information asymmetry, accounting standards, and

TRANSCRIPT

Information Asymmetry, Accounting Standards,

and Accounting Conservatism

A thesis submitted to The University of Manchester for the degree of

Doctor of Philosophy

in the Faculty of Humanities.

2017

Mostafa Harakeh

Alliance Manchester Business School

2

Table of Contents

ABSTRACT .......................................................................................................................... 5

DECLARATION .................................................................................................................. 6

COPYRIGHT STATEMENT ............................................................................................. 6

DEDICATION ...................................................................................................................... 7

ACKNOWLEDGMENTS ................................................................................................... 8

CHAPTER 1. INTRODUCTION ....................................................................................... 9

CHAPTER 2. DOES CHANGING ACCOUNTING STANDARDS AFFECT

DIVIDEND POLICY? ....................................................................................................... 14

2.1. Introduction ............................................................................................................. 15

2.2. Motivation & Literature Review ........................................................................... 18

2.2.1. IFRS, Legal Systems and Accounting Quality .................................................. 18

2.2.2. Dividend Payout Policy and the Information Environment ............................... 21

2.2.3. Dividend Value Relevance and the Information Environment .......................... 22

2.3. Hypothesis Development ........................................................................................ 23

2.4. Research Methodology............................................................................................ 27

2.4.1. Dividend Payout Regression Model .................................................................. 27

2.4.2. Dividend Payout Regressions among Code-law Firms ...................................... 29

2.4.3. Dividend Value Relevance Regression Model .................................................. 31

2.5. Data & Descriptive Statistics.................................................................................. 32

2.5.1. Sample Construction .......................................................................................... 32

2.5.2. Descriptive Statistics .......................................................................................... 33

2.6. Empirical Results .................................................................................................... 36

2.6.1. Dividend Payout following IFRS ....................................................................... 36

2.6.2. Dividend Payout among Code-Law Firms ......................................................... 40

2.6.3. Dividend Value Relevance following IFRS ....................................................... 43

2.7. Conclusion ................................................................................................................ 44

References: ...................................................................................................................... 46

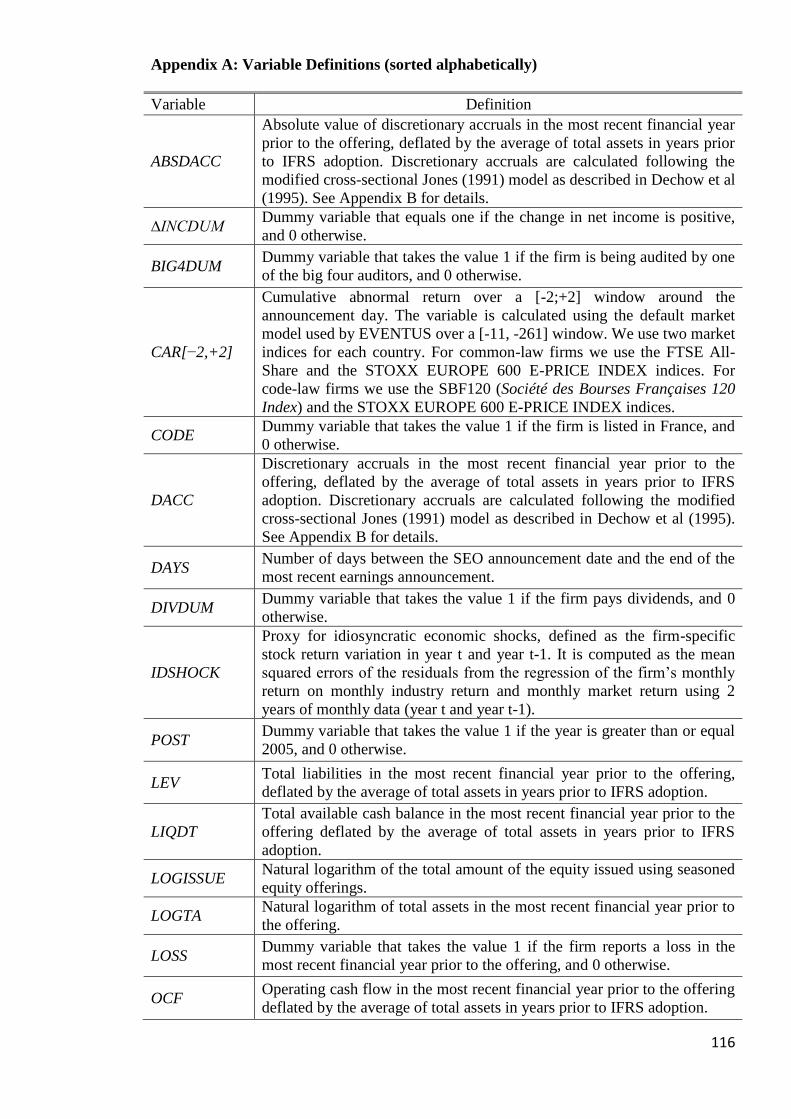

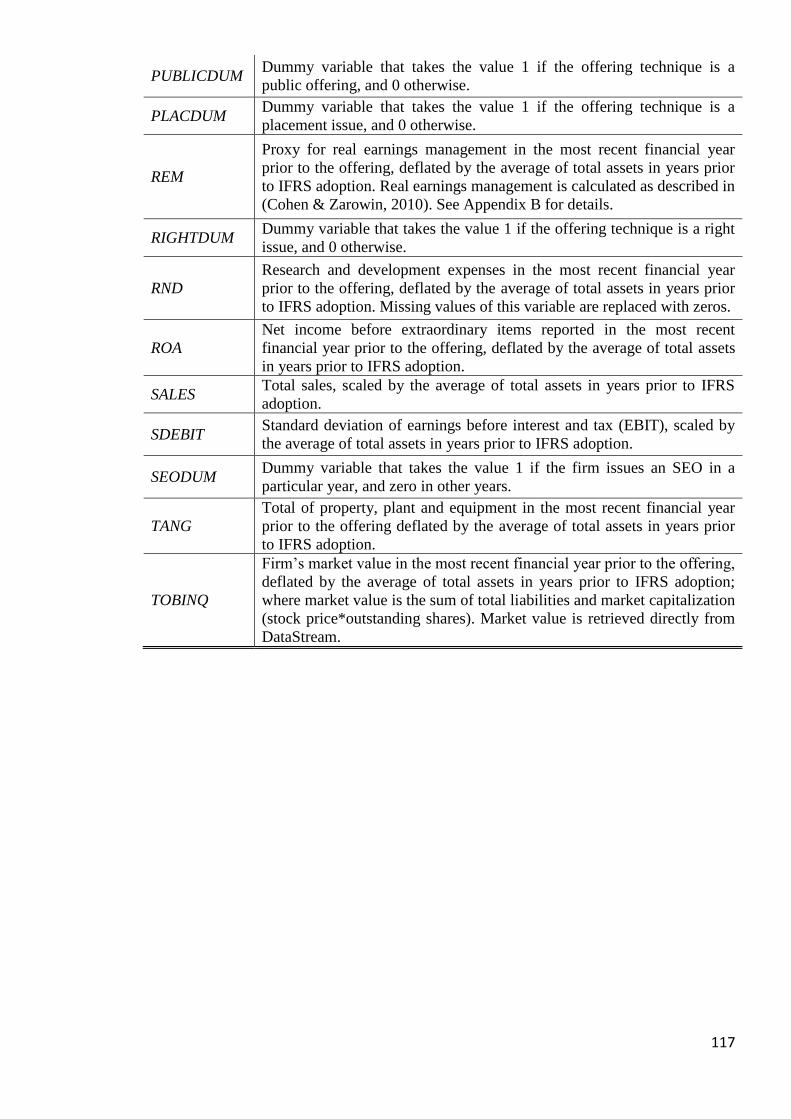

Appendix A: Variable Definitions (sorted alphabetically) ......................................... 50

Appendix B: Accounting Quality Metrics ................................................................... 52

CHAPTER 3. DOES CHANGING ACCOUNTING STANDARDS AFFECT

EQUITY FINANCING? .................................................................................................... 80

3.1. Introduction ............................................................................................................. 81

3.2. Motivation & Literature Review ........................................................................... 84

3.2.1. IFRS and Information Asymmetry in the SEO Setting ...................................... 84

3.2.2. Earnings Management around SEOs ................................................................. 85

3.2.3. The Market Reaction and the Propensity to Issue SEOs.................................... 86

3

3.3. Hypothesis Development ........................................................................................ 88

3.4. Research Methodology............................................................................................ 91

3.4.1. Test of Earnings Management ........................................................................... 91

3.4.2. Test of SEO Market Reaction ............................................................................ 94

3.4.3. Test of Propensity to Issue Equity ..................................................................... 96

3.5. Data & Descriptive Statistics.................................................................................. 97

3.5.1. Sample Construction .......................................................................................... 97

3.5.2. Descriptive Statistics .......................................................................................... 98

3.6. Empirical Results .................................................................................................. 102

3.6.1. Earnings Management around SEOs ............................................................... 102

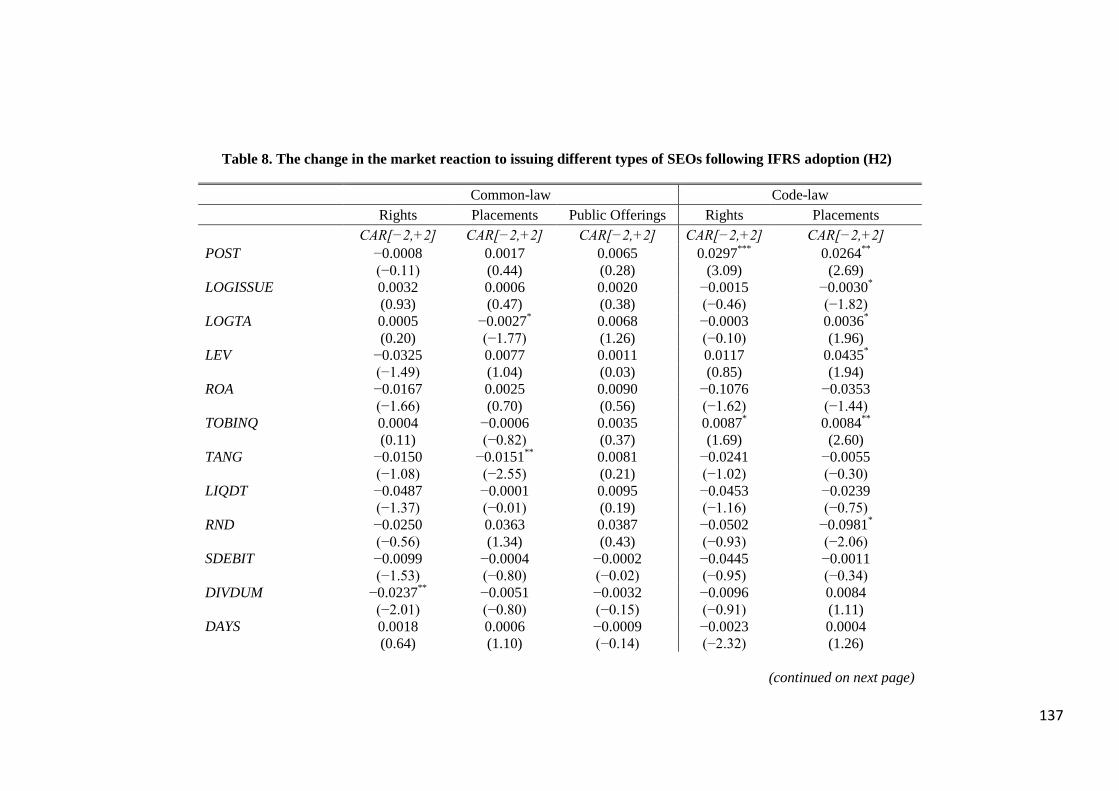

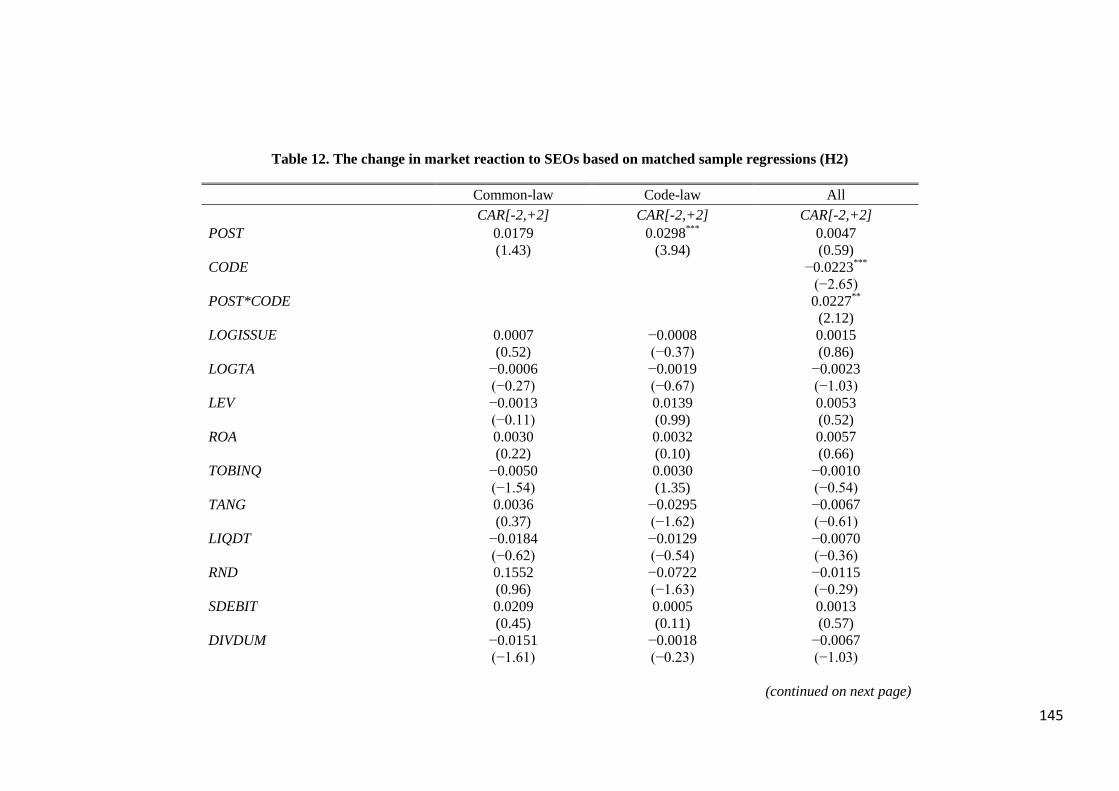

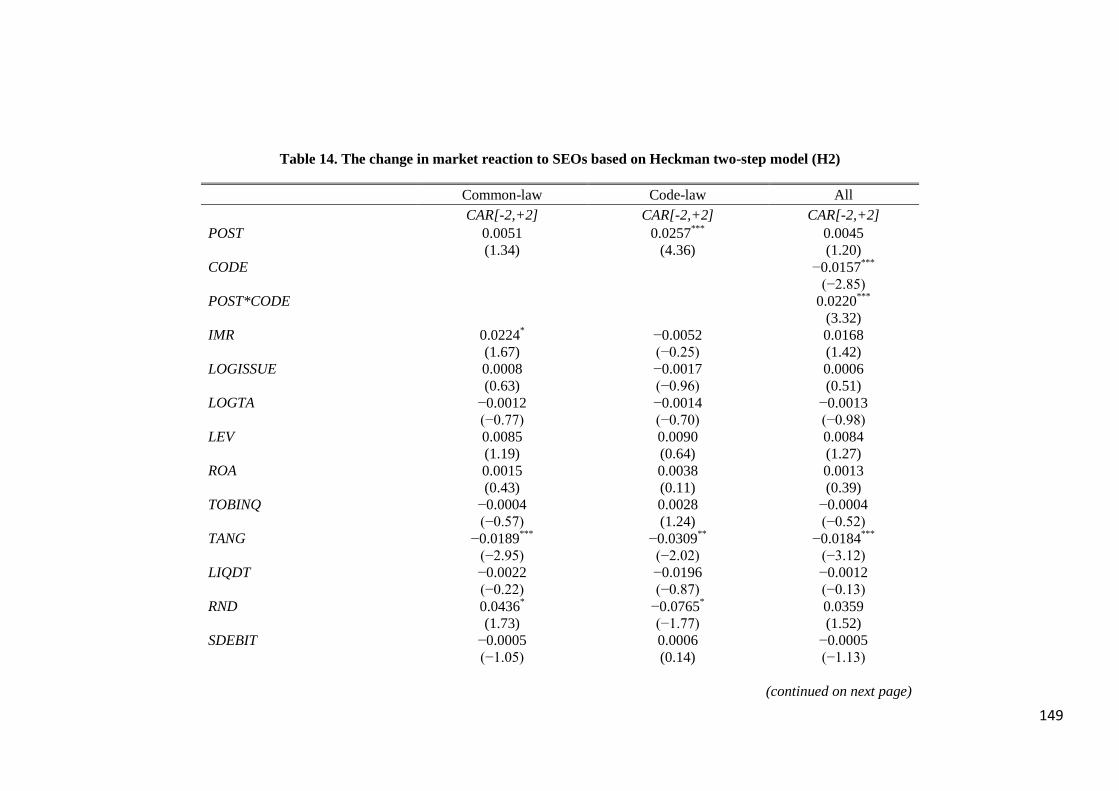

3.6.2. Market Reaction to SEOs ................................................................................. 104

3.6.3. Propensity to Issue New Equity ....................................................................... 107

3.6.4. Robustness Checks ........................................................................................... 108

3.7. Conclusion .............................................................................................................. 110

