infrastructure roll-out for non- fossil fuels, a global ... transport/presentasjoner... · 1 600 1...

TRANSCRIPT

Infrastructure roll-out for non-fossil fuels, a global perspective

Oslo, 31st October 2013 l Emmanuel Rothan-Cederberg l Air Liquide Nordic

Air Liquide, world leader in gases for industry, health and the environment

Air Liquide, a worldwide leader

2

Revenue

€15.3

billion

Present in 80

countries

Close to

50,000

employees

31/10/2013 Regional Power for Clean

Transport conference

Air Liquide, world leader in gases for industry, health and the environment

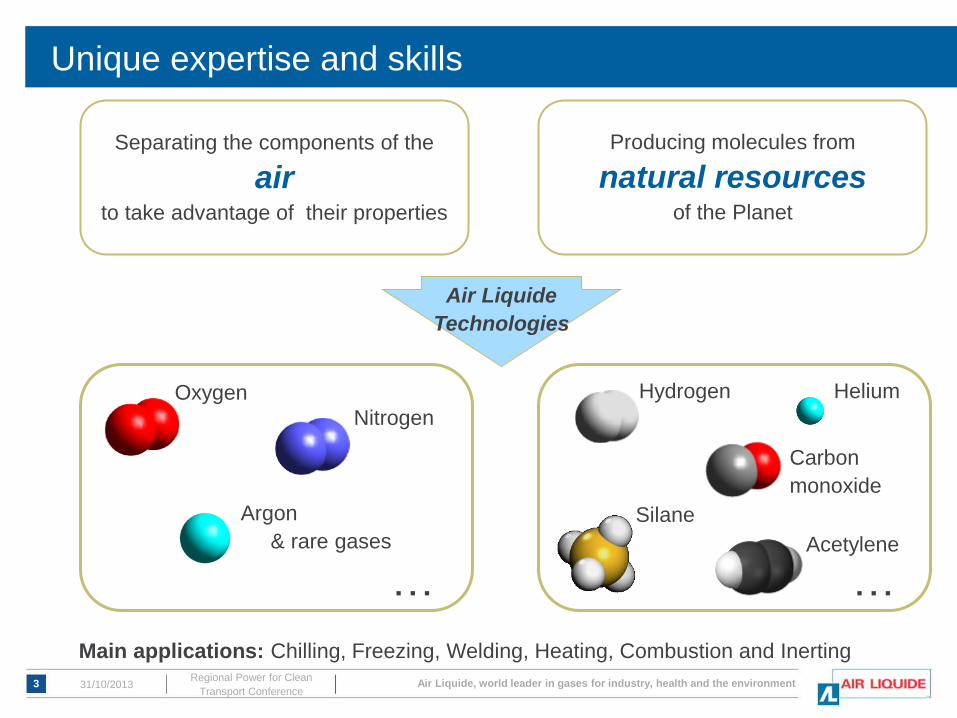

Unique expertise and skills

3

Producing molecules from

natural resources of the Planet

Air Liquide

Technologies

Oxygen

Argon

& rare gases

Hydrogen

Silane

… …

Nitrogen

Helium

Carbon

monoxide

Acetylene

Separating the components of the

air to take advantage of their properties

Main applications: Chilling, Freezing, Welding, Heating, Combustion and Inerting

31/10/2013 Regional Power for Clean

Transport Conference

Air Liquide, world leader in gases for industry, health and the environment

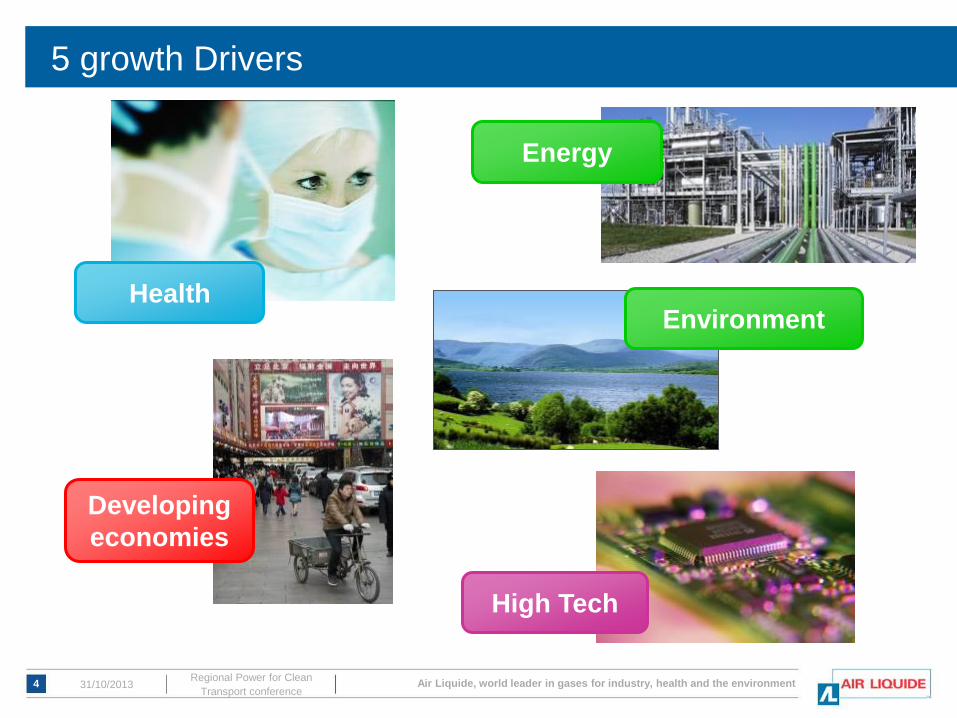

5 growth Drivers

4

High Tech

Developing

economies

Energy

Environment Health

31/10/2013 Regional Power for Clean

Transport conference

Air Liquide, world leader in gases for industry, health and the environment

Air Liquide in the Nordic countries

11/06/2012 IMS Group audit 5

Nordic management

Sales

Filling station

Offshore Filling station

Production sites

Air gases

Acetylene

Carbon dioxide

Hydrogen

High purity gases

Nitrous oxide

Medical gases

VSA

BioCH4 Liquefier

Region

DENMARK

Harjavalta

Raahe

Timrå

Surahammar

Kungsängen Västerås

Nässjö

Mölndal

Kristianstad Hedensted

Odense

Skellefteå

Odda

Kokkola

Sundbyberg

Region NORTH

Malmö

Region SOUTH

Mjøndalen

Oulu

Mullsjö

Kittilä

Helsinki

Karlsborg

