indian consumer survey -arpita_final 100702

TRANSCRIPT

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 1/32

New Insights into Modern India

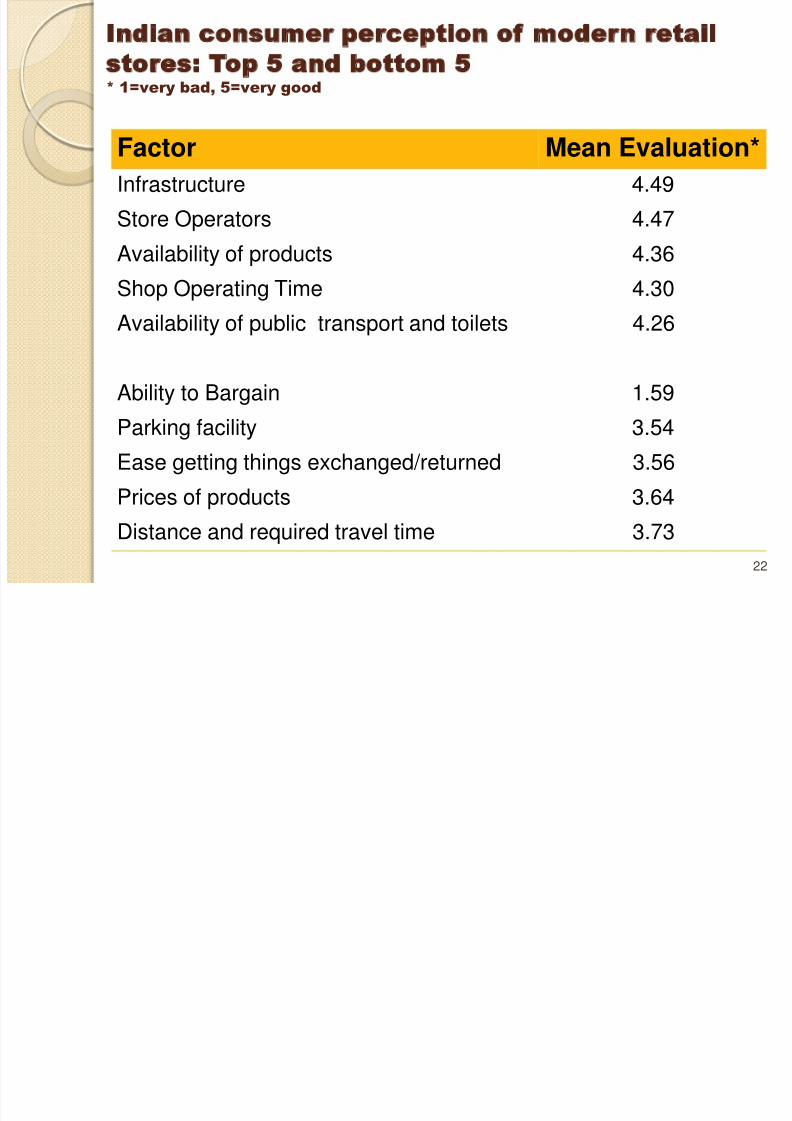

Shopper Behavior and Implications

for Global Retailers and Local

Policymakers

Arpita MukherjeeProfessor, Indian Council for Research on International Economic

Relations (ICRIER)New Delhi, India

Murali K. MantralaSam Walton Professor of Marketing

University of Missouri, Columbia

Shaoming ZouRobert J. Trulaske, Sr. Professor of Marketing

University of Missouri, ColumbiaExternal Professor of Marketing, Peking University

Presentation at 2010 China India Consumer Insights Conference, Yale Univ.-Tsinghua Univ., Beijing, July 3, 2010

1

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 2/32

Motivation Along with China, India has emerged as one of the most

attractive countries for both domestic and internationalretailers.

◦ “The Indian organized retail market is expected …to exceed $50billion by 2013. reflecting a fast-growing middle class demandinghigher quality shopping environment and stronger brands”

(A. T. Kearney Global Retail Development Index Report).

Modern retail outlets growing at 30% - major foreignbrands are entering India.

Policy changes are taking place

◦

Partial opening up of single brand retailers in 2006 (multi-brandretailers are still restricted).

◦ Government is evaluating the scope for further liberalization.

Indian consumers are changing….

