integrated pension journey planning: what does it really mean?

TRANSCRIPT

Integrated Pension Journey PlanningWhat does it really mean?

September 23, 2010

© 2010 Towers Watson. All rights reserved.

2towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Today’s Presenters

Matt Herrmann, Retirement Risk Management Group

Adam Levine, Towers Watson Investment Services

Jason Richards, Retirement Risk Management Group

3towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Today’s Discussion

Background on Journey Planning

The Role of Investment Strategy

The Role of Settlement Strategy

4towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

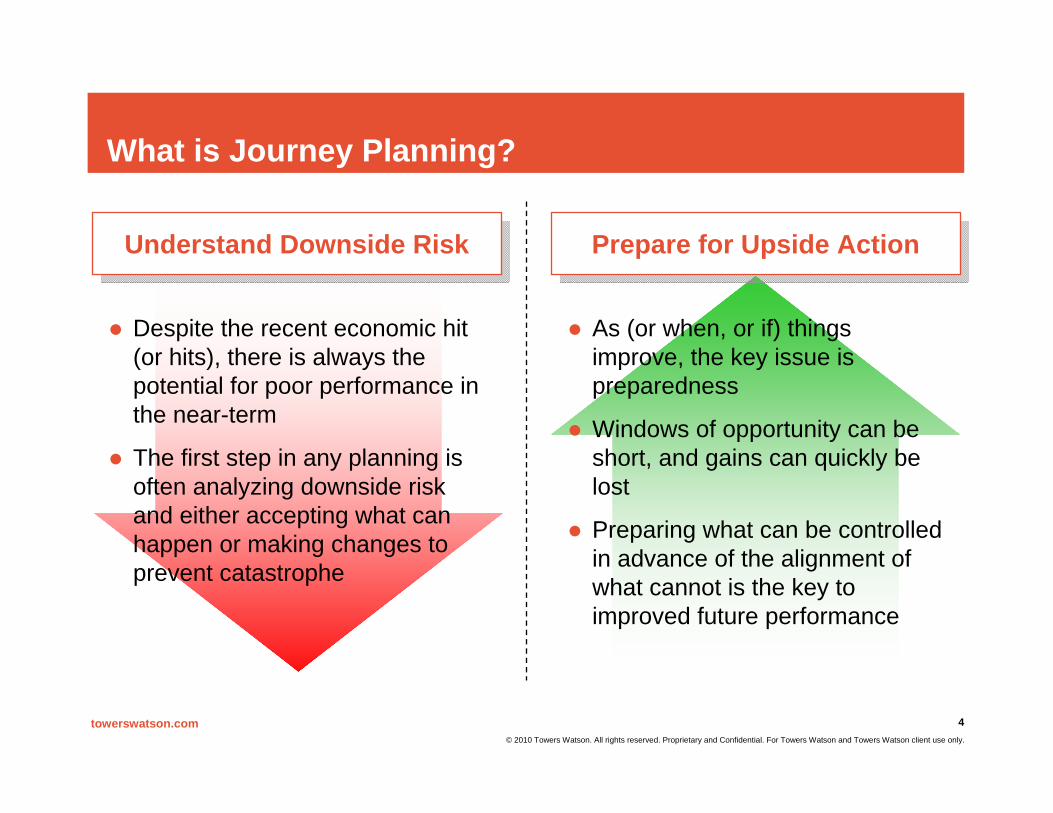

What is Journey Planning?

Understand Downside RiskUnderstand Downside Risk Prepare for Upside ActionPrepare for Upside Action

Despite the recent economic hit (or hits), there is always the potential for poor performance in the near-term

The first step in any planning is often analyzing downside risk and either accepting what can happen or making changes to prevent catastrophe

As (or when, or if) things improve, the key issue is preparedness

Windows of opportunity can be short, and gains can quickly be lost

Preparing what can be controlled in advance of the alignment of what cannot is the key to improved future performance

5towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

5

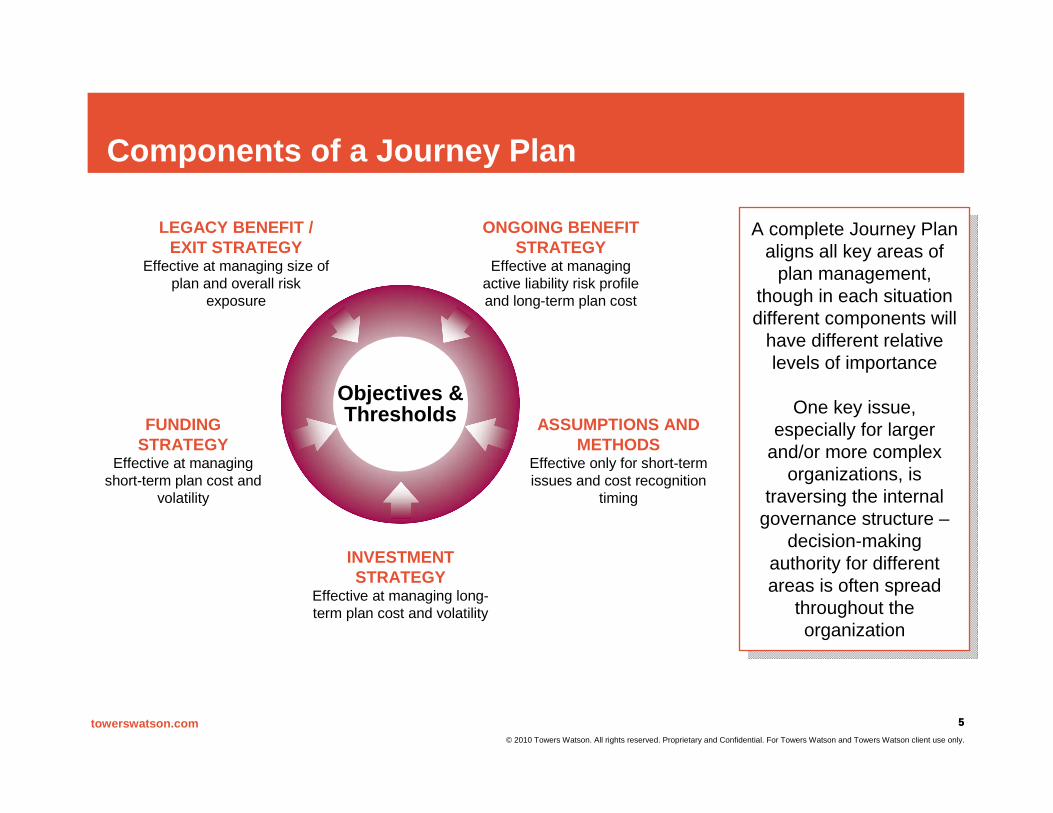

Components of a Journey Plan

Objectives & Thresholds

ONGOING BENEFIT STRATEGY

Effective at managing active liability risk profile and long-term plan cost

ASSUMPTIONS AND METHODS

Effective only for short-term issues and cost recognition

timing

INVESTMENT STRATEGY

Effective at managing long-term plan cost and volatility

FUNDINGSTRATEGY

Effective at managing short-term plan cost and

volatility

LEGACY BENEFIT / EXIT STRATEGY

Effective at managing size of plan and overall risk

exposure

A complete Journey Plan aligns all key areas of

plan management, though in each situation different components will

have different relative levels of importance

One key issue, especially for larger

and/or more complex organizations, is

traversing the internal governance structure –

decision-making authority for different areas is often spread

throughout the organization

A complete Journey Plan aligns all key areas of

plan management, though in each situation different components will

have different relative levels of importance

One key issue, especially for larger

and/or more complex organizations, is

traversing the internal governance structure –

decision-making authority for different areas is often spread

throughout the organization

6towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Past Opportunities

Towers Watson Pension Index

50

60

70

80

90

100

110

120

130

140

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

60.0 as of 8/31/10

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Strong funded status prior to 2002 would have allowed for numerous risk reduction options

Short recovery window in 2007 was available

Two week period during October 2008 showed annuity purchase rates near 8% in some instances

Decreasing rates leads to potential for lump sums in 2010 below projected year-end discount rates

