initiation: underrated geothermal powerhouse 1...

TRANSCRIPT

See important disclosures, including any required research certifications, beginning on page 36

■ Investment case We initiate coverage on Energy Development Corp (EDC) with a Buy (1) rating. Year to date, the shares have fallen by 6%, and we see the current share price weakness as a good buying opportunity – we forecast EDC to post EPS growth of 11-19% YoY for 2015-16, driven primarily by 194MW of new capacity added over the past year.

World leader in geothermal energy and diversified renewable energy (RE) player. Often seemingly overlooked by investors, EDC is the world’s largest integrated geothermal firm and is among the few with end-to-end expertise in geothermal energy. This allows it to lead exploration domestically and overseas. In October 2015, it will conduct its first major drilling overseas, in Chile. Aside from geothermal power, EDC has diversified into hydro, solar and wind power over the past 7 years. These ventures have added 233MW in

capacity, bringing EDC’s portfolio to 1,402MW. From around 3% for 2014, we expect these businesses to account for 14% of net profit in 2016E. Stronger after recent issues. EDC’s operations and earnings have fully recovered from past setbacks, in our view, adding 194MW over the past year. These developments were reflected in EDC’s 40% YoY net profit growth, and the stock’s 54% gain in 2014, and should continue to boost net profit until end-2016E. Moving forward, EDC has identified 7 new domestic projects with indicative capacity of 188MW. ■ Catalysts The share price has recovered from its YTD low of PHP7.22 on 8 July 2015. We identify these positive catalysts, which should continue to support its rebound over the next 12 months: 1) removal of transmission-line constraints at Burgos Wind, 2) construction of Bacman 3, and 3) good results from its Chile drilling. ■ Valuation We initiate with an SOTP-based 12-month TP of PHP9.24, implying upside potential of 20%, in addition to a 2016E dividend yield of 2.9%. The stock is trading currently at respective 2015-16E PERs of 14.2x and 12.0x, which are below the regional averages of 16.0x and 12.7x,

respectively (Bloomberg consensus and Daiwa forecasts). ■ Risks The main downside risks to our call would be operational risks due to natural disasters and steam field/power plant issues.

Utilities / PhilippinesEDC PM

24 July 2015

Energy Development

Initiation: underrated geothermal powerhouse

• Has added 194MW over the past year, which should boost EPS growth in 2015E (+11% YoY) and 2016E (+19% YoY)

• End-to-end technical expertise in geothermal power serves as a platform for exploration and expansion

• Recent share-price pullback presents a buying opportunity; coverage initiated with a Buy (1) rating and TP of PHP9.24

Source: FactSet, Daiwa forecasts

Utilities / Philippines

Energy DevelopmentEDC PM

Target (PHP): 9.24Upside: 20.0%24 Jul price (PHP): 7.70

Buy (initiation)

OutperformHoldUnderperformSell

1

2

3

4

5

95

105

115

125

135

6.0

6.8

7.5

8.3

9.0

Jul-14 Oct-14 Jan-15 Apr-15 Jul-15

Share price performance

Energy Dev (LHS)Relative to PCOMP Index (RHS)

(PHP) (%)

12-month range 6.14-8.96Market cap (USDbn) 3.183m avg daily turnover (USDm) 3.32Shares outstanding (m) 18,750Major shareholder Lopez Group (50.6%)

Financial summary (PHP)Year to 31 Dec 15E 16E 17ERevenue (m) 34,118 37,273 39,211Operating profit (m) 16,305 17,917 18,572Net profit (m) 10,160 12,066 12,921Core EPS (fully-diluted) 0.542 0.644 0.689EPS change (%) 10.6 18.8 7.1Daiwa vs Cons. EPS (%) (4.1) (1.1) (3.8)PER (x) 14.2 12.0 11.2Dividend yield (%) 2.6 2.9 3.5DPS 0.200 0.224 0.266PBR (x) 3.0 2.6 2.2EV/EBITDA (x) 9.5 8.7 8.2ROE (%) 22.4 23.0 21.4

Bianca Solema(63) 2 737 [email protected]

How do we justify our view?How do we justify our view?

Utilities / Philippines EDC PM

24 July 2015

- 2 -

Investment thesis ........................................................................................................................... 6

Underrated geothermal powerhouse .......................................................................................... 6

Key catalysts ................................................................................................................................. 7

A world leader in geothermal energy ............................................................................................. 8

Largest integrated geothermal company .................................................................................... 8

Coming out stronger from recent trials ...................................................................................... 9

Evolving into a diversified pure-play RE company ...................................................................... 11

Diversified into hydro, solar and wind power generation ......................................................... 11

Mid- and long-term growth opportunities in sight ...................................................................... 14

Maximising domestic resources ................................................................................................ 14

Leading overseas exploration .................................................................................................... 15

Predictable cash flow with upside from new projects .................................................................. 17

Long-term contracts provide stable and predictable cash flow ................................................ 17

New initiatives to deliver growth ............................................................................................... 18

Valuation: undemanding with attractive prospects .................................................................... 20

TP of PHP9.24 offers upside potential of 20% ......................................................................... 20

Cheap among its peers .............................................................................................................. 22

Sensitivity analysis .................................................................................................................... 24

Key risks ........................................................................................................................................ 25

Appendix I: company profile ......................................................................................................... 27

Appendix II: geothermal energy .................................................................................................. 29

Appendix III: Philippine power industry ..................................................................................... 30

Support for RE sector in the Philippines .................................................................................. 30

Power-supply demand scenario ................................................................................................. 31

Contents

Utilities / Philippines EDC PM

24 July 2015

- 3 -

Growth outlook EDC: recurring net profit after preferred dividends (PHPm)

In 2014, EDC posted record-high recurring net profit (after preferred dividends) of PHP9.19bn, up a robust 40% YoY, mainly on the back of the partial return-to-service of Bacman and commercial operations of the Nasulo plant. For 2015E and 2016E, we still expect the company to post double-digit profit growth, albeit at a lower rate than in 2014. We forecast 11% YoY growth for 2015 to PHP10.16bn still driven by Nasulo and the partial operations of Bacman. By 2016, a full contribution from Burgos Wind and Bacman, together with the return-to-service of one unit of Tongonan plant, should lift EDC’s earnings to PHP12.07bn, up 19% YoY.

Source: EDC, Daiwa forecasts

Valuation EDC: 12-month forward PER bands

Separately valuing each RE technology using the DCF method, we arrive at our SOTP-based 12-month target price of PHP9.24. This is computed using a WACC of 8.26% and terminal growth of 3%, and implies upside potential of 20%, in addition to a dividend yield of 2.9% in 2016E. EDC is trading currently at a PER discount to its regional peers in the power generation sector. Based on its closing price of PHP7.70/sh on 24 July 2015, the stock was trading at a 2015E PER of 14.2x and 12.0x for 2016E, which are well below the regional averages, as forecast by the Bloomberg consensus, of 16.0x and 12.7x, respectively.

Source: Daiwa, Bloomberg, EDC

Earnings revisions EDC: Bloomberg consensus 2015 adjusted EPS forecasts

The Bloomberg consensus lowered its adjusted 2015 EPS forecast from a high of 0.68 in February to PHP0.57 in June, which we attribute to the factoring in of continued transmission line constraints for Burgos Wind, lower rates from the repricing of the contracts of a subsidiary, as well as the repairs to one unit at the Tongonan plant. Our core EPS forecast of PHP0.54 for 2015 is slightly lower than that of the consensus, but still implies YoY growth of 11%. Following the consensus downgrades, EDC’s share price has fallen by 6% YTD. Given our EPS growth forecast of 19% YoY for 2016, we believe the current share-price weakness instead presents a buying opportunity.

Source: Bloomberg

How do we justify our view?

Growth outlook

Valuation

Earnings revisions

8,514

6,558

9,190 10,160

12,066 12,921

14,019

2012 2013 2014 2015E 2016E 2017E 2018E

-23%+92% +40% +11% +19% +7% +9%

0

2

4

6

8

10

12

14

16

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14

(PHP/sh)

4.9x

9.8x

14.7x

19.6x

24.5x

-

2.00

4.00

6.00

8.00

10.00

0.50

0.55

0.60

0.65

0.70

Jun-14 Sep-14 Dec-14 Mar-15 Jun-15

(PHP/sh)(PHP/sh)

2015 EPS (LHS) Price (RHS)

Buy (initiation)

OutperformHoldUnderperformSell

1

2

3

4

5

Utilities / Philippines EDC PM

24 July 2015

- 4 -

Key assumptions

Profit and loss (PHPm)

Cash flow (PHPm)

Source: FactSet, Daiwa forecasts

Year to 31 Dec 2010 2011 2012 2013 2014 2015E 2016E 2017EInflation (YoY%) 3.80 4.70 3.10 2.90 4.20 3.60 3.10 3.50

Consolidated volume sales incl. ancillary services (GWh)

7,548.6 7,072.0 7,518.0 6,781.0 7,832.4 8,363.3 8,677.8 8,795.0

Ave price of geothermal energy sales (PHP/kWh)

3.18 3.37 3.59 3.70 3.91 3.91 4.07 4.23

Year to 31 Dec 2010 2011 2012 2013 2014 2015E 2016E 2017ESale of electricity 22,944 24,540 28,369 25,656 30,867 34,118 37,273 39,211Sale of steam 1,209 0 0 0 0 0 0 0Other Revenue 749 0 0 0 0 0 0 0Total Revenue 24,902 24,540 28,369 25,656 30,867 34,118 37,273 39,211Other income 0 0 0 0 0 0 0 0COGS (10,474) (7,382) (6,629) (6,234) (7,650) (7,904) (8,504) (8,930)SG&A (4,529) (4,398) (4,319) (3,964) (5,329) (4,795) (5,200) (5,454)Other op.expenses (3,445) (3,442) (3,579) (3,569) (4,079) (5,114) (5,654) (6,255)Operating profit 6,454 9,318 13,841 11,889 13,809 16,305 17,917 18,572Net-interest inc./(exp.) (3,361) (3,716) (3,339) (3,090) (3,569) (4,540) (4,178) (3,865)Assoc/forex/extraord./others 4,601 (402) 411 (859) 317 0 0 0Pre-tax profit 7,694 5,199 10,913 7,940 10,556 11,765 13,738 14,707Tax (777) 115 (775) (486) (1,223) (1,246) (1,260) (1,343)Min. int./pref. div./others (287) (871) (1,624) (896) (144) (359) (412) (444)Net profit (reported) 4,108 (167) 8,995 4,732 11,674 10,160 12,066 12,921Net profit (adjusted) 6,630 4,443 8,514 6,558 9,190 10,160 12,066 12,921EPS (reported)(PHP) 0.219 (0.009) 0.480 0.252 0.623 0.542 0.644 0.689EPS (adjusted)(PHP) 0.354 0.237 0.454 0.350 0.490 0.542 0.644 0.689EPS (adjusted fully-diluted)(PHP) 0.354 0.237 0.454 0.350 0.490 0.542 0.644 0.689DPS (PHP) 0.120 0.160 0.140 0.160 0.200 0.200 0.224 0.266EBIT 6,454 9,318 13,841 11,889 13,809 16,305 17,917 18,572EBITDA 9,899 12,760 17,420 15,458 17,888 21,419 23,570 24,827

