insurance and bond - hkis · 2016-09-11 · insurance and bond sr. kenny lui bsc(qs), llb, mmgt,...

TRANSCRIPT

Insurance and Bond

Sr. Kenny LuiBSc(QS), LLB, MMgt, MACSMHKIS, MRICS, RPS (QS)

What are we going to cover today?

Introduction

Why do we have insurance?

Some insurance “jargon”

Insurance arrangement

Types of insurance

Some notes for CAR / TPL / ECI

Surety Bond

Experience Sharing (if time allowed)

Reasons for Insurance Policies

Contract Requirements

LegislationRisk

Allocation

Reasons for Insurance Policies

Contract Requirements

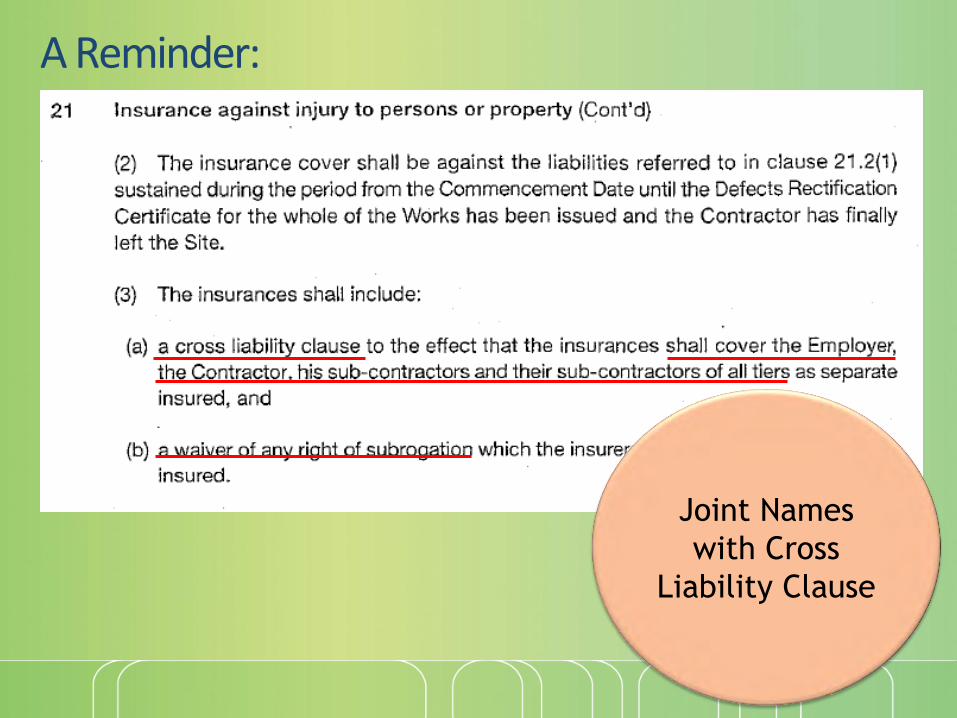

Clause 21 - Insurance against injury to persons or property

Covers both "Employees' Compensation Insurance" and "Third party liability insurance“

Both insurances are to be in the joint names of the Employer, the Contractor, his sub-contractors and their respective sub-contractors of all tiers.

The Employees’ Compensation Insurance is to be taken out by the Contractor

Clause 21 - Insurance against injury to persons or property

Third Party insurance is to be taken out by whichever party takes out the Contractors' All Risks Insurance

The Third Party insurance shall cover the Employer’s liability for damage to real or personal property other than the Works due to collapse and subsidence

The period of cover is to run from the Commencement Date until the Defects Rectification Certificate for the whole of the Works has been issued

Clause 22 - Insurance of the Works

There are 3 alternative clauses:- Clause 22A

covers the insurance of the Works by the Contractor

- Clause 22B covers the insurance of the Works by the Employer

- Clause 22C covers the insurance of the existing building and the insurance of the Works by the Employer

The insurer chosen by the party taking out the insurance have to be approved by the other party

Clause 22 - Insurance of the Works

Evidence of cover has to be supplied prior to the commencement of the Works

The remedy for a party defaulting in taking out the insurance is provided for

The conditions for using an annual policy (Clause 22A.3) maintained by the Contractor as an alternative to taking out a specific policy for insurance of the works are set out

Reasons for Insurance Policies

Legislation

Legal Requirements

Employees’ Compensation Ordinance Cap 282

Employers are required to take out employees compensation insurance policy

to cover their liability when death or injuries involving ……due to an accident arising out of and in the course of his/her employment

Reasons for Insurance Policies

Risk Allocation

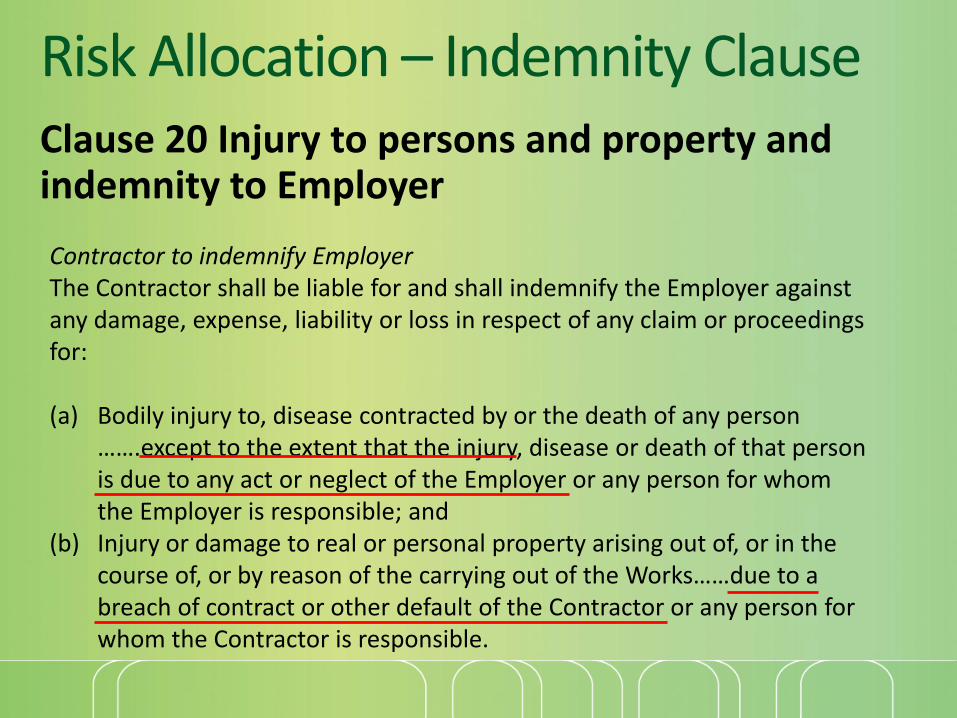

Risk Allocation – Indemnity ClauseClause 20 Injury to persons and property and indemnity to Employer

Contractor to indemnify EmployerThe Contractor shall be liable for and shall indemnify the Employer against any damage, expense, liability or loss in respect of any claim or proceedings for:

(a) Bodily injury to, disease contracted by or the death of any person …….except to the extent that the injury, disease or death of that person is due to any act or neglect of the Employer or any person for whom the Employer is responsible; and

(b) Injury or damage to real or personal property arising out of, or in the course of, or by reason of the carrying out of the Works……due to a breach of contract or other default of the Contractor or any person for whom the Contractor is responsible.

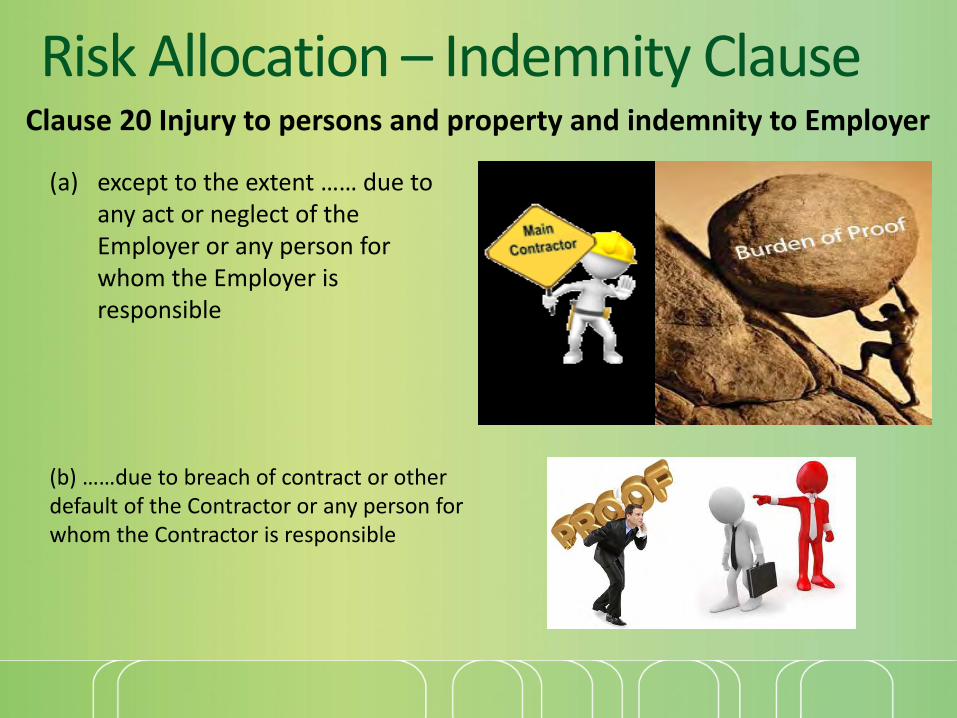

Risk Allocation – Indemnity ClauseClause 20 Injury to persons and property and indemnity to Employer

(a) except to the extent …… due to any act or neglect of the Employer or any person for whom the Employer is responsible

(b) ……due to breach of contract or otherdefault of the Contractor or any person for whom the Contractor is responsible

Risk Allocation

Insurance transfers part of a commercial risk

The risk still remains, it is now being shared with an insurer

The liability still remains

Insurance does not remove liability

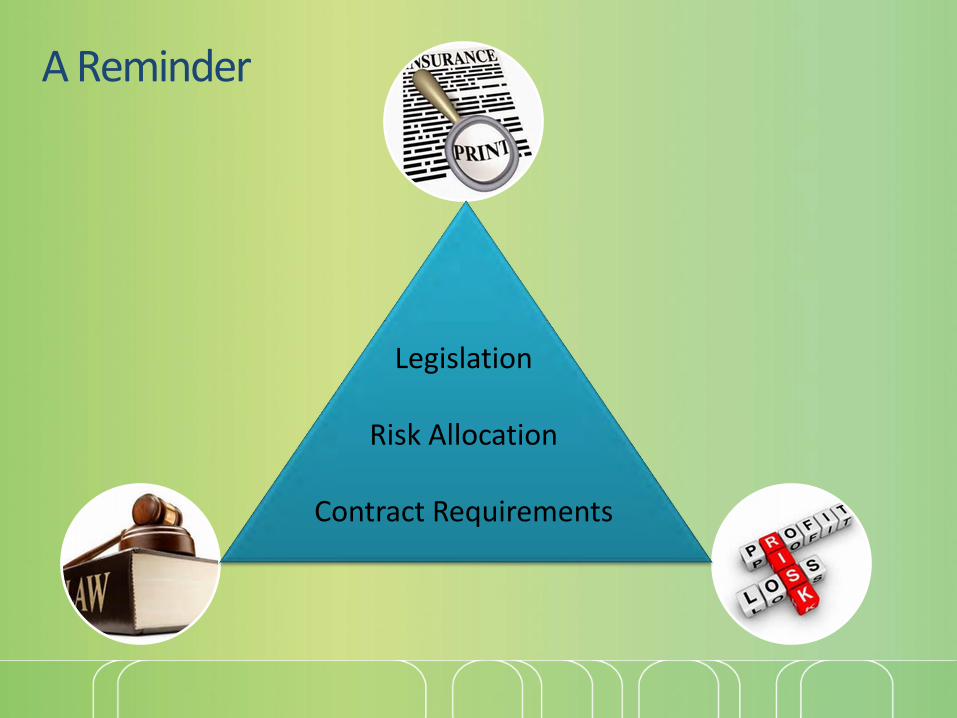

A Reminder

Legislation

Risk Allocation

Contract Requirements

Story Time

25 Most Ridiculous Insurance Claims Everhttp://list25.com/25-most-ridiculous-insurance-claims-ever/3/

A clever lawyer bought a pack of (24) cigars and had them insured against all sorts of catastrophes including floods, storms, and of course fire. A few months later he filed a claim saying his cigars had all disappeared in a series of “small fires”.

25 Most Ridiculous Insurance Claims Everhttp://list25.com/25-most-ridiculous-insurance-claims-ever/3/

The insurance company correctly assumed that he had smoked them and told him to get lost.

The judge however force the insurance company to pay up because they didn’t specify the type or size of fire in the contract.

The insurer was obligated to pay $15,000 for the lawyer’s his loss of the rare cigars lost in the "fires".

25 Most Ridiculous Insurance Claims Everhttp://list25.com/25-most-ridiculous-insurance-claims-ever/3/

After the lawyer cashed the cheque, the insurance company had him arrested on 24 counts of ARSON!!!

The lawyer was convicted of intentionally burning his insured property and was sentenced to 24 months in jail and a $24,000 fine ……

25 Most Ridiculous Insurance Claims Everhttp://list25.com/25-most-ridiculous-insurance-claims-ever/3/

Lesson Learnt from the story:

1. Do not abuse the insurance protection.

2. Insurance company can sue the wrong doer after the insurance company paid the compensation to the insured

Subrogation

Insurance “Jargon” (Glossary)

Subrogation

Joint names

Cross liability

Deductibles / Excess

Escalation

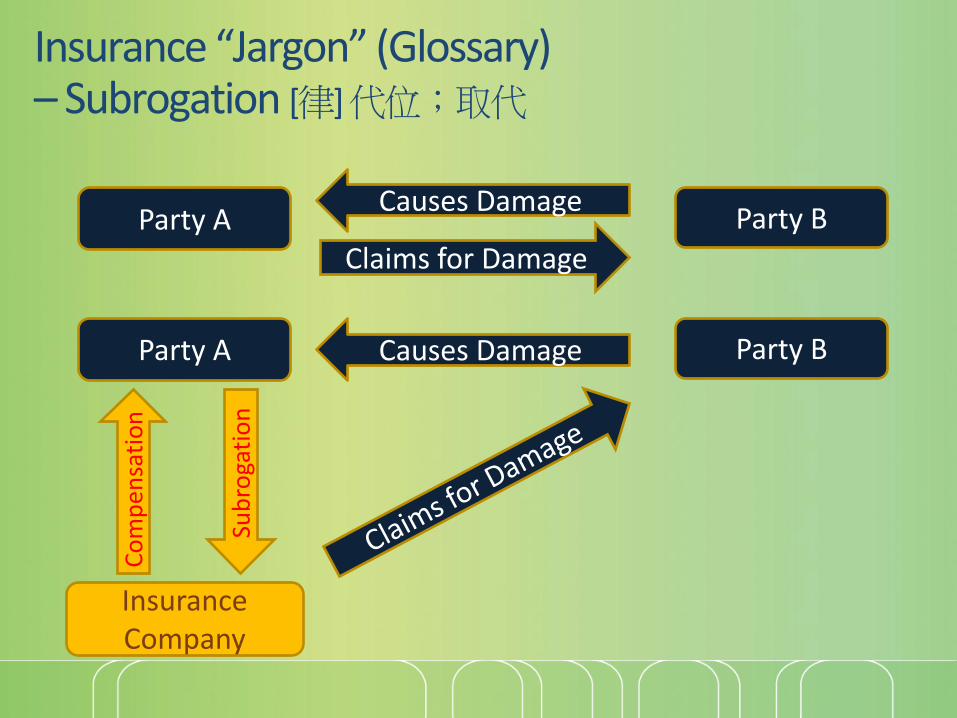

Insurance “Jargon” (Glossary) – Subrogation [律] 代位;取代

One party takes on the legal rights of another, especially substituting one creditor for another.

For example, when an insurance company compensates a policy holder for an injury, often the policy holder's right to sue the person who harmed him is subrogated, meaning it is transferred from him to the insurance company.

Party A Party B

Causes Damage

Claims for Damage

Insurance Company

Co

mp

ensa

tio

n

Sub

roga

tio

n

Insurance “Jargon” (Glossary) – Subrogation [律] 代位;取代

Party A

Causes Damage

Party B

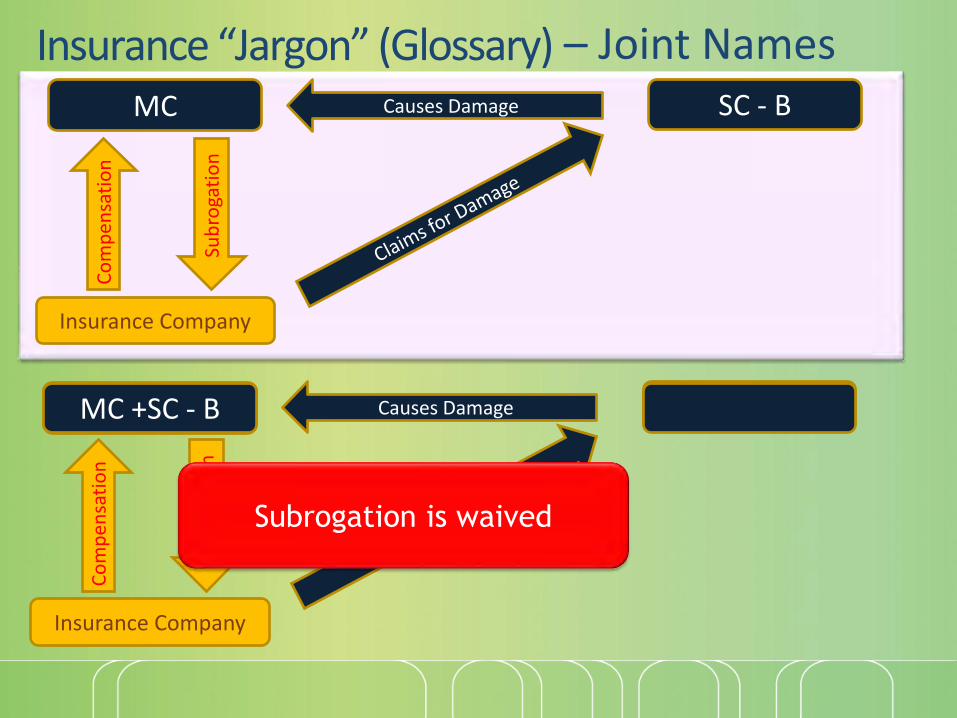

Insurance “Jargon” (Glossary) – Joint Names

An employer is insured against any liability (vicariously) incurred by reason of a breach by the contractor.

A party named under an insurance policy can make claimsunder that policy and it is also common for insurers to berequired to waive their rights of subrogation against co-insured parties.

This means that the insurer agrees not to seek to recoveragainst a co-insured party (i.e. the employer) even if theinsurer paid out on account of the actions of theemployer.

Causes Damage

Insurance Company

Co

mp

ensa

tio

n

Sub

roga

tio

n

MC SC - B

Insurance “Jargon” (Glossary) – Joint Names

Causes Damage

Insurance Company

Co

mp

ensa

tio

n

Sub

roga

tio

n

MC SC - B

Subrogation is waived

MC +SC - B

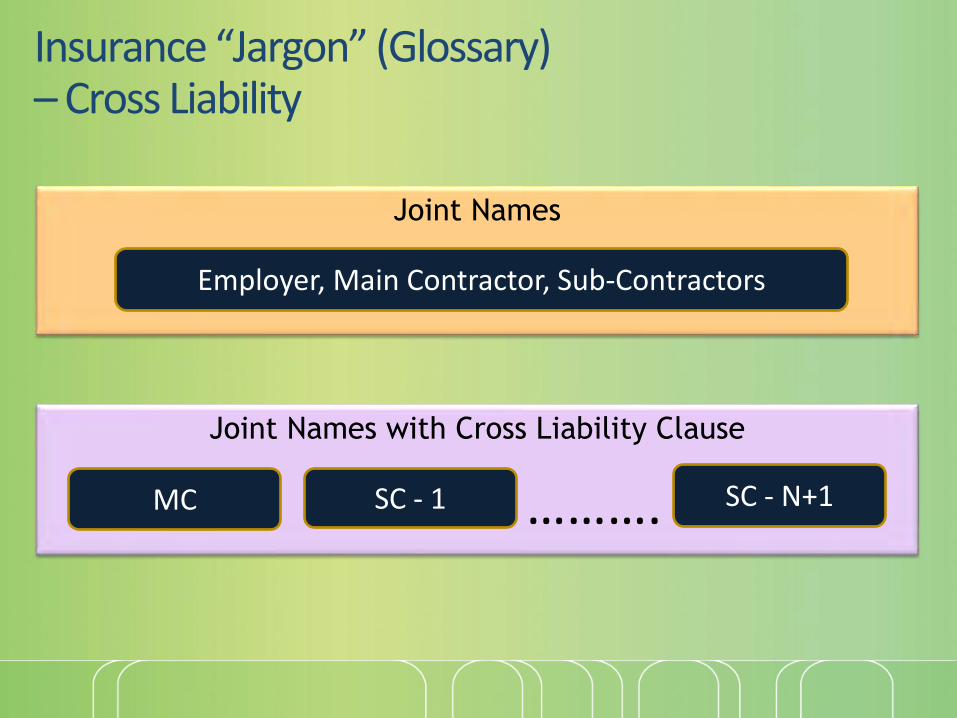

Insurance “Jargon” (Glossary) – Cross Liability

A cross liability clause essentially means that each party is insured in its own right as if a separate policy had been issued. Each of the insured gets treated as a separate entity even though they are under the same policy.

This means that one individual that is covered by the policy could potentially damage or hurt another individual that is also covered by the same policy.

