industrial policy 15yr review prepared in 2008.pdf - tips

TRANSCRIPT

A Review of Industrial Policy, Instruments and Support Programmes: 1994-2008

Zavareh Rustomjee and Stephen Hanival

A Contribution to the Presidency's 15-year Review of Government

Performance

Released June 2010

Prepared March 2008

indigenous growth

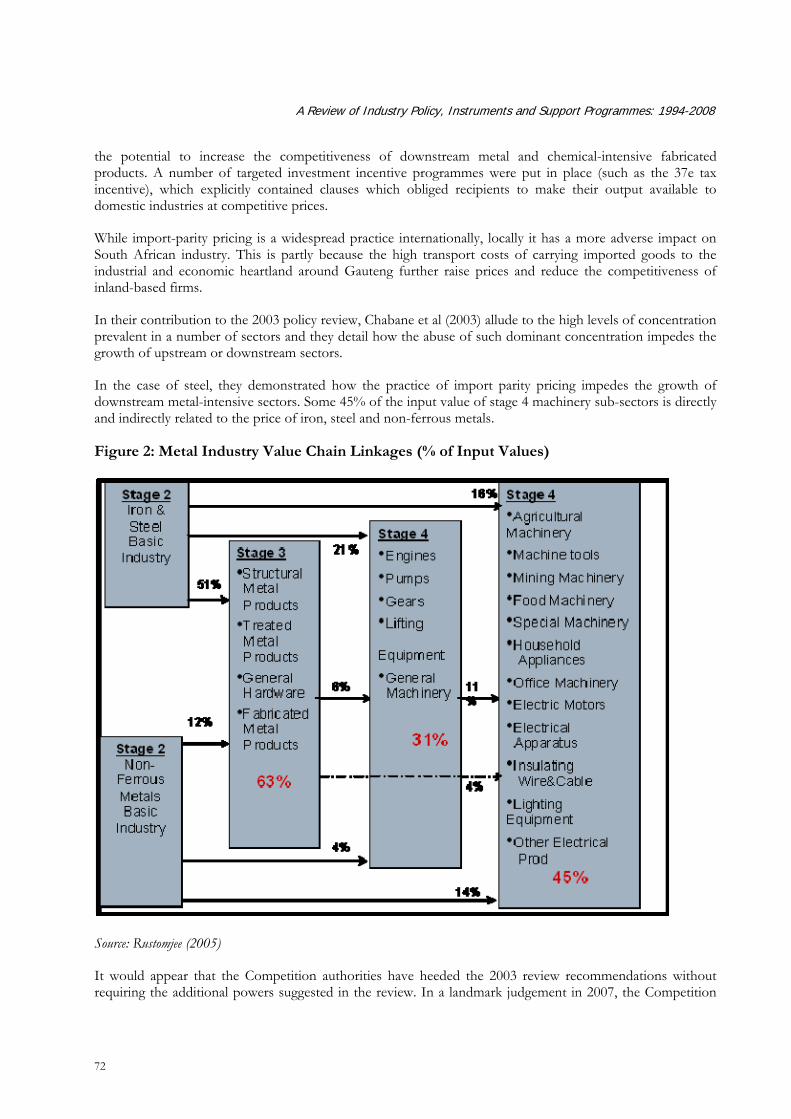

A Review of Industry Policy, Instruments and Support Programmes: 1994-2008

A Contribution to the Presidency’s 15-year Review of Government Performance1

Prepared March 2008

Released June 2010

1 Report prepared by Zavareh Rustomjee and by Stephen Hanival

A Review of Industry Policy, Instruments and Support Programmes: 1994-2008

2

Contents

TABLES....................................................................................................................................................................... 3 FIGURES..................................................................................................................................................................... 4 ABBREVIATIONS AND ACRONYMS ................................................................................................................... 5 ABBREVIATIONS AND ACRONYMS ................................................................................................................... 5 1. INTRODUCTION.............................................................................................................................................. 6 2. TEN-YEAR REVIEW: TRADE AND INDUSTRY POLICY ISSUES AND CONCLUSIONS ................. 7

2.1 MACRO-ECONOMIC STABILITY ..................................................................................................................... 7 2.2 TRADE POLICY, TRADE REFORM AND ACCESS ............................................................................................... 8 2.3 INDUSTRIAL POLICIES, COMPETITIVENESS & INDUSTRIAL PROMOTION......................................................... 8 2.4 COMPETITION POLICY AND REGULATION...................................................................................................... 9 2.5 SMALL, MEDIUM AND MICRO-ENTERPRISE SUPPORT..................................................................................... 9 2.6 BROAD-BASED BLACK ECONOMIC EMPOWERMENT....................................................................................... 9 2.7 RESEARCH AND DEVELOPMENT (R&D)........................................................................................................ 9 2.8 HUMAN RESOURCE DEVELOPMENT (HRD)................................................................................................. 10 2.9 INSTITUTION BUILDING............................................................................................................................... 10

3. TERMS OF REFERENCE AND PROPOSED METHODOLOGY............................................................ 11 3.1 TIMELINE ................................................................................................................................................... 11 3.2 METHODOLOGY.......................................................................................................................................... 11 3.3 DATA.......................................................................................................................................................... 12 3.4 INTERVIEWS ............................................................................................................................................... 12

4. REVIEW OF SOUTH AFRICA’S ECONOMIC PERFORMANCE 1994-2002 AND 2003-2007............ 13 4.1 INTRODUCTION........................................................................................................................................... 13 4.2 REVIEW OF SOUTH AFRICA’S ECONOMIC PERFORMANCE 1994-2007 ......................................................... 13

4.2.1 Domestic performance .......................................................................................................................... 13 4.3 CONCLUDING REMARKS ............................................................................................................................. 24

5. ASSESSMENT OF THE EFFECTIVENESS OF KEY INDUSTRIAL POLICIES, PROGRAMMES AND PROJECTS ...................................................................................................................................................... 26

5.1 INTRODUCTION – THE EVOLUTION OF DTI INCENTIVE PROGRAMMES: 1994-2005 ....................................... 26 5.2 THE CHANGING STRUCTURE AND APPLICATION OF DTI INCENTIVES: 1994-2005 ........................................ 27 5.3 BREADTH AND DEPTH OF TARGETS COVERED BY DTI FAMILY INCENTIVES ................................................. 29 5.4 VALUE OF DTI INCENTIVES : 2001-2005 ..................................................................................................... 31 5.5 THE PERFORMANCE OF INCENTIVE INSTRUMENTS: INCENTIVE PROGRAMME REVIEWS ............................... 31 5.6 THE PERFORMANCE OF COMPETITIVENESS PROGRAMMES.......................................................................... 32

5.6.1 Sector Partnership Fund (SPF)............................................................................................................. 32 5.6.2 Competitiveness Fund (CF) and Sector Partnership Fund (SPF)......................................................... 33 5.6.3 Technology and Human Resourced for Industry Programme (THRIP) ................................................ 34 5.6.4 Support Programme for Industrial Innovation (SPII)........................................................................... 34 5.6.5 Conclusions – competitiveness programmes......................................................................................... 35

5.7 EXPORT MARKETING AND INVESTMENT ASSISTANCE PROGRAMME (EMIA)............................................. 35 5.8 BROAD-BASED BLACK ECONOMIC EMPOWERMENT..................................................................................... 36

5.8.1 Assessment of Incentive Programme impact on MSME targets – World Bank (2006).......................... 37 5.9 ASSESSMENT OF IMPACT OF SMEDP INCENTIVE ON MEAN EFFECTIVE TAX RATES OF RECIPIENT FIRMS – FIAS (2005) REVIEW............................................................................................................................................... 38 5.10 SPATIAL DEVELOPMENT PROGRAMMES ...................................................................................................... 41

5.10.1 Spatial Development Initiatives (SDI) .............................................................................................. 41 5.10.2 Industrial Development Zones (IDZ) ................................................................................................ 41 5.10.3 Critical Infrastructure Fund (CIF) ................................................................................................... 43

