The CEO authorized toterminate Chief InternalAuditor

3.05 3.00 3.00 4.00

The audit committeedetermines Internal Audit’sannual budget

3.22 3.00 3.00 4.00

The CFO determines InternalAudit’s annual budget

3.75 4.00 3.00 4.00

The CEO determines InternalAudit’s annual budget

3.02 3.00 3.00 4.00

ACIAFINF∗∗∗ 0.41 0.42 0.26 0.61∗∗∗ACIAFINF = The ratio of the total agreement points for the audit committee in the numerator di-

vided by the total agreement points for the CFO and CEO in the denominator. The numerator is the sumof agreement points (per the 1–5 Likert-scale responses) on survey questions #12a, 12d, and 12g. The de-nominator is the sum of agreement points (per the 1–5 Likert-scale responses) on survey questions #12a–12i. The 1–5 Likert-scale responses are recalibrated to 0–4 for purposes of computing this variable.

more protected from management influence, with the 75th percentilevalue of ACIAFINF equaling 0.61.

The audit committee’s oversight is strongly manifested in reporting linesand termination authority. The respondents agree strongly with the state-ment that the IAF reports to the audit committee (mean of 4.73 and me-dian of 5.00), and only slightly less strongly with the statement that the auditcommittee has termination authority over the CIA (mean of 4.52 and me-dian of 5.00). However, in terms of reporting relationships, internal auditappears to be reporting to both the audit committee and the CFO or CEO.This could be indicative of a “solid line” or functional relationship with theaudit committee and a “dotted line” or administrative relationship with theCFO or CEO. We observe lower agreement with the statement that the au-dit committee determines the IAF’s budget (mean of 3.22 and median of3.00). Budgetary authority is greater for the CFO than the audit commit-tee (mean of 3.75 and median of 4.00). The budgetary authority responserepresents the primary difference from results reported by Abbott, Parker,and Peters [2012] in a similar survey from an earlier time period (2005).We believe that the economic situation in our sample year, 2009, is a likely

INTERNAL AUDIT QUALITY AND FINANCIAL REPORTING QUALITY 23

T A B L E 3—Continued

Panel C: Control variables descriptive statistics

Variable name Mean Median 25th % 75th %

ABNACC 0.0289 −0.0139 −0.0788 0.0269JM/BEAT∗∗∗∗ 0.1957 0.0000 0.0000 1.000ASSETS (mil) $19,602 $5,318 $2,613 $12,828AGE 20.49 25.00 15.00 25.00LEVERAGE 0.4729 0.4531 0.3598 0.5644SEGNUM 4.3280 4.000 2.0000 6.0000CFO (mil) $1,780 $566.9 $258.4 $1,126SALESGROW −0.1177 −0.0947 −0.2129 −0.0105MTB 2.5294 1.6393 1.0786 2.7566CFOVOL 496.9 132.9 66.85 340.2ROA 0.0321 0.0365 0.0038 0.0698LOSS 0.2698 0.0 1.0 0.0MATWEAK 0.0423 0.0 0.0 0.0

All variable definitions can be found in table 2.∗∗∗∗Variable used in additional analysis section only.ABNACC is Kothari, Leone, and Wasley’s (2005) version of the modified Jones model measure of ab-

normal accruals. JM/BEAT is a dichotomous dependent variable coded “1” in instances where the firm metthe consensus annual EPS forecast scaled by price at the beginning of the year or exceeded the forecastby more than 0.0005; “0” elses. ASSETS equals total assets in millions. AGE is the number of years the firmwas listed on Compustat, truncated at 25 years. LEVERAGE equals the sum of long-term debt and currentliabilities of a company divided by total assets. SEGNUM equals the number of disclosed segments in whichthe company operates. CFO equals cash flows from operations. SALESGROW equals one-year sales growthpercentage. MTB equals market-to-book ratio. CFOVOL is the standard deviation of operating cash flows for2005–2009. ROA equals return on assets. LOSS is coded “1” if the firm experienced a loss in fiscal year 2008,“0” else. MATWEAK is coded “1” for a client firm disclosing a material weakness in internal controls overfinancial reporting during the prior two years and “0” otherwise.

explanation for the difference. In tight economic conditions, it seems prob-able that all areas of the firm, including the IAF, would be scrutinized bythe CFO for possible cost savings.

