insurance risk management product design & development

TRANSCRIPT

Confidential 1

Insurance Risk Management

Product Design & Development

Underwriting

Pricing

Strategy, Policies and Procedures

18 May 2016

YOU.0020.0001.0002

2 Confidential

Contents

1. Scope & Purpose ............................................................................................................................. 3

2. Risk Management Framework ......................................................................................................... 3

3. Objectives ........................................................................................................................................ 3

4. Insurance Risk Management Strategy ............................................................................................. 4

4.1 Product design and development strategy .............................................................................. 4

4.2 Pricing Strategy ....................................................................................................................... 8

4.3 Underwriting Strategy ............................................................................................................ 12

5. Procedures and Controls ............................................................................................................... 16

5.1 Product development procedures ......................................................................................... 16

5.2 Pricing procedures ................................................................................................................ 17

5.3 Underwriting procedures ....................................................................................................... 17

6. Monitoring and review of the insurance risk management framework .......................................... 18

6.1 Approval by the Board of Directors ....................................................................................... 18

6.2 Independent review of IRMS compliance ............................................................................. 19

Appendix 1. Product Development Process ...................................................................................... 20

Appendix 2. Pricing Process ............................................................................................................. 21

Appendix 3. Underwriting Process .................................................................................................... 22

Appendix 4. Actuarial Underwriting Process ..................................................................................... 23

YOU.0020.0001.0003

Confidential 3

1. Scope & Purpose

This document relates to the insurance operations of regulated subsidiaries of Youi Holdings Pty Ltd

(“Youi”), including Youi Pty Ltd and Youi NZ Pty Ltd.

The overall purpose of this document is to outline strategies, policies and procedural guidelines

currently implemented and specifically relating to:

Product Design & Development

Underwriting

Pricing

The above areas represent key elements of Youi’s Insurance Risk Management Framework (IRMF).

The following information will identify all management responsibilities and controls designed to ensure

appropriate and effective risk management procedures are implemented and maintained within these

areas to ensure both quality and integrity of the IRMF.

2. Risk Management Framework

This document forms part of the risk management framework of Youi and is derived from the insurance

risk management arrangements of the Outsurance Holdings group (“Outsurance”). This document will

be reviewed and monitored regularly by the Executive Committee (Exco) and the Board. Senior

managers and designated employees are responsible for adherence, management & control at an

operational level. Authority has been delegated to senior employees for certain responsibilities within

the risk management framework.

Strategies, policies & procedures are subject to continual refinement as the business grows and

develops, with new lines of business or geographies covered.

3. Objectives

Insurance risk is defined as the risk that inadequate or inappropriate underwriting, product design and

pricing will expose an insurer to financial loss and the consequent inability to meet its liabilities. The

Insurance Risk Management Strategy (IRMS) has been developed by Youi to ensure the company’s

product design and development, pricing and underwriting activities are prudently and soundly

managed.

YOU.0020.0001.0004

4 Confidential

The key objectives of the IRMS which aim to mitigate insurance risk include:

Product development principles and guidelines encouraging development of new innovative

products or product enhancements which do not unnecessarily expose the company to undue

risks, produce underwriting and business profitability for Youi, but also seek to be cost-effective

from a consumer standpoint.

Pricing principles and procedures developed in accordance with Youi’s actuarial guidelines and

taking into consideration impacting market forces, designed specifically to minimise the risk of

inaccurate pricing. Procedures have also been created to timeously detect potentially

dangerous deviations of actual experience compared to estimates allowed for in premium

calculations.

Underwriting processes integrated into the operating system and workflow which allow for the

enforcement of sound underwriting principles to balance the objective of effectively managing

risk and exposure against the need to write sufficient business to cover overheads.

4. Insurance Risk Management Strategy

The Board, assisted by the Exco, is ultimately responsible for the Insurance Risk Management Strategy.

4.1 Product design and development strategy

Product design involves the introduction of a new product or the enhancement or variation of an existing

product. Youi currently intends only to provide cover for the traditional personal lines risks. These

include:

Residential Building

Householder’s Contents

Personal Property – all risks

Motor Vehicle

Motorcycle

Caravan & Trailer

Pleasurecraft – specific trailer vessels

Personal Liability and Sole Trader/Small Commercial Business Liability

The perils covered include Insurance Industry standard accidental damage, storm & tempest, theft and

liability perils.

