indonesia’s new gross split psc - pinsent masons pacific... · indonesia’s new gross split psc...

TRANSCRIPT

Indonesia’s new Gross Split PSCRight structure, wrong split?

Continued on next page >

1. BackgroundIn January 2017, the Government of Indonesia (‘Government’) issued significant changes to the fiscal terms which will apply to new production sharing contracts (‘PSCs’) for conventional oil and gas blocks1 aimed at encouraging PSC operators and oilfield services companies to streamline and operate more efficiently.2 Ministry of Energy and Mineral Resources (‘MEMR’) Regulation No. 8 of 2017, which came into force on 16 January 2017 (‘Regulation’), introduces radical changes to the allocation of production under any new Indonesian PSC to be entered into by the State and the associated upstream oil and gas producer (‘PSC Contractor’).

† This article has been reviewed by Guido, Hidayanto & Partners (GHP Law) from an Indonesian Law perspective. This article does not constitute legal advice. 1 The gross split mechanism was first introduced for non-conventional fields under MEMR

Regulation No. 38 of 2015 (regarding Expediting Non-Conventional Oil and Gas Operations) which came into effect on 2 November 2015. This regulation did not detail how the gross split concept would be applied in practice.

2 The stated objective of the Regulation is ‘increasing efficiency and effectiveness in the oil and gas production sharing model’ (Recital (a) of the Regulation).

3 For a summary of the existing Cost Recovery PSC terms, please refer to the Appendix.4 For example, it is possible that Gross Split PSCs will be an attractive option in the case of

non-conventional reservoirs, which automatically attract an additional 16% production split in favour of the PSC Contractor under the Regulation.

5 The Indonesian Petroleum Association has stated that the Regulation is simply not enough to improve Indonesia’s competitiveness in the oil and gas sector, and that it currently only serves the interests of the Government. Executive Director of the Indonesian Petroleum Association, Marjolijn Wajong, has commented that the current form of the Regulation would likely have a negative impact on the development of offshore oil and gas projects and those in remote areas, and also stressed the need to address enhanced oil recovery under this new regime. (Investor Daily, page 9, 8 March 2017).

This new scheme sees the complete elimination of the cost recovery system for new PSCs, removing the need for related project budget scrutiny by Indonesia’s upstream oil and gas regulator SKK Migas. The Government and PSC Contractors will instead split gross production without any deduction of exploration, development and production related capital expenditure, operating costs and taxes. In return, the PSC Contractor will – at least in theory – be allocated a greater share of gross oil and gas production under the PSC. Although the new mechanism will not automatically apply to existing conventional PSCs (‘Cost Recovery PSC’)3, a PSC Contractor may request to transition over to the new gross split PSC (‘Gross Split PSC’). Since the Regulation was introduced in January, it’s fair to say that PSC Contractors with existing conventional Cost Recovery PSCs are not beating down SKK Migas and MEMR’s doors requesting to transition across to the new regime.

Is the Gross Split PSC likely to spur investment? The answer largely depends on the type of project and the PSC operator’s ability to substantially reduce operating costs.4 For many projects, particularly marginal fields, mature fields in need of enhanced oil recovery, projects located in frontier areas and gas projects, the Gross Split PSC may ultimately deter investment. Nonetheless, the removal of the ever growing bureaucracy around cost recovery has been welcomed positively by the industry and the Regulation does go some way in providing a suitable framework for a new and potentially more attractive PSC model. Unfortunately, the production splits and accompanying adjustment mechanisms included in the Regulation are unlikely to sufficiently incentivise much-needed investment into Indonesia’s upstream sector. As oil and gas stakeholders in Indonesia provide their feedback on the Regulation,5 it is hoped that MEMR will be accommodating in amending and adding to the Regulation going forward, as industry players experiment with its implementation in relation to different types of projects.

99832

2. Gross Split PSC: Overview of the Regulation

Under the new Gross Split PSC there is no cost recovery mechanism, therefore the PSC Contractor’s revenue will be derived solely from its share of gross production (and it will also have to pay income tax to the Government in respect of this revenue). The Government’s revenue will consist of the Government’s gross share of production, bonuses, the PSC Contractor’s income tax and any indirect taxes paid by the PSC Contractor.

Initial Base Split

Each Gross Split PSC will have an initial base split percentage for each field developed within the PSC contract area, which is then to be adjusted by field specific factors listed in the Regulation.6 The base split for the PSC Contractor is 43% for oil blocks, and 48% for gas blocks.7

Factors amending the Initial Base Split

As this new scheme leads to the PSC Contractor shouldering greater risk, the Regulation provides certain incentives which offer an increased production split based on what the Regulation describes as ‘variable’ and ‘progressive’ factors:

(a) Variable Factors

The initial base split is subject to further adjustments in accordance with several field-specific variable factors, with the Regulation granting PSC Contractors an additional percentage share of production when operating under more challenging conditions. These include key physical characteristics of each field to be developed within the PSC contract area, such as: field status, field location, block status, reservoir depth, reservoir type (e.g. conventional or non-conventional)8, availability of supporting infrastructure, carbon dioxide content and domestic component level.9 For example, non-conventional reservoirs will entitle a PSC Contractor to an automatic additional 16% share of gross production, acknowledging the risks involved in developing fields of that nature and theoretically rendering the Gross Split PSC an appealing option for non-conventional oil and gas projects and CBM E&P companies.

6 Article 4 of the Regulation.7 Article 5(1) of the Regulation.8 Note that Article 26 of the Regulation states that ‘provisions regulating the Sliding Scale Gross Split Production Sharing Contract in the MEMR Regulation 38/2015 on the Acceleration of Non-

Conventional Oil and Gas Business’, which applied the gross split mechanism to non-conventional PSCs, are retracted and deemed not in effect as from 13 January 2017.9 Article 6(2) of the Regulation.10 Article 6(1) and Article 8(1) of the Regulation.11 Article 8(3) of the Regulation.12 According to Wood Mackenzie, Indonesia has stipulated acceptable returns of 8-12% IRR for midstream investments with up to a maximum of 15% IRR for ‘pioneering’ projects in remote areas.

Therefore it seems that 12-15% IRR might be an acceptable range from MEMR’s perspective in respect of upstream investments. The reality is that investors will be aiming for a minimum of 15% IRR in the current environment and to account for country risk factors.

