innovation in global finance: the impact on hegemony and growth since 1000 ad

TRANSCRIPT

Research Foundation of SUNY

Innovation in Global Finance: The Impact on Hegemony and Growth since 1000 ADAuthor(s): Tony PorterSource: Review (Fernand Braudel Center), Vol. 18, No. 3 (Summer, 1995), pp. 387-429Published by: Research Foundation of SUNY for and on behalf of the Fernand Braudel CenterStable URL: http://www.jstor.org/stable/40241334 .

Accessed: 04/09/2013 14:07

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

Research Foundation of SUNY and Fernand Braudel Center are collaborating with JSTOR to digitize, preserveand extend access to Review (Fernand Braudel Center).

http://www.jstor.org

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

Innovation in Global Finance The Impact on Hegemony and Growth since 1000 AD*

Tony Porter

is the relationship between finance, hegemony, and economic growth? This article argues that finance plays a

key, but poorly understood, role in the rise of hegemony and in the stimulation of long waves of economic growth in the world econo- my. It treats finance as an industry which produces institutional mechanisms for organizing economic activities and transferring value over extended stretches of time and space. It analyzes large- scale financial innovations and investigates their effect on cycles of rise and decline of both the financial industry and the wider inter- national political economy.

The article differs from prevailing views in six ways. First, it fo- cuses on finance as a practice rather than a flow of capital or a set of coherently organized agents.1 Financial practices, as sets of rules and norms that constitute and empower financial agents, can include, for example, the implicit and explicit expectations which converge around particular financial instruments, organizational technologies such as widely dispersed shareholding, and the inter- state and "private" regimes which regulate financial markets. This

* A earlier version of this research was presented as "Long Historical Patterns in the Institutional Structure of Global Finance" at the International Studies Association Annual Meeting, Washington DC, Mar. 30, 1994. I wish to thank Christian Suter and Eric Helleiner for their comments on that paper and from their own work which spurred my interest in the relationship between hegemony and finance.

On the metatheoretical significance of the concept of practice see Giddens (1984: 2-3). Liberal economists tend to focus on flows of capital, although greater attention has been devoted to institutional features of finance in recent years (Bhattacharya 8c Constantinides, 1989). Some theorists of "finance capital" in the Marxist tradition treat finance as involving a coherent class subject.

review, xviii, 3, summer 1995, 387-429 387

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

388 Tony Porter

shift to practices from deep structures and actors corresponds to present efforts to resolve the structure-agent problem in interna- tional relations theory (Wendt, 1987).

Secondly, a related difference is that finance is seen as a rela- tively autonomous sector with its own cycles rather than simply transmitting or amplifying cycles in the real economy or in military conflict, as is the view in most long-wave research. Finance will be treated as an industry with its own dynamics of innovation, maturi- ty, and decline similar to other leading industries, such as rail, chemicals, and automobiles, which have been so important in the evolution of the international political economy. Surprisingly, fi- nance has been absent from the vast literature on the relationship between innovations, industry cycles, and long waves despite its centrality to the functioning of the economy as a whole.

Thirdly, the article argues that financial dominance, prosperity and growth precede industrial and political dominance. This contra- dicts Wallerstein's (1983) view that finance is a lagging sector in the cycle of hegemony, and the view of hegemonic stability theorists (Lake, 1993) that hegemony is a cause rather than an effect of global prosperity.

Fourthly, the paper stresses logistics, long economic cycles of about 200 years, rather than Kondratieff waves of about 50 years, as is most common in long wave research. There is reason to think that these cycles are correlated with hegemony (Bousquet, 1979; Wallerstein, 1984; 1991). Furthermore, they are likely to be related to large scale financial innovations because they are most evident in price data, and because as "world-market control investments" (Wallerstein, 1984: 571) the timing is plausible. As Wallerstein has noted,

what are world-market control investments? They are both global infrastructure (transport, communications, financial networks) and politico-military infrastructure (armed forces, diplomatic networks lato sensu networks of subversion). They are what goes with and sustains the existence of a hegemonic power in the capitalist world economy (1984: 571).

Despite their potential relevance "there has been very little scholar- ly work done on these logistics" (Wallerstein, 1983: 104).

Fifthly, this article suggests that historically military and financial hegemony have often coincided in time but may have existed in dif-

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

INNOVATION IN GLOBAL FINANCE 389

ferent states, an insight relevant for understanding current U.S.- Japanese relations.

Finally, the emphasis here on the cyclical nature of global fi- nance challenges the widespread characterization of the present globalization of finance as entirely new, unilinear, and irreversible. In fact, as will become clear below, over the past 1000 years, peri- ods of intense globalization have alternated with periods of re- trenchment and crisis.

The article has three sections. In the first I identify the existing gaps in our knowledge of long-historical patterns in global finance. In the second I develop a model for analyzing such patterns. In the third I begin to assess this model with respect to the historical record. While this assessment is not a conclusive test it does pro- vide some initial support for the model.

THE GAPS IN OUR KNOWLEDGE

There are four types of waves or cycles that have been discerned in the evolution of the international political economy: short cycles of less than 20 years (Kitchins, Juglars, and Kuznets), Kondratieff cycles of about 50 years, cycles of hegemony, and logistics of rough- ly 150 to 200 years. Although some theorists (Kindleberger, 1989; Suter, 1992; Morgenstern, 1959; Minsky, 1977) have linked changes in finance to shorter cycles, these cycles are too rapid to offer meaningful insights into the relationship of finance to much slower paced cycles of hegemony, and will therefore generally be ignored in this article. Relatively little effort has gone into studying logistic cycles, to which I will turn below. The largest effort has gone into identifying and explaining Kondratieff cycles and cycles of hegemo- ny, and these will be addressed first.

While the causal connections between Kondratieff and hege- monic cycles appear to be "weak" (Goldstein, 1988: 287, Bousquet, 1979, but see Research Working Group on Cyclical Rhythms and Secular Trends, 1979), taken together these cycles have been corre- lated with fluctuations in a wide range of variables including prices, production, profits, war severity, and debt crises. Although conclu- sive empirical tests of hegemonic cycles are impossible because of the number of cases and other philosophy of science problems, the connection of hegemonic transitions with great power war and

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

390 Tony Porter

socio-economic restructuring are striking. The Kondratieff cycles lend themselves more to empirical testing and at present there is substantial evidence that they exist. Indeed Wallerstein has ex- claimed "I suggest that we waste no more time proving that the Earth revolves around the Sun" (1992: 339), although debate con- tinues on the causes, starting point, exact timing of the cycles, as well as on the most appropriate methodology for empirical testing.

Although there are many hints that finance may be relevant to long cycles, these have not been thoroughly explored in the existing literature. I shall demonstrate this by looking at three key contribu- tions to this literature, Goldstein (1988), Suter (1992), and Waller- stein (1983).

Goldstein

Goldstein (1988) has made an outstanding contribution to long- wave research by synthesizing and further testing results from all current research programs and a review of his treatment of finance is therefore a good indicator of its current status in long wave re- search more generally. Goldstein (1988: 132, 268-70) cites Rasler & Thompson and Quincy Wright in including a link between debt and the waging of war. Debt here plays an important role in the transition from an upswing to a downswing by (a) translating growth during an upswing into war, and (b) bringing about a slowdown in economic growth in the debt-laden aftermath of war. The role of the financial system here is minimal and epiphe- nomenal.

Because prices have been a key indicator of long waves, and be- cause of the close connection of the supply of money to prices, one would expect an integration of the monetary aspects of global fi- nance into long wave research. This is not the case, however. As Goldstein (1988: 272) notes, "prices seem to respond to money sup- ply as well, at least since World War II ... I have no theory that ties in money supply, however, except as it is used to finance wars."

