informational frictions, syndicate structure, and loan pricing: new evidence from international...

TRANSCRIPT

Informational Frictions, SyndicateStructure, and Loan Pricing: New Evidencefrom International Lending*

Sung C. BaeDepartment of Finance, Bowling Green State University

Byung-Uk Chong**College of Business Administration, University of Seoul

Yura KimCollege of Business Administration, University of Seoul

Received 30 September 2013; Accepted 19 December 2013

Abstract

We examine how syndicate structure affects loan pricing in international syndicated lending.

Using extensive syndicated loan data across 103 countries from 1982 to 2012, we find that

both measures of syndicate structure, the proportional number of lead arrangers, and the pro-

portion of loan amount retained by lead arrangers in syndication, are significantly negatively

related to loan risk premiums after controlling for contract and country characteristics. These

findings indicate that, under informational frictions, as the riskiness of a borrower increases,

the syndicate structure becomes more diversified in a way that lead arrangers and participating

banks share the loan amount and the associated credit risk in syndication. Hence, syndicate

participants collaboratively determine higher loan spreads to align higher compensation for

active commitments and greater risk sharing of participating banks in syndication. Our results

offer new evidence strongly supporting the diversified nature of syndicate structure but

contradicting the concentrated nature of syndicate structure prevailing in existing studies.

Keywords Syndicate structure; International syndicated lending; Loan risk premium; Infor-

mational frictions

JEL Classification: F31, F34, G15, G21

*Acknowledgments: The authors are grateful to Joong Ho Han, Ali Nejadmalayeri, an anon-

ymous referee of the Journal, and session participants at the 2013 FMA Annual Meetings and

the 8th International Conference on Asia-Pacific Financial Markets. Bae and Chong gratefully

acknowledge the financial support from the CBA Summer Research Grant at Bowling Green

State University and the 2012 Research Fund of the University of Seoul, respectively. The

usual disclaimer applies.

**Corresponding author: Byung-Uk Chong, College of Business Administration, University of

Seoul, 163 Seoulsiripdae-ro, Dongdaemun-gu, Seoul 130-743, Korea. Tel: +82-2-6490-2250,

Fax: +82-2-6490-2219, email: [email protected].

[Note: Correction added on 18 March 2014 after initial online publication on 12 March

2014. Byung-Uk Chong’s affiliation has been corrected to University of Seoul.]

Asia-Pacific Journal of Financial Studies (2014) 43, 124–155 doi:10.1111/ajfs.12042

124 © 2014 Korean Securities Association

1. Introduction

International corporate lending mainly takes the form of syndicated loans. A syndi-

cated loan is offered by a group of lenders jointly agreeing to provide financing to a

particular borrower. Over the past two decades, the syndicated corporate loan mar-

ket has become the most important and dominant source of global corporate

financing. This high growth trend reflects the key benefits that syndicated loans are

less expensive and more efficient to administer than traditional individual credit

lines.1

In syndicated lending, lead arrangers negotiate contract terms with a borrowing

firm and organize a syndicate with participating banks. In this process, a lead arran-

ger assumes a risky position as a lender by retaining a portion of the loan and acts

as the intermediary between the borrower and participating banks by allocating

remaining loan shares to the latter. This multi-party nature of syndicated lending,

in particular, the exclusive relationship between lead arrangers and a borrower and

the unobservability of lead arrangers’ screening and monitoring efforts, potentially

creates adverse selection and moral hazard problems that must be considered in

designing a syndicate structure and determining contract terms including loan

price.2 Indeed, Ivashina (2009) shows that the information asymmetry between the

lead arranger and other participating banks in the syndicate has a large economic

cost, accounting for approximately 4% of the total cost of credit. As noted in

Pichler and Wilhelm (2001), a syndicate structure is an organizational response to

the information asymmetry problem in the process of syndicate composition.

In this paper, we examine how syndicate structure and pricing of syndicate

loans are related in international syndicated lending. Under the environment of

information asymmetry on the riskiness of borrowing firms between lead arrang-

ers and participating banks, the syndicate structure will be determined primarily

by how the risk and return associated with the loan are shared among the syndi-

cate participants. The classical work of Leland and Pyle (1977) provides insight

on the information asymmetry problems between lenders and borrowers to

explain pricing and terms on debt contracts. When applying Leland and Pyle

(1977) to syndicated lending, lead arrangers may ex ante possess private informa-

tion about the borrower, not known to participating banks, by means of their

exclusive access to the borrower’s information. This environment creates an

adverse selection problem and demands a mechanism under which lead arrangers

are required to retain a portion of the loan that will vary with the severity of the

adverse selection problem.

1According to the Thomson Reuters Legal Advisory review, global syndicated lending for the first half

of 2013 reached US$1.93 trillion, representing an 18.5% increase from the first six months of 2012.2The price of a syndicated loan is typically composed of a benchmark reference interest rate

such as the London Inter-Bank Offered Rate (LIBOR) and the spread reflecting a borrowing

firm’s riskiness.

Syndicate Structure and Loan Pricing

© 2014 Korean Securities Association 125

A large body of studies has examined the issue of information asymmetry prob-

lems between lead arrangers and participating banks in syndicated lending (see, e.g.

Pennacchi,1988; Bolton and Scharfstein, 1996; Dennis and Mullineaux, 2000; Pichler

and Wilhelm, 2001; Lee and Mullineaux, 2004; Jones et al., 2005; Champagne and

Kryzanowski, 2007; Sufi, 2007; Ivashina, 2009; Panyagometh and Roberts, 2010).

For example, Pichler and Wilhelm (2001) develop a model where, in the presence

of information asymmetry among lenders, a syndicate led by lead arrangers is

Pareto-dominant over a leaderless syndicate. They argue that, in the relationship-

intensive investment banking industry, a lead arranger acts as a monitoring mecha-

nism that threatens other lenders (syndicate participants) who might shirk in their

monitoring efforts. These studies claim that lead arrangers have an exclusive access

to private information about a borrower, while participating banks rely on lead

arrangers to assess the riskiness of the borrower. Based on this premise, several

studies offer empirical evidence in support of the concentration nature of loan

syndication that as information frictions between lead arrangers and participating

banks deepen, a syndicate structure becomes more concentrated (see, e.g. Sufi,

2007).

It is reasonably expected, however, that the heightened credit risk exposure of a

lead arranger to a single borrower through the retention of a large loan share

restricts the diversification of the lead arranger’s loan portfolio. Pennacchi (1988)

and Gorton and Pennacchi (1995) show that diversification of credit risk is among

the main reasons for loan sales by lead arrangers. Furthermore, informational fric-

tions between lead arrangers and participating banks may create an environment

where the two parties negotiate and design the contract terms of a syndicated loan.

In this setting, the information lead arrangers possess on a borrower’s riskiness is

neither exclusive nor dominantly superior to that of participating banks, but the

latter also has access to the information on the borrower’s riskiness. This is possible

because in syndicated loan markets a small number of big players (lenders and

borrowers) repeatedly make large loan deals, and each lender can become either a

lead arranger or a participating bank in different loan deals with an identical

borrower (Cai et al., 2010).

The main issue to be explored in our paper is which type of syndicate structure

between concentrated and diversified lead arrangers will take under informational

frictions between lead arrangers and participating banks. In order to examine this

issue, we test two competing hypotheses, concentration hypothesis and diversifica-

tion hypothesis, using extensive firm- and contract-level syndicated loan data for

international lending. The evidence will offer new insights into syndicate partici-

pants’ behaviors in sharing information on the borrower, forming the syndicate,

and determining loan risk premiums for syndicate participants.

The two hypotheses are based on a different premise on the information asym-

metry between lead arrangers and participating banks. The concentration hypothesis

posits that lead arrangers possess private information on a borrower almost exclu-

sively and that, as the informational-friction problem deepens, other banks are less

S. C. Bae et al.

126 © 2014 Korean Securities Association

likely to participate in the syndicate. Accordingly, lead arrangers are compelled to

concentrate the syndicate structure by retaining more loan shares and hence higher

loan risk, which leads to higher loan risk premiums. In contrast, the diversification

hypothesis posits that both lead arrangers and participating banks possess informa-

tion, though different in quantity and/or quality, through which both can assess the

riskiness of the borrower. This information is made available to both parties owing

to their repeated loan deals with taking different positions between lead arranger

and participating bank. Hence, as the riskiness of a borrower increases, lead arrang-

ers and participating banks collaboratively determine the credit risk of the borrower

and negotiate the allocation of loan shares. In this setting, lead arrangers compen-

sate participating banks with higher risk premiums to seek their syndicate participa-

tion. In sum, the concentration (diversification) hypothesis postulates that a

concentrated (diversified) syndicate structure accompanies a higher loan risk

premium.

