inside this report - iifl · let’s explore the loan zone with iiisl... annual report 2010-11 ......

TRANSCRIPT

Standalone Financial Statements20 Auditors’ Report 25 Balance Sheet 26 Profit and Loss Account 27 Schedules

45 Cash Flow Statement 47 Balance Sheet Abstract 48 Statement Relating to Subsidiary Companies

Consolidated Financial Statements49 Auditors’ Report 50 Balance Sheet 51 Profit and Loss Account 52 Schedules

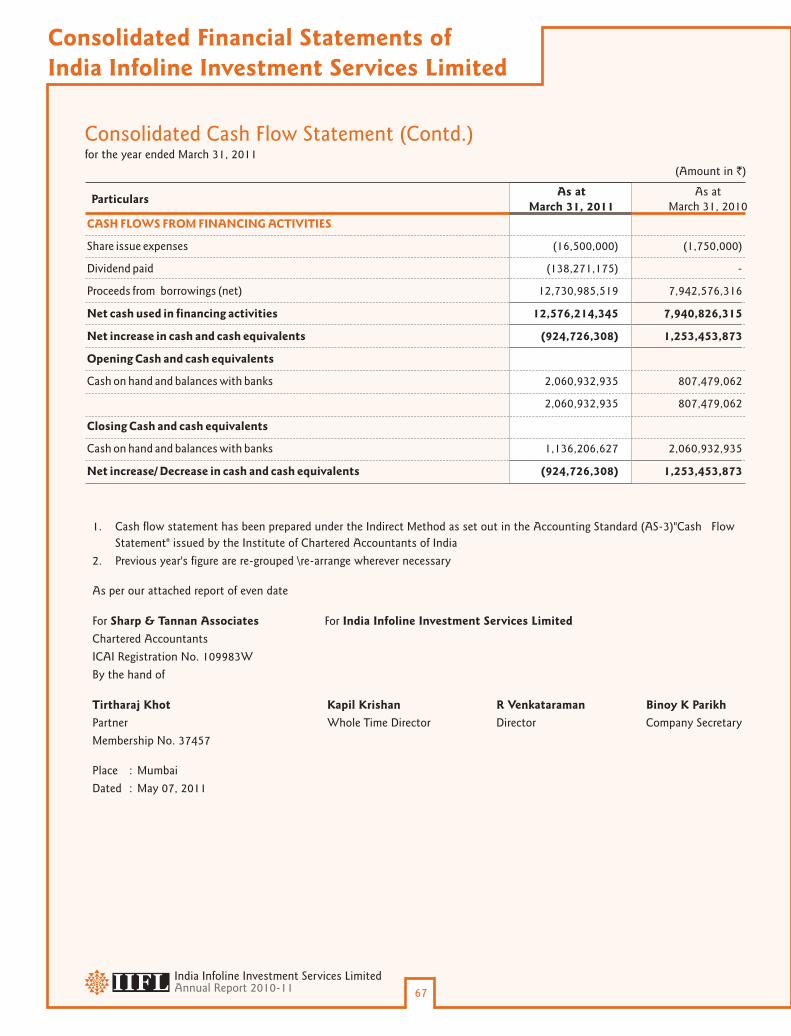

66 Cash Flow Statement

Statutory Reports13 Board of Directors 15 Directors’ Report

An Overview01 Performance Highlights 2010-11 03 Chairmans’ Message 05 Corporate Identity

07 Financial Literacy Campaign

Business Discussion09 Industry Overview 12 Performance Overview

INSIDE THIS REPORT

INDIA INFOLINE INVESTMENT SERVICES LIMITED (IIISL)

ANNUAL REPORT 2010-11Let’s Explore the Loan Zone with IIISL...For you, from IIISL. Retail Loans, Professional Loans, Corporate Loans

Roaming the loan jungle can make strong men weep. Exhaustion and despair get at you when your most sensible requirements are turned down, again and again. Know the feeling?

Now, wave goodbye to darkness and gloom. It’s good morning in the Loan Zone! This is where IIISL lifts you up, and flies you way above the confusions, anxieties and hesitations when exploring loan possibilities; giving you the quick, smooth flexibility you need.

Whether you need a loan against your property or for your home; a loan against your gold, or for the most complex Healthcare Project; even the simplest loan against shares gets our detailed guidance and personal attention.

Call us, we’ll get you on your way, an easy, trouble-free way – so you never get lost again.

Standalone Financial Statements20 Auditors’ Report 25 Balance Sheet 26 Profit and Loss Account 27 Schedules

45 Cash Flow Statement 47 Balance Sheet Abstract 48 Statement Relating to Subsidiary Companies

Consolidated Financial Statements49 Auditors’ Report 50 Balance Sheet 51 Profit and Loss Account 52 Schedules

66 Cash Flow Statement

Statutory Reports13 Board of Directors 15 Directors’ Report

An Overview01 Performance Highlights 2010-11 03 Chairmans’ Message 05 Corporate Identity

07 Financial Literacy Campaign

Business Discussion09 Industry Overview 12 Performance Overview

INSIDE THIS REPORT

INDIA INFOLINE INVESTMENT SERVICES LIMITED (IIISL)

ANNUAL REPORT 2010-11Let’s Explore the Loan Zone with IIISL...For you, from IIISL. Retail Loans, Professional Loans, Corporate Loans

Roaming the loan jungle can make strong men weep. Exhaustion and despair get at you when your most sensible requirements are turned down, again and again. Know the feeling?

Now, wave goodbye to darkness and gloom. It’s good morning in the Loan Zone! This is where IIISL lifts you up, and flies you way above the confusions, anxieties and hesitations when exploring loan possibilities; giving you the quick, smooth flexibility you need.

Whether you need a loan against your property or for your home; a loan against your gold, or for the most complex Healthcare Project; even the simplest loan against shares gets our detailed guidance and personal attention.

Call us, we’ll get you on your way, an easy, trouble-free way – so you never get lost again.

PERFORMANCE HIGHLIGHTS (Consolidated) 2010-11

AN

OV

ER

VIE

W

India Infoline Investment Services LimitedAnnual Report 2010-11

(` bn)

1.6

07-08 08-09 09-10 10-11

2.4 2.3

5.2

Revenue

(` mn) (`) (`)

Net Interest Income

07-08 08-09 09-10

781.3

1,847.81,957.0

Earning per Share

1.6

2.9

2.3

3.9

07-08 08-09 09-10 10-11

Book Value per Share

07-08 08-09 09-10 10-11

47.9

51.1

53.3

56.6

10-11

2,505.1

(` mn)

922.5

Profit after Tax

239.4

07-08 08-09 09-10 10-11

691.2

537.9

(` bn)

07-08 08-09 09-10

11.4

12.1

12.6

Net Worth Loan Outstanding

(` bn) (%)

Mar 31`08 Mar 31 09` Mar 31 10` Mar 31 11`

9.4 9.6

16.3

32.9

10-11

13.4

NPA

07-08 08-09 09-10 10-11

0.90

0.08

0.60

0.44

0.71

-0.09

0.45

0.36

Bu

siness D

iscussio

nFin

an

cial S

tate

men

tsSta

tuto

ry R

ep

orts

1 2

Gross NPANet NPA

PERFORMANCE HIGHLIGHTS (Consolidated) 2010-11

AN

OV

ER

VIE

W

India Infoline Investment Services LimitedAnnual Report 2010-11

(` bn)

1.6

07-08 08-09 09-10 10-11

2.4 2.3

5.2

Revenue

(` mn) (`) (`)

Net Interest Income

07-08 08-09 09-10

781.3

1,847.81,957.0

Earning per Share

1.6

2.9

2.3

3.9

07-08 08-09 09-10 10-11

Book Value per Share

07-08 08-09 09-10 10-11

47.9

51.1

53.3

56.6

10-11

2,505.1

(` mn)

922.5

Profit after Tax

239.4

07-08 08-09 09-10 10-11

691.2

537.9

(` bn)

07-08 08-09 09-10

11.4

12.1

12.6

Net Worth Loan Outstanding

(` bn) (%)

Mar 31`08 Mar 31 09` Mar 31 10` Mar 31 11`

9.4 9.6

16.3

32.9

10-11

13.4

NPA

07-08 08-09 09-10 10-11

0.90

0.08

0.60

0.44

0.71

-0.09

0.45

0.36

Bu

siness D

iscussio

nFin

an

cial S

tate

men

tsSta

tuto

ry R

ep

orts

1 2

Gross NPANet NPA

AN

OV

ER

VIE

W

CHAIRMANS’ MESSAGE

The Indian economy recorded a robust 8.5% growth in 2010-

11, driven by 9.4% growth in services sector. Manufacturing and

agriculture also witnessed growth rates of 8.3% and 6.6%

respectively. After a fast recovery from the global credit crisis of

2008, India remains one of the fastest growing economies in the

world. Growth is driven primarily by domestic consumption,

high savings and high investment spending. To counter rising

inflation, RBI has resorted to a series of interest rate hikes.

