insuring the poor against natural...

TRANSCRIPT

INSURING THE POOR AGAINST NATURAL DISASTERS

INNOVATIVE SOLUTIONS

Vijayasekar KalavakondaSenior Financial Sector Specialist

Finance & Markets Global PracticeThe World Bank Group

SESSION – 1: MICROINSURANCE PRODUCT INNOVATION

Microinsurance Marketplace in Indonesia Conference

Shangri-La Hotel, JAKARTA

Asia-Pacific is the world’s most disaster prone region accounting (in 2015) for…

2015 FACT SNAPSHOT ASIA-PACIFIC NATURAL DISASTERS IN 2015

• 45 percent of World’s Natural Disasters• <20 percent of insured losses, and• >41 percent of economic losses

Source: UNESCAP Report (2015)

Insured losses is significantly low compared to expected losses due to natural disasters…

EXPECTED LOSSES PER ANNUM (% OF GDP)UNINSURED LOSS (% OF TOTAL LOSS AND

AVERAGE UNINSURED LOSS PER NATURAL

CATASTROPHE 2004-2011, $BN)

Source: LLOYD’S GLOBAL UNDERINSURANCE REPORT (2012)

In 2010, agricultural insurance penetration ranged from 1.99% of GDP in high-income countries to as low as 0.01% in low-income countries, compared to 3.15% and 0.69% respectively for non-life insurance

1. World Bank support to Agriculture InsuranceWhile agricultural insurance can bring large benefits to vulnerable rural households, the market is still under-developed particularly

in low-income countries

3

Source: Mahul and Stutley (2010)

• Agriculture is an uncertain business, and improvements in risk mitigation, transfer or coping can bring large benefits to vulnerable rural households:

Although it is not a solution to every agricultural risk, agricultural insurance can be a powerful solution as part of an integrated agricultural risk management strategy

It can help prevent vulnerable rural households from falling into deep poverty following a natural disaster, and also improve their access to agricultural credit

• Globally, the market for agricultural insurance is still under-developed, particularly in low-income countries:

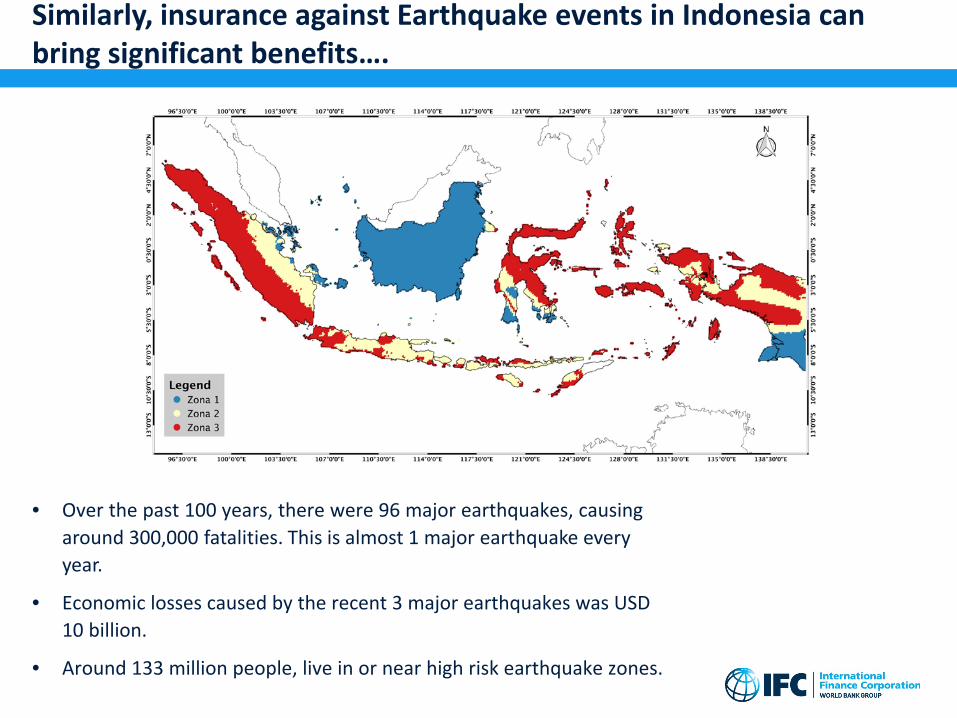

• Over the past 100 years, there were 96 major earthquakes, causing around 300,000 fatalities. This is almost 1 major earthquake every year.