If a new product or an enhancement of an existing product will be introduced by Youi, the following

procedures are to be followed:

YOU.0020.0001.0005

Confidential 5

4.1.1 A business case needs to be provided

A sound business case for any new product development or enhancement must be developed and

should include the motivation underpinning the requirement for a new product or enhancement. For

example, this motivation may have been initiated by Youi’s Sales and Client Services employees,

identifying a specific client need. This need may have been created by either a product currently being

offered in the market via a competitor, or an additional product feature is identified which adds value to

Youi’s existing offering. Further attributes of a sound business case would also include; consistency

with organisational goals & objectives, current product positioning, prior evidence of product

underwriting and expense profitability and specific market entry requirements.

4.1.2 Product Review Committee

Department Managers will review the business case to initially determine the feasibility of the new

product or enhancement, in terms of market acceptance & positioning. Should the business case not

be feasible, it will be dispensed without further consideration, with reasons for rejection being

documented. However, if upon agreement by Department Managers there is substantial benefit to Youi

via the introduction of a new product or enhancement; it will be submitted to Actuarial for further review

and testing.

4.1.3 Market Testing

Market testing is required for all new products. This testing is completed to determine if there is a

significant market need for a new product and what the market expectations would be concerning

product benefits and features. Market surveys and focus groups would be the most appropriate

research vehicles for new product testing, with this function most likely being outsourced to specialist

market research companies. For existing product development & enhancements, the decision on

whether market testing will be required resides with Actuarial and will take into account the following

rationale:

Significance of product enhancement

Cost-Benefit Analysis

Market Impact Analysis

Should the result be substantial in these cases, then market testing/research will be approved. If the

Actuarial decision determines it is only a minor or insignificant product development or enhancement or

if the enhancement will simply bring Youi up to the level of products already offered in the market,

market testing will not be conducted.

YOU.0020.0001.0006

6 Confidential

4.1.4 Cost/benefit analysis

This process will be completed to determine the viability of a new product or substantial product

enhancement, as well as prioritise the development if there are multiple new products currently

positioned for potential market release. The analysis will require a projected income statement to be

documented for the new product to determine the long term cost/benefit arising from it. This may take

the form of a variation to the latest business plan, rather than a stand-alone projected income statement.

The achievement of the required return on capital, as required by The Board, will also be tested as part

of this process. This process will be balanced against the need to offer a cost-effective product offering

to clients as a requirement to ensure adequate sales volumes and sustainability of the product. If this

balance is unable to be achieved as a result of this analysis e.g. resulting from high expenses

associated with the product, then the new product idea will be rejected at this stage, with reasons

recorded.

The impact on the amount of capital and/or reinsurance required by the company and impact on the

expected break-even date will also be considered in this analysis. Any initiative which has material

capital, reinsurance or break-even implications will require more careful planning and approval.

4.1.5 Risk identification and assessment

To determine which potential risks, accumulations and concentrations emanating from the new product

are relevant, actuarial risk identification and assessment will be undertaken. The exposure resulting

from the product will be modelled via scenario modelling, using the projected income statement.

4.1.6 Requirements for limiting risk

Various measures can be taken to limit the risk/exposure. These include:

Limits on the benefits provided – no unlimited liability to be provided.

Diversification must be achieved across different groups and geographical areas to reduce the

risk of concentration and accumulation.

Various Reinsurance measures will also be considered to limit the size of individual exposures

as well as aggregate catastrophe exposures. The greater the uncertainty, the lower the

retention levels that will be sought.

4.1.7 Policy documentation and signoff

Following completion of the above processes, all new product developments and enhancements will be

forwarded to the Exco, who will ultimately be responsible for final sign off and policy wording review.

Should the new product be substantial or enhancement likely to impact significantly on business

operations, the Exco will subsequently seek Board approval before a product implementation plan is

initiated. In the event, a product enhancement is not substantial, i.e. operational impact is only minor,

YOU.0020.0001.0007

Confidential 7

then the Exco will ensure the development is forwarded directly for implementation, whereby a Project

Plan for product implementation will be developed by Actuarial.