Repo and Reverse repo rates have risen from 5% and 3.5% to

6.75% and 5.7% respectively over the last 12 months. Interest

rates however, continue under upward pressure.

The confidence in India's future growth is founded on

favourable demographics-a rapidly expanding young

population with a propensity to earn more and spend well.

With a large number of new young wage earners, there is a big

latent demand for credit as well, due to changing mindset and

availability of opportunities.

NBFCs, which serve the vital credit needs of under-served

sectors like small and medium enterprises, emerged more or

less unscathed in the financial turmoil of 2008, thanks to a robust

framework in which they operate. In fact, the NBFCs have

witnessed healthy growth after the crisis faced by the entire sector

in the late 90s, which led to a revamp in the regulatory framework

of the sector.

This sector plays a complementary role in distribution of

credit to various segments of the population and geographies

where banks are under-penetrated. Most of the NBFCs have

created a cost effective structure for distribution of credit. Over the

years, they have developed their own credit evaluation skills and

have put in place robust risk management systems as well as asset

liability management. NBFCs also have the unique ability to handle

small amounts of cash disbursals and cash collections. For the

economy which is on rapid growth path, the need for financing

different types of risks will continue. Given their size, scale and

complexity, NBFCs play a nation-building role as it facilitates

various economic activities by making credit available.

Compared to banks, the cost of funds for NBFCs is higher,

because they do not have access to low cost deposits, and

therefore they specialize in meeting the requirements of

relatively higher risk assets. NBFCs play the role of the

intermediary where they originate their assets that meet

required specifications and complement the bank's efforts to

reach out to deliver the credit at an affordable cost, bringing

about an all-round economic development starting from the

bottom of the pyramid; and all this at affordable rates. Any

regulatory framework must afford flexibility to the system to

meet these objectives in a systematic and prudent manner.

Last year, your Company doubled its loan portfolio, which rose

from ̀ 16.3 bn as on March 31, 2010 to 32.9 bn as on March

31, 2011. Home loans/ loans against property contributed

about 60% of the portfolio while loan against shares/ margin

financing contributed 35%. Unsecured loans, which we

discontinued in 2008, was about 1% of portfolio, the balance

was contributed by our newly launched gold loans and

medical equipment loans. Our focus will remain on secured

lending, going ahead and we hope to add new lines like loans

to education sector.

In the Indian context, for the next two decades, sectors that

will require flow of debt capital on a large scale include

infrastructure, education and healthcare. The variety,

enormity and complexity of projects in these verticals will

require assistance from the entire financial system, comprising

not just banks but also complemented by NBFCs. Here,

education and healthcare should get covered as infrastructure

as is happening for the Banking system which will allow

certain tax concessions and external borrowing to ensure

rapid and healthy growth of these vital sectors. These

investments have to be made for the country to enjoy the

demographic dividend of a young population.

`

I believe that demand for housing in India will remain robust

for many years, with the overall standard of living improving

and rapid growth expected to continue. Every Indian deserves

a pakka house over his head and it is sad that penetration of

pakka houses is just about 17%. A house goes a long way in

building not only a physically healthy community but also an

emotionally secure one.

The risk of real estate sector needs to be carefully evaluated.

Prices have doubled only in certain pockets of Mumbai and

Delhi. In the rest of the country, the real estate prices remain

reasonable and affordable and in fact quite competitive. The

real estate sector is important to meet the requirements of

affordable housing as well as for key social infrastructure

facilities and healthcare. It is important to take a wholistic

view on the investment flow to real estate which goes towards

security purpose and social purposes.

In our endeavours to grow our portfolio, we will not

compromise on risk. Your company has built the asset book

steadily without taking undue risk and instead focusing on our

core strength of retail distribution. Our risk management

techniques have been robust and are reflected in the net NPA

being less than 1% of the overall portfolio. We will continue to

invest in risk management, audit and training of our most

important asset, our people.

In spite of short term challenges of rising interest rates, the

long term potential of our business is immense and we will

take all steps to ensure that we grow our book with focus on

building a quality asset portfolio and thus enhance

shareholder's value.

Chairman

A. K. Purwar

The confidence in India's future growth is founded on favourable demographics - a

rapidly expanding young population with a propensity to earn more and spend

well. With a large number of new young wage earners, there is a big latent demand

for credit as well, due to changing mindset and availability of opportunities.

India Infoline Investment Services LimitedAnnual Report 2010-11

Bu

siness D

iscussio

nFin

an

cial S

tate

men

tsSta

tuto

ry R

ep

orts

NBFCs also have the unique

ability to handle small amounts

of cash disbursals and cash

collections. For the economy

which is on rapid growth path,

the need for financing different

types of risks will continue.

Given their size, scale and

complexity, NBFCs play a nation-

building role as it facilitates

various economic activities by

making credit available.

A. K. Purwar, Non-Executive Chairman, IIISL

AN

OV

ER

VIE

W

CHAIRMANS’ MESSAGE

The Indian economy recorded a robust 8.5% growth in 2010-

11, driven by 9.4% growth in services sector. Manufacturing and

agriculture also witnessed growth rates of 8.3% and 6.6%

respectively. After a fast recovery from the global credit crisis of

2008, India remains one of the fastest growing economies in the

world. Growth is driven primarily by domestic consumption,

high savings and high investment spending. To counter rising

inflation, RBI has resorted to a series of interest rate hikes.

Repo and Reverse repo rates have risen from 5% and 3.5% to

6.75% and 5.7% respectively over the last 12 months. Interest

rates however, continue under upward pressure.

The confidence in India's future growth is founded on

favourable demographics-a rapidly expanding young

population with a propensity to earn more and spend well.

With a large number of new young wage earners, there is a big

latent demand for credit as well, due to changing mindset and

availability of opportunities.

NBFCs, which serve the vital credit needs of under-served

sectors like small and medium enterprises, emerged more or

less unscathed in the financial turmoil of 2008, thanks to a robust

framework in which they operate. In fact, the NBFCs have

witnessed healthy growth after the crisis faced by the entire sector

in the late 90s, which led to a revamp in the regulatory framework

of the sector.

This sector plays a complementary role in distribution of

credit to various segments of the population and geographies

where banks are under-penetrated. Most of the NBFCs have

created a cost effective structure for distribution of credit. Over the

years, they have developed their own credit evaluation skills and

have put in place robust risk management systems as well as asset

liability management. NBFCs also have the unique ability to handle

small amounts of cash disbursals and cash collections. For the

economy which is on rapid growth path, the need for financing

different types of risks will continue. Given their size, scale and

complexity, NBFCs play a nation-building role as it facilitates

various economic activities by making credit available.

Compared to banks, the cost of funds for NBFCs is higher,

because they do not have access to low cost deposits, and

therefore they specialize in meeting the requirements of

relatively higher risk assets. NBFCs play the role of the

intermediary where they originate their assets that meet

required specifications and complement the bank's efforts to

reach out to deliver the credit at an affordable cost, bringing

about an all-round economic development starting from the

bottom of the pyramid; and all this at affordable rates. Any

regulatory framework must afford flexibility to the system to

meet these objectives in a systematic and prudent manner.

Last year, your Company doubled its loan portfolio, which rose

from ̀ 16.3 bn as on March 31, 2010 to 32.9 bn as on March

31, 2011. Home loans/ loans against property contributed

about 60% of the portfolio while loan against shares/ margin

financing contributed 35%. Unsecured loans, which we

discontinued in 2008, was about 1% of portfolio, the balance

was contributed by our newly launched gold loans and

medical equipment loans. Our focus will remain on secured

lending, going ahead and we hope to add new lines like loans

to education sector.

In the Indian context, for the next two decades, sectors that

will require flow of debt capital on a large scale include

infrastructure, education and healthcare. The variety,

enormity and complexity of projects in these verticals will

require assistance from the entire financial system, comprising

not just banks but also complemented by NBFCs. Here,

education and healthcare should get covered as infrastructure

as is happening for the Banking system which will allow

certain tax concessions and external borrowing to ensure

rapid and healthy growth of these vital sectors. These

investments have to be made for the country to enjoy the

demographic dividend of a young population.

`

I believe that demand for housing in India will remain robust

for many years, with the overall standard of living improving

and rapid growth expected to continue. Every Indian deserves

a pakka house over his head and it is sad that penetration of

pakka houses is just about 17%. A house goes a long way in

building not only a physically healthy community but also an

emotionally secure one.