2

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 3/32

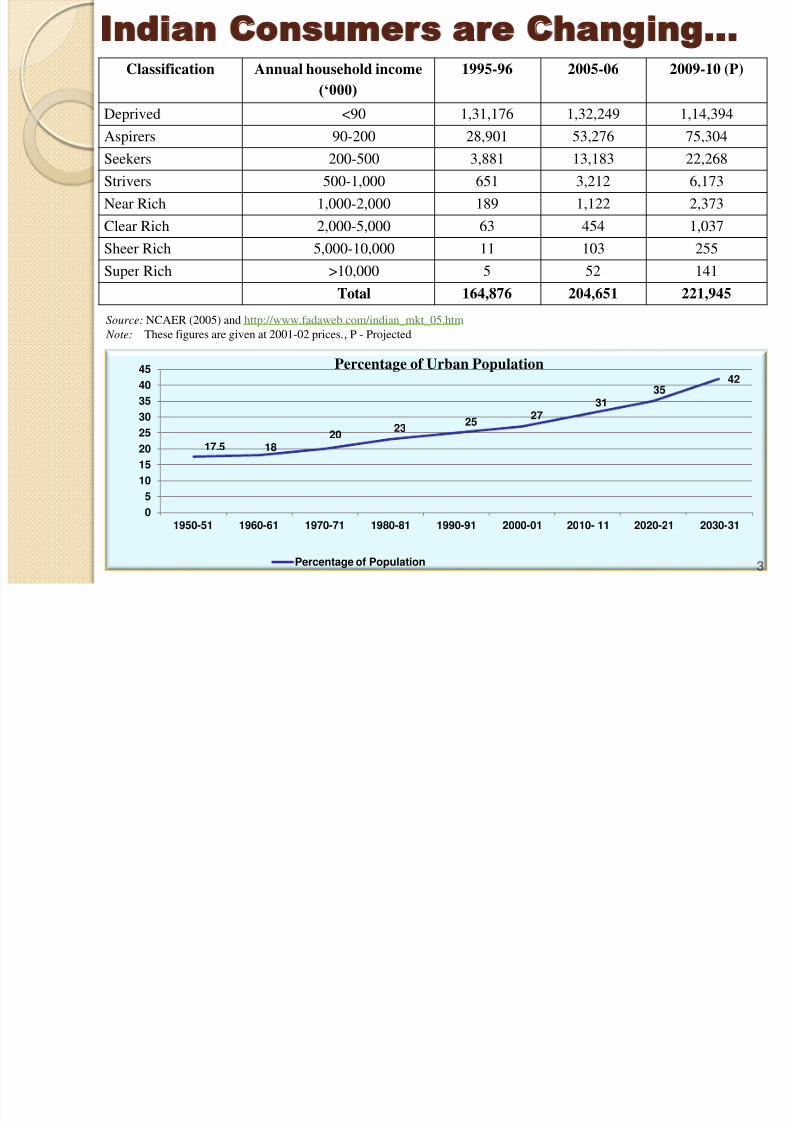

Indian Consumers are Changing…

17.5 1820

2325

2731

3542

0

5

10

15

20

25

30

35

40

45

1950-51 1960-61 1970-71 1980-81 1990-91 2000-01 2010- 11 2020-21 2030-31

Percentage of Population

Percentage of Urban Population

Classification Annual household income

(‘000)

1995-96 2005-06 2009-10 (P)

Deprived <90 1,31,176 1,32,249 1,14,394

Aspirers 90-200 28,901 53,276 75,304Seekers 200-500 3,881 13,183 22,268

Strivers 500-1,000 651 3,212 6,173

Near Rich 1,000-2,000 189 1,122 2,373

Clear Rich 2,000-5,000 63 454 1,037

Sheer Rich 5,000-10,000 11 103 255

Super Rich >10,000 5 52 141Total 164,876 204,651 221,945

Source: NCAER (2005) and http://www.fadaweb.com/indian_mkt_05.htm Note: These figures are given at 2001-02 prices., P - Projected

3

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 4/32

Our Research Objectives &

Questions

To gain insights into Indian consumers’ shoppingbehaviors

◦ What is their level of brand awareness and brandconsciousness?

◦ What type of products do they purchase? From whatkinds of retail outlets?