Year to 31 Dec 2010 2011 2012 2013 2014 2015E 2016E 2017EProfit before tax 7,694 5,199 10,913 7,940 10,556 11,765 13,738 14,707Depreciation and amortisation 3,445 3,442 3,579 3,569 4,079 5,114 5,654 6,255Tax paid (200) (444) (563) (695) (637) (1,230) (1,260) (1,343)Change in working capital 694 1,580 494 (466) (1,985) 3,102 (361) (54)Other operational CF items 2,907 4,134 2,303 4,088 4,075 4,543 4,186 3,870Cash flow from operations 14,540 13,911 16,726 14,437 16,089 23,295 21,957 23,434Capex (5,948) (9,418) (7,180) (11,718) (18,617) (16,330) (16,388) (12,846)Net (acquisitions)/disposals (1,280) 5 (162) (102) (450) 0 0 0Other investing CF items (552) (1,488) (1,172) 1,019 (1,585) 0 0 0Cash flow from investing (7,779) (10,901) (8,515) (10,801) (20,652) (16,330) (16,388) (12,846)Change in debt (6,011) 10,329 (1,353) 7,908 10,624 5,643 (4,199) (1,993)Net share issues/(repurchases) 0 0 0 0 0 0 0 0Dividends paid (2,496) (3,341) (4,495) (3,959) (4,416) (3,758) (4,215) (4,999)Other financing CF items (3,285) 441 676 495 242 8 63 15Cash flow from financing (11,792) 7,429 (5,172) 4,445 6,451 1,894 (8,352) (6,977)Forex effect/others (32) 25 (4) 19 0 0 0 0Change in cash (5,031) 10,439 3,039 8,081 1,888 8,858 (2,783) 3,612Free cash flow 3,345 5,112 8,680 3,193 (4,563) 6,188 4,698 9,737

Financial summary

Utilities / Philippines EDC PM

24 July 2015

- 5 -

Balance sheet (PHPm)

Key ratios (%)

Source: FactSet, Daiwa forecasts

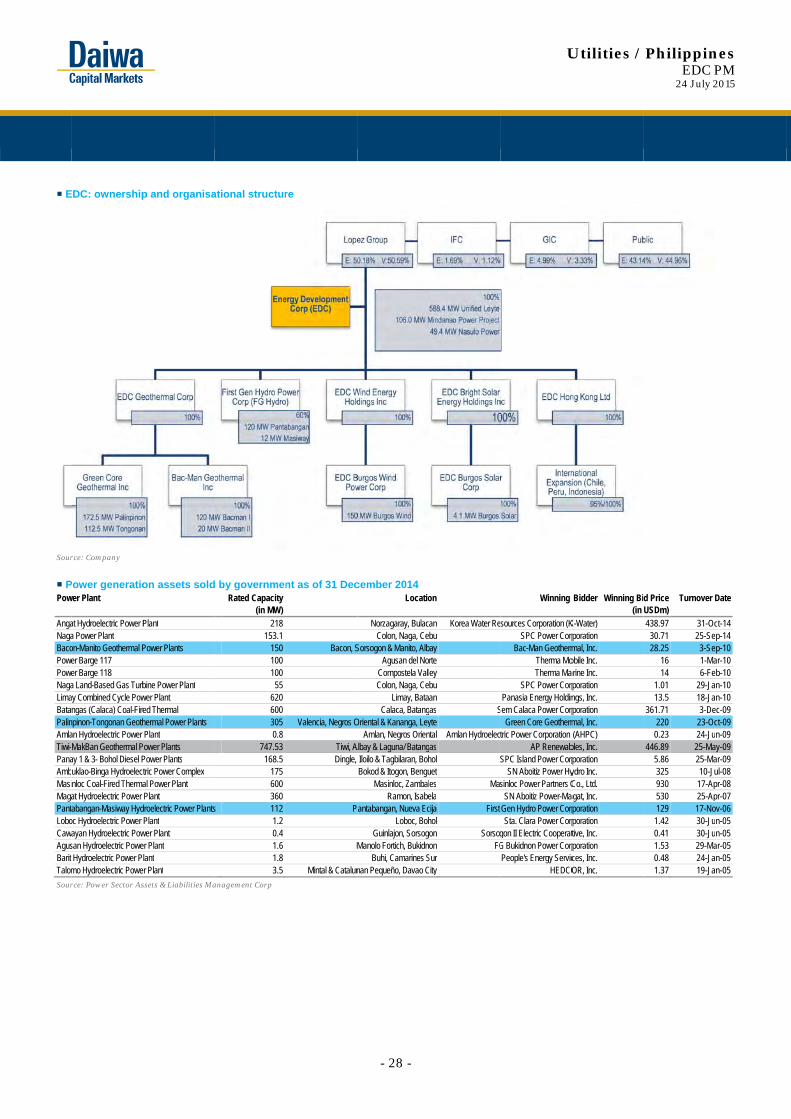

Company profile

Energy Development Corp (EDC) is a pure-play power generation company in the Philippines with capacity of 1,402MW. It is the largest integrated geothermal company in the world, but it also has ventures in hydro, wind and solar energy.

As at 31 Dec 2010 2011 2012 2013 2014 2015E 2016E 2017ECash & short-term investment 6,865 13,167 11,552 16,385 14,534 18,844 11,820 11,552Inventory 2,577 3,356 3,339 3,094 2,902 3,212 3,631 3,814Accounts receivable 4,602 3,411 4,116 3,611 6,888 6,956 7,532 7,901Other current assets 734 742 693 1,250 743 743 743 743Total current assets 14,779 20,676 19,700 24,340 25,067 29,755 23,725 24,010Fixed assets 57,850 58,764 62,284 68,621 85,875 97,205 108,054 114,760Goodwill & intangibles 4,543 4,705 4,818 4,400 4,543 4,428 4,314 4,200Other non-current assets 4,132 5,917 7,553 7,645 9,015 8,999 8,999 8,999Total assets 81,304 90,063 94,355 105,006 124,499 140,388 145,094 151,970Short-term debt 1,702 2,250 2,394 1,872 10,500 10,497 7,331 7,462Accounts payable 5,123 6,992 7,716 6,982 7,639 11,123 11,764 12,268Other current liabilities 661 79 140 54 112 112 112 112Total current liabilities 7,487 9,320 10,250 8,908 18,251 21,731 19,207 19,841Long-term debt 39,679 49,240 46,656 56,677 58,963 64,609 63,576 61,452Other non-current liabilities 1,899 2,516 2,741 3,176 3,666 3,666 3,666 3,666Total liabilities 49,065 61,076 59,647 68,761 80,879 90,006 86,448 84,959Share capital 25,110 25,111 25,122 25,127 25,130 25,130 25,130 25,130Reserves/R.E./others 5,560 1,659 7,516 9,112 17,000 23,410 31,269 39,198Shareholders' equity 30,670 26,770 32,638 34,238 42,130 48,540 56,399 64,328Minority interests 1,569 2,218 2,070 2,007 1,490 1,842 2,247 2,683Total equity & liabilities 81,304 90,063 94,355 105,006 124,499 140,388 145,094 151,970EV 180,460 184,915 183,943 188,546 200,794 202,478 205,708 204,419Net debt/(cash) 34,515 38,322 37,497 42,164 54,928 56,261 59,086 57,361BVPS (PHP) 1.636 1.428 1.741 1.826 2.247 2.589 3.008 3.431

Year to 31 Dec 2010 2011 2012 2013 2014 2015E 2016E 2017ESales (YoY) 12.8 (1.5) 15.6 (9.6) 20.3 10.5 9.2 5.2EBITDA (YoY) (0.6) 28.9 36.5 (11.3) 15.7 19.7 10.0 5.3Operating profit (YoY) (26.2) 44.4 48.5 (14.1) 16.1 18.1 9.9 3.7Net profit (YoY) (10.1) (33.0) 91.6 (23.0) 40.1 10.6 18.8 7.1Core EPS (fully-diluted) (YoY) (10.1) (33.0) 91.6 (23.0) 40.1 10.6 18.8 7.1Gross-profit margin 57.9 69.9 76.6 75.7 75.2 76.8 77.2 77.2EBITDA margin 39.8 52.0 61.4 60.3 58.0 62.8 63.2 63.3Operating-profit margin 25.9 38.0 48.8 46.3 44.7 47.8 48.1 47.4Net profit margin 26.6 18.1 30.0 25.6 29.8 29.8 32.4 33.0ROAE 22.3 15.5 28.7 19.6 24.1 22.4 23.0 21.4ROAA 8.3 6.1 11.1 7.5 8.1 7.9 8.7 9.0ROCE 22.4 15.5 28.8 19.7 24.1 22.5 23.0 21.4ROIC 8.5 5.6 10.1 7.2 8.6 8.3 9.3 9.6Net debt to equity 109.3 134.5 108.4 117.3 127.1 112.7 101.6 86.4Effective tax rate 10.1 (2.2) 7.1 6.1 11.6 10.6 9.2 9.1Accounts receivable (days) 73.9 59.6 48.4 55.0 62.1 74.0 70.9 71.8Current ratio (x) 2.0 2.2 1.9 2.7 1.4 1.4 1.2 1.2Net interest cover (x) 1.7 2.3 3.7 3.5 3.7 3.6 4.2 4.8Net dividend payout 41.4 50.0 30.3 50.3 40.2 40.0 40.0 40.0Free cash flow yield 2.3 3.5 6.0 2.2 n.a. 4.3 3.3 6.7

Financial summary continued …

Utilities / Philippines EDC PM

24 July 2015

- 6 -

Investment thesis

Underrated geothermal powerhouse

We initiate coverage of EDC with a Buy (1) rating and 12-month target price of PHP9.24, implying 20% upside potential. Moreover, the stock is trading currently at undemanding PER valuations of 14.2x for 2015E and 12.0x for 2016E, lower than the regional power generation sector averages of 16.0x and 12.7x, respectively, per the Bloomberg-consensus forecasts. EDC: SOTP valuation Equity

value EDC's stake

Attributable value

Value per share

(PHPm) (PHPm) (PHP/sh)Geothermal* 136,941 100% 136,941 7.30 Burgos Wind 23,003 100% 23,003 1.23 Burgos Solar 839 100% 839 0.04 FG Hydro 20,755 60% 12,453 0.66 Total 9.24

Outstanding common shares (m) 18,750

Source: Daiwa

Note: *Includes parent and others

We believe EDC’s market-leader position and technological expertise are underrated. It is the largest geothermal company in the world and one of only five companies that have full vertically integrated geothermal operations. Its expertise spans the entire geothermal value chain from exploration to power plant operations. It currently has over 1,169MW of installed geothermal capacity. EDC is also evolving into a diversified pure-play RE company. In addition to a 60% stake in FG Hydro, it recently completed the 150-MW Burgos Wind farm in November 2014 and the 4.1-MW Burgos Solar project in February 2015. Altogether, EDC’s attributable capacity is now 1,402MW, which accounts for 8% of the country’s total installed capacity as of end-2014. Good buying opportunity With EDC’s recovery from past setbacks reflected in its robust financial performance in 2014, the stock was one of the best-performing among the PSEi constituents in 2014, outperforming the market by more than 31pp. Year-to-date, however, the stock is down 6% and is lagging the market by 11.4pp.

