intermediate i chapter 8

TRANSCRIPT

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 1/45

Chapter8-1

Valuation of Inventories:Valuation of Inventories:

A Cost-Basis Approach A Cost-Basis Approach

Valuation of Inventories:Valuation of Inventories:

A Cost-Basis Approach A Cost-Basis Approach

ChapterChapter88

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 2/45

Chapter8-2

1.1. Identify major classifications of inventory.Identify major classifications of inventory.2.2. Distinguish between perpetual and periodic inventory systems.Distinguish between perpetual and periodic inventory systems.

3.3. Identify the effects of inventory errors on the financialIdentify the effects of inventory errors on the financialstatements.statements.

4.4. Understand the items to include as inventory cost.Understand the items to include as inventory cost... Describe and compare the cost flow assumptions used to accountDescribe and compare the cost flow assumptions used to account

for inventories.for inventories.

!.!. "#plain the significance and use of a $I%& reserve."#plain the significance and use of a $I%& reserve.

'.'. Understand the effect of $I%& li(uidations.Understand the effect of $I%& li(uidations.).). "#plain the dollar*value $I%& method."#plain the dollar*value $I%& method.

+.+. Identify the major advantages and disadvantages of $I%&.Identify the major advantages and disadvantages of $I%&.

1,.1,. Understand why companies select given inventory methods.Understand why companies select given inventory methods.

Learning Objectives Learning Objectives

Learning Objectives Learning Objectives

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 3/45

Chapter8-3

InventoryClassificationand Control

hysical!oods

Included inInventory

CostsIncluded

in Inventory

Cost "lo#Assu$ptions

LI"O:%pecialIssues

ClassificationClassification

ControlControl

BasicBasic

inventoryinventory

valuationvaluation

issuesissues

Basis for%election

Goods inGoods in

transittransit

ConsignedConsigned

goodsgoods

Special salesSpecial sales

agreementsagreements

InventoryInventory

errorserrors

Product costsProduct costs

Period costsPeriod costs

PurchasePurchase

discountsdiscounts

SpecificSpecific

identificationidentification

Average cost Average cost

FIFOFIFO

LIFOLIFO

LIFO reserveLIFO reserve

LIFOLIFO

liquidationliquidation

ollar!valueollar!value

LIFOLIFO

Comparison ofComparison ofLIFOLIFO

approachesapproaches

Advantages of Advantages of

LIFOLIFO

isadvantagesisadvantages

of LIFOof LIFO

Summary ofSummary of

inventoryinventory

valuationvaluation

methodsmethods

Valuation of Inventories:Valuation of Inventories:Cost-basis Approach Cost-basis Approach

Valuation of Inventories:Valuation of Inventories:Cost-basis Approach Cost-basis Approach

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 4/45

Chapter8-4

Inventories are-

items held for sale or

goods to be used in the production of goods to be sold.

Inventory Classification and %yste$s Inventory Classification and %yste$s

Inventory Classification and %yste$s Inventory Classification and %yste$s

LO & Identify $ajor classifications of inventory'LO & Identify $ajor classifications of inventory'

Classification

(erchandiser(erchandiser (anufacturer(anufacturer

Businesses #ith Inventory:

or

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 5/45

Chapter8-5

)ype of Business

(erchandiser(erchandiser

&ne inventoryaccount

/urchase goodsready for sale

Balance %heet 0in thousandsCurrent assets

ash 2),,,

ar5etable securities 3,,,,

6ccounts receivable 14+,,,

erchandise inventory ''',,,

/repaids 33,,,

7otal current assets 1''4,,,

Invest$ents:

Invesment in 68 bonds 321!'

Investment in U Inc. 23+),

9otes receivable 1,,,, $and held for speculation ,,,,

:in5ing fund 22,,,

/ension fund !3'+)

Inventory Classification and %yste$s Inventory Classification and %yste$s

Inventory Classification and %yste$s Inventory Classification and %yste$s

LO & Identify $ajor classifications of inventory'LO & Identify $ajor classifications of inventory'

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 6/45

Chapter8-6

)ype of Business

(anufacturer(anufacturer

7hree accounts;aw materials

<or5 in process

%inished goods

Inventory Classification and %yste$s Inventory Classification and %yste$s

Inventory Classification and %yste$s Inventory Classification and %yste$s

LO & Identify $ajor classifications of inventory'LO & Identify $ajor classifications of inventory'

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 7/45

Chapter8-7

"lo# of Costs

Inventory Classification and %yste$s Inventory Classification and %yste$s Inventory Classification and %yste$s Inventory Classification and %yste$s

Illustration )*2Illustration )*2

LO & Identify $ajor classifications of inventory'LO & Identify $ajor classifications of inventory'

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 8/45

Chapter8-8

7wo systems for maintaining inventory records-

Inventory Classification and %yste$s Inventory Classification and %yste$s Inventory Classification and %yste$s Inventory Classification and %yste$s

LO * +istinguish bet#een perpetual and periodic inventory syste$s'LO * +istinguish bet#een perpetual and periodic inventory syste$s'

Control

/erpetual system

/eriodic system

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 9/45

Chapter8-9

%eatures-

Inventory Classification and %yste$s Inventory Classification and %yste$s Inventory Classification and %yste$s Inventory Classification and %yste$s

LO * +istinguish bet#een perpetual and periodic inventory syste$s'LO * +istinguish bet#een perpetual and periodic inventory syste$s'

erpetual %yste$

1. /urchases of merchandise are debited to Inventory.

2. %reight*in purchase returns and allowances andpurchase discounts are recorded in Inventory.

3. ost of goods sold is debited and Inventory iscredited for each sale.

4. /hysical count done to verify Inventory balance.

7he perpetual inventory system provides a continuousrecord of Inventory and ost of =oods :old.

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 10/45

Chapter8-10

%eatures-

Inventory Classification and %yste$s Inventory Classification and %yste$s Inventory Classification and %yste$s Inventory Classification and %yste$s

LO * +istinguish bet#een perpetual and periodic inventory syste$s'LO * +istinguish bet#een perpetual and periodic inventory syste$s'

eriodic %yste$

1. /urchases of merchandise are debited to /urchases.