Employing over 8000 syndicated loan contracts made by US banks to borrowers

in 103 overseas countries during the January 1982 to June 2012 period, we find that

both measures of syndicate structure, the number of lead arrangers relative to the

total number of lenders in a syndicate, and the portion of a syndicated loan

retained by lead arrangers, are significantly negatively related to loan risk premiums.

This finding is consistent with the diversification hypothesis but contrary to the

concentration hypothesis. Undocumented in the existing literature, our evidence

strongly supports the diversification nature of the syndicate structure in interna-

tional loan markets but contradicts the concentration nature of the syndicate struc-

ture in the US domestic loan markets as documented in existing studies (see, e.g.

Sufi, 2007; Ivashina, 2009).

Our evidence of the strong negative effect of the syndicate structure (i.e. syndi-

cate concentration) on loan risk premium is also in accordance with the findings

in Angbazo et al. (1998) and Focarelli et al. (2008). These studies, however, inter-

pret the negative relationships between syndicate concentration and loan risk pre-

mium as they relate to the certification effect that greater loan shares of lead

arrangers provide a credible signal of borrower quality and thus alleviate informa-

tion asymmetry problems. In this setting, the determination of syndicate structure

is viewed mainly from the lead arranger’s initiative, and thus participating banks

are passive in forming the syndicate structure and the associated loan pricing. In

contrast, we view the negative relationship as attributable primarily to the strategic

interaction between lead arrangers and participating banks under the environment

of informational friction. We interpret the diversification nature of a syndicate

structure as an outcome of active and cooperative risk sharing by both parties in

the syndicate.

The remainder of our paper is organized as follows. Section 2 reviews syndi-

cated loan markets and the previous literature and develops testing hypotheses. Sec-

tion 3 describes data and conducts empirical analysis. Section 4 presents empirical

results. Section 5 provides a summary and conclusion.

Syndicate Structure and Loan Pricing

© 2014 Korean Securities Association 127

2. Background on Loan Syndication and Development of Hypotheses

2.1. Syndicated Loan Markets and Loan Syndication Process

The high growth trend in international syndicated lending implies that there exist

substantial economic and financial benefits for both lenders and borrowers. From

the perspective of relationship lending, all parties involved in syndicated loan con-

tracts such as lead arrangers, participating banks, and borrowing firms can build

stable and persistent relationships through syndicated loan deals, which are often

repeatedly made by the same borrowers and lenders, especially in the international

syndicated loan markets. For the borrowers, syndicated loans provide a relatively

easy and alternative access to large-scale financing compared to issuing corporate

bonds or stocks. In addition, the costs of syndicated loans at large are lower than

those of other financing sources due to higher competitiveness in syndicated loan

markets. Another benefit to borrowers is the flexibility in contract deals such as

currency selection, renewal of contract, and maturity. Moreover, syndicated loans

can be offered for a variety of purposes such as corporate control, project financing,

debt repayment, and so forth. For lenders, syndication allows flexible loan portfo-

lios. Lenders can either concentrate or diversify loan portfolios while sharing infor-

mation about borrowers through participating in syndication. Syndication also

helps banks cope with the regulation, which forbids excessive and concentrated

exposure to credit risk arising from repeated relationship lending.

Loan syndication is processed through three main phases. First, during the pre-

mandated phase, the borrower solicits competitive offers to arrange and manage the

syndication with one or more banks. The borrower chooses one or more lead

arrangers that are mandated to form a syndicate, and consequently negotiates a pre-

liminary loan agreement. Second, during the post-mandated phase, the lead arrang-

ers begin the syndication process. This involves drafting a preliminary loan contract

and preparing a documentation package for the potential syndicate participants,

called information memorandum. The memorandum contains information about

the borrower’s credit worthiness and loan contract terms and conditions. A road

show is then organized to present and discuss the content of the memorandum. In

the meantime, lead arrangers establish a timetable for commitments and closing,

formally invite participants, and determine loan allocations. Third, the last phase

takes place after completion of the contract and arrangement of syndicate structure,

when the loan becomes operational and binds the borrower and the syndicate par-

ticipants to the debt contract (see Godlewski, 2007, 2010; Standard & Poor’s, 2011).

2.2. Syndicate Structure and Informational Frictions

Before closing the contract, lead arrangers collect information on the borrower,

evaluate the riskiness of the borrower, and provide participating banks with infor-

mation and an evaluation of the borrower. If the private information collected by

the lead arranger(s) through due diligence or through previous lending relationships

cannot be credibly communicated to the participating banks, an adverse selection

S. C. Bae et al.

128 © 2014 Korean Securities Association

problem might arise. In other words, the lead arrangers may be inclined to syndi-

cate loans for unreliable, risky borrowers at the expense of participating banks

(Pichler and Wilhelm, 2001). After closing the contract, if the participating banks

delegate monitoring to the lead arrangers but their monitoring efforts are unobserv-

able, a moral hazard problem might arise. Lead arrangers may shirk from due dili-

gence of monitoring, as described by Holmstrom (1979), and a moral hazard

problem may intensify when the loan shares of lead arrangers are relatively small.

However, such opportunistic behavior of lead arrangers can also generate a rep-

utation risk ex post that may endanger the success of future syndications because

the syndicate is often repeated, as noted in Champagne and Kryzanowski (2007).

They find that banks repeat syndicate alliances with the same banks, and the lead

bank’s reputation contributes to syndicate composition and structure.

Several studies show evidence that in the existence of multiple lenders like syn-

dicated lending, lender composition and structure convey information asymmetry

between lenders and borrowers. These studies also investigate how to resolve agency

problems through the structuring of syndicates and designing of loan contract terms

and conditions. For example, a borrower with less information asymmetry is more

likely served with multiple syndicate lenders rather than a sole lender (Dennis and

Mullineaux, 2000).3 Bolton and Scharfstein (1996) argue that it becomes harder for

multiple lenders to reach a collective decision when a borrower is in financial dis-

tress, suggesting that a risky borrower ex ante is best served with a concentrated

syndicate. This is consistent with the findings of Jones et al. (2005) and Sufi (2007)

that lead arrangers hold a larger portion of loans and form a smaller number of

participating banks for more information-problematic loans. Similarly, Panyago-

meth and Roberts (2010) find that lead arrangers use privately obtained informa-

tion to credibly certify borrowers, rather than taking advantage of borrowers.4 Lee

and Mullineaux (2004) show that syndicates are usually smaller and more cohesive

when little information about the borrower is available, when credit risk is relatively

high, and/or when a loan is secured. By conducting cross-country analysis across 22

Western European and East Asian countries drawn from the DealScan database, Lin

et al. (2012) show that lead arrangers tend to structure syndicates that facilitate

enhanced due diligence and monitoring efforts when the control–ownership diver-

gence is large in borrower’s corporate governance. These syndicates are relatively

3Dennis and Mullineaux (2000) find that when a loan is relatively large, the borrower is a

publicly traded firm, and/or the lead arranger is relatively reputable, the loan is more likely

to be syndicated. They also find that the lead arrangers tend to hold larger shares of syndi-

cated loans with more severe information problems.4Panyagometh and Roberts (2010) use the change in Altman’s z-scores over time as a proxy

for the lead bank’s informational advantage over participating banks on the riskiness of the

borrowers and find that a potential increase in the Altman’s z-score on the borrower (i.e.

improvement in credit risk) is positively related to the loan portion allocated to participating

banks.

Syndicate Structure and Loan Pricing

© 2014 Korean Securities Association 129

concentrated and composed of domestic banks that are geographically close to the

borrowing firms and that have lending expertise related to the industries of the bor-

rowers. Ferreira and Matos (2012) show that banks are more likely to act as lead

arrangers when they have some links in the corporate governance of the borrowing

firm in the international syndicated loan market.

