insuring construction risks - hot topics related to ... construction risks - hot topics related to...

TRANSCRIPT

Insuring Construction Risks - Hot

Topics Related to Construction

Defect Claims

• Jeffrey J. Vita – Saxe Doernberger & Vita, P.C.

• Michael J. Donnelly – Murtha Cullina, LLP

• Alice Sherman – Willis of Massachusetts, Inc.

• Kathleen D. Monnes – Day Pitney, LLP

Importance of Insurance and Risk Transfer

Construction Projects . . .

Sometimes Things Go Wrong!

1. Need to make sure that your project is

covered.

2. Need to make sure that you are protected

from claims of others:a) Your insurance

b) Indemnification/Hold Harmless Clauses

c) Additional Insured Clauses

Pre-Job Insurance Issues From the Owner’s Perspective

Indemnification/Hold Harmless Clauses

• Typically provide that, to the extent

permitted by law, the contractor will

indemnify and hold harmless the owner for

any loss, damage or claim arising out of

the work—but frequently exclude damage

to the Work itself—and caused by the

Contractor or anyone working on behalf of

the Contractor.

Indemnification/Hold Harmless Clauses

• Want to ensure that you require that the

coverage extends past the completion

date.

Additional Insured Clauses

• Require that the Owner be named as

Additional Insured on Comprehensive

General Liability Policies.

• Frequently require that Contractor provide

the Owner with a Certificate of Insurance.

• The Certificate does not mean that your

client is covered.

Pre-Job Issues from the Contractor’s Perspective

1. The Owner has pushed liability down to

you, you want to push it down to subs.

2. Do you need Professional Liability

Coverage?

• As construction work changes, lines are

blurring. Contractors are doing design

work, and designers are deeply involved in

installation. Urge your clients to sit down

with you and their insurance professional

to discuss how their work is changing to

ensure that they have the right coverage.

• Contractor deals with the subs using the

same types of tools as the Owner does

with the contractor. This results in a

significant amount of redundancy.

When the claims arise

• Give Notice, and then check the policy and

give notice again to the letter.

• Section 11.3 of the A201 refers to the

Owner as a fiduciary in connection with a

number of scenarios. You will want to

negotiate that down to good faith.

Additional Insured Status

• Typically required by contract

• Contract operates in conjunction with

endorsement

• AI is treated as separate insured with

independent rights to policy

Insurance recommendations

• 1) Commercial General Liability (CGL) with limits of Insurance of not less than $1,000,000 each occurrence and $2,000,000 Annual Aggregate.

• a) If the CGL coverage contains a General Aggregate Limit, such General Aggregate shall apply separately to each project.

• b) CGL coverage shall be written on ISO Occurrence form CG 00 01 10 01 or a substitute form providing equivalent coverage and shall cover liability arising from premises, operations, independent contractors, products-completed operations, and personal and advertising injury.

• c) General Contractor, Owner and all other parties required of the General Contractor, shall be included as insureds on the CGL, using ISO Additional Insured Endorsement CG 20 10 11 85 or CG 2010 (10/93) AND CG 20 37 or CG2033 AND CG2037 or an endorsement providing equivalent coverage to the additional insureds. This insurance for the additional insureds shall be as broad as the coverage provided for the named insured subcontractor. It shall apply as Primary and non-contributing Insurance before any other insurance or self-insurance, including any deductible, maintained by, or provided to, the additional insured.

• d) Subcontractor shall maintain CGL coverage for itself and all additional insuredsfor the duration of the project and maintain Completed Operations coverage for itself and each additional insured for at least 3 years after completion of the Work.

• 2) Automobile Liability

• a) Business Auto Liability with limits of at least $1,000,000 each accident.

• b) Business Auto coverage must include coverage for liability arising out of all

owned, leased, hired and non-owned automobiles.

• c) General Contractor, Owner and all other parties required of the General Contractor, shall be

included as insureds on the auto policy.

• 3) Commercial Umbrella

• a) Umbrella limits must be at least $5,000,000.

• b) Umbrella coverage must include as insureds all entities that are additional insureds on the CGL.

• c) Umbrella coverage for such additional insureds shall apply as primary before any other insurance

or self-insurance, including any deductible, maintained by, or provided to, the additional insured other

than the CGL, Auto Liability and Employers Liability coverages maintained by the Subcontractor.

• 4) Workers Compensation and Employers Liability

• a) Employers Liability Insurance limits of at least $500,000 each accident for bodily injury by

accident and $500,000 each employee for injury by disease.

• b) Where applicable, U.S. Longshore and Harborworkers Compensation Act Endorsement shall be

attached to the policy.

