integrated annual repor t 2014 - south african share prices, jse … · 2014-10-15 · the king...

TRANSCRIPT

Integrated annual report 2014

Seardel Investment Corporation Limited (“Seardel” or “the Group”) is pleased to

present its 2014 Integrated Annual Report to stakeholders in accordance with

the King Code of Governance Principles (King III). As a JSE-listed company, the

Group subscribes to the principles of integrated reporting, which strive to provide

insight into the business practices which have a material influence on the future

sustainability of the Group.

The Integrated Report aims to provide a greater understanding of the Group’s

business model, its social and environmental impact and insight into how the

Group’s businesses are managed. We see this report as an evolving process

and undertake to provide further enhanced reporting each year, where deemed

appropriate.

Scope and BoundaryThe 2014 Integrated Report covers the activities and performances of the Group

for the financial year 1 April 2013 to 31 March 2014. The Group operates principally

in South Africa and generates the majority of its revenue from South Africa.

The Integrated Report and the Financial Statements have been prepared

according to International Financial Reporting Standards (IFRS), the requirements

of the Companies Act (71 of 2008, as amended), and the Listings Requirements

of the JSE. The Group has implemented the recommendations of King III, except

where noted to the contrary, and management has also considered the guidelines

published by the Integrated Reporting Committee of South Africa.

It has further applied the principles of materiality in determining the content and

levels of disclosure throughout the Integrated Annual Report.

approval of the integrated reportThe integrity of the Integrated Report is the responsibility of the board of directors.

The directors confirm they have collectively reviewed the content of the Integrated

Report and are of the opinion that it is a fair representation of the integrated

performance of the Group.

external aSSuranceAssurance and the contents of the Integrated Report were considered

throughout the process. The board, assisted by the audit and risk committees,

is ultimately responsible for overseeing the integrity of the Integrated Report. The

Group’s external auditors have assured the financial statements and accredited

specialist agencies have verified the disclosure on broad-based black economic

empowerment, property valuations and carbon emissions. The Group has

implemented a combined assurance framework which considers the assurance

provided by all independent assurance providers.

additional informationOur 2014 Integrated Report is available online at: www.seardel.co.za. A printed

copy of the financial statements is available on request from [email protected].

aBout thiS report

contentSour groupProfile ............................................................................ 2

Financial highlights ......................................................... 4

Ten-year review ............................................................. 6

Directors’ profile .......................................................... 10

CEO’s report ................................................................ 12

Sustainability report ......................................................16

Cash value added statement ....................................... 21

our governance

Corporate governance ................................................. 22

Social and ethics committee report .............................. 29

Risk committee report ................................................. 30

Remuneration report .................................................... 31

our numBerSAudit committee report ................................................ 40

Directors’ responsibility

statement and certificate of company secretary ........... 42

Directors’ report .......................................................... 43

Independent auditor’s report ........................................ 45

Financial statements .................................................... 46

our ShareholderS Analysis of shareholders ............................................ 125

Notice of annual general meeting ............................... 128

Form of proxy ............................................................ 135

our contact detailSCorporate information ................................................ IBC

Seardel integrated annual report 20141

PROFILE

Seardel Group Properties (SGP) owns and manages a portfolio of industrial and commercial properties situated in KwaZulu-Natal, Western Cape and Gauteng with a market value in excess of R1 billion.

PROPERtIEs

The businesses reported in our branded product distribution segment consist of operations which focus on igniting sustainable and long-term momentum for brands in the South African and sub-Saharan African markets. These enterprises supply an extensive selection of prestigious brands to the South African consumer, including Microsoft X-Box, Leapfrog, Butterfly stationery, Sharp, 466/64 fashion and a large variety of well-known toys.

The businesses operating in this segment include Prima Toys, Prima Interactive, The Empire Group, Seartec and Brand ID.

Subsequent to year-end the businesses of Limtech and Office Box joined the Group and we added 14 new sport brands, including Canterbury, Dunlop and Slazenger.

BRANDED PRODUCt DIstRIBUtION

The Group’s textile investments include the textile businesses of Romatex, Frame Knitting Manufacturers, Winelands Textiles (previously Berg River Textiles and Hextex) and First Factory Shops.

These businesses manufacture high-quality home textiles and cotton, worsted and polyester fabrics predominantly for the South African medical, hospitality and retail markets.

tEXtILEs

Keith Robson Ian Morris, Wayne Bebb, Mark McChleryPiet Van Wyk, Mike McGeever, Jerry Govender, Garry Milne

Seardel is a diverse investment group, operating primarily in South Africa and is listed on the JSE under the Consumer Goods – Personal and Household Goods Sector.

Gross revenue

(R’000): R118 926

Operating profit (R’000): R103 769

Gross revenue

(R’000): R957 545

Operating profit (R’000):

R37 359

Gross revenue

(R’000): R736 920

Operating profit (R’000):

R21 990

2

Stuart Queen (Chief Executive Officer)

Gys Wege (Financial Director)

Dave Duncan (Chief Operating Officer)

Amon Ntuli (Human Resources)

EXECUtIVE DIRECtORs

The Group holds a 63,9% interest in Sabido, which in turn houses investments in e.tv, eSat.tv, Yfm, Sasani Studios and Platco, amongst others. The primary asset, television channel e.tv, is South Africa’s favourite free-to-air television channel providing broad appeal programming spanning all age, race and income groups across 80,5% of the South African population.

The Group has further expanded into new platforms such as enca.com, an online news service and OpenView HD, the first commercially available, free-to-air, direct-to-home satellite offering in South Africa.

MEDIA

The Group’s industrial investments comprise Gold Reef Speciality Chemicals, Brits Automotive Systems, Brits Non-Woven, Integrated Polypropylene Products and Custom Extrusion.

These businesses are manufacturers of specialised industrial products for the mining, agricultural, building, automotive, paint and bedding industries.

INDUstRIALs

The clothing segment comprises Seardel Apparel and Easywear factory shops.

During the year the Group disposed of its South African-based clothing manufacturing investments to an associate company of SACTWU and its Lesotho manufacturing plant to an external party.

Marcel GoldingDesmond Beemiah, Werner Peter, Cliff Van Niekerk, Leon schoeman Ian stein, Anita de souza

CLOthING

Gross revenue

(R’000): R1 223 603

Operating profit (R’000):

R241 194

Gross revenue

(R’000): R424 701

Operating profit (R’000):

R32 194

Gross revenue

(R’000): R627 651

Operating loss (R’000):

(R151 304)

sEARDEL INtEGRAtED ANNUAL REPORt 20143

financial highlightSRand thousands, unless otherwise indicated 2014 2013*Revenue 3 387 121 1 845 524 Profit before taxation from continued operations 282 784 84 907 Loss before taxation from discontinued operations (159 901) (45 173)Profit before taxation 122 883 39 734 (Loss)/profit attributable to shareholders (11 157) 40 851 Equity attributable to equity holders 2 717 969 1 460 586 Total tangible assets (excluding cash) 3 957 161 2 467 279 Return from continued operations on total tangible assets (%) 11,4 4,4%Return on shareholders’ interest (%) (0,4) 2,8 Ratio of borrowings to capital and reserves (%) 195 34

StatiSticS per ShareIn cents, where applicable 2014 2013Headline earnings 0,10 2,92Headline earnings – continued operations 14,13 9,37Headline loss – discontinued operations (14,03) (6,44)Basic (loss)/earnings (1,26) 5,96Basic earnings – continued operations 16,83 12,55Basic loss – discontinued operations (18,09) (6,59)Operating cash flow 25 30 Net asset value 229 214 Market price – End of period

– Ordinary 200 120 – N Ordinary 174 120

High price range – Ordinary 320 154 – N Ordinary 315 145

Low price range – Ordinary 116 86 – N Ordinary 120 96

Revenue, total tangible assets (excluding cash and deferred tax) and return on total tangible assets

Segment

Revenue Total tangible assetsReturn on totaltangible assets

2014 2013* 2014 2013 2014 2013*Rm % Rm % Rm % Rm % % %

Media 1 224 36 – – 1 416 36 – – 17 – Branded Product Distribution 954 28 793 43 542 14 451 18 7 3 Properties 71 2 47 3 1 075 27 997 41 10 6 Textiles 690 20 650 35 478 12 474 19 5 7 Industrials 425 13 328 18 246 6 206 8 13 8 Clothing 23 1 27 1 165 4 334 14 (3) (1)Head office – – – – 35 1 5 – 69 (275)

3 387 100 1 845 100 3 957 100 2 467 100 11 4 2013* 1 845 2 467 4

2012 2 507 2 384 8

2011 2 359 2 058 6

2010 2 166 2 110 3

* Restated, refer to note 36.

