interim report 2016 - mutares

TRANSCRIPT

Interim report 2016Group Interim Management Report and Consolidated Financial Statements for the period from January 1 to June 30, 2016

3

Contents

To our shareholders

Letter of the Executive Board 4Highlights of the first half year 2016 6 mutares on the capital markets 7

Group interim management report

Economic report 9Assets, financial position and results 25 Forecast, opportunities and risks 27Other information 29

Consolidated interim financial statements

Consolidated income statement 31Consolidated balance sheet 32Consolidated cash flow statement 34Condensed notes to the consolidated financial statements 36

Investor relations

Financial calendar 49Imprint & contact details 50

CONTENTS

3,137Employees

13Portfolio companies

15Countries

310.6*

Revenues

4.0*

EBITDA

44.7*

Cash funds

417.0*

Total assets

*) m EUR

In the period under review, the M&A team examined potential acquisitions on an ongoing basis, also for existing portfolio companies. As there are many interesting takeover candidates in the pipeline, we assume that we will complete at least another acquisition by the end of the year.

The development and performance of the individual portfolio companies, which were very positive in some cases, are not yet reflected in the share price. Due to the restructuring pro- gress anticipated for key investments, we are confidently looking towards the second half of the year and believe that we will increase Group revenues again during the rest of the year and achieve positive consolidated net income.

We would like to thank all our employees for their commitment and our business partners for their fruitful cooperation. We would also like to thank the Supervisory Board for the construc-tive dialogue and particularly thank our shareholders for their trust and support.

Yours sincerely

The Executive Board of mutares AGMunich, September 2016

Dr Axel Geuer Robin Laik Dr Kristian Schleede CEO CEO CRO

Dr Wolf Cornelius Mark FriedrichCOO CFO

Letter of the Executive Board

4 5

Dr Axel Geuer, CEO Robin Laik, CEO Dr Kristian Schleede, CRO Dr Wolf Cornelius, COO Mark Friedrich, CFO

Dear shareholders,

In the first half of 2016, the focus was on the strategic development of mutares AG and the takeover of Sonoco Paper France, now known as Cenpa. In the period under review, revenues stabilised at the previous year’s level and amounted to EUR 310.6 million (first half of 2015: EUR 311.6 million). Due to the currently challenging market environment at EUPEC, the Group’s operating earnings (EBITDA) decreased to EUR 4.0 million (first half of 2015: EUR 12.9 million). By contrast, the majority of the portfolio companies developed very positively – especially STS Acoustics, Artmadis, A+F, Zanders and Norsilk.

The portfolio was divided into five segments – Automotive & Industrial, Consumer Goods & Logistics, Wood & Paper, Construction & Infrastructure and Engineering & Technology – that highlight the core competences and profile of mutares AG as a production-oriented specialist. The Wood & Paper segment was supplemented with the acquisition of Cenpa, a French core board manufacturer, and now comprises three investments. In addition to the strategic repositioning and optimisation of the cost structure, the restructuring also focuses on the modernisation of existing production capacity.

STS Acoustics has already landed a second contract for the location in Poland, which is currently being established. Thanks to two acquisitions, Artmadis drove its expansion forward and opened up new business areas in the period under review. By reducing waste in the production process and successfully implementing the capacity adjustment, Zanders made significant process in the restructuring.

In the first half of the year, mutares AG also pressed ahead with the announced strategic developments in HR. In addition to the move to a larger office, multiple experienced and quali- fied employees were hired for both the operating and M&A activities of mutares AG. Since the start of the year, the number of employees at mutares AG has considerably increased. As a result of this development, we have laid the groundwork to achieve our growth targets in the medium term.

TO OUR SHAREHOLDERS

April 25, 2016

mutares achieved record results in FY 2015 and proposes a dividend of EUR 0.60 per share

Today, the mutares Group published its Annual Report for FY 2015. The group achieved again record levels in its consolidated revenues, operating earnings, cash and equity position, and NAV. The Executive Board and Supervisory Board want their shareholders to participate in the great success of the company by proposing a dividend payment of EUR 0.60 per share.

May 10, 2016mutares increases again profitability in the first quarter 2016

The mutares Group increased its operating earnings (EBITDA) to EUR 4.4m by generating re-venues of EUR 152.8m in the first quarter.

May 25, 2016mutares acquires Sonoco Paper France

mutares AG acquires the French core board manufacturer Sonoco Paper France from Sonoco Products Company. The company has been renamed into Cenpa SAS and generated a turnover of EUR 32m with 73 employees in 2015.

June 6, 2016

AGM 2016 approves dividend payment of EUR 0.60 per share

The annual general meeting of mutares AG, which took place in Munich on June 3, 2016, approved all resolutions proposed by the management with large majority. The dividend pay-ment of EUR 0.60 per share was approved.

June 30, 2016mutares portfolio: Artmadis acquires JD Diffusion and Excédence

Artmadis, a portfolio company of mutares AG, is the leading distributor for tableware and kitchenware in France. After the successful takeover of the Belgian distributor Verbeelen, Artmadis has made two further add-on acquisitions leading the company to a post-merger sales level of more than EUR 100m.

Highlights of the first half year 2016

6 7

Share price performance in the first half of 2016

Concerns regarding the development of the global economy following the UK’s decision to leave the EU in addition to persistent weaknesses on the oil and gas market had a negative impact on the price performance of the mutares share in the first half of the year. The share traded at EUR 13.00 as at June 30, 2016.

From January 1 to June 30, 2016, the average daily trading volume in the mutares share re-mained stable on all German stock exchanges at 5,262 shares (previous year: 5,163 shares). At the end of the period under review, there were no significant changes to the shareholder structure. Free float amounts to 45%. 55% of the shares are owned by the company’s founders (all information is based on XETRA prices while taking into account capital measures in 2015).

Dividend payment

On June 3, 2016 the Executive Board provided information on the company’s business per-formance in 2015 and took questions from the owners at the Annual General Meeting of mutares AG in Munich. All resolutions proposed by management were approved by a great majority and the actions of the Executive Board and Supervisory Board were formally approved. The Annual General Meeting also resolved a dividend payment of EUR 0.60 per share (while considering capital measures in the past financial year). As a result, the total divi-dend payments amounted to EUR 9.3 million (previous year: EUR 11.0 million).

Investor Relations

In the first half of the year, mutares AG’s management continuously informed institutional investors and financial analysts of current business performance and events of significance for the share’s price performance at numerous roadshows in various financial centres, such as Frankfurt, London and New York. In addition, mutares AG’s management regularly discussed the company’s strategy with institutional investors and the financial and business press during personal discussions. The mutares share is regularly analysed and rated by two renowned banks – Hauck & Aufhäuser Institutional Research and Baader Helvea Equity Research – as well as SMC Research, a team of analysis specialists for medium-sized enterprises. In their current studies, all analysts confirmed their recommendation to buy the mutares share and confirmed their price targets between EUR 20.00 and EUR 24.60. The complete research studies can be found under Investor Relations on the homepage www.mutares.de.

The mutares share is listed in the Entry Standard of the Frankfurt Stock Exchange. As designa- ted sponsors, Dero Bank AG and Baader Bank AG ensure binding bid/ask prices, appropriate liquidity and the adequate tradeability of the mutares share. Further relevant information for interested investors can be found in the Investor Relations section on the homepage www.mutares.de.

mutares on the capital market

TO OUR SHAREHOLDERS

Group interim management reportfor the period from January 1 to June 30, 2016

Reports from the portfolio companies

To better reflect the further diversification of the portfolio, mutares grouped its investments into the following five segments in the period under review:

Automotive&Industrial

ConsumerGoods&Logistics

Wood&Paper

Construction&Infrastructure

Engineering&Technology

The Executive Board believes that this segmentation further enhances the profile of the mutares Group and thus increases its growth opportunities.

The following commentary reflects the development of the mutares Group’s individual in-vestments. As at 30 June 2016, the Group consolidates 13 operating investments:

Automotive & Industrial segment

No. Investment Industry Headquarters Acquisition

1 ElastomerSolutionsGroup Automotive supplier Wiesbaum_DE Aug_2009 of rubber mouldings

2 STSAcousticsGroup Automotive supplier for Turin_IT July_2013 acoustic and heat insulation

3 GeesinkNorbaGroup Manufacturer of refuse Emmeloord_NL Feb_2012 collection vehicles

Consumer Goods & Logistics segment

No. Investment Industry Headquarters Acquisition

4 ArtmadisGroup Retailer of household goods Wasquehal_FR Aug_2012

5 Grosbill E-commerce retailer of Paris_FR Aug_2015 consumer electronics

6 KlAnnPackaging Manufacturer of metal Landshut_DE June_2011 packaging

1. Economic report

98

GROUP INTERIM MANAGEMENT REPORT

Wood & Paper segment

No. Investment Industry Headquarters Acquisition

7 ZandersGroup Manufacturer of speciality paper Bergisch Gladbach_DE May_2015

8 Norsilk Manufacturer of wood Honfleur_FR Oct_2015 panelling and floor coverings

9 Cenpa Core board manufacturer Schweighouse_FR May_2016

Construction & Infrastructure segment

No. Investment Industry Headquarters Acquisition

10 EupECGroup Supplier of coatings for Gravelines_FR Jan_2012 oil and gas pipelines Sassnitz_DE

11 BSLPipes&Fittings Manufacturer of Billy Sur Aisne_FR July_2015 pipeline components

Engineering & Technology segment

No. Investment Industry Headquarters Acquisition

12 FTW Supplier for the machine Weißenfels_DE Feb_2010 tool industry

13 A + F Manufacturer of end-of-line Kirchlengern_DE Dec_2014 packaging machinery

1110

European footprint

Subsidiaries of mutares

The following data on business performance refers to pro rata Group revenues, unless stated otherwise. In the first half of 2016, the business performance of the individual investments was as follows:

GROUP INTERIM MANAGEMENT REPORT

Automotive & Industrial Segment

Paula DiasCEO

Elastomer Solutions Group

CompanyprofileThe Elastomer Solutions Group (ESG) develops, produces and distributes rubber mouldings for the automotive industry. It employs approximately 400 employees at its five locations in Germany, Portugal, Slovakia, Morocco and Mexico. the core focus of ESG lies on the deve- lopment and production of covers for the protection of wiring harnesses in automotive wiring systems, e.g. between vehicle doors and bodywork. the Elastomer Solutions Group (ESG) was acquired from Diehl Group in August 2009.

