interest rates & credit derivatives - inr bonds fixed...

TRANSCRIPT

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Interest Rates & Credit Derivatives

Ashish Ghiya

Derivium Tradition (India)

25/06/14 1

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Agenda Introduction to Interest Rate & Credit Derivatives

Practical Uses of Derivatives

Derivatives Going Wrong – Practical Examples

25/06/14 2

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Interest Rate Derivatives

Interest Rate Futures

Interest Rate Swaps

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

What Are Futures ?

A futures contract is an agreement between a buyer

(seller) and an exchange or its clearinghouse in

which the buyer (seller) agrees to take (give) delivery

of a standard quantity of a specific asset / financial

instrument at a specified price at the end of a

designated date

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Characteristics of Futures

Exchange Traded

Standardized

Counterparty risk is absent

Settlement of trades is guaranteed by the clearing

corporation of the exchange

Margining system

Daily Marked-to-Market (MTM) settlement

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Role of The Clearing House Central counterparty to every contract

Matched position

Enables netting of contracts

Guarantees contract performance to clearing members

Operates centralised margining and daily MTM

settlement process

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Client

A

Client

B

Clearing

MemberClearing

Member

Clearing

House

Bought Sold

Registered

TradeRegistered

Trade Sold Bought

Role of The Clearing House

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Interest Rate Futures

Face value of underlying bonds in IRFs is INR 100 & each contract

represents 2000 underlying bonds of a total FV of INR 200,000

Quotes in clean price format

Serially monthly contracts with a maximum maturity of 3 months &

quarterly contracts maximum upto 1Y

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

IRF : ExampleDAY 1 : P.M. Sell 250 Feb Futures @ 100.84 (Close of business)

Initial Margin @ 2.5% = 1,260,500

DAY 2 : P.M. Feb Futures Closes at 100.95

DAY 3 : A.M. Pay 0.11 (100.84 -100.95) MTM Margin (- Rs. 55,000)

P.M. Feb Futures Closes at 100.80

DAY 4 : A.M. Receive 0.15 (100.95 -100.80) MTM Margin (Rs. 75,000)

P.M. Buy 250 Feb Futures at 100.64

DAY 5 : A.M. Receive 0.16 (100.80 - 100.64) MTM Margin (Rs. 80,000)

and Rs. 1,260,500 Initial margin refunded

Net Profit/Loss = Rs. 100,000

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Bond Futures In India Notional 10Y bond, with a cheapest to deliver option on maturity

Actual bond with the underlying maturity of close to 10Y, with cash

settlement on maturity

5Y, 7Y & 15Y cash settled bond futures are approved but yet to be

introduced

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Practical Applications Hedge against interest rate risk

Arbitrage between cash and futures markets

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

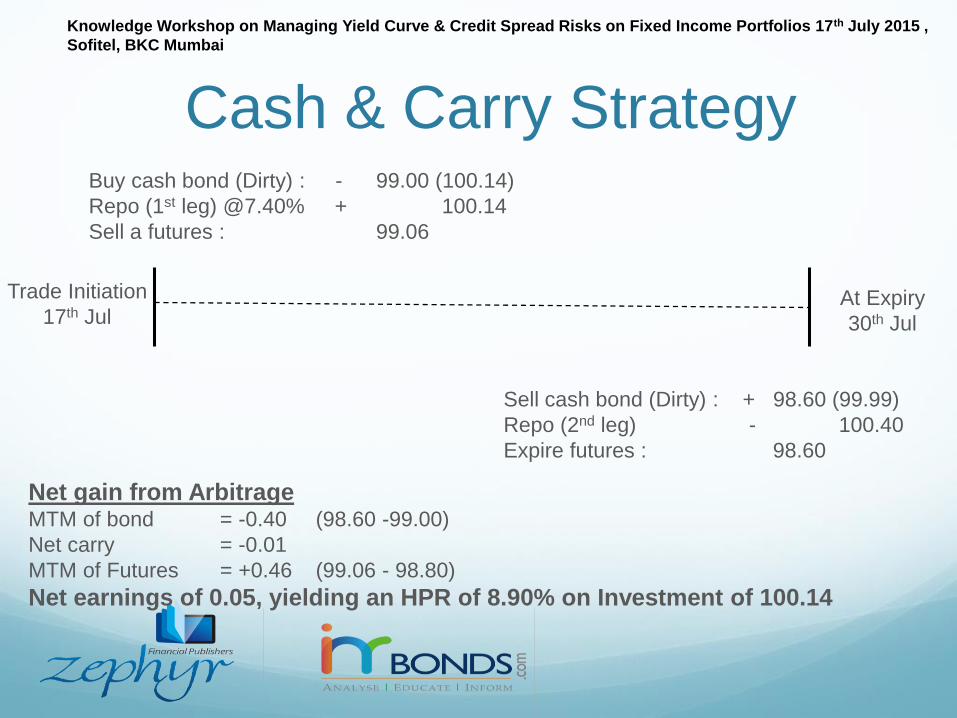

Cash & Carry Strategy

Buy the bond and fund the long bond position

through short term borrowing (repo)

Sell the futures

At expiry, cover the short futures and reverse the

repo transaction & selling the bond in cash markets

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Cash & Carry Strategy

Trade Initiation

17th JulAt Expiry

30th Jul

Buy cash bond (Dirty) : - 99.00 (100.14)

Repo (1st leg) @7.40% + 100.14

Sell a futures : 99.06

Net gain from ArbitrageMTM of bond = -0.40 (98.60 -99.00)

Net carry = -0.01

MTM of Futures = +0.46 (99.06 - 98.80)

Net earnings of 0.05, yielding an HPR of 8.90% on Investment of 100.14

Sell cash bond (Dirty) : + 98.60 (99.99)

