interest rate risk i chapter 8 © 2008 the mcgraw-hill companies, inc., all rights reserved....

TRANSCRIPT

Interest Rate Risk IInterest Rate Risk I

Chapter 8

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.McGraw-Hill/Irwin

Part ACovers pages 190-200

8-2

Overview

This chapter discusses the interest rate risk associated with financial intermediation: Federal Reserve monetary policy Interest rate risk models *Term structure of interest rate risk *Theories of the term structure of interest

rates

8-3

Interest Rate Risk Models

Repricing model Maturity model Duration model In-house models

Proprietary Commercial

8-4

Loanable Funds Theory

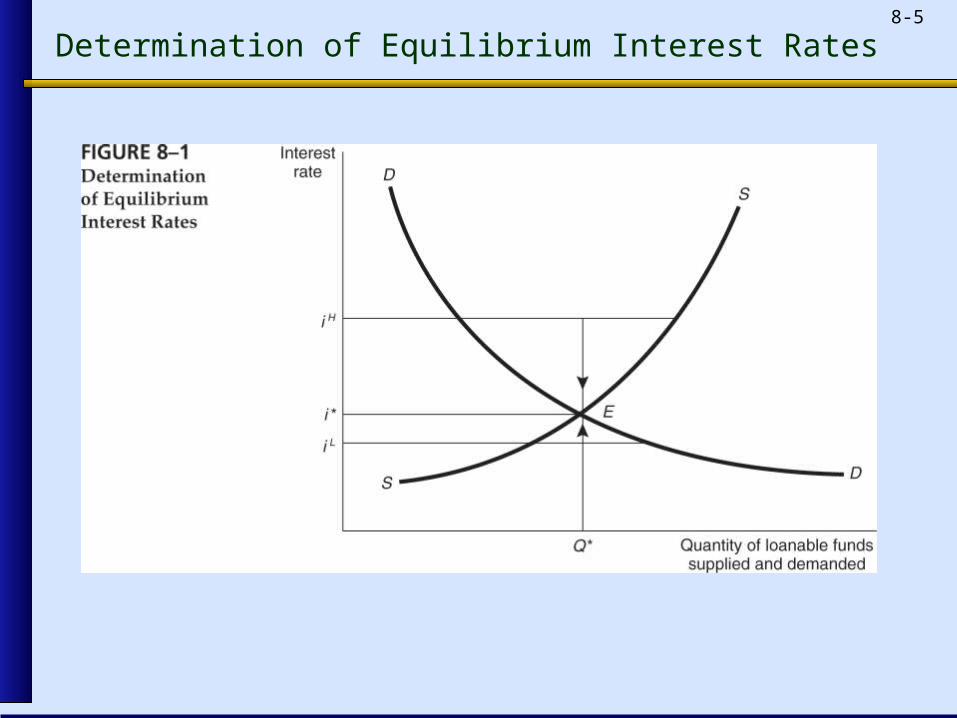

Interest rates reflect supply and demand for loanable funds

Shifts in supply or demand generate interest rate movements as market forces establish a new equilibrium