• c) Where applicable, the Maritime Coverage Endorsement shall be attached to the policy

• Waiver of Subrogation

• To the fullest extent permitted by law, subcontractor waives all rights against Contractor, Owner and Architect and their agents, officers, directors and employees for recovery of damages to the extent these damages are covered by commercial general liability, commercial umbrella liability, business auto liability or workers compensation and employers liability insurance maintained per requirements stated above

Evolution of the AI Endorsement

2001 20041985

CG 20 10 11 85

“Arising out of”

CG 20 10 10 01

Excludes coverage

for completed

operations

CG 20 10 07 04

Replaces

“arising out of”

with “caused in

whole or in part.”

Excludes

completed

operations

CG 20 37 10 01

Reinstates

completed

operations coverageCG 20 37 07 04

Reinstates

completed

operations coverage

AI Insurance – Primary v. Excess

• As AI, GC is entitled to same protection as

named insured (sub)

• Make sure contract and policy are clear

that sub’s insurance (primary and excess)

will act as primary with GC’s insurance as

excess

Comprehensive Coverage is Critical

Essential Insurance for Constr. Projects

A. “Third Party Coverage”

CGL – Primary, Umbrella, AI,

Wrap-ups

Professional Liability – A&E, CM,

OPPI, CPPI, Wrap-ups

B. “First Party” Coverage

Builders Risk – Physical Loss and

Business Interruption

Coverage Deficiencies

All insurance programs have holes!

♦ Coverage Grant Restrictions

♦ Exclusions

♦ Deductibles/SIRs

♦ Sublimits

♦ Time Limits

♦ Waiting Periods

♦ Valuation Conditions

Disputes arise over the application and meaning of such policy limitations.

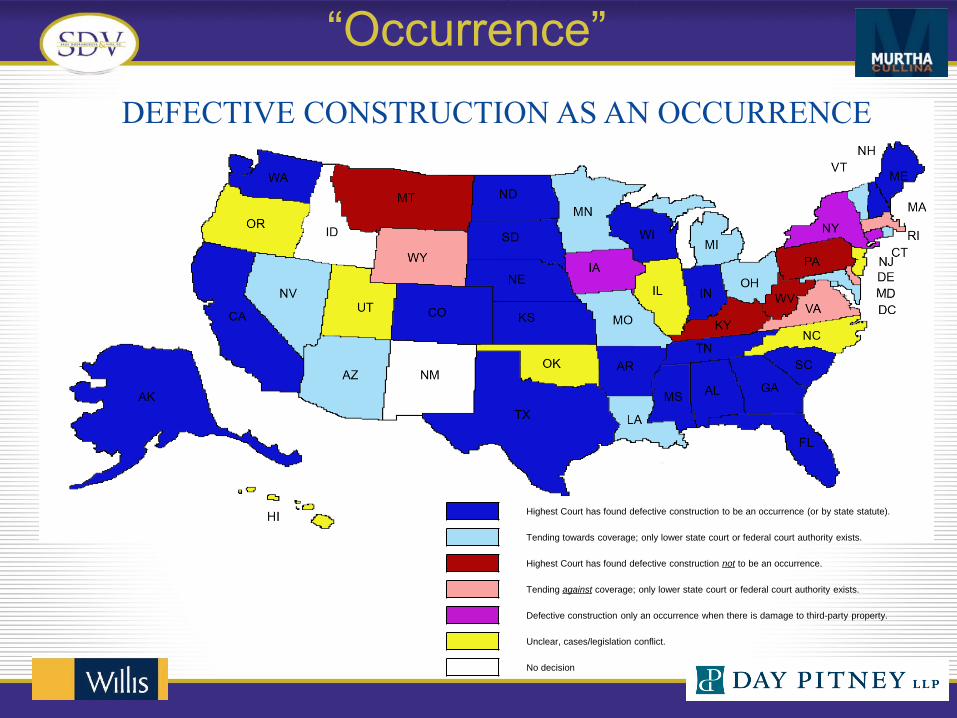

“Occurrence”

DEFECTIVE CONSTRUCTION AS AN OCCURRENCE

Highest Court has found defective construction to be an occurrence (or by state statute).

Tending towards coverage; only lower state court or federal court authority exists.

Highest Court has found defective construction not to be an occurrence.

Tending against coverage; only lower state court or federal court authority exists.

Defective construction only an occurrence when there is damage to third-party property.

Unclear, cases/legislation conflict.