The base split will be adjusted based on the above fixed factors, applied by MEMR (acting on the recommendation of the head of SKK Migas) at the time of the approval of each field’s first Plan of Development (‘PoD’).10

(b) Progressive Factors

Over time, this initial gross split will be further adjusted based on a number of progressive factors as follows:

(i) Further changes to the field-specific components

If, on commencement of commercial production, it becomes apparent that the field-specific components are different to what was anticipated at the time of agreeing the PoD, the splits may be further adjusted to reflect conditions after commercial production.11

(ii) ‘Certain economic level’

The Regulation stipulates that, in the event that commercial evaluation of a field (or a number of fields) does not meet a ‘certain economic level’, MEMR may grant an additional production share percentage of up to 5% to the PSC Contractor. However, where commercial evaluation of a field (or a number of fields) exceeds this level, MEMR may grant an additional production share percentage up to 5% to the Government (deducted from the PSC Contractor’s share). It’s worth noting that ‘certain economic level’ is not defined in the Regulation, meaning it is difficult at this stage to predict how the appropriate level will be calculated and applied by the Government in practice – although, as drafted, it does appear to give MEMR a significant amount of discretion.12

(iii) Monthly oil price adjustment

An adjustment to the splits will also be carried out, based on SKK Migas’s evaluation of the crude oil price (using the monthly Indonesia Crude Price (‘ICP’)). This means that the respective percentage shares of production will be re-evaluated on a month to month basis – which has the potential to become administratively burdensome.

Pinsent Masons | Indonesia’s new Gross Split Production Sharing Contract

3

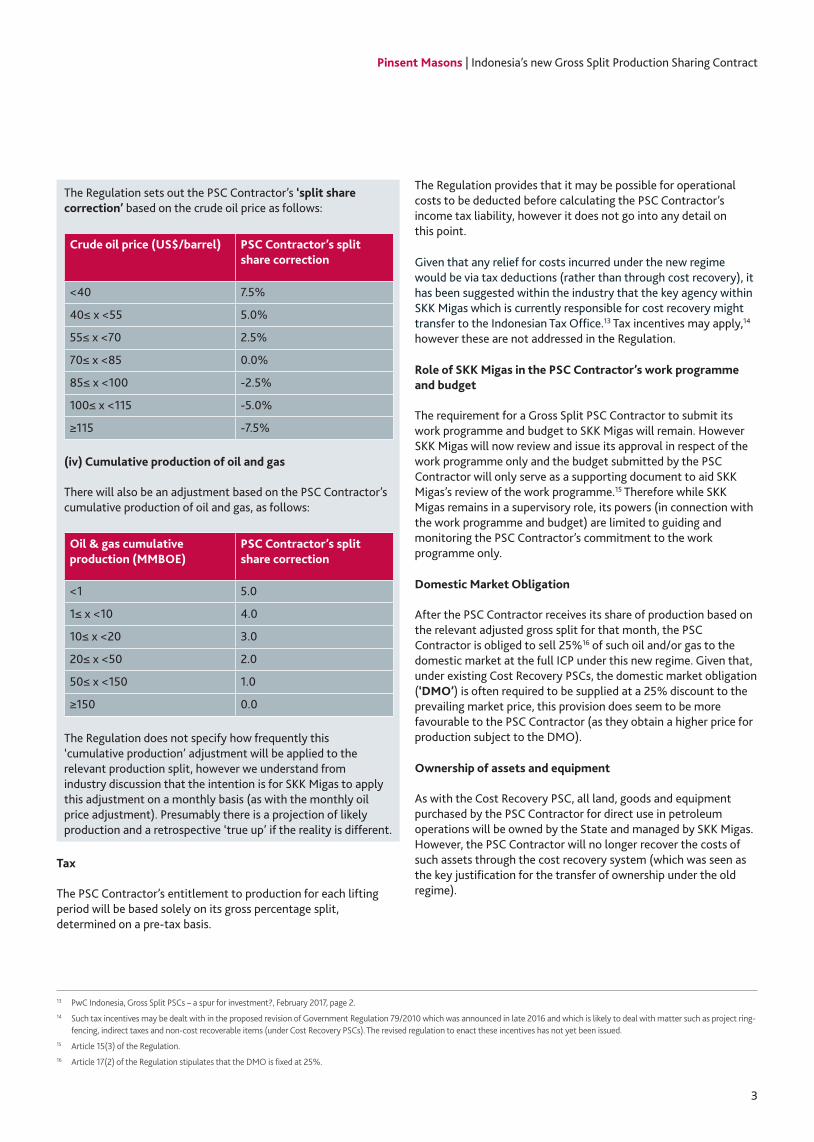

The Regulation sets out the PSC Contractor’s ‘split share correction’ based on the crude oil price as follows:

Crude oil price (US$/barrel) PSC Contractor’s split share correction

<40 7.5%

40≤ x <55 5.0%

55≤ x <70 2.5%

70≤ x <85 0.0%

85≤ x <100 -2.5%

100≤ x <115 -5.0%

≥115 -7.5%

(iv) Cumulative production of oil and gas

There will also be an adjustment based on the PSC Contractor’s cumulative production of oil and gas, as follows:

Oil & gas cumulative production (MMBOE)

PSC Contractor’s split share correction

<1 5.0

1≤ x <10 4.0

10≤ x <20 3.0

20≤ x <50 2.0

50≤ x <150 1.0

≥150 0.0

The Regulation does not specify how frequently this ‘cumulative production’ adjustment will be applied to the relevant production split, however we understand from industry discussion that the intention is for SKK Migas to apply this adjustment on a monthly basis (as with the monthly oil price adjustment). Presumably there is a projection of likely production and a retrospective ‘true up’ if the reality is different.

Tax

The PSC Contractor’s entitlement to production for each lifting period will be based solely on its gross percentage split, determined on a pre-tax basis.

The Regulation provides that it may be possible for operational costs to be deducted before calculating the PSC Contractor’s income tax liability, however it does not go into any detail on this point.