References: .................................................................................................................... 112

Appendix A: Variable Definitions (sorted alphabetically) ....................................... 116

Appendix B: Calculation of DACC and REM ........................................................... 118

Appendix C: Sample Construction ............................................................................. 120

CHAPTER 4. THE BIAS IN MEASURING CONDITIONAL CONSERVATISM . 151

4.1. Introduction ........................................................................................................... 152

4.2. Motivation & Literature Review ......................................................................... 155

4.2.1. Accounting Conservatism ................................................................................ 155

4.2.2. Asymmetric Timeliness Measures of Conditional Conservatism .................... 156

4.2.3. The Source of Bias in the AT Measure ............................................................ 158

4.2.4. An Alternative Measure of Conditional Conservatism .................................... 162

4.3. Hypothesis Development ...................................................................................... 164

4.3.1. The Bias in the AT Measure ............................................................................ 164

4.3.2. Assessing the Potential Bias in the C_Score Measure ..................................... 165

4.3.3. The AT Measure in an Interrupted Time-series Research Design ................... 166

4.3.4. The AT Measure in a Cross-sectional Research Design .................................. 167

4.4. Data & Descriptive Statistics................................................................................ 168

4.5. Research Designs and Results .............................................................................. 170

4.5.1. The Unconditional Relation between AT and VR ........................................... 170

4.5.2. Test Statistics for Comparing AT and VR Measures ....................................... 171

4.5.3. Examination of Conservatism Measures .......................................................... 172

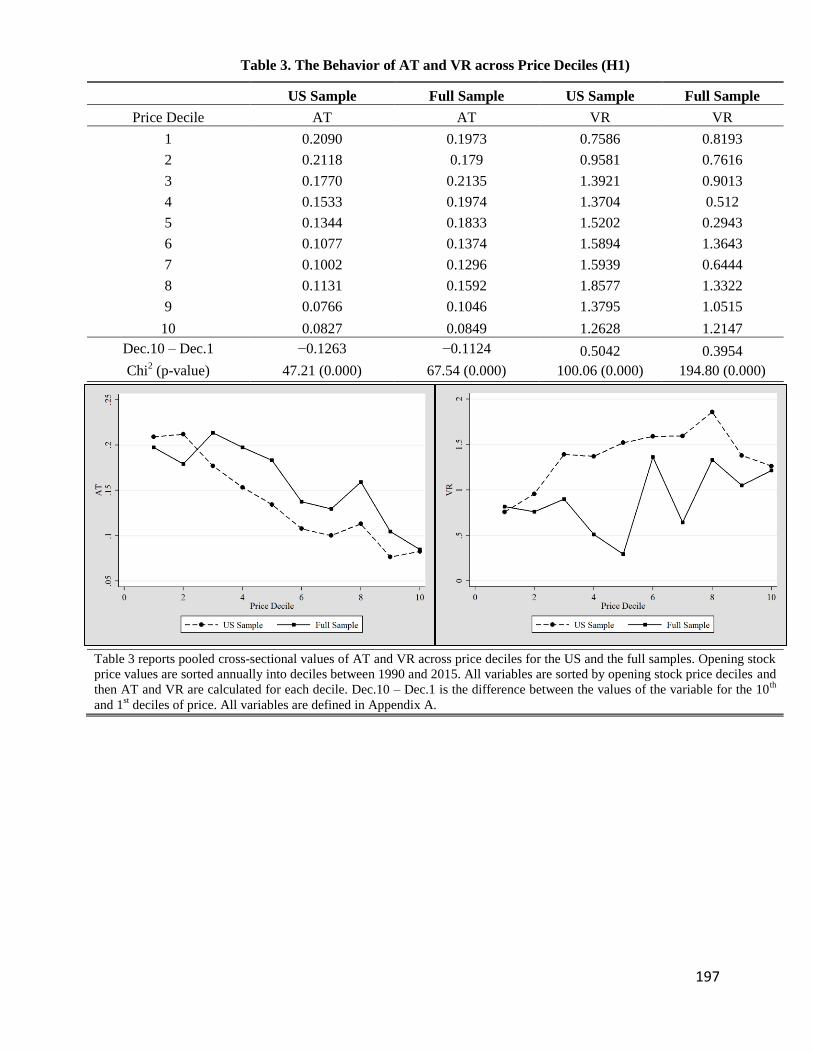

4.5.3.1. Comparing the Scale Effect in AT and VR – (H1) ................................... 172

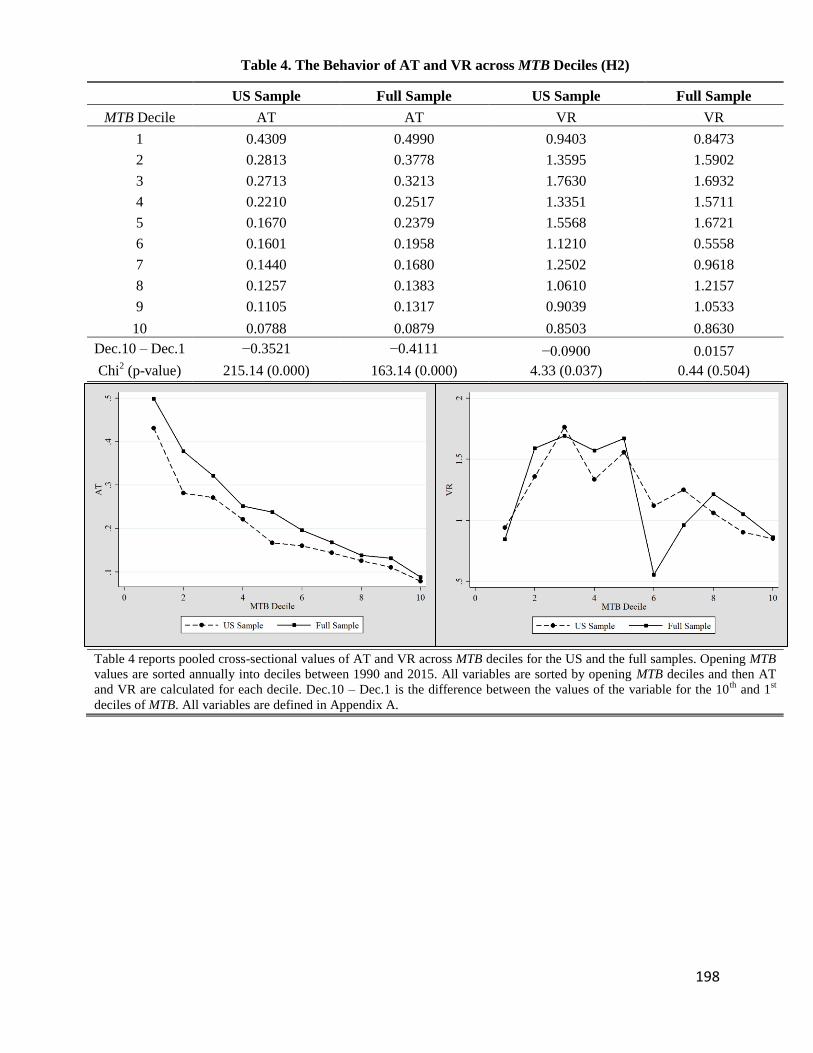

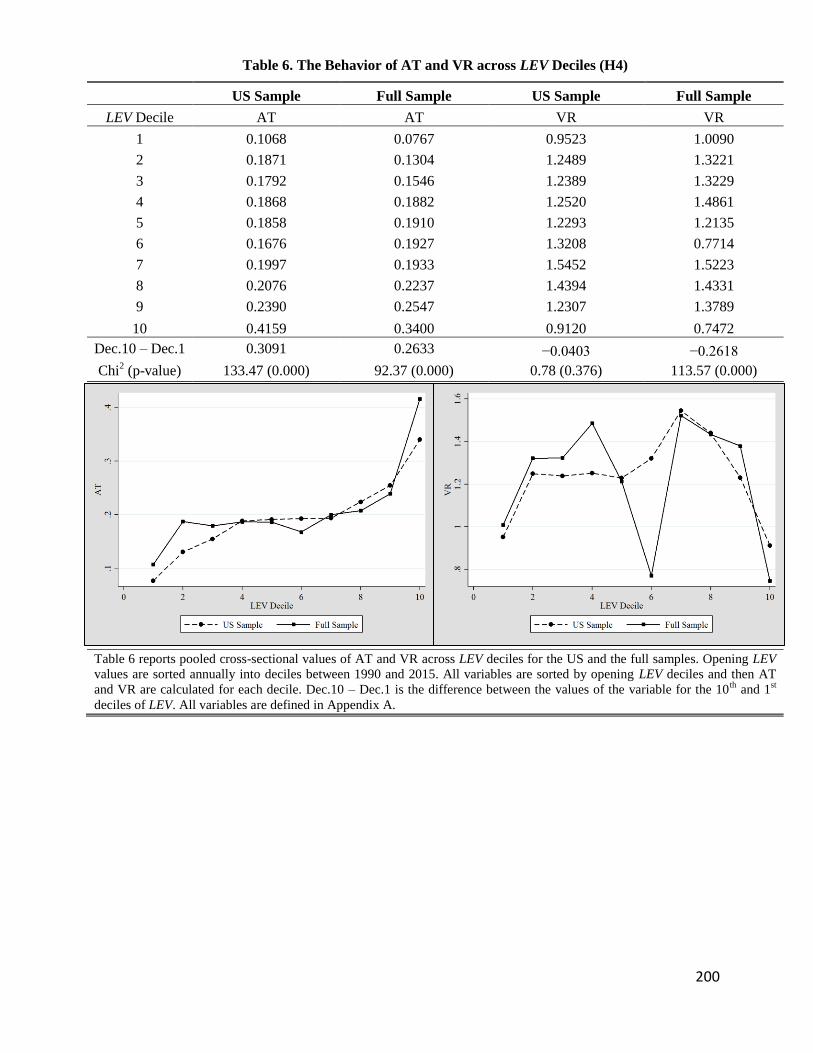

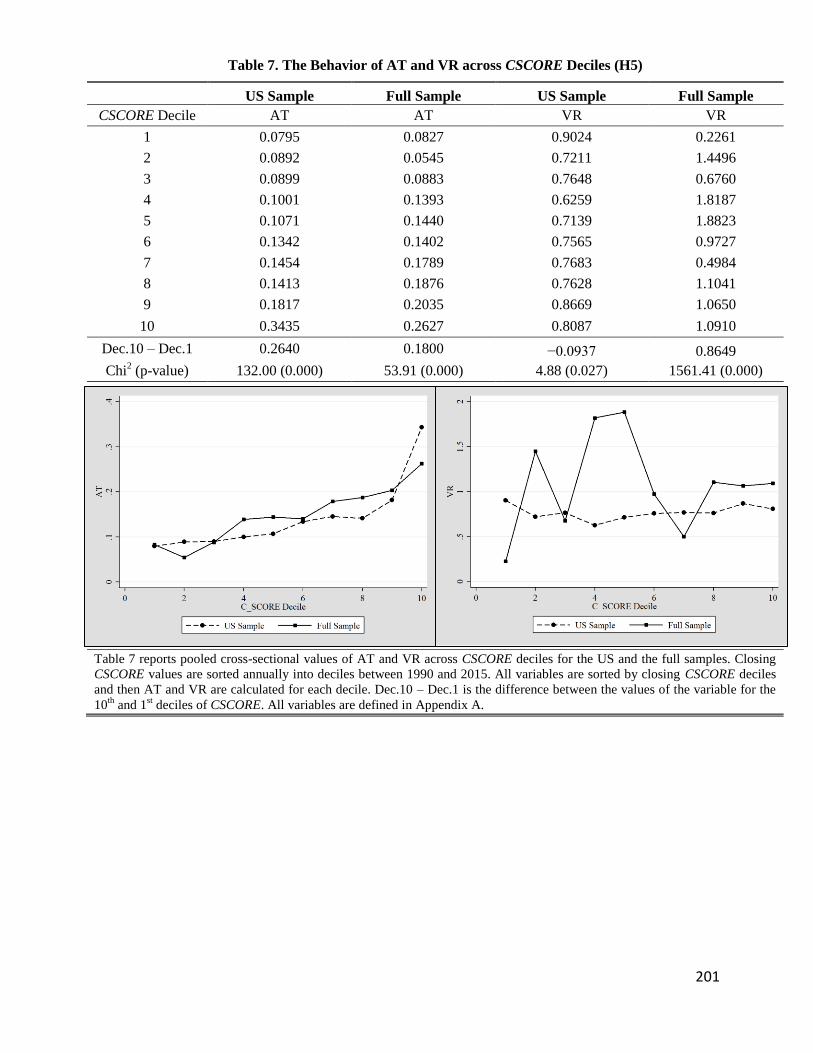

4.5.3.2. Comparing AT and VR across the Constituents of CSCORE – (H2-H5) 173

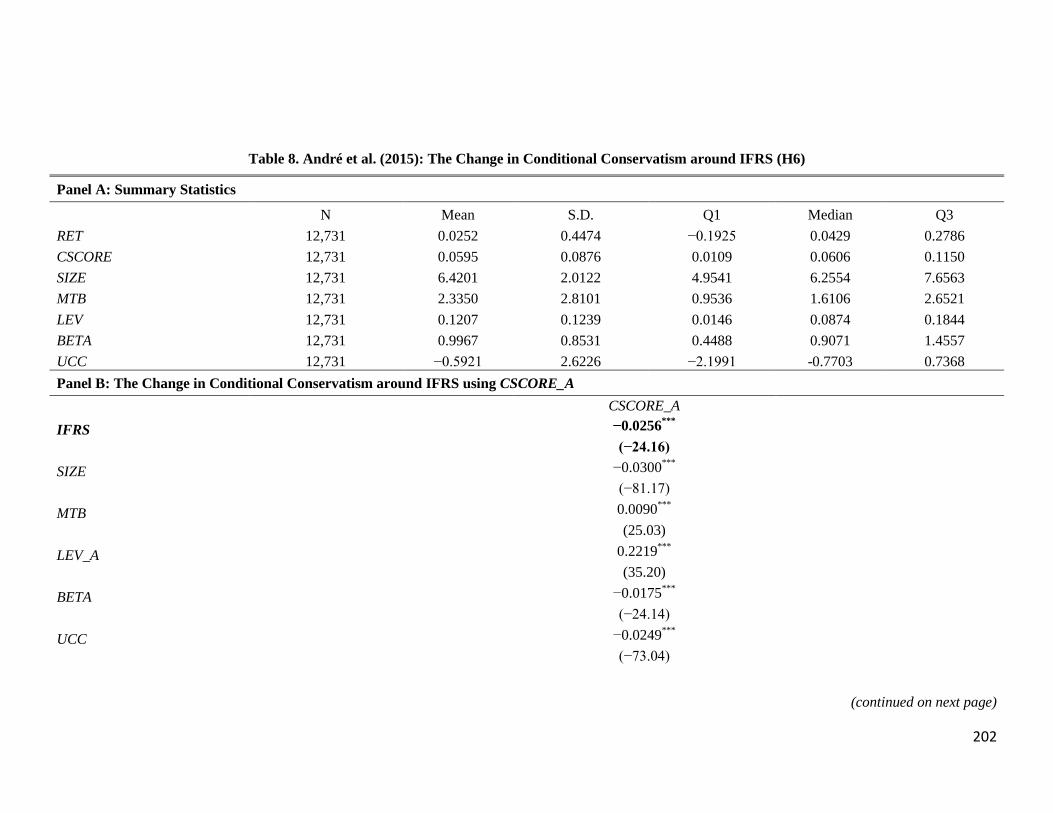

4.5.4. Comparing AT and VR in Interrupted Time-series Settings – (H6) ................ 177

4

4.5.4.1. André, Filip and Paugam (2015) – (H6) ................................................... 177

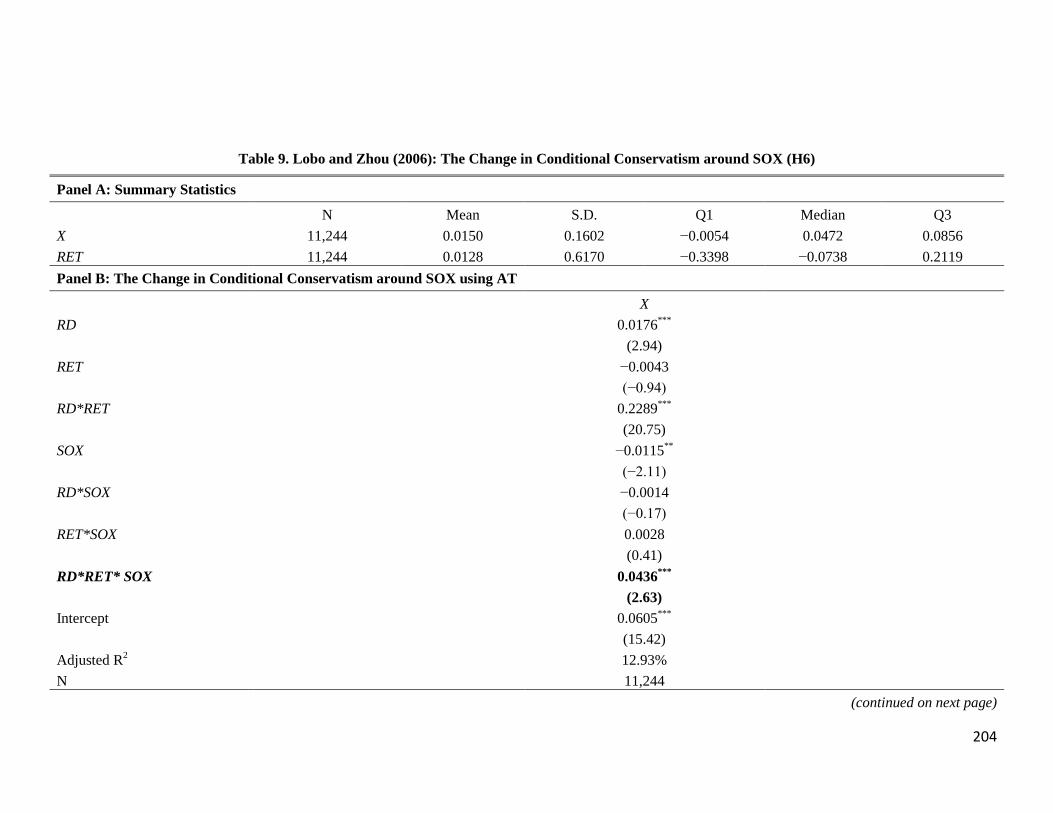

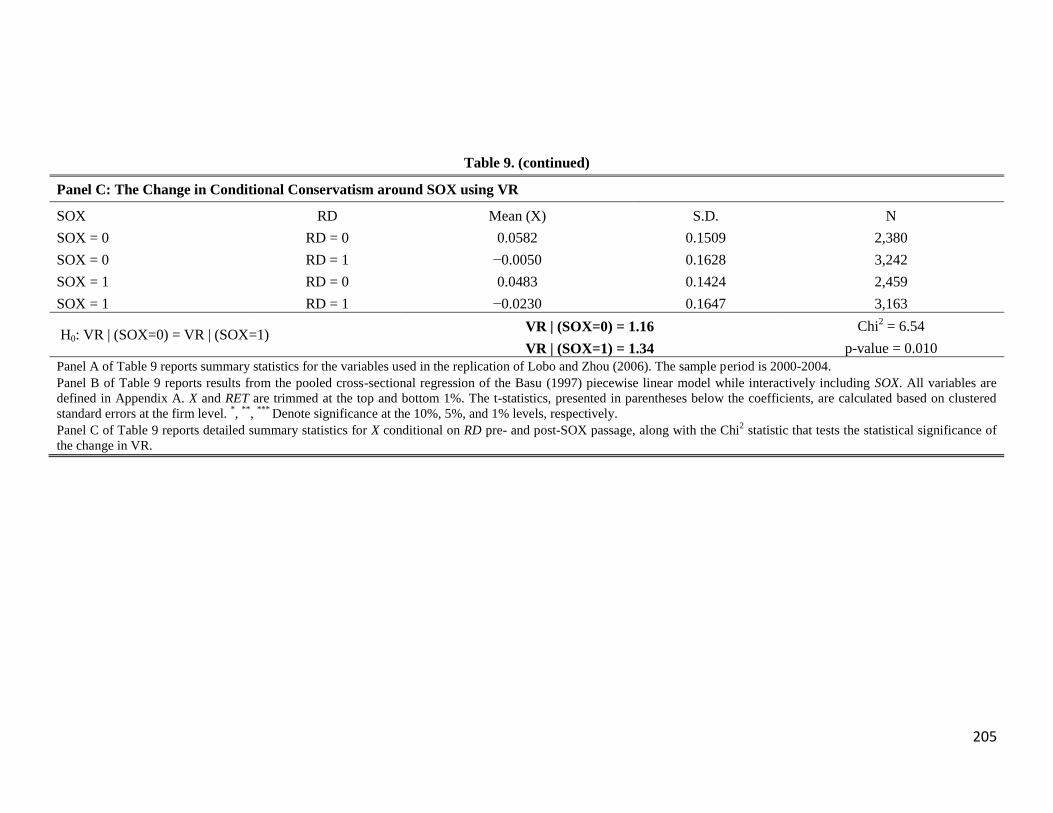

4.5.4.2. Lobo & Zhou (2006) – (H6)...................................................................... 179

4.5.5. Comparing AT and VR in Cross-sectional Settings – (H7a & H7b) ............... 181

4.5.5.1. Ball, Sadka and Robin (2008) – (H7a) ...................................................... 181

4.5.5.2. Gassen, Fulbier and Sellhorn (2006) – (H7a & H7b) ............................... 184

4.6. Conclusion .............................................................................................................. 188

References: .................................................................................................................... 189

Appendix A: Variable Definitions (sorted alphabetically by section) ..................... 192

CHAPTER 5. SUMMARY AND SUGGESTIONS FOR FUTURE RESEARCH .... 217

This thesis contains 53,040 including title page, tables, and footnotes.

5

Abstract

The University of Manchester

Mostafa Harakeh

Doctor of Philosophy (PhD)

Information Asymmetry, Accounting Standards, and Accounting Conservatism

2 April 2017

This thesis consists of three self-contained essays, each assessing the interaction between

financial accounting and information asymmetry from a different aspect. In the first two

essays, I examine how a change in the information environment affects the behavior of

market participants. In the third essay, I evaluate the empirical measurement of conditional

conservatism in accounting data. Together, these studies contribute to the understanding of

the role of financial reporting in mitigating the information gap between stakeholders.

In the first essay, I explore the impact of the mandatory adoption of the International

Financial Reporting Standards (IFRS) on dividend payout policy and the value relevance

of dividends in two Western European economies. I select the UK as a major common-law

country (control group) and France as a code-law country (treatment group) in order to

implement a difference-in-differences methodology. My findings suggest that IFRS

adoption is a major contributor in increasing dividend payouts among code-law firms,

compared to common-law firms, due to a greater reduction in information asymmetry

following the IFRS mandate. This makes investors in code-law firms more willing to rely

on accounting measures of firm performance, thereby causing a significant and material

decrease in dividend value relevance among code-law firms relative to common-law firms.

In the second essay, I examine the potential for IFRS to influence the market for SEOs. I

utilize a difference-in-differences methodology, where the UK (i.e. common-law firms) is

the control group and France (i.e. code-law firms) is the treatment group. I argue that IFRS

adoption serves to mitigate information asymmetry and improve accounting quality.

Accordingly, I find that, following IFRS adoption, earnings management activities

decrease among code-law firms prior to issuing SEOs. As a result of the lower levels of

earnings management and information asymmetry, I predict and find that the market