Read more: http://www.finweb.com/insurance/what-is-an-insurance-cross-liability-clause.html#ixzz3ZVJg9E2n

Insurance “Jargon” (Glossary) – Cross Liability

Joint Names

Employer, Main Contractor, Sub-Contractors

Joint Names with Cross Liability Clause

MC SC - 1 ………. SC - N+1

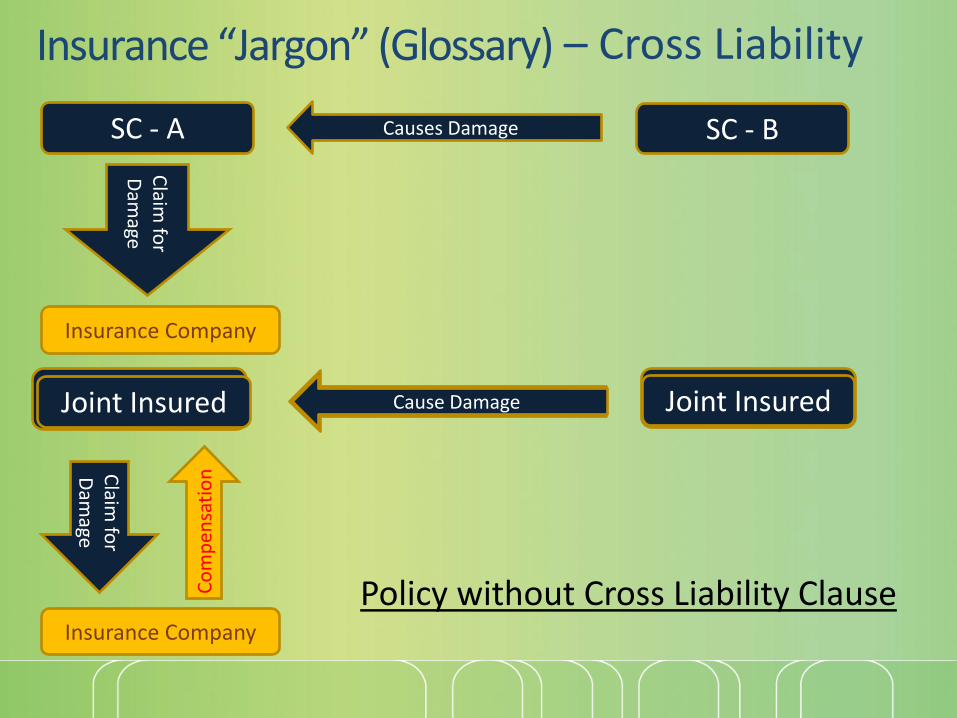

Causes Damage SC - BSC - A + SC - B

Insurance “Jargon” (Glossary) – Cross Liability

Co

mp

ensa

tio

n

Causes Damage

Insurance Company

SC - A SC - B

Claim

for

Dam

age

Insurance Company

Cause DamageJoint Insured Joint Insured

Claim

for

Dam

age

Policy without Cross Liability Clause

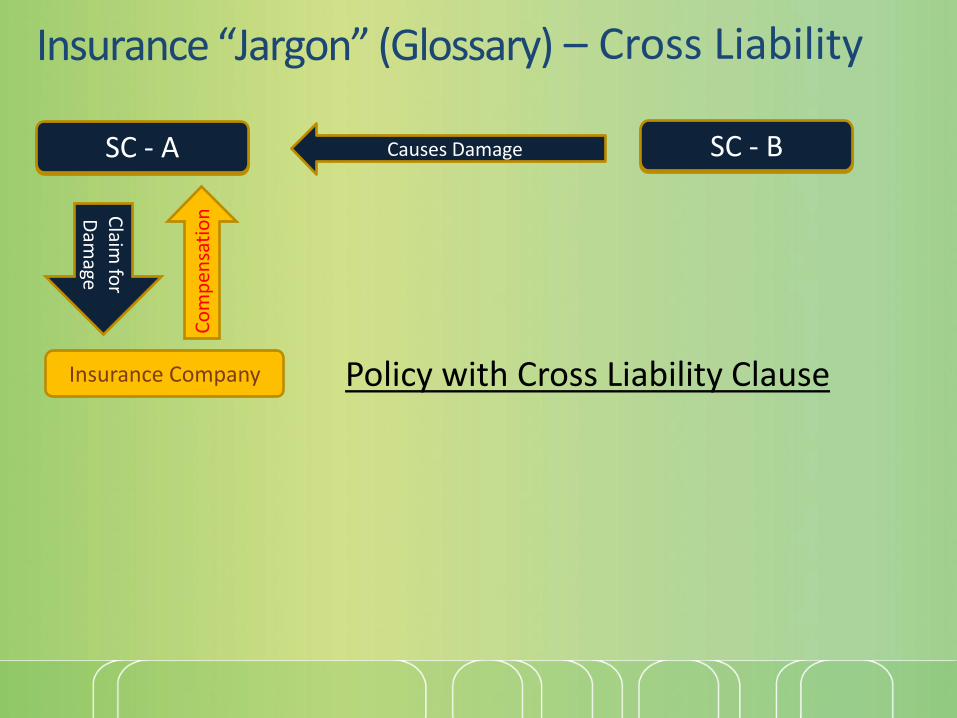

Insurance “Jargon” (Glossary) – Cross Liability

Co

mp

ensa

tio

n

Insurance Company

Causes DamageJoint Insured Joint Insured

Claim

for

Dam

age

Policy with Cross Liability Clause

SC - BSC - A

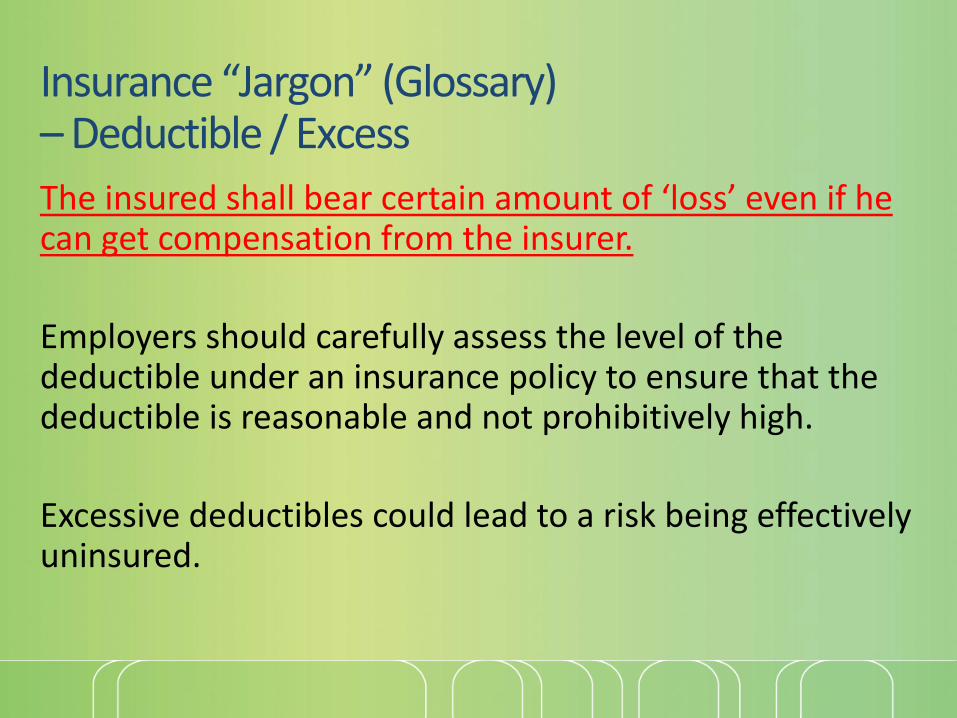

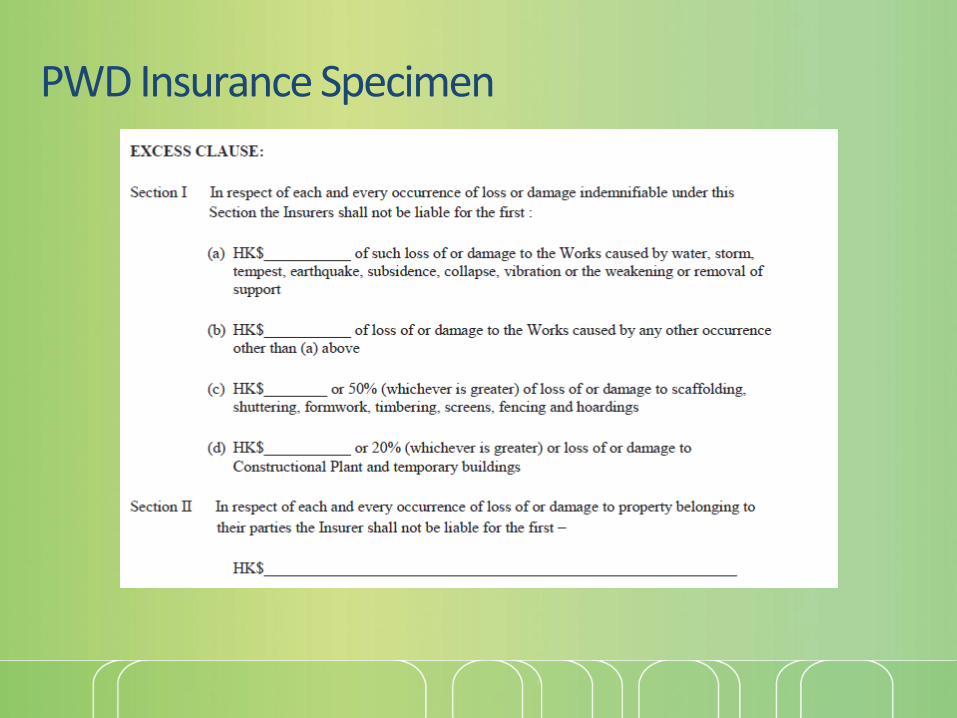

Insurance “Jargon” (Glossary) – Deductible / Excess

The insured shall bear certain amount of ‘loss’ even if he can get compensation from the insurer.

Employers should carefully assess the level of the deductible under an insurance policy to ensure that the deductible is reasonable and not prohibitively high.

Excessive deductibles could lead to a risk being effectively uninsured.

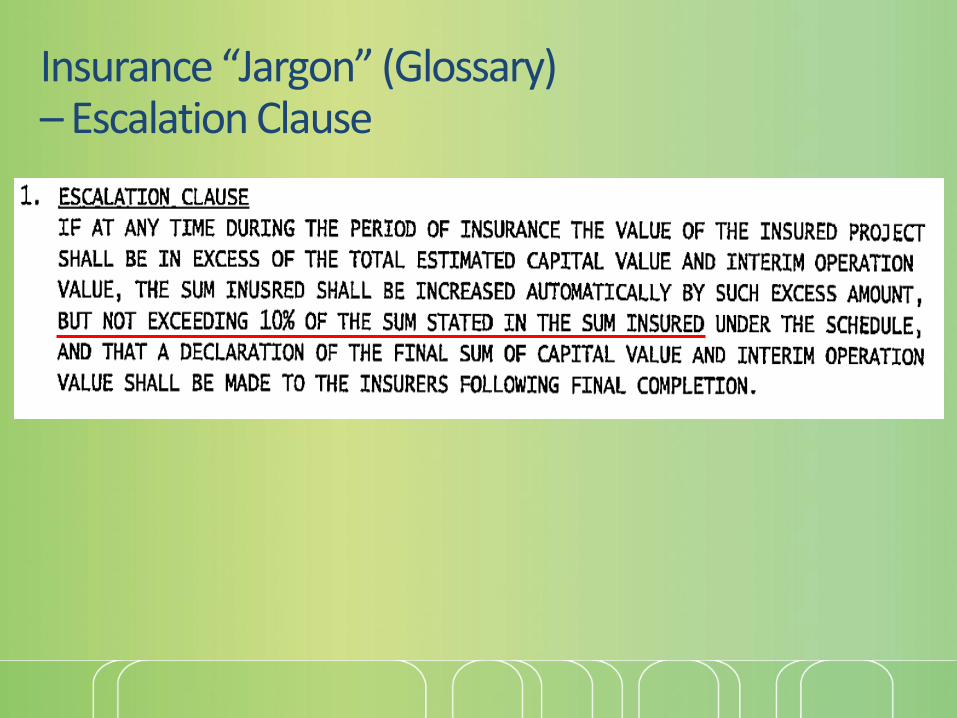

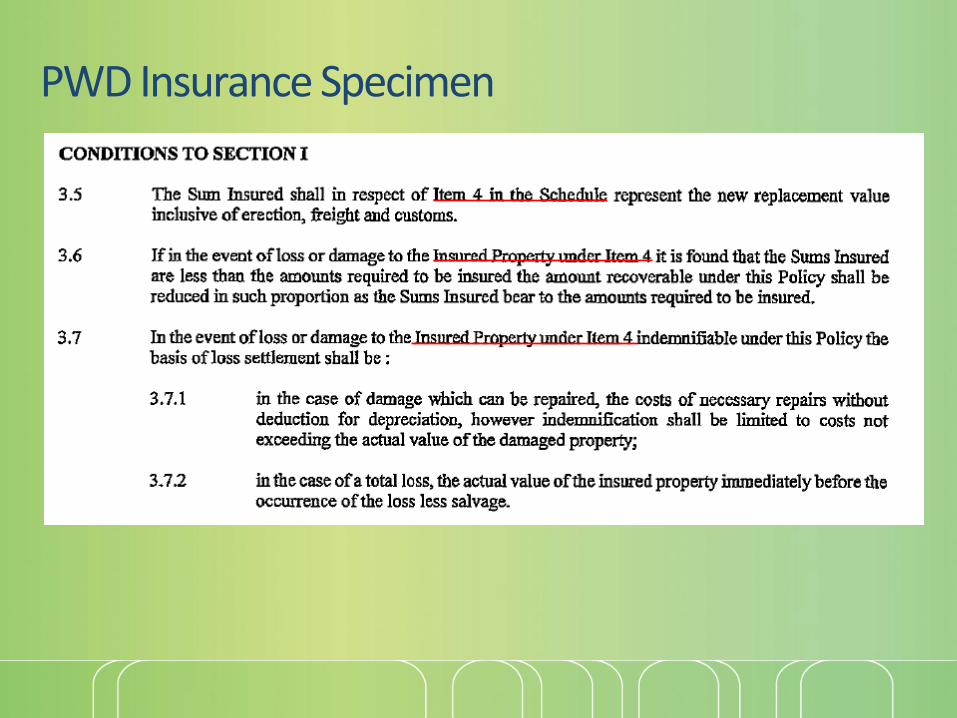

Insurance “Jargon” (Glossary) – Escalation ClauseTo avoid under-insurance especially for long term projects, it is important to regularly review the total contract value upwards.

Inflation can also cause the contractor to be under-insured due to the increase in the contract value of the project. Hence, the Escalation Clause is inserted in the policy to ensure the Total Contract Value is reviewed upwards and protects the insured from being under-insured when a claim arises. 10 - 15% per annum is usual the increase in value of projects.

http://www.answers.com/Q/What_is_an_escalation_clause_under_construction_all_risks_Insurance

Insurance “Jargon” (Glossary) – Escalation Clause

A Reminder:

SubrogationJoint

Names

Joint Names

with Cross

Liability Clause

Contractor

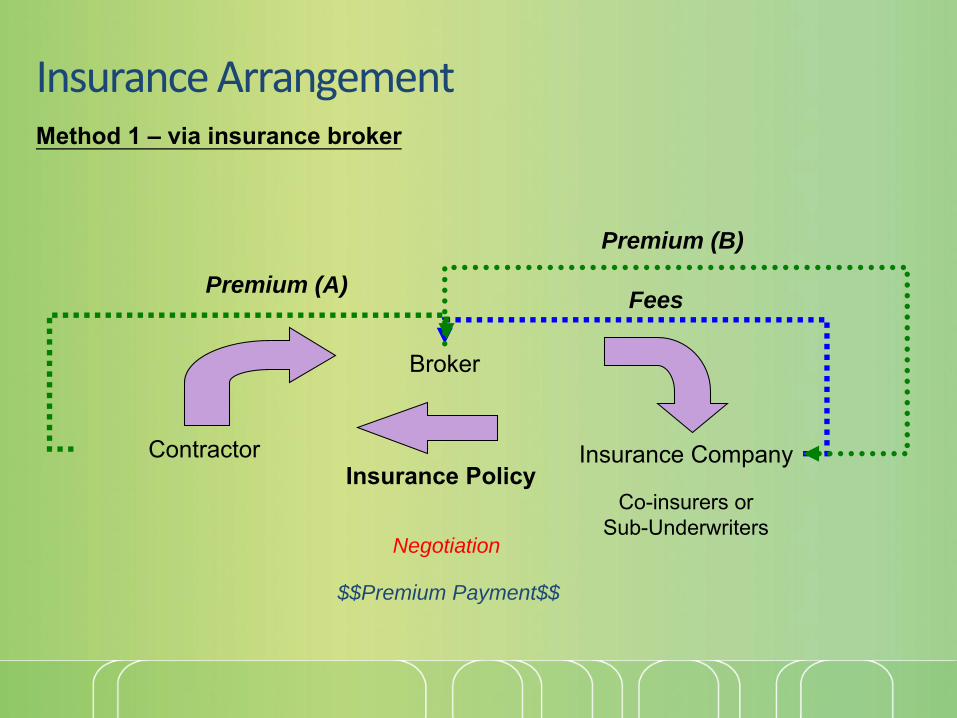

Broker

Insurance Company

Co-insurers or Sub-Underwriters

Insurance Policy

Premium (A)

Method 1 – via insurance broker

Fees

Premium (B)

Negotiation

$$Premium Payment$$

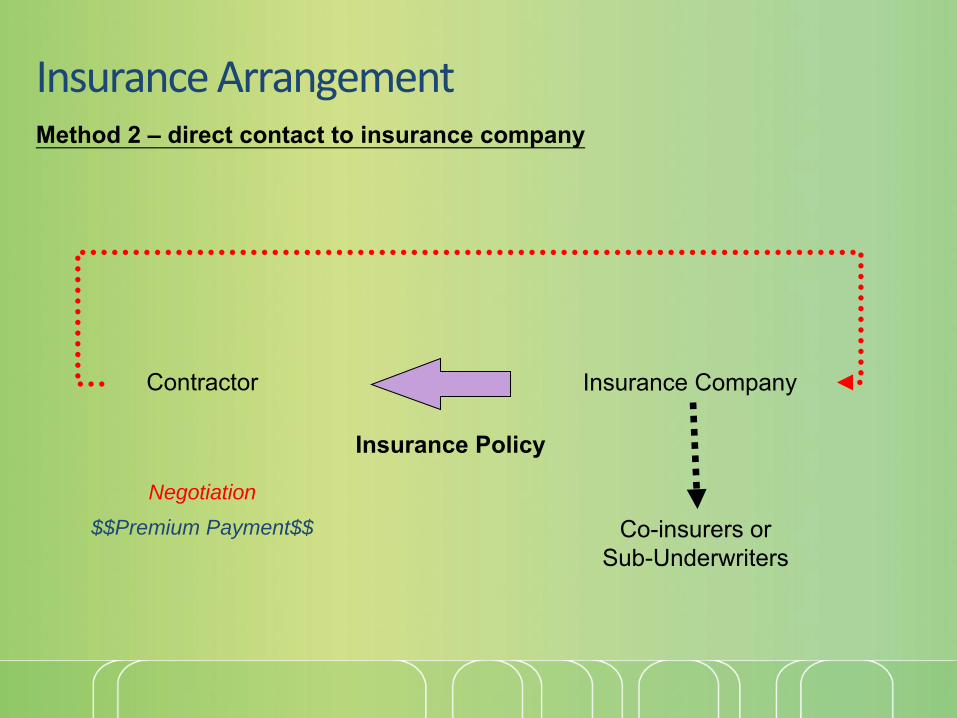

Insurance Arrangement

Contractor Insurance Company

Co-insurers or Sub-Underwriters

Insurance Policy

Method 2 – direct contact to insurance company

Negotiation

$$Premium Payment$$

Insurance Arrangement

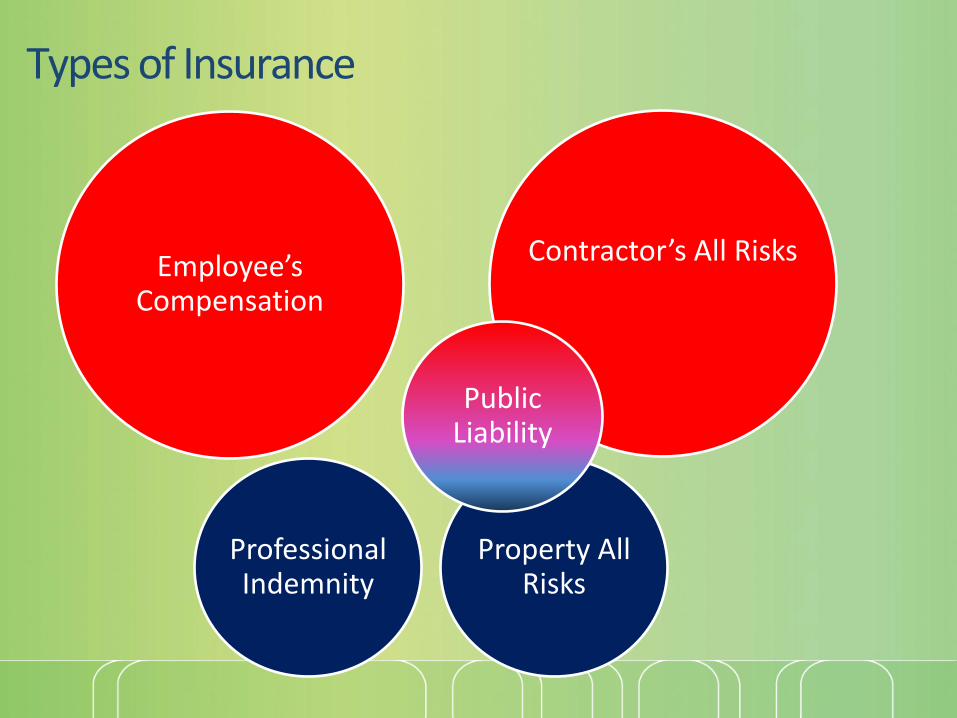

Types of Insurance

Contractor’s All Risks

Property All Risks

Professional Indemnity

Employee’s Compensation

Public Liability

Premium depends on

• Contract Sum• Excess• Limit of Indemnity (Coverage)• Contract Period• Nature of the projects