Information quality not only dictates the syndicate structure but also influences

the composition of top-level lead and co-lead banks. The presence of multiple spe-

cialized co-agents can mitigate potential agency conflicts between informed lead

arrangers and participating banks through strengthened screening and monitoring

(Franc�ois and Missonier-Piera, 2007). In selecting partners, lead arrangers are more

likely to choose co-agents with comparable lending expertise such as similar indus-

try specialization that would allow lead banks to allocate more shares to co-agents

(Cai et al., 2010). One can find such a similarity in the international loan market.

The syndicate structure of international corporate lending becomes more concen-

trated as the law enforcement of the borrowing firm’s country becomes stronger

(Godlewski, 2007). This is because the lead arrangers increase shares in syndication

as monitoring costs decrease due to stronger law enforcement in the borrower’s

country.

2.3. Syndicate Structure and Loan Risk Premium

The existing literature provides evidence that syndicates are structured to enhance

screening and monitoring efforts, which in turn affect the loan pricing mechanism.

We review these studies and develop two competing hypotheses regarding the test-

able relationship between the syndicate structure and the loan risk premium of a

loan contract.

2.3.1. Concentration hypothesis

In the framework of Holmstrom and Tirole (1997), lead arrangers have an incentive

to shirk due to the higher costs of monitoring efforts. The lack of monitoring is

typically aggravated, as the lead arranger’s monitoring efforts are not visible and the

lead arrangers retain a small portion of loans. Conversely, Sufi (2007) and Ivashina

(2009) show that a larger portion of the loan retained by the lead arrangers not

only signals a credible commitment in due diligence and ex post monitoring efforts,

but also provides a strong signal of borrower quality ex ante. In particular, Ivashina

(2009) conducts her analyses based on the assumption that the lead arrangers aim

to diversify syndicate structure to reduce risk while private information in the

hands of the lead arrangers that are not known to syndicate participants would trig-

ger the latter to demand a risk premium. Her results show that borrowing costs can

be effectively managed by controlling the share of the loan retained by the lead

arrangers. In this severe information asymmetry environment, lead arrangers would

attempt to diversify the syndicate structure by decreasing their shares as the infor-

mation problem deepens. Given the lack of information on the borrower, however,

participating banks are unwilling to participate in the syndicate by decreasing their

own loan shares in the syndicate. Accordingly, the lead arrangers are compelled to

S. C. Bae et al.

130 © 2014 Korean Securities Association

concentrate the syndicate structure and in return demand higher loan risk premi-

ums for their undiversified loan portfolios and increased credit risk.

Therefore, an increase in the loan shares retained by lead arrangers will increase

the loan spread required by the lead arrangers while this will reduce the loan spread

required by the participating banks. However, because only the lead arrangers have

the dominant initiative in designing loan contracts, as Ivashina (2009) argues, a

loan spread increases as the syndicate structure becomes concentrated. Based on

these discussions, we state the concentration hypothesis as follows:

Concentration hypothesis: A concentrated syndicate structure accompanies a higher

loan risk premium demanded by lead arrangers for their unshared (or less shared)

risk-taking in syndication under information asymmetry between lead arrangers and

participating banks. Hence, a positive relationship between measures of syndicate

concentration and loan risk premium is expected.

2.3.2. Diversification hypothesis

Cai et al. (2010) show that in syndicated loan markets, repeated transactions

between the same lenders and borrowers are frequently made, resulting in relation-

ship banking within a group of lenders and borrowers. In this environment, a len-

der can be either a lead arranger or a participating bank in different debt contracts

with an identical borrower. This implies that private information retained by the

lead arrangers may be transparent to participating banks to a certain extent, and

the lead arrangers are no longer in a superior position in owning private informa-

tion (Champagne and Kryzanowski, 2007). Hence, depending on the contents and

quality of information they possess, lead arrangers and participating banks may

strategically interact in determining their shares of exposure to risk and the return

commensurate with that risk, that is, the loan risk premium.

An important implication of these studies is that the informational frictions

between lead arrangers and participating banks may not always lead to a concen-

trated syndicate structure. Rather, if the appropriate compensation for risk-taking is

aligned in contract terms and conditions, especially in loan pricing, the strategic

interaction between lead arrangers and participating banks can lead to a diversified

syndicate structure.

As a competing hypothesis to the concentration hypothesis, we develop the

diversification hypothesis. Unlike the concentrated syndicate structure, where lead

arrangers possess private information but participating banks do not, the diversified

syndicate structure represents a situation where both lead arrangers and participat-

ing banks possess information on the borrowing firm’s riskiness, although the qual-

ity and content of information could be different between the two parties. As the

risk of the borrowing firm increases, lead arrangers and participating banks share

the loan shares and the associated credit risk in the syndicate, leading to a diversi-

fied syndicate structure. In this setting, lead arrangers agree to take a smaller share

of the syndicated loan while offering a higher risk premium to participating banks

to seek for their active commitments to the syndicate and compensate for their

Syndicate Structure and Loan Pricing

© 2014 Korean Securities Association 131

bearing additional risk in the syndicate. This discussion leads us to the diversifica-

tion hypothesis as follows:

Diversification hypothesis: A diversified syndicate structure accompanies a higher

loan risk premium demanded by participating banks for their active commitment

to syndicate and risk-sharing under informational frictions between lead arrangers

and participating banks. Hence, a negative relationship between measures of syndi-

cate concentration and the loan risk premium is expected.

It is worth noting that although the diversification hypothesis in our paper pre-

dicts the same negative relationship between measures of syndicate concentration

and loan risk premium as the certification effect in the studies of Angbazo et al.

(1998) and Focarelli et al. (2008), there is a distinctive difference between the diver-

sification hypothesis and the certification effect. Angbazo et al. (1998) report that

syndicated loans have lower loan risk premiums, which are further lowered by the

presence of a lead arranger who retains a large share. In their study, the negative

relationship between syndicate concentration and loan spread is attributed to the

certification effect that a large loan share of lead arrangers provides a credible signal

about the creditworthiness of a borrower and the due diligence in monitoring

responsibilities. This certification effect alleviates the screening and monitoring

problems in informationally opaque debt contracts and reduces the related loan risk

premium. Employing data from over 80 countries, Focarelli et al. (2008) show simi-

lar evidence in support of the certification effect.

These studies, however, explain the determination of syndicate structure and

contract terms mainly from the lead arrangers’ perspective. Hence, participating

banks are just passive in designing the syndicate structure and the associated loan

price. In this setting, active discretion in credit analysis is not exercised by partici-

pating banks and thus strategic risk sharing is not conducted by lead arrangers and

participating banks in a syndicate.

In contrast, the predicted negative relation in the diversification hypothesis

results primarily from the strategic interactions between lead arrangers and partici-

pating banks under the information friction environment. We interpret the diversi-

fied syndicate structure as an outcome of active commitments to the syndicate,

especially by participating banks. This becomes possible due to the repeated deals of

syndicated loan contracts with taking different positions of lead arranger and partic-

ipating bank.

3. Empirical Design

3.1. Regression Model and Measurement of Variables

For our analysis, we model the loan risk premium of a syndicated loan mainly as a

function of the loan’s syndicate structure. The dependent variable of Loan Risk Pre-

mium is measured by all-in-drawn spread added to LIBOR as reported in Loan

Pricing Corporation’s DealScan. The key test variable of syndicate structure is

S. C. Bae et al.

132 © 2014 Korean Securities Association

measured by two proxies: (i) the number of lead arrangers relative to the total

number of lenders, denoted as Number Concentration; and (ii) the loan amount

allocated to lead arrangers relative to the total loan amount, denoted as Amount

Concentration, both of which are manually collected from DealScan.5 It is worth

noting that Number Concentration has rarely been used as a measure of syndicate

structure in previous studies.6

We hypothesize that syndicate structure reflects the active commitments and

strategic interactions of all syndicate participants and test whether and how the syn-

dicate structure, the embracive representation of strategic interactions of all lenders

within a syndicate, affects the loan risk premium, the comprehensive device of

aligning risk-adjusted compensation to all parties in the syndicate, in the process of

designing loan contracts.7

Because the loan risk premium of a syndicated loan can be affected by factors

other than the syndicate structure, we employ several explanatory variables in the

loan risk premium regressions. Following the existing literature, we first include five

widely known debt-related factors of loan risk premium to control for the charac-

teristics of syndicated loan contracts: Maturity, Loan Size, Covenant, Collateral, and

Loan Purpose. Maturity is measured by the length of loan maturity in months. Loan

