interest rate ethics : an aspect of social performance in microfinance arvind ashta chairholder in...

TRANSCRIPT

Interest Rate ethics : an aspect of social performance in microfinance

Arvind Ashta

Chairholder in Microfinance

Burgundy School of Business, CEREN

E-MFP conference, Luxembourg, Nov . 24-26

Thanks to the Banque Populaire de Bourgogne –Franche Comté for financing.

2Ashta European Microfinance Week, Nov. 2009

Plan

Interest rate levels

Questions of governance

Interest rate transparency

3Ashta European Microfinance Week, Nov. 2009

Donations and Equity to Compartamos

Public funds

Private funds

International Development institutions : CGAP, IFC

Compartamos AC (NGO)

Compartamos

(for-profit)

US AID

68%

32%

Accion

4Ashta European Microfinance Week, Nov. 2009

Compartamos IPO in 2007

$ 1.8M

$ 38M

$ 470M

$ 600M

30%

$ 6M

$ 126M

$1550M

$2000M

100%

Paid up capital 2000

Book Value 2006

IPO Proceeds 2007

Market Value 2007

5Ashta European Microfinance Week, Nov. 2009

The problem of governance

For-profit or Not-for-profit

Those who convert from not-for profit to for-profit: is this ethical

Should not-for-profits own for-profits?

2008 Legal StatusFormer status

SKS NBFC since 2006 Society before

Spandana NBFC since 2005 Society before

SHARE NBFC since 2000 Society before

Bandhan NBFC since 2007 Society before

Asmitha NBFC since 2002

SKDRDP Trust

BASIXNBFC and Bank since 1997

Grama Vidiyal NBFC since 2008 Trust before

BISWA Society since 1994

Equitas NBFC since 2007

6Ashta European Microfinance Week, Nov. 2009

Interest rates worldwide (Rosenberg et al. CGAP 2009)

7Ashta European Microfinance Week, Nov. 2009

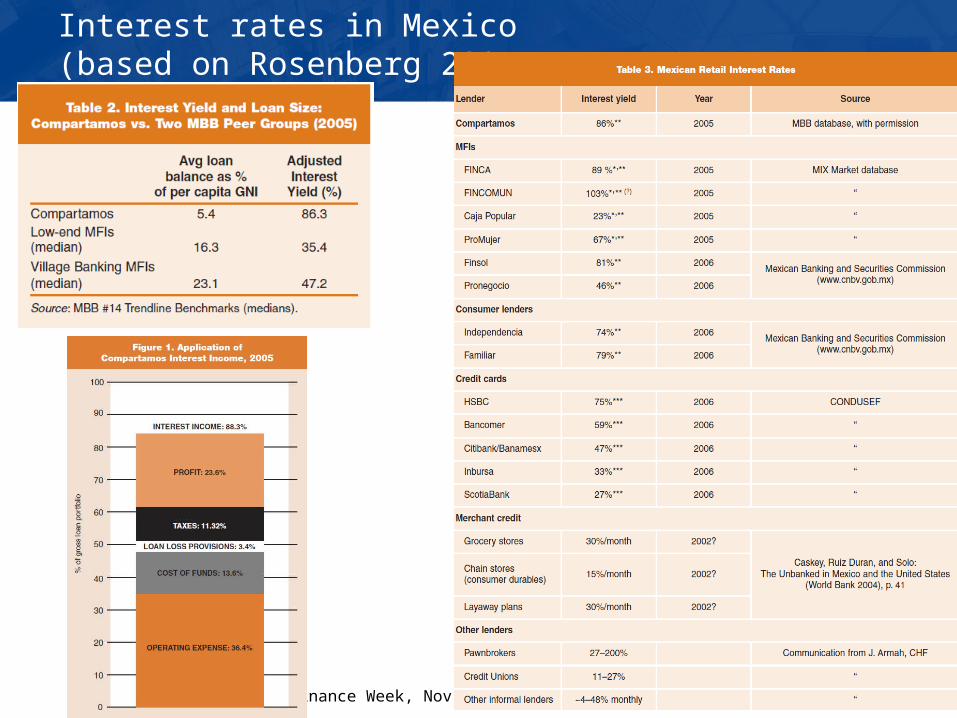

Interest rates in Mexico (based on Rosenberg 2007, CGAP)

8Ashta European Microfinance Week, Nov. 2009

Power versus Interest Grid of Compartamos stakeholders (Ashta & Hudon, 2009)

Interest

Power and influence

Low

Low

High

High

Regulators

Potential Borrowers

ExistingBorrowers

Donors

Managers

Shareholders

Employees

Stakeholder Overall objectives Expected interest rate desiredExisting Borrowers Availability, Impact Low interest ratesPotential Borrowers Availablility, Impact Mixed: High if it enables outreach but Low as

future borrowerDonors Outreach, impact Mainly low interest rates?

(but also sustainability) Employees Profit, growth, job stability, (but some may have social

objectives)Mainly high interest rates?

Regulators Client protection (Outreach, impact, employment?) Not related to interest rate (Low interest rates?)

Shareholders Profit, growth High interest rates(but 2/3 also have development goals) (some may want lower interest rates)

9Ashta European Microfinance Week, Nov. 2009

Ashta & Hudon (2009 a and b)

Impact on existing borrowers would be greater if interest rates were lower (donors, existing borrowers)

Need to be profitable for sustainability (shareholders)

For growth (impact on new borrowers)

How to balance these two objectives?