• External Wall Renovation • Any Scaffolding or demolition work involved

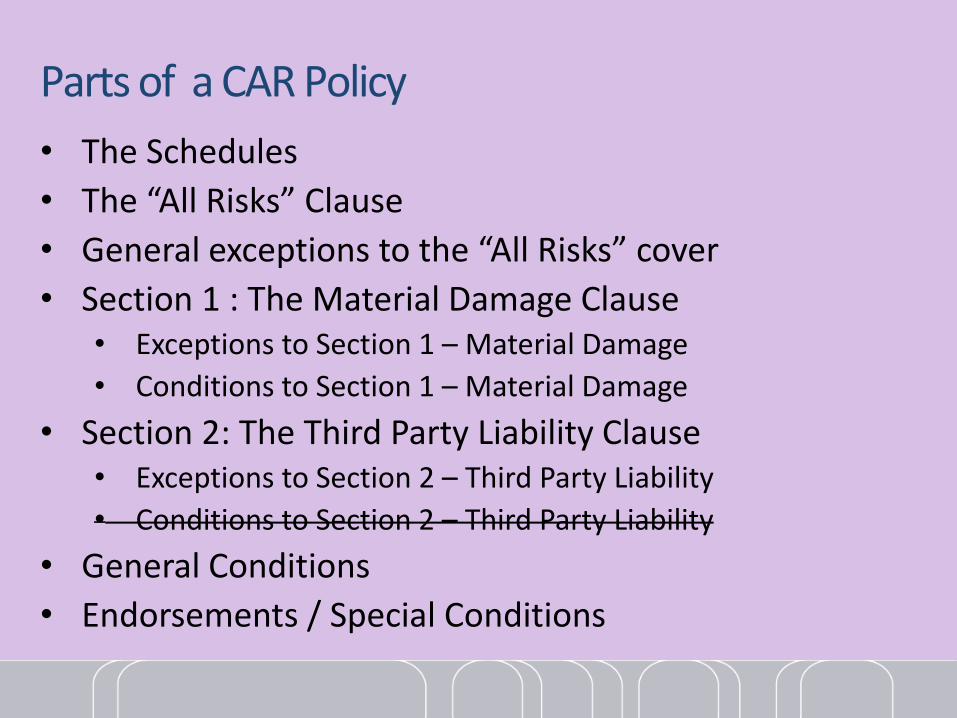

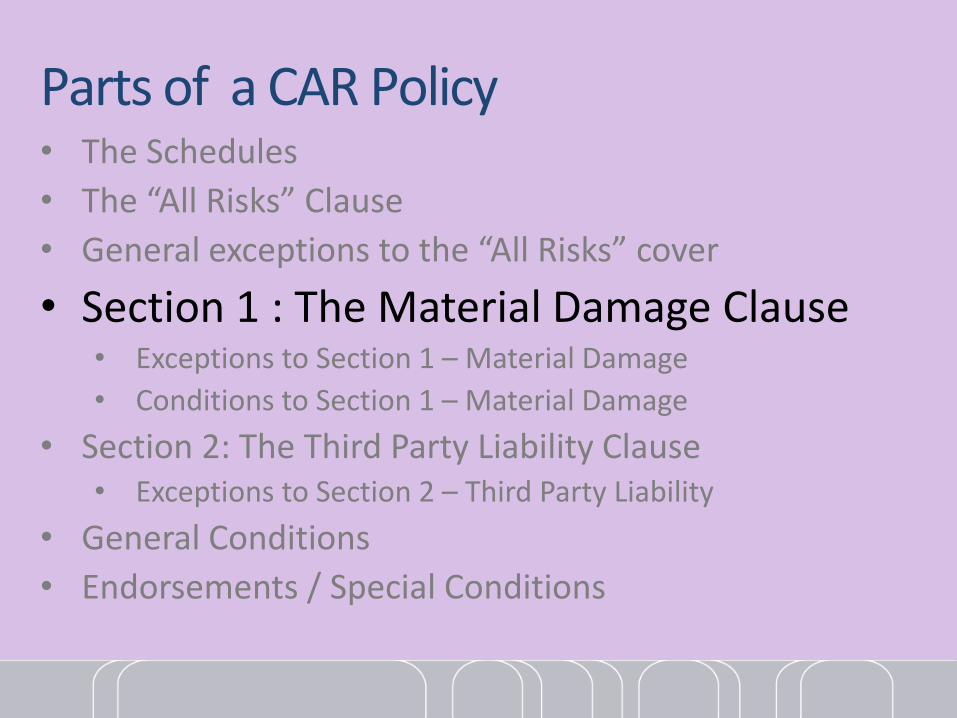

Parts of a CAR Policy

• The Schedules

• The “All Risks” Clause

• General exceptions to the “All Risks” cover

• Section 1 : The Material Damage Clause• Exceptions to Section 1 – Material Damage

• Conditions to Section 1 – Material Damage

• Section 2: The Third Party Liability Clause• Exceptions to Section 2 – Third Party Liability

• Conditions to Section 2 – Third Party Liability

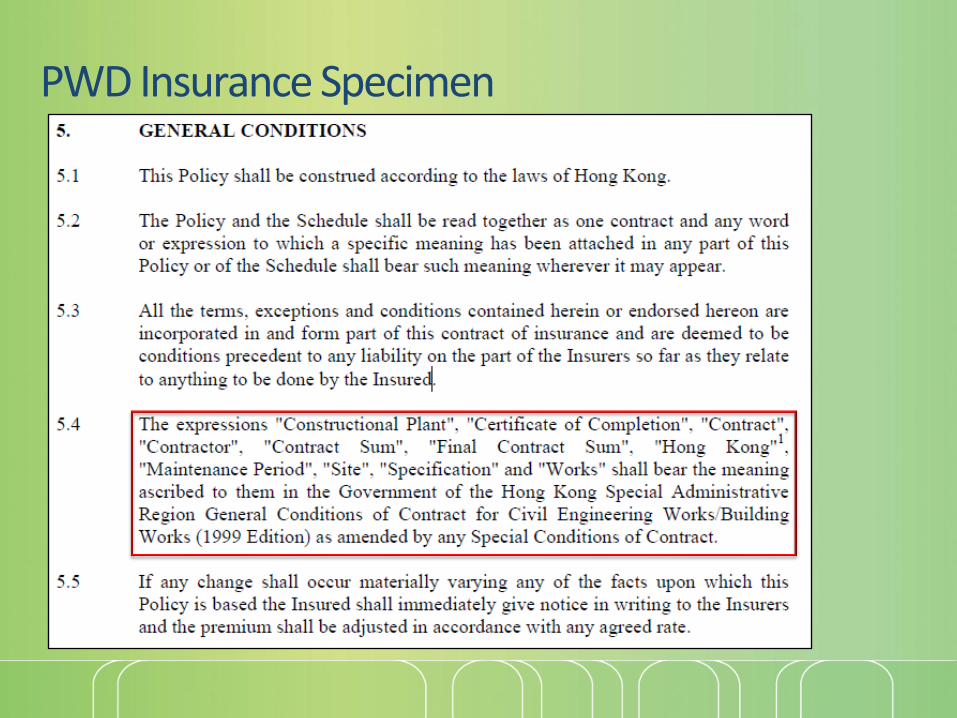

• General Conditions

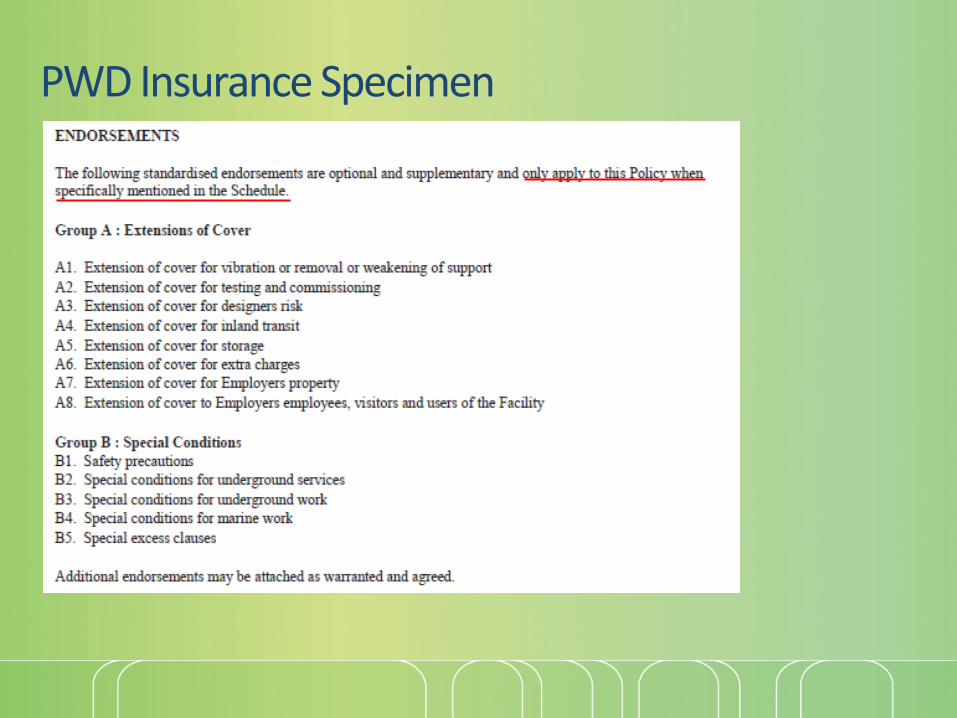

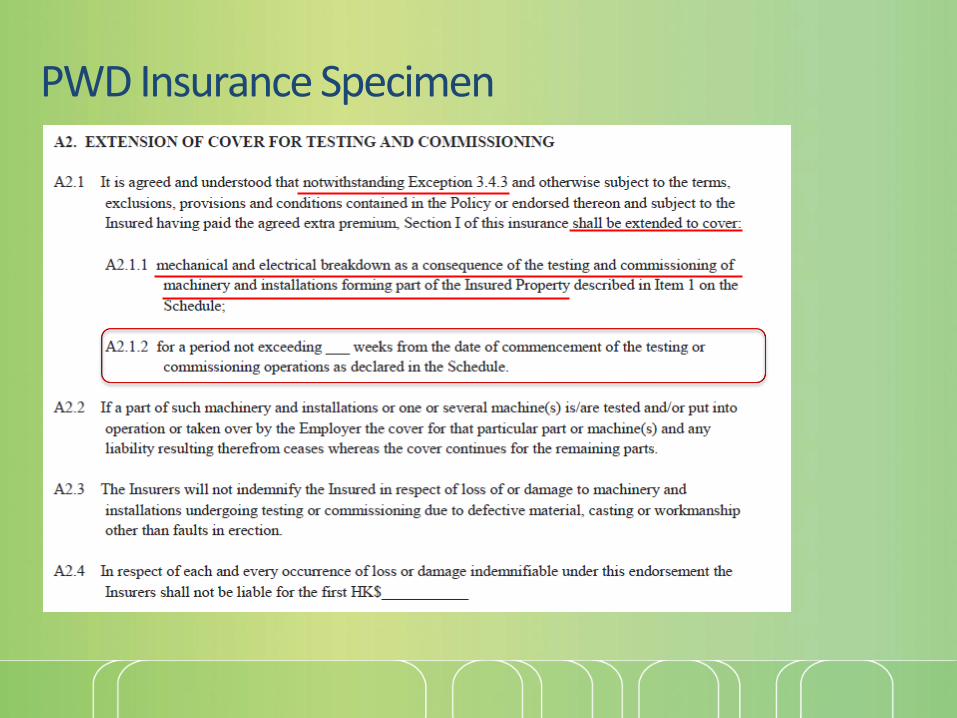

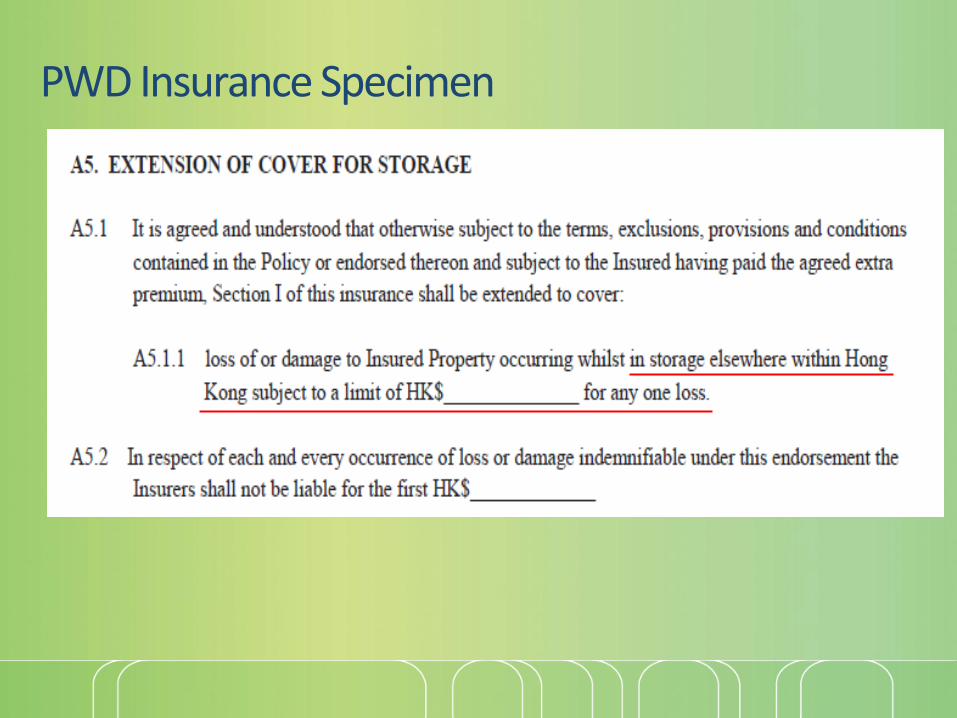

• Endorsements / Special Conditions

Parts of a CAR Policy• The Schedules• The “All Risks” Clause

• General exceptions to the “All Risks” cover

• Section 1 : The Material Damage Clause• Exceptions to Section 1 – Material Damage

• Conditions to Section 1 – Material Damage

• Section 2: The Third Party Liability Clause• Exceptions to Section 2 – Third Party Liability

• General Conditions

• Endorsements / Special Conditions

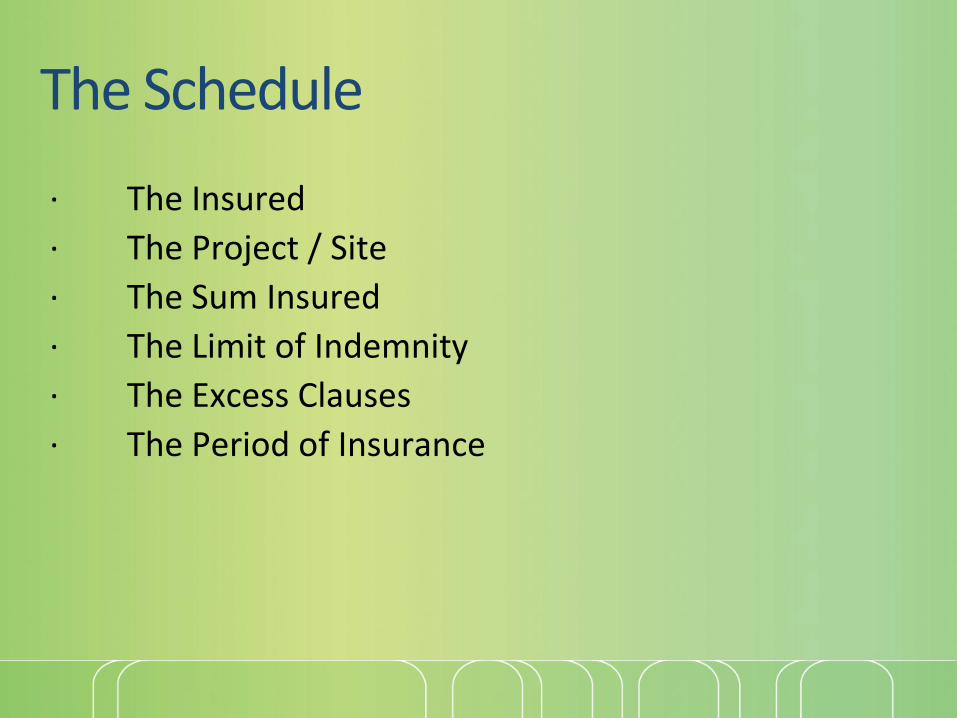

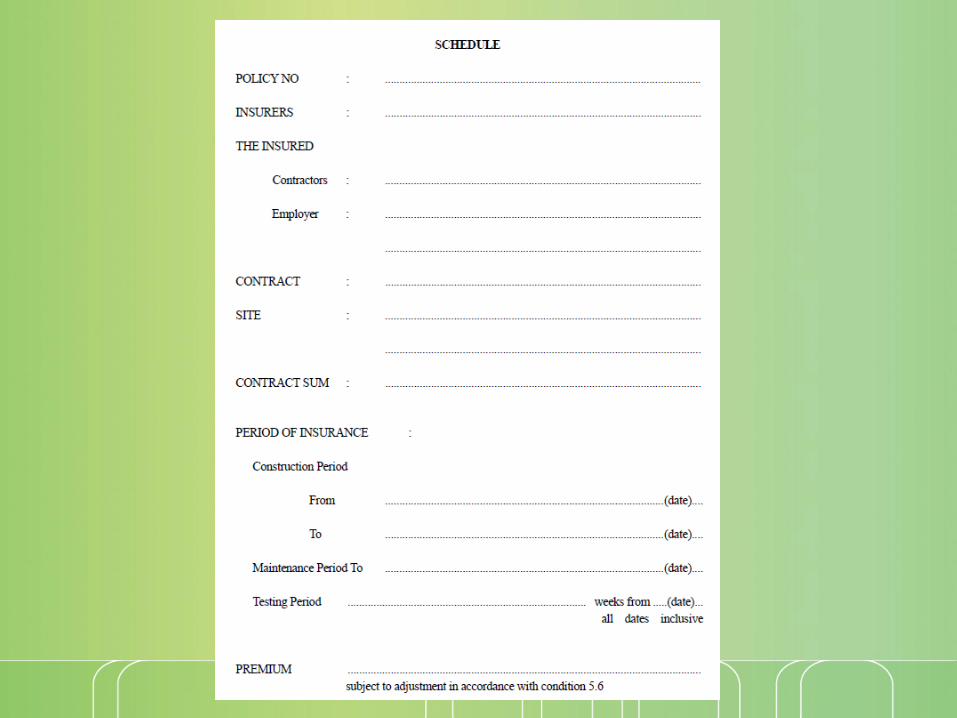

The Schedule

· The Insured

· The Project / Site

· The Sum Insured

· The Limit of Indemnity

· The Excess Clauses

· The Period of Insurance

Parts of a CAR Policy• The Schedules

• The “All Risks” Clause• General exceptions to the “All Risks” cover

• Section 1 : The Material Damage Clause• Exceptions to Section 1 – Material Damage

• Conditions to Section 1 – Material Damage

• Section 2: The Third Party Liability Clause• Exceptions to Section 2 – Third Party Liability

• General Conditions

• Endorsements / Special Conditions

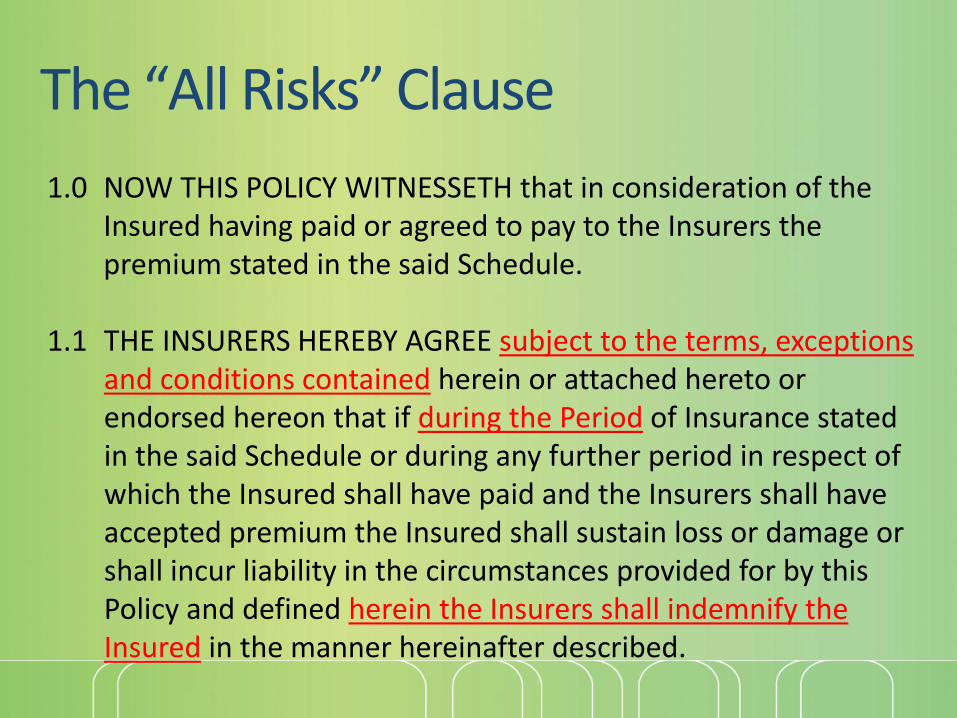

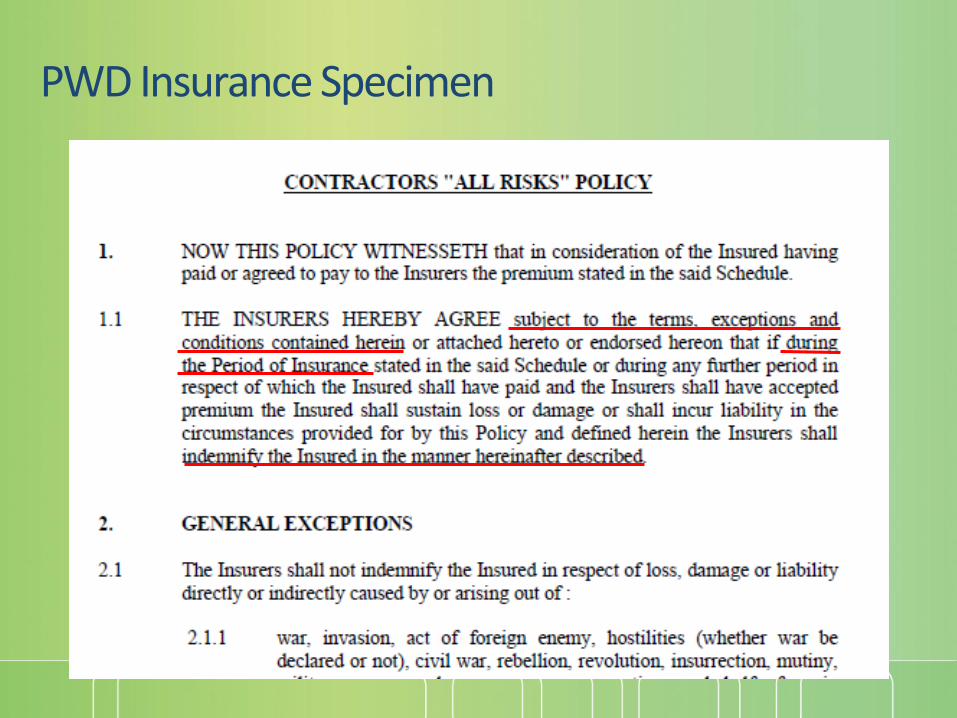

The “All Risks” Clause

1.0 NOW THIS POLICY WITNESSETH that in consideration of the Insured having paid or agreed to pay to the Insurers the premium stated in the said Schedule.