DevelopmentIn the past, production capacity at the locations in Morocco, Mexico, Portugal and Slovakia was increased thanks to extensive investments in the production facilities. As a result, the in-dustrialisation of products, especially at the new plants in Mexico and Morocco, developed successfully. After continuing the successful ramp-up at the site in Morocco, a contract was signed to further expand the site, which is expected to take place in the second half of 2016 once the building has been completed. The plant in Mexico significantly increased its revenues thanks to the production ramp-up. On the market side, ESG further acquired new contracts, most notably from Yazaki and Porsche. In the first half of financial year 2016, revenues slightly increased year-on-year to EUR 15.2 million. Despite ongoing start-up costs for the two new plants, significantly positive operating earnings (EBITDA) were achieved. An-other year-on-year increase in revenues and positive EBITDA are expected for financial year 2016.

1312

STS Acoustics Group

CompanyprofileIn July 2013, mutares acquired Autoneum Italy S.p.A, which was renamed to STS Acoustics.STS develops and produces innovative solutions in acoustic and heat insulation systems for the engine compartment and interior of vehicles. As one of the leading suppliers, the STS customer base includes large truck manufacturers such as Daimler, MAN, Scania and Volvo as well as automotive manufacturers such as Alfa Romeo, Fiat, Jeep, Ferrari and Maserati. STS operates from three different sites in Italy and employs around 700 employees in total.

DevelopmentIn financial year 2015, a major and strategically important customer order in the heavy com-mercial vehicles business line was acquired to sustain more profitable growth for the location in Poland, which is currently being established. In the first half of 2016, STS also acquired another lucrative contract with a total annual volume in the mid-seven-figure range. The new site in Poland is to be commissioned according to plan in the fourth quarter of this financial year. As a result, STS is in the best position to achieve more growth thanks to its strategically advantageous location and the cost advantages that exist. The management is also as-sessing the option of add-on acquisitions to generate more growth for the Group. At EUR 71.9 million, revenues were significantly above the previous year’s level and operating earnings were substantially positive again in the first half of 2016. For 2016 as a whole, STS anticipates a slight increase in revenues compared to fiscal year 2015 and significantly positive operating earnings.

Andreas BeckerCEO

GROUP INTERIM MANAGEMENT REPORT

Acquisition August 2009

Seller Diehl Group_DE

Revenues2015 approx. EUR 29 million

Employees approx. 400

Acquisition July 2013

Seller Autoneum Group_CH

Revenues2015 approx. EUR 135 million

Employees approx. 700

14 15

GeesinkNorba Group

CompanyprofileThe GeesinkNorba Group (GNG) is a leading provider of solutions for waste collection. GeesinkNorba develops, produces and distributes innovative, high quality garbage trucks and stationary presses. The company sells its products mainly in Europe and has its own sales and service departments in the Netherlands, Sweden, United Kingdom, France, Germany, Spain and Italy. Other European and non-European countries are served via an export sales team and a network of agents and distributors. GNG operates a main plant in the Netherlands as well as an assembly plant in Sweden and employs around 390 employees in total.

DevelopmentIn the first half of 2016, GNG sustainably adjusted production to the rise in demand and sta-bilised incoming orders at a significantly higher level compared to the previous year. In the first half of 2016, revenues increased year-on-year by 6.4% to EUR 41.1 million. Prefinancing large orders and financing working capital for higher production levels have a negative impact on GNG’s liquidity. Furthermore, GNG still depends on financing from shareholders or other sources of financing. Given the tight liquidity situation, the company‘s management is therefore focusing on stabilising cash flows (see section 2.3). Optimising working capital, maintaining a high level of production in the long term and significantly increasing the efficiency of the Geesink Group as a whole will be the focus for the rest of the year. For 2016 as a whole, GNG expects a sharp increase in revenues and a significant improvement in operating earnings as against the previous year based on persistently strong incoming orders and the high order backlog.

Jens BeckerCEO

Consumer Goods & Logistics Segment

Artmadis Group

CompanyprofileIn August 2012, mutares acquired Artmadis, the leading French wholesaler of household goods, from ARC International, the world’s largest manufacturer of crystal and glass ware. The company’s customers include all major French retail chains such as Carrefour, Intermarché, Auchan, Leclerc, Casino, Système U as well as specialised retailers and leading online mail order houses. Artmadis employs around 220 employees.

DevelopmentIn the period under review, the Group’s expansion made progress following the establish- ment of a procurement branch in Hong Kong in 2014 and the successful takeover of the Belgian wholesaler Verbeelen in 2015. In the first half of 2016, Artmadis acquired two other companies: JD Diffusion is a French wholesaler of household goods and gift items with a focus on retail that complements the sales channels of Artmadis. In addition, Artmadis is expanding its product range with additional new categories such as gift and decoration items. The takeover of Cogemag, a French stock clearance specialist, is contributing towards the optimisation of working capital and provides access to direct digital sales channels thanks to its website “Excédence”. In the first half of 2016, the revenues and operating earnings of Artmadis were at the previous year’s level. The management is convinced that the Group’s revenues will be significantly higher than EUR 100 million in the medium term. At the same time, the gross profit margin is expected to improve and positive operating earnings are anticipated again for 2016 as a whole thanks to the rise in revenues with own brands.

Pascal DupenloupCEO

Automotive & Industrial Segment

GROUP INTERIM MANAGEMENT REPORT

Acquisition February 2012

Seller Platinum Equity_US

Revenues2015 approx. EUR 76 million

Employees approx. 390

Acquisition August 2012

Seller ARC International_FR

Revenues2015 approx. EUR 76 million

Employees approx. 220

16 17

Consumer Goods & Logistics Segment

Grosbill

CompanyprofileGrosbill was acquired in August 2015 from the French Auchan Group. The company is an independent omni-channel retailer for IT components and consumer electronics and the market leader in France. The products are sold via its own website and the network of nine own shops. Grosbill employs around 140 employees at its headquarters in Paris as well as in the shops.

DevelopmentFollowing the acquisition by mutares, with the support of a CEO with experience in the indus-try, the Grosbill brand was stronger focused on the gaming business and became more attrac- tive for other customers by expanding the product range. At the same time, the company in-vested in the repositioning of the brand and the website and the modernisation of shops to consolidate its position in the omni-channel business. Administrative functions previously car-ried out by the parent company have now been fully integrated into in-house processes. In the first half of financial year 2016, Grosbill achieved revenues of EUR 41.6 million. For the second half of 2016, Grosbill anticipates a further rise in revenues and an improved gross profit margin, which will have a positive impact on operating earnings, as a result of the strategic measures that have been introduced as well as the seasonality of business activities.

Philip SzlangHead of mutares France

* Relates to period of being included in the group’s financial statements.

KLANN Packaging

CompanyprofileIn June 2011, mutares acquired the Decorative business unit from the HUBER Packaging Group and renamed it KLANN Packaging. With approximately 100 employees, KLANN develops and produces high-quality promotional and sales packaging made of printed tinplate at its compa-ny location in Landshut. KLANN’s outstanding expertise is the development and production of high-quality packaging with special colour intensity and particular embossing techniques. the customers of KLANN are well-known brand manufactures and commercial companies of different sectors.

DevelopmentIn 2015, the customer base was successfully expanded thanks to new products in particular. The volume sold to several reference customers was increased. These positive develop- ments were driven by a new sales-oriented CEO, also in the first half of financial year 2016. In the first half of financial year 2016, total output increased accordingly year-on-year. For 2016 as a whole, KLANN expects revenues to be at the same level as the previous year and expects to break even in operating earnings thanks to the improved cost structure.

Dr Lennart SchleyManaging Director

Acquisition August 2015

Seller Auchan Group_FR

Revenues2015* approx. EUR 32 million

Employees approx. 140

Acquisition June 2011

Seller Huber Group_DE

Revenues2015 approx. EUR 14 million

Employees approx. 100

GROUP INTERIM MANAGEMENT REPORT

18 19

Wood & Paper Segment

Zanders Group

CompanyprofileIn May 2015, the paper manufacturer Zanders GmbH was acquired from the Finnish Metsä Group. Zanders is an internationally renowned manufacturer of speciality paper and employs around 530 employees. The long-established company was founded in 1829 and has impressed with innovation and premium quality ever since. The company’s product portfolio includes various high-quality labelling and packaging papers as well as premium cardboards. These are represented in particular by the globally recognised brand CHROMOLUX. Many customers in the consumer and luxury goods industry, such as Danone, Heineken, Nestlé, Chanel and the LVMH Group trust in the high quality of Zanders’ products for their labels and packaging.