2. "nding Inventory determined by physical count.3. alculation of ost of =oods :old-

8eginning inventory

1,,,,,/urchases net

),,,,,

=oods available for sale

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 11/45

Chapter8-11

|

1. Beginning inventory (100 units at 7 ! 700"

|

2. #ur$hase 900 units at 7% |

|

&nventory 6'300 | #ur$hases 6'300

$$ounts paya)*e 6'300 | $$ounts paya)*e 6'300

|

3. +a*e o, 600 untis at 14% |

|

$$ounts re$eiva)*e 8'400 | $$ounts re$eiva)*e 8'400

+a*es 8'400 | +a*es 8'400

Cost o, goo-s so*- 4'200 |

&nventory 4'200 |

|

4. -usting entries (en-ing inventory ! 400 units / 7 ! 2'800"

|

o ntry e$essary | &nventory 2'100

| Cost o, goo-s so*- 4'200

| #ur$hases 6'300

Inventory Classification and %yste$s Inventory Classification and %yste$s Inventory Classification and %yste$s Inventory Classification and %yste$s

LO * +istinguish bet#een perpetual and periodic inventory syste$s'LO * +istinguish bet#een perpetual and periodic inventory syste$s'

erpetual %yste$ eriodic %yste$vs'

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 12/45

Chapter8-12

;e(uires the following-

Basic Issues in Inventory Valuation Basic Issues in Inventory Valuation Basic Issues in Inventory Valuation Basic Issues in Inventory Valuation

LO * +istinguish bet#een perpetual and periodic inventory syste$s'LO * +istinguish bet#een perpetual and periodic inventory syste$s'

>aluation of Inventories

7he physical goods 0goods on hand goods in transit

consigned goods special sales agreements.7he costs to include 0product vs. period costs.

7he cost flo# assu$ption 0%I%& $I%& 6verage cost:pecific Identification ;etail etc..

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 13/45

Chapter8-13

6 company should record purchases when itobtains legal title to the goods.

hysical !oods Included in Inventory hysical !oods Included in Inventory hysical !oods Included in Inventory hysical !oods Included in Inventory

LO * +istinguish bet#een perpetual and periodic inventory syste$s'LO * +istinguish bet#een perpetual and periodic inventory syste$s'

/hysical =oods

%pecial Consideration:=oods in 7ransit 0%&8 shipping point %&8 destination

onsigned goods

:ales with buybac5 agreement

:ales with high rates of return

:ales on installment

Inventory errors

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 14/45

Chapter8-14

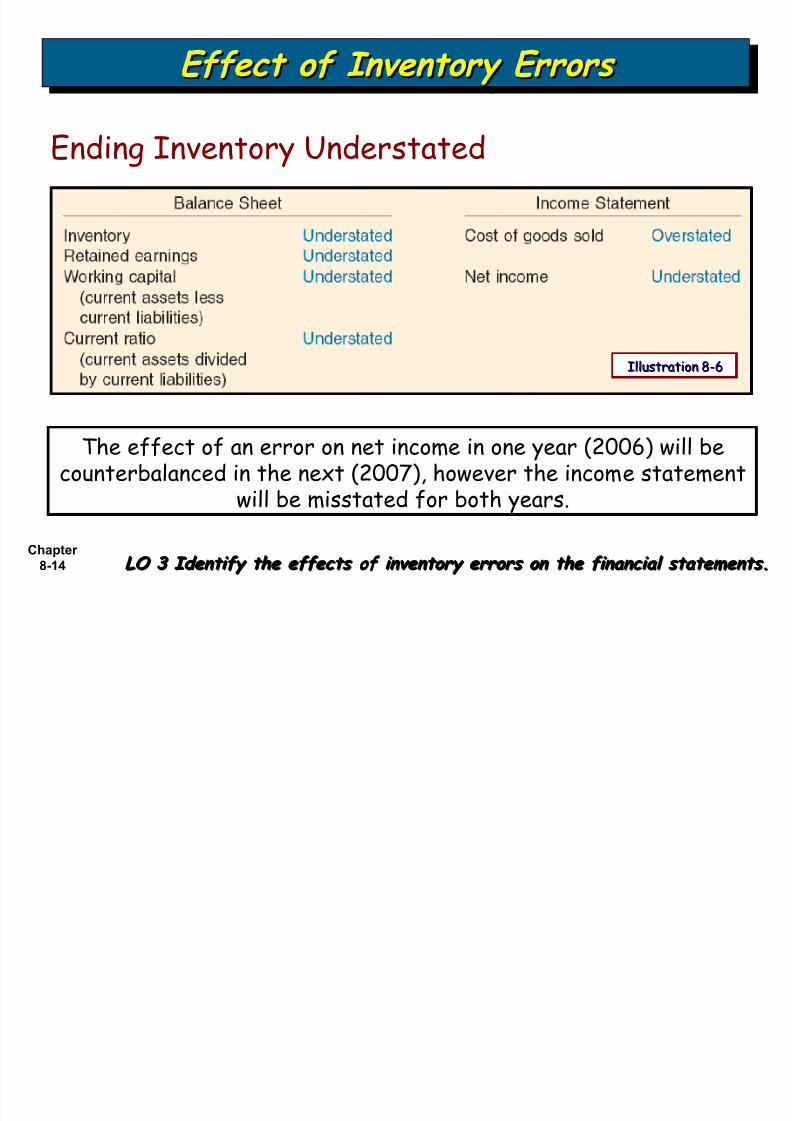

,ffect of Inventory ,rrors ,ffect of Inventory ,rrors ,ffect of Inventory ,rrors ,ffect of Inventory ,rrors

LO Identify the effects of inventory errors on the financial state$ents'LO Identify the effects of inventory errors on the financial state$ents'

"nding Inventory Understated

7he effect of an error on net income in one year 02,,! will becounterbalanced in the ne#t 02,,' however the income statement

will be misstated for both years.

Illustration )*!Illustration )*!

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 15/45

Chapter8-15

,ffect of Inventory ,rrors ,ffect of Inventory ,rrors ,ffect of Inventory ,rrors ,ffect of Inventory ,rrors

LO Identify the effects of inventory errors on the financial state$ents'LO Identify the effects of inventory errors on the financial state$ents'

/urchases and Inventory Understated

7he understatement does not affect cost of goods sold and netincome because the errors offset one another.