Given that any relief for costs incurred under the new regime would be via tax deductions (rather than through cost recovery), it has been suggested within the industry that the key agency within SKK Migas which is currently responsible for cost recovery might transfer to the Indonesian Tax Office.13 Tax incentives may apply,14 however these are not addressed in the Regulation.

Role of SKK Migas in the PSC Contractor’s work programme and budget

The requirement for a Gross Split PSC Contractor to submit its work programme and budget to SKK Migas will remain. However SKK Migas will now review and issue its approval in respect of the work programme only and the budget submitted by the PSC Contractor will only serve as a supporting document to aid SKK Migas’s review of the work programme.15 Therefore while SKK Migas remains in a supervisory role, its powers (in connection with the work programme and budget) are limited to guiding and monitoring the PSC Contractor’s commitment to the work programme only.

Domestic Market Obligation

After the PSC Contractor receives its share of production based on the relevant adjusted gross split for that month, the PSC Contractor is obliged to sell 25%16 of such oil and/or gas to the domestic market at the full ICP under this new regime. Given that, under existing Cost Recovery PSCs, the domestic market obligation (‘DMO’) is often required to be supplied at a 25% discount to the prevailing market price, this provision does seem to be more favourable to the PSC Contractor (as they obtain a higher price for production subject to the DMO).

Ownership of assets and equipment

As with the Cost Recovery PSC, all land, goods and equipment purchased by the PSC Contractor for direct use in petroleum operations will be owned by the State and managed by SKK Migas. However, the PSC Contractor will no longer recover the costs of such assets through the cost recovery system (which was seen as the key justification for the transfer of ownership under the old regime).

13 PwC Indonesia, Gross Split PSCs – a spur for investment?, February 2017, page 2.14 Such tax incentives may be dealt with in the proposed revision of Government Regulation 79/2010 which was announced in late 2016 and which is likely to deal with matter such as project ring-

fencing, indirect taxes and non-cost recoverable items (under Cost Recovery PSCs). The revised regulation to enact these incentives has not yet been issued. 15 Article 15(3) of the Regulation.16 Article 17(2) of the Regulation stipulates that the DMO is fixed at 25%.

99834

17 These blocks are: Tuban, Sanga-Sanga, South East Sumatra, Ogan Komering, B-Block North Sumatra Offshore (NSO), Tengah, East Kalimantan and Attaka.

18 Article 25(d) of the Regulation (but with a maximum additional percentage in favour of Contractor of 5% – see Article 7).

19 Article 24(1) of the Regulation.20 Article 24(2) of the Regulation.

Continued on next page >

3. Application

New oil and gas blocks

The Government has made it clear that the Gross Split PSC is mandatory for all new oil and gas PSCs. As an example, it was reported on 31 January 2017 that MEMR will grant subsidiaries of Pertamina 100% participating interests in eight oil and gas blocks where the existing Cost Recovery PSCs are due for expiry during 2018.17 All of these blocks will reportedly operate under new and separate Gross Split PSCs.

Existing PSCs

Existing Cost Recovery PSCs are not automatically affected by the new Regulation, however PSC Contractors under such contracts may request to transition to the new terms if preferred. This decision will depend on the characteristics of the field in question. Where there are outstanding recoverable costs that have not yet been recovered through cost recovery, such costs may be taken into account upon transition to the Gross Split PSC - and may lead to an increase in the PSC Contractor’s gross split.18 Otherwise, existing Cost Recovery PSCs will continue in line with their original terms until expiry.

Expiring PSCs

Where the expiring PSC is not being extended, the new contract will take the form of a Gross Split PSC.19 However, where the expiring PSC is to be extended, the Government will decide whether to continue with the Cost Recovery PSC, or move to a Gross Split PSC.20

To us, this provision does not seem inequitable given that when the PSC was entered into by the PSC Contractor there was no guarantee of an extension.

Expiring PSCs, with extension already approved

For existing Cost Recovery PSCs in respect of which an extension had, as of 13 January 2017, already been approved but not yet executed, the cost recovery regime will continue to apply in respect of the extension period unless the PSC Contractor requests (and the Government approves) the transition to a new Gross Split PSC.

Pinsent Masons | Indonesia’s new Gross Split Production Sharing Contract

5

4. Analysis

(A) From the Government’s perspective (including SKK Migas)

Increasing the flow of cash to the State, especially in the early years of production when cash would otherwise be going to the PSC Contractor as cost production, is a key motivation behind the Regulation. The management of cost recovery has been challenging for the Government and has long been reported in Indonesia as a burden on the State budget.21

Cost recovery in Indonesia is a complex, sensitive and contentious issue, whether between SKK Migas and the PSC Contractor, or SKK Migas and the State auditor. The removal of the need to oversee cost recovery should free up some capacity within SKK Migas to focus on other issues (although in practice there will still be considerable work involved in relation to existing Cost Recovery PSCs). In this context, some might question whether this reduced role should lead to a more streamlined and smaller SKK Migas. It is however possible that a lessening of SKK Migas’s control over a PSC Contractor could be interpreted as contradicting Article 33(3) of the Indonesian Constitution of 194522- i.e. as a lessening of State power exerted over PSC Contractors.23

Nonetheless, significant dialogue will need to occur in connection with the various adjustments required to the initial base production split under the Regulation. This could potentially lead to disputes and for projects to stall at PoD stage (which is when the base split will be adjusted to take account of any field specific variable factors), particularly as there is no appeal process provided in the Regulation where the PSC Contractor does not agree with the proposed split determinations. It is unclear at this stage which entity would adjudicate on any disputes. SKK Migas and the Government undoubtedly enjoy a high level of discretion under the Regulation and should ensure that the adjustments are transparent and applied fairly across new PSCs.

(B) From an Indonesian oil and gas services company perspective

For existing Cost Recovery PSCs, the procurement of all goods and services by the PSC Contractor is subject to PTK 007/2015 (which provides for ‘guidance’ by SKK Migas on asset management, customs and project management) and procurement costs above a fixed amount require SKK Migas approval.24 Where procurement does not comply with PTK 007/2015, the related costs are not cost-recoverable. The Regulation simply states that, under the new regime, the procurement of goods and services shall be conducted by the PSC Contractor ‘independently’.25 The industry’s expectation is that a Gross Split PSC Contractor will therefore no longer be subject to PTK 007/2015. Many in the industry see the potential withdrawal of PTK 007/2015 compliance for PSC Contractors as being the most fundamental and far reaching aspect of the Regulation.