EDC: share-price performance

Source: Bloomberg

We believe the current share-price weakness instead presents a good buying opportunity. Fundamentals remain intact with a healthy project pipeline of 7 identified domestic projects, equivalent to a total of 188MW, for the medium term and ongoing exploration overseas (Chile and Peru) for long-term earnings growth.

Double-digit growth as new projects begin to contribute In addition, we look for EDC’s core net profit to increase by 11% YoY for 2015E to PHP10.16bn, driven by fresh contributions from the 140-MW Bacman power plants which were brought back into service in 3Q14-1Q15 and the new 40-MW Nasulo plant. By 2016E, a full contribution from the 150-MW Burgos wind farm should boost our earnings forecast up by 19% YoY to PHP12.07bn. EDC: recurring net income after preferred dividends (PHPm)

Source: EDC, Daiwa forecasts

Technical backbone a unique platform for growth, in our view The company’s end-to-end expertise in geothermal energy which covers exploration up to power plant operations, allows it to lead greenfield exploration projects and maximise resources in existing concession areas. Aside from domestic undertakings, EDC is now

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

0

2

4

6

8

10

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14

(PH

P/sh

)

EDC PM Equity PCOMP Index

8,514

6,558

9,190 10,160

12,066 12,921

14,019

2012 2013 2014 2015E 2016E 2017E 2018E

-23%+92% +40% +11% +19% +7% +9%

Utilities / Philippines EDC PM

24 July 2015

- 7 -

actively exploring sites in Latin America (Chile and Peru) and looking for opportunities in Indonesia. We believe EDC’s technical expertise sets it apart from the other power companies in the Philippines, serving as a good way to ensure growth in both the domestic and international markets. Even in the global arena, EDC is one of very few companies with complete technical expertise in geothermal energy development. Coming out stronger from recent trials EDC has fully recovered from several setbacks over the past few years, but more importantly, we see that management has adopted measures to improve operations and prevent similar issues occurring in the future. In particular, it completed the transfer of the equipment of the impaired Northern Negros facility to Nasulo in 2014 and fully rehabilitated its Bacman facility in 1Q15. In addition, as a lesson from Bacman, it rolled-out a similar retrofit programme for other old units. It is also strengthening its facilities to withstand up to 300kph of wind, as much stronger typhoons are hitting its facilities including Super Typhoon Haiyan in November 2013. EDC: timeline of additional capacity included in forecasts 2014 2015E 2016E 2017E 2018EProject (MW) (MW) (MW) (MW) (MW)Existing Nasulo (net*) 29.4 Bacman rehabilitation/retrofit** 5.0 5.0 Burgos Wind 150.0 Burgos Solar 4.1 Bacman 3*** 30.0Tongonan retrofit 12.0Total 184.4 9.1 0.0 12.0 30.0

Source: Company, Daiwa estimates

Note: *Net of the 20-MW Nasuji unit of the Palinpinon plant which was put in preservation mode

**Only refer to the additional capacity resulting from the rehabilitation/retrofit. Total capacity of Bacman post-rehabilitation is 140MW

***Assumed completion by end-2017, start of operations beg-2018

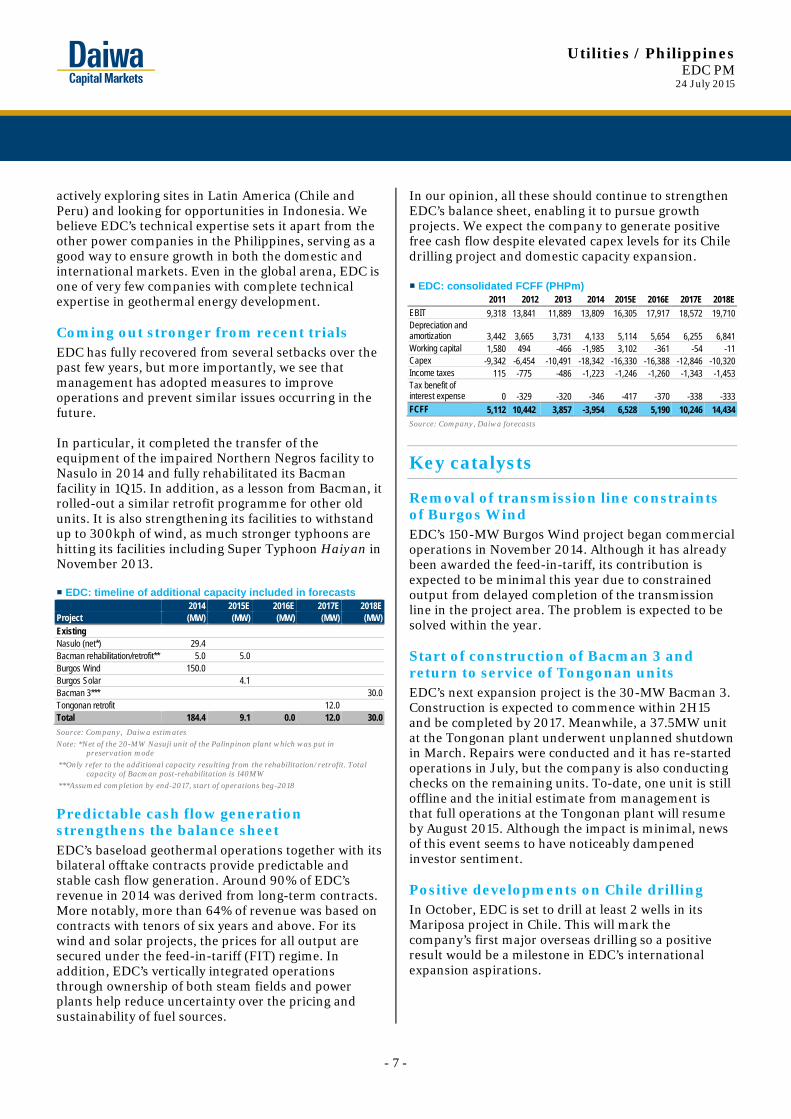

Predictable cash flow generation strengthens the balance sheet EDC’s baseload geothermal operations together with its bilateral offtake contracts provide predictable and stable cash flow generation. Around 90% of EDC’s revenue in 2014 was derived from long-term contracts. More notably, more than 64% of revenue was based on contracts with tenors of six years and above. For its wind and solar projects, the prices for all output are secured under the feed-in-tariff (FIT) regime. In addition, EDC’s vertically integrated operations through ownership of both steam fields and power plants help reduce uncertainty over the pricing and sustainability of fuel sources.

In our opinion, all these should continue to strengthen EDC’s balance sheet, enabling it to pursue growth projects. We expect the company to generate positive free cash flow despite elevated capex levels for its Chile drilling project and domestic capacity expansion. EDC: consolidated FCFF (PHPm) 2011 2012 2013 2014 2015E 2016E 2017E 2018EEBIT 9,318 13,841 11,889 13,809 16,305 17,917 18,572 19,710Depreciation and amortization 3,442 3,665 3,731 4,133 5,114 5,654 6,255 6,841Working capital 1,580 494 -466 -1,985 3,102 -361 -54 -11Capex -9,342 -6,454 -10,491 -18,342 -16,330 -16,388 -12,846 -10,320Income taxes 115 -775 -486 -1,223 -1,246 -1,260 -1,343 -1,453Tax benefit of interest expense 0 -329 -320 -346 -417 -370 -338 -333FCFF 5,112 10,442 3,857 -3,954 6,528 5,190 10,246 14,434

Source: Company, Daiwa forecasts

Key catalysts

Removal of transmission line constraints of Burgos Wind EDC’s 150-MW Burgos Wind project began commercial operations in November 2014. Although it has already been awarded the feed-in-tariff, its contribution is expected to be minimal this year due to constrained output from delayed completion of the transmission line in the project area. The problem is expected to be solved within the year. Start of construction of Bacman 3 and return to service of Tongonan units EDC’s next expansion project is the 30-MW Bacman 3. Construction is expected to commence within 2H15 and be completed by 2017. Meanwhile, a 37.5MW unit at the Tongonan plant underwent unplanned shutdown in March. Repairs were conducted and it has re-started operations in July, but the company is also conducting checks on the remaining units. To-date, one unit is still offline and the initial estimate from management is that full operations at the Tongonan plant will resume by August 2015. Although the impact is minimal, news of this event seems to have noticeably dampened investor sentiment. Positive developments on Chile drilling In October, EDC is set to drill at least 2 wells in its Mariposa project in Chile. This will mark the company’s first major overseas drilling so a positive result would be a milestone in EDC’s international expansion aspirations.

Utilities / Philippines EDC PM

24 July 2015

- 8 -

A world leader in geothermal energy

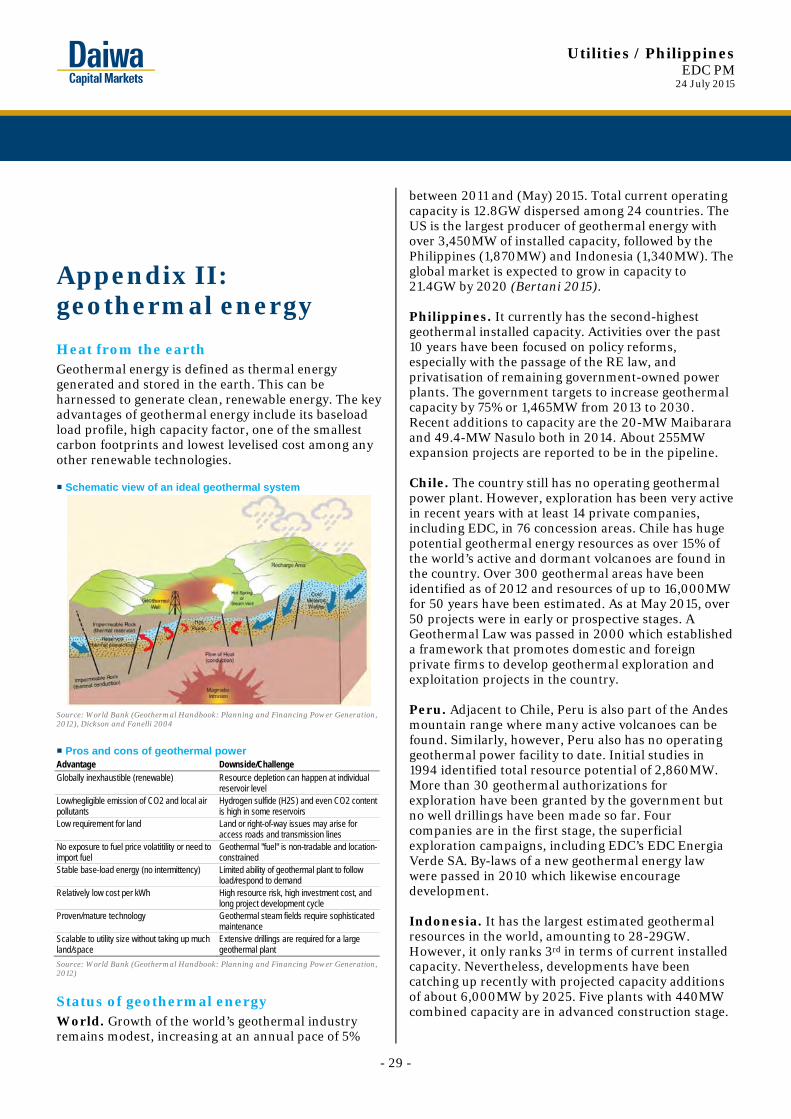

Often overlooked is EDC’s top market position and technical expertise. It is the world’s largest vertically integrated geothermal company and is among a very few with expertise spanning the entire geothermal value chain.