Illustration )*)Illustration )*)

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 16/45

Chapter8-16

Costs Included in Inventory Costs Included in Inventory Costs Included in Inventory Costs Included in Inventory

LO . /nderstand the ite$s to include as inventory cost'LO . /nderstand the ite$s to include as inventory cost'

roduct Costs * costs directly connected withbringing the goods to the buyer?s place ofbusiness and converting such goods to a salablecondition.

eriod Costs @ generally selling general andadministrative e#penses.

urchase +iscounts @ =ross vs. 9et ethod

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 17/45

Chapter8-17

|

#ur$hase $ost 20'000' ters 210' net 30%

|

#ur$hases 20'000 | #ur$hases 19'600

$$ounts paya)*e 20'000 | $$ounts paya)*e 19'600

|&nvoi$es o, 15'000 are pai ithin is$ount perio%

|

$$ounts paya)*e 15'000 | $$ounts paya)*e 14'700

#ur$hase is$ounts 300 | Cash 14'700

Cash 14'700 |

|

&nvoi$es o, 5'000 are pai a,ter is$ount perio%

|

$$ounts paya)*e 5'000 | $$ounts paya)*e 4'900

Cash 5'000 | #ur$hase is$ount *ost 100

| Cash 5'000

)reat$ent of urchase +iscounts )reat$ent of urchase +iscounts )reat$ent of urchase +iscounts )reat$ent of urchase +iscounts

!ross (ethod 0et (ethodvs'

LO . /nderstand the ite$s to include as inventory cost'LO . /nderstand the ite$s to include as inventory cost'

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 18/45

Chapter8-18

Ans#er: ethod adopted should be onethat most clearly reflects periodic income.

ost %low 6ssumption 6dopted

/hysical ovement of =oodsdoes not need to e(ual

"I"O

1hat Cost "lo# Assu$ption to Adopt2 1hat Cost "lo# Assu$ption to Adopt2 1hat Cost "lo# Assu$ption to Adopt2 1hat Cost "lo# Assu$ption to Adopt2

LI"O

Average Cost %pecific Identification

LO 3 +escribe and co$pare the cost flo# assu$ptionsLO 3 +escribe and co$pare the cost flo# assu$ptionsused to account for inventories'used to account for inventories'