The risk of real estate sector needs to be carefully evaluated.

Prices have doubled only in certain pockets of Mumbai and

Delhi. In the rest of the country, the real estate prices remain

reasonable and affordable and in fact quite competitive. The

real estate sector is important to meet the requirements of

affordable housing as well as for key social infrastructure

facilities and healthcare. It is important to take a wholistic

view on the investment flow to real estate which goes towards

security purpose and social purposes.

In our endeavours to grow our portfolio, we will not

compromise on risk. Your company has built the asset book

steadily without taking undue risk and instead focusing on our

core strength of retail distribution. Our risk management

techniques have been robust and are reflected in the net NPA

being less than 1% of the overall portfolio. We will continue to

invest in risk management, audit and training of our most

important asset, our people.

In spite of short term challenges of rising interest rates, the

long term potential of our business is immense and we will

take all steps to ensure that we grow our book with focus on

building a quality asset portfolio and thus enhance

shareholder's value.

Chairman

A. K. Purwar

The confidence in India's future growth is founded on favourable demographics - a

rapidly expanding young population with a propensity to earn more and spend

well. With a large number of new young wage earners, there is a big latent demand

for credit as well, due to changing mindset and availability of opportunities.

India Infoline Investment Services LimitedAnnual Report 2010-11

Bu

siness D

iscussio

nFin

an

cial S

tate

men

tsSta

tuto

ry R

ep

orts

NBFCs also have the unique

ability to handle small amounts

of cash disbursals and cash

collections. For the economy

which is on rapid growth path,

the need for financing different

types of risks will continue.

Given their size, scale and

complexity, NBFCs play a nation-

building role as it facilitates

various economic activities by

making credit available.

A. K. Purwar, Non-Executive Chairman, IIISL

CORPORATE IDENTITY

India Infoline Investment Services LimitedAnnual Report 2010-11

VISIONTo become the Most Respected Company in the financial services space in India.

Team IIFL adheres to a set of values that can be summarized as GIFTS, namely, Growth, Integrity, Fairness, Transparency and Service

VALUES

GROWTH

We are driven to grow faster than the rest of the industry. The

culture therefore encourages calculated risks and

empowerment at all levels.

We ensure utmost honesty and integrity, in letter and in spirit,

in all our dealings with people – internal or external.

We believe in fair dealings, devoid of any fear or favor, with all

stakeholders including employees, customers and vendors.

INTEGRITY

FAIRNESS

TRANSPARENCY

We believe in as much transparency as practically possible, with

our stakeholders, media and public at large.

We are a service organization, committed to delight our

customers with superior advice and service, delivered with

humility and sincerity.

SERVICE

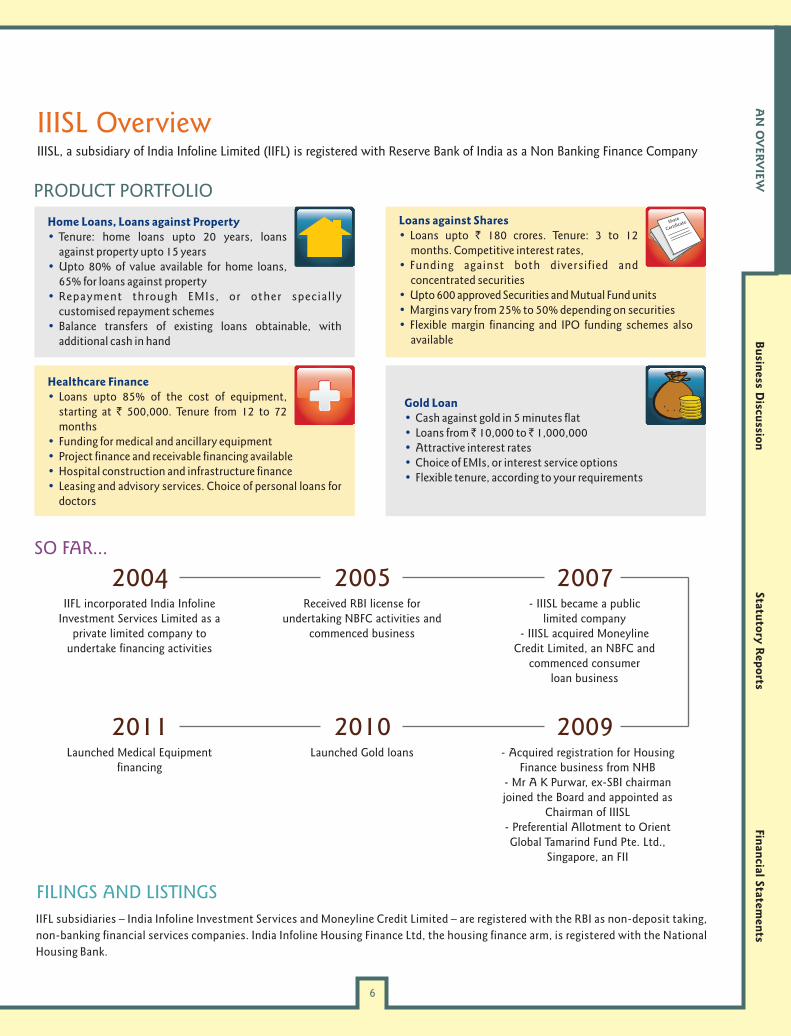

IIISL OverviewIIISL, a subsidiary of India Infoline Limited (IIFL) is registered with Reserve Bank of India as a Non Banking Finance Company

IIFL Group

3000+Business locations

across India

1+ million customers

across various businesses

10,000+India Infoline team

as on March 31, 2011FILINGS AND LISTINGS

COMPREHENSIVE PORTFOLIO

IIFL subsidiaries – India Infoline Investment Services and Moneyline Credit Limited – are registered with the RBI as non-deposit taking,

non-banking financial services companies. India Infoline Housing Finance Ltd, the housing finance arm, is registered with the National

Housing Bank.

Received RBI license for undertaking NBFC activities and

commenced business

Launched Gold loans

2010

- IIISL became a public limited company

- IIISL acquired Moneyline Credit Limited, an NBFC and

commenced consumer loan business

- Acquired registration for Housing Finance business from NHB

- Mr A K Purwar, ex-SBI chairman joined the Board and appointed as

Chairman of IIISL- Preferential Allotment to Orient Global Tamarind Fund Pte. Ltd.,

Singapore, an FII

2009

200720052004IIFL incorporated India Infoline

Investment Services Limited as a private limited company to

undertake financing activities

2011Launched Medical Equipment

financing

SO FAR...

Retail Broking Institutional Equities Commodities and Currency Broking Credit and Finance

Wealth Advisory Asset Management Financial Products Distribution Investment Banking

PRODUCT PORTFOLIO

Home Loans, Loans against Property•

•

•

•

Tenure: home loans upto 20 years, loans against property upto 15 yearsUpto 80% of value available for home loans, 65% for loans against propertyRepayment through EMIs, or other specially customised repayment schemesBalance transfers of existing loans obtainable, with additional cash in hand

Healthcare Finance•

••••

Loans upto 85% of the cost of equipment, starting at ` 500,000. Tenure from 12 to 72 months

Funding for medical and ancillary equipmentProject finance and receivable financing availableHospital construction and infrastructure financeLeasing and advisory services. Choice of personal loans for doctors

Loans against Shares•

•

•••

Loans upto ` 180 crores. Tenure: 3 to 12 months. Competitive interest rates, Funding against both diversified and concentrated securitiesUpto 600 approved Securities and Mutual Fund unitsMargins vary from 25% to 50% depending on securitiesFlexible margin financing and IPO funding schemes also available

Gold Loan•••••

Cash against gold in 5 minutes flatLoans from ̀ 10,000 to 1,000,000Attractive interest ratesChoice of EMIs, or interest service optionsFlexible tenure, according to your requirements

`

Finan

cial S

tate

men

tsA

N O

VER

VIE

WB

usin

ess D

iscussio

nSta

tuto

ry R

ep

orts

CORPORATE IDENTITY

India Infoline Investment Services LimitedAnnual Report 2010-11

VISIONTo become the Most Respected Company in the financial services space in India.

Team IIFL adheres to a set of values that can be summarized as GIFTS, namely, Growth, Integrity, Fairness, Transparency and Service

VALUES

GROWTH

We are driven to grow faster than the rest of the industry. The

culture therefore encourages calculated risks and

empowerment at all levels.

We ensure utmost honesty and integrity, in letter and in spirit,

in all our dealings with people – internal or external.

