infineeti january 2014

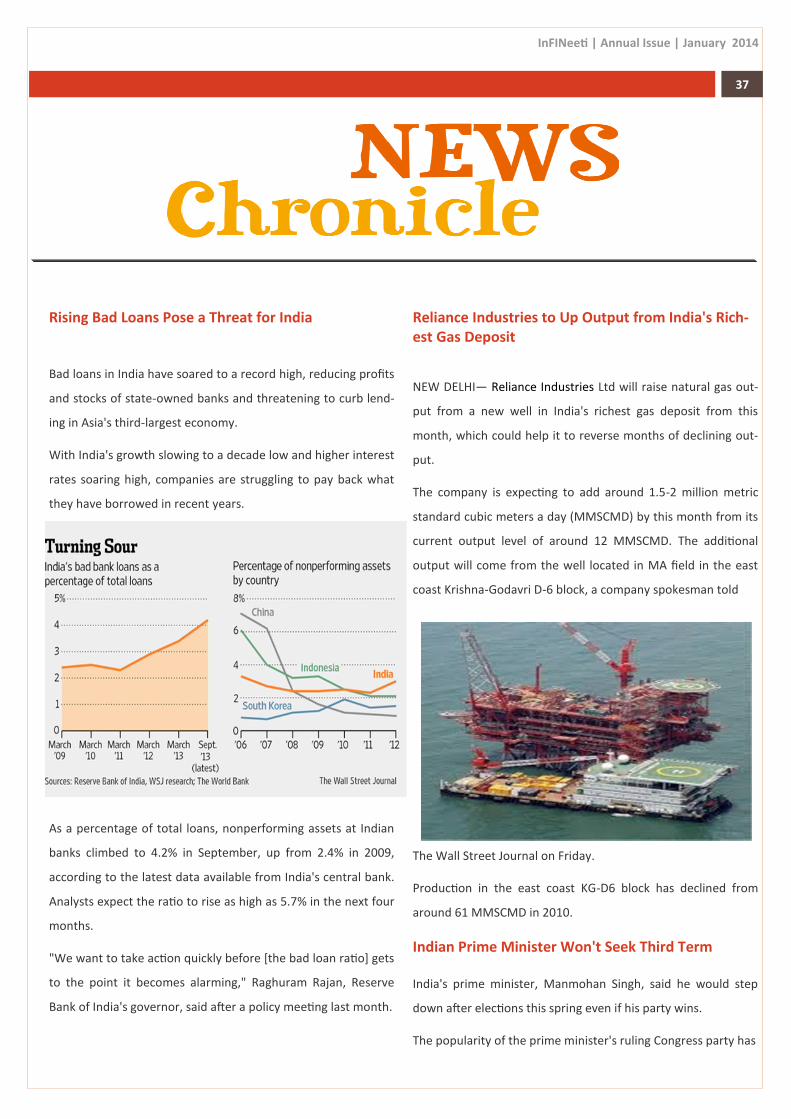

DESCRIPTION

The Quarterly Issue of the Business & Finance Magazine of IIFTTRANSCRIPT

InFINeeti | Annual Issue | January 2014

InFINeeti | Annual Issue | January 2014

InFINeeti | Annual Issue | January 2014

Dear Friends,

Greeting from Team InFINeeti…

Indian economy is going through a tough period. Inflation is high, fuel prices are touching the roofs and the government is f inding

it difficult to meet its fiscal and current account deficit targets. And above all, this being the election year, it is expected that popu-

list measures may triumph over good economic decisions. The Food Security Bill is one such example.

On the international front, the tapering of QE has started and whether it will have a positive or a negative effect- only time will tell.

European economy is still recovering and it can be only hoped that it will only improve from here on and we would see some im-

provement by the end of this year. The same is applicable to the countries falling under the BRICS.

This is an election year in India, and the impending government will have a huge bearing on the Indian economy and the financial

markets. We know that there is loads of money that is spent in the national elections. How these elections are funded is the ques-

tion running on everybody’s mind. Keeping this in mind, we have made election funding as our central theme of this edition and

have looked into the history of how funding has been done previously. We have also proposed numerous solutions as to how the

methods of election fund raising can be improved so as to bring the cost of elections down as well as to bring in more transparency

in the system.

We also saw Sensex touching the 21000 mark last year. We have published an article which deals with the role of instinct and ra-

tionale behind how stock market works. Apart from this, we have articles covering topics such as Basel III norms, QE tapering and

M-banking in India. We also have an article which analyzes the great Indian investment story in some depth.

Besides the insightful articles, the edition also features regular columns like FIN Trivia, FIN-lingos and News Chronicles. Since the

next edition would be the budget edition we have presented few budget related trivia to make it interesting for the edition to fol-

low. We have also included a new column which looks into the top 10 financial happenings of the year.

To add to it, we have two special sections: One being an interview given by a CEO of a renowned Mutual Funds player; and the

other being a guest article written specially for InFINeeti by an analyst working in the premier Consulting Firm.

We are extremely delighted to share with you all that IIFT completed its 50 years of existence this academic year. On this auspi-

cious occasion, a stamp commemorating IIFT was released by the Hon’ble Prime Minister of India. IIFT is distinguished to be the

only B-School to share such an honor. We have posted few snapshots of the ceremony.

We hope that you will enjoy reading this New Year edition .Wishing you a very Prosperous and a Happy New Year!

Happy Reading!!!

ANKIT TIWARI & ASHUTOSH DESHPANDE

FROM THE EDITOR’S DESK 3

InFINeeti | Annual Issue | January 2014

CONTENTS 2 CONTENTS 4

>>> Page 5 >>> Page 25 >>> Page 30

Basel III norms:

Are the Indian Banks Prepared to bite the bul-let

5

m-banking: The game changer for telecom sector

9

Guest article— the ills of indian econo-my: causes, effects & measures

18

Qe tapering: is ru-pee doomed amid fear of QE?

Effects of proposed QE in Indian economy

22

Psychology of stock markets:

Understanding the role of rationality and instinct

25

Honest answers

Candid chat with Mr. Naresh Kumar Garg (CEO, Sahara Mutual Funds)

28

COVER

STORY

FINANCING THE

2014 ELECTION

“Financing the new ways to fund the elections of the big-

gest democracy”

13 The great indian in-vestment story:

An Analysis of India’s In-vestment story

30

35

FIN Trivia

News chronicles 37

Fin lingos 08

39

fIIFTy Years of IIFT:

Release of the stamp on the auspicious occasion of completion of fifty years

33

Fun with fin 41

Regulars

Top 10 events of 2013:

Review of important events of 2013

Budget trivia:

Contains interesting facts

regarding Indian Budg-

ets presented in parlia-

ment

29

InFINeeti | Annual Issue | January 2014

5

INTRODUCTION

Basel was developed as a set of standards and practices for

banks to ensure that they maintain adequate capital during a

financial crisis

The word Basel is derived from the name of a city in Switzerland,

Basel, which is the headquarters of the Bank for International

Settlement (BIS). BIS is the world’s oldest international financial

organization and exists to serve central banks in their pursuit of

monetary and financial stability, to foster international coopera-

tion in those areas and to act as a bank for central banks.

Basel guidelines refer to broad supervisory standards formulated

by the group of central banks- called the Basel Committee on

Banking Supervision (BCBS). The set of agreement by the BCBS,

which mainly focuses on risks to banks and the financial system

are called Basel accord.

According to BCBS, "Basel III is a comprehensive set of reform

measures, developed by the Basel Committee on Banking Super-

vision, to strengthen the regulation, supervision and risk man-

agement of the banking sector". The purpose of this accord is to

ensure that financial institutions have enough capital on account

to meet obligations, to improve the banking sector's ability to

deal with financial and economic stress, improve risk manage-

ment and strengthen the banks' transparency.

The guidelines set by RBI for the implementation of Basel III

norms is stricter than as set by the BCBS. It requires banks to

maintain a Minimum Total Capital (MTC) of 9% against 8% of

total Risk Weighted Assets (RWAs) as prescribed by the Basel

Committee. Also, the requirement for Minimum Common Equity

Tier I capital has been set at 5.5% of total RWAs as compared to

4.5% set forth in the Basel accord. In addition to these capital

requirements, Capital Conservation Buffer (CCB) has been intro-

duced which requires banks to maintain 2.5% of RWAs in the

form of Common Equity Tier 1 capital. RBI has set the leverage

ratio at 4.5% (3% under Basel III). Leverage Ratio is calculated as

Tier 1 capital divided by banks on and off balance sheet expo-

sures. Letters of credit, derivatives and loan commitments are

some of the items that banks keep off their books to portray a

better position of their balance sheet. Basel III has been criti-

cized as the stringent capital requirements have been intro-

duced at a time when the global economy is facing a slowdown.

Since the deadline for implementation is March’2018, the Indian

banks face the challenge to raise capital in order to meet the

requirements of Basel III. It has been estimated that this would

require capital infusion of nearly ₹5 trillion. Out of this, ₹1.75

trillion should come in the form of equity capital and ₹3.25 tril-

lion as non-equity capital.

