institutional research hdfc secbreport.myiris.com/hdfc/infenter_20141022.pdf · 2014-10-24 ·...

TRANSCRIPT

INSTITUTIONAL RESEARCH

HDFC sec Diwali Picks – Vikram Samvat 2071

22 October 2014

FINANCIALS DCB Bank, Federal Bank, SKS Microfinance, SBI Darpin Shah, Shivraj Gupta IT SERVICES Cyient, Infosys, Mindtree Madhu Babu OIL & GAS Indraprastha Gas, Reliance Industries Satish Mishra AUTOMOBILES Hero Motocorp, LG Balkrishnan & Bros Navin Matta CONSUMER Asian Paints, Siyaram Silk Mills, Speciality Restaurants Harsh Mehta

REAL ESTATE & INFRA KNR Constructions, Kolte-Patil Developers, Prestige Estates Projects Adhidev Chattopadhyay INDUSTRIALS L&T, Texmaco Abhinav Sharma MATERIALS Orient Cement, Sanghi Industries, Mangalam Cement, JSW Steel Ankur Kulshrestha HEALTHCARE Alembic Pharma, Indoco Remedies Meeta Shetty CONGLOMERATES Aditya Birla Nuvo

STOCK RECOMMENDATIONS & CONTRIBUTING ANALYSTS

Page | 2

India : a rediscovery

As Samvat 2070 draws to a close, the chant above resonates with

India’s new-found optimism and cheer. HDFC securities is happy

to present its Diwali picks ! Given our broad-based optimism on

India, it is not surprising that these stocks span large and mid

caps, covered and unrated companies and almost all industries

and sectors. We believe these businesses have multi-year growth

potential and astute, capable managements that will allocate

capital in a way that enhances shareholder value.

A year ago, the economy was grappling with the outflow of capital,

diminishing hope in government and governance, a weak currency,

stubborn inflation and high oil prices. This Diwali, most macro indicators

are on the right trajectory, the crackers are louder and the mood is

dramatically different ! Why ?

Ask any long time and credible observer of India’s economic journey

what its fundamental stumbling blocks really are. You will find two

recurring themes : poor governance and a high reliance on imported

fossil fuels.

On BOTH counts, it looks like India has never been better placed. For all

the impatience on reforms, can you imagine any OTHER government

delivering meaningful and sustainable policy reforms coupled with

steady multi-year improvement in governance? And can you find anyone

who’s bullish on crude today? If so, how can you NOT be constructive on

India ?

Admittedly, global factors are not too encouraging, with contagion risks

rising in Europe. But China’s slowdown means lower commodity prices

(another structural positive for India) even as strong macros in the US

will lead to steady demand for Indian goods and services. Should an

outflow of capital occur from Indian shores, it will only end up creating

opportunities for longer term investors who now understand that India

has rediscovered its long lost mojo.

Dipen Sheth, Head - Research [email protected] +91-22-6171-7339

Parag Thakkar, Head - Sales [email protected] +91-22-6171-7332

From ignorance, lead me to truth From darkness, lead me to light

From death, lead me to immortality - Brihadaranyaka Upanishad (1.3.28)

Page | 3

(Rs mn) FY13 FY14 FY15E FY16E FY17E

Net Interest Income 2,844 3,684 4,815 5,709 7,073

PPOP 1,261 1,880 2,704 3,313 4,335

PAT 1,021 1,514 1,844 2,225 2,882

EPS (Rs) 4.1 6.0 6.6 7.9 10.3

Earnings Growth (%) 85.3 48.3 21.8 20.7 29.5

ROAE (%) 11.0 14.1 13.5 13.1 14.9

ROAA (%) 1.02 1.25 1.29 1.30 1.39

Adj. BVPS (Rs) 38.0 43.0 53.6 61.4 70.6

P/ABV (x) 2.20 1.95 1.56 1.36 1.19

PE (x) 20.52 13.9 12.7 10.6 8.2

DCB Bank (CMP Rs 87, Mcap Rs 23.8bn, NOT RATED)

During FY10-14, DCB put a lid on costs and mended its loan book, even as it maintained high growth with granularity. The bank emerged stronger with good operational performance across parameters viz margin, growth, asset quality and overall return ratios. This will persist as macros improve. Though the stock has outperformed and valuations have moved up, we believe there is room for further rerating.

• Operating efficiencies to improve : Cost rationalisation was the first lever that DCB’s management pulled in FY10. At 12% CAGR over FY10-14, costs grew significantly slower than business. As a result, C-I fell to 63% in FY14 from 69/75% in FY13/12. Given DCB’s focus on Tier II-VI cities and healthy core earnings growth, its C-I ratio is expected to improve further, thus driving RoA.

• Quality and growth hand in hand : Over the past couple of years, DCB reduced its concentration risk by exiting a few large corporate/SME loans, while maintaining loan growth of 24% CAGR FY11-14. Improving granularity adds comfort to quality, as seen in the steady decline in G/NNPA. As macros improve, we expect loan book to double over the next three years without sacrificing asset quality and profitability.

FINANCIAL SUMMARY

Source: Company, HDFC sec Inst Research

Federal Bank (CMP Rs 141, TP Rs 177, Mcap Rs 121bn)

We believe Federal Bank has set its house in order, post a sluggish phase that reflected broader macro pains. The bank has healthy tier I, large branch network and stable deposit franchise. FB reported flattish loan growth in FY14, and turned cautious on corporate loans (degrew 27% YoY). However, it continued to build granularity with strong growth of 36/16% in SME & Retail (ex-gold) portfolio. We think 20%+ CAGR is feasible over FY15-17. Op lev will drive up the stock.

• Asset quality heals : Revamped underwriting practices have led to steady decline in Retail & SME. Quarterly slippages averaged Rs 620mn in FY14 vs. Rs 728/910mn in FY13/12. Also, corporate slippages have turned less volatile over the last 3-4 quarters. Further, the stressed assets watch-list has fallen ~70% to Rs 3bn (3 accounts) over the trailing year. This will drive down provisioning cost (64/61bps in FY13/14), and boost profits even as coverage remains high.

• Improvement in operating leverage, key RoA driver : During FY11-14, FB added 430 branches (35% of the current network), leading to 20% CAGR in opex (17% CAGR in staff cost). However, a sluggish economy led to lower revenue growth (NII +8% CAGR and non Interest Income +10% CAGR). This double whammy resulted in a ~1,200bps deterioration in C-I to 49%. On the positive side, deposit franchise improved (CASA +370bps to ~31%). Strong loan growth and steady NIMs, coupled with controlled opex, will push efficiencies and drive RoAs over FY15-17E. The case for re-rating will thus become stronger.

FINANCIALS

(Rs mn) FY13 FY14 FY15E FY16E FY17E

Net Interest Income 19,747 22,286 24,540 29,123 34,754

PPOP 14,546 14,804 16,568 20,016 23,925

PAT 8,382 8,389 9,890 12,207 14,443

EPS 9.8 9.8 11.6 14.3 16.9

Earnings Growth (%) 7.9 0.1 17.9 23.4 18.3

ROAE (%) 13.9 12.6 13.5 14.9 15.7

ROAA (%) 1.27 1.15 1.24 1.31 1.30

Adj. BVPS (Rs) 69.2 77.4 86.3 97.5 110.9

P/Adj BV (x) 2.03 1.82 1.63 1.44 1.27

P/E (x) 14.3 14.3 12.2 9.8 8.3

FINANCIAL SUMMARY

Source: Company, HDFC sec Inst Research

Page | 4

SKS MicroFinance (CMP Rs 317, Mcap Rs 40bn, NOT RATED)

SKS Microfinance (SKS) has overcome the Andhra Pradesh (AP) microfinance crisis, with its AP loan book (~Rs 14bn) fully written off (incurred losses in FY12/13). With lower provisioning requirements, SKS turned profitable in FY14. Going ahead, SKS is well positioned to report strong growth (book & earnings) led by high CRAR (33% in Sept-14, post a well timed fund raise of Rs 4.5bn), unavailed tax benefits (Rs 5.2bn), stable regulatory environment and improving operating leverage. SKS is expected to more than double its book & grow earnings by ~5x over FY14-17E, thus justifying premium valuations (2.4x FY17 consensus BV for RoEs of 23 and ~5.5% RoA)

• Mitigating risk : SKS diversified its loan book by capping the contribution of any state to 15% of the total loans & 50% of its networth. In previous years (before the crisis), SKS had the highest exposure in AP (27% of loans). By Mar-14, the co had 17% of its loans in Karnataka, followed by Odisha (15%), Bihar (12%), Maharashtra (11%) and West Bengal (12%). Further, SKS has tightened its credit appraisal norms with no disbursements from branches with NPA of >1%.

• Distribution business and recoveries to boost profitability : Co earned Rs 180mn in 1HFY15 through the sale of mobile phones and solar lamps. The mobile phones are priced at Rs 2,000-3,000, on which the co. earns a gross commission of Rs 200/handset distributed. In FY14, the co. distributed 0.26mn phones & solar lamps. Further, recoveries from AP were Rs 260mn in 1HFY15.

State Bank of India (CMP Rs 2,584, TP Rs 2,833, Mcap Rs 1,929bn)

We remain positive on SBI given its healthy Tier I (highest amongst peers), best in class deposit franchise and relatively lower impaired assets. SBI remains a high quality cyclical play on improving macros. FY14 performance was marred by higher wage costs of Rs 43bn dragging overall RoA/RoE to 0.7/10%. Margin performance was better than expected, cushioned by strong deposit franchise (domestic CASA ~44%). Management continuity (~2.5 years) is an advantage.

