insurance for real estate: crucial knowledge for today moderator marie a. moore, esq. sher garner...

TRANSCRIPT

1

Insurance for Real Estate:

Crucial Knowledge for TodayModerator

Marie A. Moore, Esq.Sher Garner Cahill Richter Klein & Hilbert, L.L.C.

New Orleans, LA

Panelists:

Maggie McIntyre Marilyn C. Maloney Grace Tate

Gallagher Real Estate and Liskow & Lewis, PLC Butler Snow O’Mara

Hospitality Services Houston, TX Stevens & Cannada, PLLC

Parsippany, NJ Ridgeland, MS

2

LIABILITY INSURANCE

Protects against third party claims and lawsuits that result

from accidents on property.

3

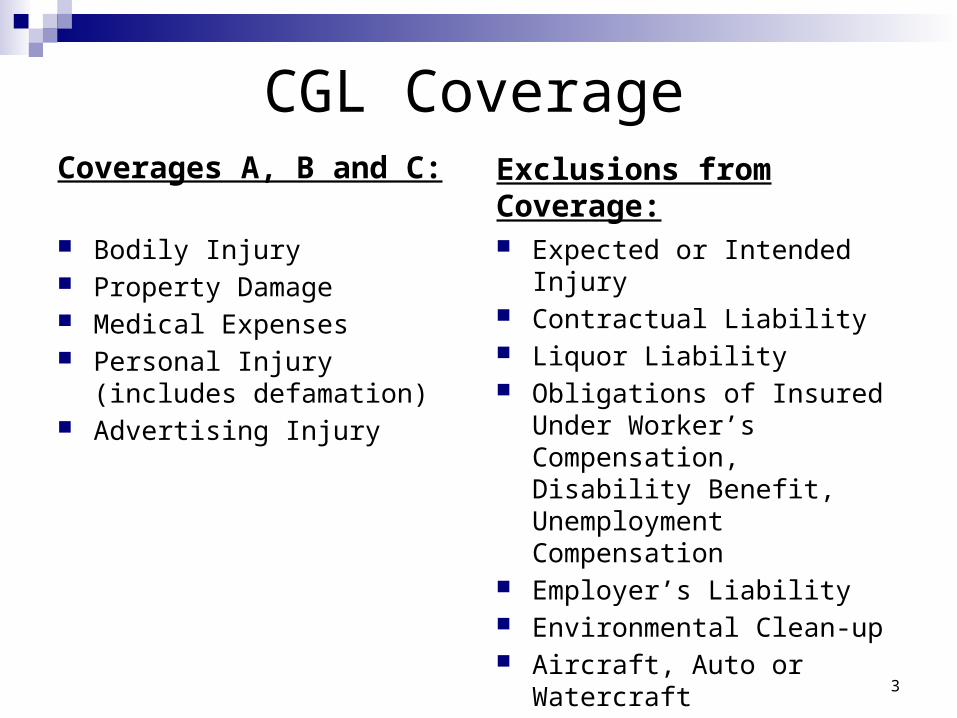

CGL Coverage

Coverages A, B and C: Bodily Injury Property Damage Medical Expenses Personal Injury (includes

defamation) Advertising Injury

Exclusions from Coverage: Expected or Intended Injury Contractual Liability Liquor Liability Obligations of Insured Under