Joutseno

Äänekoski

Bergen

Nokia

Horsens

Tåstrup

Helsingborg Mörrum & Nymölla

Kalundborg

Rosenholm

~ 230 million € revenue

~ 500 employees

~ 50,000 customers

> 50 AL sites

Present since 1912 in Sweden (Alfax)

31/10/2013 5 Regional Power for Clean

Transport conference

Lidköping

Air Liquide, world leader in gases for industry, health and the environment

10/

05/

201

2

ALH2E 2012

How to transition towards a new energy mix?

Air Liquide’s Blue Hydrogen initiative

At least 50% of hydrogen energy produced

through carbon-free processes by 2020

renewable energy sources, water electrolysis and

biogas reforming,

carbon capture and storage technologies with natural

gas reforming

A commitment to meet both environmental requirements

and social and economic constraints.

7 Air Liquide, world leader in gases for industry, health and the environment

Hydrogen & Biogas solutions by Air Liquide

■ Air Liquide is committed to leveraging a strong know-how in gas

technologies to offer complete solutions for clean energies

Electrolysis

Fuel-Cells

High pressure (700bar) filling

Membrane technology

Gas liquefaction

Hydrogen energy solutions for

stationary power and transport

Biogas upgrading &

liquefaction solutions

Ruter Hydrogen Refueling Station close to Oslo, Norway Air Liquide’s membrane solution for biogas upgrading

31/10/2013 Regional Power for Clean

Transport conference

Air Liquide, world leader in gases for industry, health and the environment 31/10/2013 8 Regional Power for Clean

Transport conference

Air Liquide, world leader in gases for industry, health and the environment

A broad coalition shared performance estimates on different power trains

Oil and gas

Utilities

Industrial gas

companies

Equipment

OEMs

NGOs, GOs

Car OEMs

Wind

Electrolyser

companies

Industry participants

Approach and principles

▪ All relevant powertrains

(ICE, BEV, PHEV, FCEV)

