indonesia economic quarterly -...

TRANSCRIPT

Indonesia Economic Quarterly Current challenges, future potential

Shubham ChaudhuriIndonesia Lead EconomistWorld Bank

28 June 2011BKPM, Jakarta

OutlineWhat I will be talking about

Indonesia’s economic outlook Strong recent performance and even greater future potential

What is the plan to get there? The Master Plan 2011-2025

What are the current challenges? Relating to energy subsidies, food prices and financial markets

How to reach Indonesia’s potential and deliver on the ambitions of the Master Plan? Implementation is the key – prioritization, coordination,

financing

Indonesia’s economic outlook

Indonesia’s economic outlookPositive recent growth performance…

GDP growth in Q1 2011 moderated but was still 6.5 percent year-on-year. Growth projections for 2011 and 2012 are 6.4 percent and 6.7 percent

Source: Thomson Financial Datastream

-10

-5

0

5

10

15

-10

-5

0

5

10

15

2006Q1 2007Q1 2008Q1 2009Q1 2010Q1 2011Q1

Indonesia China India Malaysia Philippines ThailandPercent, yoy

Indonesia’s economic outlook …plus record balance of payment inflows…

Note: Errors and omissions not shownSource: BI

The overall balance of payment inflows in Q1 reached USD 7.7 billion, the second highest on record

-8

-4

0

4

8

12

-8

-4

0

4

8

12

Mar-05 Mar-07 Mar-09 Mar-11

Current account Net portfolioNet direct investment Net otherOverall balance

USD billion

Indonesia’s economic outlook …and an upward trend in FDI inflows …

0

1

2

3

4

5

0

1

2

3

4

5

2004Q1 2005Q1 2006Q1 2007Q1 2008Q1 2009Q1 2010Q1 2011Q1

Quarterly net FDI inflows

4-quarter rolling average

USD billion USD billion

Source: BI

Indonesia’s economic outlook …attracted by Indonesia’s economic potential

Source: World Bank staff projections

What is the plan to reach Indonesia’s economic potential?

The plan to reach Indonesia’s potentialThe Master Plan 2011-2025…

“Plantations Production and Processing Center and National

Energy Reserve"

“Mining Production and Processng Center and

National Energy Reserve"

“National Plantation, Agriculture, and Fisheries Production and Processing

Center''

Sumatera CorridorKalimantanCorridor Sulawesi Corridor

'‘National Tourism Gate and National Food

Support''

“National Industry and Services Booster"

“Abundant Natural Resources Processing and

Prosperous Human Resources"

Jawa CorridorBali Nusa Tenggara Corridor

Papua Corridor

Source: Coordinating Ministry for Economic Affairs “Acceleration and Expansion of Indonesia’s Economic Development Master Plan 2011-2025”

The plan to reach Indonesia’s potential ..aims to increase investment…

The plan to reach Indonesia’s potential ..and reverse the decline in infrastructure spending…

Infrastructure investment to GDP has yet to recover from the post-1997/1998 crisis declines

Source: MoF, World Bank, PPI database, company reports, BPSmarket, FAO

0

2

4

6

8

0

2

4

6

8

1994-1997 1998-2002 2003-2006 2007-2009

Percent of GDP Percent of GDP

The plan to reach Indonesia’s potential …to improve its quality … Indonesia ranks relatively low on measures of infrastructure quality

such as in the World Economic Forum Global Competitiveness Report

Note: Brackets indicate global rankingSource: WEF Global Competitiveness Report

1 2 3 4 5 6 7

Vietnam (123)

Philippines (113)

India (91)

Indonesia (90)

China (72)

Thailand (46)

Malaysia (27)

Quality of infrastructure index (scale 1-7 where 7 is the best)

The plan to reach Indonesia’s potential …which currently is a major constraint for firms

Note: * Most recent survey conducted in 2010 but question concerned the situation in 2009. Rank amongst 22 surveyed obstaclesSources: World Bank – LPEM-UI firm level investment climate

Share of firms citing issue as major obstacle to operating and investing, percent

46

21

26

21

1 3

10

0

20

40

60

80

0

20

40

60

80

Transportation Electricity Telecom.

2005 2007 2009*

Percent (label indicates rank as obstacle)

What are the current challenges?