◦ What are the factors determining the choice of retailoutlets & frequency of shopping for particular

products? To draw useful implications for retailers and

policymakers

4

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 5/32

Our Intended Contribution

Our research is based on a primary

survey of 300 high and middle-income,educated consumers’ shopping behavior

across eight product categories

conducted in 2009.

Despite growing size and importance of the Indian Retail sector, existing primary research data on Indian

shoppers are very limited.

5

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 6/32

Presentation Organization

Description of the primary survey

Sample profile

Summary results of Indian shopperbehavior

Lessons for retailers and policymakers

Next Steps

6

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 7/32

Survey Procedures

A three-tier survey was conducted through door-to-door

interviews and through interviews with consumers inshopping malls

Focused on the consumers’ level of brand consciousness,where they purchase such brands from, and what factors

determine their purchase decisions.

Cities covered during the Survey

Tier I Mumbai, Chennai, Delhi, Kolkata,Hyderabad, Ahmedabad

Tier II & Tier IIIAllahabad, Bhubaneswar, Kanpur,

Surat, Visakhapatnam

7

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 8/32

Product Categories

Clothing and Fashion Accessories

Footwear and Leather Goods

Gems and Jewellery

Food and Grocery

Home Furnishing and Home Appliances

Sports Goods

Health and Wellness Products

Gifts and Stationery Items 8

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 9/32

Sample Profile

61.67%

38.33%

Gender Distribution

Males

Females

13

132

151

40

20

40

60

80

100

120

140

160

19-22 23-30 31-60 >60

Age Distribution

6 11

160

123

0

20

40

60

80

100

120

140

160

180

Schooling Some collegebut not

graduate

Graduate Post Graduate

Education Distribution11

72

94

109

9

3 2

Income-wise Distribution

50 Lakhs - 1 Crore 20 Lakhs - 50 Lakhs 10 Lakhs - 20 Lakhs

5 Lakhs - 10 Lakhs 2 Lakhs - 5 Lakhs 1 Lakh - 2 Lakhs

Up to 1 Lakh

In per cent

9

1 Lakh = $2,220

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 10/32

Sample Distribution across City-tiers

67%

23%

10%

Percentage Distribution

Tier I

Tier II

Tier III

Location Total

Tier 1 citiesDelhi 51

Mumbai 47

Kolkata 40

Chennai 38

Hyderabad 25

Total 201

Tier II Cities

Surat 13

Ahemdabad 10

Vishakhapatnam 12

Kanpur 16Allahabad 18

Total 69

Tier III Cities

Bhubaneswar 30

Total 30

Grand Total 30010

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 11/32

Ownership of Autos

11

L uxury car

Small car 2 - Wheeler

176

34 15

12

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 12/32

Media and Brand Awareness

12.33%

87.67%

Percentage of RespondentsTravelled Internationally

Yes No

• 65% of the respondentswho travel abroadpurchase foreign brandsduring their international

