inequality and the financial crisis - acca · pdf fileinequality and the financial crisis:...

TRANSCRIPT

Headline News: US Income Inequality Soars to Highest Levels on Record since 1917

3

Inequality troubles not only the poor but also the rich & powerful

Janet Yellen

Lee Ka Shing

World Economic Forum

4

2013 - top 5% HH own 63% wealth; bottom 50% own 1%

5

Li Ka-shing

6

WEF: Wealth Gap –biggest global risk in coming years

7

Objectives

To show how inequality is both a cause of the recent Great Financial Crisis (GFC)– the neglected imbalance in financial crisis

And also a consequence of the GFC

Move beyond just reforming international financial architecture

Need to address international economic architecture

8

Three Levels of Causes to the Financial Crisis

I Level of Theory and Methodology

Efficient Market Hypothesis (EMH)

Fallacy of Composition in Econ Theory

II Level of Banking Industry

III Level of structural imbalances

Current account imbalances

Imbalance btw finance & real econ

Wealth & Income imbalance

9

Level of Theory & Methods - Failure of Economics

Paul Krugman:

“Much of the past 30 years of macroeconomics was spectacularly useless at best, and positively harmful at worst.”

Barry Eichengreen: “the crisis has cast into doubt much of what we thought we knew about economics.”

10

Level of Banking Industry: Financial Deregulation & Frequency of Financial Crises

11

Structural Imbalance – Financialization of Economy – Finance largest share of GDP

12

0%

5%

10%

15%

20%

25%

30%

1960 1970 1980 1990 2000 2006

Per C

en

t o

f U

.S.

GD

P

Year

U.S. - Financial vs Manufacturing Sector as

% of GDP

Manufacturing Sector Financial Sector

Structural Imbalance – Finance highest profit share

13

Structural Imbalance – Financial debt is largest

14

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

US

$

Billi

on

s

Year

U.S. Domestic Debt

1960-2007

Financial Sector Non-Financial Corporate

Household Sector Government

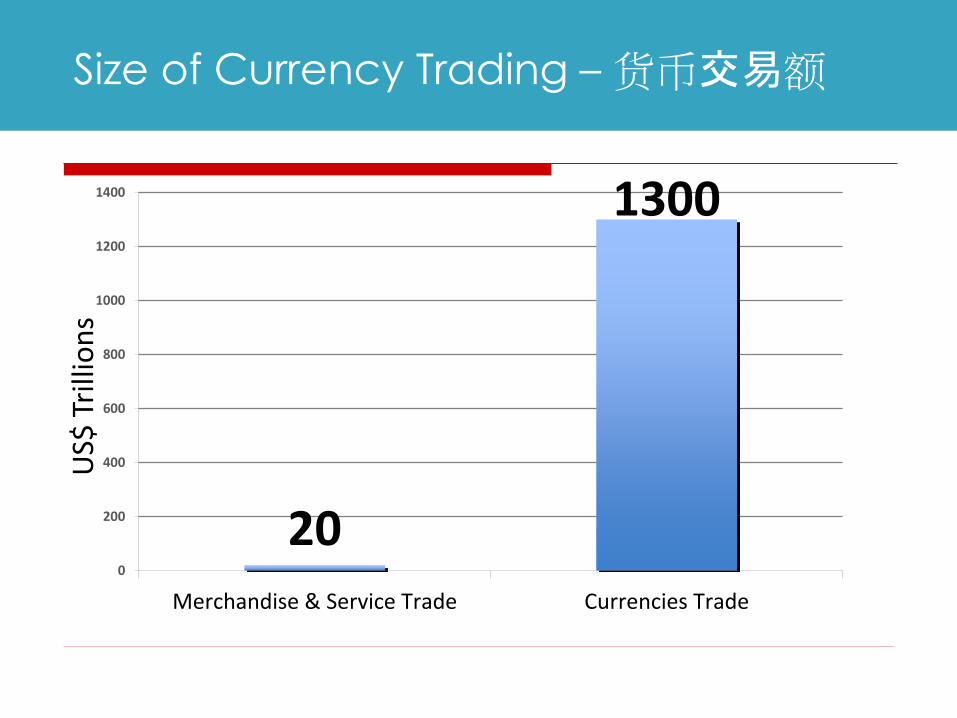

Size of Currency Trading – 货币交易额

20

1300

0

200

400

600

800

1000

1200

1400

Merchandise & Service Trade Currencies Trade

US$

Tri

llio

ns

Financial derivatives - 13x world’s GDP (2007)

16

Inverted Liquidity Pyramid - $607 trillion - 13 x world GDP

IMF 2012 Study – Too Much Finance? by J-L Arcand

Relation btw finance & growth is non-monotonic; fin contributes to growth

After a certain point too much finance is negative for growth – its marginal benefits are outweighed by marginal costs i/t of effect on fin instability and crises

17

Barclays --巴克莱银行

Fundamental Problem in Financial Industry

Too big

Too speculative

Finance -from servant of real economy to master

From being a means to an end in itself

19

Great Myth – rising tide lifts all boats

Neglected Imbalance in Financial Crises - Inequality

21

Functional Income Distribution (FID) – another measure of inequality

Definition of FID = How GDP distributed btw Labour (Wage + benefits) & Capital

Labor or Wage Share declining in most countries

22

Declining Wage Share of GDP in many countries (1970-2010)

