india · pdf file · 2007-07-22country profile 2006 india this country profile is a...

TRANSCRIPT

Country Profile 2006

India This Country Profile is a reference work, analysing the country's history, politics, infrastructure and economy. It is revised and updated annually. The Economist Intelligence Unit's Country Reports analyse current trends and provide a two-year forecast.

The full publishing schedule for Country Profiles is now available on our website at www.eiu.com/schedule The Economist Intelligence Unit 26 Red Lion Square, London WC1R 4HQ United Kingdom

The Economist Intelligence Unit

The Economist Intelligence Unit is a specialist publisher serving companies establishing and managing operations across national borders. For over 50 years it has been a source of information on business developments, economic and political trends, government regulations and corporate practice worldwide.

The Economist Intelligence Unit delivers its information in four ways: through its digital portfolio, where the latest analysis is updated daily; through printed subscription products ranging from newsletters to annual reference works; through research reports; and by organising seminars and presentations. The firm is a member of The Economist Group.

London The Economist Intelligence Unit 26 Red Lion Square London WC1R 4HQ United Kingdom Tel: (44.20) 7576 8000 Fax: (44.20) 7576 8500 E-mail: [email protected]

New York The Economist Intelligence Unit The Economist Building 111 West 57th Street New York NY 10019, US Tel: (1.212) 554 0600 Fax: (1.212) 586 0248 E-mail: [email protected]

Hong Kong The Economist Intelligence Unit 60/F, Central Plaza 18 Harbour Road Wanchai Hong Kong Tel: (852) 2585 3888 Fax: (852) 2802 7638 E-mail: [email protected]

Website: www.eiu.com

Electronic delivery This publication can be viewed by subscribing online at www.store.eiu.com

Reports are also available in various other electronic formats, such as CD-ROM, Lotus Notes, online databases and as direct feeds to corporate intranets. For further information, please contact your nearest Economist Intelligence Unit office

Copyright © 2006 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication nor any part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author's and the publisher's ability. However, the Economist Intelligence Unit does not accept responsibility for any loss arising from reliance on it.

ISSN 1473-9127

Symbols for tables "n/a" means not available; "–" means not applicable

Printed and distributed by Patersons Dartford, Questor Trade Park, 151 Avery Way, Dartford, Kent DA1 1JS, UK.

DarjilingDarjilingDarjiling

PAKISTAN

AFGHANISTAN

CHINA

MYANMAR

SRILANKA

BANGLADESH

TAJIKISTAN

NEPAL

INDIAINDIAINDIA

ANDHRAANDHRAPRADESHPRADESHANDHRAPRADESH

ANDAMANAND NICOBAR

ISLANDSLAKSHADWEEP

KARNATAKAKARNATAKAKARNATAKA

MAHARASHTRAMAHARASHTRAMAHARASHTRA

GUJARATGUJARATGUJARAT

RAJASTHANRAJASTHANRAJASTHAN

PUNJABPUNJABPUNJAB

MADHYA PRADESHMADHYA PRADESHMADHYA PRADESH

CHHATTISGARHCHHATTISGARHCHHATTISGARH

ORISSA

BIHARBIHARBIHAR

JHARKHANDJHARKHANDJHARKHAND

UTTAR PRADESHUTTAR PRADESHUTTAR PRADESH

RALARALAKERALA

GOA

TAMILTAMILNADUNADUTAMILNADU

NEW DELHINEW DELHINEW DELHI

KoKolkatalkata(Ca(Calcutta)lcutta)Kolkata(Calcutta)

Chennai(Madras)BangaloreBangaloreBangalore

HyderabadHyderabadHyderabad

NagpurNagpurNagpur

BhopalBhopalBhopalIndoreIndoreIndore

AhmadabadAhmadabadAhmadabad

JaipurJaipurJaipur

KanpurKanpurKanpur

Mumbai(Bombay)

SuratSuratSurat

NasikNasikNasik AurangabadAurangabadAurangabad

NandedNandedNanded

AkolaAkolaAkola

PunePunePune

HubliHubliHubli

BelgaumBelgaumBelgaum

Gandhidham

BhavnagarBhavnagarBhavnagar

Rann ofKachchh

Cuttack

Port Blair

Puri

CoimbatoreCoimbatoreCoimbatore

Puduchcheri (Pondicherry)

Nagappattinam

Vizagapatam (Vishakhapatnam)

Cocanada (Kakinada)

MachilipatnamKurnoolKurnoolKurnool

NizamabadNizamabadNizamabad

ChandrapurChandrapurChandrapur

Nellore

Vizianagaram

Brahmapur

MysoreMysoreMysore

SalemSalemSalem

Mangalore

hitradurgahitradurgaChitradurga

VijayawadaVijayawadaVijayawada

KhandwaKhandwaKhandwa

RaichurRaichurRaichur

Kochi (Cochin)

Kollam (Quilon)

Kozhikode(Calicut)

Thiruvananthapuram(Trivandrum) Nagercoil

MaMaMadurai

TuticTuticTuticorin

SolapurSolapurSolapurGulbargaGulbargaGulbarga

purpurKolhapur

Madgaon

SambalpurSambalpurSambalpur

KharagpurKharagpurKharagpur

Agartala

GoalparaGoalparaGoalparaShiliguriShiliguriShiliguri

JamshedpurJamshedpurJamshedpur

BilaspurBilaspurBilaspur

RanchiRanchiRanchi

RaipurRaipurRaipur

JhansiJhansiJhansi

JabalpurJabalpurJabalpur

MurwaraMurwaraMurwara

PatnaPatnaPatna

GayaGayaGaya

GorakhpurGorakhpurGorakhpur

BhagalpurBhagalpurBhagalpurVaranasi Varanasi Varanasi AllahabadAllahabadAllahabad

DhanbadDhanbadDhanbad

Baleshwar

BardBarddhamandhamanBarddhaman

BaharampuraharampurBaharampur

Imphal

Aizawl

KargilSrinagSrinagararSrinagar

JammuJammuJammu

AmritsarAmritsarAmritsar

LudLudhianahianaLudhianaJalandharJalandharJalandhar

AgraAgraAgra

BikanerBikanerBikaner

Jodhpur

UdaipurUdaipurUdaipur

Ajmer

Sikar AligarhAligarhAligarh

KotaKotaKota

GwaliorGwaliorGwaliorEtawahEtawahEtawah LucknowLucknowLucknow

ShahjahanpurShahjahanpurShahjahanpur

Leh

UnderChinesecontrol

ChandigarhChandigarhChandigarhDehra DunDehra DunDehra Dun

SaharanpurSaharanpurSaharanpur

MeerutMeerutMeerutMoraMoraMoradabad

ShillongShillongShillong

GuwahatiGuwahatiGuwahati

DibrugarhDibrugarhDibrugarhNorthNorthNorth Lakhimpur

KoKoKohima

RajkotRajkotRajkot VadodaraVadodaraVadodaraPorbandar

Veraval

BhujBhujBhuj

Bay of Bengal

AndamanIslands

NicobarIslands

IN DIA N OC EA N

LaccadiveIslands

Arabian Sea

Line of Control

Gulf of Kachch h

Gulf ofKhambhat

Gulf ofMannar

Palk Strait

Brahmaputra R.

Brahmaputra R.

Yamuna R.

Yamuna R.

Ghaghara R.

Ghaghara R.

Son R.Son R.

Mahanadi R.

Kris hn a R.Kris hn a R.

Godav ari R.

Narmada R.

Narmada R.

Tapi R.Tapi R.

D e c c a nD e c c a n

Ea

ste

rnE

ast

ern

Gh

ats

We

stern

We

s tern

Gh

ats

Gh

ats

Ganga

R. BHUTAN ItItanagaranagarItanagar

0 km 200 400 600 800

0 miles 200 400

© The Economist Intelligence Unit Limited 2006

August 2006

Main railway

Main road

International boundary

Province boundary

Main airport

Capital

Major town

Other town

ARUNACHAL PRADESH1

1

2

1515

2

33

44

ASSAM2

CHANDIGARH3

DADRA AND NAGAR HAVELI4

DAMAN AND DIU5

5

6

HIMACHAL PRADESH7

JAMMU AND KASHMIR8

MANIPUR9

9

MEGHALAYA10

10

MIZORAM11

11

NAGALAND12

12

PONDICHERRY13

13

13

13

SIKKIM14

14

15

TRIPURA15

17

17

HARYANA

6

7

8

UTTARANCHAL

WEST BENGAL

16

16

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

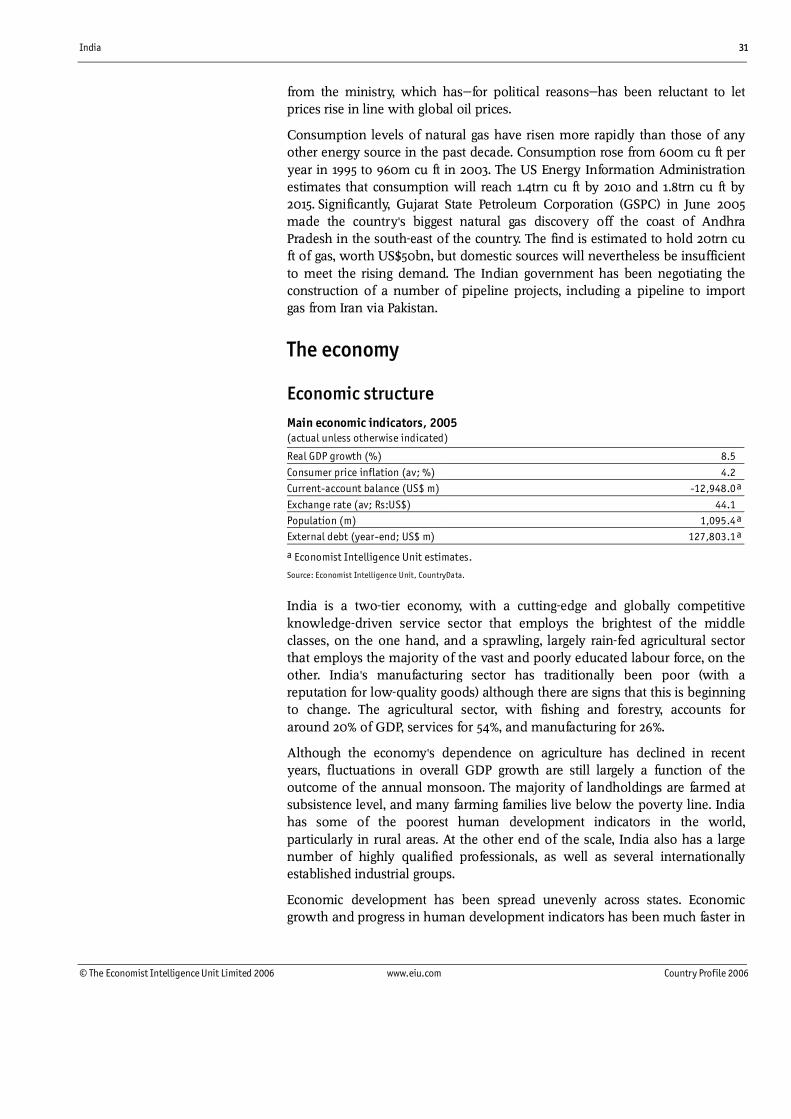

Comparative economic indicators, 2005

Gross domestic product(US$ bn)

Sources: Economist Intelligence Unit estimates; national sources.