5.10.4 2006 Regional Industrial Development Strategy (RIDS) and associated Spatial Industrial Development Strategy ........................................................................................................................................ 44 5.10.6 Conclusion – RIDS Proposals .......................................................................................................... 45

6. ESTIMATED VALUE, SECTORAL SPREAD AND IMPACT ON GFCF 2000-2005 OF DTI INCENTIVES............................................................................................................................................................ 47

6.1 TAX-BASED INCENTIVES............................................................................................................................. 47 6.2 GRANT-BASED INCENTIVES ........................................................................................................................ 49 6.3 MOTOR INDUSTRY DEVELOPMENT PROGRAMME (MIDP) ........................................................................... 51 6.4 DUTY CREDIT CERTIFICATE SCHEME (DCCS)............................................................................................. 52 6.5 INDUSTRIAL PARTICIPATION PROGRAMME (NIP)....................................................................................... 55 6.6 ROLE OF DEVELOPMENT FINANCE INSTITUTIONS AND ENTERPRISE DEVELOPMENT AGENCIES ................. 56 6.7 INCENTIVES – IDC CONCESSIONARY FINANCING PROGRAMMES 1994-2004 ............................................. 58 6.8 THE IDC’S APPROACH TO FINANCING PROJECTS ....................................................................................... 59 6.9 POST 2006 - NATIONAL INDUSTRIAL POLICY FRAMEWORK (NIPF) AND THE INDUSTRIAL POLICY ACTION PLAN (IPAP) ........................................................................................................................................................... 62 6.10 CONCLUSIONS – IMPACT OF THE DTI’S PAST INCENTIVES ON INDUSTRY ..................................................... 64

7 WHAT PROGRESS SINCE 2003?................................................................................................................. 68 7.1 MACROECONOMIC STABILITY .................................................................................................................... 68 7.2 TRADE POLICY, TRADE REFORM AND ACCESS ............................................................................................. 68 7.3 INDUSTRIAL POLICIES, COMPETITIVENESS AND INDUSTRIAL PROMOTION ................................................... 69 7.4 COMPETITION POLICY AND REGULATION.................................................................................................... 71 7.5 SMALL, MEDIUM AND MICRO-ENTERPRISE SUPPORT................................................................................... 73 7.6 BROAD-BASED BLACK ECONOMIC EMPOWERMENT..................................................................................... 74 7.7 RESEARCH AND DEVELOPMENT (R&D)...................................................................................................... 74 7.8 HUMAN RESOURCE DEVELOPMENT (HRD)................................................................................................. 74 7.9 INSTITUTION BUILDING............................................................................................................................... 75

REFERENCES.......................................................................................................................................................... 76

Tables Table 1: Structure of South Africa’s economy.......................................................................................................................15 Table 2: Structure of South Africa’s economy: primary sector ...........................................................................................16 Table 3: Structure of South Africa’s economy: secondary sector .......................................................................................16 Table 4: Growth trends: manufacturing sectors, 2004-2006 ...............................................................................................18 Table 5: Growth trends: manufacturing sectors, 2000-2003 ...............................................................................................19 Table 6: 1994-2006: changes in incentive structure and application...................................................................................28 Table 7: dti family investment incentives...............................................................................................................................29 Table 8: dti trade facilitation incentive programmes ............................................................................................................30 Table 9: dti competitiveness programmes .............................................................................................................................30 Table 10: Historic value of dti incentives (Rm) ....................................................................................................................31 Table 11: dti budget analysis....................................................................................................................................................31 Table 12: Programmes that have been reviewed since 1994 ...............................................................................................32 Table 13: Summary of key FIAS (2005) issues and recommendations ..............................................................................39 Table 14: Impact of incentives on recipient mean effective tax rate (METR) ..................................................................40 Table 15: SDI initiatives ...........................................................................................................................................................41 Table 16: SIP tax incentive impact as %GFCF.....................................................................................................................47 Table 17: SMEDP grant incentive impact on % GFCF ......................................................................................................50 Table 18: NIP investment impact on % GFCF ....................................................................................................................56 Table 19: IDC Financing Instruments 1988 - 2000 ..............................................................................................................60

3

A Review of Industry Policy, Instruments and Support Programmes: 1994-2008

4

Table 20: NIPF Strategic Programmes...................................................................................................................................63 Table 21: Proposed NIPF Sector Clusters .............................................................................................................................63

Figures Figure 1: Ten-year review: Trade and industrial policy components.................................................................................... 7 Figure 2: GDP year-on-year growth rate................................................................................................................................14 Figure 3: Structure of South Africa’s economy ....................................................................................................................14 Figure 4: Year-on-year growth of total economy and manufacturing................................................................................17 Figure 5: Manufacturing performance by sector (weighted annual % change).................................................................18 Figure 6: Underperformance of the South African economy in creating jobs..................................................................20 Figure 7: Key manufacturing sectors’ employment performance.......................................................................................21 Figure 8: Manufacturing employment sorted by year: 2000-2003.......................................................................................21 Figure 9: GDFI, 2000-2003 and 2004-2006...........................................................................................................................22 Figure 10: Growth in manufacturing sector capacity utilisation .........................................................................................23 Figure 11: Manufacturing GDFI, 2000-2003 and 2004-2006..............................................................................................23 Figure 12: Manufacturing GDFI: shares ................................................................................................................................24 Figure 15: CIP payments – key sector investments supported 2003-2006 ........................................................................43 Figure 16: SIP tax incentive impact as %GFCF....................................................................................................................48 Figure 17: SMEDP grant incentive impact as %GFCF .......................................................................................................50 Figure 18: DCCS incentive benefit as % Textile GFCF ......................................................................................................53 Figure 19: DCCS incentive benefit as % Textile exports.....................................................................................................53 Figure 20: DCCS incentive benefit as % Apparel GFCF ....................................................................................................54 Figure 21: DCCS incentive benefit as % Apparel Exports..................................................................................................54 Figure 22: NIP investment value by sector – 2001-2005 .....................................................................................................55 Figure 23: IDC Financing as % Total National GFCF ........................................................................................................59 Figure 24: IDC Project Value by Beneficiation Stage – Metals & Chemicals 1994-2004................................................60 Figure 25: IDC Project Value by Beneficiation Stage – Metals and Chemicals 2000-2004.............................................61 Figure 26: IDC Financing as % GFCF in Chemicals 1994-2004........................................................................................61 Figure 27: IDC Financing as % GFCF in Metals 1994-2004 ..............................................................................................62 Figure 28: All dti investment incentives as %GFCF 2001-2005 ........................................................................................66 Figure 18: Metal Industry Value Chain Linkages (% of Input Values) ..............................................................................72

Abbreviations and acronyms ASGISA Accelerated and Shared Growth Initiative for South Africa BBSDP Black Business Supplier Development Programme BOSME Black-Owned Small and Medium Enterprises BPO Business Process Outsourcing CF Competitiveness Fund CIF Critical Infrastructure Fund CIP Critical Infrastructure Programme CPPP The Community Public Private Partnership Programme CSA Customs Secured Areas CSIR Council for scientific and industrial research CSP Customised Sector Programme DCCS Duty Credit Certificate Scheme the dti Department of Trade and Industry ECDC Eastern Cape Development Corporation EIG Empowerment Investment Grant EMIA Export Marketing and Investment Assistance FIAS Foreign Investment Advisory Service GAP Geospatial Analysis Platform GDFI Gross Domestic Fixed Investment GDP Gross Domestic Product GFCF Gross Fixed Capital Formation GFCF Gross fixed capital formation HDI H istorically disadvantaged individual IDZ Industrial Development Zone IRCC Import Rebate Credit Certificates ISRDP Integrated Sustainable Rural Development Programme LED Local Economic Development METR Mean effective tax rate MIDP Motor Industry Development Programme MSME Micro, small and medium enterprises MTEF Medium term expenditure framework NIP National Industrial Participation Programme NIPF National Industrial Policy Framework NSDP National Spatial Development Perspective RIDS Regional Industrial Development Strategy SDI Spatial Development Initiatives SETI Sector education and training institute SIDS Spatial Industrial Development Strategy SIP Strategic Investment Programme SMEDP Small and Medium Enterprise Development Programme SMMDP Small and Medium Manufacturing Development Programme SOE State-owned Enterprises SPF Sector Partnership Fund SPII Support Programme for Industrial Innovation THRIP Technology and Human Resources for Industry Programme TWIB Technology for Women in Business URP Urban Renewal Programme

5

A Review of Industry Policy, Instruments and Support Programmes: 1994-2008

6

1. Introduction

In 2003, as part of the Presidency’s review of the ten-year period 1994-2003, the impact of trade and industry policy was assessed. The review came to a generally positive conclusion, recording that while some progress had been made. However, certain adjustments and prioritisation were needed. The details of this trade and industry policy analysis are contained in Section two below.

