initial public offering on the warsaw stock...

TRANSCRIPT

1

Sofia, June 2010

Initial Public Offering on the Warsaw Stock Exchange

Member of the Group

2

BRE Bank Group

70%

� Biura / Przedstawicielstwa� Oddziały� Podmioty Grupy Kapitałowej13 � Brno

6 � � � Brussels

7 � Rome

1 � Copenhagen

2 � Dublin

3 � Amsterdam

4 � � London

5 � Antwerp

8 � � Moscow

9 � Minsk

10 � Kiev

11 � � Warsaw

12 � � Prague

14 � Bratislava

15 � Budapest

22 � Istanbul

16 � Bucharest

17 � Zagreb

18 � � Paris

19 � Zurich

20 � Geneva

21 � Milan

23 � Barcelona

24 � Madrid

25 � Lisbon

12

34 5

6

7

89

10

11

1213

1415

1617

181920 2

1

22

23

24

25

Rio de Janeiro

CaracasGrand Cayman

Mexico CityLos Angeles

San Francisco

Chicago Toronto

New York

Atlanta

Casablanca Cairo

BeirutBahrain

Tehran

Taschkent

Almaty

Novosibirsk

Mumbai

Jakarta

SingaporeLabuan

BangkokTaipei

Hongkong Shanghai

Beijing TokyoSeoul

Buenos Aires

São Paulo

Johannesburg

Sydney�

�

�

��

�

�

�

�

�

�

� �

�

�

�

�

�

�

�

��

�

�

��

�

��

�

�

�

�

�

�

�

�

�� �

Commerzbank AGCommerzbank AG

� Established in 1870.

� Present in Central and Eastern Europe: BRE Bank (Poland), Bank

Forum (Ukraine), Commerzbank Zrt. (Hungary), Commerzbank

(Eurazja) SAO (Russia)

� Years of experience learned from transactions conducted on the

global capital markets - present in 40 countries

� Wide international institutional client base

BRE BankBRE Bank

� Established in 1986, listed on the WSE since 1992, listed in WIG20

index (blue chips);

� 24 corporate and 224 retail branches, 14 subsidiaries

� Corporate Banking, Investment Banking, Retail Banking and

Private Banking

� 3.26 m individual clients, 12,800 corporate clients (2009)