Worker’s Compensation, Disability Benefit, Unemployment Compensation

Employer’s Liability Environmental Clean-up Aircraft, Auto or Watercraft

4

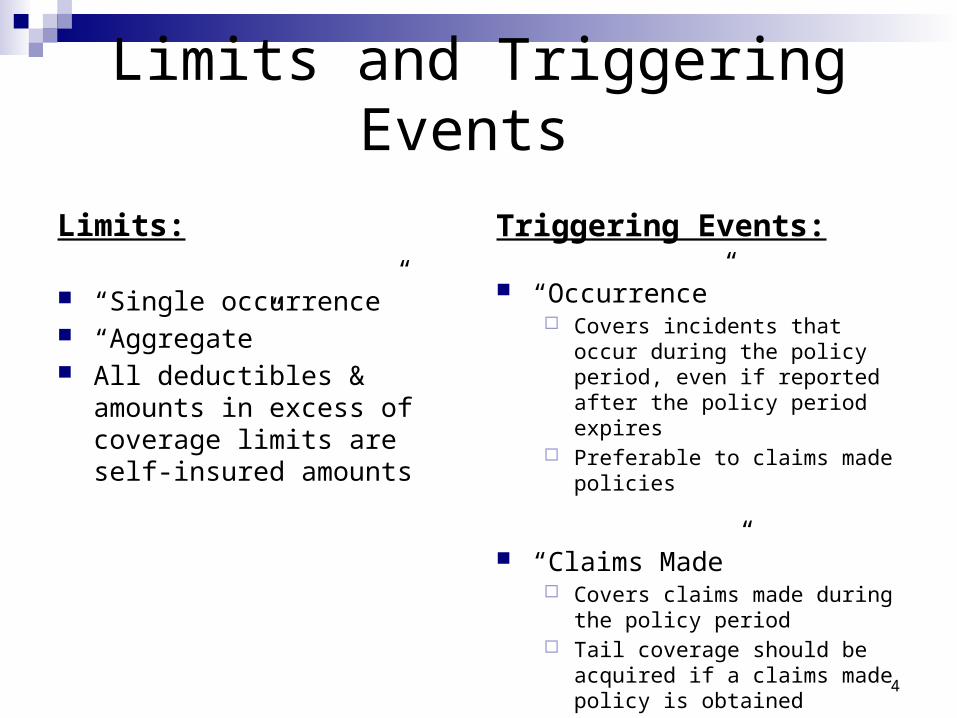

Limits and Triggering Events

Limits:

“Single occurrence” “Aggregate” All deductibles & amounts in

excess of coverage limits are self-insured amounts

Triggering Events:

“Occurrence” Covers incidents that occur during

the policy period, even if reported after the policy period expires

Preferable to claims made policies

“Claims Made” Covers claims made during the

policy period Tail coverage should be acquired

if a claims made policy is obtained

5

Primary and Excess Coverage

Primary & Non-Contributing – Primary policy limits must be depleted before a claimant can tap into the second party’s insurance

Excess Coverage “Following Form” Specific Excess Umbrella Stand Alone

6

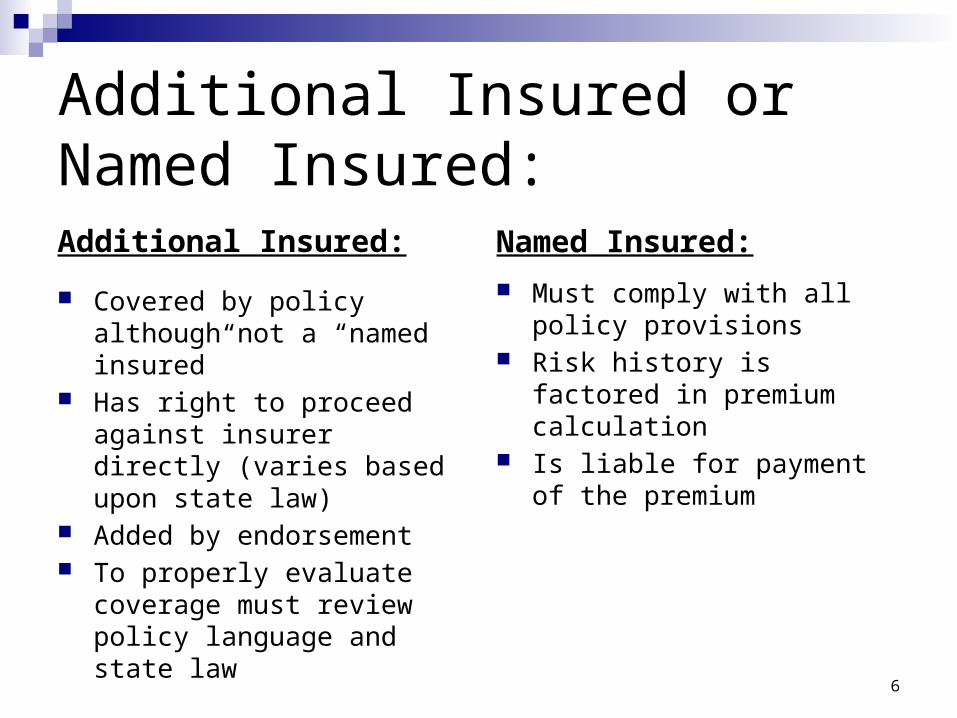

Additional Insured or Named Insured:Additional Insured:

Covered by policy although not a “named insured”

Has right to proceed against insurer directly (varies based upon state law)

Added by endorsement To properly evaluate coverage

must review policy language and state law

Named Insured:

Must comply with all policy provisions

Risk history is factored in premium calculation

Is liable for payment of the premium

7

Insurer’s Qualifications: Licensed in state where property is located Financial Solvency