Section three records the terms of reference (TOR) for this study and outlines the methodology utilised in conducting this study. The methodology essentially builds on the policy analysis, themes and priorities that were recognised during the 2003 review, drawing on and integrating the considerable wealth of primary research on trade and industry policy that exists.

Using the same approach as the 2003 review, South Africa’s economic performance between 2002 and 2007 is analysed in Section four. For consistency, the datasets and analysis of Cassim et al. (2003) are adopted and updated.

The TOR calls for a cost-benefit analysis of the various government industrial support measures, and Section five addresses this by drawing from recent work commissioned by the dti2. In Section six, particular attention is paid to the key investment incentive programmes which absorb the bulk of fiscal resources allocated to industrial policy.

In Section seven, trade and industry policies are organised in accordance with the policy themes/tools used in the 2003 review. Progress since 2003, measured against the empirical analysis of Sections five and six, is assessed and an attempt is made to draw out the main policy debates, policy contestations and implementation issues during these past five years.

At the same time, the key policy ideas and debates are periodised over the fifteen year period. The choices made, and the determinants of such policy decisions (where they are identifiable) are captured. The chapter concludes by linking the historical flow of policy ideas with the main trade and industry policy ideas that are currently seeking to influence policy makers.

Conclusions are drawn in Section eight on whether government’s industrial and trade policies, programmes and projects have been effective or not, since 2003 and over the 15 year period under review.

2 Rustomjee (2005), dti Incentives review process (Phase 1) – Incentives policy framework, Final report, 16 November. A study commissioned by the dti, Pretoria

2. Ten-year review: trade and industry policy issues and conclusions

The ten-year review set out to answer the following questions:

Has the government achieved its policy objectives?

Are these the appropriate objectives?

Against the backdrop of sound macroeconomic fundamentals, a strong fiscus, relatively low private sector investment and steadily increasing public sector investment in the economy, the Presidency (2003) noted certain achievements regarding economic policy and trade and industry policy, as well as a number of challenges that required prioritised attention after 2003. These achievements and challenges over the ten-year period 1994-2003 are listed below using the 2003 review thematic headings/tools; headings which are used in subsequent Sections that review progress from 2003-2008.

Figure 1: Ten-year review: Trade and industrial policy components

Source: The Presidency (2003; p.32)

2.1 Macro-economic stability

The 2003 review concluded that the government had been successful in ensuring macro-economic stability, improving the trade regime, and taking advantage of the country’s natural resources and financial and physical infrastructure. Significant progress was recorded in the main areas primarily under the control of the State (such as fiscal and monetary policy, and trade and industrial policy) but government had had less success in other areas (competition policy, restructuring and improving the performance of government and regulatory institution and agrarian reform).

7

A Review of Industry Policy, Instruments and Support Programmes: 1994-2008

8

Continuing with prudent macro-economic policies to achieve a more stable currency and lower real interest rates, and to improve the public sector’s investment performance, were to be prioritised post 2003.

2.2 Trade policy, trade reform and access

The 2003 review observed that industrial support measures between 1994 and 2003, coupled with the implementation of tariff reform as an instrument of industrial policy in line with the RSA’s WTO commitments, have led to a more competitive economy and an improved trade balance.

The improved trade balance, reflected in the growth of higher value added, secondary and tertiary exports, had also arisen from the renegotiated SACU trade agreement, the negotiation of a Southern African Development Community (SADC) free trade agreement, the negotiation of a bilateral trade and aid agreement with the European Union and through the unilateral USA-African Growth and Opportunity Act (AGOA) provision, which had also aided South Africa’s exports,

Going forward, the review recommended that South Africa should continue to lead developing country participation in the Doha Round of the World Trade Organisation WTO and continue to pursue mutually beneficial free trade talks with the USA and with fast growing emerging regions such as Mercosur and countries such as China and India.

2.3 Industrial policies, competitiveness & industrial promotion

The 2003 review noted that industrial policy had shifted focus since 2001, as articulated in the Integrated Manufacturing Strategy and the Micro-economic Reform Strategy, extending incentive programmes beyond traditional manufacturing sectors.

Certain key industries had been targeted for special attention, including growth sectors such as automotive and tourism, and cross-cutting sectors such as information and communications technology. In the case of the latter two, these sectors had become recipients of considerable resources allocated through government’s science and technology and human resource development programmes.

As a result of policy interventions, the competitiveness of the South African economy had improved since the early 1990s as reflected by the improvement in and diversification of exports, as well as the significant improvement in labour productivity. However, most measures still indicate that the availability of skilled labour remains a key constraint to further growth.

Arising from the improved investment climate in South Africa, foreign direct investment (FDI) had been net positive since 1994, although it was regarded as being low in comparison with other developing economies. FDI had been largely associated with state-leveraged deals and through the privatisation of state assets.

A simultaneous outflow of capital into the Southern African region had occurred, reflecting the increasing economic integration that is taking place, consciously encouraged by policymakers.

The review noted that the country’s small skills base, the volatility of the exchange rate and the interest rate, the cost of inputs such as transport and telecommunications, lack of competition in the domestic market, and poor perceptions of Africa and southern Africa were holding back higher rates of investment and required focused attention.

The review pointed to the opportunity to better use South Africa’s infrastructure to provide low-cost services, to continue to add more value to the processing and manufacturing sectors, and to reduce South

Africa’s risk rating through better marketing. However, it noted that competition from Asia and other parts of Africa, slow improvements in skills and input costs, and weaknesses in implementation continued to hold back such progress.

The 2003 review resolved to implement the Growth and Development Summit (GDS) recommendations to identify sectors for urgent investment and learnerships, to support focused sector strategies in key growth and employment industries following the examples of the motor industry and the tourism sector, and to speed up the restructuring of all industries to ensure global competitiveness, lower input prices and better access to key markets. The review further recommended the development of suitable instruments to direct 5% of the investible income of a wide range of public and private organisations, including the pension funds and insurance companies, towards job creating and poverty alleviating projects.

2.4 Competition policy and regulation

The Competition Commission and Tribunal had built up a solid reputation in implementing the new Competition Act of 1996. However, the review concluded that they had not been as effective as expected in addressing abuses of dominant positions in certain key intermediate product groups such as beverages, paper and paper products, coke and petroleum products, basic chemicals, basic non-ferrous metals, and, to a lesser extent, ferrous metals, whereby price mark-ups were regarded as high by international standards.

The review also noted concerns about the high cost of transport and telecommunications, key factors in an economy at such great distance from major world markets, and that a focus was needed on the microeconomic reform strategy on input costs and skills.

The review called for increased effectiveness of SOE restructuring in accordance with prevailing policy, through more effective managed liberalisation and stronger regulators, and that the powers of the competition authorities to deal with anticompetitive practices be strengthened.