Largest integrated geothermal company

EDC is the largest integrated geothermal company in the world with total installed capacity of 1,169MW, which accounts for 9.1% of the world’s total of 12.8GW. All of its operating geothermal facilities are located in the Philippines, but the company is now actively exploring sites in Latin America and looking for opportunities in Indonesia and Africa. EDC has 12 operating geothermal power plants in 5 concession areas across the Philippines.

EDC: geothermal facilities Plant Capacity (MW) Manufacturer Location RegionBacman I 120.0 Toshiba/ Alstom Bicol LuzonBacman II 20.0 Mitsubishi Bicol LuzonTongonan 112.5 Mitsubishi Leyte VisayasPalinpinon I 112.5 Fuji Southern Negros VisayasPalinpinon II 60.0 Fuji Southern Negros VisayasUpper Mahiao 125.0 GE/ Ormat/ Kato Leyte VisayasMalitbog 232.5 Fuji Leyte VisayasMahanagdong 180.0 Toshiba Leyte VisayasOptimization 50.9 Various Leyte VisayasNasulo 49.4 Fuji Southern Negros VisayasMindanao I 52.0 Mitsubishi Mt. Apo MindanaoMindanao II 54.0 Mitsubishi Mt. Apo MindanaoTotal 1,168.8

Source: EDC

Note: *Excludes the 20MW Nasuji power plant placed on preservation

Geothermal energy companies Company

Country

Steam capacity (MW)

Plant Capacity (MW)

EDC Philippines 1,169 1,169Comision Federal de Electricidad Mexico 958 958Enel Green Power Italy 915 915Chevron USA 1,329 887*Ormat Israel 689 749Calpine USA 725** 725**Mighty River Power New Zealand 385 385Terra Gen USA 337 338Contact Energy New Zealand 335 335Orkuveita Reykjavikur Iceland 333 333CalEnergy Generation USA 329 329Star Energy Ltd Indonesia 227 227Northern California Power Agency USA 220 220

Source: Bertani, Rugero (Geothermal Power Generation in the World 2005-2010 Update Report), EDC, **Calpine

Note: *Not included is the 442MW operated by the Indonesian government

One of very few with technological expertise covering the entire geothermal value chain We believe that one of the most underrated strengths of EDC is its technological expertise in the geothermal field. The company’s expertise covers the entire geothermal value chain from exploration to power plant operations. There are at most 4 other companies in the world (Ormat, Chevron, Enel and Calpine) that have a similar technological background. This technological expertise serves as EDC’s platform for growth, as it is equipped to lead greenfield exploration projects both domestically and abroad. Vertically integrated operations allow operational efficiency and stability EDC successfully won the bidding for all remaining unowned power plants associated with its steam fields during the privatization of government-owned power assets. These were the Palinpinon-Tongonan facility in 2009 and the Bacman plant in 2010. Its high level of vertical integration allows it to control and more effectively run existing geothermal operations. Control over both steam field and power plant operations is valuable for geothermal operations because unlike power plants using conventional

Geothermal energy value chain and players

R&D Exploration Drilling Confirmation Engineering Construction O&M EDC (PH), Ormat (US), Chevron (US), Enel (IT), Calpine (US)

PT pertamina (ID), Reykjavik Energy (IS) Boart Longyear (US), Halliburton (US) Sumitomo (JP), Shaw Group (US)

Gov't/Univ Labs (All) Iceland Drilling Co (IS), GeothermEx (US), Baker Drilling (US), Parker Drilling (US), ThermaSource (US)

Siemens (DE), Enex (IS) Mannvit (IS), Power Eng

(US) MHI (JP), GE (US), Fuji (JP),

UTC Source: New Energy Finance, 2008

Note: DE = Denmark, ID = Indonesia, IS = Iceland, IT = Italy, JP = Japan, PH = Philippines, US = United States

Utilities / Philippines EDC PM

24 July 2015

- 9 -

sources of fuel (like coal, diesel, and gas), a geothermal power plant is dependent on a specific on site steam field for fuel. In addition, continuous maintenance of steam fields is necessary to ensure sustainability of steam production. Having control over the entire value chain allows EDC to make all-inclusive investment decisions, unlike in the case of the Tiwi-Makban geothermal facility wherein steam production, and consequently electricity generation, has been declining because Chevron, the steam field operator, has not conducted new well drillings. Aboitiz Power Corp (AP PM, not rated) owns the associated power plants.

Coming out stronger from recent trials

EDC has fully recovered from its misfortunes in past years, particularly from the impairment of its Northern Negros facility, repeated delays in the rehabilitation of the Bacman plant, and natural calamities. More importantly, beyond just recovering, we note that management has applied solutions and adopted learnings from these events to enhance operations and strengthen its facilities. What went before? Northern Negros impairment. In 2011, EDC recognised the full impairment of its Northern Negros Geothermal plant (NNGP) amounting to PHP8.74bn. NNGP was commissioned in 2007 with installed capacity of 49.4MW, but only generated 15MW over the 2007 to June 2008 period, due to low discharge from the steam field. Bacman rehab’s repeated delays. EDC begun rehabilitation of the Bacman geothermal power plant after it acquired the plants from the government in September 2010. Repairs were completed in December 2011, but units 1 and 2 experienced problems with the generator-rotor during reliability runs. The units were again repaired, but upon re-commissioning, issues once again surfaced in February 2013 for unit 2 and in September 2013 for unit 1. Because of this, management decided to implement a more permanent solution by fully replacing the units’ steam paths (turbine, rotors and diaphragms). Simultaneously, an interim fix through the repair of the units was applied while the company waited for the new parts. EDC completed its permanent fix for Bacman in February 2015.

Hit by the world’s strongest typhoon. In November 2013, Central Philippines was hit by Super Typhoon Haiyan. It was the strongest storm on record to make landfall with sustained winds of 230kph and a peak of 315kph. Directly hit and damaged by the Super Typhoon were EDC’s Leyte-based plants, which consist of over 700MW and accounted for about 54% of the company’s revenue at the time. The initial estimate to restore operations was almost 11 months, but EDC was able to completely bring capacity back to pre-Haiyan levels after 123 days (by 11 March 2014). EDC: cooling tower damaged by Typhoon Haiyan

Source: EDC presentation materials

Recently, much stronger typhoons have passed through EDC’s facilities. After Haiyan, 3 more strong typhoons in 2014 affected EDC’s operations, namely, typhoon Glenda in July, which affected operations in Bacman and typhoons Ruby and Seniang in December, which affected its Leyte facilities. EDC’s responses and actions Transferred NNGP equipment to Nasulo. The 49.4-MW Nasulo geothermal plant started commercial operations in July 2014. This was part of EDC’s Northern Negros to Nasulo (N2N) project which involved the transfer of equipment from its 49.4MW NNGP to Nasulo. The transfer also resulted in a PHP1.8bn net impairment recovery in 2014. However, the adjacent 20-MW Nasuji unit (part of Palinpinon facility) was put in preservation mode to accommodate the steam requirements of Nasulo. With full-year operations, we expect revenue and EBITDA from Nasulo (net of the Nasuji shutdown) to reach PHP874m and PHP586m, respectively, for 2015.

Utilities / Philippines EDC PM

24 July 2015

- 10 -

EDC: N2N transfer programme

Source: Google Maps

Retrofitting old plants. When Bacman’s old turbine and generator were replaced with the latest designs (“retrofit”), EDC was able to realise efficiency gains and life extension of the facility. Following this retrofit, Bacman’s electricity production has increased by 10%, while its steam consumption has declined by 9.75%. Even with just partial completion in 2014, Bacman already returned to black last year with a net profit contribution of PHP271m from a loss of PHP1.19bn in 2013. The permanent fix or retrofit of all 3 units at Bacman was completed in February 2015 and Bacman’s rated capacity was upgraded to 140MW from 130MW.

With its return-to-service, upgraded capacity and more efficient steam consumption, we expect Bacman’s revenue to reach PHP4.24bn in 2015 and PHP5.25bn in 2016. In terms of EBITDA, we forecast PHP2.33bn and PHP2.89bn contributions for 2015 and 2016, respectively.

EDC: replacement turbines for Bacman unit 1

Source: Daiwa

Similar to the permanent fix at Bacman, EDC is now rolling-out retrofit programmes for some of its old units. First on the list are the 3 units at the 112.5MW Tongonan power plant. The equipment was already ordered in January 2015 and target completion is between 3Q16 and 1Q17. This should add about 12MW to Tongonan. “Typhoon-proofing” facilities. Since 2006, the company has been reinforcing critical geohazard-prone areas within its concession areas. By end-2014, EDC had completed the necessary geohazard mitigating measures in 150 areas it has identified. More recently, however, much stronger typhoons are hitting the Philippines which pose a greater threat to EDC’s facilities. From its experience with Super Typhoon Haiyan, most of the damage was to the cooling towers at the power plants. As such, the company is implementing a solution which replaces the cooling towers with a new design that can withstand up to 300kph winds. Based on the Philippines wind zones, priority 1 are the Bacman and Leyte cooling towers, followed by the Palinpinon and Mindanao cooling towers. The designs were completed by SPX Marley, the manufacturer of 68% of EDC’s cooling towers, in 2014 and are due to be installed starting July 2015. In addition, EDC remodelled its control rooms into “bunker type” rooms which are solid, waterproof, concrete structures in order to protect all critical electronic instruments and control systems.

Utilities / Philippines EDC PM

24 July 2015

- 11 -

Evolving into a diversified pure-play RE company

We forecast EDC’s projects in hydro, wind and solar power to contribute 14% of consolidated earnings by 2016.