Financial Strength Rated by A.M. Best Company Ratings range from A++ and A+ (superior)

to A and A- (excellent) to B++ and B+ (good) and continue downward

A- to B+ are generally the lowest acceptable ratings

8

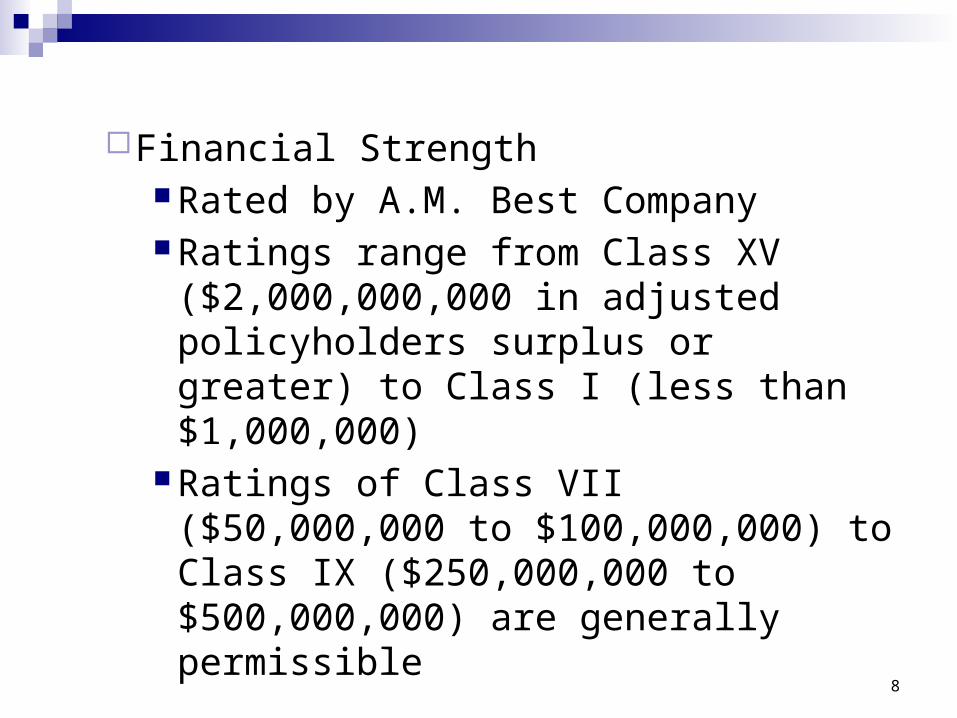

Financial Strength Rated by A.M. Best Company Ratings range from Class XV

($2,000,000,000 in adjusted policyholders surplus or greater) to Class I (less than $1,000,000)

Ratings of Class VII ($50,000,000 to $100,000,000) to Class IX ($250,000,000 to $500,000,000) are generally permissible

9

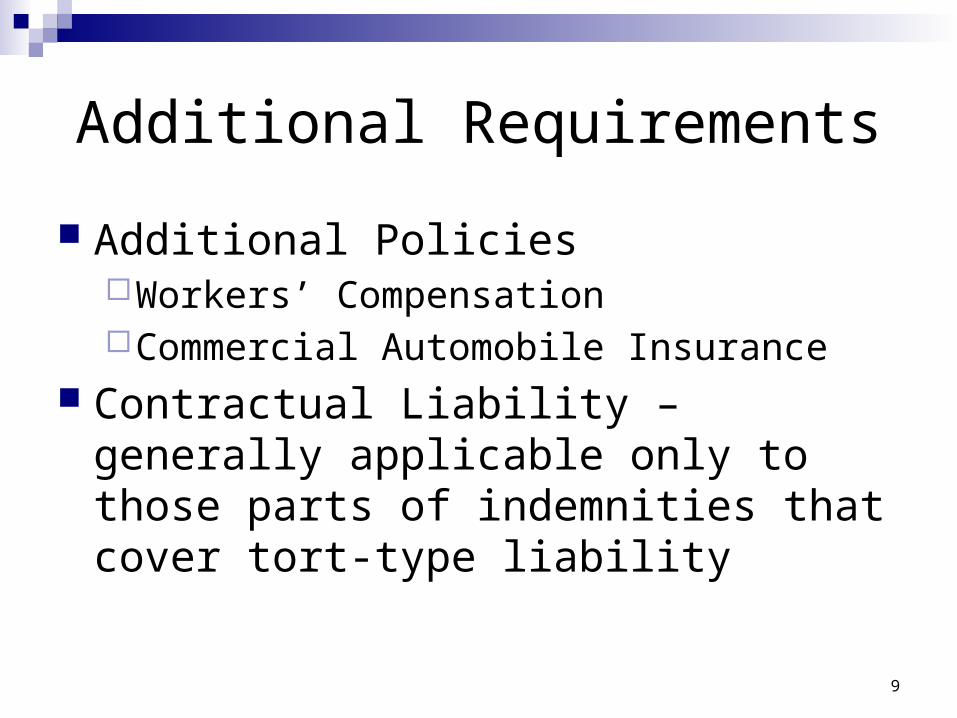

Additional Requirements

Additional Policies Workers’ CompensationCommercial Automobile Insurance

Contractual Liability – generally applicable only to those parts of indemnities that cover tort-type liability