0 50 100 150 200 250 300

Afghanistan

Sri Lanka

Vietnam

Bangladesh

Pakistan

Singapore

Indonesia

India

0.0 0.2 0.4 0.6 0.8 1.0 1.2

Afghanistan

Bangladesh

Vietnam

Pakistan

India

Sri Lanka

Indonesia

Singapore

0.0 2.0 4.0 6.0 8.0 10.0 12.0

Singapore

India

Bangladesh

Vietnam

Pakistan

Indonesia

Afghanistan

Sri Lanka

0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0

Bangladesh

Indonesia

Sri Lanka

Singapore

Pakistan

Vietnam

India

Afghanistan

Gross domestic product(% change, year on year)

Sources: Economist Intelligence Unit estimates; national sources.

Consumer prices(% change, year on year)

Sources: Economist Intelligence Unit estimates; national sources.

Gross domestic product per head(US$ '000)

Sources: Economist Intelligence Unit estimates; national sources.

796.5 26.9

India 1

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Contents

India

3 Basic data

4 Politics 4 Political background 5 Recent political developments 9 Constitution, institutions and administration 11 Political forces 15 International relations and defence

22 Resources and infrastructure 22 Population 23 Education 24 Health 25 Natural resources and the environment 26 Transport, communications and the Internet 29 Energy provision

31 The economy 31 Economic structure 33 Economic policy 35 Economic performance 38 Regional trends

38 Economic sectors 38 Agriculture 40 Mining and semi-processing 41 Manufacturing 43 Construction 44 Financial services 45 Other services

46 The external sector 46 Trade in goods 47 Invisibles and the current account 48 Capital flows and foreign debt 49 Foreign reserves and the exchange rate

51 Regional overview 51 Membership of organisations

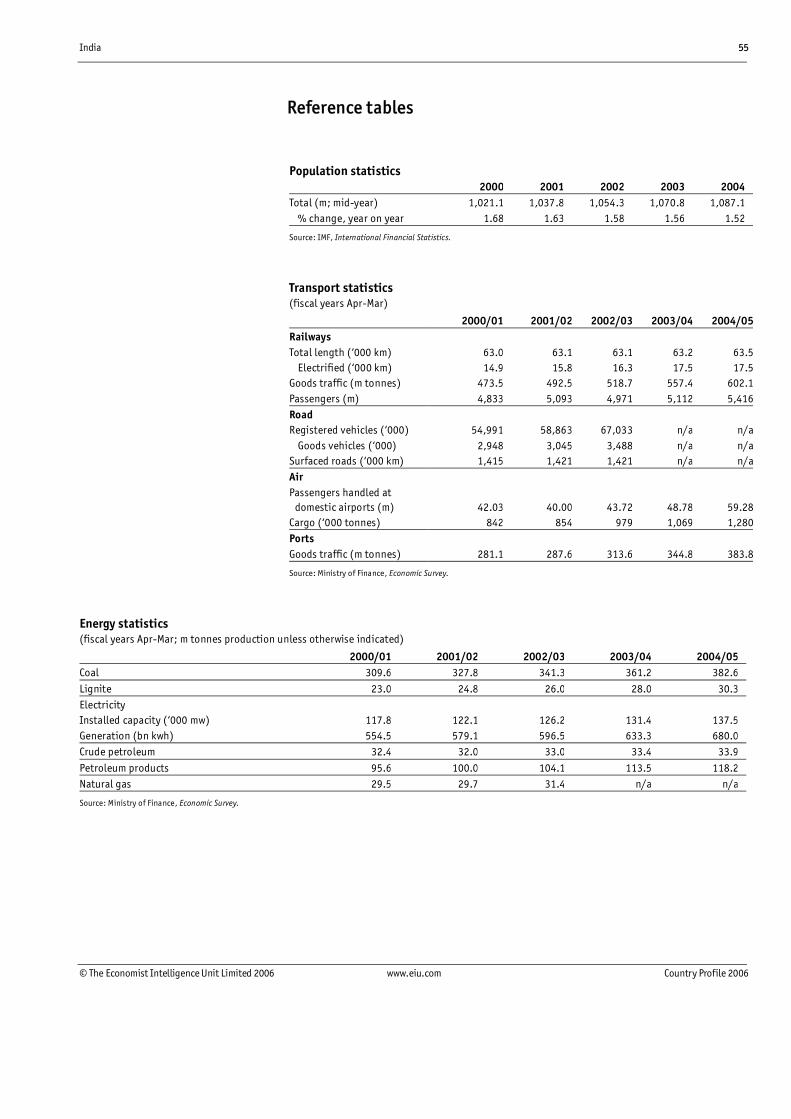

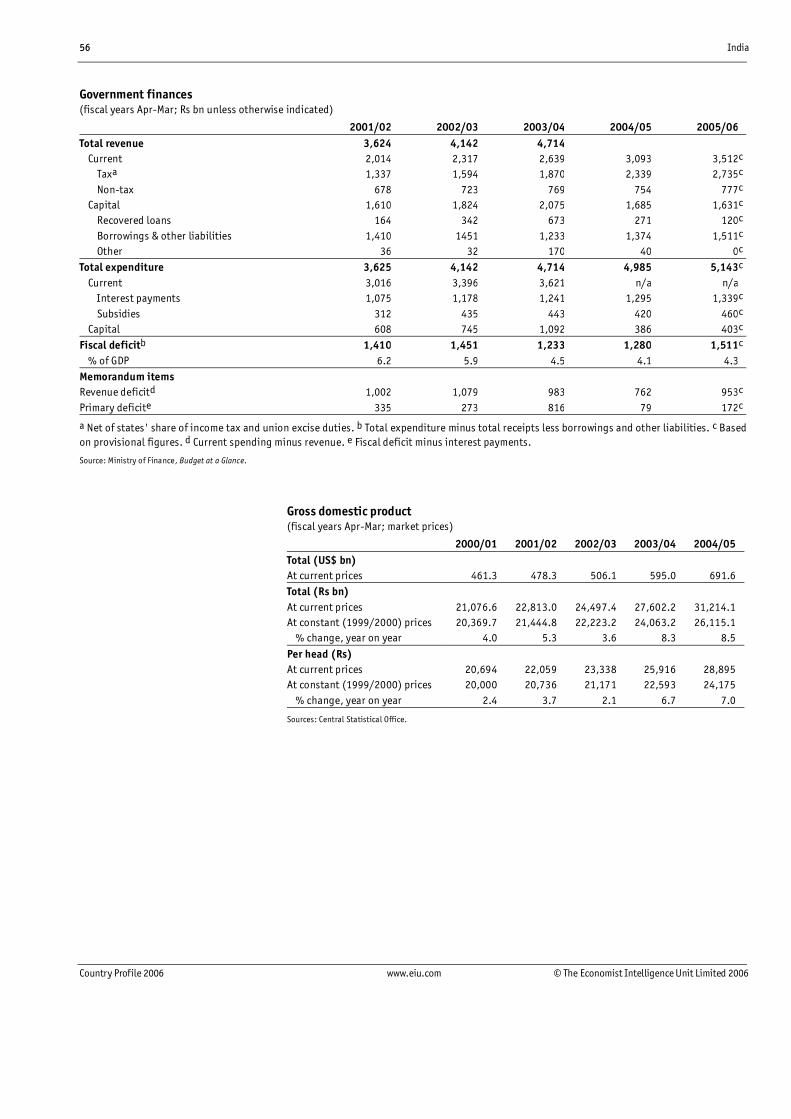

53 Appendices 53 Sources of information 55 Reference tables 55 Population statistics 55 Transport statistics 55 Energy statistics 56 Government finances