Table 3, panel C, shows the control variable descriptive statistics. Ourcompanies are quite large and “old,” as might be expected, with a mean(median) asset size of $19.6 billion ($5.3 billion) and a mean (median)age of 20.49 (25) years. Their leverage is fairly high (mean of 47%, medianof 45%), and most have been public companies for at least 25 years, andmany for much longer. Our sample firms have on average 4.32 operatingsegments. Operating cash flow is $1.78 billion (mean), $567 million(median). Notably, mean sales growth from 2008 to 2009 was −11.8%,and mean ROA was 3.2%, reflecting the 2009 economic environment.The mean market-to-book ratio is 2.6, while mean cash flow volatility is496.9. Reflecting the economic downturn during our sample period, theincidence of a prior year loss (LOSS) is almost 27%. All these measures(except loss incidence) are lower than those reported in Prawitt, Smith,and Wood [2009], again likely reflective of the updated economic environ-ment in our study. We also note a very low incidence of reported materialweaknesses, with the mean of MATWEAK of 0.0405. This is consistent witha dramatic decrease in Section 404 weaknesses after the issuance of AuditStandard No. 5 (PCAOB [2007]). Table 3, panel C, also shows that themean ABNACC is 0.0289, and the median is −0.0139.

24 L. J. ABBOTT, B. DAUGHERTY, S. PARKER, AND G. F. PETERS

5.2 UNIVARIATE RESULTS

Table 4 provides the results of examining the sample, based uponwhether the respondent firms do not use the IAF as an MTG (NONMTG)or do not have substantial OSP (NONOSP20). In panel A, firms not utiliz-ing the IAF as an MTG (n = 28) are larger and have higher cash flows thanfirms that use the IAF as an MTG (n = 161). This is generally consistentwith larger IAFs being able to provide an internal audit “career” (Messieret al. [2011]). Panel B of table 4 provides univariate differences based uponfirms with less than 20% of their budgets attributed to outsourcing (n =125) and those with more than 20% (n = 64). We note that firms withouta substantial OSP presence have a greater audit committee IAF influenceand a less severe deceleration in sales. The former result suggests that auditcommittees may exert a preference for in-house IAF. The latter result indi-cates that outsourcing may be an attractive means of cutting costs. We findno difference in the lack of an MTG between the two subsamples.