10

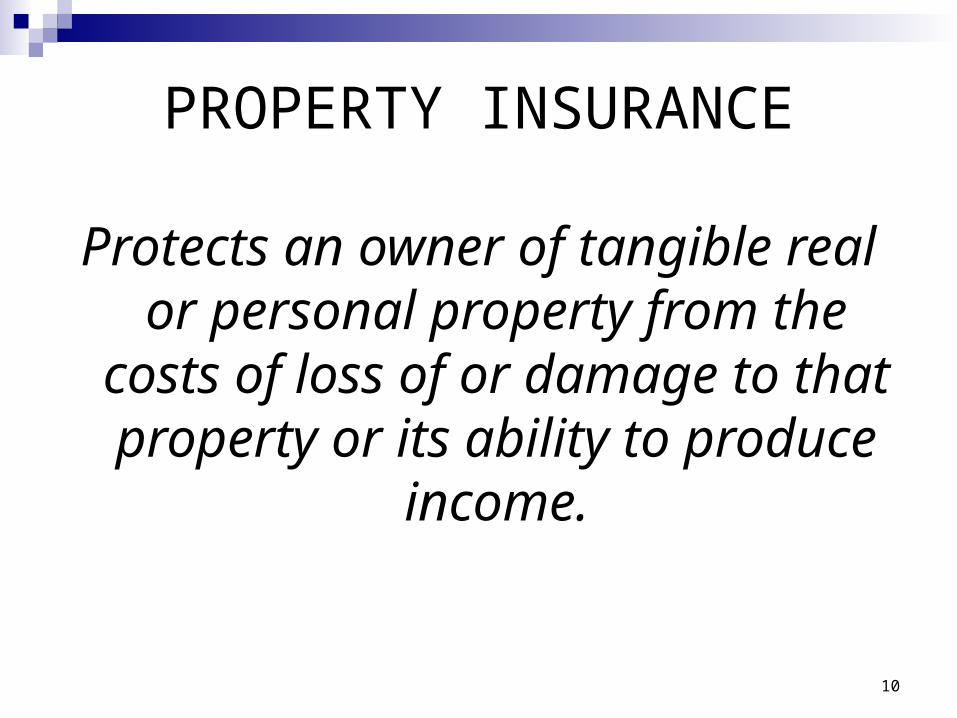

PROPERTY INSURANCE

Protects an owner of tangible real or personal property from the

costs of loss of or damage to that property or its ability to produce

income.

11

Basic ISO and Personal Coverage Form #CP 00 10:Describes what is insured, but the “Covered Cause of Loss” must be covered by another form that describes the type of property policy:

Basic Form Fire Lightening Windstorm Vehicles Aircraft Civil Commotion(Generally ISO Form #CP 10 10)

Broad Form Basic Form plus

additional perils such as Structural Collapse Sprinkler Leakage Losses caused by ice,

sleet or snow weight

(Generally ISO Form #CP 10 20)

12

Basic ISO and Personal Coverage Form #CP 00 10Continued:

Special Form

Covers “risks of direct physical loss” except those perils that are specifically excluded

(Generally ISO Form #CP 10 30)

Examples of Exclusions from Special Form

Water (flood and other water-related occurrences)

War and Military Action Earth Movement (earthquake) Governmental Action Nuclear Hazard Utility Services Boiler and Machine Failure Dishonest Acts Pollutants Terrorism Mold Insects & Vermin

13

Special Types of Coverage (when appropriate):

Windstorm – Basic Form and Broad Form Policies –

windstorm needs to be added as an included risk.

Special Form Policy – windstorm might be an exclusion in some locations (coastal areas).