8-5

Determination of Equilibrium Interest Rates

8-6

Note that y-axis is

bond PRICE

8-7

Increase in Demand for Bonds

8-8

Factors that

impact bond

demand

8-9

Bond Supply Shift – Increase in Supply

8-10

Factors that

impact bond

supply

8-11

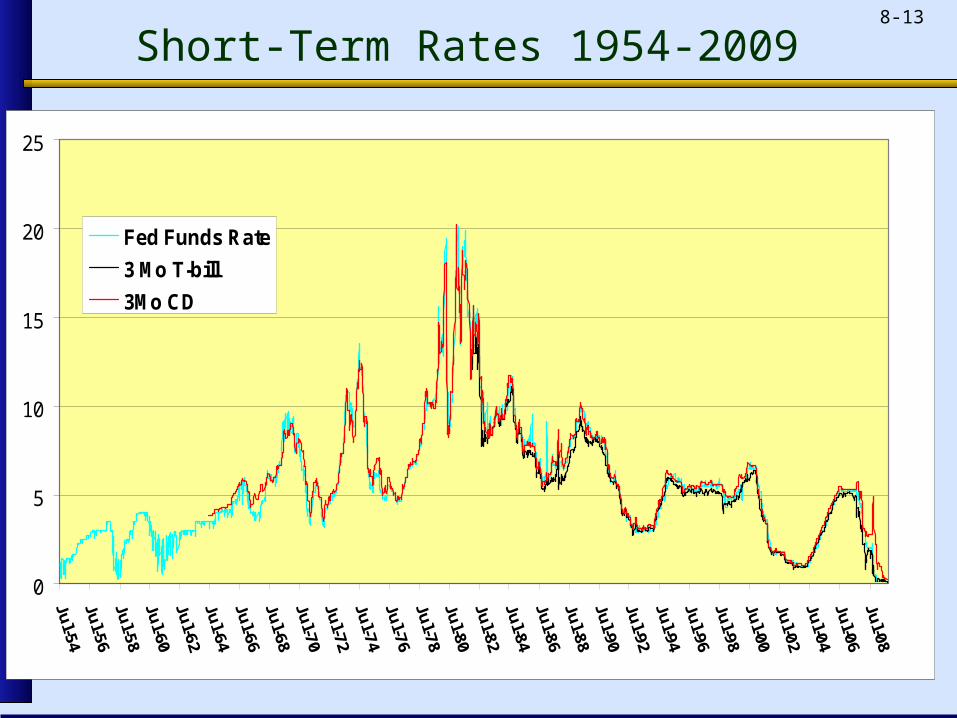

Level & Movement of Interest Rates

Federal Reserve Bank: U.S. central bank Open market operations influence money

supply, inflation, and interest rates Actions of Fed in response to 2001 attacks on

World Trade Center Lowered interest rates 11 times during the year

June 2004- August 2006 inflation concerns take prominence 17 consecutive increases in interest rates

2008/2009 Short rates lowered to virtually zero

8-12

Central Bank and Interest Rates

Target is primarily short term rates Focus on Fed Funds Rate in particular

Interest rate changes and volatility increasingly transmitted from country to country Statements by Ben Bernanke can have

dramatic effects on world interest rates.