� BRE Bank Securities – leading Polish brokerage house with

extensive expertise in the area of ECM and trading

Member of the Commerzbank AG Group

3

BRE Bank Group

Research / Derivates Sales & TradingCapital Markets

Capital Markets & Advisory Debt Capital MarketsCapital Structuring

Leveraged Finance

Financial Sponsor Coverage Industry Groups

Equity

MarketsM&A Bonds

Asset

Finance

Rating

Advisory

Syndicated

Loans

Corporate

Banking

Corporate

Banking

Investment

Banking

Investment

BankingRetail Banking &

Insurance

Retail Banking &

InsurancePrivate Banking

Asset Management

Private Banking

Asset Management

Private Banking & Private Banking &

Wealth ManagementWealth Management

Most competitive and universal bank in Poland

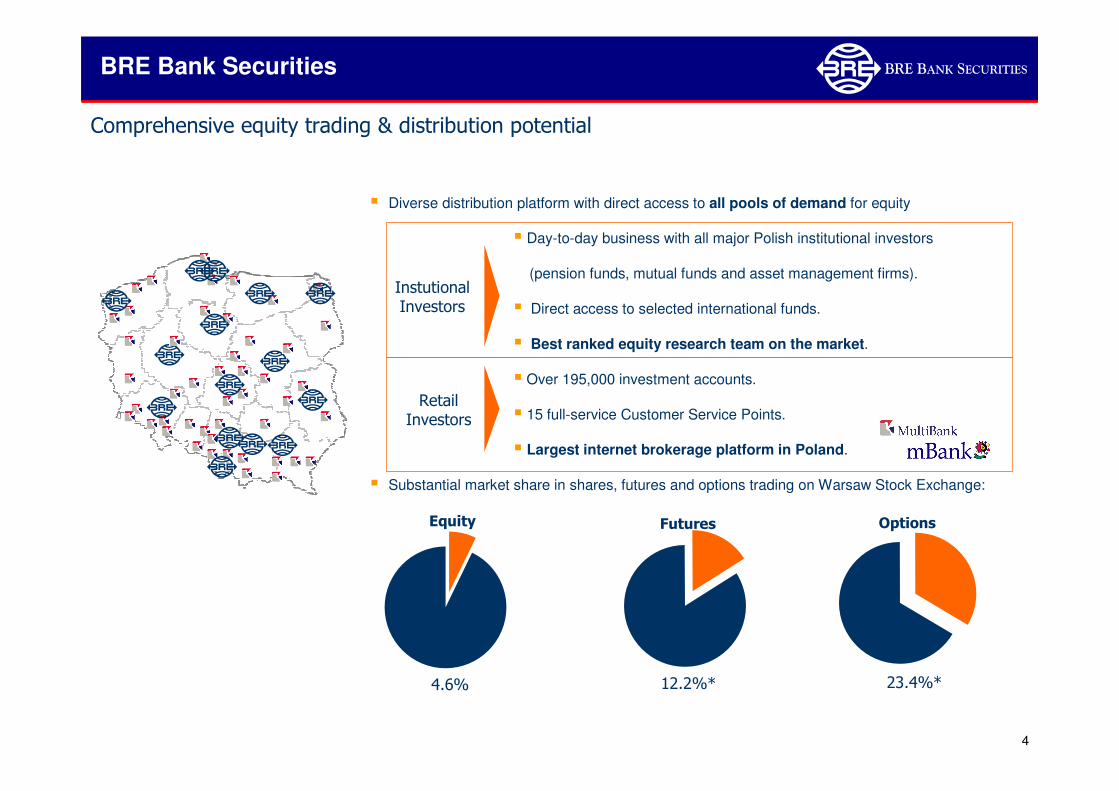

4

� Diverse distribution platform with direct access to all pools of demand for equity

� Day-to-day business with all major Polish institutional investors

(pension funds, mutual funds and asset management firms).

� Direct access to selected international funds.

� Best ranked equity research team on the market.

� Over 195,000 investment accounts.

� 15 full-service Customer Service Points.

� Largest internet brokerage platform in Poland.

� Substantial market share in shares, futures and options trading on Warsaw Stock Exchange:

Equity Futures Options

Comprehensive equity trading & distribution potential

InstutionalInvestors

Retail Investors

4.6% 12.2%* 23.4%*

BRE Bank Securities

5

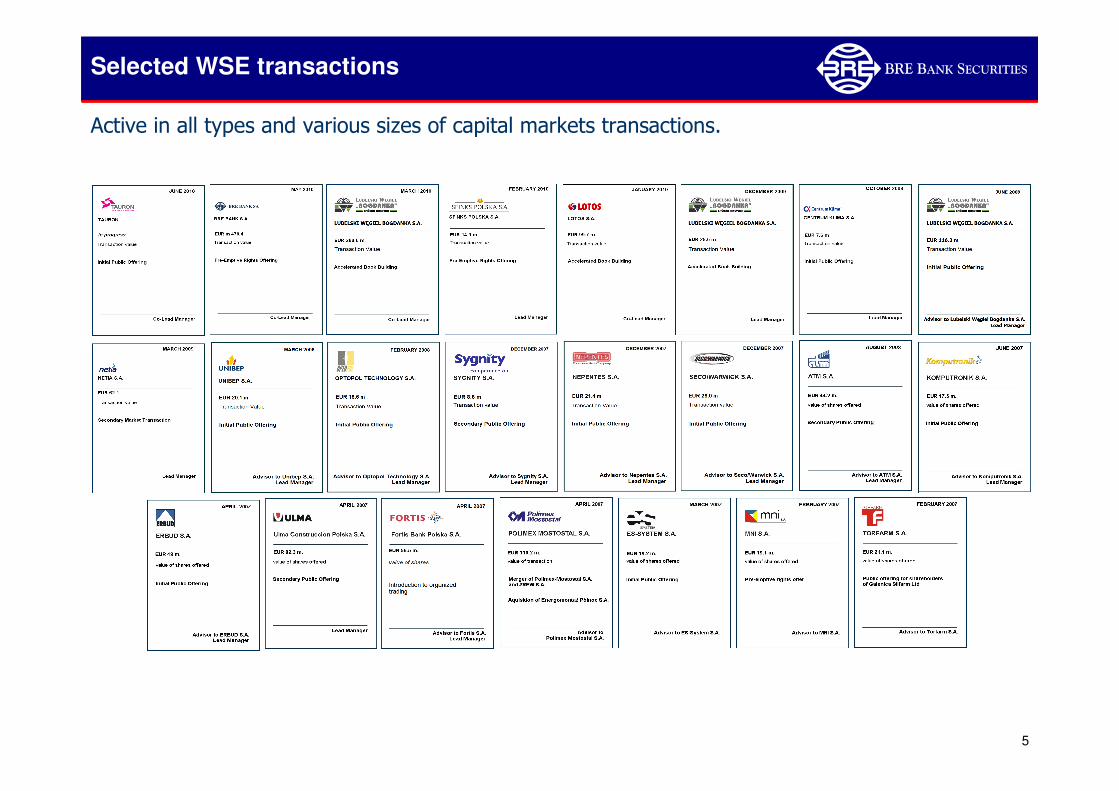

Selected WSE transactions

Active in all types and various sizes of capital markets transactions.