▪ 3 reference car segments

▪ Cost, emissions, energy

efficiency, driving

performance

▪ Well-to-wheel

▪ >10,000 company data

in a “clean room”

environment

31/10/2013 9 Regional Power for Clean

Transport conference

Air Liquide, world leader in gases for industry, health and the environment

A mix of all drive trains is required to realize full decarbonization

FCEV BEV PHEV ICE

Perfor-

mance

Environ-

ment

Econo-

mics

31/10/2013 10 Regional Power for Clean

Transport conference

Air Liquide, world leader in gases for industry, health and the environment 11 31/10/2013 Regional Power for Clean

Transport conference

Reference

vehicle

Power-

trains

Evaluation

criteria

Small

(A/B)

Medium

(C/D)

SUV

(J)

BEV

FCEV

ICE -

diesel

ICE -

gasoline

PHEV

Overall

sustain-

ability1

Perfor-

mance

User

economics

Purchase price

Running cost

Total cost of

ownership

Payoff time

Production

Operation

End-of-life

…

…

…

…

Data were collected on all drive trains and at a granular level

▪ Potential for biofuels not assessed.

Biofuels are assumed to be blended

achieving 10% CO2 reduction in 2020

and 24% in 2050

▪ Power sector will gradually

decarbonize from 2010 to 2050

▪ Oil price slowly increasing to

$119/bbl in 2030 (IEA)

▪ No taxes on purchase price and fuels

▪ No cherry picking of ‘best data’.