There is a concern that the Gross Split PSC could have a detrimental impact on local Indonesian oil and gas services companies. Since PSC Contractors will undoubtedly seek to minimise operating costs as far as possible under the new regime (as such costs are no longer guaranteed to be recovered), it follows that PSC Contractors will seek to procure cheaper goods and services. This has led to concerns that the local oil and gas services industry would be unable to compete with international suppliers and that lower spending on the local services industry could contravene the requirements of the Constitution.

While the Regulation does state that the PSC Contractor must ‘prioritise’ domestic goods, services and technology, as well as national engineering and construction abilities,26 it is unclear how this will be enforced. Will PTK 007/2015 and local content regulations be enforced by SKK Migas in connection with Gross Split PSCs to ensure this happens and, if so, will PSC Contractors then actually achieve the cost reductions necessary to make the new terms attractive?27

21 Many argue that cost recovery should not form part of the State budget at all, as it reflects the costs of extracting the resources out of the ground, and the production splits afforded to the Government and to the PSC Contractor under the Cost Recovery PSC takes this ‘reimbursement’ for cost recovery into account. In addition, the recovery of exploration costs from the Government is limited to production arising from the contracted ‘field’ that has an approved Plan of Development – effectively quarantining cost recovery to exploration costs incurred in respect of the initial and then subsequent producing fields which are subject to a Plan of Development rather than the entire PSC contract area.

22 Article 33(3) of the Indonesian Constitution of 1945 (the ‘Constitution’) provides that ‘the land, the waters and the natural resources within shall be under the powers of the State and shall be used to the greatest benefit of the people’. Therefore, pursuant to the Constitution, ownership of petroleum ought to remain with the State.

23 The situation is not quite analogous to that of BP Migas, which was dissolved in November 2012 by the Constitutional Court of Indonesia. Unlike BP Migas, which had enjoyed a certain degree of autonomy in its day-to-day operations, SKK Migas is supervised by and under the direct control of MEMR.

24 Guidance No. 007/SKKO0000/2015/S0 on the Management Framework for the Supply Chain for Cooperation Contracts (‘PTK 007/2015’). Under PTK 007/2015, a PSC Contractor can write its own tenders but requires SKK Migas approval at the planning stage if the package is worth over Rp50 billion or US$5 million, and further approval to appoint the supplier when the package is over Rp200 billion or US$20 million.

25 Article 18(2) of the Regulation.26 Article 18(1) of the Regulation. Note that the variable factors outlined above also include an adjustment based on ‘domestic component level’. For example, where 70% or more of the goods

used directly in the field’s exploration and production activities are produced domestically in Indonesia, the PSC Contractor is afforded an additional 4% production split adjustment. This may not be enough of an incentive to offset the cost reductions which could otherwise be obtained in procuring goods from other countries, but at least it does give the PSC Contractor the option.

27 If, in an attempt to reduce operating costs, PSC Contractors secure cheaper goods and oilfield services from outside of Indonesia (and are not prohibited from doing so under any additional regulations implemented by SKK Migas or any other Government authority), it may invoke arguments that the natural resources are no longer being used ‘to the greatest benefit of the [Indonesian] people’ (in line with Article 33(3) of the Constitution).

Continued on next page >

99836

(C) From a PSC Contractor’s perspective

Supporters of the new Gross Split PSC claim it will allow PSC Contractors greater authority and flexibility in operating its respective contract area. Indeed, the relaxation of the bureaucratic micro-management of cost recovery will surely be a welcome change for PSC Contractors. While the Cost Recovery PSC model did not itself encourage inefficiency; its implementation was inefficient - both from the perspective of the State and the PSC Contractors. Advocates of the new model claim that – in a perfect environment – exploration programmes and cycle times could be shortened by as much as one third. The potential benefits lie in the PSC Contractor’s ability and freedom to reduce costs and accelerate schedules. Is this possible?

Based on our discussions with many PSC Contractors operating in Indonesia, the Regulation in its current form evidently lacks sufficient detail and leads to concerns on a number of issues, which we raise below:

(i) Existing cost recovery pools

Thirty-five Indonesian PSCs are due for expiry between 2017 and 2026, which have been valued at close to US$10billion.28 For expiring PSCs which are not being extended, the Gross Split PSC will apply to that working area going forward (under a new contract). For expiring PSCs which are being extended, the Government can decide whether the Gross Split PSC terms should apply during the extension period. In both cases, the Regulation is silent on the issue of operating costs which have been spent under the previous Cost Recovery PSC, but not yet recovered. The carrying-forward of any unrecovered costs is therefore not expressly permitted.

PSC Contractors in these situations will need certainty as to whether such costs may be taken into account as an adjustment to the production split,29 or otherwise reimbursed in the event that the expired work area is to be managed by Pertamina going forward. For expiring PSCs with a small cost pool, migrating to a new Gross Split PSC may be acceptable. In relation to those with considerable cost pools, unless the Government develops a mechanism to account for at least some of the unrecovered costs, moving to the Gross Split PSC might not make much economic sense for many existing PSC Contractors. The outcome would be further relinquishments at the point of expiry.30

PT Pertamina Hulu Energi ONWJ (‘PHE ONWJ’), a subsidiary of Indonesia’s state-owned oil and gas company PT Pertamina (Persero), is the first PSC Contractor to enter into a Gross Split PSC, having signed a renewed PSC for the Offshore North West Java (‘ONWJ’) block on 18 January 2017. According to press reports, the new ONWJ PSC includes a gross production split in favour of the PSC Contractor of 57.5% for oil and 62.5% for natural gas. However, only one week after signing, it was reported in the Indonesian press31 that PHE ONWJ had already requested an increase in the split in favour of PHE ONWJ to take account of the remaining US$453 million of unrecovered costs under the previous Cost Recovery PSC.32 The lack of clarity on PSC extensions (in terms of whether MEMR may determine that the field should instead be managed by Pertamina upon expiry,33 the treatment of existing cost pools, and also in relation to which contractual form the new PSC may take), together with the sheer scale of production at risk, make expiring PSCs one of the key issues facing Indonesia’s upstream sector. 34

(ii) Increased PSC Contractor risk

Under both types of PSC, exploration risk is shouldered entirely by the PSC Contractor. However under a Cost Recovery PSC, upon commercial discovery, development, production and abandonment risk is shared with the State through cost recovery. Under the Gross Split PSC regime, all of the risk associated with exploration through to abandonment of the field(s) will now sit with the PSC Contractor. Whether cheaper and more suitable goods and services can be procured to allow for cost reductions, or whether PSC Contractors will in reality be prevented by the Government or SKK Migas from achieving such savings, remains to be seen.