4

2 5072012

1 8462013

3 3872014

REVENUE (rm)

1 4122012

1 4612013

2 7182014

CAPITAL AND RESERVES (rm)

1792012

1092013

4562014

OPERATING PROFIT (rm)

39

2012

2032013

2172014

FREE CASH FLOW (rm)

158 86 2012012 2013 2014

PROFIT FROm CONTINUING OPERATIONS (rm)

2 3832012

2 4672013

3 9572014

TANGIBLE ASSETS (rm)

Brand ID

Seardel integrated annual report 20145

ten-year revieWRand thousands 2014 2013* 2012 2011 2010

20099 months 2008 2007 2006 2005

operationSRevenue 3 387 121 1 845 524 2 506 794 2 358 986 2 165 727 2 169 584 3 867 565 3 793 357 3 583 702 3 745 145

Continued operations

Operating profit/(loss) before finance costs 456 123 108 625 179 015 121 658 66 907 (117 312) (165 455) 111 668 152 276 129 210

Net finance costs 167 972 23 718 33 873 27 726 22 268 38 253 81 645 57 078 46 572 56 030

Share of losses from joint venture 5 367 – – – – 2 503 9 181 2 973 446 –

Profit/(loss) before taxation 282 784 84 907 145 142 93 932 44 639 (158 068) (256 281) 51 617 105 258 73 180

Taxation 81 270 (1 117) (13 131) (10 084) 1 740 (27 470) (72 212) 855 18 841 23

Profit/(loss) from continued operations for the year 201 514 86 024 158 273 104 016 42 899 (130 598) (184 069) 50 762 86 417 73 157

Loss from discontinued operations for the year (159 901) (45 173) (21 442) (95 440) (246 355) (153 962) – – – –

Profit/(loss) attributable to shareholders (11 157) 40 851 136 944 8 567 (203 593) (279 344) (178 842) 50 770 85 471 73 255

caSh floWNet cash flow 332 448 50 843 175 954 105 594 62 788 (195 652) (86 619) 98 185 159 902 98 899

Cash generated from/(utilised by) operations – nominal 217 444 202 584 39 386 (57 281) 149 628 (162 040) 6 023 (161 019) 128 246 102 863

Net cash (outflow)/inflow from investing activities (191 614) (210 751) (170 076) 22 786 6 521 (56 616) (78 608) (4 629) 4 560 (34 756)

Operating cash flow per share (cents) 25 30 6 (8) 21 (37) 19 (150) 134 99

financial poSitionCapital and reserves (including negative goodwill) 2 717 969 1 460 586 1 411 645 1 253 982 1 291 348 1 408 949 1 390 233 1 541 093 1 373 205 1 394 782

Net borrowings 5 312 476 503 502 474 564 338 810 304 315 460 464 542 157 466 364 296 571 319 368

Other debt (excluding deferred liabilities) 885 124 460 481 452 509 424 319 456 360 574 399 753 410 625 349 588 023 500 047

Working capital 588 190 168 291 354 458 365 204 407 359 634 868 527 054 886 730 817 179 850 251

Total tangible assets (excluding cash and deferred tax) 3 957 161 2 467 279 2 383 917 2 058 119 2 110 160 2 556 781 2 831 028 2 853 994 2 473 202 2 435 313

* Restated, refer to note 36.

Years prior to 2012 have not been restated for discontinued operations.

6

Rand thousands 2014 2013* 2012 2011 20102009

9 months 2008 2007 2006 2005

operationSRevenue 3 387 121 1 845 524 2 506 794 2 358 986 2 165 727 2 169 584 3 867 565 3 793 357 3 583 702 3 745 145

Continued operations

Operating profit/(loss) before finance costs 456 123 108 625 179 015 121 658 66 907 (117 312) (165 455) 111 668 152 276 129 210

Net finance costs 167 972 23 718 33 873 27 726 22 268 38 253 81 645 57 078 46 572 56 030

Share of losses from joint venture 5 367 – – – – 2 503 9 181 2 973 446 –

Profit/(loss) before taxation 282 784 84 907 145 142 93 932 44 639 (158 068) (256 281) 51 617 105 258 73 180

Taxation 81 270 (1 117) (13 131) (10 084) 1 740 (27 470) (72 212) 855 18 841 23

Profit/(loss) from continued operations for the year 201 514 86 024 158 273 104 016 42 899 (130 598) (184 069) 50 762 86 417 73 157

Loss from discontinued operations for the year (159 901) (45 173) (21 442) (95 440) (246 355) (153 962) – – – –

Profit/(loss) attributable to shareholders (11 157) 40 851 136 944 8 567 (203 593) (279 344) (178 842) 50 770 85 471 73 255

caSh floWNet cash flow 332 448 50 843 175 954 105 594 62 788 (195 652) (86 619) 98 185 159 902 98 899

Cash generated from/(utilised by) operations – nominal 217 444 202 584 39 386 (57 281) 149 628 (162 040) 6 023 (161 019) 128 246 102 863

Net cash (outflow)/inflow from investing activities (191 614) (210 751) (170 076) 22 786 6 521 (56 616) (78 608) (4 629) 4 560 (34 756)

Operating cash flow per share (cents) 25 30 6 (8) 21 (37) 19 (150) 134 99

financial poSitionCapital and reserves (including negative goodwill) 2 717 969 1 460 586 1 411 645 1 253 982 1 291 348 1 408 949 1 390 233 1 541 093 1 373 205 1 394 782

Net borrowings 5 312 476 503 502 474 564 338 810 304 315 460 464 542 157 466 364 296 571 319 368

Other debt (excluding deferred liabilities) 885 124 460 481 452 509 424 319 456 360 574 399 753 410 625 349 588 023 500 047

Working capital 588 190 168 291 354 458 365 204 407 359 634 868 527 054 886 730 817 179 850 251

Total tangible assets (excluding cash and deferred tax) 3 957 161 2 467 279 2 383 917 2 058 119 2 110 160 2 556 781 2 831 028 2 853 994 2 473 202 2 435 313

* Restated, refer to note 36.

Years prior to 2012 have not been restated for discontinued operations.

* Restated, refer to note 36.

2010 2011 2012 2013* 2014

2 1662 359 2 507

1 845

3 387

Branded product distribution

properties

media

textiles

industrials

SEGmENT REVENUE (rm)

clothing

Seardel integrated annual report 20147

ten-year revieW (continued)

Rand thousands 2014 2013* 2012 2011 20102009

9 months 2008 2007 2006 2005

ratioSProfitability

Operating profit/(loss) as percentage of revenue – continued operations (%) 13,5 5,9 7,1 5,2 3,1 (5,4) (4,3) 2,9 4,2 3,5

Profit/(loss) for the period as percentage of revenue – continued operations (%) 5,9 4,7 6,3 4,4 2,0 (6,0) (4,8) 1,3 2,4 2,0

Return on total tangible assets – continued operations (%) 11,4 4,4 7,5 5,9 3,2 (6,2) (6,2) 3,8 6,1 5,3

Return on investments (%) (0,3) 1,7 5,7 0,4 (9,6) (14,6) (6,3) 1,8 3,5 3,0

Return on shareholders’ interest (%) (0,4) 2,8 9,7 0,7 (15,8) (26,4) (12,9) 3,3 6,2 5,2

Leverage

Ratio of borrowings to capital and reserves (%) 195 34 34 27 24 33 39 31 22 23

Ratio of debt to capital and reserves (%) 228 66 66 61 59 73 93 71 64 58

Liquidity

Current ratio (times) 1,4 1,2 1,4 1,5 1,5 1,7 1,4 1,9 2,0 2,2

Solvency ratio (%) 5,2 5,2 18,9 13,6 7,5 (23,9) (6,4) 7,9 15,1 7,2

Finance charges cover (times) 2,7 4,6 5,3 4,4 3,0 (3,1) (2,0) 2,0 3,3 2,3

Productivity

Total assets turn 0,9 0,7 1,1 1,1 1,0 1,1 1,4 1,3 1,4 1,5

Number of employees 6 301 6 475 7 887 9 541 11 771 13 221 14 847 15 343 15 170 15 280

Revenue per employee (Rand) 537 553 285 023 317 839 247 247 183 988 218 802 260 495 247 237 236 236 245 101

Operating profit/(loss) per employee (Rand) 72 389 16 776 22 697 12 751 5 684 (11 831) (11 144) 7 278 10 038 8 456

Assets per employee (Rand) 628 021 381 047 302 259 215 713 179 268 193 388 190 680 186 013 163 032 159 379

Cash value added factor (%) 97 51 54 55 85 39 61 55 69 65

Share StatiSticS (Refer to page 125 for analysis of shareholders)

Weighted average number of shares issued (000) 884 013 685 310 703 398 702 946 702 946 443 253 90 048 91 015 105 224 122 362

Headline earnings/(loss) per share (cents) 0,1 2,9 20,9 (3,5) (22,2) (45,6) (111,0) 22,7 73,0 58,6

Earnings/(loss) per share (cents) (1,3) 6,0 19,5 1,2 (29,0) (63,0) (198,6) 55,8 81,2 58,3

Proposed dividend – – – – – – – 12,0 27,0 11,0

Headline earnings/(loss) yield at period-end (%) 0,1 2,4 17,6 (4,2) (62,5) (157,3) (33,1) 3,0 10,6 16,4

Dividend yield at period-end (%) – – – – – – – 1,6 4,0 3,0

Proposed dividend cover (times) – – – – – – – 1,9 2,7 5,3

Net asset value per share – excluding intangible assets (cents) (321) 212 199 177 183 197 1 514 1 703 1 502 1 212

Total number of shares traded (000) (000) 54 555 19 711 23 732 57 982 8 957 9 870 6 962 7 136 36 715 31 137

Total value of shares traded (R000) (R000) 134 992 24 513 19 260 28 979 3 491 5 372 41 609 49 384 173 247 86 883

Percentage of issued shares traded (%) 4,5 2,8 3,4 8,2 1,3 1,9 7,6 7,8 39,3 0,3

Market price – highest – ordinary (cents) 320 154 120 100 50 350 1 000 810 700 430

– N ordinary (cents) 315 145 115 90 60 330 785 825 700 425

– lowest – ordinary (cents) 116 86 71 32 33 33 340 651 365 205

– N ordinary (cents) 120 96 72 31 30 32 220 600 350 181

– period-end – ordinary (cents) 200 120 119 85 36 38 350 750 700 360

– N ordinary (cents) 174 120 111 83 31 42 330 750 670 370

* Restated, refer to note 36.