Current challenges Rising oil prices…

0

40

80

120

160

0

40

80

120

160

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11

USD per Barrel

Indonesian CrudeOil price

Average price of Indonesian Crude Oil forJan-May 2011: USD 113

2011 Budgetassumption: USD 80

Sources: MoF, CEIC, World Bank

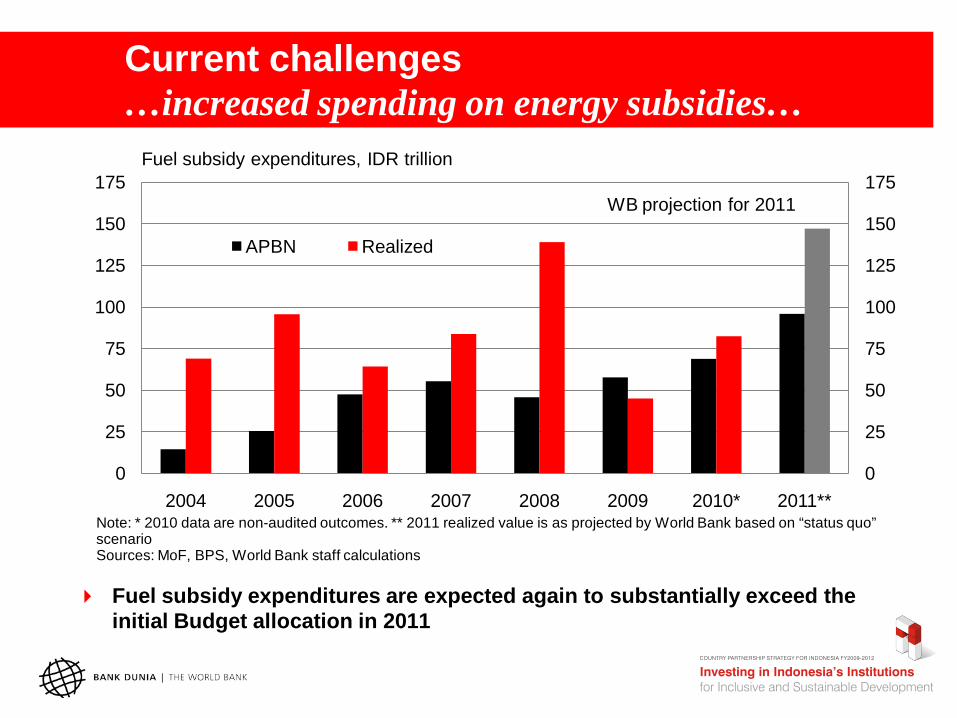

Current challenges …increased spending on energy subsidies…

Note: * 2010 data are non-audited outcomes. ** 2011 realized value is as projected by World Bank based on “status quo” scenarioSources: MoF, BPS, World Bank staff calculations

0

25

50

75

100

125

150

175

0

25

50

75

100

125

150

175

2004 2005 2006 2007 2008 2009 2010* 2011**

APBN Realized

Fuel subsidy expenditures, IDR trillion

WB projection for 2011

Fuel subsidy expenditures are expected again to substantially exceed the initial Budget allocation in 2011

Current challenges …imposing a high opportunity cost

Note: Data is actual expenditures. * 2010 data are non-audited outcomesSources: MoF, World Bank staff calculations

0

50

100

150

200

250

0

50

100

150

200

250

2005 2006 2007 2008 2009 2010*

Energy subsidies

Capital expenditures

Social expenditures

IDR trillion

Current challenges Potential spillovers from Euro zone debt crisis…

Source: BI, CEIC, Thomson Financial Datastream Note: Portfolio flows are sum of non-resident purchases of equities plus changes in their holdings of SUN (government securities) and SBI (BI certificates). CDS spreads are on five year external sovereign bonds

-15

-10

-5

0

5

10

0

500

1,000

1,500

2,000

2,500

Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Jan-11

USD billionBasis points

Greece sovereign CDS spreads, LHS

Portfolio capital inflows into Indonesia, RHS

Current challenges …and vulnerabilities to capital flow reversals

0 20 40 60 80 100 120 140

Total FX Reserves

Short-term external debt*

Non-resident equity holdings

Non-resident local gov. securities holdings

Non-resident SBI holdings

Sep 2008

May 2010

Sept 2010

Apr 2011

USD billionNote: * short-term external debt by remaining maturity. Data denoted April is as of end-March 2011 Sources: BI, CEIC, KSEI, CEIC, MoF

Current challengesPotential for further food prices shocks…

0

2,000

4,000

6,000

8,000

10,000

12,000

0

2,000

4,000

6,000

8,000

10,000

12,000

Jan-08 Nov-08 Sep-09 Jul-10 May-11

Rice price IDR/kg (medium quality)

Domestic

International (Thai)

Sources: Jakarta wholesale markets, FAO

Current challenges…which affect poorer households the most Food accounts for more than 50 percent of expenditures for half

of the population in Indonesia

Rice alone is 17 percent of the expenditures of the poorest 20 percent of the population but just 4 percent for top 20 percent

Estimated impact of a rise in prices by 10 percent on the poverty rate

10 percent rise in price for:

Estimated increase in the poverty rate (percentage points)

Rice 1.3Food price index 3.5Gasoline 0.2Energy price index 0.4

Sources: World Bank staff calculations based on Susenas

How to reach Indonesia’s potential and deliver on the ambitions of the Master Plan?

Reaching Indonesia’s potentialPrioritization - improving connectivity

GEOGRAPHICAL distance between major cities in

Indonesia and Singapore

ECONOMIC distance within Indonesia based on SEA

transport costs

ECONOMIC distance within Indonesia based on AIR

transport costs

Reaching Indonesia’s potential Prioritization of catalytic public sector investments Requires addressing ongoing disbursement challenges for

capital expenditures

0

20

40

60

0

20

40

60

Personnel Material Capital Energy subsidies

Social Central exp.

Transfers

2008 2009 2010 2011

Percent PercentSpending in first five months as share of full-year Budget allocation

Sources: MoF, World Bank staff

Reaching Indonesia’s potential Coordination and financing … Successful implementation can also be aided by

mechanisms for: coordination across ministries and levels of government; in-depth monitoring and evaluation; ongoing adjustments to the plan as needed

How to finance the targeted USD 468 billion of investments over 2011-2025? Private sector participation is ambitious - half of the total

– and requires support from: Long-term infrastructure financing mechanisms Improvements in regulatory and legal certainty Enhancing skills (3rd pillar) and complementary “soft”

infrastructure to increase returns from investment

Indonesia Economic QuarterlyCurrent challenges, future potential

Shubham ChaudhuriIndonesia Lead EconomistWorld Bank

28 June 2011BKPM, Jakarta