(iii) Delay in return on investment

The absence of cost recovery under the new regime means that the Government will have an increased share of oil and gas produced during the early years of production under a Gross Split PSC. It will therefore take longer for the PSC Contractor to recover its investment costs, leading to increased uncertainty and placing a heavy financial burden on the PSC Contractor during those early years. The removal of the arduous process of cost recovery should, at least in theory, allow PSC Contractors latitude to use more innovative technology and greater discretion

28 Wood Mackenzie, ‘Indonesia’s expiring PSCs: $10 billion of potential upstream value’, October 2016. During 2017, the Lemtang, Warim, Makahan and Attaka PSCs are also due for expiry (in addition to the ONWJ PSC which expired in January 2017).

29 The PSC Contractor may be able to argue that an adjustment should be made to the production split under Article 7(1) of the Regulation given that the commercial evaluation of the field might otherwise fail to meet a ‘certain economic level’. However this would only allow for an additional production share of up to 5%, which in practice may not offset the burden of the existing cost pool.

30 It has been reported that the Government plans to launch a Minister’s Regulation in connection with the depreciation of oil and gas blocks which are nearing the end of their PSC term and plan to switch to the Gross Split PSC regime, aimed at ‘smoothing out the process’ of switching. (Investor Daily, page 9, 8 March 2017).

31 Investor Daily, page 9, 25 January 2017.32 PT Pertamina Hulu Energi President, Director Gunung Sardjono Hadi, reportedly commented that the Government had previously intended to renew the ONWJ PSC on a traditional cost

recovery basis, instead of terminating and replacing with a Gross Split PSC. As a result, PHE ONWJ was unable to have its investments under the existing Cost Recovery PSC reimbursed before the ONWJ PSC’s expiry on 18 January 2017. On 15 March, it was reported that PHE ONWJ is still evaluating the possibility of applying efficiency measures at OWNJ and that, if an opportunity can be found to be more efficient without reducing production, then PHE ONWJ would not request an increased split from the Government. (Kontan, page 14, 15 March 2017).

33 MEMR Regulation No. 15 of 2015, dated 8 May 2015.34 On 27 March 2017, it was reported that the Government is ‘ready to accept suggestions’ concerning PHE ONWJ’s request for an increased production split (Investor Daily, page 9, 27 March

2017). Continued on next page >

Pinsent Masons | Indonesia’s new Gross Split Production Sharing Contract

7

in the development of the fields. However cost recovery undoubtedly provides the PSC Contractor with the ability to de-risk its development and production costs (to some extent).

(iv) Oil price related adjustments

The Regulation allows for an increased share in the split of production to be awarded to the PSC Contractor when the ICP is lower than US$70/barrel, and vice versa during periods when the price is greater than US$85/barrel. While this provision, taken in isolation, may appeal to investors during periods of lower oil price, it does mean that the gross percentage share of production afforded to the PSC Contractor will vary on a month to month basis. This could prove to be administratively burdensome.

Further, the Regulation does not state how the progressive adjustment (based on the monthly ICP) will be applied to gas sales. Where gas produced in relation to a Gross Split PSC is sold under the relevant gas sales agreement on a fixed-price basis (without any link to crude oil prices), presumably there will be no adjustment based on the Indonesian Crude Price? This uncertainty should be clarified by the Government.

(v) Regular adjustments to the gross split

As we know, the gross split percentages between the PSC Contractor and the Government will be adjusted initially and then on an ongoing basis, based on a number of factors. This will involve a significant amount of discussion between the PSC Contractor and SKK Migas, may cause uncertainty from the PSC Contractor’s perspective and increase the risk of potential disagreements arising on the adjustments. Further, it remains to be seen whether SKK Migas will adopt a consistent approach among different PSC Contractors. Different negotiations, and different negotiators, could lead to different outcomes in practice.

(vi) Delays prior to the development stage

There is also a high likelihood of disagreements arising between the Government and PSC Contractors in determining the adjustments to the initial base split, at the point of approval by the Government of the PSC Contractor’s PoD. In coming to an agreement on the adjustments, the determining considerations are likely to include long term assumptions of commodity prices, production volumes and investment and operational costs. Taking into account the long term nature of the oil and gas industry, it will be difficult to determine the long term economic variable assumptions which will be agreeable to both parties. This has raised concerns over discoveries (particularly marginal discoveries) being stalled at the development stage.

Given the significant cost pools attached to these types of project, the new terms are not likely to encourage the relevant PSC Contractors for these projects to transition across to the new scheme.

(vii) Ownership of assets

As outlined above, title to goods, equipment and land purchased or acquired by the PSC Contractor under a Gross Split PSC and directly used in petroleum operations will continue to vest in the State (as was the case with the existing Cost Recovery PSCs). However the cost recovery mechanism (as supported by the Constitution) was always the key justification for this. Now, PSC Contractors may query the rationale for ownership vesting in State, particularly where the cost of those assets has not been recovered by the PSC Contractor through production (i.e. where the production levels are not high enough to allow recovery of such costs).

(viii) Abandonment costs

Indonesian PSCs have included an abandonment clause since 1995 which provides that PSC Contractors must include in their budgets provisions for clearing, cleaning and restoring the site upon completion of the work. As any funds set aside for abandonment and restoration under the Cost Recovery PSC are cost recoverable once funded or spent, unused funds following decommissioning are transferred to SKK Migas. The Regulation is silent on the issue of abandonment, however it seems clear that abandonment costs will no longer be cost recoverable when funded or spent. Gross Split PSC Contractors will therefore be keen to ensure that, where Pertamina or another entity takes over the contract area following PSC expiry, any portion of the funds (set aside by the PSC Contractor during the initial period) which remain unused following decommissioning will now be returned to the PSC Contractor. With the mammoth costs involved in decommissioning, clarity on this issue from the Government would be welcomed by PSC Contractors and investors who are weighing up the advantages of using the Gross Split PSC.