1.1 THE INSURERS HEREBY AGREE subject to the terms, exceptions and conditions contained herein or attached hereto or endorsed hereon that if during the Period of Insurance stated in the said Schedule or during any further period in respect of which the Insured shall have paid and the Insurers shall have accepted premium the Insured shall sustain loss or damage or shall incur liability in the circumstances provided for by this Policy and defined herein the Insurers shall indemnify the Insured in the manner hereinafter described.

Parts of a CAR Policy• The Schedules

• The “All Risks” Clause

• General exceptions to the “All Risks” cover• Section 1 : The Material Damage Clause

• Exceptions to Section 1 – Material Damage

• Conditions to Section 1 – Material Damage

• Section 2: The Third Party Liability Clause• Exceptions to Section 2 – Third Party Liability

• General Conditions

• Endorsements / Special Conditions

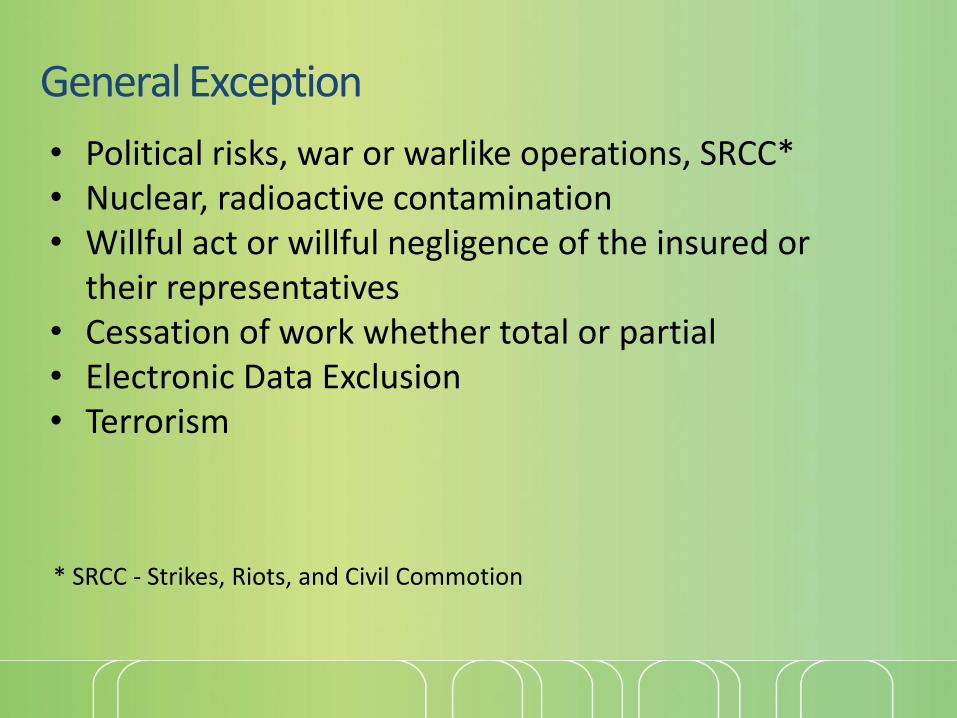

General Exception

• Political risks, war or warlike operations, SRCC*• Nuclear, radioactive contamination• Willful act or willful negligence of the insured or

their representatives• Cessation of work whether total or partial• Electronic Data Exclusion• Terrorism

* SRCC - Strikes, Riots, and Civil Commotion

Parts of a CAR Policy• The Schedules

• The “All Risks” Clause

• General exceptions to the “All Risks” cover

• Section 1 : The Material Damage Clause• Exceptions to Section 1 – Material Damage

• Conditions to Section 1 – Material Damage

• Section 2: The Third Party Liability Clause• Exceptions to Section 2 – Third Party Liability

• General Conditions

• Endorsements / Special Conditions

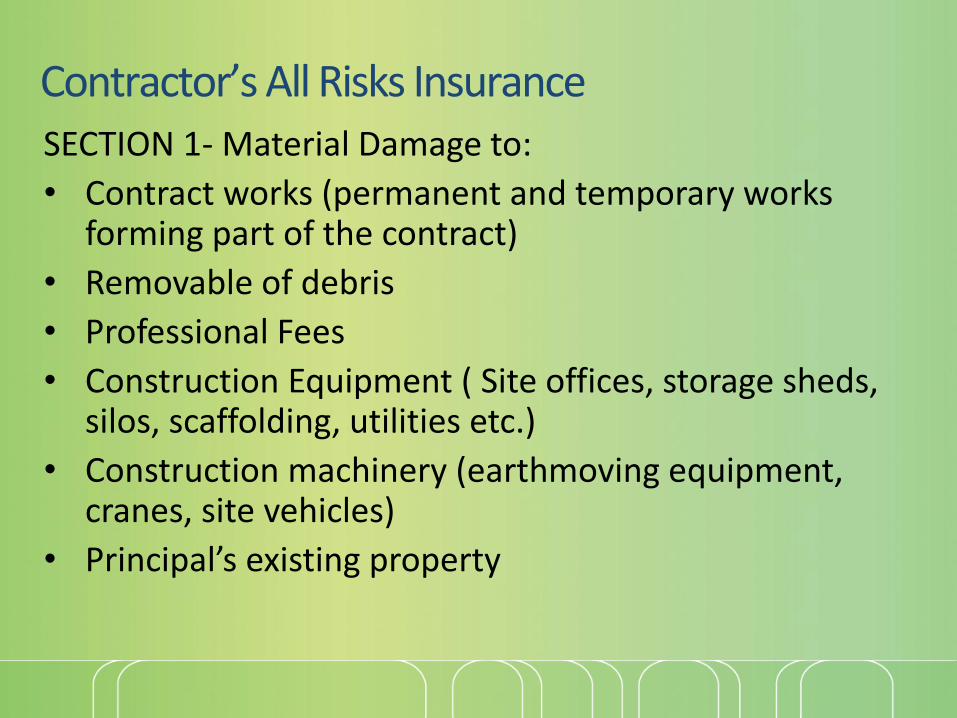

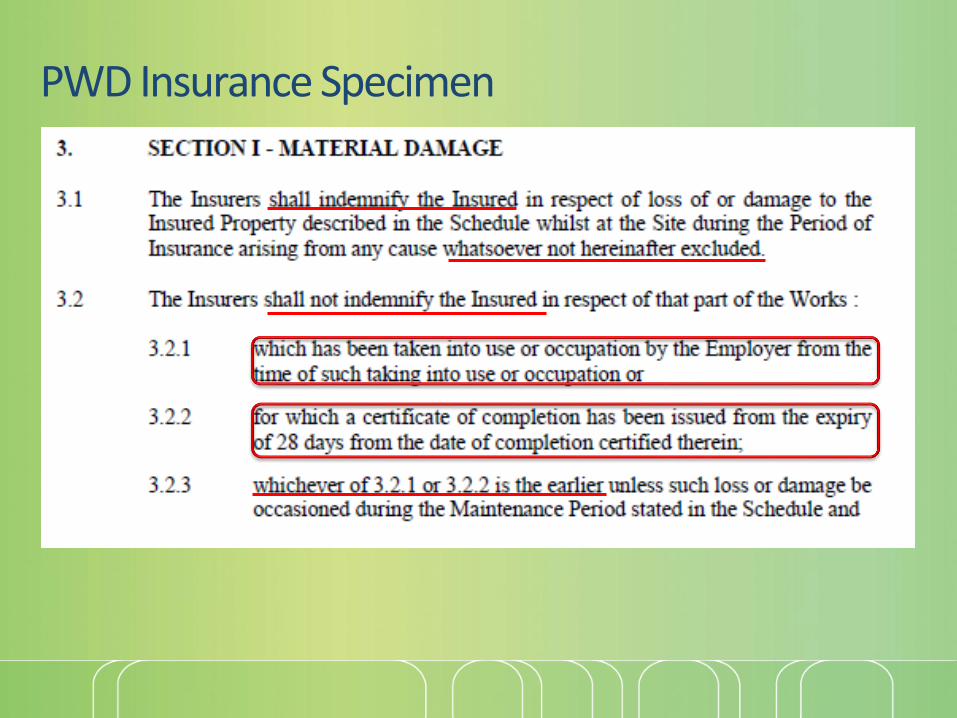

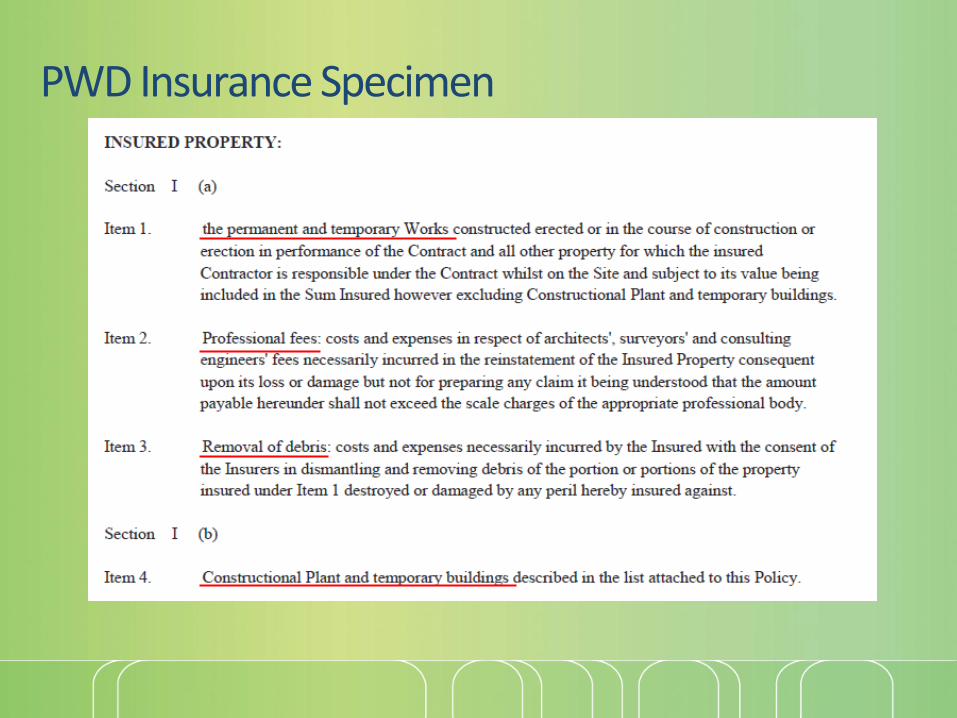

Contractor’s All Risks InsuranceSECTION 1- Material Damage to:

• Contract works (permanent and temporary works forming part of the contract)

• Removable of debris

• Professional Fees

• Construction Equipment ( Site offices, storage sheds, silos, scaffolding, utilities etc.)

• Construction machinery (earthmoving equipment, cranes, site vehicles)

• Principal’s existing property

Parts of a CAR Policy• The Schedules

• The “All Risks” Clause

• General exceptions to the “All Risks” cover

• Section 1 : The Material Damage Clause

• Exceptions to Section 1 – Material Damage• Conditions to Section 1 – Material Damage

• Section 2: The Third Party Liability Clause• Exceptions to Section 2 – Third Party Liability

• General Conditions

• Endorsements / Special Conditions

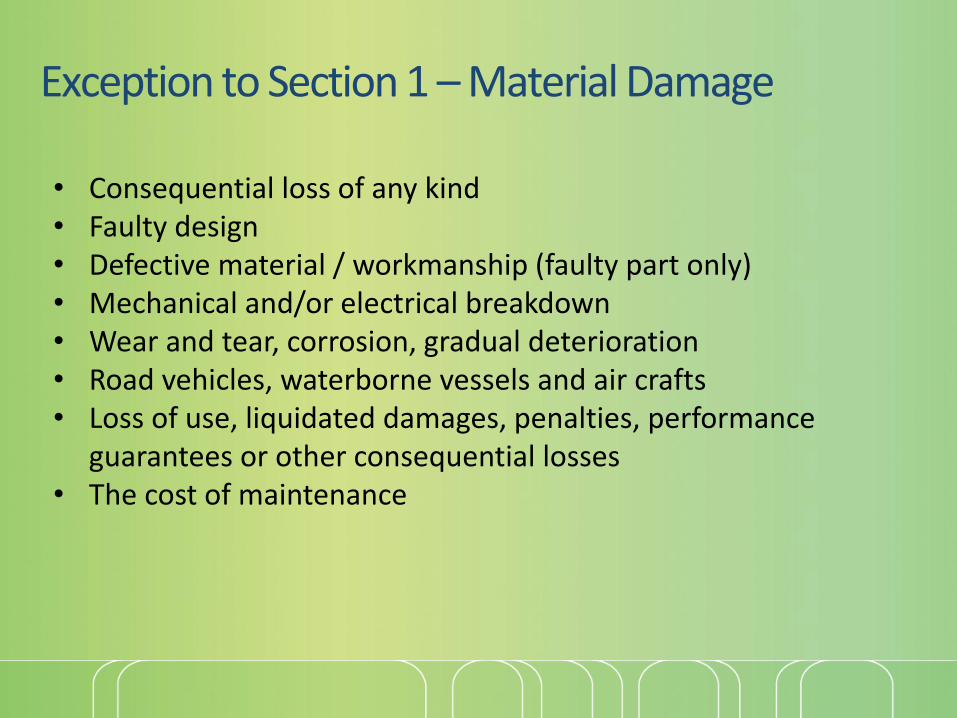

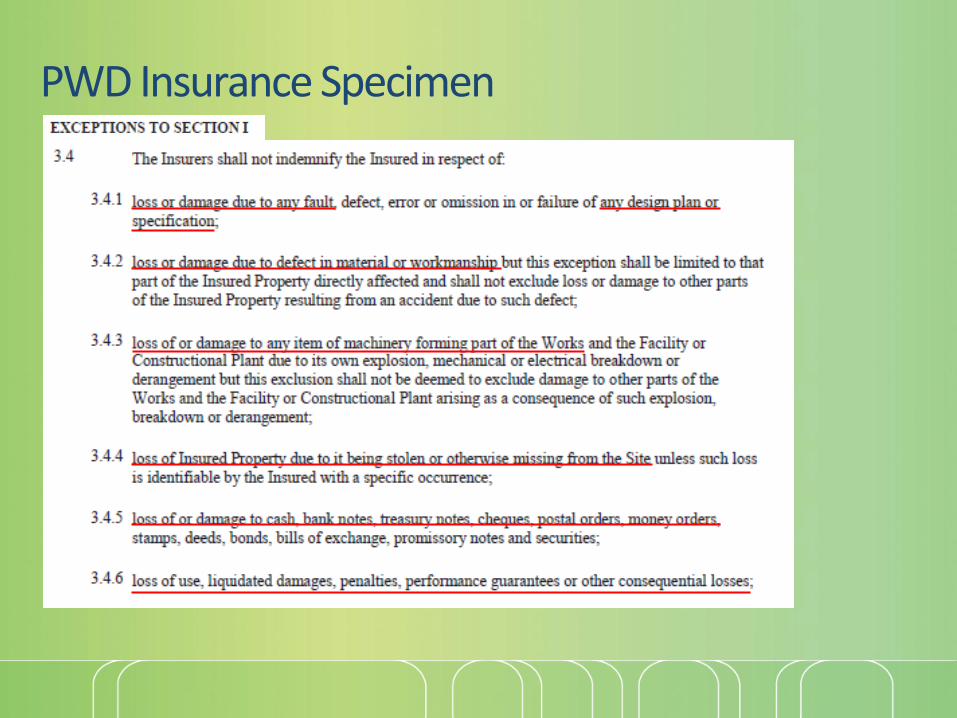

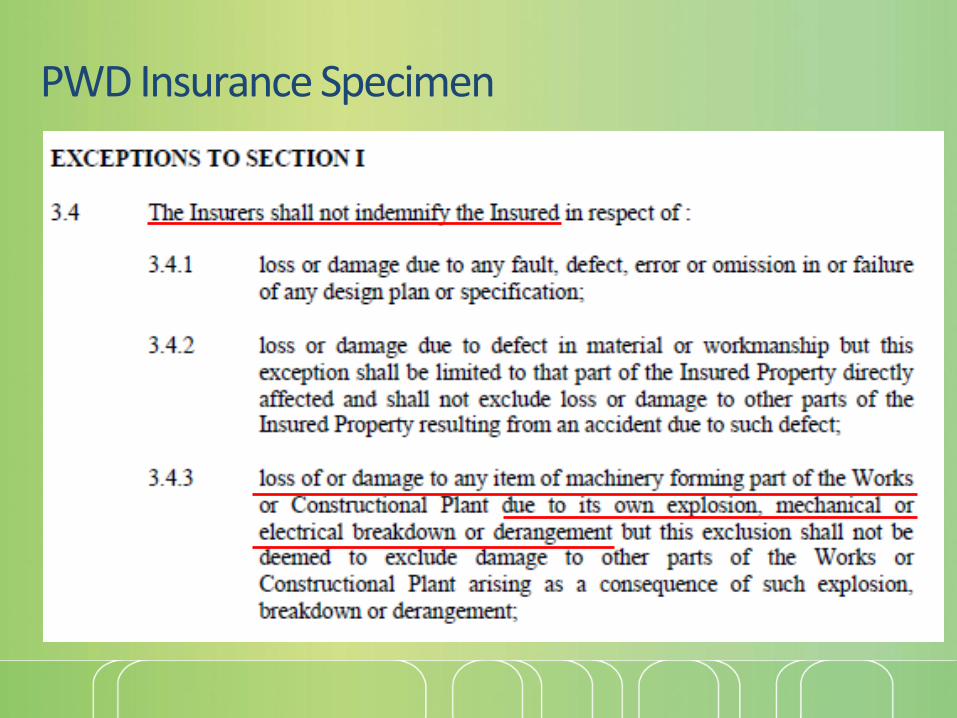

Exception to Section 1 – Material Damage

• Consequential loss of any kind• Faulty design• Defective material / workmanship (faulty part only)• Mechanical and/or electrical breakdown• Wear and tear, corrosion, gradual deterioration• Road vehicles, waterborne vessels and air crafts• Loss of use, liquidated damages, penalties, performance

guarantees or other consequential losses• The cost of maintenance

Parts of a CAR Policy• The Schedules

• The “All Risks” Clause

• General exceptions to the “All Risks” cover

• Section 1 : The Material Damage Clause• Exceptions to Section 1 – Material Damage

• Conditions to Section 1 – Material Damage

• Section 2: The Third Party Liability Clause• Exceptions to Section 2 – Third Party Liability

• General Conditions

• Endorsements / Special Conditions

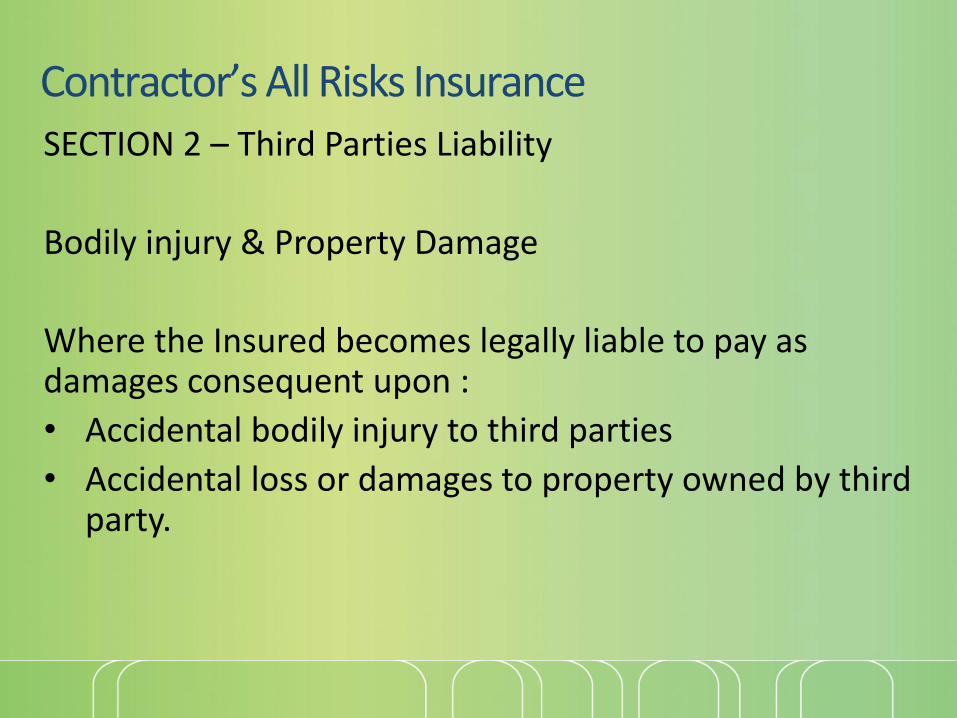

Contractor’s All Risks InsuranceSECTION 2 – Third Parties Liability

Bodily injury & Property Damage

Where the Insured becomes legally liable to pay as damages consequent upon :

• Accidental bodily injury to third parties

• Accidental loss or damages to property owned by third party.