8-13

Short-Term Rates 1954-2009

0

5

10

15

20

25

Fed Funds Rate

3 Mo T-bill

3Mo CD

8-14

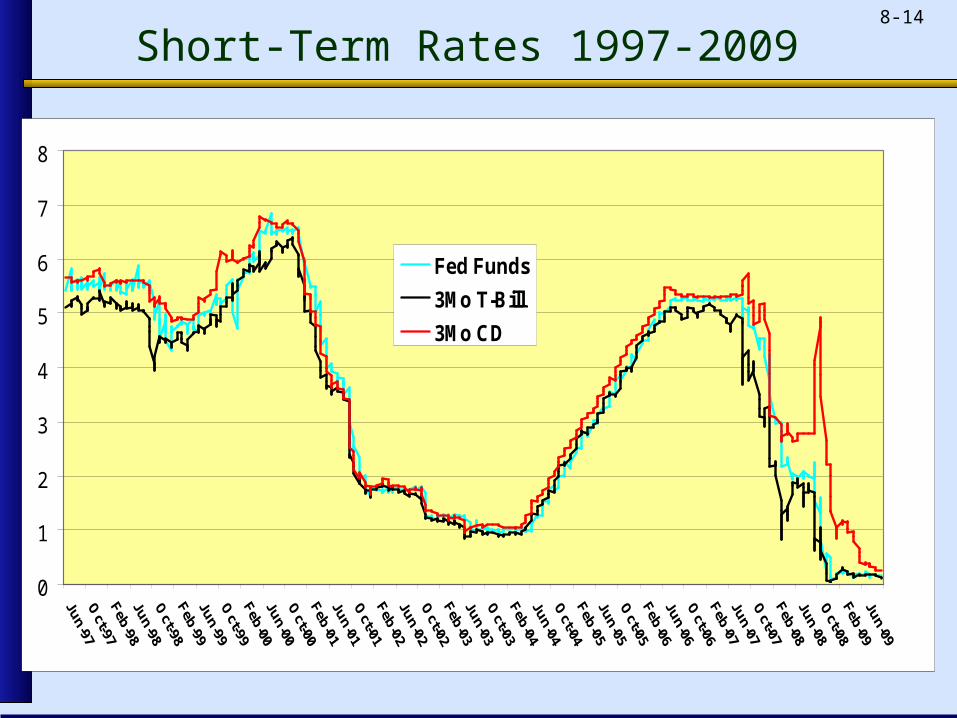

Short-Term Rates 1997-2009

0

1

2

3

4

5

6

7

8

Fed Funds

3Mo T-Bill

3Mo CD

8-15

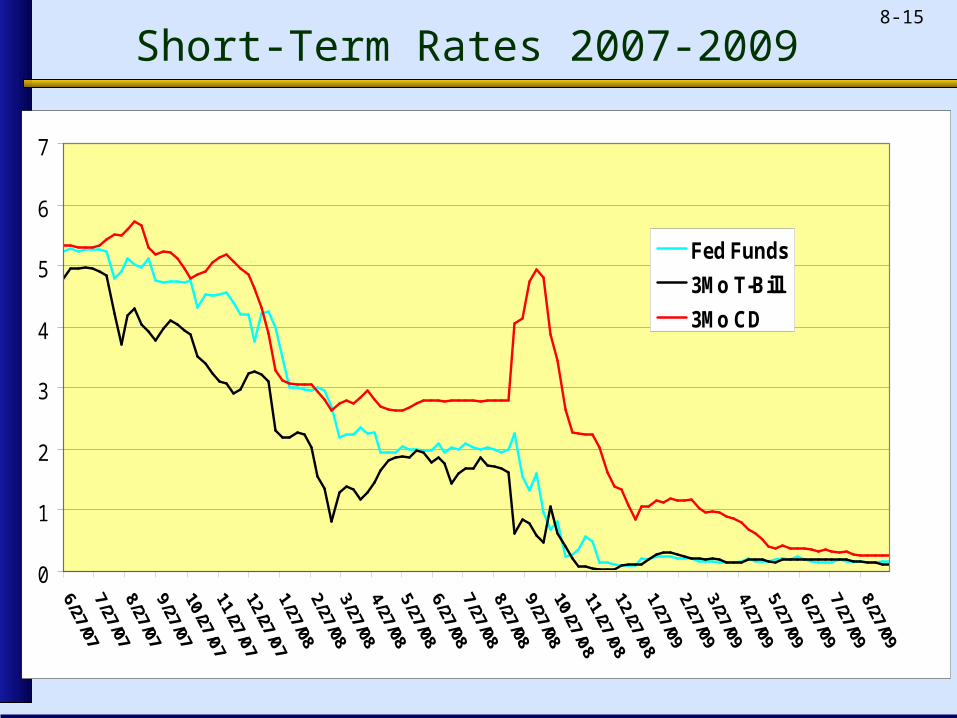

Short-Term Rates 2007-2009

0

1

2

3

4

5

6

7

Fed Funds

3Mo T-Bill

3Mo CD

8-16

Rate Changes Can Vary by Market

Note that there have been significant differences in recent years

If your asset versus liability rates change by different amounts, that is called “basis risk” May not be accounted for in your interest rate

risk model

8-17

Repricing Model

Repricing or funding gap model based on book value.

Contrasts with market value-based maturity and duration models recommended by the Bank for International Settlements (BIS).