DevelopmentThe restructuring plan developed immediately after mutares’ takeover of Zanders is aimed particularly at the adjustment of the company’s infrastructure and capacity to the utilisation expected in the medium term. In the first half of 2016, significant progress was made in key parts of this restructuring plan. The collective agreement concluded for the restructuring was implemented and unused commercial space was profitably let. In addition, the drop in commodity prices and the decrease in waste in the production process had a positive impact on Zanders’ profitability. Liquidity increased with the establishment of a factoring line. In the first half of 2016, Zanders achieved revenues of EUR 48.0 million, which was thus slightly below the level of the previous year. This was due to the transaction-related termination of contract manufac-turing in the area of paper finishing. In the second half of 2016, this business will grow again thanks to new customers. For the 2016 financial year as a whole, the management anticipates an increase in revenues and a significant improvement in operating earnings resulting from the further implementation of improvement projects.

Dr Lennart SchleyManaging Director

Norsilk

CompanyprofileIn October 2015, mutares acquired the Finnish Metsä Group‘s wood business in France. Norsilk is a French manufacturer and retailer of wood panelling and floor coverings and employs a total of around 110 employees at its sites in Boulleville and Honfleur. Norsilk has a diversified cus-tomer structure in the DIY, wholesale and industry segments.

DevelopmentThe restructuring programme implemented immediately after the acquisition of Norsilk in the past financial year focuses on increasing revenues, optimising the product portfolio, reducing cost items in the long term and significantly increasing production efficiency. In financial year 2016, initial success was achieved with the renegotiation of framework agreements, which led to a significant decrease in logistics costs. In addition, production efficiency significantly in-creased thanks to the initiation of process optimisations. Other projects were initiated to achieve savings in administrative functions and structures. The implementation of an ERP system as a further basis to create transparency and increase efficiency has nearly been completed. In the first half of 2016, Norsilk achieved revenues of EUR 24.7 million, which was thus slightly be- low the level of the previous year. For 2016 as a whole, the management anticipates a slight decrease in revenues and a significant increase in operating earnings compared to financial year 2015.

Patrick OschustManaging Director

GROUP INTERIM MANAGEMENT REPORT

* Relates to period of being included in the group’s financial statements

Acquisition May 2015

Seller Metsä Group_FI

Revenues2015* approx. EUR 57 million

Employees approx. 530

* Relates to period of being included in the group’s financial statements

Acquisition October 2015

Seller Metsä Group_FI

Revenues2015* approx. EUR 9 million

Employees approx. 110

20 21

Wood & Paper Segment

Cenpa

CompanyprofileIn May 2016, Sonoco Paper France was taken over from the US-based Sonoco Products Company and was given a new traditionrich name: Cenpa. This manufacturer of core board using recycled paper is based in Schweighouse, Alsace. Products are mainly used for tubes and cores, particularly in the hygiene industry. The company has a strong market position in France and Germany and employs around 80 people.

DevelopmentA strategic concept was developed immediately after the acquisition of Cenpa. This particu- larly aims at saving costs in other operating expenses and optimising energy and material purchases. In addition, targeted investments are to be made in the modernisation of existing production capacity. Immediately after the takeover, indirect functions, particularly in the areas of sales, purchasing, production planning, finance and HR, that were previously performed by service centres of the former parent company had to be completely reestablished. A CEO with experience in the industry will further develop customer relationships. For the period belonging to mutares Group, Cenpa achieved revenues of EUR 3.1 million and almost broke even in oper-ating earnings. For financial year 2016, the company anticipates a slight year-on-year decrease in revenues and expects operating earnings to remain negative for the time being.

André CalistiCEO

Construction & Infrastructure Segment

EuPEC Group

CompanyprofileIn January 2012, the EUPEC Group was acquired from the Indonesian Korindo Group. EUPEC has been the largest European provider of coatings for oil and gas pipelines for over 40 years. The EUPEC Group currently has three French plants in the Dünkirchen area and one plant in Germany in Mukran on the island of Rügen and employs around 100 employees. EUPEC proved its high level of expertise in delivering technologically advanced solutions in numerous international projects. During the years 2008 to 2012, EUPEC provided all concrete coatings for the gas pipelines of the Nord Stream Project (Nord Stream I) in the Baltic Sea.

DevelopmentDue to the ongoing drop in oil prices, many customer projects were postponed or not put out to tender. As a result, EUPEC’s revenues dropped significantly in the first half of 2016. EUPEC further intensified its sales activities to acquire new projects in a highly challenging environment. The contract for the construction of two additional gas pipelines from Russia to Germany based on the model of Nord Stream I was awarded to a competitor. Thanks to the advantageous location of the production site in Mukran on Rügen Island, the EUPEC Group may be able to benefit in Nord Stream II. For the rest of the year, the management is assessing capacity adjustments and expects a significant drop in revenues and considerably lower operat-ing earnings year-on-year due to the decline in market demand.

Bernard GuisolCEO

* According to statutory financial statements

Acquisition May 2016

Seller Sonoco_US

Revenues2015* approx. EUR 33 million

Employees approx. 80

Acquisition January 2012

Seller Korindo Group_ID

Revenues2015* approx. EUR 72 million

Employees approx. 100

GROUP INTERIM MANAGEMENT REPORT

22 23

Construction & Infrastructure Segment

BSL Pipes & Fittings

CompanyprofileBSL Pipes & Fittings (BSL) was acquired by mutares from the Génoyer industrial group in July 2015. The company is a renowned French pipeline manufacturer with an international customer base. BSL produces welded pipeline components of up to 12 metres in length. The company employs around 90 employees at its headquarters in Billy-sur-Aisne. Its custom-ers include international companies from the oil and gas industry, such as ExxonMobil, Shell, total and BP.

DevelopmentThe increase in revenues in the medium term and immediate cost savings were key elements of the restructuring plan implemented immediately after the takeover. While BSL’s revenues significantly declined due to a drop in demand in the oil and gas business, the company made a lot of progress with various measures to achieve cost savings. Negative development in the industry will still have an adverse impact on the company’s liquidity. Therefore, the implemen-tation of planned restructuring measures is a key element to secure liquidity. In the first half of financial year 2016, BSL achieved revenues of EUR 7.5 million and realised planned operating earnings. For the rest of the year, the company anticipates a significant decrease in revenues and a slight improvement in operating profitability year-on-year as a result of the implementa-tion of restructuring projects.

François MartinCEO

Engineering & Technology Segment

Fertigungstechnik Weißenfels

CompanyprofileFertigungstechnik Weissenfels (FTW) develops, manufactures and distributes highly accurate and dynamic NC rotary table systems and special devices for the machine tool industry. It employs about 100 employees at its site in Weissenfels near Leipzig. FTW offers end-to-end solu- tions tailored to customers’ specifications, which can be integrated optimally in their machines. FTW’s customers are leading European machine tool manufacturers. the company was ac- quired in February 2010 from the German Römheld Group.

DevelopmentThe expansion of the customer base in financial year 2015 was apparent in the first half of 2016, for instance, in the successful delivery to a new major customer in Asia. In the first half of 2016, revenues saw a sharp year-on-year increase to EUR 6.8 million. Operating earnings were at the level of 2015. The company’s liquidity is adversely affected by its persistently weak earnings situation. Thanks to agreements with external investors, funding for FTW’s business operations was secured with liquidity. For 2016 as a whole, FTW anticipates a significant increase in revenues associated with a considerable increase in operating earnings.

Norbert GabrielManaging Director

* Relates to period of being included in the group’s financial statements

Acquisition July 2015

Seller Génoyer Group_FR

Revenues2015* approx. EUR 9 million

Employees approx. 90

Acquisition February 2010

Seller Römheld Group_DE

Revenues2015* approx. EUR 13 million

Employees approx. 100

GROUP INTERIM MANAGEMENT REPORT

24 25

A + F Automation + Fördertechnik

Companyprofilemutares acquired A+F Automation + Fördertechnik in December 2014. A+F, which has been a leading provider of final packaging machines for more than 40 years, has an excellent reputation worldwide for its expertise in implementing high-quality packaging solutions. The company currently employs 150 employees at its location in Kirchlengern. As a globally active provider of integrated and innovative system solutions, A+F offers a comprehensive range of customer-specific solutions. The company’s customer base includes well-known market leaders in the dairy and foodstuffs industry.

DevelopmentFurther expanding sales structures, winning back former customers and contacting new ones as well as optimising the product portfolio and efficiency when handling large projects were cornerstones in the company’s successful development in the first half of 2016. Sales activities were supported by the establishment and reactivation of global sales representatives and a strong presence at trade fairs, also in Asia and the USA. The service business is further expanding. This is reflected in the significant year-on-year increase in incoming orders and order backlog. In the first half of 2016, A+F’s revenues were only slightly below the level of the previous year at EUR 11.7 million. By contrast, operating earnings significantly improved. For 2016 as a whole, A+F expects revenues to be considerably higher than the previous year’s level and expects profitability to remain positive.

Engineering & Technology Segment

Robert RoigerManaging Director

The mutares Group acquires companies or groups with weak earnings and provides them with operational support.

For comments on the comparability of the assets, financial position and cash flow due to changes in the consolidation group for the period from January 1 to June 30, 2016, we refer to our comments in the condensed notes to the consolidated financial statements.

Group companies are distinguished by market segment, business model, progress in the restruc-turing cycle and date of acquisition, which all lead to fluctuations in Group EBITDA. Therefore, the mutares Group’s EBITDA is only a very limited indicator for the actual operating perfor-mance of the portfolio companies.

The Executive Board is very pleased with the performance of some portfolio companies in the first half of 2016 but still sees considerable improvement potential for other portfolio compa-nies. The Executive Board still believes that mutares is well equipped to further increase Group revenues and improve earnings in the long term. A benchmark for the Group’s success is essentially the progress achieved in the restructuring and the development of its invest- ments as well as M&A transactions that make a quantifiable contribution to value.