Diversified into hydro, solar and wind power generation

Total attributable capacity of 1,402MW EDC is evolving into a pure-play RE company. Although geothermal remains its biggest asset and core competency, the company has diversified into the hydro, solar and wind power businesses over the past 7 years (it moved into hydro power in 2008, and wind and solar businesses since 2014.) Combined, these add 233MW and bring EDC’s portfolio to 1,402MW, equivalent to 8% of the total installed capacity of the country as of end-2014. EDC: other RE projects Type Plant Capacity

(MW)

Stake Attributable capacity

(MW)

Manufacturer Location Region

Wind Burgos 150.0 100% 150.0 Vestas Ilocos LuzonSolar Burgos 4.1 100% 4.1 Juwi Ilocos LuzonHydro Pantabangan

(FG Hydro) 120.0 60% 72.0 Adritz Nueva

EcijaLuzon

Hydro Masiway (FG Hydro)

12.0 60% 7.2 Toshiba Nueva Ecija

Luzon

Total 286.1 233.3

Source: EDC

Non-geothermal RE projects expected to contribute 14% of total profit by 2016 We expect the contribution of EDC’s 3 other RE projects – FG Hydro, Burgos Wind and Burgos Solar – to increase from around 3% of earnings in 2014 to 14% (or PHP1.68bn) in 2016 with the full contribution of Burgos Wind. Although all 3 projects are already operational this year, we expect a minimal contribution from Burgos Wind due to the delay in completion of transmission line facilities. Nevertheless, we expect the combined contribution from the 3 projects to amount

to PHP795m in 2015, which is equivalent to 8% of EDC’s consolidated net profit. EDC: breakdown of earnings

Source: EDC, Daiwa forecasts

Note: *Includes parent and others

FG Hydro: seasonal earnings kicker EDC’s acquisition of a 60% stake in FG Hydro, the owner and operator of the 132-MW Pantabangan-Masiway hydroelectric power plants, in 2008, marked its diversification into other RE technologies. The acquisition cost was USD105m. In 2014, FG Hydro added PHP399m or 4% of EDC’s total profit. However, its performance has varied over the past 4 years, as its power generation has been greatly affected by weather patterns, such as El Niño. In addition, about half of FG Hydro’s sales are tied to the spot market. FG Hydro’s highest contribution to EDC of PHP1.69bn was recorded in 2012 driven by high generation with the dams’ high water levels and elevated spot market prices. Nevertheless, we expect a baseline contribution from FG Hydro of between PHP528m and PHP607m this year and next.

4,443

8,514

6,558

9,190 10,160

12,066 12,921

14,019

(2,000)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2011 2012 2013 2014 2015E 2016E 2017E 2018E

Geothermal* Burgos wind Burgos solar FG Hydro (at 60%) Total

Utilities / Philippines EDC PM

24 July 2015

- 12 -

FG Hydro: 130-MW Pantabangan power plant FG Hydro: 12.5-MW Masiway power plant

Source: EDC company brochure Source: EDC company brochure

FG Hydro: operating and financial highlights 2012 2013 2014 2015E 2016E 2017E 2018ETotal Revenue (PHPm) 4,753 2,501 1,624 2,186 2,254 2,333 2,414 EBITDA (PHPm) 4,246 2,067 1,127 1,683 1,690 1,749 1,811 Net Income (PHPm) 3,404 1,467 540 880 1,011 1,090 1,172 Gross rated capacity (MW) 132.0 132.0 132.0 132.0 132.0 132.0 132.0 Total volume (GWh) 932 453 425 474 474 474 474 Price (PHP/kWh) 5.10 5.52 3.82 4.61 4.75 4.92 5.09 Capacity factor (%) 39.0% 28.0% 21.0% 25.0% 25.0% 25.0% 25.0%Source: EDC, Daiwa

Burgos Wind: the largest wind project in Southeast Asia Following the finalisation of the FIT rules in 2013, EDC fast-tracked the development of its 150-MW Burgos Wind located in Ilocos Norte, one of the northernmost provinces in the Philippines. The project was initially planned with only 87-MW and a cost of USD300m, but EDC decided to upsize this to 150-MW with a total cost of USD450m. The Burgos Wind project was formally started in March 2013 with the signing of the supply deal with Denmark’s Vestas, the world’s largest wind turbine manufacturer. It was completed in November 2014 and became the first wind project under the new FIT regime of the government. With FIT, Burgos Wind’s power generation will be sold at a fixed rate of PHP8.53/kWh (with annual inflation and forex

adjustments). The Burgos Wind project also holds the title of the largest wind power project in Southeast Asia. FIT was awarded to the project in April 2015, with the retroactive effect beginning 11 November 2014. However, its power generation is still curtailed due to delays in the completion of a transmission facility in the Ilocos region. The target set by the grid operator is August, but management guides for end-of-year completion to give room for further delays. In line with management’s guidance, Burgos Wind, despite its output curtailment, is expected to add around PHP2.0bn in revenue. This is equivalent to an annual capacity factor of 17.8%, lower than the expected normal average of 25%. We estimate the project will contribute minimally to net profit this year

Utilities / Philippines EDC PM

24 July 2015

- 13 -

at PHP245m. Full contribution of the project should be seen in 2016, when we forecast revenue and net profit of PHP2.95bn and PHP1.04bn, respectively. Burgos Wind

Source: Manila Bulletin

Burgos Wind: operating and financial highlights 2014 2015E 2016E 2017E 2018ETotal Revenue (PHPm) 188 1,995 2,951 3,054 3,161EBITDA (PHPm) 151 1,596 2,361 2,443 2,529Net Income (PHPm) -81 245 1,037 1,165 1,302 Gross rated capacity (MW) 150.0 150.0 150.0 150.0 150.0Total volume (GWh) 49 234 329 329 329Price (PHP/kWh) 3.86 8.53 8.98 9.30 9.62Capacity factor (%) 4.0% 17.8% 25.0% 25.0% 25.0%

Source: Company, Daiwa

Burgos Solar: small but gives experience Burgos Solar is EDC’s 4.1-MW solar project located within the Burgos Wind concession area. The project started commercial operations on 2 March 2015 and cost PHP410m, which was fully funded by equity. Although relatively small, this marks EDC’s first foray into solar power. It should provide EDC with the necessary experience to guide it in future solar energy projects. FIT of PHP9.68/kWh was awarded to the project in March 2015. It is also directly connected to a local electricity cooperative in Ilocos so it is not affected by the transmission line constraint. We look for the project to add revenue of PHP39m and PHP55m, as well as net profit of PHP22m and PHP33m in 2015 and 2016, respectively.

Burgos Solar

Source: EDC presentation materials

Burgos Solar: operating and financial highlights 2015E 2016E 2017E 2018E

Total Revenue (PHPm) 39 55 57 59EBITDA (PHPm) 37 52 54 56Net Income (PHPm) 22 33 35 38 Gross rated capacity (MW) 4.1 4.1 4.1 4.1Total volume (GWh) 4 5 5 5Price (PHP/kWh) 9.68 10.19 10.55 10.92Capacity factor (%) 11.3% 15.0% 15.0% 15.0%

Source: Company, Daiwa

Utilities / Philippines EDC PM

24 July 2015

- 14 -

Mid- and long-term growth opportunities in sight

Domestic projects, albeit small in size, should provide growth over the mid-term. Latin America projects have big potential over the long term.

Maximising domestic resources

EDC has a robust pipeline of projects in the Philippines which are in varying stages of development. These are a mix of greenfield, expansion and upgrade projects. In 2014 and 1H2015, a total of 194MW was added through Burgos Wind, Burgos Solar, Nasulo and the Bacman retrofit. In addition to this, 7 projects with combined indicative capacity of 188MW are in varying stages of development. These should provide growth over the medium term. Frontier areas across the country are also continuously being explored by EDC. Maximising current geothermal service areas The company’s priority is to develop resources within operating geothermal concessions (Leyte, Southern Negros, Bacon-Manito, Mt. Apo, and including Northern Negros). This strategy should prove to be more cost efficient because of existing civil works and shared facilities in these areas. Currently, EDC has 6 new sites within existing concessions and 1 retrofit in its pipeline. Bacman 3 is the most advanced among the 6 new projects in the pipeline. It will be located within the existing Bacman concession area and resources of 30MW have been confirmed. Notice to proceed is targeted to be issued within the year, and the plant is expected to commence commercial operations by 2017.

EDC: Bacman expansion projects

Source: EDC presentation materials

With the success of the Bacman retrofit (replacement of turbine and generator with latest models), EDC is replicating this programme to its other old units. First on the list are the three units of the 112.5-MW Tongonan power plant. The equipment was already ordered in January 2015 and target completion of the three units is between 3Q16 to 1Q17. There is also ongoing discussion about the possible retrofit of the 192.5-MW Palinpinon plant, but no clear details are available as of the moment. We estimate incremental EBITDA from the Tongonan retrofit of PHP114m in 2017 and PHP302m in 2018, while Bacman 3 is expected to contribute PHP662m beginning 2018. Exploring new frontiers In addition to EDC’s project pipeline, the company is exploring frontier sites across the country. Aside from current operating areas, it holds 5 geothermal service contracts, 9 wind energy service contracts, and 3 solar energy service contracts.

E

Sour

Le

EDdevovetheconparrespotyeadricou1,8 LaPe

SimPaactmoThcouonshocou16,

EDC: domestic

rce: Company, Daiw

eading o

DC’s strong tevelopment alerseas. Curree Philippinesncrete develorticularly in source explortential contrars or more, iver. Currentuntries show

800MW.

atin Amerieru

milar to the Pcific Ring of tive regions iost active geo

here are no opuntries yet, bly 14 private ow huge geotuntries, with,000MW for

projects and fr

wa

overseas

echnical expellows it to leaently, all of Es. In recent yopments by ELatin Americration in Chi

ribution will lthese could b

t estimates ow total capaci

ica: closin

Philippines, LFire and is a

in the world.othermal playperating geotbut active exp

companies pthermal ener

h estimates for 50 years and

rontier areas

s explor

ertise in geotad exploratio

EDC’s assets years, howeveEDC on its veca. It is in thile and Peru. likely be accrbe EDC’s lonn 4 advance ity ranging fr

ng in on Ch

Latin Americalso one of th Today, EDC

ayers in Chilethermal planploration is oparticipatingrgy potentialor Chile in thd for Peru at

ration

thermal on projects are located ier, we have sentures abroe early stageAlthough an

retive only inng-term growsites in the 2

rom 760-

hile and

ca belongs tohe geologicallC is one of thee and Peru. nts in the 2 ongoing, withg. Earlier studl in the 2

he order of t 3,000MW.

- 15 -

n seen oad, es of ny n 5 wth 2

o the ly e

h dies

Dirgeoand201AussevewithCorstakproj

Initresorepinst EDComp(EntryAlterraHot REDC ATotal

Sourc

Note:(fromprojec

ectly and throthermal cond 2 in Chile) a13, EDC acqustralian geotheral concessih global renerp (Alterra) inke in Alterra’

ojects in the 2

tial studies oources of betresents a 65-talled geothe

DC: Latin Amerpany y into Latin Americaa Power Corp ock Ltd Applied/Bid sites

ce: Company

* Peru: Achumani am Alterra JVA); Chile

ct from Alterra JVA)

U

rough joint vcessions in thand 19 applic

uired in phashermal firm,ions in Chile ewable energn 2013 where’s subsidiarie2 countries.

n 4 of EDC’stween 760MW-154% increaermal capacit

rica sites

) Peru 1 2 0 3

and Quello Apacheta : Laguna del Maule

)

Utilities /

ventures, EDCthe 2 countriecations. Betw

ses the subsid, Hot Rock Lt

e and Peru. Itgy player Altere EDC acquies holding th

s sites show tW and 1,800ase from EDCty.