reaction to issuing SEOs improves significantly for code-law firms following IFRS. Given

that equity financing becomes less costly, I find that the propensity to issue new SEOs

increases among code-law firms after IFRS adoption.

In the third and final essay, I examine the empirical measurement of conditional

conservatism (CC) in accounting data. Prior studies have raised serious concerns about the

bias in the asymmetric timeliness (AT) measure of CC. This measure, along with the

C_Score measure, underpins a large body of empirical research on CC. Thus I endeavor to

assess the extent to which prior literature may need to be revised because of its reliance on

these measures. In exploring this issue, I replicate prior studies that rely on the AT or the

C_Score measure, and then compare the replicated results with those generated by

applying the variance ratio (VR) measure of CC, proposed by Dutta & Patatoukas (2017). I

show that the AT and the VR measures are associated unconditionally. Furthermore, my

findings suggest that the observed variation in the C_Score measure is driven by variation

in the bias implicit in the AT measure rather than variation in CC. I also provide evidence

showing that the AT measure yields similar conclusions to the VR measure in research

designs that model the change in CC following an exogenous change in accounting policy;

however, I find that using the AT measure to document cross-sectional differences in CC is

highly likely to have given rise to invalid conclusions in a large number of studies.

6

Declaration

No portion of the work referred to in the thesis has been submitted in support of an

application for another degree or qualification of this or any other university or other

institute of learning.

Copyright Statement

i. The author of this thesis (including any appendices and/or schedules to this thesis) owns

certain copyright or related rights in it (the “Copyright”) and s/he has given The University

of Manchester certain rights to use such Copyright, including for administrative purposes.

ii. Copies of this thesis, either in full or in extracts and whether in hard or electronic copy,

may be made only in accordance with the Copyright, Designs and Patents Act 1988 (as

amended) and regulations issued under it or, where appropriate, in accordance with

licensing agreements which the University has from time to time. This page must form part

of any such copies made.

iii. The ownership of certain Copyright, patents, designs, trademarks and other intellectual

property (the “Intellectual Property”) and any reproductions of copyright works in the

thesis, for example graphs and tables (“Reproductions”), which may be described in this

thesis, may not be owned by the author and may be owned by third parties. Such

Intellectual Property and Reproductions cannot and must not be made available for use

without the prior written permission of the owner(s) of the relevant Intellectual Property

and/or Reproductions.

iv. Further information on the conditions under which disclosure, publication and

commercialisation of this thesis, the Copyright and any Intellectual Property and/or

Reproductions described in it may take place is available in the University IP Policy (see

http://documents.manchester.ac.uk/DocuInfo.aspx?DocID=487), in any relevant Thesis

restriction declarations deposited in the University Library, The University Library’s

regulations (see http://www.manchester.ac.uk/library/aboutus/regulations) and in The

University’s policy on Presentation of Theses.

7

Dedication

I dedicate this work to my wife, who has faithfully loved me and supported me unconditionally,

Ghida

8

Acknowledgments

Writing this section was as difficult as writing a full chapter of this thesis. In what follows,

I express my indebtedness to everyone who helped and supported me, directly or

indirectly, to successfully complete my PhD. I love you all from the bottom of my heart.

First and foremost, I shall express my heartfelt gratitude to the holy God, Allah. I know

that you have granted me more than I deserve because you are generous and gracious, not

because I am worthy of your countless blessings. I promise you that I will employ the

graces you have endued me with to serve only righteous deeds.

To my great supervisors, Prof. Martin Walker and Prof. Edward Lee, you are just

awesome. I learned a lot from you, more than you can imagine. You made me believe that

the value of any PhD is derived from its supervisors in the first place. Your wisdom,

guidance, intelligence, and support have made my PhD journey one of the most

overwhelming experiences in my life. On top of that, I admire the humane attitude you

have always shown in several incidents. This only makes me respect you more and

appreciate how lucky I was when you accepted me to pursue my doctoral degree under

your supervision. I must also thank my internal and external examiners, respectively, Prof.

Norman Strong and Prof. Colin Clubb, for agreeing to examine my thesis. Indeed, being

examined by such reputable professors gives my PhD more value and credibility.

To my good friend Nikos, no words can express how grateful I am for your presence in

my life during my stay in the UK. You are a true friend that one can count on. I am proud

to have such a loyal and smart friend, with whom I can share my personal matters and

collaborate throughout my academic career. Also, to my friends in Lebanon, to the best

friends a man can have, our WhatsApp chats and Skype calls have made my journey away

from home much easier. Thank you for your support and prayers; I love you guys.

To my brother Maytham, thank you for being a good friend and a loving brother at

once. I will always be there for you when you need me, just like you have always been to

me. To my nerdy sister, Mira, you are the joy of our family. You will always have my full

support in fulfilling your promising academic ambitions. And to my kind-hearted father,

thank you for shaping my personality and for giving me your bright mind.