2.5 Small, medium and micro-enterprise support

Noting that the institutional support for SMMEs since 1994 had led to increasing measured contributions of such firms to economic activity and employment, the review regarded the challenge for the next period to be to disaggregate and focus strategies with regard to distinctively different sectors of the SMME community, i.e. micro businesses (often informal), small businesses, small technology start-ups and medium-sized businesses.

2.6 Broad-based black economic empowerment

The review recommended that adequate resources be provided to strengthen the broad-based empowerment programme, including the agrarian reform programme and micro-credit to support productive enterprises.

2.7 Research and development (R&D)

The review noted that industrial policy had not yet resulted in greater levels of domestic innovation and R&D, but that this was expected to improve as a result of the increasing coherence of, and resources being applied to, the national system of innovation that had been adopted as policy in the late 1990s – particularly after the introduction of the 2002 R&D Strategy which established new, relevant missions for the NSI. Expenditure on R&D averaged around 0.75% of GDP for most of the 1990s, and was recorded at 0.8% in 2003.

9

A Review of Industry Policy, Instruments and Support Programmes: 1994-2008

10

Post 2003, government should ensure implementation of the Research and Development Strategy, both in high-level niche areas such as fuel cell technology and issues related to immediate poverty eradication and protection of the environment.

2.8 Human resource development (HRD)

The 2003 review noted that government had made less immediate progress in a significant number of areas that require partnership with others (small business development, HRD, innovation and R&D, restructuring of SOEs and BEE). In those areas that depended significantly on private sector and civil society attitudes and behaviour and are only indirectly influenced by the State (investment and employment creation), government had had even less success. Acknowledging externalities between these areas, the review noted that, by 2003, the soundness of macro-economic policy and industrial strategy was beginning to positively influence investor attitudes. Unfortunately, this change in attitude had yet to translate into significantly increased employment and consequent poverty reduction.

Post 2003, the review pointed to the need to focus on targeted skills development and steady improvement in the education system and the functioning of the labour market.

2.9 Institution building

In 2003 the review recognised that, although successes were recorded in fiscal reform, these successes had not yet reached a few of the provinces and many municipalities. Consequently, existing policies and programmes needed to embed themselves more effectively across national, provincial and municipal levels of government.

Though economic policy processes had been sound, one of the key limitations in the implementation of economic policy had been the cost of institution building. Institutions such as some of the small business agencies, the National Empowerment Fund, the National Development Agency, the Umsobomvu Fund, some of the SETAs, and many local government -level economic agencies had taken a great deal of time to become effective. Some key lessons had been that the cost of institution building should not be underestimated, and that, where possible, new tasks should be incorporated into the work of existing successful agencies. In addition, some rationalisation of existing institutions might lead to medium-term gains, though these would have to be weighed against the costs of rationalisation.

3. Terms of reference and proposed methodology

The terms of reference for this study are as follows:

The Policy Unit in the Presidency is conducting a fifteen-year review of government business. The main aim of the review is:

To assess the outcome and impact of policies, programmes and projects as implemented by government since 1994, with particular emphasis on the current electoral mandate period (i.e. since 2004). The study/paper should take into consideration (be based on) the conclusions of the ten-year review,

To identify the impact of government industrial programmes and instruments, To provide analysis and evidence of reasons for the success (and sustainability) or failure of the dti

SMEDP, SIP, IDZs, SDIs, MIDP and other support measures such as customised sector programmes, including an analysis of various industrial support programmes at a local and provincial level,

To provide an overall cost-benefit analysis of the various government industrial support measures and programmes at national, provincial and local level,

To establish how effective government’s industrial support measures have been, To undertake systematic analysis of various government industrial support measures from national,

provincial and local level, and to use that as a basis for deducing the success or failure of government industrial support for the period under review. Data should cover the period since 1994 if possible, and longer if desired. Data series used should be included in the report in tabulated form (in addition to graphs and formulae).

3.1 Timeline

First draft – 30 January 2008

Workshop discussion/discussions – 1-12 March 2008

Final report – 30 March 2008

3.2 Methodology

The 2003 review organised its analysis of trade and industrial policy according to the following themes/policy tool areas:

Macro-economic stability,

Trade reform and market access,

Industrial policies,

Foreign direct investment,

Competition policies,

Encouraging SMMEs,

Skills development,

Affirmative action (empowerment),

11

A Review of Industry Policy, Instruments and Support Programmes: 1994-2008

12

Support innovation, research and development,

Land reform.

In each of these areas, the 2003 review highlighted the progress made over the period 1994-2003 and recommended certain priorities for the next five-year period. Subsequent sections of this report assess the impact of implementing the 2003 priorities by drawing on and integrating a considerable wealth of primary research on trade and industry policy, including the research on which the ten-year review was based.

Relevant research, analysis and literature mainly (but not exclusively) since 2003 has been reviewed and organised into a comprehensive industrial policy bibliography and database. This is currently maintained on the Trade and Industrial Policy Strategies (TIPS) website and can be further updated and utilised beyond the life of this project.

3.3 Data

The data used include selected Stats SA and SARB statistical data series as well as the Quantec database.

3.4 Interviews

Following the planned review workshop, selected interviews may be conducted with key policy decision makers and implementers within the dti and government as part of the methodology.

4. Review of South Africa’s economic performance 1994-2002 and 2003-2007

4.1 Introduction

Industrial policy has long been a cornerstone of South African economic policy under both the previous and current governments. The previous government, by virtue of its international pariah status, was forced to develop a particularly interventionist industrial policy with significant state funding for ‘strategic’ investments and a raft of financial support measures. The latter spanned the full range of the life-cycle of a firm, including R&D, support, manipulation of consumer demand, production support and, indeed, export and tariff assistance. Although often excessively wasteful, the degree of coordination and financial support provided to industry was impressive.

The current government’s interest in industrial policy can be traced as far back as the Freedom Charter –

‘The national wealth of our country, the heritage of South Africans, shall be restored to the people;

The mineral wealth beneath the soil, the Banks and monopoly industry shall be transferred to the ownership of the people as a whole;

All other industry and trade shall be controlled to assist the wellbeing of the people;

All people shall have equal rights to trade where they choose, to manufacture and to enter all trades, crafts and professions.’

– which alludes to a broad range of what have become the de rigeur tools of industrial policy, including competition policy and economic regulation, as well as the clear linking of industrial policy to improvement in living standards. These commitments were further detailed in the RDP and GEAR policy statements and have played a significant role in influencing the policy and programme content of the South Africa’s industrial policy, primarily coordinated by the dti.

The purpose of this report is to review government’s progress on industrial policy and programmes and the effectiveness thereof over the 15-year period, 1994 to 2008, thereby coinciding with the end of the current Administration’s electoral mandate. We attempt to do this through an assessment of South Africa’s industrial performance, including in relation to global developments, and a detailed review of the performance of current industrial policy programmes and incentive schemes.

4.2 Review of South Africa’s economic performance 1994-2007

4.2.1 Domestic performance

Growth

South Africa’s economic performance has been positive and stable over the last 15 years. Figure 1 shows the extent to which the SA economy has progressed from the boom-bust cycles of the 1980s and early 1990s. The economy is currently experiencing its longest continuous growth phase in SA recorded history and this has been accompanied by a substantial acceleration of growth in the last 3/4 years as domestic investor confidence has grown. Moreover, the SA economy has also developed resilience to global developments with the East Asian crisis of 1998 only temporarily slowing the positive rate of growth.

13

A Review of Industry Policy, Instruments and Support Programmes: 1994-2008

14

Figure 2: GDP year-on-year growth rate (%, 1981-2006)

1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

6.00

5.00

4.00

3.00

2.00

1.00

0.00

-1.00

-2.00

The structure of the SA economy has, however, changed substantially during this period. Figure 3 shows the substantial increase in the importance of the tertiary sector of the economy which has become an important – and increasingly autonomous – driver of growth in SA.