trips

• 79% of those whopurchase duringinternational trips say

that products aredifferent from India

30%

70%

Level of Awareness – Use

of Media

Do not follow updates Follow updates

12

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 13/32

Summary Findings of

Indian Shopper

Behavior

13

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 14/32

Regional and City-wise Distribution of

Branded Product Purchases

Products

North

Region

South

Region

East

Region

West

Region

Sample Distribution

(No.)85 75 70 70

In per cent

Fresh Fruits &

Vegetables10.6 2.7 2.9 12.9

Preserved Food &

Agro Products64.7 21.3 51.4 20.0

Apparel 24.7 56.0 48.6 35.7

Handbags 65.9 28.0 61.4 37.1

Footwear 78.8 93.3 92.9 91.4

Jewellery 68.2 57.3 68.6 47.1

Consumer Durables 100.0 89.3 90.0 90.0

Costume Jewellery 32.9 4.0 18.6 27.1

Furniture 51.8 30.7 32.9 27.1

Ceramic

Tiles/Sanitary ware 83.5 65.3 50.0 28.6

Products Delhi Kolkata

Sample Distribution

(No.)51 39

In per cent

Fresh Fruits &

Vegetables5.9 5.0

Preserved Food &

Agro Products56.9 60.0

Apparel 29.4 32.5

Handbags 51.0 62.5

Footwear 94.1 87.5

Watches 100.0 97.5

Jewellery 52.9 62.5

Costume Jewellery 25.5 15.0

Furniture 49.0 35.0

Ceramic

Tiles/Sanitary ware72.5 40.0

Consumer Durables 100.0 95.014

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 15/32

Knowledge about Foreign Brands

BrandYear ofEntry

Mode of OperationKnow/Not

UseDo Not Know Know/Use

Bata 1931 Wholly owned subsidiary 22 2.67 75.33

Rayban 1990 Wholly owned subsidiary 33.67 3 63.33United Colors ofBenetton

1991 Wholly owned subsidiary 64 11.67 24.33

Nike 1995Exclusive licensingagreement

44.67 4.33 51

ErmenegildoZegna

2000 Franchise agreement 13 86.67 0.33

Louis Vuitton 2003 Distribution Agreement 18 78 4Versace 2006 Franchise agreement 35.33 61.33 3.33

Da Milano 2006 Privately held company 57.67 34.67 7.67

Gucci 2006Exclusive licensingagreement

55.67 14.33 30

SalvatoreFerragamo

2006 Joint Venture 12.67 87 0.33

Mango 2006 Exclusive licensingagreement

33.33 63 3.67

NEXT 2006 Franchise agreement 52.33 41 6.67

Dolce &Gabbana

2007 Joint Venture 35.67 55.67 8.67

Giorgio Armani 2008 Joint Venture 52.67 35.33 12

Bottega Veneta 2008 Exclusive licensingagreement 12.67 87 0.33

(in percent )

15

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 16/32

Why do Consumers Choose Branded

Products?

149

128

69

0

2040

60

80

100

120

140

160

Better Quality Better Design More Variety

Leather Goods

24

4

0

5

10

15

20

25

30

Better Quality More Variety

Fresh Fruits and Vegetables

116109

92

0

20

40

60

80

100

120

140

Better Design Better Quality More Variety

Apparel

114

14 11

0

20

40

60

80

100

120

Better Packaging Affordibility More Variety

Preserved Food and Agro Products

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 17/32

Where do Consumers Purchase?

Sectors Small Retailers CorporateRetailers Both

Fresh Fruits andVegetables

274 22 4

FMCG products 258 40 2

Preserved Foodand Agro products

191 41 1

Jewellery 92 182 11

Handbags 82 148 3

Apparel 3 202 95

Footwear 3 269 28

17

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 18/32

224232

297

240

2 3 3 5

74

65

0

55

0

50

100

150

200

250

300

350

Spending Frequency of Purchase Brand Conciousness Quality Copnciousness

P o p u l a t i o

n

Purchasing Pattern

Increased Decreased Unchanged

Effects of Emergence of Corporate Retail

Outlets/ Malls on Purchasing Pattern

18

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 19/32

Periods of Purchase for different

Product Categories

3756

253

22

225

30

50

100

150

200

250

300

New Product

Released in

market

Seasonal Sales

& Discounts

Festivals Family

Occasions

Regular

Purchases

Seaonal

Pruchase

Apparel

5

51

108

6

179

20

20406080

100120140160180200

New

Product

Released in

market

Seasonal

Sales &

Discounts

Festivals Family

Occasions

Regular

Purchases

Seaonal

Pruchase

Leather Goods

1

299

0

50

100

150

200

250

300

350

Festivals Regular Purchases

Fresh fruits

19

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 20/32

Importance of Various Factors in

Consumers’ Choice of Modern Retail Stores

Note: Scale of 1 to 5, higher is better. Percentage calculated on the basis of “high (4)” and “very high (5)” on factor