Frozen input data before sharing

results

▪ Impact of potential technology

breakthroughs not included

Air Liquide, world leader in gases for industry, health and the environment

0

20

40

60

80

100

120

140

160

180

200

0 200 400 600 800 1 000 1 200 1 400 1 600

CO2 emissions

gCO2 / km

Range

km

ICE – gasoline

2050

ICE – diesel

2010

BEV

2050

FCEV

2010

2050

2010

2010

2050

PHEV

Low emissions and high range

Battery and fuel cell vehicles can achieve low emissions

C/D SEGMENT

31/10/2013 12 Regional Power for Clean

Transport conference

Air Liquide, world leader in gases for industry, health and the environment

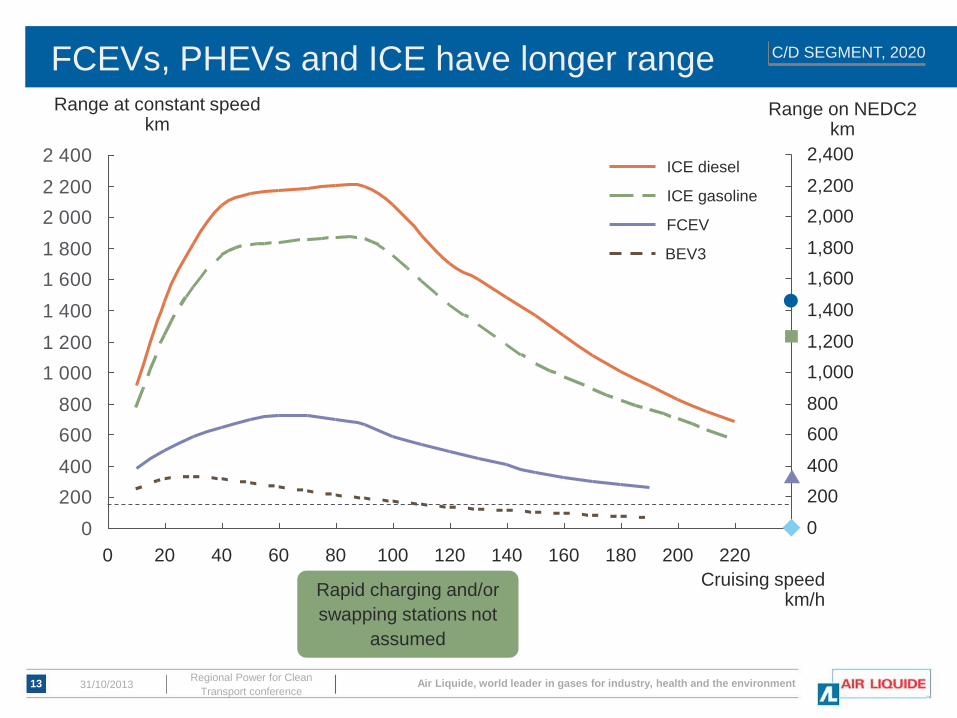

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2 000

2 200

2 400

80 0 140 100 60 120 160 40

800

600

400

200

0

Range at constant speed km

20

2,400

2,200

2,000

1,800

1,600

1,200

1,000

200 220 180

1,400

C/D SEGMENT, 2020

Range on NEDC2 km

BEV3

FCEV

ICE gasoline

ICE diesel

Cruising speed km/h

Rapid charging and/or

swapping stations not

assumed

FCEVs, PHEVs and ICE have longer range

31/10/2013 13 Regional Power for Clean

Transport conference

Air Liquide, world leader in gases for industry, health and the environment

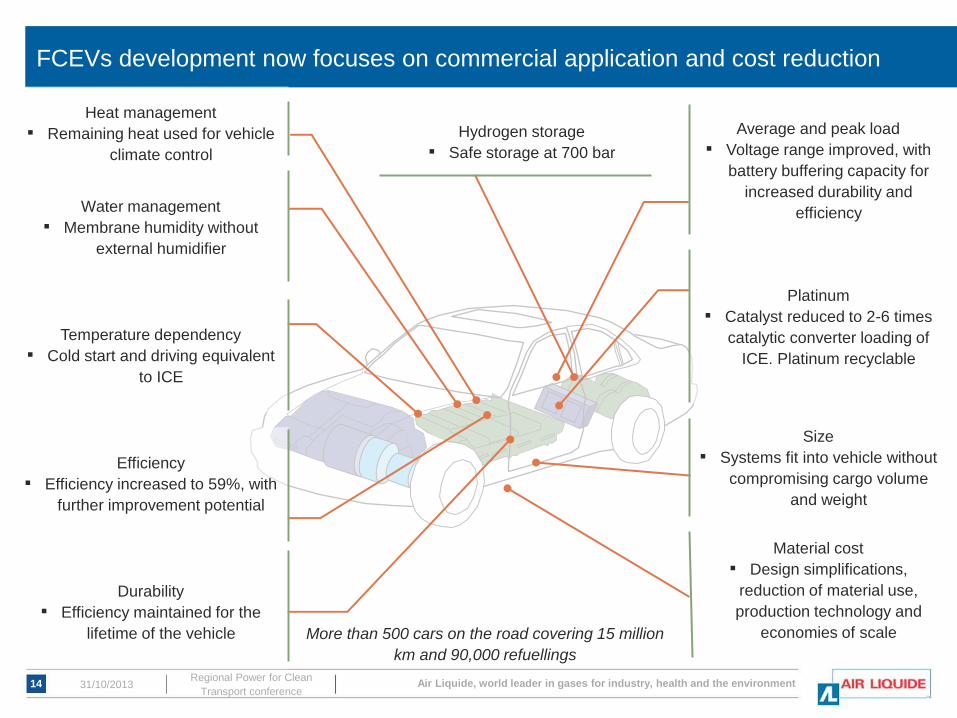

Heat management

▪ Remaining heat used for vehicle

climate control

FCEVs development now focuses on commercial application and cost reduction

Temperature dependency

▪ Cold start and driving equivalent