Figure 3: Structure of South Africa’s economy – main economic sectors as % of total

0%

20%

40%

60%

80%

100%

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006Years

Primary Sector Secondary Sector Tertiary Sector

15

Table 1 provides more detail and shows three key trends:

The steady decline in the importance of the primary sector;

The early decline and later stabilisation of the secondary sector; and

The steady and substantial growth in the importance of the tertiary sector in overall GDP.

Table 1: Structure of South Africa’s economy – main sector as % of GDP, 1980 to 2006, selected years

1980 1985 1990 1995 2000 2005 2006

Primary Sector 15.5 14.3 13.1 11.7 10.8 9.7 8.8

Secondary Sector 27.6 26.1 26.0 25.0 24.2 23.5 23.6

Tertiary Sector 56.9 59.6 61.0 63.3 64.9 66.9 67.6

The main cause of the decline in the importance of the primary sector is the near halving of the contribution of the mining sector, with gold mining in particular in long-term decline as deposits are depleted or become increasingly difficult to mine. The substantial growth of the platinum mining industry is overshadowed by developments in gold, but has at least softened what would otherwise have been a near catastrophic – especially in employment terms – reduction in the primary sector’s contribution to economic growth. Substantial investments have been undertaken by both private sector and state agencies in the development of technology to support more productive gold mining – at lower depths and to recover precious metals not previously viable – but it is increasingly clear that the sector is a ‘grandfather’ industry and that its long term outlook is deeply negative.

Some of the social implications of this have already been addressed but there remain a number of key questions surrounding the extent to which the technical and intellectual capacity that has been accreted over its lifespan can be protected and re-focused on other important growth sectors. Moreover, the currently stalled General Agreement on Trade in Services (GATS) negotiations could provide a significant opportunity for SA. In terms of Mode 4 Access (movement of people) the ‘export’ of technical staff in mining and its associated industries could become a significant source of additional revenue for SA.3 Moreover, with SA’s large mining houses already exploiting mineral opportunities in a range of both developed – but mainly developing – countries, a successful GATS negotiation could assist in accelerating SA firms’ ability to viably prospect, develop and mine deposits around the globe. Sub Saharan Africa and SADC in particular remain difficult countries for foreign investors including – or in some cases especially for – SA firms.

3 One line of argument is that highly skilled expatriates working abroad eventually return to SA, often with significant savings which enters the domestic economy through consumer spending, additional demand for housing and investment.

A Review of Industry Policy, Instruments and Support Programmes: 1994-2008

16

Table 2: Structure of South Africa’s economy: primary sector - % of sector’s contribution, 1980 to 2006, selected years

1980 1985 1990 1995 2000 2005 2006 Primary Sector 15.5 14.3 13.1 11.7 10.8 9.7 8.8

Agriculture, Forestry and Fishing [1] 3.7 3.3 3.7 2.9 3.3 2.9 2.4

Mining and Quarrying [2] 11.8 11.0 9.4 8.9 7.6 6.8 6.4

Coal Mining [21] 1.9 2.3 1.7 1.5 1.4 1.3 1.0

Gold and Uranium Ore Mining [23] 4.9 4.6 3.9 2.9 2.0 1.2 1.0

Other Mining [22/24/25/29] 4.9 4.0 3.8 4.5 4.1 4.3 4.5

Table 2 shows that Agriculture too has not performed very strongly and, although subject to climatic conditions and the availability of arable land, its growth has not kept pace with the growth of the economy more generally. Moreover, the decline in its contribution comes against the backdrop of strong local and international consumer demand, especially in the last four years. As is argued in the 15 Year Review of Agriculture, the sector has remained largely unchanged over the review period with a large and generally stagnant commercial agriculture component and a fledgling, heavily under-resourced emergent sub-class.

Table 3 presents the secondary sector and sub-sectors’ shares of total GDP. Manufacturing has declined in significance somewhat, although it remains substantial at just under 20% of total GDP. The sector underwent a widespread and generally painful restructuring in the mid and late 1990s, although it had already been in decline for extended periods during the 1980s.

Table 3: Structure of South Africa’s economy: secondary sector - % of sector’s contribution, 1980 to 2006, selected years

1980 1985 1990 1995 2000 2005 2006 Secondary Sector 27.6 26.1 26.0 25.0 24.2 23.5 23.6

Manufacturing [3] 21.3 20.1 20.1 19.3 19.0 18.0 18.0

Electricity, Gas and Water [4] 2.0 2.4 2.6 2.8 2.7 2.4 2.4

Electricity, Gas and Steam [41] 1.4 1.7 2.2 2.4 2.3 2.1 2.1

Water Supply [42] 0.5 0.6 0.4 0.5 0.4 0.3 0.3

Construction (Contractors) [5] 4.4 3.7 3.3 2.8 2.5 3.1 3.3

Building Construction [51] 2.4 2.4 2.1 1.8 1.5 1.8 1.9

Civil Engineering and Other Construction [52-53] 2.0 1.3 1.2 1.0 1.1 1.3 1.4

Figure 4: Year-on-year growth of total economy and manufacturing - %, 1981 to 2006

-8.00

-6.00

-4.00

-2.00

0.00

2.00

4.00

6.00

8.00

10.00

1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Simple Year on Year Growth Rate All Sectors Simple Year on Year Growth Rate ManufacturingSimple Year on Year Growth Rate Tertiary Simple Year on Year Growth Rate Primary

Figure 4 highlights a number of important trends. Firstly, the manufacturing sector’s very poor performance during the 1980s is apparent, accompanied by significant volatility up to 1994. Post 1994, the restructuring of the sector took place between 1996 and 2000 with generally low growth rates dragging down the growth of the Total Economy. From 2001, with the effects of the East Asian crisis largely muted for SA, the manufacturing sector appears to be on a more stable growth path. In addition, manufacturing growth now more closely tracks (or vice versa as some argue) the growth performance of the tertiary sector.

The rest of this section analyses trends in manufacturing sub-sectors in more detail.

Figure 5 shows annual average growth rates calculated for two five-year periods and two three-year periods. The periods have been deliberately chosen in order to periodise important developments in the domestic economy.

Figure 5 ranks manufacturing sector by annual change in the period 2004-2006. It is apparent that almost all manufacturing sectors are currently growing. Only five of the 28 manufacturing sectors are not growing in the latest period. Of these five sectors, only Machinery and Beverages are of any real consequence. Printing, Tobacco and Professional & Scientific equipment are all relatively small sectors (each accounting for less than a 3% share of total manufacturing) and are not particularly strategic. What is of concern, however, is the composition of the ten fastest-growing sectors.

17

A Review of Industry Policy, Instruments and Support Programmes: 1994-2008

18

Figure 5: Manufacturing performance by sector - weighted annual % change by main periods

-12

-8

-4

-

4

8

12

16

Pap

er

Bas

ic ir

on a

nd s

teel

Aut

os

Gla

ss

Leat

her

Oth

er m

anuf

actu

ring

etro

leum

pro

duct

s

Food

ther

tran

spor

t equ

ip.

Bas

ic c

hem

ical

s

Rub

ber p

rodu

cts

Clo

thin

g

Met

al p

rodu

cts

Non

-met

allic

min

eral

s

Foot

wea

r

Ele

ctric

al m

achi

nery

Pla

stic

o an

d co

mm

unic

atio

n

Non

-ferro

us m

etal

s

Woo

d

Furn

iture

Oth

er c

hem

ical

s

Text

iles

Toba

cco

Mac

hine

ry

Bev

erag

es

and

sci

entif

ic e

quip

.

Prin

ting

Cok

e an

d p

O

TV, r

adi

Pro

fess

iona

l

1990-1994 1995-1999 2000-2003 2004-2006

In what would appear to be a re-emergence of a trend first noted in the early 2000s by Simon Roberts, many of the fastest growing sectors are resource or capital intensive. With the exception of Autos and Other Transport Equipment, most of the fastest growing sectors are resource intensive with Glass and Basic Chemicals highly capital intensive. However, although this combination of sectors may not lead to substantial employment creation, they collectively account for more than 50% of total manufacturing output and the strong growth performance therefore easily outweighs the decline in relatively small sectors. This should be a key factor in policymakers’ decisions of where to focus resources.