Size represents the size of loan facility in US dollars and enters the regressions as a

natural log form. Covenant is an indicator variable that equals 1 if a covenant is

required in a loan contract and 0 otherwise. Collateral is an indicator variable that

equals 1 if collateral is required in a loan contract and 0 otherwise. Loan Purpose

reveals important information on potential credit risk to lenders. We use four indi-

cator variables for the types of loan purpose; Corporate Purpose is equal to 1 if the

5In this paper, lead arrangers include agents, managers, arrangers, and co-agents in syndicated

loan contracts. See Ivashina (2009) for defining lead arrangers and participating banks from

DealScan.6Sufi (2007) uses various measures of syndicate structure such as total number of lenders,

total number of participating banks, the percentage of loan volume held by lead arrangers,

and the Herfindahl–Hirschman index. The use of total number of lenders as a measure of

syndicate structure may have some defects in that it cannot be fully independent from loan

and borrower characteristics such as loan size, loan purpose, and borrower riskiness. Hence,

the syndicate structure needs to be a measure standardized, for example, by the total number

of lenders and/or total loan amount, as in our paper. The use of the Herfindahl–Hirschman

index as a measure of syndicate structure in previous studies also poses some pitfalls mainly

because this index captures the loan volume of a pre-determined number of lead arrangers

(e.g. top three, four, etc.) and thus fails to consider the interactive determination of a syndi-

cate structure among lead arrangers and participating banks.7In investigating the effect of ownership structure on bank loan syndicate structure, Lin et al.

(2012) use various measures of syndicate structure such as amount kept by lead arrangers,

percentage of loan kept by lead arrangers, and the Herfindahl index of lenders’ share. Among

these, the percentage of loan kept by lead arrangers is similar to the measure of syndicate

structure, amount concentration, in our paper.

Syndicate Structure and Loan Pricing

© 2014 Korean Securities Association 133

purpose of the loan is corporate purpose and 0 otherwise; Debt Repayment is equal

to 1 if the purpose of the loan is debt repayment and 0 otherwise; Corporate Control

is equal to 1 if the purpose of the loan is corporate control and 0 otherwise; and

Project Finance is equal to 1 if the purpose of the loan is project finance and 0

otherwise.

We also employ four indicator variables of industry to control for the effect of

the borrower’s business sector on loan pricing; Manufacturing is equal to 1 if the

business sector is manufacturing and 0 otherwise; High-tech is equal to 1 if the

business sector is high-tech and 0 otherwise; Mining is equal to 1 if the business

sector is mining and 0 otherwise; and Services is equal to 1 if the business sector is

services and 0 otherwise.

Since international lending involves more aspects of risk such as macroeconomic

conditions and country characteristics in addition to the credit risk factors that

domestic lending faces, we take into account a wide range of determinants of the risk

premiums of international syndicated loans including potential cross-country differ-

ences in these characteristics. For this purpose, we include several variables repre-

senting macroeconomic conditions and the characteristics of borrowing firms’

countries: GDP Growth, Global Financial Crisis, OECD, foreign exchange rate volatil-

ity (FX Volatility), and a credit protection measure. GDP Growth is employed to

control for the aggregate demand for funds in the borrower’s country and measured

by the annual GDP growth rate of the borrower’s country. Global Financial Crisis is

included to control for the significant structural shift during the 2007–2008 global

financial crisis period and equal to 1 if a loan is offered during the crisis period and

0 otherwise. The global financial crisis period is from October 2007 to December

2008, and the non-crisis period is the remaining period.8 During the global financial

crisis of 2007–2008, global corporate debt markets were contracted substantially due

to the higher uncertainty of future economic growth, resulting in a higher risk aver-

sion and thus curtailing financing activities significantly for both lending institutions

and borrowing firms (Ivashina and Scharfstein, 2010). Santos (2011) also shows that

the bank-dependent borrowers were forced to pay a higher spread on loans issued

during the global financial crisis than during the pre-crisis period. OECD represents

a country’s membership to the Organization for Economic Cooperation and Devel-

opment (OECD) and is equal to 1 if a country belongs to the OECD and 0 other-

wise.9 FX Volatility is used to control for the volatility of a country’s exchange rate,

measured by the annual standard deviation of the daily exchange rate. Note that we

8Following De Haas and Van Horen (2010) and Godlewski (2010), we suppose that the glo-

bal financial crisis started in October 2007 rather than in August 2007 when the collapse of

the US subprime financial markets began. This choice for the start of the takes into account

an average of eight weeks’ time lag between starting loan negotiations and signing the deal.9The OECD was created for global development by 18 European countries and the USA and

Canada in 1960, and currently has 34 member countries, including many of the world’s most

advanced countries and emerging economies like Mexico, Chile, and Turkey.

S. C. Bae et al.

134 © 2014 Korean Securities Association

do not include the aggregate income level of each country, for example, GDP and

per capita GDP, as country characteristics because these variables are redundant in

the presence of GDP growth and the OECD indicator.

Previous studies show that the degree of country-level credit protection affects

credit decisions in international lending (La Porta et al., 1998; Djankov et al., 2007;

Qian and Strahan, 2007; Bae and Goyal, 2009). Godlewski (2007) further shows that

the degree of concentration in the syndicate structure of international corporate

lending depends largely on the strength of the law enforcement of the borrower’s

country. Following these studies, we use Country Credit Rating as a proxy variable

for a borrowing country’s credit protection measure, following Moody’s sovereign

ratings.

Putting all variables together, we estimate the following cross-sectional ordinary

least squares regression model to test two competing hypotheses of the concentra-

tion and diversification hypotheses:

Loan Risk Premiumi ¼ bþ b1Syndicate Structureþ b2Maturityi þ b3Loan Sizei

þ b4Covenanti þ b5Collaterali þ b6Loan Purposei þ b7Industryiþ b8GDP Growthi þ b9OECDi þ b10Global Financial Crisisiþ b11FX Volatilityi þ b12Country Credit Ratingi þ �i ð1Þ

where the key test variable is Syndicate Structure, which takes one of two proxy

variables, Number Concentration and Amount Concentration. The concentration

(diversification) hypothesis predicts a positive (negative) sign of the estimated

regression coefficient of Syndicate Structure. Loan Purpose is one of four indicator

variables of Corporate Purpose, Debt Repayment, Corporate Control, and Project

Finance. Industry is one of four indicator variables of Manufacturing, High-tech,

Mining, and Services. Table 1 presents brief definitions of variables employed in

the regression model.

It is worth noting that in estimating regression model (1), there may exist an

endogeneity problem between Loan Risk Premium and Syndicate Structure. Recog-

nizing the endogenous nature of such a regression, Ivashina (2009) attempts to

overcome this problem by using the instrumental variable approach, while Focarelli

et al. (2008) resolve a similar problem by employing a broad range of control vari-

ables which would have direct effects on the determination of the loan risk pre-

mium. Following Focarelli et al. (2008), we cope with this endogeneity problem by

employing control variables that cover a variety of factors affecting loan deals in

international syndicated lending.

3.2. Data and Sample Selection

We collect our sample of firm-level syndicated corporate loan contracts from

Thomson Reuters’ DealScan, a rich and unique database covering extensive interna-

tional syndicated loan contracts, during the period January 1982 to June 2012.

Syndicate Structure and Loan Pricing

© 2014 Korean Securities Association 135

We limit our sample to loan contracts offered by US banks in US dollars

because US banks cover the largest volume of syndicated loans primarily offered in

US dollars in international financial markets. In addition, by focusing on interna-

tional syndicated loans offered by US lenders, we attempt to investigate the behav-

ior of lenders with some uniform characteristics in offering loans to borrowing

firms in foreign countries. Although syndicated loans are sometimes priced by

prime rate and other benchmark interest rates than LIBOR, the majority of syndi-

cate deals are made in LIBOR as the base interest rate plus the risk premium to

reflect the riskiness of a borrower. Hence, we further limit our analysis to loan con-

tracts priced by LIBOR to maintain consistency across individual loan contracts.

We use the loan spread as the market price of syndicated corporate loans.