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 19/45

Chapter8-19

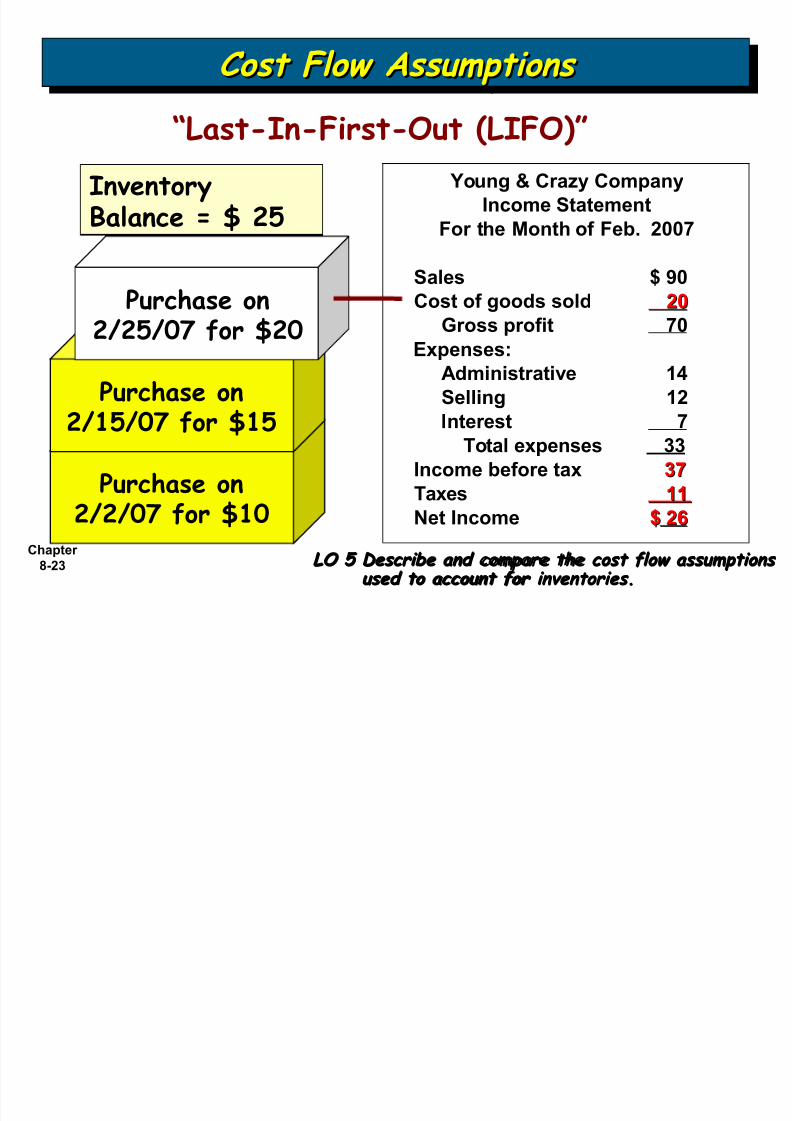

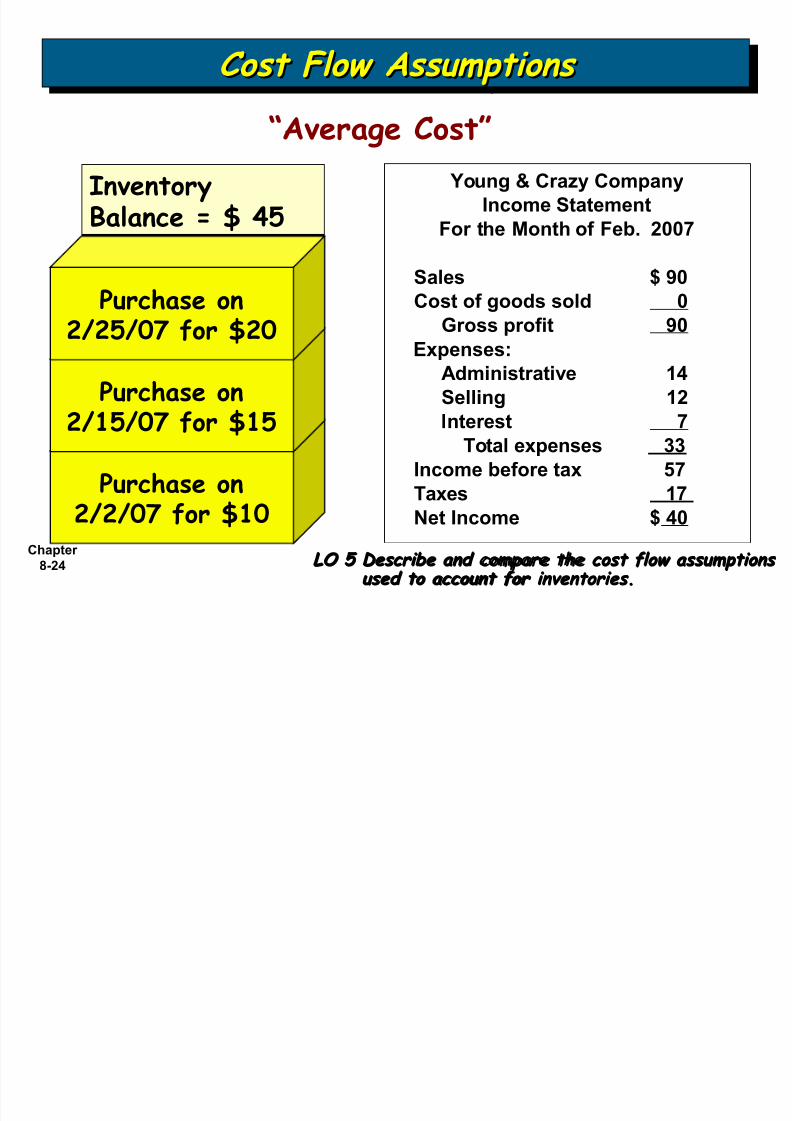

Aoung B raCy ompany ma5es the following purchases-

1. &ne item on 22,' for 1,

2. &ne item on 21,' for 13. &ne item on 22,' for 2,

Aoung B raCy ompany sells one item on 22),' for+,. <hat would be the balance of ending inventory and

cost of goods sold for the month ended %eb. 2,,'assuming the company used the "I"O LI"O AverageCost and %pecific Identification cost flow assumptionsE6ssume a ta# rate of 3,F.

"#ample

Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions

LO 3 +escribe and co$pare the cost flo# assu$ptionsLO 3 +escribe and co$pare the cost flo# assu$ptionsused to account for inventories'used to account for inventories'

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 20/45

Chapter8-20

urchase on*4*456 for 7&5

urchase on

*4&3456 for 7&3

urchase on*4*3456 for 7*5

InventoryBalance 7 .3

oung Cray Copany&n$oe +tateent

or the onth o, e). 2007

+a*es 90 Cost o, goos so* 0 :ross pro,it 90

;penses% (inistrative 14 +e**ing 12

&nterest 7 <ota* e;penses 33 &n$oe )e,ore ta; 57 <a;es 17

et &n$oe 40

Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions

9"irst-In-"irst-Out "I"O;<

LO 3 +escribe and co$pare the cost flo# assu$ptionsLO 3 +escribe and co$pare the cost flo# assu$ptionsused to account for inventories'used to account for inventories'

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 21/45

Chapter8-21

urchase on*4*456 for 7&5

urchase on

*4&3456 for 7&3

urchase on*4*3456 for 7*5

Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions

InventoryBalance 7 3

oung Cray Copany&n$oe +tateent

or the onth o, e). 2007

+a*es 90 Cost o, goos so* 10 10 :ross pro,it 80

;penses% (inistrative 14 +e**ing 12

&nterest 7 <ota* e;penses 33 &n$oe )e,ore ta; 4747 <a;es 1414

et &n$oe 33 33

9"irst-In-"irst-Out "I"O;<

LO 3 +escribe and co$pare the cost flo# assu$ptionsLO 3 +escribe and co$pare the cost flo# assu$ptionsused to account for inventories'used to account for inventories'

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 22/45

Chapter8-22

urchase on*4*456 for 7&5

urchase on

*4&3456 for 7&3

urchase on*4*3456 for 7*5

InventoryBalance 7 .3

oung Cray Copany&n$oe +tateent

or the onth o, e). 2007

+a*es 90 Cost o, goos so* 0 :ross pro,it 90

;penses% (inistrative 14 +e**ing 12

&nterest 7 <ota* e;penses 33 &n$oe )e,ore ta; 57 <a;es 17

et &n$oe 40

Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions

9Last-In-"irst-Out LI"O;<

LO 3 +escribe and co$pare the cost flo# assu$ptionsLO 3 +escribe and co$pare the cost flo# assu$ptionsused to account for inventories'used to account for inventories'

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 23/45

Chapter8-23

urchase on*4*456 for 7&5

urchase on

*4&3456 for 7&3

Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions

InventoryBalance 7 *3

urchase on*4*3456 for 7*5

oung Cray Copany&n$oe +tateent

or the onth o, e). 2007

+a*es 90 Cost o, goos so* 20 20 :ross pro,it 70

;penses% (inistrative 14 +e**ing 12

&nterest 7 <ota* e;penses 33 &n$oe )e,ore ta; 37 37 <a;es 1111

et &n$oe 2626

9Last-In-"irst-Out LI"O;<

LO 3 +escribe and co$pare the cost flo# assu$ptionsLO 3 +escribe and co$pare the cost flo# assu$ptionsused to account for inventories'used to account for inventories'

