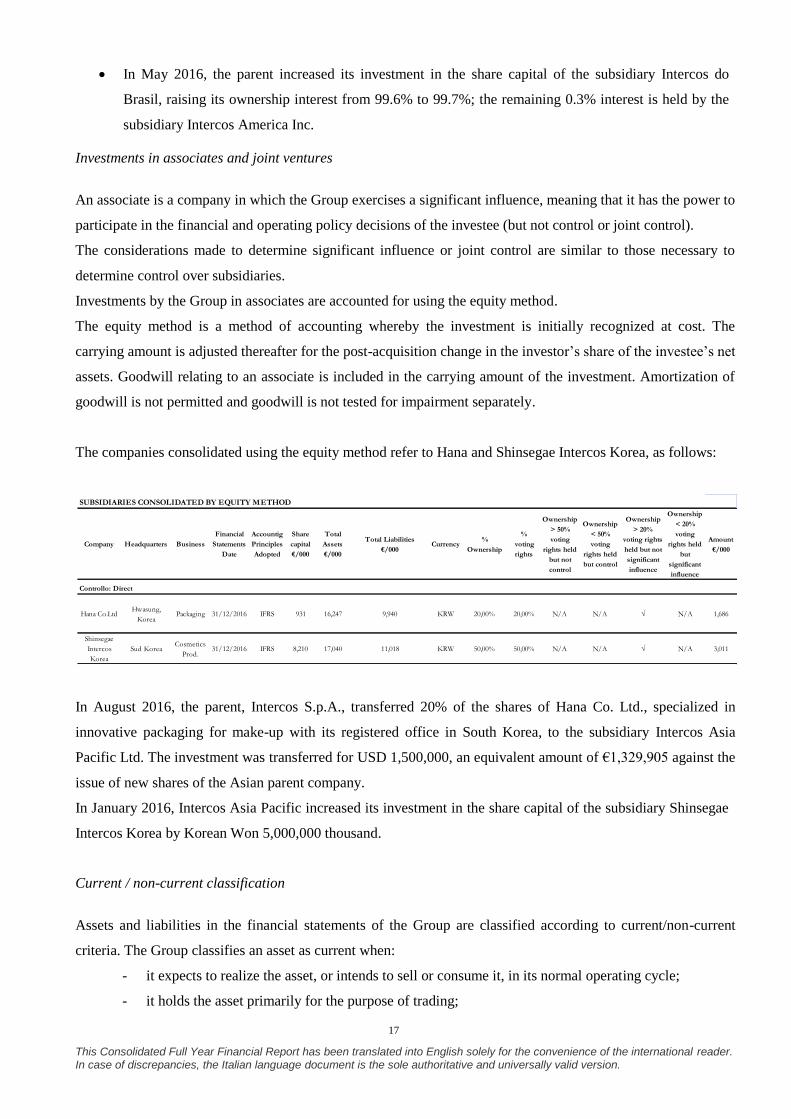

intercos group global cosmetic manufacturer …web.intercos.it/bond/files/fin/intercos spa -...

TRANSCRIPT

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

INTERCOS GROUP

Global Cosmetic Manufacturer

CONSOLIDATED FINANCIAL STATEMENTS

AT DECEMBER 31, 2016

PREPARED IN CONFORMITY WITH IFRS

ADOPTED BY THE EUROPEAN UNION

Intercos S.p.A.

Registered Office

Milan - Piazza Generale Armando Diaz 1

1

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

Intercos S.p.A. Registered Office in Milan – Piazza Generale Armando Diaz 1

Share capital Euros 10,710,193 fully paid-in

Consolidated Financial Statements at December 31, 2016

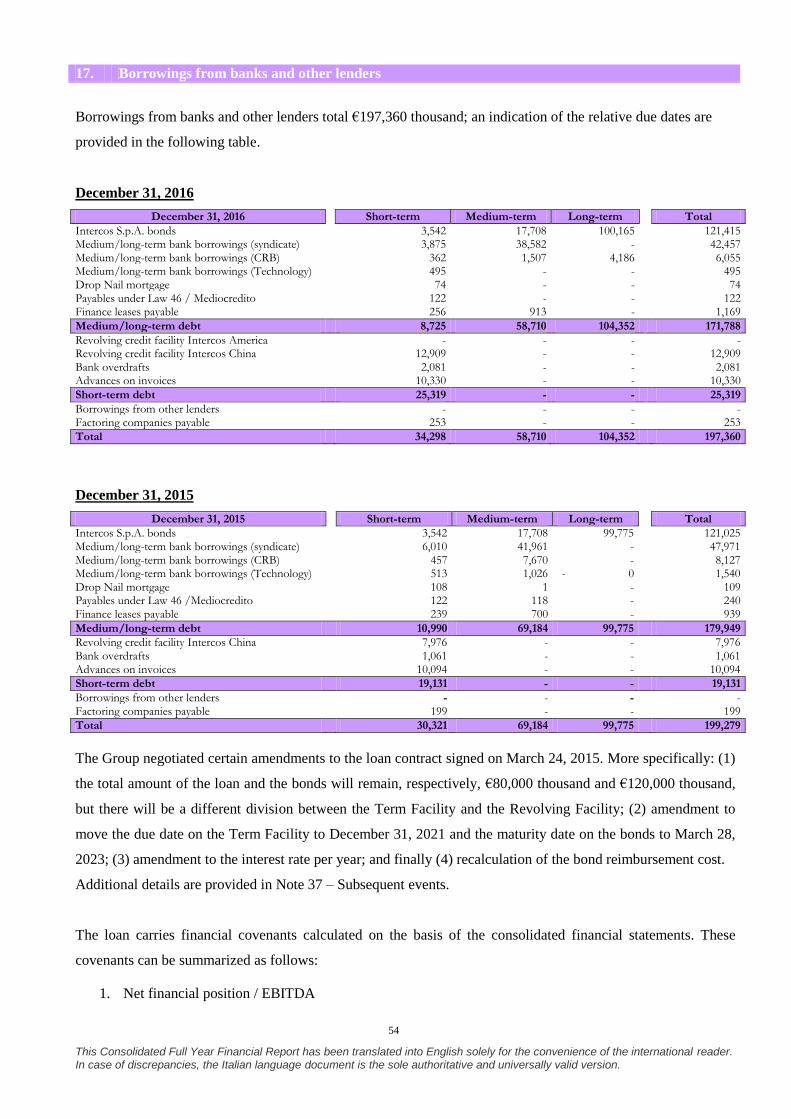

REPORT ON OPERATIONS

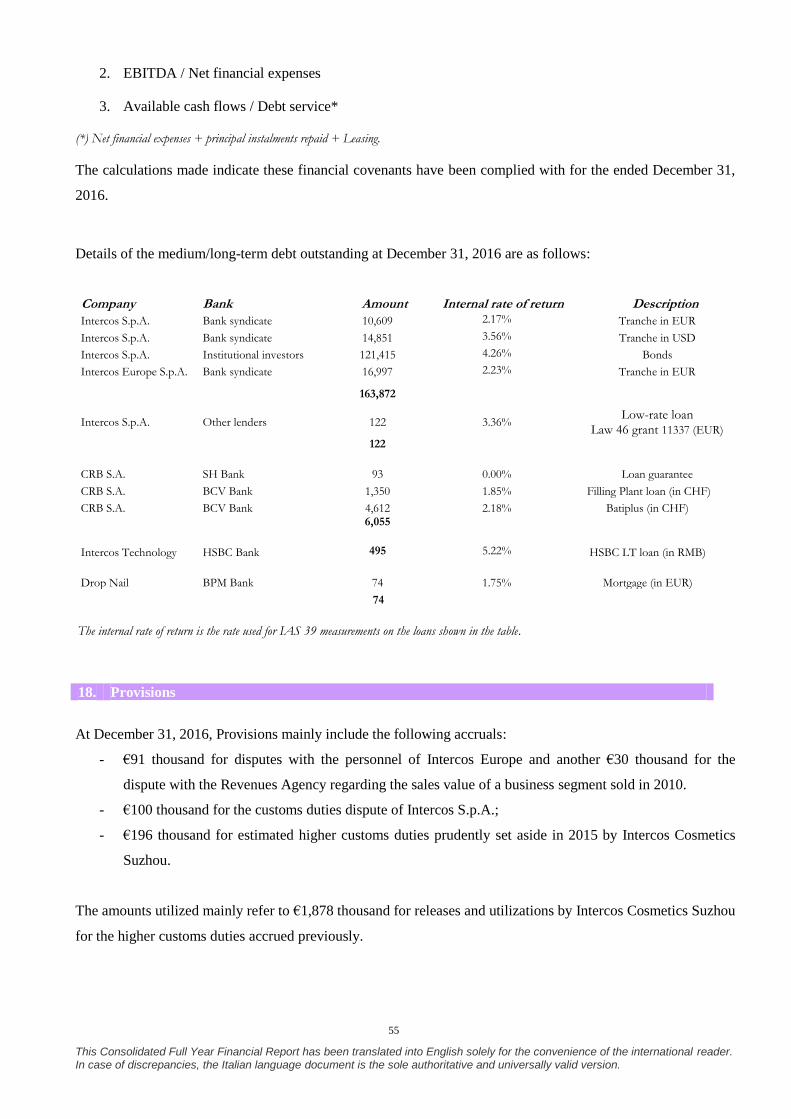

1. Profit and Financial Performance

2016 saw the Intercos Group confirm the success of its strategy and its leadership in the field of innovation

through product diversification, in the Color Cosmetic and Skin Care markets,

Both Business Units of the Group continue to grow in all distribution segments and in the full service

platforms, where it recorded a rise in orders and revenues, especially in the EMEA region.

The Group reported Revenues from sales for a total of €448,690 thousand in 2016 compared to €401,767

thousand in 2015, showing an increase of €46,923 thousand (+11.7%).

Adjusted EBITDA* in 2016 is a positive €62,467 thousand, with a 13.9% adjusted EBITDA margin against

14.9% in the prior year.

Operating profit (EBIT) is €41,331 thousand, with a 9.2% EBIT margin compared to 9.3% in 2015

(€37,297 thousand).

Capital expenditures in property, plant and equipment and intangible assets total €20,161 thousand and

€8,695 thousand, respectively.

The net financial position is €132,835 thousand compared to €148,596 thousand at December 31, 2015. The

considerable improvement of €15,761 thousand is due to better management of net working capital, which

decreases by €4,259 thousand despite a significant increase in volumes.

Equity is €137,493 thousand compared to €118,391 thousand at December 31, 2015, up by

€19,103 thousand.

* Adjusted EBITDA is represented by operating profit (loss) before depreciation, amortization and impairment reversals (losses) adjusted

from the management by nonrecurring income (expenses).

