insight wimax outlook in the us market: implications for service

TRANSCRIPT

insight

WiMAX has recently gained a lot of traction and attention in the market and media. We believe the technology has a large addressable market in the US but realistically may capture only a small share of that, competing against incumbent fixed and wireless technologies that are also evolving in terms of bandwidth and costs.

The market penetration and success of WiMAX will be determined by how quickly its ecosystem organizes and collaborates to prioritize target segments, develop and market simple-to-use and affordable end-user applications and devices. Potential WiMAX players need to accelerate the adoption of the service and attract a critical mass of users before competing technologies can catch up.

There is a diverse range of potential owned or leased-facility WiMAX players—pure wireless carriers, integrated carriers, cable and satellite operators, fixed incumbent and competitive operators, MVNOs, and content owners and aggregators. Each player should ask the right strategic questions to objectively assess the economics of WiMAX, only as one of the potential enabling technologies to support incremental growth, drive customer retention, or reduce its operating or capital cost structure.

WiMAX Outlook in the US Market: Implications for Service ProvidersBy Hamilton Sekino, John Kwon and David Gates

Introduction . . . . . . . . . . . .2

Context and Background . . . . . . . . 3

Positive Momentum for WiMAX . . . 5

WiMAX Market Forecast and Economics . . . . . . . . . . .7

Implications for Service Providers . . 12

Conclusion . . . . . . . . . . 17

About the Firm . . . . . . . . . . . . 18

About the Authors . . . . . . . . . . 18

table of contents

WiMAX, the trade name given to technologies based on the IEEE 802.16 standards for broadband wireless communications, is finally emerging as a credible alternative for US telecom service providers looking to deploy next-generation broadband wireless networks. WiMAX is gaining momentum among both vendors and service providers in part due to its promise to be a viable technology to provide wireless broadband and to reduce the mobility premium of 3G networks. WiMAX-focused startup Clearwire, which already operates fixed WiMAX networks in more than 30 cities, received more than $1 billion from investors led by Intel and Motorola. Meanwhile, Sprint has announced it will build a mobile WiMAX network, for which it may spend $3 billion to reach 100 million people in major metropolitan areas across the US.

Despite the growing attractiveness of WiMAX, service providers are only beginning to grapple with potential offer

strategies as they face many unanswered questions on both the demand and supply sides of a WiMAX business case. In this paper Diamond addresses the demand question by segmenting the market for both fixed and mobile WiMAX and by estimating the addressable market for each of these segments. In addition, we use market benchmarks of new technology introductions in the telecom industry to further estimate the potential market that WiMAX can capture. We also determine the breakeven capital investment of fixed and mobile WiMAX based on demand and WiMAX’s expected market share estimates. Finally, we address the supply question by identifying nine categories of potential WiMAX providers, including RBOCs, cable operators, local exchange carriers, Web portals and media companies, reviewing the potential fixed and mobile WiMAX plays available to each set of players, and highlighting key strategic questions these players will need to address before they decide on any WiMAX initiatives.

2

Introduction

For more information contact:

Hamilton Sekino, Partner Telecom & High Tech Practice [email protected]

3

Context and Background

WiMAX Time-to-Market AdvantageWiMAX will offer service providers an attractive alternative to current and future generations of CDMA 1xEV-DO and WCDMA HSDPA technologies. In the United States, today’s EV-DO networks (Verizon Wireless and Sprint) are theoretically capable of reaching peak speeds of 2.4 Mbps (downlink) and 150 Kbps (uplink). Theoretical peak rates are higher for Cingular’s HSDPA network, approaching 3.6 Mbps (downlink) and 384 Kbps (uplink).

EV-DO and HSDPA will be challenged to compete against mobile WiMAX once the latter technology becomes commercially available in the US (Sprint aims to launch a mobile WiMAX network covering about 100 million people by mid-2008, and other players could light up metropolitan networks even sooner). EV-DO and HSDPA will offer higher speeds by this date. Verizon and Sprint are upgrading their EV-DO networks

to RevA, which has theoretical speeds of up to 3.1 Mbps (downlink) and 1.8 Mbps (uplink). AT&T/Cingular will also continue to bolster its HSDPA network. Future versions of HSDPA could achieve peak rates of 14.4 Mbps (downlink) and 2 Mbps (uplink) although actual speeds will probably be much lower. Despite these speed increases, the EV-DO and HSDPA networks will be challenged to match the data transfer rates of mobile WiMAX, which are projected to reach 14 Mbps (downlink) and 5.3 Mbps (uplink).

The performance gap between WiMAX and the 3G mobile technologies may widen when service providers deploy new versions of each of the technologies, starting in 2008. Integration of MIMO and beamforming technologies to mobile WiMAX will dramatically increase its potential data transfer rates to 32 Mbps (downlink) and 8 Mbps (uplink). By comparison, theoretical

WiMAX Time-to-Market Advantage

Evolution of 3G and WiMAX

3G

WiMAX

WCDMA• 2 x 5 MHz FDD• Peak = 384/384 Kbps

(DL/UL)• 850/1900 MHz bands

in the US

HSDPA• 2 x 5 MHz FDD• Enhanced DL• Peak = 14.4/2.0 Mbps• 850/1900 MHz bands

HSUPA• 2 x 5 MHz FDD• Enhanced UL• Peak = 14.4/5.8 Mbps• 850/1900 MHz bands

HSPA+ LTE• Multi-carrier

(1.25 - 20 MHz)• Peak = 100/50

Mbps

EV-DO Rev0• 2 x 1.25 MHz FDD• Enhanced DL• Peak = 2.4/0.15 Mbps (DL/UL)• 850/1900 MHz bands in the US

EV-DO RevA• 2 x 1.25 MHz FDD• Enhanced DL/UL• Peak = 3.1/1.8 Mbps• 850/1900 MHz bands