importance ratings. This is a multiple choice question

55

92

90

76

95

94

60

52

20

63

86

85

76

31

87

41

78

70

40

60

62

0 10 20 30 40 50 60 70 80 90 100

Price

Fresh New Stock/Exclusive Design

Preffered Brand/Variety

Better Packaging

Better Product Quality

Quality Assurance

Fixed Rate

Promotional Offers

Credit Facility Availability

Use of Credit/Debit Card

Better Customer Service

Better Ambience

Convenient Timings

Closer to House

Brand Image/Goodwill

Home Delivery

After Sales Service

Easy in Product Exchange

Customer Loyalty Card

Blend of Shopping and Entertainment

Availability of Foreign Brands

Per cent

20

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 21/32

Additional Analysis

Results

21

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 22/32

Indian consumer perception of modern retail

stores: Top 5 and bottom 5 * 1=very bad, 5=very good

Factor Mean Evaluation*

Infrastructure 4.49

Store Operators 4.47

Availability of products 4.36

Shop Operating Time 4.30

Availability of public transport and toilets 4.26

Ability to Bargain 1.59

Parking facility 3.54

Ease getting things exchanged/returned 3.56

Prices of products 3.64

Distance and required travel time 3.73

22

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 23/32

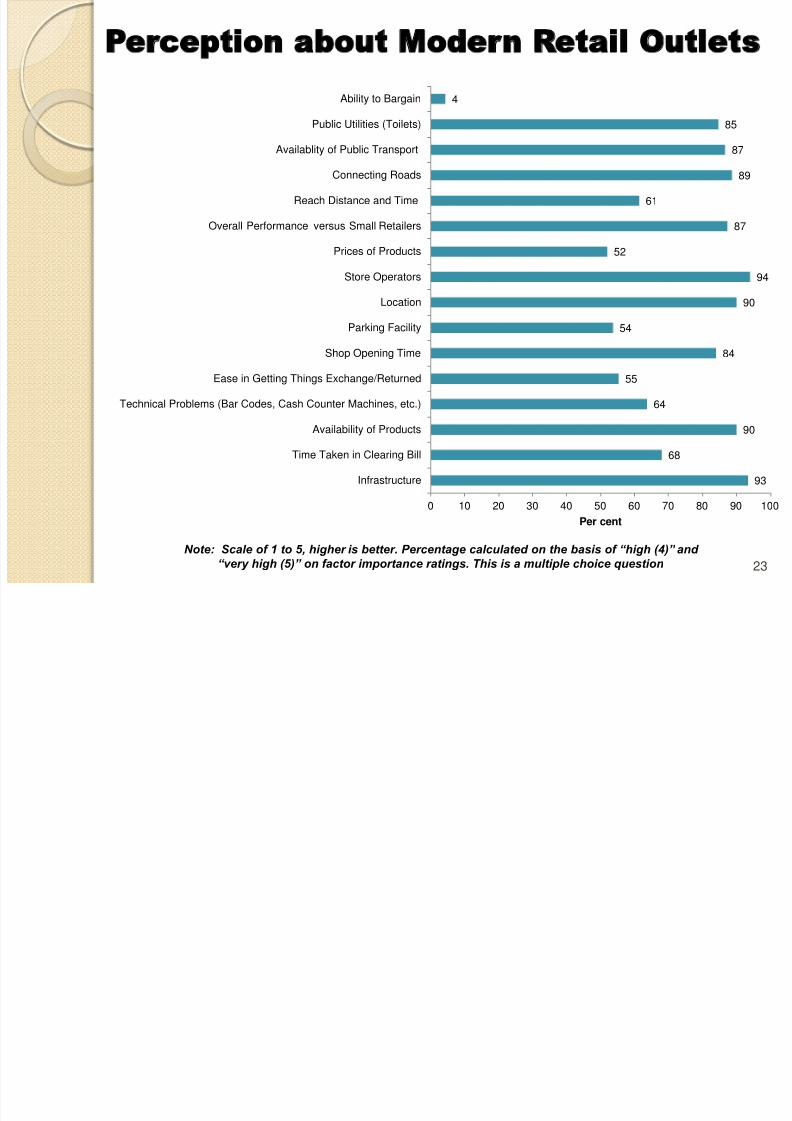

Perception about Modern Retail Outlets

93

68

90

64

55

84

54

90

94

52

87

61

89

87

85

4

0 10 20 30 40 50 60 70 80 90 100

Infrastructure

Time Taken in Clearing Bill

Availability of Products

Technical Problems (Bar Codes, Cash Counter Machines, etc.)