• Economic losses caused by the recent 3 major earthquakes was USD 10 billion.

• Around 133 million people, live in or near high risk earthquake zones.

Similarly, insurance against Earthquake events in Indonesia can bring significant benefits….

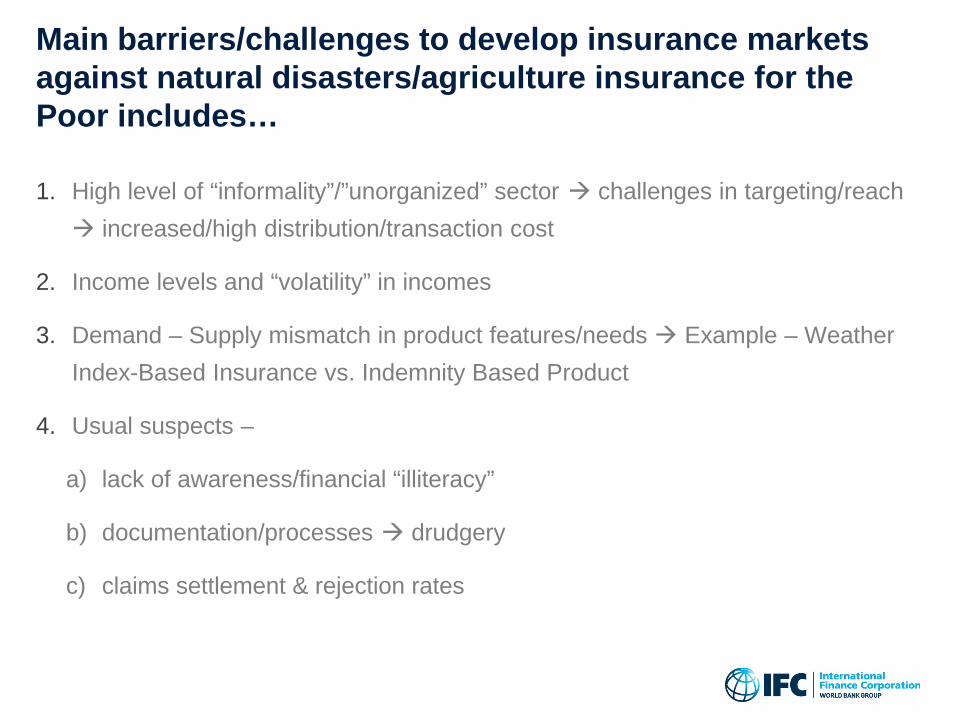

Main barriers/challenges to develop insurance markets against natural disasters/agriculture insurance for the Poor includes…

1. High level of “informality”/”unorganized” sector challenges in targeting/reach increased/high distribution/transaction cost

2. Income levels and “volatility” in incomes

3. Demand – Supply mismatch in product features/needs Example – Weather Index-Based Insurance vs. Indemnity Based Product

4. Usual suspects –

a) lack of awareness/financial “illiteracy”

b) documentation/processes drudgery

c) claims settlement & rejection rates

S-curve demonstrates the empirical relationship between disposable income and insurance penetration

• A minimum GDP per capita of $5,000 appears to be the magic number at which insurance take-up really picks up, as this reflects the growth of an economy's middle class

• For low income countries elasticity between insurance & GDP is around one insurance market growth is at the same pace as GDP