Repo (2nd leg) - 100.40

Expire futures : 98.60

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Interest Rate Swaps

A custom-tailored bilateral agreement

Two counterparties agree to exchange

specified cash flows

at periodic intervals

over a pre-determined life of the swap

on a notional principal

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

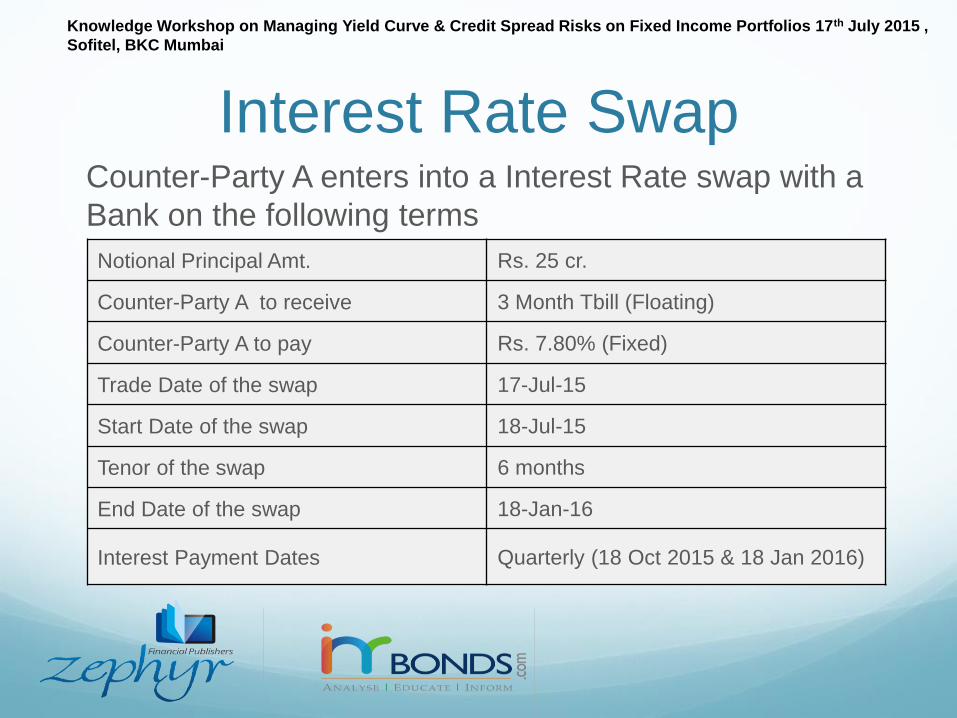

Interest Rate SwapCounter-Party A enters into a Interest Rate swap with a

Bank on the following terms

Notional Principal Amt. Rs. 25 cr.

Counter-Party A to receive 3 Month Tbill (Floating)

Counter-Party A to pay Rs. 7.80% (Fixed)

Trade Date of the swap 17-Jul-15

Start Date of the swap 18-Jul-15

Tenor of the swap 6 months

End Date of the swap 18-Jan-16

Interest Payment Dates Quarterly (18 Oct 2015 & 18 Jan 2016)

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Interest Rate Swap

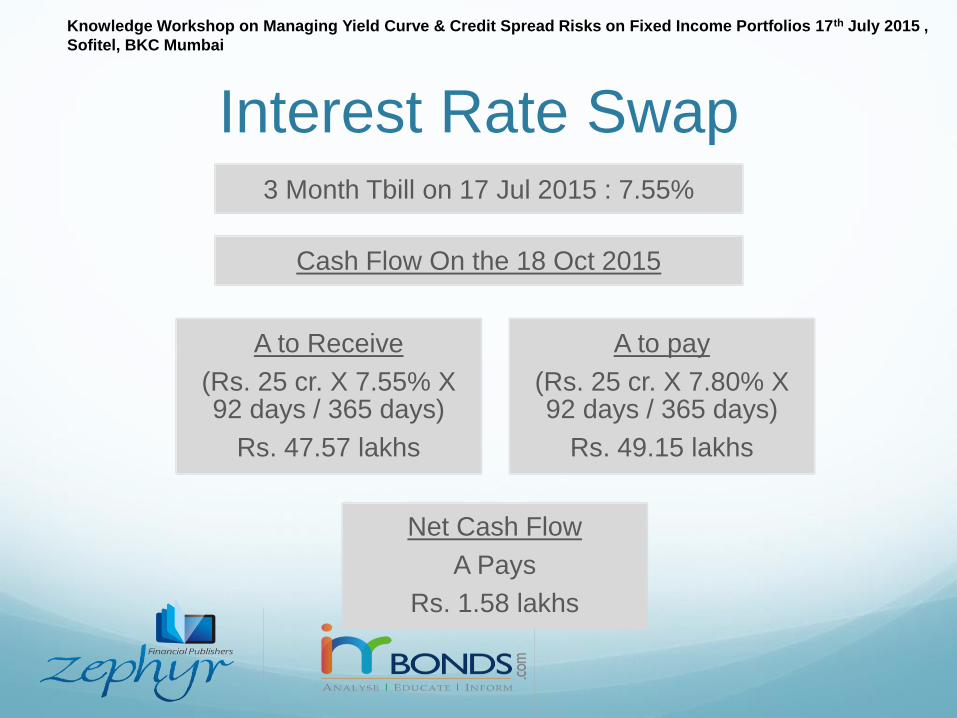

A to Receive

(Rs. 25 cr. X 7.55% X 92 days / 365 days)

Rs. 47.57 lakhs

A to pay

(Rs. 25 cr. X 7.80% X 92 days / 365 days)