EV-DO RevB• Multi-carrier (1.25 - 20

MHz) & Enhanced DL• Peak = 4.9/1.8 Mbps

(2 x 1.25 MHz FDD)• 850/1900 MHz bands

EV-DO RevC• “Ultra Mobile Broadband”• Multi-carrier, Flexible

spectrum allocationoption & Enhanced DL/UL

• Peak = 70+/30+ Mbps

• 2 x 5 MHz FDD• Enhanced DL/UL• Peak = 40/10 Mbps• 850/1900 MHz

bands

Fixed WiMAX Mobile WiMAX• Scalable bandwidth

(5, 7, 8.75, 10 MHz)• OFDM & LOS• Peak = 14/5.3 Mbps

(1 x 10 MHz TDD)• 2.5/5.8 GHz bands

• Scalable bandwidth(5, 7, 8.75, 10 MHz)

• SISO, OFDMA & NLOS• Peak = 14/5.3 Mbps

(1 x 10 MHz TDD)• 2.5 GHz band

Mobile WiMAX• Scalable bandwidth• MIMO, OFDMA &

Beamforming• Peak = 32/7 Mbps

(1 x 10 MHz TDD)

2005 2010+2006 2007 2008 2009

Note: Timeline depicts initial commercial availability. Those introduced beyond 2008 are under standardization and are subject to variability.

Sources: WiMAX Forum, CDG, 3GPP.

Figure 1

WiMAX is expected to have a time-to-market advantage of approximately 12 months and offer higher data rates suitable for broadband wireless access.

4

WiMAX Wireless Enablement and Premium Reduction

Source: Forrester Research, Company Websites, Diamond analysis.

40.1 64.1Laptops

24.4 81.0MP3 Phones

31.8 47.2MP3 Players

65.3 93.7Digital Cameras

45 91.9Camera Phones

Wireless Enablement of Consumer Devices

US Households Owning a Data-Centric Device (Millions)

20062011

91%$60 per month 2$32 per month1Wireless

BroadbandAccess

127%$2.25 per song 4$0.99 per song 3Wireless

MusicDownload

$0.89 6 N/AFree

(advertising-based model)5

WirelessPhotoUpload

3G Pricing WirelessPremium

Fixed SubstitutePricingApplication

1. Average of BellSouth DSL ($32.95) and AT&T DSL ($29.95), excluding promotions.2. EVDO and HSDPA unlimited plans from Verizon Wireless, Sprint and Cingular.3. Apple iTunes. 4. Average of Verizon VCAST ($1.99 via mobile) and Sprint Vision Music ($2.50 via mobile).5. Photo upload and storage services by Yahoo! Photos, HP Snapfish, Sony ImageStation and Kodak EasyShare Gallery.6. Based on cost per photo upload for 1.3 MP cameras on most US mobile phones.

Figure 2

peak rates for EV-DO RevB will be 4.9 Mbps (downlink) and 1.8 Mbps (uplink) while HSUPA will reach 14.4 Mbps and 5.8 Mbps, respectively. If enhanced mobile WiMAX indeed realizes superior data transfer rates without requiring significantly greater capital expenditures, the technology will weigh heavily on US service providers’ data network deployment strategies after 2008. Although subsequent generations of 3G technologies (e.g. EV-DO RevC and HSPA+) will provide substantially improved speeds, they will still trail behind WiMAX in commercial availability, coming to the market only in 2009. Their later arrival will give mobile WiMAX a critical time-to-market advantage of approximately 12 months.

WiMAX Wireless Enablement and Premium Reduction WiMAX has the potential to boost demand for wireless data by reducing the cost of integration of wireless interfaces into consumer devices such as laptops, MP3 players, digital cameras and portable video games, and by minimizing the “wireless premium” to accessing the same application with a fixed broadband connection. WiMAX could broaden the portfolio of wireless-enabled consumer electronics devices by lowering the wireless interface chipset costs in these devices. EV-DO chipsets currently cost $30 or more, while WiMAX chipsets are projected to be as inexpensive as $3 once demand for the emerging

technology creates enough economies of scale to drive down costs.

Additionally, WiMAX could dramatically lower the “wireless premium” for data services (in other words, the difference between the price of accessing an application using a fixed broadband connection as opposed to a wide-area wireless network) by leveraging potentially superior network performance (which implies lower price-per-MB to consumers). To date, the much higher cost of 3G compared to fixed broadband (a 127 percent wireless premium for downloading an MP3 song, or a 91 percent premium for high-speed Internet access) has inhibited demand for wireless connectivity.

WiMAX can reduce the wireless premium and drive penetration of device-specific applications across a wide range of portable consumer electronics such as digital cameras, laptops and MP3 players.

5

WiMAX is gaining traction in the marketplace as the establishment of industry-wide standards enables both service providers and technology vendors to make commercial commitments to the technology, thereby forming the foundation for a WiMAX ecosystem.

The WiMAX Forum The WiMAX Forum has been the key organization promoting WiMAX among technology vendors and service providers. The WiMAX Forum was created in 2001 by a handful of equipment vendors and two major semiconductor companies—Intel and Fujitsu—for the purpose of establishing universal standards for the IEEE 802.16 family of wireless metropolitan area network standards. Since 2001, the WiMAX Forum has grown to encompass more than 300 companies, including technology vendors such as Alcatel, Lucent, Motorola, Nortel, and Samsung, and service providers such as British Telecom, KDDI, and Sprint Nextel. The WiMAX Forum

established standards for fixed WiMAX (802.16-2004) in October 2004 and for mobile WiMAX (802.16e) in December 2005. Fixed WiMAX equipment was first certified by the WiMAX Forum’s certification laboratory in Spain in January 2006. Since then, a number of vendors such as Airspan, Alvarion, Motorola, Navini Networks, and Nortel have developed fixed WiMAX-certified equipment. The rollout of certified mobile WiMAX equipment is expected in early 2007, although several vendors are already promoting “pre-WiMAX” equipment, and the WiBRO mobile broadband network in Korea, which is a variant of mobile WiMAX, is already operating.