Years prior to 2012 have not been restated for discontinued operations.

8

Rand thousands 2014 2013* 2012 2011 20102009

9 months 2008 2007 2006 2005

ratioSProfitability

Operating profit/(loss) as percentage of revenue – continued operations (%) 13,5 5,9 7,1 5,2 3,1 (5,4) (4,3) 2,9 4,2 3,5

Profit/(loss) for the period as percentage of revenue – continued operations (%) 5,9 4,7 6,3 4,4 2,0 (6,0) (4,8) 1,3 2,4 2,0

Return on total tangible assets – continued operations (%) 11,4 4,4 7,5 5,9 3,2 (6,2) (6,2) 3,8 6,1 5,3

Return on investments (%) (0,3) 1,7 5,7 0,4 (9,6) (14,6) (6,3) 1,8 3,5 3,0

Return on shareholders’ interest (%) (0,4) 2,8 9,7 0,7 (15,8) (26,4) (12,9) 3,3 6,2 5,2

Leverage

Ratio of borrowings to capital and reserves (%) 195 34 34 27 24 33 39 31 22 23

Ratio of debt to capital and reserves (%) 228 66 66 61 59 73 93 71 64 58

Liquidity

Current ratio (times) 1,4 1,2 1,4 1,5 1,5 1,7 1,4 1,9 2,0 2,2

Solvency ratio (%) 5,2 5,2 18,9 13,6 7,5 (23,9) (6,4) 7,9 15,1 7,2

Finance charges cover (times) 2,7 4,6 5,3 4,4 3,0 (3,1) (2,0) 2,0 3,3 2,3

Productivity

Total assets turn 0,9 0,7 1,1 1,1 1,0 1,1 1,4 1,3 1,4 1,5

Number of employees 6 301 6 475 7 887 9 541 11 771 13 221 14 847 15 343 15 170 15 280

Revenue per employee (Rand) 537 553 285 023 317 839 247 247 183 988 218 802 260 495 247 237 236 236 245 101

Operating profit/(loss) per employee (Rand) 72 389 16 776 22 697 12 751 5 684 (11 831) (11 144) 7 278 10 038 8 456

Assets per employee (Rand) 628 021 381 047 302 259 215 713 179 268 193 388 190 680 186 013 163 032 159 379

Cash value added factor (%) 97 51 54 55 85 39 61 55 69 65

Share StatiSticS (Refer to page 125 for analysis of shareholders)

Weighted average number of shares issued (000) 884 013 685 310 703 398 702 946 702 946 443 253 90 048 91 015 105 224 122 362

Headline earnings/(loss) per share (cents) 0,1 2,9 20,9 (3,5) (22,2) (45,6) (111,0) 22,7 73,0 58,6

Earnings/(loss) per share (cents) (1,3) 6,0 19,5 1,2 (29,0) (63,0) (198,6) 55,8 81,2 58,3

Proposed dividend – – – – – – – 12,0 27,0 11,0

Headline earnings/(loss) yield at period-end (%) 0,1 2,4 17,6 (4,2) (62,5) (157,3) (33,1) 3,0 10,6 16,4

Dividend yield at period-end (%) – – – – – – – 1,6 4,0 3,0

Proposed dividend cover (times) – – – – – – – 1,9 2,7 5,3

Net asset value per share – excluding intangible assets (cents) (321) 212 199 177 183 197 1 514 1 703 1 502 1 212

Total number of shares traded (000) (000) 54 555 19 711 23 732 57 982 8 957 9 870 6 962 7 136 36 715 31 137

Total value of shares traded (R000) (R000) 134 992 24 513 19 260 28 979 3 491 5 372 41 609 49 384 173 247 86 883

Percentage of issued shares traded (%) 4,5 2,8 3,4 8,2 1,3 1,9 7,6 7,8 39,3 0,3

Market price – highest – ordinary (cents) 320 154 120 100 50 350 1 000 810 700 430

– N ordinary (cents) 315 145 115 90 60 330 785 825 700 425

– lowest – ordinary (cents) 116 86 71 32 33 33 340 651 365 205

– N ordinary (cents) 120 96 72 31 30 32 220 600 350 181

– period-end – ordinary (cents) 200 120 119 85 36 38 350 750 700 360

– N ordinary (cents) 174 120 111 83 31 42 330 750 670 370

* Restated, refer to note 36.

Years prior to 2012 have not been restated for discontinued operations.

Seardel integrated annual report 20149

1 STuaRT Queen (42) BCompt (Hons), CA (SA)

Executive: Mr Queen was appointed to the board in

October 2008 and became chief executive officer

in December 2009. Prior to joining the board he was

financial director of Johnnic Holdings Limited and held

directorships within various subsidiaries of both Hosken

Consolidated Investment Limited and Johnnic Holdings

Limited. He is a member of the executive and risk

committees.

2 GyS WeGe (40) BCompt (Hons), CA (SA)

Executive: Mr Wege appointed to the board as financial

director in August 2009. Prior to joining the board

he served in various senior financial roles within the

automotive logistics industry. Mr Wege is a member of

the executive committee, risk committee and the social

and ethics committee.

3 amOn nTuLi (55)

Executive: Mr Ntuli was appointed to the board in

October 2008. He was the president of the Southern

African Clothing and Textile Workers Union from 1985

to 2003. Mr Ntuli joined the Seardel Group in 1978 and

was appointed as an executive in 2006. He is a director

of SACTWU Investment Group and various trade union

investment companies. He is chairman of the social and

ethics committee.

4 Dave DunCan (BRiTiSh) (59) BCom

Executive: Mr Duncan was appointed to the board in

May 2013 as chief operating officer. He has been with

the Group for more than 30 years in the industrial

manufacturing sector and is a member of the executive

committee.

eXeCutIVe

1 2 3 4

directorS’ profile

10

5 JOhn COPeLyn (64) BA Hons (Wits), BProc (UNISA)

Non-executive chairperson: Mr Copelyn was appointed

to the board in May 2005. He joined Hosken Consolidated

Investments Limited as chief executive officer in 1997.

Prior to this he was a member of parliament and general

secretary of the Southern African Clothing and Textile

Workers Union. He holds various directorships including

the Industrial Development Corporation Limited, Tsogo

Sun Holdings Limited and Niveus Investments Limited.

6 Kevin GOvenDeR (43) BCom (Hons), BCompt (Hons)

Non-executive: Mr Govender was appointed to the board

in October 2008. He joined the Hosken Consolidated

Investments Group in 1997 and was appointed to the

board of Hosken Consolidated Investments Limited as

an executive director in 2009.

7 RaCheL WaTSOn (55)

Independent, non-executive: Ms Watson was appointed

to the board in August 2009. She has 33 years’

operational experience within the clothing industry. During

her last 14 years within the industry Ms Watson served

as a trade union representative in various organisational

positions. She currently holds a position as an executive

at a regional broadcaster and was appointed to the

board of Hosken Consolidated Investments Limited in

March 2014. She is a member of the audit, risk, and

social and ethics committees.

8 yuniS ShaiK (56) BProc (UNISA)

Independent, non-executive: Mr Shaik was appointed

to the board in October 2008. Mr Shaik is an executive

director of Hosken Consolidated Investments Limited.

Prior to his appointment at HCI he was an attorney of the

High Court and served as a senior commissioner to the

CCMA in KwaZulu-Natal. He is a former deputy-general

secretary of the Southern African Clothing and Textile

Workers Union and a non-executive director of Tsogo

Sun Holdings Limited and Niveus Investments Limited.