Goldstein's work suggests that there are more connections be- tween finance and money on the one hand and long cycles on the other than are apparent from the present state of long-wave re- search. Both prices and war, key variables in this research, are espe- cially likely to be related to finance and money.

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

INNOVATION IN GLOBAL FINANCE 391

Suter

Suter (1992) provides the most comprehensive model of the role of finance in long waves in analyzing global debt cycles since 1820. His book is a highly convincing demonstration that a link exists between finance and long cycles. There are, however, several gaps in his analysis which this article seeks to address. First, the focus is limited in time and space: The focus is on core-periphery relations and little is said about financial relations between core powers, nor about patterns before 1820. Secondly, finance is seen as transmitting and exacerbating cycles in the real economy, making it possible, for instance, to move production to the periphery as it moves through a cycle of maturity and standardization, but the fi- nancial industry itself has little autonomy. Thirdly, there is no attempt to differentiate among loans, securities, and direct invest- ment, nor between government and corporate borrowers, thereby obscuring important differences between historical periods in the institutional mechanisms through which financial flows are carried.

An exception to the above assertions is Suter's identification of a secular trend towards institutionalization of global finance as evi- dent in the roles played by loan syndicates and the International Monetary Fund (IMF), which have an effect on the nature of crises. I will show that this process of institutionalization is more cyclical itself, and has a greater effect on long cycles, than is suggested by Suter's work.

Wallerstein

Wallerstein (1983) has provided an intriguing analysis of the re- lationship between political and financial hegemony. He suggests that hegemons go through an overlapping sequence of agro-indus- trial, commercial, and financial hegemony. It is quite logical that in- vestors might move capital overseas if domestic investment oppor- tunities decline due to maturity and rigidity in a hegemon's leading industries. This model appears to fit the transition from Dutch to British and from British to U.S. hegemony quite well. While Waller- stein's model strongly suggests that there is a relationship between finance and cycles of hegemony, I shall show below that financial innovation precedes rather than follows the other indicators of hegemony.

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

392 Tony Porter

The above review of three leading theorists of Kondratieff and hegemony cycles and their treatment of finance indicates both that a connection between finance and long cycles is probable, and that we need to know more about this connection. While further explo- ration of the correlation between Kondratieff and financial transfor- mation would indeed be useful, I will start instead in this article with the longer logistic cycles. In part this is due to the technical difficulty of analyzing the large number of Kondratieff fluctuations, and in part it is due to the logical compatibility of longer logistics with the present object of study, hegemony and very long-term trends in global growth. I will expand upon this assertion in the next section.

LOGISTIC CYCLES

Logistic cycles are very long term economic waves that span as much as two centuries each (Cameron, 1973). Cameron notes that in Europe both population and economic growth entered a rapid period of expansion starting in the ninth or tenth centuries, peak- ing in the twelfth, and ending with the Great Plague of 1348 (1973: 146). Subsequent cycles are shown in charts 1 and 2. Between 1330 and 1510 prices decline, from 1510 to 1630 they rise dramatically, from 1630 to 1750 they are stagnant, from 1750 to 1820 they rise, from 1820 to 1900 they decline, from 1920 to the recent past they rise. (Bousquet [1979: 510] gives slightly different starting and end- ing points.) Similar cycles are evident in real wages, although the phases are lagged substantially.2

Although they have received little attention in the study of the international political economy, there are several good reasons to pay careful attention to logistics in analyzing the relationship among finance, hegemony, and economic growth. First, unlike Kon- dratieff waves, the pattern spans the period before and after 1500, and therefore is more easily matched to the evolution of modern finance, which dates back to the eleventh century. Secondly, these

2 The construction of long-historical price series is fraught with difficulties. Ramsey notes of the authors of these charts: "the most valiant and successful effort is that of E.H. Phelps Brown 8c Shiela V. Hopkins, widely used by all historians of the period ever since its appearance in 1956" (1971: 3). He notes, however, several weaknesses of the indexes, including the assumption that the weighting of the constituents of the composite unit of consumables did not change.

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

o 1-H

i CM 1-H

W

V s

ï î 1 i U | o U O

1 r o U c« <^ o

f

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

CM r-i

e •a I «s Ï

° ! ? "S

I 1

=a S il 2 ^ S 2 ^

rn c/3 U

I»? rn c/3

# cm "3 "S cm "3 5 >S ffi -S u

II ^ !|I "Si & £ U a;

S- s *s "11 c S o c S o -ils gUbo U Vm g v o #a

-g g-K 2

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

INNOVATION IN GLOBAL FINANCE 395

very long cycles are likely to correspond more closely to the cre- ation and diffusion of large-scale financial innovations which, in an early period, are too complex to be transmitted across the world economy in the period of a Kondratieff cycle. Thirdly, the duration of logistics corresponds more closely to the duration of hegemony and therefore is more likely to be correlated to the financial aspects of hegemonic rise and decline. Finally, it would be surprising if the logistic swings in price in chart 1 did not relate to the financial sys- tem given the link between prices and finance.

Cycles in Global Finance: A Model

In this section I develop a model of the relationship among fi- nance, growth, hegemony, and logistics. I will argue that the institu- tional features of finance, as well as the quantities of wealth mobi- lized, are critical to the production and reproduction of modes of economic life and will indicate why finance, like other industries, is likely to go through cycles of innovation, maturity, and decline, which have profound influences on the economy as a whole.

Both money and finance involve the transfer of value across time and space through the use of "symbolic tokens" (Giddens, 1990). Any survey of the history of monetary and financial systems will indicate how central trust is to their functioning since the "tokens" themselves have rarely had any intrinsic value, and are presently merely pieces of paper or electronic impulses. The accep- tance of financial instruments rests on a faith that they will contin- ue to be accepted. Yet this faith is not simply an attitude, but re- flects a process of institutionalization in which a bank, a state, or a set of market practices is seen as strong enough to organize its par- ticipants' actions in predictable ways.

This stress on institutionalization is contrary to the common overemphasis on gold as a "real" foundation for the monetary sys- tem. Even in earlier times one can question the relevance of gold's intrinsic value as compared to its socially constructed value as money. Certainly by the late middle ages, however, there is no doubt that the distinction between real and symbolic money, and between money and credit, had been eroded. The bills of exchange which fueled medieval and early modern trade were promises to pay that traveled over surprisingly extended and complex circuits spanning Europe. Serving both as a medium of exchange and a

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

396 Tony Porter

source of credit, these bills were accepted because of patterned ex- pectations with respect to their issuers, to the regularity of the fairs at which they were redeemed, and to the effect of the threat of ex- clusion from developing international markets on debtors. Braudel, for instance, notes that "a hundred thousand or so 'ecus d'or en or9- that is real coins- might settle business worth millions" (1982: 91).

It has been shown both for medieval England and for the inter- national economy from 1778 to 1939 that trends in prices can only be explained when analysis of gold flows is supplemented by analy- sis of credit.3 Moreover, the supply of gold was not necessarily exo- genous: Columbus was obsessed by the prospect of finding it, and thus the inflow of gold from the Americas to Europe could be seen as driven by demand not supply.

In the present period the ambiguous nature of money is evident in the difficulty experienced by monetary authorities in measuring the money supply given the ease with which people can substitute a dazzling array of financial instruments for cash or demand depos- its, the more traditional forms of money (Podolski, 1986).

The process of institutionalization of money and finance is not at all unilinear, however. There have been frequent occasions where money and credit have been destroyed by the collapse of confi- dence, whether this involves individual banks, states, or internation- al monetary regimes.

If we could discern patterns in these collapses then it is likely that we would be better able to understand long waves, given the importance of money and finance for other economic indicators. In addition to the impact of the expansion of credit on growth and in- flation the financial system plays a key role in the organization of other sectors, as with, for instance, the impact of stockmarkets on corporate governance. Major transitions in the international politi- cal economy can therefore be expected to be accompanied by trans- formations in the financial system.