2

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

2. World Economic Overview

The state of the global economy has improved slightly. However, the future outlook is still being

affected by various factors of uncertainty. In the United States, much depends on the economic

policies of the new administration, which have not yet been defined in detail: an expansive impact,

which is currently difficult to quantify, may derive from the measures announced with regard to the

budget policy, but there may also be negative effects due to the adoption and spread of trade

restrictions. Global growth could be hindered by the upsurge of turbulence in the emerging

economies, associated with the normalization of U.S. monetary policy.

The continuous rebalancing of China from a situation of growth driven by investments to one of

growth based on consumption will probably lead to a deceleration of the driving force of its

economy. Meanwhile, the recession in Latin America may find relief from a slight recovery in the

prices of raw materials and from financial conditions which have generally been streamlined.

Sanctions have played a role in the collapse of the economy in Russia and in the negative GDP, and

the protracted period of major political upset in Brazil has had a significant impact on its economy.

In the Eurozone, growth continues at a moderate pace, in the direction of gradual consolidation. The

risks of deflation have been reduced; inflation rose in December but, overall, inflation still remains

low. In order to maintain the expansive monetary conditions which will ensure a rise in inflation,

the ECB’s Governing Council has extended the length of its securities market program until at least

December 2017, and will extend it further if necessary. From April, monthly purchases will return

to €60 billion, as in the initial phase of the program.

According to the indicators currently available, in autumn, the recovery of the Italian economy

continued, albeit at a moderate pace. Considering the trend of industrial production, electrical

consumption and goods shipments, all of these sectors increased. Economic activity was stimulated

by the restart of investments and the expansion of household expenditures. In the third quarter of

2016, total employment stabilized; the number of company employees with permanent and short-

term contracts increased. In recent months, the expansion of credit to the private non-financial

sector continued, and there was also an increase in loans to companies. However, growth remains

moderate.

The forecasts for the Italian economy, based on the most recent trends, suggest that, on average,

GDP should grow about 0.9% in 2017 and 1.1% in both 2018 and 2019. Economic activity should

again be supported by domestic demand and, already in 2017, by the gradual strengthening of

foreign demand. In 2019, the level of GDP should still be approximately lower than in 2007.

3

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

Overall it is thought that, with regard to these predictions, risks for growth are mainly orientated

downwards. Apart from financial factors, the main sources of uncertainty lie in the global context.

There is a particularly high risk that the expansion of the global economy may be affected, besides

what was considered in the forecasts, by the upsurge and spread of protectionist measures, as well

as by potential turbulence in the emerging economies.

3. Market Scenario

The global market of the Color Cosmetics sector has a retail value of approximately USD 60 billion, with

a 6.6% year-over-year increase against 6.5% in 2015.

With regard to the various geographical regions, Western Europe continues to expand, growing 3.9%

compared to 3.4% in 2015.

In North America, the market gain is 7.1% versus 2.3% in the prior year.

The Asian market (excluding Japan) expanded by 10% compared to 2015. China, in particular, grew 10.5%

against 2015 in a market worth USD 4.5 billion.

Emerging markets displayed a positive trend of +9.6%, with Brazil logging a 5% increase over 2015.

4. Important Factors significantly impacting Operating Performance

Technological innovation

The Intercos Group has adopted an R&D investment policy geared to identifying and developing innovative

products and efficient and competitive manufacturing processes. The search for innovation in terms of both

process and final product begins from the knowledge of the Make-up and Skin Care markets and the relative

distribution channels; this know-how gives the Group an advantage in adapting to the changing demand of

consumers, actively anticipating them and influencing them.

In 2016, the Intercos Group employed about 617 resources dedicated to innovation, creating, over the course

of just one year more than 594 new color cosmetics formulae that became products, 34 new raw materials

and over 628 new skin care formulae.

Market expansion thanks to new customer categories

The entry of new players in the market such as Emerging Regional Brands and Retailers have contributed to

the expansion of the market in which the Group operates, now no longer limited to multinational brands.

More specifically, the development of these categories of clients has made it possible to reach end consumers

that were not previously served. This has enabled the Intercos Group to extend its offering of services since

these new categories of customers do not have their own manufacturing capabilities and require a “full

4

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

service” platform. The platform comprises not only the creation of the product but also its packaging and, if

necessary, the marketing concept.

5. Profit and Financial Review of the Intercos Group

For the purpose of providing information along the lines of the performance analysis and control parameters

of the Group, the non-IFRS alternative performance measures used by management to provide information

for a better assessment of the results of operations and financial position of the Group are presented below.

Such performance measures should not be interpreted as a substitute for the performance measures

established by the IFRS.

The content of the alternative performance measures that are not arrived directly in the financial statements

are defined as follows:

EBITDA: is calculated as profit before taxes, financial income (expenses) without any adjustment

and depreciation, amortization and impairment reversals (losses). EBITDA also excludes income

(expenses) from the result of unconsolidated companies and securities, as well as gains or losses on

disposal of consolidated investments, classified under Financial income (expenses) or, for the share

of the profit (loss) of investments accounted for using the equity method (non-operating), within the

item Result from investments.

Adjusted EBITDA: is calculated by the deducting the following, if applicable, from EBITDA, as

defined above:

impairment of goodwill, if any;

amortization of the portion of the purchase price allocated to intangible assets in a business

combination, as established in IFRS 3;

restructuring costs, under specific and significant restructuring plans;

nonrecurring other income (expenses) referring to particularly significant events unrelated to

ordinary business operations.

Operating Working Capital includes inventories and trade receivables and payables;

Net Working Capital: is given by operating working capital net of other current assets and

liabilities;

Net invested capital: is the sum of non-current assets, non-current liabilities and Net Working

Capital.

Net debt (cash) or net financial position: is given by the sum of current and non-current financial

liabilities net of short- and long-term financial receivables, including cash and cash equivalents;

Workforce: is given by the number of employees registered in the payroll book on the last day of

the period under consideration.

5

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

(in € thousands)

2016 2015 Change

Revenues 448,690 401,767 46,923

EBITDA 63,105 58,761 4,344

Adjusted EBITDA 62,467 59,844 2,623

EBITDA margin 13.9% 14.9% -1.0%

Operating profit (EBIT) 41,331 37,297 4,034

EBIT margin 9.2% 9.3% -0.1%

EBT 31,782 24,815 6,967

EBT margin 7.1% 6.2% 0.9%

Profit 19,814 14,804 5,010

Profit margin 4.4% 3.7% 0.7%

(in € thousands) 2016 2015 Change

Net working capital 61,882 66,141 (4,259)

Working capital turnover

7.25 6.07 1.18

Net invested capital 270,328 266,986 3,342

Non-current assets 226,788 221,245 5,542

Net financial position 132,835 148,596 (15,761)

2016 2015 Change

Workforce (number) 2,747 2,409 338

Earnings per share (basic and diluted) 0.22 0.16 0.06

For the purpose of providing additional disclosure on the results of operations, financial position and cash

flows of the Group, the following Reclassified consolidated income statement, Reclassified consolidated

statement of financial position and consolidated net debt (cash) schedule are presented below.

6

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

Reclassified Consolidated Income Statement by function

(in € thousands)

2016

2015

Revenues 448,690

401,767

Cost of sales (342,446)

(302,852)

Industrial gross margin 106,244

98,915

% of revenues 23.7% 24.6%

R&D and innovation costs (26,052)

(25,248)

Selling expenses (20,579)

(18,944)

General and administrative expenses (22,939)

(19,978)

Other operating income (expenses) 4,998

3,636

Result from investments (operating) (978)

-

Nonrecurring income (expenses) 638

(1,083)

Operating profit (EBIT) 41,331

37,297

EBIT margin 9.2% 9.3%

Depreciation, amortization and impairment reversals (losses) (21,774)

(21,463)

EBITDA (*) 63,105

58,761

Nonrecurring income (expenses) 638

(1,083)

Adjusted EBITDA (*) 62,467

59,844

EBITDA margin 13.9% 14.9%

Financial income (expenses), net (**) (9,812)

(12,588)

Result from investments (financial) 263

106

Profit before taxes (EBT) 31,782

24,815

Income taxes (11,968)

(10,011)

Profit for the year 19,814

14,804

Of which:

- attributable to the parent 19,514

14,701

- attributable to non-controlling interests

300

103

Earnings per share: Basic and diluted 0.22

0.16

(*) For additional details, please refer to page 4.

(**) Financial income (expenses) is the sum of financial income (expenses) without any adjustment.

7

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

In 2016, consolidated revenues total €448,690 thousand, up 11.7% compared to 2015, at a higher growth rate

than the market rate.

Breakdown of revenues by geographical region

A comparison of revenues by geographical region in the two years is as follows:

(in € thousands)

Revenues by geographic region 2016 2015

Americas 161,479 162,313

EMEA 242,398 190,632

Asia 44,813 48,822

Total 448,690 401,767

Americas: this region recorded lower revenues compared to the prior year of 1%, mainly in the

Prestige market.

EMEA: posted sales of €242,398 thousand versus €190,632 thousand in the prior year, with the

€51,766 thousand (+27.2%) increase recorded in all customer segments, whereas the market increase

in the region was 3.9% overall.

60 59

37

25 15

62 63

41 32 20

Adjusted EBITDA EBITDA EBIT Profit before taxes Profit for the period

2015 2016

8

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

Asia: reported a decrease in revenues of 8.2% compared to 2015 (€44,813 thousand from €48,822

thousand), mainly in respect of multinational customers.

Breakdown of sales by Business Unit

Details of the composition of Revenues in 2016 compared to 2015 by Business Unit are the following:

Year Change

(in € thousands) 2016 2015 2016 over 2015 2016 over 2015

%

Make-up 393,118 349,651 43,467 12.43%

Skin Care 55,571 52,116 3,455 6.63%

Total 448,690 401,767 46,923 11.68%

The contribution to revenues by Group companies is summarized below:

(in € thousands)

Company

2016 2015

Intercos Europe S.p.A.

249,387 206,359

Intercos America Inc.

94,525 105,096

Intercos Cosmetics Suzhou Co. Ltd

22,605 14,891

Intercos Technology Co. Ltd

37,623 43,310

Interfila Cosmetics (Shanghai) Co. Ltd

19,753 16,491

CRB Sa.

35,867 36,753

Other companies

20,758 15,759

Aggregate Total

480,518 438,659

Eliminations (31,828) (36,893)

Consolidated Total 448,690 401,767

Adjusted EBITDA is a positive €62,467 thousand, an increase of €2,623 thousand compared to €59,844

thousand in 2015, with a 13.9% EBITDA margin that is 1% lower than in 2015. Higher sales and keeping

fixed costs in check compensated the higher cost of sales caused by a different product and service mix.

Additional details on the results of the BUs are provided under Segment reporting, in Note 5 of the

consolidated financial statements.

Operating profit (EBIT) is a positive €41,331 thousand compared to 2015, reflecting a higher EBITDA and

lower incidence of nonrecurring income (expenses).