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 24/45

Chapter8-24

urchase on*4*456 for 7&5

urchase on

*4&3456 for 7&3

urchase on*4*3456 for 7*5

InventoryBalance 7 .3

oung Cray Copany&n$oe +tateent

or the onth o, e). 2007

+a*es 90 Cost o, goos so* 0 :ross pro,it 90

;penses% (inistrative 14 +e**ing 12

&nterest 7 <ota* e;penses 33 &n$oe )e,ore ta; 57 <a;es 17

et &n$oe 40

Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions

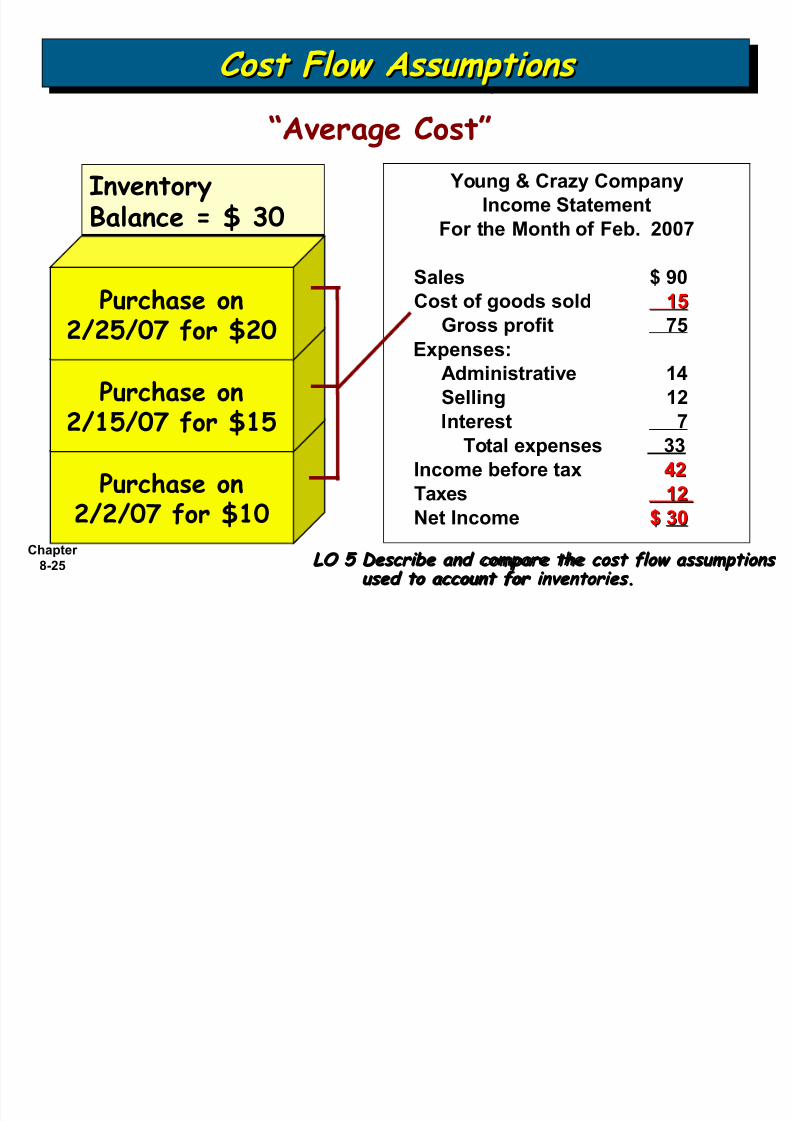

9Average Cost<

LO 3 +escribe and co$pare the cost flo# assu$ptionsLO 3 +escribe and co$pare the cost flo# assu$ptionsused to account for inventories'used to account for inventories'

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 25/45

Chapter8-25

urchase on*4*456 for 7&5

urchase on

*4&3456 for 7&3

urchase on*4*3456 for 7*5

InventoryBalance 7 5

Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions

oung Cray Copany&n$oe +tateent

or the onth o, e). 2007

+a*es 90 Cost o, goos so* 15 15 :ross pro,it 75

;penses% (inistrative 14 +e**ing 12

&nterest 7 <ota* e;penses 33 &n$oe )e,ore ta; 42 42 <a;es 1212

et &n$oe 3030

9Average Cost<

LO 3 +escribe and co$pare the cost flo# assu$ptionsLO 3 +escribe and co$pare the cost flo# assu$ptionsused to account for inventories'used to account for inventories'

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 26/45

Chapter8-26

urchase on*4*456 for 7&5

urchase on

*4&3456 for 7&3

urchase on*4*3456 for 7*5

InventoryBalance 7 .3

oung Cray Copany&n$oe +tateent

or the onth o, e). 2007

+a*es 90 Cost o, goos so* 0 :ross pro,it 90

;penses% (inistrative 14 +e**ing 12

&nterest 7 <ota* e;penses 33 &n$oe )e,ore ta; 57 <a;es 17

et &n$oe 40

Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions

9%pecific Identification<

LO 3 +escribe and co$pare the cost flo# assu$ptionsLO 3 +escribe and co$pare the cost flo# assu$ptionsused to account for inventories'used to account for inventories'

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 27/45

Chapter8-27

urchase on*4*456 for 7&5

urchase on

*4&3456 for 7&3

urchase on*4*3456 for 7*5

InventoryBalance 7 .3

oung Cray Copany&n$oe +tateent

or the onth o, e). 2007

+a*es 90 Cost o, goos so* 0 :ross pro,it 90

;penses% (inistrative 14 +e**ing 12

&nterest 7 <ota* e;penses 33 &n$oe )e,ore ta; 57 <a;es 17

et &n$oe 40

Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions

9%pecific Identification<

+epends #hich one is sold+epends #hich one is sold

LO 3 +escribe and co$pare the cost flo# assu$ptionsLO 3 +escribe and co$pare the cost flo# assu$ptionsused to account for inventories'used to account for inventories'

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 28/45

Chapter8-28

"inancial %tate$ent %u$$ary"inancial %tate$ent %u$$ary&= >&= verage

+a*es 90 90 90

Cost o, goos so* 10 20 15

:ross pro,it 80 70 75

=perating e;penses%inistrative 14 14 14

+e**ing 12 12 12

&nterest 7 7 7

<ota* e;penses 33 33 33

&n$oe )e,ore ta;es 47 37 42 &n$oe ta; e;pense 14 11 12

et in$oe 33 26 30

&nventory Ba*an$e 302535

Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions

LO 3 +escribe and co$pare the cost flo# assu$ptionsLO 3 +escribe and co$pare the cost flo# assu$ptionsused to account for inventories'used to account for inventories'

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 29/45

Chapter8-29

Inventory information for /art !)! for the month of Gune.