Rs. 49.15 lakhs

Net Cash Flow

A Pays

Rs. 1.58 lakhs

3 Month Tbill on 17 Jul 2015 : 7.55%

Cash Flow On the 18 Oct 2015

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Interest Rate Swap

A to Receive

(Rs. 25 cr. X 8.25% X 92 days / 365 days)

Rs. 51.99 lakhs

A to pay

(Rs. 25 cr. X 7.80% X 92 days / 365 days)

Rs. 49.15 lakhs

Net Cash Flow

A Receives

Rs. 2.84 lakhs

3 Month Tbill on 17 Oct 2015 : 8.25%

Cash Flow On the 18 Jan 2016

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Interest Rate Swaps in India Overnight Indexed Swaps (OIS)

Floating benchmark linked to daily overnight MIBOR

INBMK Swaps

Floating benchmark linked to 1Y Gsec yield

MIFOR Swaps

Floating benchmark linked to FX forwards rates

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

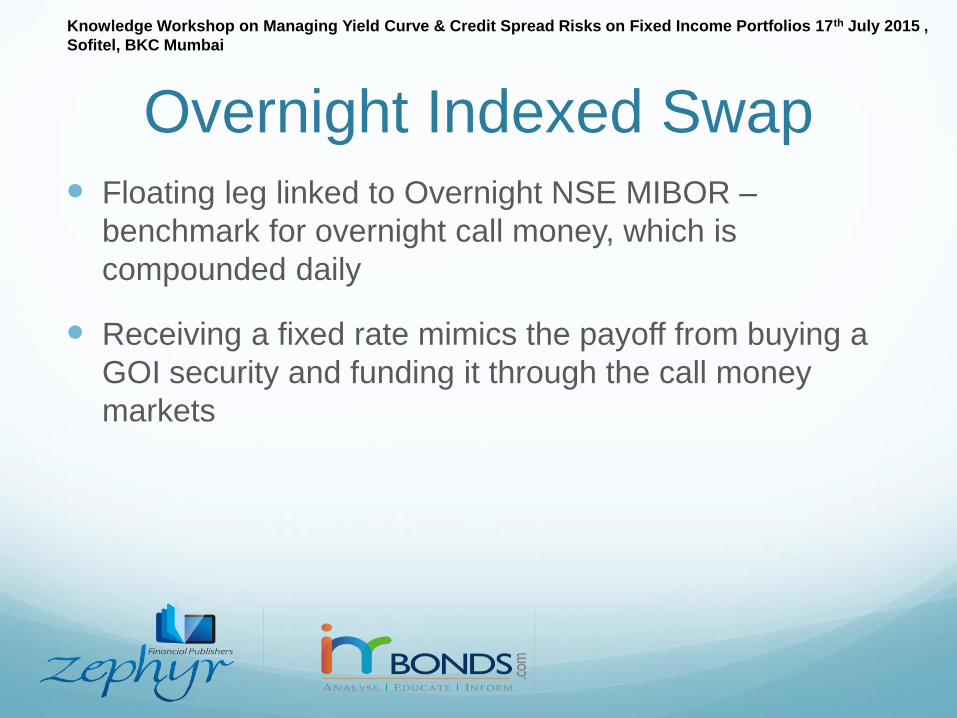

Overnight Indexed Swap Floating leg linked to Overnight NSE MIBOR –

benchmark for overnight call money, which is

compounded daily

Receiving a fixed rate mimics the payoff from buying a

GOI security and funding it through the call money

markets

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Overnight Indexed Swap

Notional Principal Amt. Rs. 25 cr.

Counter-Party A to Pay O/N NSE MIBOR (Floating)

Counter-Party A to Receive Rs. 7.32% (Fixed)

Trade Date of the swap 17 Jul 2015

Start Date of the swap 18 Jul 2015

Tenor of the swap 7 days

End Date of the swap 23 Jul 2015

Interest Payment Dates On Maturity

Compounding Applicable

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Overnight Indexed SwapDay 1 Day 2 Day 3 Day 4 Day 5 Day 6 Day 7

NSE

MIBOR

7.20% 7.25% 7.35% 7.40% 7.50% 7.75% 7.60%

((1+7.20%/365)*(1+7.25%*/365)*(1+7.35%/365)*(1+7.40%/365)*(1+7.50%/365)

