information nation crossing borders - new york...

TRANSCRIPT

Creative Thinking:Entrepreneurship in the Digital Age

STERNbusinessInformation Nation

S P R I N G / S U M M E R 2 0 0 3

Crossing Borders

CEO Interviews: How UPS Delivers How Bic Stays on the BallNiall Ferguson on Anglobalization India’s Software GiantWhy Major Economies Don't Move in Sync UnderstandingNew Consumer Markets Wal-Mart ’s Foreign TravelsR x C o v e r a g e : C u r i n g Te l e c o m a n d A r g e n t i n a

a l e t t e r f r o m t h e deanIt’s more than fit-

ting that this issue

focuses on the topic

of globalization and

crossing borders. In

recent months, Stern

has seen significant

milestones in our

international efforts. This past January the inaugu-

ral, 28-person class of executive MBA students from

TRIUM, the program Stern offers jointly with the

London School of Economics and the HEC School of

Management in Paris, completed their studies. The

second TRIUM class, with 35 members, completed

its first module at our campus in New York that

same month. This innovative program, geared

toward inculcating a global perspective in its stu-

dents, will continue throughout the year with

sessions in Paris, London, Brazil, and Hong Kong.

While many of our alumni remain in the New

York area, and hence can easily maintain connec-

tions to Stern, and with one another, Stern graduates

who live in 98 countries have fewer opportunities to

do so. In October, we held our second international

alumni conference at La Pietra, NYU’s conference

center in Florence, Italy.

At La Pietra, where nearly 160 people gathered

for a weekend of fine food, fine art, and fine discus-

sion, Stern’s approach toward business – and busi-

ness education – was on full display. Panels brought

together executives and scholars to discuss topics

ranging from corporate governance to the direction

of the global economy. A session on the business of

opera included the administrators of New York’s

Metropolitan Opera, Munich’s Bayerische Staatsoper,

and Milan’s La Scala.

Meeting in the heart of Europe, and with people

from different business cultures and scholarly

disciplines, added a great deal of context to all our

discussions. Of course, history is an important com-

ponent of context. Business history – long a strength

at Stern – has been augmented by the arrival in

January of Professor Niall Ferguson, who recently

joined us from Oxford University and is the author

of the definitive two-volume history of the

Rothschild banking empire. His most recent book,

Empire – which is partially excerpted in this issue –

is a significant contribution to the growing literature

on globalization.

As several articles in this issue argue,

understanding the historical development of

international markets, companies, and financial

systems is crucial for leaders grappling with

contemporary questions and challenges. After

all, locating our place and role in an increasingly

connected world is the fundamental task of all edu-

cational endeavors, but in particular of business

and management education.

We look back on recent accomplishments with

pride and a sense that we are affording all members

of the Stern community a greater understanding of

the world in which we live and work. And we look

forward eagerly to the future – and to this issue of

STERNbusiness.

Thomas F. CooleyDean

STERNbusinessA publication of the Stern School of Business, New York University

President, New York University � John E. SextonDean, Stern School of Business � Thomas F. CooleyChairman, Board of Overseers � William R. BerkleyChairman Emeritus, Board of Overseers � Henry KaufmanAssociate Dean, Marketing

and External Relations � Joanne HvalaEditor, STERNbusiness � Daniel GrossProject Manager � Rika NazemDesign � Esposite Graphics

Letters to the Editor may be sent to:NYU Stern School of BusinessOffice of Public Affairs44 West Fourth Street, Suite 10-83New York, NY 10012http://www.stern.nyu.edu

contents S P R I N G / S U M M E R 2 0 0 3 C r o s s i n g B o r d e r s

Illustrations byChris McAllister,Timothy Cook,Warren Gebert Gordon Studer,Robert O’Hair, and Michael Caswell

10A Passage From Indiaby Raghu Garud,Arun Kumaraswamy andMonica Malhotra

18The Market Next Doorby Peter Golder andDebanjan Mitra

24Anglobalizationby Niall Ferguson

30Don’t Cry For ArgentinaA Roundtable Discussion

34The Big Store GoesGlobalby David Liang

40It’s A Small WorldAfter All?by Jonathan Heathcote and Fabrizio Perri

44Telecommunications:Excess Capacityby Lawrence J. White

48 Endpaperby Daniel Gross

SternChiefExecutiveSeries

Interviews withBruno Bich, page 2Michael Eskew, page 4

8Crossing Bordersby Daniel Gross

ML: You certainly are thequintessential multi-national,multi-lingual executive. Tell uswhat's going on in the globaleconomy. Is it really as difficult,demanding, and daunting as itappears?BB: We are slightly affectedby the downturn in the econo-my. There are good reasons tobe careful right now. We creat-ed a bubble and we are payingthe price. There was a bubblein Asia, which corrected a cou-ple of years ago, and now istrying to recover. In Europe,there was an Internet bubble,but to a lesser extent than inthe U.S. It's just like a pendu-lum. We went too far one way,we go too far the other way.Short term, I'm concerned.Long term, I'm very optimistic.

In three years or so, businesswill come back to its normalpace.

ML: Do any of your majorproducts face specific chal-lenges now? For example,lighters. We see what's hap-pened with cigarette smokingin this country, and notably inthis city, and presumably thatwill spread. Or your White Outbusiness, when more andmore people are using com-puters?BB: Smoking is going downone to two percent per year inthe U.S. or world. That's a verysmall decline. In fact, we haveincreased our sales of lightersabout four percent a year overthe last five years. We keep ongaining market share despite

the tough market. Computershave not really done much toour White Out business. Thatmarket also grows two, threepercent a year. Our highlighterbusiness has actuallyincreased quite a bit. Peopleare highlighting a lot of com-puter reports.

ML: Shavers must be a chal-lenging market, especially witha goliath of a competitor likeGillette. How do you make thatbusiness grow?BB: Our company was startedright after World War II by myfather. In the U.S., we went inthe shaver business againstGillette. Gillette was strong inwhat I call the system andreplaceable blade. To gothrough the door and attack

that market head on wouldhave been extremely difficult.Instead, we went into the one-piece or disposable razor. Wewent through the side door.And today, if you look at thewestern world, 55 to 60 per-cent of the people shave witha disposable razor. There aremore people shaving with thedisposable razor than with thesystem razor. Now, the systemis bigger in value. But, in vol-ume, we are about equal withGillette, in the U.S. and inEurope.

ML: What is your strategy forexpanding in terms of new anddifferent products?BB: First of all, the consumergoes to the store, and has achoice. Consumers usually

Bruno Bich is the Chairman and CEO of Société Bich, a leadingmanufacturer of stationery products, lighters, and shavers thatwas founded by his father, Marcel Bich, in 1945. Based in Paris,France, Bich has subsidiaries in several different countries andsells products in more than 160 countries. The company’s U.S.subsidiary, Bic Corporation, based in Milford, CT, accounted forabout 53 percent of Bich’s 1.53 billion in 2001 sales. Bic man-ufactures three million ball point pens, 2.5 million shavers, and 1million lighters each day. Mr. Bich graduated from NYU Sternwith a Bachelor’s Degree in Marketing, and has worked atSociété Bich for more than three decades. After holding posi-tions including national sales manager, vice president of salesand marketing, and Chairman and CEO of Bic Corp., Mr. Bichwas elected to succeed Marcel Bich as Chairman and CEO ofSociété Bich in 1993.

sternChiefExecutiveseries

Bruno Bichchairman and chief executive officer

Société Bich

2 Sternbusiness

spend about 20 secondsdeciding which product to buy.The quality of the brand namein the subconscious of the con-sumer becomes very impor-tant, as does his recollection ofhow well he was served by theproduct in the past. That isreally where we concentrateour strategy.

The second thing is, wedevelop products with newtechnologies that offer differentservices to the consumer inrelation to their purchasingpower. Thirty years ago, youhad a ball point pen and youhad a mechanical pencil. Thencame the first felt products, thefirst flair pens. Instead of fourcolors, now there are 12 colorsof ink. And the point size,which dictates the width of aline of color on a piece ofpaper. There used to be only0.7 millimeter and 1 millimeter.Now we have 1.2, 1.0, 0.7,0.5, and even 0.3 in Japan. Soall those technologies offerchoices to consumers, whichthey like to indulge.

Then there are differenttypes of markets. In bothdeveloped markets and emerg-ing markets, but particularly inthe developed markets, youhave the need market and thepleasure market. People wanta basic ball pen that writeswell. On the other hand, peo-ple--particularly young people--want to find a little bit of pleas-ure in their everyday life. Andthat's where they really look atthe design of the product, andnew technologies with differentink colors. At the same time,

we can never forget that intoday’s world, approximately20 percent of the people earnless than $2 a day. So ourstrategy is serve the con-sumer, never forget the basicproduct, and work on the quali-ty all the time. If people wantto spend a bit more money,and they have the money incertain countries of the world,then we'll present a widerchoice, with newer technology.