The Project Plan will be forwarded to various Departments for further creative work and testing, inclusive

of – IT, Compliance, Claims, Communications, Marketing and external legal review. The Project Plan

will include the following schedule items as well as responsible persons, due dates and dependencies:

Computer administration system specification

Development and testing plan

Documentation changes including wordings, schedules and scripting on system

Communication to staff

Training of staff and updating of training manuals

Marketing plan

Development of reports to measure progress/success of new product

4.1.8 Levels of delegation for approval

The levels of delegation for the approval of a new product will depend on the following:

1. Additional capital requirements for new product or enhancement; and

2. Higher Degree of risk/uncertainty associated with new product or enhancement in comparison

to existing products

If any of the factors described above are present, full Board approval will be required to proceed with

such a product. Any other product changes, regardless of how insignificant it may appear, will require

approval of the Exco.

4.1.9 Post implementation review

A post implementation review is critical to determine if the new product or enhancement is performing

as expected, or otherwise. Data Warehouse reports will enable the measurement of all assumptions as

prescribed in the model income statement and developed as part of the cost/benefit analysis. This will

enable the speedy identification of deviations from expected numbers to allow corrective action to be

taken, if required. In the case of a new product or enhancement performing poorly, with limited corrective

measures available to alter performance, the post implementation review will allow for the product to

be discontinued before any significant adverse damage has impacted upon the business. Conversely,

this post implementation review will also identify reasons for a new product or enhancement performing

above expectations.

YOU.0020.0001.0008

8 Confidential

4.1.10 Monitoring compliance

Elements of the compliance monitoring will be conducted using data warehouse reports. Audits will be

undertaken on policies and claims to ensure correct application of policies and procedures. Client

satisfaction surveys and Youi wall feedback analysis will also be conducted to ensure the client

experience of the new product has been accepted, as intended. These surveys will also enable Youi to

receive valuable feedback regarding possible product improvements or alterations.

4.1.11 Product Evolution

Over time, it is expected that policy wordings will be reviewed and updated no less than once a year.

This evolution will respond to observations relating to claims trends, contentious/claimsco claims, IDR

matters and formal feedback from operational departments, including sales, retention, client services

and all parts of claims. A formal sharepoint site will be maintained to allow suggested enhancements

to be logged.

The actuarial department will be responsible for managing the timely update and maintenance of the

Product Disclosure Statements (PDS) including aspects not specifically related to the insurance product

that are also contained in the PDS.

Changes to the PDS will be reviewed by a committee comprising all relevant operational and support

areas with all wording changes signed off by a representative of each area.

Where a major change in product design is proposed, the Board will be informed and the process

described earlier in this section will be followed. Examples of such a major change include covering

flood when flood previously was not covered.

4.2 Pricing Strategy

Pricing of an insurance product involves the estimation of claims costs and other business costs arising

from the product and the estimation of investment income arising from the investment of the premium

income attaching to the product. Pricing risk may occur where the claims, costs, or investment returns

arising from the sale of a product are inaccurately estimated.

4.2.1 Delegation of Pricing Authority

The Youi Board approved delegation of authority in relation to pricing and underwriting is included in

the company Delegation of Authority document. This is categorised in 6 ‘Tiers’, examples of which

include:

Tier 0:

YOU.0020.0001.0009

Confidential 9

Where an underwriting change has been implemented since a policy was written in conjunction

with a pricing change. The price must be adjusted manually at the same time the underwriting

is over-ridden.

Override of driving suspension relating to ‘acceptable’ reasons such as medical conditions.

Tier 1:

Discounts of more than 50% per individual policy

Adding new vehicles or areas

Other underwriting overrides including Flood area reviews

Tier 2:

Changes to rating differentials or underwriting rules affecting less than 10% of quotes

Accepting risks with sums insured of more than the upper limits of current XOL treaties

Underwriting overrides where precedent is set where no override has previously been done

Changes to the discount authority by skill set

Tier 3:

Changes to rating differentials or underwriting rules affecting more than 10% of quotes

Tier 4:

Changes to the absolute level of the premium rate in any capital city

Tier 5:

Changes to the Pricing & Underwriting Strategy

Formal processes are maintained in sharepoint to record pricing changes made in accordance with

Tiers 1 to 5.