2.1. Assets and financial position

As at June 30, 2016, total assets in the mutares Group amounted to EUR 417.0 million (December 31, 2015: EUR 426.8 million). This change is mainly attributable to lower cash and cash equivalents. An increase in property, plant and equipment to EUR 87.8 million (December 31, 2015: EUR 81.9 million), higher inventories of EUR 121.5 million (December 31, 2015: EUR 112.1 million) and a rise in receivables and other assets of EUR 147.0 million (December 31, 2015: EUR 143.2 million) had an offsetting effect on total assets. Cash and cash equivalents and other securities amounted to EUR 52.1 million on the reporting date (December 31, 2015: EUR 81.2 million), while liabilities to financial institutions amounted to EUR 34.6 million (December 31, 2015: EUR 35.1 million), which largely resulted from the recognition of “recourse” factoring as in the previous year.

Equity in the mutares Group decreased from EUR 73.3 million as at December 31, 2015 to EUR 56.1 million as at June 30, 2016. This change was mainly due to the dividend payment to shareholders in the amount of EUR 9.3 million that was resolved by the Annual General Meeting in addition to negative comprehensive income of EUR 7.1 million in the first half of 2016. Consequently, the equity ratio declined to 13.4% as against December 31, 2015 (December 31, 2015: 17.2%).

2.2. Results of operations

In the period under review, the requirements set forth in the German Accounting Guidelines Implementation Act (Bilanzrichtlinie-Umsetzungsgesetz – BilRUG) were implemented for the first time. For these condensed consolidated interim financial statements, this primarily resulted in an amendment to the definition of revenues.

2. Assets, financial position and results

Acquisition December 2014

Seller Oystar Group_DE

Revenues2015 approx. EUR 24 million

Employees approx. 150

GROUP INTERIM MANAGEMENT REPORT

26 27

At EUR 310.6 million, revenues were at the previous year’s level in the first half of 2016 (first half of 2015: EUR 313.5 million). In contrast, production output increased by EUR 5.7 million to EUR 316.9 million. For information on the impact of changes within the consolidation group, please refer to our comments in the condensed notes to the consolidated financial statements for the period from January 1 to June 30, 2016. In particular, the currently challenging market environment at EUPEC had a further impact. Other portfolio companies, most notably STS and GNG, reported significant increases in revenues. Please refer to our comments on the current development in the reports from the portfolio companies.

Other operating income decreased considerably by EUR 8.7 million to EUR 24.2 million. This was mainly due to the lower release of provisions of EUR 2.2 million (first half of 2015: EUR 5.5 million) and the lower release of the difference resulting from capital consolidation of EUR 18.2 million (first half of 2015: EUR 21.4 million).

The cost of materials, personnel expenses and other operating expenses moved around the level of the the first half of 2015. For information on the impact of changes within the consolidation group, please refer to our comments in the condensed notes to the consolidated financial statements for the period from January 1 to June 30, 2016. In the first half of 2016, EBITDA amounts to EUR 4.0 million (first half of 2015: EUR 12.9 million). The decrease was mainly caused by development at EUPEC. By contrast, development at Zanders and Norsilk had a positive impact. Consolidated net income was -EUR 7.1 million (first half of 2015: EUR 1.6 million). The Executive Board plans to achieve a positive result for 2016 as a whole since the business activities of a number of investments that are subject to seasonal fluctuations are significantly stronger in the second half of the year. In addition, the Executive Board ex- pects significant progress to be made in the restructuring of key investments during the rest of financial year 2016 and thus anticipates an associated improvement in earnings.

2.3. Companies whose status as a going concern is at risk

As a result of the rise in working capital to increase production levels and prefinance orders, the liquidity situation of the GeesinkNorba sub-group continues to be tense. The company fell short of planned operating earnings due to a slower than planned production increase in the period under review. The sub-group relies on continuation of existing financing from the shareholders and the bank in addition to an improvement in the prefinancing of made-to-order production to avoid the threat of liquidity bottlenecks. The management will concentrate on stabilising cash flow, optimising working capital and maintaining the increase in production levels during the rest of financial year 2016. Based on the strong incoming orders, high order backlog and measures initiated to increase efficiency, the management assumes that it will manage to overcome the currently tense liquidity situation. Should it fail to do so, the status of the sub-group as a going concern would be at risk.

3.1. Forecast

The future development of mutares AG strongly depends on the acquisition and disposal of investments and on the development of existing portfolio companies. mutares AG will assess new acquisitions on an ongoing basis and further develop based on company size and the attractiveness of their business.

The Executive Board has no new knowledge of material changes to the forecasts and other statements made in the last Group management report regarding the Group’s anticipated development in financial year 2016. In financial year 2016, mutares thus intends to achieve a slight year-on-year increase in Group revenues and positive operating earnings.

3.2. Opportunities and risks

GeneralbusinessperformanceThe future business performance of the mutares Group is associated with risks and opportu-nities related to the business model. Risk management plays an essential role as it is aimed at identifying risks at an early stage, minimising them, or bringing potential risks in line with associated benefits. In particular, deviations from target figures need to be identified at an early stage in order to react appropriately.

On June 23, 2016, the United Kingdom voted to leave the EU by way of referendum. Repre-sentatives from London and Brussels now have to negotiate the terms of the UK’s departure. In addition to the immediate effects, such as the significant devaluation of the British Pound and its negative impact on EU imports, this may have medium and long-term effects on the economic situation. However, these effects cannot be reliably predicted at the moment. The Executive Board is currently evaluating the possible effects on the mutares Group’s future business performance and will take suitable measures if this is considered necessary.

Guarantees/lettersofcomfortThere is an indemnification guarantee, which will expire in December 2016, in favour of the seller of an affiliated company for claims that may be raised against the seller if the affiliated company becomes insolvent in the period up to December 2016. Due to the subsidiary’s economic situation, the Executive Board currently assumes that the indemnification guarantee will not be utilised.

There are other guarantees and commitments totalling EUR 13.8 million (December 31, 2015: EUR 12.6 million). Due to the investments’ economic situation, the Executive Board currently assumes that the guarantees will not be called.

mutares AG has also issued a letter of comfort, which will expire in December 2018, to a third party for the fulfilment of a subsidiary’s obligations, the amount of which is not limited. Due to the subsidiary’s economic situation, the Executive Board currently assumes that the letter of comfort will not be utilised.

3. Forecast, opportunities and risks

GROUP INTERIM MANAGEMENT REPORT

28 29

Litigationsmutares AG is involved in a lawsuit with Diehl in connection with the acquisition of the Photovoltaics division from Diehl AKO Stiftung & Co. KG (“Diehl”) through its (indirect) subsidiary Platinum GmbH (“acquisition”) in 2013.

mutares AG entered into certain obligations towards Diehl in connection with the acquisition of the Photovoltaics division. Firstly, mutares AG had agreed to guarantee the continued existence of Platinum GmbH and the fulfilment of all liabilities of Platinum GmbH in favour of Diehl for a limited period (“letter of comfort”). Secondly, mutares AG had guaranteed the fulfilment of certain obligations of Platinum GmbH arising from the agreement to acquire the company in favour of Diehl (“guarantee”).

mutares AG and Platinum GmbH have contested all declarations made in favour of Diehl in December 2013 in connection with the acquisition of the Photovoltaics division on the grounds of fraudulent misrepresentation. Platinum GmbH filed for insolvency on 3 March 2014. The insolvency proceedings were initiated on June 1, 2014.

On March 3, 2014, mutares AG filed a lawsuit against Diehl together with Platinum GmbH at the Ravensburg District Court to have the obligations entered into in connection with the acquisition of the Photovoltaics division declared void. In this connection, mutares AG is assert- ing claims for damages against Diehl. Diehl for its part filed a (partial) lawsuit with the Ravens-burg District Court in May 2014, asking mutares AG to pay approximately EUR 15.4 million under the letter of comfort and the guarantee. Diehl also demands the Court to declare that mutares AG is obliged to reimburse Diehl for all additional losses Diehl incurs from non-fulfilment of the obligations entered into by mutares AG in connection with the acquisition of the Photovoltaics division. Diehl has estimated the provisional value of the lawsuit at approxi-mately EUR 22.5 million in total. mutares AG disputes the basis for damages and the amount of the loss. The two proceedings before the Ravensburg District Court were merged into a single proceeding. The insolvency administrator started rescission proceedings against the assets of Platinum GmbH i.I. in September 2014 on the side of Platinum GmbH i.l.

In financial year 2015, composition discussions repeatedly took place between the parties. However, these have not resulted in an amicable settlement so far. On October 16, 2015, the Ravensburg District Court issued a decision that evidence should now be taken by hearing various witnesses in oral proceedings. On June 8, 2016 and on June 15, 2016, the Ravens-burg District Court heard evidence from the first witnesses as to whether Diehl misled mutares AG and Platinum GmbH with regard to its revenue expectations for the Photovoltaics divi- sion. However, all evidence has not yet been heard and the Court has not yet revealed the conclusions it intends to draw from the testimonies that have already been given. Other testimonies are planned for October 2016.

The Executive Board of mutares AG as well as its legal advisors are still of the opinion that mutares AG effectively contested the obligations entered into in connection with the acquisi-tion in December 2013 and mutares AG also has a claim to be released from the obligations

3. Forecast, opportunities and risks

entered into in favour of Diehl. The Executive Board of mutares AG and its legal advisors there- fore assume that mutares AG will not have to make any significant payments to Diehl under the letter of comfort described above and the guarantee. mutares AG has therefore made provisions for legal costs only. Should the effectiveness of the appeals filed not be substantiated – contrary to the Executive Board’s current assessment – mutares AG may be defeated in the aforementioned legal dispute and may have to pay substantial claims that could have a negative impact on the future development of mutares AG in the long term.