The famous poet William Ross Wallace says “The hand that rocks the cradle is the hand

that rules the world”; my mother is indeed one of those mothers who Mr. Wallace was

referring to. To the most caring, affectionate, and loving mother, no words can express

how much I love and admire you. The best years of your life went by while holding my

hand and doing all it takes to make that kid become a man – a man you can be proud of. I

hope that one day I will be able to compensate for a small part of your unlimited sacrifice.

Last but definitely not least, to the only girl I have ever loved, to the girl who has stood

by my side at all times, to the blessing of my life, to my best friend, to Ghida, thank you

for believing in me and for patiently spending four years waiting for me to come back. It is

said that outstanding accomplishments start with a dream. Ghida had this dream for me and

she made all it takes to make this dream come true. Without Ghida’s motivation and

support in getting this PhD, I wouldn’t have been writing these words now.

Mostafa Harakeh

Manchester, April 2017

9

Chapter 1

Introduction

In his famous paper “The Market for Lemons”, the Nobel Prize Laureate George

Akerlof started in 1970 a long standing literature on the economic consequences of

information asymmetry (Akerlof, 1970). Since its introduction to the field of financial

economics, the concept of information asymmetry has played a major role in accounting

and finance research (see the surveys of Biais, Glosten, & Spatt, 2005; Healy & Palepu,

2001). Scott (2015, p. 137) states that information asymmetry is undoubtedly the most

important concept of financial accounting theory. Information asymmetry derives its

critical role in financial markets from the fact that severe levels of asymmetric

information might lead to a complete collapse of markets. A recent example is the so-

called subprime crisis in 2008 (Ryan, 2008, p. 1626). Given these tragic consequences,

regulators and accounting standard setters strive to mitigate information asymmetry

through enforcing policies and financial reporting standards which aim to diminish the

information gap between market participants.

As far as the financial accounting research is concerned, financial reporting and

disclosure affect information asymmetry, which in turn influences economic decisions

made by market participants. In general, there are two kinds of market participants in an

information asymmetry setting: insiders and outsiders. I refer to managers and informed

(institutional) investors as insiders and to less informed (individual) investors as

outsiders. In capital markets, information asymmetry exists because of two main

problems: moral hazard and adverse selection. Moral hazard problems arise when

insiders misuse the firm resources to serve personal interests rather than maximizing the

firm value (i.e., hidden action). Such problems are exacerbated when outsiders do not

have enough information to monitor the economic decisions taken by insiders. Adverse

selection problems arise when one side of a potential economic transaction has relevant

information that the other side does not have (i.e., hidden information). Such problems

10

negatively affect investment efficiency and capital allocation and, accordingly, increase

the deadweight loss in the society.

A fundamental role of financial reporting is to mitigate moral hazard and adverse

selection problems through diminishing the informational gap between insiders and

outsiders (Mora & Walker, 2015). This brings the existing firm value closer to its

fundamental value (Scott, 2015, p. 141). In the same context, my thesis examines the

interaction between financial accounting and information asymmetry from three

different aspects. This thesis is structured around three self-contained essays in Chapters

2, 3, and 4. These essays examine original and different research questions, have

separate literature reviews, and exploit different datasets. While I recommend reading

each chapter independently, yet the concept of information asymmetry keeps a coherent

theme across all chapters. Chapters 2 and 3 examine how the behavior of market

participants changes following a positive information shock caused by the mandatory

adoption of the International Financial Reporting Standards (IFRS). This exogenous

improvement in the supplied information mitigates information asymmetry and reduces

the frictional costs of financial transactions between insiders and outsiders. In Chapter

4, I assess the measurement of a major feature of financial reporting: conditional

accounting conservatism. Conditional conservatism is a financial reporting attribute that

is meant to mitigate information asymmetry arising from adverse selection and moral

hazard problems. Specifically, investors (i.e. shareholders and bondholders) need to

assess their investment payoffs based on conservative estimations of firms’ net assets

due to their incomplete information (Balakrishnan, Watts, & Zuo, 2016). I re-examine

the empirical measurement of conditional conservatism in accounting data, which was

initially introduced in Basu (1997), in light of a contemporary study by Dutta &

Patatoukas (2017). I briefly discuss the three essays below.

In the first essay, I examine the effect of the mandatory adoption of IFRS on aspects

of dividend policy. Myers & Majluf (1984) theorize that, under information asymmetry,

11

firms pay less dividends due to high costs associated with external financing. I test

whether the reduction in information asymmetry, following the mandatory adoption of

IFRS, encourages managers to pay more dividends due to a reduction in financing costs.

At the same time, the mandatory adoption of IFRS is expected to improve accounting

quality especially in situations where accounting standards are of low quality. This

improvement in the quality of accounting numbers is expected to decrease dividend

value relevance while increasing accounting value relevance. That is, the signaling

power of dividends decreases following IFRS adoption. The empirical results I report

are consistent with the previous hypotheses. Specifically, I find an increase in the level

of dividend payout following IFRS adoption, especially among firms that had lower

accounting quality in the pre-IFRS period. In addition, I find a simultaneous change in

the value relevance of accounting line items and dividends following IFRS adoption,

where accounting value relevance increases while dividend value relevance decreases.

The second essay is sequel to the first, where I examine the effect of mandatory

adoption of IFRS on aspects of equity financing. As mentioned earlier, Myers & Majluf

(1984) theorize that external financing is costly under asymmetric information. I

examine whether the frictional costs associated with equity financing becomes less

pervasive following the IFRS mandate. Specifically, previous studies document that

managers engage in aggressive earnings management activities prior to issuing equity in

an attempt to elevate the value of the offered stocks (e.g., Teoh, Welch, & Wong, 1998).

I first examine whether the level of earnings management activities prior to issuing

equity decreases following IFRS adoption. Then I examine if the change in the levels of

earnings management and information asymmetry improves the market reaction to

issuing new equity. Finally, the change in the market reaction to equity financing is

expected to affect firms’ propensity to issue new equity. Consistent with the preceding

hypotheses, I find that the level of earnings management prior to issuing equity

decreases following IFRS adoption. This finding is significant in situations where the

12

accounting quality was relatively low before IFRS adoption. Then, I provide evidence

suggesting that the market reaction to issuing new equity improves significantly

following IFRS adoption due to the reduction in levels of information asymmetry and

earnings management. Finally, the improved market reaction indicates a reduction in the

cost associated with equity financing and, accordingly, I provide evidence showing an

increase in the propensity to issue new equity following IFRS.

In the third essay, I re-examine the empirical estimation of conditional conservatism

in accounting data. The accounting conservatism literature relies mainly on the

asymmetric timeliness (AT) measure of conditional conservatism, proposed by Basu

(1997), and on the derivative measure of Khan & Watts (2009), the C_Score measure.

Recent studies show a considerable bias in the AT measure (Dietrich, Muller, & Riedl,

2007; Patatoukas & Thomas, 2011, 2016). I extend these studies and use the variance

ratio (VR) measure, proposed by Dutta & Patatoukas (2017), to show that the bias in the

AT measure also applies to the C_Score measure. In addition, I re-examine prior studies

and find that the AT and the VR measures yield similar conclusions when used in time-

series settings that model the change in conditional conservatism for the same sample

following an exogenous change in accounting policy. On the other hand, I provide

evidence suggesting that the use of the AT measure to document cross-sectional

differences in conditional conservatism is highly likely to have given rise to invalid

conclusions about the role of accounting conservatism in capital markets. In conclusion

to this chapter, I find that a large number of prior studies that model cross-sectional

variations in conditional conservatism using the AT measure needs to be revised in light

of the VR measure.

Overall, the three empirical studies in this thesis contribute to the market-based

accounting research literature by improving our understanding of how financial

reporting affects the information gap between insiders and outsiders in capital markets.

13

References:

Akerlof, G. (1970). The Market for "Lemons": Quality Uncertainty and the

Market Mechanism. The Quarterly Journal of Economics, 84(3), 488–500.

Balakrishnan, K., Watts, R., & Zuo, L. (2016). The effect of accounting conservatism on

corporate investment during the Global Financial Crisis. Journal of Business Finance

& Accounting, 43(5–6), 513–542.

Basu, S. (1997). The conservatism principle and the asymmetric timeliness of earnings.

Journal of Accounting and Economics, 24(1), 3–37.

Biais, B., Glosten, L., & Spatt, C. (2005). Market microstructure: A survey of

microfoundations, empirical results, and policy implications. Journal of Financial

Markets, 8(2), 217–264.

Dietrich, D., Muller, K., & Riedl, E. (2007). Asymmetric timeliness tests of accounting

conservatism. Review of Accounting Studies, 12(1), 95–124.

Dutta, S., & Patatoukas, P. (2017). Identifying conditional conservatism in financial

accounting data: theory and evidence. The Accounting Review, Forthcoming.

Healy, P., & Palepu, K. (2001). Information asymmetry, corporate disclosure, and the

capital markets: A review of the empirical disclosure literature. Journal of Accounting

and Economics, 31(1), 405–440.

Khan, M., & Watts, R. (2009). Estimation and empirical properties of a firm-year measure

of accounting conservatism. Journal of Accounting and Economics, 48(2–3), 132–

150.

Mora, A., & Walker, M. (2015). The implications of research on accounting conservatism

for accounting standard setting. Accounting and Business Research, 45(5), 620–650.

Myers, S., & Majluf, N. (1984). Corporate financing and investment decisions when firms

have information that investors do not have’. Journal of Financial Economics, 12,

187–221.

Patatoukas, P., & Thomas, J. (2011). More Evidence of Bias in the Differential Timeliness

Measure of Conditional Conservatism. The Accounting Review, 86(5), 1765–1793.

Patatoukas, P., & Thomas, J. (2016). Placebo tests of conditional conservatism. The

Accounting Review, 91(2), 625–648.

Ryan, S. (2008). Accounting in and for the Subprime Crisis. The Accounting Review,

83(6), 1605–1638.

Scott, W. (2015). Financial Accounting Theory (7th ed.). Pearson.

Teoh, S. H., Welch, I., & Wong, T. J. (1998). Earnings management and the

underperformance of seasoned equity offerings. Journal of Financial Economics,

50(1), 63–99.

14

Chapter 2

Does Changing Accounting Standards Affect Dividend Policy?

ABSTRACT: This study explores the impact of the mandatory adoption of International

Financial Reporting Standards (IFRS) on dividend payout policy and the value relevance

of dividends in two of the largest Western European economies. We1 select the United

Kingdom as a major common-law country and France as a code-law country. These two

countries are highly comparable economically, which allows us to implement a difference-

in-differences methodology. The genesis of our theoretical argument is that IFRS adoption

is expected to mitigate information asymmetry, a major reason behind corporate

underinvestment and cash over-retention (Myers & Majluf, 1984). Our findings thus

suggest that IFRS adoption is a major contributor in increasing dividend payouts among

code-law firms through enhancing the corporate financial information environment and

reducing asymmetric information. The reduction in information asymmetry helps investors

become more confident about using accounting measures in assessing firm financial

performance, which causes a significant reduction in dividend value relevance among

code-law firms. On the other hand, common-law firms witness no significant change in

dividend payouts and a lower reduction in dividend value relevance relative to code-law

firms.

Keywords: Information Shocks; IFRS; Dividend Payout; Dividend Value Relevance.

1 I use “we” hereafter because the three essays (chapters 2, 3 and 4) are co-authored with my supervisors,

Prof. Martin Walker and Prof. Edward Lee.

15

2.1. Introduction

Publicly listed companies in the European Union were required to report their financial

statements in compliance with the International Financial Reporting Standards (IFRS) as of

the beginning of January 2005 (European Union, 2002). The purpose of this paper is to

examine the effect of the introduction of IFRS on dividend payout policy and dividend value

relevance. Specifically, we study the change in the level of dividend payout and the change in

dividend value relevance following IFRS adoption, after controlling for the differences in

accounting and legal systems between the selected control and treatment group.

Hail, Tahoun, & Wang (2014) use an international sample in testing the effect of IFRS on

dividend policy. They find that IFRS adoption decreases dividend payouts because it mitigates

information asymmetry and consequently mitigates the problem of free cash flow (Jensen,

1986). We believe that their results are over generalized due to their non-comparable control

and treatment groups. We select two comparable countries in Western Europe (the United

Kingdom and France) with different legal and accounting systems.2 Our sample selection

criterion enables a geographic regression discontinuity research design, where the geographic

boundaries assign firms into treatment and control groups (Keele, Titiunik, & Zubizarreta,

2015). In our setting, the geographic boundary splits the two groups based on their distinctive

accounting and legal systems. Specifically, the UK is a common-law country with an

accounting system similar to IFRS (Ball, Kothari, & Robin, 2000), while France is a code-law

country with an accounting system that differs materially from a common-law based

accounting system (Joos & Lang, 1994). In contrast to Hail et al. (2014), we find that IFRS

adoption increases dividend payouts in the code-law country relative to the common-law

2 We provide a detailed explanation for the sample selection in section 3.5.

16

country due to the improved information environment relating to assets in place (Myers &

Majluf, 1984).

In general, the accounting and finance literature concludes that the introduction of IFRS has

been broadly beneficial (see the surveys by Ball, Li, & Shivakumar, 2015; Brüggemann, Hitz,

& Sellhorn, 2013; Singleton-Green, 2015). The present paper contributes further evidence on

the effects of IFRS by focusing specifically on the possibility that IFRS may have served to

reduce information asymmetry in situations where asymmetry was relatively high. We

compare France with the UK because these two economies are similar in terms of political

institutions, industrial composition, size, and enforcement of accounting standards. In

addition, our focus on mandatory adoption in two very similar economies with different

accounting standards pre-IFRS helps mitigate potential issues of selection bias and omitted

correlated variables in voluntary adoption studies (Leuz & Wysocki, 2016). This makes

implementing a difference-in-differences research design a feasible identification strategy,

after ensuring the high comparability between the treatment and the control groups. This

allows us to observe whether the effect of IFRS depends on the nature of the accounting

system prior to IFRS implementation.

We focus on the level of dividend payout and on dividend value relevance because prior

theory and empirical findings suggest that these variables are driven by information

asymmetry relating to assets in place (Hand & Landsman, 2005; Myers & Majluf, 1984;

William Rees, 1997). In this paper we argue that a potentially important feature of IFRS is that

it serves to reduce the level of information asymmetry relating to assets in place. We anticipate

that the reduction in asymmetric information would make external financing less costly and,

consequently, encourages managers to pay more dividends. Moreover, as a result of the

improved information environment, investors would rely more on accounting measures, rather

than on dividends, in assessing firms’ financial performance. Thus, we anticipate a significant

17

reduction in dividend value relevance under IFRS. We expect the reduction in information

asymmetry to be greater for the economy which has the greater difference between its pre-

IFRS financial reporting system and the IFRS reporting system, i.e., the code-law country.

First, we examine the difference in the change in the dividend payout level between

common-law and code-law firms. Then we test the difference in the change in the dividend

payout level between high- and low-accounting quality firms in the code-law country, where

lower accounting quality firms are expected to be more affected by IFRS. Finally, we examine

the change in the value relevance of dividends. We believe that this triangulation strategy

gives more credibility and reliability to our study.