(ix) Accelerated procurement process?

The procurement process in relation to the Cost Recovery PSC requires work contracts to be tendered in accordance with complex bidding procedures. In addition to controlling costs, PTK 007/2015 also functions as somewhat of a protectionist policy for local oil and gas services players in Indonesia. In practice, these local content requirements tend to inflate the associated costs of procurement for PSC Contractors.

Continued on next page >

99838

As the procurement process under the new regime will be run independently by the PSC Contractor34 and appears to denote a relaxation of the work contract bidding requirements in Indonesia, exploration and other work programmes should in theory be accelerated and technological innovation stimulated.

A key question is whether Indonesia has the capacity to deliver such new technologies, or whether PSC Contractors will be permitted to procure such technology from overseas. One of the variable adjustment mechanisms under the Gross Split PSC provides an adjustment in favour of the PSC Contractor to account for the ‘domestic component level’ – perhaps recognition from the Government that domestic players will now have to compete with international companies in selling their products and services.

However more general Indonesian protectionist policies do exist outside of PTK 007/2015, including, for example, the cabotage requirements imposed by the Ministry of Transport35 which contributed to the lack of offshore drilling work being awarded in Indonesia during 2016. Therefore, in certain situations, the use of domestic goods and services will still be required (likely at greater cost to the E&P company). This will potentially counteract the possible positive benefits of embracing new technologies and cost reductions which could otherwise be achieved under this new regime.

Further, PSC Contractors should in theory enjoy cuts to overheads as a result of a reduced requirement on supply chain management linked to PTK 007/2015, however potential liability for such companies around employee severance payments in Indonesia may delay the benefits of any such cuts.

Continued on next page >

34 Article 18(2) of the Regulation.35 Cabotage is the principle regulating shipping activities which take place within a country’s

waters. Article 8 of Indonesia’s Maritime Law No 17 of 2008 provides that activities relating to domestic sea transportation must be performed by an Indonesian Sea carriage company using an Indonesian flagged vessel (manned by Indonesian crew), and that non-Indonesian sea flagged vessels are prohibited from carrying passengers and/or goods between islands or ports in Indonesian waters. The Government later changed the rules to bring oil and gas company activities under the ambit of this law.

Pinsent Masons | Indonesia’s new Gross Split Production Sharing Contract

9

5. Impact on investment

Indonesia’s growing economy is driving higher domestic demand for energy, but the country must increasingly rely on the development of smaller and more challenging fields to meet its requirements. Implementing this Regulation at a time when domestic production of oil and gas is rapidly declining, combined with the lack of exploration and the high number of aging wells, is a brave move by the Government.

Investment into the Indonesian upstream industry is lagging behind its neighbouring countries, largely due to unattractive regulations including taxes, complicated licensing, bureaucratic issues and inconsistent policies. The Indonesian Petroleum Association (‘IPA’) recently commented that, while the Government’s move was well-intentioned, it will not improve Indonesia’s oil and gas investment climate as the new regime is financially more favourable to the Government. IPA Executive Director, Marjolijn Wajong, has asked the Government to conduct a comprehensive study on potential improvements which could be made to the Regulation – especially in relation to the development of offshore oil and gas projects and those in remote areas, together with the issue of enhanced oil recovery.36

For over eight years now, the Government has been debating a new oil and gas law (as a replacement to Law No. 22 of 2001) in the hope of increasing exploration activity and reversing the production decline. From a foreign investment perspective, it is crucial to understand how the new Gross Split PSC will operate in the context of the proposed new law. However, it is likely to be some time before such law is issued. In the meantime, will investors sit back and patiently adopt a ‘wait and see’ approach?

Wood Mackenzie’s economic analysis indicates a negative impact on project economics under the Gross Split PSC. For a range of hypothetical exploration prospects, the PSC Contractor’s NPV1037 under the Gross Split PSC is lower when compared on a like-for-like basis with the existing Cost Recovery PSC terms. While oil projects fare worse under the new terms (as compared to the existing terms), the impact on gas developments is far more significant, as can be seen on page 9. For developments offshore, Wood Mackenzie found that the Gross Split PSC could render development of new gas discoveries uneconomic and thus deter new investment in exploration, particularly in offshore and frontier areas. For gas projects, the Gross Split PSC terms are particularly punitive as gas projects (a) typically require high upfront investment, (b) have a longer but flatter production profile, and (c) typically receive a lower price (fixed in Indonesia for domestic gas) than oil. Therefore it’s likely to take even longer for a PSC Contractor to recover the upfront investment, and that is before the lack of variable splits offered for gas projects is considered.

36 Investor Daily, page 9, 8 March 2017.37 NPV denotes the ‘net present value’, which refers to the total of all cash flows to (and from)

the given party. A specific discount rate is also associated with NPV and that rate (expressed as an annual percentage) is often appended. Therefore ‘NPV10’ means the NPV at a 10% discount rate.

Continued on next page >

998310

PSC Contractor NPV10 (US$ millions)

PSC type and cost reduction (if any)

20 mmbbl onshore oil

100 bcf onshore gas

20 mmbbl shelf oil

200 bcf shelf gas

400 mmbbl deepwater oil

2 tcf deepwater gas

Cost recovery PSC 188.9 79.5 128.9 14.8 1,346.3 259.6

Gross split PSC 142.5 30.9 101.6 -26.2 1,049.5 -10.9

Gross split PSC,10% cost reduction

154.2 42.0 122.5 -6.3 1,410.2 176.9

Gross split PSC,20% cost reduction

165.9 53.1 142.9 13.2 1,766.4 363.3

A more efficient and lower cost industry is one of the key objectives of the Gross Split PSC terms. A reduction in costs in the region of 10-20% would improve the economics for half of the hypothetical developments outlined above. However it is far from clear whether the industry will be able to reduce costs, given Indonesia’s regulatory framework and the uncertainty surrounding previously discussed elements of the Gross Split PSC implementation. For the past two years or so, with a backdrop of a US$30-$50/per barrel oil price, many operators have been striving to reduce operating costs and increase efficiencies as far as possible. We would question to what extent it is possible for such companies to achieve a further 10-20% reduction.