Basel III norms strive to maintain financial stability but hampers

growth. It seems contrary to the main goal of the 12th Five Year

Plan (2012-17) which is ‘faster, sustainable and more inclusive

growth’. To achieve the Basel regulations, banks would need to

raise their lending rates. Increasing the cost of credit mitigates

growth and investment.

Basel III norms will require banks to undertake significant chang-

BASEL III NORMS ARE THE INDIAN BANKS

PREPARED TO BITE THE BULLET?

BY-KARTIK PURI & ROHIT MADHOGARHIA

IIFT,KOLKATA

InFINeeti | Annual Issue | January 2014

6

es in its systems and processes to make upgrades, particularly in

the areas of stress testing, liquidity and capital management

infrastructure. The costs for implementation will affect the

profitability and return ratios of the banks.

There is critical difference in terms of funding of banks between

the advance economies and emerging economies like India.

Whereas the former focuses on short-term money and capital

markets for funding, the emerging economies are still dependent

on deposit-based funding. The emerging economies are there-

fore in conundrum in meeting the capital requirements. Another

issue for capital raising that will be faced by banks is the lack of

initiative on the political front. The focus of Indian politicians in

the next general elections would not see any major banking re-

forms or capitalization for the banks. Also, it is unlikely that it will

be on the priority list of the new administration that comes right

after the elections.

The Indian economy did witness the fleeing of foreign capital in

the last quarter on announcement of roll-back of stimulus by the

US Fed chairman Ben Bernanke. Though the proposed tapering

of quantitative easing has been postponed, once started in early

next year, it would lead to withdrawal of foreign capital from

India leading to more problems in capital raising for the Indian

banks.

The financing high rates of growth in the emerging market and

developing economies (EMDEs) led to the development of credit

in these economies. With increase in demand for capital backup,

when the economy is still recovering from slowdown, the banks

will have less money at disposal to lend. The cost of capital is

already high in emerging economies on account of savings-

investment gap and tighter regulations.

A proposal to meet the adequacy is to consolidate the weaker

banks with the stronger ones. Also, the capital requirements

would force the development of the Indian bonds markets for

banks to raise capital.

ROE is defined as the product of the return on assets (ROA) and

the leverage multiplier. During the past three years, the Banks

need to be pro-active and take adequate measures to protect

their interests following the implementation of Basel III regime.

Banks need to shift towards more retail loans as they typically

tend to have a lower risk weight as compared to corporate bank-

-ing. Banks should aim at maintaining a stable low-cost deposit

base to ensure high profitability margin. One of the main reasons

for the economic recession was the allocation of funds to high

risk customers. Banks need to review their capital allocation to

each customer segment and price their products in a way as to

generate higher risk-adjusted returns.

InFINeeti | Annual Issue | January 2014

7

According to a recent report by Fitch ratings, Indian public sector

banks are facing several challenges in meeting the Basel III re-

gime. The declining profitability has hindered the capability of

banks to raise the equity required to meet the regulations. It

remains to be seen if banks can reverse the scenario and main-

tain profitability while ensuring the compliance of Basel III

norms.

Average ROE for Indian banks has been 16%. The enhanced capi-

tal requirements would negatively affect the ROE and sharehold-

er’s expectations on the return.

Though the implementation of Basel III norms is going to be a

costly affair with major issues of meeting the capital require-

ments, the enhanced quality and quantity of capital with the

banks would ensure that they are well positioned to meet any

financial shock in the global economy. This would ensure

strengthening of the banking system boosting the confidence of

the investors.

InFINeeti | Annual Issue | January 2014

8

Financial lingos

Stump the Chump

The act of challenging a person in the spotlight in an attempt to

make he or she appears foolish. "Stump the chump" employs

tactics such as trying to make the hostile party look smart and in

control while trying to make the other person look incompetent.

Examples of trying to stump a chump include asking an authority

or expert who is giving a presentation a question that they won't

be able to answer and that could undermine their credibility, or

giving a co-worker incorrect information that will cause them to

reach incorrect conclusions .

Financial Shenanigans

Acts or actions designed to mask or misrepresent the true finan-

cial performance or actual financial position of a company or

entity. Financial shenanigans can range from relatively minor

infractions involving creative interpretation of accounting rules

to outright fraud over many years. In almost every instance, the

revelation that a company’s stellar financial performance has

been due to financial shenanigans rather than management

prowess will have a calamitous effect on its stock price and fu-

ture prospects. Depending on the scale and scope of the shenan-

igans, the repercussions can range from a steep sell-off in the

stock to the company’s bankruptcy and dissolution.

C-note

The term came to prominence in the 1920s and 1930s, and was

popularized in a number of gangster films. C-note is used less

frequently in modern slang, and has been replaced by

"Benjamin" as Benjamin Franklin, one of the founding fathers of

the United States, is on the $100 banknote.

Grey Wave

An investment or company thought to be profitable in the long-

term or very long-term. The investor should not plan for an im-

mediate or even short-term positive return, but rather only

when s/he is much older and has grey hair.

InFINeeti | Annual Issue | January 2014

9

INTRODUCTION

We always come across telecom companies launching new

“Talktime” or “Top Up” offers. The day has come when we will

see them launching new fixed deposit schemes, current account

offers, saving offers etc.

Providing mobile money through mobile phones is a value add-

ed service offered through telecommunication companies. The

issuance of which involves both telecommunication and bank

regulations.

INDIAN TELECOM SECTOR

India is the second largest telecommunication market in the

world, and is also one of the fastest emerging mobile markets

going global. *See Exhibit 1+. Key areas that will enable mobile

banking sector to grow auxiliary are increased revenues from

data services like the introduction of 2G, 3G services, increased

mobile penetration in the rural sector, need to reduce opera-

tional and capital expenditure because of active and passive

allotment of telecom infrastructure. There are many opportuni-

ties that lie in investments in these segments.

Hence, there lays a tremendous scope to launch

niche mobile banking products to meet the financial needs of

customers in this sector.

INDIAN BANKING

Indian banking had its first encounter with information technol-

ogy when computers made a breakthrough in India in the

1980s, which lead to the plodding eclipse of the data entry and

manual ledger. A dramatic change was observed in customer

experience when manual processes were replaced by automat-

ed ones. Services that required customers to spend hours to-

gether at the branch were completed in a few minutes.

Notwithstanding these technological changes, there lies a big

challenge in front of us. We have not been able to reach out to a

large majority of the population through the traditional brick

and mortar banking model. India has the maximum number of

households in the world (approximately 145 million) excluded

from banking services. Despite the fact that it has an wide-

spread network of bank branches and ATMs (80,000+), access-

ing banking services has always remained a distant dream for

many.

Here comes M-Banking into play which provides a resort to mil-

lions to access banking services within flash of seconds and

eliminating the need to stand in long queues.

WILL M-BANKING BE THE GAME CHANGER FOR THE TEL-

ECOM SECTOR IN INDIA

BY- ASHITA GUPTA

-IMI, DELHI

InFINeeti | Annual Issue | January 2014

10

MOBILE BANKING

Mobile banking is a term coined for a system that allows cus-

tomers of a financial institution to conduct a number of financial

transactions through a mobile device such as a mobile

phone or personal digital assistant.

The estimated banking penetration among middle and high in-

come groups in India is about 45% while for low income groups

it is less than even 5%. Comparing this with the 76.03 % of

Teledensity and the projected Teledensity of 84% by 2012

Banks have indeed realized the role that can be played by mo-

bile banking in reaching out to the unbanked areas as well as the

on the run customers and have tied up with leading providers

like Vodafone and Airtel to cater mobile banking services. Refer

Exhibit 2.

With the advent to booming use of mobile phones, banking ser-

vices and mobile money have been made available using the

phones.

LEVERAGING MOBILE COMMUNICATIONS

Connecting people, anywhere, anytime: Mobile telephony

connects more than 95 per cent of the country.

• Large distribution network: Mobile connections and various

value-added services are available across an extensive sales and

distribution network across the country. Many outlets are ser-

viced by a number of distributors, urban and rural. Telecom re-

tail outlets across the country are over 3 million.

EXAMPLE:

Pre-paid mobile recharges are bought by the customers at a

retail end and are delivered through the network straight away.

In case of any incident, call centers service the customer. The

current model is akin to banking where the service is delivered

directly by the banks to the customers.

• Service customers on a large scale: The phenomenal growth

of the Indian telecom sector has created service capacity of

enormous magnitude. All MNOs together serve more than 900

million customers, through call centers or through self-care.

• Micro transaction processing capability: Telecom companies

process billions of electronic transactions every day. There has

been a robust technological capability that has been built over

the past two decades to process high volume micro-transactions

with a high degree of precision. These capabilities can be ex-

tended (with a certain degree of co-creation and customization)

to banking and financial transactions as well.