Earthquake or volcano

14

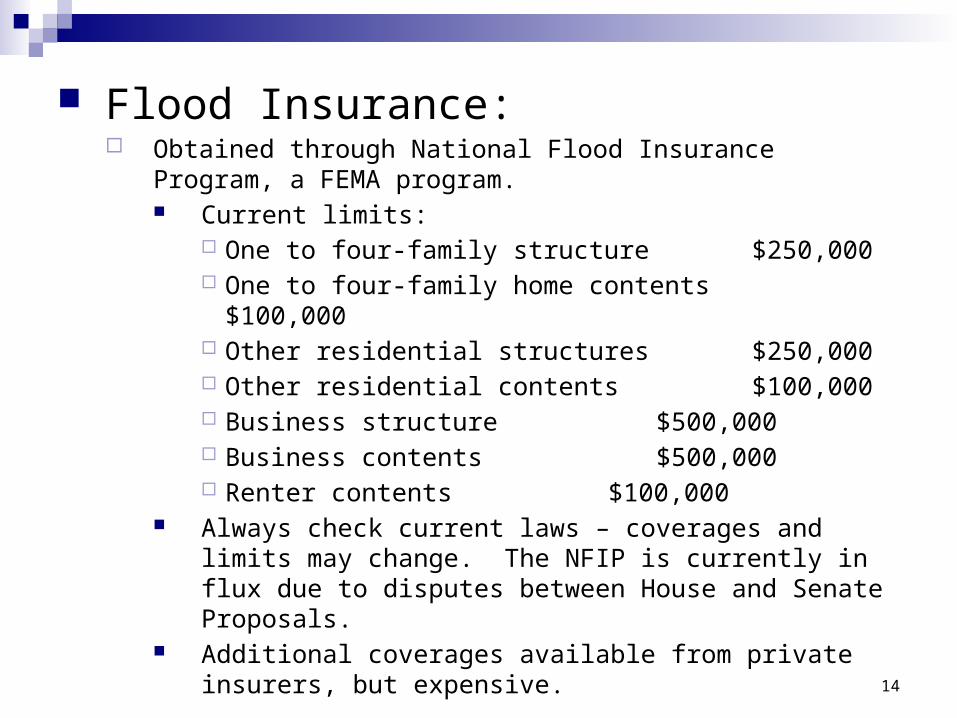

Flood Insurance: Obtained through National Flood Insurance Program, a FEMA

program. Current limits:

One to four-family structure$250,000

One to four-family home contents $100,000 Other residential structures

$250,000 Other residential contents

$100,000 Business structure

$500,000 Business contents

$500,000 Renter contents $100,000

Always check current laws – coverages and limits may change. The NFIP is currently in flux due to disputes between House and Senate Proposals.

Additional coverages available from private insurers, but expensive.

15

What Property Insurance Does the Landlord Need to Require From its Tenant? Landlord Requirements for net leased stand alone

property: Tenant must maintain a policy of Special Form

property insurance as well as flood insurance and other insurance that is important in the area covering all buildings and other improvements located on or forming part of the leased premises.

The property should be insured for its full replacement cost.

The stated limits should be high enough to avoid co-insurance.

16

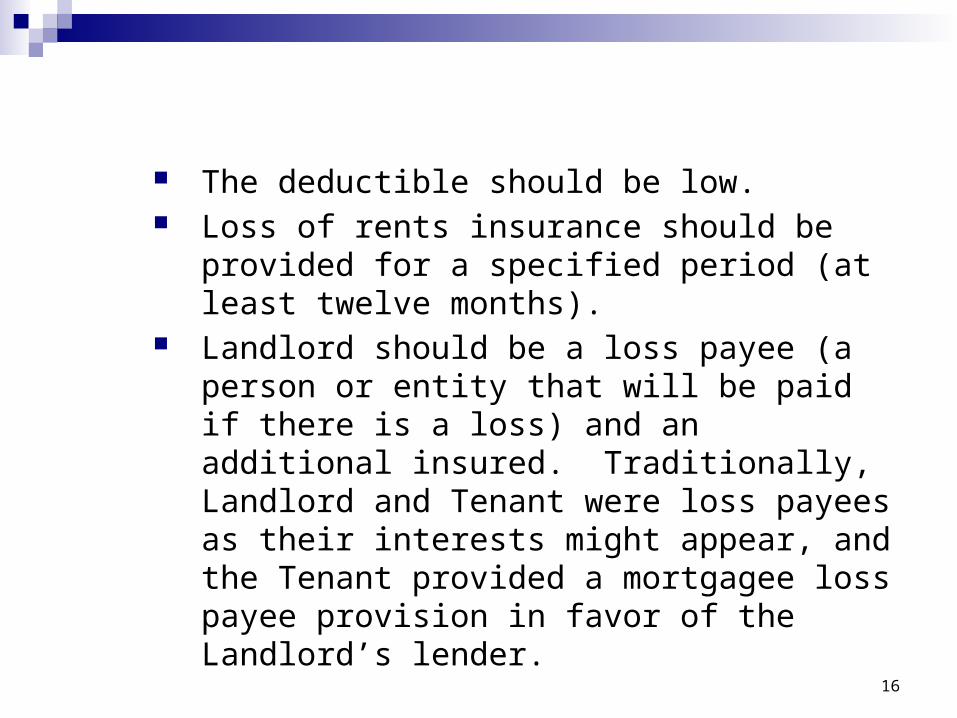

The deductible should be low. Loss of rents insurance should be provided for a

specified period (at least twelve months). Landlord should be a loss payee (a person or

entity that will be paid if there is a loss) and an additional insured. Traditionally, Landlord and Tenant were loss payees as their interests might appear, and the Tenant provided a mortgagee loss payee provision in favor of the Landlord’s lender.