On May, 18 2015, the insolvency administrator of Castelli S.p.A., Italy, took legal action against mutares AG at a court in Genoa for the payment of an amount of EUR 5.8 million. The insolvency administrator alleges in particular that mutares AG at no point intended to continue Castelli and therefore took the decision to liquidate the company too late. The Executive Board of mutares AG rejected the accusations and, together with its legal advisors, believes that the accusations are unfounded. To settle the lawsuit, the parent company made a one-off payment that was only slightly above the amount set aside for this purpose.

OtherBetween March 10 and March 13, 2015, the Directorate-General for Competition (“DG COMP”) of the European Commission searched Pixmania’s business premises. DG COMP is investigating alleged anticompetitive agreements in the e-commerce sector. Pixmania co-operated fully in the proceedings. At the present time, the size of any potential fine cannot yet be predicted.

Please see the Group management report 2015 for detailed information on opportunities and risks and the risk management system. The Group’s other material opportunities and risks have not changed since our evaluation in the Group management report 2015.

4. Other information

In accordance with Section 160 (1) No. 2 of the German Stock Corporation Act (Aktiengesetz – AktG), this information is included in the condensed consolidated financial statements under 6. Notes to the consolidated balance sheet.

GROUP INTERIM MANAGEMENT REPORT

30 31

Consolidated interim financial statementsof mutares AG for the period from January 1 to June 30, 2016

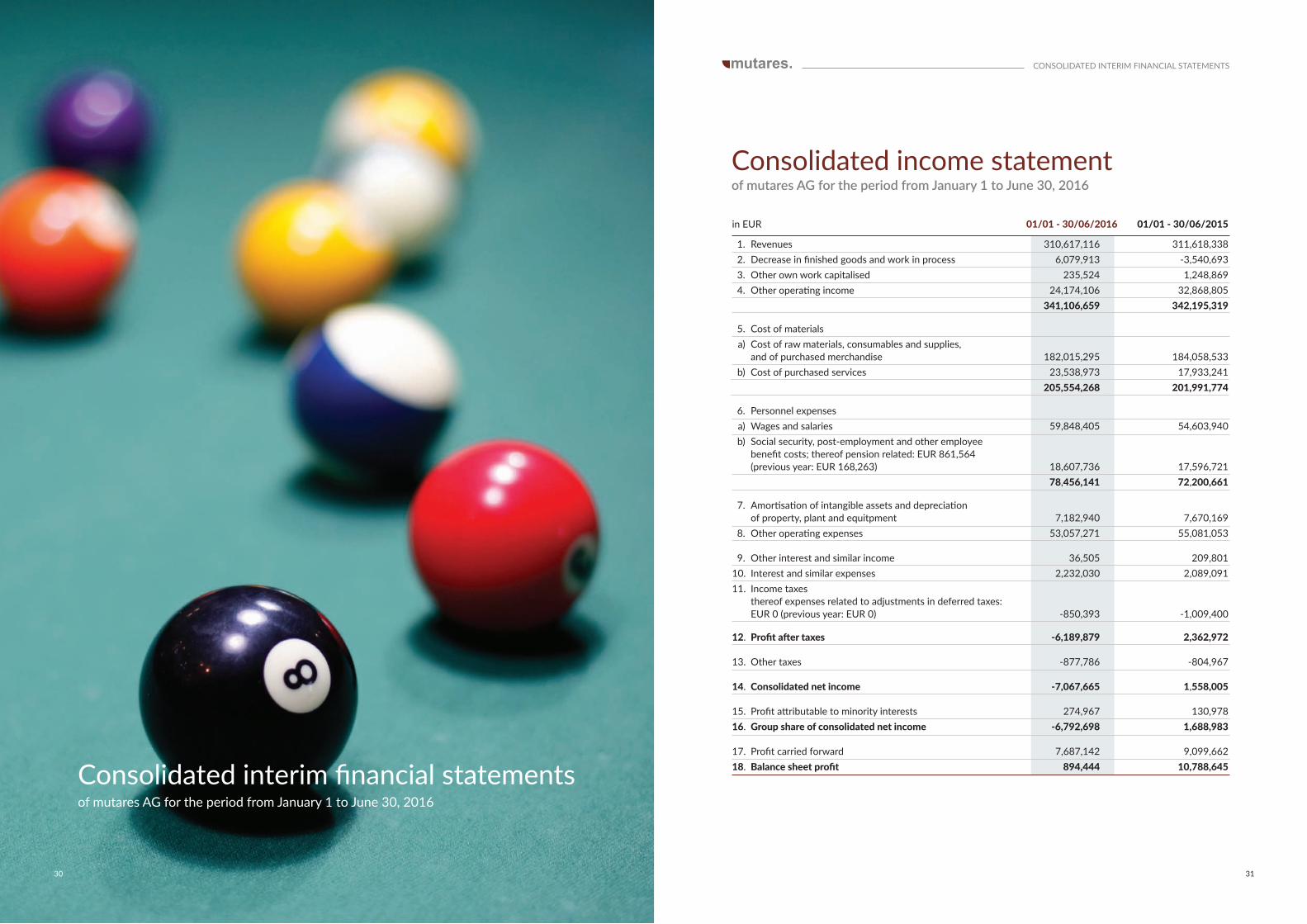

Consolidated income statementof mutares AG for the period from January 1 to June 30, 2016

in EUR 01/01-30/06/2016 01/01-30/06/2015

1. Revenues 310,617,116 311,618,338 2. Decrease in finished goods and work in process 6,079,913 -3,540,693 3. Other own work capitalised 235,524 1,248,869 4. Other operating income 24,174,106 32,868,805 341,106,659 342,195,319

5. Cost of materials a) Cost of raw materials, consumables and supplies, and of purchased merchandise 182,015,295 184,058,533 b) Cost of purchased services 23,538,973 17,933,241 205,554,268 201,991,774

6. Personnel expenses a) Wages and salaries 59,848,405 54,603,940 b) Social security, post-employment and other employee benefit costs; thereof pension related: EUR 861,564 (previous year: EUR 168,263) 18,607,736 17,596,721 78,456,141 72,200,661

7. Amortisation of intangible assets and depreciation of property, plant and equitpment 7,182,940 7,670,169 8. Other operating expenses 53,057,271 55,081,053

9. Other interest and similar income 36,505 209,80110. Interest and similar expenses 2,232,030 2,089,09111. Income taxes thereof expenses related to adjustments in deferred taxes: EUR 0 (previous year: EUR 0) -850,393 -1,009,400

12. Profitaftertaxes -6,189,879 2,362,972

13. Other taxes -877,786 -804,967

14. Consolidatednetincome -7,067,665 1,558,005

15. Profit attributable to minority interests 274,967 130,97816. Groupshareofconsolidatednetincome -6,792,698 1,688,983

17. Profit carried forward 7,687,142 9,099,66218. Balancesheetprofit 894,444 10,788,645

CONSOLIDATED INTERIM FINANCIAL STATEMENTS

ASSETS

in EUR 30/06/2016 31/12/2015

A. Non-currentassets 93,517,508 87,547,973I. Intangibleassets 5,042,260 5,072,873 1. Internally generated industrial and similar rights and assets 1,495,491 1,640,5782. Acquired concessions and industrial rights 2,334,451 2,526,8913. Prepayments 1,212,318 905,404

II. property, plant and equipment 87,809,191 81,888,975 1. Land and leasehold rights 43,497,585 43,459,5732. Technical equipment and machinery 36,070,727 32,526,1813. Other equipment 6,000,854 5,023,2794. Prepayments and assets under construction 2,240,025 879,942

III. Financial assets 666,057 586,125 1. Shares in affiliated companies 2 52. Investment securities 219,496 71,1323. Other loans 446,559 514,988

B. Current assets 320,613,809 336,470,524 I. Inventories 121,518,315 112,086,826 1. Raw materials, consumables and supplies 35,458,712 32,075,2452. Work in process 29,195,782 21,972,0093. Finished goods and merchandise 54,947,047 53,668,2174. Prepayments 1,916,774 4,371,355

II. Receivablesandotherassets 147,045,049 143,194,3481. Trade receivables 113,969,325 105,789,9532. Other assets 33,075,724 37,404,395

III. Securities 7,366,707 11,510,180 Other securities 7,366,707 11,510,180

IV. Cash and cash equivalents 44,683,738 69,679,170

C. Prepaidexpenses 2,842,101 2,688,117

D. Deferredtaxassets 19,000 19,000

E. Excessofplanassetsoverpensionliabilities 50,103 50,103

Total Assets 417,042,521 426,775,717

32 33

CONSOLIDATED INTERIM FINANCIAL STATEMENTS

EQuITY AnD lIABIlITIES

in EUR 30/06/2016 31/12/2015

A. Equity 56,087,694 73,272,609 I. Subscribedcapital 15,496,292 15,496,292 (Conditional capital) (1,500,000) (0) Less nominal value of treasury shares -6,012 -6,012 15,490,280 15,490,280

II. Capital reserve 36,145,026 36,145,026 III. Revenue reserves 3,855,756 3,956,1171 1. Legal reserve 131,688 131,6882. Other revenue reserves 3,724,068 3,824,429

IV.Currencytranslationdifferences -481,443 226,638

V. Minority interests 183,631 473,238

VI.Balancesheetprofit 894,444 16,981,310

B. Differenceresultingfromcapitalconsolidation 52,365,019 51,476,910

C. provisions 133,960,329 141,246,286 1. Provisions for pensions and similar obligations 68,659,125 67,791,7552. Tax provisions 2,725,769 2,865,2733. Other provisions 62,575,435 70,589,258