CAN BE USED FOR:

Potentially provide a viable alternative as a cheapest way

to reach rural customers

Some recent estimates peg the cost of setting up a micro

banking outlet in the range of US$500 to US$800.

Disbursals made by government constitute a large part of

monetary transactions in rural India

Transfer of government payments electronically to the

paupers will pay for itself as well as connect households

to a formal and secure financial grid.

DESIGN AND DELIVERY OF THE ECOSYSTEM

There are three enablers that hold the key to mobile banking

quickly becoming a truly mass phenomenon in India.

In its current state, the mobile payments system is com-

plicated and hence has remained limited to a small seg-

ment of customers with high-end mobile phones. The

answer lies in ushering in easy-to-use technology which

can be configured in low-end handsets.

Educating customers about the security of mobile trans-

actions and customizing them through vernacular inter-

faces will be important.

The partnerships that build up the ecosystem among

different stakeholders like banks, systems providers,

MNOs need to be encouraged.

Risks involved can be fraud, security, outsourcing, consumer aware-

ness, technological risks and anti-money laundering controls.

InFINeeti | Annual Issue | January 2014

11

MOBILE BANKING MODEL (SERVICES OFFERED)

A MODEL: MOBILE BANKING AS A KENYA’S GAME CHANGER

FINANCIAL services growth in Kenya has been phenomenal

over the past seven years. FinAccess survey released in Nairo-

bi on October 31 suggests that the proportion of Kenyan

adults using formal financial services have more than doubled

from about 30% in 2006 to 63% at present and over 75% in

urban areas.

This growth has been powered by the adoption of mobile

money transfer. The world leader with two-thirds of adults-

Kenya uses such a service. A service called “M-Pesa” transfers

nearly a third of GDP each year in transactions whose aver-

age value is just R290.

Though this growth has been the most strapping in mobile

money, usage of bank accounts has also more than doubled,

from about 15% of Kenyans in 2006 to over 30% today.

A mobile banking product called “M-Shwari” was launched in

November 2012 as an opportunity to seek additional financial

needs for the large number of Kenyans who were using mo-

bile money but not bank accounts.

ROLE OF A GOVERNMENT

Gauging at the benefits, Governments of certain countries

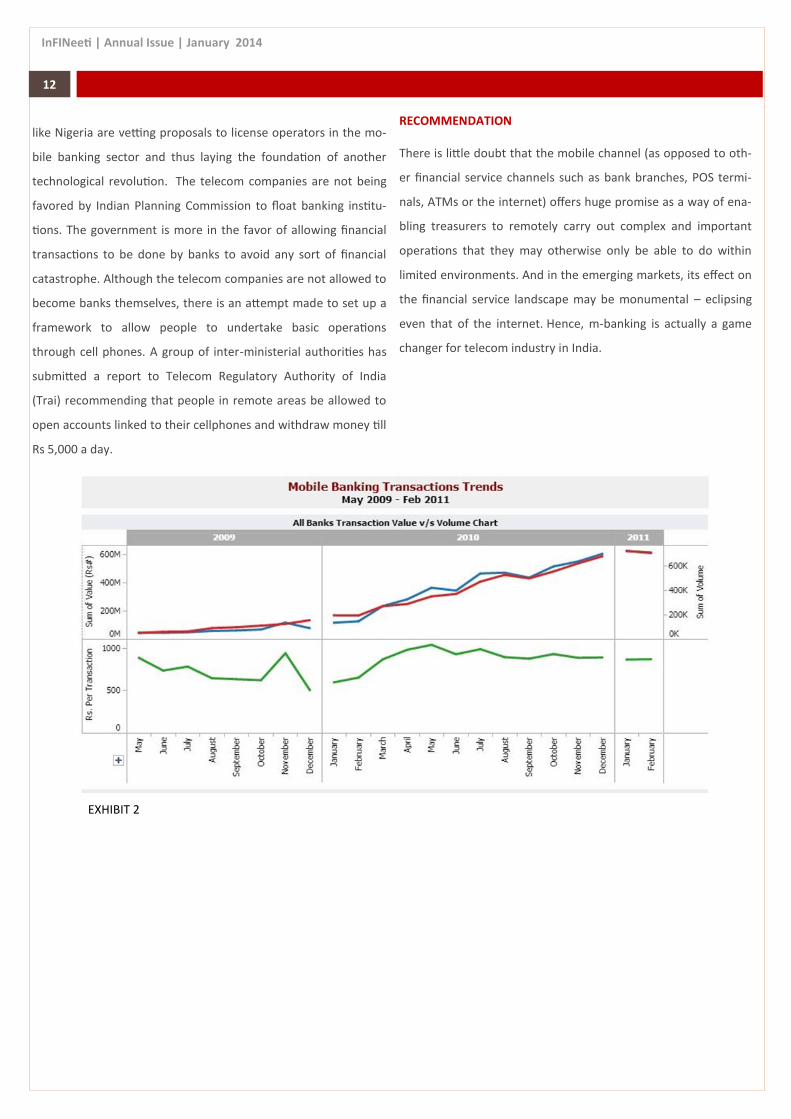

EXHIBIT 1

InFINeeti | Annual Issue | January 2014

12

like Nigeria are vetting proposals to license operators in the mo-

bile banking sector and thus laying the foundation of another

technological revolution. The telecom companies are not being

favored by Indian Planning Commission to float banking institu-

tions. The government is more in the favor of allowing financial

transactions to be done by banks to avoid any sort of financial

catastrophe. Although the telecom companies are not allowed to

become banks themselves, there is an attempt made to set up a

framework to allow people to undertake basic operations

through cell phones. A group of inter-ministerial authorities has

submitted a report to Telecom Regulatory Authority of India

(Trai) recommending that people in remote areas be allowed to

open accounts linked to their cellphones and withdraw money till

Rs 5,000 a day.

RECOMMENDATION

There is little doubt that the mobile channel (as opposed to oth-

er financial service channels such as bank branches, POS termi-

nals, ATMs or the internet) offers huge promise as a way of ena-

bling treasurers to remotely carry out complex and important

operations that they may otherwise only be able to do within

limited environments. And in the emerging markets, its effect on

the financial service landscape may be monumental – eclipsing

even that of the internet. Hence, m-banking is actually a game

changer for telecom industry in India.

EXHIBIT 2

InFINeeti | Annual Issue | January 2014

COVER STORY 13

FINANCING THE 2014 ELECTION

“Financing the new ways to fund the elections of the biggest democracy”

By- Ankit Tiwari & Ashutosh Deshpande Indian Institute of Foreign Trade, Kolkata

COVER STORY 14

Former Prime Minister Atal Bihari Vajpayee once given the

statement to a parliamentary committee that ‘‘every legislator

starts his career with the lie of the false election return he

files.’’

INTRODUCTION

This quote from our former Prime Minister aptly describes the

sorry state of affairs of election funding in India. General elec-

tions in India are due in a few months and the whole world will

be watching with awe and admiration as to how a populace of

more than 100 crores vote to elect the new government. But,

increasingly, electing a new government is becoming a costly

affair and the expenditure on elections is humongous. It raises

several pertinent questions like how do political parties gener-

ate revenues? What are the sources through which they raise

funds? Are the channels from where they raise funds legal, or

there are shades of grey involved? Are the present forms of

election funding rules transparent enough? Or can there be

better way of funding the political parties so that transparency

can be brought into the system? In this article we have tried to

answer these questions.

HISTORY OF POLITICAL FUNDING

The overhaul and reform of the means by which candidates

and political parties fund their election campaigns is one of the

most important challenges in front of Indian democracy. Tradi-

tionally, political parties had different channels through which

they use to garner funds, like membership dues, individual do-

nations and corporate funding. Parliament had passed, in 1951,

The Representation of People Act (RPA) of 1951 which sets the

limits on the total amount that can be spent on election cam-

paigns. But in 1960s, there were increasing concerns on the

minds of the policy makers regarding the black money route

covertly adopted by political parties to get election funding.

The situation further exacerbated when in 1968, the then PM

Indira Gandhi had put a ban on corporate funding to political

parties on one hand and on the other hand did not open the

option of state funding. The reason for the ban was to prevent

large corporate houses to unfairly influence the policy deci-

sions. But that decision created big problem for political parties

regarding election funding. Now they can’t get funding from

corporates which used to contribute the largest chunk of their

funding and they would also not get the state funding. So, as a

consequence black money funding increased drastically in In-

dia.