3 As De Roover notes: "there can be no question that the medieval money-changers created credit to the extent that deposits were not covered by their cash reserves. In other words, their activities in this respect were as inflationary as if they had been given the privilege of issuing notes" (1974: 215). See also Dupriez (1951), Hammar- strôm (1971: 53), Miskimin (1989: Chapter XV), Postan (1973). For a debate in the U.S. context see Friedman (1986).

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

INNOVATION IN GLOBAL FINANCE 397

There are several reasons to treat finance as an economic sector in order to discern such patterns. First, over much of history, fi- nance has been supplied by private institutions as much as by the state. Secondly, financial instruments are produced and do not just exist. Thirdly, and most important, the production of these instru- ments has involved constant innovation, and it is possible that the technological dynamics that explain the rise and decline of indus- tries in other sectors are present here as well.

Let us therefore run through a schematic financial cycle, treat- ing a set of financial institutions as an innovation comparable to transportation, a more traditional sector. Examples of such sets of financial institutions could include bills of exchange, transferable annuities, merchant banks, joint stock companies, direct foreign investment, stock markets, East-West joint ventures, the Eurocur- rency markets, and loan syndicates. Markets may be segmented geo- graphically as well as by product: The Euroyen market may involve a different set of actors and practices than does the Eurodollar market. These distinctions are comparable to shipbuilding, canals, railways, and automobiles, as well as between Canadian and Russian railway systems.

Like transportation systems, financial institutions are likely to follow an S pattern: Initial investments in building confidence for a new financial institution are heavy, but once established, the vol- ume of transactions can increase rapidly with unit costs declining. Once established, initial profits are likely to be high as a few firms will earn rents on the technological innovation. New firms will rapidly enter, however, reducing profits. Market saturation will lead to a slowing of growth. Impending saturation may not be perceived by investors, however, leading to a crisis of overproduction. Be- cause the financial system produces credit instruments that can be a close substitute for money, this overproduction can lead to price rises.4

4 The assumption in this sentence and in other places in this article is that an ex- pansion in the money supply and in the provision of credit will lead to price increases. While this relationship has generally been widely accepted it has also had its critics. See for instance the conventional and alternative explanations of the sixteenth century price increases in Ramsey (1971). For a brief account that links bank credit to inflation in 1520 Venice and during seventeenth and eighteenth century wars see de Roover (1974: 215).

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

398 Tony Porter

Financial institutions are designed to respond to an emerging possibility of mobilizing supply and demand in another sector, much as a railway might be designed to transport wheat. At the same time there may be dynamics that are best treated as endoge- nous to the financial sector and not simply transmitted to or through it.

This model draws on, resembles, but differs from Kindle- berger's (1989) explanation of manias, panics, and crashes. Kindle- berger suggests that in a boom there is a rapid expansion of credit that spreads the boom into other sectors. The expansion of credit and demand is likely to lead to rising prices. The prices of financial instruments which are based on expected returns are driven up by the inflow of investment and capital gains, rather than returns from the underlying assets. Once confidence is shaken, there is a rapid collapse in the prices of the financial instruments. Kindleberger sees cycles of about ten years duration, which he explains by the length of time needed to forget about past disasters. Yet many of the innovations in financial institutions lasted for much more than ten years, and I hope here by focusing on these longer sequences, to connect them to the literature on long waves and hegemony.

In short, the hypothesis developed here is that the spread of a significant financial innovation should be associated with the begin- ning of an upswing in the world-economy, that a rise in prices should be evident as the innovation becomes more firmly estab- lished, and that financial crisis should initiate a downturn with its associated deflation. The extent to which this is an alternative ex- planation of long swings, rather than just an associated effect, will be evaluated in the concluding section.

ASSESSING THE MODEL AGAINST THE HISTORICAL RECORD

There are two steps in assessing the above model of long finan- cial cycles. The first is to establish key transition dates with respect to hegemony, economic growth, and prices. The second is to do an analysis of the institutional transformation of global finance. Cer- tain limitations of this assessment are apparent from the outset. While measures of long waves are quite well established on the basis of quantitative analysis of time series, the use of such a meth-

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

INNOVATION IN GLOBAL FINANCE 399

od for assessment of patterns of financial innovation is not possible due to lack of data and the need to catch significant qualitative changes in financial institutions. In the larger literature on innova- tion and long cycles much effort has gone into specifying criteria for the identification of key innovations, an impossible task for the present study of financial innovation given the paucity of data and the need for qualitative assessment.5 In assessing the above hypoth- esis, therefore, I will need to use a less rigorous combination of qualitative and quantitative analysis.

Dating Hegemony, Economic Growth, and Prices

There is considerable dispute about the exact sequence and dat- ing of the rise and fall of hegemons. In part this dispute centers around the relative importance of economic dominance versus war, and of land wars versus sea wars. I adopt Wallerstein's (1983) dating for Dutch, British, and American hegemony because of its emphasis on economic dominance, likely to be most relevant to understanding the impact of financial innovation.

Florence, although often overlooked, has striking similarities with these other hegemons. As Cipolla puts it,

Florence grew dramatically in the course of the thirteenth century, and by the end of that century it had come to repre- sent to the world of the time what London was to the nine- teenth century: not only a great cultural, commercial, and manufacturing center, but also the principle financial market of the period (1982: 2).

I've also, following Braudel (1984: 148), included Venetian hegemo- ny because of the similarity in its financial dominance to later hege- mons. Although Braudel stresses Venetian commercial dominance, it is clear that it was the northern Italian cities as a whole, including Genoa, Florence, and Siena, that organized the European economy

5 The method here can be termed adductive. See Goldstein for an explanation and justification of this method for long wave research (1988: 2, 12, 179). On the difficul- ties of assessing the significance of innovations in general see Clark, Freeman, 8c Soete (1984). In this study, as in others, determining the timing of innovations is also diffi- cult For instance, the organization of the joint stock company drew on practices that had been developed over centuries. In such a situation the fixing of innovative moments is unavoidably interpretive.

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

400 Tony Porter

at this time. In sum, then we have the following periods of hegemo- ny: Florentine from 1252 to 1339; Venetian from 1378 to 1498; Dutch from 1625 to 1672; British from 1815 to 1873; and American from 1945 to 1967.

Chart 1 will be basis of my analysis of price changes over this pe- riod. Although the data is from southern England it is likely that the economy was sufficiently globalized over this period that this series can be a proxy for European prices as a whole.6 As Rostow notes, "the analysis of price movements is a complex art" (1978: 81) due to the variety of factors that can influence them. However, because we are focusing on very long waves we can assume that the effects of short term factors such as bad harvests are unlikely to play a key part.

Timing upswings in growth is more difficult. Measures of global production would be ideal, but reliable data for the period before 1740 are not available (see Goldstein, 1988: 81-92; Rostow, Appen- dix A). Here I will rely on the real wage data of Chart 2 based on the following logic. Much long wave research has concluded that innovations cluster in troughs and have a major impact in initiating an upturn. Real wages are likely to increase soon after the begin- ning of an upturn in production for two reasons. First, the demand for labor will increase. Secondly, increasing production (and an in- crease in "relative surplus value") will increase the possibility of labor obtaining a greater share of "surplus value." A downturn in real wages will indicate that the upswing is beginning to end, as the demand for labor declines. Chart 3, which displays trends in world

6 This point is arguable. For the complexities of price analysis see Braudel 8c Spooner (1967), which indicates that there were lags in the rise and decline of prices in different regions of Europe. This cautionary note is amplified by Wallerstein (1974) who points out that there was a vast difference in prices of labor between the core and periphery and that these were altering over this period, indicating that the English transition from periphery to core would significantly alter the relationship of its prices to European prices as a whole. At the same time Braudel 8c Spooner (1967, Fig. 19) show that across Europe there is a substantial convergence over time around the larger patterns expressed in Chart 1. See also Braudel (1984: 75) which states that there was substantial synchronization of price fluctuations across Europe by the fifteenth century. Other historians have also identified a similar dating of logistics in prices in other countries (Research Working Group on Cyclical Rhythms and Secular Trends, 1979: 489; Rostow, 1978: 84-85). The careful pan-European time series of Braudel 8c Spooner (1967) are only reliable for the period after 1450. Price data for Krakow and Spain are available from the middle of the fourteenth century (Hammarstrom, 1971: 43-44). For the earlier period assessment of the correlation of prices and wages across Europe is more impressionistic and speculative.