Technology Vendors Component vendors, infrastructure vendors, and device manufacturers are each playing a role to advance the development and commercialization of WiMAX. Intel has been WiMAX’s greatest champion since it helped launch the WiMAX Forum five years

Positive Momentum for WiMAX: Technology Providers

Component Vendors Infrastructure Vendors

•

•

WiMAX’s largest promoter, Intel stands to gain from WiMAX chipset sales to device OEMs1

• Beceem Communications released the first commercially available terminal chipsets for mobile WiMAX in January 2006

• Motorola dominates the US market after capturing equipment contracts with Clearwire and Sprint

• Israel’s Alvarion claims 80% of the WiMAX market, with installations in 30 countries

Texas Instruments, Motorola and Samsung are also active in WiMAX chipset and component development

• Nortel announced the first MIMO-powered mobile WiMAX solution to deliver 4G mobile broadband content 2

Device Manufacturers WiMAX Forum

• The WiMAX Forum promotes WiMAX by establishing standards, certifying equipment and devices and ensuring the global compatibility and inter-operability of WiMAX products

• Currently, it has over 350 members, including leading equipment manufacturers, service providers and system integrators

• Infrastructure vendors such as Motorola and Alvarion provide fixed WiMAX CPEs

• Samsung and LG have been introducing a handful of WiBrodevices (PDA types and laptops) in Korea

3

• Samsung has unveiled a prototype dual-mode phone that supports WiBro and 3G CDMA in June 2006

• Nokia plans to release dual-mode phones in 2008

1. Intel announced its first dual-mode (fixed and mobile) baseband WiMAX chipset for device manufacturers in October 2006.2. Nortel reported that its MIMO-based (Multiple Input Multiple Output antenna technology) mobile WiMAX would deliver three times the speed and twice the subscriber

capacity with greater range and building penetration in urban areas compared to non-MIMO WiMAX.3. WiBro is a Korean-developed variant of the 802.16e-2005 mobile WiMAX standard and was commercially launched in Korea in June 2006.

Figure 3

Positive Momentum for WiMAX

Growing participations and activities by various stakeholders have considerably accelerated the maturation of the WiMAX ecosystem over the past few years.

6

Positive Momentum for WiMAX: Service Providers

Wireless Operator Cable Operators

• Plans to invest up to $3B in 2007 and 2008 to deploy a mobile WiMAX network initially covering 100M POPs

• Owns 90 MHz of 2.5 GHz spectrum covering 85 markets• Partly motivated FCC deadline for Sprint to utilize its 2.5 GHz

spectrum assets to cover 30M POPs by 2011• Partnering with Intel, Motorola and Samsung to develop

chipsets, network equipment and WiMAX handsets

• Formed a consortium and acquired 137 licenses in “B” block (20 MHz) of AWS spectrum (covering 267M POPs and most major markets) for $2.4B in September 2006

• Planning to “evaluate all options” including possible WiMAX testing in limited markets

• May consider incorporating the new spectrum assets into the existing joint venture with Sprint

RBOCs Clearwire

• Deploying nationwide WiMAX network on 2.5 GHz band (162Kcustomers in 31 markets with 5.6M POPs by Sept. 2006; 90M POPs covered by current licenses)

• Owns 2.5 GHz licenses for 100 small-city markets and another 60 markets from a trade with Sprint Nextel

• Received $1B in new financing from Intel and Motorola• Bell Canada to be an exclusive VoIP supplier for Clearwire

around the globe (in addition to making $100M investment)• Expected to provide US roaming to Inukshuk, a wireless

broadband JV between Bell Canada and Rogers

• Conducting trials of fixed WiMAX services in small communities throughout the US

• BellSouth having the most assets with 50+ licenses in 2.5-2.6GHz bands and 22 licenses in 2.3 GHz band

• Other RBOCs relying more on unlicensed bands• Exploring to roll out WiMAX selectively in areas where they

currently do not offer DSL services

Figure 4

ago. The microprocessor manufacturer stands to benefit from the popularization of WiMAX, especially because WiMAX’s source technology is not dominated by other companies such as Qualcomm. Other component vendors, including Texas Instruments, Motorola, and Samsung, are following Intel’s lead and developing their own chipsets for fixed and mobile WiMAX. In addition, several infrastructure vendors are placing large bets on WiMAX. Motorola was among the first to commit to WiMAX, and it now stands to dominate the US market for years to come after locking in exclusive contracts with Clearwire and Sprint. Smaller vendors, such as Airspan, Alvarion, and Navini Networks, are also focusing much of their businesses on WiMAX, eyeing additional global market

opportunities. Device manufactures are intensifying their WiMAX initiatives as well. While fixed WiMAX CPEs are largely developed by infrastructure vendors as a part of their turn-key solutions, both Samsung and LG have unveiled CDMA-compatible smartphones for the Korean WiBRO network.

Service Providers Service providers in several countries, including the US, are driving demand for both fixed and mobile WiMAX. In the US, Clearwire and Sprint have committed to building nationwide networks for fixed and mobile WiMAX. Clearwire, which currently offers fixed WiMAX services in more than 30 mid-size cities, aims to expand to many more rural and suburban markets around the

country and eventually offer mobile WiMAX. Sprint has announced plans to build a nationwide mobile WiMAX network covering 100 million people (mostly in large cities) by 2008. Sprint’s cable partners (Comcast, Time Warner, Cox and Advance/Newhouse) may participate in this venture. They recently acquired nationwide AWS spectrum licenses that could be used for deploying mobile WiMAX, although they are in preliminary stages of reviewing how to best use these assets. Other players are taking a more tactical approach to WiMAX. The Regional Bell Operating Companies (RBOCs) are viewing WiMAX as a potential broadband technology of choice for towns or regions that lie outside of DSL coverage. AT&T, Qwest and Verizon are each trialing fixed WiMAX networks among several technology options.

Recent announcements of WiMAX investments and commercial interests by high-profile telecom companies, more specifically the service providers, have created positive boost for the WiMAX ecosystem.

7

WiMAX will enable two types of broadband offers—a fixed broadband offer as a substitute to DSL and Cable and a mobile broadband offer as an upgrade or complement to existing 3G technologies such as EV-DO and HSDPA.