• Best play on economic recovery : SBIN is probably the best placed PSB to ride an anticipated uptick in the Indian economy with strong CRAR, superior liability franchise, lowest impaired assets and management continuity.

• Strong Capital cushion : SBIN is the best placed PSB with Tier I at 9.9/%. We estimate capital requirement of ~Rs 634bn over the next five years, mere ~33% of current MCap, even as a large part of it is likely to be back ended. Thus, we see lower dilution risk.

• Lowest stressed assets : In spite of conservative NPA recognition, SBIN has the lowest stressed assets (6.2% of loans) amongst PSB. Given a high proportion of slippages in the mid corp/SME segments, any uptick in the economy would benefit SBIN.

• Earnings growth to pick up : After two years of decline in core PPoP (~7% CAGR), SBIN is expected to report ~18% CAGR over FY14-16E driven by steady core earnings of 15% CAGR and controlled opex structure (11% opex CAGR). After factoring 130bps of provisioning cost over FY15-16E, we expect the bank’s net earnings to grow at ~26% CAGR.

FINANCIALS

Particulars Rs bn Per Share Rationale

State Bank (standalone) 1,680 2,250 1.6x FY16E core ABV (Rs 1,406)

Bank subsidiaries 224 300 1.2x FY16E ABV

SBI Life 122 163 18% APE CAGR FY14-16E; NPAB Margin at 16%.

SBI AMC 26 34 5% FY14E AUM

Others 63 85 Stake in NSE, UTI MF, SBI Caps and others

Total Value 2,115 2,833

Current Value 1,929 2,584

Upside (%) 9.6 9.6

SOTP

Source: Company, HDFC sec Inst Research

Page | 5

(Rs mn) FY13 FY14 FY15E FY16E FY17E

Net Sales 18,730 22,063 27,284 32,378 36,903

EBITDA (adj.) 3,417 4,100 4,517 5,733 6,377

APAT 2,310 2,660 3,721 4,262 4,701

Diluted EPS (Rs) 20.7 23.8 33.3 38.1 42.1

P/E (x) 21.6 18.9 13.5 11.8 10.7

EV / EBITDA (x) 13.0 10.5 9.2 6.9 5.8

RoE (%) 18.6 18.3 21.5 21.1 20.0

Cyient (CMP Rs 449, TP Rs 533, Mcap Rs 50.9bn)

Cyient enjoys a niche position among Indian IT vendors with strong presence in Engineering Design Services and Data Transformation, Network and Operations (DNO) segments. Engineering Design (~61% of Cyient’s revenues) is relatively under-penetrated by offshore vendors and offers scope for scalability. Cyient has delivered strong USD revenue growth over the trailing four quarters (6% CQGR). Higher growth in DNO and traction in top 10 accounts (~49% of revenues) are driving growth. We expect 20% CAGR in USD revenues (FY14-FY17E) and 21% CAGR in EPS over FY14-FY17E. Our TP is Rs 533/sh (14x FY16E EPS). BUY

• Cyient’s offerings span multiple industries such as Aerospace, Railways, Energy, Medical, Heavy Equipment, Hi-Tech, Transportation, Telecom and Utilities.

• The company offers services across the Engineering Design Outsourcing value chain. Major clients include Pratt and Whitney, Hamilton Sundstrand, Bombardier, Alstom, Caterpillar. In DNO, the company provides network solutions to Utilities, Telecom and Digital Map providers. Major clients in the segment include Tom Tom, Airtel and AT&T.

• We expect Cyient to deliver 18% organic USD revenue growth for FY15 (24% including the impact of Softential acquisition). Improving scale, scope for improvement in utilization rates and offshore shift should enable margins. We expect EBIDTA margin at ~16.6/17.7% for FY15/FY16E. Net cash at Rs 6.76bn (Rs 60/sh), is ~13% of MCap. We see scope for further inorganic initiatives which could add to growth and enable improvement in ROE.

FINANCIAL SUMMARY

Source: Company, HDFC sec Inst Research

(Rs mn) FY13 FY14 FY15E FY16E FY17E

Net Sales 403,520 501,330 539,125 609,489 673,845

EBITDA (adj.) 115,580 136,340 152,360 168,928 184,799

APAT 94,210 108,670 124,795 138,276 152,349

Diluted EPS (Rs) 164.9 190.2 218.4 242.0 266.6

P/E (x) 22.9 20.2 17.3 15.6 14.1

EV / EBITDA (x) 16.6 13.7 11.9 10.5 9.2

RoE (%) 25.7 24.4 24.5 23.9 23.2

Infosys (CMP Rs 3,775, TP Rs 4,265, Mcap Rs 218bn)

We believe that Infosys is poised for a multi-year turnaround under the leadership of the new CEO, Dr. Sikka. He has guided for an increased focus on using Automation, Artificial Intelligence and Design Thinking to improve delivery efficiencies across service lines. We model USD revenue growth of 8.1/13% for FY15/FY16E. Infosys’ valuations remain reasonable (15.6x FY16E EPS) and are at a 19% discount to TCS. Our TP is Rs 4,265/sh (16x FY17E EPS). BUY

• Dr. Sikka has emphasized on leveraging Infosys’ training infrastructure to re-skill its employees on new technologies. Management also intends to strengthen Finacle and Infosys’ platforms business unit. We expect the new initiatives to boost employee productivity and stabilise margins. Increased investments in Products and Platforms could provide non-linear growth opportunities.

• Infosys has also been showing steady improvement in operational parameters. Utilisation rates (excluding trainees) came at 82.3% as of 2QFY15, which is an improvement of 480bps YoY. Infosys has also shown improvement in effort mix towards offshore. For 2QFY15, percentage effort from offshore stood at 71.3% up 250bps QoQ. Hence, EBIT margin at 26.1% for 2QFY15 has seen an improvement of 250bps YoY. We think this is sustinable.

• We believe that FY15 is a year of transition for the company. Expect acceleration of growth in FY16. We see scope for Infosys to narrow the growth differential with peers, which could boost P/E expansion for the stock. Cash and equivalents stand at Rs 336bn (Rs 587/sh), which is ~15% of its Mcap. Better clarity on capital allocation could be an additional trigger.

FINANCIAL SUMMARY

Source: Company, HDFC sec Inst Research

IT SERVICES

Page | 6

(Rs mn) FY13 FY14 FY15E FY16E FY17E

Net Sales 23,618 30,316 36,039 42,328 47,937

EBITDA (adj.) 4,864 6,100 7,138 8,893 9,946

APAT 3,393 4,507 5,348 6,579 7,426

Diluted EPS(Rs) 40.9 53.8 63.8 78.4 88.5

P/E (x) 25.2 19.2 16.2 13.2 11.7

EV / EBITDA (x) 16.3 13.1 10.8 8.2 6.9

RoE (%) 29.9 30.5 29.1 29.0 26.7

Mindtree (CMP Rs 1,032, TP Rs 1,176, MCap Rs 82.3bn)

We are confident that Mindtree is at an inflection point and can break out of the midcap league (~USD 502mn revenues in FY14, headcount ~13k as of 2QFY15). We expect 17% USD revenue CAGR over FY14-17E. Improving scale will lead to P/E rerating for the stock. Stable performance on EBIDTA margin (~20.1% for FY14) is another key positive. Post the recent correction, valuations are reasonable at 13.2x FY16E EPS. BUY with TP of Rs 1,176/sh (15x FY16 EPS).

• Mindtree Is positioned as a ‘multi-segment specialist player’ with strong client traction in its focus verticals. The company’s vertical offerings span BFSI, Retail, CPG & Manufacturing. Marquee clients include AIG, SITA, Volvo, and Unilever. Cross-selling of under-penetrated services to top clients is driving growth. IMS accounts for ~18.7% of revenue mix as of 2QFY15 and has grown at 9.7% CQGR over the past twelve quarters.

• Mindtree’s growth has majorly been driven by higher traction in its top 10 accounts (~49% of revenues, 4.4% CQGR over the past twelve quarters). Mindtree has four USD 30mn+ clients. Company has been trimming its tail accounts to increase sales focus on existing top clients. It now intends to broaden this focus on the next set of top accounts. This is likely to be another growth driver.

• Notably, Mindtree’s onsite effort has been increasing gradually over the past twelve quarters (17.6% as of 2QFY15 vs. 13% as of 2QFY12). This was aided by expansion of service mix and higher traction of front end offerings. Company has also opened delivery centers in USA (Gainesville, Redmond). We believe that strengthening of onsite delivery could help better positioning for large deal wins.

FINANCIAL SUMMARY

Source: Company, HDFC sec Inst Research

IT SERVICES

Page | 7

(Rs mn) FY13 FY14 FY15E FY16E FY17E

Net Sales 33,670 39,222 42,180 49,441 54,232

EBITDA 7,581 7,824 7,930 8,364 8,980

APAT 3,541 3,603 4,225 4,571 5,041

Diluted EPS (Rs) 25.3 25.7 30.2 32.6 36.0

P/E (x) 16.7 16.4 14.0 13.0 11.7

EV / EBITDA (x) 7.6 7.5 7.5 7.4 7.2

RoE (%) 26.0 22.1 21.9 20.1 19.0

Indraprastha Gas (CMP Rs 411, TP Rs 455, Mcap Rs 58bn)

Government’s focus on energy security and reducing oil bills is leading to higher emphasis on natural gas. With the new consumer friendly gas pricing policy and 100% domestic gas allocation, CNG prices will be significantly cheaper than petrol/diesel. Consumption will grow faster. Conducive macros, IGL’s inherent strength (pricing power/low cost network/strong balance sheet) make IGL a hi-conviction BUY. Our TP of Rs 455 faces serious upside as triggers emerge.