In 2015, net nonrecurring expenses, in fact, were €1,083 thousand mainly due to €449 thousand for legal

expenses incurred by Intercos S.p.A. in respect of an open dispute relating to a proprietary patent of the

Intercos Group and €543 thousand for the increase in the provision for risks as a result of higher customs

duties prudently estimated by Intercos Cosmetics Suzhou.

9

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

In 2016, net nonrecurring income was recorded for €638 thousand. It includes: €256 thousand of income

from the sale of a building owned by the subsidiary CRB S.A.; €360 thousand of net nonrecurring income by

the Asian subsidiaries mainly due to the release of the provision for risks set aside previously for higher

customs duties not due and extra costs incurred to complete the project to create a second Intercos Group

headquarters run by the subholding company Intercos Asia Pacific Limited; €522 thousand of net

nonrecurring income referring to Intercos S.p.A. owing to the amicable settlement of a dispute with a third

party over trade secret misappropriations; €305 thousand of expenses by the subsidiary Intercos Europe

S.p.A. for employee social security contributions that arose on the completion of the question regarding the

closing of the Limbiate factory; €196 thousand of expenses by the subsidiary Drop Nail S.r.l. incurred for the

realization of the industrial project to strengthen its product range represented by nail polishes and nail care

projects.

Profit for the year is €19,814 thousand or 4.4% of revenues, compared to a profit of €14,804 thousand

reported in 2015 (3.7% of revenues).

10

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

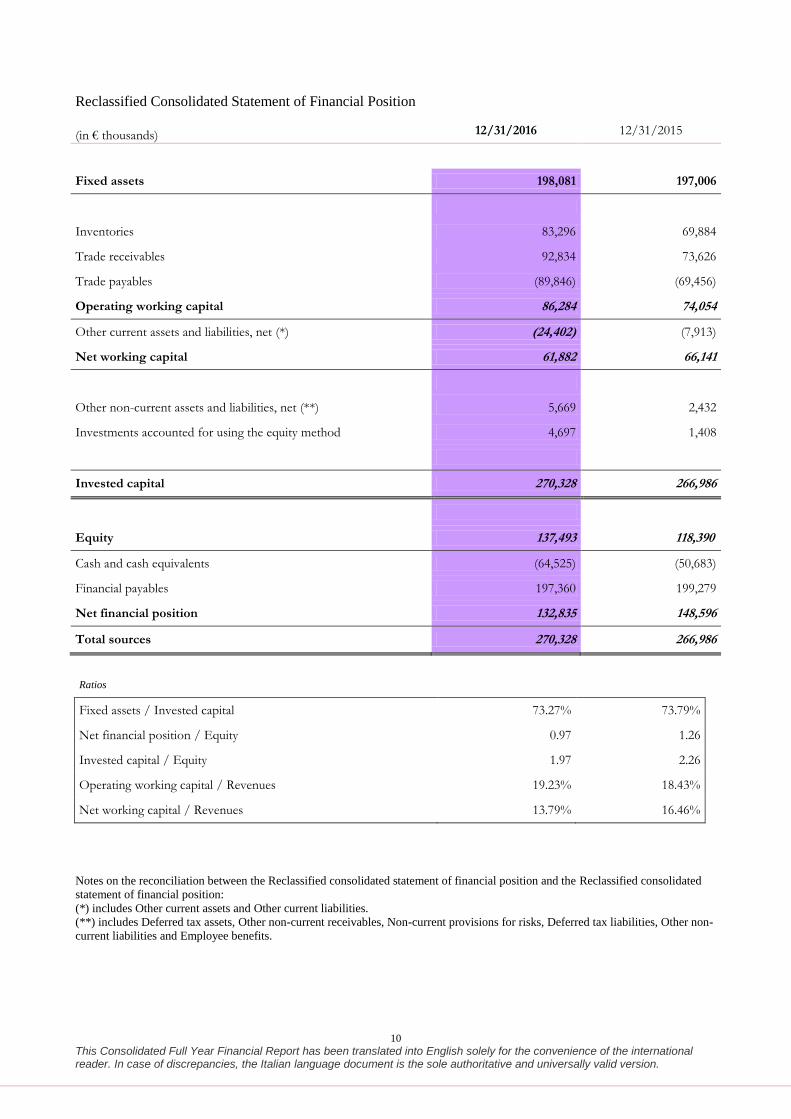

Reclassified Consolidated Statement of Financial Position

(in € thousands) 12/31/2016 12/31/2015

Fixed assets 198,081 197,006

Inventories 83,296 69,884

Trade receivables 92,834 73,626

Trade payables (89,846) (69,456)

Operating working capital 86,284 74,054

Other current assets and liabilities, net (*) (24,402) (7,913)

Net working capital 61,882 66,141

Other non-current assets and liabilities, net (**) 5,669 2,432

Investments accounted for using the equity method 4,697 1,408

Invested capital 270,328 266,986

Equity 137,493 118,390

Cash and cash equivalents (64,525) (50,683)

Financial payables 197,360 199,279

Net financial position 132,835 148,596

Total sources 270,328 266,986

Ratios

Fixed assets / Invested capital 73.27% 73.79%

Net financial position / Equity 0.97 1.26

Invested capital / Equity 1.97 2.26

Operating working capital / Revenues 19.23% 18.43%

Net working capital / Revenues 13.79% 16.46%

Notes on the reconciliation between the Reclassified consolidated statement of financial position and the Reclassified consolidated

statement of financial position:

(*) includes Other current assets and Other current liabilities.

(**) includes Deferred tax assets, Other non-current receivables, Non-current provisions for risks, Deferred tax liabilities, Other non-

current liabilities and Employee benefits.

11

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

Capital expenditures in Property, plant and equipment and Intangible assets in 2016 total €28,856

thousand.

The improvement in the Net Financial Position continued into 2016 thanks to the optimization of the supply

chain processes and working capital management. This resulted in a total reduction in the current and the

medium-/long-term financial position of €15,761 thousand. The net debt at December 31, 2016 is therefore

€132,835 thousand compared to €148,596 thousand at December 31, 2015.

Consolidated net debt (cash)

(in € thousands) 12/31/2016 12/31/2015

Cash and cash equivalents (64,525) (50,683)

Borrowings from banks and other lenders 34,187 30,321

Current financial position (30,338) (20,362)

Borrowings from banks and other lenders 163,173 168,959

Non-current financial position 163,173 168,959

Debt (cash) 132,835 148,596

Equity at December 31, 2016 is €137,493 thousand compared to €118,390 thousand at December 31, 2015,

with an increase of €19,103 thousand. Additional details are provided Note 16 of the consolidated financial

statements.

66

221

267

149

118

62

227

270

133 137

Net Working Capital Fixed Assets Net Invested Capital Net Financial Position

Equity

2015 2016

12

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

6. Significant Events in 2016

The following significant events took place during the year 2016:

On January 19, 2016, Intercos S.p.A. (parent) signed a settlement agreement with Woojung Tech.

Co., Ltd. and Mr Dong-Pil Choi to definitively and amicably close, in the company’s favor, the

dispute initiated in September 2014 between the company and the latter, in relation to which a

summons was filed by Intercos S.p.A. for trade secret misappropriation before the Courts in Los

Angeles, California.

On January 30, 2016, Intercos Asia Pacific increased its investment in the share capital of the

subsidiary Shinsegae Intercos Korea by Korean Won 5,000,000 thousand. The shareholder

Shinsegae also increased its investment in the company’s share capital so that its percentage

investment in capital would remain unchanged.

On February 9, 2016, the board of directors of Intercos S.p.A. approved the transfer of the

company’s registered office from Milan, Piazza Eleonora Duse 2, to Milan, Piazza Generale

Armando Diaz 1. The registered offices of the subsidiaries were also transferred: Drop Nail S.r.l. (on

February 15, 2016), Intercos Europe S.p.A. and Vitalab S.r.l. (on March 25, 2016).

On February 10, 2016, following the intent manifested by Drop Nail S.r.l.’s minority shareholder,

Paragon Cosmetics S.r.l., to: 1) divest of its 40% interest in the capital of Drop Nail S.r.l., equal to a

nominal amount of €20 thousand and 2) sell its remaining receivable due from Drop Nail S.r.l., for

the shareholder loans extended in the past, for a total amount of €1 thousand – Intercos S.p.A, as part

of its business plan aimed at strengthening its product range represented by nail polishes and nail

care products, purchased Paragon’s investment and receivable for €543 thousand, thus bringing its

investment to €1,186,234, representing 100% of the capital of the company Drop Nail S.r.l.

On March 25, 2016, the parent waived a part of its non interest-bearing shareholder loan due from

Drop Nail S.r.l. and, precisely, a total of €1,000 thousand, with such amount to be recorded in equity,

under Other reserves, subaccount Payment against share capital, bringing its investment to

€2,186,234 thousand.

13

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

On May 2, 2016, a share capital increase was approved by the company Intercos Do Brasil Indùstria

e Comércio de Productos Cosmeticos LTDA (“IDOBRASIL”) for R$8,000,000, subscribed to and

fully paid in by Intercos S.p.A. as a shareholder of IDOBRASIL.

Following the above capital increase, the share capital of IDOBRASIL amounts to

R$30,377,143, divided into 30,377,143 shares of R$1.00 each, held by the shareholders as

follows: (a) 30,280,543 shares for a total of R$30,280,543 held by Intercos S.p.A. and (b)

96,600 shares for a total of R$96,600 held by Intercos America Inc.

On July 28, 2016, the Drop Nail S.r.l. shareholders’ meeting appointed Vincenzo Misitano as the

sole Director.

On August 1, 2016, Intercos S.p.A. conferred its investment in the company Hana Co. Ltd

(representing 20% of the entire share capital) to the company Intercos Asia Pacific Limited.

On August 1, 2016, Intercos S.p.A., as the sole shareholder of Intercos America Inc., subscribed to a

capital increase by Intercos America Inc. for a total of $25,000,000 to be paid in several tranches as

follows: 1) $5,000,000 by a cash injection; 2) $10,000,000 by the partial waver of intercompany

loans that were extended by Intercos S.p.A. to Intercos America Inc., which amounted to a total of

$37,900,000; and 3) $10,000,000 by payment in separate tranches based on resolutions passed

previously by the board of directors of Intercos America, in the event of specific and significant

financial needs of the same Intercos America Inc., with the understanding that the last tranche will be

paid no later than one year from the date of August 1, 2016.

On August 17, 2016, the sales agreement was signed between CRB S.A. – as the seller – and the

company Solufonds S.A. – as the buyer (on behalf of Procimmo Swiss Commercial Fund 56) (the

“Buyer”) – for a building owned by CRB situated in ZI du Verney 1 in Puidoux, Canton of Vaud,

Switzerland (the “Building”). This Sales Agreement has effect from December 1, 2016 and the sales

price is CHF 6,200,000 (in addition to VAT of CHF 347,760).

