insurance premium increase optimization: case...

TRANSCRIPT

Insurance Premium Increase Optimization:

Case Study

Charles Pollack B.Ec F.I.A.A.

Agenda

• Introduction• Business Rules• CART analysis to identify customer groups• Elasticity modelling for each group• Setting optimal levels of capping• Model Validation• Conclusion

Introduction

• Business Background– Property Insurance (Auto and Home)– Australia’s 2nd biggest Insurer

• Result of merger between 2 companies• 2 million customers for auto/home

– Project to bring pricing structures in to line• Some premiums increase, others decrease• Want to minimise cost of transition to new pricing

structures.

Introduction

• Retention Rate drops whether premiums go up or down.Difference between New and Old Premiums

0

5000

10000

15000

20000

25000

-300 -270 -240 -210 -180 -150 -120 -90 -60 -30 0 30 60 90 120 150 180 210 240 270 300

$ Price Change

Num

ber

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Ret

entio

n R

ate

Number Offered Retention Rate

Introduction

• Usual response is to limit premium increases to maximise customer renewal rates.– Known as ‘Capping’ increases

• Legacy systems traditionally constrain business in application of the capping limit.– Eg One % based limit for all customers.

Introduction

• Opportunity to break free of old legacy constraints and start afresh with a ‘blank sheet of paper’

• Combination of $ and % capping limits• Limits able to be varied by customer

groups.• But how do we define those customer

groups?

Business Rules

• The business managers wanted 3 groups of customers ‘uncapped’, irrespective of their elasticity or other characteristics.– Customers making claims– Customers changing their risk profile– Customers on risk for less than 1 full year.

• Customers not in the groups above are candidates for capping.

Business RulesAll Customers

Claim?Yes

No Capping

No

Business Rules

Yes Risk Profile Change?No Capping

No

Short-term policy?No Capping Yes

No

Customers to limit price increases.

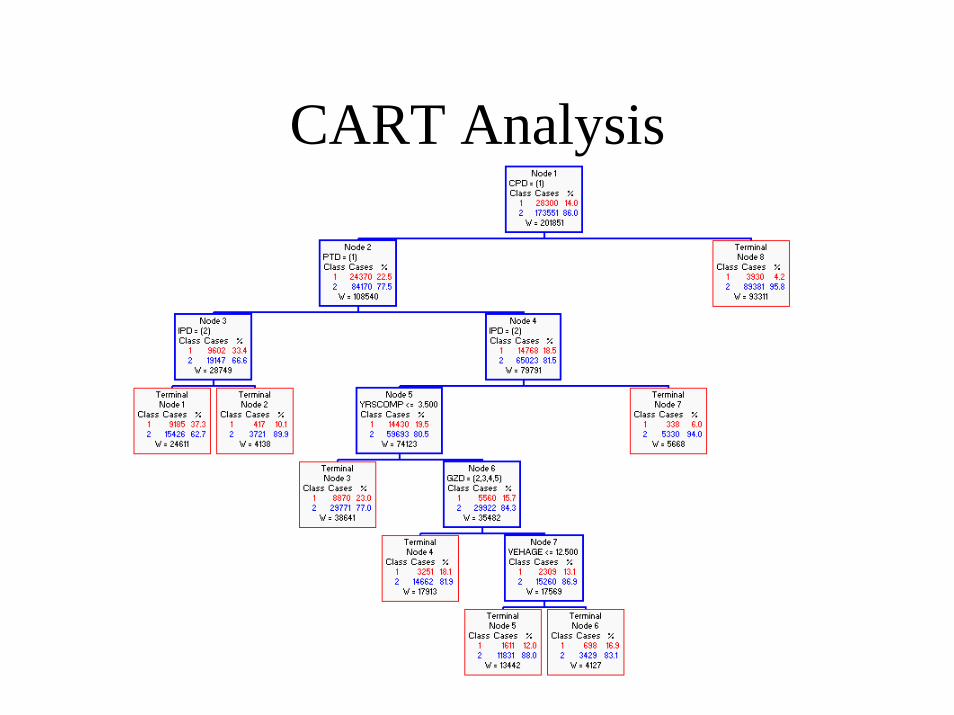

CART Analysis

• Use CART to identify different groups of customers.