Granted sites*

Chile 2 0 0 2

a (from HRL acquisitand Pellado (both co

PhilippinEDC P

24 July 2

C now holds es (3 in Peru

ween 2012 andiaries of td, which helt also partnererra Power ired a 70% he latter’s

total probabl0MW which C’s current

Applica

Peru834

15

tion) and Pinchollo Lomprise the Maripos

nes PM 2015

5 u nd

ld red

le

ations

Chile0044

Libre sa

Utilities / Philippines EDC PM

24 July 2015

- 16 -

EDC: resource potential of select Chile and Peru projects

Prospects Temp

(deg Celsius)Resource

probability Area (sqm) MWe

Achumani project 250-320 P90 7 70 (Peru) P50 26 260

P10 70 700 Quello Apacheta project 220-240 P90 6 55

(Peru) P50 17 168 P10 49 487

Tutapaca project 220-290 P90 0 0 (Peru) P50 27 270

[Under EDC application] P10 40 400 Mariposa project* 250-290 P90 10 105

(Chile) P50 15 155 P10 21 210

Source: Company

Note: *EDC has a 70% stake in the JV with Alterra Power Corp

Significant progress is being made in the Mariposa project in Chile wherein EDC has a 70% interest through its JV with Alterra. The project is estimated to have geothermal resources of 105-210MW, with the mean resource probability (at P50) showing capacity of 155MW. Drilling for the top holes of 3 wells and installation of the water line have been completed in preparation for the first major drilling in October 2015, which will also mark EDC’s first major well drilling overseas. EDC has budgeted for USD58m between 2014 and 2016 for the drilling campaign. EDC: Mariposa project in Chile

Source: EDC presentation materials

Indonesia: long-standing prospects Even prior to its Latin America entry, EDC had already set its sights on Indonesia for overseas expansion. Indonesia also belongs to the Pacific Ring of Fire and actually has the world’s biggest geothermal potential of around 28-29GW. Despite this, Indonesia is only the third-largest producer of geothermal power, next to the US and the Philippines, with installed capacity of 1,340MW.

EDC has established an office in Indonesia and has applied for preliminary survey rights covering pre-identified areas. Although it has yet to acquire or win any concessions in Indonesia, a positive development came when the Indonesia Ministry of Energy and Mineral Resources assigned the geothermal introduction survey of the GrahoNyabu region in Sumatra to EDC in 2013. EDC has already completed the survey activities in GrahoNyabu in Sumatra and submitted the results to the Indonesia Ministry of Energy and Mineral Resources. The same information will be used as the basis for the upcoming tender of the GrahoNyabu concession. In addition, EDC said it is currently in partnership discussions with a geothermal concession holder for a JV in one of their sites in Indonesia which has an estimated capacity of 220MW and development cost of USD1bn.

Utilities / Philippines EDC PM

24 July 2015

- 17 -

Predictable cash flow with upside from new projects

Robust and predictable cash flow generation, provided by baseload geothermal operations and offtake contracts, strengthens EDC’s balance sheet which should support growth.

Long-term contracts provide stable and predictable cash flow

90% of capacity contracted Around 90% of EDC’s revenue in 2014 was derived from long-term contracts. More notably, 64%+ of revenue was based on contracts with tenors of 6 years and above. Coming from legacy contracts when EDC was still a government-owned entity, the biggest single customer of EDC remains the government’s National Power Corp (NPC). However, from almost 100%, EDC has managed to expand its revenue base such that only 43% of revenue is now tied to NPC through power purchase agreements expiring in 2022/24. EDC: term structure of contracts

Source: EDC

Prefers stability over short-term gains The company made a big decision last year when it renegotiated its contracts for its subsidiary, Green Core Geothermal Inc (GCGI), the owner and operator of the Palinpinon and Tongonan geothermal plants, to reduce its base price by around PHP0.40/kWh beginning 2015. The move was driven by low pricing by the competition, particularly from newly built coal plants which are taking advantage of the current low coal prices. In return, it saw requests for additional capacity and extensions of the life of some of the existing contracts up to 2025, 2030 and even 2040. In the short run, the lowered rates will cost EDC around PHP911m. However, the move is testament to the company’s preference towards a more secure and stable cash flow over the long run. FIT scheme also provides stable revenue

EDC’s existing wind and solar projects also enjoy relatively stable revenue through the government’s FIT regime. Under the FIT scheme, EDC’s Burgos Wind and Burgos Solar have secured fixed base prices of PHP8.53/kWh and PHP9.68/kWh for all power generated up to 20 years. Control over steam fields reduces uncertainty EDC’s vertically integrated operations through its ownership of both steam fields and power plants reduce uncertainty over the long-term operations of the geothermal facility. As such, investment decisions on maintenance of the steam fields are easier and issues on pricing of steam can be avoided. Solid balance sheet to finance growth All of the above factors should contribute to stable and predictable cash flow generation for EDC. As a result, its balance sheet should continue to strengthen, allowing it to pursue growth projects. Due to the risks and costs associated with geothermal energy exploration, particularly in early-stage exploration and drillings, initial investments are often funded by the investor’s balance sheet. At end-1Q15, EDC’s cash balance stood at PHP23.98bn, while its current ratio and net debt-to-equity ratio were 1.60x and 1.22x, respectively.

Last year, we estimate the company’s FCF on a consolidated basis was a negative PHP3.95bn due largely to its capital expenditure for the USD450m Burgos Wind project. Moving forward, we expect the company to be able to generate positive FCF despite still-elevated capex levels for its Chile drilling project

Consolidate revenues (2014): PHP30,867m

SP OT 1-2 YR S 3-5 YR S >6 YR SWESM 10% - - - N GC P - 2% - - D U - 17% 7% 20%T R A N SC O - - - 1%N P C - - - 43%

TranscoPHP188m

0.6%

NPCPHP13,437m

43.5%

DUPHP13,417m

43.5%

NGCPPHP720m

2.3%

WESMPHP3,105m

10.1%

Utilities / Philippines EDC PM

24 July 2015

- 18 -

and domestic capacity expansion. For 2015E and 2016E, we forecast FCF (on a consolidated basis) of PHP6.53bn for 2015E and PHP5.19bn for 2016E. Aside from maintenance capex and ongoing domestic exploration costs, we have taken into account the USD58m or around PHP2.59bn budget between 2014 and 2016 for drilling at the Mariposa drilling facility, and around a PHP4.7bn cost for Bacman 3 between 2015 and 2017.

EDC: consolidated FCFF (PHPm) 2012 2013 2014 2015E 2016E 2017E 2018E

EBIT 13,841 11,889 13,809 16,305 17,917 18,572 19,710Depreciation and amortization 3,665 3,731 4,133 5,114 5,654 6,255 6,841Working capital 494 -466 -1,985 3,102 -361 -54 -11Capex -6,454 -10,491 -18,342 -16,330 -16,388 -12,846 -10,320Income taxes -775 -486 -1,223 -1,246 -1,260 -1,343 -1,453Tax benefit of interest expense -329 -320 -346 -417 -370 -338 -333FCFF 10,442 3,857 -3,954 6,528 5,190 10,246 14,434

Source: Company, Daiwa forecasts

New initiatives to deliver growth

Complementing the stable cash flow generation are EDC’s growth initiatives, which should provide the boost to profits. Recently completed projects between 2014 and 1Q15 are the return-to-service of Bacman, Nasulo, Burgos wind, and Burgos Solar, while upcoming projects are the 30-MW Bacman 3, Tongonan retrofit, as well as Mariposa drilling in Chile. EDC: timeline of additional capacity included in forecasts 2014 2015 2016 2017 2018Project (in MW) (in MW) (in MW) (in MW) (in MW)Existing Nasulo (net*) 29.4 Bacman rehabilitation/retrofit** 5.0 5.0 Burgos Wind 150.0 Burgos Solar 4.1 Bacman 3*** 30.0Tongonan retrofit 12.0Total 184.4 9.1 0.0 12.0 30.0

Source: Daiwa

Note: *Net of the 20-MW Nasuji unit of the Palinpinon plant which was put in preservation mode

**Only refers to the additional capacity resulting from the rehabilitation/retrofit. Total capacity of Bacman post-rehabilitation is 140MW

***Assumed completion by end-2017, start of operations beg-2018

Full-year impact of Bacman, Nasulo and Burgos in 2015 and 2016 In 2014, EDC posted record-high recurring net profit (after preferred dividends) of PHP9.19bn. Core net profit grew robustly, up 40% YoY, mainly on the back of the partial return-to-service of Bacman and commencement of commercial operations at the Nasulo plant.

EDC: consolidated revenue historical and forecast (PHPm)

Source: EDC, Daiwa forecasts

EDC: recurring net profit historical and forecast (PHPm)

Source: Company, Daiwa forecasts

For 2015 and 2016, we still expect the company to post double-digit EPS growth, albeit at a lower rate than 2014’s. We forecast an 11% YoY increase in core net profit for 2015 to PHP10.16bn still driven by fresh contributions from Bacman and Nasulo. Although Burgos Wind has been operational since November 2014, we expect it to contribute minimally in 2015 due to transmission line constraints, which are scheduled to be fixed by end of year. By 2016, full contribution of both Burgos Wind and Bacman, together with the return-to-service of a 37.5-MW unit of Tongonan plant, should lift EDC’s earnings to PHP12.07bn, up 19% YoY, on our forecasts. Long-term growth hinges on the success of exploration, new projects EDC’s pipeline of projects, particularly the expansion of its operating concession areas and increased capacity from its retrofit programme, should be the main source of earnings growth for the company over the medium term. We have factored in its 30-MW Bacman 3 expansion project, as well as the retrofit of the 112.5-MW Tongonan plant, which are expected to both be completed in 2017. With the incremental contribution from these projects, we forecast EDC’s recurring net profit to increase by 7% YoY to

28,369 25,656

30,867 34,118

37,273 39,211

42,064

2012 2013 2014 2015E 2016E 2017E 2018E

-20%+26%

+20%

+11%

+9% +5% +7%

8,514

6,558

9,190 10,160

12,066 12,921

14,019

2012 2013 2014 2015E 2016E 2017E 2018E

-23%+92% +40% +11% +19% +7% +9%

Utilities / Philippines EDC PM

24 July 2015

- 19 -

PHP12.92bn for 2017 and by 9% YoY to PHP14.02bn for 2018. Although admittedly small-sized, these domestic projects should provide decent growth for EDC while its bigger overseas projects are under development. Beyond Bacman 3, we have not yet factored in any contribution from either domestic or overseas projects.

Utilities / Philippines EDC PM

24 July 2015

- 20 -

Valuation: undemanding with attractive prospects

Despite EDC’s top market position and technical expertise, predictable cash flows, and growth prospects, its current share price offers hefty upside potential and undemanding valuations.