to ICE

Water management

▪ Membrane humidity without

external humidifier

Efficiency

▪ Efficiency increased to 59%, with

further improvement potential

Durability

▪ Efficiency maintained for the

lifetime of the vehicle

Material cost

▪ Design simplifications,

reduction of material use,

production technology and

economies of scale

Hydrogen storage

▪ Safe storage at 700 bar

Size

▪ Systems fit into vehicle without

compromising cargo volume

and weight

Average and peak load

▪ Voltage range improved, with

battery buffering capacity for

increased durability and

efficiency

Platinum

▪ Catalyst reduced to 2-6 times

catalytic converter loading of

ICE. Platinum recyclable

More than 500 cars on the road covering 15 million

km and 90,000 refuellings

31/10/2013 14 Regional Power for Clean

Transport conference

Air Liquide, world leader in gases for industry, health and the environment

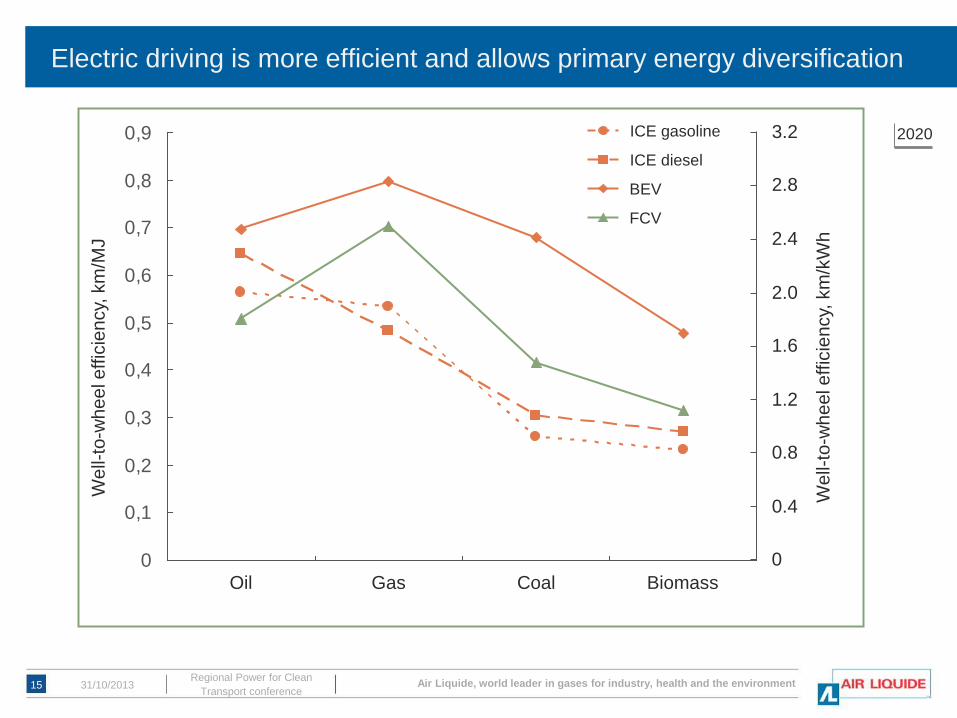

We

ll-to

-wh

ee

l e

ffic

ien

cy,

km

/MJ

FCV

BEV

ICE diesel

ICE gasoline

0

0,1

0,2

0,3

0,4

0,5

0,6

0,7

0,8

0,9 3.2

2.8

2.4

2.0

1.6

1.2

0.8

0.4

0

Biomass Coal Gas Oil

We

ll-to

-wh

ee

l e

ffic

ien

cy,

km

/kW

h

2020

Electric driving is more efficient and allows primary energy diversification

15 31/10/2013 Regional Power for Clean

Transport conference

Air Liquide, world leader in gases for industry, health and the environment

Annual

driving

distance

(1,000 km)