We believe in fair dealings, devoid of any fear or favor, with all

stakeholders including employees, customers and vendors.

INTEGRITY

FAIRNESS

TRANSPARENCY

We believe in as much transparency as practically possible, with

our stakeholders, media and public at large.

We are a service organization, committed to delight our

customers with superior advice and service, delivered with

humility and sincerity.

SERVICE

IIISL OverviewIIISL, a subsidiary of India Infoline Limited (IIFL) is registered with Reserve Bank of India as a Non Banking Finance Company

IIFL Group

3000+Business locations

across India

1+ million customers

across various businesses

10,000+India Infoline team

as on March 31, 2011FILINGS AND LISTINGS

COMPREHENSIVE PORTFOLIO

IIFL subsidiaries – India Infoline Investment Services and Moneyline Credit Limited – are registered with the RBI as non-deposit taking,

non-banking financial services companies. India Infoline Housing Finance Ltd, the housing finance arm, is registered with the National

Housing Bank.

Received RBI license for undertaking NBFC activities and

commenced business

Launched Gold loans

2010

- IIISL became a public limited company

- IIISL acquired Moneyline Credit Limited, an NBFC and

commenced consumer loan business

- Acquired registration for Housing Finance business from NHB

- Mr A K Purwar, ex-SBI chairman joined the Board and appointed as

Chairman of IIISL- Preferential Allotment to Orient Global Tamarind Fund Pte. Ltd.,

Singapore, an FII

2009

200720052004IIFL incorporated India Infoline

Investment Services Limited as a private limited company to

undertake financing activities

2011Launched Medical Equipment

financing

SO FAR...

Retail Broking Institutional Equities Commodities and Currency Broking Credit and Finance

Wealth Advisory Asset Management Financial Products Distribution Investment Banking

PRODUCT PORTFOLIO

Home Loans, Loans against Property•

•

•

•

Tenure: home loans upto 20 years, loans against property upto 15 yearsUpto 80% of value available for home loans, 65% for loans against propertyRepayment through EMIs, or other specially customised repayment schemesBalance transfers of existing loans obtainable, with additional cash in hand

Healthcare Finance•

••••

Loans upto 85% of the cost of equipment, starting at ` 500,000. Tenure from 12 to 72 months

Funding for medical and ancillary equipmentProject finance and receivable financing availableHospital construction and infrastructure financeLeasing and advisory services. Choice of personal loans for doctors

Loans against Shares•

•

•••

Loans upto ` 180 crores. Tenure: 3 to 12 months. Competitive interest rates, Funding against both diversified and concentrated securitiesUpto 600 approved Securities and Mutual Fund unitsMargins vary from 25% to 50% depending on securitiesFlexible margin financing and IPO funding schemes also available

Gold Loan•••••

Cash against gold in 5 minutes flatLoans from ̀ 10,000 to 1,000,000Attractive interest ratesChoice of EMIs, or interest service optionsFlexible tenure, according to your requirements

`

Finan

cial S

tate

men

tsA

N O

VER

VIE

WB

usin

ess D

iscussio

nSta

tuto

ry R

ep

orts

SPREADING THE LIGHT OF FINANCIAL LITERACY

India Infoline Investment Services LimitedAnnual Report 2010-11

SPREADING THE LIGHT OF FINANCIAL LITERACY

India Infoline Investment Services LimitedAnnual Report 2010-11

FLAME

(Financial Literacy Agenda for Mass Empowerment)

a. Financial awareness workshops across cities and

towns all over India

FLAME is IIFL's unique CSR initiative disseminating knowledge

for financial literacy among the masses. Financial literacy can

aid financial inclusion, which can result in long term

sustainable growth and poverty alleviation. FLAME was

launched by Dr K C Chakrabarty, Deputy Governor, RBI and Mr

Deepak S Parekh, Chairman, HDFC at a function attended by

the leading luminaries from the financial service space. As a

part of the FLAME initiative, IIFL has planned an elaborate set

of activities, which comprise:

As a part of this initiative, IIFL has been organizing

financial awareness workshops all over India. Here our

expert speakers spread financial literacy by disseminating

knowledge about various financial products and the

associated risks and returns.

b. A comprehensive mass media campaign

c. Books and publications

d. Financial awareness helpline

The idea is to convey the various concepts which are a part

of the literacy drive in an easy-to-grasp way. A daily

campaign using cartoon illustrations, facilitating faster

comprehension and assimilation is underway in leading

publications.

Multiple publications are planned which would seek to

highlight the various concepts of finance as a part of this

initiative. Our first book called '108 mantras for Financial

Success' targeted at small investors is now available at

multiple bookstores across the nation. The publication is

also distributed at the workshops held is various cities.

IIFL will setup a helpline, in our own call center, where anyone

can call up and get answers to their queries pertaining to

financial services. This helpline, manned by IIFL's trained

professionals, will provide a solution to such queries. We are

also using sms and social media to reach out to people all

over the country and address their queries.

e. FLAME portal - www.flame.org.in,

f. Tie-ups with educational institutes

g. Leaderspeak

is a dedicated to the

cause of spreading financial literacy. This portal carries

concepts of financial literacy and awareness and is equipped

with innovative features like 'chat with a FLAME-bearer'

where users can direct their queries to IIFL's financial

experts for resolution. The website is rapidly becoming

popular by virtue of its rich content.

IIFL will tie-up with educational institutes including B -

Schools across the country to deliver guest lectures. The

objective of this is to educate the investors of tomorrow, today.

These will be financial awareness workshops where we will

get industry luminaries to interact with the audience to

explain the various concepts in the field of finance and

investing.

Financial Literacy Campaign in leading newspapers IIFL publication - ‘108 Mantras for Financial Success’

Dr. K C Chakrabarty, Deputy Governor, RBI

Launch of FLAME Campaign by FLAME

Mr. Deepak Parekh, Chairman, HDFC

Launch of the FLAME book

IIFL FLAME Meet at Bhavnagar, GujaratFLAME portal www.flame.org.in is dedicated

to the cause of spreading financial literacy

AN

OV

ER

VIE

WB

usin

ess D

iscussio

nFin

an

cial S

tate

men

tsSta

tuto

ry R

ep

orts

FLAME - An IIFL Group Initiative

SPREADING THE LIGHT OF FINANCIAL LITERACY

India Infoline Investment Services LimitedAnnual Report 2010-11

SPREADING THE LIGHT OF FINANCIAL LITERACY

India Infoline Investment Services LimitedAnnual Report 2010-11

FLAME

(Financial Literacy Agenda for Mass Empowerment)

a. Financial awareness workshops across cities and

towns all over India

FLAME is IIFL's unique CSR initiative disseminating knowledge

for financial literacy among the masses. Financial literacy can

aid financial inclusion, which can result in long term

sustainable growth and poverty alleviation. FLAME was

launched by Dr K C Chakrabarty, Deputy Governor, RBI and Mr

Deepak S Parekh, Chairman, HDFC at a function attended by

the leading luminaries from the financial service space. As a

part of the FLAME initiative, IIFL has planned an elaborate set

of activities, which comprise:

As a part of this initiative, IIFL has been organizing

financial awareness workshops all over India. Here our

expert speakers spread financial literacy by disseminating

knowledge about various financial products and the

associated risks and returns.

b. A comprehensive mass media campaign

c. Books and publications

d. Financial awareness helpline

The idea is to convey the various concepts which are a part

of the literacy drive in an easy-to-grasp way. A daily

campaign using cartoon illustrations, facilitating faster

comprehension and assimilation is underway in leading

publications.

Multiple publications are planned which would seek to

highlight the various concepts of finance as a part of this

initiative. Our first book called '108 mantras for Financial

Success' targeted at small investors is now available at

multiple bookstores across the nation. The publication is

also distributed at the workshops held is various cities.

IIFL will setup a helpline, in our own call center, where anyone

can call up and get answers to their queries pertaining to

financial services. This helpline, manned by IIFL's trained

professionals, will provide a solution to such queries. We are

also using sms and social media to reach out to people all

over the country and address their queries.

e. FLAME portal - www.flame.org.in,

f. Tie-ups with educational institutes

g. Leaderspeak

is a dedicated to the

cause of spreading financial literacy. This portal carries

concepts of financial literacy and awareness and is equipped

with innovative features like 'chat with a FLAME-bearer'

where users can direct their queries to IIFL's financial

experts for resolution. The website is rapidly becoming

popular by virtue of its rich content.

IIFL will tie-up with educational institutes including B -

Schools across the country to deliver guest lectures. The

objective of this is to educate the investors of tomorrow, today.

These will be financial awareness workshops where we will

get industry luminaries to interact with the audience to

explain the various concepts in the field of finance and

investing.