Unwind dollar duration strategies after swap yields fall below Treasuries

7towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Marketplace Update

Termination/Immunization

Partialsettlement

Annuity products/LDI

Lump sums/ Dynamic allocations

5%6%14%47%EOY 20093%6%14%31%EOY 200830%53%80%95%EOY 2007

> 110%> 100%> 90%> 80 %Funded Status

Distribution of Funded Status of Large Plans by Year

Note: Average funded status dropped 10% + from EOY 2009 to June 30, 2010

8towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

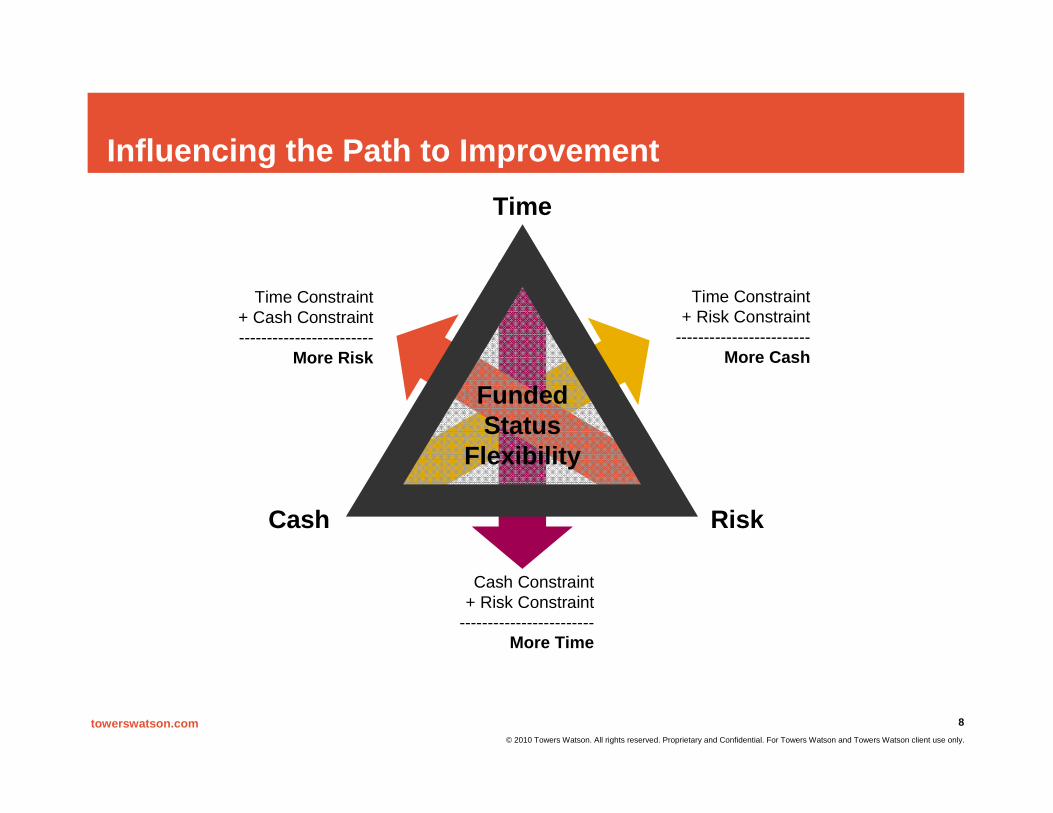

Influencing the Path to ImprovementTime

Cash Risk

Funded Status

Flexibility

Time Constraint+ Cash Constraint------------------------

More Risk

Time Constraint+ Risk Constraint

------------------------More Cash

Cash Constraint+ Risk Constraint

------------------------More Time

9towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Setting Objectives and Thresholds

Debt to Capitalization - Target Asset Allocation, Ongoing Plan

0% 10% 20% 30% 40% 50%

60% 70% 80% 90%

100%

2009 2010 2011 2012 2013 2014

5th-25th percentile 25th-50th 50th-75th 75th-95th Baseline Mean

Debt to Capitalization - Target Asset Allocation, Ongoing Plan

0% 10% 20% 30% 40% 50%

60% 70% 80% 90%

100%

2009 2010 2011 2012 2013 2014

5th-25th percentile 25th-50th 50th-75th 75th-95th Baseline Mean

Debt to Capitalization - Target Asset Allocation, Ongoing Plan

0% 10% 20% 30% 40% 50%

60% 70% 80% 90%

100%

2009 2010 2011 2012 2013 2014

5th-25th percentile 25th-50th 50th-75th 75th-95th Baseline Mean

Cat 4Cat 3

Cat 2Cat 1

$0

$100

$200

$300

$400

$500

2010 2011 2012 2013 2014 2015 2016 2017 2018

5th-25th percentile 25th-50th 50th-75th 75th-95th Mean

Debt to CapitalizationUnreimbursed Contributions – Utility Client

51%

31%

42%

38%

23%

0% 10% 20% 30% 40% 50% 60%

Probabi l i ty

Funded status exceeds 120%

Year over year change in contribution of more than 50%

Present value of cumulative contributions more than $100M

Funded status falls below 80% in any year after 2010

Contribution in any year more than $20M

Funded status exceeds 120%

Year over year change in contribution of more than 50%

Present value of cumulative contributions more than $100M

Funded status falls below 80% in any year after 2010

Contribution in any year more than $20M

Probability of Exceed Key Thresholds

Trapped SurplusThreshold

RestrictionThreshold

50%

75%

100%

125%

150%

175%

2008 2009 2010 2011 2012 2013 2014

Projection of Funded Status vs. Thresholds

10towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Combined: PV Total Cont + Deficit ($M) - 2019

$0

$500

$1,000

$1,500

$2,000

Target (No Shutdown) Settle at 110% Dynamic Allocation to Settlement

5th-25th percentile 25th-50th 50th-75th 75th-95th Mean

The Value of PreparednessImpactApproaches Being Considered

Settling obligations once 110% funded status is reached improvesboth expected cost and downside risk, essentially through significant reduction in asymmetric riskWhen coupled with the settlement strategy, the dynamic allocation does not have much of an impact on long-term costs (results are dependent on order analyzed)

Settling obligations once target funded status is reachedDynamically reducing equity exposure as plan funded status improves

11towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

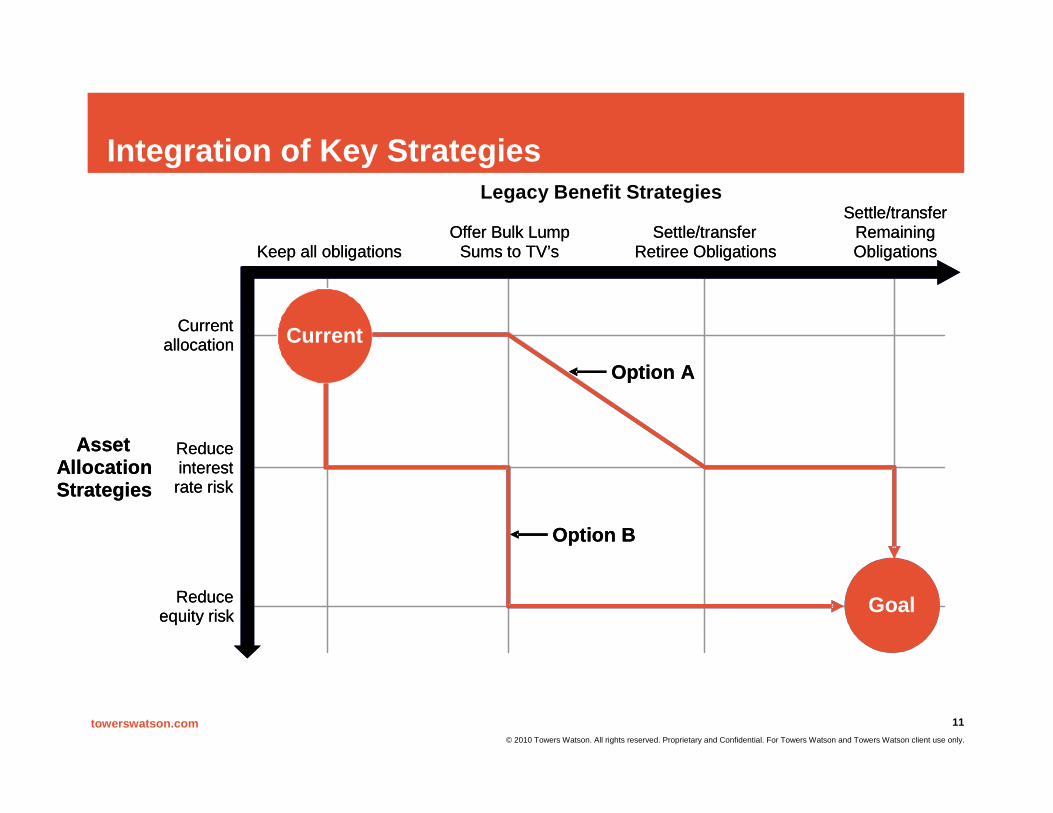

Integration of Key StrategiesLegacy Benefit Strategies

Asset Allocation Strategies

Current

Keep all obligationsOffer Bulk Lump

Sums to TV’sSettle/transfer

Retiree Obligations

Settle/transfer Remaining Obligations

Currentallocation

Reduce interest rate risk

Reduce equity risk Goal

Option A

Option B

Asset Allocation Strategies

Current

Keep all obligationsOffer Bulk Lump

Sums to TV’sSettle/transfer

Retiree Obligations

Settle/transfer Remaining Obligations

Currentallocation

Reduce interest rate risk

Reduce equity risk Goal

Option A

Option B

towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

12

The Role of Investment Strategy

13towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

1313

Dynamic StrategiesFu

nded

Rat

ioBond A

lloca

tion

One-Way Dynamic

Fund

ed R

atioBon

d Allo

catio

n

Two-Way Dynamic

Standard Approach

Funded Ratio

Bond Allocation

14towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

1414

Dynamic Strategy Options

Question Examples of ConsiderationsOne-way or two-way? Frozen or ongoing

Potential for surplus usageWhat is the speed and magnitude of allocation shifts?

Duration of liabilitiesAccrual ratesStarting funded statusStarting asset allocation

What is the end point? Frozen or ongoingDiversification benefitsImmunization versus settlement

15towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

1515

Dynamic Asset Allocations: Annual Funded RatioCombined: TL Funded Ratio

50%

75%

100%

125%

150%

175%

2010

40%F

I (LGC

)

Dyna

mic (

6%)

2011

40%F

I (LGC

)

Dyna

mic (

6%)

2012

40%F

I (LGC

)

Dyna

mic (

6%)

2013

40%F

I (LGC

)

Dyna

mic (

6%)

2014

40%F

I (LGC

)

Dyna

mic (

6%)

2015

40%F

I (LGC

)

Dyna

mic (

6%)

2016

40%F

I (LGC

)

Dyna

mic (

6%)

2017

40%F

I (LGC

)

Dyna

mic (

6%)

2018

40%F

I (LGC

)

Dyna

mic (

6%)

2019

40%F

I (LGC

)

Dyna

mic (

6%)