4.2.2 Risk identification and assessment

Risk identification and assessment is undertaken by means of monitoring various reports. These

include:

Claim frequencies, average claim size and loss ratio by each rating factor as well as certain

combinations of rating factors. This is also referred to as one-way and multi-way analysis.

Analysis is conducted over various time periods to identify possible trends.

Analysis is also performed by the period in which the business was underwritten to determine

the performance of the different underwriting and rating policies.

Exposures by region or suburb to determine potential losses and accumulations.

YOU.0020.0001.0010

10 Confidential

4.2.3 Reflecting Emerging Experience in Prices

Premiums are determined on a cost plus basis. A generalised linear model is fitted to claims and

exposure data to estimate the underlying risk premium. Allowance is factored for expenses and then

the cost of capital to arrive at the internal office premium, excluding government charges. Expenses are

divided between those varying according to the number of claims, amount of claims, number of policies

and premium amount to be able to achieve the most accurate premium loadings for these expenses.

The model is updated on an ongoing basis to reflect changes in experience. Adjustments to the

premiums of existing clients are also reviewed on a monthly basis to reflect the latest changes in

underlying experience and inflationary forces on costs.

In addition, analysis of sale success by means of conversion rate analysis and mix of business analysis

will be used to highlight segments where potential underpricing exists.

4.2.4 Profit and loss analysis/Monitoring price movements

Loss ratios and operating ratios are monitored per period and per underwriting period to determine the

effect of pricing changes on profitability of the different tranches of business that were subject to

different prices.

The development of profit margins on tranches of business over time is also projected to estimate

ultimate profitability of the different tranches of business.

Business performance and material price changes are report to the Exco monthly and the Board

quarterly, including product and underwriting period breakdowns as appropriate.

4.2.5 Price discounting and extended underwriting authorities

Price discounting authorities are controlled via SUMMIT. Mandates vary according to staff classification

on SUMMIT.

In sales areas, the default maximum discount available is 10% with the team manager able to override

this to 15%. Client care and retention employees on some policies will have up to 50% discount.

The client services and retention department managers have discount authority up to 35% to allow

timely processing of customer grievances arising due to staff errors. They also have access to extended

ranges of agreed value to allow agreed values to be reset to the previous value in cases of an erroneous

change.

Client services and retention department managers also have access to allow the addition of optional

covers on a policy at times when ordinarily the options would not be available.

The Chief Actuary and senior Actuaries are able to give up to 100% discount and have further

extensions to agreed value ranges.

YOU.0020.0001.0011

Confidential 11

The absolute maximum discount is set by reference to the target operating margin and appropriate

delegation controls. Discounts resulting in an expected loss can therefore not be authorised unless

there are mitigating circumstances.

The normal agreed value ranges are selected based on the underlying vehicle (car or motorcycle), its

usage and the glass-guide value of the vehicle.The main category of mitigating circumstances is

correcting staff or systems errors. Such discounts can only be applied once necessary processes have

been completed, including the review of the sales call in question and entry of the feedback item in the

compliance process.

All discounts will be monitored using standard data warehouse reports.

4.2.6 Process for pricing to respond to competitive and other external environmental

pressures

Market pricing and environmental changes must be monitored carefully to enable premium adjustments

to be implemented wherever necessary. Examples of external influences are:

changes in cost due to climate changes

changes in legislation

demographic trends

economic trends

changes in the level of competition. Competitor premiums will be used as a guideline but not

as the main determinant of pricing in future, as the pricing philosophy is primarily based on a

cost plus system.

4.2.7 Monitor deviations of actual price from technical underwriting pricing

Given the centralised business model and the small mandates provided to sales advisors, the deviation

from the technical underwriting pricing will be small. However, deviations are monitored by calculating

the ratio between actual prices and the true underlying prices on a monthly basis. These ratios are also

affected by updates to the underlying technical rates over time as the latest technical rates are used for

this comparison. These ratios are also used in the renewal process of existing clients.

4.2.8 Monitoring Compliance

The Youi premium calculation is centralised and controlled from a single source. This means premiums

cannot be varied from the true price except for the discounting mandates. Discounting mandates are

small and also system controlled, based on the seniority of the responsible employees.