D.Liabilities 173,527,939 160,032,381 1. Liabilities to financial institutions 34,652,757 35,090,6932. Advance payments received 20,758,514 11,812,5253. Trade payables 82,126,367 75,276,3494. Other liabilities 35,990,301 37,852,814

E. Deferredincome 1,101,540 747,531

Totalequityandliabilities 417,042,521 426,775,717

Consolidated balance sheetof mutares AG as of June 30, 2016

Consolidated cash flow statementof mutares AG for the period from January 1 to June 30, 2016

kEUR 01/01-30/6/2016

Consolidated net income -7,068

Amortisation of intangible assets and depreciation of property, plant and equitpment 7,182

Increase (+)/decrease (-) of provisions -11,179

Other non-cash expenses (+)/income (-) -15,423

Gain (-)/loss (+) from disposal of non-current assets -739

Increase (-)/decrease (+) in inventories, trade receivables and other assets, that are not allocated to investing or financing activities -6,786

Increase (+)/decrease (-) of trade payables and other liabilities, that are not allocated to investing or financing activities 10,167

Interest expenses (+)/interest income (-) 2,195

Income tax expenses (+)/income (-) 850

Income taxes paid (-) -990

Cashflowfromoperatingactivites -21,791

kEUR 01/01-30/6/2016

Proceeds (+) from disposals of property, plant and equipment 894

Payments (-) for investments in property, plant and equipment -3,268

Payments (-) for investments in intangible assets -1,160

Proceeds (+) from disposals of financial assets 95

Payments (-) for investments in financial assets -25

Proceeds (+) from additions to the consolidation group 7,366

Payments (-) for additions to the consolidation group -15

Interest payments received (+) 37

Cashflowfrominvestingactivities 3,924

34 35

kEUR 01/01-30/6/2016

Dividend payments (-) to shareholders of the parent company -9,294

Proceeds (+) from raising (financial) loans 6,398

Repayments (-) of (financial) loans -6,497

Interest paid (-) -520

Cashflowfromfinancingacitivities -9,913

kEUR 01/01-30/6/2016

Change in the financial funds from cash relevant transactions -27,780

Exchange rate and consolidation scope related changes of the financial funds -1,019

TOTAL -28,799

Financial funds at beginning of the period 74,497

Financialfundsatendoftheperiod 45,698

Compositionofthefinancialfunds (kEUR) 30/06/2016

Cash and cash equivalents 44,684

Securities 7,367

Bank liabilities repayable at any time -6,353

TOTAl 45,698

CONSOLIDATED INTERIM FINANCIAL STATEMENTS

1 Facts about mutares AG

mutares AG was founded on 1 February 2008. It is headquartered in Munich and registered under number 172278 in the commercial register (section B) at the District Court of Munich.

2 General information on accounting standards

The condensed consolidated interim financial statements of mutares AG as at June 30, 2016 were prepared in accordance with Section 19 (1) lit. b) of the General Terms and Conditions of Deutsche Börse AG for the Open Market on the Frankfurt Stock Exchange that were appli-cable on the reporting date and in accordance with the provisions of the German Commercial Code (Handelsgesetzbuch – HGB) and based on the supplementary provisions of the German Stock Corporation Act (Aktiengesetz – AktG). The consolidated balance sheet is structured in accordance with Section 266 HGB. The consolidated income statement is structured using the total cost method outlined in Section 275 (2) HGB. The principle of presentation continuity was observed. All figures are shown in millions of euros (in short: EUR million) unless stated otherwise.

3 Scope and methods of consolidation

The condensed consolidated interim financial statements include both mutares AG as a parent company and the affiliated companies in which mutares AG owns the majority of voting rights, either directly or indirectly. As at June 30, 2016, the consolidation group changed as follows as against December 31, 2015:

_Acquisition and first-time consolidation of Sonoco Paper France SAS (Schweighouse, France) with effect of May 24, 2016 (“Sonoco”). The corporate name change to Cenpa SAS (“Cenpa”) has been registered for entry in the local commercial register in the meantime.

_Acquisition of Cogemag SAS (Croix, France) as at June 30, 2016. In accordance with Section 296 (1) no. 2 HGB, this entity is not included in the consolidated financial statements as at June 30, 2016.

_Acquisition of the remaining shares (10%) in BGE Eisenbahn Güterverkehr GmbH, Bergisch Gladbach, (“BGE”) by Zanders GmbH as at June 10, 2016.

Foundations, acquisitions and deconsolidations of holding companies are not listed separately.

The methods of consolidation have not changed as against the consolidated financial state-ments as at December 31, 2015.

Valuation was performed in accordance with uniform group principles. The condensed con-solidated half-year financial statements were prepared on the assumption that the company is a going concern. Please see our comments in section 2.3 of the interim Group management report.

Condensed notes

4 Comparability of the financial statements

Due to the aforementioned changes to the consolidation group, the condensed consolidated interim financial statements as at June 30, 2016 can be compared to the comparative period only to a limited extent.

Comparabilityofthecondensedconsolidatedbalancesheet

The subsidiary Cenpa (formerly: Sonoco Paper France SAS), which was consolidated for the first time as at May 24, 2016, is presented in the condensed consolidated interim financial statements in the key items as listed below:

Balance sheet (EUR m) CenpaProperty, plant and equipment 8,9Inventories 3,5Receivables and other assets 4,1Cash and cash equivalents 6,1Other provisions 1,5Trade payables 4,1

Comparabilityofthecondensedconsolidatedincomestatement

Subsidiaries consolidated for the first time in the period under reviewCenpa, a subsidiary consolidated for the first time in the period under review, is included in the condensed consolidated income statement for 2016 as follows:

Income statement (EUR m) CenpaRevenues 3,1Cost of materials -2,4Personnel expenses -0,6Other operating expenses -0,7Share of consolidated net income 0,0

Subsidiaries consolidated for the first time in the comparative periodZanders, a subsidiary consolidated for the first time in the comparative period, is included in the condensed consolidated income statements for 2015 and 2016 as follows:

Income statement (EUR m) 2016 2015Revenues 48,0 9,1Cost of materials -29,7 -6,4Personnel expenses -13,7 -3,0Other operating expenses -9,0 -1,7Share of consolidated net income 0,5 0,0

36 37

CONSOLIDATED INTERIM FINANCIAL STATEMENTS

Subsidiaries included for the first time in the period under reviewAfter the end of the comparative period but before the beginning of the period under review, other subsidiaries were consolidated for the first time. These are included in the condensed consolidated income statement for 2016 as follows:

Income statement (EUR m) BSL Grosbill NorsilkRevenues 7,5 41,6 24,8Cost of materials -4,3 -36,4 -18,0Personnel expenses -2,4 -3,2 -2,6Other operating expenses -1,2 -6,4 -3,6Share of consolidated net income 2,1 0,0 1,7

Deconsolidated subsidiariesIn the condensed consolidated income statement of the comparative period, the following in-vestments, which are now deconsolidated, were included as follows:

Income statement (EUR m) Suir pIX Revenues 8,5 89,8Cost of materials -5,1 -76,7Personnel expenses -2,7 -12,2Other operating expenses -4,9 -12,5Share of consolidated net income -4,0 0,0

5 Accounting policies and valuation methods

The accounting policies and valuation methods have not changed compared to the consoli- dated financial statements as at December 31, 2015. In the reporting period, the require-ments set forth in the German Accounting Guidelines Implementation Act (Bilanzrichtlinie- Umsetzungsgesetz – BilRUG) were implemented for the first time. For these condensed conso-lidated interim financial statements, this primarily resulted in an amendment to the definition of revenues.

If the respective provisions were applied in the comparative period, an amount of EUR 1.9 million would have been reported in revenues instead of other operating income. This means that revenues would have amounted to EUR 313.5 million and other operating income would have amounted to EUR 30.9 million in the comparative period.

Condensed notes

6 Notes to the consolidated balance sheet

Non-currentassetsThe development of non-current assets is shown in the table of assets (see annex 2 to the condensed notes to the consolidated financial statements).

EquityBy resolution of the Annual General Meeting on June 3, 2016, an amount of EUR 9,294,168.00 was paid out from retained earnings of EUR 9,539,478.83 as at December 31, 2015 in the form of a dividend of EUR 0.60 for each dividend-bearing share. The remaining amount of EUR 245,310.83 was carried forward.

The Annual General Meeting on June 3, 2016 authorised the Executive Board to issue up to 1,500,000 subscription rights (“stock options”), with the approval of the Supervisory Board, to members of the Executive Board of the company, members of the management of affiliated companies in Germany and abroad and to the company’s staff and staff of affiliated companies in Germany and abroad until June 2, 2020 (“2016 mutares stock option plan”). The stock options authorise the subscription of up to 1,500,000 bearer shares in the company with a notional portion of the share capital of EUR 1 for each share. To operate the 2016 mutares stock option plan, the Annual General Meeting also resolved to contingently increase the share capital of the company by EUR 1,500,000.00 by issuing up to 1,500,000 bearer shares (“conditional capital 2016/I”).

By resolution of the Annual General Meeting on November 25, 2011, the Executive Board is authorised, until November 25, 2016 and with the approval of the Supervisory Board, to in-crease the company’s share capital once or multiple times by up to EUR 322,000.00 against contributions in cash or in kind by issuing up to 322,000 new bearer shares (authorised capital 2011/I). In the case of capital increases for cash, shareholders are entitled to subscrip-tion rights. With the approval of the Supervisory Board, the Executive Board is still authorised to bar shareholders’ subscription rights in the case of capital increases against cash contribu- tions in some cases. Authorised capital 2011/I was partially utilised in the amount of EUR 311,962.00 by resolution of the Executive Board and Supervisory Board on 9 May 2014.