PSC Contractor IRR39 comparison: Gross split PSC vs. Cost recovery PSC, for exploration prospects40

PSC Contractor IRR, %

PSC type and cost reduction (if any)

20 mmbbl onshore oil

100 bcf onshore gas

20 mmbbl shelf oil

200 bcf shelf gas

400 mmbbl deepwater oil

2 tcf deepwater gas

Cost recovery PSC 60.2% 31.9% 27.8% 11.7% 17.9% 11.4%

Gross split PSC 47.2% 19.7% 24.0% 5.5% 16.5% 9.9%

Gross split PSC,10% cost reduction

53.8% 24.2% 28.3% 8.8% 19.4% 11.5%

Gross split PSC,20% cost reduction

61.8% 29.5% 33.3% 12.7% 22.8% 13.3%

38 Wood Mackenzie,’Indonesia’s gross split PSC: Improved efficiency at risk of lower investment?’ This data assumes an oil price of US$60/bbl; US$6/mcf, 2.0% p.a.

39 IRR means ‘internal rate of return’, which measures the profitability of potential investments. 40 Wood Mackenzie,’Indonesia’s gross split PSC: Improved efficiency at risk of lower

investment?’ Again, this data assumes an oil price of US$60/bbl; US$6/mcf, 2.0% p.a.

PSC Contractor NPV10 comparison: Gross split PSC vs. Cost recovery PSC, for exploration prospects38

Continued on next page >

Pinsent Masons | Indonesia’s new Gross Split Production Sharing Contract

11

6. Comparison to other SE Asian jurisdictions

The Government is facing the challenge of attracting much-needed investment into oil and gas exploration in Indonesia. How does it compare to other countries in the region?

In a study carried out by Wood Mackenzie,41 Indonesia is ranked 137th out of 148 global oil and gas fiscal regimes. Despite relatively attractive fiscal terms and prospectivity in comparison with other Southeast Asian regimes, Indonesia suffers due to uncertainty and instability surrounding the country’s regulatory environment. While the introduction of (and the uncertainties around) the Gross Split PSC will reduce Indonesia’s fiscal attractiveness ranking, the impact on the regulatory environment remains unclear.

41 Wood Mackenzie, ‘A balancing act: global fiscal terms and benchmarking’, October 2016.

Continued on next page >

Shows the Indonesian Gross Split PSC terms Shows the existing Cost Recovery PSC Terms

998312

42 Unfortunately it was reported on 20 March 2017 that MEMR is not planning to add any more incentives in connection with exploration activities. Energy and Mineral Resources Deputy Minister Arcandra Tahar commented that: “There will not be any [incentives for exploration]. Realistically, every oil company wants to conduct exploration activities and all the factors have been included in the Gross Split [PSC] scheme. It’s the same with the [Cost Recovery PSC]. Failed explorations will lead to sunk costs” (Petromindo.com, 20 March 2017).

43 At present, no enhanced oil recovery projects are taking place in Indonesia as such projects prove uneconomic under the Cost Recovery PSC. The issue is not specifically addressed, or incentivised under the Gross Split PSC.

7. Conclusions

Given Indonesia’s rapidly declining production rate and lack of exploration, many argue that an overhaul of the PSC regime was long overdue. Radical change was needed; but does the Regulation introduce the ‘right kind of radical’? While the new model should remove layers of inefficient regulation and micro-management, this will come at the cost of an ultimately lower take for PSC Contractors. Is it worth it? Investors will be keen to see the new gross split regime in the context of a new overarching oil and gas law, but the latter has been debated for over eight years and still appears some way off.

Many of Indonesia’s producing fields are mature and will require significant additional investment to prolong their life. While an increased focus on reducing costs (which the Gross Split PSC aims to achieve) is one part of the equation, Indonesia also needs to stimulate investment into its upstream industry. This requires an increase in the rewards available for the risks being run. Huge exploration potential still remains but, without such investment, this will remain untapped. Recent exploration performance suggests that Indonesia cannot attract companies based on prospectivity alone – Indonesia will need to adjust its fiscal split and bureaucratic climate, as well as its contractual platform, to increase its competitiveness in the global market for exploration spend.42

Ultimately, with greater IOC scrutiny on exploration budgets, capital costs and project returns in this new lower-for-longer oil price environment, Indonesia is competing for a share of a smaller and more focused supply of capital. Is the Gross Split PSC mechanism likely to spur investment? Unfortunately, our analysis demonstrates that, for many projects (particularly frontier, marginal fields, enhanced oil recovery43 and gas projects), the Gross Split PSC may result in a higher take for the Government and a drop in both the NPV and IRR for the PSC Contractor. Indeed, the Government’s overall share in production may actually decrease compared to current levels if fewer companies are willing to invest.

Pinsent Masons | Indonesia’s new Gross Split Production Sharing Contract

13

Steven PotterPartnerSingaporeT: +65 6309 5671M: +65 9711 7334E: [email protected]

Ashley WrightPartnerSingaporeT: +65 6309 5672M: +65 8869 2471E: [email protected]

Elizabeth Muir AssociateSingaporeT: +65 6309 5663M: +65 8869 4062E: [email protected]

Widya RianitaAssociateSingaporeT: +65 6305 8497M: +65 8798 1081E: [email protected]

Key contactsFor further details relating to this article, the Indonesian oil and gas market, or any other oil and gas related matter in Asia Pacific, please contact:

Continued on next page >

Pinsent Masons:

Andrew HarwoodResearch DirectorAsia Pacific, Upstream Oil & GasSingaporeT: +65 6518 0850E: [email protected]

Ashima TanejaSenior Research ManagerAsia-Pacific, Upstream Oil & GasSingaporeT: +65 6249 0739E: [email protected]

Wood Mackenzie:

998314

Pinsent Masons | Indonesia’s new Gross Split Production Sharing Contract

Appendix: Overview of the existing Cost Recovery PSC

This Appendix sets out background on the existing cost recovery mechanism, which is applicable to all conventional PSCs executed before the enactment of the Regulation on 13 January 2017. Under the cost recovery mechanism, which has become a trademark of Indonesian regulation in recent years, the Government reimburses the relevant PSC Contractor for all (allowable) exploration, development and production costs.