Gune 1 8eg. 8alance 3,, units H 1, 3,,,

1, :old 2,, units H 24

11 /urchased ),, units H 12 +!,,1 :old ,, units H 2

2, /urchased ,, units H 13 !,,

2' :old 3,, units H 2'

"#ample @ /erpetual and /eriodic ethods

Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions

LO 3 +escribe and co$pare the cost flo# assu$ptionsLO 3 +escribe and co$pare the cost flo# assu$ptionsused to account for inventories'used to account for inventories'

1. 6ssuming the /erpetual Inventory ethod compute the ost of =oods:old and "nding Inventory under %I%& $I%& and 6verage cost.

2. 6ssuming the /eriodic Inventory ethod compute the ost of =oods:old and "nding Inventory under %I%& $I%& and 6verage cost.

=oods6vailable

1+1,,

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 30/45

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 31/45

Chapter8-31

Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions

LO 3 +escribe and co$pare the cost flo# assu$ptionsLO 3 +escribe and co$pare the cost flo# assu$ptionsused to account for inventories'used to account for inventories'

>&=%

<ransa$tions% &nventory Ba*an$e%?ate @nits >ayer 1 >ayer 2 >ayer 3 <ota*

Aun 1 300 300

Aun 10 (200" (200"

Aun 11 800 800

Aun 15 (500" (500"

Aun 20 500 500 Aun 27 (300" (300"

100 300 200 600

Cost 10 12 13

600 1'000 3'600 2'600 7'200

Ca*$u*ation o, Cost o, :oos +o*% @nits ?o**ars

Beg. inventory 300 3'000

#ur$hases 1'300 16'100

:oos avai*a)*e 1'600 19'100

ning inventory (600" (7'200"

C=:+ 1'000 11'900

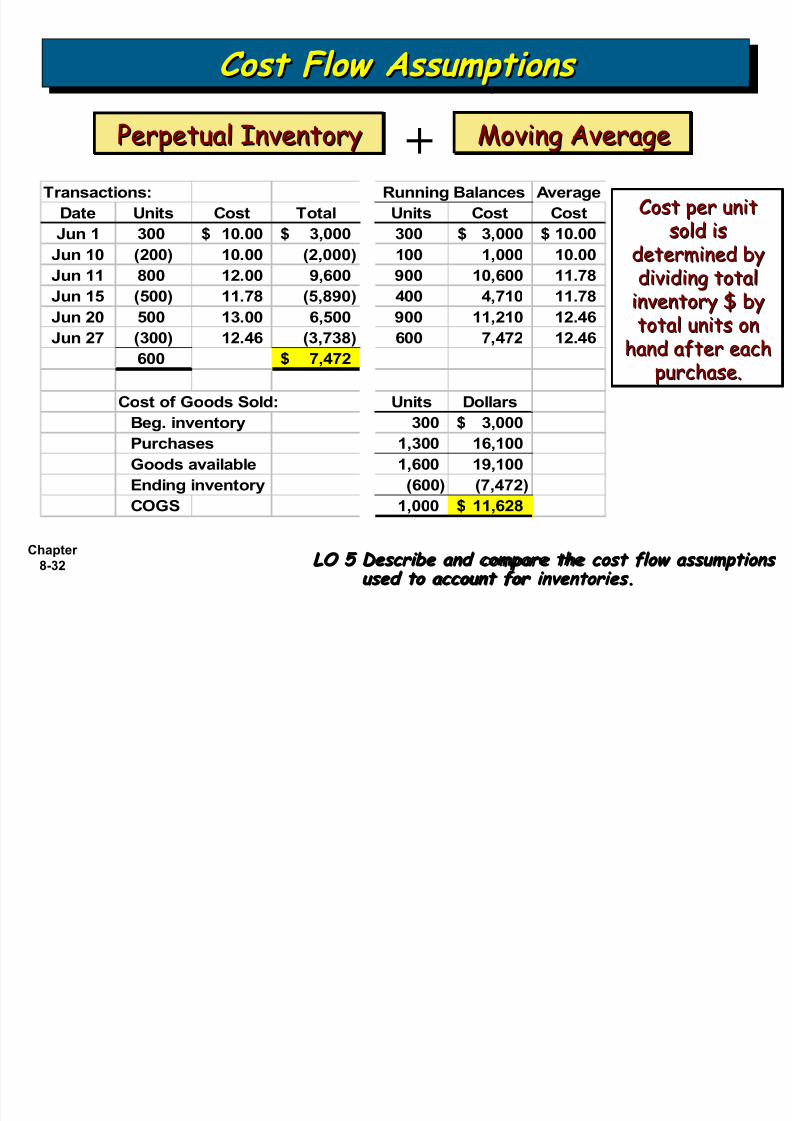

/erpetual/erpetualInventoryInventory/erpetual/erpetualInventoryInventory

$I%& ethod$I%& ethod$I%& ethod$I%& ethod

+

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 32/45

Chapter8-32

<ransa$tions% verage

?ate @nits Cost <ota* @nits Cost Cost

Aun 1 300 10.00 3'000 300 3'000 10.00

Aun 10 (200" 10.00 (2'000" 100 1'000 10.00

Aun 11 800 12.00 9'600 900 10'600 11.78 Aun 15 (500" 11.78 (5'890" 400 4'710 11.78

Aun 20 500 13.00 6'500 900 11'210 12.46

Aun 27 (300" 12.46 (3'738" 600 7'472 12.46

600 7'472

Cost o, :oo-s +o*-% @nits ?o**ars

Beg. inventory 300 3'000#ur$hases 1'300 16'100

:oo-s avai*a)*e 1'600 19'100

n-ing inventory (600" (7'472"

C=:+ 1'000 11'628

unning Ba*an$es

Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions

LO 3 +escribe and co$pare the cost flo# assu$ptionsLO 3 +escribe and co$pare the cost flo# assu$ptionsused to account for inventories'used to account for inventories'

/erpetual Inventory/erpetual Inventory/erpetual Inventory/erpetual Inventory oving 6verageoving 6verageoving 6verageoving 6verage

ost per unitost per unitsold issold is

determined bydetermined by

dividing totaldividing totalinventory byinventory bytotal units ontotal units on

hand after eachhand after eachpurchase.purchase.