No decision

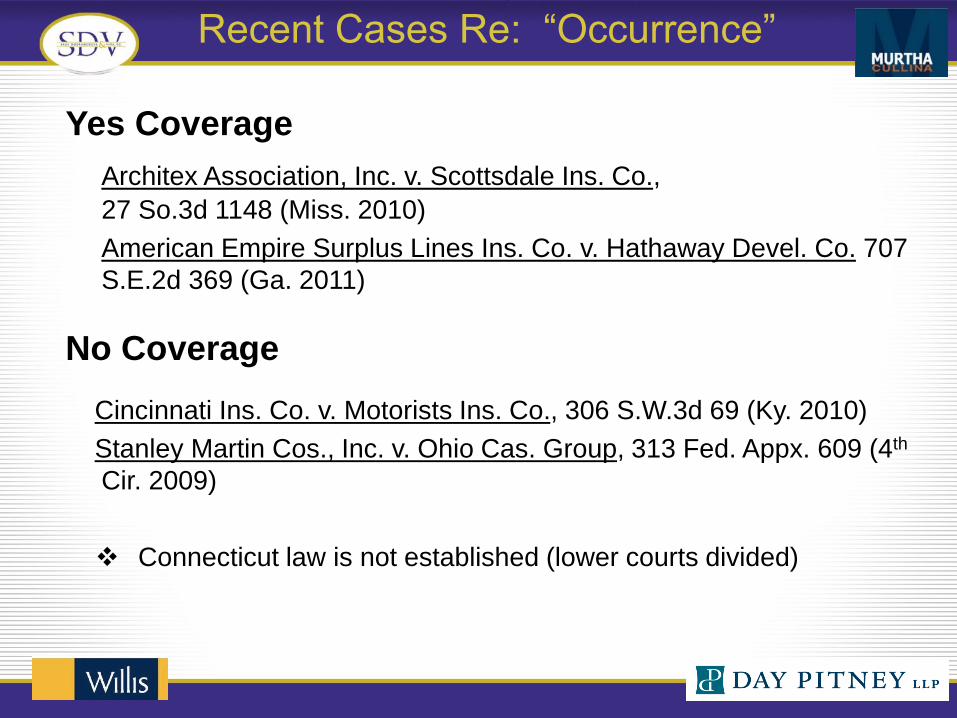

Recent Cases Re: “Occurrence”

Yes Coverage

Architex Association, Inc. v. Scottsdale Ins. Co.,

27 So.3d 1148 (Miss. 2010)

American Empire Surplus Lines Ins. Co. v. Hathaway Devel. Co. 707

S.E.2d 369 (Ga. 2011)

No Coverage

Cincinnati Ins. Co. v. Motorists Ins. Co., 306 S.W.3d 69 (Ky. 2010)

Stanley Martin Cos., Inc. v. Ohio Cas. Group, 313 Fed. Appx. 609 (4th

Cir. 2009)

Connecticut law is not established (lower courts divided)

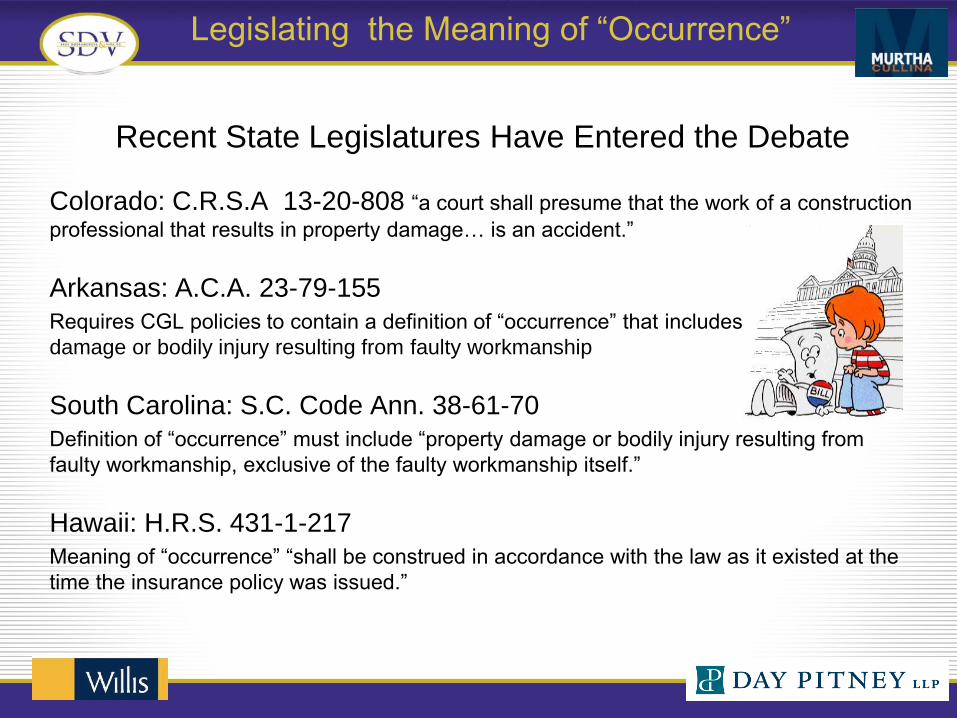

Legislating the Meaning of “Occurrence”

Recent State Legislatures Have Entered the Debate

Colorado: C.R.S.A 13-20-808 “a court shall presume that the work of a construction

professional that results in property damage… is an accident.”