On 9 May 2014, the Annual General Meeting resolved authorised capital 2014/I of up to EUR 691,000.00. This was rescinded by resolution of the Annual General Meeting on May 22, 2015 and authorised capital 2015/I was created. With the approval of the Supervisory Board, the Executive Board is authorised to increase the company’s share capital by up to EUR 7,000,000.00 in total by issuing up to 7,000,000 new bearer shares until May 21, 2020. Entry in the commercial register of the District Court of Munich took place on July 2, 2015. After partial utilisation, authorised capital 2015/I still amounted to EUR 5,600,000.00 as at June 30, 2016.

As at June 30, 2016, authorised capital thus amounted to EUR 5,610,038.00 in total and comprised authorised capital 2011/1 (EUR 10,038.00) and authorised capital 2015/1 (EUR 5,600,000.00).

38 39

CONSOLIDATED INTERIM FINANCIAL STATEMENTS

provisionsOther provisions are mostly personnel-related obligations and outstanding invoices. LiabilitiesLiabilities comprise the following:

Liabilities (EUR m) 30/06/2016 31/12/2015Liabilities to financial institutions 34,6 35,1Advance payments received 20,8 11,8Trade payables 82,1 75,3Other liabilities 36,0 37,8TOTAl 173,5 160,0

Other liabilities comprise the following:

Otherliabilities(EUR m) 30/06/2016 31/12/2015Taxes 5,5 4,6Social security 4,3 4,5Former shareholders 14,6 15,2Other 11,6 13,5TOTAl 36,0 37,8

7 Notes to the consolidated income statement

Other operating income decreased considerably by EUR 6.8 million to EUR 26.1 million. This is due in particular to the lower release of provisions and of the difference from capital consolidation, as described above.

8 Contingent liabilities

There is an indemnification guarantee, which will expire in December 2016, in favour of the seller of an affiliated company for claims that may be raised against the seller if the affilia-ted company becomes insolvent in the period up to December 2016. Due to the subsidiary’s economic situation, the Executive Board currently assumes that the indemnification guarantee will not be utilised.

There are also other guarantees and commitments totalling EUR 13.8 million (December 31, 2015: EUR 12.6 million). Due to the investments’ economic situation, the Executive Board currently assumes that the guarantees will not be called.

By way of resolution, the Annual General Meeting on May 22, 2015 authorised the compa-ny’s Executive Board to acquire own shares amounting to up to 10% of share capital. The shares acquired together with any own shares acquired for other reasons, which are held by the company or assigned to it in accordance with Section 71a et seq. AktG, may not exceed 10% of the company’s share capital at any time. The authorisation may be exercised by the company in full or in smaller amounts, on one occasion or several, but also by companies dependent on or majority-owned by the company or by third parties for its account or their account. The acquisition authorisation is valid until May 21, 2020.

As at June 30, 2016, mutares AG held 6,012 own shares, each representing EUR 1.00 of share capital. The excess of EUR 69,698.42 over the notional value as of the acquisition of the original 1,002 shares (in the period from January 15, 2015 to March 6, 2015) was offset against retained earnings. As a result of the capital increase from company funds in financial year 2015, the shares increased accordingly to 6,012 shares. The increase of EUR 5,010.00 was offset against the capital reserve.

ActionforannulmentOn June 10, 2014, a shareholder took action at the Munich District Court I to have the annual financial statements of mutares AG as at December 31, 2013 declared invalid and to appeal against individual resolutions by the Annual General Meeting of mutares AG on May 9, 2014. mutares AG submitted its defence on October 6, 2014, to which the opposing party responded in a reply dated December 8, 2014. mutares AG submitted another response on March 5, 2015. Following the hearing on April 23, 2015, the proceedings with respect to the composition proceedings in relation to the legal dispute before the Ravensburg District Court were suspended until further notice. The Executive Board of mutares AG and its legal advisors are of the opinion that the action is unjustified. Another shareholder has joined the legal dispute on the side of mutares AG. The plaintiff disputes the third-party intervention.

On June 22, 2015, a shareholder took action at the Munich District Court I to have the annual financial statements of mutares AG as at December 31, 2014 declared invalid and to appeal against the resolution confirming the dividend of the Annual General Meeting of mutares AG on May 22, 2015. By the order of July 30, 2015, the case was merged with the complaint of June 10, 2014 to be negotiated and decided jointly. The Executive Board of mutares AG and its legal advisors are of the opinion that the action is unjustified. Another shareholder has joined the legal dispute on the side of mutares AG.

Differenceresultingfromcapitalconsolidation In the first half of 2016, the net difference resulting from capital consolidation increased by EUR 0.9 million to EUR 52.4 million. Releases in the amount of EUR 18.2 million (first half of 2015: EUR 21.4 million) are reported in other operating income. These releases relate to ex-pected expenditures or losses or expected expenditures or losses that were originally planned and did not materialise. Consolidation measures, particularly the first-time consolidation of shares in Cenpa, resulted in an increase in this balance sheet item by EUR 16.4 million.

Condensed notes

40 41

CONSOLIDATED INTERIM FINANCIAL STATEMENTS

The Executive Board of mutares AG as well as its legal advisors are still of the opinion that mutares AG effectively contested the obligations entered into in connection with the acquisi-tion in December 2013 and mutares AG also has a claim to be released from the obligations entered into in favour of Diehl. The Executive Board of mutares AG and its legal advisors there- fore assume that mutares AG will not have to make any significant payments to Diehl under the letter of comfort described above and the guarantee. mutares AG has therefore made provisions for legal costs only. Should the effectiveness of the appeals filed not be substantia-ted – contrary to the Executive Board’s current assessment – mutares AG may be defeated in the aforementioned legal dispute and may have to pay substantial claims that could have a negative impact on the future development of mutares AG in the long term.

On May 18, 2015, the insolvency administrator of Castelli S.p.A., Italy, took legal action against mutares AG at a court in Genoa for the payment of an amount of EUR 5.8 million. The insolvency administrator alleges in particular that mutares AG at no point intended to continue Castelli and therefore took the decision to liquidate the company too late. The Executive Board of mutares AG rejected the accusations and, together with its legal advisors, believes that the accusations are unfounded. We also refer to our comments in the report on subsequent events.

9 Employees

In the first half of 2016, the mutares Group employed 3,137 people on average in accordance with Section 267 (5) HGB. These comprise 1,842 waged workers, 1,254 salaried employees and 41 apprentices.

10 Subsequent Events

By pleading of July 4, 2016, a shareholder recessionary and revocation claim was submit- ted to the Munich District Court I against the resolution confirming the dividend at the Annual General Meeting of mutares AG on June 3, 2016. The Executive Board of mutares AG and its legal advisors are of the opinion that the action is unjustified.

On July 14, 2016, the affected parties signed a composition deed to finally settle the lawsuit with the insolvency administrator of Castelli through mutares AG.

mutares AG has also issued a letter of comfort, which will expire in December 2018, to a third party for the fulfilment of a subsidiary’s obligations, the amount of which is not limited. Due to the subsidiary’s economic situation, the Executive Board currently assumes that the letter of comfort will not be utilised.

mutares AG is involved in a lawsuit with Diehl in connection with the acquisition of the Photo-voltaics division from Diehl AKO Stiftung & Co. KG (“Diehl”) through its (indirect) subsidiary Platinum GmbH (“acquisition”) in 2013.

mutares AG entered into certain obligations towards Diehl in connection with the acquisition of the Photovoltaics division. Firstly, mutares AG had agreed to guarantee the continued existence of Platinum GmbH and the fulfilment of all liabilities of Platinum GmbH in favour of Diehl for a limited period (“letter of comfort”). Secondly, mutares AG had guaranteed the fulfilment of certain obligations of Platinum GmbH arising from the agreement to acquire the company in favour of Diehl (“guarantee”).

mutares AG and Platinum GmbH have contested all declarations made in favour of Diehl in December 2013 in connection with the acquisition of the Photovoltaics division on the grounds of fraudulent misrepresentation. Platinum GmbH filed for insolvency on March 3, 2014. The insolvency proceedings were initiated on June 1, 2014.

On March 3, 2014, mutares AG filed a lawsuit against Diehl together with Platinum GmbH at the Ravensburg District Court to have the obligations entered into in connection with the acquisition of the Photovoltaics division declared void. In this connection, mutares AG is asserting claims for damages against Diehl. Diehl for its part filed a (partial) lawsuit with the Ravensburg District Court in May 2014, asking mutares AG to pay approximately EUR 15.4 million under the letter of comfort and the guarantee. Diehl also demands the Court to declare that mutares AG is obliged to reimburse Diehl for all additional losses Diehl incurs from non-fulfilment of the obligations entered into by mutares AG in connection with the acquisi- tion of the Photovoltaics division. Diehl has estimated the provisional value of the lawsuit at approximately EUR 22.5 million in total. mutares AG disputes the basis for damages and the amount of the loss. The two proceedings before the Ravensburg District Court were merged into a single proceeding. The insolvency administrator started rescission proceedings against the assets of Platinum GmbH i.I. in September 2014 on the side of Platinum GmbH i.l.

In financial year 2015, composition discussions repeatedly took place between the parties. However, these have not resulted in an amicable settlement so far. On October 16, 2015, the Ravensburg District Court issued a decision that evidence should now be taken by hearing various witnesses in oral proceedings. On June 8, 2016 and on June 15, 2016, the Ravens-burg District Court heard evidence from the first witnesses as to whether Diehl misled mutares AG and Platinum GmbH with regard to its revenue expectations for the Photovoltaics division. However, all evidence has not yet been heard and the Court has not yet revealed the conclusions it intends to draw from the testimonies that have already been given. Other testimonies are planned for October 2016.