ML: Where are you going tomake your major thrust forexpansion?BB: My father started the busi-ness in France. But France,today, represents only ninepercent of our sales. Overall,Europe is about 34 percent,North America about 56 per-cent, South America eight per-cent. We have the most oppor-tunity in Asia. We started doingbusiness two years ago inAsia, but building a businessthere will take 10 or 20 years. Ithink that in the 1970s, youcould not call yourself an inter-national company if you werenot strong in the United States.I think in 10 or 20 years youwill not call yourself a strongglobal company if you are notstrong in Asia.

ML: You have a managementteam that is stationed all overthe world. How do you managethat?BB: Well, I have two offices--one in Paris and one in NewYork. And I commute. I'm inNew York 50 percent of mytime, Europe 30 percent of the

time, and somewhere else 20percent of the time. We haveput together a group of man-agers who come from differentbackgrounds and different civi-lizations, because there is a lotof value to finding what are thecommon points between con-sumers in Europe and theUnited States, South Americaand Europe, and even Asia. Ithink too often, people start totalk about the differences.First, let's talk about the com-mon points. Ethics. Teamwork.Internationalism. When youlook at consumers, they writethe same way, they shave thesame way. We use English asour language of business,which is pretty advanced for aFrench company. Once amonth, we video-conferencewith top managers around theworld. We get together face toface every three months.

If there's one weakness inthe United States, it is thatAmerican companies callthemselves international whenin fact, there are very fewexecutives at American compa-nies who are multi-lingual andvery few people who comefrom foreign backgrounds.

ML: What are some of the dif-ferences between Americanmanagers and non-Americanmanagers?BB: The main difference isthat the American managersare very results oriented. Andthe French, who are moreintellectuals, love to discussand do more research. I thinkEuropeans are extremelyinventive in terms of technolo-gy. And when you put themtogether with Americans, whoare very good at process, youhave stupendous machinery.The idea is to use the strength

of each toward the same goal,versus focusing on the differ-ences. That's arduous work.But the payoff is great.

ML: You have some of theworld's best known brands.How do you develop a brand,and how important is that toyou?BB: Our brand name is myfamily name so I look at it as asignature. I think that a brandstands for an agreement or acontract, your signature to theconsumer that what you deliv-er to him is what he expects.You can build a brand, withadvertising, with a very goodproduct, and with consistentquality in your product. But youcan lose it very, very quickly. Idon't think that any brand inthe world can be number oneor number two by offering infe-rior quality. The strength of abrand is in the long-term faithof the consumer around theworld. The important ingredi-ents are quality, reliability, andvalue. After that, you're goingto add the pride of having theproduct. And this is whereadvertising comes in. Forexample, we used JohnMcEnroe in our shaver adver-tising. That campaign showedthe consumer that Bic has asimpatico side to it. When itcomes to the advertising or thedesign of the product, I per-sonally spend a lot of time onit, because it affects the longterm strength of the company.Our managers know exactlyhow to manage things like pric-ing. But they are not responsi-ble for the soul of the compa-ny, which is the brand name,or the design of the product.

ML: When you seek to hire

Marshall Loeb, the former managing editor of Moneyand Fortune, conducts a regular series of conversationswith today’s leading chief executives on the Stern campus.

"We can never forget that in today’sworld, approximately 20 percent of thepeople earn less than $2 a day."

continued, page 6

Sternbusiness 3

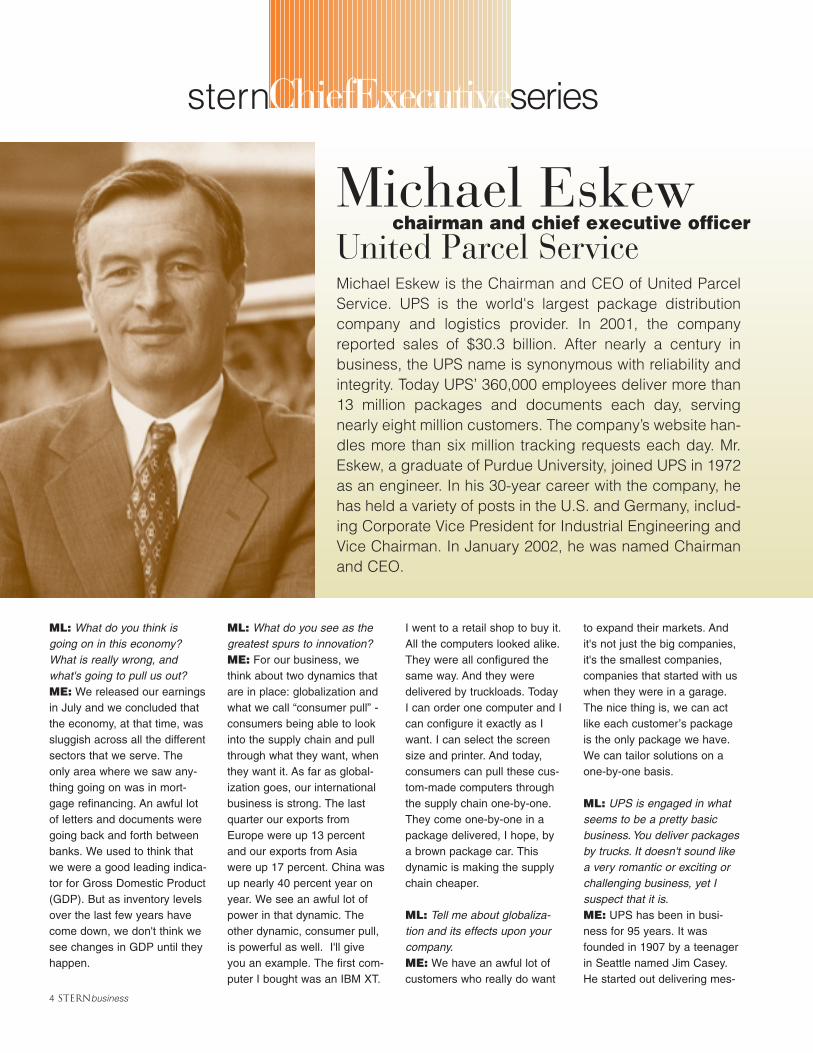

Michael Eskew is the Chairman and CEO of United ParcelService. UPS is the world's largest package distributioncompany and logistics provider. In 2001, the companyreported sales of $30.3 billion. After nearly a century inbusiness, the UPS name is synonymous with reliability andintegrity. Today UPS’ 360,000 employees deliver more than13 million packages and documents each day, servingnearly eight million customers. The company’s website han-dles more than six million tracking requests each day. Mr.Eskew, a graduate of Purdue University, joined UPS in 1972as an engineer. In his 30-year career with the company, hehas held a variety of posts in the U.S. and Germany, includ-ing Corporate Vice President for Industrial Engineering andVice Chairman. In January 2002, he was named Chairmanand CEO.

ML: What do you think isgoing on in this economy?What is really wrong, andwhat's going to pull us out?ME: We released our earningsin July and we concluded thatthe economy, at that time, wassluggish across all the differentsectors that we serve. Theonly area where we saw any-thing going on was in mort-gage refinancing. An awful lotof letters and documents weregoing back and forth betweenbanks. We used to think thatwe were a good leading indica-tor for Gross Domestic Product(GDP). But as inventory levelsover the last few years havecome down, we don't think wesee changes in GDP until theyhappen.

ML: What do you see as thegreatest spurs to innovation? ME: For our business, wethink about two dynamics thatare in place: globalization andwhat we call “consumer pull” -consumers being able to lookinto the supply chain and pullthrough what they want, whenthey want it. As far as global-ization goes, our internationalbusiness is strong. The lastquarter our exports fromEurope were up 13 percentand our exports from Asiawere up 17 percent. China wasup nearly 40 percent year onyear. We see an awful lot ofpower in that dynamic. Theother dynamic, consumer pull,is powerful as well. I'll giveyou an example. The first com-puter I bought was an IBM XT.

I went to a retail shop to buy it.All the computers looked alike.They were all configured thesame way. And they weredelivered by truckloads. TodayI can order one computer and Ican configure it exactly as Iwant. I can select the screensize and printer. And today,consumers can pull these cus-tom-made computers throughthe supply chain one-by-one.They come one-by-one in apackage delivered, I hope, bya brown package car. Thisdynamic is making the supplychain cheaper.

ML: Tell me about globaliza-tion and its effects upon yourcompany.ME: We have an awful lot ofcustomers who really do want

to expand their markets. Andit's not just the big companies,it's the smallest companies,companies that started with uswhen they were in a garage.The nice thing is, we can actlike each customer’s packageis the only package we have.We can tailor solutions on aone-by-one basis.