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

Pi m

I \ 8 |

S -S "5 us 3 o ° i : T3 cm

i

.a a; a. a < à) oo o>

c 'S -d "S O c

i •s

I 2 i o u

i

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

402 Tony Porter

production since 1750, when taken together with chart 2, indicates that this pattern is present over the past 200 years. A 170 year up- turn in production begins in 1770, followed by an upturn in real wages in 1800. The growth rate of production remains high until the beginning of the twentieth century and then begins to falter as does the growth in wage rates. Although there are differences in the shape of the curve in the twentieth century it does appear that there is a 170 year logistic in which high real wages correspond to high rates of growth of world production. This provides some sup- port for the use of the real wage rate data displayed in chart 2 as an indicator of world growth from 1264.7

If one compares the dating of the four periods of hegemony listed above with the phases of real wage cycles in chart 2 one sees that each period of hegemony falls right in the middle of an up- swing in real wages. Hegemony therefore seems to appear in the middle of the high-growth periods of logistic waves. We will come back to the significance of this in relating it to financial transforma- tion below.

MAJOR FINANCIAL INNOVATIONS

The dating of the emergence of significant new financial institu- tions will be carried out by a reading of the literature on the history of banking and finance. This will be organized by logistic.

Logistic 1, to 1350 and Florentine hegemony

In this period statistics do not permit us to analyze price trends, nor do they permit an exact estimate of the timing of the resur- gence of growth in the emerging European world-economy at the end of the first millennium. According to Cipolla (1956: 12) it was

7 Cameron (1973: 146) similarly sees per capita world output as increasing in logistic cycles: "It is virtually certain that each of the accelerating phases of population growth was accompanied by economic growth in the sense that both total and per capita output were increasing This is most clearly attested for the third logistic (and the incipient fourth) for which statistical evidence is relatively plentiful; but there is also much indirect evidence for similar behaviour during the first and second." For an alternative but overlapping representation of growth surges based on urban growth in provincial capitals see Hohenburg & Lees (1985: 8).

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

INNOVATION IN GLOBAL FINANCE 403

in the second half of the tenth century that "the splendid recovery of Western Europe" took place. Cameron notes that

during the eleventh, twelfth, and thirteenth centuries Europe- an civilization expanded from its heartland between the Loire and Rhine rivers to the British Isles, the Iberian Peninsula, Sicily and Southern Italy, into central and eastern Europe, and even, temporarily, during the Crusades, to Palestine and the eastern Mediterranean (1973: 146).8

I will therefore examine the period from the eleventh century to 1350 to see whether there were important financial innovations at the beginning which were exhausted by the end.

Three financial innovations stand out in this historical period, each of which enhanced Italian control of commerce and finance and helped create a European world-economy. The first is the crea- tion of banks. The second is the minting of gold coins. The third is the circulation and balancing of bills of exchange at the Cham- pagne fairs.9 I will examine each in turn.10

That there is a link between the economic upswing of this peri- od and financial innovation is well known in the history of banking. As Orsingher puts it,

It was, indeed, in Italy that economic prosperity was most rapidly re-established and to meet its own needs Italian com- merce gave rise to the first truly professional organization devoted to financial and credit operations, even on an inter- national plane (1967: II).11 These financial innovations, which were not limited to the

acceptance of deposits and the making of loans, involved the crea- tion of multinational companies. For instance, the Bardi bank of

8 See also Bautier (1971) for an account of this economic revival. 9 "Italy . . . the triumphant leader of the thirteenth century, remained above all a

commercial centre, leading the world in business techniques: she had introduced to Europe minted gold money, the bill of exchange and the practice of credit" (Braudel, 1984: 112). 10 All of these innovations built on the accumulated experience of the Middle Eastern and Central Asian worlds. A useful extension of the present paper would be to explore this earlier period. See Abu-Lughod (1989) and Udovitch (1979).

11 For an analysis of the importance of finance and credit in the revival of econom- ic growth in this period see Bautier (1971: 146-61).

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

404 Tony Porter

Florence had more than 30 offices in Italy, France, Paris, London, Bruges, Spain, North Africa, and the Greek, Latin, and Moslem Levant (Bautier, 1971: 151; see also Orsingher, 1967: 12). The im- portance of this innovation is evident in the tracing of the origins of the English joint-stock company back to the transfer of such Ital- ian financial innovations to England in this early period (Scott, 1993: 1; Postan, 1973: 338-39).

The creation of an international monetary system was the sec- ond innovation of northern Italy in this period. In the preceding period the monetary system created by Charlemagne at the end of the eighth century in France, Germany, and Italy deteriorated through the debasement of its single silver coin (Cipolla, 1956: vii- ix). In response to the need for a new international money, the northern Italian cities began minting new coins, first with silver and then gold. The Venetian silver money was very important in Middle Eastern markets (Cipolla, 1956: xii). The Florentine gold florin, first minted in 1252, "established itself as the dominant international currency in continental Europe."12

The third remarkable financial innovation of this period is the use of the bill of exchange internationally and the settlement sys- tem at the Champagne fairs. A bill of exchange is a buyer's promise to pay, at a later date, for goods received.13 A market for these began to develop and they circulated widely through Europe. They served both as money and credit. Yet, not surprisingly, this new in- ternational financial market only worked because of specific institu- tions that provided confidence among traders that these pieces of paper would be redeemed and that made these bills more efficient than gold or silver. Initially confidence was enhanced by ethnic loyalties, but this was replaced by confidence in the reputation of particular firms as those firms grew. Most important, however, was the settlement system that developed at the fairs.

The fairs at Champagne were the key node of European trade in this period, organizing the exchange of wool and wool products

12 Cipolla (1956: xiii). For a more detailed account of the international monetary

system see Bautier (1971: 161-70). 1S See Kindleberger (1984: 465) for a formal definition. The bill of exchange

evolved substantially over this period. Bautier (1971: 152) labels the earlier versions "letters of payment" De Roover (1974: 203) notes however that the distinction between these early instruments and the later bills of exchange was "superficial."

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

INNOVATION IN GLOBAL FINANCE 405

from the north with Mediterranean and Asian products from the south. Most important for their fairs, however, was their innovative financial function in allowing bills of exchange to be efficiently can- celled out.14 As Braudel notes,

the originality of the Champagne fairs lay less however in the superabundance of goods on display than in the money market and the precocious workings of credit on display there . . . Italian credit would be able, through the gatherings at these international fairs, to exploit to its own advantage the huge market with its cash returns (1984: 112).

Although Florence and its neighboring city-states were not a hegemonic system in a military sense (and indeed engaged in wars among themselves), they did exercise a surprising degree of politi- cal influence through their funding of the Crusades, the collection of revenues for the Pope and other European states, and the fund- ing of government debt. For instance, Postan notes that in the first quarter of the fourteenth century the English king owed two Italian banks over a quarter of a million pounds, equivalent to the annual war budget at its highest point (1973: 339).