• Portfolio-based Insurance is one solution for such markets

• Publicly funded & social insurance programs are options

Source: insurancelinked.com/the-s-curve/

VIDEO AGBBI

Bahasa Indonesia: https://www.youtube.com/watch?v=G6OSnFCE0RE

English: https://www.youtube.com/watch?v=_YK6uVxsiw4

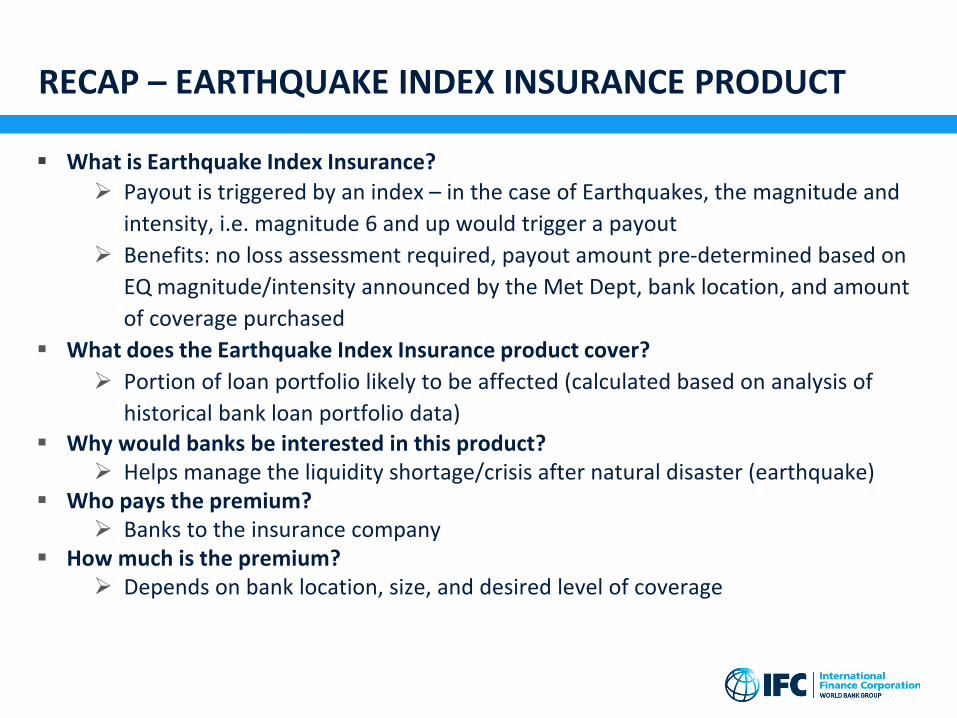

RECAP – EARTHQUAKE INDEX INSURANCE PRODUCT

What is Earthquake Index Insurance? Payout is triggered by an index – in the case of Earthquakes, the magnitude and

intensity, i.e. magnitude 6 and up would trigger a payout Benefits: no loss assessment required, payout amount pre-determined based on

EQ magnitude/intensity announced by the Met Dept, bank location, and amount of coverage purchased

What does the Earthquake Index Insurance product cover? Portion of loan portfolio likely to be affected (calculated based on analysis of

historical bank loan portfolio data) Why would banks be interested in this product?

Helps manage the liquidity shortage/crisis after natural disaster (earthquake) Who pays the premium?

Banks to the insurance company How much is the premium?

Depends on bank location, size, and desired level of coverage

BENEFITS OF EQII – DEVELOPMENTAL IMPACTS

For Banks: Enables continued lending after an event when the community needs it the

most Access to finance: frees up emergency capital reserves to expand lending Can spur growth and profitability of MFI Allows banks to manage risks better

For Insurance Companies: Innovative and new product, not offered anywhere else New opportunity for expanding business Vast potential client base Global reinsurance very interested in this market

EQII TARGET MARKET IN INDONESIA

• BPR (Bank Pengkreditan Rakyat) - Rural Banks • BPRs are only allowed to operate at the province where they are registered• As per May 2015 there are 1,643 BPRs registered in Indonesia with total loan

portfolio reaching 7 billion USD

• BPD (Bank Pembangunan Daerah) - Regional Banks• There is one regional bank per province• Owned by provincial government

• Other Banks, that do not have opportunities for diversifying risk and/or have concentrated geographic presence

INDONESIA EQII PROJECT STAKEHOLDERS

Portion Covered by Insurance

Market Stimulation Data gathering Capacity building

TA in Product Design

Market stimulationLoan

por

tfol

io

MFI

Loan

por

tfol

io

MFI

Loan

por

tfol

io

MFI

Financial Services Regulator

Primary Insurance companies

International reinsurers

TERIMA KASIH