Source: UNCTAD, TDR 2012 & CEIC

23

U.K. Wage Share of GDP, 1970-2013

Source: OECS Stats

24

U.S. – Rising & Declining Wage Share

25

26

CEO’s Pay, Corp Profits, S&P 500 Prodn Workers Pay, Fed Min wage

1990-2005

Minm wage minus 9% Prodn Workers Pay + 4% Corp Profits + 107% S&P 500 +141% CEO’s Pay +300%

27

Why Wage Share Declining? U.S.- Wages Lag Behind ProductivityGrowth

U.K. Productivity vs Wage Growth 1990-2012

28

How Inequality - A Cause of Great Financial Crisis

Wage – not just a cost item as assumed by neo-classical economists

Wage- imp factor aggregate demand

Falling Wage share of GDP means falling private demand/consumption

How to counter falling aggr demand?

Two ways : (a) increase personal (household) debt (b) increase exports

29

U.S. Debt Driven Economy

Econ growth powered by household debt – credit card, home mortgages > debt bubble

Private consumption is 72% of GDP

Fin industry recycled savings to debt

30

U.S. GDP Grew 27x; Total Debt Grew 64x btw 1960 & 2007

31

Hsehold Debt rose 64x from 40% to 100% GDP(1960-2007)

32

Debt Bubble

Excess Savings of Rich Invested in Risky Financial Products

Most of income gains accrued to top 1% of households

Marginal Propensity to consume of rich much lower than the poor

Excess savings chasing for high yields and invested in risky assets (financial innovation) > asset bubble

BOTH BUBBLES IMPLODED 2007

34

Asset Bubble

Fin Innovations – ATM Machines is abt the

only beneficial fin innovation in recent yrs

Fin Innovations – liken to financial weapons

of mass destruction

Turn to the China Story

China (current account surplus)

Declining wage share > decline in private consumption fr over 50% to 35% of GDP

Growth propped up through investments and export

Export rose fr <5% to 20% of GDP

Export earnings invested in US treasury & agency securities

Poor try financing rich country

39

China: Falling Wage Share & Consumption; Rising Exports

40

Summary

Global trade imbalance related to inequality & declining wage share

Shows up as debt & current account deficit in some ctries (U.S.) and export & current account surplus in others (China)

Both debt driven & export driven growth - financial & economically unstable & unsustainable

41

Any Significant Change in International Fin Architecture?

42

Consequence of Financial Crisis

World wide – pump priming & loose monetary policies

Unconventional monetary policy – quantitative easing world-wide

Fed balance sheet swollen to $4 trillion

Excess liquidity – flowing more into financial markets than real economy

43

U.S. - Private non-residential fixed investm–stagnating around 10% GDP

44

Asset Bubbles in the making

With negative real interest rates, funds flowing into property, stocks and bonds

Only people with money able to take advantage of rise in fin assets prices resulting fr QEs, exacerbating inequality

45

U.S. S&P, Corp Profit, Wage Indices 1990-2012

46

Conclusion and Policy Implications

Inequality + Financialization = a toxic mix that resulted in financial crisis

Policy Implications:

Need to fix inequality issue

Need to fix finance

47

Addressing issue of Inequality

Senator Elizabeth Warren:

“Any effective policy has to start with the households. Years of flat wages, low savings and high debt have left America’s households extremely vulnerable”

48

Reducing Inequality : can be ex-ante or ex-post

Ex-ante – wages tied to productivity growth; should not be less or more than productivity growth

Ex-post – have correct fiscal policies; reduce present bias in favor of capital

Increase capital gains tax-graduated, esp for ST speculative transactions

> 50% of stock trading avg holding time 10 seconds –high freq trading

49

Better Regulation of Finance

Need finance to serve real economy but NOT financialization which drives speculation and bubbles

Finance needs to be better regulated because finance is an industry with high negative externalities

50

3 Issues in Restructuring Internat’l Fin Architecture

More comprehensive

Capital Controls

Tax Havens

51

I- Comprehensive

Include shadow banking system as banks acct for only 25% of tot fin assets; hedge funds leverage much higher

Focus on systemic risks not just individual institutions

Must have global regulatory system

Global resolution system for failed banks & sovereign debt restructuring

52

II – Capital Controls

A major source of financial & econ volatility & instability is related to free capital flows esp of short-term nature

Carry trades undermine national monetary policies e.g., raise int rate to cool inflation can end up attracting more ST capital inflows – US,NZ

QE major source surge in international liquidity & asset bubbles

53

Capital Controls

Emerging mkt economies need the policy space to control inflow and outflow of capital; difficult to do it at individual level

Problem needs to be dealt with globally or at least regionally

International financial architecture must allow for use of capital controls as part of policy tools

54

III- Tax Havens

More international coordination to control tax havens that encourage regulatory arbitrage

Standardize accounting standards and country by country reporting of key data beyond extractive inds

Require declaration of beneficial ownership

55

Last Words

George Santayana(philosopher)

“Those who cannot remember the past are condemned to repeat it”

56

Thanks.