6

WSE – equity market overview

WSE indices performance in 2007 - 2010

Current situation …

� Mid- and small caps – the most sensitive to changes of the economic conditions (wig80).

� Substantial redemptions in mutual funds („MF”) since 2007 end till 2009, pension funds („PF”) as main players on WSE.

� Retained interest in participation in IPOs by Polish pension funds („PF”) but conservative approach to quality and liquidity of issuers.

� 13 IPOs in 2009 (EUR 1.62 bn allocated to Polish investors), inc. 11 private issuers (EUR 0,12 bn).

� State Treasury as the main source of equity supply in 2009 and 2010 (approx. EUR 4.8 bn).

Total number & value of the IPOs

… and perspectives

� Number and value of public offerings dependent on: benchmarks and the secondary market trend.

� Economic situation on the WSE and worldwide exchanges dependent on the pace of global economy recovery.

� Situation of key Polish institutional investors: - inflow/outflow balance in MF determining demand for equities including IPOs,

- PF investment strategy – stable utilisation of transfers from Polish social security office (ZUS).

� Foreign investors activity correlated with global sentiment towards emerging markets.

� Higher number of IPOs expected in 2011 with smaller average size.

� Institutional investors expectations: medium or large sized, promising/stable growth, discount to fair value expected.

0

20

40

60

80

100

120

200

7-0

7-0

2

200

7-0

9-0

2

200

7-1

1-0

2

200

8-0

1-0

2

200

8-0

3-0

2

200

8-0

5-0

2

200

8-0

7-0

2

200

8-0

9-0

2

200

8-1

1-0

2

200

9-0

1-0

2

200

9-0

3-0

2

200

9-0

5-0

2

200

9-0

7-0

2

200

9-0

9-0

2

200

9-1

1-0

2

201

0-0

1-0

2

201

0-0

3-0

2

201

0-0

5-0

2

WIG20 sWIG80 mWIG40

(37)

Value of theofferings (in

PLN bn.).

(number ofIPOs)

7

(38)

4 (16)

(6)

9

1 (25)

(81)

6

200820072006200520042003

WIG Index

2009 2010

(15-20?)

Preparation of transactions,

new privatisations.

2

Significant scale

and smaller

number of IPOs.

Sharp decline in IPOs due to overall

unfavorable economic situation.

Predicted value of the IPOs of the Polish issuers

10

(13)

SPOs14

IPOs

(40-50?)

Higher number of IPOs of private

companies.

Smaller scale of value of IPOs.

2011

Record year in the history of WSE in

terms of value of the IPOs

(37)

Value of theofferings (in

PLN bn.).

(number ofIPOs)

7

(38)

4 (16)

(6)

9

1 (25)

(81)

6

200820072006200520042003

WIG Index

2009 2010

(15-20?)

Preparation of transactions,

new privatisations.

2

Significant scale

and smaller

number of IPOs.

Sharp decline in IPOs due to overall

unfavorable economic situation.

Predicted value of the IPOs of the Polish issuers

10

(13)

SPOs14

IPOs

(40-50?)

Higher number of IPOs of private

companies.

Smaller scale of value of IPOs.

2011

Record year in the history of WSE in

terms of value of the IPOs

7

Foreign companies listed on WSE

Foreign companies listed on WSE

by sector in terms of market capBanks

Energy

Gas & Oil

Real Estate

Mining

Wholesale

Food

Hotels & Restaurants

IT

Media

Chemicals

Light

Metals

Finance

Dual

Dual

Dual

Dual

Single

Single

Dual

Dual

Dual

Dual

Dual

Dual

Single

Single

Dual

Dual

Single

Dual

Dual

Single

Single

Single

Single

Single/dual listing

4 327FoodKERNEL

741Oil & GasKOV

271,203Total

440Real EstateWARIMPEX

137 592BanksUNICREDIT

306FoodSOBIESKI

228LightSILVANO

468Real EstateRONSON

62Real EstateREINHOLD

1 419Real EstatePLAZACNTR

655ChemicalsPEGAS

348Real EstateORCOGROUP

870Hotels & RestaurantsOLYMPIC

10 045MiningNEWWORLDR

27 583Oil & GasMOL

75 480EnergyCEZ

6 064WholesaleCEDC

1 838MediaCCIINT

54FinanceBMPAG

229Real EstateATLASEST

1 444FoodASTARTA

501ITASSECOSLO

255WholesaleASBIS

254MetalsACE

Market Cap (PLNm)SectorCompany

Number of foreign companies listed on WSE 2001 - 2010

230217

203230

255284

351374 379 382

0 0 1 5 7 12 23 25 25 23

0

50

100

150

200

250

300

350

400

450

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Companies listed Foreign companies

Capitalisation of foreign companies listed on WSE 2001 - 2010 (in

PLN bn)

103 111168

291

424

636

1080

465

716 740

0 0 2877 116

198

570

198295 271

0

200

400

600

800

1000

1200

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

All companies Foreign companies

EUR 67,801 m

8

Key targeted investors – Polish pension and mutual funds

� Mandatory pension system ensures monthly inflow of ca. EUR

404 m in 2009.