Ease in Getting Things Exchange/Returned

Shop Opening Time

Parking Facility

Location

Store Operators

Prices of Products

Overall Performance versus Small Retailers

Reach Distance and Time

Connecting Roads

Availablity of Public Transport

Public Utilities (Toilets)

Ability to Bargain

Per cent

Note: Scale of 1 to 5, higher is better. Percentage calculated on the basis of “high (4)” and “very high (5)” on factor importance ratings. This is a multiple choice question 23

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 24/32

Top 5 factors influencing Indian consumers’ shopping

at modern retail stores * 1=very low importance, 5=very high importance

Factor MeanImportance*

Product Quality 4.64

Assortment Selection and Newness 4.47

Customer Service 4.29

Store Ambience and Convenience 4.27

Price 3.71

24

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 25/32

Demographic effects on Indian consumer annual

spending on branded clothing and footwear(Stepwise Regression)

Significant Variable

Standardized

regression

coefficient t-ValueSignificance

level

Yearly household income .282 5.161 .000

Travelled abroad .188 3.440 .001

Model R2 = .120, F = 20.19, p < .001

25

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 26/32

Demographic effects on Indian consumer

purchase of branded products (Stepwise

Logistic Regression)

DependentVariable >

Handbags andJewelry

Furniture Fresh Fruits

Independent

VariableExp(B) Wald Sig. Exp(B) Wald Sig. Exp(B) Wald Sig.

Yearly household

income.598 16.13 .000 .509 9.23 .000

Travelled abroad .336 8.14 .004 .268 12.79 .000

Model Statistics:

-2 Log likelihood =

379.75

p < .001

-2 Log likelihood =

381.35

p < .001

-2 Log likelihood =

166.83

p < .005

26

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 27/32

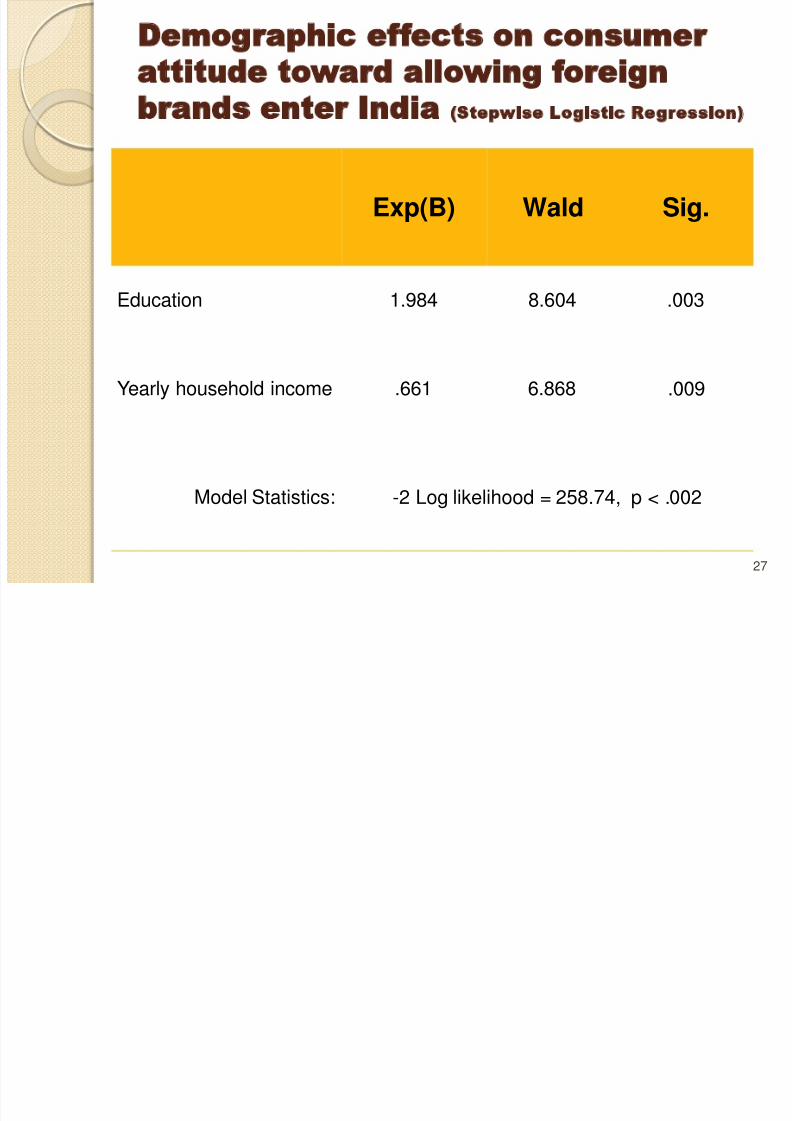

Demographic effects on consumer

attitude toward allowing foreign

brands enter India (Stepwise Logistic Regression)

Exp(B) Wald Sig.