A/B C/D J

<10

10-20

>20

PHEV/BEV/FCEV

Lowest cost CO2 abatement solution

2050

FCEV

FCEVs are specifically suited for larger cars, that represent 70% of CO2

emissions

16 31/10/2013 Regional Power for Clean

Transport conference

Air Liquide, world leader in gases for industry, health and the environment

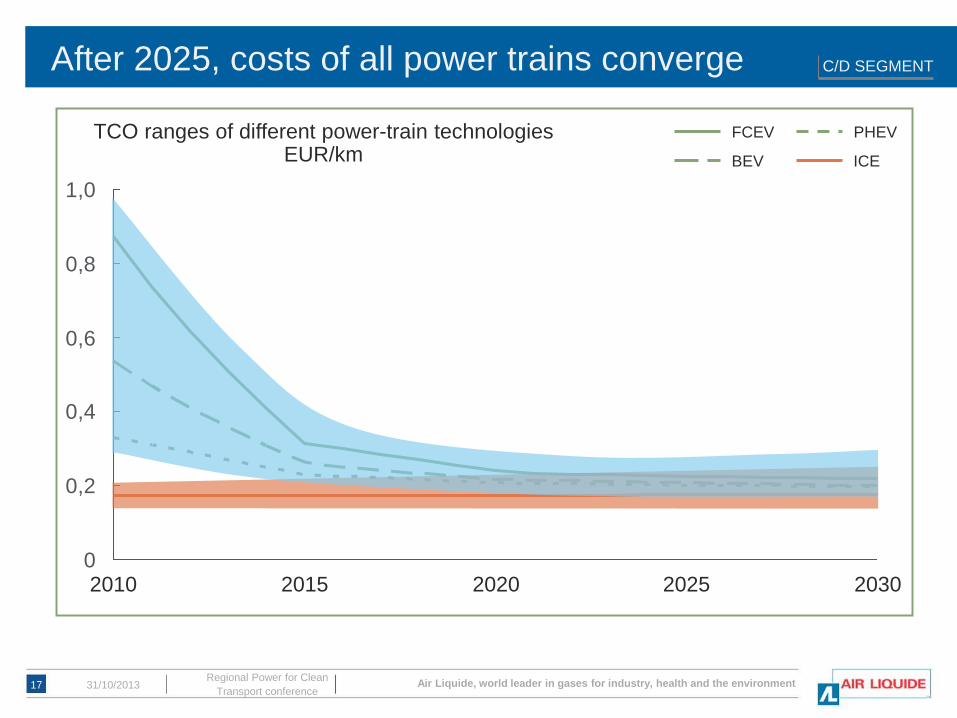

0

0,2

0,4

0,6

0,8

1,0

TCO ranges of different power-train technologies EUR/km

2030 2025 2020 2015 2010

BEV

FCEV

ICE

PHEV

C/D SEGMENT After 2025, costs of all power trains converge

17 31/10/2013 Regional Power for Clean

Transport conference

Air Liquide, world leader in gases for industry, health and the environment