We collect from the DealScan database detailed characteristics of contract infor-

mation on corporate loan contacts such as benchmark reference interest rate, mar-

gin (spread), loan amount, debt maturity, loan purpose, security, and deal

Table 1 Definition of variables

Variables Definition

Dependent variable

Loan Risk Premium All-in-drawn spread added to LIBOR reported in DealScan

Test variable: Syndicate structure

Number Concentration Number of lead arrangers/Total number of lenders

Amount Concentration Shares of lead arrangers/Total loan amount

Control variables: Contract characteristics

Maturity Length of loan maturity in months

Loan Size Size of loan facility in US dollars (million)

Covenant 1 if covenant required in contract and 0 otherwise

Collateral 1 if collateral required in contract and 0 otherwise

Loan Purpose

Corporate Purpose 1 if loan purpose is corporate purpose and 0 otherwise

Debt Repayment 1 if loan purpose is debt repayment and 0 otherwise

Corporate Control 1 if loan purpose is corporate control and 0 otherwise

Project Finance 1 if loan purpose is project finance and 0 otherwise

Industry

Manufacturing 1 if business sector is manufacturing and 0 otherwise

High-tech 1 if business sector is high-tech and 0 otherwise

Mining 1 if business sector is mining and 0 otherwise

Services 1 if business sector is services and 0 otherwise

Control variables: Macroeconomic conditions and country characteristics

GDP Growth Annual GDP growth rate of borrower’s country

OECD 1 if borrower is in OECD country and 0 otherwise

Global Financial Crisis 1 if loan is offered during the crisis period and 0 otherwise

FX Volatility Annual standard deviation of daily exchange rate

Country Credit Rating Moody’s sovereign rating

S. C. Bae et al.

136 © 2014 Korean Securities Association

currency, along with borrower characteristics such as name, nationality, business

sector, and sales. We also obtain data for country and macroeconomic characteris-

tics from various sources including the World Development Indicators of the World

Bank, International Financial Statistics from the International Monetary Fund, and

the databases of the US Federal Reserve Bank.

Our final sample consists of 8257 syndicated loan contracts in 103 countries to

which at least one syndicate loan contract is offered by US banks over the sample

period. Table 2 reports the sample distributions of syndicated loan contracts across

103 countries. During our sample period, US banks made the largest number of

syndicated loans (1458) to borrowers in the UK, which represent about 17.7% of all

loans in the sample, followed by Canada (1028), France (639), Germany (555), and

the Netherlands (440).

4. Empirical Results

4.1. Descriptive Statistics

Table 3 reports descriptive statistics of several key variables for syndicated loan

deals across 103 countries in our sample. Note that the number of observations for

Amount Concentration is substantially smaller than that for Number Concentration

because a large number of syndicated loan contracts reported in the DealScan data-

base do not report the loan amount allocated to lenders in the syndicate. Also, the

number of observations for the variables varies due to missing data.

The average Number Concentration and Amount Concentration are 0.42 and

0.46, respectively. Hence, lead arrangers in syndicated loans offered to borrowers in

103 countries by US banks typically represent about 42% of total lenders and retain

about 46% of the total loan amount in the syndication. It is also shown that a typi-

cal syndicated loan in our sample carries a loan risk premium (all-in-drawn spread)

of 173.83 basis points or 1.7383% above LIBOR, has a maturity of 55.63 months,

and amounts to $698 million in size. A borrower’s country has on average an

annual GDP growth rate of 8% and a country credit rating of 18.53.10

4.2. Univariate Analysis

Panels A and B of Table 4 show the means and medians of loan risk premium clas-

sified by the levels of Number Concentration and Amount Concentration, respec-

tively, along with t- and z-statistics for the differences-in-means and medians tests.

With respect to the level of Number Concentration as reported in Panel A, borrow-

ing firms carry significantly higher loan risk premiums for syndicated loans with

low Number Concentration than for those with high Number Concentration (119.70

versus 104.90 bps). Similarly, with respect to the level of Amount Concentration as

reported in Panel B, higher loan risk premiums are associated with loans with low

Amount Concentration.

10The country credit rating of the borrower’s country ranges from 2 to 21 in our sample.

Syndicate Structure and Loan Pricing

© 2014 Korean Securities Association 137

Table 2 Distribution of sample syndicated loans by country

The sample includes syndicated loan contracts issued by US banks to borrowers in 103 countries during

1982–2012.

Country Frequent Percent Country Frequent Percent Country Freq. Percent

Andorra 2 0.02 Germany 555 6.72 Oman 9 0.11

Angola 2 0.02 Ghana 6 0.07 Other 5 0.06

Argentina 156 1.89 Greece 50 0.61 Panama 30 0.36

Australia 139 1.68 Guatemala 13 0.16 Paraguay 1 0.01

Austria 24 0.29 Honduras 4 0.05 Peru 33 0.40

Azerbaijan 9 0.11 Hong Kong 39 0.47 Philippines 4 0.05

Bahamas 15 0.18 Hungary 31 0.38 Poland 25 0.30

Bahrain 21 0.25 Iceland 15 0.18 Portugal 21 0.25

Bangladesh 2 0.02 India 43 0.52 Qatar 22 0.27

Barbados 7 0.08 Indonesia 12 0.15 Romania 14 0.17

Belgium 80 0.97 Ireland 98 1.19 Russia 197 2.39

Bermuda 212 2.57 Israel 14 0.17 Saudi

Arabia

26 0.31

Bolivia 3 0.04 Italy 167 2.02 Singapore 23 0.28

Brazil 238 2.88 Jamaica 4 0.05 Slovakia 10 0.12

British

Virgin

Islands

1 0.01 Japan 49 0.59 Slovenia 14 0.17

Bulgaria 1 0.01 Kazakhstan 50 0.61 South Africa 79 0.96

Cameroon 2 0.02 Korea (South) 30 0.36 Spain 231 2.80

Canada 1028 12.45 Kuwait 14 0.17 Sri Lanka 1 0.01

Cayman

Islands

18 0.22 Latvia 3 0.04 Sweden 109 1.32

Chile 134 1.62 Liberia 1 0.01 Switzerland 257 3.11

China 8 0.10 Lithuania 3 0.04 Taiwan 9 0.11

Colombia 58 0.70 Luxembourg 85 1.03 Tanzania 2 0.02

Congo 1 0.01 Macau 10 0.12 Thailand 1 0.01

Costa Rica 4 0.05 Malaysia 6 0.07 Trinidad

and

Tobago

8 0.10

Croatia 18 0.22 Malta 4 0.05 Tunisia 3 0.04

Cyprus 2 0.02 Mauritania 2 0.02 Turkey 282 3.42

Czech

Republic

17 0.21 Mexico 413 5.00 Ukraine 26 0.31

Denmark 62 0.75 Morocco 4 0.05 United

Arab

Emirates

38 0.46

Dominican

Republic

5 0.06 Netherlands 440 5.33 United

Kingdom

1458 17.66

S. C. Bae et al.

138 © 2014 Korean Securities Association

The results from the univariate analysis indicate that risk premiums on syndi-

cated loans are significantly negatively related to the levels of both measures of syn-

dicate structure, lending empirical support, though preliminary, for the

diversification hypothesis.

4.3. Correlation Analysis

Table 5 presents the Pearson correlation coefficients between key variables for the full

observations across all 103 countries. Among others, Loan Risk Premium (all-in-

drawn spread) is significantly (at the 1% level) negatively correlated with both mea-

sures of syndicate structure (Number Concentration and Amount Concentration), Loan

Size, OECD, and Country Credit Rating, but is significantly (at the 1% level) positively

correlated with contract characteristics such as Maturity, Covenant, and Collateral,

and macroeconomic conditions such as GDP Growth and Global Financial Crisis.

The negative and significant correlation coefficients between loan risk premium

and both measures of syndicate structure lend evidence in support of the diversifi-

cation hypothesis but are contradictory to the concentration hypothesis.

Table 2 (Continued)

Country Frequent Percent Country Frequent Percent Country Freq. Percent

Egypt 34 0.41 Netherlands

Antilles

3 0.04 Uruguay 9 0.11

El Salvador 6 0.07 New Zealand 6 0.07 Venezuela 26 0.31

Estonia 1 0.01 Nicaragua 2 0.02 Zimbabwe 2 0.02

Finland 74 0.90 Nigeria 1 0.01

France 639 7.74 Norway 82 0.99 Total 8257 100

Table 3 Descriptive statistics for full sample

The sample includes syndicated loan contracts issued by US banks to borrowers in 103 countries during

1982–2012. Number Concentration is the number of lead arrangers relative to the total number of lenders

in a syndicate. Amount Concentration is the shares of loan volume of lead arrangers relative to the loan

amount. Loan Risk Premium is all-in-drawn spread added to LIBOR reported in DealScan. GDP Growth

is measured by the annual growth rate of GDP. Country Credit Rating follows Moody’s sovereign ratings.