Earmark Share capital to borrowers As part of interest payment

As free/ bonus shares

10Ashta European Microfinance Week, Nov. 2009

The problem of transparency

Flat rates

APR EAR

Other elements to take into account compulsory savings,

up front fees

Particular problems when period is short

11Ashta European Microfinance Week, Nov. 2009

What is the whole truth in lending?

Example: you buy a good for 140 $. You pay 20$ cash and 150$ to be repaid in 6 monthly instalments (for a total of 170$)

Method 1 2 3 4 5 6Calculation method

(GP–RP) / RP

[(GP-RP)/ RP] x 2

[(GP-RP)/LA]

x 2

[(GP-RP)/

AOB] x 2

(GP–RP)² - 1

IRR x 12

IRR12-1Interest

rate21.4% 42.8% 50% 86%

(APR)

104%

(EAR)

81% (APR)

119%(EAR)GP: global price

RP: real priceLA: loan amountAOB: average opening balance = (LA+D)/2D: downpaymentAPR: annual percentage rate of chargeEAR: effective annual rate IRR: Internal rate of return

For finance professionals, last method is the whole truth: 119%

12Ashta European Microfinance Week, Nov. 2009

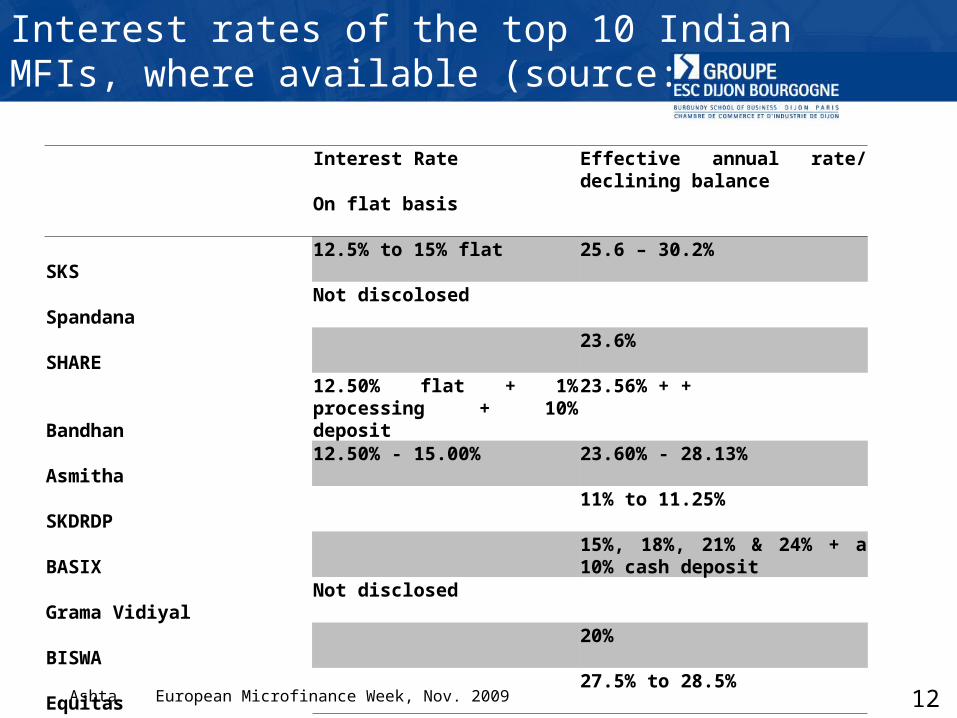

Interest rates of the top 10 Indian MFIs, where available (source: websites Oct. 2009)

Interest Rate Effective annual rate/ declining balance

On flat basis

SKS12.5% to 15% flat 25.6 – 30.2%

SpandanaNot discolosed

SHARE 23.6%

Bandhan

12.50% flat + 1% processing + 10% deposit

23.56% + +

Asmitha 12.50% - 15.00% 23.60% - 28.13%

SKDRDP11% to 11.25%

BASIX 15%, 18%, 21% & 24% + a 10%

cash deposit

Grama VidiyalNot disclosed

BISWA 20%

Equitas 27.5% to 28.5%

13Ashta European Microfinance Week, Nov. 2009

Conclusion: How to link interest rates with Social performance measures

Deviation from average rates International Country

Deviation from celings Deviation from usury rates Deviation from money lender rates

Governance Is part of intrest going back to borrowers in terms of share

capital Are profits lower if there are more NGOs on the board/

more donor funds

Transparency in interest rates Flat rates ? APR disclosed ? EAR disclosed ? Other fees/ compulsory deposits disclosed?

Figure 4: Minimum Reservation prices

Range of negotiation

Pmin1

Pmax

Price

Quantity of loan

AC 1: Average operating cost curve

AC2: Average operating and financing cost curve

AC 3: Average total cost curveincluding inflation and cost of subsidized faciilities

Pmin 2

Pmin 3

14Ashta European Microfinance Week, Nov. 2009

Future research questions

How should you distribute benefits with the range?

How do you feel if your NGO becomes a profitable entity? Former Donors to NGO

Former volunteers to NGO

If you separate your loan from insurance services –to lower interest rates

Will people still take your insurance services

Does packaging oblige them to take all?