Fixed WiMAX enables users to communicate wirelessly within the range of a specific antenna attached to their home or office, while mobile WiMAX frees users to migrate from one antenna to another. The customer experience of fixed WiMAX echoes that of a local-area WiFi network, while the experience of mobile WiMAX resembles that of a wide-area 3G network. Fixed WiMAX will be most attractive to those households in primarily rural geographies that are not covered by cable or DSL networks, while mobile WiMAX will be more attractive to those end-users who desire wireless broadband access or who are frequent users of data-intensive mobile applications (e.g. audio, video, bulk data). A large majority of these customers will likely be found in urban and suburban as opposed

to rural geographies. Figure 5 illustrates a framework that represents the range of fixed and mobile WiMAX offers to customers in rural, suburban, and urban areas. We use this geographical division as a basis for developing addressable market sizes for both fixed and mobile WiMAX in the US.

Market Segmentation by PRIZM Clusters We leveraged Claritas’ PRIZM Cluster segmentation methodology to estimate addressable market sizes for fixed and mobile WiMAX in the US. Each PRIZM cluster describes a household-based market segment whose categorization is based on family structure, income and lifestyle factors (see Figure 6). For example, “Hometown Retired” represents pension-dependent seniors who live in aging suburban homes while “Bohemian Mix” refers to progressive young singles and couples—both students and professionals—living in urban areas. For our study, we grouped

Potential WiMAX Offers

Potential WiMAX Offers

MOBILITY

LOCA

LITY

Fixed Mobile• High data intensity• Indoor residential & business with

stationary equipment• Speed critical

•Moderate data intensity

•

Outdoor, on-the-go with portableequipment

•

Roaming & coverage critical

Rural• Low population density• Residential & small business• Little or no broadband access technologies

available

Suburban• Moderate population density• Single family residences, business parks &

strip malls• Some technologies not universally available

Urban• Highest population density• Many multiple tenant office & residential

buildings• Multiple technologies available

3G Upgrade(Mobile Broadband)

• Voice– VoIP with WiFi phones

(WiMax as backhaul)– Soft hand-offs between WiFi and

Cellular with dual mode phones

• Data– Broadband access via PCs &

laptops (range of speed that may be even better than current DSL/Cable offers)

• Audio/Video– Media content download &

streaming via PCs & laptops

• Voice– VoIP with WiMax phones & other

portable devices– Soft hand-offs between WiMax and

Cellular with dual mode phones

• Data– Broadband access via laptops &

other portable devices (range ofspeed that is better than near future 3G offers)

• Audio/Video– Media content download &

streaming via laptops, otherportable devices, car units

– Audio/video broadcasting tolaptops, other portable devices, car units

DSL and Cable Substitute(Fixed Broadband)

Figure 5

WiMAX Market Forecast and

Economics

WiMAX will enable two types of broadband offers—a fixed broadband offer as a substitute to DSL and Cable and a mobile broadband offer as an upgrade to 3G.

8

these 66 PRIZM Clusters into nine categories based on income and geography. Low income segments have household incomes ranging from $15,000 to $25,000 (33 and 55 percent of the national average of about $45,000) while wealthy segments have incomes exceeding $65,000 (44 percent of the national average).

Urban segments include those living near the urban cores of large metropolitan areas such as New York or Portland, Oregon. Rural segments encompass those living in small towns, farms or ranches. Suburban segments cover everyone in between, including not only stereotypical suburbanites but also residents of

mid-size cities such as Birmingham, Alabama or Missoula, Montana, who may live near city centers, and residents of “exurbs,” typically tract housing developments rising at the margins of metropolitan areas. Figure 7 shows the market sizes of each of these nine super-segments derived from the PRIZM Clusters.

Potential WiMAX Market Clusters: Demotraphic Descriptions

Low Income Medium Income High Income

Rural

Suburban

Urban

• “Money and Brains”–Marriedcouples with high incomesand sophisticated tastes

Rural Poor (RP) Rural Middle (RM) Rural Rich (RR)

Suburban Poor (SP) Suburban Middle (SM) Suburban Rich (SR)

Urban Poor (UP) Urban Middle (UM) Urban Rich (UR)

• “Young Digerati”–Tech-savvysingles and couples living infashionable neighborhoods

• “Bohemian Mix”–Progressive, young singles and couples,students and professionals

• “The Cosmopolitans”– Affluent, hard-working,typically immigrant families

• “Urban Elders”–Ethnically- mixed, low-income apartmentrenters in large inner cities

• “Low-Rise Living”–Very poor, young, ethnically diversesingles and single parents

• “Second City Elite”–Wealthy highly educated elites ofAmerica’s satellite cities

• “Country Squires”–Wealthyfamilies living in newly-builtexurban “McMansions”

• “Greenbelt Sports”–Middle-class exurban couples with ataste for outdoor activities

• “Red, White & Blues”–Blue- collar residents of exurbantowns rapidly suburbanizing

• “City Startups”–Young, multi-ethnic singles living in apartments in satellite cities

• “Hometown Retired”–Pension- dependent seniors living inaging suburban homes

•“Big Fish, Small Pond”–Older, upper-class leaders of theirsmall-town communities

• “Big Sky Families”–Young rural families with high schooleducations and blue-collar jobs

• “Shotguns & Pickups”– Working-class couples withlarge families and small homes

• “Bedrock America”–Young,economically challengedfamilies in isolated towns

• “Crossroads Villagers”– Middle-aged, blue collarfamilies who hunt and fish

Figure 6

Sizing of WiMAX Market Clusters

0%

20%

40%

60%

80%

100%

High

Income Level

Medium Low

35M HHs = 88M POPs

% of Total Householdsin the Locality

Rural

RP (13.8M HHs, 31.9M POPs, $24K)

RM (18.7M HHs, 50.5M POPs, $43K)

RR (2.5M HHs, 5.6M POPs, $68K)

SP (10.0M HHs, 23.6M POPs, $22K)

SM (31.5M HHs, 85.0M POPs, $46K)

SR (15.6M HHs, 50.0M POPs, $77K)

UP (5.6M HHs,13.1M POPs, $21K)

UM (11.0M HHs,28.0M POPs, $40K)

UR (3.7M HHs,10.0M POPs, $68K)

57M HHs = 159M POPs 20M HHs = 51M POPsSuburban Urban

Note: Figures in parentheses represent total households, total population and median household income for each segment.

Sources: Claritas, US Census, Diamond analysis.

Figure 7

Profiles of the 9 potential WiMAX market clusters can be described in terms of the granular segments allocated to each cluster. The use of these clusters enables a bottom-up calculation of WiMAX addressable market size through proxy variables such as Internet and mobile data penetration.