Variables Mean

Lower

quartile Median

Upper

quartile

No. of

observations

Number Concentration 0.42 0.14 0.36 0.67 8257

Amount Concentration 0.46 0.17 0.43 0.75 1398

Loan Risk Premium (bps) 173.83 50.00 140.00 250.00 8257

Maturity (months) 55.63 36.00 60.00 82.00 8257

Loan Size ($millions) 698.00 100.00 265.00 718.00 8257

GDP Growth 0.08 �0.23 0.00 0.27 7061

Country Credit Rating 18.53 19.00 21.00 21.00 6160

Syndicate Structure and Loan Pricing

© 2014 Korean Securities Association 139

4.4. Regression Estimates

Though preliminary, the results from the univariate analysis in Table 4 and the cor-

relation coefficient analysis in Table 5 highlight the negative and significant empiri-

cal relationship between syndicate structure and loan risk premium. We now

examine this relationship in a more rigorous regression analysis after controlling for

characteristics related to loan contracts and borrower’s countries.

Panels A and B of Table 6 present the regression estimates of Loan Risk Pre-

mium with Number Concentration and Amount Concentration as key test variables

of syndicate structure, respectively. Note that the number of observations in the

estimations with Amount Concentration in Panel B is substantially smaller than

that with Number Concentration in Panel A because many loan contracts in the

DealScan database do not report the loan amount allocated to lenders in the syn-

dicate.

Looking first at the variables representing loan contract characteristics, regres-

sion estimates of these variables in general carry the expected signs. As reported in

Panels A and B, Loan Risk Premium of a typical syndicated loan is significantly (at

least at the 5% level) positively related to Debt Maturity, Covenant, and Collateral,

and significantly (at the 1% level) negatively related to Loan Size, regardless of the

syndicate structure variable employed. Hence, the risk premium of a syndicated

loan increases with longer maturity and the existence of covenant and/or collateral,

while the loan risk premium declines with bigger loan size.

Table 4 Univariate analysis

The sample includes syndicated loan contracts issued by US banks to borrowers in 103 countries during

1982–2012. Number Concentration is the number of lead arrangers relative to the total number of lenders

in a syndicate. Amount Concentration is the shares of loan volume of lead arrangers relative to the loan

amount. Loan Risk Premium is all-in-drawn spread added to LIBOR reported in DealScan. GDP Growth

is measured by the annual growth rate of GDP. Country Credit Rating follows Moody’s sovereign ratings.

t- and z-statistics are for testing for differences in means and medians, respectively. ***, **, and * indi-

cate significance at the 1%, 5%, and 10% levels, respectively.

High NC Low NC

Mean (Median) Mean (Median) t-statistics z-statistics

Panel A: Based on Number Concentration (NC)

Number Concentration 0.686 (0.666) 0.162 (0.143) 150.00*** 78.74***

Loan Risk Premium 168.480 (125.000) 179.181 (150.000) 5.89*** 5.47***

No. of observations 4126 4131

Panel B: Based on Amount Concentration (AC)

Amount Concentration 0.742 (0.750) 0.183 (0.175) 66.94*** 32.38***

Loan Risk Premium 114.582 (70.000) 129.940 (87.500) 3.82*** 3.92***

No. of observations 699 699

S. C. Bae et al.

140 © 2014 Korean Securities Association

Table

5Correlationanalysisforkeyvariables

Thesampleincludes

syndicated

loan

contracts

issued

byUSbanks

toborrowersin

103countriesduring1982–2012.

SeeTable

1fordefinitionsofvariables.

***,**,and*indicatesignificance

atthe1%

,5%

,and10%

levels,respectively.

Variable

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

(11)

(12)

(1)All-in-drawn

Spread

1.000

(2)Number

Concentration

�0.046***

1.000

(3)Amount

Concentration

�0.111***

0.916***

1.000

(4)Maturity

0.250***

0.118***

0.084***

1.000

(5)LoanSize

�0.434***

0.078***

0.064***

�0.054***

1.000

(6)Covenant

0.063***

�0.116***

�0.167***

0.030***

0.018*

1.000

(7)Collateral

0.370***

0.038***

�0.033

0.181***

�0.122***

0.184***

1.000

(8)GDPGrowth

0.119***

0.055***

0.099***

0.042***

0.064***

�0.025**

0.151***

1.000

(9)OECD

�0.072***

�0.021**

0.035

0.120***

0.159***

�0.021**

0.012

�0.008

1.000

(10)

Country

Credit

Rating

�0.042***

�0.039***

�0.016

0.192***

0.233***

0.076***

0.093***

0.040***

�0.197***

1.000

(11)

Global

Financial

Crisis

0.034***

�0.000

�0.023

0.007

0.060***

0.021**

0.074***

0.291***

�0.010

0.065***

1.000

(12)

FXVolatility

�0.013

�0.018*

�0.022

�0.192***

�0.054***

�0.058***

0.001

0.040***

0.095***

�0.444***

0.047***

1.000

Syndicate Structure and Loan Pricing

© 2014 Korean Securities Association 141

Table

6Regressionestimates

ofloan

risk

premium

Thesample

includes

syndicated

loan

contracts

offered

byUSbanks

toforeignborrowingfirm

sin

103countriesduring1982–2012.

SeeTable

1forthedefinitionsof

variables.t-values

inparentheses

arecomputedusingrobust

standarderrors

forfirm

clusters.**

*,**,and*indicatesignificance

atthe1%

,5%

,and10%

levels,respec-

tively.

Variables

Dependentvariable:All-in-drawnspread

added

toLIBOR

Model

(1)

Model

(2)

Model

(3)

Model

(4)

Model

(5)

Model

(6)

Panel

A:Regressionestimates

ofLoanRiskPremium

withNumberConcentration

NumberConcentration

�0.105**

�0.127**

�0.177***

�0.179***

�0.144***

�0.147***

(�2.13)

(�2.47)

(�3.38)

(�3.38)

(�2.74)

(�2.79)

Maturity

0.230***

0.186***

0.197***

0.224***

0.186***

0.196***

(11.85)

(7.92)

(8.50)

(9.17)

(7.94)

(8.04)

LoanSize

�0.278***

�0.260***

�0.245***

�0.233***

�0.261***

�0.257***

(�23.92)

(�20.21)

(�19.31)

(�18.09)

(�20.27)

(�19.91)

Covenant

0.020

0.116**

0.128**

0.150***

0.127**

0.129**

(0.39)

(2.16)

(2.36)

(2.79)

(2.39)

(2.40)

Collateral

0.668***

0.503***

0.523***

0.521***

0.504***

0.507***

(20.69)

(13.99)

(14.21)

(13.91)

(14.04)

(13.98)

Corporate

Purpose

�0.251***

�0.257***

�0.265***

�0.249***

�0.242***

(�5.80)

(�5.84)

(�5.83)

(�5.74)

(�5.52)

DebtRepay

�0.354***

�0.365***

�0.363***

�0.355***

� 0.354***

(�7.47)

(�7.76)

(�7.61)

(�7.55)

(�7.49)

Corporate

Control

0.366***

0.386***

0.411***

0.365***

0.376***

(8.39)

(8.71)

(9.05)

(8.41)

(8.62)

Project

Finance

�0.018

�0.086

�0.110

�0.018

�0.008

(�0.23)

(�1.09)

(�1.44)

(�0.24)

(�0.10)

S. C. Bae et al.

142 © 2014 Korean Securities Association

Table

6(C

ontinued)

Variables

Dependentvariable:All-in-drawnspread

added

toLIBOR

Model

(1)

Model

(2)

Model

(3)

Model

(4)

Model

(5)

Model

(6)

Manufacturing

0.028

0.041

0.046

0.027

0.029

(0.64)

(0.94)

(1.03)

(0.62)

(0.66)

High-tech

�0.048

�0.035

�0.008

�0.058

�0.051

(�0.63)

(�0.46)

(�0.11)

(�0.77)

(�0.68)

Mining

�0.041

�0.054

�0.036

�0.042

�0.035

(�0.65)

(�0.85)

(�0.56)

(�0.68)

(�0.56)

Services

0.109**

0.150***

0.181***

0.116**

0.124**

(2.07)

(2.80)

(3.38)

(2.18)

(2.33)