*(1+7.75%/365) *(1+7.60%/365)) -1 X 365 / 7

Effective

MIBOR

7.44%

Fixed Rate 7.32%

Difference 12 bps

25 crs * 0.12% * 7 days / 365

Net

Settlement

5753

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

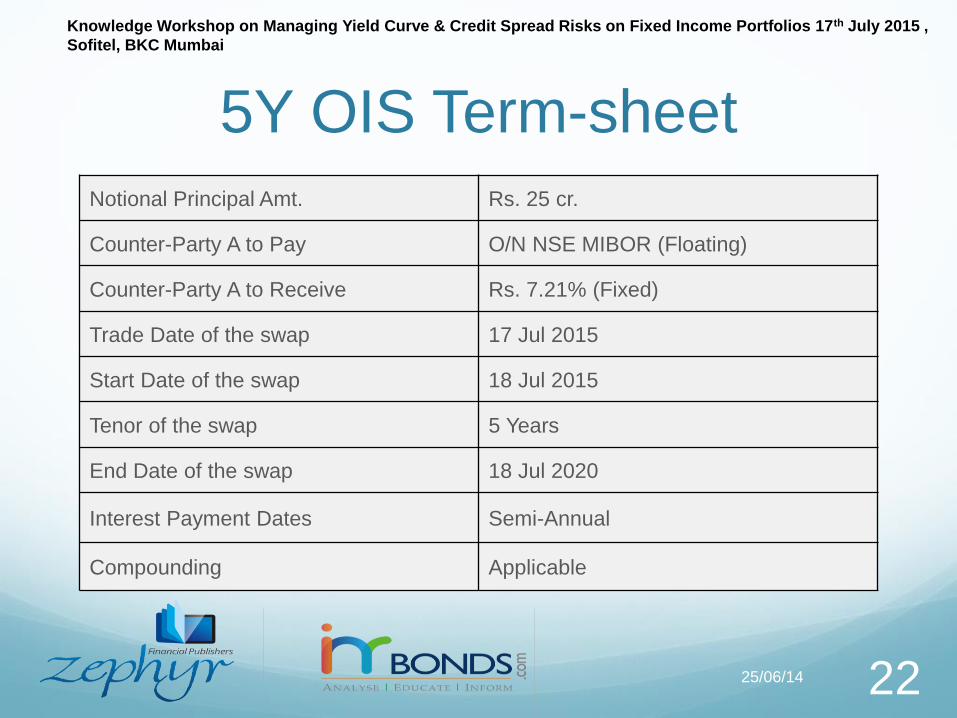

5Y OIS Term-sheet

25/06/14 22

Notional Principal Amt. Rs. 25 cr.

Counter-Party A to Pay O/N NSE MIBOR (Floating)

Counter-Party A to Receive Rs. 7.21% (Fixed)

Trade Date of the swap 17 Jul 2015

Start Date of the swap 18 Jul 2015

Tenor of the swap 5 Years

End Date of the swap 18 Jul 2020

Interest Payment Dates Semi-Annual

Compounding Applicable

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Applications of Interest Rate

Derivatives

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Hedging

Fair Value Hedge

- To reduce or eliminate the exposure to a change in fair value that is associated with an existing asset or a liability

Cash Flow Hedge

- To reduce the variability in the expected future cash flows due to changes in variable rates or prices

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

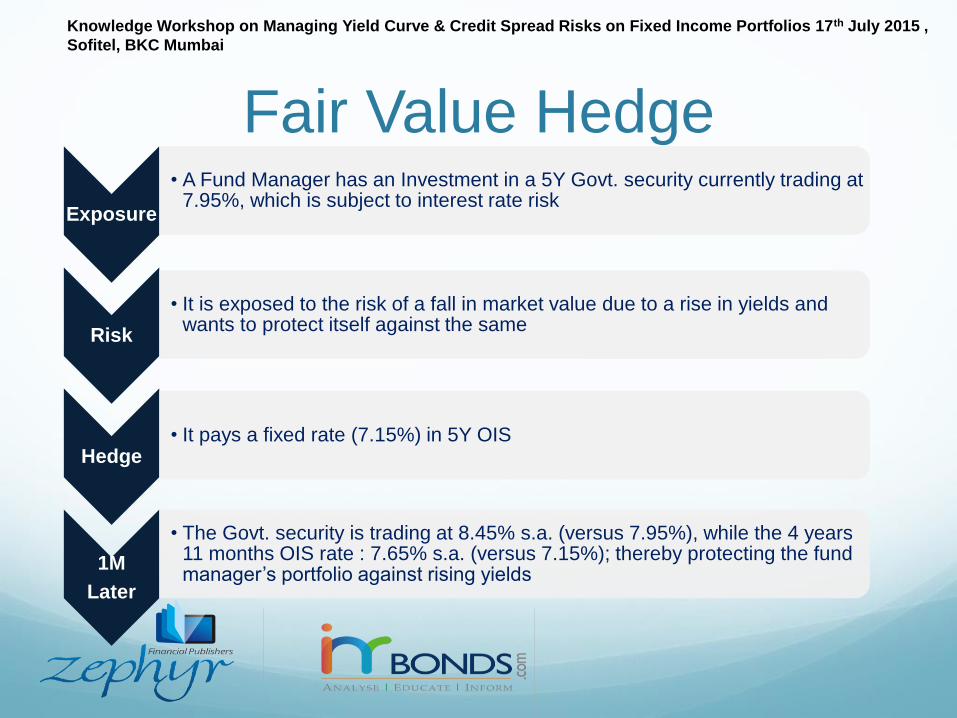

Fair Value Hedge

Exposure

• A Fund Manager has an Investment in a 5Y Govt. security currently trading at 7.95%, which is subject to interest rate risk

Risk

• It is exposed to the risk of a fall in market value due to a rise in yields and wants to protect itself against the same

Hedge• It pays a fixed rate (7.15%) in 5Y OIS

1M

Later

• The Govt. security is trading at 8.45% s.a. (versus 7.95%), while the 4 years 11 months OIS rate : 7.65% s.a. (versus 7.15%); thereby protecting the fund manager’s portfolio against rising yields

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Fair Value Hedge

The underlying could be a fixed rate asset viz. GOI

security, corporate bond, loan etc.

The risk being hedged would be the interest rate risk,

excluding the credit risk embedded in a corporate

bond or a loan.

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Hedging Portfolio PVBP Fixed income portfolios carries an interest rate risk

against any upward movement in interest rates

This can be hedged actively through the Interest Rate

derivatives

The consolidated portfolio can be measured in terms of

Price Value Basis Points (PVBP) to maintain only

desirable amount of risk

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Hedging in a Rising Interest

Rate Scenario

In a rising interest rate scenario, the fixed income portfolio runs the risk of portfolio devaluation as yields rise & bond prices fall

In order to immunize the portfolio in such a scenario, it can enter into pay fixed-receive floating interest rate swaps or sell futures