2 India

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

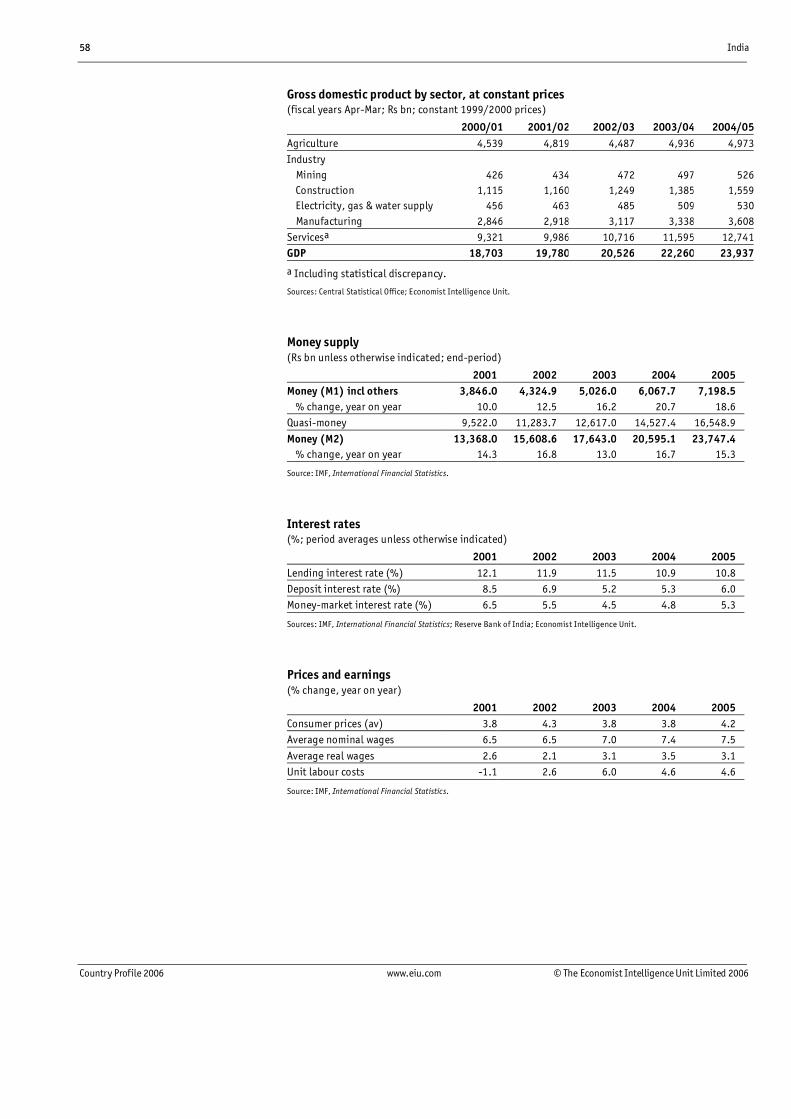

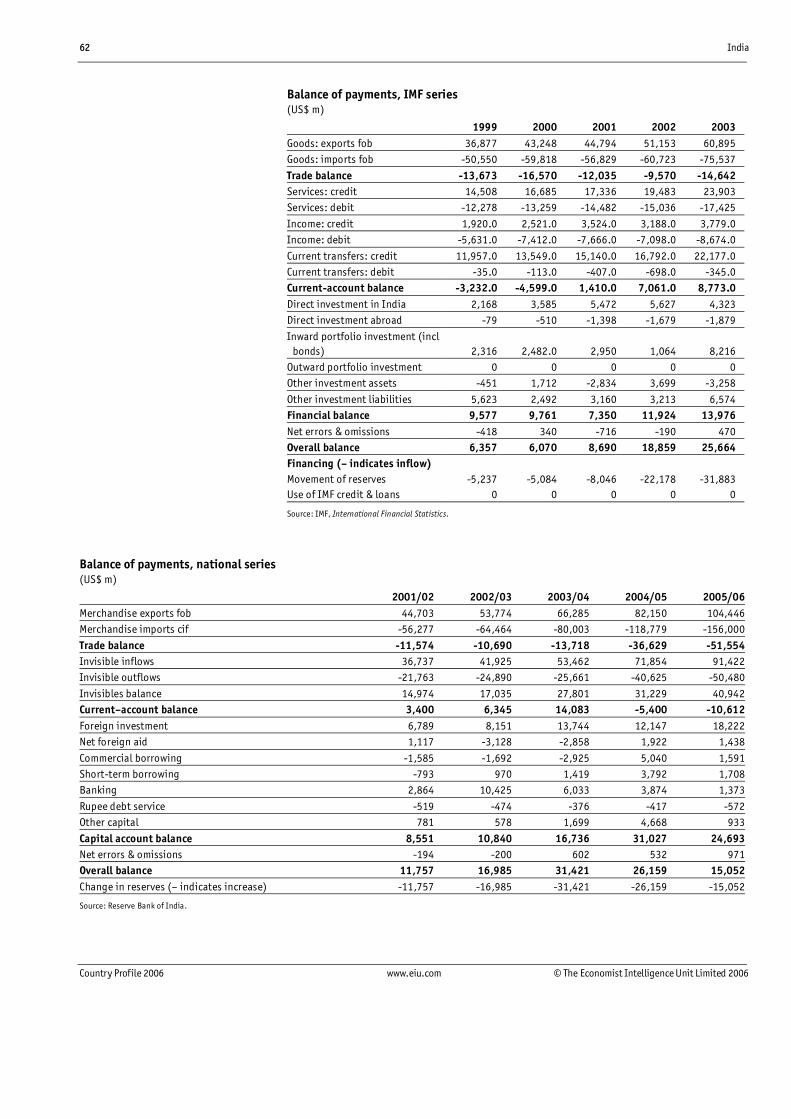

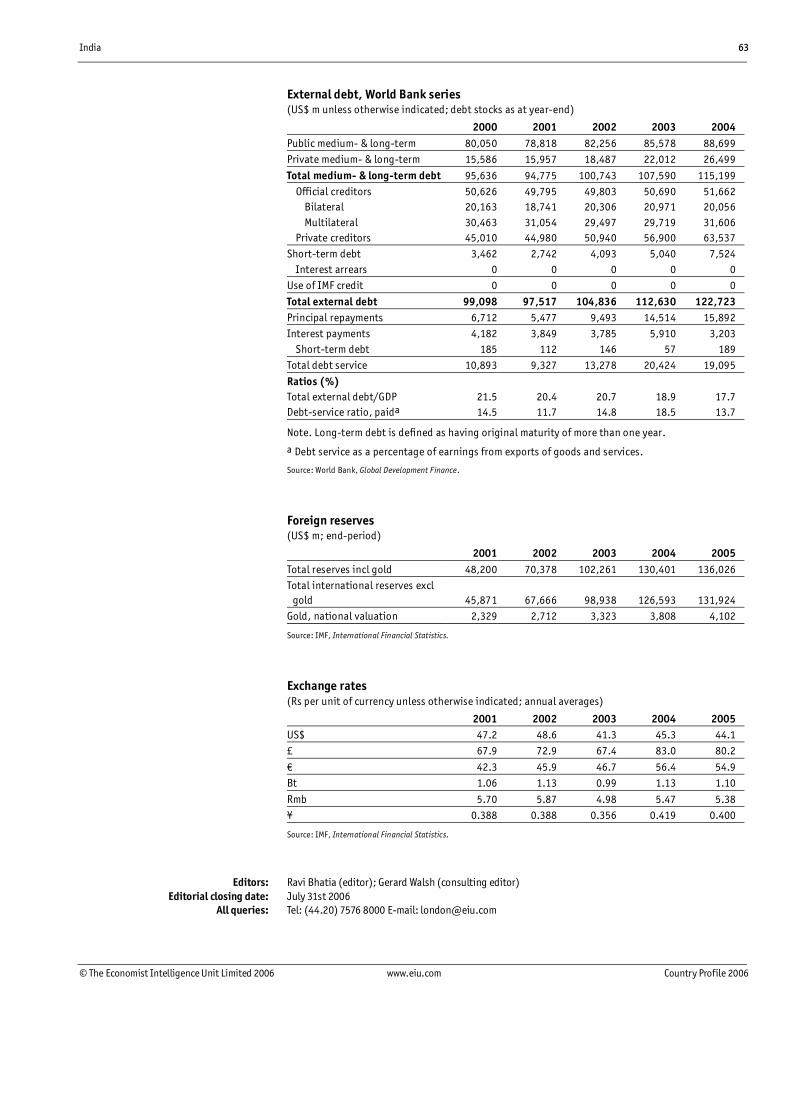

56 Gross domestic product 57 Nominal gross domestic product by expenditure 57 Real gross domestic product by expenditure 58 Gross domestic product by sector, at constant prices 58 Money supply 58 Interest rates 58 Prices and earnings 59 Agricultural production 59 Mineral production 60 Industrial production 60 Gross domestic savings 60 Stockmarket indicators 61 Main composition of trade 61 Main trading partners 62 Balance of payments, IMF series 63 External debt, World Bank series 63 Foreign reserves 63 Exchange rates

India 3

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

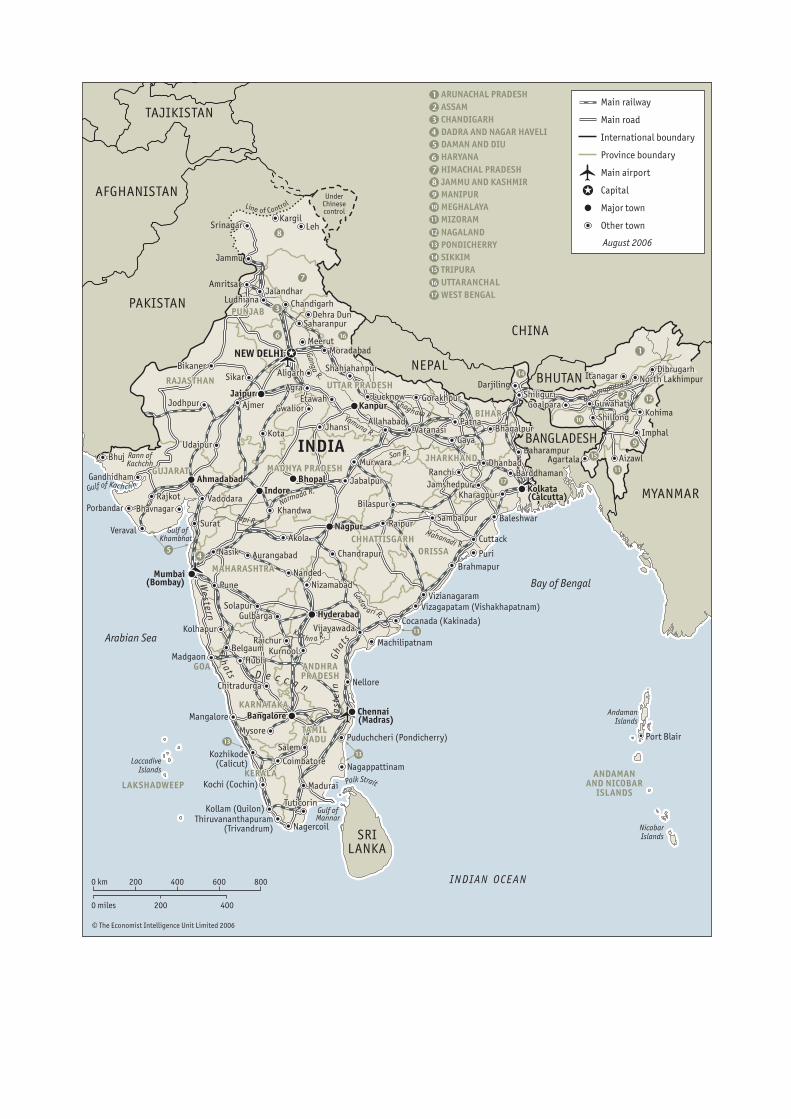

India Basic data

3,287,263 sq km (including Indian-administered Kashmir); 57% is agricultural land and 16% forest area

1.087bn (mid-2004)

Population in millions, 2001 census

Mumbai (Bombay) 16.4 Kolkata (Calcutta) 13.2 Delhi 12.8 Chennai (Madras) 6.4 Bangalore 5.7 Hyderabad 5.5

Varied; humid subtropical in Ganges basin, semi-arid in the north-west, tropical humid in north-east and most of the peninsula, tundra in the Himalayas; all areas receive rain from the south-west monsoon in June-September; the south is also served by the north-east monsoon in January-March