Parts of a CAR Policy• The Schedules

• The “All Risks” Clause

• General exceptions to the “All Risks” cover

• Section 1 : The Material Damage Clause• Exceptions to Section 1 – Material Damage

• Conditions to Section 1 – Material Damage

• Section 2: The Third Party Liability Clause

• Exceptions to Section 2 – Third Party Liability• General Conditions

• Endorsements / Special Conditions

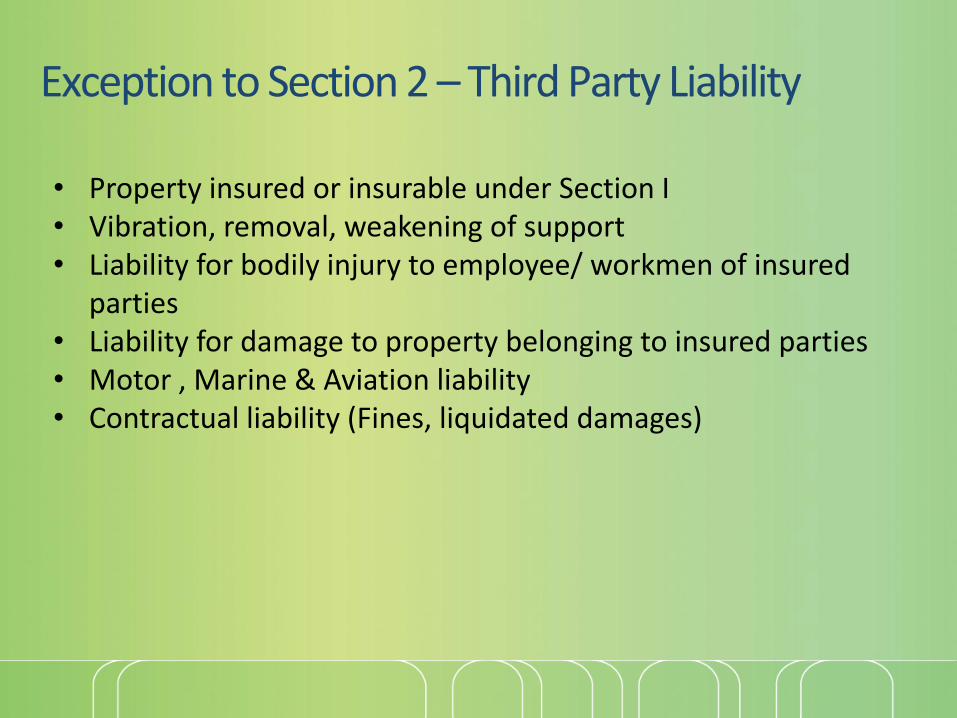

Exception to Section 2 – Third Party Liability

• Property insured or insurable under Section I• Vibration, removal, weakening of support• Liability for bodily injury to employee/ workmen of insured

parties • Liability for damage to property belonging to insured parties• Motor , Marine & Aviation liability• Contractual liability (Fines, liquidated damages)

PWD Insurance Specimen

PWD Insurance Specimen

PWD Insurance Specimen

PWD Insurance Specimen

PWD Insurance Specimen

PWD Insurance Specimen

PWD Insurance Specimen

PWD Insurance Specimen

PWD Insurance Specimen

PWD Insurance Specimen

PWD Insurance Specimen

PWD Insurance Specimen

PWD Insurance Specimen

PWD Insurance Specimen

PWD Insurance Specimen

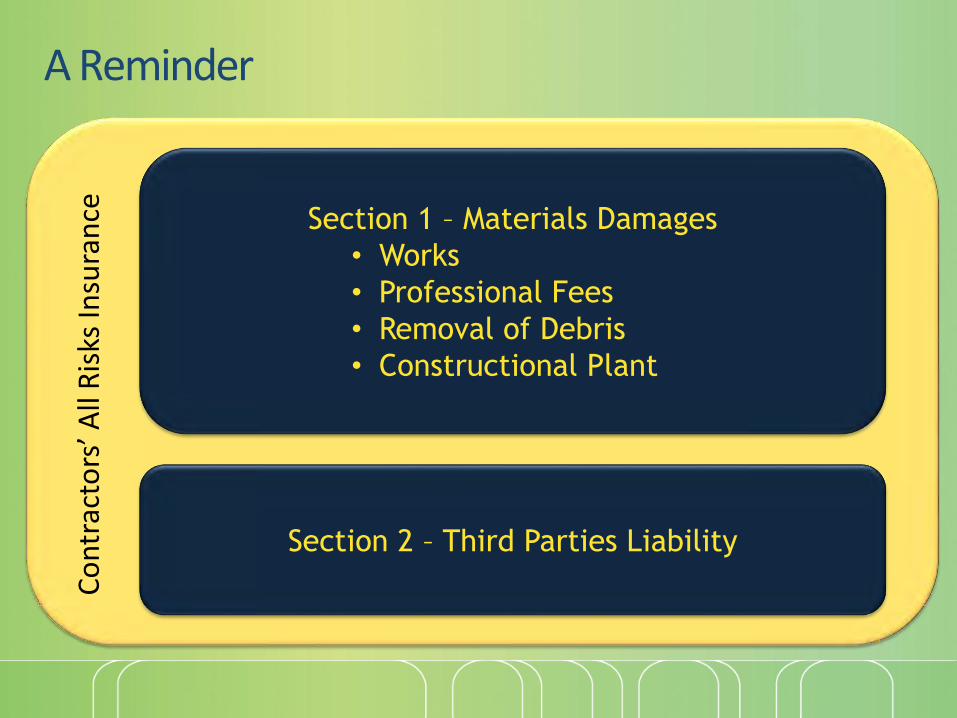

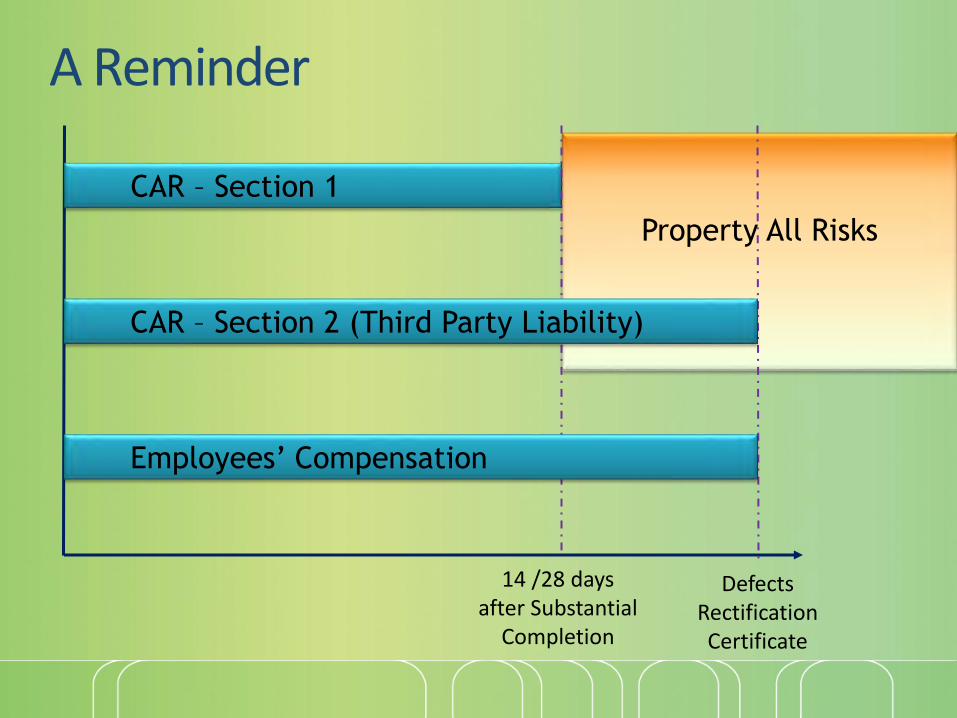

A Reminder

Section 1 – Materials Damages

• Works

• Professional Fees

• Removal of Debris

• Constructional Plant

Section 2 – Third Parties Liability

Co

ntr

acto

rs’ A

ll R

isks

Insu

ran

ce

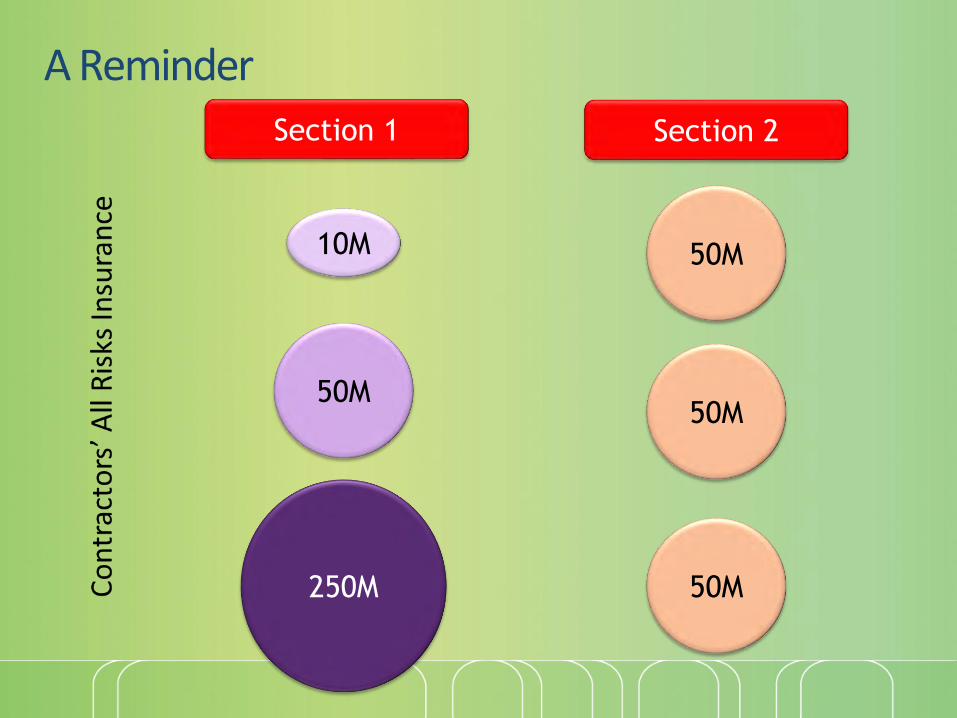

A Reminder

Section 1 Section 2

50M

10M

50M

50M

250M

50M

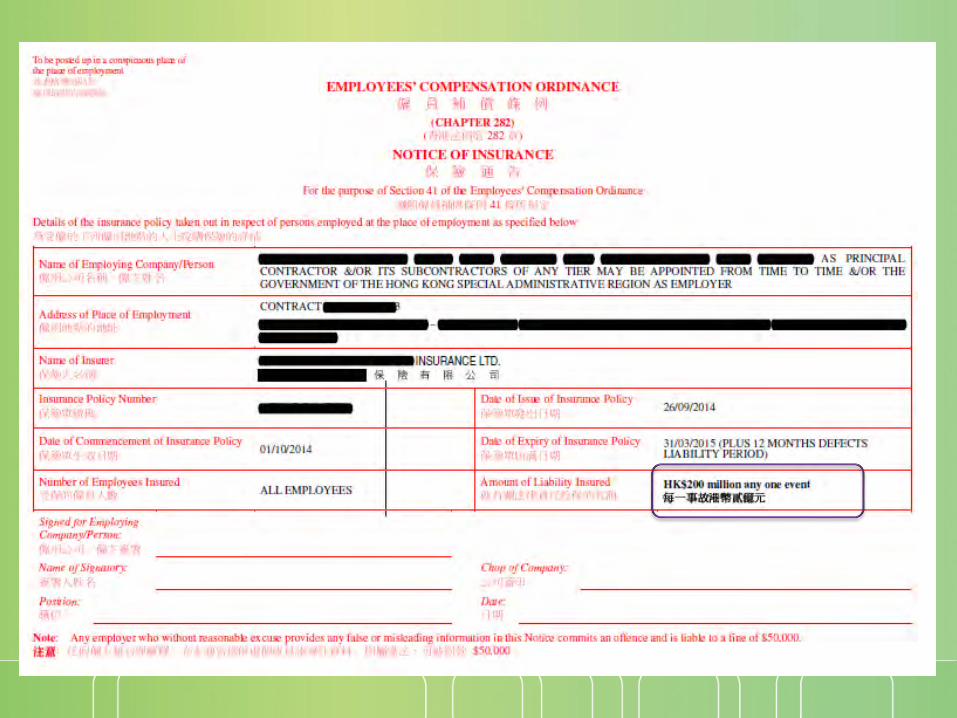

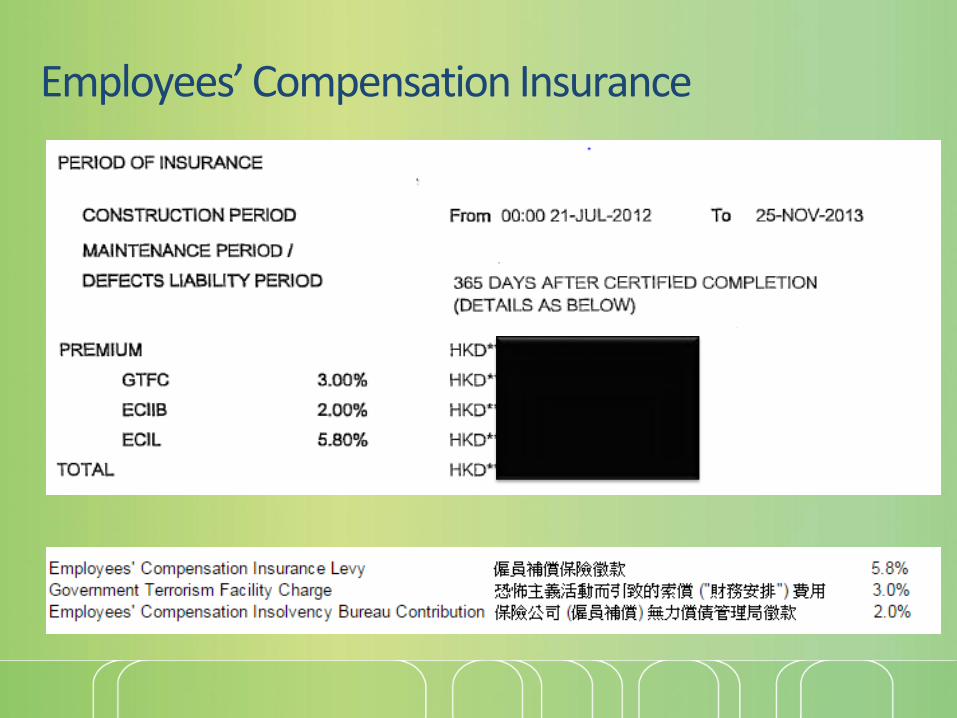

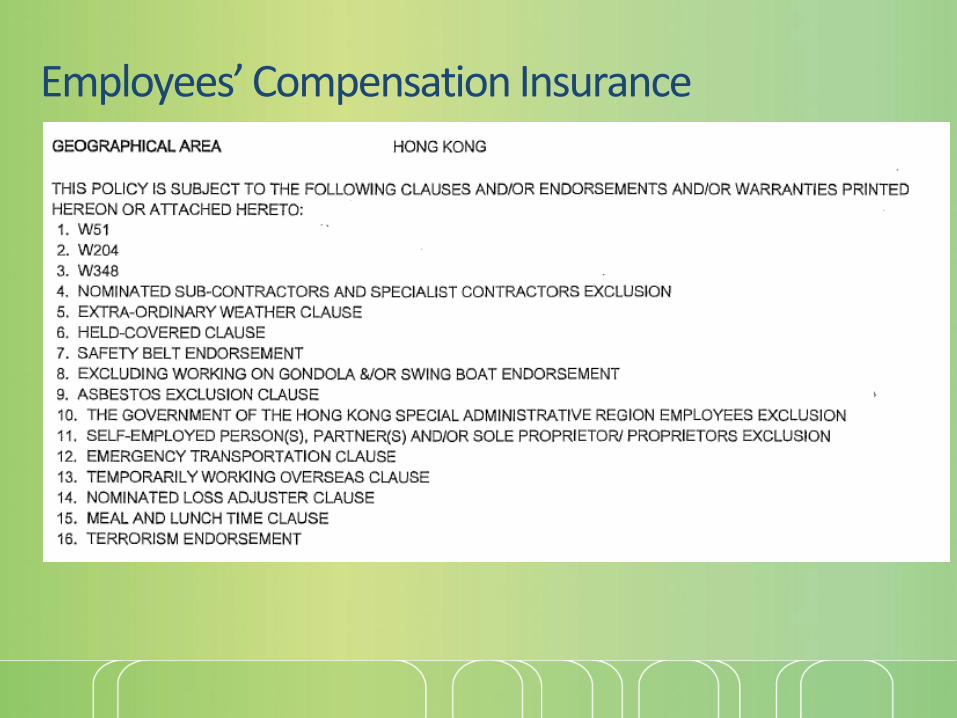

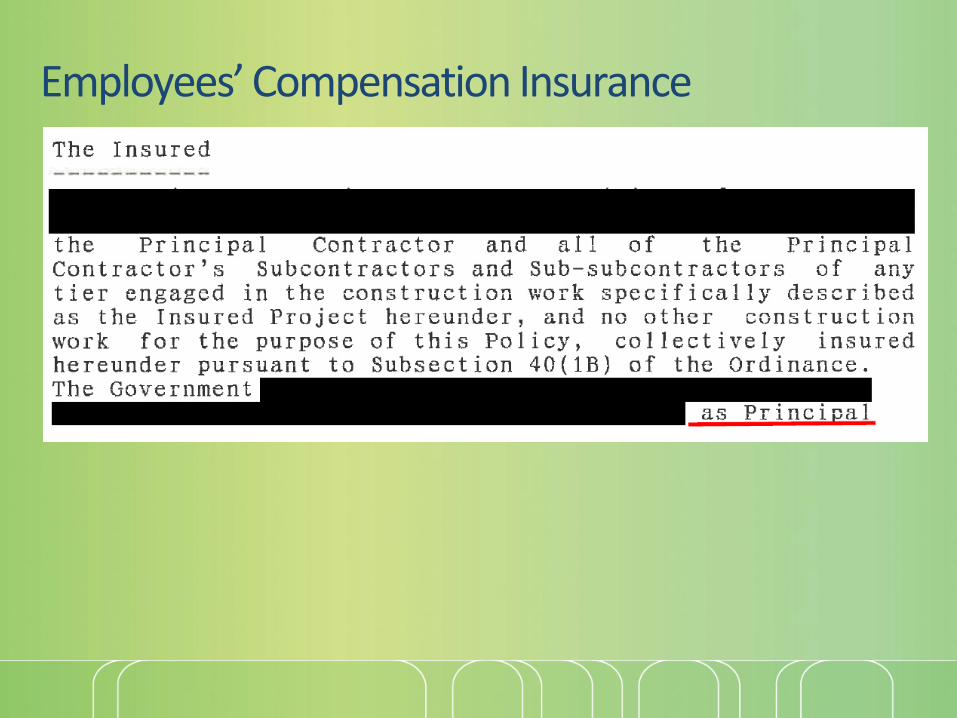

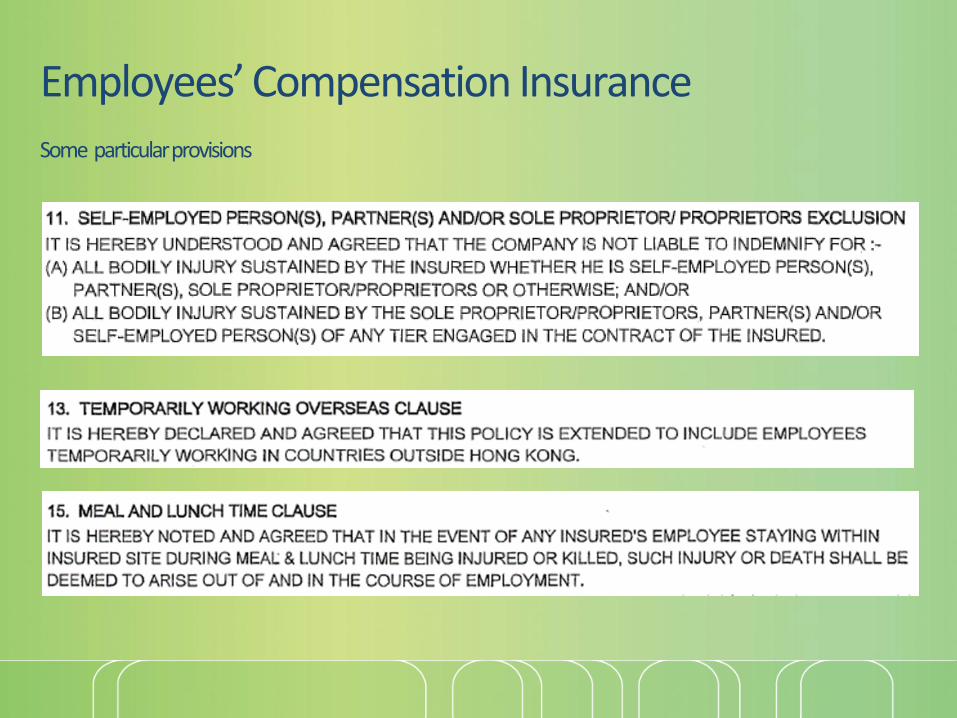

Employees’ Compensation Insurance

Employees’ Compensation Insurance

Employees’ Compensation Insurance

Employees’ Compensation Insurance

Employees’ Compensation Insurance

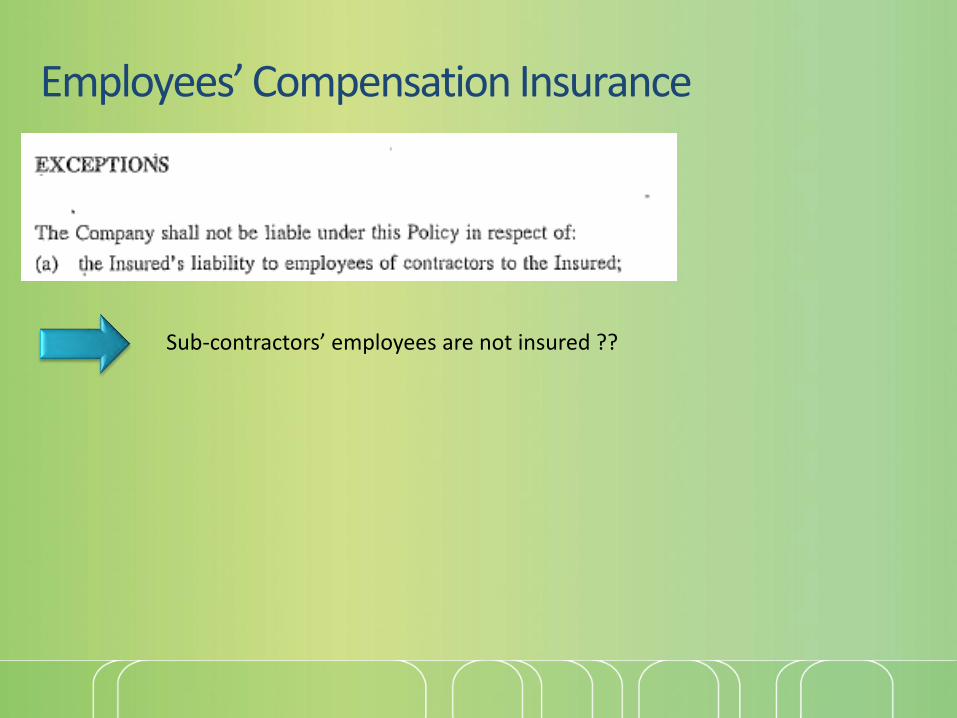

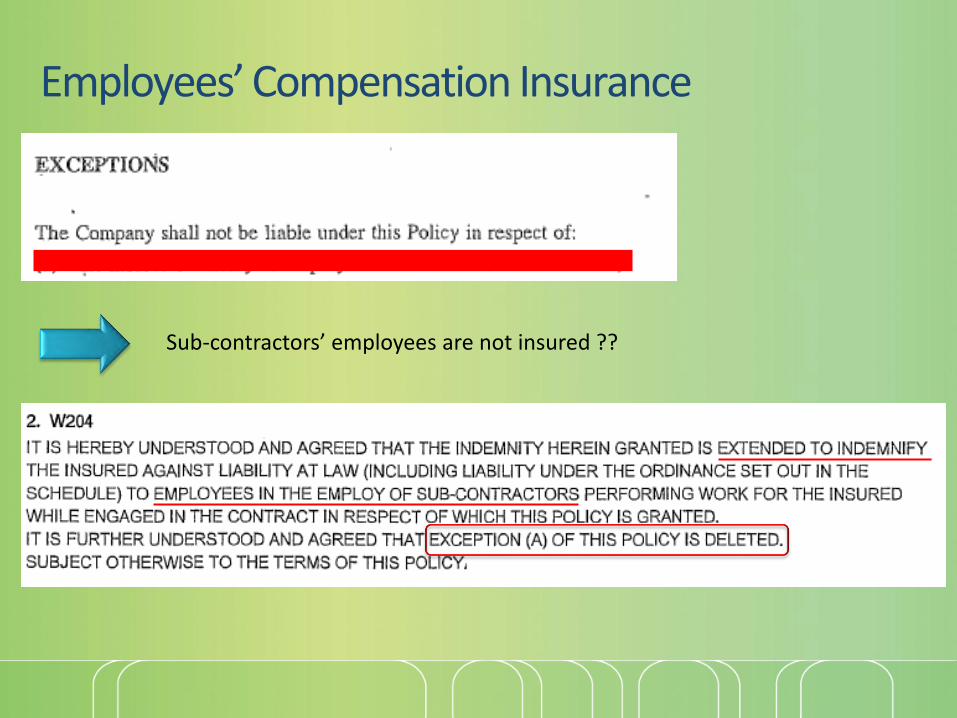

Sub-contractors’ employees are not insured ??