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

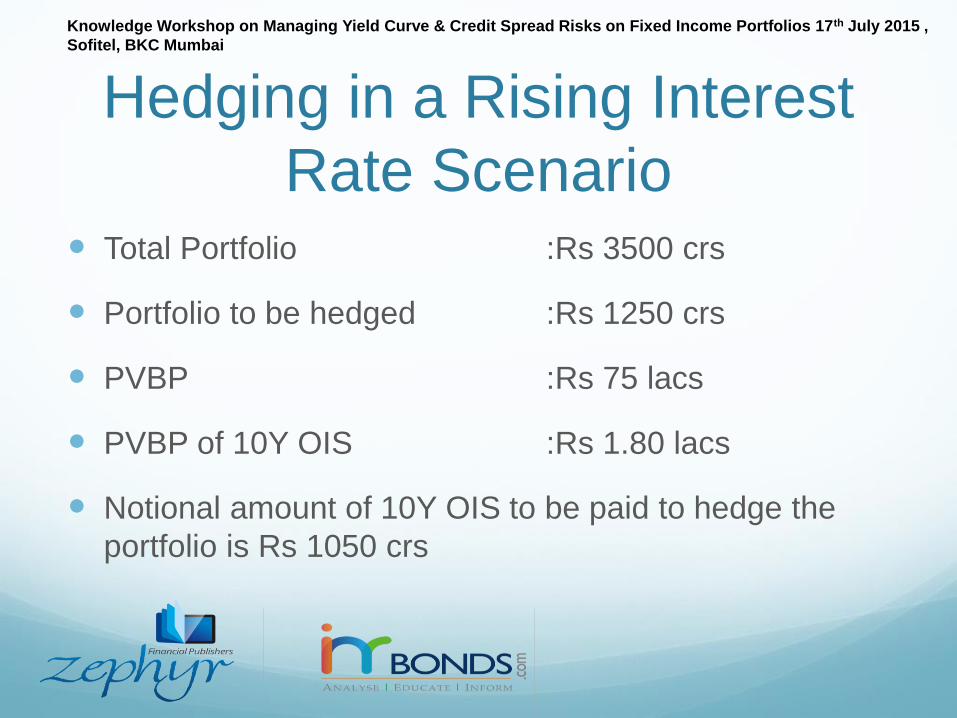

Hedging in a Rising Interest

Rate Scenario Total Portfolio :Rs 3500 crs

Portfolio to be hedged :Rs 1250 crs

PVBP :Rs 75 lacs

PVBP of 10Y OIS :Rs 1.80 lacs

Notional amount of 10Y OIS to be paid to hedge the

portfolio is Rs 1050 crs

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Cash Flow Hedge A cash flow hedge is a hedge of the exposure to

variability in cashflows that is attributable to a particular

risk associated with a recognized asset or liability or a

highly probable forecasted transaction or an

unrecognized firm commitment, and could affect P&L

Cash flow hedges are structured to reduce the variability

in the expected future cash flows due to changes in

market rates or prices

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

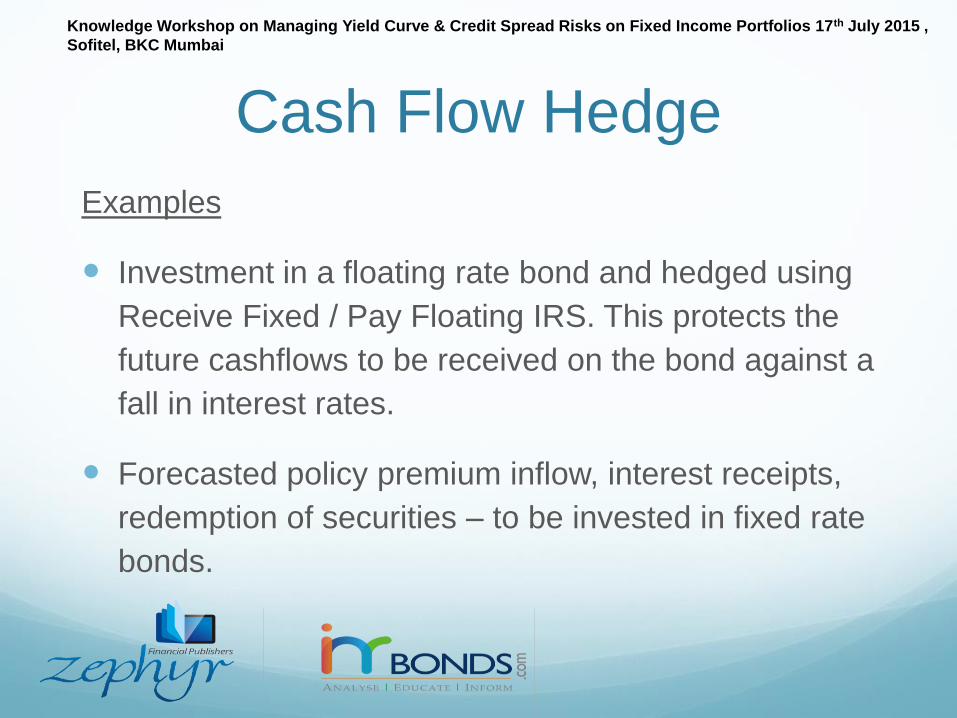

Cash Flow Hedge

Examples

Investment in a floating rate bond and hedged using

Receive Fixed / Pay Floating IRS. This protects the

future cashflows to be received on the bond against a

fall in interest rates.

Forecasted policy premium inflow, interest receipts,

redemption of securities – to be invested in fixed rate

bonds.