Hottest month, May, 26-41°C (average daily minimum and maximum); coldest month, January, 7-21°C; driest month, November, 4 mm average rainfall; wettest month, July, 180 mm average rainfall

Hindi is the national language and primary tongue of 30% of the population. There are 14 other official languages: Bengali, Telugu, Marathi, Tamil, Urdu, Gujarati, Malayalam, Kannada, Oriya, Punjabi, Assamese, Kashmiri, Sindhi and Sanskrit. English is widespread in business circles and as a second language

Hindu (80.5% in 2001 census); Muslim (13.4%); Christian (2.3%); Sikh (1.9%); Buddhist (0.8%); Jain (0.4%)

Metric system. Numbers are often written in lakhs (100,000) and crores (10m)

Rupee (Rs)=100 paise. Average exchange rate in 2005: Rs44.10:US$1. Exchange rate on July 31st 2006: Rs46.80:US$1

April 1st-March 31st

5 hours 30 minutes ahead of GMT

January 26th; August 15th; October 2nd; also major Hindu, Muslim, Christian and other religious holidays

Land area

Population

Main towns

Climate

Weather in New Delhi (altitude 218 metres)

Languages

Measures

Currency

Fiscal year

Time

Public holidays

Religion

4 India

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Politics

India is a parliamentary federal democracy with an indirectly elected president, currently Abdul Kalam. The prime minister, Manmohan Singh, leads the United Progressive Alliance (UPA), a coalition dominated by the Congress party, which fell short of a majority in the May 2004 general election. The minority UPA government is currently being supported by the Left Front, a group of left-wing parties dominated by the Communist Party of India (Marxist).

Political background

The urban Indus civilisation flourished in west and north-west India around 5,000 years ago. India was a major exporter of textiles and spices and traded with Arabia, Egypt, Rome, south-east Asia and China. Migrants and invaders from central and western Asia have entered India many times since, if not before, Alexander the Great did so in the 4th century BC. As a result India, the world's second-largest country by population and sixth-largest in terms of area, exhibits a great diversity of people, religions and culture.

In 1526 a central Asian warrior, Babur, invaded India and established the Mughal empire. After Vasco Da Gama discovered the sea route to India via the Cape of Good Hope in 1498, a series of European chartered companies—Portuguese, British, Dutch, French and Danish—set up trading posts and colonies in India. The British East India Company eventually dominated, and in 1757 the Mughal emperor granted it the right to administer Bengal. By then the Mughal dynasty was in decline and the Marathas from the west had become the dominant power. After the East India Company defeated the Marathas in 1818, it had no military rival. Following a major Indian revolt in 1857, the East India Company deposed the last Mughal emperor, Bahadur Shah. Within months its charter to trade with India was abrogated by the British government, which annexed the Company's Indian territories, and India became a fully-fledged British colony.

British rule in India ended in 1947 after a sustained campaign for independence, led by the Indian National Congress (Congress). British India was partitioned, amid great bloodshed, to create Muslim-majority Pakistan and the secular state of India. India's first prime minister was the Congress leader, Jawaharlal Nehru. Under his government, India established a complex system of socialist economic controls that remained in place until the 1980s. Congress and its successor—Congress (Indira), or Congress (I), named after Nehru's daughter, Indira Gandhi, who became prime minister in 1966—dominated politics in India until the 1990s. Indira Gandhi's administration continued to implement an inward-looking economic policy and adopted increasingly authoritarian measures. In 1975 she declared a state of emergency that lasted for two years. Civil rights were suspended, the press was controlled, many of her critics were imprisoned and her son, Sanjay, began an unpopular mass-sterilisation programme to stem population growth. In the 1977 general election voters rejected Mrs Gandhi. Her party was defeated and she lost her seat.

Early history

Independence and dominance of Congress

India 5

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Having returned as prime minister in 1980, Mrs Gandhi tacitly supported a violent movement against the Akali Dal, the ruling Sikh party in Punjab. However, the violence became uncontrollable and she finally ordered the army to storm the Golden Temple, the prime Sikh shrine in Amritsar, and kill the terrorists' leader. In retaliation, in 1984 she was assassinated by her Sikh bodyguards, and her elder son, Rajiv Gandhi, succeeded her as prime minister. In a sympathy vote he won an unprecedented majority in an election later that year, and his administration began to take cautious steps towards economic liberalisation. However, Congress lost its majority in the 1989 general election amid a series of corruption scandals, and Mr Gandhi stepped down. He was assassinated by a Sri Lankan Tamil extremist during the 1991 election campaign.

Following the 1991 general election Congress formed a minority government under Narasimha Rao, which initiated a series of economic reforms that set India on a path of stronger economic growth. The May 1996 election returned another hung parliament. The Hindu-nationalist Bharatiya Janata Party (BJP) formed a government that lasted just 13 days; this was followed by a left-leaning United Front (UF) coalition, which was supported from the backbenches by Congress. The UF government continued to implement the economic reforms begun under Congress, but when Congress withdrew its support in November 1997, the government fell. A general election held in February-March 1998 produced yet another hung parliament. The BJP finally formed a governing coalition, the National Democratic Alliance (NDA), with 22 other parties under the leadership of Atal Behari Vajpayee, a moderate.

In April 1999 the NDA government collapsed after narrowly losing a vote of confidence. It remained as a caretaker administration for six months before re-establishing itself in power following a general election held in September-October 1999. The alliance of more than 20 parties included a number of smaller regional and caste-base parties, which exercised disproportionate influence in government, often holding the administration to ransom to gain concessions in their home states. Coalition governance has become a continuing feature of Indian politics at the federal level, and increasingly also at the state level, since 1996. On both levels it seems that coalition governments have found it hard to push through policies, particularly those requiring legislative action.

Recent political developments

The BJP government in 1998 gave the go-ahead for the testing of nuclear bombs—a reflection of the party's determination to raise India's profile as an aspiring world power—even at the cost of economic sanctions. Economically, the BJP remained pragmatic during its time in government and pursued reformist policies. Politically, the BJP had to abandon some of the party's policy cornerstones, including the building a Hindu temple on the site of the Ayodhya mosque and abolishing India's separate civil code for India's Muslims to get the support of secular parties. Mr Vajpayee's popularity and integrity did much to move the party towards the political mainstream and put pragmatism over ideology. Consistent with this attempt to reinvent the essentially still

The age of coalition politics

The BJP leads a coalition government from 1998 to 2004

6 India

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Hindu-nationalist party, the BJP government toned down its hardline Hindu-nationalist rhetoric in a bid to appeal to more mainstream voters as the 2004 general election approached. It presented itself both as a party that delivered economic prosperity and as a steward of a strong India with a presence on the global stage. The BJP promoted its "India is Shining" campaign, which aimed to capitalise on a buoyant economy—partly the result of its economic reforms, but also of good fortune. In contrast, the opposition Congress party presented itself as the defender of India's inclusive, secular heritage. It tried to appeal to voters across castes and religions, as well as to the poor, who had not seen the fruits of economic reform.

Composition of the Lok Sabhaa, Jun 2004 United Progressive Alliance (governing coalition) 222 Indian National Congress 145 Rashtriya Janata Dal 24 Dravida Munnetra Kazhagam 16 Nationalist Congress Party 9 Pattali Makkal Katchi 6 Telangana Rashtra Samithi 5 Jharkhand Mukti Morcha 5 Marumalarchi DMK 4 Lok Jan Shakti Party 4 Others 4

Left Front (supporting the governing coalition) 59 Communist Party (Marxist) 43 Communist Party of India 10 Others 6National Democratic Alliance (opposition) 186 Bharatiya Janata Party (BJP) 138 Shiv Sena 12 Biju Janata Dal 11 Shiromani Akali Dal 8 Janata Dal (United) 8 Telugu Desam Party 5 All India Trinamool Congress 2 Nagaland People's Front 1 Mizo National Front 1

Other parties 76 Samajwadi Party 36 Bahujan Samaj Party 19 Other parties 13 Independents 8Totalb 545

a The lower house of parliament. b Including two representatives of Anglo-Indians appointed by thepresident.

The "India is Shining" campaign backfired, with poor rural voters denied any new-found prosperity, and in a surprise victory a Congress-led coalition, the UPA, was narrowly elected to power in the May 2004 general election—the Congress party (on its own) won only eight seats more than the BJP. However, the UPA fell short of a majority and is being supported in parliament by the Left Front group of communist parties, although these parties have chosen not to join the government and are supporting it "from outside". The minority

Congress returns to power

India 7

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

government is led by Manmohan Singh, who was sworn in as prime minister following the refusal of the Congress leader, Sonia Gandhi, to take up the post. Mrs Gandhi remains the Congress party president and is the Congress leader in parliament. Mr Singh, who has held many important positions in the economic and civil service hierarchy in India, is a respected economist and a pragmatist and is highly regarded across the political spectrum. In his two first years in government he has managed to hold together an unwieldy coalition and has pursued a gradualist economic reform agenda. On the foreign policy front, Mr Singh, a Sikh born in the Pakistani portion of Punjab province, has continued a policy of rapprochement with Pakistan and has pushed India's bid for a permanent seat on the reformed UN Security Council. A nuclear deal with the US (which has still to be formally approved by the US Congress) has changed US-Indo relations and is likely to make India a vital US military and economic ally in coming years.

The opposition BJP has been plagued by internal tensions and in-fighting since it fell from power and is therefore unlikely to pose a substantial threat to the UPA government. A major Islamic terrorist attack or sectarian violence could, however, galvanise its traditional Hindu constituency. At the end of 2005 Lal Krishna Advani was forced to step down as party president, following ideological differences that upset the Rashtriya Swayamsevak Sangh (RSS), the party's powerful parent organisation. Under a new president, Rajnath Singh, seen by many as an interim leader, the debate over the party's ideology has continued. The outcome of what could be a long-drawn-out leadership struggle will determine whether the BJP will go back to its traditional values of Hindu nationalism, or whether it will evolve into a more moderate force in Indian politics.