9 mOhameD ahmeD (49) BCompt

Independent, non-executive: Mr Ahmed was appointed

to the board in October 2008. He previously held

directorships in Hosken Consolidated Investments

Limited, MTN, Real Africa Holdings and numerous

entities within the clothing and textile industry. He is a

member of the audit and risk committees and the lead

independent non-executive director.

non-eXeCutIVe

5 6 7 8

Seardel integrated annual report 201411

The year ended 31 March 2014 has been a transformative

year for the Group, with two very significant events being

reflected in the financial results as presented:

• Firstly, theGroupacquireda63,9% interest inSabido

Investments Proprietary Limited (Sabido). Sabido is the

investment vehicle that houses e.tv, eSat.tv, Yfm and

Sasani Studios, amongst others. The acquisition was

funded through a combination of R4,4 billion of debt and

R800 million of equity. The equity portion was settled

by the issue of 350 million N ordinary shares to Hosken

Consolidated Investments Limited (HCI) and 150 million

N ordinary shares to SACTWU. Subsequent to the

financial year-end the Group successfully concluded a

R5 billion rights issue, the proceeds of which have gone

to reducing the Group’s debt, including repayment of the

debt associated with the Sabido acquisition.

• Secondly, the Group disposed of its apparel

manufacturing business to an associate company of

SACTWU. The effect of the transaction on the current

year’s results is a R160 million loss which is reflected as

a loss from discontinued operations.

In addition to the above transactions, the businesses

themselves are also going through transformative periods,

the most notable of which being Sabido/e.tv, which is

transitioning from a single channel to a multi-channel

business. Some of the non-media businesses of Seardel are

also transitioning themselves from a defensive turnaround

phase into a growth phase. These transitional initiatives will

require increased costs being absorbed, ahead of future

benefit.

The effect of the above renders any year-on-year

comparisons meaningless and the results are best analysed

within the segmental results. Having said that, the following

items reflected in the results are important considerations

in analysing the overall financial performance for the year

ended 31 March 2014:

a) The Group recorded a R160 million loss attributable to

its apparel manufacturing business, disclosed as a loss

from discontinued operations.

b) Financing expenses include R110 million relating to the

debt assumed on the acquisition of Sabido. This debt

was fully repaid on 25 April 2014.

c) Accounting convention dictates that on the acquisition

of a new business, certain intangible assets need to be

identified, valued and then amortised against the cost

of the acquisition in future years. The amortisation of

the intangible assets included for the six-month period

that Sabido has been owned by the Group amounted to

R40 million.

d) R7 million of transaction costs associated with the

Sabido transaction were expensed during the current

financial year.

e) The current period’s results include non-recurring

income of R38 million relating to the final piece of the

litigation with former directors as disclosed in the SENS

announcement of 10 May 2013.

mediaThis is the first year that the Group is reporting on the

Sabido numbers. Therefore, as can sometimes be the

case, particularly in the first year of reporting, accounting

convention often makes it difficult to reconcile the numbers

as reported back to the underlying performance of the

business acquired. We believe that users of these financial

statements will benefit from some information on Sabido’s

full-year performance, before commenting on what has

ultimately been reported in the Group numbers.

Sabido performanceIn the year ended 31 March 2014 Sabido has undergone significant expansion. The investments into this expansion, which consisted primarily of investments into Platco Digital’s free-to-view OpenView HD platform, e.tv’s new multi-channel

chief executive officer’S report

12

offering and the online news business, enca.com, has had

a negative effect on the profits in the current year. However,

these businesses will assist Sabido, over time, to transition

from a single-channel business to a multi-channel business

operating across multiple platforms.

Sabido’s full-year profit after taxation from continuing

operations was R447 million, which is down from

R499 million in the previous year. If the impact of the

expansion operations was to be excluded, the profit from

continuing operations would have increased by 19% from

R508 million in the prior year, to R604 million in the current

year. The improved performance was achieved by a 12%

increase in revenue, on the back of continued advertising

and subscription revenue growth. On the EBITDA line

Sabido delivered R763 million in the current year, down from

R820 million in the previous year. However, if the impact

of the expansion operations was to be excluded, EBITDA

would have increased by R98 million to R926 million.

Sabido numbers as reflected in the Group numbersUsing the R447 million profit after taxation recorded by

Sabido as a starting point, Seardel has made the following

adjustments in arriving at its own numbers:

• R266millionwerepre-acquisitionprofitsandhencenot

accounted for in the Seardel numbers.

• R110millionof financecostswere incurred relating to

acquisition debt. Following the rights issue this debt has

been repaid in full on 25 April 2014.

• R33millionof amortisationcosts (net of taxation)was

recorded, being the amortisation of the intangible assets

identified on acquisition. This amortisation cost is for the

six months since the effective date of the acquisition.

• R7 million of transaction costs, associated with

the Sabido transaction, were expensed during the

current period.

Seardel non-mediaThe results of the continuing Seardel non-media businesses

were pleasing, with good growth being shown across all

the segments. Revenue was up 17% to R2,2 billion, whilst

gross margins improved by 900 basis points to 25,5%.

The combination of revenue growth and improved margins

resulted in operating profit before interest improving by 98%

to R215 million. Excluding the effects of the non-recurring

items (once-off settlement income, revaluation of investment

properties and impairment reversals) operating profit before

interest increased by 72% to R154 million.

What is encouraging is that, despite what remain very

challenging economic times, collectively these non-media

businesses have been on a consistent growth path for

the past few years. However, their performance was

often overshadowed by the poor results of the apparel

manufacturing division.

Seardel integrated annual report 201413

Property segmentThe property segment results exclude Sabido properties,

valued at R504 million, which are accounted for under the

media segment.

Overall property values increased by 6% to R1 005 million

from R944 million in the prior year. The increase is driven

by R37 million spent on redevelopments, R39 million on

property acquisitions, R39 million in upward revaluations at

year-end, less disposals and transfers to assets held for sale

of R54 million.

Revenue increased 28% to R119 million as the developed

properties were either completed during the year or

accounted for a full twelve-month period, as opposed to a

portion of the corresponding period. Revenue from external

tenants increased by 51% to R72 million and now represents

60% of the total revenue for this segment.

Operating profit before finance costs increased by 61%

to R104 million, up from R64 million in the prior period.

However, it should be noted that the current year’s profit

number includes a R21 million upwards revaluation of

investment properties, whilst the prior period included a

downward revaluation of R2 million. Excluding the effects of

the revaluations sees operating profit up 26%.

Branded product segmentThe branded product segment recorded pleasing revenue

growth of 20% to R958 million while operating profit before

finance costs climbed 141% to R37 million, admittedly off a

low base in the prior year. Although the growth in operating

profit is pleasing, operating margins remain low at 3,9%.

We have previously mentioned that we were continuing to

invest in marketing and building our distribution platforms

in this segment, with much of this investment being ahead

of expected future revenue growth. This remains the case,

particularly within our office automation business and Brand

ID. We expect operating margins to improve once these

businesses find the requisite traction. To aid in this, post

the year-end we have concluded a transaction to acquire

the distribution rights for a number of sporting brands, most

notably Canterbury, Mizuno, Skins, Karrimor, Dunlop and

Slazenger. These brands will be housed within the Brand

ID business and the revenue they generate will allow for a

better amortisation of the fixed costs.

Textile segmentAlthough trading conditions for the businesses within this

sector remained tough throughout the current financial

period, the businesses managed to achieve revenue growth

of 7%.

chief executive officer’S report (continued)

14

To compare the current year’s operating profit to the prior year the non-recurring items from the prior period need to be excluded. These non-recurring items included a R23 million impairment reversal, as well as R9 million of extra energy costs due to liquidation of an external steam supplier. Adjusting for these items sees operating profits on a normalised basis climb 20% to R20 million.

Although the improved profitability is pleasing, operating margins at a little over 2,5% are extremely thin, especially considering that they include the benefits derived from the government’s production incentive scheme. The thin margins reflect the vulnerability of these businesses despite them having, in our view, very able and committed management teams. Our challenge over the next few years will be to guide and transition these businesses into areas where they can glean higher margins.

industrial segmentThe manufacturing businesses within the industrial sector

continue to deliver pleasing growth. During the course of the

current financial year the Group completed an acquisition

of a bulk bag manufacturer, which helped grow segmental

revenue by 27% to R425 million.

The revenue growth enabled operating margins to be

widened from 5,1% in the prior period to 8,3% in the current

period, which resulted in operating profit more than doubling

to R33 million.

diScontinued apparel manufacturingThe Group has disposed of its loss-making apparel

manufacturing business to an associate company of

SACTWU. The R160 million loss reflected in the discontinued

operations line includes the operating losses through to

30 September 2013 of R46 million, the discount on the assets

sold of R105 million, as well as associated closure costs.

appreciationWe would like to take this opportunity to thank all our

employees for their concerted efforts during the past financial

year. The improvements reflected in this report are as a

direct result of the commitment shown by our management

teams and all the staff that support them.

Stuart Queen

Chief Executive Officer

Cape Town

18 September 2014

Seardel integrated annual report 201415

SuStainaBility reportThis report aims to provide insight into the way the Group manages its businesses pertaining to sustainability. During 2014 Seardel continued to improve its sustainability reporting standards, implemented various projects to reduce its carbon footprint and increased adherence to internationally recognised environmental standards. Human capital transformation and socio-economic development remained important focus areas and our progress and successes are reflected below.

This report focuses on the following three key areas of sustainability:

1 environmental SuStainaBility 2 tranSformation of

human capital 3 Socio-economic development

Lavender Hill High School

16

environmental Carbon footprint measurement

A greenhouse gas (GHG) emissions report (carbon footprint)

is the basis for accounting emissions-related risks and

opportunities for the Group. The group continues to report

in terms of the GHG Protocol and units of tonnes CO2e, the

universal unit measure.