Table 4: Growth trends: manufacturing sectors, 2004-2006 - weighted annual % change

Sector 2004-2006Paper 14.68Basic Iron and Steel 12.72Autos 10.85Glass 10.15Leather 8.65Other Manufacturing 7.80Coke and Petroleum Products 6.99Food 5.57Other Transport Equipment 5.51Basic Chemicals 4.14

It may be worth looking at the growth trends of manufacturing sectors sorted by their growth in the 2000-2003 period where a very different pattern presents itself. In this period, although the growth rates are largely comparable, the fastest growing sectors are generally very small with Plastic, Furniture, Textiles and Prof & Scientific Equipment each accounting for less than 3% of manufacturing GDP. The growth of these small

sectors and the decline of a small number of large sectors had a significant impact by cutting the overall manufacturing sector’s performance. What is particularly interesting about the group of fastest growing sectors is the prominence of labour intensive sectors such as Leather, Plastics, Furniture and Metal Products. Unfortunately this trend seems to have been reversed in the 2004-06 period and, apart from Leather, no labour intensive sectors have featured.

Table 5: Growth trends: manufacturing sectors, 2000-2003 - weighted annual % change

Sector 2000-2003Professional And Scientific Equipment 12.32Glass 11.71Leather 11.69Basic Iron and Steel 10.07Furniture 8.91Plastic 8.13Other Transport Equipment 6.40Machinery 5.92Textiles 3.68Other Chemicals 3.60Metal Products 2.55

Employment

Whilst we emphasize that employment data from the Quantec database should be treated with some caution, particularly for services, we use these next. Generally, figure 6 shows the underperformance of the economy generally in creating jobs. Although business services and retail services have seen rapid and sustained growth over the last few years, the former creates mainly high-skill jobs. Perhaps the biggest disappointment is the agriculture sector where jobs continue to be lost.

19

A Review of Industry Policy, Instruments and Support Programmes: 1994-2008

20

Figure 6: Underperformance of the South African economy in creating jobs - weighted average % change

-8.00

-6.00

-4.00

-2.00

-

2.00

4.00

6.00

8.00

10.00

1990-1994 1995-1999 2000-2003

A111: Agriculture, forestry and fishing [1] A112: Mining and quarrying [2]A121: Manufacturing [3] A122: Electricity, gas and water [4]A123: Construction (contractors) [5] A131: Trade, catering and accommodation services [6]A1321: Transport and storage [71-74] A1322: Communication [75]A1331: Finance and insurance [81-82] A1332: Business services [83-88]A13411: Medical, dental and veterinary services [93] A13412: Excluding medical, dental and veterinary services [94-96]

Figure 7, below, provides a breakdown of the key manufacturing sectors’ employment performance. Based on these data it is clear that the sectors creating jobs at the fastest rate are, in fact, relatively capital and/or resource intensive. What is key though is that the largest sectors (in terms of absolute employment numbers) are not creating jobs. These are the food sector (the largest employer accounting for 160 000 jobs), Autos with 135 000 jobs and metal products with 126 000 jobs.

Moreover, if we compare the performance of sectors in the 2000-03 period with the later 2004-06 period, it is clear that a reversal similar to that seen for output growth has occurred in respect of employment too. Figure 8 shows that, in the 2000-03 period, a number of labour intensive sectors such as Furniture, Metal Products, Machinery and Autos grew at around 1-2.5% per year. This rather modest growth nonetheless accounted for 16 000 of the total of 20 000 new jobs created in manufacturing between 2000 and 2003. In the 2004-06 period, although the highest growth rate achieved was 4.5% for non-metallic minerals, the sector was simply too small (in employment terms at least) to be of any great significance.

The point we made in an earlier section of the report is worth repeating: strong growth rates in sectors of manufacturing are not of themselves notable. The key issue is the size of the sector in both output and employment terms. In a similar vein, support to labour intensive sectors may be less effective than supporting sectors which account for large numbers of the employed.

21

Figure 7: Key manufacturing sectors’ employment performance - weighted annual % change

-12

-8

-4

-

4

8

Non

-met

allic

min

eral

s

Oth

er c

hem

ical

s

Bev

erag

es

Mac

hine

ry

Non

-ferro

us m

etal

s

Ele

ctric

al m

achi

nery

Gla

ss

Met

al p

rodu

cts

Aut

os

Prin

ting

Cok

e an

d pe

trol.

prod

ucts

V, r

adio

& c

omm

unic

atio

n

Oth

er m

anuf

actu

ring

Bas

ic c

hem

ical

s

Food

Pro

f. &

sci

entif

ic e

quip

.

Bas

ic ir

on &

ste

el

Oth

er tr

ansp

ort e

quip

.

Woo

d

Toba

cco

Pla

stic

Leat

her

Furn

iture

Pap

er

Foot

wea

r

Rub

ber p

rodu

cts

Text

iles

Clo

thin

g

T

2000-2003 2004-2006

Figure 8: Manufacturing employment sorted by year: 2000-2003 - weighted annual % average

-12

-8

-4

-

4

8

Oth

er tr

ansp

ort e

quip

.

Oth

er m

anuf

actu

ring

Pro

f. &

sci

entif

ic e

quip

.

Cok

e &

pet

ro p

rodu

cts

Mac

hine

ry

Met

al p

rodu

cts

Furn

iture

Bas

ic ir

on &

ste

el

Aut

os

Prin

ting

Gla

ss

Non

-met

allic

min

eral

s

Toba

cco

Non

-ferro

us m

etal

s

Oth

er c

hem

ical

s

Pap

er

Pla

stic

Text

iles

Rub

ber p

rodu

cts

Woo

d

Food

Clo

thin

g

Bas

ic c

hem

ical

s

Bev

erag

es

Ele

ctric

al m

achi

nery

Leat

her

Foot

wea

r

V, r

adio

& c

omm

unic

atio

nT

2000-2003 2004-2006

A Review of Industry Policy, Instruments and Support Programmes: 1994-2008

22

Gross domestic fixed investment

Figure 9, below, indicates trends in GDFI by main sector. In general, the growth rates of GDFI are substantially better than in all of the previous periods from 1994. Although some sectors have fared better than others, overall GDFI was strong in the 2004-06 period. Coal Mining, Transport, Communication and Retail Trade all grew by more than 10% per year. The worst performers were the Agriculture sector and Gold Mining.

Figure 9: Real GDFI, 2000-2003 and 2004-2006 - weighted annual % change

-40

-30

-20

-10

-

10

20

30

40

Coa

l min

ing

al a

nd v

eter

inar

y se

rvic

es

edic

al, d

enta

l and

vet

erin

ary

serv

ices

Com

mun

icat

ion

Bus

ines

s se

rvic

es

Wat

er s

uppl

y

Tran

spor

t and

sto

rage

Who

lesa

le a

nd re

tail

trade

Man

ufac

turin

g

Fina

nce

and

insu

ranc

e

Con

stru

ctio

n

Elec

trici

ty, g

as a

nd s

team

d ac

com

mod

atio

n se

rvic

es

ener

al g

over

nmen

t ser

vice

s

ultu

re, f

ores

try a

nd fi

shin

g

Oth

er m

inin

g

ld a

nd u

rani

um o

re m

inin

g

Med

ical

, den

t

Excl

udin

g m

Cat

erin

g an G Ag

ric

Go

2000-2003 2004-2006

For sectors in manufacturing, the picture is similar with the majority of these growing GDFI at high and sustained levels for the 2004-06 period. The pattern in investment is not particularly clear, but the prevalence of a number of consumer durable sectors may suggest that manufacturers were investing in anticipation of a continued consumer boom. Sectors such as Wood, Footwear and Furniture, as well as Mechanical and Electrical Machinery suggest a wide-ranging sense of confidence in the economy.