In 1974, in one of the judgements, Supreme Court ordered that

in calculating a candidate’s election’s expenditure, the party’s

expenditure on that candidate must be included and then limit

as to whether the candidate has spent the stipulated amount is

checked. This was an attempt by the top court to bring the cost

of election down. However the parliament, in 1975, through

amendment to RPA act, nullified this judgement and the candi-

dates were spending seamless amounts in the elections. From

1979 onwards, political parties were exempted from wealth

and income tax provided they have filed annual income tax

returns, listed their donations of above Rs 10,000 and declared

the name of the donors. Corporate funding were again allowed

from 1985 by the amendment in Companies Act, through sec-

tion 293A with the condition that corporates can donate only

InFINeeti | Annual Issue | January 2014

COVER STORY 15

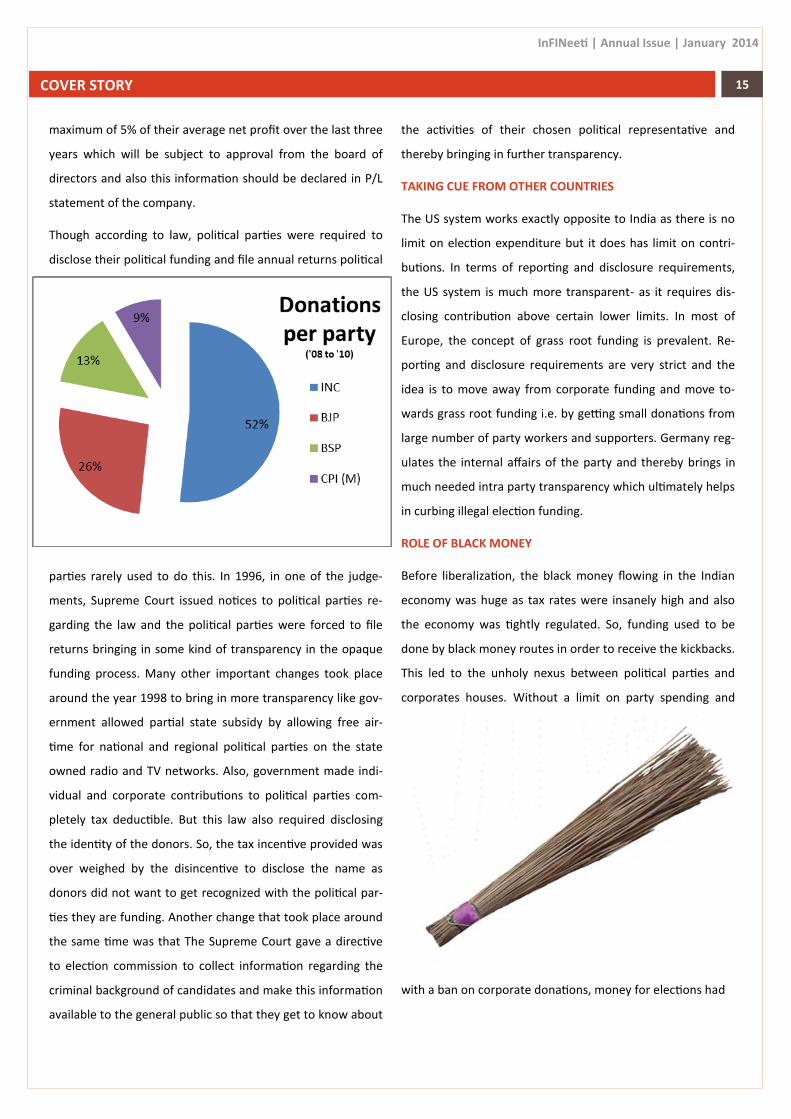

maximum of 5% of their average net profit over the last three

years which will be subject to approval from the board of

directors and also this information should be declared in P/L

statement of the company.

Though according to law, political parties were required to

disclose their political funding and file annual returns political

parties rarely used to do this. In 1996, in one of the judge-

ments, Supreme Court issued notices to political parties re-

garding the law and the political parties were forced to file

returns bringing in some kind of transparency in the opaque

funding process. Many other important changes took place

around the year 1998 to bring in more transparency like gov-

ernment allowed partial state subsidy by allowing free air-

time for national and regional political parties on the state

owned radio and TV networks. Also, government made indi-

vidual and corporate contributions to political parties com-

pletely tax deductible. But this law also required disclosing

the identity of the donors. So, the tax incentive provided was

over weighed by the disincentive to disclose the name as

donors did not want to get recognized with the political par-

ties they are funding. Another change that took place around

the same time was that The Supreme Court gave a directive

to election commission to collect information regarding the

criminal background of candidates and make this information

available to the general public so that they get to know about

the activities of their chosen political representative and

thereby bringing in further transparency.

TAKING CUE FROM OTHER COUNTRIES

The US system works exactly opposite to India as there is no

limit on election expenditure but it does has limit on contri-

butions. In terms of reporting and disclosure requirements,

the US system is much more transparent- as it requires dis-

closing contribution above certain lower limits. In most of

Europe, the concept of grass root funding is prevalent. Re-

porting and disclosure requirements are very strict and the

idea is to move away from corporate funding and move to-

wards grass root funding i.e. by getting small donations from

large number of party workers and supporters. Germany reg-

ulates the internal affairs of the party and thereby brings in

much needed intra party transparency which ultimately helps

in curbing illegal election funding.

ROLE OF BLACK MONEY

Before liberalization, the black money flowing in the Indian

economy was huge as tax rates were insanely high and also

the economy was tightly regulated. So, funding used to be

done by black money routes in order to receive the kickbacks.

This led to the unholy nexus between political parties and

corporates houses. Without a limit on party spending and

with a ban on corporate donations, money for elections had

InFINeeti | Annual Issue | January 2014

COVER STORY 16

to be raised somehow. This appears to have accentuated the

slide towards dependence on black money.

Also, given the amount of money needed to spend on elec-

tions, nowadays, political parties prefer those candidates who

can fund their election campaigns and this is increasing the

trend of people with money and muscle getting the tickets and

not the common man. So, this will increase the trend of wealth-

ier people entering into politics to further enhance their wealth

and not with the intention of serving the people. This is an in-

creasingly dangerous trend as they will be the people who will

be deciding the policy issues in the parliament. Also, this will

also increase the people with criminal background entering into

the politics as they have both money and muscle power and

this fact can be judged by the fact that many of the sitting MPs

and MLAs has criminal cases pending against them. So, it be-

comes even more important to reduce the election funding so

as to keep politics clean.

CURRENT TRENDS AND HAPPENINGS

A prominent leader from the Lok Sabha had once made a can-

did confession a few months ago regarding his electoral spend-

ing. While speaking at a book release function, he admitted to

have spent Rs. 8 crores in the 2009 Lok Sabha campaign,

whereas the prescribed limit is only Rs. 25 Lacs, which is 32

times the official limit! Despite the stunning revelations, the

matter was not picked up aggressively picked up by the main-

stream media, because the leader spoke of something which

everyone knew of! A notice from the Election Commission of

India followed, as expected, as a routine exercise with no con-

sequence.

A Member of Parliament from Bihar had once famously claimed

that candidates slotted as under BPL category also spend in

crores! It is also said that the average expenditure per candi-

dates comes to around Rs 4-5 crores. In many cases, money

spent on campaigning from the constituency exceeds the mon-

ey they spend for the development of the constituency. These

are facts which we should not be proud of, especially as the

largest democracy in the world. We should be able to find a

sustainable model of funding as well as spending of the availa-

ble resources, especially given the trend that to win an election

in India, a huge amount of investment is almost necessary. Is

such a model possible to be implemented practically? We have

one good example.

Arvind Kejriwal- led Aam Aadmi Party (AAP) demonstrated an

almost ideal model for funding the Delhi Stat elections they

fought and achieved commendable success. They had set a lim-

it of Rs. 20 crores in accepting donations. At the same time they

revealed all the donations made to them, an unprecedented act

which put them on a very high moral pedestal .Once they had

crossed the figure, they stopped taking donations. At the same

time, they did not take help of any corporate funding- which

are said to play an important role in deciding the win-ability of

an election. AAP volunteers went from street to street, house

to house to solicit donations starting from as small an amount

as Rs. 10. They also inculcated sophisticated online money

transfers and international cheques so as to increase the reach

of their funding.

SOLUTIONS

So as to reduce the total expenditure on elections, long term

strategies should be adopted by the major political players.

These include use of advancing technologies and analytics to

achieve better reach and results. Use of Social Media- which is

one of the cheapest and easiest way to communicate- should

be inculcated. Even if a candidate spends money to promote

himself on social media, the total expenditure will be a fraction

of the prescribed limit. At the same time, if he inculcates ana-

lytics into his system, he can reach out to his

InFINeeti | Annual Issue | January 2014

COVER STORY 17

targeted segment in a much better way.

It is not always that money and muscle power wins, if one has

the right agenda, a clean background and a focus on what one is

going to do for the constituency and is able to communicate it to

the voters, then there is no reason why one should spend mil-

lions of rupees.

AAP has taken the initiative in showing us the way forward, but

questions will be raised on whether the model is scalable

enough? Delhi, which was an epicentre for the anti-corruption

movement and the launch pad for India Against Corruption (IAC)

was a home ground for Arvind Kejriwal to implement his meth-

odology.