TP of PHP9.24 offers upside potential of 20%

We initiate coverage on EDC with a Buy (1) rating. Separately valuing each RE technology using the DCF method, we arrive at a SOTP-based target price of PHP9.24. Our target price suggests 20% upside potential, while the stock is trading currently at PERs of 14.2x for 2015E and 12.0x for 2016E. Geothermal remains as the core asset, but other projects add value Based on our estimates, EDC’s geothermal business has an equity value of PHP136.94bn or PHP7.30/sh, equivalent to around 79% of our target price. Our valuation for the geothermal business is composed of the 12 operating geothermal facilities, future projects (30-MW Bacman 3 and retrofit of Tongonan plants), as well as initial capex for Mariposa drilling. SOTP valuation Equity

value EDC's stake

Attributable value

Value per share

(PHPm) (PHPm) (PHP/sh)Geothermal* 136,941 100% 136,941 7.30 Burgos Wind 23,003 100% 23,003 1.23 Burgos Solar 839 100% 839 0.04 FG Hydro 20,755 60% 12,453 0.66 Total 9.24

Outstanding common shares (m) 18,750

Source: Daiwa

Note: *Includes parent and others

Although we believe geothermal will remain EDC’s core asset and biggest value driver, its diversification into other RE technologies (hydro, solar and wind) has slowly increased in contribution. Combined, its other RE assets now account for 21% of the company’s total equity value and add PHP1.94/sh to our target price. The newly-operational Burgos Wind has the biggest share with PHP1.23/sh contribution, followed by EDC’s 60% stake in FG Hydro with PHP0.66/sh. The 4-MW Burgos Solar, albeit small, adds positively to value by PHP0.04/sh. Steady dividends EDC’s dividend policy is to pay at least 30% of the previous year’s recurring net profit. The dividend payout has ranged from 30-50% since 2008. In 2014, EDC paid PHP0.20/sh in cash dividends (PHP0.10/sh regular and PHP0.10/sh special cash dividends) or a total of PHP3.75bn, which was equivalent to 50% of 2013’s recurring net income. However, we expect the payout for 2014’s profit to be lower at 40%, given that its board just maintained the PHP0.10/sh cash dividend in its latest dividend declaration in 9 March 2015. We expect the company to declare a similar fixed amount of PHP0.10/sh as special cash dividends in September or October this year, bringing the total cash dividends for the year to PHP0.20/sh. Moving forward, we opt to maintain the 40% dividend payout. We forecast dividend yields for 2015E and 2016E of 2.6% and 2.9%, respectively. EDC: dividend payments and payout ratio

Source: Company, Daiwa forecasts

Note: Payout ratio is based on recurring net profit. For presentation purposes, both DPS and the payout ratio are adjusted based on the reckoning year of the recurring net income.

0.14 0.16

0.20 0.20 0.22 0.27 0.29

0.31

50%30%

50%40% 40% 40% 40% 40%

2011 2012 2013 2014 2015E 2016E 2017E 2018E

Common cash dividends (PHP/sh) Dividend payout

Utilities / Philippines EDC PM

24 July 2015

- 21 -

EDC geothermal (includes parent and others): DCF valuation Burgos Wind: DCF valuation

(in PHPm) 2015E 2016E 2017E 2018E2019E -

2024EEBIT 14,234 15,065 15,577 16,566 101,481Depreciation and amortization 3,868 4,402 5,003 5,590 43,811Working capital 3,852 -200 -20 24 -8Capital expenditures -16,000 -16,063 -12,520 -9,995 -63,520Income taxes -1,034 -1,148 -1,222 -1,323 -8,486Tax benefit of interest expense -380 -355 -324 -322 -1,595Free Cash Flow to Firm 4,540 1,702 6,493 10,540 71,682Terminal value 126,142 PV of discounted FCFF 63,471PV of terminal value 120,875Enterprise value 184,346 Less: Debt -58,490Add: Cash 11,085Equity value 136,941

(in PHPm) 2015E 2016E 2017E 2018E2019E -

2024EEBIT 787 1,552 1,634 1,720 12,076Depreciation and amortization 809 809 809 809 4,854Working capital -484 -152 -16 -17 -100Capital expenditures 0 0 0 0 -809Income taxes 0 0 0 0 -613Tax benefit of interest expense 0 0 0 0 -81Free Cash Flow to Firm 1,112 2,209 2,427 2,512 2,600Terminal value 35,112 PV of discounted FCFF 16,315PV of terminal value 16,204Enterprise value 32,519 Less: Debt -11,615Add: Cash 2,099Equity value 23,003

Source: Daiwa estimates and forecasts Source: Daiwa estimates and forecasts

Burgos Solar: DCF valuation FG Hydro: DCF valuation

(in PHPm) 2015E 2016E 2017E 2018E2019E -

2024EEBIT 22 31 33 35 250Depreciation and amortization 15 21 21 21 125Working capital -6 -3 0 0 -2Capital expenditures -5 0 0 0 -21Income taxes 0 0 0 0 -11Tax benefit of interest expense 0 0 0 0 0Free Cash Flow to Firm 26 50 54 56 340Terminal value 725 PV of discounted FCFF 363PV of terminal value 335Enterprise value 698 Less: Debt 0Add: Cash 141Equity value 839

(in PHPm) 2015E 2016E 2017E 2018E2019E -

2024EEBIT 1,262 1,269 1,328 1,389 9,594Depreciation and amortization 422 422 422 422 2,529Working capital -259 -7 -18 -18 -107Capital expenditures -325 -325 -325 -325 -2,048Income taxes -211 -112 -121 -130 -972Tax benefit of interest expense -37 -16 -13 -11 -22Free Cash Flow to Firm 850 1,230 1,272 1,326 8,973Terminal value 27,573 PV of discounted FCFF 9,471PV of terminal value 12,701Enterprise value 22,172 Less: Debt -2,901Add: Cash 1,483Equity value 20,755

Source: Daiwa estimates and forecasts Source: Daiwa estimates and forecasts

DCF parameters We have discounted the 10-year free cash flow to the firm (FCFF) of each of EDC’s 4 segments – geothermal (including parent and others), hydro, solar and wind – using a WACC of 8.26% and a terminal growth rate of 2.5%. We have computed a cost of common equity of 10.13%, after-tax cost of debt of 4.73%, and used the dividend rate of 8.0% for its cost of preferred equity.

EDC: DCF parameters WACC 8.26%Cost of common equity 10.13%Risk free rate 4.50%Beta 0.94 Market risk premium 6.00%Cost of preferred equity 8.00%Cost of debt (after-tax) 4.73%Corporate tax rate 10%Capital structure: Common Equity 65.39%Preferred Equity 0.04%Debt 34.57%

Source: Daiwa

Utilities / Philippines EDC PM

24 July 2015

- 22 -

Cheap among its peers

EDC is trading currently at a PER discount to its regional peers in the power generation sector. Based on its closing price of PHP7.70 on 24 July 2015, the stock is trading at PERs of 14.2x for 2015E and 12.0x for 2016E, which are well-below the regional averages for power generators of 16.0x and 12.7x, respectively. Similarly, in terms of EV/EBITDA multiple, the stock’s current trading multiples of 9.5x for 2015E and 8.7x for 2016 are lower than the regional peer averages of 11.0x and 9.5x, respectively, based on the Bloomberg-consensus and Daiwa forecasts. Compared with other renewable energy companies in the Asia region, EDC is also trading below their PER averages of 17.4x and 14.0x for 2015E and 2016E, as well as the EV/EBITDA multiple averages of 15.8x and 14.5x, respectively, based on the Bloomberg consensus and Daiwa forecasts. We believe this discount imposed on EDC is unwarranted because:

(1) It has now fully recovered from its issues with NNGP, Bacman and natural calamities.

Further, it has implemented long-term solutions to enhance operations and strengthen facilities.

(2) It has a competitive advantage through its technical expertise in the geothermal field against other power generation companies. It has good prospects for international expansion, particularly in Latin America.

At our target price of PHP9.24, the stock would trade at PERs of 17.1x for 2015E and 14.4x for 2016E. These are slightly higher than the regional averages for the power generators, but we believe this slight premium is justifiable given EDC’s quality RE portfolio and growth potential. Compared with the regional averages for RE developers, our target PERs are in line. Meanwhile, our target EV/EBITDA estimates are 10.7x and 9.9x, respectively, which are below the regional averages for both power generators and RE developers.

EDC: 12-month forward PER bands EDC: 12-month forward EV/EBITDA bands

Source: Daiwa, Bloomberg, Company

Note: Based on recurring EPS

Source: Daiwa, Bloomberg, Company

0

2

4

6

8

10

12

14

16

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14

(PHP/sh)

4.9x

9.8x

14.7x

19.6x

24.5x

0

2

4

6

8

10

12

14

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14

(PHP/sh)

6.2x

7.7x

9.2x

10.7x

12.3x

Utilities / Philippines EDC PM

24 July 2015

- 23 -

Power generators: regional peer comparison Company Ticker & Market PER PER PBV PBV EV/EBITDA EV/EBITDA Div Yld Div Yld ROE ROE ROA ROA

Exchange Cap 2015E 2016E 2015E 2016E 2015E 2016E 2015E 2016E 2015E 2016E 2015E 2016E(PHPm) (x) (x) (x) (x) (x) (x) (%) (%) (%) (%) (%) (%)

Aboitiz Power Corp AP PM 331,137 18.20 16.62 3.32 3.08 12.94 11.47 3.48 3.66 18.53 18.72 8.60 8.16Beijing Jingneng Clean Ene-H 579 HK 110,117 7.34 6.41 1.05 0.92 8.65 7.69 3.11 3.52 14.43 15.26 3.93 4.05China Datang Corp Renewabl-H 1798 HK 46,547 19.41 13.03 0.66 0.64 9.55 8.46 0.69 1.03 3.28 4.63 0.52 0.81China Longyuan Power Group-H 916 HK 428,878 15.87 13.64 1.63 1.48 9.54 8.51 1.18 1.46 10.40 10.97 3.24 3.39China Yangtze Power Co Ltd-A 600900 CH 1,781,007 20.07 19.61 2.61 2.42 13.69 13.23 2.62 2.65 11.99 11.51 8.59 8.55Electricity Generating PCL EGCO TB 105,083 10.71 9.70 1.04 0.98 22.98 18.91 4.08 4.21 10.01 10.59 4.38 4.64Energy Development Corp* EDC PM 144,375 13.63 11.83 2.91 2.49 9.84 9.02 2.56 2.95 23.04 22.60 9.60 10.14First Gen Corp FGEN PM 99,944 13.64 10.53 1.54 1.34 6.25 5.50 1.67 1.83 10.83 12.27 5.27 5.91Glow Energy PCL GLOW TB 163,171 14.01 13.95 2.49 2.46 9.51 9.63 4.32 5.01 18.88 17.49 7.48 7.95Huaneng Renewables Corp-H 958 HK 186,187 14.67 11.66 1.43 1.29 8.97 7.33 1.26 1.65 10.16 11.62 2.17 2.37Jaiprakash Power Ventures LT JPVL IN 14,007 35.64 n.a. 0.33 0.31 10.44 8.38 n.a. n.a. 0.13 1.63 0.24 1.75Manila Electric Co MER PM 332,269 18.10 19.21 4.00 3.86 9.09 9.77 4.37 4.30 22.82 20.66 6.74 6.09NHPC Ltd NHPC IN 150,463 9.73 9.23 0.71 0.67 7.49 7.21 3.29 3.36 7.48 7.75 4.19 3.95Reliance Power Ltd RPWR IN 89,224 12.70 9.62 0.61 0.57 14.78 8.56 n.a. 0.29 4.91 6.29 1.91 2.32Average 15.98 12.70 1.74 1.61 10.98 9.55 2.72 2.76 11.92 12.28 4.78 5.00

Daiwa estimates Energy Development Co 22.41 23.00 7.67 8.45

At current price 14.21 11.97 2.97 2.56 9.40 8.66 2.6* 2.91* n.a. n.a. n.a. n.a.At target price 17.05 14.36 3.57 3.07 10.74 9.88 2.16* 2.43* n.a. n.a. n.a. n.a.