15 In short, financial innovation was central to the revival of

growth in Western Europe, and to the emergence of the leading role of Florence. This corresponds closely to the model elaborated in the previous section. To what extent can the waning of this first growth logistic be traced to the maturity and exhaustion of these fi- nancial institutions? I now turn to this question.

Although the trough at the end of the first logistic is marked by the plague in 1348, the decline started earlier and is evident in the crises experienced in each of the financial innovations upon which this period of growth had been built.

The decline of Italian banks was apparent in the declining pro- ductivity of their assets, and in their relative loss of power with respect to their clients and competing banks. The first two of these are revealed by the involvement of leading Italian banks in war fi- nance and their collapse when the English crown repudiated its

14 "The fairs were effectively a settling of accounts, in which debts met and can- celled each other out, melting like snow in the sun" (Braudel, 1982: 90-91).

15 See also Bautier (1971: 151).

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

406 Tony Porter

debts. As Postan puts it, the Italians taught the English important lessons in the art of commerce and finance:

By the second half of the fourteenth century the lesson was so well learned that the teacher could be dismissed . . . King Edward III defaulted on his vast obligations to the banking houses of Bardi and Peruzzi [in 1340], and the consequent ruin of Italian merchants' houses in England enabled natives to take the place of Italians in almost every branch of com- merce and finance (1973: 336).

The third problem of Italian banks was the diffusion and appropria- tion of banking technology by competitors. As Orsingher (1967: 20) notes, "gradually the Italians lost their de facto near-monopoly and banking operations became a commonplace of European civiliza- tion" (1956: 20). 16

The crisis of Italian banking was not limited to its foreign operations, however. The impact on Florence was so severe and profound that Cipolla calls it "[the] great crash of 1343-1346" (1982: Gh. 1). Public debt became unsustainable, was made transfer- able, and then collapsed in value: "the effect was comparable to that of a collapse of a stock exchange in our times" (Cipolla, 1982: 4). Loss of confidence in banks spread from one to another until nine leading banks had collapsed (Cipolla, 1982: 9).

The collapse of the Italian banks had a profound effect on the economy as a whole. Depositors of "all social classes and groups" (Cipolla, 1982: 9) were hurt. Cipolla comments:

Nor was this all. The collapse of the banks triggered the ruin of people in other sectors both directly and indirect- ly-directly, because the great companies carried on mercan- tile and manufacturing activities in addition to their banking ones; indirectly, because the banks' failure caused a drastic shortage of credit. Actually, once the crisis had started, a perverse multiplier effect was set in motion by which the crisis fed upon itself and spread like an oil stain (1982: 9-10).

16 Excessive rigidity in the context of these challenges has also been blamed for the collapse of Italian banks. Subsequently a more flexible system of autonomous partner- ships was devised. See de Roover (1963: 78; 1974: 209).

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

INNOVATION IN GLOBAL FINANCE 407

The monetary system initiated by Florence also entered into crisis at this time. As in other bimetallic systems the high and ap- preciating value of gold, the main currency of finance and interna- tional trade, with respect to the currency used by workers and domestic firms, was an important contributor to the wealth of Flor- entine exporters and bankers during Florence's heyday. Starting in 1343 the market moved against gold and in favor of silver (Cipolla, 1982: 17). The Florentines were subsequently forced into a series of devaluations of their gold coins, seriously damaging the credibility of this international money. Cipolla attributes this decline in the price of gold to an unexpected and unexplained influx (1982).

One explanation for the crisis of the Florentine money is that the innovation was imitated in other countries, stimulating the search for gold and increasing the number of gold coins in circula- tion. As Wiseley notes, "when the Italian city-states began the fashion for gold coinage others felt obliged to follow, in the com- petitive quest for both commercial advantage and political prestige" (1977: 22). Between 1250 and 1344 gold coins were struck for the first time in France, Spain, Germany, England, and the Low Coun- tries. Once these competing currencies were introduced there was a tendency on the part of England and France to try to control the flow of gold across borders (Orsingher, 1967: 18). In the case of England this was accompanied by a sustained attack on the bills of exchange which were so central to Italian international finance (Munro, 1979).

An additional part of the explanation relates to the crisis of the third Italian innovation- the Champagne fairs- a crisis which itself contributed to Florentine decline. One common explanation of their decline was a "commercial revolution" in which firms used permanent representatives abroad and professional transporters. This indicates the exhaustion of the Italian financial innovation of the fairs and its replacement by alternative institutional arrange- ments.17 Additionally, the competition from the sea routes, initiated

17 See for instance de Roover: "the rise of this new system of business organization based on correspondence and representation abroad is intimately connected with the rapid decline of the fairs of Champagne after 1300" (1963: 43, 72). See also de Roover (1974: 204-5). Braudel (1984: 115) is skeptical of this factor but his reasons do not seem convincing since such a shift clearly did occur on a large scale with the emer- gence of Amsterdam's lead later on.

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

408 Tony Porter

by the Genoese in 1277, became intense after 1320 (Braudel, 1984: 114; De Roover, 1963: 133). There was a connection here with the monetary crisis: Florence's rival sea-going city-states sought, and succeeded, to obtain access to the German silver mines and to the silver-based Mongol commercial networks, undermining the domi- nant role of gold.18

In sum, in this first logistic a financial cycle of innovation, maturity, crisis and decline was central to the initial period of ex- pansion and growth, to the emergence of Florentine hegemony, and to the downturn and hegemonic decline. By the mid-fourteenth century Europe was in severe recession.19

Logistic 2, 1350-1600: Venice, Genoa, and South Germany

The second logistic is marked by three momentous financial transformations. The first is the creation of a market for flexible short-term trade credit oriented to shipping. The second is the ap- propriation of large-scale supplies of bullion from the Americas and its use to expand the money supply. The third is the use of large- scale banking firms to finance states. While Florence initially contin- ued to play an important role in these transformations, it relied too heavily on old institutions and therefore faded.20 Venice, South Germany and Genoa, by contrast, were the leading innovators, and were able to translate their financial power into an unprecedented

18 This interpretation is based on Bautier (1971), Braudel (1984), and Cipolla (1982). Braudel (1984: 114) suggests that the Italian fleets were interested in German silver. Silver had been more central to the Venetian economy than the Florentine due to its role in Venice's Middle Eastern trade (Cipolla, 1982: xii). Thus one could inter- pret the sea route as involving a further erosion of the Florentine gold-based interna- tional monetary system. On the other hand it should be noted that de Roover (1963: 134) argues that the increased importance of gold at the end of the thirteenth century played a role in the demise of the financial firms at the Champagne fairs. 19 For an account that also emphasizes the centrality of finance and credit in the onset of this depression see Bautier (1971: 153, 169).

^° In this second logistic influential Florentine financial practices did not completely disappear. Florentine firms continued to be active in the fairs in France in the period of their revival, which peaked around 1500. The Florentine Medici Bank, for a period of time, played a role similar to the Fuggers of south Germany, except for the French state rather than for the Hapsburgs. These activities, while important, were not as cen- tral to the transformation of the European economy during this logistic, however. On the significance of the innovations that separated pre-1348 and post-1348 practices see de Roover (1963: 44).

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

INNOVATION IN GLOBAL FINANCE 409

political influence. By the end of the logistic, however, they too had passed their zenith, clearing the way to the rise of Dutch hegemony in the third logistic. I will trace these events in this section.

The importance of trade credit was evident in the changing rela- tive positions of the Italian city-states. After the crisis of the mid- fourteenth century, Florentine influence began to be displaced by those Italian city states which were more oriented to the sea route to northern Europe. Foremost among these city-states was Venice, but Genoa also played a key role.21 Indeed, Venetian ascendancy was marked by a halt to military conflict between these two rivals with a peace treaty signed in 1381 after the battle of Chioggia (Braudel, 1984: 118).