One of the good suggestions to curb the black money flowing in

the election funding and to bring the cost down was given by

MP Chief Minister Shivraj Singh Chauhan wherein he proposed

that all elections i.e. assembly elections of all state and loksabha

election should take place together every five years. This will

bring down the cost of elections as India sees every year 2-3

elections and Election Commission as well as political parties

have to spend a lot of money in these elections. While there are

many things that need to be sorted out in this solution like now-

adays many state doesn’t produce stable government and give

fractured mandate. This is increasingly true at national level al-

so. But still, if we see largely in majority of states government do

complete their five years so if somehow this solution is worked

out than we can definitely reduce the cost of elections as well

will be able to curb the black money which is alleged to flow into

these elections.

Lastly, a few changes that can help raising funds cleanly like

maintaining the confidentiality of donors which will remove the

risk of political parties penalizing the people who will be funding

the opposition parties. Also, public spending on elections can be

increased and also government can encourage grass-root fund-

ing like in European countries. Also, like Germany regulates the

internal democracy in the parties we can also follow the same

by putting the condition that only those parties who have proper

internal democracy and those who have transparent processes

in place will be given the state funding. We hope that this year’s

election will throw more light on this issue and political parties

and candidates will move forward and will be able to find better

routes to garner funds . They can take a cue from Aam Admi

party. Though the solutions include some decisions which may

be harsh on the political parties, initiatives and strides towards

the direction are essential for a clean and fair election process.

InFINeeti | Annual Issue | January 2014

18

INTRODUCTION

Ever since Goldman Sachs coined ‘BRICs’ in 2003, the world has

watched with expectant eyes the rise of an Indian economy

(democracy of a billion people along with Washington-styled

free markets makes an interesting case study) growing in excess

of 7% year on year. However, the last couple of years have seen

a slowdown in growth, leading to doubts whether we will make

it to escape velocity from the orbit of under-development. What

this article tries to do is a take a first –principles view of the

economy and what might be going wrong, and then highlight

what are a few things we could do differently.

A. The Ills of our Economy

Over the last few months, financial newspapers have written

countless number of editorials on the economic slowdown, the

sliding rupee and the endless delays in implementation of infra-

structure projects. But, beyond the news- bites is Economics 101

playing itself out on India, demanding long-term, hard solutions

beyond the industry cry for lowering interest rates to boost

growth.

Some key economic issues that demand understanding are -

1. India’s economic growth is slowing down: A subject widely

covered in press reports, India’s GDP growth rate has been slow-

ing down, from 7-9% in FY04-FY08 to 6.2% in FY12, 5% in FY13

and an expected 4.5-5.5% in FY14.

A few reasons why India is suffering from a slowdown are –

a. Policy Paralysis: Due to political reasons, reforms have been

slow. Investors’ wish list for reforms in direct tax via DTC, indi-

rect tax via GST, FDI in various sectors, ease of doing business

(permits, licenses, clearances et al) have remained unfulfilled.

b. Structural Issues: As I will highlight below, the Indian econo-

my grew rapidly over the last decade but has a few structural

GUEST ARTICLE: ILLS OF INDIAN

ECONOMY CAUSES | IMPACTS | MEASURES

BY– Aniket Nikumb

Business Analyst, McKinsey & Company.

(Views mentioned here are personal)

InFINeeti | Annual Issue | January 2014

19

issues – high trade deficit, significant fiscal deficit and sticky in-

flation.

c. External Factors: Most of the economic growth over the last

few years was mainly seen in the service and manufacturing sec-

tor and hardly any in agriculture, industry and mining. A slow-

down in the West – primary consumer of outsourcing services

out of India – subsequently reduced overall growth rate.

2. India’s trade is imbalanced: The summary of trade in goods

and services below will show how starkly we are over-spending –

The gap between imports and exports must be ‘financed’ via

borrowing. Of course, having a trade deficit isn’t necessarily bad;

if the deficit is “invested” wisely such that the return on that

investment exceeds the cost of borrowing, then the country

effectively gains. The above chart clearly shows why this is not

the case in India- since the major import items without corre-

sponding exports are oil and gold - which are not investments

but domestic consumables. Reducing this deficit will be a critical

priority for the Finance Ministry, since a structural trade deficit

will be harmful to the economy in the following ways -

a. Currency Depreciation and Domestic Inflation: Higher imports

mean relatively higher demand for foreign currency vis-à-vis do-

mestic currency – leading to the value of the domestic currency

decreasing. This can in turn lead to a vicious circle where more

and more of domestic currency is spent on importing same

amount of goods, leading to a wider deficit and further leading

to a depreciating currency and so on.

b. Higher Debt: Trade deficit may also be ‘financed’ through bor-

rowing the foreign currency (instead of paying with your domes-

tic currency) – which must be serviced with interest in the fu-

ture. More foreign currency interest payments could mean a

wider deficit further depreciating the currency. At some point,

the deficit must convert to surplus or rising debt and interest

levels will bankrupt the nation.

3. India’s budget is imbalanced: Highlighted below is a summary

of India’s revenue and expenditure-

Similar to the trade deficit we saw above, the gap between Gov-

ernment expenditure and revenue must be financed via borrow-

ings – either from its own citizens or via external institutions

such as the IMF. As the chart above shows, Government reve-

nues are a mere 63% of its expenditure, and a large part of the

gap goes into –

Banking Sector Expanded—Handbook of Statistics

InFINeeti | Annual Issue | January 2014

20

a. Servicing interest payments on existing debt, and

b. Subsidies – primarily on food, fuel and fertilizers

Deficit financing is desirable when spent on creating valuable

assets to accelerate economic growth (highways, power plants,

ports et al) – but the nature of the subsidy spend in India is

mostly welfare-driven (e.g.. subsidized kerosene gas, low cost

food grains etc.) – which are in the nature of consumption as

opposed to investments into the future.

A fiscal deficit may be financed in one of two ways –

a. Borrowings: Borrowing the difference from citizens (domestic

debt) or external agencies (IMF, World Bank etc.) means the

same must be repaid in future along with interest (which was

already 3.2% of GDP in FY13, almost 3 times our defense budg-

et). Additional debt burden has the following consequences –

i. Interest Rate: Higher debt of a country makes it more risky in

the marketplace – leading investors to demand a higher rate of

return (interest) to compensate for it. In recent times, this was

seen in problem European countries with Greece debt carrying

interest rate as high as 22%

ii. Crowding Out effect: Interest rates are set by the relative

demand and supply of money, and when Government borrow-

ings increase, the funds available for private investment become

lesser and more expensive – thereby affecting the economic

growth of a country.

iii. Foreign Currency Risk: If debt is denominated in foreign cur-

rency, the liability is volatile to the movement of currency i.e. If

one borrows $1Bn at US$1 = INR 40 and the INR depreciates to

50, then the capital liability itself increases by 25%.

b. Printing additional currency: Another way to finance deficits

is to print more money – since the world moved off the Gold

standard (ie. having a commensurate precious metal for every

currency note in circulation), currency notes are backed only by

the solemn promise of the issuing Government. This is akin to a

consistent inflation - an ‘invisible tax’ on the people because it

reduces the purchasing power of money as more and more cur-

rency chases similar amount of goods.

Sustained inflation can be harmful for the following reasons:

i. Expensive Borrowings: When inflation expectations are high,

lenders adjust interest rates for expected drop in purchasing

power of money, making capital more expensive. (If an investor

believed that an apple that costs Rs 10 today will cost Rs 11 in a

year, he will demand at least a 10% interest to merely maintain

his purchasing power, plus an additional interest for privilege of

using his money). A higher rate of inflation thus makes borrow-

ings and therefore, investments more expensive.

ii. Currency Depreciation: In general, exchange rates of coun-

tries adjust as per inflation i.e. a country with a higher rate of

inflation will experience a depreciation in the currency value to

the extent of the incremental inflation it experiences. This dis-

courages foreign investment and erodes domestic wealth.

B. What we can do differently

Being neither an economist nor an expert on public policy, I only

resort to first-principles to propose a few solutions. Below listed

are a few starting point ideas that I think could be politically fea-

sible and will go a long way in establishing the economic founda-

tion of India:

1. Subsidy Restructuring: India spends billions on fuel subsidy

selling diesel at below-market prices (Petrol was recently moved

to a market-driven pricing model). Numerous committees have

advised the Government to liberalize diesel pricing, and while

steps have been taken in the right direction, the taxpayers will

continue to subsidize diesel consumers till market-based pricing

is introduced.

Unlike kerosene, diesel is not a direct item of consumption and

given the limited weight of fuel in the inflation index itself, the

benefits (such as reduced subsidy burden, oil companies have

more surplus for new exploration, consumers shift to fuel-

efficient/cheaper fuel engines) far outweigh the short-term in-

crease in inflation.

It may also make sense to re-consider the food subsidy: numer-

InFINeeti | Annual Issue | January 2014

21

ous studies have shown large wastage in distribution via the

public distribution shops, and the Government itself is keen to

pursue a direct cash subsidy. Technology is a big constraint in

implementation, but if we can move key subsidies (kerosene/

cooking gas, food et al) to direct transfer, they can be made

much more targeted and effective.