Financial Literacy Campaign in leading newspapers IIFL publication - ‘108 Mantras for Financial Success’

Dr. K C Chakrabarty, Deputy Governor, RBI

Launch of FLAME Campaign by FLAME

Mr. Deepak Parekh, Chairman, HDFC

Launch of the FLAME book

IIFL FLAME Meet at Bhavnagar, GujaratFLAME portal www.flame.org.in is dedicated

to the cause of spreading financial literacy

AN

OV

ER

VIE

WB

usin

ess D

iscussio

nFin

an

cial S

tate

men

tsSta

tuto

ry R

ep

orts

FLAME - An IIFL Group Initiative

BUSINESS DISCUSSION

BU

SIN

ESS D

ISC

USSIO

N

India Infoline Investment Services LimitedAnnual Report 2010-11

Credit and Finance

INDIAN CONSUMER LENDING MARKETDespite the rapid growth of the financial services, India

remains an under-penetrated market in terms of credit

penetration.

India has a large and rapidly growing middle class with

increasing levels of discretionary income available for

consumption and investment purposes. As investments

among Indian consumers increase, the available credit in India

has correspondingly increased. The last five years have seen

not only a great expansion of the Indian economy but also a

great expansion of consumer lending. Previously, Indian

consumers were averse to the concept of using credit to fund

purchases and preferred to save prior to spending. Today, with

a variety of consumer credit products being widely available,

Indian consumers are more willing to acquire assets through

borrowing.

The consumer credit market in India has undergone a

significant transformation over the last decade and

experienced rapid growth due to consumer credit becoming

cheaper, more widely available and increasingly a more

acceptable avenue of funding for consumers. The market has

changed dramatically due to the following factors:

1. Increasing desire by customers to acquire assets such as

cars, consumer durables and houses on credit.

2. Fast emerging middle class and growing number of

households who are credit worthy.

3. Improved terms of credit as interest rates in India fell

sharply during early and mid-2000s and further reduced

interest rates offerings for sophisticated products.

4. Legislative changes that offer greater protection to lenders

against fraud and potential default increasing the incentive

to lend.

5. Growth in assignment and securitisation arrangements

for consumer loans has enabled non-deposit based

entities to access wholesale funding and compete in the

market based on ability to originate, underwrite and

service consumer loans.

of players in the non-banking financial services

space. Non-banking financial companies asset base

have grown rapidly over the last few years (27%

CAGR between FY07 and FY11). A rapidly growing

economy is likely to create strong demand for credit

from small businesses and consumers. A

combination of growing demand and lack of

adequate focus from commercial banks on these

banks is likely to create significant growth

opportunity for NBFC.

NBFCs are an integral part of the country's financial

system, catering to a large market of niche

customers, and have emerged as one of the major

purveyors of retail and SME credit in India. It is a

heterogeneous group of institutions (other than

commercial and co-operative banks) performing

financial intermediation in a variety of ways, such

as accepting deposits, making loans and advances,

providing leasing/hire purchase services, among

others. There are over 12,000 NBFCs in India,

(Source: Reserve Bank of India, Annual Report,

August 2009) mostly in the private sector.

Opportunity landscape for NBFC spans across

many products ranging from secured to unsecured

products. Opportunity within each segment

remains significantly large given the current level of

penetration (ranging from <1% to 9% of GDP). The

potential market opportunity could be as high as

5%-10% of GDP in each product segment.

Opportunity in the mortgage market remains very

large. Mortgage loans/ GDP ratio stands at 9% in

FY10 (Source: IMF, European Mortgage Federation).

There is significant opportunity to grow this market

driven by huge demand and supply mismatch for

dwelling units, rising income levels and favourable

affordability. Mortgage market has sustained over

25% CAGR over the last 10 years. Given the latent

demand for mortgages, loan growth could be

HOUSING FINANCE SECTOR

Despite high loan growth in consumer financing, it remains an

under-penetrated market. We believe demand for consumer

loans will increase going forward in view of household gearing

remaining low and disposable income continues to rise rapidly.

Commercial banks play a dominant role in the financial

services landscape by virtue of their wide distribution set up,

ability to raise cheap retail deposits through brand identity.

However, a majority of the commercial banks have maintained

their focus in lending on industrial and corporate loans. As a

result, lending to small business and consumer has always

remained a smaller share of their overall lending portfolio.

Lending by Banks to small business and consumer declined

from 32% in FY08 to 27% in Fy11.

Commercial banks share in business and consumer lending

3334 34

3230

27 27

FY05 FY06 FY07 FY08 FY09 FY10 FY11

(in %) Source: RBI

LOAN AGAINST PROPERTYLoan against property is a secured avenue for lending to small businesses

against their working capital and or project finance needs. The

estimated outstanding volume of loans by way of loan against property

stood at ` 240 bn as at end March 2011. The opportunity landscape is

very large given that small businesses do not get adequate flow of credit

from the commercial banks but make a significant contribution to the

economic growth. According to Annual Survey of Industries estimate

for 2008-09 published by Ministry of Statistics and Program

Implementation, firms with capital invested with ` 100 mn or below

accounted for 21% of the capital invested by industry and 31% of the

value of output. Bank financing accounted for less than 20% of the

invested capital of these firms.

sustained at historical levels. The focus of most lenders in mortgage

lending is confined to salaried urban middle to high income segments. The

opportunity could be significantly expanded if the players were to focus

on self employed segments as well. If the market landscape were to be

expanded, potential growth rate could be even higher.

Mortgage Loans/ GDP ratio

Source: European Mortgage Federation, 2010, World Bank, 2010

India

Thai

lan

d

Ch

ina

Kore

a

Mal

aysi

a

Sin

gapore

Taiw

an

Hon

gkon

g

Ger

man

y

UK

USA

Den

mar

k

9%

17%20%

26%29% 32%

39% 41%

48%

81%84%

95%

NON-BANKING FINANCE COMPANIES

(NBFCS)Under-penetrated and rapidly growing opportunities in small

business and consumer lending has lead to heralding a new set

An

Overv

iew

Finan

cial S

tate

men

tsSta

tuto

ry R

ep

orts

BUSINESS DISCUSSION

BU

SIN

ESS D

ISC

USSIO

N

India Infoline Investment Services LimitedAnnual Report 2010-11

Credit and Finance

INDIAN CONSUMER LENDING MARKETDespite the rapid growth of the financial services, India

remains an under-penetrated market in terms of credit

penetration.

India has a large and rapidly growing middle class with

increasing levels of discretionary income available for

consumption and investment purposes. As investments

among Indian consumers increase, the available credit in India

has correspondingly increased. The last five years have seen

not only a great expansion of the Indian economy but also a

great expansion of consumer lending. Previously, Indian

consumers were averse to the concept of using credit to fund

purchases and preferred to save prior to spending. Today, with

a variety of consumer credit products being widely available,

Indian consumers are more willing to acquire assets through

borrowing.

The consumer credit market in India has undergone a

significant transformation over the last decade and

experienced rapid growth due to consumer credit becoming

cheaper, more widely available and increasingly a more

acceptable avenue of funding for consumers. The market has

changed dramatically due to the following factors:

1. Increasing desire by customers to acquire assets such as

cars, consumer durables and houses on credit.

2. Fast emerging middle class and growing number of

households who are credit worthy.

3. Improved terms of credit as interest rates in India fell

sharply during early and mid-2000s and further reduced

interest rates offerings for sophisticated products.

4. Legislative changes that offer greater protection to lenders

against fraud and potential default increasing the incentive

to lend.

5. Growth in assignment and securitisation arrangements

for consumer loans has enabled non-deposit based

entities to access wholesale funding and compete in the

market based on ability to originate, underwrite and

service consumer loans.

of players in the non-banking financial services

space. Non-banking financial companies asset base

have grown rapidly over the last few years (27%

CAGR between FY07 and FY11). A rapidly growing

economy is likely to create strong demand for credit

from small businesses and consumers. A

combination of growing demand and lack of

adequate focus from commercial banks on these

banks is likely to create significant growth

opportunity for NBFC.

NBFCs are an integral part of the country's financial

system, catering to a large market of niche

customers, and have emerged as one of the major

purveyors of retail and SME credit in India. It is a

heterogeneous group of institutions (other than

commercial and co-operative banks) performing

financial intermediation in a variety of ways, such

as accepting deposits, making loans and advances,

providing leasing/hire purchase services, among

others. There are over 12,000 NBFCs in India,

(Source: Reserve Bank of India, Annual Report,

August 2009) mostly in the private sector.