5th‐25th percentile 25th‐50th 50th‐75th 75th‐95th

The dynamic strategy has a significantly more noticeable impact on future funded ratios, specifically future deficits

In 2019, under the dynamic strategy the 5th percentile funded ratio is 95% versus 86% under the static 40% policy

16towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

1616

1. Securing Funded Status

2. Capitalizing on Yield Curve Movements

100%

80%

60%

Static Policy Dynamic PolicyTime

Dynamic Asset Allocations: Sources of Improvement

Long G/C Return = -6.5%

Long G/C Return = 14.8%

17

Dynamic Asset Allocations: Possible Glidepaths

0102030405060708090

100

60 70 80 90 100 110 120

Ret

urn

See

king

Allo

catio

n

Funded Ratio

Static Asset Allocation

0102030405060708090

100

60 70 80 90 100 110 120

Ret

urn

See

king

Allo

catio

n

Funded Ratio

Linear Dynamic Allocation

0102030405060708090

100

60 70 80 90 100 110 120

Retu

rn S

eeki

ng A

lloca

tion

Funded Ratio

Non- Linear Dynamic Allocations

0102030405060708090

100

60 70 80 90 100 110 120

Retu

rn S

eeki

ng A

lloca

tion

Funded Ratio

Possible Combinations

18

18.518.3

1.0 78

0.0 -0.6-15.1

$(323.4)

$(220.5)

69%

78%

50%

60%

70%

80%

90%

100%

(400)

(350)

(300)

(250)

(200)

(150)

(100)

(50)

0

50

100

Beginning Deficit

12/31/09

Equity Returns FI Returns / Change in

Discount Rate

Alternatives Returns

Cash Contributions

Benefit Payments

Plan Expenses/

Census Update

Service Cost Interest Cost Ending Deficit 2/28/2010

Fund

ed R

atio

Sup

lus/

Def

icit

base

d on

PP

A Li

abili

ties (

in $

mill

ions

)

2010 Year to Date - Funded Status On a dollar basis, the funded ratio has increased from ($323) to ($220) during 2010On a percentage basis, the funded ratio has increased to 78% as a result of:

Asset gains of ~$24M;A decrease in the liabilities of ~$17M; andA contribution of $78M

With the March 31 funded ratio of 78%, the plan has reached the 2nd trigger of the Journey Plan

The new target allocation to fixed income is 35% of assetsTo reach the new target allocation to fixed income, approximately $43M will need to be reallocated from equities

If the additional $120M contribution had been made on March 31, the Plan would have reached the 5th Journey Plan trigger

Target fixed income allocation would increase to 57.5%An additional $181M would need to be re-allocated to fixed income