Consistent with our hypotheses, our findings suggest that IFRS adoption had a significantly

larger effect on code-law firms than on common-law firms. The level of dividend payouts

increases in the code-law country. This increase in dividend payouts is more significant for

code-law firms who had a lower accounting quality prior to IFRS, compared to code-law firms

who had a higher accounting quality. In addition, we find that the reduction in the level of

information asymmetry and the enhancement in the financial reporting environment improve

investors’ confidence in accounting numbers. This results in a significant reduction in the

value relevance of dividends among the treatment firms relative to the control firms.

The remainder of the paper is structured as follows: section 2.2 provides the motivation and

literature review; section 2.3 includes hypotheses development; section 2.4 discusses the

research design; section 2.5 describes the data sample; section 2.6 discusses the results; and

section 2.7 concludes the study.

18

2.2. Motivation & Literature Review

2.2.1. IFRS, Legal Systems and Accounting Quality

In 2005, the European Union (EU) imposed IFRS as obligatory reporting standards on

publicly listed companies in all countries that fall under its authority (European Union, 2002).3

IASB’s initial objectives were to develop a set of global accounting standards that are relevant

to economic decisions made by capital market participants (Choi, Peasnell, & Toniato, 2013;

Pope & McLeay, 2011). In a recent survey on IFRS adoption, De George, Li, & Shivakumar

(2016) discuss the differences between the code-law and the common-law financial reporting

systems. They show how crucial it is to differentiate between legal systems when studying the

effect of IFRS adoption across countries because IFRS are developed in the spirit of the

common-law system (Ball et al., 2000). To be more specific, the demand for financial

reporting is higher in common-law countries because firms are more financially dependent on

capital markets, whereas firms in code-law countries are mainly reliant on banks for raising

money. Accordingly, relying on capital markets in raising funds requires firms to maintain

transparent and decision-relevant financial statements. In addition, the common-law financial

reporting system tends to be less regulated by laws than the code-law financial reporting

system. In code-law countries, accounting regulations are incorporated in national laws. On

the other hand, national laws in common-law countries are less detailed regarding financial

reporting, which allows managerial judgment and permits accounting standards to play a

major role in financial reporting. Similar to the common-law financial reporting system, IFRS

are principles-based accounting standards that specify more general rules, where firms are

responsible for presenting credible financial statements. Finally, on top of that, firms in code-

3 Some publicly listed companies were exempted from reporting under IFRS. For example, Alternative

Investment Market (AIM) companies were not required to adopt IFRS in the UK until 2007.

19

law countries resolve information asymmetry conflicts through private communication;

however, firms in common-law countries use public disclosure in resolving such conflicts.4

In light of the aforementioned points, we expect a minor change in the financial reporting

system in the common-law country following IFRS adoption. On the other hand, the code-law

country is expected to experience a more substantial change in the financial reporting system

after adopting IFRS (Armstrong, Barth, Jagolinzer, & Riedl, 2010; Barth, Landsman, Lang, &

Williams, 2012).

Another determinant of the effectiveness of IFRS adoption is the enforcement of these

standards (Leuz & Wysocki, 2016). IFRS might enhance accounting quality given that it is

accompanied with a rigid enforcement and a robust institutional infrastructure (Hail & Leuz,

2006). Christensen, Hail, & Leuz (2013) find that European countries that have improved their

accounting enforcement have experienced a greater effect for IFRS on their capital markets.

Thus, it is important for our study to make sure that the improvement in the financial reporting

environment in the code-law country, following IFRS adoption, is not due to a change in the

enforcement of accounting standards. Prior studies document that the enforcement of laws and

the institutional infrastructure are similar in the UK and France (La Porta, Lopez-De-Silanes,

Shleifer, & Vishny, 1998). Yet, Brown, Preiato, & Tarca (2014) argue that using legal systems

as a proxy for measuring the enforcement of accounting standards is general rather than

specific to financial accounting. Specifically, the authors argue that accounting standards

would not promote the supply of sufficient financial information without a regulatory

intervention. For instance, the experience of the Security and Exchange Commission (SEC) in

the US points out that juristic penalties and adverse stock price reaction form the main

incentives for firms’ compliance with accounting standards (Dechow, Sloan, & Sweeney,

4 For example, Gajewski & Quéré (2013) find that earnings announcements in France do not significantly reduce

information asymmetry compared to earnings announcements in the U.S.

20

1996). This motivates the importance of independent enforcement bodies (by governments or

private institutions) since their existence is essential for achieving high quality financial

reporting (SEC, 2002). Accordingly, we must consider any changes in the enforcement of

accounting standards in the UK and France around IFRS.

Brown et al. (2014) construct a comprehensive index that measures the enforcement of

accounting standards in 51 countries before, during, and after IFRS adoption.5 Their index of

enforcement of accounting standards in France shows a score of 19 in 2002, 19 in 2005, and

16 in 2008. This shows that the enforcement of accounting standards in France stayed stable

before and around IFRS adoption, and then it fell slightly after IFRS adoption in 2008.6 The

same index in the UK shows a score of 14 in 2002, 22 in 2005, and 22 in 2008. This slight

increase in the enforcement of accounting standards in the UK around IFRS would have a

counter effect on our findings, if present. Therefore, we rule out the possibility that changes in

the enforcement of accounting standards in both countries might drive the obtained results.

This facilitates the implementation of the difference-in-differences methodology because the

only changing factor in this case is accounting standards.

Generally, the financial accounting literature documents that accounting standards directly

affect information asymmetry through determining the quality of financial reporting and

disclosure (Armstrong et al., 2010; Ball, 2008; Barth, Landsman, & Lang, 2008; Charitou,

Karamanou, & Lambertides, 2015; Daske, Hail, Leuz, & Verdi, 2008; Leuz & Verrecchia,

2000; Leuz & Wysocki, 2016; Muller, Riedl, & Sellhorn, 2011; Panaretou, Shackleton, &

Taylor, 2013; Ramalingegowda, Wang, & Yu, 2013; Wang & Welker, 2011). Brüggemann et

al. (2013) argue that financial reporting under IFRS should produce positive economic

5 The index constructed by Brown et al. (2014) consists of an ‘auditing’ index and an ‘enforcement’ index. We

are particularly interested in the enforcement of accounting standards index. The maximum score for the

aforementioned index is ‘24’ and it is measured in 2002, 2005 and 2008. 6 This decrease of the enforcement index in 2008 might be due to the global financial crisis. We run all the

regressions while excluding year 2008 from the sample period and the results persist.

21

consequences for investors through providing enhanced transparency and comparability. Leuz

& Verrecchia (2000) and Leuz & Wysocki (2016) conclude that International Accounting

Standards (represented by IFRS) are able to decrease adverse selection among investors

through imposing an increased level of accounting disclosure on adopting firms. Their

analyses show that this increased disclosure reduces the cost of capital among firms.

Therefore, we treat IFRS as a positive shock to the corporate financial reporting environment

(Hail et al., 2014).

2.2.2. Dividend Payout Policy and the Information Environment

The relationship between IFRS adoption and dividend payout policy is characterized by the

change in the level of information asymmetry (DeAngelo, DeAngelo, & Skinner, 2008). In

their survey of the corporate payout policy literature, DeAngelo et al. (2008) propose a

theoretical framework which develops the pioneering theory of Miller & Modigliani (1961) in

determining the optimal payout policy through introducing information asymmetry in light of

Myers & Majluf (1984) and Jensen (1986). Miller & Modigliani (1961) theorize that dividend

payout policy is irrelevant under certain assumptions.7 However, these assumptions do not

hold in a corporate world that suffers from asymmetric information. This suggests that the

dividend payout policy is a relevant financial decision to the firm under information

asymmetry. The surveys by Allen & Michaely (2003) and DeAngelo et al. (2008) document

that the finance literature selects information asymmetry as a major factor in determining the

behavior of dividend policy.

In the presence of asymmetric information, the firm might experience corporate

underinvestment, especially when the firm is reliant on external financing (Myers & Majluf,

1984). The possibility of underinvestment comes from the ‘lemons problem’. This problem

7 The assumptions that support Miller and Modigliani (1961) are: (a) no friction costs and no taxes, (b) investors

are rational and securities are fairly priced, and (c) firms are price takers and not price makers and all investors

are equally informed.

22

occurs when the firm issues new equity or new debt and investors undervalue equity or

overprice debt due to high uncertainty. The framework of Myers & Majluf (1984) suggests

that the higher the level of information asymmetry relating to assets in place, the higher the

likelihood of underinvestment. The authors argue that the firm may limit the underinvestment

problem through increasing cash retention, which means a lower dividend payout. Thus, a

higher level of asymmetric information leads to a lower dividend payout in order to lessen the

underinvestment problem.

We build on the theory of Myers & Majluf (1984) and argue that we expect dividend

payouts to increase after the adoption of IFRS due to the improved information environment

induced by the new reporting regime, after ruling out the argument of the improved

enforcement of accounting standards in section 2.2.1. Less asymmetric information enables

investors to better evaluate assets in place and growth potential. This encourages managers to

pay dividends because a reduction in asymmetric information is expected to decrease the

likelihood of encountering underinvestment problems.

2.2.3. Dividend Value Relevance and the Information Environment

Under perfectly symmetric information, dividends should be irrelevant in determining the

market value of the firm (Miller & Modigliani, 1961). However, when insiders possess more

valuable information than outsiders, dividends become value relevant as they convey signals

about the firm’s future (Bhattacharya, 1979; Miller & Rock, 1985). Fama & French (1998)

provide evidence suggesting that, under information asymmetry, dividends are highly value

relevant and have a positive effect on the market value of the firm. Rees (1997) argues that,

under information asymmetry, the positive significant association between dividends and

market value is attributed to the role of dividends in conveying credible information relating

the firm’s future. This information-carrying role of dividends is more prominent when

23

earnings quality is low (Rees, 2005). Hand & Landsman (2005) use the Ohlson (1995) model

in order to test four explanations for the high value relevance of dividends. They propose four

possible explanations for the positive pricing of dividends: (1) dividends proxy for public

information that help predict future earnings, (2) managers use dividends as a signaling tool

for their private information, (3) managers pay dividends in order to signal their good

intentions about maximizing shareholders value, and (4) dividends are positively priced

because of analysts’ mis-forecasting or investors’ mispricing of earnings and book equity.

Their results are mostly consistent with the fourth proposition. After controlling for one-year-

ahead analysts’ forecast errors, Hand and Landsman (2005) rule out the possibility of analysts’

mis-forecasting. Thus, they conclude that the positive value relevance of dividends is caused

by investors’ mispricing of current earnings and book equity. We exploit the information

shock caused by IFRS, which is expected to decrease information asymmetry and improve

financial reporting, in order to argue that investors are more willing to rely on accounting

measures of financial performance post-IFRS. This is expected to reduce the value relevance

of dividends, especially where IFRS have a higher impact.

2.3. Hypothesis Development

In our setting, the common-law accounting system (i.e., UK GAAP) does not materially differ

from IFRS (Ball et al., 2000). However, the code-law accounting system (i.e., French GAAP)

differs materially from IFRS in several aspects (Hong, Hung, & Lobo, 2014; Joos & Lang,

1994; Kaufmann, Kraay, & Mastruzzi, 2007; Soderstrom & Sun, 2007). Specifically,

accounting standards in common-law countries are set by private organizations (FASB in the

US and IASB in the UK) and not by governments. The rationale for setting accounting

standards in common-law countries is derived from the information demands of investors;

therefore, the purpose of standard setters in these countries is to satisfy the information needs

24

of investors (Soderstrom & Sun, 2007). On the other hand, accounting standards in code-law

countries are a part of commercial laws, set by governments and instituted by courts.

Accounting standards in code-law countries are influenced and developed by governments,

according to governments’ priorities and not directly related to investors’ needs (Ball et al.,

2000). Given that IFRS are developed to provide investors with the relevant information for

making economic decisions (Brüggemann et al., 2013; Pope & McLeay, 2011), we expect a

greater improvement in the financial reporting environment in the code-law country than in

the common-law country following IFRS adoption.

The UK and France are both developed countries with good implementation of laws

(Kaufmann et al., 2007), which proxy for the enforcement of accounting standards. Yet, a

viable argument might be that the improvement in the financial reporting environment in

France after IFRS adoption might be due to a stricter enforcement of accounting standards. As

described in section 2.2.1, the enforcement of accounting standards did not improve in France

after IFRS adoption (Brown et al., 2014). This means that the financial reporting environment

did not improve because of the improvement in the enforcement of accounting standards, but

it improved due to imposing a set of a higher quality accounting standards. In addition, Brown

et al.'s (2014) index of accounting standards’ enforcement show a score of 19 for France and a

score of 22 for the UK (out of 24) in 2005; therefore, IFRS are properly enforced in both

countries, which increases the comparability of the selected countries.

After explaining the assumptions relating to accounting standards and legal systems,8 we

hypothesize that code-law firms might increase their dividend payouts as a result of the

reduction in asymmetric information following IFRS adoption (DeAngelo et al., 2008; Myers

8 The first assumption is that the accounting standards in code-law countries differ significantly from IFRS

whereas the accounting standards in common-law countries are similar to IFRS. The second assumption is that

the enforcement of accounting standards did not improve in France after the adoption of IFRS and, therefore, the

differences in accounting quality are due to the change in accounting standards and not to the change in the

enforcement of these standards.

25

& Majluf, 1984). When financial information becomes less asymmetric, firms will be able to

finance their investments more easily through issuing public debt and/or new equity. Under

high financial reporting quality, uncertainty is lessened and, consequently, issued bonds and

shares are expected to be more fairly priced (a lower interest rate for bonds and a better market

reaction for shares). As such, managers of code-law firms will have no need to maintain a

strict cash retention policy and, thus, will be able to pay more dividends.

Hypothesis (1):

H1: Following IFRS, there is a greater increase in the average dividend payout among code-

law firms than among common-law firms.

If IFRS are expected to improve the financial reporting environment where accounting

quality is relatively low, then firms with lower accounting quality are expected to be more

affected by IFRS than those with higher accounting quality. Given that we expect IFRS to

induce a greater change in accounting quality among code-law firms, we also believe that

IFRS will have a greater influence on code-law firms with lower accounting quality. That is,

we predict that the level of dividend payout will increase among code-law firms with low

accounting quality more than it will among code-law firms with high accounting quality.

Hypothesis (2):

H2: IFRS adoption affects the average dividend payout for low accounting quality firms more

significantly than it does for high accounting quality firms in the code-law country.

When the quality of reported earnings and book value of equity is low, the value relevance

of dividends is expected to be high because it provides a source of information to investors

26

(Rees, 2005). In this case, dividends will have a higher impact on the market value of the firm.

Rees & Valentincic (2013) study the association between the market value of equity and

dividends. They find a strong association between market value and dividends among UK

firms. They explain their findings by reference to the study of Clubb (2013) who concludes

that dividends exert a strong positive effect on market value from their role as a proxy for

financial expectations. In the same vein, Hand and Landsman (2005) conclude that dividends

are value relevant because investors are unwilling to rely entirely on accounting numbers and,

therefore, place some weight on dividends as an alternative proxy for financial expectations.

Another source for financial expectations is analysts’ forecasts. Choi et al. (2013) find that

forecasted earnings become less value relevant under IFRS whereas reported earnings become

more value relevant to investors. This suggests that IFRS were successful in improving the

decision usefulness of reported numbers through reducing information asymmetry.

We hypothesize that investors become more confident about using accounting measures in

assessing the financial performance of the firm after IFRS adoption in code law countries.

This is due to lower information asymmetry and enhanced financial reporting. As a result,

dividends are expected to lose some of their signaling power and convey less information (i.e.,

become less value relevant).