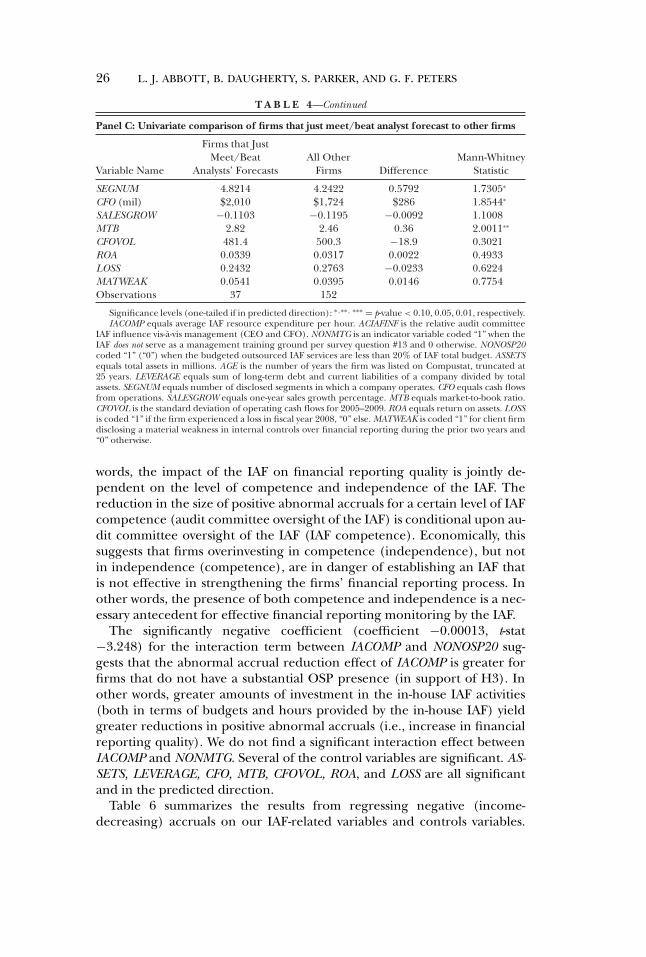

Table 4, panel C, provides univariate comparisons based upon whetherfirms just meet or beat their analyst’s EPS forecast (n = 37) and those thatdo not (n = 152). We find a low level of just meeting or beating analystforecasts (less than 20%), consistent with the Sarbanes-Oxley Act curtail-ing (but not eliminating) earnings management (Koh, Matsumoto, andRajgopal [2008]). Consistent with prior literature, firms that just meet orbeat analysts’ forecasts have more leverage, are more complex, have moreoperating cash flow, and have a greater market-to-book ratio. We find amarginally smaller IACOMP value for firms that just meet or beat analysts’forecasts. Consistent with panels A and B, there are no univariate differ-ences in IACOMP, NONMTG, or NONOSP20. Overall, the univariate resultsare consistent with (1) our three IAF independence measures capturingdifferent independence mechanisms and (2) the inability of competenceand independence to significantly influence financial reporting quality ona stand-alone basis.

5.3 MULTIVARIATE RESULTS

Tables 5 and 6 present our main results.23 Table 5 summarizes the re-sults from regressing positive (income-increasing) accruals on our IAF-related variables and controls variables. In table 5, our predicted signsfor our interaction variables are all negative, as we predict lower income-increasing accruals when the IAF exhibits both greater competence and in-dependence.24 With respect to the interactive term between IACOMP andACIAFINF (coefficient = −0.00017, t-stat. = −2.302), our results suggestthat the effect of competence depends on the amount of oversight pro-vided by the audit committee and vice versa (in support of H1). In other

23 In the interest of brevity, we do not report the coefficient estimates on our INDUSTRYdummy variables.

24 We are careful to not overinterpret our stand-alone variables, as they are not necessarilyreflective of main effects due to the continuous nature of some of our test variables (Jaccardand Turrisi [2003]).

INTERNAL AUDIT QUALITY AND FINANCIAL REPORTING QUALITY 25

T A B L E 4Univariate Comparisons

Panel A: Univariate comparison of IAF’s management training grounds

Firms with Firms with Mann-WhitneyVariable Name NONMTG = 1 NONMTG = 0 Difference Statistic

IACOMP $107.59/hr $101.52/hr $6.07/hr 1.0051ACIAFINF 0.439 0.405 0.034 1.2323NONOSP20 0.6786 0.6584 0.0202 0.9974ASSETS (mil) $24,145 $18,812 $5,333 1.6736∗

AGE 19.97 20.62 −0.65 0.9929LEVERAGE 0.4907 0.4698 0.0209 0.6788SEGNUM 4.4643 4.2919 0.1724 0.7505CFO (mil) $1,929 $1,754 $175 1.5029∗

SALESGROW −0.1332 −0.1150 0.0182 0.7471MTB 2.41 2.54 −0.1300 0.8515CFOVOL 448.2 505.4 −57.2 0.4793ROA 0.0298 0.0325 −0.0027 0.5555LOSS 0.2500 0.2733 −0.0233 0.6099MATWEAK 0.0357 0.0435 −0.0078 0.3311Observations 28 161

Panel B: Univariate comparison of IAFs lacking/with a significant (>20%) OSP presence

Firms with Firms with Mann-WhitneyVariable Name NONOSP20 = 1 NONOSP20 = 0 Difference Statistic

IACOMP $104.89/hr $97.59/hr $7.30/hr 1.1011ACIAFINF 0.441 0.349 0.092 1.6993∗

NONMTG 0.168 0.157 0.011 0.0694ASSETS (mil) $20,038 $18,750 $1,288 0.8828AGE 20.53 20.41 0.12 0.3324LEVERAGE 0.4780 0.4629 0.0151 0.7247SEGNUM 4.2480 4.4844 −0.2364 0.8791CFO (mil) $1,775 $1,789 −$14 1.0801SALESGROW −0.0988 −0.1546 −0.0558 3.4804∗∗