Discount reports are reviewed regularly to monitor the discount averages, maximums and discounts

per individual sales person. Where discounts exceed targets, sales commission is adjusted downwards.

In a worst case scenario, the mandate can also be removed.

YOU.0020.0001.0012

12 Confidential

Risk exists around data being collected that does not reflect the actual situation of the customer. Such

errors result in premium leakage. Adherence of sales advisors to mandatory scripting, as well as

following appropriate sales processes including faithfully reflecting customers’ answers in data entry,

providing accurate advice and not leading customers is monitored through call audits performed by

sales managers and group risk and compliance. Where errors are found, the appropriate feedback

loops are completed and the advisors appropriately trained on correct approach.

Additional data quality analysis is performed using routine MIS reports of mix of business by key factors

and characteristics such as address match rate. Automated outlier reporting is also used to identify

improbably mixes of data at an individual advisor or team level.

4.3 Underwriting Strategy

Underwriting is the process by which an insurer determines whether or not to accept a risk and, if

accepted, the terms and conditions to be applied and the level of premium to be charged. Weaknesses

in the underwriting process and in the types and levels of controls and systems can expose an insurer

to the risk of operational losses which may threaten the long-term viability of the insurer.

4.3.1 Youi’s willingness and capacity to accept risk

The Outsurance group, inclusive of Youi, has a preference to large volume, small risks which are

independent and not exposed to undue accumulation risks. For this reason Youi will only cover personal

lines risks for industry standard conventional perils. Youi also believes in buying adequate reinsurance

cover to provide protection against volatility. Two important principles which are followed in deciding

whether to accept a risk or not, are:

If the risk is exceptionally complex, it should not be underwritten and therefore declined.

A price cannot be fixed for a moral risk.

4.3.2 Youi’s risk appetite and geographical scope

Youi only intends on underwriting personal lines classes of business and sole trader/small commercial

lines. These currently include motor, householders and houseowners, motorcycles, caravan/trailer,

watercraft and (small) business liability.

The geographical areas in which these classes are underwritten are all states and mainland territories

of Australia and New Zealand excluding:

Northern Territory (All products)

WA North of Geraldton (Home insurance)

Locations identified as having greater than 1% ARI Flood Risk (Home insurance)

YOU.0020.0001.0013

Confidential 13

4.3.3 Formal Risk Assessment Process

Criteria for risk assessment.

o The criteria for risk assessment are similar to those used for premium rating including

some additional factors. These factors include: age, licence type, licence duration,

previous claims experience, licence demerit points, risk address, use, security, vehicle

model, safety features like ABS, vehicle modifications etc.

Methods for monitoring emerging experience.

o Emerging experience is monitored for each level of criteria. Single way and multi way

analysis is conducted. Ultimately this will provide an indication of the effectiveness of

current measures and whether any changes are required or not.

Methods by which emerging experience is used in the underwriting process.

o Based on the analysis completed, thresholds for underwriting processes can be altered

to improve underwriting. Insured amounts above a certain threshold will activate

additional questions to be asked to enable additional underwriting to be completed.

Thresholds for the acceptance of risks can also be altered, depending on the results of

the analysis. Special conditions will also be activated, based on certain criteria and

these can also be altered, based on the results of the analysis.

o A post claims underwriting review is also conducted. This review takes the form of an

increase in the requirements set for risks, increases for excesses, limitations or

exclusions of cover, endorsements, or in the worst case example - cancellation of

cover. A formal multi-claimant process is used to identify outlier risks based on their

experience and to actively manage them and align them within the scope of

underwriting guidelines.

4.3.4 Approval authorities and Definitive limits

Underwriting rules and authorities are programmed into SUMMIT. All information & data is centralised,

with no brokers using separate systems. There are two (2) levels of approval.

Underwriting limits.

o Risks above these limits (driven by the value of the insured item or certain other risk

profiles) are automatically referred to the Actuarial department. These risks cannot be

accepted without the necessary approval by Actuarial. These approvals will require

additional information and only certain Actuarial employees will possess the system

authority to process these approvals. A username and password is also a requirement

for this process.

o Within the actuarial function, 6 Tiers of underwriting delegation exist as outlined in the

Board-approved delegation of authority.