• There are multiple triggers ahead for IGL (1) With government mandated 100% allocation of cheaper domestic gas to CNG/domestic PNG (75/5% of vols for IGL), CNG prices stand at ~Rs 43/kg, far below previous peaks even after the recent gas price reset (2) DTC has issued a tender for ~1.4k CNG buses on a ~19.5k base (3) Investments in fast growing CGD players in non-metros (4) Softening crude-linked RLNG prices.

• IGL purchased 50% stake in two CGD companies, Central UP Gas Ltd and Maharashtra Natural Gas for Rs 0.7bn & Rs 1.9bn respectively. They will have a combined volume of ~0.7 mmscmd by FY16 and will add ~10% to IGL’s consolidated PAT. We expect 2-3 more acquisitions to follow in the coming years. Small base and favourable macros will lead to robust growth for these companies.

• Outlook for industrial segment should improve, led by a pickup in economic activity and falling LNG prices.

• Key risk : The dispute with PNGRB on reduced network tariff/compression changes is sub-judice. Unfavourable outcome (unlikely, in our view) can be a big negative for the stock.

FINANCIAL SUMMARY (STANDALONE)

Source: Company, HDFC sec Inst Research

(Rs bn) FY13 FY14 FY15E FY16E FY17E

Net Sales 3,602.97 3,901.18 3,958.46 4,039.51 4,360.12

EBITDA 307.87 308.78 330.72 355.51 483.23

APAT 210.03 219.85 236.97 246.59 338.12

Diluted EPS (Rs) 65.0 68.0 73.3 76.3 104.6

P/E (x) 14.4 13.7 12.8 12.3 8.9

EV / EBITDA (x) 9.8 9.8 9.1 8.5 6.3

RoE (%) 12.1 11.7 11.5 10.9 13.5

Reliance Industries (CMP Rs 935, TP Rs 1,100, Mcap Rs 3,006bn)

With the new gas pricing policy, the bad news is in RIL’s price, which has underperformed NIFTY by ~22% post the formation of the new Indian govt. This is mostly attributed to concerns around its Indian E&P biz and its massive USD 12bn investment in telecom. Premium pricing for deep water discoveries is a silver lining. Meanwhile, there is increasing visibility on a quantum jump in EBITDA by FY17E (56% higher than FY14), driven by RIL’s USD 13bn capex in the core refining/petchem business. Our SOTP for RIL is Rs 1,100/sh.

• While FY15/16 should see initial benefits of capacity additions in polyester and intermediates, FY17 can see a quantum shift. Our estimate is that ~80% benefit of the petchem/polyesters capex will be visible in FY17. Moreover, these are almost immune to policy vagaries.

• Along with the remaining ~20% benefits from the core capex, RIL will also gain from imported ethane in FY18. RIL is incurring a capex of USD 1.6bn to import ethane as cracker feed to replace high cost domestic gas/naphtha. We expect additional EBITDA of ~USD 0.5bn/yr from FY18 onwards.

• There are other reasons to like RIL (1) Retail has achieved critical mass and was PAT positive in FY14. Management expects ~30% EBITDA CAGR (2) Positive outlook for domestic deep water upstream assets (3) Ramp up in shale gas volumes in the US (4) Strong balance sheet (cons net D/E at 0.3).

• Key Risk : RIL has plans to invest USD 14bn in telecom ($ 6bn invested till FY14). We think it is difficult to ascertain returns on these investments.

FINANCIAL SUMMARY (STANDALONE)

Source: Company, HDFC sec Inst Research

OIL & GAS

Page | 8

(Rs mn) FY13 FY14 FY15E FY16E FY17E

Net Sales 2,37,681 2,52,755 2,83,202 3,24,540 3,67,384

EBITDA (adj.) 32,845 35,402 39,060 48,703 55,883

APAT 21,182 21,090 28,361 37,032 42,325

Diluted EPS (Rs) 106 106 142 185 212

P/E (x) 28.2 28.4 21.1 16.2 14.1

EV / EBITDA (x) 17.3 15.9 14.5 11.4 9.8

RoE (%) 42.3 37.7 44.0 50.4 52.1

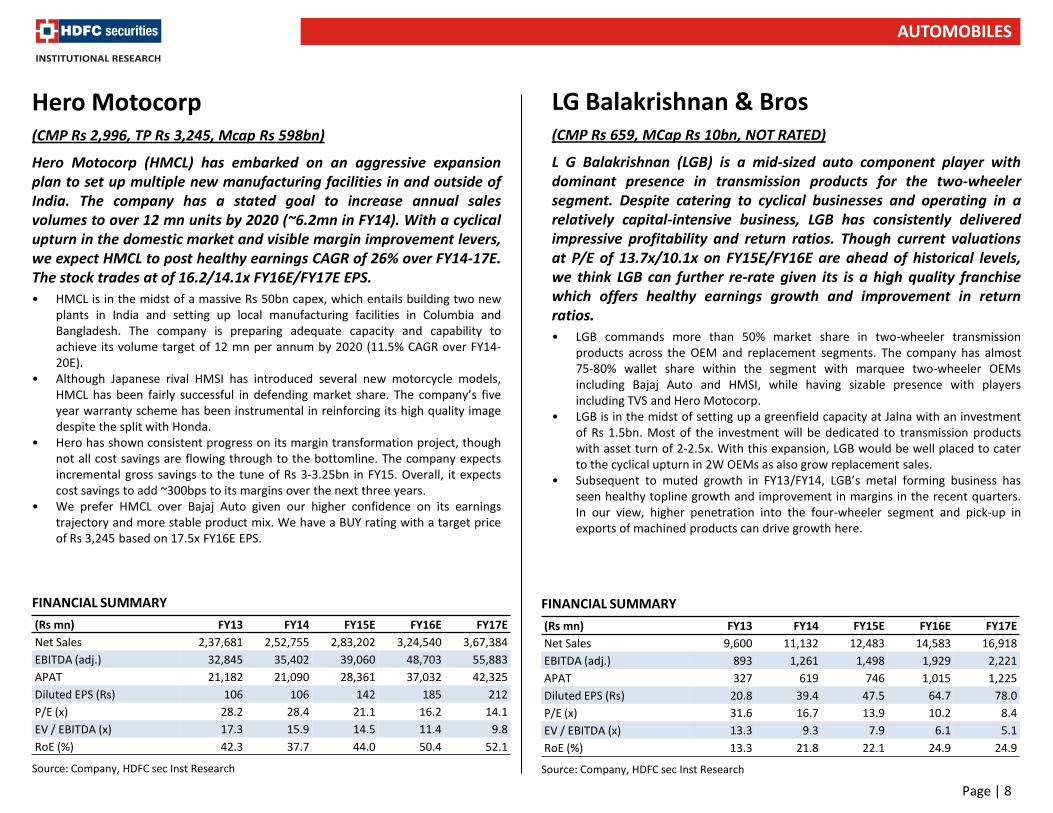

Hero Motocorp (CMP Rs 2,996, TP Rs 3,245, Mcap Rs 598bn)

Hero Motocorp (HMCL) has embarked on an aggressive expansion plan to set up multiple new manufacturing facilities in and outside of India. The company has a stated goal to increase annual sales volumes to over 12 mn units by 2020 (~6.2mn in FY14). With a cyclical upturn in the domestic market and visible margin improvement levers, we expect HMCL to post healthy earnings CAGR of 26% over FY14-17E. The stock trades at of 16.2/14.1x FY16E/FY17E EPS.

• HMCL is in the midst of a massive Rs 50bn capex, which entails building two new plants in India and setting up local manufacturing facilities in Columbia and Bangladesh. The company is preparing adequate capacity and capability to achieve its volume target of 12 mn per annum by 2020 (11.5% CAGR over FY14-20E).

• Although Japanese rival HMSI has introduced several new motorcycle models, HMCL has been fairly successful in defending market share. The company’s five year warranty scheme has been instrumental in reinforcing its high quality image despite the split with Honda.

• Hero has shown consistent progress on its margin transformation project, though not all cost savings are flowing through to the bottomline. The company expects incremental gross savings to the tune of Rs 3-3.25bn in FY15. Overall, it expects cost savings to add ~300bps to its margins over the next three years.

• We prefer HMCL over Bajaj Auto given our higher confidence on its earnings trajectory and more stable product mix. We have a BUY rating with a target price of Rs 3,245 based on 17.5x FY16E EPS.

FINANCIAL SUMMARY

Source: Company, HDFC sec Inst Research

(Rs mn) FY13 FY14 FY15E FY16E FY17E

Net Sales 9,600 11,132 12,483 14,583 16,918

EBITDA (adj.) 893 1,261 1,498 1,929 2,221

APAT 327 619 746 1,015 1,225

Diluted EPS (Rs) 20.8 39.4 47.5 64.7 78.0

P/E (x) 31.6 16.7 13.9 10.2 8.4

EV / EBITDA (x) 13.3 9.3 7.9 6.1 5.1

RoE (%) 13.3 21.8 22.1 24.9 24.9

LG Balakrishnan & Bros (CMP Rs 659, MCap Rs 10bn, NOT RATED)

L G Balakrishnan (LGB) is a mid-sized auto component player with dominant presence in transmission products for the two-wheeler segment. Despite catering to cyclical businesses and operating in a relatively capital-intensive business, LGB has consistently delivered impressive profitability and return ratios. Though current valuations at P/E of 13.7x/10.1x on FY15E/FY16E are ahead of historical levels, we think LGB can further re-rate given its is a high quality franchise which offers healthy earnings growth and improvement in return ratios.

• LGB commands more than 50% market share in two-wheeler transmission products across the OEM and replacement segments. The company has almost 75-80% wallet share within the segment with marquee two-wheeler OEMs including Bajaj Auto and HMSI, while having sizable presence with players including TVS and Hero Motocorp.