Rural and Suburban together account for 82% of the total US households, and Suburban Middle is the single biggest segment with over 31M households.

9

Total Addressable Market We used broadband and mobile data penetrations of each PRIZM Cluster to estimate the potential addressable market for fixed and mobile WiMAX respectively. Figure 8 shows the weighted average broadband and mobile data penetrations for the nine groups we have defined based on income and urbanicity. These numbers represent the share of households that subscribe to broadband Internet services, or, in the case of mobile data, individuals that frequently browse the wireless Web or download content. All nine groups show generally increasing penetration in correlation with their income level and degree of urbanicity. One exception to note is that broadband subscription rates among middle and upper income urban households are lower than those

of their suburban counterparts. This may be explained by urbanites’ greater access to free Internet services, whether by benefit of free public WiFi networks, neighbors’ unsecured networks, or by inclusion of broadband in apartment rental or condominium maintenance fees.

Figure 8 also shows the growth forecasts for each of the groups, derived from market research projections for household-level broadband and mobile data penetrations. We used these growth forecasts to calculate the total addressable market for WiMAX (see Figure 9), assuming that the potential universe of fixed and mobile WiMAX users will be a sub-set of the total number of broadband and mobile data users. This high-level calculation yields addressable markets of 87 million households for fixed WiMAX

and 161 million people for mobile WiMAX. Of course, these total addressable markets comprise a range of customer segments much broader than the core groups that WiMAX operators will likely target.

Fixed WiMAX will have a difficult time competing against cable and DSL in urban and suburban geographies, and mobile WiMAX will not be attractive to ”light-data” users. In fact, the value proposition of fixed and mobile WiMAX services will rise significantly for those customer segments that can derive more utility from WiMAX than from existing competitive alternatives. Such customers could include dial-up Internet users in far-flung geographies not touched by broadband networks or EV-DO/HSDPA aircard subscribers who desire a faster service at lower cost.

Potential WiMAX Market Clusters Penetration Rates and Forecast

Low Income Medium Income High Income

Rural

Suburban

Urban

Rural Poor (RP) Rural Middle (RM) Rural Rich (RR)

Suburban Poor (SP) Suburban Middle (SM) Suburban Rich (SR)

Urban Poor (UP) Urban Middle (UM) Urban Rich (UR)

0%Broadband Mobile Data

100%

25%

50%

75%

0%Broadband Mobile Data

100%

25%

50%

75%

0%Broadband Mobile Data

100%

25%

50%

75%

0%Broadband Mobile Data

100%

25%

50%

75%

0%Broadband Mobile Data

100%

25%

50%

75%

0%Broadband Mobile Data

100%

25%

50%

75%

0%Broadband Mobile Data

100%

25%

50%

75%

0%Broadband Mobile Data

100%

25%

50%

75%

0%Broadband Mobile Data

100%

25%

50%

75%

20062011

37%54%

13%31%

46%

68%

20%

48%

44%64% 62%

26%

41%60%

16%38%

54%

80%

23%

56%

53%

78%65%

27%

50%

73%

13%32%

63%

92%

27%

64%

61%

90%78%

33%

Sources: Indexing of clusters from Claritas; Baseline figures from Forrester and Technology Futures (Internet and BB), Telephia and Diamond (mobile data).

Figure 8

At an aggregate level, broadband penetration will increase from 50% of US households in 2006 to 73% in 2011 while mobile data penetration will grow from 21% to 52% of the population.

10

WiMAX Share of Addressable Market The current absence of clearly defined business models or service provision strategies clouds any effort to dictate how fixed and mobile WiMAX will be received in the US market. However, there are some guiding benchmarks within the telecom industry that may facilitate an understanding of the potential market shares fixed and mobile WiMAX may achieve.

The introduction of digital satellite television service in the 1990s serves as a proxy for fixed WiMAX. Competing against cable companies, satellite operators, led by DirecTV and EchoStar, captured 12.5 percent of the US pay-TV market five years after launching commercial services. Similarly, the launch of Hutchison 3, the first greenfield 3G operator in the United Kingdom, serves as a proxy

for mobile WiMAX. Hutchison is projected and is close to capturing 8 percent of the competitive UK mobile market in the five years since its launch in March 2003. While these examples are only indicative of what fixed and mobile WiMAX may achieve, they demonstrate how new technologies can produce a competitive and differentiated offering and rapidly grab an important slice of the market in industries previously dominated by other technologies and players.

Breakeven Costs for Network Operators We can project breakeven costs for potential WiMAX operators, since breakeven capital investment can be determined as a function of addressable market penetration. For example, if a provider captures 10 percent of its addressable market, then to break even,

its per-subscriber cost of deploying WiMAX should not exceed one-tenth of the average lifetime value of its subscriber. Each penetration rate will determine a breakeven point to deploy WiMAX on a household or POP basis, as illustrated in Figure 10. Using DSL and EV-DO, respectively, as benchmarks to support CPGA, ARPU, CCPU, and churn assumptions for fixed and mobile WiMAX, we estimate lifetime values of $411 for a fixed WiMAX household and $625 for a mobile WiMAX subscriber.

Assuming the satellite TV and Hutchison 3 benchmarks provide reasonable market penetration forecasts for WiMAX, we can project breakeven costs for potential WiMAX network operators. For fixed WiMAX, we use the 12.5 percent combined market share of DirecTV and EchoStar to estimate that a single fixed WiMAX operator may capture

Total Addressable Market for WiMAX

Fixed Mobile

Rural

Suburban

Urban

Total161M People

(52% of US Population)87M Households

(73% of US Households)

21.8M Households

• Total Households (2011): 36.9M• Broadband HH Penetration (2011): 59%

31.3M People

• Total Population (2011): 92.1M• Mobile Data Pop. Penetration (2011): 34%

94.6M People

35.3M People16.3M Households

48.8M Households

• Total Households (2011): 60.2M• Broadband HH Penetration (2011): 81%

• Total Population (2011): 166.0M• Mobile Data Pop. Penetration (2011): 57%

• Total Households (2011): 21.4M• Broadband HH Penetration (2011): 76%

• Total Population (2011): 53.5M• Mobile Data Pop. Penetration (2011): 66%

Figure 9

WiMAX will compete with other technologies for shares of the US broadband households and mobile data users—estimated at 87M households and 161M people.