Capacity utilisation

During the period under review, manufacturing sector capacity utilisation has been growing steadily, and is currently at very high levels.

23

Figure 10: Growth in manufacturing sector capacity utilisation, % per month, 2000 to 2006, trend and actual

Figure 11: Real Manufacturing GDFI, 2000-2003 and 2004-2006 - weighted annual % change

-60

-40

-20

-

20

40

60

80

Woo

d

Mac

hine

ry

TV, r

adio

and

Foot

wea

r

Non

-met

allic

Prin

ting

Cok

e an

d

Oth

er

Oth

er

Furn

iture

Ele

ctric

al

Food

Met

al p

rodu

cts

Pap

er

Toba

cco

Aut

os

Pla

stic

Bas

ic

Gla

ss

Leat

her

Pro

fess

iona

l

Text

iles

Bev

erag

es

Bas

ic ir

on a

nd

Rub

ber

Clo

thin

g

Oth

er tr

ansp

ort

Non

-ferro

us

2000-2003 2004-2006

A Review of Industry Policy, Instruments and Support Programmes: 1994-2008

24

Figure 12: Manufacturing GDFI: shares as % of total for selected years

0%

20%

40%

60%

80%

100%

1980 1985 1990 1995 2000 2005

Wood Machinery TV, radio and communication FootwearNon-metallic minerals Printing Coke and petroleum products Other manufacturingOther chemicals Furniture Electrical machinery FoodMetal products Paper Tobacco AutosPlastic Basic chemicals Glass LeatherProfessional and scientific equip. Textiles Beverages Basic iron and steelRubber products Clothing Other transport equip. Non-ferrous metals

Trade

The 15 Year Review of Trade Policy paper covers this theme in detail. Here we only highlight that, overall, the patterns of structure of SA trade remain largely unchanged from 1994. Moreover, although manufactured exports are a larger share of total exports today, SA trade remains distinctively that of a developing country: exports are dominated by primary products and imports by capital goods. The costs and benefits of the consumer boom of recent years are reflected in the increase in imports of consumer goods from China in particular. In general, however, import penetration has increased only slightly in recent years. Export performance has slowed in recent years, partially a result of the volatility and exchange rate levels.

From a policy perspective, perhaps the most worrying aspect of SA’s trade performance is the very small – and declining – share SA has of dynamic product exports. These sectors, defined broadly as demonstrating sustained, high export growth, are seen as an indicator of export dynamism. SA’s weak showing in this category suggests that trade policy has not been very successful in changing the product profile of its exports.

4.3 Concluding remarks

This part of the Review has attempted to deconstruct some of the competing trends influencing the performance of the real economy – and especially manufacturing – in recent years. Our initial assessment suggests that the service sector is now firmly the most important contributor to SA growth and is, increasingly, a stable source of growth. There are significant opportunities for further growth in service sectors to be facilitated. In particular, the Health, Education and Communication sectors could benefit from further policy assessment. For example, trade in Education Services through distance learning – especially at postgraduate level – has become a substantial global industry with many of the top 100 universities globally seeing this as a new route for expansion.. SA universities already accommodate large numbers of SADC students, but the opportunities have not yet been maximised. In Health, the Netcare group has pioneered the movement of doctors and dentists, to the UK especially, for the provision of health services. This has

become a significant source of income for the Netcare Group and provides a non-threatening channel for ‘importing’ countries whilst potentially reducing the risk of a further exodus of SA doctors and nurses.

The primary sector – and mainly agriculture – continues to under-perform its potential. For agriculture and more broadly defined agribusiness, potential remains high but largely unexploited. Anecdotal evidence suggests that simply expanding access to land and agricultural services would have a significant impact on the sector. The commercial sector is moderately competitive and it is unlikely that substantial growth opportunities exist here.

Manufacturing’s performance has been positive throughout much of the Review period. However, three clear phases are visible. In the period immediately after 1994, many manufacturing sectors were in a state of restructuring. In general, deindustrialisation was successfully avoided. The structure of manufacturing GDP changed significantly in this period with clearly uncompetitive sectors such as TV and electronic appliances losing their share of Manufacturing GDP. By 2000, much of the restructuring activity appears to have been completed and the depreciation and relative weakness of the rand offered labour intensive sectors such as Furniture, Leather (though attached to the MIDP), Plastics and Metal products some respite. The third phase has seen a reversal of these trends and, coupled with the appreciation of the rand and China’s entry into key labour intensive export sectors, resource and capital intensive sectors have become more prominent.

Paper, Glass, Iron and Steel, and Coke products have all shown strong and sustained growth in the recent period. As a number of these sectors are large – in the production sense – the effect has been good manufacturing output growth. However, as these sectors are relatively small employers and the large employment sources such as Food and Metal products have grown less quickly, the effect on employment creation has been small.

25

A Review of Industry Policy, Instruments and Support Programmes: 1994-2008

26

5. Assessment of the effectiveness of key industrial policies, programmes and projects

Drawing from recent work commissioned by the dti,4 this chapter assesses the performance of government’s main industrial support measures. In fulfilling the cost-benefit component of the terms of reference, each industrial support programme is considered in terms of the impact of the allocated financial resources of the programme on its target/objective. The analysis also profiles the individual and collective sectoral coverage of the programmes.

5.1 Introduction – the evolution of dti incentive programmes: 1994-2005

This framework of the South African trade and industry policy incentive regime was set between 1995 and 1998, when the dti reorganised itself and all trade and industry support programmes underwent review and were restructured to provide support in three areas; Competitivess (through a range of supply-side measures), Export Marketing Assistance and Industrial Investment Promotion. The key changes included:

The introduction of a suite of new incentive programmes aimed at increasing the competiveness of South African industry,

Enhancement of the Export Marketing and Investment Assistance Programme (EMIA),

Increased focus on small and medium enterprises (SME),

Accelerated termination of the General Export Incentive Scheme (GEIS), the costs of which vastly exceeded the benefits delivered, and which was proving to be unsustainable and to be undermining improved competitiveness,

Phasing out of old programmes – the Regional Industrial Development Programme (RIDP) was replaced with the Manufacturing Development Programme (MDP),

The MDP was extended by opening a Small and Medium firm Manufacturing Development Programme (SMMDP)

Introduction of Spatial Development Initiatives (SDI), clearly defined projects, which were managed by a special unit within the dti.

These changes resulted in a real reduction in the overall value of on-budget dti programmes, mainly as a result of terminating the GEIS programme, and during the period 1994-1999, although the lower budget was not a significant constraint to programme implementation.

During this period there was also a growth in the value of tax-based incentives which were not recorded on the balance sheet of the dti in particular through:

Duty credit incentives for the motor industry through the revised Motor Industry Development Programme (MIDP) - (see below),

4 Rustomjee (2005), DTI Incentives review process (Phase 1) – Incentives policy framework, Final report, 16 November. A study commissioned by the dti, Pretoria

27

Duty credit incentives for the clothing and textile industry through the Duty Credit Certificate Scheme (DCCS),

Tax incentives utilising Section 37E of the Tax code (not on the dti’s budget), which terminated in 1999 according to its original timeline

Between 2000 and about 2003, further review and refocussing of policy and programmes, captured in a number of policy documents5, were initiated with the following changes:

Broadening of sector target definitions of the Small and Medium Enterprise Development Programme (SMEDP), the biggest of the dti’s budgeted programmes, to include service enterprises,

Industrial Development Corporation (IDC) targets were also broadened – its mandate was relaxed to include non manufacturing investments and Southern African Development Community (SADC) investments, the latter in order to promote regional economic integration,

Broadening of the dti’s sector target scope, in recognition of the sectoral linkages with core manufacturing sectors. Specific new support incentive programmes were introduced, such as:

• The Critical Infrastructure Programme (CIP), aimed at financing the necessary bulk infrastructure required to support other (mainly) industrial investment projects,

• Incentive packages, modelled on the MDP, which targeted non-manufacturing, labour-intensive sub-sectors, including:

− A Film & TV rebate scheme,

− A Business Process Outsourcing (BPO) incentive scheme,

Reintroduction of tax-based incentives through the new Strategic Investment Programme (SIP) initiated with a finite window and a defined overall value of fiscal benefit which, once reached, would automatically terminate the programme. The SIP programme value was not formally on the dti’s budget,

Regular review and modification of individual programmes.