• LGB is in the midst of setting up a greenfield capacity at Jalna with an investment of Rs 1.5bn. Most of the investment will be dedicated to transmission products with asset turn of 2-2.5x. With this expansion, LGB would be well placed to cater to the cyclical upturn in 2W OEMs as also grow replacement sales.

• Subsequent to muted growth in FY13/FY14, LGB’s metal forming business has seen healthy topline growth and improvement in margins in the recent quarters. In our view, higher penetration into the four-wheeler segment and pick-up in exports of machined products can drive growth here.

FINANCIAL SUMMARY

Source: Company, HDFC sec Inst Research

AUTOMOBILES

Page | 9

Particulars FY13 FY14 FY15E FY16E

Net Sales (in Rs Mn) 109,386 127,148 150,363 176,398

EBIDTA (in Rs Mn) 17,320 19,979 24,110 28,783

Net profit (in Rs Mn) 11,139 12,188 14,950 17,714

EPS (Rs.) 11.6 12.7 15.6 18.5

P/E (x) 55.5 50.7 41.3 34.9

EV/EBITDA 35.2 30.2 24.7 20.5

RoE (%) 36.3 33.1 33.8 33.7

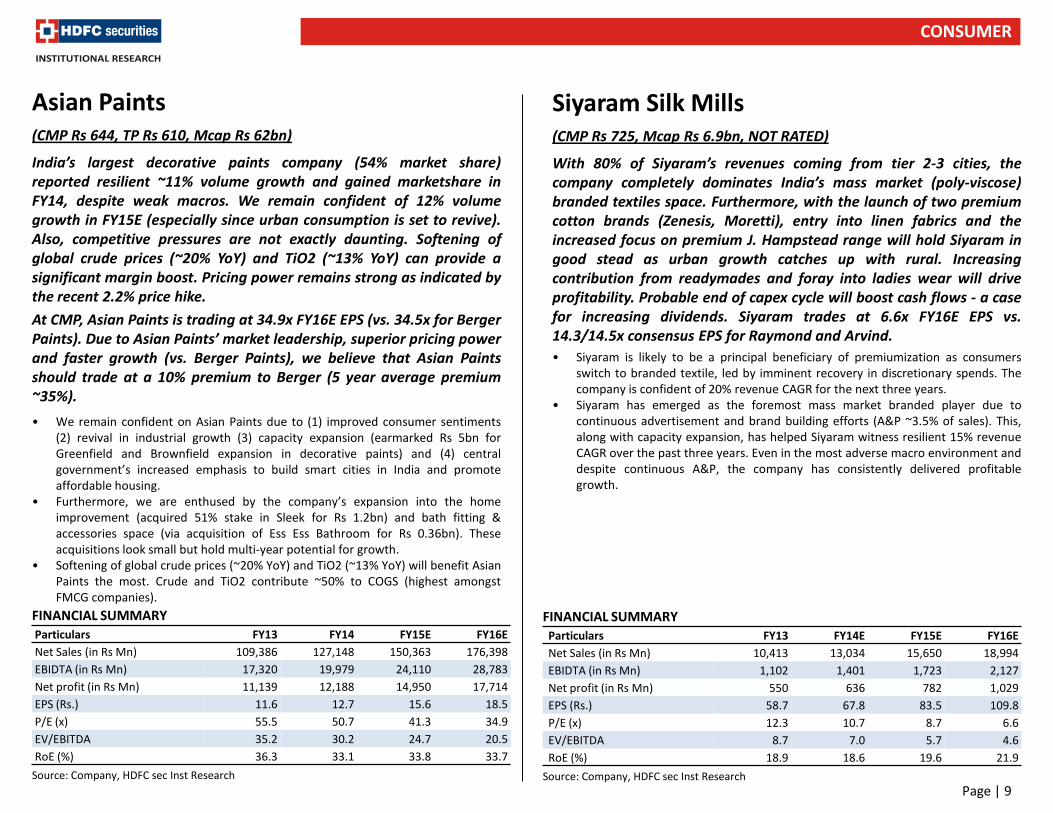

Asian Paints (CMP Rs 644, TP Rs 610, Mcap Rs 62bn)

India’s largest decorative paints company (54% market share) reported resilient ~11% volume growth and gained marketshare in FY14, despite weak macros. We remain confident of 12% volume growth in FY15E (especially since urban consumption is set to revive). Also, competitive pressures are not exactly daunting. Softening of global crude prices (~20% YoY) and TiO2 (~13% YoY) can provide a significant margin boost. Pricing power remains strong as indicated by the recent 2.2% price hike.

At CMP, Asian Paints is trading at 34.9x FY16E EPS (vs. 34.5x for Berger Paints). Due to Asian Paints’ market leadership, superior pricing power and faster growth (vs. Berger Paints), we believe that Asian Paints should trade at a 10% premium to Berger (5 year average premium ~35%).

• We remain confident on Asian Paints due to (1) improved consumer sentiments (2) revival in industrial growth (3) capacity expansion (earmarked Rs 5bn for Greenfield and Brownfield expansion in decorative paints) and (4) central government’s increased emphasis to build smart cities in India and promote affordable housing.

• Furthermore, we are enthused by the company’s expansion into the home improvement (acquired 51% stake in Sleek for Rs 1.2bn) and bath fitting & accessories space (via acquisition of Ess Ess Bathroom for Rs 0.36bn). These acquisitions look small but hold multi-year potential for growth.

• Softening of global crude prices (~20% YoY) and TiO2 (~13% YoY) will benefit Asian Paints the most. Crude and TiO2 contribute ~50% to COGS (highest amongst FMCG companies). FINANCIAL SUMMARY

Source: Company, HDFC sec Inst Research

Particulars FY13 FY14E FY15E FY16E

Net Sales (in Rs Mn) 10,413 13,034 15,650 18,994

EBIDTA (in Rs Mn) 1,102 1,401 1,723 2,127

Net profit (in Rs Mn) 550 636 782 1,029

EPS (Rs.) 58.7 67.8 83.5 109.8

P/E (x) 12.3 10.7 8.7 6.6

EV/EBITDA 8.7 7.0 5.7 4.6

RoE (%) 18.9 18.6 19.6 21.9

Siyaram Silk Mills (CMP Rs 725, Mcap Rs 6.9bn, NOT RATED)

With 80% of Siyaram’s revenues coming from tier 2-3 cities, the company completely dominates India’s mass market (poly-viscose) branded textiles space. Furthermore, with the launch of two premium cotton brands (Zenesis, Moretti), entry into linen fabrics and the increased focus on premium J. Hampstead range will hold Siyaram in good stead as urban growth catches up with rural. Increasing contribution from readymades and foray into ladies wear will drive profitability. Probable end of capex cycle will boost cash flows - a case for increasing dividends. Siyaram trades at 6.6x FY16E EPS vs. 14.3/14.5x consensus EPS for Raymond and Arvind.

• Siyaram is likely to be a principal beneficiary of premiumization as consumers switch to branded textile, led by imminent recovery in discretionary spends. The company is confident of 20% revenue CAGR for the next three years.

• Siyaram has emerged as the foremost mass market branded player due to continuous advertisement and brand building efforts (A&P ~3.5% of sales). This, along with capacity expansion, has helped Siyaram witness resilient 15% revenue CAGR over the past three years. Even in the most adverse macro environment and despite continuous A&P, the company has consistently delivered profitable growth.

FINANCIAL SUMMARY

Source: Company, HDFC sec Inst Research

CONSUMER

Page | 10

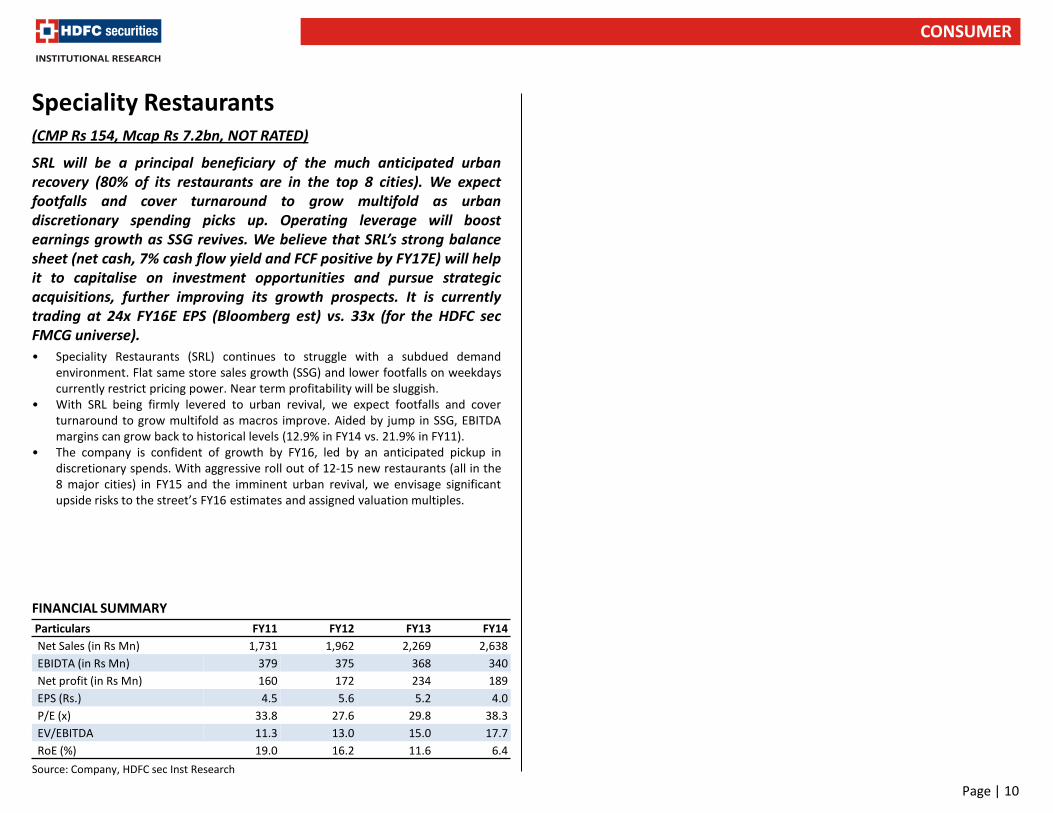

Particulars FY11 FY12 FY13 FY14

Net Sales (in Rs Mn) 1,731 1,962 2,269 2,638

EBIDTA (in Rs Mn) 379 375 368 340

Net profit (in Rs Mn) 160 172 234 189

EPS (Rs.) 4.5 5.6 5.2 4.0

P/E (x) 33.8 27.6 29.8 38.3

EV/EBITDA 11.3 13.0 15.0 17.7

RoE (%) 19.0 16.2 11.6 6.4

Speciality Restaurants (CMP Rs 154, Mcap Rs 7.2bn, NOT RATED)