Rate sensitivity means time to repricing. Repricing gap is the difference between the rate

sensitivity of each asset and the rate sensitivity of each liability: RSA - RSL.

Refinancing risk However, theoretically could be reinvestment risk

(positive gap)

8-18

Repricing Model

We are interested in the Repricing Model as an introduction to the importance of Net Interest Income Variability of NII is really what we are trying to

protect NII is the lifeblood of banks/thrifts

8-19

Maturity Buckets

Commercial banks must report repricing gaps for assets and liabilities with maturities of: One day. More than one day to three months. More than 3 three months to six months. More than six months to twelve months. More than one year to five years. Over five years.

Note the cut-off levels

8-20

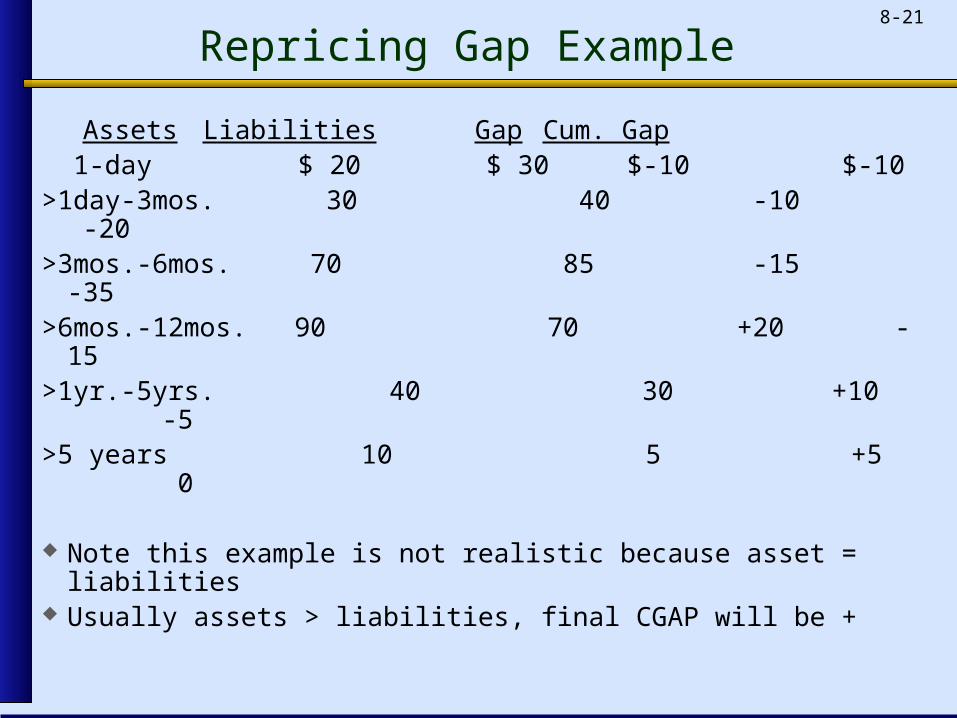

Repricing Gap Example

Assets Liabilities Gap Cum. Gap

1-day $ 20 $ 30 $-10 $-10

>1day-3mos. 30 40 -10 -20

>3mos.-6mos. 70 85 -15 -35

>6mos.-12mos. 90 70 +20 -15

>1yr.-5yrs. 40 30 +10 -5

>5 years 10 5 +5 0

8-21

Repricing Gap Example

Assets Liabilities Gap Cum. Gap

1-day $ 20 $ 30 $-10 $-10>1day-3mos. 30 40 -10 -20>3mos.-6mos. 70 85 -15 -35>6mos.-12mos. 90 70 +20 -15>1yr.-5yrs. 40 30 +10 -5>5 years 10 5 +5 0

Note this example is not realistic because asset = liabilities

Usually assets > liabilities, final CGAP will be +

8-22

Applying the Repricing Model

NIIi = (GAPi) Ri = (RSAi - RSLi) Ri

Example: In the one day bucket, gap is -$10 million. If rates

rise by 1%,

NII(1) = (-$10 million) × .01 = -$100,000.