+

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 33/45

Chapter8-33

<ransa$tions% verage

?ate @nits Cost <ota* @nits Cost Cost

Aun 1 300 10.00 3'000 300 3'000 10.00

Aun 10 (200" 10.00 (2'000" 100 1'000 10.00

Aun 11 800 12.00 9'600 900 10'600 11.78 Aun 15 (500" 11.78 (5'890" 400 4'710 11.78

Aun 20 500 13.00 6'500 900 11'210 12.46

Aun 27 (300" 12.46 (3'738" 600 7'472 12.46

600 7'472

Cost o, :oo-s +o*-% @nits ?o**ars

Beg. inventory 300 3'000#ur$hases 1'300 16'100

:oo-s avai*a)*e 1'600 19'100

n-ing inventory (600" (7'472"

C=:+ 1'000 11'628

unning Ba*an$es

Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions

LO 3 +escribe and co$pare the cost flo# assu$ptionsLO 3 +escribe and co$pare the cost flo# assu$ptionsused to account for inventories'used to account for inventories'

/erpetual Inventory/erpetual Inventory/erpetual Inventory/erpetual Inventory oving 6verageoving 6verageoving 6verageoving 6verage

ost per unitost per unitsold issold is

determined bydetermined by

dividing totaldividing totalinventory byinventory bytotal units ontotal units on

hand after eachhand after eachpurchase.purchase.

+

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 34/45

Chapter8-34

Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions

LO 3 +escribe and co$pare the cost flo# assu$ptionsLO 3 +escribe and co$pare the cost flo# assu$ptionsused to account for inventories'used to account for inventories'

&=%

<ransa$tions% &nventory Ba*an$e%?ate @nits >ayer 1 >ayer 2 >ayer 3 <ota*

Aun 1 300

Aun 10 (200"

Aun 11 800 100

Aun 15 (500"

Aun 20 500 500 Aun 27 (300"

- 100 500 600

Cost 10 12 13

600 - 1'200 6'500 7'700

Ca*$u*ation o, Cost o, :oos +o*% @nits ?o**ars

Beg. inventory 300 3'000

#ur$hases 1'300 16'100

:oos avai*a)*e 1'600 19'100

ning inventory (600" (7'700"

C=:+ 1'000 11'400

/eriodic/eriodicInventoryInventory/eriodic/eriodic

InventoryInventory

%I%& ethod%I%& ethod%I%& ethod%I%& ethod

+

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 35/45

Chapter8-35

Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions

LO 3 +escribe and co$pare the cost flo# assu$ptionsLO 3 +escribe and co$pare the cost flo# assu$ptionsused to account for inventories'used to account for inventories'

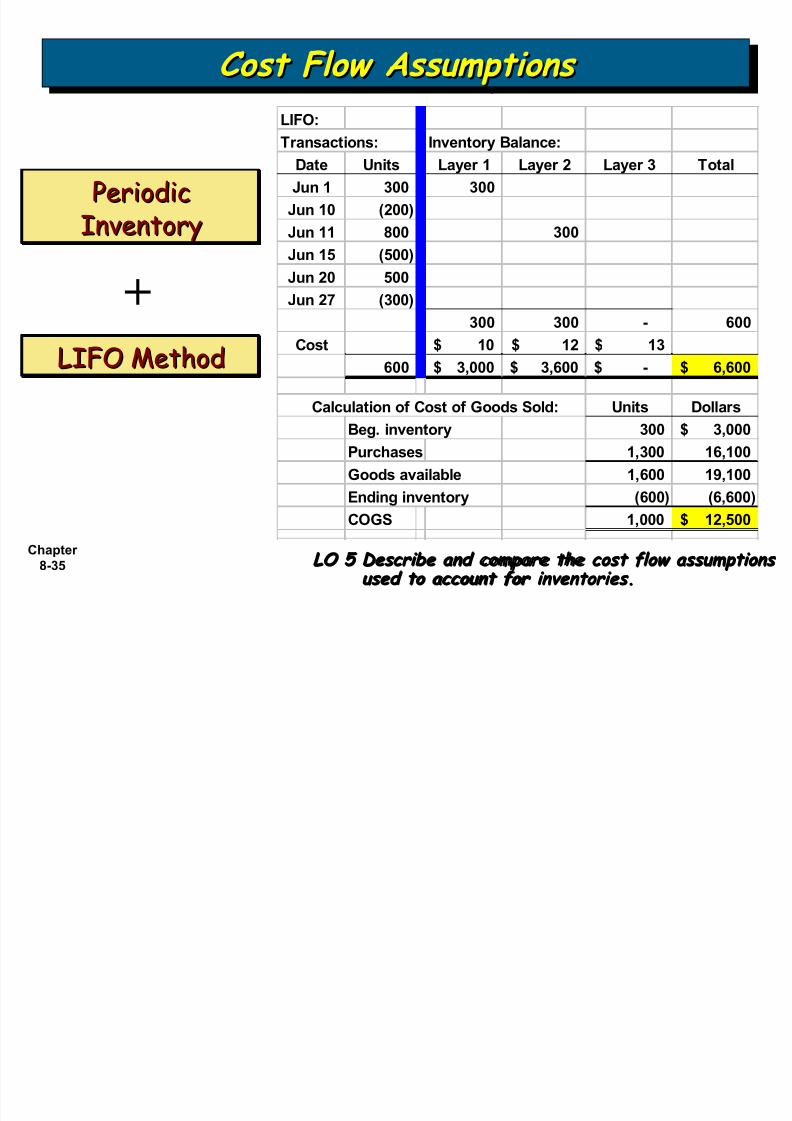

>&=%

<ransa$tions% &nventory Ba*an$e%?ate @nits >ayer 1 >ayer 2 >ayer 3 <ota*

Aun 1 300 300

Aun 10 (200"

Aun 11 800 300

Aun 15 (500"

Aun 20 500 Aun 27 (300"