� Investment activity less dependant on the current market

sentiment.

� Investment policy based on allocation rather than stock picking.

Polish Mutual Funds total AUM (PLN m)

Polish Mutual Funds AUM (PLN thou.) Polish Pension Funds AUM (PLN thou.)

Polish Pension Funds total AUM (PLN m)

� No limits for investments in equity, related to fund's strategy.

� Investment activity dependant on the current market sentiment

i.e. in case of investment certificates redemption.

� Investment strategy based on stock picking rather than

benchmarks.

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

20 000

Pioneer

Pekao

BZ WBK

AIB

ING Aviva

Investors

PKO Union

Investment

KBC Skarbiec Copernicus

Capital

BPH Legg

Mason

PZU Millennium Ipopema0

10 000

20 000

30 000

40 000

50 000

60 000

Aviva

Commercial

Union

ING PZU "Złota

Jesień"

Amplico (d.

AIG)

Axa Generali Aegon Nordea Allianz

Polska

PKO BP

Bankow y

Pocztylion Pekao Warta Polsat

0,0

20 000,0

40 000,0

60 000,0

80 000,0

100 000,0

120 000,0

140 000,0

160 000,0

2007-0

1-3

1

2007-0

2-2

8

2007-0

3-3

1

2007-0

4-3

0

2007-0

5-3

1

2007-0

6-3

0

2007-0

7-3

1

2007-0

8-3

1

2007-0

9-3

0

2007-1

0-3

1

2007-1

1-3

0

2007-1

2-3

1

2008-0

1-3

1

2008-0

2-2

9

2008-0

3-3

1

2008-0

4-3

0

2008-0

5-3

1

2008-0

6-3

0

2008-0

7-3

1

2008-0

8-3

1

2008-0

9-3

0

2008-1

0-3

1

2008-1

1-3

0

2008-1

2-3

1

2009-0

1-3

1

2009-0

2-2

8

2009-0

3-3

1

2009-0

4-3

0

2009-0

5-3

1

2009-0

6-3

0

2009-0

7-3

1

2009-0

8-3

1

2009-0

9-3

0

2009-1

0-3

1

2009-1

1-3

0

2009-1

2-3

1

2010-0

1-3

0

2010-0

2-2

8

2010-0

3-3

1

2010-0

4-3

0

Assets

(P

LN

th

ou

san

d)

0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

30,0%

35,0%

Sh

are

of

Eq

uit

y F

un

ds' A

sse

ts in

MF

's p

ort

folio

s (

in %

)

0,0

50 000,0

100 000,0

150 000,0

200 000,0

250 000,0

2007-0

1-3

1

2007-0

2-2

8

2007-0

3-3

1

2007-0

4-3

0

2007-0

5-3

1

2007-0

6-3

0

2007-0

7-3

1

2007-0

8-3

1

2007-0

9-3

0

2007-1

0-3

1

2007-1

1-3

0

2007-1

2-3

1

2008-0

1-3

1

2008-0

2-2

9

2008-0

3-3

1

2008-0

4-3

0

2008-0

5-3

1

2008-0

6-3

0

2008-0

7-3

1

2008-0

8-3

1

2008-0

9-3

0

2008-1

0-3

1

2008-1

1-3

0

2008-1

2-3

1

2009-0

1-3

1

2009-0

2-2

8

2009-0

3-3

1

2009-0

4-3

0

2009-0

5-3

1

2009-0

6-3

0

2009-0

7-3

1

2009-0

8-3

1

2009-0

9-3

0

2009-1

0-3

1

2009-1

1-3

0

2009-1

2-3

1

2010-0

1-3

0

2010-0

2-2

8

2010-0

3-3

1

2010-0

4-3

0

As

sets

(P

LN

th

ou

san

d)

0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

30,0%

35,0%

40,0%

45,0%

Sh

are

of

eq

uit

ies i

n P

F's

ass

ets

(in

%)

Most effective marketing strategy : to attract „anchor” investors Most effective marketing strategy : to attract „anchor” investors