On September 8, 2016 and September 12, 2016, respectively, Intercos S.p.A. and Intercos

Europe S.p.A. – in agreement with their respective Boards of Statutory Auditors – adopted a new

14

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

Organizational, Management and Control Model pursuant to Legislative Decree 231/2001. On the

same date, the Ethics Code and the Code of Conduct were updated by the Group.

On October 21, 2016, Intercos S.p.A. formed a new company called Intercos Concept S.r.l., with

beginning share capital of €10,000 fully paid in by Intercos S.p.A. Intercos Concept is dedicated,

among other things, to the performance of services to companies, including commercial, marketing,

promotional, organizational, technical, consulting and other types of services, as it pertains to private

labels, and, therefore, directed to the development of brands for clients that operate in the retail

commercial sector of colored products for make-up, creams, personal-care products, nail polish,

perfume and cosmetic products in general, as well as like products, accessories or, in any case,

products that complement cosmetics.

On October 21, 2016, in order to render management of the company more efficient, the

shareholders’ meeting of Intercos S.p.A. amended the bylaws to increase the possible number of

members of the board of directors from 5 to 7 and appointed new Board members: Paolo Valsecchi –

who is already COO of the Intercos Group and has power of attorney in the company with important

powers in various areas of corporate activities – and Renato Semerari.

In December 2016, the parent, as the sole shareholder of Intercos Concept S.r.l., made a payment

against share capital of €350,000 to Intercos Concept S.r.l., to be recognized in equity and recorded

in the Other reserves, subaccount Payment against share capital, bringing its investment to €360,000,

representing 100% of the company’s share capital.

15

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

7. Related Party Transactions

Related party transactions do not qualify as either atypical or unusual but fall under the ordinary course of

the business operations of the Group companies. Such transactions, when not concluded at standard

conditions or dictated by specific laws, are nevertheless carried out on an arm’s length basis.

The details of the effects of related party transactions on the income statement for 2016 and the statement of

financial position at December 31, 2016 are described in Note 32.

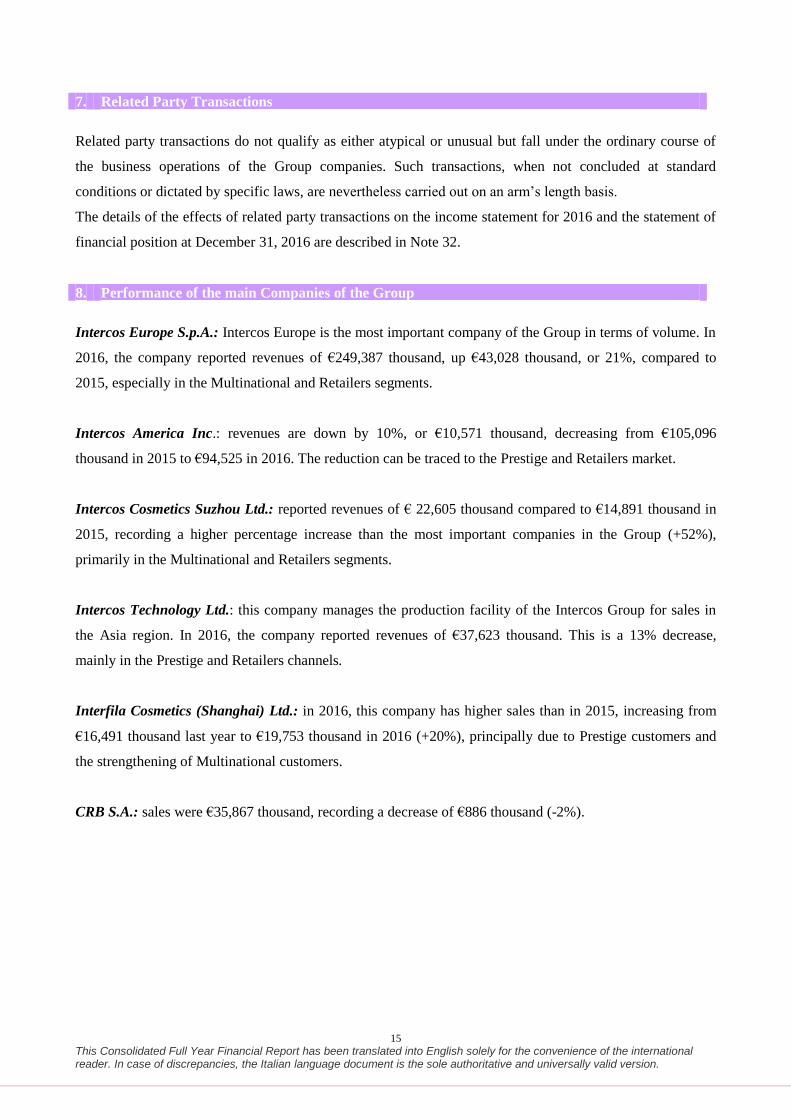

8. Performance of the main Companies of the Group

Intercos Europe S.p.A.: Intercos Europe is the most important company of the Group in terms of volume. In

2016, the company reported revenues of €249,387 thousand, up €43,028 thousand, or 21%, compared to

2015, especially in the Multinational and Retailers segments.

Intercos America Inc.: revenues are down by 10%, or €10,571 thousand, decreasing from €105,096

thousand in 2015 to €94,525 in 2016. The reduction can be traced to the Prestige and Retailers market.

Intercos Cosmetics Suzhou Ltd.: reported revenues of € 22,605 thousand compared to €14,891 thousand in

2015, recording a higher percentage increase than the most important companies in the Group (+52%),

primarily in the Multinational and Retailers segments.

Intercos Technology Ltd.: this company manages the production facility of the Intercos Group for sales in

the Asia region. In 2016, the company reported revenues of €37,623 thousand. This is a 13% decrease,

mainly in the Prestige and Retailers channels.

Interfila Cosmetics (Shanghai) Ltd.: in 2016, this company has higher sales than in 2015, increasing from

€16,491 thousand last year to €19,753 thousand in 2016 (+20%), principally due to Prestige customers and

the strengthening of Multinational customers.

CRB S.A.: sales were €35,867 thousand, recording a decrease of €886 thousand (-2%).

16

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

9. Research & Development

In 2016, the Group continued to invest in new products and technologies, confirming its global leadership

position in the Make-up and Skin Care businesses.

The increase in Research & Development costs in 2016 totals €6,395 thousand and refers mainly to €2,701

thousand for projects that are not yet completed and classified in Assets under development and payments in

advance, conducted principally by Intercos S.p.A. and €3,694 thousand classified in Research and

development costs, of which €2,490 thousand relates to Intercos S.p.A., €512 thousand to Intercos America,

€183 thousand to CRB S.A. projects and, lastly, €509 thousand for research conducted by Vitalab S.r.l.

The increase in Assets under development of €2,701 thousand is mainly composed of costs on the

uncompleted R&D projects of Intercos S.p.A. The projects refer for the most part to:

(i) €490 thousand for the “Sharpenable Pencils” project begun in June 2016. The objective is to research

new, eco-compatible and sustainable raw materials capable of characterizing new patentable formulae for a

new pencil in plastic.

(ii) €529 thousand for the “Nail Polish” project begun in the second quarter of 2016. The objective is to

create and manufacture new nail polish materials capable of making nail polishes last longer than those

traditionally found on the market.

(iii) €682 thousand for the “Diplaticoni” project begun towards the end of the second quarter of 2016. The

objective is to obtain a family of new eco-sustainable cosmetic raw materials, owned by Intercos and not

otherwise available on the market, that can take different physical forms and thus can be used in all product

categories.

(iv) €487 thousand for the “PLA” project begun during the year. The objective is to develop biodegradable

polymers.

(v) €126 thousand for the “Silicone ogive”, project. The objective is to identify a new silicone to develop

suitable ogives for the manufacture of lipsticks that perform better than those currently in use.

(vi) €113 thousand for the “Patch” project. The objective is to develop a cosmetic patch, with a multilayer

structure similar to that of transdermal patches with a decorative and/or corrective function for the eye area.

(vii) €273 thousand for the “CMR” project begun during the year. The objective is to develop ceramic

materials.

For capitalized projects, management carefully assesses their expected economic benefits and the benefits

obtained over the course of their useful life, testing for any onset of impairment.

17

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

10. Personnel and Organization

The headcount of the Group at December 31, 2016, including temp workers, numbers 4,591 compared to

3,822 at year-end 2015, with an increase of 769 people, of whom 338 are employees of the Group and 431

are temporary workers.

The breakdown by category is as follows:

Group headcount December 31, 2016 December 31, 2015

Executive and mid-level managers 242 221

White-collars 946 866

Blue-collars 1,559 1,322

Total 2,747 2,409

Temporary 1,844 1,413

Total 4,591 3,822

The breakdown by permanent and fixed-term personnel is the following:

Group headcount December 31, 2016 December 31, 2015

Permanent 2,727 2,395

Fixed-term 20 14

Total 2,747 2,409

During the year, there were no deaths or accidents in the workplace which caused serious injury to personnel.

Employee benefit expenses increased €11,518 thousand, from €121,726 thousand in 2015 to €133,245

thousand in 2016, or 9.5%. The change is mainly due to an increase in the Group’s workforce as a result of

higher manufacturing and sales volumes.

The Group uses temp work contracts for its manufacturing activities in order to render direct manufacturing

costs more flexible. The growth in business in 2015 and 2016 led to an increase in these costs of €6,321

thousand compared to the prior year, from €25,748 thousand in 2015 to €32,069 thousand in 2016.

18

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

11. Risk Management and Uncertainties

The Group’s business is exposed to various types of risk including exchange rate risk, interest rate risk,

credit risk and liquidity risk.

Exchange rate risk

The Group operates globally and is exposed to foreign exchange risk arising from fluctuations in the

equivalent amount of commercial and financial flows denominated in currencies other than the functional

currency of the individual companies of the Group.

The Group’s exposure is mainly concentrated in the following exchange rates:

- EUR/USD exchange rate: with reference to commercial and financial transactions entered into

by Eurozone companies operating on the North American market and vice versa.

- EUR/GBP exchange rate: with reference to commercial and financial transactions entered into

by Eurozone companies operating on the British market and vice versa.

- USD/RMB: with reference to commercial and financial transactions entered into by Chinese

companies operating on the North American market and vice versa.

- EUR/RMB: with reference to commercial and financial transactions entered into by Eurozone

companies operating on the Chinese market and vice-versa.

- CHF/EUR/USD: with reference to commercial and financial transactions entered into by the

Group company operating in Switzerland.

It is the Group’s policy to hedge, where possible, exposures denominated in currencies other than the

functional currency of the individual companies, particularly the following:

certain flows: commercial flows and exposures generated by loans receivable and payable;

forecast flows: commercial flows originating from certain or highly probable contractual

commitments.

These hedges are monitored by net currency positions managed by the Group or by using derivative

contracts.