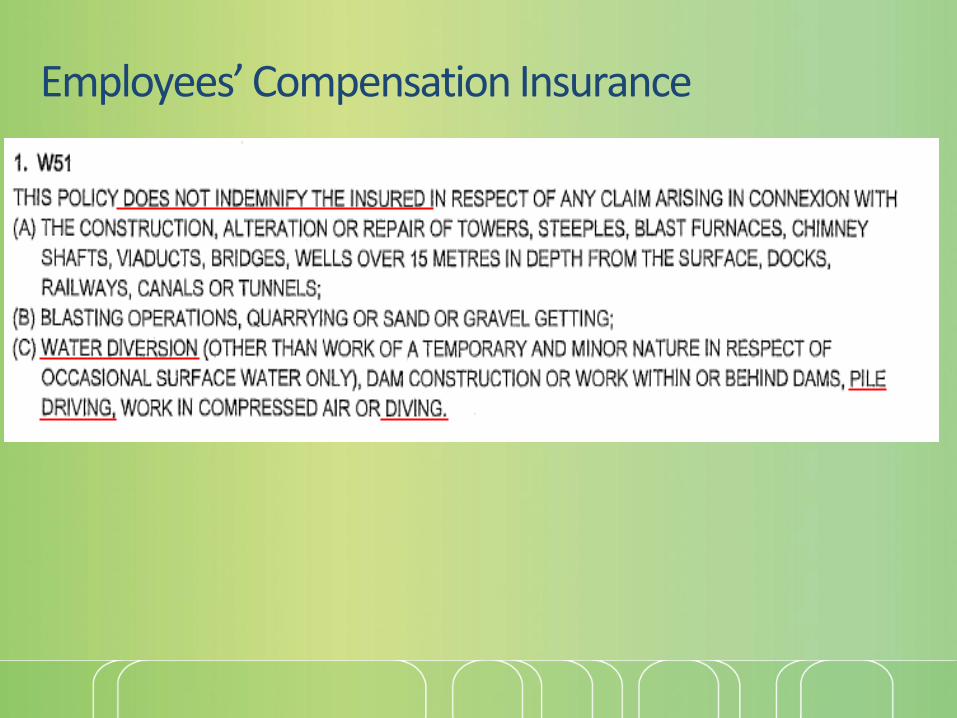

Employees’ Compensation Insurance

Sub-contractors’ employees are not insured ??

Employees’ Compensation Insurance

Employees’ Compensation Insurance

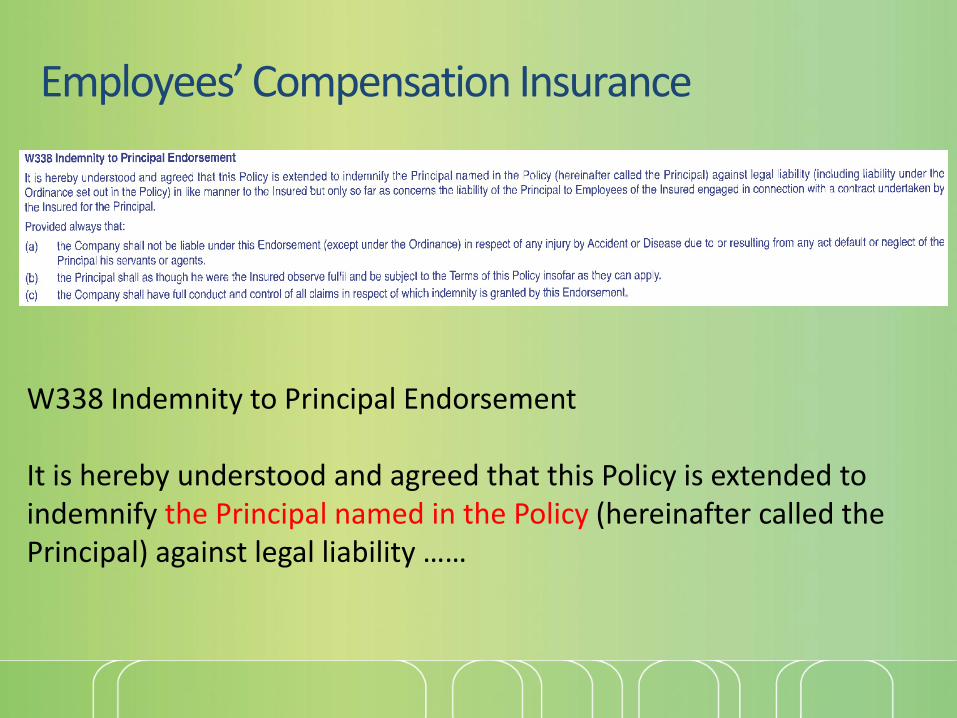

W338 Indemnity to Principal Endorsement

It is hereby understood and agreed that this Policy is extended to indemnify the Principal named in the Policy (hereinafter called the Principal) against legal liability ……

Employees’ Compensation Insurance

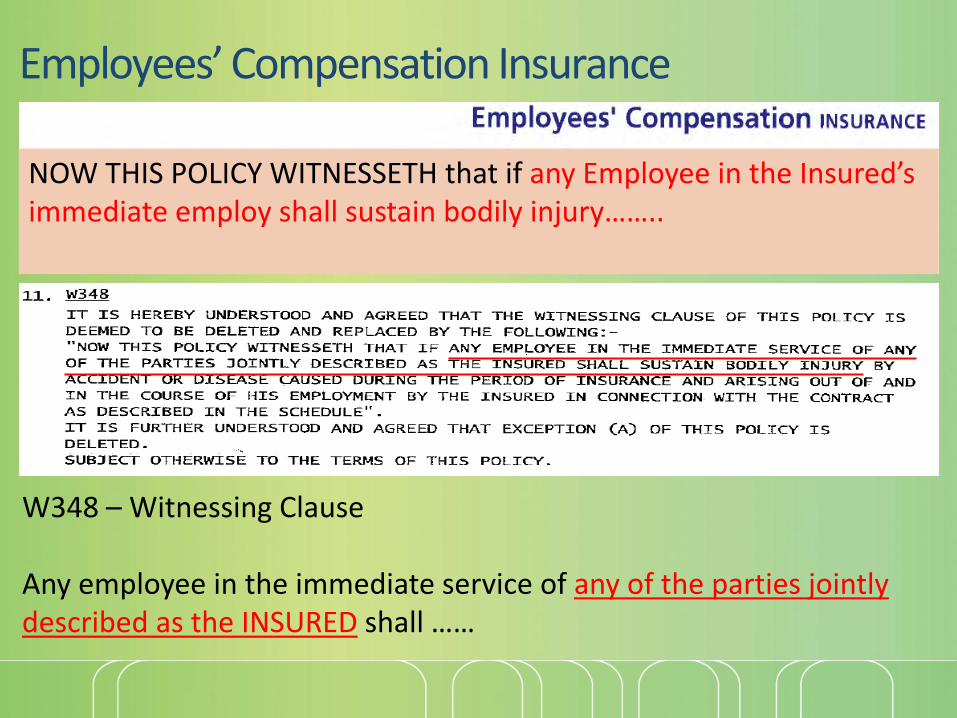

W348 – Witnessing Clause

Any employee in the immediate service of any of the parties jointly described as the INSURED shall ……

NOW THIS POLICY WITNESSETH that if any Employee in the Insured’s immediate employ shall sustain bodily injury……..

Employees’ Compensation Insurance

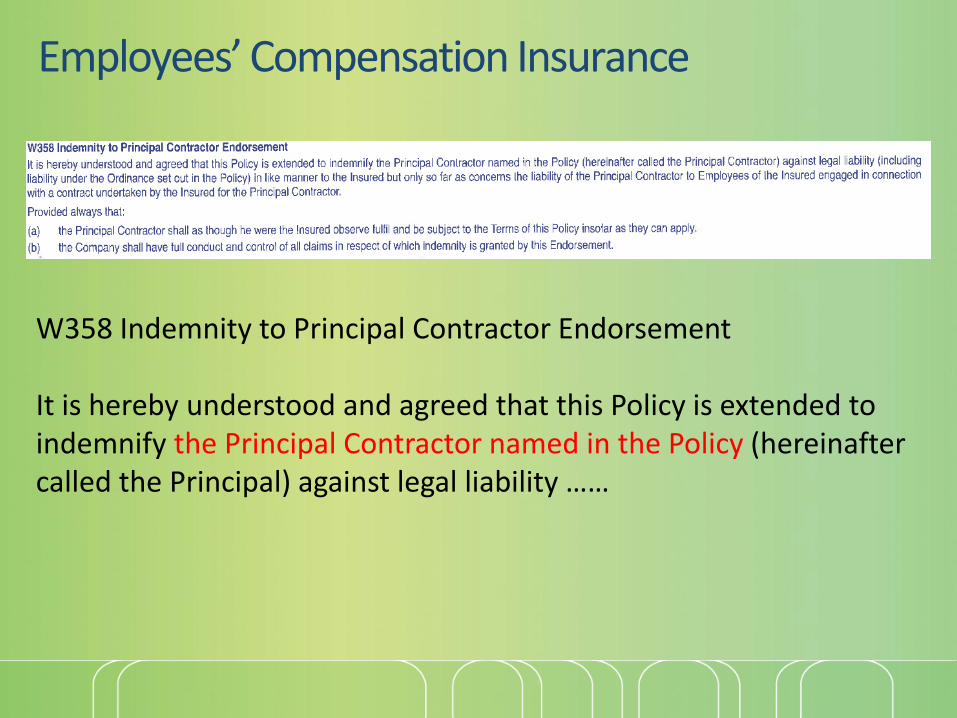

W358 Indemnity to Principal Contractor Endorsement

It is hereby understood and agreed that this Policy is extended to indemnify the Principal Contractor named in the Policy (hereinafter called the Principal) against legal liability ……

Employees’ Compensation Insurance

Some particular provisions

Property All Risks

A Reminder

CAR – Section 1

CAR – Section 2 (Third Party Liability)