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Cash Flow Hedge

Exposure

• A Fund Manager has an Investment in a 3Y floating rate bond linked to MIBOR, which is subject to interest rate risk

Risk

• Future cashflows on the bond are variable / uncertain. It is exposed to the risk of a fall in interest rates, which could result in lower interest income from the bond

Hedge

• It receives a fixed rate in 3Y OIS to convert its floating rate asset into a synthetic fixed rate asset

On Maturity

• This enables the fund manager to lock-into a fixed rate, and immunize its interest income due to a fall in interest rates

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

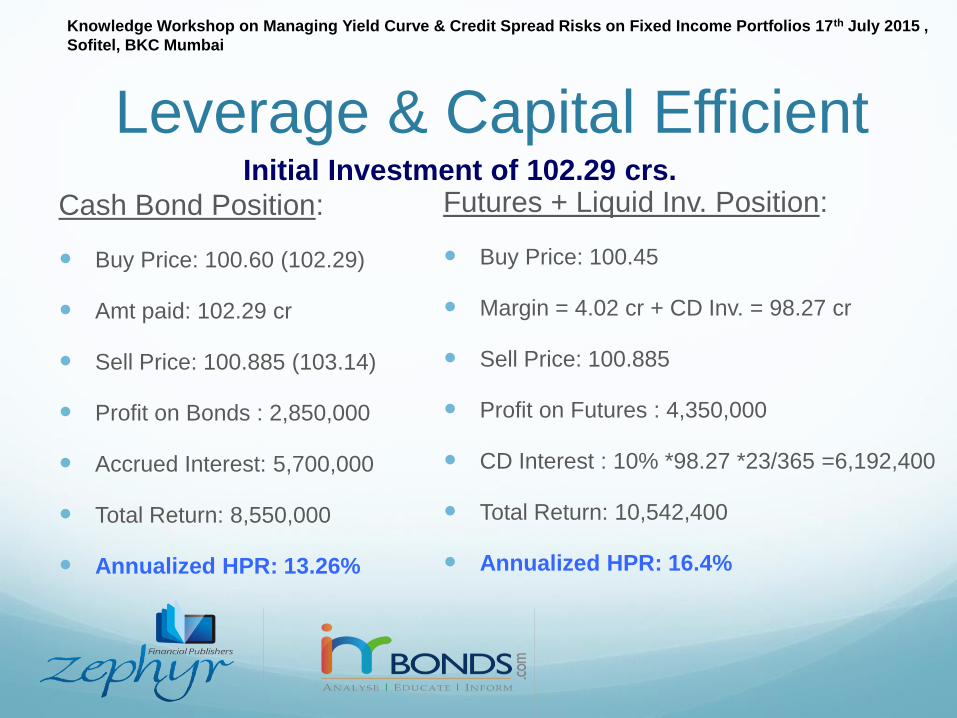

Leverage & Capital Efficient

Given a positive view on softening interest rates,

strategy can either be to buy GSecs directly in cash for

100 crs OR

Buy futures contract (pay margin money) and invest the

rest in high yielding security (CD @10%) or liquid fund

Holding period of 23 days

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Leverage & Capital Efficient

Cash Bond Position:

Buy Price: 100.60 (102.29)

Amt paid: 102.29 cr

Sell Price: 100.885 (103.14)

Profit on Bonds : 2,850,000

Accrued Interest: 5,700,000

Total Return: 8,550,000

Annualized HPR: 13.26%

Futures + Liquid Inv. Position:

Buy Price: 100.45

Margin = 4.02 cr + CD Inv. = 98.27 cr

Sell Price: 100.885

Profit on Futures : 4,350,000

CD Interest : 10% *98.27 *23/365 =6,192,400

Total Return: 10,542,400

Annualized HPR: 16.4%

Initial Investment of 102.29 crs.

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Credit Default Swaps

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Credit Default Swaps Credit Default Swap (CDS) is a bilateral OTC

agreement, which transfers a defined credit risk from

buyer to the seller of the contract, for a fee

The buyer of credit protection pays a periodic fee to the

seller in return for protection against a Credit Event of

an underlying Reference Entity

In essence it is similar to a traditional insurance policy,

in as much as it obliges the seller of the CDS to

compensate the buyer in the event of a default

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Via a Credit Default Swap, the Protection Buyer transfers risk

that the Reference Entity will default

Protection Seller receives a fee, similar to an insurance

premium, and assumes the risk that the Reference Entity will

default

Upon a default or Credit Event, protection seller makes a

contingent payment to the protection Buyer

Credit Default SwapsX bps per annum

Contingent Payment

(Par — Recovery)