MTB 2.47 2.61 −0.14 0.3779CFOVOL 515.1 487.6 27.5 0.1155ROA 0.0293 0.0335 −0.0042 0.9013LOSS 0.2720 0.2656 0.0640 0.6528MATWEAK 0.0400 0.0468 −0.0680 0.4999Observations 125 64

Panel C: Univariate comparison of firms that just meet/beat analyst forecast to other firms

Firms that JustMeet/Beat All Other Mann-Whitney

Variable Name Analysts’ Forecasts Firms Difference Statistic

IACOMP $99.87/hr $103.04/hr −$3.17/hr 1.4011ACIAFINF 0.3606 0.4220 −0.0614 1.7804∗

NONMTG 0.1622 0.1513 0.0109 1.0501NONOSP20 0.6486 0.6652 −0.0166 0.7822ASSETS (mil) $18,087 $19,971 −$1,904 1.8736∗

AGE 19.57 20.65 −1.0800 0.4424LEVERAGE 0.4994 0.4664 0.0330 1.9942∗

(Continued)

26 L. J. ABBOTT, B. DAUGHERTY, S. PARKER, AND G. F. PETERS

T A B L E 4—Continued

Panel C: Univariate comparison of firms that just meet/beat analyst forecast to other firms

Firms that JustMeet/Beat All Other Mann-Whitney

Variable Name Analysts’ Forecasts Firms Difference Statistic

SEGNUM 4.8214 4.2422 0.5792 1.7305∗

CFO (mil) $2,010 $1,724 $286 1.8544∗

SALESGROW −0.1103 −0.1195 −0.0092 1.1008MTB 2.82 2.46 0.36 2.0011∗∗

CFOVOL 481.4 500.3 −18.9 0.3021ROA 0.0339 0.0317 0.0022 0.4933LOSS 0.2432 0.2763 −0.0233 0.6224MATWEAK 0.0541 0.0395 0.0146 0.7754Observations 37 152

Significance levels (one-tailed if in predicted direction): ∗ ,∗∗ , ∗∗∗ = p-value < 0.10, 0.05, 0.01, respectively.IACOMP equals average IAF resource expenditure per hour. ACIAFINF is the relative audit committee

IAF influence vis-a-vis management (CEO and CFO). NONMTG is an indicator variable coded “1” when theIAF does not serve as a management training ground per survey question #13 and 0 otherwise. NONOSP20coded “1” (“0”) when the budgeted outsourced IAF services are less than 20% of IAF total budget. ASSETSequals total assets in millions. AGE is the number of years the firm was listed on Compustat, truncated at25 years. LEVERAGE equals sum of long-term debt and current liabilities of a company divided by totalassets. SEGNUM equals number of disclosed segments in which a company operates. CFO equals cash flowsfrom operations. SALESGROW equals one-year sales growth percentage. MTB equals market-to-book ratio.CFOVOL is the standard deviation of operating cash flows for 2005–2009. ROA equals return on assets. LOSSis coded “1” if the firm experienced a loss in fiscal year 2008, “0” else. MATWEAK is coded “1” for client firmdisclosing a material weakness in internal controls over financial reporting during the prior two years and“0” otherwise.

words, the impact of the IAF on financial reporting quality is jointly de-pendent on the level of competence and independence of the IAF. Thereduction in the size of positive abnormal accruals for a certain level of IAFcompetence (audit committee oversight of the IAF) is conditional upon au-dit committee oversight of the IAF (IAF competence). Economically, thissuggests that firms overinvesting in competence (independence), but notin independence (competence), are in danger of establishing an IAF thatis not effective in strengthening the firms’ financial reporting process. Inother words, the presence of both competence and independence is a nec-essary antecedent for effective financial reporting monitoring by the IAF.

The significantly negative coefficient (coefficient −0.00013, t-stat−3.248) for the interaction term between IACOMP and NONOSP20 sug-gests that the abnormal accrual reduction effect of IACOMP is greater forfirms that do not have a substantial OSP presence (in support of H3). Inother words, greater amounts of investment in the in-house IAF activities(both in terms of budgets and hours provided by the in-house IAF) yieldgreater reductions in positive abnormal accruals (i.e., increase in financialreporting quality). We do not find a significant interaction effect betweenIACOMP and NONMTG. Several of the control variables are significant. AS-SETS, LEVERAGE, CFO, MTB, CFOVOL, ROA, and LOSS are all significantand in the predicted direction.