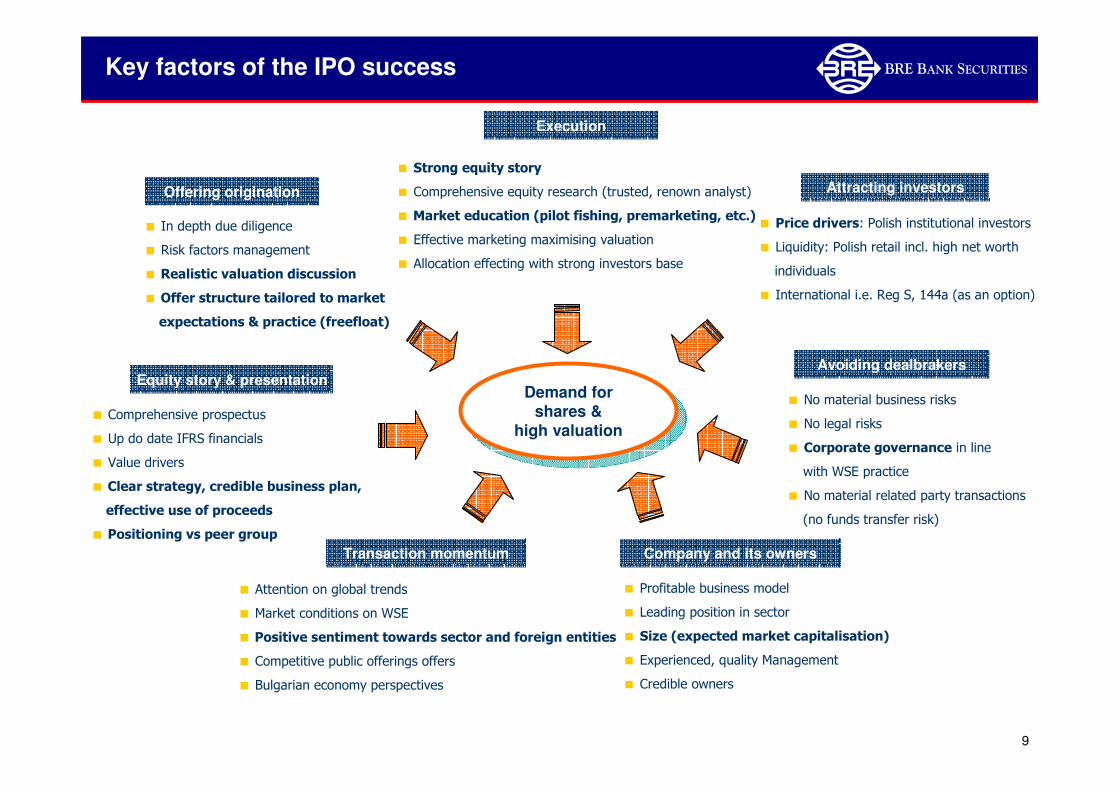

9

Demand for shares &

high valuation

Demand for shares &

high valuation

Offering origination

Execution

� In depth due diligence

� Risk factors management

� Realistic valuation discussion

� Offer structure tailored to market

expectations & practice (freefloat)

Transaction momentum

Attracting investors

Avoiding dealbrakers

� Attention on global trends

� Market conditions on WSE

� Positive sentiment towards sector and foreign entities

� Competitive public offerings offers

� Bulgarian economy perspectives

� Strong equity story

� Comprehensive equity research (trusted, renown analyst)

� Market education (pilot fishing, premarketing, etc.)

� Effective marketing maximising valuation

� Allocation effecting with strong investors base

� Price drivers: Polish institutional investors

� Liquidity: Polish retail incl. high net worth

individuals

� International i.e. Reg S, 144a (as an option)

� No material business risks

� No legal risks

� Corporate governance in line

with WSE practice

� No material related party transactions

(no funds transfer risk)

� Profitable business model

� Leading position in sector

� Size (expected market capitalisation)

� Experienced, quality Management

� Credible owners

Company and its owners

Key factors of the IPO success

� Comprehensive prospectus

� Up do date IFRS financials

� Value drivers

� Clear strategy, credible business plan,

effective use of proceeds

� Positioning vs peer group

Equity story & presentation

10

Choosing IPO momentum

Investors will „buy” the future of the company, historical data is only a point of reference for estimated forecasts.

They will also verify IPO efficiency against other methods of financing.

Investors will „buy” the future of the company, historical data is only a point of reference for estimated forecasts.

They will also verify IPO efficiency against other methods of financing.

financial

results

time

Acquisitions, investments,

internal restructuring, etc.

Base for future growth

IPOPast performance forecasts

Predictable

growth

11

Advisors appoint.Working groups organisationDetailed timetable discussion

Preparation phase

Determiningthe IPOstructure

Drafting the issue prospectus

Financial statements availability

Valuation exercise

Relevant EU FSA procedure

Equity researchreport preparation

1-3 months VI monthI month II month III month V monthIV month

PremarketingRoadshow

Passporting prospectus in Polish FSA & publication

Discussion on the valuation

Due diligence

General Meeting of Shareholders

Example of the WSE IPO timetable

WSE listing

Key factors of the timetable

� Restructuring the issuer (group consolidation, shareholders` tax optimisation, etc.).