Education 1.984 8.604 .003

Yearly household income .661 6.868 .009

Model Statistics: -2 Log likelihood = 258.74, p < .002

27

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 28/32

Implications for Global Retailers

• Brand consciousness is increasing but varies across

different product categories• Brands with longer presence are more likely to be knownand used

• Mode of entry is not related to brand knowledge• International travel increases brand awareness• Branded product should be same as in international

markets in terms of price and quality. Additionalrequirement of after-sale services and productcustomisation

• Indian consumers are price sensitive – right product pricing• May explore possibilities of sourcing from Indian market

• Customer brand loyalty is low. It varies across productcategory, gender, etc.

• India is not a homogenous market – vast difference acrossregions

• Modern retailers cater to a small segment of the Indian

population 28

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 29/32

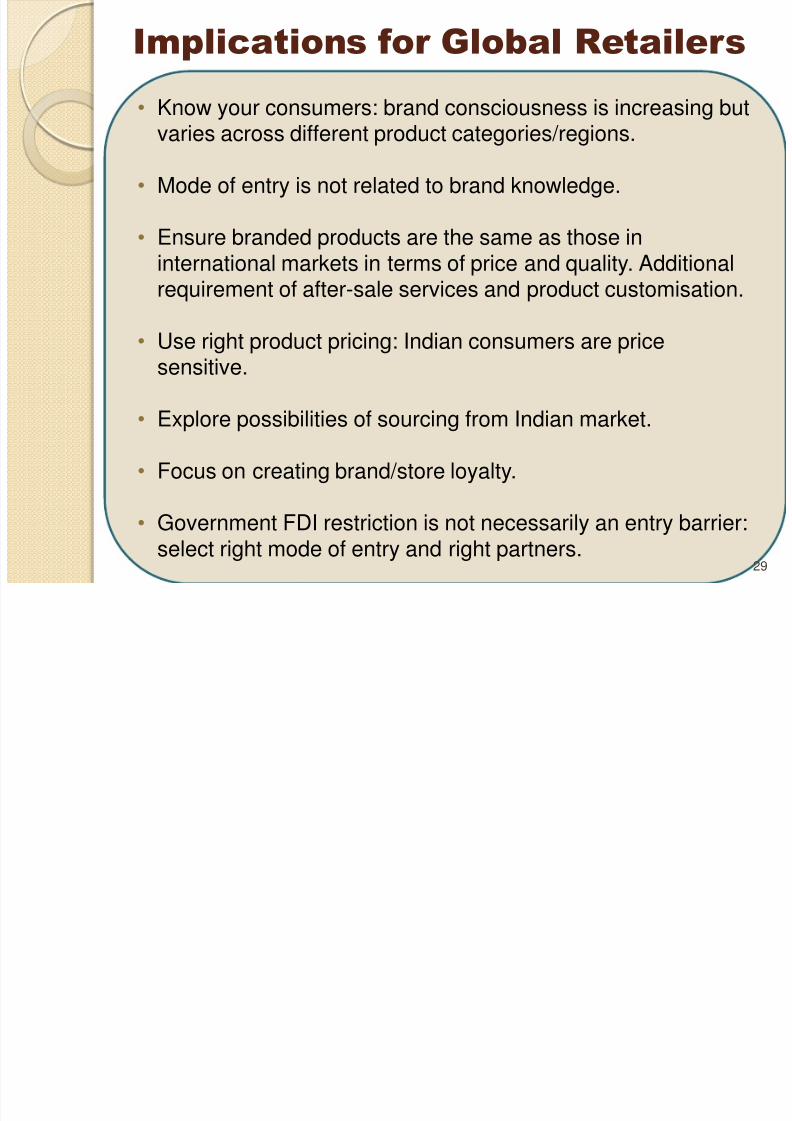

Implications for Global Retailers

• Know your consumers: brand consciousness is increasing but

varies across different product categories/regions.

• Mode of entry is not related to brand knowledge.

• Ensure branded products are the same as those ininternational markets in terms of price and quality. Additionalrequirement of after-sale services and product customisation.

• Use right product pricing: Indian consumers are pricesensitive.

• Explore possibilities of sourcing from Indian market.

• Focus on creating brand/store loyalty.