Hypothesis (3):

H3: Dividend value relevance decreases by a significantly greater magnitude among code-law

firms than it does among common-law firms.

27

2.4. Research Methodology

We test our hypotheses using a difference-in-differences research design. The common-law

sample (UK firms) serves as the control group and the code-law sample (French firms) serves

as the treatment group. A detailed discussion of sample selection is available in section 2.5.

The sample period starts in 2001 and ends in 2008 (Hail et al., 2014).9 We argue that IFRS

adoption serves as a proxy for the change in the level of information asymmetry because it is a

positive exogenous information shock to the information environment (Florou & Kosi, 2015).

We denote the IFRS adoption period using the dummy variable POST that takes the value 1 if

the year is 2005 or beyond, and 0 otherwise. It is important to point out that we do not claim

that IFRS is the only driving factor to our findings; however, we develop a research design

and perform additional tests which make us confident of attributing our findings to the change

in the information environment following IFRS adoption (after showing that the enforcement

of accounting standards did not improve in the code-law country).

Finally, we differentiate the code-law sample from the common-law sample using the

dummy variable CODE that takes the value 1 if the firm is listed in France (i.e. treated firm),

and 0 otherwise. We identify the difference-in-differences estimator as the interaction of

POST and CODE. The variable POST*CODE takes the value 1 if the firm is listed in the code-

law country between 2005 and 2008, and 0 otherwise.

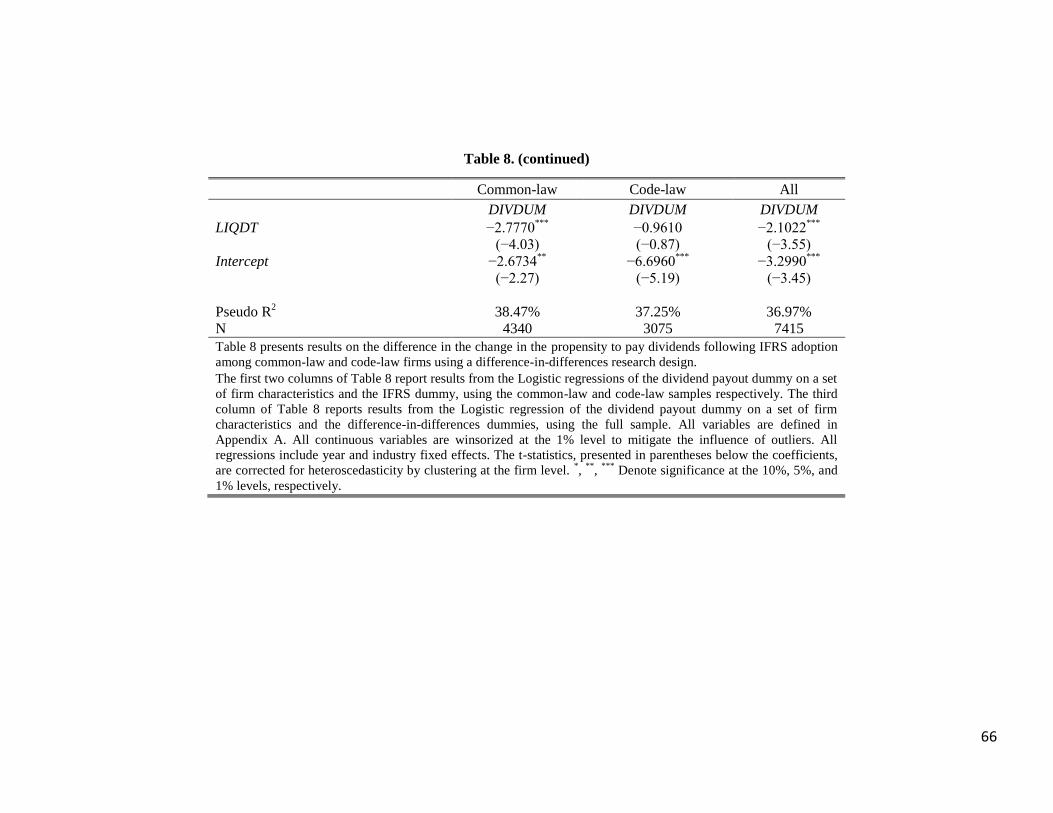

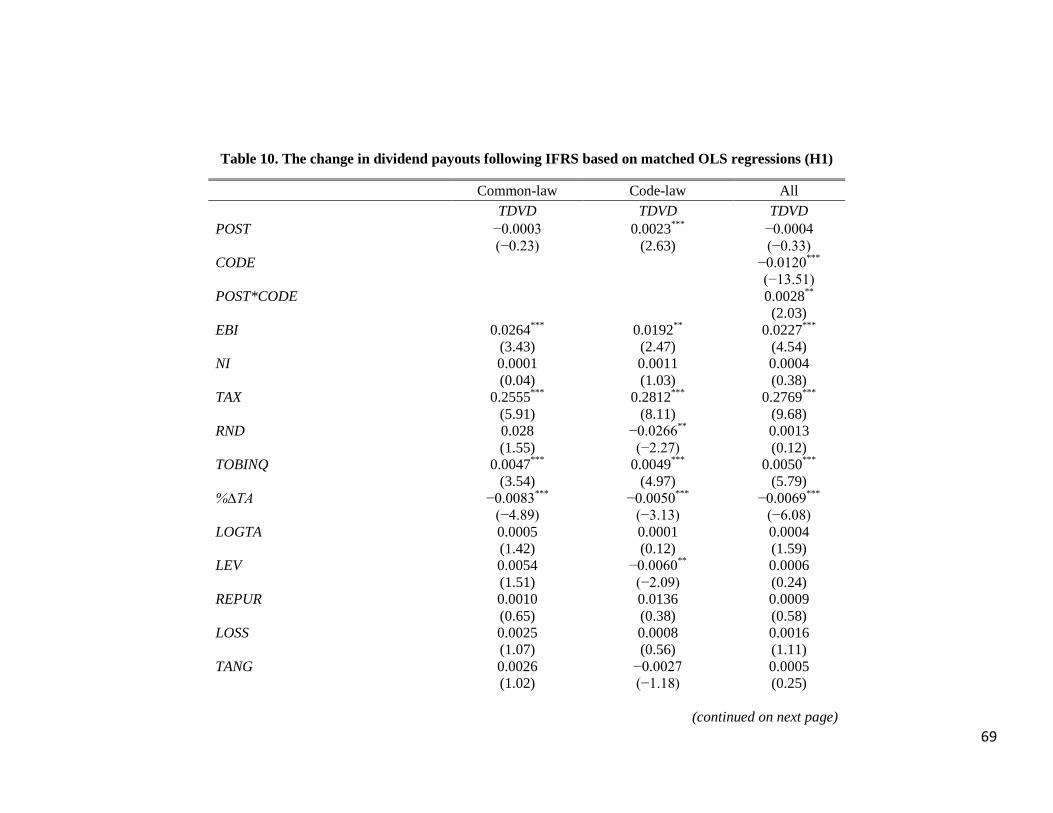

2.4.1. Dividend Payout Regression Model

In order to model the behavior of dividend payouts, we mainly follow (Fama & French

2001;2002) in modelling dividends. Their model includes four economic characteristics of the

9 As a robustness check, we run the regressions after excluding year 2008, the beginning of the world financial

crisis. In addition, we run the regressions after excluding year 2005 as it is considered a transitionary period with

high level of asymmetric information (Wang and Welker, 2011). The results remain unchanged when excluding

year 2008/2005 from the sample period.

28

firm that determine its dividend payout: profitability, investment opportunities, leverage and

size. These determinants are consistent with the DeAngelo et al. (2008) literature survey.

Denis & Osobov (2008) find that dividend payers tend to be more profitable firms as they

can maintain their dividend payout level whilst keeping some reserve funds for unseen

circumstances. We proxy profitability using three variables: earnings before interest and after

tax (EBI), net income available to common stock holders (NI), and income taxes (TAX).10

Firms with high investment opportunities usually pay fewer dividends because they need to

finance their ongoing projects (Fama & French, 2001). We proxy the firm’s investment

opportunities using three variables: the percentage change in total assets (%∆TA), research and

development expenses (RND), and a proxy for Tobin’s Q using the market-to-book ratio

(TOBINQ).

The level of debt should be taken into consideration since it is one of the obstacles that

delay dividend payments (DeAngelo, DeAngelo, & Stulz, 2006; Eije & Megginson, 2008).

We proxy the level of debt using the variable LEV, the ratio of total liabilities to the average of

total assets in years prior to IFRS.11

A major determinant of dividend payout is the firm’s maturity. DeAngelo et al. (2008) state

that prior literature finds a positive association between the firm’s maturity and dividend

payouts. Fama & French (2001) proxy the firm’s maturity by its size since a more mature firm

is expected to have a bigger size. We measure the firm’s size using the natural logarithm of

total assets (LOGTA).

10

Income taxes proxy profitability because higher taxes are paid by more profitable firms. In addition, Mills,

Nutter, & Schwab (2013) find that firms with higher political cost pay higher taxes, in general, as they experience

higher scrutiny. Therefore, the inclusion of taxes in the model might capture some of the political cost which put

more pressure on firms to pay dividends in order to silence investors. 11

We deflate the variables by the firm’s average of total assets in years 2001, 2002, 2003 and 2004 in order to

isolate the fair value adjustment effect on total assets after IFRS. Yet, our results remain unchanged when

deflating by lagged total assets. An alternative deflator is market value; however, we cannot use market value

because it is the dependent variable in equation (2).

29

Finally, following Ramalingegowda et al. (2013), we add the tangibility ratio TANG, the

liquidity ratio LIQDT, and share repurchases REPUR – an alternative method of distributing

profits to shareholders. All variables are defined in Appendix A.

In the light of these ideas, the initial regression model is given in equation (1) where the

dependent variable TDVD is total dividend payout deflated by to the average of total assets in

years prior to IFRS.

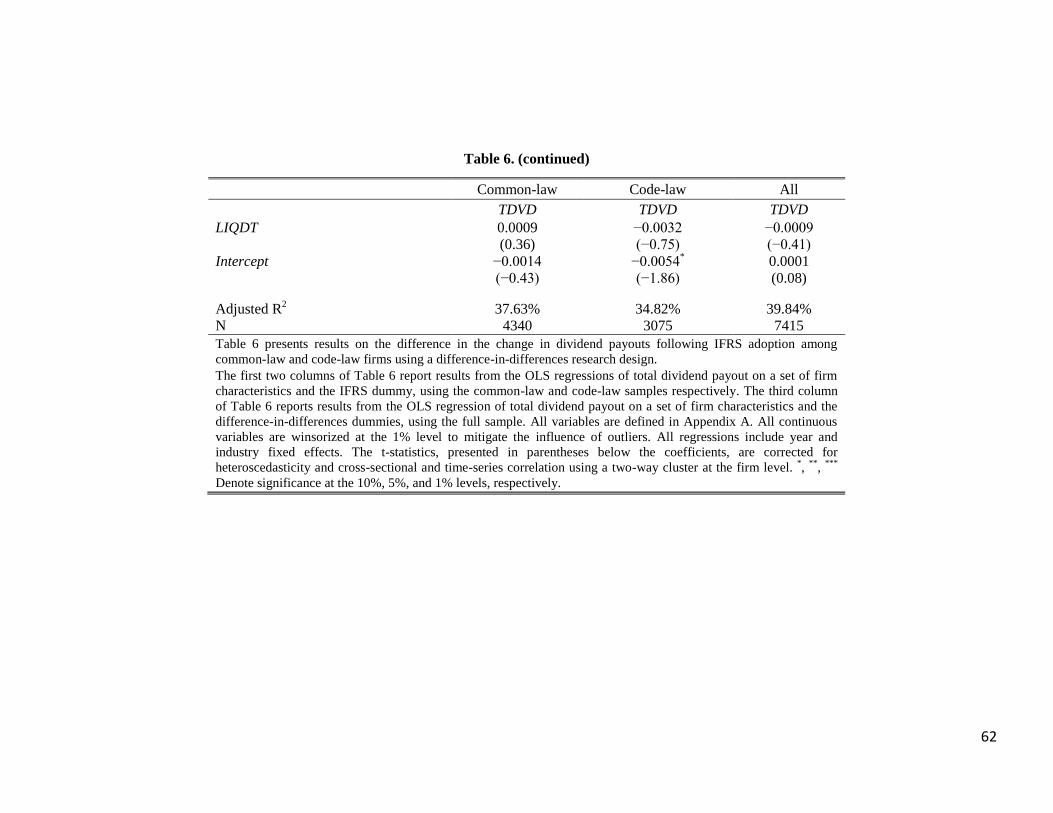

TDVD = α0 + α1 POST + α2 CODE + α3 POST*CODE

+ ∑ αi Controlsi + ∑ αj Year FEj + ∑ αk Industry FEk + ε (1)

The coefficients of interest are α1, α2, and α3. When running this regression equation for

each country separately, we are especially interested in the coefficient on POST. We expect

this coefficient to be insignificant (significantly positive) when using the common-law (code-

law) sample. On the other hand, when running the regression using the full sample, α1 captures

the change in total dividends after IFRS adoption among common-law firms, α2 captures the

difference in the level of dividend payout between both groups prior to IFRS adoption, and α3

captures the difference-in-differences effect (i.e. the difference in the effect of IFRS adoption

on the level of dividend payouts between common-law and code-law firms).