� Smoothness of the due diligence process (documentation accessibility, etc.).

� Availability of financial statements to the prospectus.

� Consensus between shareholders and lead manager as to potential value at IPO and the offer structure.

� Timing and complexity of relevant legal actions including EU FSA prospectus approval procedure.

� Market trends i.e.: investors` sentiment towards IPOs or sector, concurring IPOs.

Quarterly abbreviated financials update

Pricing, allocation, subscription

Discussion on thecorporate governance

Restructuring phase

Execution phase

12

Road showBookbuilding

� Working on equity story

� Equity research report preparation

� Preparing roadshow presentation

� Management training

� Presounding meetings with selected

investors – pilot fishing (as an option)

� Launch of limited PR activities (corporate PR)

� Full scale PR/IR campaign

� Publishing of the prospectus

� Equity research report distribution

� Presentation for sales team

� Investor meetings with bookrunners’ analysts

� Gathering investors’ feedback

� Recommendation on the price range

� Roadshow in Poland/internationally:

- one-on-one Management meetings,

- group meetings.

� Bookbuilding

� Recommendation on pricing and allocation

Execution phase & marketing effort

PremarketingFSA procedure

Prospectus approval by the Polish FSA

Setting the price range

Setting the issue price

Overlaping efforts - assuring reliable investors` feedback

Process of market education: gaining continuous feedback from investors and providing

issuer with recommendation as to the transaction status and feasibility.

Advisors` should be always „on the same page” with the issuer.

Process of market education: gaining continuous feedback from investors and providing

issuer with recommendation as to the transaction status and feasibility.

Advisors` should be always „on the same page” with the issuer.

13

POLISH BROKER

Global coordinator, Polish bookrunner, Polish Offering Agent

POLISH BROKER

Global coordinator, Polish bookrunner, Polish Offering Agent

Legal advisorLegal advisor

Scope of roles in the IPO

BULGARIAN/INTERNATIONAL BROKER

Joint co-leader, International bookrunner

BULGARIAN/INTERNATIONAL BROKER

Joint co-leader, International bookrunner

� Discussion with WSE re. listing requirements

� Feedback from Polish institutional investors

� Valuation exercise

� Structure of the IPO

� Participating in drafting sessions of the prospectus

� Polish FSA, WSE, National Depository for Securities procedures

� Equity research report

� Road-show presentations

� Premarketing among Polish institutional investors

� Price range recommendation

� Polish roadshow

� Bookbuilding

� Price and allocation recommendation

� Subscription and settlement

� Feedback from international investors

� Participation in valuation exercise

� Structure of the IPO

� Participation in drafting sessions of the prospectus

� Road-show presentations

� Equity research report

� Premarketing among international institutional investors

� Price range recommendation

� International roadshow

� Bookbuilding

� Price and allocation recommendation

� Advising in the legal aspects of the Offering structure & execution

� Drafting of the issue prospectus

� Relevant Governing Bodies procedures in the mother country

� Preparation of all relevant resolutions

� Advising on the corporate governance

AuditorAuditor

� Opinions to the IFRS financial statements

� Opinions to the pro-forma statements

� Opinions to the forecasts

� Comfort letters

as an option

as an option

PR ardvisorPR ardvisor

14

Subsidiary

IssuerIssuer

shares

InvestorsInvestors

Position in management

/supervisory board,

shares

Subsidiary Subsidiary

Subsidiary

Potential risk of profit transfer may be a

dealbreaker for minority investors

Avoiding related party transaction risks

Equal rights

ShareholdersShareholders

15

ISSUERISSUER New shares

Sale of existing shares

New shares

Sale of existing shares

Institutional Investors:- Polish - International* (as an option)

Institutional Investors:- Polish - International* (as an option)

Polish retail investorsPolish retail investors

Clawback facility

80%

20%

Hypothetical IPO structure

Shareholders(as an option)

Shareholders(as an option)

� The split of the IPO between institutional and individual investors should assure:

� stability of the shareholders structure (institutional investors), and

� appropriate liquidity of shares (retail investors).

� Split between Polish and international investors based on pricing sensitivity*.

� Potential sale of existing shares options to be carefully addressed :

� investors strongly prefer to fuel the company than finance shareholders pockets,

� sale of shares may be perceived as a lack of confidence in future growth.

� Remaining existing shares stake shall be locked-up (min. 12 months).

� WSE investors strongly prefer shares over depositary receipts (none listed yet).

*Based on market practice transactions of the size up to 100m EUR do not require marketing among

foreign investors (not active on the WSE).

*Based on market practice transactions of the size up to 100m EUR do not require marketing among

foreign investors (not active on the WSE).