The government faces no immediate threat to its survival and looks on course to last a full five-year term until 2009. However, it is severely hobbled in its ability to formulate and implement policy. Politics remains centred more on tensions within the UPA coalition and between the UPA and its notional allies, than on competition from the BJP. The main tension is between the reformist economic liberalism of several leading Congress figures, notably Mr Singh and the finance minister, Palaniappan Chidambaram, and the leftist populism of many government supporters. These include members of Congress and of its coalition partners, and in particular the communist parties, which are not in the UPA, but which lend parliamentary support to the UPA. Curiously, the largest of these, the Communist Party of India (Marxist), or CPI (M), has come to resemble the official opposition. Its strategy appears to be to use the leverage it now enjoys to expand its influence beyond those states where it is a major force—West Bengal, Tripura and Kerala—to the rest of India. To do this, it is relying on its supporters in the trade unions. This means that it has tried to block any reform seen as damaging the interests of the workforce in the "organised" sector—a definition covering workplaces with more than ten employees. There are about 30m such workers out of a total labour force of more than 400m. They have become disproportionately powerful.

The BJP has been in disarray

The Left has come to resemble the official opposition

8 India

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Important recent events

April 2003

The prime minister, Atal Behari Vajpayee, initiates moves to defuse tensions with Pakistan, re-establishing communication and diplomatic links.

June 2003

India and China reach de facto agreement over the status of Tibet and also of Sikkim—a state whose accession to India in 1975 China still refuses to recognise officially—in a crossborder trade agreement.

November 2003

India matches Pakistan's offer of a ceasefire along the Line of Control in Kashmir. Pakistan's unilateral offer followed measures announced unexpectedly by the Indian government in October to improve ties with its neighbour.

December 2003

India and Pakistan agree to resume direct air links and to allow overflights. India had suspended air links after the December 2001 attack on the Indian parliament, which it blamed on Pakistani terrorists.

January 2004

A groundbreaking meeting is held between the Indian government and moderate Kashmiri separatists, marking a new chapter in the 14-year stand-off between the Indian government and the separatists.

February 2004

Formal peace talks over the disputed region of Kashmir are held in the Pakistani capital, Islamabad.

May 2004

A general election brings the Congress-led United Progressive Alliance (UPA) to power. Sonia Gandhi, the Congress leader, refuses to become prime minister. The post goes to Manmohan Singh, a former finance minister and reformer.

December 2004

Thousands die in the Asian tsunami; the Andaman and Nicobar Islands are devastated.

April 2005

A bus service between Srinagar, in Indian-controlled Kashmir, and Muzaffarabad, in Pakistani-controlled Kashmir, comes into operation.

July 2005

Islamist militants attack a holy site in Ayodhya—the flash-point of Hindu-Muslim strife in 1992—raising concerns over possible renewed inter-community violence in India and a stalling of improving relations between India and Pakistan.

October 2005

A devastating earthquake, with its epicentre in Pakistani-administered Kashmir, kills more than 1,000 people in Indian-administered Kashmir. Tens of thousands die in neighbouring Pakistan.

India 9

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

October 2005

Three bombs in a crowded marketplaces in Delhi kill 62 people and injure over 200. A little-known Kashmiri group claims responsibility for the attack.

February 2006

India's larges ever rural jobs scheme is launched with the aim of lifting around 60m families out of poverty.

March 2006

India and the US sign a landmark nuclear deal, which gives India access to civilian nuclear technology, while India agrees to greater scrutiny of its civilian nuclear programme.

May 2006

Congress performs poorly in four important state elections in Assam, Kerala, Tamil Nadu and West Bengal. The communists, on whose support the UPA relies, win convincingly in West Bengal and Kerala.

July 2006

Several bombs target Mumbai's commuter train system, killing over 200 people. Pakistan's president condemns the attack, and the Indo-Pakistani peace process continues.

Constitution, institutions and administration

The Republic of India is a constitutional federal democracy made up of 28 states and seven union territories. The Indian constitution defines the division of most powers between the centre and the states, although the centre takes precedence in relation to residual powers. Representation in parliament has been frozen on the basis of the results of the 1971 census. Given that population growth is much higher in the northern states, the relative value of votes cast in the north in terms of political representation has fallen. The National Population Council has recommended an extension of the "freeze" on representation until 2026. This is likely to become a source of major tension between the country's northern and southern states. India's federal structure often leads to demands for further devolution of powers to the states, as well as demands for new states to be created. In 2000 three new states—Chhattisgarh, Jharkhand and Uttaranchal (all three northern states with strong tribal representations)—were formed from Madhya Pradesh, Bihar and Uttar Pradesh respectively.

The Indian constitution provides for an independent judiciary, with high courts in every state and a Supreme Court in New Delhi. There are two houses of parliament. The lower house, or Lok Sabha (house of the people), is elected every five years by universal adult suffrage. The prime minister is elected by the Lok Sabha. Members of the upper house, or Rajya Sabha (house of the states), are elected by their respective state legislatures, according to state quotas based on population. The president is elected every five years by both houses of parliament and the state legislatures. He is confined to acting on the advice of the Council of Ministers, which is chosen by the prime minister.

Federalism

The judiciary and the legislature

10 India

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

India is the world's most populous democracy and has held regular and largely free elections since 1947. For members of parliament, the chances of re-election to the Lok Sabha are low (as anti-incumbency is a key trend in Indian politics), tending to increase the incentives for politicians to maximise their personal gains rather than working for the welfare of their electorate. The Election Commission of India (ECI) has wide powers to requisition the government machinery for elections and has ensured fairly orderly elections; in 2003 it won the right to make candidates disclose criminal records. However, there are occasional cases of poll rigging and intimidation; spending limits on candidates are poorly enforced and candidates with criminal records are sometimes elected, particularly to the state assemblies. Generally, a high level of political awareness and the sheer size of the electorate nevertheless ensure that the final results reflect the wishes of the people, and the ousting of incumbent administrations has become increasingly frequent.

Congress, which led the agitation for independence, emerged as the dominant party thereafter and won elections in most states in the 1950s and 1960s, although the communists and Tamil separatists occasionally won state-level elections. The situation changed following the 1975-77 state of emergency. Caste and regional splinters from the opposition alliance that won the 1977 election were increasingly successful in state elections. In the current political landscape, none of the three national parties—Congress, the BJP and the CPI (M)—can hope to win a majority in the central government on its own, and each needs to ally itself with regional or caste-based parties.

India's 28 states vary enormously in size, population and natural resources. The centre's powers to tax income, production and foreign trade give it far greater access to revenue, a large part of which is shared out among the states by the planning commission and by finance commissions that are appointed every five years. The states cannot borrow without the centre's permission. However, as the central government has become increasingly reliant on the support of regional allies, it has found it harder to refuse the states' demands to manage their own finances. The deficits of both the centre and the states are largely financed by banks and financial institutions, which channel public savings to the governments. This pre-emption of bank funds to finance excess consumption by the government—amounting to about 10% of GDP per year—has become a drag on economic growth.

As central controls on industry, finance and foreign trade have been relaxed since the early 1990s, industry has received the freedom to relocate, but has faced greater competition. These competitive pressures have been passed on to the states, which have tried to attract and retain industry. In this competition, the advanced western and southern states have been more successful: as foreign trade has become freer, industry has moved closer to Gujarat, Maharashtra, Karnataka and Tamil Nadu. In an effort to cut costs, producers have also moved closer to suppliers and markets. This has led to a prolonged slump in long-distance road transport, from which it is now slowly emerging.

Democracy and corruption

The centre versus the states

India 11

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Political forces

Congress led the campaign for independence and has remained a powerful force in Indian politics, transcending religious, ethnic and caste divisions. However, it is also a party tightly focused on its heritage: members of the Nehru-Gandhi family have led the party throughout most of its history. India's first prime minister, Jawaharlal Nehru, was succeeded by Lal Bahadur Shastri, who died within a year of taking office. The party then turned to Nehru's daughter, Indira Gandhi, who remained leader until her assassination in 1984, after which her son Rajiv took over as party leader. He was assassinated in 1991, and Congress is now led by his widow, Sonia. The decline of Congress began when Indira Gandhi declared a state of emergency. Her opponents combined to form the Janata Party, which won the 1977 election. In 1980 Mrs Gandhi brought down the Janata government and returned to power. Rajiv Ghandi came to power in 1984 with the largest majority ever and the aim of liberalising and modernising government, but he was soon mired in a corruption scandal and lost the 1989 election. He managed to split and finally bring down the Janata Dal government that followed him, but he was killed before the 1991 general election. Although falling just short of a majority, Congress formed a government, and after the election carried out considerable economic liberalisation in an attempt to solve the country's balance-of-payments crisis. That did not, however, save it from defeat in the 1996 election.

As repeated efforts to form a national alternative failed, the electorate turned to regional and caste-based parties. Following Congress's poor performance in the 1998 general election, Rajiv Gandhi's Italian-born widow, Sonia, gave in to repeated requests and took over as party leader. However, her foreign birth has prompted criticism in parts of Congress as well as from the BJP. Following Congress's surprise victory in the 2004 general election, Mrs Gandhi declined to take up the post of prime minister, instead nominating Manmohan Singh. But Mrs Gandhi remained the leader of Congress, and until March 2006 chair of the National Advisory Council—a post she had to relinquish on technical grounds, which also led to her resignation as member of parliament in early 2006. However, in May 2006 she was re-elected with a landslide victory in the Nehru-Gandhi stronghold constituency of Rae Bareilly in Uttar Pradesh. Most commentators believe that the centre of power within the government lies with Mrs Gandhi rather than Mr Singh.

The stability of the current Congress-led minority government depends crucially on how readily the Left Front parties withdraw their support in case of disagreement over policy. They boycotted the co-ordination committee, in which the Left Parties agree policy with the UPA, for four months in 2005 and eventually got their way, scuppering the economic reforms the government sought to implement. The Left Front has an effective veto over any reform that requires a vote in parliament. Following the Communist parties' landslide wins in state elections in West Bengal and Kerala in the first half of 2006, they are likely to become more assertive at the national level. Congress will probably be forced to consult the Left Front more than it has in the past. The Left Front has already stymied several important reforms, notably labour market reform and privatisation. Given that it has three years of its five-year term still to run, the

The Congress party

12 India

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

government will need to tread a fine line between its reform ambitions and policy compromises with its political allies. While the government will try to distribute the benefits of economic growth more widely, its overriding objective will be to ensure the continuation of India's economic boom.

Equally important, however, are divisions within Congress that could result in government instability. Loyalties in the Council of Ministers are likely to be split between Mr Singh and Mrs Gandhi. Mrs Gandhi will have to reconcile the demands of individual members of the government as well as interest groups within the diverse Congress party to secure a stable government. Congress's success in the 2004 general election is evidence that the dynastic claim still exerts considerable force, particularly in rural areas. Congress profited from the excitement created by the candidacy of Rahul Gandhi, Mrs Gandhi's son, and her charismatic daughter, Priyanka. Rahul Gandhi is widely believed to be a likely future candidate to lead the party.