300 300 - 600

Cost 10 12 13

600 3'000 3'600 - 6'600

Ca*$u*ation o, Cost o, :oos +o*% @nits ?o**ars

Beg. inventory 300 3'000

#ur$hases 1'300 16'100

:oos avai*a)*e 1'600 19'100

ning inventory (600" (6'600"

C=:+ 1'000 12'500

/eriodic/eriodicInventoryInventory/eriodic/eriodic

InventoryInventory

$I%& ethod$I%& ethod$I%& ethod$I%& ethod

+

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 36/45

Chapter8-36

Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions Cost "lo# Assu$ptions

LO 3 +escribe and co$pare the cost flo# assu$ptionsLO 3 +escribe and co$pare the cost flo# assu$ptionsused to account for inventories'used to account for inventories'

/eriodic Inventory/eriodic Inventory/eriodic Inventory/eriodic Inventory <eighted 6verage<eighted 6verage<eighted 6verage<eighted 6verage+

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 37/45

Chapter8-37

any companies use

$I%& for ta# and e#ternal financial reporting purposes

%I%& average cost or standard cost system forinternal reporting purposes.

;easons-

%pecial Issues =elated to LI"O %pecial Issues =elated to LI"O %pecial Issues =elated to LI"O %pecial Issues =elated to LI"O

LO > ,?plain the significance and use of a LI"O reserve'LO > ,?plain the significance and use of a LI"O reserve'

$I%& ;eserve

1./ricing decisions2. ;ecord 5eeping easier

3. /rofit*sharing or bonus arrangements

4. $I%& troublesome for interim periods

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 38/45

Chapter8-38

%pecial Issues =elated to LI"O %pecial Issues =elated to LI"O %pecial Issues =elated to LI"O %pecial Issues =elated to LI"O

LO > ,?plain the significance and use of a LI"O reserve'LO > ,?plain the significance and use of a LI"O reserve'

$I%& ;eserve is the difference between theinventory method used for internal reporting purposesand $I%&.

,?a$ple: %I%& value per boo5s%I%& value per boo5s 1!,,,,1!,,,,

$I%& value$I%& value 14,,,14,,,$I%& ;eserve$I%& ;eserve 1,,,1,,,

ost of goods sold 1,,,$I%& reserve 1,,,

Gournal entry to reduce inventory to $I%&-

ompanies should disclose either the $I%& reserve or the replacementcost of the inventory.

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 39/45

Chapter8-39

&lder low cost inventory is sold resulting in a lower costof goods sold higher net income and higher ta#es.

%pecial Issues =elated to LI"O %pecial Issues =elated to LI"O %pecial Issues =elated to LI"O %pecial Issues =elated to LI"O

LO 6 /nderstand the effect of LI"O li@uidations'LO 6 /nderstand the effect of LI"O li@uidations'

$I%& $i(uidation

Illustration )*2,Illustration )*2,

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 40/45

Chapter8-40

hanges in a pool are measured in terms of totaldollar value not physical (uantity.

6dvantage-8roader range of goods in pool.

/ermits replacement of goods that are similar.

Jelps protect $I%& layers from erosion.

%pecial Issues =elated to LI"O %pecial Issues =elated to LI"O %pecial Issues =elated to LI"O %pecial Issues =elated to LI"O

LO 8 ,?plain the dollar-value LI"O $ethod'LO 8 ,?plain the dollar-value LI"O $ethod'

Dollar*>alue $I%&

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 41/45

Chapter8-41

%pecial Issues =elated to LI"O %pecial Issues =elated to LI"O %pecial Issues =elated to LI"O %pecial Issues =elated to LI"O

LO 8 ,?plain the dollar-value LI"O $ethod'LO 8 ,?plain the dollar-value LI"O $ethod'

,?ercise 8-*> 7he following information relates to theGimmy Gohnson ompany.

Use the dollar*value $I%& method to compute the endinginventory for 2,,3 through 2,,.

Dollar*>alue $I%&

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 42/45

Chapter8-42

%pecial Issues =elated to LI"O %pecial Issues =elated to LI"O %pecial Issues =elated to LI"O %pecial Issues =elated to LI"O

LO 8 ,?plain the dollar-value LI"O $ethod'LO 8 ,?plain the dollar-value LI"O $ethod'

Inventory at Inventory at 7 Value

,nd-of-ear Base-ear Base 7 Value LI"O LI"O

ear rices Inde? rices Layers Inde? LI"O )O)AL =eserve

*55 655557 &'55 655557 655557 &'55 655557 655557 -7

*55. 555 &'53 8>555 65555 &'55 65555

&>555 &'53 &>855 8>855 355

*553 3&*5 &'&> 8*555 65555 &'55 65555

&*555 &'53 &*>55 8*>55 &*3*5

+ec' & +ec' & +ec' &

Balance %heet *55 *55. *553Inventory 655557 5557 3&*57LI"O =eserve - :355; :&*3*5;

655557 8>8557 8*>557Dournal entry

Cost of goods sold 355 5*5 Lifo reserve :355; :5*5;

,?ercise 8-*> %olution

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 43/45

Chapter8-43

:pecific*goods $I%& * costing goods on a unit basisis e#pensive and time consuming.

:pecific*goods /ooled $I%& approachreduces record 5eeping and clerical costs.more difficult to erode the layers.using (uantities as measurement basis can lead to

untimely $I%& li(uidations.

Dollar*value $I%& is used by most companies.

%pecial Issues =elated to LI"O %pecial Issues =elated to LI"O %pecial Issues =elated to LI"O %pecial Issues =elated to LI"O

LO 8 ,?plain the dollar-value LI"O $ethod'LO 8 ,?plain the dollar-value LI"O $ethod'

omparison of $I%& 6pproaches

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 44/45

8/19/2019 Intermediate I Chapter 8

http://slidepdf.com/reader/full/intermediate-i-chapter-8 45/45

Chapter

$I%& is generally preferred-1. if selling prices are increasing faster than costs and

2. if a company has a fairly constant Kbase stoc5.L

Basis for %election of Inventory (ethod Basis for %election of Inventory (ethod Basis for %election of Inventory (ethod Basis for %election of Inventory (ethod

$I%& not appropriate-

1. if prices tend to lag behind costs

2. if specific identification traditionally used and

3. when unit costs tend to decrease as productionincreases.