ML: UPS is engaged in whatseems to be a pretty basicbusiness. You deliver packagesby trucks. It doesn't sound likea very romantic or exciting orchallenging business, yet Isuspect that it is.ME: UPS has been in busi-ness for 95 years. It wasfounded in 1907 by a teenagerin Seattle named Jim Casey.He started out delivering mes-

sternChiefExecutiveseries

Michael Eskewchairman and chief executive officer

United Parcel Service

4 Sternbusiness

sages in Seattle. In about1911, a new technology putJim's company out of busi-ness: the telephone. The needto run messages all overSeattle went down dramatical-ly. So he changed his businessand started to deliver goods forstores. Jim had to go convincethe stores of Seattle that if acustomer came downtown onthe streetcar and didn't want tocarry his goods home, hiscompany could deliver thosegoods to the customer’s home.And he could put all the pack-ages together and createscope and scale and put themall in a clean car with a uni-formed driver and do it profes-sionally. That's how the wholething started. That businesswent on until after World WarII. Then people didn't go down-town to shop anymore. Theydrove to suburbs and shoppingcenters, bought things anddrove them home. So the busi-ness model was again threat-ened by technology. JimCasey had to go into the com-mon carriage business andcompete directly with the postoffice. The business spreadfrom there.

I joined UPS in 1972. Wewere in 37 states and had rev-enues of about a billion dollars.Since then, we've moved into200 countries and we'vemoved beyond just ground, toair, to ocean, to international.And we've moved beyond justsmall packages. We now serv-ice the whole supply chain. Allcommerce is all about threeflows. Goods flow, informationflows, and funds flow. Ourbusiness is the flow of goods.And today, thanks to technolo-gy, we facilitate the flow ofinformation and funds. Weknow exactly when a package

was picked up, when it wasdelivered, and whether it wassigned for.

Think about a camera or acomputer or an elevator or aprinter or an aircraft or a med-ical device, any high techdevice. Usually folks that buythose devices need two-to-four-hour part replacementwhen something breaks. Youcan't run a McDonald's if thecash register doesn't work.Satisfying the need for twohour part replacement any-where in the world requires thebest transportation company inthe world, which we've beenbuilding for 95 years. Itrequires a lot of technology. Itrequires central stocking,keeping those critical parts inone or two or three locations inthe world. It requires forwardstocking locations, placeswhere you can keep parts sothat they can be where theyare needed two hours afterthat phone call is made. Wecan put all those servicestogether anywhere in theworld.

We also have repair loca-tions. We do repairs on thoseparts also, because it all needsto come together at one timeand place. Those companiesin the U.S., and in Asia, and inSouth America, and in Europewant one throat to choke. Weare it. They want one entity tomanage the supply chain. Sowe do get excited about thismundane business. It's makingcustomers better.

ML: You have a very strongbrand. How would you defineit? How do you preserve andprotect it? ME: Our brand was just evalu-ated and we determined thatwe have the second best busi-

ness brand in the U.S., next toCoke. We've done a lot ofwork with our brand recently. Itused to be that our purposewas to satisfy the small pack-age needs of our customers.Now our purpose is to enableglobal commerce. We went tobrand consultants. They toldus that we don't use our colorsthe way we should use our col-ors. We need to call attentionto brown, the color we own.We also need to think aboutmore than just the package,how to make the brand aboutenabling global commerce.

When the brown campaigncame out, we did a lot of sur-veys and we felt that therewere two other colors thatcompanies owned. Blue wasone of them, that was IBM.And pink was the other one,and that was Owens-Corning.And so we felt like we reallycould stake brown.

ML: What is unique and dis-tinctive about the UPS cul-ture?ME: We have two strengths atUPS. One is the way we'reorganized. We have districtorganization so we can beclose to the customer. Thepeople that run our businessday-to-day are in the field. Theother strength is our culture.We have 360,000 employeesin 200 countries around theworld. And there are no super-stars. None of us are moreimportant than the other. Noneof us are sufficient by our-

selves. We are a team. Thereare no private jets. We driveourselves to the airport. Iparked my own car and carriedmy own bag today. And Ianswer my own phone. Ourculture is that we are onegroup. We try to treat eachother the same. For instance, Ieat in the cafeteria every dayand I don't bring coffee anddrinks to my desk because weask the drivers not to drinkcoffee and eat lunch in theircars. That driver is as impor-tant as I am. That's part of ourculture.

ML: Do your executives getout and actually drive thetrucks?ME: We all did, every one ofus. I started at UPS as anengineer. I did some basicengineering for about the firsttwo months. Then I went on todeliver packages for about twoor three months. And younever forget the look in thecustomer's eye, the things theylook for. If a package is late,you'll never, ever forget it. Andwhen you get it there on timeand it delights and they need-ed it, you'll never forget it.When I was a district managerin New Jersey I would rideonce a month. I would ask thestaff to ride once a month.That’s not uncommon.

ML: You have a lot of longtime, long-term employees.ME: We do. We have about

"Our business is the flow of goods. Andtoday, thanks to technology, we facili-tate the flow of information. We knowexactly when a package was picked up,when it was delivered, and whether itwas signed for."

continued, page 7

Sternbusiness 5

somebody, what do you lookfor?BB: Personal values. I don'tthink leopards change theirspots. We want to find peoplewho believe in the same val-ues that we do. Respect forthe consumer. Respect foryour fellow workers. That leadsyou to teamwork. Modesty.That leads you to the accept-ance that there are good ideasall over the world. Then youmove on to professionalism.Internationalism. There was atime when I used to say, atti-tude is more important thanaptitude. I don't say this to thehuman resources departmentanymore. I tell them, I wantboth. There are good peopleall over the world, people withthe right values, and the rightbrain. I also look for peoplewho are hungry.

ML: Yours is a family busi-ness. The family owns a littlemore than a third of the sharesand has a little more than 50percent of the voting power.What are some of the particu-lar advantages and the partic-ular challenges of being in afamily business?BB: Over all, being a familybusiness is a big plus. The bigplus is that you build the busi-ness for the long-term. InEurope, we don't report quar-terly earnings. We report semi-annually. Of course, when youare a public company in theU.S., you must report quarterlyearnings. That puts pressureon management to do thingsthat are not necessarily goodfor the long-term. But if you'rea family business, you canbuild for the long-term. Andthat means, in our view, that

you don't have debt in such away that you are under pres-sure to make short-term deci-sions in order to cover yourdebt. And you don't over prom-ise to Wall Street. I sense thatsome of the things that havehappened recently on WallStreet are the result of pres-sure to generate earnings,which frankly were not realisticin relation to the growth of themarket. Also, the people whowork in the company mustknow that they will be evaluat-ed and fairly promoted, eventhough they are not in the fam-ily. And we in the family mustdo an excellent job. When Icame to the U.S., and when Igot more and more responsi-bility, my father was testingme. If I had not succeeded inthe U.S., I would not have thejob I have today. I tell my chil-dren and nephews and nieces,first you'll have to ask to jointhe business and then you'llhave to prove yourself.

Student questionsQ: How do you create syner-gies between your managersof different nationalities aroundthe world and what kind of dif-ferent talents do you expectfrom them?BB: You create synergies bychoosing the right people.You've got to have people whodeliver on a regular basis. Andyou have to be very carefulabout communication. Whenyou have people from differentbackgrounds who speak differ-ent languages, you have to bevery, very attentive. One of ourphilosophies is, "It's notenough to explain. You have tobe understood."

Q: Do you sell the same razorat the same price in the U.S.

as you do in China, India, orSouth America? Many retailershave a terrible problem whenthey price discriminatebecause their merchandise issmuggled from third worldcountries into developed mar-kets and sold at below marketprices.BB: We do price to marketand we do have that issue. Ifyou want to grow in EasternEurope, you have to offer yourproduct at a price that is lowerthan in Western Europebecause people in EasternEurope don't have the money.But you need to know yourbusiness. You need to know anaccount well enough to seethat if you get an order from awholesaler four times biggerthan any order that you haveever got from that wholesalerbefore, there is somethingfishy about it.

Q: Failure is part of the grow-ing process to become a goodmanager. Could you share withus one of the most humblinglosses that you had whilegrowing up in your business?BB: My biggest failure was theacquisition of Shaeffer Pen. Ithasn't worked out yet. I thinkone of the reasons is that a lotof the Shaeffer business is inAsia. And shortly after webought the business, Asia wentstraight downhill. The secondthing is that people today,executives, do not have asense of pride in having a

Continued from page 3

high-quality, high-end writinginstruments. We need to revivethat part of the industry. We didnot thoroughly analyze thehigh-end of the business. Wedid not do enough homeworkbefore the acquisition.