SRL will be a principal beneficiary of the much anticipated urban recovery (80% of its restaurants are in the top 8 cities). We expect footfalls and cover turnaround to grow multifold as urban discretionary spending picks up. Operating leverage will boost earnings growth as SSG revives. We believe that SRL’s strong balance sheet (net cash, 7% cash flow yield and FCF positive by FY17E) will help it to capitalise on investment opportunities and pursue strategic acquisitions, further improving its growth prospects. It is currently trading at 24x FY16E EPS (Bloomberg est) vs. 33x (for the HDFC sec FMCG universe).

• Speciality Restaurants (SRL) continues to struggle with a subdued demand environment. Flat same store sales growth (SSG) and lower footfalls on weekdays currently restrict pricing power. Near term profitability will be sluggish.

• With SRL being firmly levered to urban revival, we expect footfalls and cover turnaround to grow multifold as macros improve. Aided by jump in SSG, EBITDA margins can grow back to historical levels (12.9% in FY14 vs. 21.9% in FY11).

• The company is confident of growth by FY16, led by an anticipated pickup in discretionary spends. With aggressive roll out of 12-15 new restaurants (all in the 8 major cities) in FY15 and the imminent urban revival, we envisage significant upside risks to the street’s FY16 estimates and assigned valuation multiples.

FINANCIAL SUMMARY

Source: Company, HDFC sec Inst Research

CONSUMER

Page | 11

(Rs mn) FY13 FY14 FY15E FY16E FY17E

Net Sales 7,073 8,398 9,334 11,111 13,750

EBITDA (adj.) 1,316 1,308 1,380 1,656 2,013

APAT 521 610 601 762 954

Diluted EPS (Rs) 18.5 21.7 21.4 27.1 33.9

P/E (x) 14.8 12.7 11.7 9.3 7.4

EV / EBITDA (x) 6.4 6.5 5.4 4.4 3.6

RoE (%) 12.1 12.6 11.1 12.6 13.9

KNR Constructions (CMP Rs 275, TP Rs 341, Mcap Rs 7.8bn)

We like KNR Constructions (KNRC) given (1) strong EBITDA margin profile of ~15% (2) low working capital cycle of 35 days (3) strong balance sheet with net debt/equity at 0.2x and (4) backward integration leading to on-time completion of projects.

• KNRC is a specialised player in road construction having completed ~5,400 lane kms that comprises over 90% of its order book. KNRC’s backward integration into quarries and RMC plants, own equipment and no sub-contracting have led to EBITDA margins of over 15% in FY09-14.

• Although balance sheets of most road contractors and developers are stressed, KNRC is one of the notable exceptions in the sector. Consequently, it is well placed to benefit from the expected order uptick in EPC road tenders from the NHAI and State Governments from H2FY15E onwards. KNRC currently has an order book of ~Rs 12bn as of Jun-14 (1.5x FY14 revenues, 90% in roads segment).

• KNRC has bid for orders worth ~Rs 110bn and is expecting fresh orders of ~Rs 20bn in FY15E. Owing to fresh order wins, we expect revenues to grow at 18% CAGR over FY14-17E to Rs 13.8bn. We estimate PAT CAGR of 16% over FY14-17E, marginally below revenue CAGR owing to lower EBITDA margins of ~14.6%. We expect KNRC to achieve RoEs of 12.6% in FY16E and 13.9% in FY17E owing to strong execution.

• We currently have a BUY rating on KNRC with SOTP value of Rs 341/sh. Our valuation includes Rs 275/sh for standalone EPC business (9x P/E on average FY16-17E EPS of Rs 30.5 and 1x P/B of investments of Rs 66/share (Kerala BOT project and land parcels).

FINANCIAL SUMMARY

Source: Company, HDFC sec Inst Research

(Rs mn) FY13 FY14 FY15E FY16E FY17E

Net Sales 7,275 7,642 7,744 12,702 19,669

EBITDA (adj.) 1,921 2,208 2,366 3,936 5,878

APAT 1,074 920 993 1,764 2,748

Diluted EPS (Rs) 14.2 12.1 13.1 23.3 36.3

P/E (x) 12.5 14.6 13.5 7.6 4.9

EV / EBITDA (x) 7.3 7.3 6.7 4.0 2.3

RoE (%) 14.4 11.7 11.7 18.2 23.4

Kolte-Patil Developers (CMP Rs 176, TP Rs 257, Mcap Rs 13bn)

Kolte-Patil Developers is another hi-conviction idea in real estate given its (1) Strong brand with 7-8% market share in the Pune residential market (2) Capital consciousness and aversion to leverage (3) Strong project pipe, and (4) Dividend distribution policy of 15-25% of profits.

• Kolte-Patil (KPDL) is a dominant player in the Pune residential market with ~7-8% market share led by robust execution across locations. With ~90% of KPDL’s portfolio concentrated in residential projects of which ~60-65% is targeted at the Rs 5-10mn ticket size, KPDL has been able to tap the sweet spot of Rs 4,000-6,000/psf to achieve sales bookings of Rs 35bn over FY12-14.

• After achieving its sales booking target of 7.6msf worth Rs 35bn over FY12-14, KPDL is well poised for the next leg of growth and is looking to achieve 12msf of sales worth Rs 72bn over FY15-17E. We believe that this is achievable given the strong launch pipeline (~19msf of approvals received in CY14) and its exposure to a stable Pune market.

• We model for 11.8msf of sales worth Rs 66.6bn over FY15-17E and expect KPDL to generate post interest cash surplus of Rs 1.7bn driven by ramp up in collections. We have a BUY rating on KPDL based on FY16E NAV of Rs 257/sh. The stock trades at 31% discount to NAV. Key upside risks are addition of more redevelopment projects in Mumbai, development manager fees from other projects and increase in township FSI from 0.5x to 1.0x in Pune.

FINANCIAL SUMMARY

Source: Company, HDFC sec Inst Research

REAL ESTATE & INFRA

Page | 12

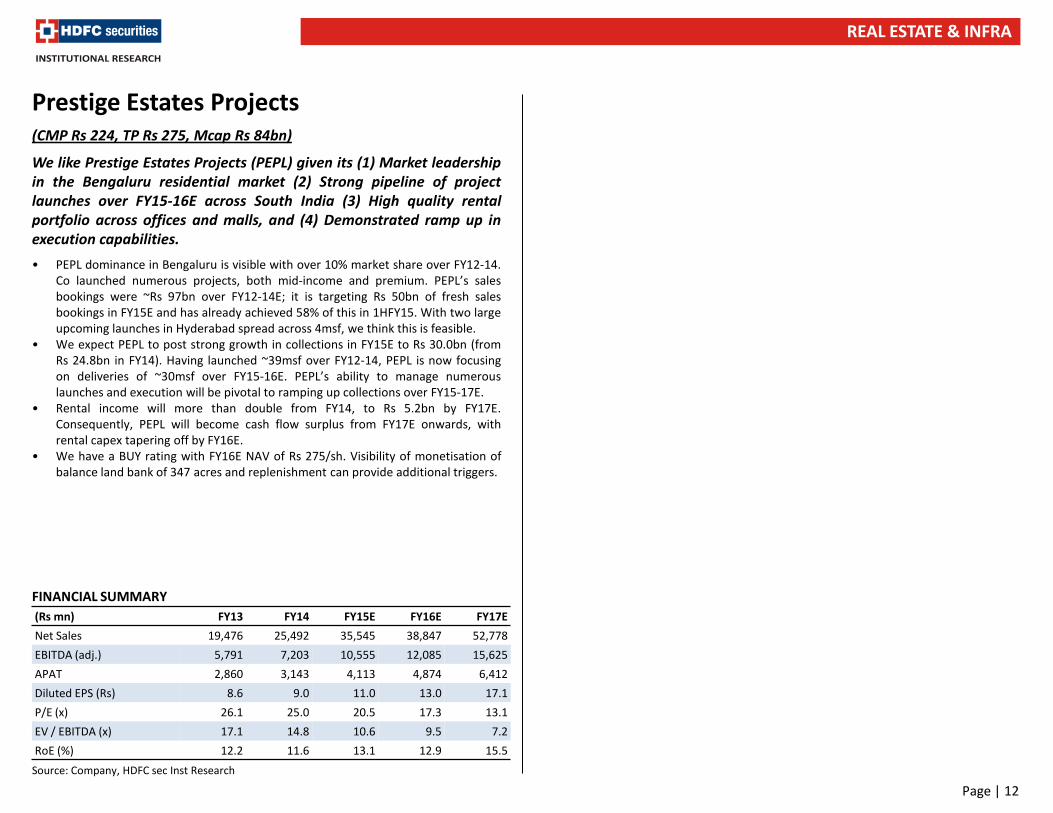

(Rs mn) FY13 FY14 FY15E FY16E FY17E

Net Sales 19,476 25,492 35,545 38,847 52,778

EBITDA (adj.) 5,791 7,203 10,555 12,085 15,625

APAT 2,860 3,143 4,113 4,874 6,412

Diluted EPS (Rs) 8.6 9.0 11.0 13.0 17.1

P/E (x) 26.1 25.0 20.5 17.3 13.1

EV / EBITDA (x) 17.1 14.8 10.6 9.5 7.2

RoE (%) 12.2 11.6 13.1 12.9 15.5

Prestige Estates Projects (CMP Rs 224, TP Rs 275, Mcap Rs 84bn)

We like Prestige Estates Projects (PEPL) given its (1) Market leadership in the Bengaluru residential market (2) Strong pipeline of project launches over FY15-16E across South India (3) High quality rental portfolio across offices and malls, and (4) Demonstrated ramp up in execution capabilities.