Tier 0:

YOU.0020.0001.0014

14 Confidential

Where an underwriting change has been implemented since a policy was

written in conjunction with a pricing change. The price must be adjusted

manually at the same time the underwriting is over-ridden.

Override of driving suspension relating to ‘acceptable’ reasons such as medical

conditions.

Tier 1:

A list of ‘acceptable review’ items is maintained in sharepoint. This list shows

‘knockout reasons’ which are acceptable for review.

A member of the department may prepare a formal document, stored in

sharepoint, outlining the risk and recommendation for acceptance or rejection

and any additional conditions or premium loadings.

The authorised team member will review the document and then formally

approve, reject or approve with further changes.

Following approval necessary overrides and conditions are applied.

Examples include high value individual items or high value buildings or

contents in home insurance,

Tier 2:

For extremely high value premises where facultative reinsurance is required,

or other precedents, a similar process to a Tier 1 is followed, except two

delegated team members must approve.

Underwriting overrides where precedent is set where no override has

previously been done

Tier 3:

Changes to underwriting rules affecting more than 10% of quotes will be

discussed in the actuarial forum including the CEO, Chief Actuary and Group

Actuary and as appropriate minuted for action.

Tier 4:

Are presented to and approved by the Exco

Tier 5:

Changes to the Underwriting Strategy are approved by the Board.

Reinsurance limits

o Risks above these limits (driven by the value of the insured item) are automatically

referred to the Actuarial department. These risks cannot be accepted without

appropriate additional reinsurance being arranged, as described in the Reinsurance

Management Strategy (REMS). Tier 2 Approval must be gained from two of the Group

YOU.0020.0001.0015

Confidential 15

Head of Actuarial, Youi Chief Actuary and Experienced Actuary before an override is

performed. They will ensure appropriate reinsurance cover is in place. Reports are

also generated to ensure these limits have not been breached.

Cover limits.

o These represent absolute limits of cover. No risks above these limits may be accepted.

No overrides are permitted to accept risks above these limits. These limits represent

the level beyond which even facultative reinsurance will not be purchased due to the

unique nature of the individual risks and the specialist assessment required. Reports

are also generated to ensure these limits have not been breached.

4.3.5 Risk and aggregate concentration limits

These limits are controlled as follows:

1. Risk limits are programmed within the insurance administration system and cannot be accepted

without the required authority and processes being followed.

2. Risks above thresholds at individual addresses are referred to the Actuarial/Underwriting

department to underwrite and evaluate the concentration at the specific address.

3. Aggregate concentrations per suburb or region are monitored by means of standard

aggregation reports and are reported to the Board quarterly.

4.3.6 Monitoring compliance

Risk and Compliance.

o Risk and Compliance will conduct audits as part of their audit plan to confirm that:

Policy Definitions were applied as per the underwriting requirements.

All website scripting, including additions and proposed changes, were passed

through the Youi business and compliance sign-off regime; and that no

variations were included without such sign-off.

Service Quality.

o Service Quality will conduct audits as part of their audit plan to confirm that:

Where customer contact took place by telephone, scripting was read by

employees as prescribed by the system, in particular mandatory scripting.

Where customer contact took place by telephone, all questions were conveyed

accurately by Youi employees, and that the information was fully understood

and accepted by clients.

All overrides, approvals and discounts were conducted per approved business

rules. To this end exception reports are used to identify potential problem

areas; including analysis of data grouped by product, risk, period, team and

responsible persons.

Team Managers.

YOU.0020.0001.0016

16 Confidential

o Team Managers will conduct audits as part of their audit plan to confirm that:

Where customer contact took place by telephone, scripting was read by

employees as prescribed by the system, in particular mandatory scripting.

Where customer contact took place by telephone, all questions were conveyed

accurately by Youi employees, and that the information was fully understood

and accepted by clients.

Reviews by Department Managers or portfolio management.

o Department Managers will review and report on portfolio performance and individual

underwriting quality assessments on a monthly basis. These reports will be discussed

at general management meetings.

Peer review.

o Peer review is completed on a regular ongoing basis with policies written being

randomly selected for evaluation. The whole underwriting process is confirmed, voice

recordings are reviewed and feedback is provided to Department managers and

employees regarding potential problem areas, where additional training may be

required.