The key Venetian financial innovation was the creation of a sys- tem of short-term flexible trade credit organized around commer- cial shipping. While Venice lagged behind Florence in the creation of banks and the use of the bill of exchange, its innovations in trade credit were ideally suited to a role in re-establishing a new European growth logistic:

The entire Venetian population seems to have been advanc- ing money to the merchant venturers, thus perpetually creat- ing and renewing a sort of commercial society embracing the whole town. This constantly available and spontaneously offered supply of credit made it possible for merchants to operate alone or in temporary associations of two or three partners, without the need for the long-term companies with capital funds which characterized the most advanced commer- cial activity in Florence (Braudel, 1984: 130-31). Genoa too was highly flexible in commercial and financial mat-

ters, and like Venice was building sea-based trade routes which were to become central to the emerging European economy of this growth logistic (Braudel, 1984: 162-63). Indeed, Abu-Lughod notes that participation in trade finance was even broader than Venice, and involved the creation of a market in transferrable shares that bore a close resemblance to modern joint-stock companies (1989: 118-19).22

21 Abu-Lughod attributes a persistent underestimation of Genoa's influence to the

attractiveness of present-day Venice as a tourist site for visiting scholars (1989: 131). 22 For a detailed description of Venetian and Genoese overseas trade contracts see

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

410 Tony Porter

The displacement by Venice and Genoa of Florence is evident in accounts of the role of Italians in England (Fryde, 1983: Gh. 14). Until 1340, at the end of the first logistic, Florentines had played the leading role, importing wool from England to be manufactured in Florence. By contrast, in the second logistic Genoa played a lead- ing role in supplying the chemicals and dyes needed for the bud- ding English textile industry and in bringing English textiles to Iberian and other Mediterranean markets. Florentine exports and imports in this period were carried on Genoa's ships.

Genoese innovations in finance and trade played a key role in the rise of first Portugal and then Spain in this period. As Waller- stein notes, "the Genoese, the great rivals of the Venetians, decided early on to invest in Iberian commercial enterprise and to encour- age their efforts at overseas expansion" (1974: 49). Bullion was cen- tral to European trade with Asia and the successful search for it was an important factor in Iberian expansion into the Americas. In the sixteenth century the Genoese came to play a commanding role through their financing of trade and of the monarchy (Pike, 1966: 48; Wallerstein, 1974: 173).

The inflows of bullion from the Americas had a profound im- pact on the European economy and enhanced Genoese influence. In its initial phases it stimulated trade both within the continent and between Europe and Asia. Braudel comments, that "the galleys laden with chests of reals or ingots which began arriving in fabulous quantities in Genoa in the 1570s were unquestionably an instru- ment of domination. They made Genoa the arbiter of the fortune of the whole of Europe" (1984: 166). The 40% decline in revenues from Spanish colonies over the first 20 years of the seventeenth century had a severe impact on trade (Hart, 1993: 159).

The third financial innovation of this logistic, the use of large-scale banking firms to finance states, was first developed in South Ger- many, but then soon emerged in Genoa as well. The transformation, which took place between 1490 and 1520 (Bergier, 1979: 107) was evident in the collapse of the financial markets at Bruges, which had been dominated by the Italians, in the early 1490's and the transfer of banking functions to Antwerp, where German banks dominated.

de Roover (1963: 49-59). This account makes clear the dual function of these financial instruments in mobilizing credit and organizing economic life.

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

INNOVATION IN GLOBAL FINANCE 411

This transformation was not just spatial or ethnic, but more im- portantly involved the adoption of a more centralized structure that allowed the banks to more effectively mediate between dispersed lenders and borrowers (Bergier, 1979: 123), and to more effectively deal with lending to states, which had evolved into large-scale com- plex projects afflicted by severe monitoring problems.

The rise of the Fugger bank from 1473 to 1525 illustrates the importance of this new bank structure. Its success was built on its ability to lend vast sums of money to Hapsburg emperors Maximili- an I and Charles V in exchange for pledges of the production from Germany copper and silver mines. Indeed Fugger money was decisive in Charles V's election as Holy Roman Emperor (Ehren- berg, 1963: Ch. 1; Packard, 1927: 21). In part this success was due to the inadequacy of existing forms of public finance in the face of new demands- easily mortgaged assets had been exhausted and forced loans had reached the limit of toleration of subjects (Ehren- berg, 1963: introduction). Previous decentralized private firms were also inadequate to deal with such challenges as well due to the need for a powerful monitoring and bargaining capability. This new cen- tralized institution, the largest firm that had ever existed, also per- mitted the rapid transmittal of funds across Europe for the pay- ment of the widely dispersed Hapsburg troops.

The Fugger bank's structure was also decisive in allowing it to raise capital on the blossoming Antwerp market, its key source of financing in the 1540's and 1550's (Ehrenberg, 1963: 112). This market was much more atomistic and competitive than the Bruges market had been, and the reputation of the Fugger bank was crit- ical in the willingness of dispersed investors to supply funds to the distrusted Hapsburg state. As Ehrenberg says, "they borrowed large sums in Antwerp, usually at 8-10% per annum, and their credit was so good that in the general mistrust and the absence of 'good bor- rowers' everyone 'looked out for the Fugger Bonds' " (1963: 116).

The demise of the Fugger bank was in part due to the diffusion of its unique organizational structure. Starting in 1557 the Genoese began displacing the south Germans, specializing in loans to Spain, and drawing on alternate capital markets in northern Italy, Lyons, and Lisbon (Ehrenberg, 1963: 126).

The demise of the Fugger bank, however, also indicates the limits of this form of organization. Ehrenberg notes that "in the spring of 1557 the over expansion of credit in Antwerp had reached

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

412 Tony Porter

the danger-point" (1963: 114). The second half of the sixteenth century was marked by financial crisis. "Bourse loans in Antwerp reached manic proportions in the 1550's" (Kindleberger, 1984: 45) and collapsed when the Hapsburgs defaulted. As "Spanish finances staggered from crisis to crisis" (Kindleberger, 1984: 45) the Fugger bank found it increasingly difficult to raise money, and could not cut back its loans sufficiently, folding in 1596. The institutional innovation of a highly centralized bank, led by a family with close personal ties to state leaders, had reached its limits: "the Fugger were so closely linked with the Hapsburgs that . . . they could not escape their demands for money" (Ehrenberg, 1963: 117). While the Genoese banks were able to prolong their arrangements with the Spanish state, they too began to decline after the Spanish bank- ruptcy of 1627 (Braudel, 1984: 170). The foretaste of the successor to these highly centralized banks was present in the Antwerp capital markets which would soon be displaced by more sophisticated ar- rangements organized around Amsterdam.

In part the downturn of the second logistic, and of the financial arrangements that had sustained its upswing, was driven by the de- structiveness of the frequent wars of this period. Yet the downturn could also be viewed as the exhaustion of the innovative financial and commercial institutions that had been so important in opening the Atlantic trade routes, expanding the production of money through the import of bullion, linking Europe to the Asian econo- my, and financing state creation through the use of large banks linked to emerging capital markets. The wars would certainly not have been possible without the financial system, and they subsided when they could no longer be financed. When the financial system developed further, in the third logistic, a new round of warfare erupted. Thus it is as plausible that the direction of causation runs from finance as the reverse.