• PEPL dominance in Bengaluru is visible with over 10% market share over FY12-14. Co launched numerous projects, both mid-income and premium. PEPL’s sales bookings were ~Rs 97bn over FY12-14E; it is targeting Rs 50bn of fresh sales bookings in FY15E and has already achieved 58% of this in 1HFY15. With two large upcoming launches in Hyderabad spread across 4msf, we think this is feasible.

• We expect PEPL to post strong growth in collections in FY15E to Rs 30.0bn (from Rs 24.8bn in FY14). Having launched ~39msf over FY12-14, PEPL is now focusing on deliveries of ~30msf over FY15-16E. PEPL’s ability to manage numerous launches and execution will be pivotal to ramping up collections over FY15-17E.

• Rental income will more than double from FY14, to Rs 5.2bn by FY17E. Consequently, PEPL will become cash flow surplus from FY17E onwards, with rental capex tapering off by FY16E.

• We have a BUY rating with FY16E NAV of Rs 275/sh. Visibility of monetisation of balance land bank of 347 acres and replenishment can provide additional triggers.

FINANCIAL SUMMARY

Source: Company, HDFC sec Inst Research

REAL ESTATE & INFRA

Page | 13

Texmaco (CMP Rs 88, Mcap Rs 16bn, NOT RATED)

The argument for investing in Texmaco can be summed up in just two sentences.

(1) There could not have been a worse year than FY14 for India’s most capable Railway wagon maker. Revenues fell 50% to Rs 5.2bn, PAT tanked 82% to Rs 170mn even as the Railways placed ZERO wagon orders. A small order was, indeed, placed late in the year on account of supply defaults from other wagon makers.

(2) There cannot be a better business environment that Texmaco can aspire for than the current one. With a stated emphasis on building out the railway network and adding rolling stock, the Modi-fication of the Indian Railways can deliver multi-year growth for Texmaco. It is sitting pretty on the highest order of 2,400 wagons among all Indian wagon makers (from Indian Railways).

• About 81% of FY14 wagon revenues were from non-Railways customers. It is noteworthy that Texmaco’s gutsy management has continuously invested in building skills and capacities (EMU, DEMU, passenger coaches, loco shells/components, speciality wagons for cars and cement, steel castings, hydro mechanical equipment) even as Railway wagon orders dried up.

• Texmaco’s tie-ups with overseas entities such as Kawasaki Heavy Inds (for Locomotives and EMUs), UGL Rail Australia (for wagons) and Touax Rail France (for wagon leasing) are poised to deliver multi-year opportunities as they mature.

• Apart from rolling stock and equipment, the broader opportunity set in the Railways will be better addressed via Texmaco’s key acquisition (Kalindee Rail, a railway projects contractor with excellent credentials), which is proposed to be merged into the parent. Kalindee posted revenues of Rs 2.5bn for FY14 at a marginal loss. The merged entity continues to be net debt free.

• The first few salvos of the up-cycle are showing up in both order flow and corporate developments at Texmaco. The co received an order of Rs 4 bn for 974 wagons from the Ministry of Defence in early Oct-14. More recently, Texmaco has announced a JV with Westinghouse Air Brake Technologies Corp (Wabtec Corp, USA) for modern railway equipment and services in India.

• Post merger with Kalindee, the equity capital will rise to 191mn shares (from 182 mn currently), implying a mkt cap of Rs 16.4bn at CMP (Rs 86). Our view is that the merged entity can deliver revenues in excess of Rs 20 bn by FY17 (compared to Rs 8bn in FY14). We do not have Texmaco under formal coverage. However, this does not preclude us from noticing deep value at under 1x EV/revs.

INDUSTRIALS

Larsen & Toubro (CMP Rs 1,512, TP Rs 1,688, Mcap Rs 1,403bn)

L&T is fundamentally levered to India’s infrastructure cycle in a way that few companies are. We expect infra spends to revive gradually as the central government takes steps to ease execution constraints while also framing policies for increasing investments in under invested sectors. L&T stands to gain from this as well as the anticipated revival of railways, defence, mining and private sector capex. Our SOTP of Rs 1,688 assigns 18.5x to FY16E EPS of Rs 70 and Rs 393/sh for subsidiaries.

• That we are near an inflexion in L&T’s business is increasingly obvious. First, its net working capital (receivables + inventory - payables) is at 23% of revenues which is ~2.5x the levels seen four years ago. A new government is in the saddle and is seized of the urgency to push (and complete) infra spends. This is likely to bring down the working capital cycle for L&T as well as increase order inflow, execution, revenues and profits. While this reduction will be gradual, the change in direction is likely to be appreciated by investors.

• Second, investments in subsidiary and associate cos have recently fallen after continuously rising for six quarters. This will free up capital incrementally and lead to higher valuation multiples.

• Near term concerns persist on the hydrocarbon business and margin sustainability on overseas projects. However, as India order inflows and revenues pickup, this will become a smaller concern.

VALUATION SUMMARY

Source: Company, HDFC sec Inst Research

Value

(Rs mn) Value per

share Basis of valuation

L&T Standalone 1,192,609 1,295 18.5x FY16E EPS

L&T Infotech 75,533 82 14x FY14E PAT

L&T Finance holding 68,488 75 20% Disc. to Market cap

Infrastructure development pvt ltd. 62,775 68 3x FY13 investment

Manufacturing subs., JVs and associates

13,912 15 14x FY13 PAT

L&T international subsidiaries 27,528 30 14x FY13 PAT

Hydrocarbons 85,218 93 0.8x FY16E Sales

L&T Power development and Ship Building

27,813 30 1x FY13 book value

TOTAL SUBS 361,267 393

TARGET PRICE 1,553,876 1,688

Page | 14

(Rs mn) FY13 FY14 FY15E FY16E FY17E

Net Sales 15,015 14,385 16,823 23,674 28,311

EBITDA (adj.) 3,223 2,240 3,312 5,239 6,781

APAT 1,617 1,010 1,767 1,605 2,785

Diluted EPS (Rs) 7.9 4.9 8.6 7.8 13.6

P/E (x) 16.1 25.8 14.8 16.3 9.4

EV / EBITDA (x) 8.3 12.7 11.8 7.6 5.5

RoE (%) 21.4 12.7 19.7 15.6 22.9

Orient Cement (CMP Rs 128, TP Rs 177, Mcap Rs 26bn)

Orient Cement (Orient) is catching up with the industry leaders in South. It already runs one of the most efficient operations in the country (LTM operating costs at Rs 2,945/t vs Rs 3,400-3,800 for peers, barring Shree). From its current base in Devapur (Telangana, 3 mTPA) and Jalgaon (Maha. 2 mTPA), Orient is adding 3 mTPA at Gulbarga (Karnataka). At a total project cost of ~Rs 17bn (~US$95/t) and a commissioning by 1QFY16 (within 24 months of ordering), the upcoming plant should set new benchmarks in project execution.

• Orient’s next challenge is to replicate its best-in-class current operations at the new plant. Two solid advantages at Devapur (1) low landed cost of coal (due to proximity to the Singareni Collieries) and (2) fly ash (from NTPC’s Ramagundam TPP) are not replicable. However, savings may accrue from newer, more efficient equipment (new kiln, VRMs instead of ball mill-roller press combination). This will help the new plant generate similar profitability.

• At 8 mTPA capacity, operations in two regions and established cost leadership, Orient’s valuations at 11.8/7.6x FY15/FY16E EV/EBITDA and US$81/t (on FY16 exit financials) are still below peers like Ramco which trades at US$140/t.

• Given the booster from Gulbarga operations, we believe that the company can command premium valuations, especially given its best-in-class cost profile. While Orient may not yet have the scale of Ramco, it is clearly the cost leader in South. We have a BUY rating and a TP of Rs 170 based on 9.5x FY16 EV/EBITDA.

FINANCIAL SUMMARY

Source: Company, HDFC sec Inst Research

(Rs mn) FY13 FY14E FY15E FY16E FY17E

Net Sales 10,550 11,906 12,426 14,447 15,691

EBITDA (adj.) 2,009 1,948 2,307 2,835 3,508

APAT 459 496 634 1,327 1,968

Diluted EPS (Rs) 2.1 2.3 2.9 6.0 8.9

P/E (x) 27.8 25.7 20.1 9.6 6.5

EV / EBITDA (x) 9.8 9.2 7.3 5.4 3.6

RoE (%) 5.6 5.7 6.9 13.0 16.6

Sanghi Industries (CMP Rs 57, TP Rs 83, MCap Rs 12bn)

Sanghi Industries (SNGI) operates a 3 mTPA clinker capacity (2.6 mTPA grinding) in Kutch, Gujarat. It has access to soft marine limestone spread over ~1,500 hectares (containing ~1 bnt of proven reserves). The operations are fully integrated with captive power (63 MW), have the ability to use lignite in both kiln and CPP and a captive jetty within 1 km of the cement grinding plant.