11

6.25 percent of its addressable market. For mobile WiMAX, we assume the 8 percent share of Hutchison 3. At 6.25 percent market share, a fixed WiMAX operator may maintain a positive business case if it can limit capital investments to $26 per addressable household. Similarly, at 8 percent market

share, a mobile WiMAX operator may invest up to $50 per addressable POP before becoming unprofitable. Next, we must modify these values to accommodate the fact that operators must deploy networks to cover entire populations, not just addressable markets. Addressable markets for fixed and

mobile WiMAX correspond to 73 percent of households and 52 percent of the population, respectively (as noted in Figure 9). As a result, the adjusted per-subscriber breakeven costs are $19 for fixed WiMAX and $26 for mobile WiMAX.

Breakeven WiMAX Costs for Network Operators

Fixed WiMAX Mobile WiMAX

0%

10%

20%

30%

40%

WiMAX Share of theAddressable Market

25 50 75 100 125 150 175 200

($26, 6.3%)

Note: Since fixed WiMAX would primarily compete with DSL, an averageDSL household’s metrics were used as a baseline to estimate a lifetimevalue of a fixed WiMAX household ($411). Calculation is based on $250CPGA, $25 ARPU, 65% gross margin and 2.0% churn. CPGA includes$100 marketing, $50 subsidy and $100 distribution.

Breakeven Cost per Addressable HH

0%

10%

20%

30%

40%

WiMAX Share of theAddressable Market

25 50 75 100 125 150 175 200

($50, 8.0%)

Note: Since mobile WiMAX would largely compete with 3G, an averageDSL household’EV-DO subscriber’s metrics were used as a baseline to estimate a lifetime value of a mobile WiMAX subscriber ($625). Calculation is based on $400 CPGA, $50 ARPU, 60% gross margin and 2.5% churn. CPGA includes $50 marketing, $200 subsidy and $150 distribution.

Breakeven Cost per Addressable POP

Sources: Bear Stearns, JP Morgan, Diamond analysis.

Profitable at 6.3% market shareUnprofitable at 6.3% market share

Profitable at 8.0% market shareUnprofitable at 8.0% market share

Figure 10

Assuming benchmarks to guide reasonable market share for WiMAX, WiMAX providers may have a positive business case if they can limit CAPEX to $26 per addressable household for fixed WiMAX and to $50 per addressable POP for mobile WiMAX.

12

Fixed and mobile WiMAX present a wide range of potential business opportunities for different types of communications and content providers. Fixed-line incumbents, wireless-focused players, cable operators, satellite television service providers, local exchange carriers, mobile virtual network operators, VoIP providers, Web portals, and media companies each have an opportunity to exploit fixed or mobile WiMAX to create incremental revenues, either through direct investments or through partnerships with WiMAX network operators. However, before committing to WiMAX investments, each

of these players must answer critical questions about the specific value of WiMAX to their core business and long-term offer strategies.

In this section, we describe the key WiMAX opportunities facing different types of communications and media players. For each set of players, we list the key strategic questions they need to address before pursuing a WiMAX play. Finally, we specify the prioritized types of WiMAX service (fixed or mobile) and geographies (urban, suburban or rural) for each category of service providers (see Figure 11).

Implications for Service Providers

Priority WiMAX Offers and Markets

RBOCs Satellite Operators

RLECs

MVNOs

VoIP Providers

Web Portals

Media Companies

F: 71M HHM: 130M POP

M F

S

R

U

M:

F:M:

Wireless Players

Cable Operators

M F

S

R

U

M F

S

R

U

M F

S

R

U

M F

S

R

U

M F

S

R

U

M F

S

R

U

M F

S

R

U

M F

S

R

U

F: 65M HHM: 130M POP

M: 130M POP

F: 65M HH

65M HH130M POP

M: 130M POP

F: 87M HH

F: 71M HH

130M POP

Source: Diamond analysis.

High

Priority Level

Medium Low

Figure 11

13

Fixed/Wireless Incumbents The RBOCs could deploy fixed WiMAX as a DSL substitute in areas of limited DSL coverage. For example, BellSouth, prior to the merger with AT&T, was planning to use WiMAX as one way to reach the 16 percent of the households in its service area that currently do not have DSL access. RBOCs with integrated wireless operations (e.g. AT&T, BellSouth, and Verizon) could also provide mobile WiMAX as an extension of their current fixed broadband and mobile data service offerings. In addition, they could leverage mobile WiMAX to offload data traffic from 3G networks in congested metropolitan areas.

• What is the return on investment of fixed WiMAX as a replacement for DSL in rural areas?

• Will the market demand for mobile data be large enough to support mobile WiMAX as well as 3G networks?

• What is the effect of WiMAX cannibalization on existing 3G networks?

• Can integrated RBOC/wireless carriers wait for substitute technologies such as RevC and LTE, or does mobile WiMAX carry a substantial time-to-market advantage?

• Will integrated RBOC/wireless carriers have enough spectrum to deploy WiMAX? Can they leverage AWS spectrum as an option?

Wireless-focused Players Wireless-focused players could provide bundles of fixed WiMAX and mobile voice and data from their 3G networks. They could also deploy mobile WiMAX as an extension of their current 3G services and leverage it to offload traffic from 3G networks in metropolitan areas. Sprint would be the leading case study for these players.

Strategic Questions for Fixed/Wireless Incumbents

• Can fixed WiMAX compete against DSL and Cable broadband price points?

• Will the market demand for mobile data be large enough to support mobile WiMAX as well as 3G networks?

• What is the effect of WiMAX cannibalization on existing 3G networks?

• Can wireless operators wait for substitute technologies such as RevC and LTE, or does mobile WiMAX carry a substantial time-to-market advantage?

• What are the spectrum options to deploy WiMAX? In addition to 2.5GHz, is AWS spectrum an option?