The Group’s effort to reduce its carbon footprint is focused

on Scope 1 direct emissions and Scope 2 indirect emissions

as a result of purchased energy requirements. The bulk

of its focus is directed to the manufacturing businesses

which have high energy requirements. The GHG Protocol

related to Scope 1 and Scope 2 emissions are set out in the

below table:

SCOPe 1

Direct GHG

emissions

Direct emissions occur from sources

that are owned or controlled by the

company. For example, emissions

from company-owned vehicles

and kilns.

SCOPe 2

Electricity/Steam

indirect emissions

Scope 2 accounts for GHG

emissions from the generation

of purchased electricity/steam

consumed by the company.

Scope 2 emissions physically occur

at the facility where electricity or

steam is generated.

The Group’s dedication to drive continuous energy efficiency improvements has resulted in further progress to reduce

production input costs and reduce total emissions compared to the prior reporting period.

Scope

2014 Tonnes of CO2

2013 Tonnes of CO2 Notes

Scope 1 – Direct emissions from 30 342 12 169

Diesel used 642 957 ê

Petrol used 1 062 1 241 ê

Coal used 19 661 7 218 é� n2

Heavy fuel oil used 4 637 1 041 ê

Liquified petroleum gas used 1 271 1 712 ê

Natural gas used 3 068 – é� n1

Scope 1 from new companies acquired through business combinations 411 – � n3

Scope 2 – indirect emissions from 53 434 74 945

Purchased electricity 41 029 43 424 ê

Purchased stream – 31 521 é� n2

Scope 2 from new companies acquired through business combinations 12 405 – � n3

Total scope 1 and 2 emissions 83 776 87 114

n1 Natural gas not previously recorded.

n2 Steam previously purchased from an external steam supplier is now produced in-house after the commissioning of a modern coal-fired boiler. This intervention represents the bulk of the Group’s reduction in carbon emissions. (Please note: Externally procured steam is reported in Scope 2 as opposed to internally produced steam, which is in Scope 1.)

n3 To enhance the comparability of the data, businesses acquired during the year is disclosed separately.

The Group’s overall carbon emissions reduced by 3,8% year on year. However, if carbon emissions from new business

acquisitions are excluded, year-on-year emissions reduced by 18,5%.

Seardel integrated annual report 201417

tranSformation of human capitalSeardel is committed to the transformation of its human

capital and its efforts are aligned with the principles and

objectives of broad-based black economic empowerment

as envisaged by the Department of Trade and Industry.

The Group continued to improve its transformation score

compared to the prior year. This improvement is reflective of

the Group’s efforts to practically implement its empowerment

philosophies.

Transformation is monitored and managed within a

governance framework which includes the social and ethics

committee, an internal transformation committee, in which

the chief executive participates, and the business unit

transformation forums.

Seardel’s broad-based black economic empowerment profile is summarised below:

BBBee Max 2014 2013

Ownership 20,00 23,00 23,00

Management control 10,00 5,39 6,00

Employment equity 15,00 11,18 10,34

Skills development 15,00 7,33 8,07

Preferential procurement 20,00 20,00 18,60

Enterprise development 15,00 15,00 15,00

Socio-economic development 5,00 5,00 5,00

Total % 100,00 86,90 86,01

Level 2 Level 2

The Group’s transformation objectives are set out below:

• developmentofhumancapital tosustainaskilledand

motivated workforce;

• monitoringtheGroup’sadherencetoandperformance

under the BBBEE Codes;

• monitoringtheGroup’scompliancewiththerequirements

of the Department of Labour in respect of employment

equity; and

• maintainingtheoverallLevel2BBBEEaccreditation.

Transformation rating

Seardel has maintained its Level 2 BBBEE status with an

overall score of 86,9 out of 100. This places Seardel firmly

amongst the top empowerment companies listed on the JSE.

23,00 / 20,00

ownership

5,39 / 10,00

management control

11,18 / 15,00

employment equity

7,33 / 15,00

Skills development

20,00 / 20,00

preferential procurement

15,00 / 15,00

enterprise development

5,00 / 5,00

Socio-economic development

86,90 / 100,00

Total

Seardel’s 2014 broad-based black economic empowerment profile

SuStainaBility report (continued)

18

Ownership and management controlSeardel’s majority shareholder is Hosken Consolidated Investments Limited (HCI), which in turn is a black-owned and controlled company with 34% exercisable voting rights by women. The Group’s ownership element remained exemplary. A change in the board of directors’ composition resulted in a decrease in the management control element in the current period.

Employment equity During the year under review the Group continued to progress and implement its transformation policies. The Group’s employment equity plan focuses on increasing the representation of designated groups, mainly in the senior management and professionally qualified areas.

Strategies have been developed to achieve internal employment equity targets. These strategies include, amongst other things, the implementation of in-house training and development projects. The Group has also implemented a management trainee programme whereby graduates are employed and given the opportunity to work within the Group’s various businesses, gaining valuable exposure across various business functions. The ultimate goal is to equip the students with the required knowledge and skills to facilitate a permanent employment within the Group.

Skills developmentInvesting in our employees is integral in maintaining high levels of competency. During the year the Group continued to focus on the development of its people, with a wide range of skills programmes being offered internally and externally.

These training interventions have been implemented across all levels of employment. Such interventions include operator training, quality training, mentoring, experiential training, engineering apprenticeships, information technology, IR and disciplinary handling, world-class manufacturing, employment equity, supervisory and team leader training, root cause analysis/risk management training, ISO 14000/ISO 9000 training. In addition to the aforementioned, the Group continued with the NQF Level 2 learnership programmes in the respective divisions. Training focused on providing a safe workplace for all employees, continued relentlessly during the reporting period. This includes the training of first-aid, workplace health and safety, and fire-fighting skills. Whilst statutory training is required to ensure compliance with the provisions of the Occupational Health

and Safety (OHS) Act, the company also believes that such

training is critical to ensure a safe working environment

for our employees and every effort is made to reduce and

eliminate risks in all spheres of the organisation.

Changes in the accreditation requirements, as well as

restructuring within the Group, meant that the Seardel

College, which was registered as a Workplace Further

Education and Training (FET) institution with the Department

of Higher Education and Training, had to apply for voluntary

deregistration. Whilst the college has been deregistered, we

are still able to register and train NQF Level 2 learnership

programmes via our in-house accredited training facilities.

The Seardel Mentorship Programme continued during the

reporting period. Management in the respective businesses

participated in the programme on a voluntary basis and give

of their time and expertise to mentor and assist students

who participate in the Group’s bursary programmes.

The students are full-time students at recognised tertiary

institutions in South Africa. The programme has been in

operation for three years and was initially introduced as an

intervention to improve the success/pass rate of students

participating in the Group’s bursary programme. We are

proud of the positive results that have been achieved

through the mentorship programme and the success/pass

rate since the inception of the programme has been 91,5%,

93,9% and 89,4% for the last three years respectively.

These statistics are encouraging when compared with the

high failure rate at tertiary institutions.

Preferential procurement

The Group procured in excess of 96% of its total qualifying

spend from black-owned companies. This reaffirms the

Group’s commitment to source merchandise and services

from empowered local suppliers.

Enterprise development

Enterprise development presents an opportunity to stimulate

sustainable economic growth by assisting the development

and sustainability of black-owned small and medium

businesses in South Africa. Financial assistance is given

to multiple small to medium suppliers, the vast majority of

which are black-owned. The support is mainly in the form

of favourable payment terms to support the cash flows of

these operations.

Seardel integrated annual report 201419

Socio-economic developmentSeardel acknowledges its social responsibility towards

the communities in which we operate. Together with the

HCI Foundation the Group has been involved in various

community projects. These projects have covered a diverse

spectrum, from supporting orphaned and abandoned

children, people with disabilities, to HIV/AIDS rehabilitation

centres.

The Group’s projects have been focused on education,

women, children and wildlife-related organisations. In order

to create awareness, direct involvement and ownership of

projects, the various businesses within the Seardel Group

are encouraged to adopt a needy organisation in the area

in which they operate. This results in the management and

employees in the businesses taking a direct interest in the

organisation and, in addition to financial support, giving

freely of their own time and expertise. This direct involvement

adds great value to the Group’s CSI project. In support of

the aforementioned and dependent on circumstances,

businesses are encouraged to adopt a charity for more than

one year. We have also supported a principle of assisting a

smaller number of organisations to ensure a more meaningful

contribution and support.

y.e.S. ProjectDuring the year under review we continued our support and

involvement in the Lavender Hill Development Trust Project.

The Y.E.S. Project – Youth Encouragement through School

Project – is a joint project with the HCI Foundation. The project

has been very rewarding and resulted in great success for

the Lavender Hill Secondary School. Pupils have been given

renewed hope of an education and a future. Furthermore, they

have become involved in school and extramural activities,

which ensure they are kept off the streets and limit exposure

to drugs and undesirable activities. Through the Y.E.S. Project

and other activities undertaken by Lavender Hill Development

Trust the school has made massive strides to improve its

facilities and infrastructure. The current project is the building

of a school hall.