• SNGI’s profitability is driven by low cost raw material, essentially surface mined limestone. Proximity to lignite mines of GMDC, ability to import coal at its captive jetty and excess captive power allow it low energy costs. However, low blending (C:C ratio at 1.1 in FY14) and a high proportion of road transport eat away large chunks of profitability.

• SNGI is investing in a 1 mTPA cement grinding unit at the existing location, likely to be commissioned in FY16. Further, increasing focus on low cost coastal freight should reduce costs, while accessing newer markets. In addition to existing terminals, SNGI is looking at setting up distribution capacity on the western coast and is acquiring vessels for transportation.

• SNGI has multiple levers of profitability improvement : product mix, volumes, and transportation. Current cash flows (at existing profitability) are strong enough to pare down the debt in next 2-3 years (Net debt FY14 ~Rs5.7bn, d/e: 0.69x). The next phase of capacity build-out can then begin, truly exploiting the billion tonne limestone reserves. We have a BUY rating, and a TP of Rs 83 (7.5x FY16E EV/EBITDA, US$100/t).

FINANCIAL SUMMARY

Source: Company, HDFC sec Inst Research

MATERIALS

Page | 15

(Rs mn) FY13 FY14 FY15E FY16E FY17E

Net Sales 6,987 6,875 9,086 11,762 13,090

EBITDA (adj.) 1,306 558 1,775 2,549 2,865

APAT 776 267 753 1,388 1,665

Diluted EPS (Rs) 29.0 10.0 28.2 52.0 62.4

P/E (x) 8.3 21.7 8.5 4.6 3.9

EV / EBITDA (x) 5.8 17.3 5.2 3.4 2.2

RoE (%) 16.8 5.3 14.1 22.3 22.1

Mangalam Cement (CMP Rs 239, TP Rs 415, Mcap Rs 6.4bn)

Mangalam Cement is available for under 50$/t. It has recently added 63% cement capacity to reach 3.25 mTPA. Gains will be manifold (1) the expanded kiln/grinding unit will have vastly improved energy efficiency (2) improvement in PPC proportion and (3) tie up of ~1,500tpd (~0.5 mTPA) of grinding capacity in NCR to lower freight costs. The expansion has been prudently executed, leaving the company only ~Rs3.2bn in net debt.

• The company sits on >50 years of limestone reserves in its current location. Next phase of expansion may likely include a split grinding unit in Aligarh (as previously planned) and clinker upgradation/new line at Morak. Given the ability of current operations to sustain a 2-3 year build cycle, we believe Mangalam is well set to leapfrog into the 5 mTPA league.

• Co is likely to post 23/25% EBITDA/ PAT CAGR over FY13-17. We have not built in any benefits from a 7-year VAT exemption in Rajasthan for the new capacity (for sales within Rajasthan).

• Outlook and view : The stock trades at 5.2/3.4x EV/EBITDA and US$44/t on FY16 numbers. Given the impending improvements in cost structure and its comfortable balance sheet for another transformative expansion (2 mTPA implies 62% capacity addition), the stock can rerate sustainably.

FINANCIAL SUMMARY

Source: Company, HDFC sec Inst Research

(Rs mn) FY13 FY14 FY15E FY16E FY17E

Net Sales 380,950 504,089 573,584 607,957 659,279

EBITDA (adj.) 65,073 91,655 111,663 120,995 152,556

APAT 9,552 3,510 29,323 30,654 49,467

Diluted EPS (Rs) 43.2 18.7 117.1 122.6 200.4

P/E (x) 27.2 62.9 10.0 9.6 5.9

EV / EBITDA (x) 8.1 7.7 6.5 5.7 4.1

RoE (%) 5.6 2.3 12.2 11.5 16.6

JSW Steel (CMP Rs 1,176, TP Rs 1,310, MCap Rs 284bn)

Cost and operational leadership set JSW Steel (JSTL) apart from peers and motivate us to recommend it notwithstanding global sluggishness in steel. Co has scripted a solid turnaround at Dolvi (Ispat) after acquisition. Commissioning and ramp-up on the coke oven battery and pellet plant should lower operational costs. Further, ramp-ups on the newly commissioned value added capacity (part of the 2.3 mTPA CRM-2) will further increase margins (value added products at 29% in 2QFY15). We have a BUY rating with a TP of Rs 1,310 (6.0x FY16 EV/EBITDA)

• JSTL has started executing 1.7mTPA expansion at Dolvi works. The proposed expansion includes setting up a sinter plant, blast furnace modification, debottlenecking of SMS and HSM, setting up a new biller caster and 1.4 mTPA Bar Mill. The expansion will cost Rs 33bn and will likely come on stream in FY16.

• The company plans to have an eventual capacity of 15 mTPA in the Dolvi complex. Recent acquisition of Welspun Maxsteel’s assets, close to Dolvi works, with a large land parcel and captive jetty will come in handy for the same.

• With margin expansion on course, aided by CRM-2 in Vijaynagar and increasing RM integration at Dolvi, JSTL is nicely poised to reap benefits from its recent capex. Further expansion at Dolvi will provide the next stage of volume expansion. While a benign RM environment helps, easing of domestic iron ore supplies may further boost prospects. JSTL is trading at an attractive valuation of 5.7x FY16 EV/EBITDA.

FINANCIAL SUMMARY

Source: Company, HDFC sec Inst Research

MATERIALS

Page | 16

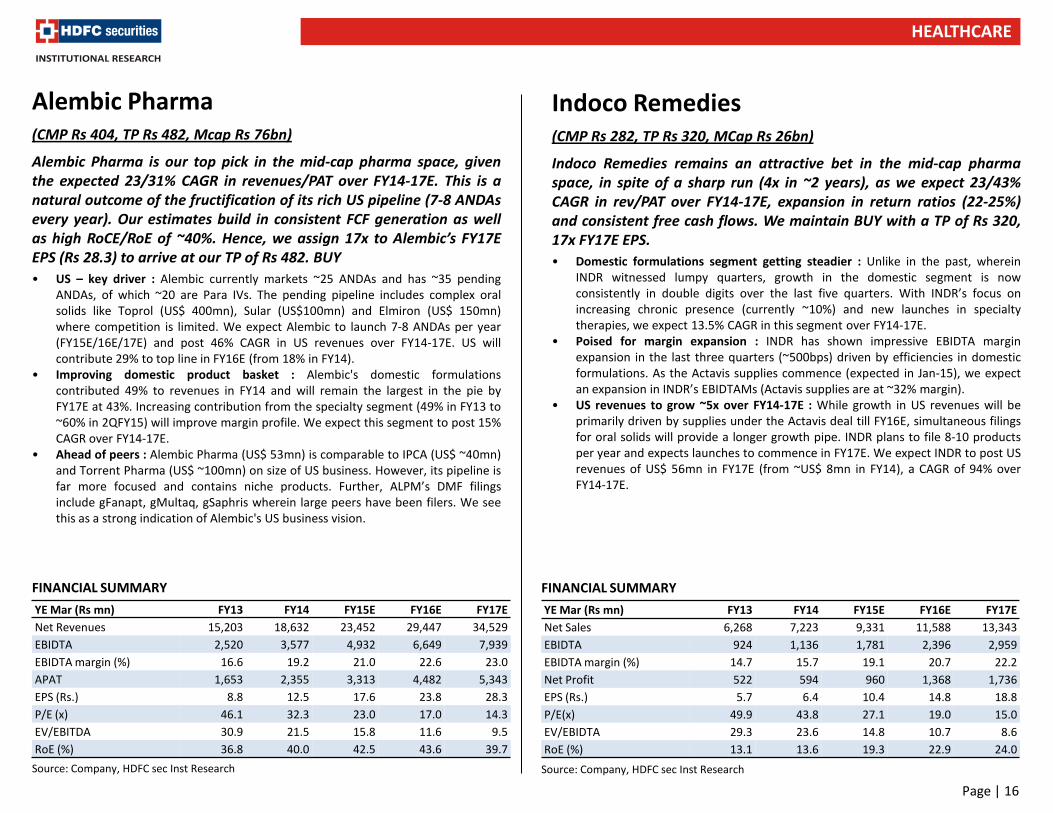

YE Mar (Rs mn) FY13 FY14 FY15E FY16E FY17E

Net Revenues 15,203 18,632 23,452 29,447 34,529

EBIDTA 2,520 3,577 4,932 6,649 7,939

EBIDTA margin (%) 16.6 19.2 21.0 22.6 23.0

APAT 1,653 2,355 3,313 4,482 5,343

EPS (Rs.) 8.8 12.5 17.6 23.8 28.3

P/E (x) 46.1 32.3 23.0 17.0 14.3

EV/EBITDA 30.9 21.5 15.8 11.6 9.5

RoE (%) 36.8 40.0 42.5 43.6 39.7

Alembic Pharma (CMP Rs 404, TP Rs 482, Mcap Rs 76bn)

Alembic Pharma is our top pick in the mid-cap pharma space, given the expected 23/31% CAGR in revenues/PAT over FY14-17E. This is a natural outcome of the fructification of its rich US pipeline (7-8 ANDAs every year). Our estimates build in consistent FCF generation as well as high RoCE/RoE of ~40%. Hence, we assign 17x to Alembic’s FY17E EPS (Rs 28.3) to arrive at our TP of Rs 482. BUY

• US – key driver : Alembic currently markets ~25 ANDAs and has ~35 pending ANDAs, of which ~20 are Para IVs. The pending pipeline includes complex oral solids like Toprol (US$ 400mn), Sular (US$100mn) and Elmiron (US$ 150mn) where competition is limited. We expect Alembic to launch 7-8 ANDAs per year (FY15E/16E/17E) and post 46% CAGR in US revenues over FY14-17E. US will contribute 29% to top line in FY16E (from 18% in FY14).