Assessment of broker procedures.

o Not relevant because of direct business model negates the requirement for brokers.

Audits of ceding companies.

o Not relevant as Youi is only a direct writer and not a reinsurer.

5. Procedures and Controls

5.1 Product development procedures

All product development procedures and controls forming part of the Insurance Risk Management

Framework are illustrated in Appendix 1: Product Development Process, inclusive of:

Establishing a business case for new or enhanced products;

Product Review Committee

Actuarial Review

o Market testing and analysis;

o Cost/benefit analysis;

o Impact Study;

o Risk identification and assessment;

Requirements for limiting risk e.g.: diversification, exclusions and reinsurance (including

confirmation that either the existing reinsurance will provide protection or new reinsurance

protection is being provided);

YOU.0020.0001.0017

Confidential 17

Executive Committee (Exco) Review;

Board Review (where applicable);

Project Plan including Specifications; Scoping; Development Testing & Implementation

(including milestones);

Processes to ensure policy documentation is adequately drafted to ensure both organisational

& legal compliance;

Clearly defined and appropriate levels of delegation for approval of all material aspects of

product design;

Post-implementation review; and

Methods for monitoring compliance with product design policies and procedures.

5.2 Pricing procedures

Youi’s pricing procedures and controls forming part of the Insurance Risk Management Framework are

illustrated in Appendix 2: Pricing Process.

This process reflects product pricing being responsive to competitive and other external environmental

pressures via:

Pricing Drivers

o Claims loss Ratio

o Claims Risk Identification

o Emerging Experience

o Profit/Loss Analysis

o Competition Analysis

o Sales Conversion

Review and implementation is conducted at the following levels of authority within Youi