COmPaSSSeartec continued to support a COMPASS (Community

Provision and Social Services) project to provide support

and sustain three babies, triplets, for a year.

KZn Cerebral Palsy Reunion SchoolGold Reef Speciality Chemicals supports the KZN Cerebral

Palsy Reunion School. The management and staff have

embraced the concept of adopting the Reunion School.

They have provided much-needed assistance and made a

difference in the lives of these severely handicapped children.

Save the RhinoPrima Toys, in association with the HCI Foundation and Pick

n Pay, was involved in the Save the Rhinos Project/Baby

Rhino Campaign. The project was highly successful and, in

collaboration with Pick n Pay, some R235 000 was raised

towards this worthy cause. In the current calendar year

658 rhinos have succumbed to poaching, whilst more than

1 000 rhinos were poached in 2013.

Saartjie Baartman Centre For Women and ChildrenThe Saartjie Baartman Centre in the Western Cape is

supported by Group’s Western Cape clothing operation. The

organisation provides much-needed support and education

for abused woman and children. Women are taught skills

to be able to earn an income and thereby become self-

sufficient, which reduces the risk of abuse against them.

Jess Foord FoundationThe Jess Foord Foundation is a new project supported by

Brits Automotive Systems. The foundation was created

in 2008 to support women who have been victims of

physical or sexual abuse and/or rape. Statistics indicate

that 282 women are raped in South Africa every 80 minutes.

Brits Automotive Systems, with the support of the HCI

Foundation, was a major contributor towards the creation

of a community and crisis centre at Marianhill, Durban. Most

of our employees live in the area and will benefit from the

services provided by the Community Crisis Centre.

The Seardel Group is proud to be associated with these

worthy causes and appreciates the contribution and

sacrifices made by management and staff in support of

these organisations. We also record our appreciation of the

ongoing support provided by the HCI Foundation towards

our CSI projects. Together we have made a difference.

SuStainaBility report (continued)

20

caSh value added Statement2014

R000’s2013

R000’s2012

R000’s2011

R000’s2010

R000’s

Cash derived from revenue 2 979 401 2 564 619 2 514 194 2 489 813 2 586 923

Paid to suppliers for materials and services 1 509 093 1 703 613 1 616 967 1 610 024 1 580 839

Cash value added 1 470 308 861 006 897 227 879 789 1 006 084

Interest received 2 080 2 971 4 594 7 925 22 563

Total wealth created 1 472 388 863 977 901 821 887 714 1 028 647

Distributed as follows:

employees

Administration 302 801 180 009 168 638 233 758 207 692

Production 279 338 267 710 379 291 396 680 468 763

Sales 165 217 142 444 147 554 120 798 136 759

747 356 590 163 695 483 751 236 813 214

Providers of capital

Interest paid on borrowings 170 052 43 095 38 467 35 651 58 438

Dividend to shareholders – – – – –

170 052 43 095 38 467 35 651 58 438

monetary exchanges with government

Taxation (including customs and excise duty) 226 983 46 579 46 899 22 983 40 770

PAYE 107 531 64 968 84 499 94 956 111 404

VAT 42 867 12 560 35 797 77 833 131 266

Incentives (39 845) (95 972) (38 710) (37 664) (14 851)

337 536 28 135 128 485 158 108 268 589

Retained to develop future growth/(utilised in operations) 217 444 202 584 39 386 (57 281) (111 594)

Total wealth distributed 1 472 388 863 977 901 821 887 714 1 028 647

Value added is a measure of the wealth that the Group has created in its broadcasting, letting, manufacturing and distribution operations by adding value to the cost of its raw materials and services purchased.

The statement above shows how that wealth was created, and also how it was shared between employees and the providers of funds to the Group.

The statement takes into account the amounts retained and reinvested in the Group for the replacement of assets and the development of future operations.

Distribution of wealth 2014 2013 2012 2011 2010

Employees (%) 50,8 68,3 77,1 84,6 79,1

Government (%) 22,9 3,3 14,2 17,8 26,1

Retained/(utilised) (%) 14,8 23,4 4,4 (6,4) (10,9)

Lenders (%) 11,5 5,0 4,3 4,0 5,7

Shareholders (%) – – – – –

(%) 100,0 100,0 100,0 100,0 100,0

Seardel integrated annual report 201421

corporate governance

The Seardel Group’s directors, officers and senior

management remain committed to the highest level of

corporate governance and endorse the Code of Corporate

Practices and Conduct as enshrined in the Third King Report

on Corporate Governance. Sound corporate governance

structures are viewed as pivotal to delivering on the Group’s

sustainability objectives.

application of King iiiThe JSE Limited Listings Requirements made adherence

to selected King III requirements compulsory. The directors

assessed the Group’s compliance to the recommendations

of King III and confirmed that, except where indicated, the

Group complied with all material aspects of these corporate

governance principles. With reference to the remainder of

the King III requirements, where the directors’ assessment

has indicated that certain practices are not in the best

interest of Seardel, we explain the reasons for our alternative

approach as follows:

Principle 2.16 recommends that the board should elect

a chairman who is an independent non-executive director.

The board has appointed a non-executive chairman and,

in terms of the definition provided, he is not regarded as

independent. The board is of the opinion that the experience

and specialist knowledge of the environment in which

Seardel operates, makes it appropriate for him to hold this

position. The board has appointed Mr M Ahmed as lead

independent non-executive director.

Principle 2.18 recommends that the majority of non-

executive directors should be independent. As a result

of Mr Shaik accepting the appointment as an executive

director of Hosken Consolidated Investments Limited, the

majority shareholder of Seardel, he no longer meets the

definition of independent in terms of the definition provided.

Consequently, at the reporting date, the majority of the non-

executive directors were not independent. Subsequent to

year-end Mrs N Jappie was appointed to the board as an

independent non-executive member.

Principle 2.26 recommends that the remuneration of each

individual director and the three most highly paid employees

who are not directors in the company be disclosed. The

remuneration report discloses the remuneration of the three

most highly paid employees, however the names of the

employees who are not directors have not been disclosed as

the board is of the opinion that such information is private to

the individuals concerned and adds no value to stakeholders.

Principle 4.6 recommends that frameworks and

methodologies are implemented to increase the probability

of anticipating unpredictable risks. It is the view of the

risk committee that the existing governance principles

and levels of risk tolerance embedded within the Group

provide sufficient coverage of the risks associated with the

probability of anticipated unpredictable risks.

Principles 4.9 and 9.3 recommends that the effectiveness

of the risk management process and sustainable reporting

and disclosure should be independently assured. The

Group’s external auditors have assured the financial

statements and accredited specialist agencies have

verified the disclosure on broad-based black economic

empowerment, property valuations and carbon emissions.

The Group has implemented a combined assurance

framework which considers the assurance provided by

all independent assurance providers. The extent of the

independent assurance received is deemed to be sufficient.

Detailed disclosure of the Group’s adherence to the King III

principles is published on our website, www.seardel.co.za

Board of directorSSeardel has a unitary board which is tasked with both

leading and controlling the Group’s strategy and operations.

The collective experience and diversity of the directors bring

This report provides our stakeholders with insight as to how the board and its underlying committees are overseeing and guiding the Group’s performance and strategy. It further outlines our corporate structure which is responsible to ensure compliance with internal policies and external regulation.

22

a broad perspective and invaluable wealth of insight. Their

knowledge comes from a diverse array of backgrounds

and specialist skills across a range of sectors including law,

accounting, manufacturing, logistics and industrial relations.

Board compositionAt year-end the board of directors comprises nine members,

five non-executive directors and four executive directors.

Two of the five non-executive directors are independent.

Subsequent to year-end the board appointed an additional

independent non-executive director. The composition

of the board is a reflection of the demographics of the

Group’s diversified investments and attempts to ensure a

representative voice of all relevant stakeholders.

The composition of the board is regularly reviewed to ensure a

balance of power and authority, negate individual dominance

in the decision-making processes and promote objectivity.

The board has appointed a non-executive director as

chairman. The roles of chairman and chief executive officer

are separate with a clear division of responsibilities.

During the year Mr N Lazarus resigned from the board

and Mr Ahmed, Mr Shaik and Ms Watson were re-elected

as directors at the annual general meeting (AGM) held on

28 October 2013.

The company’s ultimate controlling shareholder is Hosken

Consolidated Investments Limited (HCI). Mr Copelyn,

Mr Govender, Mr Shaik and Ms Watson also serve on the

HCI board.

Board appointment The appointment to the board of directors is governed by

a formal board-approved mandate regulating the terms of

reference and incorporates the provisions of the Companies

Act of 2008, as amended, the mandatory provisions

as stipulated in paragraph 3.84 of the JSE Listings

Requirements, recommendations of the King Code and the

memorandum of incorporation of the company.

There is a distinctive division of responsibilities at board

level so that not one individual has unfettered powers of

decision-making. The board as a whole, within its powers

and in a formal and transparent manner, is responsible for

the selection and appointment of directors.