17

What is subrogation? Subrogation is the insurer’s right to stand in the

shoes of its insured and sue the person that caused the damage for the amounts paid by the insurer: (i) Landlord damages Tenant’s property; (ii) Insurer pays Tenant; (iii) Insurer sues Landlord.

Many insurance policies now permit the insured to waive the insurer’s rights of subrogation as to its Landlord (the Commercial Property Conditions in ISO Form CP 00 90 07 88), but an endorsement might be required.

18

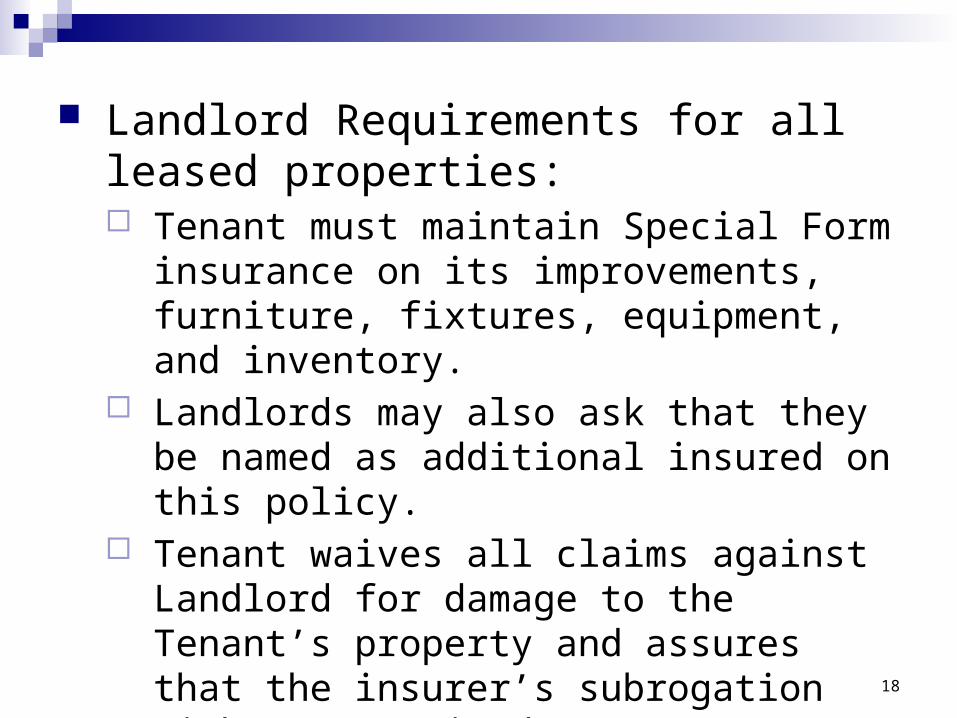

Landlord Requirements for all leased properties: Tenant must maintain Special Form

insurance on its improvements, furniture, fixtures, equipment, and inventory.

Landlords may also ask that they be named as additional insured on this policy.

Tenant waives all claims against Landlord for damage to the Tenant’s property and assures that the insurer’s subrogation rights are waived.

19

What Property Insurance Do Tenants Need to Require From Their Landlords: No insurance if Tenant is occupying the entirety of a

net leased building and the Tenant is the party maintaining the property insurance on the building.

In all other cases, Tenant should require that the Landlord: Carry Special Form property insurance on the

building or the shopping center in which the leased space is located (Tenant wants to be sure that the Landlord has the funds to re-build).

Waive all claims against Tenant for damage to Landlord’s property and assure that the insurer’s subrogation rights are waived.

20

How Much Property Insurance Does a Landlord or Tenant Need?

Special Form covers buildings and other structures described in the policy.

May cover the business personal property located in or on this described property.

21

Does not generally cover foundations below the lowest basement floor or the surface of the ground if there is no basement.

Other exclusions may include vehicles and electronic data, information on valuable papers and records, and satellite dishes and antenna (special coverage may be obtained).

The deductible amount should be viewed as self-insurance.

22

Without “replacement cost” coverage, the insurer will generally pay the lesser of:

The amount that it would cost to repair, rebuild, or replace the property, less fair and reasonable physical depreciation (“actual cash value”), or

The stated policy limits.

If the “replacement cost” is insured, the insurer will be required to pay the lesser of: The cost to replace on the same premises the

lost or damaged property with other comparable property, with no deduction for depreciation; or

23

The stated policy limits.

Landlords and lenders generally require “replacement cost” coverage.

However, if no restoration, only actual cash value paid.

24

What is Co-Insurance?

Co-insurance provisions reduce the recovery if the stated policy limits are too low. The co-insurance percentage, generally 80% or 90%, is shown in the policy Declarations.

The insurance limits must be higher than the co-insurance percentage multiplied by the anticipated total value of the property insured, whether this value is calculated as the “actual cash value” or the “replacement cost.”