The Bharatiya Janata Party (BJP) traces its roots back to the Bharatiya Jan Sangh, a party representing traditional Hindu values and the interests of small businesses, traders and the middle class. It is the political wing of a group of interconnected cultural and religious movements—the Sangh Parivar—of which the most politically significant is the Rashtriya Swayamsevak Sangh (RSS), a disciplined cadre organisation that counts the president of the BJP, Rajnath Singh, and the party's senior leaders, Lal Krishna Advani and Atal Behari Vajpayee, among its former members. A member of the RSS assassinated Mahatma Gandhi, and the group is seen by its critics as sinister and anti-Muslim.

The BJP emerged as a significant force in the 1989 general election, winning 88 seats. A central campaign issue was the demand that a Hindu temple be constructed on the site of the Babri mosque in Ayodhya in Uttar Pradesh—which many Hindus believe was built upon the site of a temple marking the birthplace of the Hindu god-king Ram. In the 1991 election the BJP established itself as the main national opposition and won power in four states. In December 1992 Sangh Parivar activists demolished the Babri mosque, triggering communal riots that left thousands dead. In the 1993 state elections the BJP suffered setbacks and won control of just one state, but in the 1996 general election it won 160 seats in the Lok Sabha.

In May 1996 the BJP formed its first national government, led by Mr Vajpayee, which lasted just 13 days. The BJP re-emerged as the power broker in 1998, when it won 182 seats in the general election and cobbled together a coalition of 13 parties under Mr Vajpayee's leadership. The coalition proved unwieldy, collapsing in April 1999. However, Mr Vajpayee proved himself able to rally parties of disparate political persuasions to form a government. Another election in September-October 1999 returned a BJP-led coalition of 20 partners to power. Members of the new coalition, the National Democratic Alliance, campaigned under a common platform and won 302 seats. Despite the increased majority, however, the range of parties involved in government left the alliance vulnerable to the whims of smaller regional parties.

The BJP

India 13

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Mr Vajpayee sought to rein in the party's more extreme Hindu-nationalist members, particularly in relation to questions of economic reform. But the party's reformist credentials proved increasingly shaky in the face of conflicting demands from coalition members and resistance from the BJP's nationalist wing. The close relations the party cultivated with leading industrialists also resulted in increased protection for some industries from foreign competition. On the foreign policy front, Mr Vajpayee sought improved relations with neighbouring Pakistan and paved the way for further confidence-building measures implemented by the UPA government, including the partial with-drawal of Indian troops from Kashmir in November 2004 and the establish-ment of a crossborder bus link in April 2005.

Since the electoral defeat in May 2004, the BJP has been in disarray. Following a further electoral defeat in October of that year in the politically important state of Maharashtra, the party appointed Lal Krishna Advani, one of the founders of the BJP and previously Mr Vajpayee's right-hand man, as party president. The BJP's identity crisis worsened in June 2005, when Mr Advani offered to stand down as party president after an official visit to Pakistan, during which he described Pakistan's founder, Mohammed Ali Jinnah, as a "secular" leader. The comments, possibly made by Mr Advani in an attempt to shed his image as a hardliner and to move the party more towards the mainstream, divided the BJP down the middle and outraged Hindu-nationalist organisations close to the BJP—one of the cardinal tenets of modern Indian history is that Mr Jinnah was the non-secular architect of the two-nation theory (an India for Hindus and a Pakistan for Muslims).

Eventually, a considerably weakened Mr Advani was forced to resign at the end of 2005. His successor is the less controversial Rajnath Singh, who is seen as a skilful grass-roots organiser and effective administrator, but his appointment has only temporarily suspended a divisive succession battle. Few of the younger generation of BJP leaders, such as Arun Jaitley, have the mass base enjoyed by Mr Advani or Mr Vajpayee. An exception on the Hindu right is the chief minister of Gujarat, Narendra Modi, who commands grass-roots support in right-wing Gujarat, but few see him as a potential national election-winner (as he remains too far on the right). The outcome of the struggle is likely to determine whether the BJP will go back to its traditional values of Hindu nationalism or evolve into a more moderate force in Indian politics.

The Communist Party of India (CPI) emerged from Congress, splitting from the Indian National Congress during the second world war. The CPI itself later split to form a Marxist group, the Communist Party of India (Marxist) or CPI (M). The CPI (M) is strongest in West Bengal, where it has been in power for 26 years, and it has frequently held power in Kerala and Tripura. Although the "third force" includes several powerful regional parties that are increasingly important in a fractured political scene, these parties have no strong ideological commitment to a common agenda. Instead, they are motivated by state or caste interests that can often be better served through alliances with the BJP or Congress. More recently, the Left Front group of communist parties decided not to join the Congress-led UPA government formally, but to support it from "the outside". The communists strongly oppose the deregulation of the labour

The communist parties

14 India

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

market and privatisation, but have at times been more pragmatic on other policy issues, such as foreign investment.

Main political figures

Manmohan Singh

Prime minister. Mr Singh has held many important positions in the economic and civil service hierarchy, including governor of the Reserve Bank of India (the central bank) and deputy chairman of the Planning Commission. An Oxford-educated economist, Mr Singh is widely respected across political parties and has a reputation of being a pragmatist. However, his critics argue that he is a weak political figure governing at the request of Sonia Gandhi. Throughout his political life he has been an appointee—he has never won a seat in India's lower house of parliament, the Lok Sabha.

Sonia Gandhi

Indian National Congress party leader in parliament, and Congress party president. Mrs Gandhi is the Italian-born widow of a former prime minister, Rajiv Gandhi. She led Congress to success in the 2004 general election but declined the offered post of prime minister. This move enhanced her moral stature in a culture with a long history of renunciation. In March 2006 Mrs Gandhi resigned as member of parliament and chair of the National Advisory Council, an "office of profit" she was not supposed to hold under Indian law to avoid a conflict of interests. She was re-elected with an overwhelming majority from her constituency Rae Bareilly in Uttar Pradesh in May 2006.

Rahul and Priyanka Gandhi

Mrs Gandhi's children and heirs to the Nehru-Gandhi dynasty. In the 2004 election campaign Rahul and his sister Priyanka emerged as the Congress's star campaigners, galvanising the campaign by their youth and emphasising the fact that the century-old Gandhi-Nehru dynasty remains India's most powerful and charismatic political family. Rahul was elected to the lower house of parliament for the first time and is being groomed as the next leader of the Congress party.

Palaniappan Chidambaram

Finance minister. Mr Chidambaram is a suave, articulate politician from the southern Indian state of Tamil Nadu. He is well-known for his pro-market reforms, particularly tax reform and budgetary discipline, during his tenure as finance minister in 1996-98. A Harvard-educated lawyer and a strong supporter of the World Trade Organisation, Mr Chidambaram is popular in business circles.

Arjun Singh

The minister for human resources and development. His plans in early 2006 to increase the number of reserved places for backward castes in higher education are highly controversial and have put him at loggerheads with the prime minister, whose job he believes should be his.

Shivraj Patil

A respected and experienced politician, he held several ministries under the Congress governments of Indira and Rajiv Gandhi. His appointment as interior minister came as surprise because he had lost his seat in the May 2004 general election.

Pranab Mukherjee

Defence minister. A prominent Gandhi family loyalist, Mr Mukherjee held at least half a dozen important ministries in past Congress governments, including finance and external affairs. He has close links with the left.

Laloo Prasad Yadav

Railway minister. Informally rules the most lawless state of Bihar by proxy. He formed the Rashtriya Janata Dal (RJD) in 1997, after breaking away from the Janata Dal party. His party is a key ally of Congress in the United Progressive Alliance (UPA) government.

India 15

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Rajnath Singh

President of the opposition Bharatiya Janata Dal (BJP) since the start of 2006. Mr Singh held various important posts in his political career, including chief minister of Uttar Pradesh and minister of agriculture in the Vajpayee government. He is an effective administrator and grassroots organiser, but has the reputation of being uncharismatic.

Lal Krishna Advani

A senior figure in the Bharatiya Janata Dal (BJP) party. Mr Advani is credited with making the BJP a major political force since 1984, when it held only two parliamentary seats. He resigned as party president in December 2005, but remains the leader of the opposition in the Lok Sabha. Despite his age (77) Mr Advani has not ruled out running for the post of prime minister in 2009.

Atal Behari Vajpayee

Former prime minister and former foreign minister (in a left-right anti-Indira Gandhi coalition in the late 1970s), Mr Vajpayee has had a distinguished parliamentary career. Following the BJP's defeat in the May 2004 general election he became the party's chairman, a newly created and largely symbolic position, and has been acting as an elder statesman guiding the party.

Abdul Kalam

President of India. A former scientist and founding father of India's nuclear-missile programme. A Muslim, Mr Kalam, who is widely respected, was elected president by an overwhelming majority in July 2002.

Somnath Chatterjee

Speaker of the Lok Sabha. A veteran Marxist leader, Mr Chatterjee is the first communist leader to occupy this position. A member of parliament for the tenth time, Mr Chatterjee has established a rapport with politicians across party lines.

Mulayam Singh Yadav

Chief minister of Uttar Pradesh, India's most populous state. Leader of the Uttar Pradesh-based Samajwadi Party and former defence minister in the United Front (UF) coalition. Important among the new breed of "backward caste" politicians.

International relations and defence

India became independent in 1947 at the start of the cold war. Mr Nehru had visited the Soviet Union in the 1930s and felt that it provided the best economic model for India's development. Consequently, India did not join the Western alliance, and instead followed a policy of neutrality between the two blocs. Pakistan, meanwhile, joined the US-led South-East Asian Treaty Organisation. India's defeat by China in a short war in 1962 brought the US and India briefly closer, but as Indian relations with Pakistan deteriorated, US sympathy for India waned. In 1971, when Hindu refugees from East Pakistan flooded into India, India decided to attack Pakistan, and to ward off the US, entered into a treaty with the Soviet Union. The treaty provided India with low-cost security for the next 18 years.