• Government FDI restriction is not necessarily an entry barrier:

select right mode of entry and right partners. 29

I li ti f P li M k

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 30/32

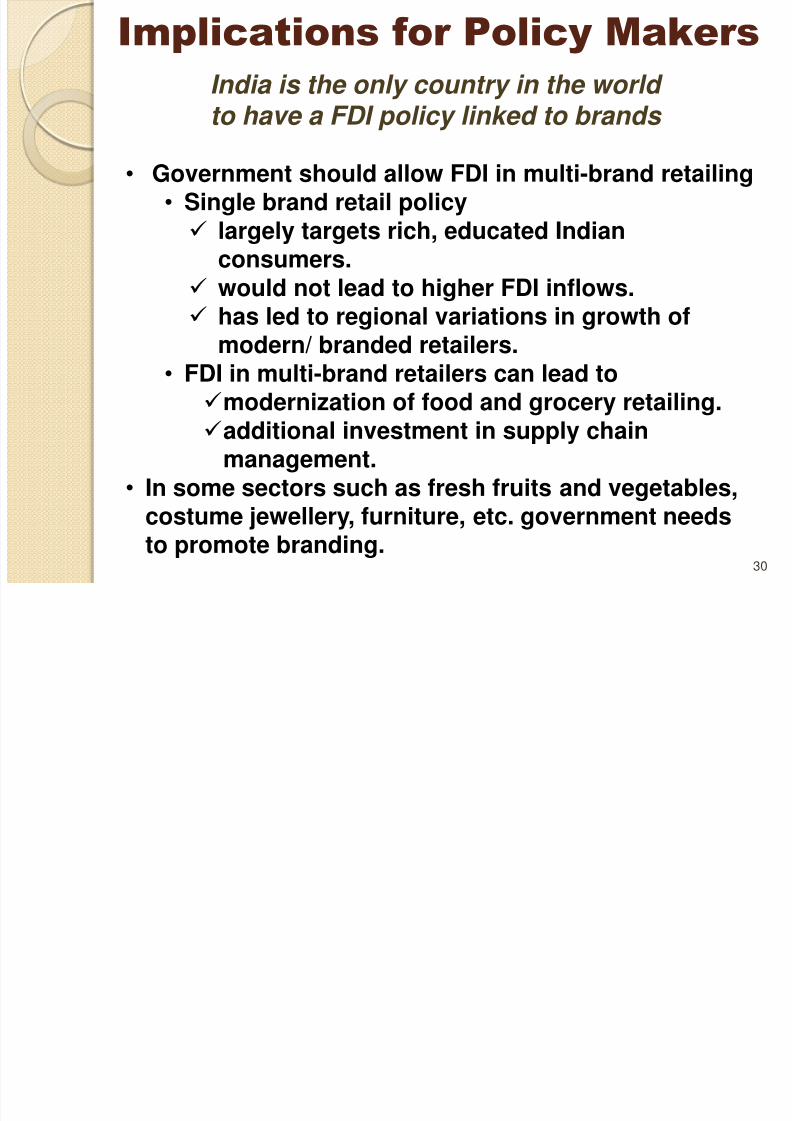

India is the only country in the world to have a FDI policy linked to brands

Implications for Policy Makers

• Government should allow FDI in multi-brand retailing• Single brand retail policy largely targets rich, educated Indian

consumers.

would not lead to higher FDI inflows. has led to regional variations in growth of

modern/ branded retailers.• FDI in multi-brand retailers can lead to

modernization of food and grocery retailing.additional investment in supply chainmanagement.

• In some sectors such as fresh fruits and vegetables,costume jewellery, furniture, etc. government needs

to promote branding. 30

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 31/32

Next Step

• Larger survey of Indian consumers (sample sizearound 1,000 focusing on heterogeneity acrossregions, cities, products, etc.)

• A survey of Indian large and small retailers to

understand how they cater on Indian shopper’sbehavior

• A survey of retail consumers in four Chinese cities(Sample size 200)

• Comparison of Indian and Chinese consumers – brand consciousness, shopping behavior, etc.through primary survey and stakeholder’sconsultation

31

8/3/2019 Indian Consumer Survey -Arpita_final 100702

http://slidepdf.com/reader/full/indian-consumer-survey-arpitafinal-100702 32/32