25

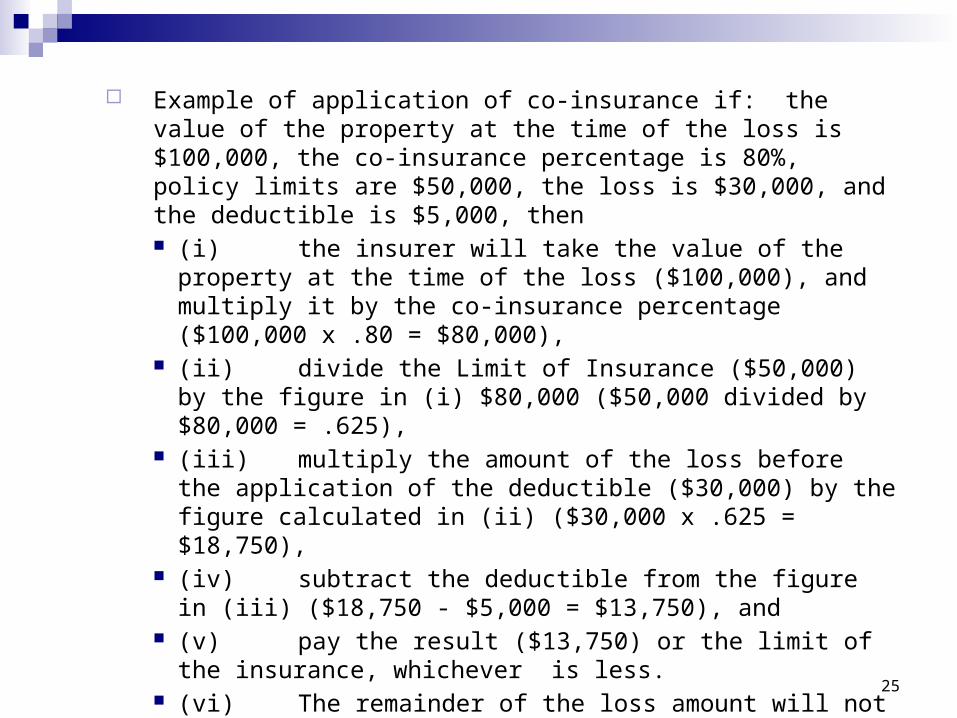

Example of application of co-insurance if: the value of the property at the time of the loss is $100,000, the co-insurance percentage is 80%, policy limits are $50,000, the loss is $30,000, and the deductible is $5,000, then (i) the insurer will take the value of the property at the time

of the loss ($100,000), and multiply it by the co-insurance percentage ($100,000 x .80 = $80,000),

(ii) divide the Limit of Insurance ($50,000) by the figure in (i) $80,000 ($50,000 divided by $80,000 = .625),

(iii) multiply the amount of the loss before the application of the deductible ($30,000) by the figure calculated in (ii) ($30,000 x .625 = $18,750),

(iv) subtract the deductible from the figure in (iii) ($18,750 - $5,000 = $13,750), and

(v) pay the result ($13,750) or the limit of the insurance, whichever is less.

(vi) The remainder of the loss amount will not be covered.

26

Blanket Coverage: A “blanket” policy covers more than one of the

insured party’s properties. Consider a Schedule of Values (a “SOV”) that

can be attached to the policy and accepted by both the insured and the insurer.

Evaluate anticipated increases needed during the year and an inflation guard factor before selecting the final limit and co-insurance percentage.

The insurer may agree that the values on the SOV will be “agreed amounts” that will avoid the application of co-insurance.

27

Loss of Rents Coverage: Landlords include loss of rents coverage in

their property insurance policies (may be part of a business interruption package) to cover the rents they will lose after a casualty.

Coverage should be in an amount adequate to cover anticipated rental loss (12 months is generally a good measure).

Business Interruption Coverage: Tenants maintain business interruption

insurance to cover their business losses after a casualty.

28

CONSTRUCTION RISKS Separate Policies are needed for

Commercial General Liability Insurance to protect against liability to third parties;

Property insurance to cover damage to the improvements being constructed and the materials; and

Workers’ Compensation Policies to covery statutory liability to the Contractor’s injured workers.

29

Liability Insurance/Obligations to Defend:

AIA Forms (if not altered) generally

Require the Contractor to maintain CGL insurance and to defend the Owner only for accidents caused by the Contractor, the Architect, a Subcontractor, or anyone employed by them or for whom they are responsible.

The Owner will need to maintain coverage for accidents caused by the Owner or Third Parties.

30

Owner-modified AIA Forms can: Require the Contractor to cover and protect the Owner for

accidents caused by a Third Party on the construction site or even all accidents on the site, regardless of cause.