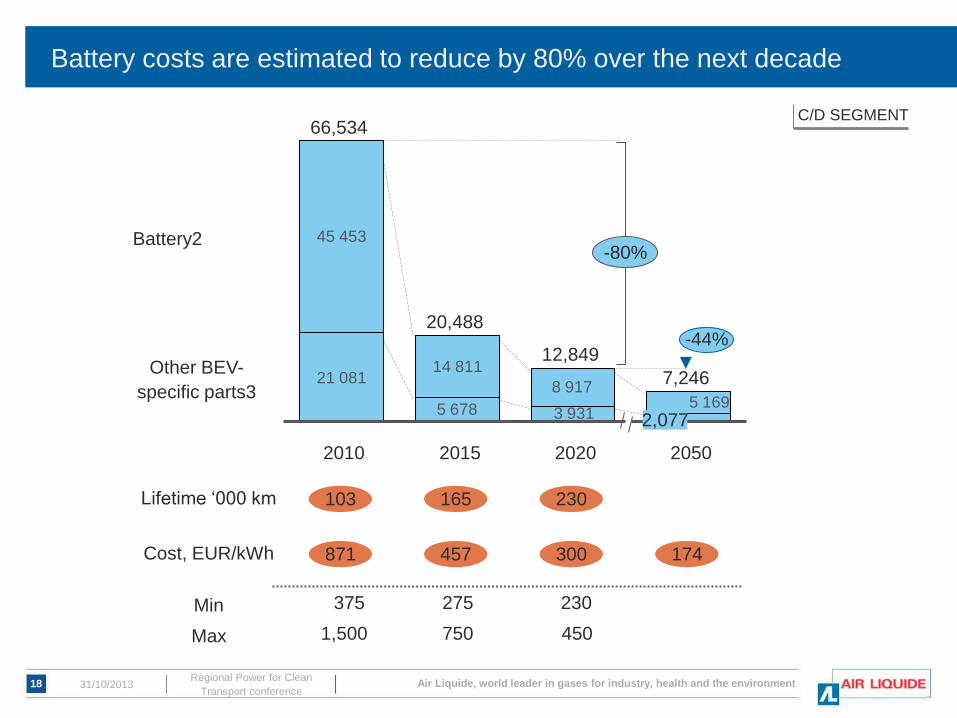

21 081

45 453

14 811

8 917

3 9315 678 5 169

7,246

12,849

20,488

Other BEV-

specific parts3

Battery2

2050

2,077

2020 2015 2010

66,534

-44%

Lifetime ‘000 km 103 165 230

Cost, EUR/kWh 871 457 300 174

Min 375 275 230

Max 1,500 750 450

-80%

Battery costs are estimated to reduce by 80% over the next decade

C/D SEGMENT

31/10/2013 18 Regional Power for Clean

Transport conference

Air Liquide, world leader in gases for industry, health and the environment

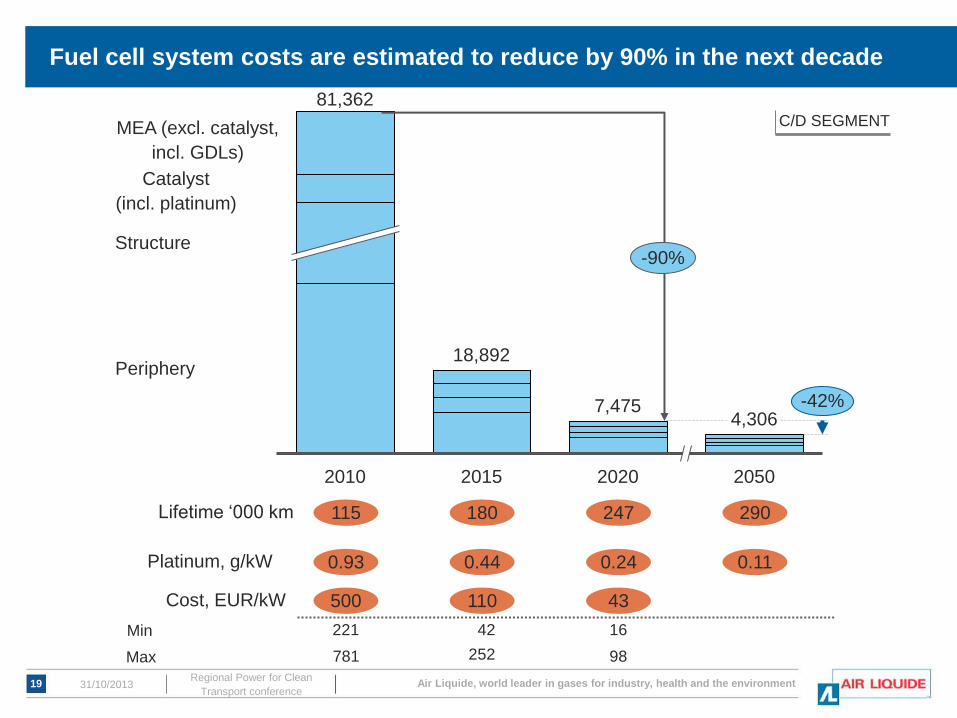

4,306

Periphery

Structure

Catalyst

(incl. platinum)

MEA (excl. catalyst,

incl. GDLs)