GDPGrowth

0.177***

0.157***

0.164***

0.175***

0.167***

(5.49)

(4.88)

(5.02)

(5.30)

(5.15)

OECD

Dummy

�0.377***

(�6.58)

CountryCreditRating

�0.029***

(�6.55)

GlobalCrisisDummy

0.015

(0.27)

FXVolatility

0.000*

(1.89)

Constant

5.275***

5.473***

5.625***

5.635***

5.414***

5.342***

(54.29)

(46.22)

(47.80)

(43.72)

(47.67)

(44.89)

Observations

8257

6160

6160

6108

6160

6121

R-square

0.314

0.400

0.411

0.414

0.399

0.402

F-value

334.45***

144.73***

139.01***

137.92***

135.28***

136.03***

Syndicate Structure and Loan Pricing

© 2014 Korean Securities Association 143

Table

6(C

ontinued)

Variables

Dependentvariable:All-in-drawnspread

added

toLIBOR

Model

(1)

Model

(2)

Model

(3)

Model

(4)

Model

(5)

Model

(6)

Panel

B:Regressionestimates

ofLoanRiskPremium

withAmountConcentration

AmountConcentration

�0.217*

�0.150

�0.210*

�0.215*

�0.185

�0.204*

(�1.96)

(�1.38)

(�1.84)

(�1.88)

(�1.64)

(�1.79)

Maturity

0.111***

0.064

0.074

0.090*

0.069

0.092*

(2.76)

(1.34)

(1.52)

(1.75)

(1.41)

(1.82)

LoanSize

�0.215***

�0.218***

�0.216***

�0.211***

�0.224***

�0.214***

(�8.98)

(�8.28)

(�8.02)

(�7.82)

(�8.71)

(�8.04)

Covenant

0.127

0.250***

0.278***

0.302***

0.267***

0.283***

(1.52)

(2.69)

(2.97)

(3.20)

(2.90)

(2.96)

Collateral

0.717***

0.612***

0.609***

0.584***

0.600***

0.597***

(9.02)

(6.82)

(6.72)

(6.19)

(6.78)

(6.59)

Corporate

Purpose

�0.246***

�0.250***

�0.267***

�0.248***

�0.245***

(�2.75)

(�2.79)

(�2.95)

(�2.82)

(�2.73)

DebtRepayment

�0.301***

�0.303***

�0.321***

�0.290***

�0.306***

(�3.45)

(�3.51)

(�3.64)

(�3.37)

(�3.53)

Corporate

Control

0.392***

0.388***

0.382***

0.398***

0.399***

(3.08)

(3.11)

(2.93)

(3.22)

(3.21)

Project

Finance

0.121

0.116

0.094

0.095

0.119

(0.56)

(0.53)

(0.43)

(0.42)

(0.55)

Manufacturing

�0.007

�0.015

0.006

�0.002

�0.023

(�0.09)

(�0.17)

(0.07)

(�0.02)

(�0.27)

S. C. Bae et al.

144 © 2014 Korean Securities Association

Table

6(C

ontinued)

Variables

Dependentvariable:All-in-drawnspread

added

toLIBOR

Model

(1)

Model

(2)

Model

(3)

Model

(4)

Model

(5)

Model

(6)

High-tech

�0.045

�0.067

�0.032

�0.091

�0.065

(�0.30)

(�0.45)

(�0.21)

(�0.65)

(�0.44)

Mining

�0.024

�0.038

�0.008

�0.035

�0.002

(�0.18)

(�0.27)

(�0.06)

(�0.26)

(�0.02)

Services

�0.042

�0.027

0.002

�0.026

�0.026

(�0.29)

(�0.18)

(0.01)

(�0.17)

(�0.18)

GDPGrowth

0.072

0.063

0.078

0.035

0.063

(1.04)

(0.86)

(1.10)

(0.47)

(0.88)

OECD

Dummy

�0.072

(�0.62)

CountryCreditRating

�0.013*

(�1.66)

GlobalCrisisDummy

0.334***

(2.75)

FXVolatility

0.000***

(2.60)

Constant

5.141***

5.574***

5.462***

5.536***

5.432***

5.298***

(25.67)

(24.15)

(22.41)

(22.24)

(23.29)

(20.85)

Observations

1398

1044

1044

1010

1044

1036

R-square

0.266

0.334

0.331

0.341

0.336

0.332

F-value

65.30***

27.41***

26.02***

24.83***

25.74***

25.20***

Syndicate Structure and Loan Pricing

© 2014 Korean Securities Association 145

The positive effect of debt maturity on loan risk premium reflects the added

maturity risk premium for longer-term maturity loans. This finding is also in accor-

dance with Eichengreen and Moody (2003) and Flannery (1986) who indicate that

lenders’ monitoring efforts increase as the loan maturity lengthens. A longer matu-

rity loan is penalized with a higher risk premium charged by lenders because a bor-

rower is given longer to exercise moral hazard behaviors ex post the loan contract.

In a similar argument, a short-term debt is viewed as an effective tool to discipline

risky borrowers by forcing them to expose to refunding risk in a way that a risky

borrower may not be able to rollover the short-term debt as their short-term debt

expires more frequently than longer-term debt. Owing to the frequent requests for

renewal, short-term loans provide fewer opportunities to the agent bank to shirk on

monitoring (Dennis and Mullineaux, 2000). Frequent renewals of short-term debt

also require more monitoring by external screeners like credit rating agencies and

financial market participants upon new debt issuance (Guedes and Opler, 1996).

The positive regression coefficients of Loan Maturity in Panels A and B of Table 5

confirm the above argument.

The negative and significant relationship between loan size and loan risk pre-

mium is consistent with the findings in Altunbas and Gadanecz (2003), Eichengreen

and Moody (2003), and Kleimeier and Megginson (2000). The positive and signifi-

cant effect of Collateral (security-indicator) on loan risk premium is in line with Al-

tunbas and Gadanecz (2003), Berger and Udell (1990), Berger et al. (2011), and

Nini (2004). In particular, Berger and Udell (1990) find that the most risky borrow-

ers are required to pledge collateral.11

Regarding loan purpose, an important factor that lenders assess for potential

credit risk, Table 6 shows that while Corporate Purpose and Debt Repay are both sig-

nificantly (at the 1% level) negatively related to loan risk premium, Corporate Con-

trol is significantly (at the 1% level) positively related to loan risk premium. Hence,

syndicated loans for the purpose of corporate control, involving activities such as

LBOs and M&As, are associated with higher risk premiums compared to loans for

other loan purposes. These findings are in line with those in Altunbas and Gadan-

ecz (2003). It is also shown that borrowing firms belonging to the services industry

are associated with relatively high-risk premiums.

Examining the regression estimates of the variables representing country-related

characteristics, the loan risk premium is significantly positively related to GDP

Growth, Global Financial Crisis Dummy (only in Panel B), and FX Volatility, but is

significantly negatively related to OECD Dummy and Country Credit Rating.12 Thus,

borrowing firms in OECD countries and/or countries with a higher credit rating

enjoy lower debt costs, whereas borrowers in countries with a higher GDP growth

11In contrast, Besanko and Thakor (1987) argue that when borrowers have informational

advantages about their default probabilities, the least risky borrowers pledge collateral.12Owing to the high correlations among country-related variables as shown in Table 5, these

variables enter the regression models separately.

S. C. Bae et al.

146 © 2014 Korean Securities Association

(most likely non-OECD countries) and/or higher foreign exchange risk, bear higher

loan risk premiums. It is also shown that borrowing firms bear higher spreads in

international syndicated loan markets during the global financial crisis period than

during other periods.

Turning to the regression estimates of our key test variables of syndicate struc-

ture, Number Concentration, measured by the proportional number of lead arrang-

ers in a syndicate, carries a negative and significant (at the 1% level) regression

coefficient in all six regression models in Panel A. Similarly, though slightly weak,

Amount Concentration, measured by the proportional shares of loans of lead arrang-

ers, has a negative and significant (at the 10% level) regression coefficient in four of

six regression models in Panel B. Accordingly, both the relative number of lead

arrangers and the portion of a syndicate loan retained by lead arrangers have signif-

icant and negative effects on loan risk premium.