18

Implementation of Dynamic Strategies: Sample Funded Status Monitoring

towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

19

The Role of Settlement Strategy

20towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

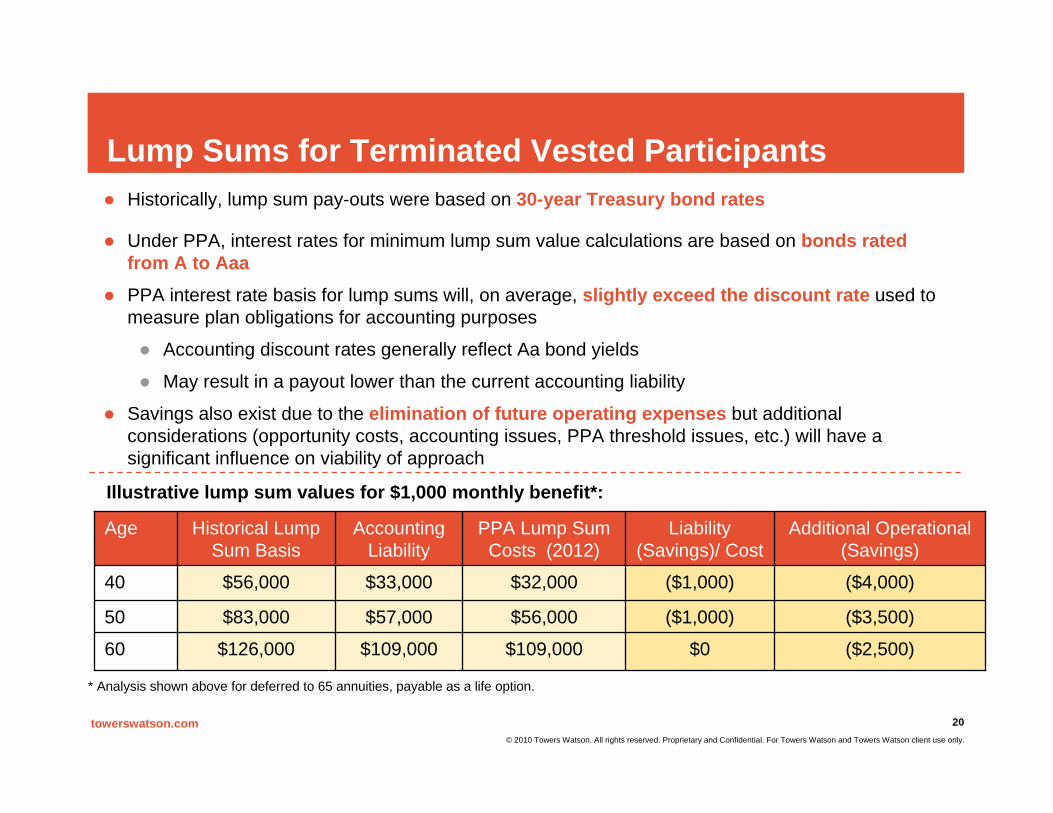

Lump Sums for Terminated Vested ParticipantsHistorically, lump sum pay-outs were based on 30-year Treasury bond rates

Under PPA, interest rates for minimum lump sum value calculations are based on bonds rated from A to AaaPPA interest rate basis for lump sums will, on average, slightly exceed the discount rate used to measure plan obligations for accounting purposes

Accounting discount rates generally reflect Aa bond yields

May result in a payout lower than the current accounting liability

Savings also exist due to the elimination of future operating expenses but additional considerations (opportunity costs, accounting issues, PPA threshold issues, etc.) will have a significant influence on viability of approach

$0

($1,000)

($1,000)

Liability (Savings)/ Cost

($2,500)

($3,500)

($4,000)

Additional Operational (Savings)

$126,000

$83,000

$56,000

Historical Lump Sum Basis

$109,000

$56,000

$32,000

PPA Lump Sum Costs (2012)

$109,00060

$57,00050

$33,00040

Accounting Liability

Age

Illustrative lump sum values for $1,000 monthly benefit*:

* Analysis shown above for deferred to 65 annuities, payable as a life option.

21towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

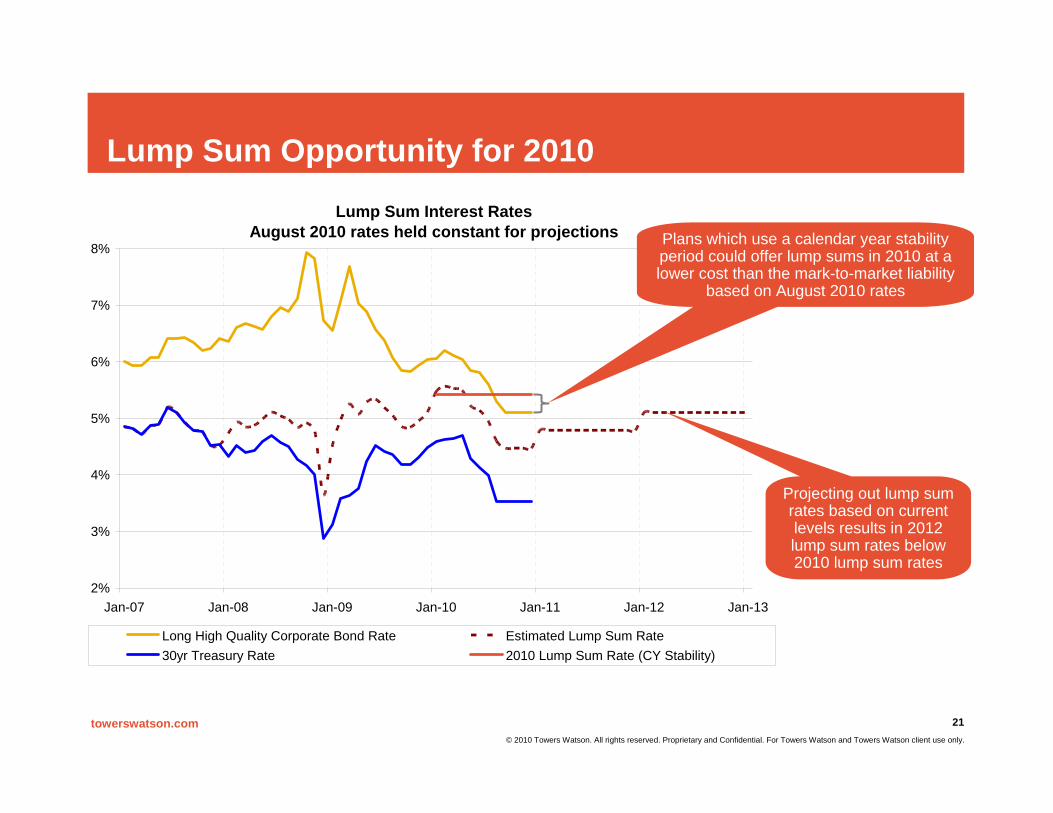

Lump Sum Interest RatesAugust 2010 rates held constant for projections

2%

3%

4%

5%

6%

7%

8%

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13

Long High Quality Corporate Bond Rate Estimated Lump Sum Rate30yr Treasury Rate 2010 Lump Sum Rate (CY Stability)