2. Tax Reform: Our tax structure is complicated, antiquated and

doesn’t seem to stop the billions in ‘black money’ that are out

there. A few logical tax reforms would be –

a. Tax on agriculture: There seems to be no logical reason why

agricultural income is exempt from tax, especially given that the

sector is one of the most uncompetitive in the world. Normal

slab rates (no tax upto 2L etc) should be extended to income

from agricultural activity: driving capital rationalization in the

sector while expanding the tax base.

b. Simplification: Tax law in India is arcane, difficult and volatile:

with numerous sections and provisions, with rules and notifica-

tions over and above the text of the Act itself. Simplifying and

consolidating taxes (income tax, wealth tax, STT, VAT, service

tax to name a few!) will be key to minimizing compliance costs

while maximizing compliance.

While a few steps have been take in the right direction (service

tax, for instance, is one of the simplest tax laws in India), the

drafts of DTC and GST have been stuck in the Legislature for

years now. A simpler tax regime has time and again led to in-

creased compliance – and this should be the top priority for any

Government.

3. Policy overhaul: Admittedly much easier said than done, it is

important for our law-makers to consider a policy overhaul to-

wards a more prosperous economy in the future:

a. Ease of doing business: The World Bank ranks India 134th out

of 189 in ease of doing business based on factors including reg-

istering property, getting credit, enforcing contracts etc. With

the help of technology and outsourcing, a lot of standardized

legal requirements can be made online and highly user-friendly.

(For instance, I recall using a paper visa – which is just a simple

print out to visit Singapore).

b. Policy Consistency: Over the last few years, we have had ma-

jor policy flip-flops in terms of direction – and what bothers in-

vestors more than a tough regime is a volatile one. We have

seen the Government effectively reverse a Supreme Court deci-

sion (a long-fought one at that) in the Vodafone tax case – with

the law getting amended retrospectively. It is important to avoid

such 180 degree directional changes, and project a consistent

policy front to earn investor confidence.

InFINeeti | Annual Issue | January 2014

22

INTRODUCTION

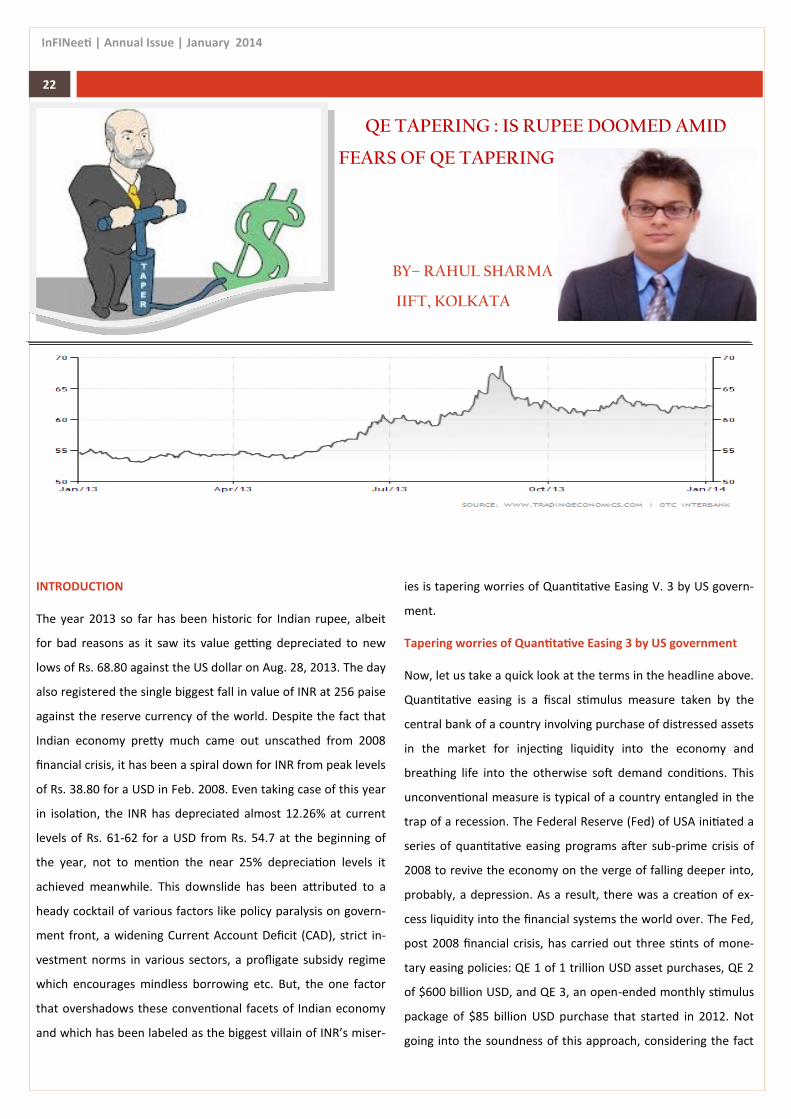

The year 2013 so far has been historic for Indian rupee, albeit

for bad reasons as it saw its value getting depreciated to new

lows of Rs. 68.80 against the US dollar on Aug. 28, 2013. The day

also registered the single biggest fall in value of INR at 256 paise

against the reserve currency of the world. Despite the fact that

Indian economy pretty much came out unscathed from 2008

financial crisis, it has been a spiral down for INR from peak levels

of Rs. 38.80 for a USD in Feb. 2008. Even taking case of this year

in isolation, the INR has depreciated almost 12.26% at current

levels of Rs. 61-62 for a USD from Rs. 54.7 at the beginning of

the year, not to mention the near 25% depreciation levels it

achieved meanwhile. This downslide has been attributed to a

heady cocktail of various factors like policy paralysis on govern-

ment front, a widening Current Account Deficit (CAD), strict in-

vestment norms in various sectors, a profligate subsidy regime

which encourages mindless borrowing etc. But, the one factor

that overshadows these conventional facets of Indian economy

and which has been labeled as the biggest villain of INR’s miser-

ies is tapering worries of Quantitative Easing V. 3 by US govern-

ment.

Tapering worries of Quantitative Easing 3 by US government

Now, let us take a quick look at the terms in the headline above.

Quantitative easing is a fiscal stimulus measure taken by the

central bank of a country involving purchase of distressed assets

in the market for injecting liquidity into the economy and

breathing life into the otherwise soft demand conditions. This

unconventional measure is typical of a country entangled in the

trap of a recession. The Federal Reserve (Fed) of USA initiated a

series of quantitative easing programs after sub-prime crisis of

2008 to revive the economy on the verge of falling deeper into,

probably, a depression. As a result, there was a creation of ex-

cess liquidity into the financial systems the world over. The Fed,

post 2008 financial crisis, has carried out three stints of mone-

tary easing policies: QE 1 of 1 trillion USD asset purchases, QE 2

of $600 billion USD, and QE 3, an open-ended monthly stimulus

package of $85 billion USD purchase that started in 2012. Not

going into the soundness of this approach, considering the fact

QE TAPERING : IS RUPEE DOOMED AMID

FEARS OF QE TAPERING

BY– RAHUL SHARMA

IIFT, KOLKATA

InFINeeti | Annual Issue | January 2014

23

that the 2008 crisis was itself a result of an unsustainable mort-

gage bubble and now there is an enormous investment bubble

in making, the improvements in the economic indicators of the

US economy, primarily politically sensitive job stats, has led the

Fed considering to cease the fiscal stimulus provided by these

QE programs. The reverse of QE, commonly referred to as QE

tapering is the suction of liquidity from the market by withdraw-

ing from the purchase of assets by selling them once the econo-

my is out from the danger of recession.

Now, why is that so detrimental for Indian economy and its cur-

rency to this extent? In global markets, this measure to bring

back the US economy from a painful and sticky recession has

brought liquidity to the most underdeveloped of financial mar-

kets around the world. These relatively less developed markets

like that of India and other emerging economies have been

offering a far higher return on the investments as compared to

western markets with near zero levels of interest rates and still

anemic growth rates. In US, with the improvement in job data,

GDP growth rate and other vital economic indicators the Fed

would be very happy to initiate the tapering of the QE program

which has swelled its balance sheet to a massive 3.7 trillion USD

from 1 trillion USD in pre-crisis days. This as a result will deal a

double whammy to Indian and other markets which are flushed

with Fed sponsored liquidity. First, there won’t be a sustained

stream of investment due to dwindling liquidity caused by taper-

ing. Second, which is even worse, initiation of tapering is an indi-

cation of an improving US economy and investors may as well

pull out their money from Indian markets for investment in their

domestic economy.