Opportunity landscape for NBFC spans across

many products ranging from secured to unsecured

products. Opportunity within each segment

remains significantly large given the current level of

penetration (ranging from <1% to 9% of GDP). The

potential market opportunity could be as high as

5%-10% of GDP in each product segment.

Opportunity in the mortgage market remains very

large. Mortgage loans/ GDP ratio stands at 9% in

FY10 (Source: IMF, European Mortgage Federation).

There is significant opportunity to grow this market

driven by huge demand and supply mismatch for

dwelling units, rising income levels and favourable

affordability. Mortgage market has sustained over

25% CAGR over the last 10 years. Given the latent

demand for mortgages, loan growth could be

HOUSING FINANCE SECTOR

Despite high loan growth in consumer financing, it remains an

under-penetrated market. We believe demand for consumer

loans will increase going forward in view of household gearing

remaining low and disposable income continues to rise rapidly.

Commercial banks play a dominant role in the financial

services landscape by virtue of their wide distribution set up,

ability to raise cheap retail deposits through brand identity.

However, a majority of the commercial banks have maintained

their focus in lending on industrial and corporate loans. As a

result, lending to small business and consumer has always

remained a smaller share of their overall lending portfolio.

Lending by Banks to small business and consumer declined

from 32% in FY08 to 27% in Fy11.

Commercial banks share in business and consumer lending

3334 34

3230

27 27

FY05 FY06 FY07 FY08 FY09 FY10 FY11

(in %) Source: RBI

LOAN AGAINST PROPERTYLoan against property is a secured avenue for lending to small businesses

against their working capital and or project finance needs. The

estimated outstanding volume of loans by way of loan against property

stood at ` 240 bn as at end March 2011. The opportunity landscape is

very large given that small businesses do not get adequate flow of credit

from the commercial banks but make a significant contribution to the

economic growth. According to Annual Survey of Industries estimate

for 2008-09 published by Ministry of Statistics and Program

Implementation, firms with capital invested with ` 100 mn or below

accounted for 21% of the capital invested by industry and 31% of the

value of output. Bank financing accounted for less than 20% of the

invested capital of these firms.

sustained at historical levels. The focus of most lenders in mortgage

lending is confined to salaried urban middle to high income segments. The

opportunity could be significantly expanded if the players were to focus

on self employed segments as well. If the market landscape were to be

expanded, potential growth rate could be even higher.

Mortgage Loans/ GDP ratio

Source: European Mortgage Federation, 2010, World Bank, 2010

India

Thai

lan

d

Ch

ina

Kore

a

Mal

aysi

a

Sin

gapore

Taiw

an

Hon

gkon

g

Ger

man

y

UK

USA

Den

mar

k

9%

17%20%

26%29% 32%

39% 41%

48%

81%84%

95%

NON-BANKING FINANCE COMPANIES

(NBFCS)Under-penetrated and rapidly growing opportunities in small

business and consumer lending has lead to heralding a new set

An

Overv

iew

Finan

cial S

tate

men

tsSta

tuto

ry R

ep

orts

BUSINESS DISCUSSION

BU

SIN

ESS D

ISC

USSIO

N

India Infoline Investment Services LimitedAnnual Report 2010-11

LOAN AGAINST CAPITAL MARKET

INSTRUMENTS

GOLD LOAN MARKET

Loan against security is yet another avenue for lending to

corporates, HNIs, individuals for financing their capital market

exposures as well as households to tide over their financing

gaps that arise from time to time. Potentially, this could be a

significant opportunity given that many small and medium

enterprises aspire to grow large. This product effectively serves

the purpose of providing bridge financing for asset acquisition

as well as infusion of capital into new ventures. There is no

estimate of potential market available, however, given the role

that small businesses play in the overall economic

development, this would likely be a huge opportunity.

India is one of the largest markets for gold. The organised gold

loan market has grown from ` 416 bn in 2009 to ` 616 bn in

RETAIL FINANCE DISBURSEMENTS

Car finance Utility vehicles 2 Wheelers CVs

Mortgages Credit cards Personal loans Consumer durables

` 2.5 tn55.3%

8.2%3.2%

0.7%

12.6%

3.7%3.5%

12.8%

` 4.2 tn 55.5%

8.4%2.7%0.9%

12.9%

3.9%

3.2%12.5%

FY10 FY12E

BRIEF SNAPSHOTIndia Infoline Investment Services Ltd (a 98.82% subsidiary of IIFL) and its subsidiaries provide a wide array of secured loan products. The

Company offers home loans, loans against property and loans against shares / debentures. The Company has recently launched gold loans

and medical equipment financing.

IIFL's robust credit and risk management processes have resulted in less than 1% NPAs. The Company has deployed proprietary loan-

processing software that enables stringent credit checks and fast application processing.

`32.9 bn Loan book doubled

during the year

<1%Less than one percent

NPAs indicates a healthy loan book

MAJOR HIGHLIGHTS, 2010-11•

•

•

•

CORE COMPETENCIES•

•

•

•

The loan book more than doubled during the year to ̀ 32.9 bn in

FY11 from ̀ 16.3 bn in FY10

Home loans and loans against property contributed 60% of the

loan portfolio, while capital market products contributed 35%.

Our unsecured portfolio of personal loans is 1% of the total

portfolio. Our personal loans business was discontinued in

2008.

Launched healthcare financing, which includes project

financing for brown field health projects, medical equipment

and ancillary equipment finance and refinance on existing

equipment. The loans are given to doctors, clinics, nursing

homes, diagnostic centres and hospitals.

Also launched gold loans during the year

Experienced team of professionals with work experience at

globally respected financial houses

Well spread out, pan India distribution network and a large

client base gives cross sell opportunities.

Sound credit management system and procedures, and a

resultant quality portfolio with less than 1% NPAs

Centralised credit and finance operations with connectivity to

every branch and office, facilitating efficient and smooth loan

servicing.

FUTURE ROAD MAP •

•

Expand the recently launched healthcare and gold loans

portfolio

Strengthen customer relationships for upsell and cross

sell opportunities

Performance Overview

PORTFOLIO BREAK-UP

42%

16%

36%

6%

FY10 FY11

` 32.9 bn` 16.3 bn 60%

16%

19%1%

4%

Mortgage Loan LAS/ Debentures Margin Funding

Personal Loan Others

2010. It is expected to witness a 35% CAGR between 2009-

12. (Source: IDFC Indian Retail Finance). Indian consumers

have a strong preference for gold that emanates from cultural

factors. Further, low level of financial inclusion and poor access

to financial products and services make gold a safe and

attractive investment proposition.

Driven by various catalysts such as increasing population,

rising income levels, changing demographics, and illness

profiles with a shift from chronic to lifestyle diseases,

Healthcare industry is expected to witness a strong growth

of 23% p.a. to become a US$ 77 Bn industry by 2012.

(Source: Yes Bank ASSOCHAM: Healthcare Services in India.

2012: The path ahead)

HEALTHCARE FINANCING MARKET

Source: IDFC Research Report

An

Overv

iew

Finan

cial S

tate

men

tsSta

tuto

ry R

ep

orts

BUSINESS DISCUSSION

BU

SIN

ESS D

ISC

USSIO

N

India Infoline Investment Services LimitedAnnual Report 2010-11

LOAN AGAINST CAPITAL MARKET

INSTRUMENTS

GOLD LOAN MARKET

Loan against security is yet another avenue for lending to

corporates, HNIs, individuals for financing their capital market

exposures as well as households to tide over their financing

gaps that arise from time to time. Potentially, this could be a

significant opportunity given that many small and medium

enterprises aspire to grow large. This product effectively serves

the purpose of providing bridge financing for asset acquisition

as well as infusion of capital into new ventures. There is no

estimate of potential market available, however, given the role

that small businesses play in the overall economic

development, this would likely be a huge opportunity.

India is one of the largest markets for gold. The organised gold

loan market has grown from ̀ 416 bn in 2009 to ̀ 616 bn in

RETAIL FINANCE DISBURSEMENTS

Car finance Utility vehicles 2 Wheelers CVs

Mortgages Credit cards Personal loans Consumer durables

` 2.5 tn55.3%

8.2%3.2%

0.7%

12.6%

3.7%3.5%

12.8%

` 4.2 tn 55.5%

8.4%2.7%0.9%

12.9%

3.9%

3.2%12.5%

FY10 FY12E

BRIEF SNAPSHOTIndia Infoline Investment Services Ltd (a 98.82% subsidiary of IIFL) and its subsidiaries provide a wide array of secured loan products. The

Company offers home loans, loans against property and loans against shares / debentures. The Company has recently launched gold loans

and medical equipment financing.

IIFL's robust credit and risk management processes have resulted in less than 1% NPAs. The Company has deployed proprietary loan-

processing software that enables stringent credit checks and fast application processing.