Q: Would you please tell usabout your trajectory to the topof Bic?BB: When I was 16 or 17,instead of going to England tolearn English, I came here forthe summer. And I loved it.Later, I took a year off andtraveled all over the UnitedStates driving a car. It was1964 and we were a verysmall company. And I would goto retail stores and check onour distribution. I became veryinterested. After a year, myfather asked me what I wantedto do. I said, I want to go tobusiness school in America. In1964, there was no other placeto go to business school. AfterI graduated from NYU Stern, Iwent into investment banking. Iworked for White Weld in theU.S. and Europe for about fouryears, and then joined Bic. Ibecame president of the U.S.business in 1983. That's whenwe started to introduce newproducts which we didn't havein Europe. And that's howNorth America became 56 per-cent of our global business. Myfather gave me the chance toshow what I could do here inthe U.S.

"I think that in the 1970s, you could notcall yourself an international company ifyou were not strong in the United States.I think in ten or twenty years you will notcall yourself a strong global company ifyou are not strong in Asia."

6 Sternbusiness

four percent turnover, whichmeans that people last onaverage 25 years among thefull-time ranks. The loyalty thatthey have is terrific.

ML: What kind of characteris-tics and qualities do you lookfor when you are hiring some-one?ME: We really think aboutfolks that can work with peo-ple. This is a people business.It's not a place for everyone. Ifyou want private cars and pri-vate jets and country clubs andyou want to see your name upin lights, don't come to UPS.It's not that kind of place. But itis a place that you can workand know that you do some-thing that's honest and noble.Delivering a package is noble.We are enabling commerce,making our customers better,taking them places. It's anhonest job and it's a greatplace to work. And we think wemake a difference.

Student questionsQ: Can you give us an exam-ple of how you create highvalue, innovative solutions forcustomers? ME: We think about this interms of four dynamics. Wethink about things we do inter-nally and things we do exter-nally, things we do for existingbusinesses and things we do

Continued from page 5 for new businesses. In termsof things we do internally, welook at the product processwith our marketing group. Forexample, they take next dayair and second-day air andmake it 8:30 and 10:30, andthey replicate that model andintegrated delivery networkthroughout 200 countries. Theway we grow existing busi-nesses externally is throughmergers, acquisitions, partner-ships, and alliances. We'vedone several acquisitions.We've done hundreds of part-nerships and alliances, gener-ally in the high- tech space.We know that we have to go toexternal sources to be able togrow existing some businesses.

With new businesses, we

can try new things and we can

fail small fast, so we try to

innovate down there. For

example, we investigated web-

based grocery delivery. We

tried it and failed fast. But we

didn't fail with a lot of money.

We use a strategic enterprise

fund to examine new business

opportunities. We use that to

fund pre-IPO companies that

do things in spaces that we're

interested in. And we support

research at universities. One

of those companies was a

company named Savi, which

does radio frequency (RF)

transponders. We move 13

million packages across the

world every day and we want

to know where every one is at

every moment. Right now, we

do that by scanning every

package several times. That's

a lot of labor. What we'd like to

do is use RF transponders as

a way to track packages.

Q: What items are on your

capital expenditures wish list?

ME: We spend a billion dollars

every year on technology, and

we have for the last 15 years.

We've been described as a

technology company with

trucks and that's a fair descrip-

tion. We're going to continue to

spend money on technology.

We just opened our new air

sort in Louisville. It's the most

phenomenal sort you've ever

seen in your life. The pack-

ages sort themselves! The

packages move 400 feet a

minute but if you could make

time stand still, you could find

that package within 12 inches

in a building that is the size of

the Pentagon. It's a phenome-

nal thing. Also, we're going to

continue to add to the 300 air-

craft we own, to be able to

take our customers' packages

around the world.

Q: In your ongoing effort to

globalize your market, how has

it been different doing busi-

ness in other countries?

ME: We did our first interna-

tional expansion in Germany in

1976. We all thought that we

could do things there just like

we did them in the U.S. For

example, we called each other

by our first names in the U.S.

Well, Germans don't do that

because of the formality of the

language. We want to be able

to build our overall brand so

that folks all over the world

learn to think of UPS. Our

website is available in 19 dif-

ferent languages. It's tailored

to 109 different countries. So if

you're in a remote part of

Nigeria, you can find out how

long it takes to get a package

to Japan.

Q: UPS has invested very

heavily in aviation over the

past decade. I know that you

have experimented with using

that aviation equipment in

other ways. Can you tell us

about that?

ME: We do sometimes experi-

ment in that kind of new busi-

ness. We look at three differ-

ent dynamics. First, it has to

be an attractive market, a

growing market. Second, it has

to leverage our strengths, our

skills, our brand, our customer

base, our technology, our peo-

ple. Third, it has to fit our strat-

egy. Again, that strategy is to

enable global commerce. We

didn't think flying passengers

on the weekends to cruise

ships necessarily was an

attractive market. It almost dis-

tracted us. So we got out.

"We went through brand consultants.They told us that we don't use our colorsthe way we should use our colors. Weneed to call attention to brown, thecolor we own."

"We have 360,000 employees in 200countries around the world. And thereare no superstars. There are no privatejets. I parked my own car and carriedmy own bag today. And I answer myown phone."

Sternbusiness 7

rom the ability to communicate with friends inLondon via instant messaging to the presenceof canned okra from Lebanon in the aisles ofStop’n’Shop, there is evidence all around us

that the world is becoming a smaller place. So too, alas,are indicators that significant distances – political, cul-tural, and economic – stand between us and our fellowinhabitants of the earth.

In his 2000 best-seller, “The Lexus and the OliveTree,” New York Times columnist Thomas Friedmanrhapsodized about the positive implications of global-ization and the proliferation of the latest development ininformation technology. No two countries withMcDonald’s, he reported, had ever gone to war. His2002 best-seller, “Longitudes and Attitudes,” focusesmore on the downsides of globalization. It turns out, ofcourse, that in our global village, terrorists can use theInternet to organize, and that even isolated countrieslike North Korea can gain the expertise needed to pro-duce highly sophisticated weaponry.

Despite today’s uncertainties – many of which havebeen economically disruptive – the forces that spurredglobalization are still immensely powerful. The trade ingoods, services, and ideas is increasing, not decreasing.In a fascinating interview, Michael Eskew, the chairmanand chief executive officer of United Parcel Service(UPS), provides insight into one of the workhorses ofthe global economy (p. 4). UPS, which began life as amessenger operation in Seattle, now employees 370,000people in 200 countries. But while UPS’ fleet of browntrucks and brown-clad delivery people provide themuscle, the human element is only half the story. “Whatreally makes us the best is information,” Mr. Eskewsays. “Information that tells us where that package is,when it's late, what building it's been in, where it went,who sorted it in the wrong direction.”

Yes, information – and information technology (IT) –increasingly drive commerce. Unlike oil or bananas, bitsand bytes can move freely and cheaply from prettymuch any point on the globe to another at the click of amouse. That allows an enterprising company to provide

IT services to U.S.clients from alocation as seem-ingly remote asIndia. Today,Infosys, a soft-ware giant basedin India andlisted on theNasdaq, countsdozens of blue-chip U.S. compa-nies among itsclients. In theircase study (p. 10)Raghu Garud, ArunaKumaraswamy and MonicaMalhotra show how Infosysis creating a new paradigmthat can be emulated by compa-nies from Bangalore to Boston.“What most distinguishes Infosys is theway it systematically built up a post-modern,scalable enterprise for harnessing intellectual capital inthe new information economy,” they write.

The realization that gaping cultural, political, andeconomic gulfs exist in a world theoretically made smalleris just one of many apparent contemporary paradoxes.Here’s another: In recent years, the trade in internation-al financial assets has increased sharply. And yet at thesame time, the major economies have seen their pathsdiverge. We’re growing together while growing apart.These two phenomena – financial globalization and realregionalization – as Fabrizio Perri and JonathanHeathcote tell us, are directly related (p. 40). After all,when capital moves more freely, it can follow and pursuereturns, and react quickly to local shocks.

The recent experience of Argentina, whose decision todevalue the peso has caused massive economic disloca-tion, shows that discussions about capital flows are notsimply academic exercises. At a lively Stern forum last

F

8 Sternbusiness

C R O S S I N GBy Daniel Gross

fall (p. 30), Argentina’sformer economy min-

ister Domingo F.Cavallo (a HenryKaufman VisitingProfessor at NYUStern), Mario Blejer,a former governorof the Central Bankof Argentina, andNYU Stern profes-

sor Nouriel Roubinidebated the causes of –

and potential solutions to– the Argentina morass.

Surprisingly perhaps, theeconomists spent a good deal of

time talking politics. “For eco-nomic growth, you need strong insti-

tutions. And for that, you need a well-functioning political system,” Professor

Cavallo said. “The functioning of the constitu-tional system is more important than any question

related to the exchange rate system.”Niall Ferguson, the distinguished Oxford historian

who is a professor at NYU Stern, similarly argues thatinstitutions matter. In an elegant and provocative essay –drawn from his most recent book, “Empire” – Fergusonargues that the institutions and practices promulgated bythe British Empire in the 19th and early 20th centurymade it one of the original progenitors of globalization(p. 24). “A case can be made that the British Empire waseconomically beneficial, not only to Britain herself, butalso to her Empire – and perhaps even to the world econ-omy as a whole,” he writes.