16

� Acquiring financing for the further expansion – access to the significant pool of Polish sophisticated institutional investors

(approx. EUR 25 bn under management in shares).

� Marketing impact improving brand awareness among:

� potential contractors in Poland,

� financial investors.

� PLC status - improving credibility among the contractors (suppliers & clients).

� Transparency due to disclosure obligations - improving credibility among financial institutions (decreasing financial costs).

� Equity analysts coverage: analysts comments and reports, support of the aware investors.

� Listing among increasing number of foreign issuers on the most dynamically growing CEE capital market.

� Acquiring market valuation of the possessed stakes on the liquid and regulated market.

� Liquidity of the market – possibility of selling shares during IPO or after.

� Adjusting company corporate culture to comply with international corporate governance standards.

� Polish market standards and legal requirements complying with EU law - regulations adjusted to international

investors and shareholder's needs.

� Relatively easy and cost effective further capital increase opportunity.

Key benefits from the WSE IPO

17

BRE Bank Securities(Dom Inwestycyjny BRE Banku S.A.)

00-684 Warsaw 47/49 Wspólna Str.

Polandwww.dibre.pl

Tel. +48 22 697 47 10

18

Appendix 1 (hard copy) - estimated transaction costs

19

Estimated transaction & listing costs

Listing costs

National Depository of Securities (NDS) Fees

� Registration Fee – 0,01% of the shares value (not less than PLN 2,500 (EUR 625) & not more than PLN 100,000 (EUR 25,000))

� other minor fees apply

Warsaw Stock Exchange (WSE) Fees

� Introducing to trading Fee – 0.03% (not less than PLN 8,000 (EUR 2,000) & not more than PLN 96,000 (EUR 24,000))

� Access to trading Fee – PLN 3,000 (EUR 750)

� other minor fees apply

Annual Fees

� Participation Fee – PLN 6,000 (EUR 1,500) - NDS

� Listing Fee – 0.02% of the shares value (not less than PLN 9,000 (EUR 2,250) & not more than PLN 70,000 (EUR 17,500))* - WSE

� other minor fees apply

* In the first year of listing, the Listing Fee is 50% of the Registration Fee

Transaction costs

Investment Bank remuneration

� fixed fee – management fee for the transaction origination

� success fee – placement/underwriting fee calculated as % of value of shares allocated to investors

Legal counsel

� fixed fee – documentation and transaction advisory

Auditor

� fixed fee – opinion to financial statements, opinion to forecast

PR advisor

� retainer fee – media relations, advertisements, prospectus printing, etc.

20

Appendix 2 (hard copy) – financial statements in the prospectus

21

Financial Statements in the prospectus

General obligations regarding historical financial information included in the prospectus:

� Audited historical financial information covering the latest 3 financial years;

� Audited historical financial information for the last two years presented and prepared in a form consistent with that which will be

adopted in the issuer’s next published annual financial statements.

� Audited pro-forma financial information in the case of a „significant gross change” (25%) in any measure of issuers size.

� If the prospectus dated more than nine months after the end of the last audited financial year – interim financial information must be

included (may be unaudited) covering at least the first six months (incl. comparative statements data).

� The last year of audited financial information not older than one of the following: (a) 18 months from the date of the prospectus if the

issuer includes audited interim financial statements in the prospectus; (b) 15 months from the date of the prospectus if the issuer

includes unaudited interim financial statements in the prospectus.

� If quarterly or half yearly financial information published – must be included in the prospectus (with audit of review report, if prepared).

Issuers with complex financial history:

� Where the issuer has a complex financial history, or has made a significant financial commitment, and in consequence the inclusion in

the prospectus of certain items of financial information relating to an entity other than the issuer is necessary in order to satisfy the legal

obligations, those items of financial information shall be deemed to relate to the issuer.

� Where, in the individual case, the obligation to include financial information required by the regulation may be satisfied in more than one

way, preference shall be given to the way that is the least costly or onerous.

� The scope of financial information to be included in the prospectus of issuers with complex financial history should be carefully

discussed with auditors and legal counsel. Seeking acceptance of Polish FSA before filing the prospectus for approval is also

recommended.

Investors expectations

� Most up to date financial information must be included.

� IFRS standard required (in case of consolidation IFRS is required formally).

22

Appendix 3 (hard copy) – case studies of BREs transactions

23

Pre-Emptive Rights Offering BRE BANK S.A. - case study

Details of the transaction

Deutsche Bank AG, London Branch

Global Coordinator

Commerzbank Corporates & Markets

Joint Lead Manager

DI BREDomestic Lead Manager / Offering Agent

EUR 38.9 per shareIssue price

Investors entitled to exercise pre-emptive rights

Structure of the offering

12,371,200 of shares (capital increase)

Shares offered

EUR m 483.9Transaction value

12,371,200Number of shares

Pre-Emptive Rights OfferingTransaction type

WSEMarket

BRE Bank S.A.Issuer

Offering highlights

BRE Bank share price performance vs WIG index

� All shares offered by BRE Bank in its rights issue have been subscribed

with x1,6 oversubscription.