19

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

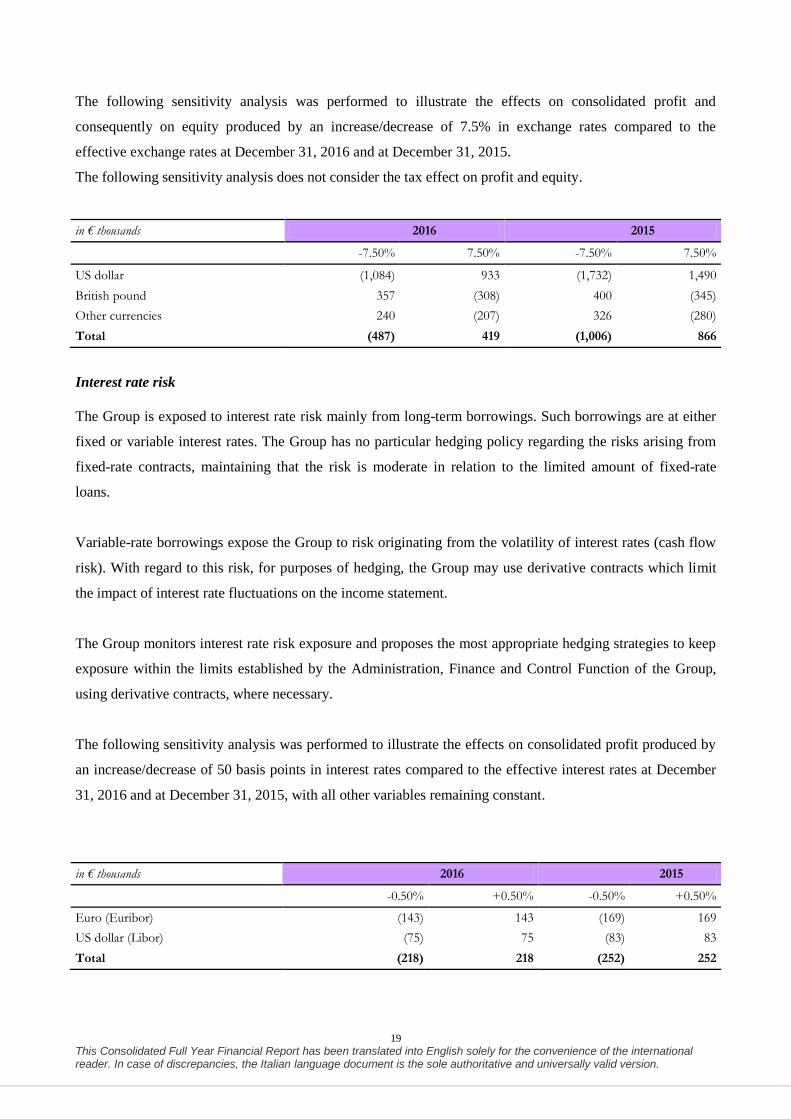

The following sensitivity analysis was performed to illustrate the effects on consolidated profit and

consequently on equity produced by an increase/decrease of 7.5% in exchange rates compared to the

effective exchange rates at December 31, 2016 and at December 31, 2015.

The following sensitivity analysis does not consider the tax effect on profit and equity.

in € thousands 2016 2015

-7.50% 7.50% -7.50% 7.50%

US dollar (1,084) 933 (1,732) 1,490

British pound 357 (308) 400 (345)

Other currencies 240 (207) 326 (280)

Total (487) 419 (1,006) 866

Interest rate risk

The Group is exposed to interest rate risk mainly from long-term borrowings. Such borrowings are at either

fixed or variable interest rates. The Group has no particular hedging policy regarding the risks arising from

fixed-rate contracts, maintaining that the risk is moderate in relation to the limited amount of fixed-rate

loans.

Variable-rate borrowings expose the Group to risk originating from the volatility of interest rates (cash flow

risk). With regard to this risk, for purposes of hedging, the Group may use derivative contracts which limit

the impact of interest rate fluctuations on the income statement.

The Group monitors interest rate risk exposure and proposes the most appropriate hedging strategies to keep

exposure within the limits established by the Administration, Finance and Control Function of the Group,

using derivative contracts, where necessary.

The following sensitivity analysis was performed to illustrate the effects on consolidated profit produced by

an increase/decrease of 50 basis points in interest rates compared to the effective interest rates at December

31, 2016 and at December 31, 2015, with all other variables remaining constant.

in € thousands 2016 2015

-0.50% +0.50% -0.50% +0.50%

Euro (Euribor) (143) 143 (169) 169

US dollar (Libor) (75) 75 (83) 83

Total (218) 218 (252) 252

20

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

The potential effects reported above were calculated by taking the liabilities which represent the most

significant part of the Group’s borrowings at the reference date and calculating, on that amount, the potential

impact of a change in the interest rates on an annual basis.

The liabilities in this analysis include variable-rate financial payables and receivables, cash and cash

equivalents and derivative financial instruments whose value is affected by changes in interest rates.

Credit risk

Credit risk is associated with trade receivables, cash and cash equivalents, financial instruments, deposits at

banks and other financial institutions and is defined as the risk that a counterparty does not fulfill the

obligations associated with a financial instrument or a commercial contract, thus resulting in a financial loss.

The credit risk related to trading counterparties is managed by the individual subsidiaries and monitored

centrally by the corporate Administration, Finance and Control Function. The Intercos Group does not have

significant concentrations of credit risk. However, there are policies in place to ensure that sales of products

and services are made to customers with a high degree of creditworthiness, taking into consideration their

financial position, past experience and other factors. Credit limits for major customers are based on internal

and external valuations according to ceilings approved by management in the individual countries. The use

of credit limits is monitored periodically at a local level. It should be noted that at the end of the year 2016,

the Group, for the subsidiary Intercos Europe S.p.A., sold receivables that are not past due under non-

recourse factoring contracts for €7,247 thousand.

As for credit risk relating to the management of financial resources and cash, the risk is monitored by the

Administration, Finance and Control Function of the Group which has policies in place to ensure that the

companies of the Group enter into transactions with independent high-credit-quality counterparties.

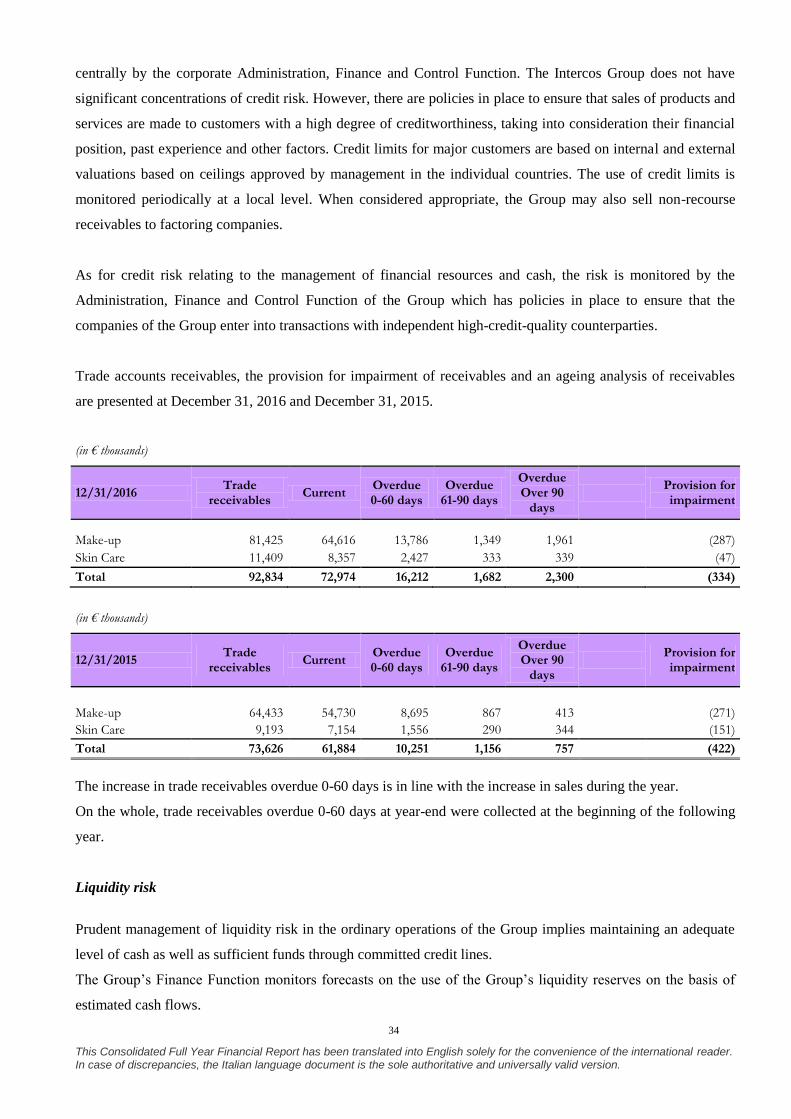

Trade accounts receivables, the provision for impairment of receivables and an ageing analysis of receivables

are presented at December 31, 2016 and December 31, 2015.

(in € thousands)

12/31/2016 Trade

receivables Current

Overdue 0-60 days

Overdue 61-90 days

Overdue over 90

days

Provision for impairment

Make-up 81,425 64,616 13,786 1,349 1,961

(287)

Skin Care 11,409 8,357 2,427 333 339

(47)

Total 92,834 72,974 16,212 1,682 2,300

(334)

21

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

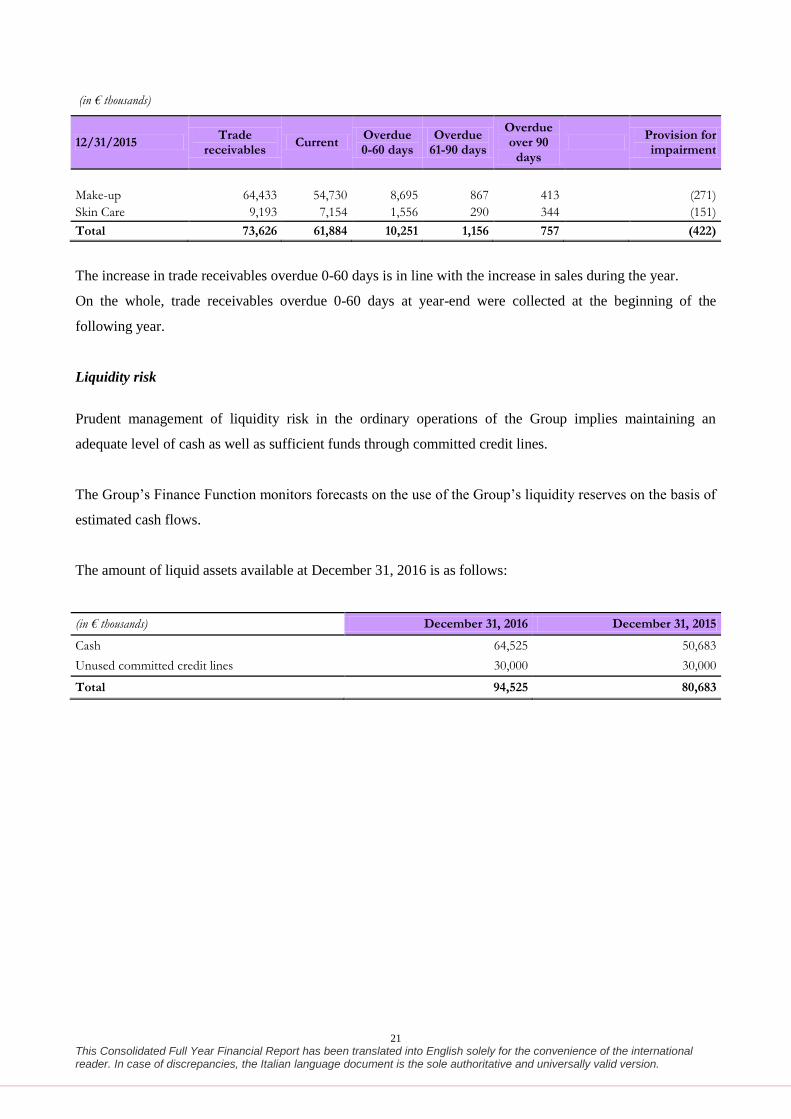

(in € thousands)