History similarly informs Lawrence J. White’s pres-ent-minded discussion of the telecommunications melt-down (p. 44). Drawing parallels between the current tele-com glut and the overcapacity of railroads in the 1880sand 1890s, the savings and loan debacle of the late 1980s,and Japan’s rolling crises of the past decade, ProfessorWhite offers some advice for regulators and entrepreneurs:

declare bankruptcy, recognize and absorb losses, andmove on. And continue to use sound antitrust policy toencourage innovation. “Good public policy could steer usthrough the turmoil and allow us to emerge fairly rapid-ly with a more efficient telecommunications sector.”

ature companies must expand in order tocontinue growing. But the leap into a foreignmarket can be daunting. Many companiesgain initial knowledge from the experience

they build up at home. But, report Peter Golder andDebanjan Mitra, crucial knowledge “can also be gener-ated in foreign markets in which the firm already oper-ates that are similar to potential new markets.” Inexamining Wal-Mart’s mixed efforts to expand overseas(p. 34), David Liang concludes that the retailing giantscould have benefited from what Professors Golder andMitra call “near-market knowledge.” When it firstopened in Argentina, Wal-Mart stores stocked 110-voltappliances; the local standard was 220 volts. Wal-Marthas stumbled, Mr. Liang concludes, in part because ithas failed to replicate sufficiently the sources of com-petitive advantage – its brand, product mix, logisticsoperations, among them – that it has developed athome.

Increasingly, growth-seeking giants like Wal-Martare going to turn to Asia, says Bruno Bich, the secondgeneration chairman and CEO of the French consumerproducts company. “I think that in the 70s, you couldnot call yourself an international company if you werenot strong in the United States,” he said in a NYU Sterninterview (p. 2). “I think in 10 or 20 years you will notcall yourself a strong global company if you are notstrong in Asia.”

Today, globalization is a loaded term. It inspiresvisionary idealists and embittered protesters alike.There’s a tendency on both sides of the debate to inflatethe costs and benefits of this powerful and unstoppabletrend. But if you take the long view, and analyze trends,and place them in their proper context – as the authorsin this issue do – you can’t help but think that the way ofthe future lies more in crossing borders than in isolation.

D A N I E L G R O S S is editor of STERNbusiness.

M

Sternbusiness 9

B O R D E R S

A Passage From

I N D I AInfosys has emerged as a titan of the global software industry by carefullydesigning and constructing a unique corporate culture. Continued growthwi l l tes t the qua l i t y and soundness o f the company ’s a rch i tec tu re .

By Raghu Garud, Arun Kumaraswamy and Monica Malhotra

he software companyInfosys is one of India’sgreat business success sto-ries. Infosys was founded

in 1981, when seven professionalsled by N.R. Narayana Murthy, cur-rently the chairman and chief men-tor, collectively invested $1000.Now, Infosys is the third largestcompany in India, with a marketcapitalization of more than $10 bil-lion. Based in the emerging informa-tion technology (IT) center ofBangalore, Infosys in 1999 becamethe first Indian company to be listedon the Nasdaq. In a country wheremany companies have opaquefinancial statements, Infosys hasvoluntarily adopted stringentaccounting practices. In a country

where ownership and control ofbusinesses have been concentrated inthe hands of a few families, Infosyshas distributed ownership and con-trol broadly among its 10,000employees, known as “Infoscions.”

But what most distinguishesInfosys is the way it systematicallybuilt up a post-modern, scalableenterprise for harnessing intellectualcapital in the new information econ-omy. Nandan Nilekani, Infosys’sCEO and managing director, usesthe term “scalability” to refer toInfosys’s ability to grow from pastexperiences even while maintainingthe integrity of operations. In abroader sense, scalability meansInfosys can simultaneously increaserevenues and profitability while

growing across cultural valuesystems and value chains. Thisscalability is built into the compa-ny’s DNA, and it pervades the waythe company develops software,mentors employees, formulatesstrategy, and governs itself.

ndeed, this scalability hasallowed Infosys to evolve con-tinually. In particular, Infosyshas created a malleable andresponsive learning organiza-

tion that continually uses its experi-ence to replenish and transform itsstock of resources and capabilities.In other words, Infosys is an organi-zation that is perpetually in themaking – which is what it takes tosucceed in the fluid, global, rapidlyevolving IT industry.

T

I

10 Sternbusiness

ILLUS

TRATIO

NS

BY

CH

RIS

MC

ALLIS

TER

Sternbusiness 11

Scalable StrategyProfessor Marti G. Subrahmanyam

of NYU Stern School of Business,and an independent director ofInfosys, pointed out that “A key ele-ment of a strategy for survival andeven rejuvenation in a downturn isa flexible financial frameworkwithin which a company operates.”Infosys’s PSPD Model that empha-sizes predictability, sustainability,profitability, and “derisking,” is anintegral component of such a flexi-ble framework. These four strategicgoals are, in turn, accomplishedthrough a set of sub-models andguiding principles. For instance, theCustomer Relationship Model, whichemphasizes the creation of long-term relationships with each client,helps ensure the predictability andsustainability of revenues. More

For the years ended March 31,

RevenuesCost of revenues

Gross profit

Operating expenses:Selling, general and administrative expensesAmortization of deferred stock

compensation expenseCompensation arising from stock split

Total operating expenses

Operation income

Equity in loss of deconsolidated subsidiaryOther income, netIncome before income taxesProvision for income taxesSubsidiary preferred stock dividends

Net Income

Earnings per share:BasicDiluted

Cash dividend per equity share

Balance sheet data:Cash and cash equivalentTotal assetsTotal long-term debtTotal stockholders equity

$413,851 $203,444 $120,955 $68,330 $39,586 $26,607 $18,105 $9,534213,614 111,081 65,331 40,157 22,615 15,638 10,606 5,621

200,000 92,363 55,624 28,173 16,971 10,969 7,499 3,913

57,641 26,656 16,199 13,225 7,010 4,351 3,344 1,314

5,081 5,118 3,646 1,520 768 361 46 –– – 12,906 1,047 – – – –

62,722 31,864 32,751 15,792 7,778 4,712 3,390 1,314

137,515 60,499 22,873 12,381 9,193 6,258 4,109 2,598

– – (2,086) – – – –9,505 9,039 1,537 801 769 1,460 746 322

147,020 69,538 22,324 13,182 9,962 7,718 4,856 2,92015,072 8,193 4,878 770 1,320 895 893 251

– – – 68 – – – –

$131,948 $61,345 $17,446 $12,344 $8,642 $6,824 $3,963 $2,670

$2.01 $0.93 $0.28 $0.21 $0.15 N/A N/A N/A$1.98 $0.93 $0.28 $0.20 $0.15 N/A N/A N/A

$0.14 $0.11 $0.09 $0.04 $0.02 N/A N/A N/A

$124,084 $116,599 $98,875 $15,419 $8,320 $7,769 $8,046 $2,885342,348 219,283 153,658 48,782 32,923 27,261 23,051 9,400

– – – – – – – –311.792 198,137 139,610 41,146 30,640 23,925 19,668 8,852

2001 2000 1999 1998 1997 1996 1995 1994

$ in thousands (except per share data)

Source: Infosys Annual Reports

EXHIBIT 1INFOSYS AUDITED FINANCIAL INFORMATION, 1994-2001

Source: Infosys Annual Reports

EXHIBIT 3INFOSYS PSPD MODEL

Quality

PredictabilityMaintenance

Higher value services

Increase revenue productivity

Offshore model – Global delivery

Upsell to existing clients

Iterative model of development

Exposure limits for client concentration

Exposure limit for dotcom businesses

Exposure limit for opportunitybusinesses (like Y2K)

Geographical diversification

Translating clients to partners

Long-term Relationship

Offshore SoftwareDevelopment Center

Sustainability

Profitability

Growth

De-risking

People Transparency

12 Sternbusiness

A PASSAGE FROM INDIA

than 80 percent of Infosys’s businessis generated from repeat customers.The Global Delivery Model, underwhich a major portion of project exe-cution costs is shifted from costly“on-site” client locations to relativelycheaper locations in India, plays animportant role in ensuring profitabil-ity. Derisking is accomplished by, forexample, limiting exposure to anyspecific client, domain or type ofproject to less than 10 percent ofannual revenues, and by adopting aconservative financial policy thatlimits debt.

Of course, the PSPD model is notapplied without reflection to addressnew challenges that continuallyarise. Models cannot replace humanjudgment, which is why Infosys hascreated several processes to study,review, and coordinate strategic ini-tiatives and operational priorities.These processes unfold in severalforums, including the Board ofDirectors, and the 57-memberManagement Counci l , whichincludes the board and departmentheads, as well as nine representa-tives from the younger generation atInfosys. The Management Councilmeets frequently to discuss markettrends and any other issues of strate-gic/tactical relevance.