Board Review

Actuarial Review

o MIS

The Exco

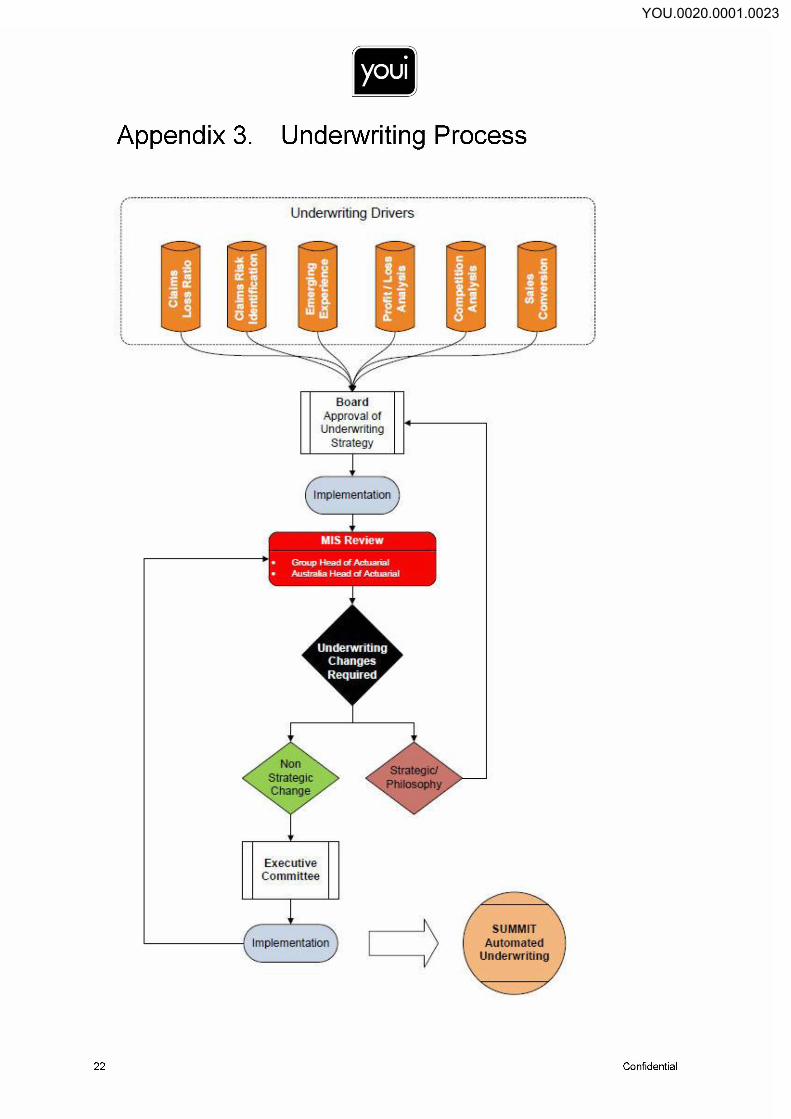

5.3 Underwriting procedures

Actuarial & Underwriting procedures and controls forming part of the Insurance Risk Management

Framework are illustrated in Appendix 3: Underwriting Process and Appendix 4: Actuarial Underwriting

Process, these include:

Details of the formal risk assessment process in the underwriting of insurance including:

o the criteria used for risk assessment;

YOU.0020.0001.0018

18 Confidential

o the process for monitoring emerging experience; and

o the process by which the emerging experience is taken into consideration in the

underwriting process;

o the process for setting approval authorities and the definitive limits to those authorities

(including controls surrounding delegations given to intermediaries of the insurer);

o consideration of risk and aggregate concentration limits; and

o the process for monitoring compliance with underwriting policies and procedures such

as:

1. internal audit (where it is established that the internal audit unit has the appropriate

skills and experience to perform such activities);

2. reviews by Department Managers or portfolio management;

3. peer review of policies underwritten (including details of the staff responsible for

undertaking the peer review, the frequency of such reviews and the reporting

arrangements for the results);

4. assessments of systems to ensure quality information.

6. Monitoring and review of the insurance risk

management framework

The Chief Actuary or his nominee will review the company’s IRMF at least annually (or as close to

annually as is practicable) to ensure that it accurately documents the company’s insurance risk

management strategies (IRMS). The review will take place in consultation with the Head of Actuarial of

Outsurance.

The IRMS will also be reviewed when there are material changes to the operations of the company.

The Chief Actuary or his nominee must review and amend the insurance risk management framework

and the IRMS to take into account the changes.

Any changes to any policy or procedure covered in the Insurance Risk Management Framework need

to be approved by the Exco.

6.1 Approval by the Board of Directors

The Exco will review the IRMS at least annually or whenever it has been amended. Following his review,

the IRMS will then be submitted to the Board Risk Committee (BRC) for review. Following their review,

the BRC will refer the IRMS to the Board for approval.

YOU.0020.0001.0019

Confidential 19

6.2 Independent review of IRMS compliance

The Risk and Compliance function will review the IRMS, adherence to the insurance risk management

framework, policies and procedures and compliance with Prudential Standard GPS 220 Risk

Management as part of their audit plan.

The Appointed Actuary will also review the IRMS when doing the Financial Condition Report (FCR) as

required by Prudential Standard GPS 310. The FCR covers the key risks and issues impacting upon

the financial situation of Youi. The Appointed Auditor will also perform regular independent reviews of

the IRMS, adherence to the insurance risk management framework, policies and procedures and

compliance with Prudential Standard GPS 220 Risk Management.

YOU.0020.0001.0020

20 Confidential

Appendix 1. Product Development Process

YOU.0020.0001.0021

youi

Appendix 2 Pricing Process

Group Head of Actuarial is

ultimately responsible for Pricing

Contained

Adjustment

Pricing Drivers

Board

Implementation

MIS Review

Gioup Head ct Aptuanal

Australia Head of Adman

Pricing

Adjustment

Required

Executive

Committee

obi Implementation I

NPhilosophyvz

Confidential 21

YOU.0020.0001.0022

youi

Appendix 3 Underwriting Process

Underwriting Drivers

Board

Approval of

Underwriting

Strategy

I Implementation I

Gnoup Head of Actuanal

Austrafia Head of Actuanal

Underwriting

Changes

Required

Non

Strategic

Change

Executive

Cornmittee

Implementation

7110

Strategic

Philosoptry

SUMMITAutomated

Underwriting

22 Confidential

YOU.0020.0001.0023

Confidential 23

Appendix 4. Actuarial Underwriting Process

YOU.0020.0001.0024