5.2 The changing structure and application of dti incentives: 1994-2005

Over the past 15 years, the dti has gained considerable experience in developing and administering investment incentive programs, having adopted, adapted and discarded a range of incentives over two periods, 1994-1999 and 1999-2005.

This has taken place during a period of significant restructuring of the domestic economy and far-reaching changes to the global economy and the way in which different domestic sectors have interacted with it.

The table below attempts a preliminary analysis of how the changes in the economy have prompted changes in the incentive regime.

5 the dti (2001) Driving competitiveness: Towards a new integrated industrial policy for sustainable employment and growth, Department of Trade and Industry,

the dti (2003), 10-Year Review and Strategic Planning. Sustainable economic development – investment promotion and growth, Trade and Industry South Africa, the dti

A Review of Industry Policy, Instruments and Support Programmes: 1994-2008

28

Table 6: 1994-2006: changes in incentive structure and application

1994-1999 1999-2004 2005-

Overall trajectory of national economy

Mixed sectoral growth & decline during period of significant internal restructuring

Dangerous fiscal risks and adverse macroeconomic position of RSA economy

Spluttering global economy. RSA economy affected adversely by Asian crisis, Russian crisis, Latin American crisis

Continuation of restructuring of existing sectors

Major growth of the telecommunication/cellphone-related sector

RSA economy structurally sound & increasingly driven by domestic consumption & infrastructure investment

Emergence of increasing alignment and stabilisation of global growth drivers

Dragon-driven global growth impacting favourably on medium-term commodity price outlook

Major global risks - Dollar devaluation

RSA economy amongst most open of emerging market economies

Restructuring of domestic sectors – upstream

Upstream capital intensive Metals and Chemicals sectors restructure and expand significantly

Recapitalisation of Textile industry less successful than anticipated

Cyclical commodity price dip strains upstream metals sectors as new capacity comes onstream – driving further restructuring

Later, infrastructure & logistical capacity constraints begin to impede primary extraction and beneficiation sectors

Environmental specifications drive investment in the liquid fuel value chain

Competitive upstream sectors running at full capacity with Metals-related potential to expand on global demand

Environmental specifications and supply constraints to drive investment in the liquid fuel value chain

Monopoly control of upstream has potential to constrain downstream and economic growth

Restructuring of domestic sectors – downstream and other linked sectors like services

Little aggregate growth in fixed investment during restructuring period

Auto industry exception, due mainly to MIDP and existing investment incentives

Significant growth in services sub-sectors, partly driven by growing domestic consumption

Significant competitive threats from imported products

High capacity utilisation – significant investment needed to support 6% growth target

Incentive restructuring

Termination of wasteful incentives

Phased tariff liberalisation used to pressure industrial restructure

Conscious continuation to significantly incentivise capital intensive export-oriented beneficiation sectors

Restructuring of investment incentives to target downstream sectors

Particular focus on supporting SMEs

Reorganisation of institutions disbursing incentives

Extension of incentives to support capital intensive upstream industries

Expansion of investment incentives to support downstream small and medium firms

Broadening of incentives to cover non-manufacturing economic activities

Broadening of support to MSMEs by promoting entrepreneurship

Increasing alignment of investment incentives to support domestic vs. imported supply to meet infrastructure-led and domestic consumption demand-led growth

Consolidation of MSME support institutions

As at 2007, the economy and the manufacturing sector in particular, appear to be robust in the face of a much more open economy than might have existed in 1994. The key drivers of the economy now seem to be a mix of:

More sustainable domestic consumption demand,

A sustained plan of state-led infrastructure investment, based on a relatively strong fiscus,

Expected and sustained global demand for the RSA’s resource commodities,

5.3 Breadth and depth of targets covered by dti family incentives

In 2006, the dti embarked on a comprehensive review of its incentive programmes, in parallel with the development of the National Industrial Policy Framework and its associated Industrial Policy Action Plan.

The following tables show the wide array of programmes that are currently offered by the dti and its family of associated institutions.

As is apparent, the programmes are aimed at a variety of targets which include sector targets, small and medium enterprises, women-owned firms, spatial development targets, research, supplier development and many others.

Table 7: dti family investment incentives

Investment Grants & Tax Incentives Loan Finance & Loan Guarantees

Critical Infrastructure Programme Foreign Investment Grant Small and Medium Enterprise Development Programme

(SMEDP) Small and Medium Manufacturing Development Programme

(SMMDP) Capital Goods Feasibility Study Fund Business Process Outsourcing/ Offshoring scheme Cooperative Incentive Scheme Accelerated Depreciation Allowance Assistance by Individual Primary Steel Producers Comprehensive Business Asset Reinvestment Relief Depreciation Allowance Development Programme for the textile and clothing

industry Productive Asset Allowance Start-up allowances Strategic Industrial Projects Tax Stimulus in Support of Small Businesses Urban Renewal Tax Incentive Film and TV Production Rebate Scheme The National Industrial Participation Programme Developmental Electricity Pricing IDZ Regional Industrial Development Programme

Agro-Industries Development Finance Bridging Finance for Contractors and Tenders Business Loans for Retail Finance Intermediaries Empowerment Finance Entrepreneurial Mining and Beneficiation Finance Finance for the Textiles, Clothing, Leather and Footwear

Industries Financing for the Expansion of the Manufacturing Sector Orchards Schemes Seed Loans for Retail Finance Intermediaries Techno-Industry Development Finance Technology Transfer Guarantee Fund The Land Reform Credit Facility Tourism Development Finance Wholesale Finance

Loan Guarantees Danida Business to Business Programme Khula Credit Guarantee Khula Equity Fund Khula Start

29

A Review of Industry Policy, Instruments and Support Programmes: 1994-2008

30

Table 8: dti trade facilitation incentive programmes

Export Marketing and Investment Assistance (EMIA) • Missions • Primary Market Research • Individual Exhibitions • National Pavilions • Sector Specific Assistance • Exporter Training • SA Trust Fund

Export Credit Insurance: Financial Credit, Investment Insurance,Project Credit,Suppliers credit Industrial Development Zones

Reducing anti-export bias - Rebate Schedules to Customs and Excise Act – 470.03, etc Duty Credit Certificate Scheme Motor Industry Development Programme (MIDP)

Table 9: dti competitiveness programmes

Sector Partnership Fund Skills Support Programme Support Programme for Industrial Innovation (SPII) Technology and Human Resources for Industry Programme (THRIP) Workplace Challenge Competitiveness Fund Black Business Supplier Development Programme Learnership Tax Allowance Research and Development Allowance Techno-Girl Technology for Women in Business (TWIB) The Community Public Private Partnership Programme (CPPP)

31

5.4 Value of dti incentives : 2001-2005

Table 10: Historic value of dti incentives (Rm)

Year Investment Promotion6

Trade Facilitation

(EMIA only)

Competitiveness (SPII, THRIP,

Competitiveness fund, Sector

partnership fund only)

Total Budget

DCCS MIDP

National Industrial

Participation Programme 7

2001 1,009.7 121 0 2,554.8 532.0 500 2002 1,074.7 71 227 2,245.4 1,087.5 500 2003 1,133.8 100 272 2,280.0 1,557.1 15,000 500 2004 1,359.4 67 276 2,796.3 959.0 500 2005 538.1 287 3,623.3 357.3 17,000 500

Source : the dti