First Tranche Petroleum

Under pre-2002 contracts, PSC Contractors and the Government were both entitled to take first tranche petroleum (‘FTP’) and received petroleum equal to 20% of the production before the deduction for operating costs. FTP was then split according to their respective equity shares as states in the contracts. Under later PSCs, the Government was entitled to take the entire FTP (although at a lower rate of 10%) with no sharing with the PSC Contractor. For recent conventional PSCs, the FTP of 20% is now once again shared with the PSC Contractor. The fairly obvious reason behind FTP is to secure Government revenue from the asset. In later versions of the Cost Recovery PSC, there is no cap on levels of cost recovery which could be deducted from the sales of oil and gas production.44

Cost Recovery

Cost recovery takes place after FTP. Under the latest (fifth) version of the existing Cost Recovery PSC in Indonesia, the PSC Contractor is entitled to recover all allowable costs (including production costs) as well as amortised exploration and capital costs. However the recovery of exploration costs is limited to the production arising from the contracted ‘field’ that has an approved PoD – effectively quarantining cost recovery to exploration costs incurred in respect of the initial and then subsequent ‘fields’ which are subject to a PoD rather than the entire PSC contract area.

Approval of work programmes and budgets

Since the recoverable costs incurred by the PSC Contractor reduces the Goverment’s take, Indonesia’s upstream oil and gas regulator, currently SKK Migas must approve each PSC Contractor’s work programme, budget and certain AFEs. BP Migas/SKK Migas’s tendency to push back on Contractor’s proposed budgets due to State budget-related concerns has in some cases limited PSC Contractors’ planned production programme, delayed projects and reduced technological improvements devised by PSC Contractors.45

Investment Credits

An ‘investment credit’ may also have been available to the PSC Contractor on direct development and production capital costs, only where as negotiated and approved by SKK Migas. A key characteristic of the process of exploration is the inherent delay in generating income. To mitigate this, a credit ranging from 17% to 55% of the capital cost of development, transport and production facilities46 was historically available. The investment credit can be taken in oil or gas in the first year of production, but typically may also be carried forward.

Profit oil/gas

Any oil or gas that remains after FTP, cost recovery and the investment credit is then split between SKK Migas and the PSC Contractor. This after-tax allocation would vary depending on the generation of the PSC in question, but oil PSCs could award as much as 85% of the production output to SKK Migas. In relation to gas PSCs, the after-tax split would usually be 70% for the Government share.

Bonuses

The PSC Contractor would ordinarily be required to pay a range of bonuses to the Government, including a signing and production bonus. Unsurprisingly, these are neither cost-recoverable nor tax deductible.

Domestic Market Obligation

44 Pre-1976 PSCs included a cost recovery cap of 40% of revenue (Oil and Gas in Indonesia Investment and Taxation Guide, PwC, May 2016, page 45).45 Agithama, K., New PSC Mechanism: Gross Split, The Challenge of its Implementation in Indonesia, International In-house Counsel Journal Vol. 10, No. 38, Winter 2017, 1, page 2. 46 Oil and Gas in Indonesia Investment and Taxation Guide, PwC, May 2016, page 51.

Continued on next page >

15

Pinsent Masons | Indonesia’s new Gross Split Production Sharing Contract

In addition, the PSC Contractor is required to sell a share of crude oil production to satisfy domestic needs, through the DMO. The quantity and price of the DMO is set out in the relevant PSC, and newer contracts have also required a gas DMO. At present, the PSC Contractor is generally required to supply a maximum of 25% of total oil production to the domestic Indonesian market out of its equity share of production.47 Under the Cost Recovery PSC, for the first five years the after commencing commercial production, the PSC Contractor is generally paid by SKK Migas the full value for its oil DMO (using the weighted average price). This is reduced to 10% of that price for subsequent years.

Equipment and data ownership

Under the Cost Recovery PSC, all equipment, machinery, inventory, materials and supplies purchased by the PSC Contractor become the property of the Government once landed in Indonesia. The PSC Contractor then enjoys a right to use and retain custody of such assets during the operations. The PSC Contractor has access to exploration, exploitation, and geological and geophysical data, but such data remains the property of MEMR.

47 Ibid, page 54.

Continued on next page >

998316

Key contactsPinsent Masons’ Global Oil and Gas Team

Bob RuddimanSector HeadEnergy & Natural ResourcesAberdeenT: +44 (0)1224 377925M: +44 (0)7767 316970E: [email protected]

Paul McGoldrickPartnerProjects, Energy & FinanceLondonT: +44 (0)20 7490 6613M: +44 (0)7764 659779E: [email protected]

Shirley AllenPartnerProjects, Energy & FinanceAberdeenT: +44 (0)121 629 1580M: +44 (0)7809 584243E: [email protected]

UK

Steven PotterPartnerProjects, Energy & Finance SingaporeT: +65 6309 5671M: +65 9711 7334E: [email protected]

Ashley WrightPartnerProjects, Energy & FinanceSingaporeT: +65 6309 5672M: +65 8869 2471E: [email protected]

George BoothPartnerProjects, Energy & FinanceLondonT: +44 (0)20 7490 6984 / +971 4 373 9700M: +44 (0)7766 820814 / +971 50 621 0537E: [email protected]

Akshai FofariaPartnerProjects, Energy & FinanceLondonT: +44 (0)20 7418 8242M: +44 (0)7860 606316E: [email protected]

Asia Pacific

Middle East

Africa

9983

This note does not constitute legal advice. Specific legal advice should be taken before acting on any of the topics covered.Pinsent Masons LLP is a limited liability partnership, registered in England and Wales (registered number: OC333653) authorised and regulated by the Solicitors Regulation Authority and the appropriate jurisdictions in which it operates. The word “partner”, used in relation to the LLP, refers to a member or an employee or consultant of the LLP, or any firm or equivalent standing. A list of the members of the LLP, and of those non-members who are designated as partners, is available for inspection at our registered office: 30 Crown Place, London, EC2A 4ES, United Kingdom. © Pinsent Masons 2017.

For a full list of the jurisdictions where we operate, see www.pinsentmasons.com