Arkansas: A.C.A. 23-79-155

Requires CGL policies to contain a definition of “occurrence” that includes “property

damage or bodily injury resulting from faulty workmanship

South Carolina: S.C. Code Ann. 38-61-70

Definition of “occurrence” must include “property damage or bodily injury resulting from

faulty workmanship, exclusive of the faulty workmanship itself.”

Hawaii: H.R.S. 431-1-217

Meaning of “occurrence” “shall be construed in accordance with the law as it existed at the

time the insurance policy was issued.”

Risk Transfer

Additional

Insured

Coverage

3rd Party Liability

Insurance

CGL

Professional

Pollution

1st Party

Insurance

Subcontractor

Indemnity

Commercial

Property

Builders Risk

Contractual Rights

Subcontractor

Default Insurance

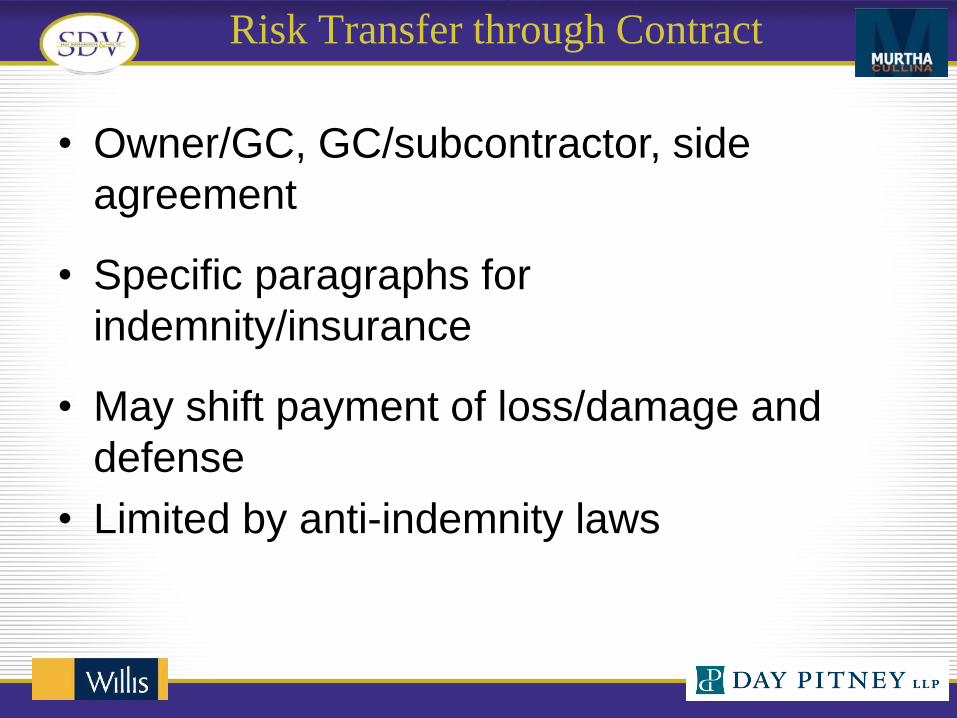

Risk Transfer through Contract

• Owner/GC, GC/subcontractor, side

agreement

• Specific paragraphs for

indemnity/insurance

• May shift payment of loss/damage and

defense

• Limited by anti-indemnity laws

Contractual Indemnity v. AI Coverage

• AI coverage and indemnity operate

independently

• AI coverage determined by policy and AI

endorsement

• AI coverage not limited by states’ anti-

indemnity laws (exceptions)

CGL Ins. Emerging Issue – Allocation

Horizontal Exhaustion – Primary Policies Pays First

Vertical Exhaustion – Sub’s Policies Pay First

Promise to Procure

Insurance

Sub-Contractor

(“Sub”)

General Contractor

(“GC”)

GC’s Corporate

Primary Insurance

GC’s Corporate

Excess Insurance

Sub’s Primary

Insurance

(GC’s AI Carrier)

Sub’s Excess

Insurance

(GC’s AI Excess Insurance)

Promise to Indemnify

Questions

Jeffrey J. Vita

Saxe Doernberger & Vita, P.C.

(203) 287-2103

Michael J. Donnelly

Murtha Cullina, LLP

(860) 240-6058

Alice Sherman

Willis of Massachusetts, Inc.

(860) 989-4341

Kathleen D. Monnes

Day Pitney, LLP

(860) 275-0103