`32.9 bn Loan book doubled

during the year

<1%Less than one percent

NPAs indicates a healthy loan book

MAJOR HIGHLIGHTS, 2010-11•

•

•

•

CORE COMPETENCIES•

•

•

•

The loan book more than doubled during the year to ̀ 32.9 bn in

FY11 from ̀ 16.3 bn in FY10

Home loans and loans against property contributed 60% of the

loan portfolio, while capital market products contributed 35%.

Our unsecured portfolio of personal loans is 1% of the total

portfolio. Our personal loans business was discontinued in

2008.

Launched healthcare financing, which includes project

financing for brown field health projects, medical equipment

and ancillary equipment finance and refinance on existing

equipment. The loans are given to doctors, clinics, nursing

homes, diagnostic centres and hospitals.

Also launched gold loans during the year

Experienced team of professionals with work experience at

globally respected financial houses

Well spread out, pan India distribution network and a large

client base gives cross sell opportunities.

Sound credit management system and procedures, and a

resultant quality portfolio with less than 1% NPAs

Centralised credit and finance operations with connectivity to

every branch and office, facilitating efficient and smooth loan

servicing.

FUTURE ROAD MAP •

•

Expand the recently launched healthcare and gold loans

portfolio

Strengthen customer relationships for upsell and cross

sell opportunities

Performance Overview

PORTFOLIO BREAK-UP

42%

16%

36%

6%

FY10 FY11

` 32.9 bn` 16.3 bn 60%

16%

19%1%

4%

Mortgage Loan LAS/ Debentures Margin Funding

Personal Loan Others

2010. It is expected to witness a 35% CAGR between 2009-

12. (Source: IDFC Indian Retail Finance). Indian consumers

have a strong preference for gold that emanates from cultural

factors. Further, low level of financial inclusion and poor access

to financial products and services make gold a safe and

attractive investment proposition.

Driven by various catalysts such as increasing population,

rising income levels, changing demographics, and illness

profiles with a shift from chronic to lifestyle diseases,

Healthcare industry is expected to witness a strong growth

of 23% p.a. to become a US$ 77 Bn industry by 2012.

(Source: Yes Bank ASSOCHAM: Healthcare Services in India.

2012: The path ahead)

HEALTHCARE FINANCING MARKET

Source: IDFC Research Report

An

Overv

iew

Finan

cial S

tate

men

tsSta

tuto

ry R

ep

orts

BOARD OF DIRECTORS

India Infoline Investment Services LimitedAnnual Report 2010-11

STA

TU

TO

RY

REP

OR

TS

Mr. A. K. Purwar (Non Executive

Chairman)

Mr. Nirmal Jain (Director)

Mr. Purwar is the Chairman of

IndiaVenture Advisors Pvt. Ltd.,

IL&FS Renewable Energy Limited and

India Infoline Investment Services

Ltd. He is working as an Independent

Director in leading companies in

Telecom, Steel, Textiles, Power, Auto

components, Renewable Energy,

Engineering Consultancy, Financial Services and Healthcare

Services. He is an Advisor to Mizuho Securities in Japan and is

also a member of Advisory Board for Institute of Indian

Economic Studies (IIES), Waseda University, Tokyo, Japan.

Mr. Purwar was the Chairman of State Bank of India, the largest

bank in the country from November '02 to May '06 and held

several important and critical positions like Managing Director

of State Bank of Patiala, CEO of the Tokyo branch, covering

almost the entire range of commercial banking operations in

his illustrious career at the bank from 1968 to 2006. Mr.

Purwar also worked as Chairman of Indian Bank Association

during 2005 – 2006.

He is also the recipient of several awards like “CEO of the year”

Award from the Institute for Technology & Management

(2004); “Outstanding Achiever of the year” Award from Indian

Banks' Association (2004); “Finance Man of the Year” Award

by the Bombay Management Association in 2006.

Mr. Nirmal Jain is the founder and

Chairman of India Infoline Ltd. He is a

PGDM (Post Graduate Diploma in

Management) from IIM (Indian

Institute of Management) Ahmedabad,

a Chartered Accountant and a Cost

Accountant. His professional track

record is equally outstanding. He

started his career in 1989 with

Hindustan Lever Limited, the Indian

arm of Unilever. During his stint with Hindustan Lever, he

handled a variety of responsibilities, including export and trading

He is elected member of the Central Council of Institute of

Chartered Accountant of India (ICAI), the Apex decision

making body of the second largest accounting body in the

world, 2010–2013. He is Chairman of its Research Committee,

Vice Chairman of its Corporate Laws & Corporate Governance

Committee and member of its various other committees.

He is Representative of the ICAI on the Committee for

Improvement in Transparency, Accountability and Governance

(ITAG) of South Asian Federation of Accountants (SAFA) and

also on Committee constituted by Ministry of Corporate

Affairs (MCA) on issues of applicability of Foreign Investments

in LLPs.

He is member of Review, Reforms & Rationalization

Committee (IMC), Member of Legal Affairs Committee of

Bombay Chamber of Commerce and Industry (BCCI), member

of Accounting and Auditing Committee of Bombay Chartered

Accountant Society (BCAS) and also on its Core Group,

Corporate Members Committee of The Chamber of Tax

Consultants (CTC) and a Regular Contributor to WIRC Annual

Referencer on "Bank Branch Audit".

Mr. Vikamsey is also a Director of India Infoline Investment

Services Limited, Rodium Realty Limited, ICAI Accounting

Research Foundation and few private limited companies and

Trustee in Sayagyi U Ba Khin Memorial Trust (Vipassana

International Academy) and a few Trusts focusing on

education.

Mr. Mahesh Narayan Singh is an

Independent Director of India

Infoline Investment Services Limited.

He holds a Post-Graduate degree in

Physics from Banaras Hindu

University. Mr. Singh Joined the

'Indian Police Service' in 1967. He has

worked as the chiefs of the crime

branch of Mumbai Police, State CID

and Anti-Corruption Bureau. Mr. Singh received his initial

training at the National Academy of Administration,

Mr. Mahesh Narayan Singh,

(Independent Director)

in agro-commodities. He contributed immensely towards the

rapid and profitable growth of Hindustan Lever's commodity

export business, which was then the nation's as well as the

Company's top priority.

He founded Probity Research and Services Pvt. Ltd. (later re-

christened IIFL) in 1995; perhaps the first independent equity

research Company in India. His work set new standards for

equity research in India. Mr. Jain was one of the first

entrepreneurs in India to seize the internet opportunity, with

the launch of www. indiainfoline.com in 1999. Under his

leadership, your Company not only steered through the

dotcom bust and one of the worst stock market downtrends

but also grew from strength to strength.

R Venkataraman, Co-promoter and

Managing Director of IIFL Group, has

over two decades of experience in the

financial services space. A B.Tech

( E l e c t ro n i c s a n d E l e c t r i c a l

Communications Engineering, IIT

Kharagpur) and an MBA (IIM

Bangalore), he previously held senior

managerial positions in ICICI Group,

BZW, Taib Capital and GE Capital

India, before joining the India Infoline board in July 1999. He

spear-headed India Infoline Ltd's entry into the online broking

space in 2000 and has today steered the company to become

one of the leading players in the Indian financial services space.

Mr. Nilesh Vikamsey - Board Member

since February 2005 - is a practicing

Chartered Accountant for 25 years

and Senior Partner at M/s Khimji

Kunverji & Co. Chartered Accountants,

a member firm of HLB International, a

wor ld-wide o rgan iza t ion o f

professional accounting firms and

business advisers, ranked amongst

the top 12 accounting groups in the world.

Mr. R. Venkataraman (Director)

Mr. Nilesh Vikamsey (Independent

Director)

Mussoorie and the National Police Academy, Mount Abu.

Subsequently, government deputed him for a course in 'Senior

Command Management' in UK and a training programme in

'Disaster Management' in USA. In his long years of service

under the government, Mr. Singh held many important

positions in the police as well as in the ministry and acquired

rich experience in public administration, law enforcement and

corporate management. Mr. Singh has vast experience in

handling all types of crimes, especially organized crime,

economic offences and international terrorism. He has worked

closely with the Central Agencies at the head of 'Special Task

Force' to investigate serious crimes having national and

international ramifications. Mr. Singh also had a long stint in

the government as a Joint Secretary and as Managing Director

of Police Housing Corporation.

Mr. Singh retired from the highest rank of Director General of

Police at the end of a distinguished career in public service

spanning over a period of 35 years. His services were

recognized by the Government of India with the award of

'Indian Police Medal' for meritorious services and 'President's

Police Medal' for distinguished services.