Lump Sum Opportunity for 2010

Plans which use a calendar year stability period could offer lump sums in 2010 at a lower cost than the mark-to-market liability

based on August 2010 rates

Projecting out lump sum rates based on current levels results in 2012 lump sum rates below 2010 lump sum rates

22towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Lump Sum Considerations

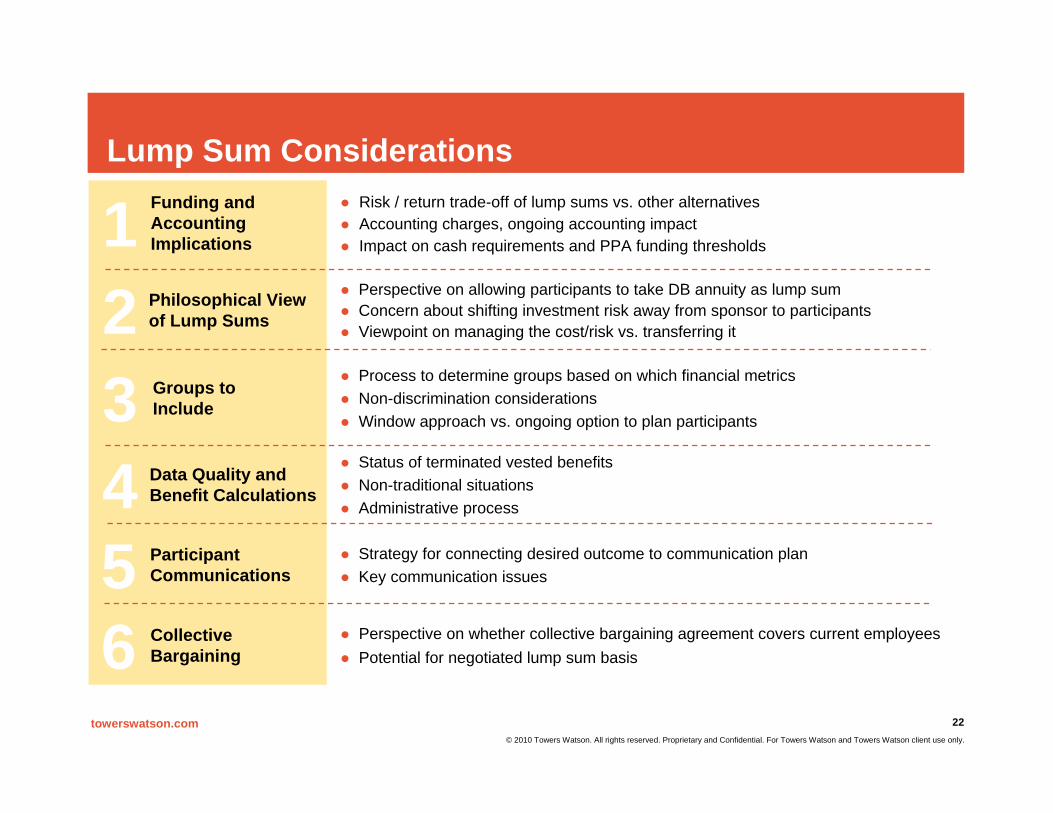

1234

Funding and AccountingImplications

Philosophical View of Lump Sums

Data Quality andBenefit Calculations

Risk / return trade-off of lump sums vs. other alternativesAccounting charges, ongoing accounting impactImpact on cash requirements and PPA funding thresholds

Perspective on allowing participants to take DB annuity as lump sumConcern about shifting investment risk away from sponsor to participantsViewpoint on managing the cost/risk vs. transferring it

Status of terminated vested benefitsNon-traditional situationsAdministrative process

Groups to Include

Process to determine groups based on which financial metricsNon-discrimination considerationsWindow approach vs. ongoing option to plan participants

5 Participant Communications

Strategy for connecting desired outcome to communication planKey communication issues

6 CollectiveBargaining

Perspective on whether collective bargaining agreement covers current employeesPotential for negotiated lump sum basis

23towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Annuity Purchase Background

Along with paying lifetime benefits (the default) and paying lump sums, an annuity purchase is the third primary mechanism plan sponsors have to fulfill their obligations

Key issues include:An annuity purchase does not require an affirmative election by participants (though collective bargaining issues should be considered)Annuity must maintain all protected provisions of the plan obligationAnnuities can only be purchased from insurers deemed among the “Safest Available”, as laid out in IRS Interpretive Bulletin 95-1Annuity pricing is driven by market interest rates and plan provisions, but is not a perfectly efficient market (e.g., subject to individual carrier situations)

24towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Annuity Purchase Marketplace Opportunities