� The Bank raised its capital by 42% i.e. EUR 4.84 bn.

� Investors subscribed 19,337,786 new shares in total, thus exercising all

their pre-emptive rights.

� Commerzbank, BRE Banks' main shareholder with 69.8% of voting

capital, fully exercised its pre-emptive rights.

� Consequently, the demand for the Bank’s shares exceeded by

6,966,586 the number of shares offered.

� The TERP (theoretical ex-right price) discount reached 33,5% and was in

line with other banks` offerings in Europe.

80

100

120

140

160

180

200

2009

-06-

0220

09-0

6-16

2009

-06-

3020

09-0

7-14

2009

-07-

2820

09-0

8-11

2009

-08-

2520

09-0

9-08

2009

-09-

2220

09-1

0-06

2009

-10-

2020

09-1

1-03

2009

-11-

1720

09-1

2-01

2009

-12-

1520

09-1

2-29

2010-0

1-12

2010-0

1-26

2010

-02-0

920

10-0

2-23

2010

-03-

0920

10-0

3-23

2010

-04-

0620

10-0

4-20

2010-0

5-04

2010-0

5-18

2010

-06-0

1

BRE Bank

WIG

%

Largest bank`s public offering in CEE 2010.

24

Details of the transaction

Structure of the offer

Retail investors

15.2%

Employees

3.0%

Institutional investors

81.8%

LWB share price performance vs WIG index

90

100

110

120

130

140

20

09

-06

-25

20

09

-06

-29

20

09

-07

-03

20

09

-07

-07

20

09

-07

-11

20

09

-07

-15

20

09

-07

-19

20

09

-07

-23

20

09

-07

-27

20

09

-07

-31

20

09

-08

-04

20

09

-08

-08

20

09

-08

-12

20

09

-08

-16

20

09

-08

-20

20

09

-08

-24

20

09

-08

-28

20

09

-09

-01

20

09

-09

-05

20

09

-09

-09

20

09

-09

-13

20

09

-09

-17

20

09

-09

-21

20

09

-09

-25

20

09

-09

-29

20

09

-10

-03

20

09

-10

-07

20

09

-10

-11

BOGDANKA WIG

IPO LW Bogdanka SA – case study

19.06.2010Date

Increasing coal extraction Use of proceeds

Local and international (Reg S)Distribution

DI BRELead Manager

EUR 10.56 per shareIssue price

EUR 9.24 – 10.56 per sharePrice range (PLN)

81.8% - Institutional investors

15.2% - Relail investors

Structure of the offering

32.3% of shares (capital increase)Shares offered

EUR 116.2 mTransaction value

11,000,000Number of shares

Initial Public OfferingTransaction type

WSEMarket

Bogdanka S.A.Issuer

IPO of LW Bogdanka worth PLN 528 m reopening the EMEA ECM market in 2009

� 1st largest IPO in EMEA capital markets since NWR offering in May 2008 and

Enea in November 2008.

� Reopening IPO market for institutional and retail investors in Poland.

� Strong demand allowed for pricing at the top price range level EUR 10.56 and

positive opening of the stock +16%.

� Market capitalisation increased at WSE from EUR 0.35 bn (at issue price) to

EUR 0.55 bn.

� Valuation came at 25% premium to its peer group (based on P/E 09P

multiple).

Offering highlights

Demand : Institutional investors 7.5x Retail investors 8,9x

25

IPO PGE domestic retail offering – case study

02.11.2010Date

EUR 5.41 per shareTransaction price

domestic retail syndicate memberRole of DI BRE

EUR 10,588,235,294Total demand

EUR 1,404,426,000Transaction value

259,513,500Number of shares

IPO – privatisationType of offer

WSEMarket

PGE S.A.Issuer

Details of the transaction

Second largest Polish privatisation IPO ever, with BRE as the leader in domestic retail distribution.

Global offering distribution

� Total demand amounted to EUR 11 bn (including retail demand of PLN 6 bn)

� DI BRE as the leader in retail distribution of PGE shares with 32.6% market

share in total retail demand

� DI BRE attracted the highest number of retail investors in PGE IPO – 48.9%

share in the total volume of retail orders

� DIBRE as major distributor among retail with 5% share in global allocation and

18.5% in global demand

Offering highlights Demand breakdown – retail offering

DI BREDI BRE

21other

Polish brokers

32.6%

67.4%

21other Polish

brokers

DI BREDI BRE

Institutional

Retail

15%

85%

5%10%

85%