Directors do not have a fixed term of appointment and there

is no mandatory retirement age for non-executive directors.

According to the company’s memorandum of incorporation

as adopted, non-executive directors retire every three years,

with at least one-third of non-executive directors to retire

every three years at the AGM. Executive directors are to

retire every five years. A retiring director shall be eligible for

re-election and, if re-elected, shall be deemed not to have

vacated office. The directors retiring at the forthcoming AGM

of the company are Mr J Copelyn and Mr K Govender. Their

reappointment is subject to shareholders’ approval.

Subsequent to year-end Mrs N Jappie was appointed to the

board. As required in terms of the company’s memorandum

of incorporation, at the forthcoming AGM, Mrs N Jappie’s

appointment is subject to shareholders’ approval.

The name and brief curriculum vitae of each director appears

on pages 10 and 11.

independence of directorsSeardel’s non-executive directors acknowledge the need

for their independence, while recognising the importance of

good communication and close co-operation with executive

management. The directors are entitled to seek independent

professional advice at the company’s expense concerning

the company’s affairs and have access to any information

they may require in discharging their duties as directors.

Seardel’s lead independent director is responsible for

verifying on an annual basis the continuing independence

and objectivity of the independent non-executive directors.

This is done by assessing any circumstance or relationships

that could affect such independence.

Board attendanceThe board meets at least four times a year and additional

meetings can be convened to consider specific business

issues which may arise between scheduled meetings. No

additional meetings were required during the year. Directors

are provided with substantive board papers to enable them

to consider the issues on which they are requested to make

decisions. The following table details each director’s board

meeting attendance during the year under review:

Seardel integrated annual report 201423

corporate governance (continued)

company SecretaryHCI Managerial Services (Pty) Ltd is the appointed company secretary of the Group. The company secretary provides support and guidance to the board in matters relating to governance, ethical conduct and their fiduciary duties. Where required, representatives of the company secretary facilitate induction and training for directors and co-ordinate the annual board and committee evaluation process.

Directors have unrestricted access to the advice and services of the company secretary. Neither the company secretary, nor any representatives of the company secretary, is a director of any of the Group’s operations and accordingly maintains an arm’s length relationship with the board and its directors.

The company secretary is responsible for the functions as set out in section 88 of the Companies Act of 2008 (as amended). The board has assessed the directors and the designated staff of the company fulfilling the role of the company secretariat and is satisfied that they have the competence, qualifications and experience to effectively fulfil the role of company secretary. All board, committee and shareholders’ meetings are properly recorded as per the requirements of the Act.

dealingS in the company’S SecuritieSSeardel complies with the continuing obligations of the Listings Requirements of the JSE. The company’s directors, executives and senior employees are prohibited from dealing

in Seardel securities during certain prescribed restricted

periods. The company secretary regularly disseminates

written notices to inform them of the insider trading

legislation and advise them of closed periods. All directors

and senior executives are required to obtain clearance from

the company secretary prior to dealings in the company

securities. All dealings in the company’s securities are

disclosed in terms of the applicable Listings Requirements.

governance of itThe board of directors are responsible for information

technology (IT) governance. The board tasks the Group

head of IT to ensure IT governance compliance within the

Seardel Group.

The Group head of IT further provides oversight and

direction on business level IT strategy, IT investment and

the efficiency and effectiveness of IT. IT risk management

is aligned with the Group risk management structure and is

channelled by way of the risk management committee. The

committee receives feedback on critical risk issues and the

solutions proposed including progress reports.

Board committeeSSeardel’s board committees play a pivotal role in guiding

and overseeing strategy, enhancing high standards of

governance and achieving increased effectiveness within

the Group. The committees comprise members of the board

and executive officers of the Group.

16 May 2013 14 August 2013 11 November 2013 17 March 2014

J A Copelyn ü ü ü üN N Lazarus ü ü ∆ ∆

M H Ahmed ü ü ü üD Duncan ü ü ü üT G Govender ü ü ü üA M Ntuli ü ü ü üS A Queen ü ü ü üY Shaik ü ü ü üR Watson ü ü ü üG Wege ü ü ü ü

√ In attendance.

∆ No longer a member of the board.

24

Board committees are free to take independent, outside professional advice within the scope of their terms of reference and as deemed necessary to carry out their duties. The Group’s chief executive officer and other members of the executive management whose presence is required for such committees’ effective performance of their responsibilities are invited to be in attendance at committee meetings.

The board has established five committees to assist in discharging its responsibilities:

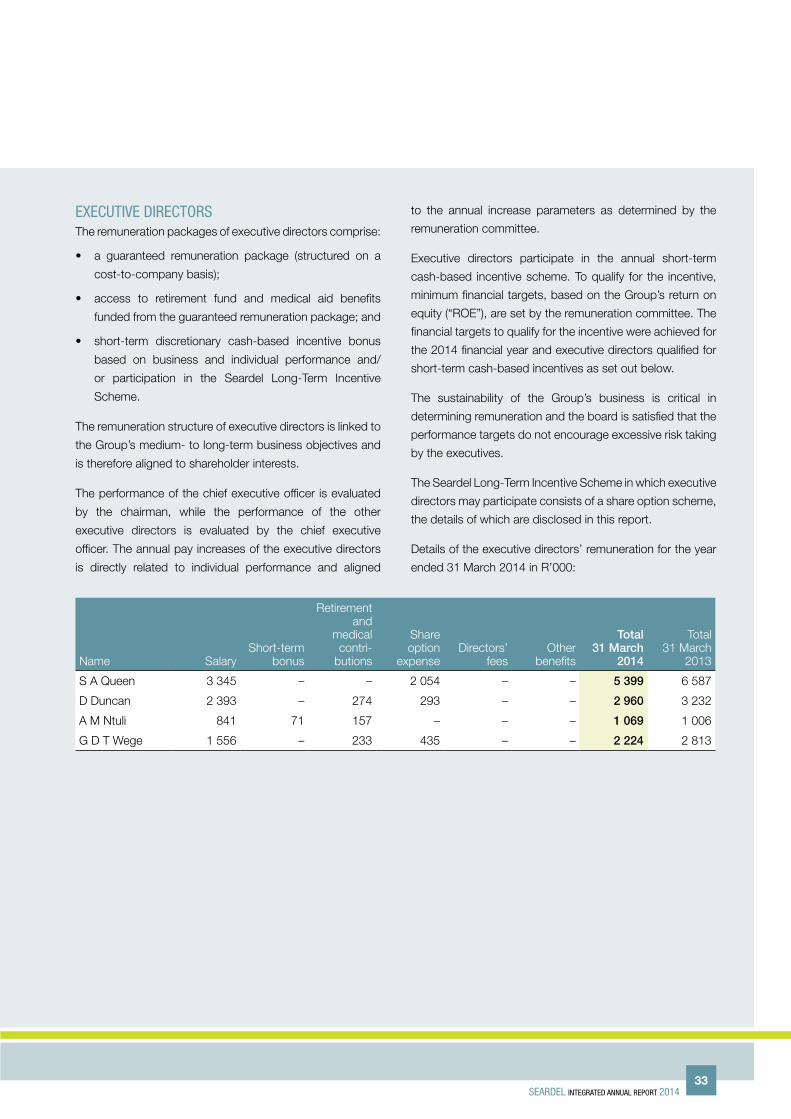

executive committeeChairman: Mr S Queen

Role: The executive committee is responsible for the day-to-day operational activities of the Group, development and implementation of strategy and board directives.

The Seardel executive committee comprises Messrs S Queen (Chairman, Group chief executive officer), G Wege (Group financial director), D Duncan (chief executive officer Industrial and Textiles), K Robson (chief executive officer Properties, Corporate and Legal Services) and I Morris (chief executive officer Prima Group).

The executive committee meets formally once a week and executive committee members attend the monthly operational meetings of each operating entity within the Group. Such formal weekly and monthly meetings include the review of strategic, operational and financial results.

The board is apprised of progress through reporting at board meetings and regular communication with management.

audit committeeChairman: Mr M Ahmed

Role: The audit committee performs an important function by overseeing the Group’s financial statements and reporting processes, including the system of internal financial controls.

The committee’s report is presented on page 40.

Risk committeeGroup risk officer: Mr D Levin

Role: The risk committee is primarily responsible for the governance of risk in accordance with the framework of the Group’s risk management policy.

The committee’s report is presented on page 30.

Remuneration committeeChairman: Mr Y Shaik

Role: The remuneration committee ensures that the Group’s

directors and senior management are fairly rewarded for

their individual contribution to overall performance and

aligned with the Group’s strategy and performance goals.

The committee’s report is presented on page 31.

Social and ethics committeeChairman: Mr A Ntuli

Role: The social and ethics committee monitors activities

relating to ethics, stakeholder engagement and the social

impact of the company on communities within which it

operates. The committee also monitors progress across all

areas of strategic empowerment as well as compliance with

transformation codes.

The committee’s report is presented on page 29.