The Third Logistic, 1620-1800: Dutch hegemony

The third logistic is marked by three consequential financial innovations: joint stock companies, sophisticated international securities and commodities markets, and a revolution in govern- ment finance. These were centered on Amsterdam, sustaining

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

INNOVATION IN GLOBAL FINANCE 413

Dutch hegemony, which Wallers tein dates from 1625 to 1672.2S The Dutch empire in Asia was facilitated by the innovative insti-

tutional structure of the Dutch East Indies Company. In 1609 the directors of the Company created shares with the following charac- teristics: The capital was permanent and could not be returned to shareholders; shares were easily transferable in the Amsterdam securities market; they conferred no control over the company which was retained by the directors; they were available to foreign- ers; and they paid out substantial dividends regularly. The perma- nent nature of the capital sharply differentiates this arrangement from the Italian companies of the earlier period, which were more temporary and were re-established every few years. These Dutch innovations preceded the adoption of similar ones by the English, their leading competitor, by 40 to 90 years (Neal, 1990: 9, 118). These innovations allowed the Company to raise large amounts of capital and to deploy this capital with a high degree of autonomy from investors.24

As Braudel makes clear, the Dutch empire in Asia relied on transferring products between one Asian market and another (1984: 220-32). The structure of the Company was ideally suited to this task, as its bureaucratic structure allowed it to coordinate these far-flung trading operations, and its autonomy allowed it to carry out these operations without the need for close monitoring by Am- sterdam capital markets.

The capital and commodity markets in Amsterdam were qualita- tively different than earlier markets in Champagne, Bruges, and Antwerp. The trading of commodities was not only ongoing, but also involved a large-scale capacity for storage, allowing greater con- trol over the flow of goods with respect to disruptions such as bad harvests or political instability. An important factor in the success of the Dutch East Indies Company was the creation of a stock

23 The creation of public banks, most notably the Exchange Bank of Amsterdam in 1609 and the Bank of England in 1694 was also important In my view these innova- tions were not as momentous as the ones discussed in this section, however, and primarily had the effect of consolidating earlier innovations in private banking. 24 Clearly novel financial practices were only one aspect of the innovativeness of the joint-stock companies. The relationship of these companies to their sponsoring states, as codified in charters (Packard, 1927: 17) was also important On the other hand, by primarily focusing on non-financial factors Coornaert (1967) provides no explanation for why the Dutch preceded the British historically.

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

414 Tony Porter

market, making shares transferrable and creating the possibility of capital gains. Neal (1990) has shown that capital markets in this peri- od were surprisingly integrated across borders, with prices of identical shares on Amsterdam and London markets moving in tandem. By 1688 innovations included futures and options (Neal, 1990: 16).

The Dutch also gained substantial advantage in political and military competition from their innovations in public finance. The most important of these was the creation of a market in long-term, low interest debt, as opposed to taxation, debasement, forced loans, or short-term, high-interest loans. Dickson (1967) and Kennedy (1988) have stressed the importance of such a financial revolution for Britain in its struggle with France- the French state relied in- stead on increased taxation and collapsed due to popular anger in 1789. The Dutch pioneered this innovation, however: Between 1611 and 1655 Holland managed to reduce interest payments on its debt from 6.25% to 4%, while the English state was paying 10% and the French state 15% (Hart, 1993: 163). The key instrument was the life annuity, a sharp contrast to the use of the Fugger bank by the Hapsburgs due to the disintermediated, popular, and commodified nature of these annuities. Hart comments "there were, in fact, an amazing number of people who brought their funds to the coffers of the state, who obviously trusted the state, and among them were quite ordinary persons" (1993: 174). As in the British financial revo- lution, the accountability of the state to its wealthy elites as a result of democracy (in England) and decentralization (in the United Provinces) enhanced creditworthiness and trust.

The innovative features of Dutch financial structures bore the seeds of their own demise and were subsequently displaced by more sophisticated English ones. This was evident in both corpo- rate and public finance. I will look at these in turn.

The crisis of Dutch corporate finance was signalled by the fall of the Dutch East Indies Company's share prices relative to those of its English competitor between 1723 and 1794 (Neal, 1990: 121). There are three key aspects of the obsolescence of Dutch struc- tures. The first aspect is that they were being imitated by competi- tors (Neal, 1990: 131).

The second aspect is that the company became inflexible and corrupt, missing opportunities and wasting its revenues. Inflexibility was evident in the loss of the Chinese connection to the British: The Dutch had been trading Indonesian pepper for Chinese tea,

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

INNOVATION IN GLOBAL FINANCE 415

but starting in 1698 they were cut out by the British who began purchasing tea directly from the Chinese with cash (Braudel, 1984: 222). Braudel cites corruption and excessive spending by the Com- pany's officers in Asia as a key reason for its economic decline (1984: 228-30). The Dutch West Indies management has been blamed for its failure to compete with the British in the Americas (Braudel, 1984: 234). Two features of English capital markets re- duced the prevalence of these problems in its companies: The first was the greater pressure that stockholders were able to put on di- rectors in England (Neal, 1990: 9), and the second was the sophis- tication of the English information network, including newspapers, periodicals, and printed stock price lists.25

The third and most serious aspect of the obsolescence of Amster- dam centered financial institutions was the crisis in international capital markets in 1719 and 1720. This crisis included the Mississippi Bubble in France, the South Sea Bubble in England, and less well- known speculative bubbles in Holland and Germany (Neal, 1990: Chs. 4, 5; Kindleberger, 1984, 1989). The key features of the Missis- sippi and South Sea bubbles illustrate the problem. In both cases there were unfounded promises of new overseas companies that would duplicate the successes of the East Indies Companies. In addi- tion the companies were used to convert short-term war debt of France and England respectively into long-term debt by having inves- tors exchange government debt for stock in the companies. The gov- ernment reduced the cost of funding the debt since shareholders accepted a lower rate of return in exchange for transferability and capital gains. In both cases the rapid appreciation of stock prices was brought about by paying generous dividends out of the capital from subsequent issues rather than from real investments. In both cases a financial arrangement that had worked well in an earlier period sub- sequently proved to be dangerous. In the wake of the bubbles there were severe limitations for over a century on the growth of joint stock companies in England and of banks in France (Neal, 1990: 62).

There are two aspects of the crisis of the Dutch model of public finance. The first was evident in the bubbles of 1719 and 1720. The conversion of short-term public debt into long-term debt was a key

25 Neal (1990: 21). Similar problems in the English East India Company were not entirely eliminated, however. See Kindleberger (1984: 190-91, and 234-36).

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

416 Tony Porter

aspect of these bubbles and the collapse of the bubbles indicated a mismatch between the financial institutions involved in transform- ing this debt and the actual revenues of the states. Neither war nor the granting of foreign trade monopolies was an adequate basis for reliably funding the debt, a fact that investors were unable to assess correctly until financial collapse had occurred.

The second aspect of the crisis of the Dutch model of public fi- nance was the migration of Dutch investments from the funding of Dutch state and industry to the financing of risky public debt in other countries. Explanations for this shift have included a loss of enthusiasm for risk-taking (see Braudel, 1984: 246, who calls the reliance on finance a "sign of autumn") and a search for the higher returns abroad, due to high labor costs at home (Riley, 1980). Most European states made abundant use of Dutch capital markets and this initially contributed to growth. As Riley notes, however,

the new credit structure was no more than an expedient re- sponse to continued, more frequent, and more substantial deficits. Its management was entrusted to a capital market inexperienced in such matters, a market that, because lenders failed to become informed about inflationary patterns, debt levels, and other trends, could not perform its regulatory charge satisfactorily. Although the Amsterdam market was adept at improving access to savings and at rapidly mobilizing large sums, it was not adept at manipulating capital availabili- ty and credit cost to restrain deficit spending. By the eve of the wars of the French revolution cumulative debts among borrowing powers were many times larger than the sum of each year's current revenues (1980: 4). These problems culminated in the "pandemic of bankruptcy on

the continent" from 1788 to 1815, with France, Austria, Sweden, Denmark, and the United Provinces defaulting on their debt obliga- tions (Riley, 1980: 201).