Protection Buyer

Protection Seller

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

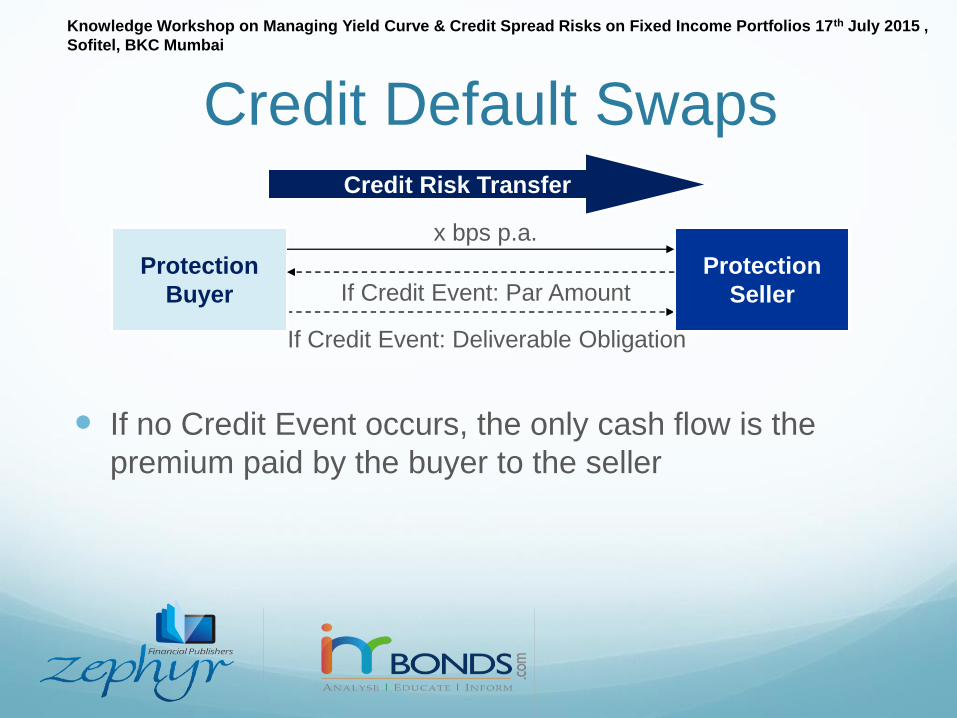

Credit Default Swaps

If no Credit Event occurs, the only cash flow is the

premium paid by the buyer to the seller

If Credit Event: Deliverable Obligation

Credit Risk Transfer

Protection

Seller

Protection

Buyer

x bps p.a.

If Credit Event: Par Amount

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

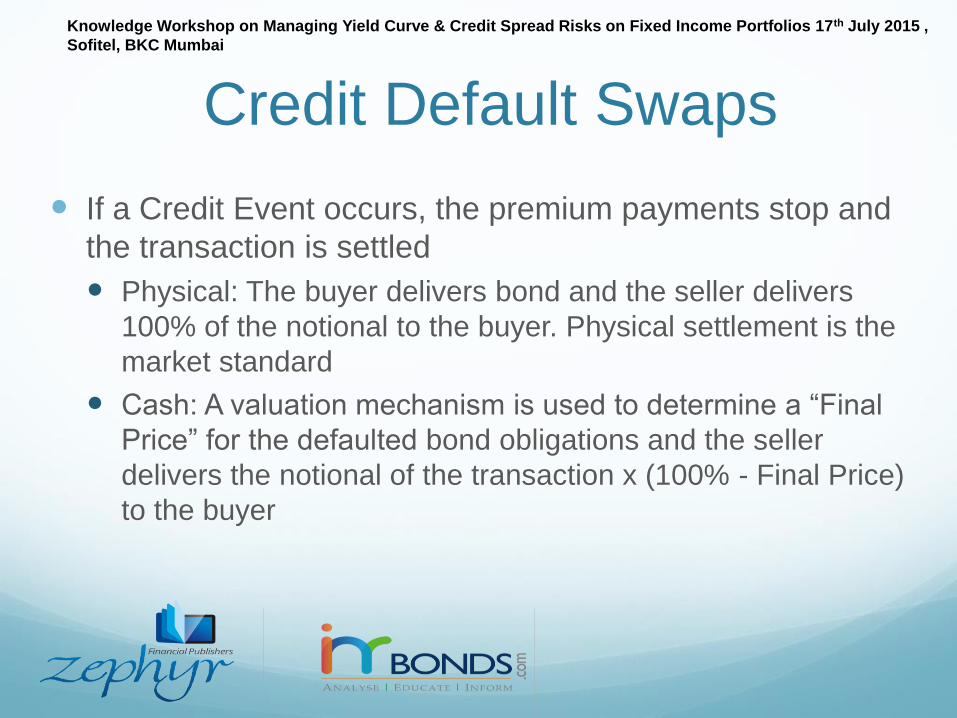

Credit Default Swaps

If a Credit Event occurs, the premium payments stop and

the transaction is settled

Physical: The buyer delivers bond and the seller delivers

100% of the notional to the buyer. Physical settlement is the

market standard

Cash: A valuation mechanism is used to determine a “Final

Price” for the defaulted bond obligations and the seller

delivers the notional of the transaction x (100% - Final Price)

to the buyer

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Transferring of Risk

Buyer decreases exposure to Reference Credit(s),

but assumes contingent exposure to Seller

Seller receives a fee in return for making a

Contingent Payment if there is a Credit Event of the

Reference Credit

Reference

Entity

Counterparty Bank

Contingent

Payment

X bps per

annum

Risk

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

– Buy CDS

– Buy Protection

– Pay periodic

payments

– Receive

contingent

payment

– Hedges Credit

Risk

Credit Default Swap

Fee/premium

Contingent Payment

upon a credit event

BProtection Buyer

AProtection Seller

Reference Entity

Risk (Notional)