Strategic Questions for Wireless-focused Players

Cable Operators Cable operators could provide fixed WiMAX as a cable broadband replacement in areas of limited coverage. Cable operators could also deploy mobile WiMAX as an extension of the fixed voice-video-broadband and/or mobile voice and data service offering they are launching through their joint venture with Sprint. In addition, they could leverage mobile WiMAX to offload their data traffic from Sprint and potentially voice traffic as well in the long term.

• What is the ROI of fixed WiMAX as a replacement for cable broadband in rural and suburban areas?

• Will the market demand for mobile data be large enough to support mobile WiMAX as well as 3G networks?

• Can cable operators reduce their dependency on Sprint with mobile WiMAX? Can it replace 3G mobile services?

• Can cable operators lease WiMAX from Sprint and Clearwire, or should they build their own network?

• Can cable operators leverage their AWS spectrum?

• What are the alternative wireless technologies for the AWS spectrum, and what is the best option?

Strategic Questions for Cable Operators

14

Satellite Service Providers The broadband and mobile service ambitions of satellite providers DirecTV and EchoStar were significantly undermined after their failure to place a winning bid at the AWS spectrum auction. However, the satellite providers could still enter the WiMAX picture through partnerships with other spectrum holders. They could add fixed WiMAX to the core satellite TV offer, thereby enabling a triple-play based on TV, broadband and VoIP. They could also leverage fixed WiMAX to offer Video-on- Demand to their customers, thereby reducing a competitive gap with the cable operators. Alternatively, satellite providers could compete against the cable-Sprint JV by leveraging mobile WiMAX to bundle wireless broadband services with their core TV offers.

• Can satellite operators compete against the cable operators without a triple-play/VOD offer?

• Can fixed WiMAX compete against DSL and Cable broadband price points?

• Can fixed WiMAX provide the bandwidth necessary to deliver video-on-demand economically?

• Can satellite operators lease WiMAX from Sprint or Clearwire?

• Is it too late for satellite operators to acquire spectrum to deploy WiMAX? What are their options?

• What are the alternative wireless technologies, and what is the best option?

Local Exchange Carriers Reseller Local Exchange Carriers could emulate the RBOCs by providing fixed WiMAX as a DSL replacement in areas of limited DSL coverage. They could also leverage fixed WiMAX to step up competition against the RBOCs to include neighborhoods outside of their current wireline footprint. In addition, they could look to mobile WiMAX to provide a wireless extension to their current wireline voice and data services. If local exchange carriers such as Embarq deploy their own mobile WiMAX networks, they could also leverage mobile WiMAX to offload their data traffic from mobile network operators and potentially voice traffic as well in the long run.

Strategic Questions for Satellite Service Providers

• What is the ROI of fixed WiMAX as a replacement for DSL in rural or suburban areas?

• Can RLEC MVNOs such as Embarq leverage mobile WiMAX to reduce dependency on their network hosts which lease them 3G network access? Can mobile WiMAX substitute 3G voice and/or data services?

• Can RLECs lease WiMAX from Sprint and Clearwire?

• Do RLECs have enough scale to acquire spectrum and deploy a WiMAX network? What spectrum options are available to them?

• What are the alternative wireless technologies?

Strategic Questions for Local Exchange Carriers

15

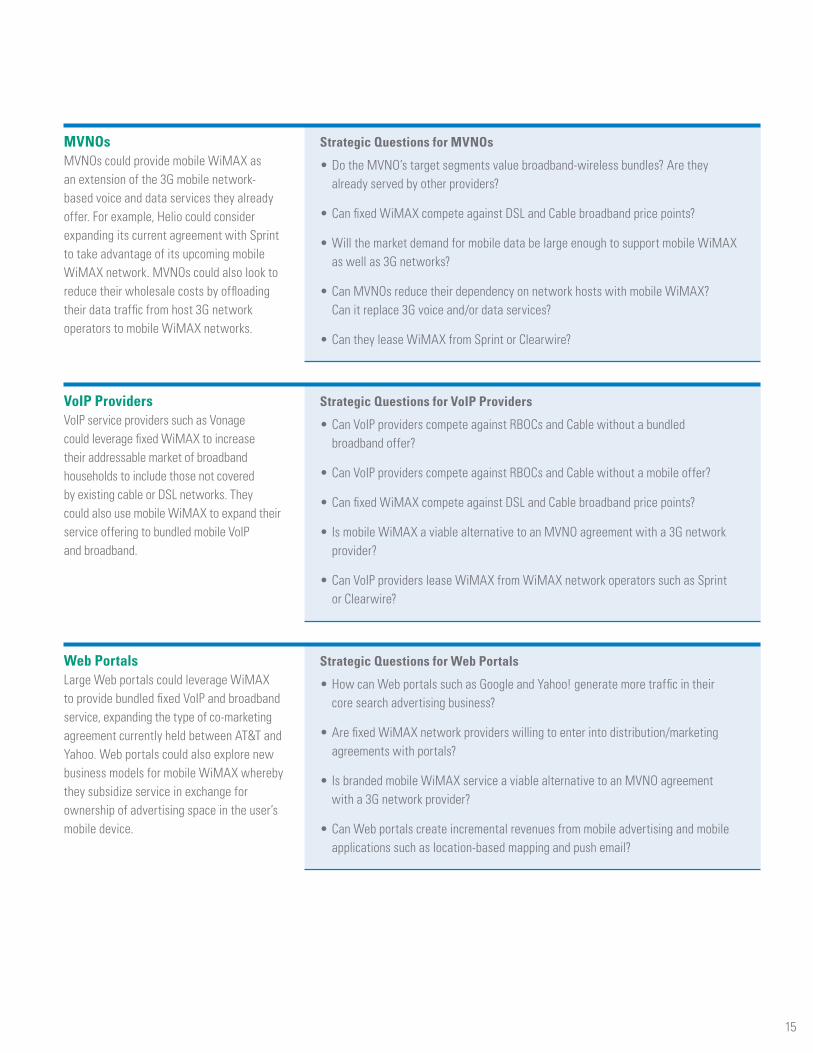

MVNOs MVNOs could provide mobile WiMAX as an extension of the 3G mobile network-based voice and data services they already offer. For example, Helio could consider expanding its current agreement with Sprint to take advantage of its upcoming mobile WiMAX network. MVNOs could also look to reduce their wholesale costs by offloading their data traffic from host 3G network operators to mobile WiMAX networks.