Even though Infosys departmentsenjoy considerable autonomy todevelop and implement strategicand operational initiatives, the coreimplementation process is essential-ly the same across the company.Infosys also takes a measuredapproach to implementation.“Usually, when we come up with apossible solution or a plan, we pilotit to see how it works,” observedS.D. Shibulal, director of customerdelivery: “Then, we go back to thesolution and correct it based on theresults. We institutionalize the solu-tion only after two or three suchcycles.” Infosys’s ability to learn andadapt as it evolves is implicit in thisapproach. Here, scalability is evi-dent in the ways Infosys encapsu-lates past experiences to shapefuture aspirations.

EXHIBIT 2 Infosys Timeline, 1981-2001

1981 • Year of incorporation in India

1987 • Opened first international office in the U.S.

1992 • IPO in India

1993 • Listed successfully in India• Obtained ISO 9001/TickIT Certification

1995 • Set up development centers across cities in India• Received best Annual Report Award from ICAI

(every year from '95)

1996 • Set up Infosys Foundation to focus on contributing back to the society

• Established e-Business practice• Set up first European office in Milton Keynes, U.K.

1997 • Attained SEI-CMM Level 4• Set up office in Toronto, Canada• Set up Engineering Services practice

1998 • Rated first in Economic Times India’s "Award for Corporate Excellence"

• Established Enterprise Solutions practice

1999 • Listed on Nasdaq• Crossed $100 mm in annual revenues• Attained SEI-CMM Level 5• Rated India's most admired company by

The Economic Times Survey• Opened offices in Germany, Sweden, Belgium and Australia• Established two development centers in U.S.• Established Infosys Business Consulting Services• Reorganization for competence building - DCG,

SETLABS,CAPS

2000 • Became first company to be awarded the "National Awardfor Excellence in Corporate Governance" conferred bythe Government of India

• Crossed $200 Million in annual revenue• Set up offices in France and Hong Kong• Set up Global Development Centers in Canada and U.K.;

Set up third Development Center in the U.S.• Combined dedicated e-Business practice with rest of the

organization

2001 • Crossed $400 mm in revenues• Rated Best Employer of India in a study by

Business Today-Hewitt Associates• Opened new offices in Singapore, UAE, and Argentina• Set up new development center in Japan

Source: www.infy.com

Sternbusiness 13

A PASSAGE FROM INDIA

Developing IntellectualCapital

o company can executestrategies without theright personnel in place.And Infosys has takengreat pains to recruit,

train, and mold a scalable work-force. In the middle of Infosys’ssprawling ‘Infosys City’ universitycampus sits an imposing structurewhere Infoscions regularly receivetraining. New employees enter a 14-week educational program. Afterthis rigorous initial training, eachInfoscion must undergo 15 days offormal training annually to upgradetechnical and managerial skills. Inaddition to training Infoscions,the company’s 50-faculty strongEducation and Research Center(E&R) conducts research on newtechnologies and pilots them as theyemerge. For example, E&R enabledInfosys to leverage the late 1990scorporate “mind-shift” towards e-commerce. Infosys’s revenues frome-commerce related projects rosefrom a mere 1.7 percent of revenuesin the first quarter of 1999 to18.8 percent of revenues in thefirst quarter of 2000.

Intellectual growth is all-perva-sive at Infosys. People learn fromone another as they rotate from oneproject group or from one knowl-edge domain to another. Whenrecruiting, Infosys looks for peoplewith “learnability” – the ability toderive generic conclusions from spe-cific situations and then apply themto a general class of unstructuredsituations. Learnability is crucial tomanage the rapid career progres-sion. “By 28, an Infoscion could wellbe a general manager, and by mid-30s, a director of the company,” saidNandita Gurjar, associate vice presi-dent of Learning and Development.“Those who have been rewarded arethose who have been able to jumpfrom one paradigm to the next.”

Under the company’s intensivementoring process, Infoscions atevery level groom and teach thoseunder them. Top executives coachnewly minted middle managerson the need to spend ample time

on networking, interdepartmentalsocializing and meetings, fire-fighting and logistics administration.To design an effective leadershipprogram, Infosys has established theLeadership Institute at Mysore,India.

Knowledge ManagementFor an entire company to be scal-

able, it must be able to leverageknowledge across all its employees.“Learn once, use anywhere,” as akey Infosys motto puts it. Infosyshas now instituted an integratedapproach to the management of

knowledge. “The vision is thatevery instance of learning withinInfosys should be available to everyInfosys employee,” said MaheshVenugopalan, a member of Infosys’sKnowledge Management (KM)Group.

The four pillars of Infosys’s KMsystem – people, content, process,and technology – comprise thearchitecture that guides the creation,transfer, and reuse of knowledge atInfosys. Its origins can be traced tocompany efforts starting around1992 to create Bodies Of Knowledge(BOK), which are nuggets of experi-ential knowledge on topics rangingfrom technologies and applicationsoftware to adapting to new cul-tures. Dr. J. K. Suresh, principalknowledge manager, pointed outthat such BOKs, and other reusablecontent, were created and reused inisolation within any given projectcontext. But they lacked visibility aswell as extensive use across theorganization till the developmentand deployment of a formal, enter-

prise-wide KM system during 1999-2000.

Besides creating and recordinginternal knowledge, white papers,and re-usable code, the KM systemaffords Infoscions access to externalcontent like websites and technologyand business news. Eighteen differ-ent content types have been identi-fied (BOK being one of them). Everyitem in the central KM repository isassociated with one or more nodes(representing areas of discourse) ina ‘knowledge hierarchy’ and taggedto facilitate ease of submission, clas-sification, and retrieval. Currently,approximately one fifth of allInfoscions have contributed atleast one knowledge artifact to thecentral KM repository, and morethan a thousand knowledge artifactsget downloaded by Infoscions forserious use every day.

Since practice units lack the timeand resources to create domain ortechnology specific knowledge,Infosys created two internal consult-ing groups: the Domain CompetencyGroup (DCG) and the SoftwareEngineering & Technology Labs(SETLabs). The DCG coversindustry dynamics and trends, keyplayers, regulatory and accountingpractices. SETLabs focuses ontechnology architectures to createframeworks that can be used byproject teams and business units.

o sow the seeds for theemergence of newknowledge and compe-tencies, Infosys createdthree new business units

to focus on the emerging e-business,ERP solutions, and telecommunica-tions sectors, and an engineeringservices group to offer engineeringservices focused on quantitativemodeling. S. Sukumar, head of cor-porate planning, explained: “Overtime, people from these businessunits are moved around to otherunits to transfer competencies.”

To facilitate the transfer ofknowledge and a culture of sharing,Infosys developed an Intranet portal– the K-Shop. If a question is postedon an electronic bulletin board thatis part of the knowledge manage-

"What most distinguishesInfosys is the way it

systematically built up apost-modern, scalableenterprise for harness-ing intellectual capitalin the new information

economy."

14 Sternbusiness

N

T

ment system, it is not surprising toget several responses from employ-ees across the organization within afew minutes. The KM group has cre-ated an application called the“expert locator,” which allowsInfoscions to declare their specificexpertise so colleagues may consultthem when necessary. The KMgroup has also instituted formalmechanisms for the sharing of bestpractices across the company –quarterly meetings of business man-agers, for example.

To encourage knowledge sharing,the KM group has instituted variousrewards, recognition, and incentiveprograms. Specifically, Infoscionscan earn Knowledge Currency Units(KCUs) for contributing, reviewingor using the BOKs or other knowl-edge assets. Another form of KCUs(termed the composite KCUs) also

serves as a metric to assess contentquality (as determined by the vari-ous attributes related to contentusage, and ratings by users acrossthe organization) and measure theeffectiveness or benefits of theknowledge management program.“Overall, the number of KCUs gen-erated and distributed to employees– currently more than 160,000 –provides a clear indicator of theincreasing level of knowledge shar-ing within Infosys,” said C.S.Mahind, a member of the KM group.

Organizing for GlobalDelivery

Infosys thrives on its ability tosolve clients' problems that lie dis-tributed across the globe with soft-ware solutions created in India. In1998, Infosys decided to abandon its

traditional strategic business unitstructure in favor of a combinationof geography and focused servicesbased business units (also known asPractice Units (PU)). The threelargest delivery units are located inthe U.S., Infosys’s largest market,which accounts for nearly 75 per-cent of its business. In keeping withInfosys’s Customer Relationship

Sternbusiness 15

"In 1998, Infosys decided to abandon its

traditional strategicbusiness unit structurein favor of a combina-tion of geography and

focused services basedbusiness units."