– Sell CDS

– Sell Protection

– Receive periodic

payments

– Pay contingent

payment

– Assumes Credit

Risk

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

CDS v/s Bond

Risk Free Rate

Funding Risk

Credit Risk

Credit Risk

Bond Credit Default Swap

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Derivatives –

Risk Management or

Risk Enhancement

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

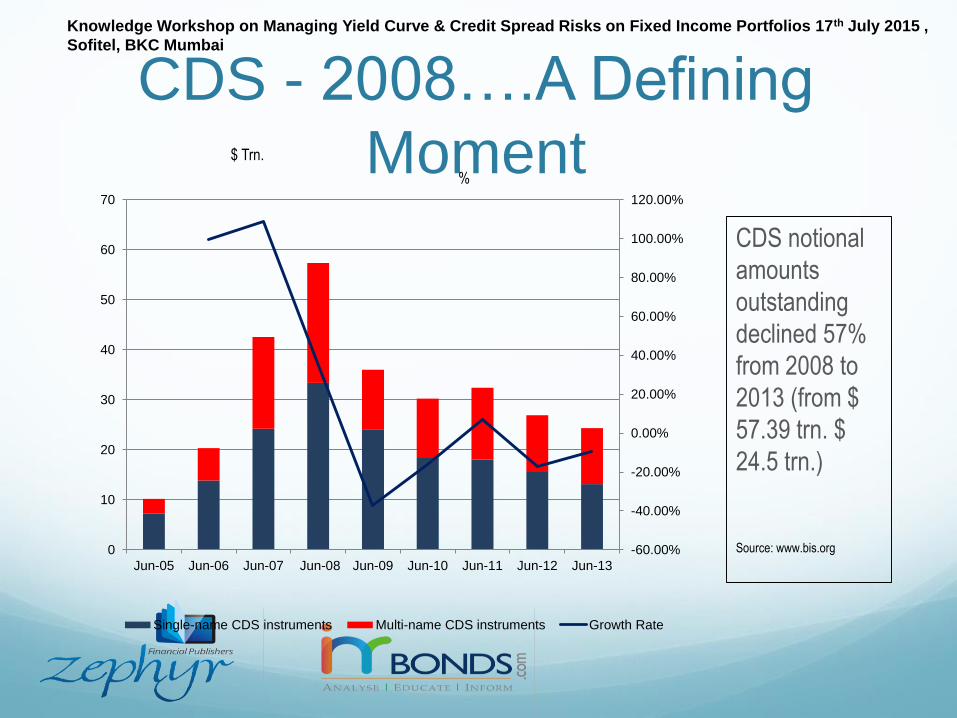

CDS - 2008….A Defining

Moment

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

CDS - 2008….A Defining

Moment

-60.00%

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

0

10

20

30

40

50

60

70

Jun-05 Jun-06 Jun-07 Jun-08 Jun-09 Jun-10 Jun-11 Jun-12 Jun-13

Single-name CDS instruments Multi-name CDS instruments Growth Rate

CDS notional

amounts

outstanding

declined 57%

from 2008 to

2013 (from $

57.39 trn. $

24.5 trn.)

%

Source: www.bis.org

$ Trn.

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

2008 – Post Lehman Crises In September 2008, CDS assumed center-stage as one

of the causes of Lehman Brothers' bankruptcy, which

accentuated the global financial crisis

In the case of Lehman collapse, market participants

and supervisors were confronted with the failure of a

CDS counterparty that was also an important reference

entity

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

2008 – Post Lehman Crises This was followed by collapse of AIG – largely due to

exposures to un-hedged CDS contracts written on sub-

prime mortgage securities & acceleration of cash

collaterals

The issue that shook the markets was that the CDS

contracts failed largely due to the financial counterparty

failing, which turned into a financial crises, thereby

accelerating the probability of the underlying reference

entities’ credit risk

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Derivatives Going Bad –

Indian Example

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

INR-JPY Structures Back in 2007, banks issued Tier II bonds and

undertook Rupee cost reduction structures - where the

cost of the Rupee liability was hedged through coupons

being swapped into Yen

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

INR-JPY Structures Why did such structures become attractive? The

genesis, maybe started as Rupee interest rates were high, which increased the liability cost of the long term borrower

Yen was the lowest interest rate currency, which made the initial carry attractive

Hence, coupon only swaps were performed, where the liability counterparty received a fixed Rupee rate (which would typically equate the interest cost on its fixed Rupee borrowing), and paid a floating JPY interest rate

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

INR-JPY Structures This transaction runs the risk of JPY interest rate rising,

and hence to protect the same low JPY interest rate caps were bought, which would protect the liability counterparty of rising JPY interest rates

The liability counterparty hence converted its fixed Rupee liability into floating JPY liability with a protection on interest rates too

Even so, it yet runs the risk of JPY appreciating against Rupee on the coupon exchange dates

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Coupon Swap Structure

Tenor 10 years

Spot Reference Rate

USD/INR 46.15

USD/JPY 112.00

JPY/INR 0.4121

INR Notional 100,00,00,000

JPY Notional 253,06,80,302

Fixed Rate Payer Bank Counterparty

Fixed Rate Currency INR

Fixed Rate 9.00%

Day Count basis Act/365

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Coupon Swap Structure

Floating Rate Payer Corporate

Floating Rate Currency JPY

Floating Rate

IF 6M JPY LIBOR <= 1.00%, then

6M JPY LIBOR + Spread

Indicative Spread 5.70% – 5.95%

Day Count basis Act/360

Interest Settlement Dates semi-annual

Principal Exchange None

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Risks In The INR JPY Structure

JPY LIBOR RISK

The liability counterparty runs the risk of Yen interest rates

rising faster than expected, which would imply a greater

outflow by the corporate under its floating rate JPY

payments. However, this risk is limited by the purchase of

an interest rate cap at 1.00%.

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Risks In The INR JPY Structure

INR / JPY CURRENCY RISK

The liability counterparty runs a JPY/INR currency risk on the

coupon exchanges under the swap. The corporate receives

the Fixed Rate in Rupee, while it pays the floating JPY LIBOR

+ spread in JPY.

Hence, it runs the risk of a sharp appreciation of the Yen

versus the Rupee on a continuous basis for the tenor of the

swap

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Risks In The INR JPY Structure

USD/JPY dropped below 80 and USD/INR breached 50,

leading to the structure losing significantly

Knowledge Workshop on Managing Yield Curve & Credit Spread Risks on Fixed Income Portfolios 17th July 2015 ,

Sofitel, BKC Mumbai

Thank You

25/06/14 57

Information herein is believed to be reliable but Arjun Parthasarathy Editor: INRBONDS.com and Zephyr Financial Publishers Private Limited does not warrant its completeness or accuracy. Opinions and estimates are subject to change without notice. This information is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The financial markets are inherently risky and it is assumed that those who trade these markets are fully aware of the risk of real loss involved. Unauthorized copying, distribution or sale of this publication is strictly prohibited. The author(s) of the content published in the site INRBONDS.com may or may not have investments in the assets discussed in the pages/posts.

Copyright © INRBONDS.com by Arjun Parthasarathy 2013