2.4.2. Dividend Payout Regressions among Code-law Firms

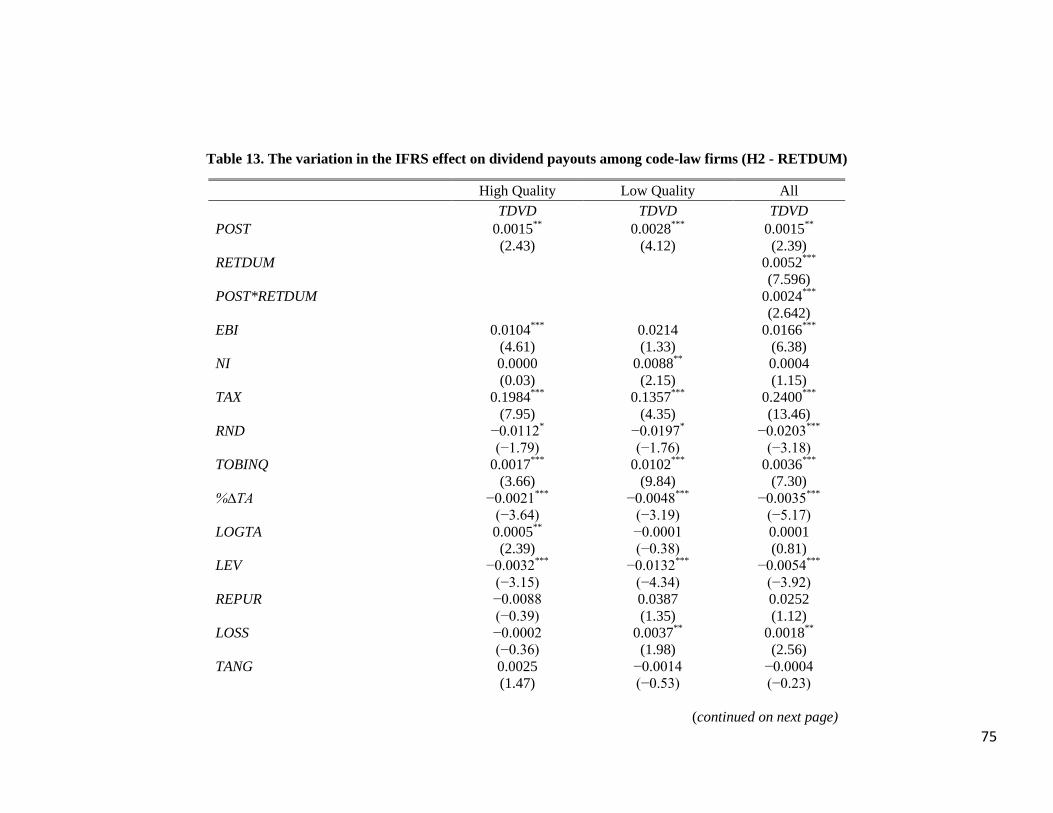

We run the subsample analysis by splitting the code-law sample into two groups: low

accounting quality firms and high accounting quality firms. We use three proxies for

accounting quality in partitioning the code-law sample. All the proxies are calculated in years

prior to IFRS. The first proxy is the average absolute value of discretionary accruals. We

calculate discretionary accruals for the first proxy following Dechow, Sloan, & Sweeney

30

(1995) and we control for idiosyncratic economic shocks following Owens, Wu, &

Zimmerman (2016), as shown in Appendix B.1.12

The dummy variable ACCDUM1 takes the

value 1 if the firm’s average absolute value of discretionary accruals is greater than the median

value of the code-law sample, and 0 otherwise. That is, firms with an average absolute value

of discretionary accruals greater than the median value of the code-law sample are assigned to

the low accounting quality group. With respect to the second proxy for accounting quality, we

calculate discretionary accruals based on the cross-sectional version of the Dechow & Dichev

(2002) model, as shown in Appendix B.2. Then, for each firm, we calculate the variance of

discretionary accruals prior to IFRS adoption, because high volatility of discretionary accruals

implies low accounting quality (Chen, Chin, Wang, & Yao, 2015). The dummy variable

ACCDUM2 takes the value 1 if the variance of the firm’s discretionary accruals is greater than

the median value of the code-law sample, and 0 otherwise. That is, firms with a variance of

discretionary accruals greater than the median variance of the code-law sample are assigned to

the low accounting quality group. Finally, the third proxy for accounting quality is calculated

as the average annualized return volatility of the firm in years prior to IFRS. We calculate the

firm’s annualized return volatility as the annualized variance of daily stock returns. Firms with

highly volatile returns tend to have a lower level of innate earnings quality (Rajgopal &

Venkatachalam, 2011). The dummy variable RETDUM takes the value 1 if the firm’s average

annualized return volatility is greater than the median value of the code-law sample, and 0

otherwise. That is, firms with an average annualized stock volatility greater than the median

value of the code-law sample are assigned to the low accounting quality group.

12

Owens et al. (2016) find that big shifts in unsigned (absolute) abnormal accruals are caused by changes in the

firm’s economics. We follow their study and proxy idiosyncratic economic shocks using the variable ECON, as

defined in Appendix B.1.

31

2.4.3. Dividend Value Relevance Regression Model

In order to model the change in dividend value relevance following IFRS adoption, we use an

accounting-based valuation model that includes a number of variables from various prior

studies. Given that the data sample consists of Western European companies, we mainly

follow Shen & Stark (2013). We also include other variables relevant to the valuation of loss

firms (Darrough & Ye, 2007; Jiang & Stark, 2013). Finally, we add the variable OINFO as a

proxy for other information which cannot be captured in accounting-based models (Ohlson,

1995). This variable is the estimated residuals from year (t-1) regression, as performed in

Akbar & Stark (2003). We deflate both sides of the equation by the average of total assets in

years prior to IFRS. This step requires supressing the constant term and including the

reciprocal of the deflator (1/TA) among the covariates. The definition of the variables in the

regression equation below is given in Appendix A.

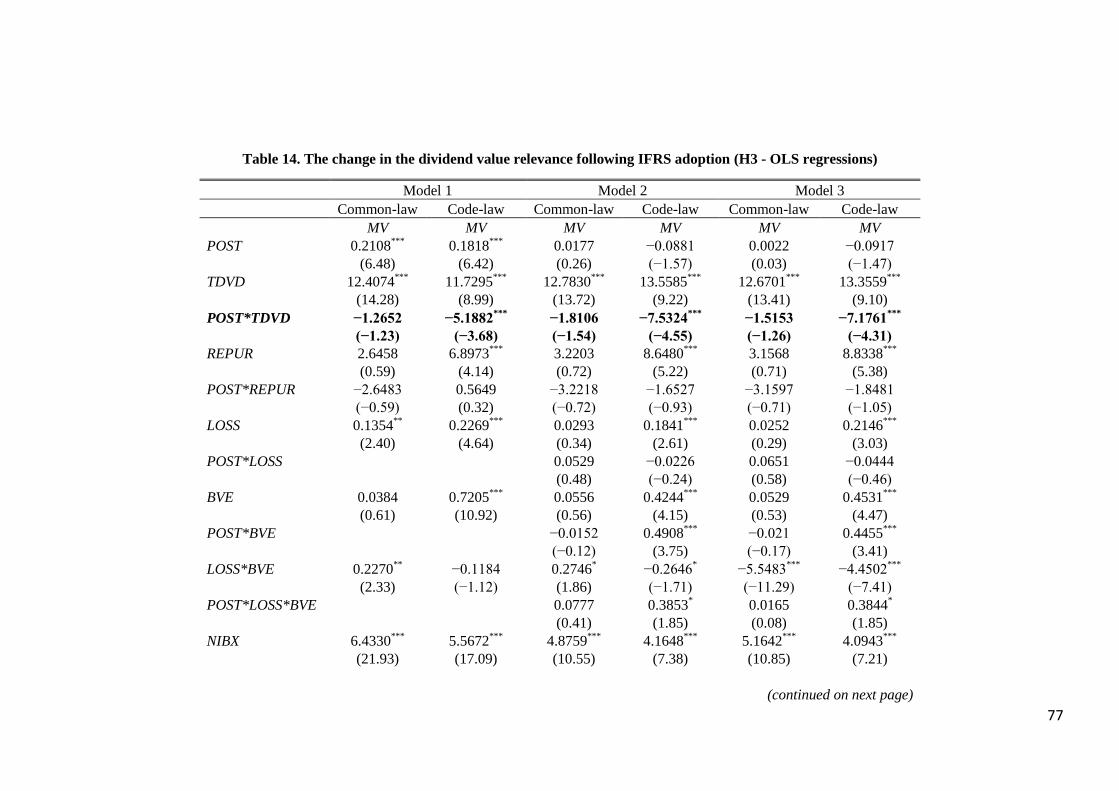

MV = 1/TA + β1 POST + β2TDVD + β3POST*TDVD

+ ∑ βi Controlsi + ∑ βj Year FEj + ∑ βk Industry FEk + ε (2)

The main coefficient of interest in this model is β3, which represents the change in the value

relevance of dividends after IFRS adoption. We run three models/versions of the above

regression equation using both samples (code-law and common-law). We compare the

estimates of β3, for both samples, using the Chi2 statistic. We expect β3 to be more negative for

the code-law sample regression, suggesting that the value relevance of dividends drops more

significantly among code-law firms than among common-law firms following the introduction

of IFRS. We are also interested in the change in the value relevance of accounting measures as

we expect the value relevance of accounting variables to increase after IFRS adoption.

32

2.5. Data & Descriptive Statistics

2.5.1. Sample Construction

As mentioned earlier, we select the UK as a major common-law country and France as a code-

law country in Western Europe. Our sample selection follows a geographic regression

discontinuity research design, where the geographic boundary assigns firms into treatment and

control groups (Keele et al., 2015). In our setting, the geographic boundary partitions both

groups based on accounting and legal systems. We believe that France is a suitable treatment

group because of several characteristics. First, the French economy is very similar in size to

the economy of the UK.13

Second, as discussed in section 2.2.1, the enforcement of accounting

standards around IFRS in France is similar to that in the UK (Brown et al., 2014; Hong et al.,

2014). Third, Enriques & Volpin (2007) compare public firms’ corporate governance and

ownership dispersion in France, Germany and Italy, relative to the UK. They conclude that

France is the most similar country to the UK when it comes to the characteristics of corporate

governance and ownership dispersion in Europe. Finally, our focus on the mandatory adoption

mitigates potential issues of selection bias and omitted variables in voluntary adoption studies

(Ahmed, Chalmers, & Khlif, 2013; Leuz & Wysocki, 2016). Following Hail et al. (2014), the

sample period starts in 2001 and ends by the end of 2008. We avoid extending the sample

period beyond year 2008 because the global financial crisis struck around 2008.14

The data source of financial variables is WorldScope and for stock returns is DataStream.

We apply two sets of sample restrictions. In the first set of restrictions, after we download all

publicly listed companies in the UK and France between 2001 and 2008, we exclude financial

13

The selected countries are highly comparable economically. The GDP growth from 2001 till 2008 in the UK

was 2.7%, 2.5%, 4.3%, 2.5%, 2.8%, 3%, 2.6% and 0.3%. On the other hand, the GDP growth in France during

the same period was 2%, 1.1%, 0.8%, 2.8%, 1.6%, 2.4%, 2.4% and 0.2%. The GDP growth numbers show that

the UK economy was performing similar to the French economy, especially during the adoption period (World

Bank, 2014). This evidence rules out potential critiques arguing that French firms have increased their dividend

payouts because of an economic boost. 14

As mentioned before, our results are robust to excluding the financial crisis year (2008), as well as excluding

the transitionary year (2005), from the sample period.

33

companies, unquoted equities, and unspecified industries. In the second set of restrictions, we

require each firm to have at least one observation in the pre-IFRS period and at least one

observation in the post-IFRS period. Then, we drop all firms with total assets below one

million Euros. Finally, we drop all firms that did not adopt IFRS in 2005.15

The final sample

consists of 673 common-law firms and 476 code-law firms. This is equivalent to 4,340 firm-

year common-law observations and 3,075 firm-year code-law observations.

2.5.2. Descriptive Statistics

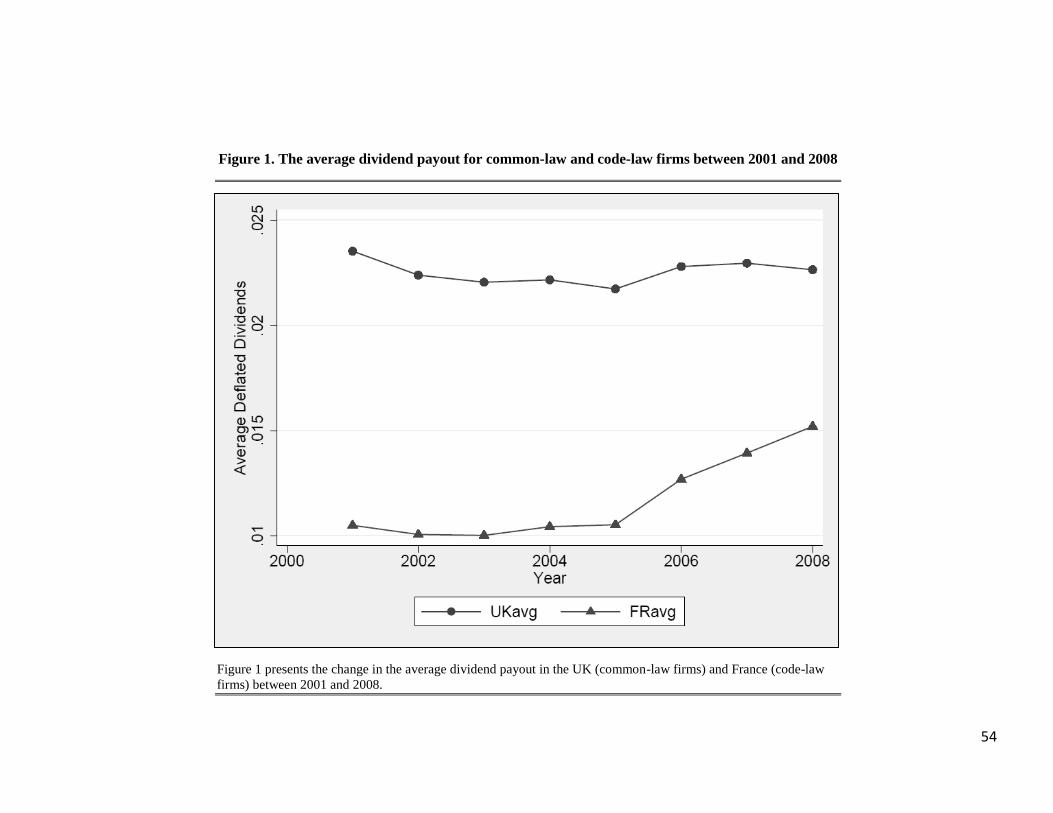

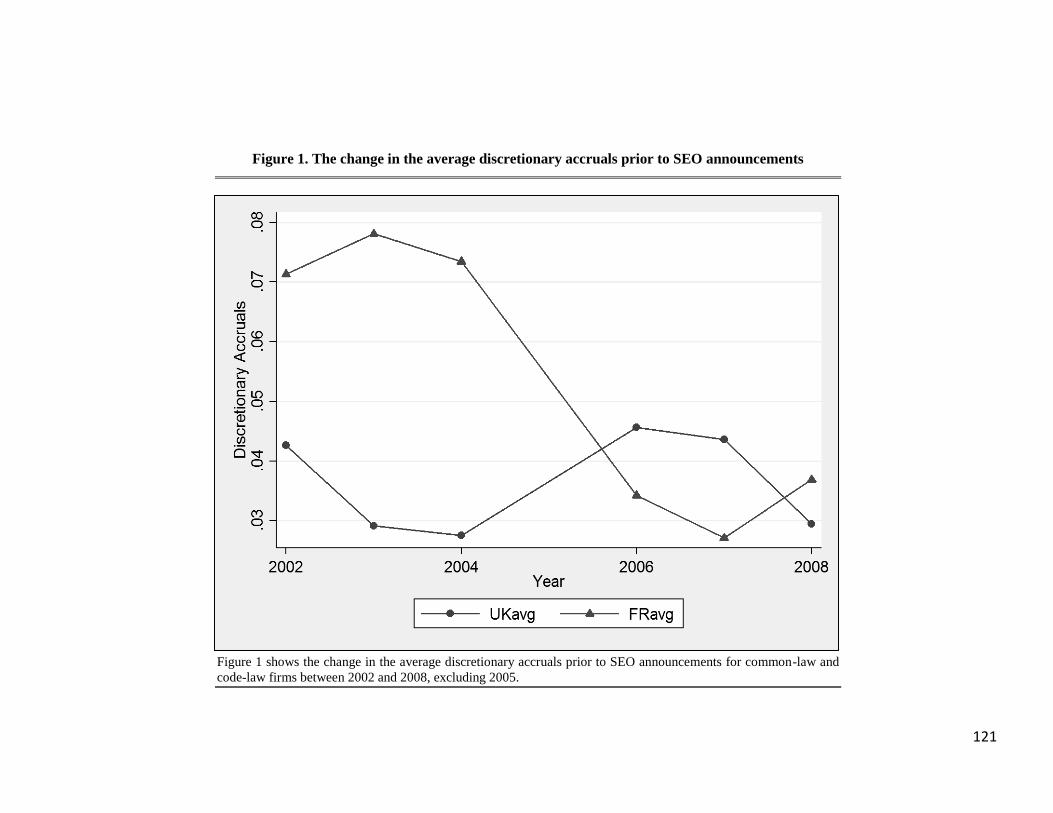

We begin the descriptive statistics with Figure 1 that shows the trend of dividend payouts for

an average common-law firm versus an average code-law firm between 2001 and 2008. The

graph shows how dividend payouts have significantly increased on average after 2005 (IFRS

adoption) among code-law firms. However, no similar change in dividend payouts occurred

among common-law firms.