Corporate Organization Structure - Infosys Corporate Organization Structure - Infosys

CHIEF MENTOR

CEO & PRESIDENT

COO & CUSTOMER SERVICE& TECHNOLOGY

CEO & President CEO & President

Nandan M. Nilekani, (Managing Director)

Gopalakrishnan S.(Deputy Managing Director)

Shibulal S.D.(Director)

HRD, IS, QUALITY &PRODUCTIVITY AND CDG

Dinesh K. (Director)

CFO, ADMINISTRATION& FACILITIES

Mohandas Pai T. V.(Director)

DELIVERY - APAC

EDUCATION & RESEARCH

COMPUTERS &COMMUNICATIONS

HUMAN RESOURCESDEVELOPMENT

FINANCE & COMPANYSECRETARY

SECURITY AUDIT &ARCHITECTURE GROUP

SALES - CENA

SALES - ES

SALES - EURP

SALES - IBCS

SALES - SONA

SALES - WENA

DC - MOHALI

DELIVERY - CAPS

SALES - CAPS

CORPORATE MARKETING

SALES - IT OUTSOURCING

QUALITY & PRODUCTIVITY

COMMERCIAL & FACILITIES

INFORMATION SYSTEMS

COMMUNICATIONDESIGN GROUP

SALES - SYSTEMSINTEGRATION

DELIVERY - CENA

CHINA INITIATIVE

PDC - BOSTON

ESCP

SALES - ESCP

DELIVERY - ES

DC - HYDERABAD

GDC - CANADA

IT OUTSOURCING

DC - MYSORE

PDC-NEW JERSEY

DC - PUNE

SET LABS

DELIVERY - QUALITY

IBCS

SPECIAL INITIATIVES

DCG

LIFE SCIENCES INITIATIVE

PDC - UK

DC - CHENNAI

DC - BHUBANESWAR

PDC - FREMONT

DC - MANGALORE

PDC - CHICAGO &SYSTEMS INTEGRATION

DELIVERY - EURP

DELIVERY - SONA

DELIVERY - WENA

BANKING BUSINESS UNIT

Girish Vaidya (SVP)

INFOSYS LEADERSHIPINSTITUTE

Jayaram G. K. (Head ILI)

CORPORATE PLANNING

Sukumar S.(Manager Acting Head)

Narayana Murthy N. R., (Chairman)

Legend:APAC = Asia PacificBPO = Business Process OutsourcingCAPS = Communication and Product Services CENA = Canada & East North AmericaDC = Development CenterDCG = Domain Competency GroupES = Enterprise SolutionsESCP = Engineering Services & Consultancy PracticeEURP = EuropeGDC = Global Development CenterPCC = Product Competency Center PDC = Proximity Development CenterIBCS = Infosys Business Consulting ServicesSONA = South North AmericaSETLabs= Software Engineering and Technology LabsWENA = West North America

Designations:AVP = Associate Vice PresidentBDM = Business Development ManagerBM = Business ManagerCMO = Chief Marketing OfficerPM = Project ManagerRM = Regional ManagerSPM = Senior Project ManagerSVP = Senior Vice PresidentVP = Vice President

SALES & MARKETING

SALES - APAC

CUSTOMER DELIVERY

INFRASTRUCTURE & SECURITY

ACCOUNTS &ADMINISTRATION

EXHIBIT 4

model, a PU is responsible for itsclients globally, even if the clients’operations are spread across regionsin other PUs. In addition to buildingclose relationships with clients, thisstructure generates scale economieswith support functions such ashuman resources and finance locat-ed in India.

Organizing for economies of scaledoes not necessarily result in scala-bility along the value chain,because PUs are purely orientedtoward execution. Infosys has creat-ed structures and processes toaddress this challenge. The domainand technology specific knowledgethat the DCG and SETLabs offer,combined with the relationshipspecific knowledge that PUs offer,generates value that is scalableacross geographical contexts. Projectteams are cross-functional withmembers possessing multiple, over-lapping skills.

ventually, whether or nota company is scalable isdetermined not just byhow its activities are par-titioned, but also by the

processes that integrate these vari-ous parts. If processes are static,the corporation may settle into anefficient structure that lacks evolu-tionary capabilities. But there isnothing static about the organiza-tional routines that governInfosys’s operations. The best wayto understand these routines is byexamining the software develop-ment and deployment process. TheCapability Maturity Model (CMM),developed by the SoftwareEngineering Institute at CarnegieMellon University, forms the back-bone of Infosys’s processes. CMMassesses the maturity level of asoftware development company’sprocesses and methodologies on ascale of one to five. Each maturitylevel requires the organization todevelop specific capabilities in cer-tain key process areas. And Infosysis one of the few organizations in theworld to be assessed at Level 5.

An important component ofCMM is the capability to learn,which ensures continuous improve-

ment in processes. CMM generallyemphasizes learning from experi-ence and feedback. But Infosyslearns not only from its own experi-ences, but also actively seeks toimport relevant external knowledge.“If there is something better, weare willing to learn,” said S.Gopalakrishnan, COO and deputymanaging director. “We look atother organizations, study them,

and then do it our own way.”The continuous improvement

philosophy inherent in CMM hasbeen institutionalized for the rest ofthe company in the InfosysExcellence Initiative. Using theseven criteria of the MalcolmBaldrige National Quality Award(MBNQA) framework, Infosysassesses its entire cross-functionalsupply chain to identify areas thatneed attention. In these areas,Infosys has enacted changes toimprove quality and productivityusing the 6-Sigma technique and theISO 9001 initiative.

Inverting TraditionalHierarchies

Managing intellectual capital ischallenging. Employees can influ-ence a company’s value propositionby determining the extent andquality of their intellectual contri-butions. As Chairman NarayanaMurthy observed, Infosys’s employ-ees walk out of the door every dayand it is the management’s task tomake sure that they come back.

The need to maintain employeeloyalty has imposed demandsupon Infosys’s management.“Bright, young people want to workin smaller companies. They don’t

want to be part of a team or workfor a large company,” said ChiefFinancial Officer T.V. MohandasPai. “So, Infosys needs to retain theflexibility, speed, collegiality, andopenness of a small company.”Infosys attempts to do so by ensur-ing that decision rights remain withthose who possess relevant knowl-edge – its front-line workers.

Such an inversion of the tradi-tional hierarchy is only possible ifpeople assume the responsibility touse information to arrive at superiordecisions. K. Dinesh, director of HR,Quality and Productivity, offered thefollowing maxim as a guiding prin-ciple for decision making: “In onlyGod we trust. The rest of you bringfacts.” Infoscions are encouraged tochallenge one another based on thefacts they can marshal. As a result,the company culture itself is builtaround a dialectic tension whereemployees agree to disagree, therebygenerating informed consensus.

What role can top managementplay if front line knowledge workersmake most decisions? At Infosys,managers are part of a largerprocess of mutual mentorship, aprocess that the founders hope willcreate an institution that survivesthem. “As we go up the corporateladder, our role becomes direction-al,” said Pai. “Our philosophy andduty is to recruit people who arebrighter than us and to mentorthem.” This paradox speaks to adeep sense of security among man-agers. On the one hand, Infosysmanagers deploy their considerableexperience to guide those underthem. On the other, they learn fromthe very employees they teach.

TransparencyBecause investors are naturally

wary of new economy companies,Infosys has proactively adopted thehighest international financial stan-dards. In 1994-95, it was the firstIndian company to adopt stringentU.S. Generally Accepted AccountingPrinciples (GAAP) for financialaccounting and to include completeand detailed disclosures of accountsand activities in annual statements.

"Infosys reports itsfinancial performance

in compliance with the generally

accepted accountingpractices of seven

countries."

16 Sternbusiness

E

A PASSAGE FROM INDIA

Also, it was the first Indian compa-ny to publish audited quarterly state-ments and release annual statementspromptly after the end of its financialyear. Now, Infosys reports its financialperformance in compliance with thegenerally accepted accounting prac-tices of seven countries.

By embracing transparent prac-tices, Infosys is compelling otherlarge businesses in India to followsuit. As V. Balakrishnan, vice presi-dent of Finance, pointed out: “Wefeel that transparency is a competi-tive advantage. Investors have morefaith in a company that is moretransparent.” Infosys has leveragedits pursuit of transparency into aninternational brand. After embrac-ing GAAP financial reporting stan-dards, Infosys listed on the Nasdaq –a strategic move that created a cur-rency to be used for stock optionsand potential acquisitions.

To date, Infosys has grown contin-ually by employing its resources asplatforms for improving existing ini-tiatives and launching new ones. Inthis sense, Infosys has demonstratedwhat it means to be a scalable corpo-ration. However, this process willsurely be put to the test as Infosys con-tinues scaling across value creationactivities and cultural value spaces. AsMr. Nilekani observed, “The chal-lenge now is to ensure that we areable to scale on all fronts – thephysical front, the global front aswell as on the soft issues front. All

this, while we are still able to retainthe quality and effectiveness we hadas a small company.”