The system of commercial credit appears to have expanded ex- cessively rapidly in this period as well, contributing to inflation (Riley, 1980: 27). As Braudel comments, "there is no comparison between these early [Italian] expansions of credit and the deluge of paper that occurred in the eighteenth century: 4, 5, 10 or 15 times the specie in circulation" (1984: 244). Braudel (1984: 267-68) and Kindleberger (1989: 136) see this overexpansion in large part respon-

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

INNOVATION IN GLOBAL FINANCE 417

sible for the crises of 1763, 1772-73, and 1780-83, the penultimate signals of the demise of the role of the Dutch in the world economy.

Looking at the third logistic as a whole, we see the creation of joint-stock companies, international securities markets, and new forms of public finance, as contributing to expansion and growth initially. At the end all three of these institutional innovations were in deep crisis. As at the end of the second logistic there was politi- cal and military turmoil as well as financial crisis. Yet, once again, one can see the direction of causation running from finance to war as opposed to the reverse. The lending to foreign governments would not have expanded so sharply had investments in Dutch in- dustry and commerce continued to be as profitable as in the heyday of the joint stock companies. The foreign governments would not have been able to fund wars as easily had the financial system been better able to exercise a monitoring function.

The Fourth Logistic, 1800-1900: British hegemony

During the fourth logistic the center of gravity of the world economy shifted to London and involved new financial institutions. Wallerstein's dates for British hegemony are from 1815 to 1873. During this logistic the major financial innovation was the creation of an international market, centered in London, for transferable bonds issued by foreign states and linked to production rather than to war or trade. The second major innovation was the gold stan- dard. I will address these in turn.

That the financial transition between the third and fourth logis- tics involves the replacement of financing of war by the financing of industry is evident in Neal's (1993) account of the French revolu- tion and subsequent wars which sundered Europe from 1793 to 1815. Neal shows that international capital markets were sufficiently developed to make possible large-scale capital flight from revolu- tionary Europe to England. In part this inflow of capital helped fi- nance the war against France. More importantly, however, it fueled investment in British industry- indeed Neal attributes the British in- dustrial revolution to this inflow. Neal notes that the British stock exchange was reorganized in 1810, stocks of waterworks, canals, railroads, and mines began to be listed, and there was a large in- crease in the number of bills passed by Parliament initiating such infrastructural projects (1990: 206, 216).

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

418 Tony Porter

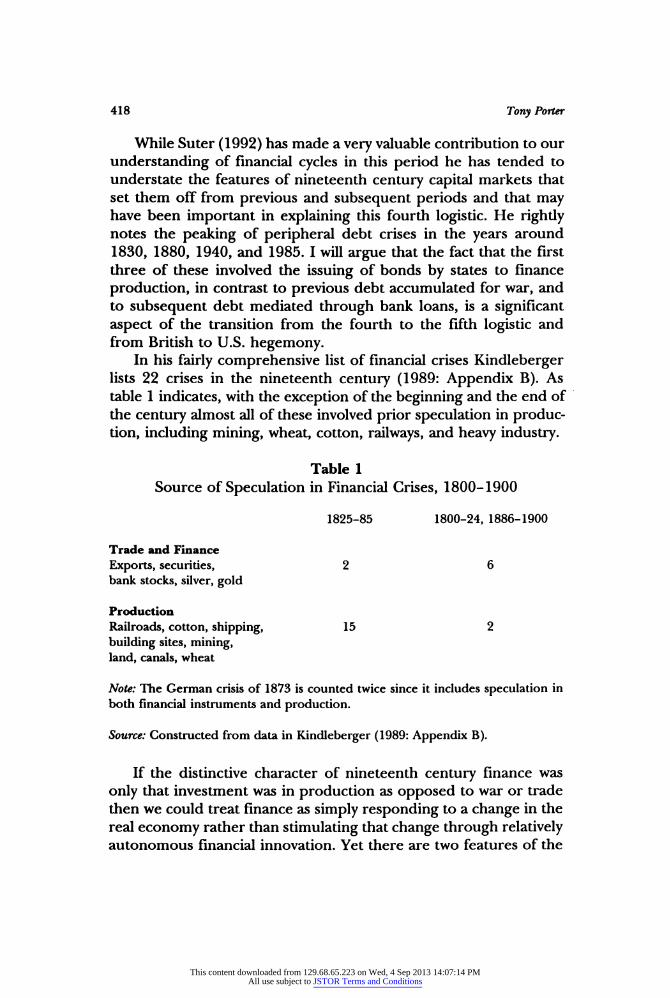

While Su ter (1992) has made a very valuable contribution to our understanding of financial cycles in this period he has tended to understate the features of nineteenth century capital markets that set them off from previous and subsequent periods and that may have been important in explaining this fourth logistic. He rightly notes the peaking of peripheral debt crises in the years around 1830, 1880, 1940, and 1985. I will argue that the fact that the first three of these involved the issuing of bonds by states to finance production, in contrast to previous debt accumulated for war, and to subsequent debt mediated through bank loans, is a significant aspect of the transition from the fourth to the fifth logistic and from British to U.S. hegemony.

In his fairly comprehensive list of financial crises Kindleberger lists 22 crises in the nineteenth century (1989: Appendix B). As table 1 indicates, with the exception of the beginning and the end of the century almost all of these involved prior speculation in produc- tion, including mining, wheat, cotton, railways, and heavy industry.

Table 1 Source of Speculation in Financial Crises, 1800-1900

1825-85 1800-24, 1886-1900

Trade and Finance Exports, securities, 2 6 bank stocks, silver, gold

Production Railroads, cotton, shipping, 15 2 building sites, mining, land, canals, wheat

Note: The German crisis of 1873 is counted twice since it includes speculation in both financial instruments and production.

Source: Constructed from data in Kindleberger (1989: Appendix B).

If the distinctive character of nineteenth century finance was only that investment was in production as opposed to war or trade then we could treat finance as simply responding to a change in the real economy rather than stimulating that change through relatively autonomous financial innovation. Yet there are two features of the

This content downloaded from 129.68.65.223 on Wed, 4 Sep 2013 14:07:14 PMAll use subject to JSTOR Terms and Conditions

INNOVATION IN GLOBAL FINANCE 419

institutional structure of finance in this period that explain the rise and decline of this type of financing: the creation of national bank- ing systems; and the institutionalization of securities markets.

We are most familiar with the key role played by national bank- ing systems in continental Europe thanks to the work of Gerschen- kron (1966) who argued that a national structure of financial inter- mediation in France and Germany substituted for the competitive capital markets upon which British industrialization had relied. Yet, as Kindleberger (1984: 77-79; 202) and Cameron (1967) argue, the creation of a national banking system and of limited liability joint stock company law was central to the funding of industry in Britain as well. An institutionalization of stock markets occurred at this time as well: In Britain a new stock exchange building was opened in 1802 and stock exchange regulations were codified in 1812 (Neal, 1990: 225).

The international financial system of the nineteenth century built on these innovations. The banking system mobilized funds for foreign investment, and this investment took place through the sale of foreign bonds on the London stock market. In addition to the more sophisticated monitoring capacity of the London market as compared to the Amsterdam market, as noted above, the system worked because the largest number of investments were held by relatively few wealthy individuals, because these individuals orga- nized themselves as the Committee of Foreign Bondholders to negotiate with foreign governments, because projects were often large infrastructural investments carried out or regulated by the state, because the technology involved in the investments was rela- tively familiar to investors, and because the focus of investment was in the countries that were well on the way to industrialization, such as the U.S., Canada, Russia, and Australia (Lipson, 1985; Stallings, 1987; Su ter, 1993). This system mobilized unprecedented quantities of capital for foreign investment.