But Contractor Anti-Indemnity Statutes and other laws in some states void some or all of the Contractor’s obligations with respect to accidents caused by the Owner or by a Third Party, including, in some cases, the Contractor’s obligation to maintain insurance.

Because of state law, in many states, the Owner should not rely on the Contractor to defend the Owner for accidents caused by the Owner, even if the AIA Contract is revised to require this defense.

31

The Contract should require the Contractor to: Maintain Commercial General Liability

Insurance naming Owner as an additional insured.

But this may not cover an accident that is not caused by the Contractor, the Architect, a Subcontractor, or anyone employed by them or for whom they are responsible.

32

Even under an Owner-modified AIA Contract, the policy itself will govern what is covered, and A standard-form additional insured

endorsement will not provide the Owner with coverage for its sole negligence (the Owner can attempt to negotiate the form), and

The laws of some states may prohibit a requirement that the Contractor maintain insurance covering the Owner’s negligence.

33

What about the Contractor’s liability for accidents after completion caused by construction defects? Completed Operations coverage will cover accidents

that occur after completion caused by defects in the original work.

The standard AIA form may need to be altered to require the Contractor to provide this coverage.

Coverage should be provided for the agreed period (generally the warranty period) on an “occurrence” basis.

Owner should be named as an additional insured.

34

Property Insurance:

The AIA Form generally requires the Owner to maintain the “Builder’s Risk” insurance that covers damage to the improvements being constructed during the construction process. The Contractor should ask for a waiver of subrogation in its favor.

If the Contractor’s construction price includes the price of the property policy, the AIA Form needs to be revised to require the Contractor to maintain this “Builder’s Risk” insurance.

35

Owner should be named as an additional insured and loss payee on this “Builder’s Risk” insurance, and if Contractor is required to replace portions of the work damaged during construction, then Contractor should also ask to be an additional insured and loss payee, as its interests may appear.

Contractor should be required to insure its tools and materials, and Owner should require a waiver of subrogation with respect to this coverage.

36

Workers’ Compensation Insurance: The Owner should require the Contractor to

maintain Workers Compensation insurance to cover the Contractor’s statutory obligations to its employees as well as any liability that state law may impose on the Owner as an alternate or statutory employer.

The Owner should ask that the Workers’ Compensation insurer waive rights of subrogation against the Owner (this may not be obtainable from some insurers).

37

Insurance Certificates After successfully negotiating insurance

requirements in a lease, construction contract, loan agreement, or other contract, how to verify that the correct coverages have been placed?

Is it safe to require production of an insurance certificate as evidence of insurance?

Short answer: NO

38

ACORD form of certificate for liability insurance was never evidence of insurance.

Prior to 2005, however, the ACORD form of certificate for property insurance did provide that it was evidence of insurance. Since 2006 ACORD property form also limits the effect of certificates.

39

As a result of the 2006 amendments, both forms of insurance certificate clearly provide that they are issued as matters of information only, and that they do not constitute evidence of insurance.

Both forms also contain provisions with respect to giving notice of cancellation to the certificate holder.

40

Why can’t lenders and other third parties get insurance certificates on which they rely?

Issue of the underwriter: they do not issue the certificate. They have issued a policy and do not want a certificate to alter its terms.

Issuing agents are not paid for certificates and may not take time to review entire file.

41

Insurance underwriters have taken their position to the legislature and insurance commissioners of the majority of the states.

Typical bulletins and legislation provide that certificates cannot alter or modify the terms of the policy.

Some states provide that only the ACORD and ISO form of certificate may be used.

Issues with lenders due to Notice of Cancellation Provision and ACORD 28 (2009/12).

42

Courts have enforced the plain language of the certificates.

Most cases deal with the liability certificate, but no reason to believe cases dealing with property coverage will be handled differently.

A certificate holder may have an E&O claim against the issuer of the certificate.

43

What alternative does a party have to verify that insurance coverages have been placed as required by lease or other contract?

Some suggest obtaining a written opinion or certification of an insurance professional that it has reviewed the policies of the insured and the operative contract, and that all coverages are in place.

44

Even if an advisor is willing to provide this certification at closing or signing of the lease, it does not guard against subsequent changes or cancellations of coverage.

Require production of the entire policy, either at the closing or at any time requested thereafter.

45

This is a meaningful exercise only if the party has the expertise to examine the policy or hires competent insurance professionals to do so.

Policies may not be immediately available with new acquisitions.

46

Binders are not alternatives to certificates; they are limited duration, they are actual insurance (rather than evidence of other insurance) and they do not contain all of the policy terms and conditions.

Binders do not incorporate all of the terms and conditions of the underlying policies and can lead to disputes such as the World Trade Center litigation.

47

Insurance Certificates: Practical Tips

Understand the limitations of certificates.

Reserve the right to review the complete policy.

Involve insurance professionals.