2050 2020

7,475

2015

18,892

2010

81,362

-42%

Lifetime ‘000 km 115 180 247 290

Platinum, g/kW 0.93 0.44 0.24 0.11

Cost, EUR/kW 500 110 43

Min

Max

42 16 221

781 252 98

-90%

Fuel cell system costs are estimated to reduce by 90% in the next decade

C/D SEGMENT

31/10/2013 19 Regional Power for Clean

Transport conference

Air Liquide, world leader in gases for industry, health and the environment

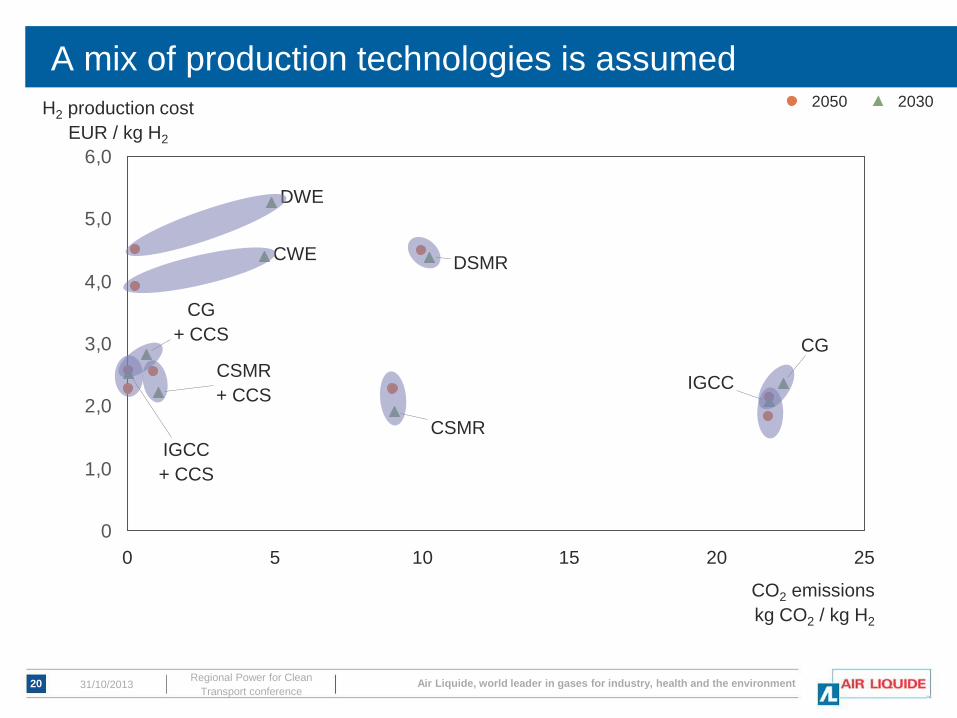

0

1,0

2,0

3,0

4,0

5,0

6,0

H2 production cost

EUR / kg H2

CO2 emissions

kg CO2 / kg H2

5 25 20 15 10 0

IGCC

+ CCS

IGCC

CG

+ CCS CG

CWE

DWE

CSMR

+ CCS

CSMR

DSMR

2030 2050

A mix of production technologies is assumed

31/10/2013 20 Regional Power for Clean

Transport conference

Air Liquide, world leader in gases for industry, health and the environment

0

5

10

15

2050

Hydrogen cost EUR per kg

2010 2045 2040 2035 2030 2025 2020 2015

-67%

Retail costs are inefficient in the first 15 years

Hydrogen

infrastructure 5%

of total cost

Retail Production Distribution

31/10/2013 21 Regional Power for Clean

Transport conference

Air Liquide, world leader in gases for industry, health and the environment

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

2050

3,363

2045

2,655

2040

3,581

2035

4,775

2030

3,922

2025

2,796

2020

890

2015

105

2010

Retail

Production

Distribution

EUR millions

Supply investments of about Eur 3 billion are required to build up a

market for 1 million vehicles

31/10/2013 Regional Power for Clean

Transport conference 22

Air Liquide, world leader in gases for industry, health and the environment

-50

0

50

100

150

200

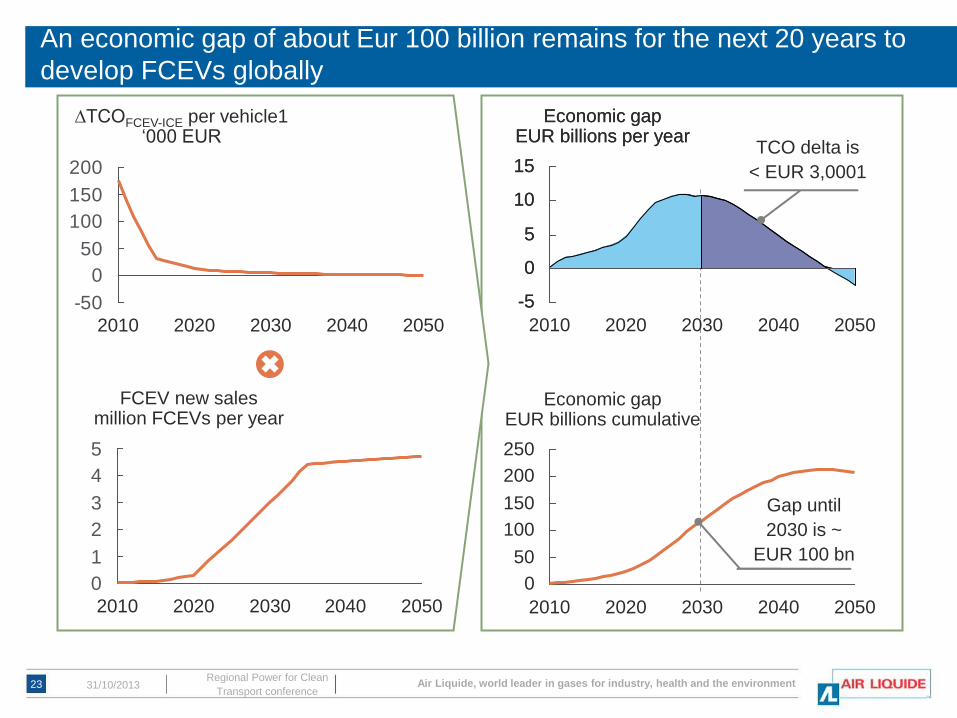

∆TCOFCEV-ICE per vehicle1 ‘000 EUR

2050 2040 2030 2020 2010

0

1

2

3

4

5

2050

FCEV new sales million FCEVs per year

2010 2020 2040 2030

2020 2010 2050

5

2030 2040

Economic gap EUR billions per year

10

-5

0

15

150

Economic gap EUR billions cumulative

200

100

250

50

0

2050 2040 2010 2030 2020

Gap until

2030 is ~

EUR 100 bn

10

5

0

-5

15

Economic gap EUR billions per year

TCO delta is

< EUR 3,0001

An economic gap of about Eur 100 billion remains for the next 20 years to

develop FCEVs globally

31/10/2013 Regional Power for Clean

Transport conference 23

End of presentation Thank you for your attention