Ms. Pratima Ram is a Whole Time

Director of our Company. She joined

the Board of our Company in May

2011. She holds a Masters Degree in

Arts from University of Virginia.

Prior to joining our Company, she

held various senior management

positions in State Bank of India

including those of country head of State Bank of India's

United States Operations based in New York. She has

worked as CEO of South Africa Operations of SBI, based in

Johannesburg. She has also headed Mergers & Acquisitions

at SBI Capital Markets and has worked with Punj Loyyds as

Group President - Finance.

Ms. Pratima Ram, (Wholetime

Director & Chief Executive

Officer)

An

Overv

iew

Finan

cial S

tate

men

tsB

usin

ess D

iscussio

n

BOARD OF DIRECTORS

India Infoline Investment Services LimitedAnnual Report 2010-11

STA

TU

TO

RY

REP

OR

TS

Mr. A. K. Purwar (Non Executive

Chairman)

Mr. Nirmal Jain (Director)

Mr. Purwar is the Chairman of

IndiaVenture Advisors Pvt. Ltd.,

IL&FS Renewable Energy Limited and

India Infoline Investment Services

Ltd. He is working as an Independent

Director in leading companies in

Telecom, Steel, Textiles, Power, Auto

components, Renewable Energy,

Engineering Consultancy, Financial Services and Healthcare

Services. He is an Advisor to Mizuho Securities in Japan and is

also a member of Advisory Board for Institute of Indian

Economic Studies (IIES), Waseda University, Tokyo, Japan.

Mr. Purwar was the Chairman of State Bank of India, the largest

bank in the country from November '02 to May '06 and held

several important and critical positions like Managing Director

of State Bank of Patiala, CEO of the Tokyo branch, covering

almost the entire range of commercial banking operations in

his illustrious career at the bank from 1968 to 2006. Mr.

Purwar also worked as Chairman of Indian Bank Association

during 2005 – 2006.

He is also the recipient of several awards like “CEO of the year”

Award from the Institute for Technology & Management

(2004); “Outstanding Achiever of the year” Award from Indian

Banks' Association (2004); “Finance Man of the Year” Award

by the Bombay Management Association in 2006.

Mr. Nirmal Jain is the founder and

Chairman of India Infoline Ltd. He is a

PGDM (Post Graduate Diploma in

Management) from IIM (Indian

Institute of Management) Ahmedabad,

a Chartered Accountant and a Cost

Accountant. His professional track

record is equally outstanding. He

started his career in 1989 with

Hindustan Lever Limited, the Indian

arm of Unilever. During his stint with Hindustan Lever, he

handled a variety of responsibilities, including export and trading

He is elected member of the Central Council of Institute of

Chartered Accountant of India (ICAI), the Apex decision

making body of the second largest accounting body in the

world, 2010–2013. He is Chairman of its Research Committee,

Vice Chairman of its Corporate Laws & Corporate Governance

Committee and member of its various other committees.

He is Representative of the ICAI on the Committee for

Improvement in Transparency, Accountability and Governance

(ITAG) of South Asian Federation of Accountants (SAFA) and

also on Committee constituted by Ministry of Corporate

Affairs (MCA) on issues of applicability of Foreign Investments

in LLPs.

He is member of Review, Reforms & Rationalization

Committee (IMC), Member of Legal Affairs Committee of

Bombay Chamber of Commerce and Industry (BCCI), member

of Accounting and Auditing Committee of Bombay Chartered

Accountant Society (BCAS) and also on its Core Group,

Corporate Members Committee of The Chamber of Tax

Consultants (CTC) and a Regular Contributor to WIRC Annual

Referencer on "Bank Branch Audit".

Mr. Vikamsey is also a Director of India Infoline Investment

Services Limited, Rodium Realty Limited, ICAI Accounting

Research Foundation and few private limited companies and

Trustee in Sayagyi U Ba Khin Memorial Trust (Vipassana

International Academy) and a few Trusts focusing on

education.

Mr. Mahesh Narayan Singh is an

Independent Director of India

Infoline Investment Services Limited.

He holds a Post-Graduate degree in

Physics from Banaras Hindu

University. Mr. Singh Joined the

'Indian Police Service' in 1967. He has

worked as the chiefs of the crime

branch of Mumbai Police, State CID

and Anti-Corruption Bureau. Mr. Singh received his initial

training at the National Academy of Administration,

Mr. Mahesh Narayan Singh,

(Independent Director)

in agro-commodities. He contributed immensely towards the

rapid and profitable growth of Hindustan Lever's commodity

export business, which was then the nation's as well as the

Company's top priority.

He founded Probity Research and Services Pvt. Ltd. (later re-

christened IIFL) in 1995; perhaps the first independent equity

research Company in India. His work set new standards for

equity research in India. Mr. Jain was one of the first

entrepreneurs in India to seize the internet opportunity, with

the launch of www. indiainfoline.com in 1999. Under his

leadership, your Company not only steered through the

dotcom bust and one of the worst stock market downtrends

but also grew from strength to strength.

R Venkataraman, Co-promoter and

Managing Director of IIFL Group, has

over two decades of experience in the

financial services space. A B.Tech

( E l e c t ro n i c s a n d E l e c t r i c a l

Communications Engineering, IIT

Kharagpur) and an MBA (IIM

Bangalore), he previously held senior

managerial positions in ICICI Group,

BZW, Taib Capital and GE Capital

India, before joining the India Infoline board in July 1999. He

spear-headed India Infoline Ltd's entry into the online broking

space in 2000 and has today steered the company to become

one of the leading players in the Indian financial services space.

Mr. Nilesh Vikamsey - Board Member

since February 2005 - is a practicing

Chartered Accountant for 25 years

and Senior Partner at M/s Khimji

Kunverji & Co. Chartered Accountants,

a member firm of HLB International, a

wor ld-wide o rgan iza t ion o f

professional accounting firms and

business advisers, ranked amongst

the top 12 accounting groups in the world.

Mr. R. Venkataraman (Director)

Mr. Nilesh Vikamsey (Independent

Director)

Mussoorie and the National Police Academy, Mount Abu.

Subsequently, government deputed him for a course in 'Senior

Command Management' in UK and a training programme in

'Disaster Management' in USA. In his long years of service

under the government, Mr. Singh held many important

positions in the police as well as in the ministry and acquired

rich experience in public administration, law enforcement and

corporate management. Mr. Singh has vast experience in

handling all types of crimes, especially organized crime,

economic offences and international terrorism. He has worked

closely with the Central Agencies at the head of 'Special Task

Force' to investigate serious crimes having national and

international ramifications. Mr. Singh also had a long stint in

the government as a Joint Secretary and as Managing Director

of Police Housing Corporation.

Mr. Singh retired from the highest rank of Director General of

Police at the end of a distinguished career in public service

spanning over a period of 35 years. His services were

recognized by the Government of India with the award of

'Indian Police Medal' for meritorious services and 'President's

Police Medal' for distinguished services.

Ms. Pratima Ram is a Whole Time

Director of our Company. She joined

the Board of our Company in May

2011. She holds a Masters Degree in

Arts from University of Virginia.

Prior to joining our Company, she

held various senior management

positions in State Bank of India

including those of country head of State Bank of India's

United States Operations based in New York. She has

worked as CEO of South Africa Operations of SBI, based in

Johannesburg. She has also headed Mergers & Acquisitions

at SBI Capital Markets and has worked with Punj Loyyds as

Group President - Finance.

Ms. Pratima Ram, (Wholetime

Director & Chief Executive

Officer)

An

Overv

iew

Finan

cial S

tate

men

tsB

usin

ess D

iscussio

n

DIRECTORS’ REPORT

STA

TU

TO

RY

REP

OR

TS

India Infoline Investment Services LimitedAnnual Report 2010-11

Dear Members,

Your Directors have pleasure in presenting the Seventh Annual Report of your Company with the audited financial statements for the

financial year ended March 31, 2011

Standalone Financial Results

Consolidated Financial Results

(` )in mn

Particulars 2010 – 2011 2009 – 2010Gross Total Income 5194.9 2,339.6Less: Expenditure (3854.5) (1,573.6)Profit /(Loss) Before Taxation 1340.5 766.0Less: Taxation - Current 427.6 210.1

- Deferred (22.3) 14.6- Short Provision of Tax for earlier year 12.7 3.4

Net Profit / (Loss) After Tax 922.5 537.9

(` )in mn

Directors’ Report

Review of Business

Your Company's product offerings include margin funding, loan

against shares, promoter funding, loan against commercial and

residential property, gold loans and healthcare equipment

financing.

Your Company's loan book doubled during the year to `32.9 bn