12/31/2015 Trade

receivables Current

Overdue 0-60 days

Overdue 61-90 days

Overdue over 90

days

Provision for impairment

Make-up 64,433 54,730 8,695 867 413

(271)

Skin Care 9,193 7,154 1,556 290 344

(151)

Total 73,626 61,884 10,251 1,156 757

(422)

The increase in trade receivables overdue 0-60 days is in line with the increase in sales during the year.

On the whole, trade receivables overdue 0-60 days at year-end were collected at the beginning of the

following year.

Liquidity risk

Prudent management of liquidity risk in the ordinary operations of the Group implies maintaining an

adequate level of cash as well as sufficient funds through committed credit lines.

The Group’s Finance Function monitors forecasts on the use of the Group’s liquidity reserves on the basis of

estimated cash flows.

The amount of liquid assets available at December 31, 2016 is as follows:

(in € thousands) December 31, 2016 December 31, 2015

Cash 64,525 50,683

Unused committed credit lines 30,000 30,000

Total 94,525 80,683

22

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

The following tables present an analysis of the maturities of borrowings and other liabilities. Borrowings

from banks in the following tables are presented at their nominal amount:

(in € thousands) Within 1 year

1 to 5 years

Beyond 5 years

At December 31, 2016

Bonds - - 120,000 120,000

Borrowings from banks and other lenders - m-l/term 4,135 38,989 0 43,124

Finance leases payable 256 913 0 1,169

Medium/long-term debt 4,391 39,903 120,000 164,294

Borrowings from banks and other lenders - s/term 26,372 1,507 4,186 32,066

Factoring companies payable 253 0 0 253

Trade payables 89,846 0 0 89,846

Short-term debt 116,471 1,507 4,186 122,165

Total 120,863 41,410 124,186 286,459

(in € thousands) Within

1 year 1 to

5 years Beyond 5

years At

December 31, 2015

Bonds - - 120,000 120,000

Borrowings from banks and other lenders - m-l/term 6,335 42,525 - 48,860

Finance leases payable 239 700 - 939

Medium/long-term debt 6,574 43,225 120,000 169,799

Borrowings from banks and other lenders - s/term 19,131 - - 19,131

Factoring companies payable 199 - - 199

Trade payables 69,456 - - 69,456

Short-term debt 88,786 - - 88,786

Total 95,360 43,225 120,000 258,585

23

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

In order to complete the disclosure on financial risks, a reconciliation is presented below between the

categories of financial assets and liabilities as identified in the statement of financial position format of the

Group and the categories of assets and liabilities identified in accordance with the requirements of IFRS7.

(in € thousands)

12/31/2016

Financial assets at fair

value through profit or loss

Receivables and loans

Available-for-sale financial

assets

Held-to-maturity

assets

Financial liabilities at fair value through

profit or loss

Other liabilities at amortized

cost

Hedging derivatives

Available-for-sale financial assets

- - - - - - -

Derivatives (assets) - - - - - - -

Securities held for trading - - - - - - -

Trade receivables - 92,834 - - - - -

Other receivables (*) - 2,925 - - - - -

Borrowings from banks and other lenders

- - - - - 197,360 -

Trade payables - - - - - 89,846 -

Other payables (*) - - - - - 21,385 -

Derivatives (liabilities) - - - - - - 447

Total - 95,760 - - - 308,951 447

(in € thousands)

12/31/2015

Financial assets at fair

value through profit or loss

Receivables and loans

Available-for-sale financial

assets

Held-to-maturity

assets

Financial liabilities at fair value

through profit or loss

Other liabilities at

amortized cost

Hedging derivatives

Available-for-sale financial assets

- - - - - - -

Derivatives (assets) - - - - - - -

Securities held for trading - - - - - - -

Trade receivables - 73,626 - - - - -

Other receivables (*) - 6,494 - - - - -

Borrowings from banks and other lenders

- - - - - 199,279 -

Trade payables - - - - - 69,456 -

Other payables (*) - - - - - 20,063 -

Derivatives (liabilities) - - - - - - 586

Total - 80,120 - - - 288,798 586

(*) Other receivables and Other payables exclude items of a tax nature which do not meet the definition of financial assets or liabilities.

24

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

Derivatives

IFRS require the fair value categorization of derivative financial instruments within the fair value hierarchy

based on inputs that are observable in the market or other financial parameters (e.g. interest rate, exchange

rate curves, etc.). Derivatives in foreign currency to hedge exchange rate risk fall under Level 2 of the fair

value hierarchy since the fair value of these instruments is determined by recalculating the present value at

the official year-end rate for exchange rates and interest rates quoted in the market.

The following table illustrates the fair value of the financial instruments portfolio:

Fair value hierarchy at the reporting date

(in € thousands) December 31, 2016

Level 2 December 31, 2015

Level 2

Assets Currency forwards / swaps/ options

Fair value hedge - -

Liabilities Currency forwards / swaps/ options

Fair value hedge 447 586

Fair value hedges are used to hedge exchange rate risk on financial assets and liabilities recorded in the

financial statements.

With reference to derivatives to hedge exchange rate risk, an indication is given below of the estimated dates

of flows in US dollars.

Notional amount in thousands of USD

December 31, 2016 December 31, 2015

Due Collection Payment Collection Payment

Within 1 year 17,500 - 24,000 -

1 to 5 years - - - -

Beyond 5 years - - - -

Total 17,500 - 24,000 -

25

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

12. Environmental Analysis

The environmental impact on the territory by the Group’s production process, especially in terms of the

disposal of expired cosmetics and waste, is duly managed with the assistance of an outside services and

environmental technologies company.

Matters associated with safety at work and protection and safeguarding of the environment are always of

major concern to the Intercos Group. The activities conducted in these areas ensured that, during the year

2016, there were no cases of accidents at work causing serious injury to employees, or charges of harming

the environment.

13. Tax Consolidation

Intercos S.p.A. has adhered to the national tax consolidation procedure under articles 117-129 of T.U.I.R. as

the “consolidating” company since 2008, valid for a three-year period, with Intercos Europe S.p.A. and

Marketing Projects S.r.l. as the “consolidated” companies. The option was also renewed for the period 2011-

2013 and the period 2014-2016. The companies participating in the national tax consolidation procedure are,

besides the parent, Intercos Europe S.p.A., Marketing Projects S.r.l. in liquidation, Ager S.r.l., Vitalab S.r.l.,

Drop Nail S.r.l. and Kit Productions S.r.l.

Each of these companies transfers its taxable income or tax loss to Intercos S.p.A. which records a receivable

(equal to the IRES tax to be paid) from the companies which contribute a taxable income, or a payable to the

companies which transfer a tax loss.

Intercos S.p.A., as the consolidating company, is responsible not only for any additional taxes assessed and

the relative fines and interest referring to its own individual total income, but also for the sums which could

become due, with reference to the consolidated tax return, from “formal control” activities pursuant to ex art.

36-ter DPR 600/73. It is also liable, jointly and severally, for the sums due in relation to fines levied on

companies in the consolidated tax return which have committed violations in determining the individual

position. Similarly, the consolidated companies are jointly and severally liable with Intercos S.p.A., as the

consolidating company, for higher taxes assessed relating to the consolidated tax return referring to

adjustments to the income in its tax return, also as a result of “formal control” activities, pursuant to ex art.

36-ter DPR 600/73. All of this is governed by the Tax consolidation agreement originally signed on June 5,

2008 and subsequent updates, the last of which is dated October 1, 2014.

26

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

14. Share Capital

Share capital at December 31, 2016 is unchanged compared to December 31, 2015, amounts to €10,710,193

and is represented by 91,319,870 no par value ordinary shares divided as follows:

51,624,356 Class A shares,

39,267,544 Class B shares,

427,970 Class C shares,

Class A, Class B and Class C shares all have the same rights and can be transferred by acts between living

persons and by succession due to death, with effect on Intercos S.p.A. pursuant to law, without prejudice to

article 5 of the bylaws.

The following table presents the situation at December 31, 2016:

At December 31, 2016 At December 31, 2015 At December 31, 2014

Class A shares - number 51,624,356 51,624,356 51,624,356 Class B shares - number 39,267,544 39,267,544 39,267,544 Class C shares - number 427,970 427,970 427,970

Total share capital in euros 10,710,193 10,710,193 10,710,193

In observance of the provisions of art. 2428 of the Italian Civil Code, note should be taken that the

subsidiaries neither hold nor have purchased or sold shares of the parent during the course of the year under

examination, not even through fiduciaries or trustees.

27

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

15. Subsequent Events

There were no events subsequent to the date of the financial statements which, if previously known, would

have required an adjustment to the financial statements.

As for developments in the early months of 2017, a description of significant subsequent events is presented

below:

In January and February 2017, the parent negotiated, with a syndicate of banks composed of

Banca IMI S.p.A., IntesaSanpaolo S.p.A., Unicredit S.p.A., BNL S.p.A. and ICBC (Europe) SA –

Milan Branch, certain amendments to the loan contract signed on March 24, 2015 by the company,

Intercos Europe S.p.A., Banca IMI S.p.A. and Unicredit S.p.A., the total amount of which, after such

amendments, will nevertheless remain at €80,000,000. More specifically, the amendments refer to:

a) an increase in the amount of the Term Facility from €50,000,000 to €60,000,000, with BNL

S.p.A. entering the loan contract as a lender of such Term Facility, with a commitment of

€20,000,000; b) a reduction in the amount of the Revolving Facility from €30,000,000 to

€20,000,000, with ICBC (Europe) SA – Milan Branch entering the loan contract as the sole lender of

such Revolving Facility, with a commitment of €20,000,000; c) an amendment to move the due date

on the Term Facility to December 31, 2021; d) a new interest rate per year for the Term Facility,

equal to the 6-month Euribor (and 6-month Libor for the tranche in U.S. dollars), plus 150 basis

points; e) a new interest rate per year for the Revolving Facility, equal to the 6-month Euribor or the

3-month Euribor, plus 100 basis points; f) a commitment fee of the Revolving Facility equal to 25

basis points; and g) an amendment to the definition of Permitted Indebtedness.