Despite the abovementioned cause and effect cycle there is an

interesting anomaly in performance of another important eco-

nomic indicator of Indian economy vis-à-vis the steep deprecia-

tion in value of INR this year; its consistently rising stock mar-

kets. This year while Indian rupee went south, stock markets

have been reaching new highs responding to an invigorated Fi-

nance Minister, since his makeshift reforms spree in September

2012, and a fresh promising face of new RBI governor. The pro-

spects of a market friendly dispensation at centre post 2014

general elections has also kept investors tuned in, besides an

artificially priced gold as a seemingly unaffordable investment

option. But, dig a bit deeper and one will find, as also published

by an Economic Times study, that the Indian stock markets are

living dangerously with the real value of Sensex somewhere

around 16000 levels. The rest is Foreign Institutional Investors’

flab who are notori-

ous for putting in

money, and pulling

it out equally fast,

for short term mar-

ket gains. So, if ta-

pering were to hap-

pen in current Indi-

an market scenario

of softening funda-

mentals, sticky and

high inflation and

policy logjam almost

a quarter of the

stock market could

be shaved off in no

InFINeeti | Annual Issue | January 2014

24

time with the FIIs having no solid reasons to stay back in the

economy.

Are we really doing this bad?

The graphic shown above tells us that despite the INR was the

worst currency vis-à-vis USD it was not the only currency to de-

preciate. Almost, all other currencies barring South Korean Won

and Chinese Juan majority of other emerging markets’ curren-

cies fell as compared to the US dollar on QE tapering fears. It

was also during the same time when the INR depreciated the

most. So, it would be safe to conclude that it was not only the

INR that depreciated versus the USD, but USD also appreciated

versus the INR, on back of revival signs in its domestic economy,

and both are not same!

So it’s not bad? No, it is obviously bad for any currency in the

world to depreciate so fast in so little amount of time. From,

1996 when INR was pegged to US dollar at Rs. 7.5 we have come

a long way today in developing a robust floating form of ex-

change rate system. The stock markets are maturing and have

been more patient than a decade ago, reserves are good and

market fundamentals one of the best and promising in the world

and one unsung hero that has been instrumental in bringing

about this transformation is the Reserve Bank of India (RBI),

often touted as the most transparent central bank in the world

for obvious reasons. The timely intervention of RBI on Aug. 29,

2013 of offering a special dollar facility to PSU Oil Marketing

Companies (OMC) to directly buy dollars helped in arresting the

nosedive of the INR, leading to biggest single day rise in 15 years

for INR at 225 paise.

Historical market trends, experts on the subject and back-end

policymakers swear to the fact that rather than the value at

which the INR is pegged against the USD it is the stability of that

value that matters in determining the health of the economy.

Whether, INR is pegged at Re. 1 or Rs. 50 or Rs. 100 for a USD, it

is just a number and will always remain so. It is the underlying

volatility, or the lack of it, behind the number which will assure

investors of the grit of the economy in the face of prevailing

global and domestic market forces (both positive and negative).

Even while INR was depreciating and IT exports became more

attractive, in comparison to their global competitors, it also at

the same time gave the overseas importers a leeway to negoti-

ate their contracts to trim costs as the take home INR revenue

for Indian IT companies increased. On the other hand, a fast de-

preciating INR would lead to inflated input costs for the IT com-

panies further denting their margins as and when this temporary

cycle takes the full circle. In long term, there is always a correc-

tion whenever the gains are quick and bubble-based. It is only

the actual increase in productivity that can add real income to an

economy. Coming back to number-value importance of any cur-

rency, or rather specifically talking about INR, suppose let’s say

we come out with a new currency tomorrow, ‘New Rupee’,

which counts the previous 100 Rupees as 1 New Rupee (100

times the previous currency). Now, at current levels, we would

be able to buy 1.6 USD for 1 New Rupee, but just this would be it

and it won’t have any affect whatsoever on the underlying econ-

omy, its productivity and the purchasing power. The New Rupee

would buy 100 times as much goods and services than the usual

Rupee in nominal terms but, it would also take 100 times the

effort to be earned as compared to the conventional Rupee. So,

having discussed most of the facets of this year’s Rupee depreci-

ation, we can conclude that an expanding economy that we are,

will probably continue to see the fall of Rupee in the longer term

and if the fall is smooth and calibrated, it is not necessarily a bad

thing to happen. Luckily, RBI is there to oversee that transfor-

mation of Rupee but, unless we fix the more chronic issues on

policy front there could be some major blips detrimental to

economy, as and when the QE tapering comes. Until then, we

can take heart from massive number-value of Japanese yen for a

USD, if a number it has to be.

InFINeeti | Annual Issue | January 2014

25

INTRODUCTION

How important a role psychology plays in the Indian stock mar-

ket? Does psychology have to do anything with the choice of

shares people buy? Is there any rationality as to how the stock

markets behave? We try to look at the answers to these ques-

tions and some more from the point of view of the Indian stock

market. After a gap of 35 months, on October 24, 2013, Indian

stock market breached the level of 21000 and also topped its

record hit in January 2008. It was on January 2008 that the

Sensex first crossed the 21000 mark after which it went down to

10000 levels. The all time closing high was on November 5, 2010

while its intraday high was clocked in January at 21,228.This was

the second time that Sensex has closed above this level. But

after touching the level, the Sensex was not able to sustain it.

If we look at the stock markets, we can witness the euphoria

(which was easily visible in 2008) behind the market touching

21000 psychological level missing. Also if we look at the P/E lev-

els, the Sensex is trading at a lower level (that of 15.8) than it

was trading in 2010 (that of 20), when it closed at this level. If

we look at the stock markets, we can witness the euphoria

(which was easily visible in 2008) behind the market touching

21000 psychological level missing. Also if we look at the P/E lev-

els, the Sensex is trading at a lower level (that of 15.8) than it

was trading in 2010 (that of 20), when it closed at this level.

The major reason that can be attributed to this is that the fun-

damentals of Indian economy continue to be weak. Rupee was

among the worst performing Asian currency after the Federal

Reserve (Fed) announced that it may start tapering towards the

CROSSING THE PSYCHOLOGICAL HURDLE OF 21000 UNDERSTANDING THE ROLE OF

RATIONALITY AND INSTINCTS IN

THE STOCK MARKET MOVEMENTS

-By Mohit Ambwani & Prince Gaurav

MDI, Gurgaon

InFINeeti | Annual Issue | January 2014

26

years’ end. The economy which was growing at an average GDP

of around 8% for the past decade and was slated to grow at a

double digit rate over the coming years is growing at its unin-

spiring lower rates. India is also reeling with huge fiscal and cur-

rent account deficit. Inflation still remains a continuing threat

with RBI having already revised the repo rates upwards twice.

Further the current rally in stock is being driven by a few select-

ed stocks which are currently priced at a considerably high level

and most of the corporates are showing slowing profit growth.

The economy is also marred by contracting manufacturing activ-

ity and uncertainty as to whether a stable government will be

formed at the centre. It has also been badly affected by innu-

merable number of scams and frauds unearthing almost daily

and lack of clear policy initiatives taken by the government.

So, does any relationship exist between the stock market and

macroeconomic growth of the country? If one looks at the stock

market on a year-to-year basis, like during the period when Indi-

an GDP was growing at a healthy rate, the BSE Sensex experi-

enced great volatility during that period. The relationship was

that it would have been impossible to establish a link between

the two factors. But when one looks at the relationship over a

longer time horizon, one could easily make out that a fair

amount of relationship exists.

As the stock market is a reflection of the corporate performance

and GDP is the collective output of agricultural, industrial and

services sector, so state of economy has a bearing on the stock

that relationship may not be visible in the immediate terms.

Further according to modern finance theory, stock price is con-

sidered as discounted present value of the firm’s payout, so

there is a connection between economic activity and stock price.

So what are the reasons that give rise to volatility in the Indian

stock market that it becomes difficult to assess the economic

condition effectively through it?

Experts are of the opinion that rally in the Indian stock market is

being driven by easy global liquidity( as taper pushed by few

months) and the other, that of Narendra Modi led government

winning the upcoming elections. But underneath these factors

are lying some psychological factors that are causing the market

to hover around its all time high despite the weak fundamentals

of the economy and are also making it difficult for the stock

market to break free of its previous highest threshold level of

21000.

The market is made up of both the value (investors who invest

for a long time horizon) and intraday or short-term traders. Val-

ue investors majorly concentrate on the stocks’ fundamentals

before investing, they work out the intrinsic value of the stock

and buy/sell accordingly, on the other hand, daily traders play

more on the psychological factors before making their decision.

They are the chief reasons for the upswings and downtrends in

the market. They are more driven by their need of immediate

gratification. Greed and fear, together with herd instinct are

supposed to be the three main emotional motivators of the

stock market and business behavior (bull and bear market) and

one of the causes for occurrence of business cycles. They make

people act irrationally without cognition.