8-23

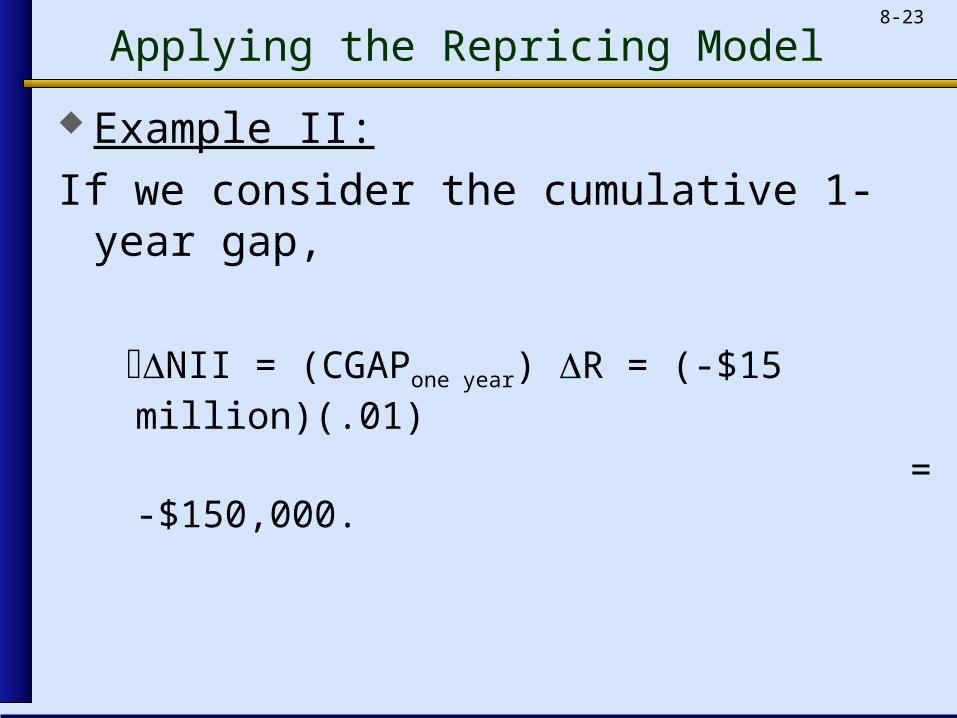

Applying the Repricing Model

Example II:

If we consider the cumulative 1-year gap,

NII = (CGAPone year) R = (-$15 million)(.01)

= -$150,000.

8-24

Rate-Sensitive Assets

Examples from hypothetical balance sheet: Short-term consumer loans. If repriced at year-

end, would just make one-year cutoff. Three-month T-bills repriced on maturity every

3 months. Six-month T-notes repriced on maturity every 6

months. 30-year floating-rate mortgages repriced (rate

reset) every 9 months.

8-25

Rate-Sensitive Liabilities

RSLs bucketed in same manner as RSAs. Demand deposits and passbook savings

accounts warrant special mention. Generally considered rate-insensitive (act as

core deposits), but there are arguments for their inclusion as rate-sensitive liabilities.

FOR NOW, we will treat these as though they reprice overnight

Text assumes that they do not reprice at all

8-26

CGAP Ratio

May be useful to express CGAP in ratio form as,

CGAP/Assets. Provides direction of exposure and Scale of the exposure.

Example- 12 month CGAP: CGAP/A = $15 million / $270 million = 0.056, or

5.6 percent.

8-27

Equal Rate Changes on RSAs, RSLs

Example: Suppose rates rise 2% for RSAs and RSLs. Expected annual change in NII,

NII = CGAP × R

= $15 million × .02

= $300,000 With positive CGAP, rates and NII move in

the same direction. Change proportional to CGAP