[Insert Figure 1 Here]

Table 1 reports summary statistics for the variables used in the dividend payout model for

the full sample, the common-law sample and the code-law sample. The percentage of

common-law dividend payers is higher than that of code-law dividend payers (74.84% vs

65.56%). Both groups have very similar ratios for the profitability proxies (EBI, NI and TAX).

Common-law firms have, on average, slightly higher investment and growth opportunities

than code-law firms. This can be deduced from comparing the ratios on investment

opportunity proxies (RND, TOBINQ and %∆TA). The average size of the firm is similar

between both groups; however, the leverage ratio shows that code-law firms are more

15

The name of the variable in DataStream is “Accounting Standards Followed”; Code: WC07536.

34

dependent on debt than common-law firms. Finally, common-law firms repurchase more

stocks and have higher tangibility and liquidity ratios than code-law firms.

[Insert Table 1 here]

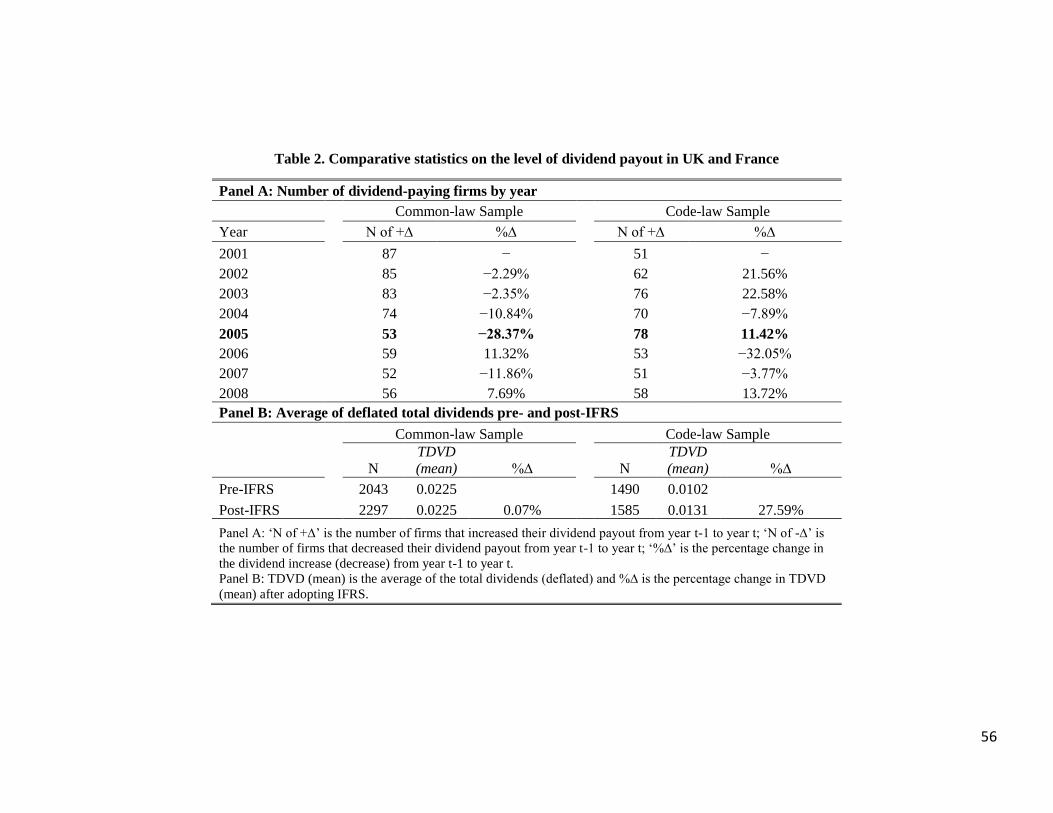

Panel A of Table 2 shows that, in 2005, 78 code-law firms increased their dividend payouts

whereas only 53 firms from the common-law sample increased their payouts. Panel B of Table

2 reports the average dividend payout for each sample before and after IFRS adoption. It

shows that the average dividend payout among code-law firms increases by 27.59% after IFRS

implementation, whereas the same figure increases by 0.07% for common-law firms.

[Insert Table 2 Here]

Finally, Table 3 reports the summary statistics for the variables used in the dividend value

relevance model. On average, common-law firms have a higher market value (MV) than code-

law firms. The summary statistics for the variable BVE show that the financial structure of an

average common-law firm is more reliant on equity than an average code-law firm. The

summary statistics for the variable NIBX show that code-law firms report slightly higher

profits than common-law firms do. This might be due to the higher capital expenditure

(CAPX) and higher research and development expenses (RND) incurred by common-law

firms. Furthermore, common-law firms have on average a greater change in sales over the

years (∆SALES), and this might be one of the reasons why common-law firms are more

solvent (LIQDT) than code-law firms. As for equity movements, the summary statistics show

that common-law firms buy and sell equity more frequently than code-law firms do (REPUR

35

and PROCD, respectively). Finally, as also shown in Table 3, an average common-law firm

pays more dividends than an average code-law firm does.

[Insert Table 3 Here]

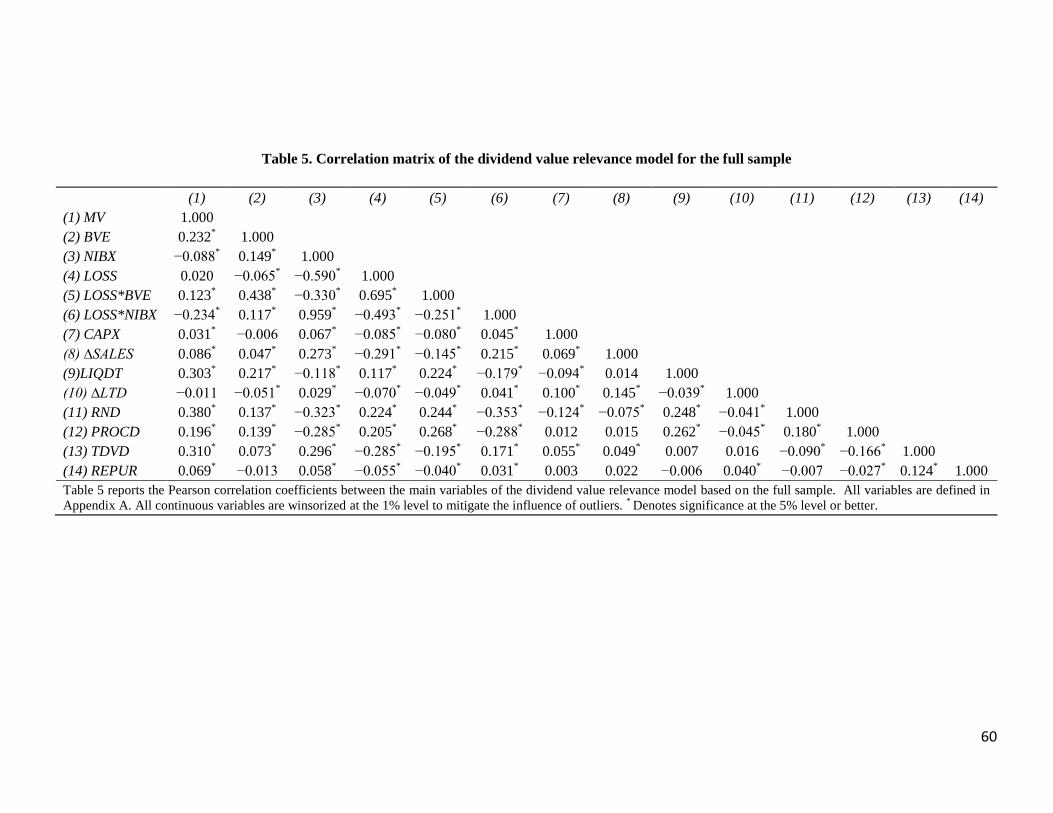

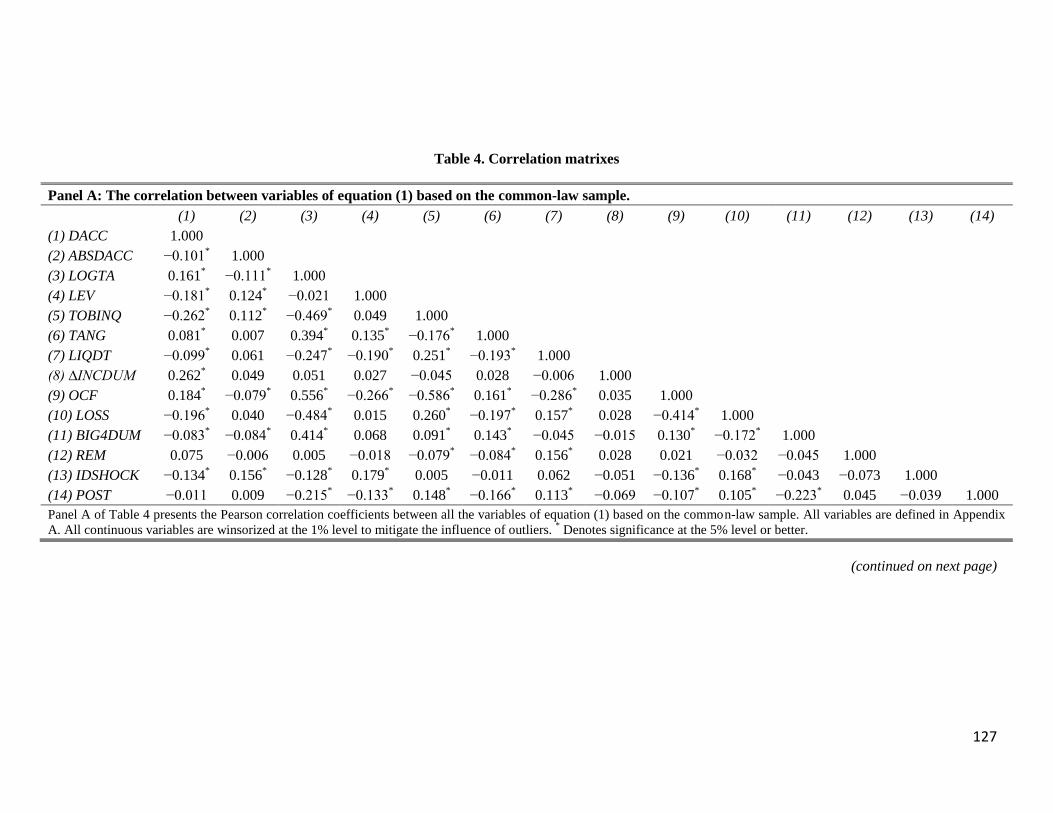

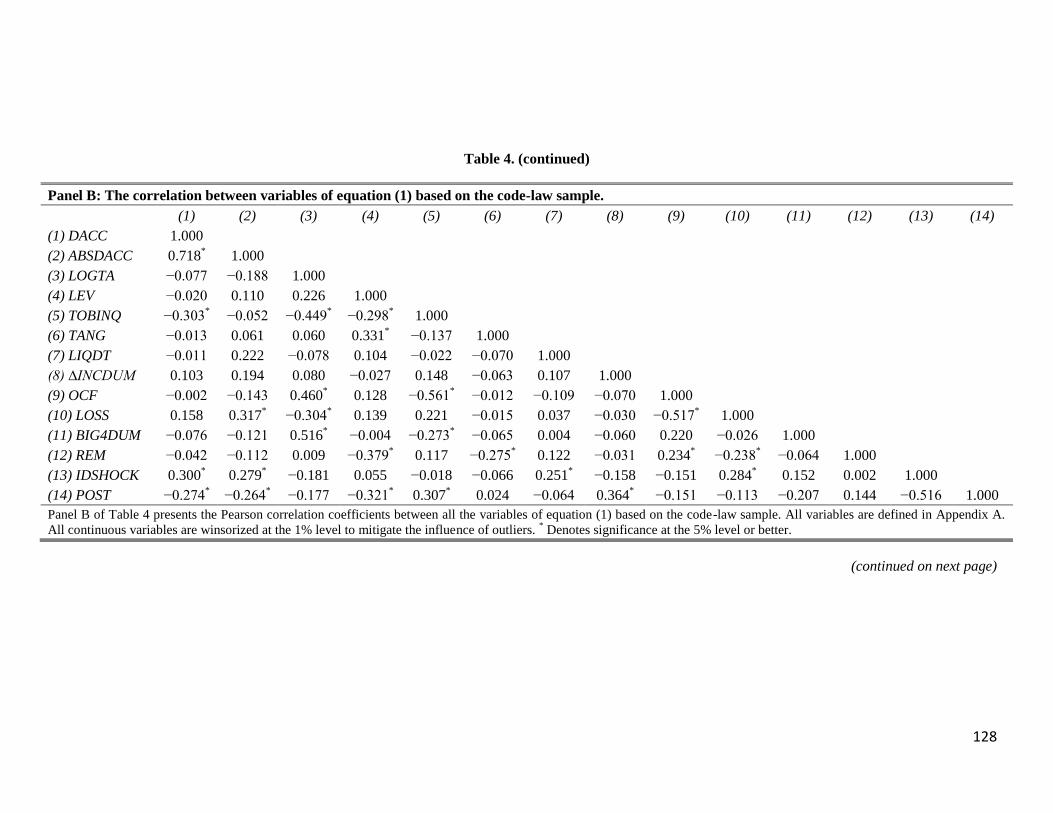

The Pearson correlation coefficients between variables are similar for common-law and

code-law samples; thus, we only report the correlation matrices of the dividend payout model

as well as the dividend value relevance model based on the full sample. The univariate

analysis of the dividend payout model shows that the correlation between the total dividend

payout and the profitability proxies is positive and significant for common-law and code-law

samples. The correlation between the total dividend payout and the investment proxies is

negative and significant, which means that firms with higher investment opportunities pay

fewer dividends. Loss-making firms pay fewer dividends in both samples than profitable

firms. The only notable difference between both samples is that the leverage ratio is positively

correlated with dividend payouts for common-law firms, while the same correlation is

negative for code-law firms. This can be explained by the argument of La Porta, Lopez-de-

Silanes, Shleifer, & Vishny (2000) that firms operating in countries with high investors’

protection (i.e., common-law countries) tend to raise more debt in order to maintain their

dividends.

[Insert Table 4 Here]

Regarding the dividend value relevance model, the univariate analysis shows that the book

value of equity is positively correlated with market value. The correlation coefficient on net

income (NIBX) shows a negative correlation with market value and this is more prominent for

36

loss firms (LOSS*NIBX). Nevertheless, we obtain a significantly positive coefficient when we

test the correlation between the non-deflated market value and non-deflated net income.

Furthermore, the statistics show that capital expenditure, research and development expenses,

change in sales, the liquidity ratio, proceeds, repurchases and dividends are positively

correlated with the market value.

[Insert Table 5 Here]

2.6. Empirical Results

2.6.1. Dividend Payout following IFRS