Table 6 summarizes the results from regressing negative (income-decreasing) accruals on our IAF-related variables and controls variables.

INTERNAL AUDIT QUALITY AND FINANCIAL REPORTING QUALITY 27

T A B L E 5OLS Regression Results: Positive Abnormal Accruals

Positive ABNACC = b0 + b1IACOMP + b2ACIAFINF + b3NONMTG + b4NONOSP20+ b5IACOMP ∗ ACIAFINF + b6 IACOMP ∗ NONMTG+ b7IACOMP ∗ NONOSP20 + b8ASSETS + b9 AGE + b10 LEVERAGE+ b11SEGNUM + b12CFO + b13SALESGROW + b14MTB + b15CFOVOL+ b16ROA + b17 LOSS + b18MATWEAK + b19−28 INDUSTRY + ε.

Independent Variable Expected Sign Coefficient Estimate t-Statistic

Intercept 0.0467 1.1099IACOMP ? −0.00004 −1.1921ACIAFINF ? −0.0369 −1.4201∗

NONMTG ? −0.0187 −0.8645NONOSP20 ? −0.0101 −0.6779IACOMP ∗ACIAFINF − −0.00017 −2.3022∗∗

IACOMP ∗NONMTG − −0.00005 −1.2199IACOMP ∗NONOSP20 − −0.00013 −3.2481∗∗∗

ASSETS + 0.0003 2.5778∗∗∗

AGE − −0.0004 −0.3101LEVERAGE + 0.0412 1.7844∗

SEGNUM + 0.0052 2.9941∗∗∗

CFO − −0.0001 −1.4245∗

SALESGROW + 0.0069 0.7274MTB + 0.0048 2.9998∗∗∗

CFOVOL + 0.0001 2.2217∗∗

ROA − −0.0101 0.3741LOSS + 0.0108 0.9577MATWEAK + 0.0128 0.5299INDUSTRY IncludedObservations 81Adjusted R2 0.2399

Significance levels (one-tailed if in predicted direction): ∗ ,∗∗ , ∗∗∗ = p-value < 0.10, 0.05, 0.01, respectively.ABNACC is the Kothari, Leone, and Wasley (2005) version of the modified Jones model measure of

abnormal accruals. IACOMP equals average IAF resource expenditure per hour. ACIAFINF is the relativeaudit committee IAF influence vis-a-vis management (CEO and CFO). NONMTG is an indicator variablecoded “1” when the IAF does not serve as a management training ground per survey question #13, and 0otherwise. NONOSP20 is coded “1” (“0”) when the budgeted outsourced IAF services are less than 20% ofthe IAF total budget. ASSETS equals total assets in millions. AGE is the number of years the firm was listed onCompustat, truncated at 25 years. LEVERAGE equals the sum of long-term debt and current liabilities of acompany divided by total assets. SEGNUM equals the number of disclosed segments a company operates in.CFO equals cash flows from operations. SALESGROW equals one-year sales growth percentage. MTB equalsthe market-to-book ratio. CFOVOL is the standard deviation of operating cash flows for 2005–2009. ROAequals return on assets. LOSS is coded “1” if the firm experienced a loss in fiscal year 2008, “0” otherwise.MATWEAK is coded “1” for a client firm disclosing a material weakness in internal controls over financialreporting during the prior two years and “0” otherwise.

Table 6 indicates that our results for income-decreasing accruals arealso generally consistent with our hypotheses. In support of H1, H2,and H3, the coefficient estimates for all three interactive competenceand independence terms (IACOMP∗ACIAFINF, IACOMP∗NONOSP20,IACOMP∗NONMGT) are significantly positive (indicating associations withsmaller negative accruals, that is, negative accruals that are closer to zero).The same control variables are significant as in table 5, except that the cashflow variables lose significance and SALESGROW gains significance. Weinterpret this as suggesting that income-decreasing (negative) abnormal

28 L. J. ABBOTT, B. DAUGHERTY, S. PARKER, AND G. F. PETERS

T A B L E 6OLS Regression Results: Negative Abnormal Accruals

Negative ABNACC = b0 + b1IACOMP + b2ACIAFINF + b3NONMTG + b4NONOSP20+ b5IACOMP ∗ ACIAFINF + b6 IACOMP ∗ NONMTG+ b7IACOMP ∗ NONOSP20 + b8ASSETS + b9 AGE + b10 LEVERAGE+ b11SEGNUM + b12CFO + b13SALESGROW + b14MTB + b15CFOVOL+ b16ROA + b17 LOSS + b18MATWEAK + b19−28 INDUSTRY + ε.