Condensed notes

42 43

CONSOLIDATED INTERIM FINANCIAL STATEMENTS

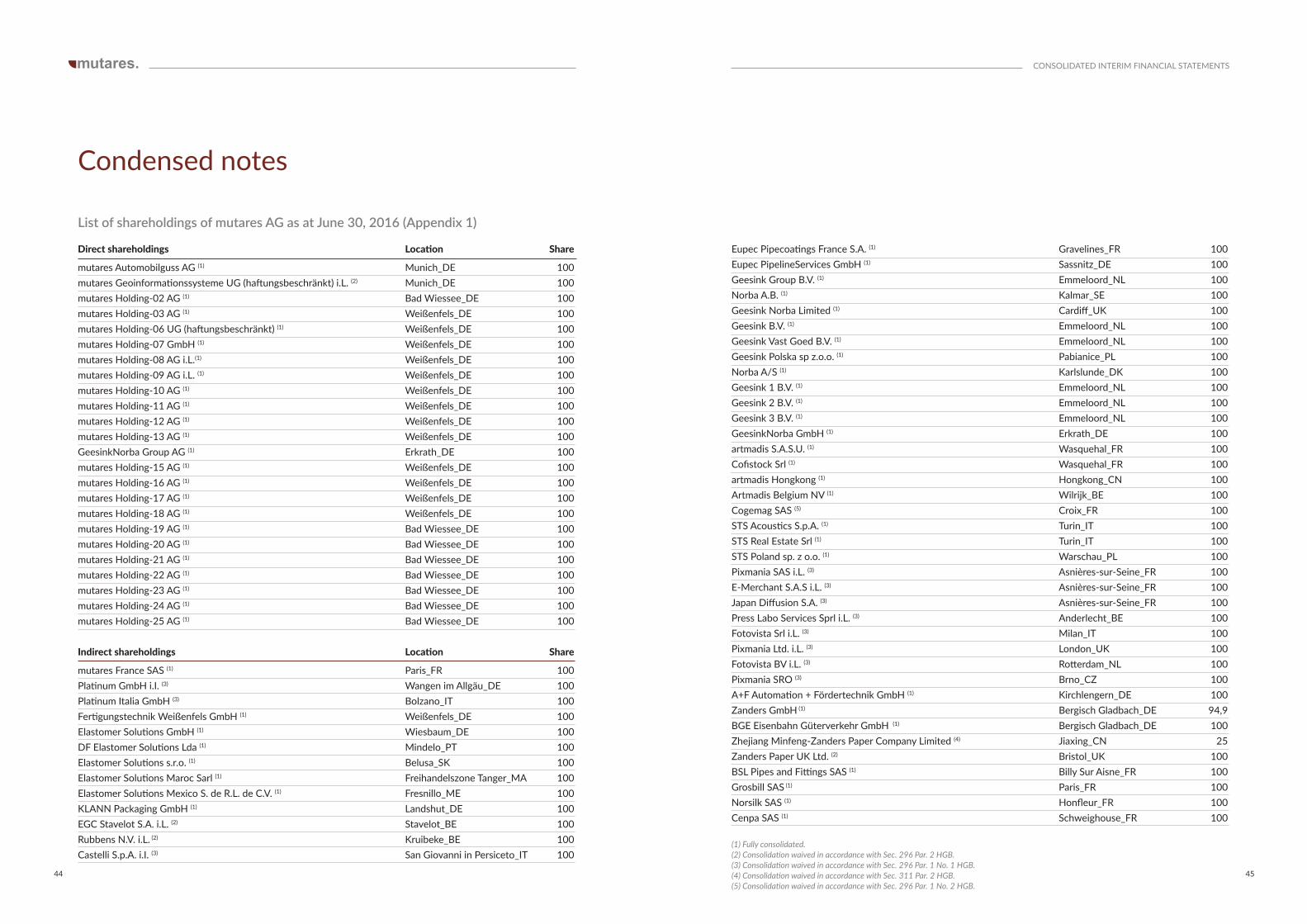

Eupec Pipecoatings France S.A. (1) Gravelines_FR 100Eupec PipelineServices GmbH (1) Sassnitz_DE 100Geesink Group B.V. (1) Emmeloord_NL 100Norba A.B. (1) Kalmar_SE 100Geesink Norba Limited (1) Cardiff_UK 100Geesink B.V. (1) Emmeloord_NL 100Geesink Vast Goed B.V. (1) Emmeloord_NL 100Geesink Polska sp z.o.o. (1) Pabianice_PL 100Norba A/S (1) Karlslunde_DK 100Geesink 1 B.V. (1) Emmeloord_NL 100Geesink 2 B.V. (1) Emmeloord_NL 100Geesink 3 B.V. (1) Emmeloord_NL 100GeesinkNorba GmbH (1) Erkrath_DE 100artmadis S.A.S.U. (1) Wasquehal_FR 100Cofistock Srl (1) Wasquehal_FR 100artmadis Hongkong (1) Hongkong_CN 100Artmadis Belgium NV (1) Wilrijk_BE 100Cogemag SAS (5) Croix_FR 100STS Acoustics S.p.A. (1) Turin_IT 100STS Real Estate Srl (1) Turin_IT 100STS Poland sp. z o.o. (1) Warschau_PL 100Pixmania SAS i.L. (3) Asnières-sur-Seine_FR 100E-Merchant S.A.S i.L. (3) Asnières-sur-Seine_FR 100Japan Diffusion S.A. (3) Asnières-sur-Seine_FR 100Press Labo Services Sprl i.L. (3) Anderlecht_BE 100Fotovista Srl i.L. (3) Milan_IT 100Pixmania Ltd. i.L. (3) London_UK 100Fotovista BV i.L. (3) Rotterdam_NL 100Pixmania SRO (3) Brno_CZ 100A+F Automation + Fördertechnik GmbH (1) Kirchlengern_DE 100Zanders GmbH (1) Bergisch Gladbach_DE 94,9BGE Eisenbahn Güterverkehr GmbH (1) Bergisch Gladbach_DE 100Zhejiang Minfeng-Zanders Paper Company Limited (4) Jiaxing_CN 25Zanders Paper UK Ltd. (2) Bristol_UK 100BSL Pipes and Fittings SAS (1) Billy Sur Aisne_FR 100Grosbill SAS (1) Paris_FR 100Norsilk SAS (1) Honfleur_FR 100Cenpa SAS (1) Schweighouse_FR 100

(1) Fully consolidated. (2) Consolidation waived in accordance with Sec. 296 Par. 2 HGB. (3) Consolidation waived in accordance with Sec. 296 Par. 1 No. 1 HGB. (4) Consolidation waived in accordance with Sec. 311 Par. 2 HGB. (5) Consolidation waived in accordance with Sec. 296 Par. 1 No. 2 HGB.

List of shareholdings of mutares AG as at June 30, 2016 (Appendix 1)

Condensed notes

44 45

Directshareholdings Location Share

mutares Automobilguss AG (1) Munich_DE 100mutares Geoinformationssysteme UG (haftungsbeschränkt) i.L. (2) Munich_DE 100mutares Holding-02 AG (1) Bad Wiessee_DE 100mutares Holding-03 AG (1) Weißenfels_DE 100mutares Holding-06 UG (haftungsbeschränkt) (1) Weißenfels_DE 100mutares Holding-07 GmbH (1) Weißenfels_DE 100mutares Holding-08 AG i.L.(1) Weißenfels_DE 100mutares Holding-09 AG i.L. (1) Weißenfels_DE 100mutares Holding-10 AG (1) Weißenfels_DE 100mutares Holding-11 AG (1) Weißenfels_DE 100mutares Holding-12 AG (1) Weißenfels_DE 100mutares Holding-13 AG (1) Weißenfels_DE 100GeesinkNorba Group AG (1) Erkrath_DE 100mutares Holding-15 AG (1) Weißenfels_DE 100mutares Holding-16 AG (1) Weißenfels_DE 100mutares Holding-17 AG (1) Weißenfels_DE 100mutares Holding-18 AG (1) Weißenfels_DE 100mutares Holding-19 AG (1) Bad Wiessee_DE 100mutares Holding-20 AG (1) Bad Wiessee_DE 100mutares Holding-21 AG (1) Bad Wiessee_DE 100mutares Holding-22 AG (1) Bad Wiessee_DE 100mutares Holding-23 AG (1) Bad Wiessee_DE 100mutares Holding-24 AG (1) Bad Wiessee_DE 100mutares Holding-25 AG (1) Bad Wiessee_DE 100

Indirectshareholdings Location Share

mutares France SAS (1) Paris_FR 100Platinum GmbH i.I. (3) Wangen im Allgäu_DE 100Platinum Italia GmbH (3) Bolzano_IT 100Fertigungstechnik Weißenfels GmbH (1) Weißenfels_DE 100Elastomer Solutions GmbH (1) Wiesbaum_DE 100DF Elastomer Solutions Lda (1) Mindelo_PT 100Elastomer Solutions s.r.o. (1) Belusa_SK 100Elastomer Solutions Maroc Sarl (1) Freihandelszone Tanger_MA 100Elastomer Solutions Mexico S. de R.L. de C.V. (1) Fresnillo_ME 100KLANN Packaging GmbH (1) Landshut_DE 100EGC Stavelot S.A. i.L. (2) Stavelot_BE 100Rubbens N.V. i.L. (2) Kruibeke_BE 100Castelli S.p.A. i.I. (3) San Giovanni in Persiceto_IT 100

CONSOLIDATED INTERIM FINANCIAL STATEMENTS

Development of non-current assets of mutares AG for the period from January 1 to June 30, 2016 (Appendix 2)

Costs