Seardel integrated annual report 201425

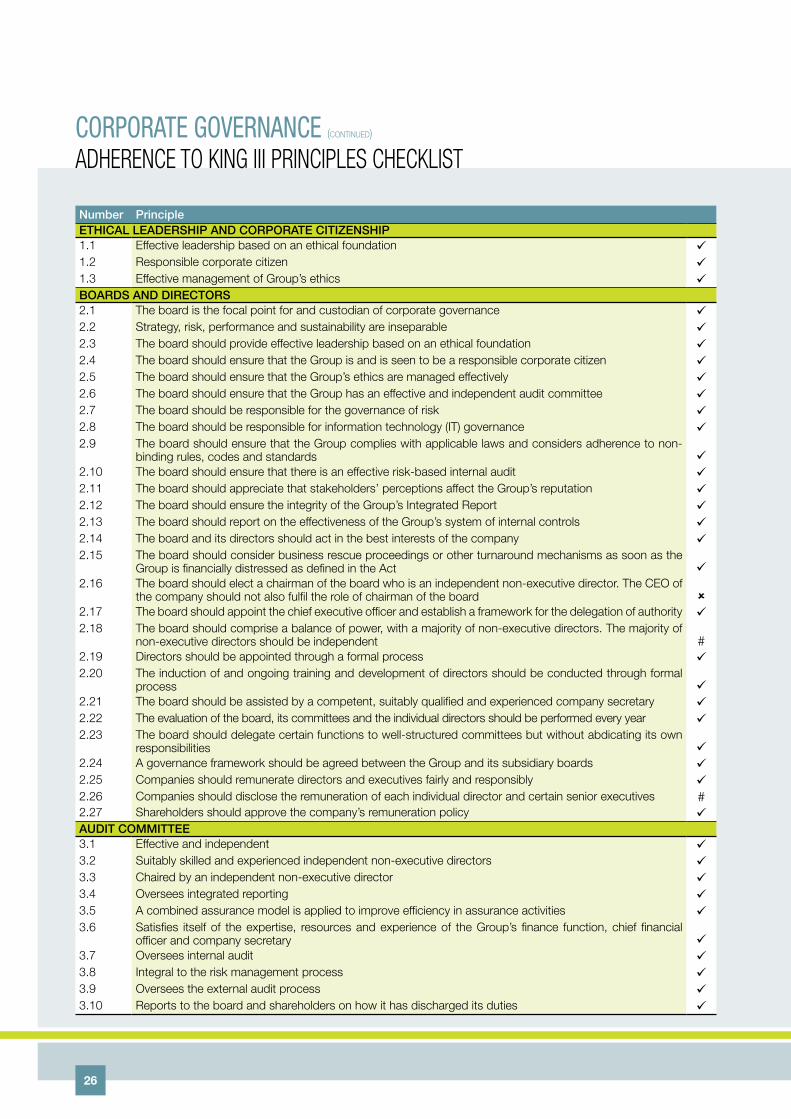

corporate governance (continued)adherenCe to KIng III prInCIples CheCKlIst

number PrincipleeThiCaL LeaDeRShiP anD CORPORaTe CiTiZenShiP1.1 Effective leadership based on an ethical foundation ü1.2 Responsible corporate citizen ü1.3 Effective management of Group’s ethics üBOaRDS anD DiReCTORS2.1 The board is the focal point for and custodian of corporate governance ü2.2 Strategy, risk, performance and sustainability are inseparable ü2.3 The board should provide effective leadership based on an ethical foundation ü2.4 The board should ensure that the Group is and is seen to be a responsible corporate citizen ü2.5 The board should ensure that the Group’s ethics are managed effectively ü2.6 The board should ensure that the Group has an effective and independent audit committee ü2.7 The board should be responsible for the governance of risk ü2.8 The board should be responsible for information technology (IT) governance ü2.9 The board should ensure that the Group complies with applicable laws and considers adherence to non-

binding rules, codes and standards ü2.10 The board should ensure that there is an effective risk-based internal audit ü2.11 The board should appreciate that stakeholders’ perceptions affect the Group’s reputation ü2.12 The board should ensure the integrity of the Group’s Integrated Report ü2.13 The board should report on the effectiveness of the Group’s system of internal controls ü2.14 The board and its directors should act in the best interests of the company ü2.15 The board should consider business rescue proceedings or other turnaround mechanisms as soon as the

Group is financially distressed as defined in the Act ü2.16 The board should elect a chairman of the board who is an independent non-executive director. The CEO of

the company should not also fulfil the role of chairman of the board û2.17 The board should appoint the chief executive officer and establish a framework for the delegation of authority ü2.18 The board should comprise a balance of power, with a majority of non-executive directors. The majority of

non-executive directors should be independent #2.19 Directors should be appointed through a formal process ü2.20 The induction of and ongoing training and development of directors should be conducted through formal

process ü2.21 The board should be assisted by a competent, suitably qualified and experienced company secretary ü2.22 The evaluation of the board, its committees and the individual directors should be performed every year ü2.23 The board should delegate certain functions to well-structured committees but without abdicating its own

responsibilities ü2.24 A governance framework should be agreed between the Group and its subsidiary boards ü2.25 Companies should remunerate directors and executives fairly and responsibly ü2.26 Companies should disclose the remuneration of each individual director and certain senior executives #2.27 Shareholders should approve the company’s remuneration policy üauDiT COmmiTTee3.1 Effective and independent ü3.2 Suitably skilled and experienced independent non-executive directors ü3.3 Chaired by an independent non-executive director ü3.4 Oversees integrated reporting ü3.5 A combined assurance model is applied to improve efficiency in assurance activities ü3.6 Satisfies itself of the expertise, resources and experience of the Group’s finance function, chief financial

officer and company secretary ü3.7 Oversees internal audit ü3.8 Integral to the risk management process ü3.9 Oversees the external audit process ü3.10 Reports to the board and shareholders on how it has discharged its duties ü

26

number PrincipleThe GOveRnanCe OF RiSK4.1/4.2 The board is responsible for the governance of risk and setting levels of risk tolerance ü4.3 The audit committee assists the board in carrying out its risk responsibilities ü4.4 The board delegates the risk management plan to management ü4.5 The board ensures that risk assessments and monitoring are performed on a continual basis ü4.6 Frameworks and methodologies are implemented to increase the probability of anticipating unpredictable risks û4.7 Management implements appropriate risk responses ü4.8 The board ensures continual risk monitoring by management ü4.9 The board receives assurance of the effectiveness of the risk management process û4.10 Sufficient risk disclosure to stakeholders üThe GOveRnanCe OF inFORmaTiOn TeChnOLOGy5.1 The board is responsible for information technology (IT) governance ü5.2 IT is aligned with the performance and sustainability objectives of the Group ü5.3 Management is responsible for the implementation of an IT governance framework ü5.4 The board monitors and evaluates significant IT investments and expenditure ü5.5 IT is an integral part of the Group’s risk management ü5.6 IT assets are managed effectively ü5.7 The audit committee assists the board in carrying out its IT responsibilities üCOmPLianCe WiTh LaWS, CODeS, RuLeS anD STanDaRDS6.1 The board ensures that the Group complies with relevant laws ü6.2 The board has a working understanding of the relevance and implications of non-compliance ü6.3 Compliance risk forms an integral part of the Group’s risk management process ü6.4 The board has delegated to management the implementation of an effective framework and processes üinTeRnaL auDiT7.1 Effective risk-based internal audit ü7.2 Follow risk-based approach to its plan ü7.3 Written assessment of the effectiveness of the Group’s system of internal controls and risk management ü7.4 Be responsible for overseeing internal audit ü7.5 Internal audit is strategically positioned to achieve its objectives üGOveRninG STaKehOLDeR ReLaTiOnShiPS8.1 Appreciation that stakeholders’ perceptions affect the Group’s reputation ü8.2 Management proactively deals with stakeholder relationships ü8.3 There is an appropriate balance amongst the Group’s various stakeholder groupings ü8.4 Equitable treatment of stakeholders ü8.5 Transparent and effective communication to stakeholders ü8.6 Disputes are resolved effectively and timeously üinTeGRaTeD RePORTinG anD DiSCLOSuRe9.1 Ensures the integrity of the Group’s Integrated Report ü9.2 Sustainability reporting and disclosure is integrated with the Group’s financial reporting ü9.3 Sustainability reporting and disclosure is independently assured û

Keyü Compliant# Partially compliantû Not compliant

The Group’s detailed response to the areas of partial or non-compliance is contained in the Corporate Governance report on

page 22.

Seardel integrated annual report 201427

Brits Non-Woven

28

corporate governance (continued)soCIal and ethICs CommIttee report

roleThe committee monitors activities relating to ethics,

stakeholder engagement and the social impact of the

company on communities within which it operates. It also

monitors progress across all areas of strategic empowerment

as well as compliance with transformation codes.

memBerSThe members of the committee consist of Mr A Ntuli

(chairman, executive director), Ms R Watson (independent

non-executive director), Mr S Rubidge (Group IR executive)

and Mr G Wege (executive director).

meetingSThe committee holds a minimum of two meetings per

annum. Additional meetings are convened on request of any

of the members.

The table below records the attendance of committee