Since the collapse of the Soviet Union India has built closer relations with the US and the West. Its liberal reforms in the early 1990s also made it more receptive to foreign trade and investment and led Western countries to take a greater interest in India. The 1998 nuclear tests caused a glitch in the process, but it has continued nevertheless. Indian-US relations entered a new era in 2005, when the two countries agreed to deepen their co-operation in the area of defence, including joint weapons production, greater technology sharing, and increased trade in arms. In March 2006 the US president, George W Bush,

Independence and its aftermath

16 India

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

visited India and signed a landmark deal that welcomed India into the club of states that the US permits to possess nuclear weapons. The deal changes the world's nuclear order by amending the Nuclear Non-Proliferation Treaty (NPT), but it will first require the approval of the US Congress. Under the agreement the US offers India "full civil nuclear energy co-operation and trade", thereby ending sanctions in place against India since its refusal to sign the NPT. (Since 1968 it has been a tenet of US foreign policy that only countries that sign the NPT are permitted access to US nuclear technology.) However, Mr Bush side-stepped the issue of backing India's bid for permanent membership on the UN Security Council by arguing that the UN first needed a series of "administrative" reforms. Meanwhile, India has stepped up its military expenditure considerably in the past five years.

Since independence, India has fought three wars with Pakistan and one with China. Disputes with Pakistan have been mainly territorial. In 1947 Pakistani tribesmen invaded the mainly Muslim princely state of Jammu and Kashmir, and Indian forces intervened at the request of the state's Hindu maharaja. The resulting war left about one-third of Kashmir with Pakistan and the remainder with India (in 1963 Pakistan ceded some of the territory it controlled to China). Kashmir remains the subject of bitter dispute between the two countries. A short war was fought in 1965 over a Pakistani incursion into disputed territory in Kutch. Another war was fought over the exodus of Hindu refugees from East Pakistan in 1971; it ended with the separation of East and West Pakistan, and the creation of Bangladesh.

The victory of the BJP-led coalition at the general election in 1998 produced a notable cooling in relations with Pakistan, compounded by both countries' nuclear tests in May that year. Talks between the two sides resumed in October 1998, culminating in the so-called bus diplomacy that saw Mr Vajpayee journey across the border for talks with his Pakistani counterpart, Nawaz Sharif, the following year. However, any thaw was quickly undone when Pakistani-backed insurgents crossed the Line of Control (LoC) dividing Indian and Pakistani positions in Kashmir, capturing several high-altitude Indian border posts in the Kargil sector in May 1999. During two months of intense fighting each side lost hundreds of men, and the conflict threatened to escalate into all-out war. The crisis was resolved in July, when the Pakistani government agreed to withdraw the intruders. Three months later the commander-in-chief of the Pakistani army, General Pervez Musharraf, staged a coup and removed Mr Sharif's elected government.

In November 2000, two years after the failed bus diplomacy, India again took the initiative on Kashmir, announcing, and subsequently extending, a unilateral ceasefire. At the end of May 2001 Mr Vajpayee called off the ceasefire and invited General Musharraf for talks in Agra in July. On the second day of talks General Musharraf said that an agreement on Kashmir must come before other normalising measures. His Indian hosts were embarrassed, and the talks broke up without an understanding being reached.

After the September 11th 2001 terrorist attacks in the US, General Musharraf supported US action against the Taliban in Afghanistan and subsequently

Relations with Pakistan look a little brighter

India 17

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

banned some terrorist organisations operating from Pakistan. India gave General Musharraf a list of 20 wanted terrorists, but Pakistan refused to hand them over. After the aborted attack on its parliament in December 2001, India identified the attackers and their handler as Pakistanis. India reduced diplomatic representation in Pakistan, suspended bus, train and air services, and stopped Pakistani overflights. The number of terrorist attacks in Jammu and Kashmir increased in the next six months, and in early 2002 both countries moved troops to the border. In October 2002, however, the People's Democratic Party (PDP) was elected to government in Jammu and Kashmir, forming an administration with the support of Congress. The PDP is committed to reconciliation, and at the invitation of the new chief minister, Mufti Mohammad Sayeed, Mr Vajpayee addressed a public meeting in Srinagar in April 2003, when he "extended the hand of friendship" to Pakistan.

In November 2003 India matched Pakistan's unilateral offer of a ceasefire along the LoC in Kashmir. The offer followed measures announced unexpectedly by the Indian government to improve ties with its neighbour a month earlier. In December 2003 India and Pakistan agreed to resume air links and to allow overflights. A ground-breaking meeting was also held between the Indian government and moderate Kashmir separatists in December 2003, marking a new chapter in the 14-year stand-off between the Indian government and Kashmiri separatists. In February 2004 formal peace talks over the disputed region of Kashmir were held in the Pakistani capital, Islamabad.

The rapprochement between the two nuclear neighbours has continued under the new Congress-led government since May 2004. India began a partial troop withdrawal from Kashmir in November 2004. In January 2005 India and Pakistan agreed to the single most important confidence-building measure in the last 50 years—a bus route that links Indian- and Pakistani-controlled Kashmir. Following their meeting in the Indian capital, New Delhi, in April, General Musharraf and the new Indian prime minister, Manmohan Singh, declared the peace process "irreversible".

Since then there has been little progress. General Musharraf has floated new ideas aimed at moving the peace process forward, but India has seemed rather unimpressed with both the style of his diplomacy and the substance of his proposals. In January 2006 he called for the demilitarisation of three cities in Indian-controlled Kashmir and the establishment of "self-governance" in both Indian- and Pakistani-controlled Kashmir. He suggested that self-governance should involve bringing both sides of the disputed Kashmir region under the joint control of India, Pakistan and the Kashmiris themselves. However, India rejected demilitarisation outright, arguing that any reduction in troop levels "within the territorial borders of India" would be its own decision.

India has been reluctant to make any concessions since bombs in the capital, Delhi, killed 66 people in October 2005, in an attack blamed on Pakistani militants. The prime minister, Mr Singh, reiterated in February 2006 that he did not have the mandate to negotiate the transfer of India's sovereign territory, in a reference to Indian-controlled Kashmir. Neither India nor Pakistan will agree to the other country ruling the whole of Kashmir or to full independence for the territory. India rejects the redrawing of the Line of Control, the de facto

18 India

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

international border. The latest proposal by General Musharraf of "self-governance"—however vague—would work, at least in principle, without violating either country's conditions. But even if India wanted to explore this path, it would also have to be acceptable to the various Kashmiri groups.

In July 2006 over 200 people died in a series of rush-hour bomb blasts on Mumbai's commuter train network. General Musharraf was quick to condemn the blasts and offered to assist in finding the perpetrators. His comments, as well as the restraint shown by the Indian government, ensured that the peace process was not derailed.

India's relations with China have long been delicate. In 1957 India discovered that China had built a road across what it regarded as the north-east corner of Kashmir. (There was no administrative presence in this remote and arid desert tract, so that the road was not immediately noticed.) China rejected India's territorial claims, and a series of violent clashes between border guards took place over the next five years. In 1962, after a particularly bloody clash Nehru ordered the army to throw out the Chinese. The army was poorly equipped and inadequately trained for mountain warfare, however, and whereas the Chinese had built roads to the border, the Indian army had to ascend along mule paths. The Chinese army dealt it a crushing defeat, but then declared a ceasefire. The defeat has made India circumspect.

Despite the fact that China has a military alliance with Pakistan and has given Pakistan considerable military assistance, the Sino-Indian border has been quiet for over 40 years. In the 1980s the two countries began talks to demarcate their frontier, but progress has been very slow. In 2005, when the Chinese prime minister, Wen Jiabao, visited New Delhi, China formally abandoned its claim to Sikkim (whose accession to India in 1975 China had previously refused to recognise officially) and pledged to support a larger role for India in the inter-national arena. In recent years Sino-Indian relations have increasingly been driven by economics. Bilateral trade between India and China has increased more than tenfold since the early 1990s; China is now India's second-largest export market and ranks fifth as a source of Indian imports. In June 2006 India and China agreed to re-open the trade route through the Nathu La that connects Sikkim and Tibet, which had been closed for trade since the 1962 conflict.

The 1971 India-Pakistan war ended with the surrender of Pakistan's entire army in the east and the establishment of Bangladesh as an independent state. Relations between India and Bangladesh are nevertheless close, if not particularly friendly. Various issues between the two countries remain unresolved, including Bangladeshi immigration into India, the sale of natural gas to India, water-sharing of the many common rivers, and Bangladesh's alleged role in harbouring Indian insurgents. India has completed the construction of over two-thirds of an iron fence along the 2,500-mile border with Bangladesh. The Bangladeshi political scene is polarised between the heirs of those who fought for independence from Pakistan on one hand, and the pan-Islamists, to whom the present governing party is close, on the other. India is Bangladesh's closest source of many goods, especially yarn for its export-oriented textile industry.

Relations with Bangladesh are strained

Relations with China have improved

India 19

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

India conducted its first atomic test in 1974, after which Pakistan embarked on its own nuclear programme. By 1994 it was widely accepted that Pakistan had acquired both the atom bomb and Chinese-supplied ballistic missiles. India has developed its own intermediate-range ballistic missile capability. In 1998 India tested nuclear devices, and Pakistan followed suit. The US president at the time, Bill Clinton, tried to persuade India to sign the NPT and the Comprehensive Test Ban Treaty (CTBT). However, India's political establishment, which regards the two treaties as "nuclear apartheid", refused to sign them as a matter of principle. The US came to accept that it was highly unlikely that India would ever sign the treaties. In 2005, in an effort to upgrade ties with India, the US changed its stance on the entire issue by stating that "as a responsible state with advanced nuclear technology, India should acquire the same benefits and advantages as other such states" and offered India sensitive civil nuclear technology. It thereby accepted India de facto as a nuclear power.

India maintains the second-largest army in the world, with total armed forces of 1.3m active servicemen and a further 1.2m reservists. However, its soldiers are poorly equipped, particularly for the demanding conditions in Kashmir. The army has a strictly non-political role, although it is often called upon to help beleaguered police forces in areas facing secessionist movements, such as Kashmir and the north-east. Defence expenditure stood at US$22bn in fiscal year 2005/06 (April-March), or about 3% of GDP, and given the historically tense relations with Pakistan, it is likely to remain high.

Military forces, 2005/06 India Pakistan ChinaArmy Personnel 1,100,000 550,000 1,600,000a

Main battle tanks 3,978 2,461 7,580

Navy Personnel 55,000 24,000 255,000a

Frigates 17 7 42Submarines 19 11 69Air force Personnel 170,000 45,000 400,000Combat aircraft 852 331 2,643

a Estimate.

Source: International Institute for Strategic Studies, The Military Balance 2005/06.