Employees’ Compensation

14 /28 days after Substantial

Completion

Defects Rectification Certificate

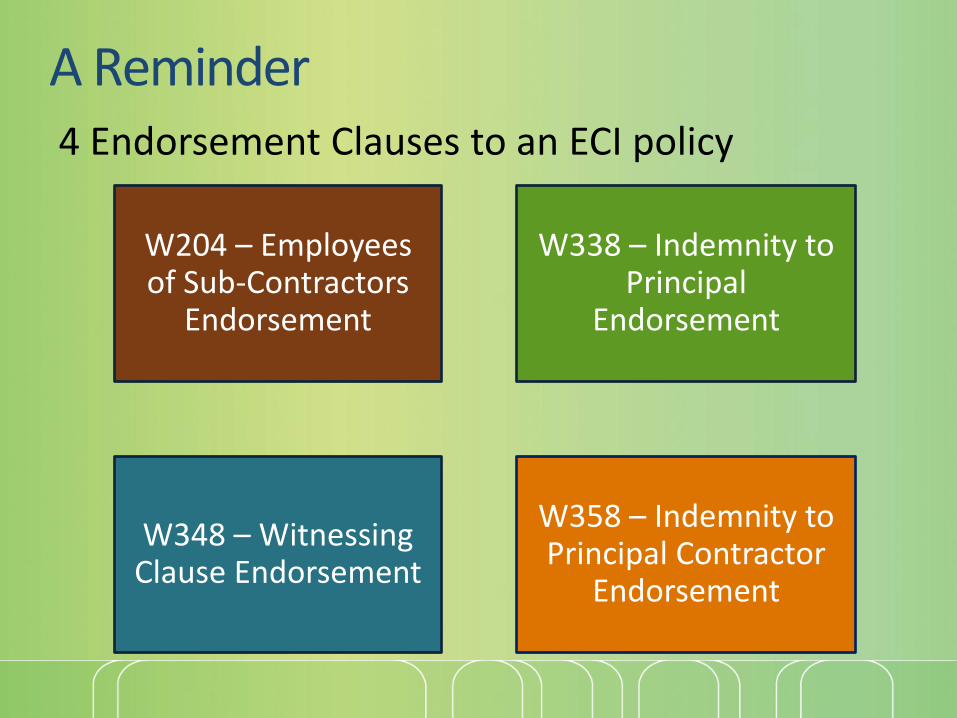

A Reminder

W204 – Employees of Sub-Contractors

Endorsement

W338 – Indemnity to Principal

Endorsement

W348 – Witnessing Clause Endorsement

W358 – Indemnity to Principal Contractor

Endorsement

4 Endorsement Clauses to an ECI policy

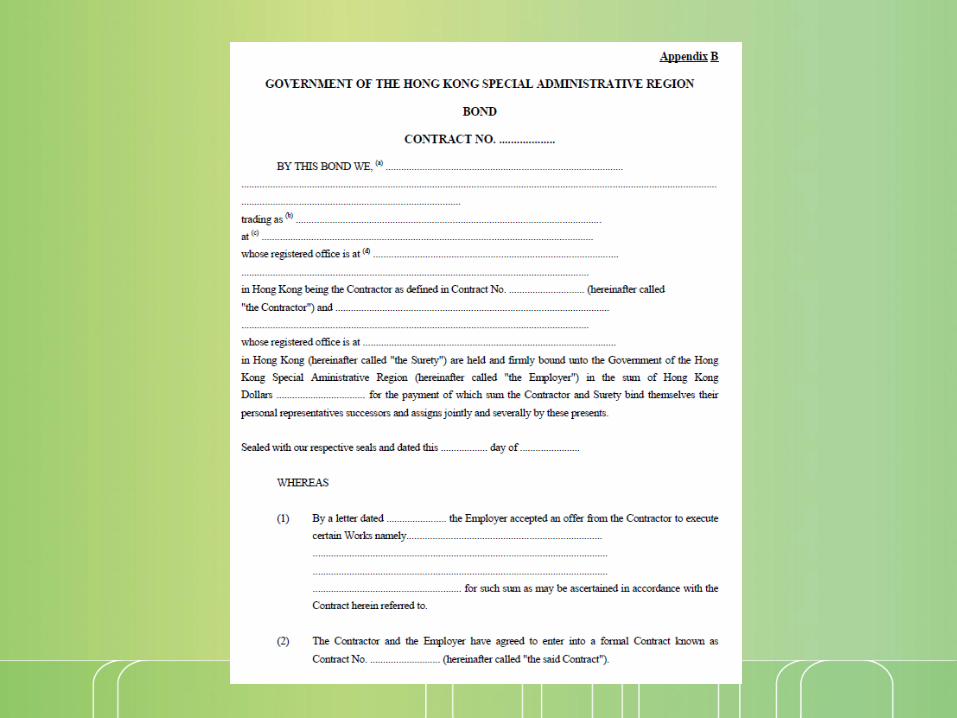

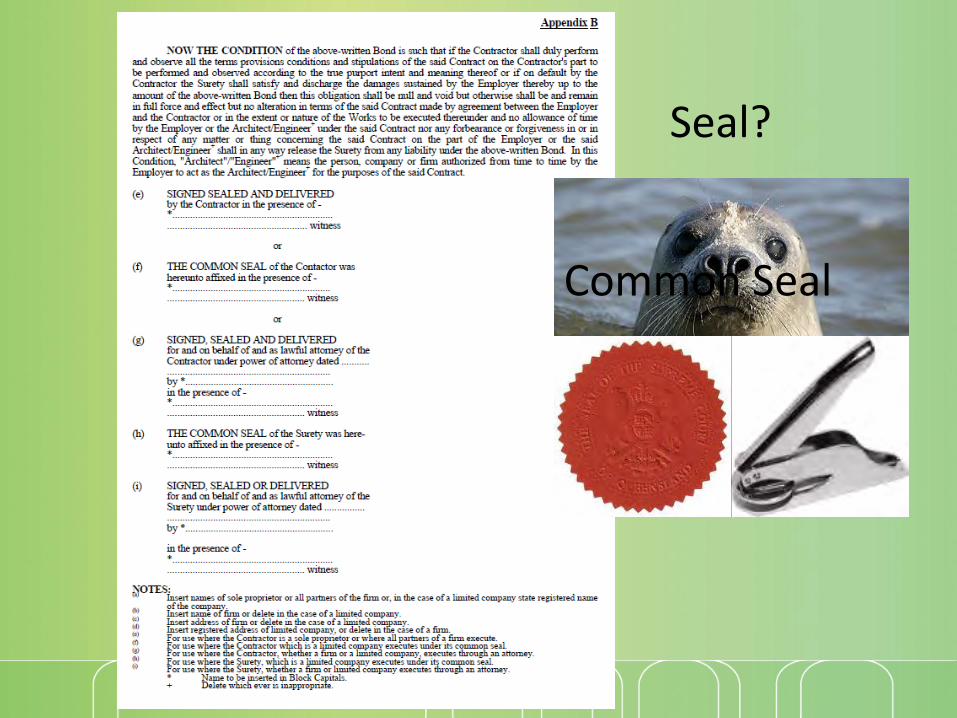

Bond

Bond

Story Time

Types of Taxi有駕駛員的計程車

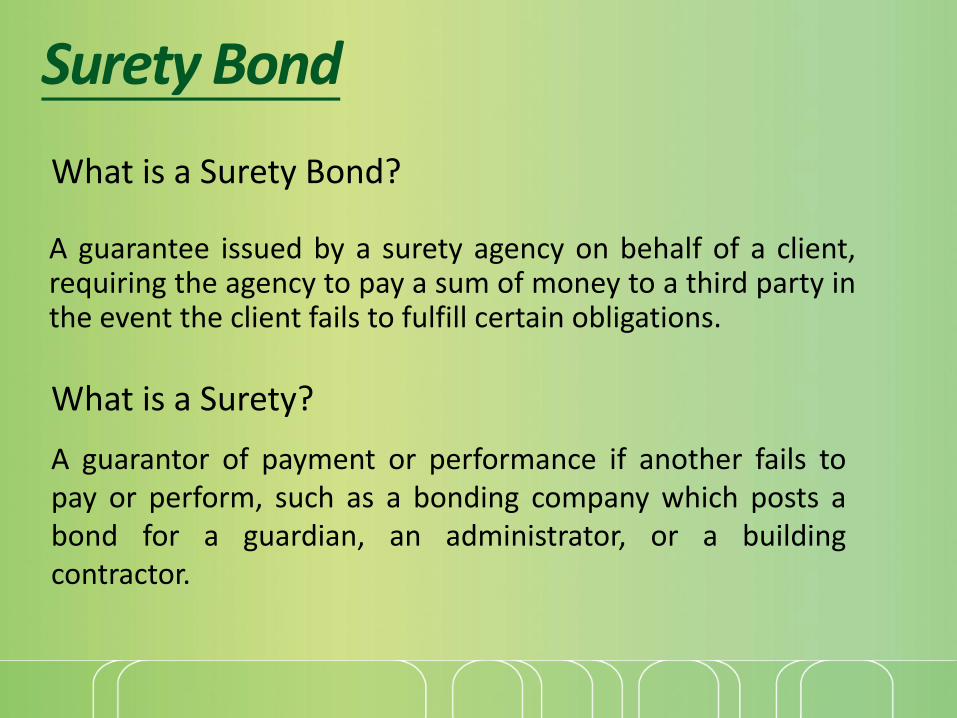

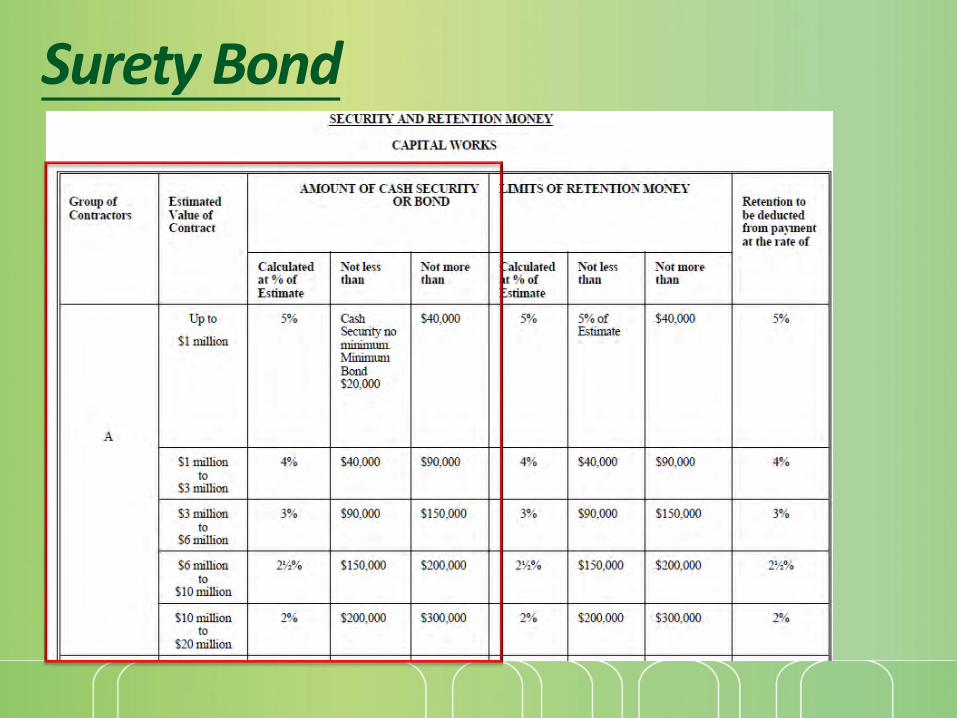

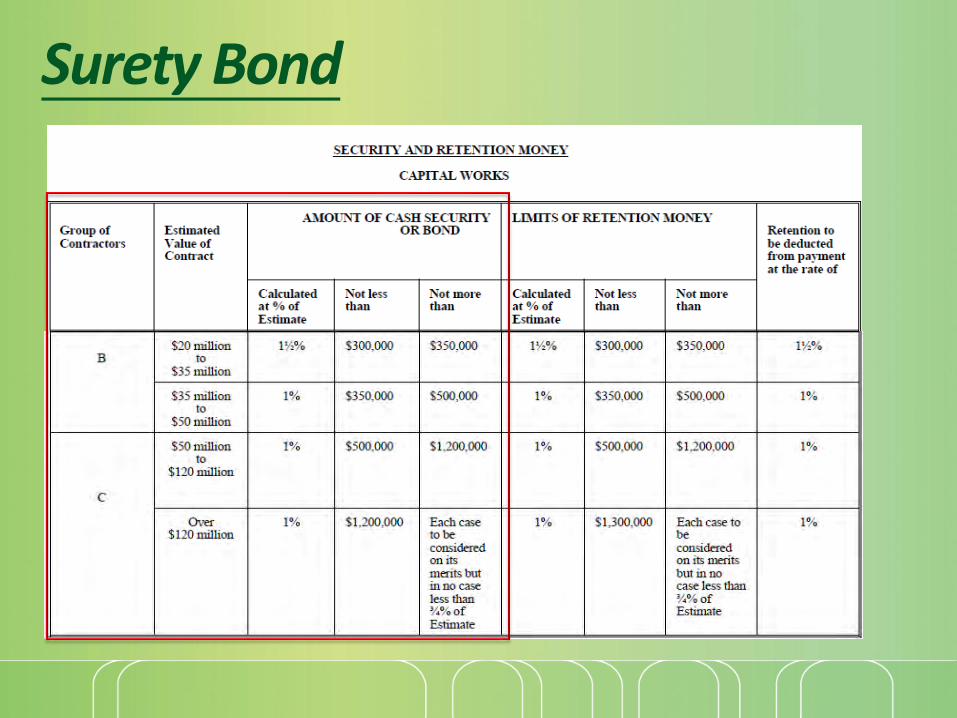

Surety Bond

A guarantee issued by a surety agency on behalf of a client,requiring the agency to pay a sum of money to a third party inthe event the client fails to fulfill certain obligations.

What is a Surety Bond?

A guarantor of payment or performance if another fails topay or perform, such as a bonding company which posts abond for a guardian, an administrator, or a buildingcontractor.

What is a Surety?

Surety Bond

Guarantee

(Employer who requires a bond)

Contractor

(who is required to provide a bond)

Surety - Guarantor

(Company who issues and guarantees a bond)

Building ContractSurety Bond

Counter Indemnity

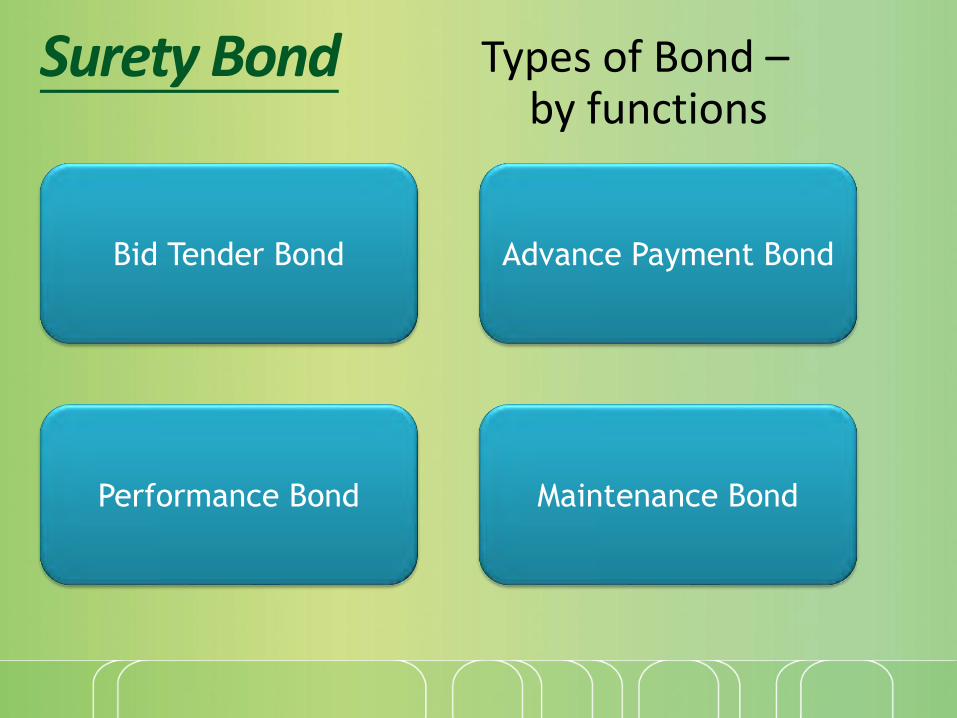

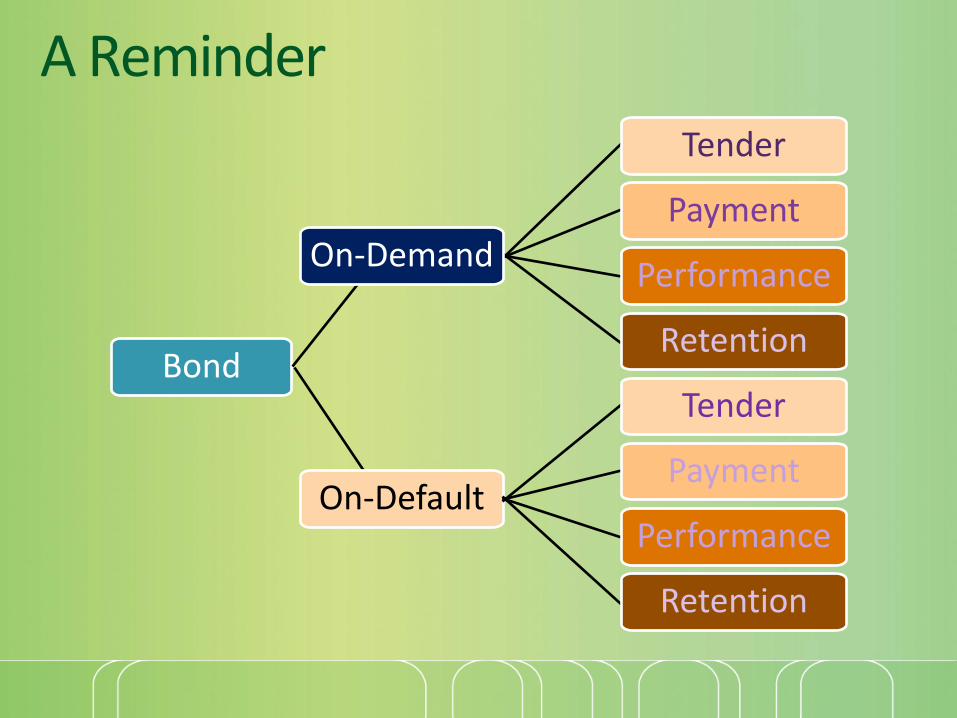

Types of Bond –by functions

Surety Bond

Bid Tender Bond

Performance Bond

Advance Payment Bond

Maintenance Bond

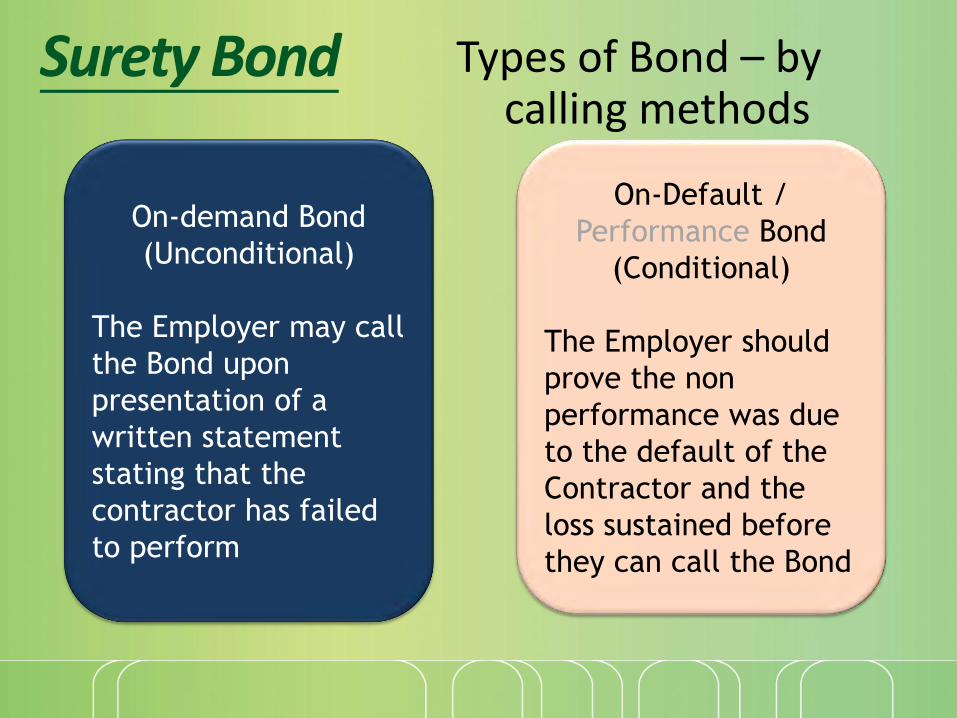

Types of Bond – by calling methods

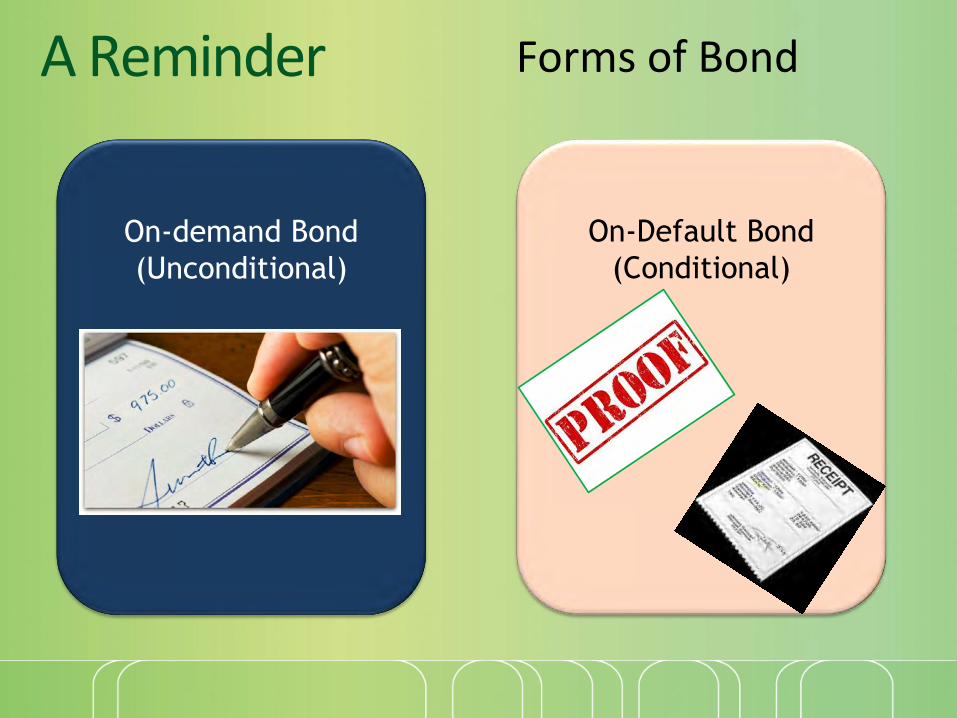

Surety Bond

On-demand Bond

(Unconditional)

The Employer may call

the Bond upon

presentation of a

written statement

stating that the

contractor has failed

to perform

On-Default /

Performance Bond

(Conditional)

The Employer should

prove the non

performance was due

to the default of the

Contractor and the

loss sustained before

they can call the Bond

Surety Bond

Surety Bond

Surety Bond

Seal?

Common Seal

Surety Bond

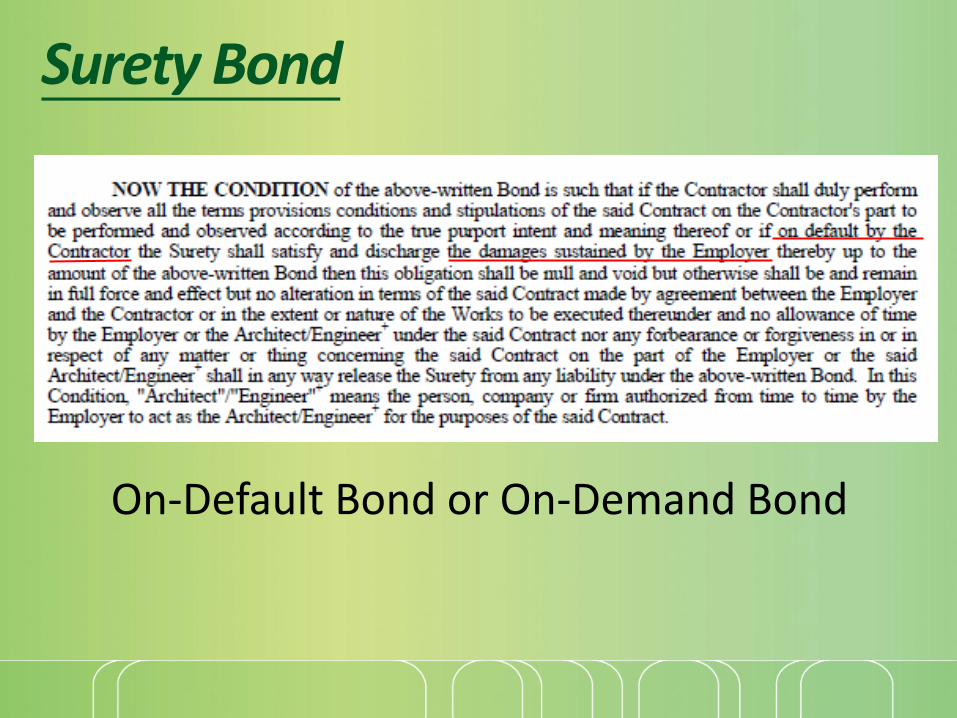

On-Default Bond or On-Demand Bond

Surety Bond

On-Default / Conditional / Performance Bond1. On Default by the Contractor2. The damages sustained by the Employer