Source: Bloomberg (as of 24 July 2015), Daiwa forecasts (EDC)

Note: *Dividend yield estimates for EDC are based on actual/estimated dividend per share for the year to conform to Bloomberg estimates.

Renewable energy developers: regional peer comparison Company Ticker & Market PER PER PBV PBV EV/EBITDA EV/EBITDA Div Yld Div Yld ROE ROE ROA ROA

Exchange Cap 2015E 2016E 2015E 2016E 2015E 2016E 2015E 2016E 2015E 2016E 2015E 2016E(PHPm) (x) (x) (x) (x) (x) (x) (%) (%) (%) (%) (%) (%)

Central Hydropower JSC CHP VN 5,105 7.15 7.59 1.48 1.36 6.14 6.48 6.69 6.69 21.80 18.70 9.80 9.30China Datang Corp Renewabl-H 1798 HK 46,547 19.41 13.03 0.66 0.64 9.55 8.46 0.69 1.03 3.28 4.63 0.52 0.81China Longyuan Power Group-H 916 HK 428,878 15.87 13.64 1.63 1.48 9.54 8.51 1.18 1.46 10.40 10.97 3.24 3.39China Yangtze Power Co Ltd-A 600900 CH 1,781,007 20.07 19.61 2.61 2.42 13.69 13.23 2.62 2.65 11.99 11.51 8.59 8.55CK Power PCL CKP TB 25,768 37.75 35.26 0.98 0.91 14.45 13.89 0.93 1.01 4.34 2.67 0.91 0.86Energy Development Corp* EDC PM 144,375 13.63 11.83 2.91 2.49 9.84 9.02 2.56 2.95 23.04 22.60 9.60 10.14Greenko Group PLC GKO LN 7,597 8.93 6.50 0.54 0.46 6.03 4.29 n.a. n.a. 7.20 14.60 n.a. n.a.Huaneng Renewables Corp-H 958 HK 186,187 14.67 11.66 1.43 1.29 8.97 7.33 1.26 1.65 10.16 11.62 2.17 2.37Hunan Development Group Co-A 000722 CH 61,734 41.72 35.24 3.17 2.88 29.73 24.16 n.a. n.a. 7.90 9.50 n.a. n.a.Jaiprakash Power Ventures LT JPVL IN 14,007 35.64 n.a. 0.33 0.31 10.44 8.38 n.a. n.a. 0.13 1.63 0.24 1.75Mytrah Energy LTd MYT LN 8,759 20.28 10.05 n.a. n.a. 7.66 5.72 n.a. 0.68 15.90 22.80 n.a. n.a.NHPC Ltd NHPC IN 150,463 9.73 9.23 0.71 0.67 7.49 7.21 3.29 3.36 7.48 7.75 4.19 3.95Sichuan Chuantou Energy Co-A 600674 CH 403,230 10.39 10.43 2.93 2.43 95.25 89.53 1.48 1.56 24.55 20.64 18.29 16.20Southern Hydropower JSC SHP VN 3,538 7.22 6.07 1.26 1.17 5.69 n.a. 4.42 n.a. 17.85 19.00 7.10 n.a.SPCG PCL SPCG TB 29,895 9.77 8.65 2.89 2.36 9.25 8.45 3.98 4.60 32.83 28.63 9.62 9.86Thai Solar Energy PCL TSE TB 15,272 23.04 17.67 3.07 2.80 24.63 14.92 1.63 1.86 13.83 16.52 7.54 9.96Vallibel Power Erathna PLC VPEL SL 2,388 7.64 9.04 n.a. n.a. 6.46 6.91 10.64 10.64 42.80 33.30 n.a. n.a.Vinh Son -Song Hinh Hydrpo VSH VN 5,937 11.01 12.02 0.92 0.86 9.08 9.42 3.62 3.62 8.54 7.50 6.27 n.a.Average 17.44 13.97 1.72 1.53 15.77 14.46 3.21 3.12 14.67 14.70 6.29 6.43

Daiwa estimates Energy Development Co 22.41 23.00 7.67 8.45

At current price 14.21 11.97 2.97 2.56 9.40 8.66 2.6* 2.91* n.a. n.a. n.a. n.a.At target price 17.05 14.36 3.57 3.07 10.74 9.88 2.16* 2.43* n.a. n.a. n.a. n.a.

Source: Bloomberg (as of 24 July 2015), Daiwa forecasts (EDC)

Note: *Dividend yield estimates for EDC are based on actual/estimated dividend per share for the year to conform to Bloomberg estimates.

Utilities / Philippines EDC PM

24 July 2015

- 24 -

Sensitivity analysis

Our sensitivity analysis on key DCF inputs (risk-free rate, terminal growth, beta, and market risk premium) show that our target price for EDC is most sensitive to changes in the risk-free rate as it affects both cost of equity and cost of debt. A 50bps decrease in our base assumptions of a 4.50% risk-free rate and 5.25% cost of debt (gross) would raise our target price to PHP10.45. Meanwhile, an equivalent 50bps reduction would bring our target price down to PHP8.22. Nevertheless, the stock is still currently trading at a discount against this low case scenario. EDC: sensitivity analysis -50bps* -25bps* Base +25bps* +50bps*Risk-free rate** (base=4.50%) 10.45 9.82 9.24 8.71 8.22 Terminal growth (base=2.50%) 8.59 8.9 9.24 9.61 10.02Market risk premium (base=6.00%) 9.98 9.6 9.24 8.9 8.57 -.10* -.05* Base +.05* +.10*Beta* (base=0.94) 10.2 9.7 9.24 8.81 8.4Source: Daiwa

Note: *For beta, increments are 5bps.

**Changes in risk-free rate are also reflected as addition (reduction) to gross cost of debt base of 5.25%.

Concerns might be raised about a possible rerating of utility stocks, including EDC, once the US Fed hikes its policy rate. However, the results of our correlation and regression analysis between EDC’s share price and the USGG10YR Index (US Generic Gov’t 10Yr) yield show an insignificant relationship with a correlation of -0.4949 and adjusted R2 of 0.2447. Although still considerably low, EDC’s share price shows a higher correlation of -0.7387 and adjusted R2 of 0.5455 against the PDSS10YR Index (Philippine Dealing and Exchange PDST-R2 Fixing 10 Yr) yield. EDC: correlation/regression analysis against bond yields Correlation of share price/bond yield EDC vs USGG10YR Index -0.4949EDC vs PDSS10YR Index -0.7387USGG10YR Index vs PDSS10YR Index 0.6915Regression: adjusted R² EDC vs USGG10YR Index 0.2447EDC vs PDSS10YR Index 0.5455USGG10YR Index vs PDSS10YR Index 0.4780

Source: Daiwa estimates

Note: Data from 14 March 2007 up to 24 July 2015

EDC: share price vs US and PH 10-yr Treasury bond yields

Source: Bloomberg, Daiwa

Note: Values in RHS are in reverse order.

0

2

4

6

8

10

120

2

4

6

8

10

Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14

Yield (%)PHP/sh

LHS: EDC PM Equity RHS: USGG10YR IndexRHS: PDSS10YR Index

Utilities / Philippines EDC PM

24 July 2015

- 25 -

Key risks

Operating risks, such as natural disasters, and steam field and plant/equipment issues, resulting in business interruptions would be the main risks to our earnings forecasts. Steam field and plant/equipment issues Geothermal plants are highly dependent on a specific steam resource, so any issue with a steam field would instantly affect the operations of the power plant, and we see this as the main risk to our earnings forecasts. A case in point is the NNGP facility wherein the company recognised impairment losses of PHP8.74bn because of the less-than-ideal geological attributes of the steam field. Another operational risk for EDC is any mechanical issues with its power plants. A prolonged shutdown of a power plant could result in lost sales for merchant plants and trading losses for plants under bilateral contracts. If a plant exceeds the allowable downtime in a given bilateral contract, EDC would be required to purchase replacement power, typically from the spot market, and trading losses could arise if the purchase price were higher than the contracted price. For geothermal plants, there is also an opportunity loss on the margins over steam. The company mitigates the risk by drilling new wells in order to sustain the steam resource and continuous maintenance of facilities. For EDC’s 2015 budget, maintenance capex accounts for 55% or PHP8.8bn of its PHP16bn budget. The retrofit programme for its old geothermal plants should also improve the reliability, efficiency and life of the power plants. Natural disasters EDC’s facilities are constantly at risk from natural disasters, and we would see any occurrence as a secondary risk to our forecasts. Its geothermal facilities are located in the mountains and volcanic regions which exposes it to natural forces especially typhoons, landslides, and earthquakes. Its Burgos Wind farm (as well as Burgos Solar), being in a strong wind area, is also susceptible to typhoons. Between 2006 and 2013,

its facilities were hit by 24 typhoons, including Super Typhoon Haiyan in late 2013. For FG Hydro, the biggest natural threat is a dry spell or El Niño which causes the water level in its dam to go down and restricts power generation. The company tries to mitigate these risks through reinforcing identified geo-hazard-prone areas, replacing cooling towers with a new design that can withstand up to 300kph winds, and building bunker-type control rooms. Change in regulatory regime Through the Electric Power Industry Reform Act (EPIRA) of 2001, the power generation sector was privatised and became unregulated. In addition, renewable energy players have been given various fiscal incentives under the Renewable Energy (RE) Law of 2008. In theory, amendments to these laws, whether favourable or unfavourable against EDC, could be passed in Congress. In reality, however, it takes a very long time before Congress can pass any amendment or a new law. Meanwhile, under the RE Law and its implementing rules, a registered RE company enjoys a lower income tax rate of 10% from 30%. However, there is a provision for a possible pass-on of savings in the form of lower power rates under such mechanism as may be determined by the Department of Energy in coordination with the RE developers. So far, the DOE has not raised the issue of implementing any pass-on savings mechanism. Exploration of new resource The biggest risks for a geothermal project are in the pre-development stages (pre-survey, exploration and test drilling) with project risk above 90%. EDC, as a vertically integrated geothermal company, continuously engages in these pre-development activities in order to find growth opportunities. In terms of cost profile, however, less than 25% of the total cost is associated with these pre-development activities with the first 2 stages (pre-survey and exploration) making up less than 5% of the total.

Utilities / Philippines EDC PM