Also in January and February 2017, the parent negotiated the amendments to certain terms and

conditions of the €120,000,000 non-convertible bonds due March 28, 2022 with a 3.875% fixed rate

per year, the issue of which was approved by the board of directors on February 19, 2015. More

specifically, the amendments refer to: a) the reduction in the interest rate from 3.875% to 3.25% per

year; b) the amendment to move the maturity date to March 28, 2023; c) the extension of the period

– from March 28, 2018 to March 28, 2020 (excluded) – in which the bonds can be repaid in advance

by paying only the so-called “Make Whole Amount”; and d) the recalculation of the reimbursement

cost of the bonds, establishing that, in the event of repayment between March 28, 2020 and March

27, 2021 (included), the cost will be 101% of the face value of the bonds (instead of 100% as

28

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

currently established for the same period) whereas in the event of repayment between March 28,

2021 and the new maturity date of the bonds, the cost will be equal to the face value of the bonds as

currently established.

In February 2017, Intercos Asia Pacific increased its investment in the share capital of the

subsidiary Shinsegae Intercos Korea by Korean Won 2,500,000 thousand. The shareholder

Shinsegae also increased its investment in the company’s share capital so that its percentage

investment in capital would remain unchanged.

16. Information regarding Policies or Factors of a governmental, economic, fiscal, monetary or

political Nature that have had or could have, directly or indirectly, significant Repercussions

on the Activities of the Group

During the year to which the foregoing reported financial information and results refer, the activities of the

Group have not been affected in a substantive manner by policies or factors of a governmental, economic,

fiscal, monetary or political nature.

17. Outlook for 2017

A substantially positive outlook is expected for the year 2017, in effect confirming the Group’s expectations

as illustrated in its Business Plan.

Milan, March 27, 2017 INTERCOS S.p.A.

On behalf of the Board of Directors

___________________________

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

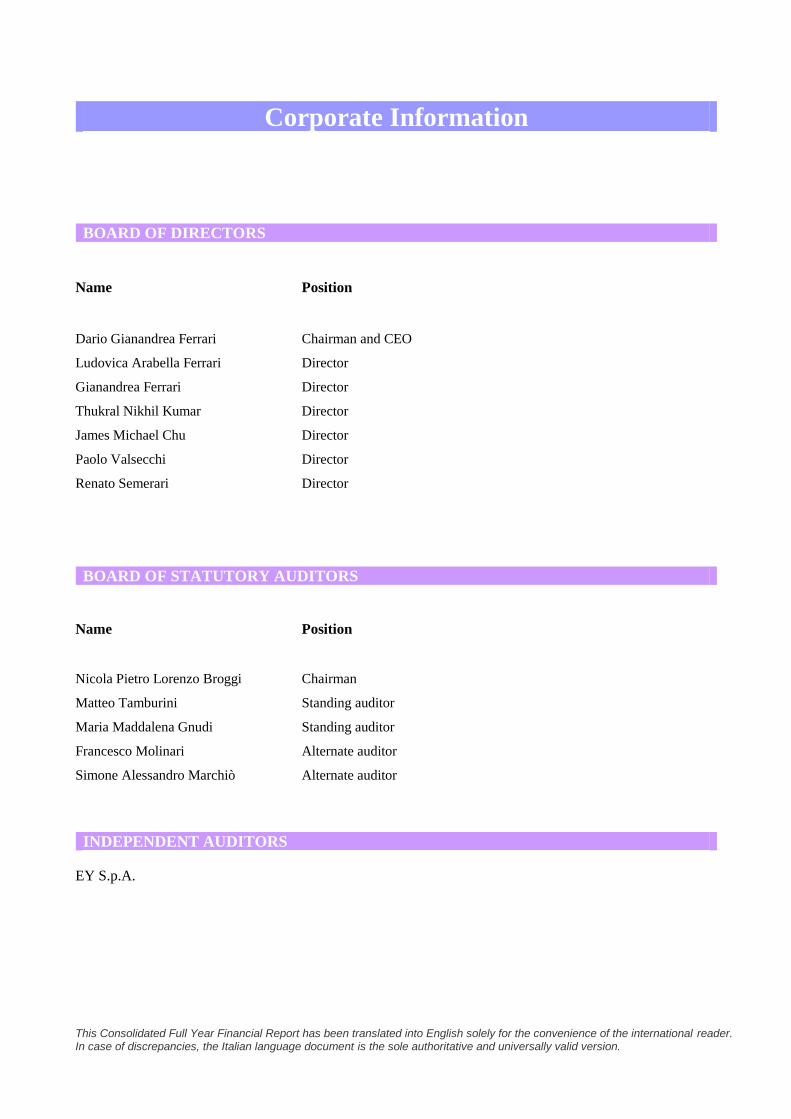

Corporate Information

BOARD OF DIRECTORS

Name Position

Dario Gianandrea Ferrari Chairman and CEO

Ludovica Arabella Ferrari Director

Gianandrea Ferrari Director

Thukral Nikhil Kumar Director

James Michael Chu Director

Paolo Valsecchi Director

Renato Semerari Director

BOARD OF STATUTORY AUDITORS

Name Position

Nicola Pietro Lorenzo Broggi Chairman

Matteo Tamburini Standing auditor

Maria Maddalena Gnudi Standing auditor

Francesco Molinari Alternate auditor

Simone Alessandro Marchiò Alternate auditor

INDEPENDENT AUDITORS

EY S.p.A.

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

2

Consolidated Statement of Financial Position at December 31, 2016

(in € thousands) Note December 31, 2016 December 31, 2015

NON-CURRENT ASSETS

Property, plant and equipment 7 96,806 98,254

Intangible assets 8 24,509 22,075

Goodwill 9 76,765 76,677

Investments 2 4,697 1,408

Deferred tax assets 10 16,768 16,603

Other non-current assets 11 7,241 6,229

Non-current assets

226,788 221,245

CURRENT ASSETS

Inventories 12 83,296 69,884

Trade receivables 13 92,834 73,626

Other current assets 14 9,301 14,503

Cash and cash equivalents 15 64,525 50,683

Current assets 249,957 208,695

TOTAL ASSETS 476,745 429,941

EQUITY

Share capital

10,710 10,710

Other reserves

66,005 66,005

Retained earnings

58,424 38,857

Equity attributable to owners of the parent

135,139 115,572

Equity attributable to non-controlling interests 2,354 2,819

TOTAL EQUITY 16 137,493 118,391

LIABILITIES

NON-CURRENT LIABILITIES

Borrowings from banks and other lenders 17 163,063 168,959

Provisions 18 1,079 2,777

Deferred tax liabilities 19 8,459 9,079

Other non-current liabilities

182 165

Employee benefit obligations 20 8,621 8,379

Non-current liabilities

181,403 189,359

CURRENT LIABILITIES

Borrowings from banks and other lenders 17 33,667 29,761

Other financial payables 17 631 560

Trade payables 21 89,846 69,456

Other current liabilities 22 33,704 22,415

Current liabilities 157,848 122,192

TOTAL EQUITY AND LIABILITIES 476,745 429,941

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

3

Consolidated Income Statement and Consolidated Statement of Comprehensive Income for the year ended December 31, 2016

CONSOLIDATED INCOME STATEMENT

(in € thousands) Note 2016 2015

Revenues 23 448,690 401,767

Cost of sales 24 (342,446) (302,852)

Industrial gross margin

106,244 98,915

Research & Development and innovation costs 25 (26,052) (25,248)

Selling expenses 26 (20,579) (18,944)

General and administrative expenses 27 (22,939) (19,978)

Other operating income (expenses)

4,998 3,636

Result from investments (operating) 30 (978) -

Nonrecurring income (expenses) 28 638 (1,083)

Operating profit (EBIT)

41,331 37,297

Financial income 29 7,923 9,985

Financial expenses 29 (17,735) (22,573)

Result from investments (financial) 30 263 106

Profit before tax (EBT)

31,782 24,815

Income taxes 31 (11,968) (10,011)

Profit for the year 19,814 14,804

Attributable to: - owners of the parent 19,514 14,701

- non-controlling interests 300 103

Earnings per share: Basic and diluted 33 0.22 0.16

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

(in € thousands)

2016 2015

Net profit 19,814 14,804

Other comprehensive income that will not be reclassified subsequently to the income statement, net of tax effect - Actuarial gains (losses) on remeasurement of employee defined benefit plans 20 (39) 396

- Tax effect 10/19 132 (113)

Total 93 283

Other comprehensive income that will be reclassified subsequently to the income statement, net of tax effect - Exchange differences on translating foreign operations 16 312 5,926

Total 312 5,926

Comprehensive income for the year 20,219 21,013

attributable to:

- owners of the parent 20,058 20,792

- non-controlling interests 161 220

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

4

Consolidated Statement of Changes in Equity at December 31, 2016

( in € thousands) Equity attributable to owners of the parent Equity attributable to

non-controlling interests Total

Description Share capital

Other reserves (Share premium

reserve)

Reserves and retained earnings

Profit for the year

Share capital

Profit (Loss) for the year

Balances at January 1, 2016 10,710 66,005 18,065 20,792 2,599 220 118,391

Appropriation of 2015 profit - - 20,792 (20,792) 220 (220) -

Exchange differences on translating foreign operations

- - - 452 - (140) 312

Other comprehensive income, net of tax effect

- - - 92 - 1 93

Consolidation reserve - - (491) - (626) - (1,117)

Profit for the year - - - 19,514 - 300 19,814

Balances at December 31, 2016 10,710 66,005 38,366 20,058 2,193 161 137,493

Consolidated Statement of Changes in Equity at December 31, 2015

(in € thousands) Equity attributable to owners of the parent Equity attributable to non-controlling

interests Total

Description Share capital

Other reserves (Share premium reserve)

Reserves and retained earnings

(accumulated losses)