Combined, the regression results in Panels A and B of Table 6 provide strong evi-

dence supporting the diversification hypothesis that a diversified syndicate structure

is associated with a higher loan risk premium demanded by participating banks to

compensate for the severity of information asymmetry and the lack of the lead

arrangers’ commitment on a loan contract. Our regression results support the under-

lying premise of the diversification hypothesis that both lead arrangers and partici-

pating banks possess information through which they can assess the riskiness of the

borrowing firm as accurately as possible. Hence, as the riskiness of a borrowing firm

increases, the syndication structure becomes more diversified and diffused in a way

that lead arrangers and participating banks share the loan amounts and the associ-

ated credit risk in syndication, while at the same time the lead arrangers offer higher

risk premiums to the participating banks to seek their syndicate participation.

4.5. Robustness Tests

In order to ensure the robustness of our empirical results regarding tests of the two

hypotheses, we conduct additional tests. A limitation of the regression model (equa-

tion (1)) employed to test our two hypotheses is the lack of variables controlling

for borrowing firms’ financial characteristics, which may also affect the risk pre-

mium of a syndicated loan. As a way to estimate a regression model with a more

complete set of control variables that include borrowers’ financial information, we

first match borrowing firms in our original sample (collected from DealScan) with

firms in the Worldscope database during our sample period. We then collect the

financial information of the matched borrowing firms from the Worldscope database

including total assets as a measure of firm size, debt ratio as a measure of financial

leverage, return on assets (ROA) as a measure of profitability, and the ratio of fixed

assets to total assets as a measure of tangibility to construct a new set of sample

firms.13 This process significantly reduces the maximum number of observations to

13We employ each borrowing firm’s tangibility to control for its financing demand of large-

scale fixed assets, which in general require large funding (Almeida and Campello, 2007).

Syndicate Structure and Loan Pricing

© 2014 Korean Securities Association 147

1472 syndicated loans for the regression models with Number Concentration and

333 loans for those with Amount Concentration.

Panels A and B of Table 7 show the summary statistics and Pearson correlation

coefficients, respectively, of key variables including the four financial variables of

borrowing firms in the reduced sample. As shown in Panel A, a borrowing firm on

average has total assets of US$1040 million, a total debt to total assets ratio of 32%,

an ROA of 11%, and a tangibility ratio of 35%. It is further shown in Panel B that

loan risk premium is significantly positively correlated with Leverage and Tangibility

but is significantly negatively correlated with Firm Size and ROA. Hence, higher

loan spreads are in general associated with smaller, more leveraged, more tangible,

Table 7 Descriptive statistics for DealScan data merged with Worldscope data

The sample includes syndicated loan contracts offered by US banks to foreign borrowing firms whose

data are initially collected from DealScan and then matched with firms in the Worldscope database during

1982–2012. See Table 1 for definitions of variables. ***, **, and * indicate significance at the 1%, 5%,

and 10% levels, respectively.

Panel A: Summary statistics of key variables

Variables Mean

Lower

quartile Median

Higher

quartile

Number Concentration 0.38 0.13 0.30 0.63

Amount Concentration 0.48 0.17 0.50 0.79

All-in-drawn Spread (bps) 79.66 0.00 35.00 115.00

Maturity (months) 44.78 12.00 45.00 60.00

Loan Size ($millions) 910.05 136.16 365.78 1000.00

Firm Size ($millions)) 1040.00 28.97 890.91 5157.97

Leverage 0.32 0.21 0.31 0.42

ROA 0.11 0.07 0.11 0.15

Tangibility 0.35 0.12 0.32 0.54

GDP Growth 0.11 �0.19 0.00 0.30

Country Credit Rating 17.71 14.00 21.00 21.00

Panel B: Correlation coefficients of key variables

Variables (1) (2) (3) (4) (5) (6) (7)

(1) All-in-drawn Spread 1.00

(2) Number

Concentration

�0.18*** 1.00

(3) Amount

Concentration

�0.19*** 0.91*** 1.00

(4) Firm Size �0.34*** 0.06*** 0.04 1.00

(5) Leverage 0.26*** �0.01 0.05 �0.04** 1.00

(6) ROA �0.17*** 0.13*** 0.09* �0.07*** �0.06*** 1.00

(7) Tangibility 0.07*** �0.11*** �0.08* �0.08*** 0.19*** 0.28*** 1.00

S. C. Bae et al.

148 © 2014 Korean Securities Association

and less profitable borrowing firms. Most importantly, both Number Concentration

and Amount Concentration are significantly negatively correlated with loan risk pre-

mium, evidence in line with our earlier findings for the original full sample

reported in Table 4 and in support of the diversification hypothesis.

For the regression analysis, we estimate regression equation (1) by adding the

four financial variables as additional control variables and report the regression

results in Table 8. As in Table 6, Panels A and B report the regression estimates

with Number Concentration and Amount Concentration, respectively, as key test vari-

ables of syndicate structure. While the regression coefficients of a few control vari-

ables such as Maturity, Services, and FX Volatility lose their significance mainly due

to the reduced number of observations, the overall regression results for the control

variables representing the characteristics of loan contracts, loan purpose, industry,

and country are in general similar to those for the original full sample in terms of

signs and significance levels. Hence, we briefly discuss the regression estimates of

the four financial variables before reviewing the regression estimates of the two key

variables of syndicate structure.

Consistent with the correlation coefficients between financial variables and loan

spread as reported in Table 7, Firm Size and ROA carry negative and significant (at

the 1% level) regression coefficients in all six regression models, while Leverage has

positive and significant (at the 1% level) regression estimates in all six regression

models. Hence, these results offer evidence that borrowing firms’ financial charac-

teristics also play important roles in the determination of their loan spreads. The

negative relation of Firm Size with loan risk premium is mainly driven by the nega-

tive effect of firm size on the firm’s default risk (Dichev, 1998). In addition, firm

size is related to information asymmetry, and a larger firm is in general associated

with less adverse selection and moral hazard problems with lenders.

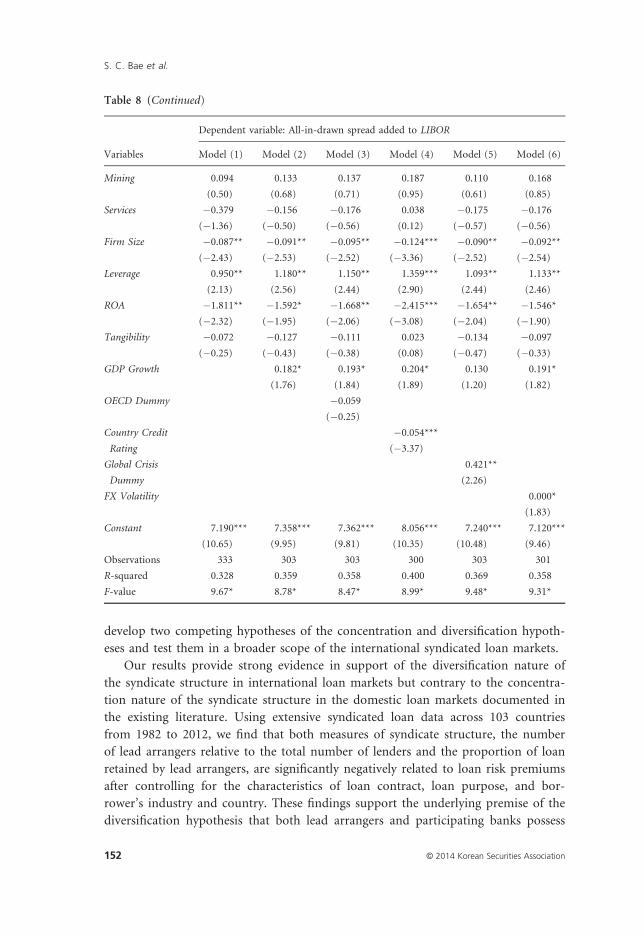

In robustness tests, the control variables of borrowing firms’ financial character-

istics are in general estimated as expected. Most importantly, the regression esti-

mates of Number Concentration are all negative and significant at the 1% level in all

six regression models in Panel A of Table 8. Similarly, the regression coefficients of

Amount Concentration are all negative and significant in two regression models in

Panel B, where several variables including Amount Concentration lose their signifi-

cance due to a substantially smaller number of observations (slightly more than

300). Though weaker than our earlier findings, the results in Table 8 provide con-

firmatory evidence that a more diversified (or a less concentrated) syndicate struc-

ture accompanies a higher loan spread, lending empirical support for the

diversification hypothesis.

5. Summary and Conclusions

We examine how lead arrangers and participating banks determine the syndicate