Surety Bond

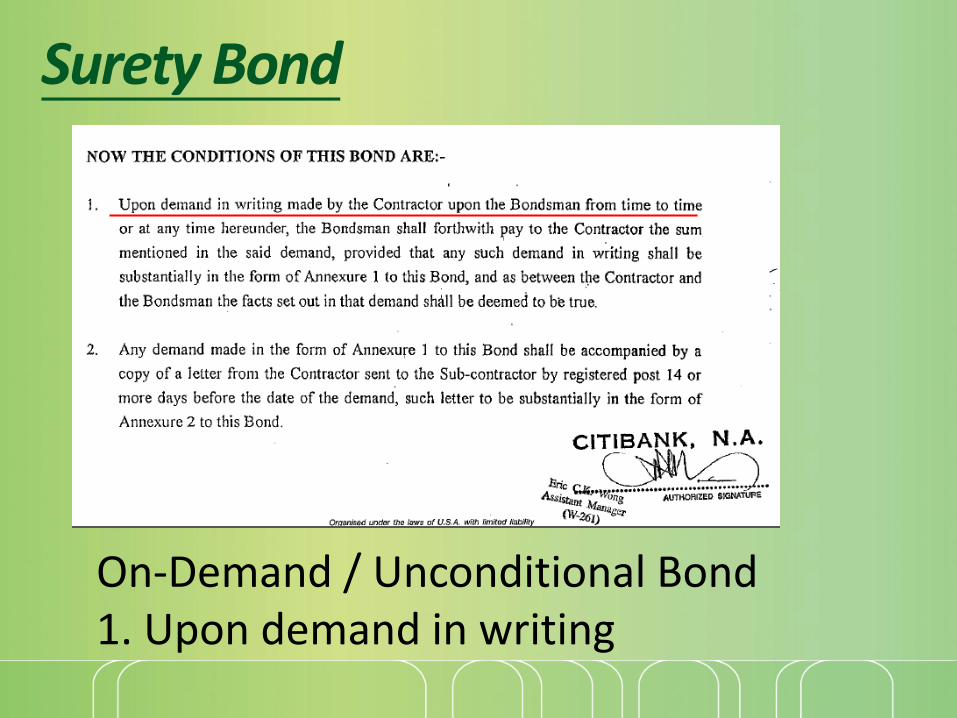

On-Default Bond or On-Demand Bond

Surety Bond

On-Demand / Unconditional Bond1. Upon demand in writing

Surety Bond

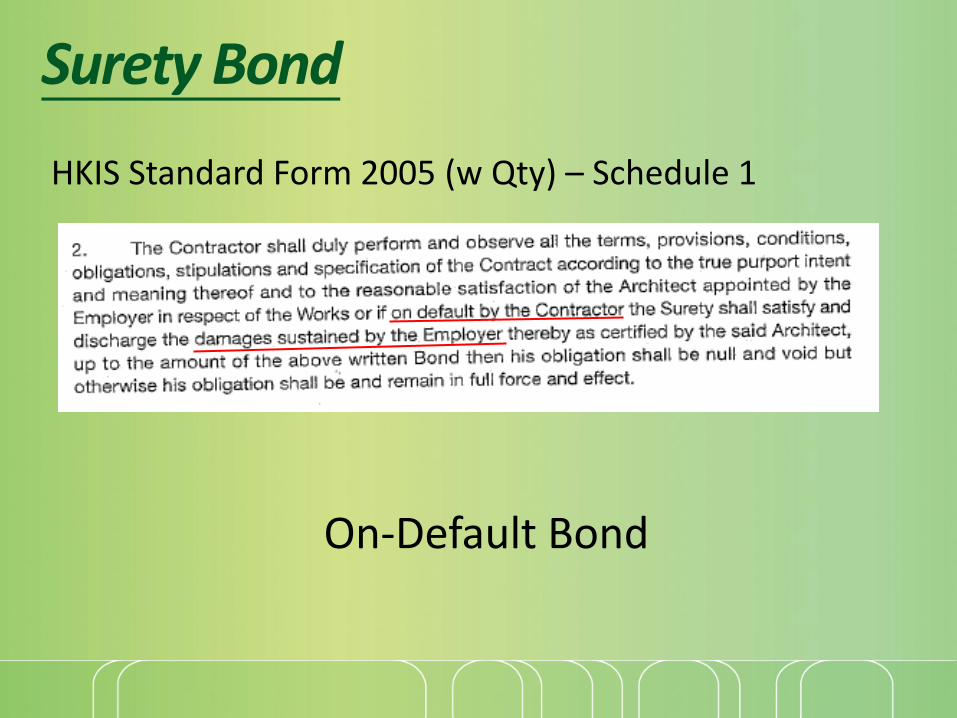

HKIS Standard Form 2005 (w Qty) – Schedule 1

On-Default Bond

Surety Bond

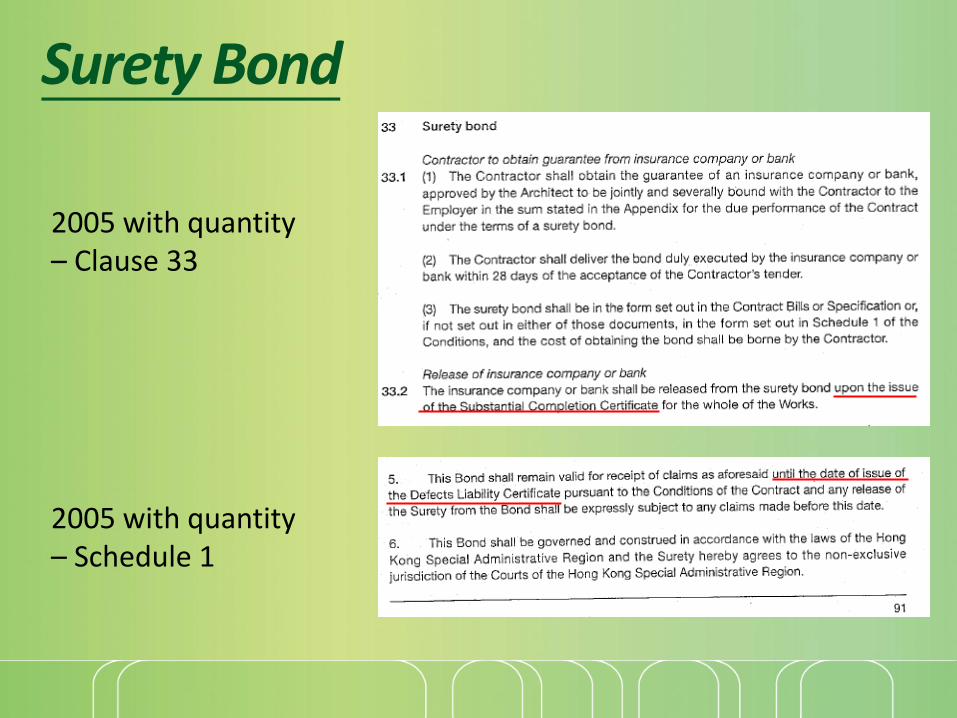

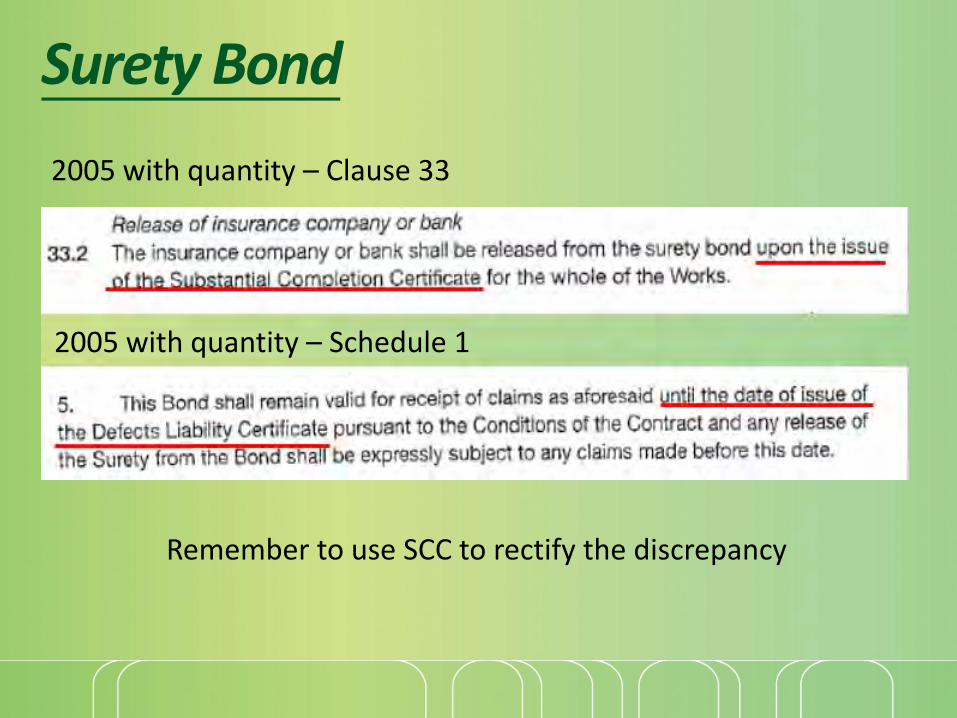

2005 with quantity – Clause 33

2005 with quantity – Schedule 1

Surety Bond

2005 with quantity – Clause 33

2005 with quantity – Schedule 1

Remember to use SCC to rectify the discrepancy

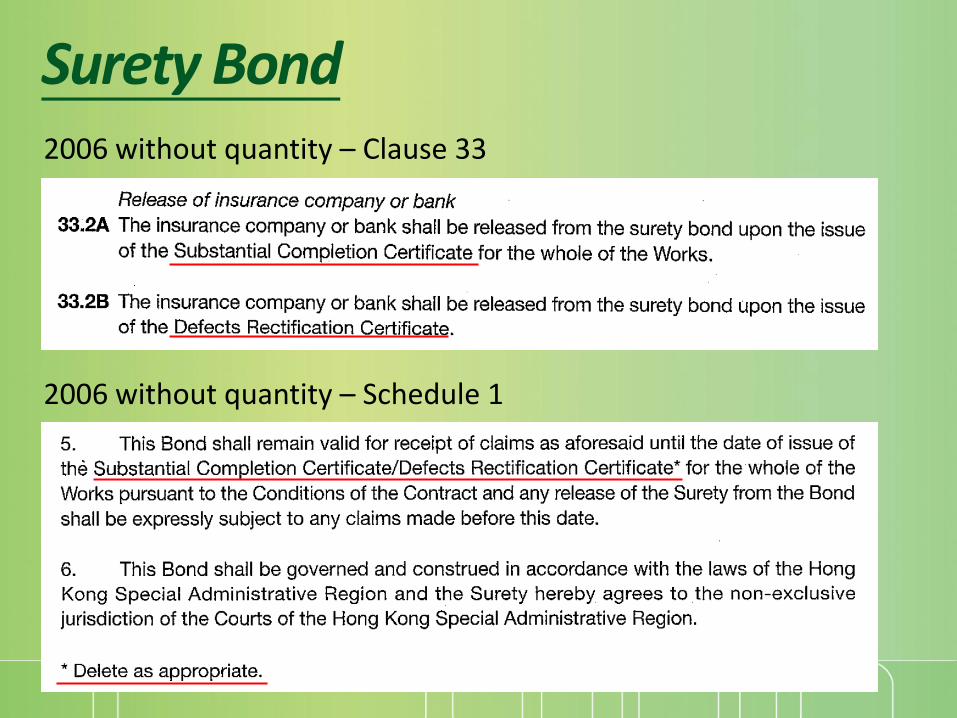

Surety Bond2006 without quantity – Clause 33

2006 without quantity – Schedule 1

Forms of BondA Reminder

On-demand Bond

(Unconditional)

On-Default Bond

(Conditional)

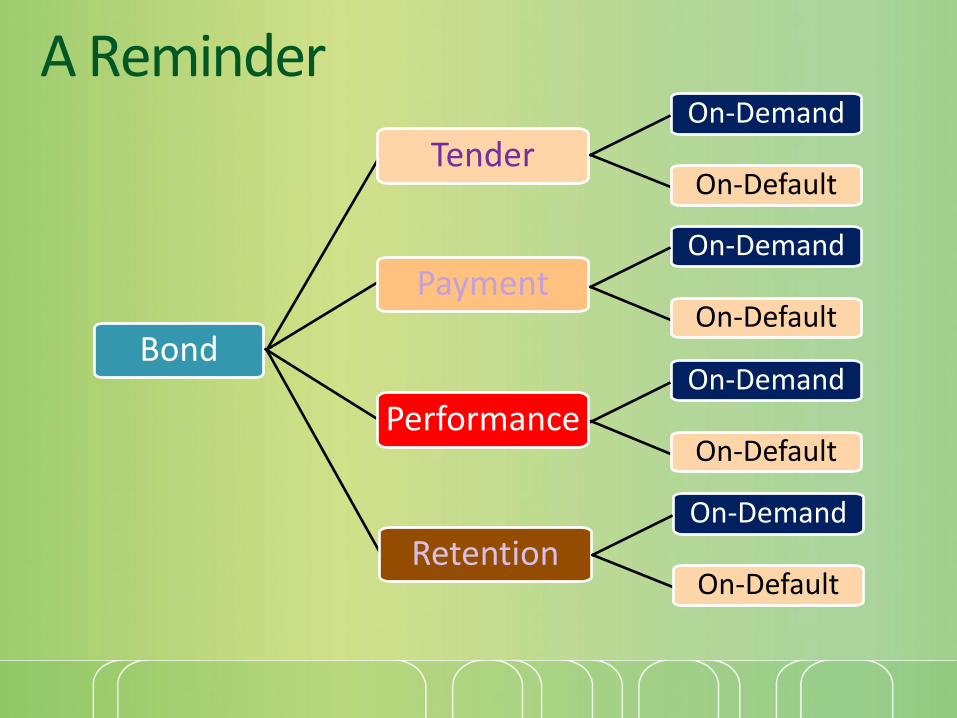

A Reminder

Bond

Tender

Payment

Performance

Retention

On-Demand

On-Default

Tender

Payment

Performance

Retention

A Reminder

BondOn-Demand

On-Default

Tender

Payment

Performance

RetentionOn-Demand

On-Default

On-Demand

On-Default

On-Demand

On-Default

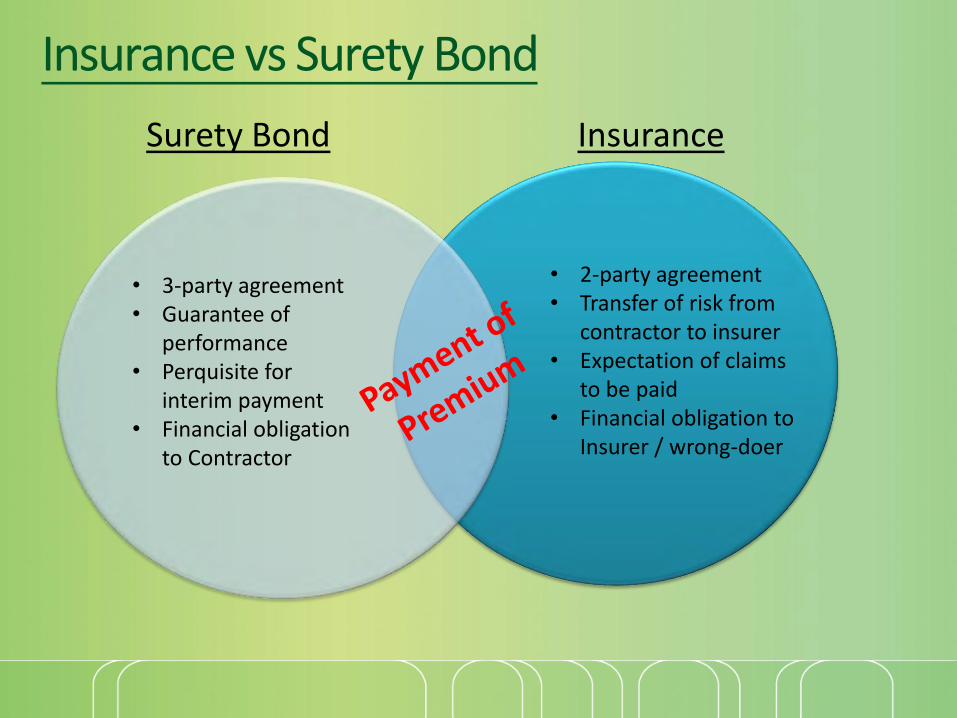

Insurance vs Surety Bond

• 3-party agreement• Guarantee of

performance• Perquisite for

interim payment• Financial obligation

to Contractor

• 2-party agreement• Transfer of risk from

contractor to insurer• Expectation of claims

to be paid• Financial obligation to

Insurer / wrong-doer

InsuranceSurety Bond

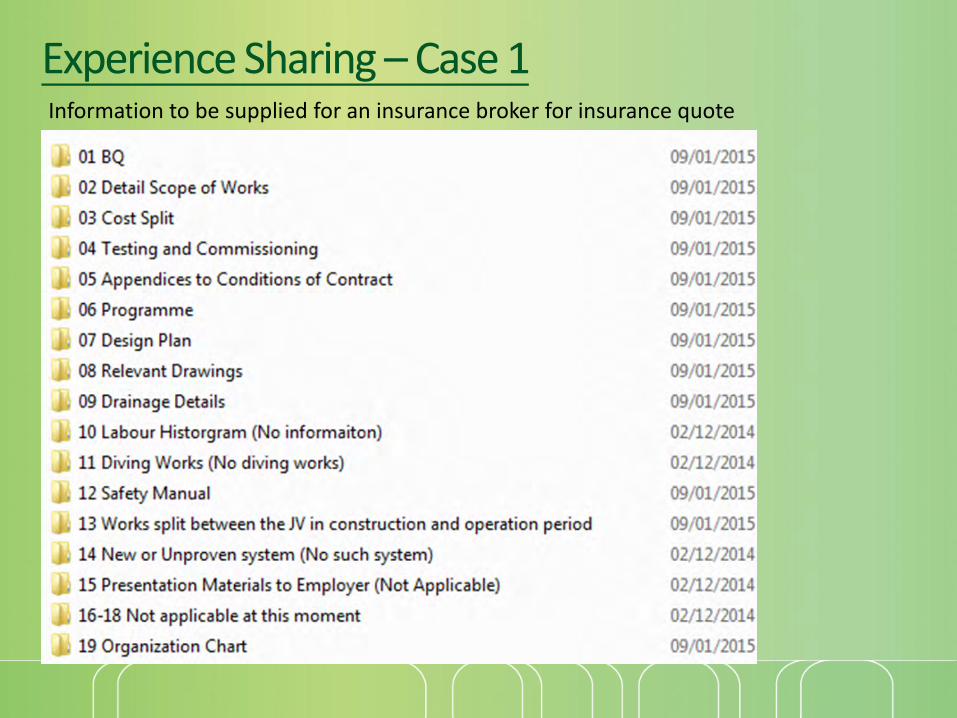

Experience Sharing – Case 1Information to be supplied for an insurance broker for insurance quote

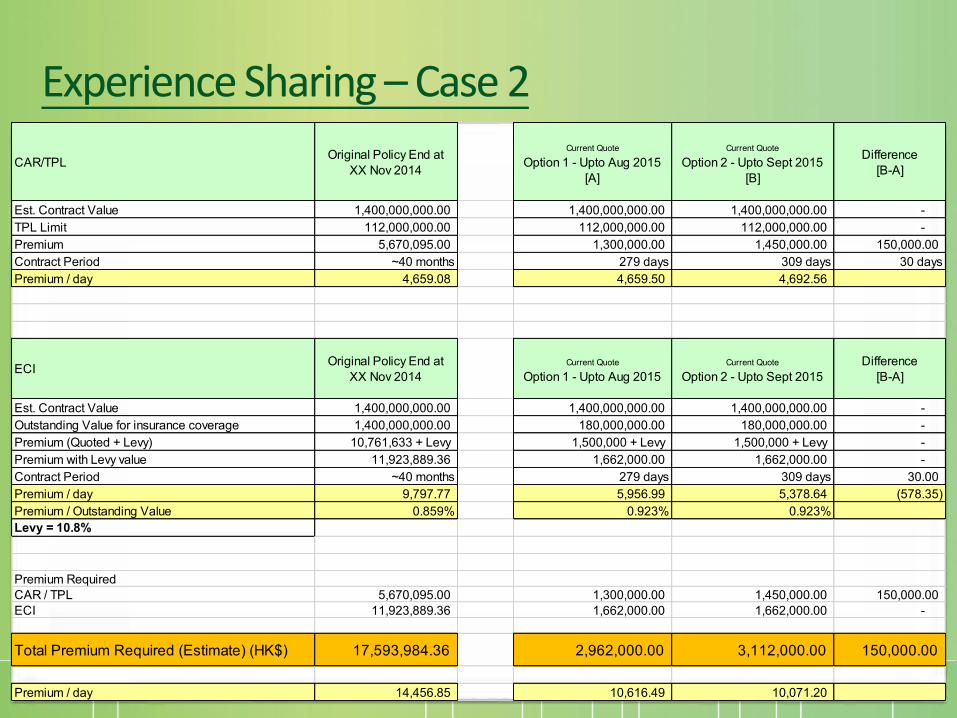

Experience Sharing – Case 2

A D&B Contract is about 40 months with about 6 months extension of time.

The Contractor anticipates that some outstanding works have to be completed during defects liability period.

The Contractor seeks quotations to cover the “outstanding works” for about 3 – 4 months beyond the extended completion date

CAR/TPL Original Policy End atXX Nov 2014

Current Quote

Option 1 - Upto Aug 2015[A]

Current Quote

Option 2 - Upto Sept 2015[B]

Difference[B-A]

Est. Contract Value 1,400,000,000.00 1,400,000,000.00 1,400,000,000.00 - TPL Limit 112,000,000.00 112,000,000.00 112,000,000.00 - Premium 5,670,095.00 1,300,000.00 1,450,000.00 150,000.00 Contract Period ~40 months 279 days 309 days 30 daysPremium / day 4,659.08 4,659.50 4,692.56

ECI Original Policy End atXX Nov 2014

Current Quote

Option 1 - Upto Aug 2015Current Quote

Option 2 - Upto Sept 2015Difference

[B-A]

Est. Contract Value 1,400,000,000.00 1,400,000,000.00 1,400,000,000.00 - Outstanding Value for insurance coverage 1,400,000,000.00 180,000,000.00 180,000,000.00 - Premium (Quoted + Levy) 10,761,633 + Levy 1,500,000 + Levy 1,500,000 + Levy - Premium with Levy value 11,923,889.36 1,662,000.00 1,662,000.00 - Contract Period ~40 months 279 days 309 days 30.00 Premium / day 9,797.77 5,956.99 5,378.64 (578.35) Premium / Outstanding Value 0.859% 0.923% 0.923%Levy = 10.8%

Premium RequiredCAR / TPL 5,670,095.00 1,300,000.00 1,450,000.00 150,000.00 ECI 11,923,889.36 1,662,000.00 1,662,000.00 -

Total Premium Required (Estimate) (HK$) 17,593,984.36 2,962,000.00 3,112,000.00 150,000.00

Premium / day 14,456.85 10,616.49 10,071.20

Experience Sharing – Case 2

Experience Sharing – Case 2

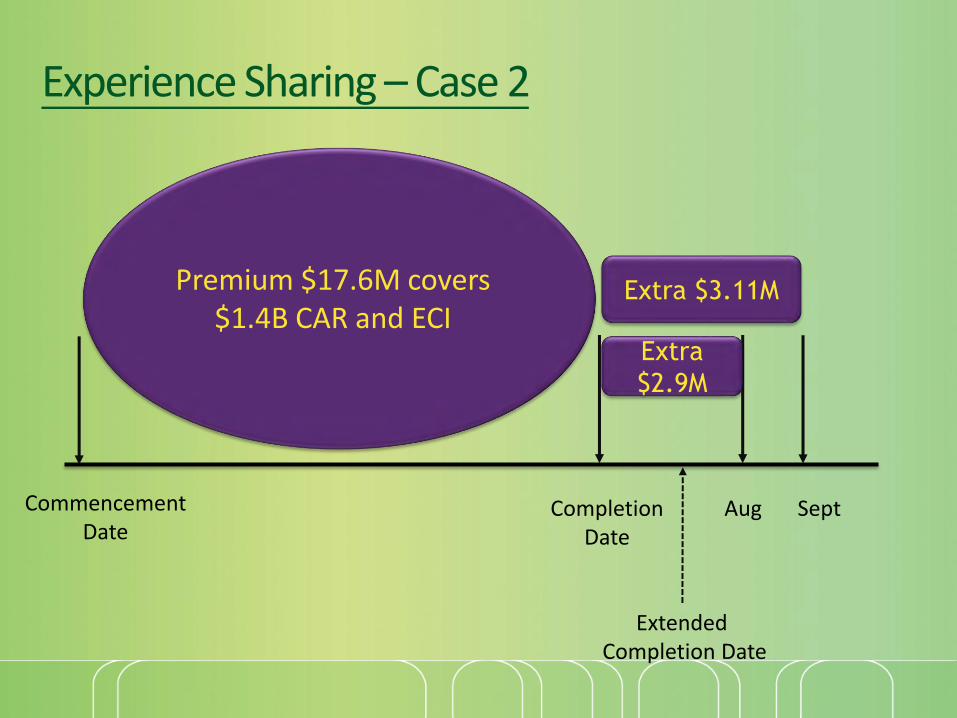

Premium $17.6M covers $1.4B CAR and ECI

Commencement Date

Completion Date

Extra

$2.9M

Extra $3.11M

Aug Sept

Extended Completion Date

Experience Sharing – Case 2

Even if you insure and pay the full premium for whole contract works, you have to pay EXTRA PREMIUM to:

1. Extend your coverage period to the extended completion date (at least)

2. Extend the insurance to cover ‘outstanding works’ unless only defects rectification works to be done during the defects liability period

Insurance Company will not consider the already paid premium for those outstanding works in the original contract.

Experience Sharing – Case 2

Duration

Work Value

Premium for CAR

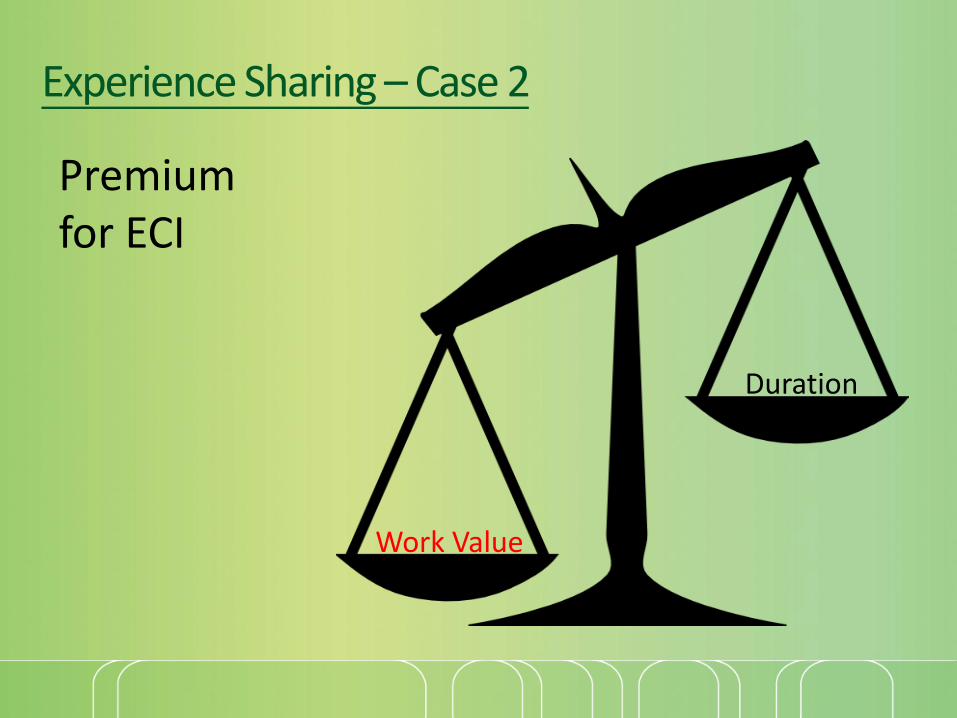

Experience Sharing – Case 2

Work Value

Duration

Premium for ECI

Disclaimer Note

This set of notes has been prepared according to the author’s ownexperience of the relevant practice and is intended for informationonly. No responsibility for loss occasioned to any person acting orrefraining from action occasioned by or as a result of any materialincluded will be accepted by the author or its company.

The materials and information contained herein are not intended tooffer or provide any insurance / legal advice concerning the topicscovered. Please consult your insurance company / brokers wherenecessary.

Copyright in all or part of this set of notes rests with the author andno part or parts of the material herein shall be reproduced in anyform or by any means electronic, mechanical, photocopyingrecording or otherwise without prior consent of the author.