• Improving domestic product basket : Alembic's domestic formulations contributed 49% to revenues in FY14 and will remain the largest in the pie by FY17E at 43%. Increasing contribution from the specialty segment (49% in FY13 to ~60% in 2QFY15) will improve margin profile. We expect this segment to post 15% CAGR over FY14-17E.

• Ahead of peers : Alembic Pharma (US$ 53mn) is comparable to IPCA (US$ ~40mn) and Torrent Pharma (US$ ~100mn) on size of US business. However, its pipeline is far more focused and contains niche products. Further, ALPM’s DMF filings include gFanapt, gMultaq, gSaphris wherein large peers have been filers. We see this as a strong indication of Alembic's US business vision.

FINANCIAL SUMMARY

Source: Company, HDFC sec Inst Research

YE Mar (Rs mn) FY13 FY14 FY15E FY16E FY17E

Net Sales 6,268 7,223 9,331 11,588 13,343

EBIDTA 924 1,136 1,781 2,396 2,959

EBIDTA margin (%) 14.7 15.7 19.1 20.7 22.2

Net Profit 522 594 960 1,368 1,736

EPS (Rs.) 5.7 6.4 10.4 14.8 18.8

P/E(x) 49.9 43.8 27.1 19.0 15.0

EV/EBIDTA 29.3 23.6 14.8 10.7 8.6

RoE (%) 13.1 13.6 19.3 22.9 24.0

Indoco Remedies (CMP Rs 282, TP Rs 320, MCap Rs 26bn)

Indoco Remedies remains an attractive bet in the mid-cap pharma space, in spite of a sharp run (4x in ~2 years), as we expect 23/43% CAGR in rev/PAT over FY14-17E, expansion in return ratios (22-25%) and consistent free cash flows. We maintain BUY with a TP of Rs 320, 17x FY17E EPS.

• Domestic formulations segment getting steadier : Unlike in the past, wherein INDR witnessed lumpy quarters, growth in the domestic segment is now consistently in double digits over the last five quarters. With INDR’s focus on increasing chronic presence (currently ~10%) and new launches in specialty therapies, we expect 13.5% CAGR in this segment over FY14-17E.

• Poised for margin expansion : INDR has shown impressive EBIDTA margin expansion in the last three quarters (~500bps) driven by efficiencies in domestic formulations. As the Actavis supplies commence (expected in Jan-15), we expect an expansion in INDR’s EBIDTAMs (Actavis supplies are at ~32% margin).

• US revenues to grow ~5x over FY14-17E : While growth in US revenues will be primarily driven by supplies under the Actavis deal till FY16E, simultaneous filings for oral solids will provide a longer growth pipe. INDR plans to file 8-10 products per year and expects launches to commence in FY17E. We expect INDR to post US revenues of US$ 56mn in FY17E (from ~US$ 8mn in FY14), a CAGR of 94% over FY14-17E.

FINANCIAL SUMMARY

Source: Company, HDFC sec Inst Research

HEALTHCARE

Page | 17

AB Nuvo is the only conglomerate among our Diwali picks. Its Idea stake is levered to telecom data growth, while leading brands (Louis Phillips, Allen Solly, Peter England, Van Heusen and Linen Club) comprise the bulk of its highly profitable lifestyle/apparel business. Its life insurance business is poised to bounce back in line with broader trends on financial savings. It owns a fast growing and diversified NBFC with good asset quality, while Birla Sunlife AMC is well poised to gain from higher allocation to equities by Indian savers as gold and real estate cool off. Our back-of-the-envelope SoTP suggests an upside of 35% from current levels.

• We believe that Idea’s operating cash flow will continue to increase with RPM & data growth in the medium term. Also, Idea has gained significant market share in most of the circles where it has operations. We believe that Telecom companies will maintain pricing discipline given leveraged balance sheets. However spectrum auctions and Reliance Jio’s launch may put pressure on valuations.

• Through Madura Fashion and Lifestyle, ABNL owns one of the biggest and most profitable branded apparel businesses in India. It also owns the largest linen fabric manufacturing capacity via Jayshree Textiles. Madura’s brands have delivered 27% CAGR over the trailing five years. The business enjoys high return ratios in excess of 60%, rising margins, capital efficiency and strong growth opportunities via category diversification and outlet expansion. Jayshree Textiles has recently completed a 50% capacity expansion. We value Madura Garments and Jayshree Textiles at Rs 75bn. We expect restructuring of operations at Pantaloons and value it at book value (Rs 6bn).

• Aditya Birla Financial Services (100% stake) runs a fast growing, profitable and broadbased NBFC portfolio. The business has delivered a PAT of Rs 1.66bn in FY14. We think profits here can grow rapidly as the operation scales up. We value this business at Rs 35bn (2x FY14 networth of Rs 17.7bn).

• Birla Sunlife Insurance is coming off a sluggish phase owing to industry specific issues. New business premium is poised to bounce back into growth after four years of decline as traditional product sales revive. Renewal premium has de-

grown for two years, but we think persistency has bottomed out at 58% in FY13 (61% in FY14). We value ABNL’s 74% in Life Insurance business at Rs 47bn (12x FY14 NBAP + embedded value Rs 32 bn)

• Birla MF touched AUM of Rs 1.2 trillion crore (Equity Rs 200bn). The AMC earned PAT of Rs 0.95 in FY14 and can grow at 20%+CAGR with an imminent revival in financial savings and top notch performance from most equity fund schemes of Birla MF. We value this business at Rs 20bn (51% stake translates to Rs 10bn)

Manufacturing business : UREA, RAYON and INSULATORS • Fertilizer, Rayon & Insulators posted a combined EBITDA of Rs 3.8 bn in FY14. Our

estimate of equity value of this business is a mere Rs 10 bn. Replacement cost of the Urea operations alone exceed Rs 50bn.

CONGLOMERATES

Business segment Value (Rs bn)

Idea stake after 20% holdco discount 110

Branded apparel (Madura, Jayshree,

Pantaloons) 81

Insurance 47

NBFC 35

AMC 10

Manufacturing businesses (urea, viscose yarn,

insulators) 10

Total Value 293

AB Nuvo’s Current Mcap 215

Upside 36%

Aditya Birla Nuvo : SoTP

Aditya Birla Nuvo (CMP Rs 1,652, Mcap Rs 215bn, NOT RATED)

Source: Company, HDFC sec Inst Research

Page | 18

Disclaimer: This report has been prepared by HDFC Securities Ltd and is meant for sole use by the recipient and not for circulation. The information and opinions contained herein have been compiled or arrived at, based upon information obtained in good faith from sources believed to be reliable. Such information has not been independently verified and no guaranty, representation of warranty, express or implied, is made as to its accuracy, completeness or correctness. All such information and opinions are subject to change without notice. This document is for information purposes only. Descriptions of any company or companies or their securities mentioned herein are not intended to be complete and this document is not, and should not be construed as an offer or solicitation of an offer, to buy or sell any securities or other financial instruments. This report is not directed to, or intended for display, downloading, printing, reproducing or for distribution to or use by, any person or entity who is a citizen or resident or located in any locality, state, country or other jurisdiction where such distribution, publication, reproduction, availability or use would be contrary to law or regulation or what would subject HDFC Securities Ltd or its affiliates to any registration or licensing requirement within such jurisdiction. If this report is inadvertently send or has reached any individual in such country, especially, USA, the same may be ignored and brought to the attention of the sender. This document may not be reproduced, distributed or published for any purposes without prior written approval of HDFC Securities Ltd . Foreign currencies denominated securities, wherever mentioned, are subject to exchange rate fluctuations, which could have an adverse effect on their value or price, or the income derived from them. In addition, investors in securities such as ADRs, the values of which are influenced by foreign currencies effectively assume currency risk. It should not be considered to be taken as an offer to sell or a solicitation to buy any security. HDFC Securities Ltd may from time to time solicit from, or perform broking, or other services for, any company mentioned in this mail and/or its attachments. HDFC Securities and its affiliated company(ies), their directors and employees may; (a) from time to time, have a long or short position in, and buy or sell the securities of the company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies) discussed herein or act as an advisor or lender/borrower to such company(ies) or may have any other potential conflict of interests with respect to any recommendation and other related information and opinions. HDFC Securities Ltd, its directors, analysts or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments made or any action taken on basis of this report, including but not restricted to, fluctuation in the prices of shares and bonds, changes in the currency rates, diminution in the NAVs, reduction in the dividend or income, etc. HDFC Securities Ltd and other group companies, its directors, associates, employees may have various positions in any of the stocks, securities and financial instruments dealt in the report, or may make sell or purchase or other deals in these securities from time to time or may deal in other securities of the companies / organisations described in this report.

Rating Definitions BUY : Where the stock is expected to deliver more than 10% returns over the next 12 month period NEUTRAL : Where the stock is expected to deliver (-)10% to 10% returns over the next 12 month period SELL : Where the stock is expected to deliver less than (-)10% returns over the next 12 month period

HDFC securities Institutional Equities Unit No. 1602, 16th Floor, Tower A, Peninsula Business Park, Senapati Bapat Marg, Lower Parel, Mumbai - 400 013 Board : +91-22-6171 7330 www.hdfcsec.com