The psychology and trend of the market are over dependent on

each other, i.e. one determines the other. As the Indian market

was moving up (trend) in lieu with the global liquidity, many

investors thinking they would lose in the profits in the emerging

market of India( psychology), they developed an optimistic ap-

proach towards their trade, and followed the suit and start in-

vesting in stocks that were driving up the market, as a result

pushing the Sensex to its all time high, but as soon as the market

PSYCHOLOGICAL FACTORS

InFINeeti | Annual Issue | January 2014

27

touched its upper cap or its resistance level; due to the anchor-

ing bias, which states that people start with a suggested refer-

ence point and make adjustment to reach their estimate, many

investors (psychology) thought that market cannot go beyond

the current level as there was no positive information stemming

in from the economy which could sustain the momentum and

started outward selling of their stocks, as a result, market came

down (trend), thus proving the other part of the above proposi-

tion.

More so, if we see this time around, the rally in stock is driven

more so by the institutional investors rather than retail inves-

tors who have been witnessing the rally more from the side-

lines. Both types of investors are affected by their respective

biases. Institutional managers following the herd instinct, try to

incorporate those stocks which the other money fund manager

are possessing, no matter if the stock fells down, so that if they

incur a loss, they won’t be the ones who will be held responsi-

ble and liable to criticism and if these stocks benefit, then they

would be acknowledged for grabbing up the opportunity, plus

also win over many customer accounts. In case of retail inves-

tors, their behavior is influenced by the experts opinion and

they more or less trade on the recommendation given by these

analysts. They are also affected by the decision of the majority

group.

Other major psychological biases that come into play and affect

he stock market on day-to-day basis are the overconfidence

factor( people tend to value their judgment highly), endowment

effect( give more value to things owned by them), loss aversion,

the prospect theory (people weigh losses more heavily than

equivalent amount of gains), gambler fallacy (onset of certain

random event is least likely to happen following an onset of

events), representativeness( people base their expectations

upon past performances) etc. Also people tend to react more to

price changes than to intrinsic value of the stock.

Efficient Market Hypothesis, Really?

Most of the principles in conventional finance are based on Effi-

cient Market Hypothesis, which states that markets are rational

and most of the information are reflected in the stock prices. It

also states that stock prices are unpredictable but time now and

then, it has been proven that stock prices can be relatively pre-

dicted based on the psychological factors, social movements,

noise trading and fashions or “fads” of irrational investors in a

speculative market. Psychological factors also give rise to mar-

ket anomalies like January Effect, winner’s curse, equity premi-

um puzzle which cannot be explained by the EMH. The EMH

misses out on a very important aspect, information is not the

only factor influencing the stock markets that the hypothesis

takes into account but expectations also plays out quite a sig-

nificant role.

Conclusion

Indian Stock market like markets around the world is influ-

enced by many psychological factors. They result in volatility

in the market and are responsible for market facing a stiff

resistance at the 21000 level. They are also responsible for

the market reaching at that level in the first place despite the

weak fundamentals that the economy is dealing with. The

current rally is driven more by irrationality than one’s focus

on fundamentals. If the markets had been rational then it

would have been possible to explain phenomenon like more

than 2000 points rise in the Indian market on a single day.

Psychological swings from over-optimism to over-pessimism

are causes for peaks and bottoms in the market.

InFINeeti | Annual Issue | January 2014

28

Team InFINeeti: Are the recent regulations in Mutual Fund industry

conducive for growth.

NARESH GARG: Regulations made by SEBI were always conductive for

growth. They are necessary and beneficial for the growth of mutual

funds. Any regulations denoted should move with time and catch the

essence of the moment. Recent regulations are absolutely in line with

time and I believe they are conductive for growth.

Team InFINeeti: What are the prospective areas for growth of Mutual

Fund industry such as rural & tier II, III cities?

Answer: Mutual Funds are excellent options for those investors resid-

ing in tier II and tier III cities, looking at the ease and convenience.

Looking back, the Unit Trust of India has focused using its officers

which reached out to the rural areas and educated the masses of the

Mutual Funds. If we see the reach of Mutual Funds, it is predominant

only in 15-20 cities- which contribute a major portion of the money.

Talking about Sahara MF, we have always focused on rural- education

programs in order to reach out to the rural masses. Once they are in-

formed of the benefits in investing in Mutual Funds, they automatically

chose MF as a preferred choice .

Team InFINeeti: What is your take on foreign Mutual Funds

entering in India?

Answer: In MF industry, entry of new players is always conductive. Not

only will the market expand but also existing players mature with the

entry. We must not forget that India is still a developing country and

we need to learn from foreign Mutual Funds which have arrived from

Developed Nations. There is a lot of which we can learn and inculcate.

At the same time competition is always good for the betterment of

Mutual Funds.

Team InFINeeti: Will the volatility in the stock market affect investor’s

attitude in looking at the Mutual Funds Industry?

Answer: If you have observed, the stock markets have always remained

volatile. If we have to compare with developed nations, Indian markets

have always been volatile. This is truly reflected in the Stock Markets.

At the same time, such conditions also gives high returns compared to

stable market. Due to high returns equity always gives more return

than Fixed Deposits. Hence the volatility of which you are talking about

will benefit the MF as people will prefer investing in more rewarding

equity than store their money in a fixed income deposit.

Team InFINeeti: Do you think a high rate of inflation will increase user

savings and affect the investment in Mutual Funds? Do you think that

tightening the monetary policy by RBI, for controlling inflation; will

negatively affect the investor’s sentiments?

Answer: As I have previously stated, equity markets give more returns.

At the same it is not profitable for a user to invest more in savings.

Those FDs will not cover the existing inflation. A 4-5% rate of inflation is

ideal for growth, which India needs. But as the rate of inflation increas-

es, it becomes more and more unacceptable. Hence for the people to

get over it, they need to invest in such a way that the higher inflation

rate is beaten- which is possible through Mutual Funds. Talking about

the tightening, I think RBI is doing a good job. From the RBI’s perspec-

tive it is necessary for it to do it.

Team InFINeeti: 2014 is an election year- do you think a change in the

political environment will affect the industry for the good?

Answer: The economy always follows a business cycle. We have seen

through recession and gloom. For the cycle to complete, it is only going

to get better. 2014 is the year, where we are expecting the situation to

change for good. People also receive the election year, the new gov-

ernment as a harbinger of change and we are also expecting that post

elections, will affect the industry for the good.

HONEST CONVERSATION

IN CONVERSATION WITH— Mr. Naresh Kumar Garg

CEO, Sahara Mutual Funds

InFINeeti | Annual Issue | January 2014

29

INTERESTING BUDGET TRIVIA

Morarji Desai has presented a record 10 budgets .

There have been 78 Budgets since 1947, 12 of them were

interim presented by 24 FMs

The word “Budget” has its origins in the French

“bougette”, a “leather bag” or “purse”, which in turn is

rooted in the Latin “bulga”, which roughly translates to a

pouch

The first words for the first budget ever passed in the

house were “when I presented my interim budget for free

India’s Parliament a few months back”

Indian Finance Ministers have made it to the PM- Charan

Singh, Morarji Desai, VP Singh, Manmohan Singh

John Mathai presented the first Railway budget for inde-

pendent India. He later became the finance minister and

had also presented the Union Budget in 1949 and 1950

Only Manmohan Singh and P Chidambaram have present-

ed all the 5 budgets for a government.

Jawaharlal Nehru, Indira Gandhi and Rajiv Gandhi all have

presented Budgets because their finance ministers had

resigned .

InFINeeti | Annual Issue | January 2014

30

INTRODUCTION

A roadmap to sustainable growth requires a nation to achieve a

stable platform that will provide it with a good launch pad. First

and foremost, the nation needs to identify its roadblocks and

leverage its strengths to overcome such obstacles.

In recent times, India has lost its image of an attractive invest-

ment location to that of an economy amidst uncertainty. Ac-

cording to Indian Born Pepsico Chairman and CEO Indra Nooyi,

India is no longer a 'must-invest' market for the foreign investors

but has been a 'must-deal-with' country in respect of the poor

investment climate prevalent in the country. Nooyi went on to

say that, "Must-invest” means it's a destination and GDP is grow-

ing. “Must deal with” means there are infrastructure issues, the

taxation policy is not clear or transparent. So people are saying,

'Do I have to deal with India?'

COMPLEXITIES OF THE INVESTMENT CLIMATE

The unchecked corruption, poor governance, looming elections

and a sluggish economy has tarnished India's image in the world

market. Investor sentiments have declined and so has the econ-

omy.

The past three decades have been phenomenal for India, grow-

ing at an average annual rate of above 6%, seeming to give Chi-

na, a close competition. However, the Indian ‘elephant’ and its

bumbling tale are no longer touted as one to look up to. After a

rapid growth of 8.5% in the last decade, the economy experi-

enced a downturn since the end of 2012, reporting a startling

figure of 4.4% growth in Q1, 2013. Despite the rise in exports

following the slump in the rupee, the Current Account Deficit

was at 4.9% in Q1, 2013, still higher than that of the previous

quarter.

However a paradox has always existed between the growth

story and the business climate regulations.

Most of the investments require government clearance. Busi-

nesses are required to seek authorization from regulatory bodies