For example, Infosys would liketo move up the value chain in thesoftware services industry – fromlow-cost project execution tohigh-margin end-to-end solutions.According to Balakrishnan, Infosys’sdream is “to get U.S. revenues atIndian costs.” But doing so meansthat the iterative model of softwaredevelopment and close contact withclients will increase. Infosys willthus lose some of its flexibility tomove higher-margin consulting proj-ects off-shore. And as competition forprogramming talent increases in theglobal IT sector, salaries in India arealso rising. That will pressureInfosys to raise its incentive andcompensation packages, which willmake it difficult for Infosys to main-tain its profit margins.

nfosys executives believe thatorganic growth may be too slow inaccomplishing the desired trans-formation. Therefore, Infosys is

evaluating acquisition opportunities.But unless the potential target has acompatible culture, it would be diffi-cult for Infosys to integrate the alienculture without disrupting its well-oiled processes and well-defined val-ues. After all, any effort at integrationwould be Infosys’s first.

Growth, coupled with geographicdispersion of employees, may alsomake it more difficult for Infosys to

leverage its collective knowledgeeffectively. Given that more than 90percent of Infosys’s revenues accruefrom outside India, any growth mustbe global in scope. As a result,employees may have to spend moretime removed from their base inIndia. Not only does this imposeenormous lifestyle and psychologicalburdens on remote employees, italso complicates the task of manag-ing and monitoring them. Infosys istrying to tackle this problem byrolling out company-wide e-mails,newsletters, and magazines.Furthermore, Infosys trains its man-agers to manage and monitor theirteams more effectively over distances.

However, as Infosys moves up thevalue chain and grows globally, thelength of time spent by employees atcustomer premises will increase. Ms.Hema Ravichander, senior vice pres-ident of Human Resources, worriedthat this may dilute the Infoscionculture, values and processes, whichmay make it difficult for an increas-ingly global organization to configureand integrate its systems, processes,and business units effectively. Suchgeographic dispersal and loss of iden-tity may also make it difficult forInfosys to develop leaders with a com-mon purpose to manage for the future.

The two faces of the Greek GodJanus symbolize an end as well as abeginning. If one were to apply thisimage to Infosys, the promise ofscalability lies in Infosys's ability tocontinually evolve from the veryplatforms it creates. Outcomes andprocesses are so intertwined that anyend state is but a new beginning. Itremains to be seen whether thispromise will continue to hold asInfosys becomes a legitimate playerin the global market.

RAGHU GARUD is an associate profes-sor of management at NYU Stern.

ARUN KUMARASWAMY , Stern Ph.D.1996, is assistant professor of manage-ment at the Rutgers University School ofBusiness, Camden.

MONICA MALHOTRA is a Stern MBA2001.

Sternbusiness 17

I

18 Sternbusiness

THE MARKET NEXT D R

arket entry decisionsare among the mostimportant strategicchoices companiesmake. Entering anymarket requires a

major commitment of financial andmanagerial resources, but foreignmarkets can be especially demand-ing. Even though many companiesestablished multinational operationslong ago, some of today’s leadingcompanies are currently making thedecisions to go global. Half ofBusiness Week’s top 50 companieswere established within the last 20years and began to internationalizeonly within the past decade – thinkof blue-chips like Dell Computer,Cisco Systems, Home Depot, andBest Buy. And many companies have

found decidedly mixed successexpanding in foreign markets. Wal-Mart, for example, did not initiallyadapt its retail format in Argentinato the local culture. Nonetheless, thegiant retailer’s experience inArgentina provided it with valuableinsights that it applied to subsequentoperations in similar countries.

Most of the research on theinternationalization process focuseson two factors as the primary deter-minants of foreign market entry:cultural similarity and economicattractiveness. Many researchersfind that cultural similarity withrespect to the domestic market is animportant determinant of entry,while others have found that marketentry decisions are positively relatedto country size and the levels of

development, trade, and infra-structure. But no current study hasconsidered the role of knowledgedeveloped by a firm’s subsidiariesin similar markets on subsequentforeign market entries.

Intuitively, it makes sense thatthe knowledge of the economic andcultural environment of a foreignmarket will affect the probability ofentering that market. Theories oforganizational learning argue thatfirms develop knowledge based ontheir experiences. This store ofknowledge constitutes an importantresource and is a source of competi-tive advantage. At first, of course,knowledge comes entirely from thehome market, and companies makecomparisons between the character-istics of the home market and those

M

Sternbusiness 19

Too frequently, companies with global ambitions simply try to export a business modelthat works well in their home markets. But international expansion is not always sosimple. Smart managers can gain valuable knowledge and experience by operatingin markets that are culturally and economically similar to their ultimate targets.

By Peter N. Golder and Debanjan Mitra

ILLU

STR

ATIO

NS

BY

CH

RIS

MC

ALL

ISTE

R

THE MARKET NEXT DOOR

of potential new markets. But suchknowledge can also be generated inforeign markets in which the firmalready operates that are similar topotential new markets. Operating inArgentina, for example, may haveprovided Wal-Mart with someinsights as to how to run a store inChile.

We have dubbed this phenome-non near-market knowledge. But theterm does not refer to markets thatare geographically close. Rather, itrefers to markets that are economi-cally and culturally similar. Suchknowledge can be broken down intonear-market cultural knowledge,and near-market economic knowl-edge. These terms refer to a firm’sunderstanding of the culture andeconomy, respectively, of potentialnew markets based on knowledgegenerated from operating in similarmarkets. When multinational corpo-rations (MNCs) internationalize,they can use such near-marketknowledge to select other foreignmarkets where the firm is more like-ly to succeed.

We set out to gauge the influenceand relative importance of near-market cultural and economicknowledge by gathering extensivedata and using it to test the validityof several widely accepted assump-tions about foreign-market entry.

Prevailing AssumptionsFirst, we assume that cultural

distance is negatively related to for-eign market entry timing. In otherwords, companies will hesitate toenter markets that are culturallyunfamiliar to them. Nearly allresearch on the impact of culture onforeign market entry has consideredthe distance between a firm’sdomestic culture and the culture ofeach potential market. Differencesin culture have been found to affectbrand image strategies, consumerinnovativeness, negotiations, andmarketing decision-making. Whencompanies operate in countries withdifferent cultures, they need to mod-ify their operations in these areas aswell as other elements of the mar-keting mix. Since such modifications

increase costs and risks, companiesare likely to enter countries with cul-tures similar to the domestic marketbefore entering countries with lesssimilar cultures.

Likewise, most people assumethat economic distance is negatively

related to foreign market entry tim-ing. Why? Firms seem more likely tobe successful operating in countrieswith economic characteristics thatare similar to the firm’s home mar-ket. Similar economic characteris-tics may reflect potentially impor-tant similarities between countrieswhere knowledge transfer is valu-able. For example, similar economicconditions might be associated withsimilarities in consumer demandand business institutions like distri-bution channels and media. Sinceknowledge of these factors can helpfirms succeed in foreign markets,companies are likely to enter coun-tries whose economies are compara-tively similar to the familiar domes-tic market.

The same set of assumptions per-tains when dealing with near-mar-ket knowledge. Since companies canacquire and share knowledgethroughout their organizations, theywill likely make some effort totransfer knowledge generated fromoperating in foreign markets toother similar markets. The knowl-edge generated in successful mar-kets should increase the probability

of entering similar markets. Whencompanies have positive experiencesin foreign markets, the cultural andeconomic knowledge generated inthose markets will lead to earlierentry in similar markets. Both con-cepts – cultural and economicknowledge – are dynamic andchange over time, with companies’experience.

Perhaps the most important fac-tor in foreign market entry decisionsis the economic attractiveness of acountry. All things being equal,firms are likely to choose more pros-perous and accessible economies.The extensive literature on foreigndirect investment (FDI) supportsthis view. FDI theory argues thatfirms face various disadvantages inforeign markets and invest onlywhen expected benefits exceed thosecosts. These benefits depend on theeconomic characteristics of eachcountry. Finally, in general,researchers have regarded economicfactors as playing a larger role incompanies’ foreign market entrytiming decisions than cultural deci-sions. Companies can mitigate thenegative impact of cultural distanceby gaining experience in similar for-eign markets and by hiring man-agers with knowledge of the localculture. But while companies canlearn about consumer demand andeconomic institutions, they havepractically no influence on the eco-nomic prosperity, size, and infra-structure of a country.

Identifying FrequentEntrants

As we set out to test theseassumptions, we conducted anextensive search for the completeentry data of many multinationalfirms. We focused on consumerproducts companies, based in a vari-ety of domestic markets, that havesuccessfully entered many countries.(The companies in our final samplegenerate more than half of their rev-enue outside their domestic mar-kets). All these firms have survivedfor at least several decades, holdleading market share positions, andhave not withdrawn from any for-

"Knowledge can also begenerated in foreignmarkets in which thefirm already operates

that are similar topotential new markets.Operating in Argentina,for example, may haveprovided Wal-Mart with

some insights as to howto run a store in Chile."

20 Sternbusiness