• 12 months of renewal offers• Take out records falling in to the 3 business

rule groups.• Split 2:1 (Train:Test)• Model ‘Renewed’ Yes/No.

CART Analysis

• Model variables include:• Age of insured• Other product holdings• Length of time with organisation• Distribution channel• Geographic Location• Age of vehicle/house• Method of Payment (Monthly/Annual)• Level of ‘No Claims Bonus’• Value of vehicle/house• Level of Deductible• …

CART Analysis

• Price NOT a model variable.– When included in models, this variable is a very strong

predictor of retention.– A number of key customer attributes are also factors in

the premium calculation. These variables come out as strong surrogates when price is a splitter.

– Exact splitting points using Premium are difficult to use when applying the model in practice due to premium inflation and competitor movements.

CART Analysis

• Assume:– price change in the data used is randomly spread across

all customer profiles.– elasticity curves for each customer group are convex.

• Assumptions imply that nodes created by CART have

• Different intercept for the same elasticity curve shape• Different shape of curve for a given intercept• Or, A combination of the above.

CART Analysis

• Validating the random-price-change assumption.– Use CART to build several models using same

data.• Very Large increase (Yes/No)• Very Large decrease (Yes/No)• Price Change within $5 (Yes/No)

– Seek a ‘no split’ tree as the optimal tree on the test file to confirm assumption is valid.

CART Analysis

• Build main model tree(s) using training data.– Standard settings except minchild – increase to

avoid excessively large trees.– Compare impact of splitting methods (gini, sym

gini, twoing)• Select optimal tree using test data.

– Further prune tree if it is ‘too big’ for business managers to cope with.

CART Analysis

CART AnalysisNCD Step Back?

Group 1 Endorsement?

Group 2 Risk added mid term?(Renewal term different

from last term)Group 3Premium Payment

Frequency

Group 14

NCD < 40%?

Group 15

Multi-Product Holdings?

Group 4 NCD Level < 40%?

Monthly

Group 5

Annual

Number of previous

renewals > 4?Group 6

State

Vehicle Age < 8?

Group 11

Other

Driver age < 49?

Group 12 Group 13

CTP Discount?

NSW, QLD

Group 7Number of Previous Renewals < 1?

Group 8 Driver age < 42?

Group 10Group 9

Business Rules

CART Analysis

• Variable importance differed somewhat from ‘business expectations’

• Notable absence of age of insured high in tree.• Length of time with company of lower order

importance than business normally assumes.• Some variables were important, however in a

different way to expected behaviour (eg multi-product holdings customers).

CART Analysis

• The convexity or elasticity curves assumption was confirmed post-modelling.

• Charts of observed elasticity by terminal node analysed.

Elasticity Modelling

• Logistic Regression– Price change by Customer Group– Use 100% of data that was previously split 2:1

for CART modelling.• Separate models for $ and % price change• Fit polynomial curves• Review curves for reasonableness

Elasticity Modelling

• Example of curves fit to observed retention.

Setting Optimal Capping Levels• Charging less than book premium on renewal (capping) is

like a discount. ‘The cost of capping’• Balance this cost with the cost of replacing the lost

customer with a new one on full rates.• Optimise (minimise) the following equation:

Predicted retention x (cost of capping + admin cost of renewing)+ (1 – predicted retention) x admin cost of acquiring a new customer

• Simulation Exercise– Recalculate new and old premiums for each customer in existing

portfolio. Difference is raw price change on renewal.– Resolve above equation for each level of capping, by customer

group.– Select optimal capping level for each customer group.

Setting Optimal Capping Levels• Even with extremely high cost of new business acquisition,

the optimal result is achieved with ‘no capping’.

Model Validation

• Used a 3 month period after the initial 12 month data period in the earlier modelling.

• Predict retention, on observed price changes, and compare to actual retention.

• Very close match.<==== ====> <= 3 months =>

CART Model TrainingValidation

Period

CART Model Testing

12 months of renewal offers

Conclusion• CART is very useful for determining customer groups with

no-preconceptions.– Tree easily explained to management and can be ‘grafted on’ to

business rules– Business ‘myths’ can be confirmed or denied– Can also be used to review important modelling assumptions (such

as randomness)• When combined with Logistic Regression, forms a

powerful elasticity modelling tool.• Validation of model performance on an independent data

set is always sensible to ensure veracity of the model.