Independent Variable Expected Sign Coefficient Estimate t-Statistic

Intercept −0.3110 −1.0772IACOMP ? 0.00054 1.6005∗

ACIAFINF ? 0.0104 1.2002NONMTG ? 0.0171 0.8895NONOSP20 ? 0.0027 0.8874IACOMP ∗ACIAFINF + 0.00018 2.9444∗∗∗

IACOMP ∗NONMTG + 0.00013 2.6222∗∗

IACOMP ∗NONOSP20 + 0.00006 2.9004∗∗∗

ASSETS − −0.0034 −0.4747AGE + 0.0012 0.1111LEVERAGE − −0.0877 −1.4123∗

SEGNUM − 0.0029 0.3133CFO − 0.0001 0.5998SALESGROW + 0.0549 1.2987∗

MTB + 0.0008 2.8956∗∗∗

CFOVOL − −0.0002 −0.0765ROA − −0.4176 −3.1767∗∗∗

LOSS − −0.0728 −2.5649∗∗∗

MATWEAK − −0.0504 −0.2772INDUSTRY IncludedObservations 108Adjusted R 2 0.201

Significance levels (one-tailed if in predicted direction): ∗,∗∗, ∗∗∗ = p-value < 0.10, 0.05, 0.01, respectively.All variable definitions can be found in table 2.ABNACC is the Kothari, Leone, and Wasley (2005) version of the modified Jones model measure of

abnormal accruals. IACOMP equals average IAF resource expenditure per hour. ACIAFINF is the relativeaudit committee IAF influence vis-a-vis management (CEO and CFO). NONMTG is an indicator variablecoded “1” when the IAF does not serve as a management training ground per survey question #13, and 0otherwise. NONOSP20 is coded “1” (“0”) when the budgeted outsourced IAF services are less than 20% ofthe IAF total budget. ASSETS equals total assets in millions. AGE is the number of years the firm was listedon Compustat, truncated at 25 years. LEVERAGE equals the sum of long-term debt and current liabilities ofa company divided by total assets. SEGNUM equals the number of disclosed segments in which the companyoperates. CFO equals cash flows from operations. SALESGROW equals one-year sales growth percentage.MTB equals market-to-book ratio. CFOVOL is the standard deviation of operating cash flows for 2005–2009.ROA equals return on assets. LOSS is coded “1” if the firm experienced a loss in fiscal year 2008, “0” oth-erwise. MATWEAK is coded “1” for a client firm disclosing a material weakness in internal controls overfinancial reporting during the prior two years and “0” otherwise.

accruals are less likely to be associated with cash flow considerations, andalso that they are less (closer to zero) when sales are growing. This is consis-tent with fewer incentives for “big bath” behavior when growth is present.

We note that, in order for IAF quality to impact financial reporting qual-ity, it is necessary for the IAF to be involved in the monitoring of the fi-nancial reporting process. Per survey question #3 in the appendix, suchopportunities include financial statement audits of subsidiaries and/or as-sisting the external auditor with the financial statement audit. We observed

INTERNAL AUDIT QUALITY AND FINANCIAL REPORTING QUALITY 29

that all respondents had nonzero budget allocations to these activities, indi-cating that all sample IAF departments had the opportunity to monitor thefinancial reporting process.25 In summary, the evidence of tables 5 and 6is consistent with the characterization of a two-factor IAF quality function,whereby competence and independence must combine with each otherto promote the IAF as an effective, internally based financial reportingmonitor.26

5.4 ADDITIONAL ANALYSIS: OTHER FINANCIAL REPORTING QUALITYPROXIES