• Do the MVNO’s target segments value broadband-wireless bundles? Are they already served by other providers?

• Can fixed WiMAX compete against DSL and Cable broadband price points?

• Will the market demand for mobile data be large enough to support mobile WiMAX as well as 3G networks?

• Can MVNOs reduce their dependency on network hosts with mobile WiMAX? Can it replace 3G voice and/or data services?

• Can they lease WiMAX from Sprint or Clearwire?

VoIP Providers VoIP service providers such as Vonage could leverage fixed WiMAX to increase their addressable market of broadband households to include those not covered by existing cable or DSL networks. They could also use mobile WiMAX to expand their service offering to bundled mobile VoIP and broadband.

Strategic Questions for MVNOs

• Can VoIP providers compete against RBOCs and Cable without a bundled broadband offer?

• Can VoIP providers compete against RBOCs and Cable without a mobile offer?

• Can fixed WiMAX compete against DSL and Cable broadband price points?

• Is mobile WiMAX a viable alternative to an MVNO agreement with a 3G network provider?

• Can VoIP providers lease WiMAX from WiMAX network operators such as Sprint or Clearwire?

Strategic Questions for VoIP Providers

Web Portals Large Web portals could leverage WiMAX to provide bundled fixed VoIP and broadband service, expanding the type of co-marketing agreement currently held between AT&T and Yahoo. Web portals could also explore new business models for mobile WiMAX whereby they subsidize service in exchange for ownership of advertising space in the user’s mobile device.

• How can Web portals such as Google and Yahoo! generate more traffic in their core search advertising business?

• Are fixed WiMAX network providers willing to enter into distribution/marketing agreements with portals?

• Is branded mobile WiMAX service a viable alternative to an MVNO agreement with a 3G network provider?

• Can Web portals create incremental revenues from mobile advertising and mobile applications such as location-based mapping and push email?

Strategic Questions for Web Portals

16

Media Companies Media content developers (e.g. Time Warner, Sony, Disney, News Corp, etc.) could leverage mobile WiMAX to enable wireless delivery of proprietary content such as music and video clips, while content aggregators (e.g. Apple iTunes and Xbox Live) could use it to make their libraries available anytime, anywhere to a much broader audience. While content owners could encourage adoption of services through various agreements with traditional WiMAX network operators, content aggregators could enter into network-leasing agreements to directly offer mobile service, thereby integrating wireless access subscriptions with their existing content libraries and proprietary mobile devices.

• Will WiMAX-enabled consumer electronics devices be widely available?

• Can WiMAX deliver a cost structure low enough to be competitive with fixed broadband access?

• Are fixed and mobile WiMAX network providers willing to enter into distribution/marketing agreements with content developers and aggregators?

• Can video content developers leverage WiMAX to dis-intermediate cable operators for video entertainment distribution?

• Can media companies compete against wireless carriers for a larger share of wireless media and entertainment revenues, leveraging their own distribution platform based on WiMAX?

Strategic Questions for Media Companies

17

WiMAX is a disruptive technology that, in the next few years, will compete against existing broadband as well as wireless technologies for a share of US consumers’ communications budgets. Two operators—Clearwire and Sprint—have already committed to bringing fixed and mobile WiMAX coverage to much of the country by 2008. These players are betting that WiMAX will propel them to the vanguard of broadband wireless services, not only by providing broadband services to underserved customer segments (fixed WiMAX) but also by reducing the current wireless premium in delivering high-bandwidth applications such as mobile media and entertainment and Web browsing (mobile WiMAX). Consequently, incumbent

network operators such as cable, mobile, and satellite companies will need to carefully evaluate how to best position themselves relative to the inevitable WiMAX disruption. Meanwhile, WiMAX may create opportunities for other service providers, such as VoIP providers, MVNOs, Web portals, and media content owners or aggregators. These players will need to

assess whether WiMAX enables mobile data service models that expand beyond their options with 3G networks. Whether threat or opportunity, all classes of telecom and content providers will need to adapt their business strategies to reflect the new competitive and technological realities brought about by the introduction of WiMAX.

Conclusion

18

About the Firm Diamond (NASDAQ: DTPI) is a management and technology consulting firm. Recognizing that information and technology shape market dynamics, Diamond’s small teams of experts work across functional and organizational boundaries to improve growth and profitability. Since the greatest value in a strategy, and its highest risk, resides in its implementation, Diamond also provides proven execution capabilities. We deliver three critical elements to every project: fact-based objectivity, spirited collaboration, and sustainable results. To learn more visit www.diamondconsultants.com.

Hamilton Sekino is a Partner in Diamond’s Telecom and High Tech practice. Hamilton has experience across North America, Latin America, Europe, and Asia in launching mobile operators and helping them grow through new technologies, new products, channels, and MVNO programs. He also has experience in generating growth for wireless handset OEMs, infrastructure vendors, and media & entertainment companies through the introduction of new technologies, services, business models, and strategic partnerships with mobile operators.

John Kwon is a Manager in Diamond’s Telecom and High Tech practice with experience across North America, Europe, and Asia in developing wireless operators’ market entry strategies and launching new products and services. His experience also comprises 3G network strategy, operations improvement, customer value management, and MVNO strategy for leading wireless operators as well as market opportunity analysis for a major wireless handset and infrastructure vendor.

David Gates is an Associate in Diamond’s Telecom and High Tech practice. David has experience in customer segmentation, marketing, and pricing strategy for leading wireless operators and alternative wireless providers. David also has expertise in fixed-mobile and telecom-media convergence, and he recently advised a telecom operator on acquisitions in the US media industry.

About the Authors

19

DiamondSuite 3000 John Hancock Center875 North Michigan Ave. Chicago, IL 60611T (312) 255 5000 F (312) 255 6000www.diamondconsultants.com

C H I C A G O • H A R T F O R D • L O N D O N • M U M B A I • N E W Y O R K • W A S H I N G T O N , D . C .

© 2007 Diamond Management & Technology Consultants, Inc. All rights reserved.