Profit for the

year

Share capital

Profit (Loss) for the

year

Balances at January 1, 2015 10,710 66,005 4,191 13,883 2,143 (78) 96,854

Appropriation 2014 profit - - 13,883 (13,883) (78) 78 -

Exchange differences on translating foreign operations

- - - 5,827 - 99 5,926

Increase in capital of non-controlling interests

- - - - 165 - 165

Other comprehensive income, net of tax effect

- - - 265 - 18 283

Consolidation reserve - - (9) - 369 - 360

Profit for the year - - - 14,701 - 103 14,804

Balances at December 31, 2015 10,710 66,005 18,065 20,792 2,599 220 118,391

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

5

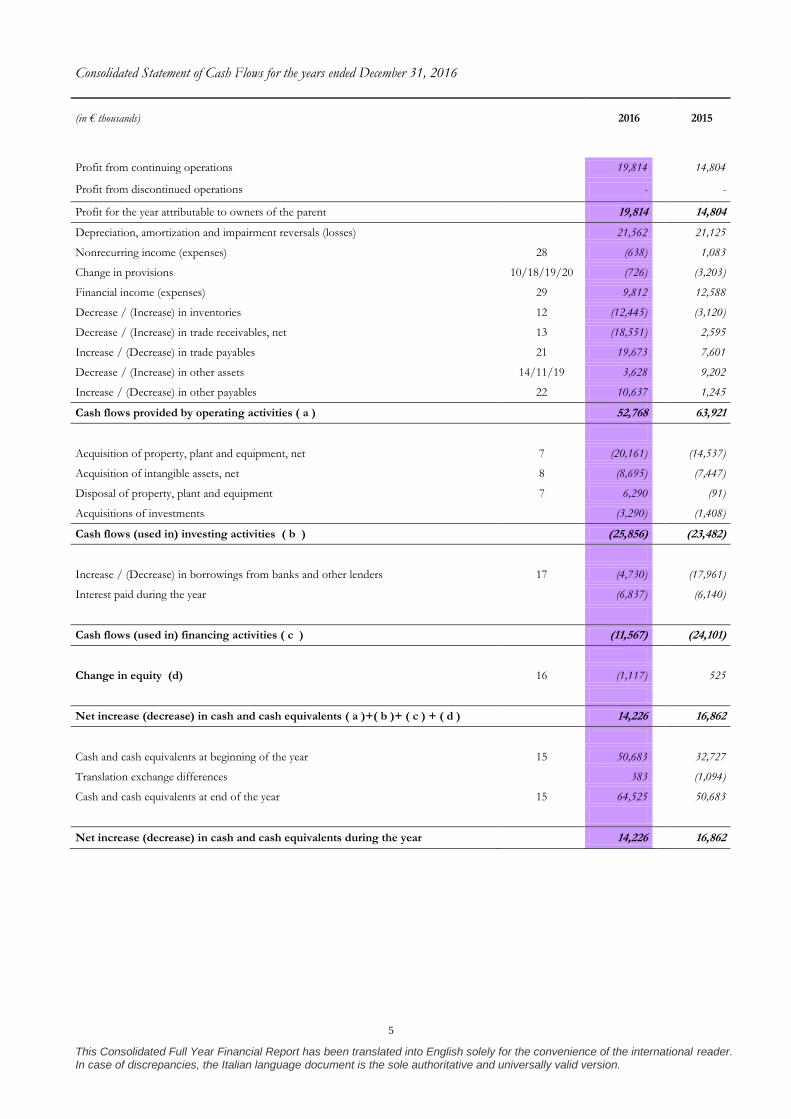

Consolidated Statement of Cash Flows for the years ended December 31, 2016

(in € thousands) 2016 2015

Profit from continuing operations

19,814

14,804

Profit from discontinued operations

-

-

Profit for the year attributable to owners of the parent

19,814 14,804

Depreciation, amortization and impairment reversals (losses)

21,562

21,125

Nonrecurring income (expenses) 28 (638)

1,083

Change in provisions 10/18/19/20 (726)

(3,203)

Financial income (expenses) 29 9,812

12,588

Decrease / (Increase) in inventories 12 (12,445)

(3,120)

Decrease / (Increase) in trade receivables, net 13 (18,551)

2,595

Increase / (Decrease) in trade payables 21 19,673

7,601

Decrease / (Increase) in other assets 14/11/19 3,628

9,202

Increase / (Decrease) in other payables 22 10,637

1,245

Cash flows provided by operating activities ( a )

52,768 63,921

Acquisition of property, plant and equipment, net 7 (20,161)

(14,537)

Acquisition of intangible assets, net 8 (8,695)

(7,447)

Disposal of property, plant and equipment 7 6,290

(91)

Acquisitions of investments

(3,290)

(1,408)

Cash flows (used in) investing activities ( b )

(25,856)

(23,482)

Increase / (Decrease) in borrowings from banks and other lenders 17 (4,730)

(17,961)

Interest paid during the year

(6,837)

(6,140)

Cash flows (used in) financing activities ( c )

(11,567) (24,101)

Change in equity (d) 16 (1,117)

525

Net increase (decrease) in cash and cash equivalents ( a )+( b )+ ( c ) + ( d )

14,226 16,862

Cash and cash equivalents at beginning of the year 15 50,683

32,727

Translation exchange differences

383

(1,094)

Cash and cash equivalents at end of the year 15 64,525

50,683

Net increase (decrease) in cash and cash equivalents during the year

14,226 16,862

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

6

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

1. General information

Group structure

Intercos S.p.A. is a corporation organized under the laws of the Republic of Italy, with its registered office in

Milan, Piazza Diaz 1.

Starting from the end of 2013, the Group’s business was reorganized and is now aggregated into two areas

identified on the basis of the following operating segments:

Make-Up Business Unit: specialized in the creation, development, manufacture and marketing of

powders, emulsions, lipsticks and types of cosmetics using delivery systems in the form of pens/pencils

for the face, eyes and lips

Skin Care Business Unit: specialized in the manufacture and marketing of cosmetic and skin care

creams.

The Group’s main manufacturing facilities are at the plant sites in Italy, America, Switzerland, China and

Brazil.

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

7

The Group’s organization structure is updated to the closing date of the consolidated financial statements at

December 31, 2016 and shows the operating companies and those in liquidation.

100% 100% 100%

65% 99.7% 0.3% 100%

100% 100% 76%

100% 75.01% 70%

100% 100% 100%

20% 100% 100% 100% 50%

100%

Intercos Technology (SIP)

Co., Ltd

(P.R. China)

Hana Co. Ltd.

(South Korea)

Intercos Daily Product

(SIP) Co. Ltd.

(P.R. China)

Intercos Cosmetics (Suzhou)

Co., Ltd

(P.R. China)

Intercos S.p.A.

(Italy)

Intercos Paris S.à r.l.

(France)

Intercos UK Ltd

(United Kingdom)

Intercos Marketing Ltd

(United Kingdom)

Kit Productions S.r.l.

(Italy)

Marketing Projects S.r.l. in a

wind-up

(Italy)

Intercos America Inc.

(United States of America)

Intercos do Brasil Indústria e

Comércio de Productos

Cosméticos LTDA

(Brazil)

CRB S.A.

(Switzerland)

Vitalab S.r.l.

(Italy)

CRB Benelux Bv

(The Netherlands)

Intercos Concept S.r.l.

(Italy)

Intercos Asia Pacific Limited

(Hong Kong)

Intercos Europe S.p.A.

(Italy)

Drop Nail S.r.l.

(Italy)

Ager S.r.l.

(Italy)

Shinsegae Intercos Korea Inc.

(South Korea)

Interfila Cosmetics

(Shanghai) Co., Ltd

(P.R. China)

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

8

2. Significant accounting policies

Basis of preparation

The consolidated financial statements for the year ended December 31, 2016 of the Intercos Group consist of

the statement of financial position, the income statement, the statement of comprehensive income, the

statement of changes in equity, the statement of cash flows and the notes thereto. All amounts in the notes are

expressed in thousands of euros, unless otherwise indicated.

The format of the income statement, as permitted by IAS 1, presents a format by function showing revenues

and cost of sales, which is considered to be a better representation of the economic and financial performance

of the Group.

The consolidated financial statements at December 31, 2016 have been prepared in accordance with

International Financial Reporting Standards (“IFRS”), issued by the International Accounting Standards Board

(“IASB”), and adopted by the European Commission for the preparation of the consolidated and separate

financial statements of companies with equity securities and/or debt listed on one of the regulated markets in the

European Union.

By IFRS is meant all “International Financial Reporting Standards”, all International Accounting Standards

(“IAS”), all interpretations of the International Financial Reporting Interpretations Committee (“IFRIC”),

formerly the Standing Interpretations Committee (“SIC”), adopted by the European Union and contained in the

relative European Union Regulations published up to the date on which the board of directors of Intercos S.p.A.

approved the draft consolidated financial statements of the Group. Any future guidance and updated

interpretations will be adopted in subsequent years in the manner established each time by the benchmark

accounting standards.

The consolidated financial statements were approved for publication by the board of directors on March 27,

2017.

New accounting standards, interpretations and amendments adopted by the Group

The accounting principles adopted in the preparation of the consolidated financial statements at December 31,

2016 are consistent with those applied in the prior year, except for the adoption of recently issued standards,

interpretations and amendments in effect from January 1, 2016, as listed below.

On January 9, 2015 the Regulations 2015/28 and 2015/29 were published in the Official Journal of the European

Union. They were both issued by the European Commission on December 17, 2014, endorsing (i) “Annual

Improvements to IFRS 2010-2012 Cycle” and (ii) the amendments to IAS 19 entitled “Defined Benefit Plans:

Employee Contributions (Amendments to IAS 19)”.

This Consolidated Full Year Financial Report has been translated into English solely for the convenience of the international reader. In case of discrepancies, the Italian language document is the sole authoritative and universally valid version.

9

The improvements contained in the “Annual Improvements to IFRS 2010-2012 Cycle” refer to the following

amendments: (i) to IFRS 2, clarifying the definition of “vesting conditions” and introducing separate definitions

of service conditions and performance conditions; (ii) to IFRS 3, clarifying that obligations to pay contingent

consideration, other than those falling within the definition of equity instruments, are assessed at fair value at

every balance sheet date, with changes recognized in the income statement; (iii) to IFRS 8, requiring disclosure

about the judgments made by management in applying aggregation criteria, describing the operating segments

that were aggregated and the economic indicators that were assessed in order to determine that the aggregated

segments share similar economic characteristics; (iv) to IAS 16 and IAS 38, clarifying the manner of

determining the gross carrying amount of assets, in the event of revaluation as a result of application of the

revaluation model; (v) to IAS 24, establishing the information to be disclosed when a related-party management

entity provides key management personnel services to a reporting entity (or the parent).

Regulation 2015/2173. issued by the European Commission on November 24, 2015 endorsed the amendments

contained in the document “Accounting for Acquisitions of Interests in Joint Operations (Amendments to IFRS

11)”, issued by the IASB on May 6, 2014. The amendments clarify the accounting for the acquisition of both the

initial interest and additional interests in a joint operation (which does not modify the type of interest) in which

the activity constitutes a business, as defined in IFRS 3, which requires the application of all of the principles on

business combinations.

Regulation 2015/2231, issued by the European Commission on December 2, 2015, endorsed the amendments

contained in the document “Clarification of Acceptable Methods of Depreciation and Amortization