2.0%2.5%3.0%3.5%4.0%4.5%5.0%5.5%6.0%6.5%7.0%7.5%8.0%8.5%9.0%

5/26

/200

86/

26/2

008

7/26

/200

88/

26/2

008

9/26

/200

810

/26/

2008

11/2

6/20

0812

/26/

2008

1/26

/200

92/

26/2

009

3/26

/200

94/

26/2

009

5/26

/200

96/

26/2

009

7/26

/200

98/

26/2

009

9/26

/200

910

/26/

2009

11/2

6/20

0912

/26/

2009

1/26

/201

02/

26/2

010

3/26

/201

04/

26/2

010

5/26

/201

06/

26/2

010

7/26

/201

0

Annuity Purchase Proxy Liability Rate Proxy 10Yr Treas 30Yr Treas Actual Transactions

Annuity purchase rates will vary with market interest rates, typically trending between corporate bond rates and Treasury rates

However, market inefficiencies and competitive pressures among insurers can create windows where annuity purchase rates reflect a much lower (or no) premium over liabilities

25towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Monitoring and Dynamic Triggers

Ongoing Accounting Implications

One-time Accounting Implications

Data Quality And Calculation Of Benefits

Regret Risk And Market Timing

Plan Value Transfer

Impact Of Operational Costs

Philosophical View Of Lump Sums

Basis For Lump Sum

YNParticipant Data Clean

TBD$5MEst. Buy-out Premium

YNLegal Due Diligence Complete

YNSafest Available Insurers Identified

TBD$22MEst. Accounting Settlement Charge

> 100 bps119 bpsSpread over 10-year Treasury Bond

Acceptable Funding Implications

Benefit Restrictions Apply

Est. Annuity Rates for Retirees

Key Statistic

YTBD

NTBD

> 6.00%4.50%

Trigger ReadinessDesired TriggerCurrent Measure

YNParticipant Data Clean

TBD$5MEst. Buy-out Premium

YNLegal Due Diligence Complete

YNSafest Available Insurers Identified

TBD$22MEst. Accounting Settlement Charge

> 100 bps119 bpsSpread over 10-year Treasury Bond

Acceptable Funding Implications

Benefit Restrictions Apply

Est. Annuity Rates for Retirees

Key Statistic

YTBD

NTBD

> 6.00%4.50%

Trigger ReadinessDesired TriggerCurrent Measure

YNCommunications developed

YNParticipants located / Data clean

> 6.00%5.75%Est. Discount Rate

> $0M-$1.3MEst. Lump Sum Gain / Loss

TBD$9MEst. Accounting Settlement Charge

= 0 bps-25 bpsSpread over Discount Rate

Acceptable Funding Implications

Benefit Restrictions Apply

Est. Lump Sum Rates

Key Statistic

YTBD

NTBD

> 6.00%5.50%

Trigger ReadinessDesired TriggerCurrent Measure

YNCommunications developed

YNParticipants located / Data clean

> 6.00%5.75%Est. Discount Rate

> $0M-$1.3MEst. Lump Sum Gain / Loss

TBD$9MEst. Accounting Settlement Charge

= 0 bps-25 bpsSpread over Discount Rate

Acceptable Funding Implications

Benefit Restrictions Apply

Est. Lump Sum Rates

Key Statistic

YTBD

NTBD

> 6.00%5.50%

Trigger ReadinessDesired TriggerCurrent Measure

Sample Annuity Purchase Dynamic Triggers

Sample Bulk Lump Sum Dynamic TriggersPotential Considerations – Bulk Lump Sums

Potential Considerations – Annuity Purchase

Market Capacity and Financial Services Industry

Plan Value Transfer

Compliance With 95-1

Data Quality and Administration

Ongoing Accounting Implications

One-time Accounting Implications

Components of Annuity Purchase Pricing

26towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Key Takeaways

Especially in the near-term, understanding downside risk may be as important as planning for upside risk reduction

Preparedness and adaptability are key

Non-financial issues need attention throughout the process

An integrated Journey Plan can add value if well aligned with corporate objectives

27towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

27

Contact Details

Matt Herrmann120 South Central Avenue, Suite 1400, St. Louis, MO 63105-1705314-290-1422

[email protected] Levine

335 Madison Avenue, New York, NY [email protected]

Jason Richards120 South Central Avenue, Suite 1400, St. Louis, MO 63105-1705314-290-1415 [email protected]

28towerswatson.com© 2010 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Disclaimer

The information included in this presentation is general information only and should not be relied upon without further review by the appropriate professional advisors. Towers Watson is not a law firm or accounting firm, and we are not providing legal, accounting or tax services or advice. Some of the information included in this presentation might involve the application of law; accordingly, we strongly recommend that audience members consult with and involve their legal counsel and other professional advisors as appropriate to ensure that they are fully advised concerning such matters. Additionally, material developments may occur subsequent to this presentation rendering it incomplete and inaccurate. Towers Watson assumes no obligation to advise you of any such developments or to update the presentation to reflect such developments.