Security risk in India

Armed conflict

India has fought three wars with Pakistan—two over the disputed territory of Kashmir and one during Bangladesh's war of independence—as well as a major skirmish in Kargil in 1999 between Pakistan-backed militants and the Indian army. Shelling along the Line of Control (LoC), the de facto border that divides Indian and Pakistani Kashmir, is commonplace. India accuses Pakistan of giving military backing to Kashmiri separatists and Islamic militants fighting against India in Kashmir, but

The armed forces are the second-largest in the world

India is accepted as a de facto nuclear power

20 India

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Pakistan claims to give only moral support to the insurgents and accuses India of repressing Muslims in Kashmir. Tensions between the two nuclear powers have been high since an attack on India's parliament building in December 2001, which India blamed on Pakistani-based militant groups. Both countries mobilised troops and stood on the brink of war. Hostility between the two countries has remained intractable, owing to the underlying Kashmir dispute: each country faces considerable domestic pressure not to make concessions to the other in relation to Kashmir. However, in April 2003 relations began to improve significantly, largely as a result of a US-backed international initiative to diffuse the crisis. India began a partial troop withdrawal from Kashmir in November 2004. The rapprochement with Pakistan has continued under the new Congress-led government. In April 2005, in the most important peace-building measure between the nuclear neighbours in four decades, a bus service between Srinagar in Indian-controlled Kashmir and Muzaffarabad in Pakistani-controlled Kashmir came into operation—the first bus route across the LoC in over 50 years. In the past, peace talks have floundered over the question of the relative importance of Kashmir. India has argued that the Kashmir dispute is one of several issues that need to be resolved, and has attempted to improve bilateral relations through the establishment of commercial links, for example, in the hope that with better relations the Kashmir dispute will diminish in relative importance. In contrast, Pakistan argues that the Kashmir dispute is the central issue and the reason behind the two countries' poor relations, and that without its resolution other confidence-building measures will be impossible. Pakistan fears that, should militancy in Kashmir end, India will feel little compulsion to offer Pakistan any concessions regarding Kashmir. India fought a war with China in 1962. Relations between the two countries are nevertheless generally neighbourly, although part of their common border in north-east India remains disputed. India's relationship with Bangladesh is also reasonable, despite occasional clashes between border guards.

Terrorism

India suffers from many bomb attacks, which often occur on buses or trains or at bus stations. Such low-level attacks are generally blamed on Pakistan's intelligence agency and Pakistani-backed Kashmiri militants. Numerous sub-nationalist groups operate within India, and although their activities are generally confined to specific areas, Kashmiri militants have conducted attacks in Delhi. The most daring of these occurred in December 2001, when a group of militants entered India's parliament building, killing at least seven people. Kashmiri militants have also taken foreign hostages, notably in 1995, when four foreigners were kidnapped in Kashmir—the four are presumed dead. More recently, in October 2005 several bombs killed 62 people and injured over 200 in market places in Delhi. A little-known Kashmiri group has claimed responsibility for the attack. Bomb blasts in the Hindu pilgrimage city of Varanasi killed 14 people in March 2006.

India 21

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Apart from Kashmiri militants, several other groups operate in north-east India, campaigning for state status or independence for their regions. Maoist rebels operate in the tribal-dominated areas of central India and are thought to be linked to the Communist Party of Nepal (Maoist). The Indian government believes there may be 10,000 Maoists in the country. In the worst terrorist incident since 1993, in July 2006 over 200 people were killed in a series of rush-hour commuter train bombings across Mumbai. The police are still gathering evidence, and the government has refrained from making sweeping allegations ahead of a thorough investigation.

Civil unrest

Religious clashes between Hindus and Muslims are not infrequent, and as events in Gujarat showed in 2002, can escalate rapidly. In February 2002 a gang of Muslims attacked a train carrying Hindus from Ayodhya, killing 57 people. Hindus responded by attacking Muslims throughout Gujarat, and up to 1,000 are thought to have died. Communal clashes are often sparked or exacerbated by property or commercial disputes, rather than simply by religious intolerance. Such riots usually take place in poor districts of cities in northern India. In the latest incident of sectarian violence, in May 2006, anti-Muslim riots in Gujarat left six dead in the city of Vadodara, as Muslims protested against the demolition of an ancient Muslim shrine by the municipal authorities. The disturbances coincided with violence in Muslim-dominated Jammu and Kashmir, where militant groups killed at least 35 Hindus.

Crime

Petty crime is common in India. According to the National Crime Records Bureau (NCRB), in 2004 there were over 270,000 incidents of theft and over 90,000 of burglary. Such statistics are likely to understate the prevalence of crime. Many crimes go unreported, owing to a lack of confidence in the police. Bag-snatching and pick-pocketing are fairly common, particularly in crowded tourist areas. According to the NCRB, there were over 33,000 murders in 2004.

Drug smuggling and organised crime

Organised crime is a concern in India, particularly in Mumbai. Protection and extortion rackets have flourished, particularly in the film industry and the media generally, including cable companies. Some gangs are believed to have moved into trade unionism. This problem is likely to have been exacerbated by the number of politicians—particularly in state assemblies—with criminal records. The worst incident connected to India's underworld took place in Mumbai in 1993, when a number of bombs exploded, resulting in 257 deaths. The stock exchange, several hotels and other offices were hit, and hand-grenades were thrown at the international airport. The incidents were blamed on a combination of the underworld and the Pakistani intelligence agency.

22 India

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Resources and infrastructure

Population

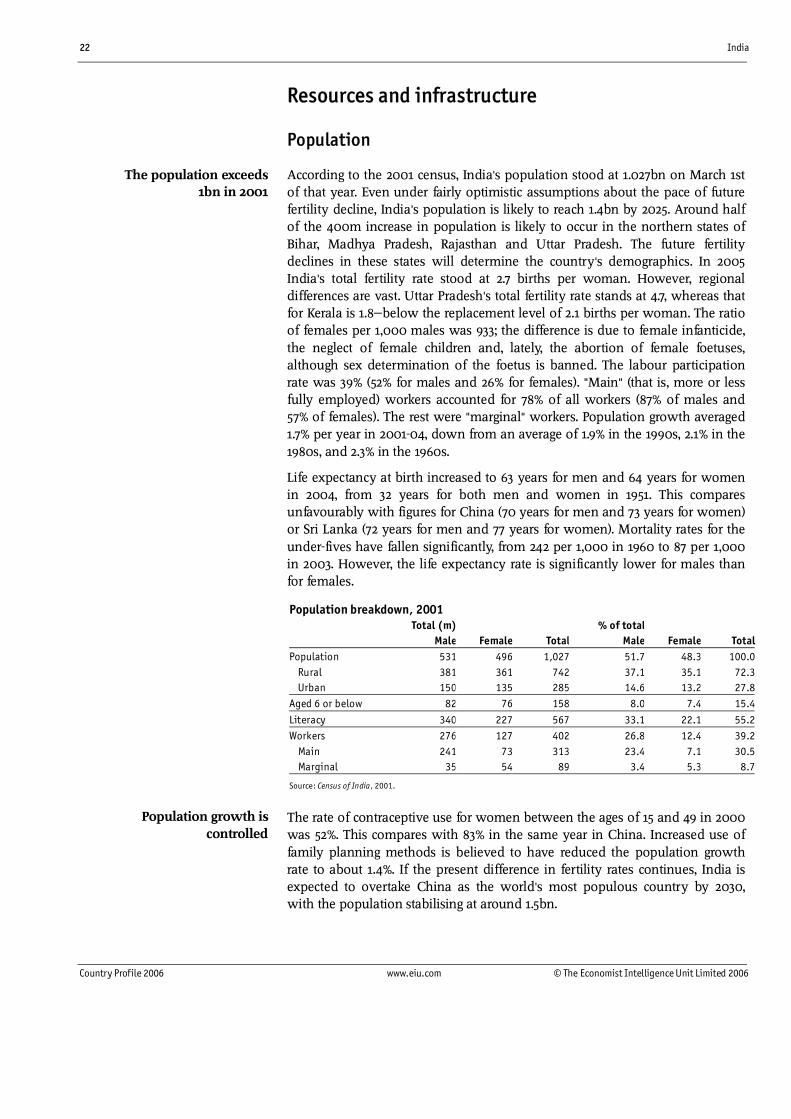

According to the 2001 census, India's population stood at 1.027bn on March 1st of that year. Even under fairly optimistic assumptions about the pace of future fertility decline, India's population is likely to reach 1.4bn by 2025. Around half of the 400m increase in population is likely to occur in the northern states of Bihar, Madhya Pradesh, Rajasthan and Uttar Pradesh. The future fertility declines in these states will determine the country's demographics. In 2005 India's total fertility rate stood at 2.7 births per woman. However, regional differences are vast. Uttar Pradesh's total fertility rate stands at 4.7, whereas that for Kerala is 1.8—below the replacement level of 2.1 births per woman. The ratio of females per 1,000 males was 933; the difference is due to female infanticide, the neglect of female children and, lately, the abortion of female foetuses, although sex determination of the foetus is banned. The labour participation rate was 39% (52% for males and 26% for females). "Main" (that is, more or less fully employed) workers accounted for 78% of all workers (87% of males and 57% of females). The rest were "marginal" workers. Population growth averaged 1.7% per year in 2001-04, down from an average of 1.9% in the 1990s, 2.1% in the 1980s, and 2.3% in the 1960s.

Life expectancy at birth increased to 63 years for men and 64 years for women in 2004, from 32 years for both men and women in 1951. This compares unfavourably with figures for China (70 years for men and 73 years for women) or Sri Lanka (72 years for men and 77 years for women). Mortality rates for the under-fives have fallen significantly, from 242 per 1,000 in 1960 to 87 per 1,000 in 2003. However, the life expectancy rate is significantly lower for males than for females.

Population breakdown, 2001 Total (m) % of total Male Female Total Male Female TotalPopulation 531 496 1,027 51.7 48.3 100.0 Rural 381 361 742 37.1 35.1 72.3 Urban 150 135 285 14.6 13.2 27.8Aged 6 or below 82 76 158 8.0 7.4 15.4

Literacy 340 227 567 33.1 22.1 55.2Workers 276 127 402 26.8 12.4 39.2 Main 241 73 313 23.4 7.1 30.5 Marginal 35 54 89 3.4 5.3 8.7

Source: Census of India, 2001.

The rate of contraceptive use for women between the ages of 15 and 49 in 2000 was 52%. This compares with 83% in the same year in China. Increased use of family planning methods is believed to have reduced the population growth rate to about 1.4%. If the present difference in fertility rates continues, India is expected to overtake China as the world's most populous country by 2030, with the population stabilising at around 1.5bn.

The population exceeds 1bn in 2001

Population growth is controlled

India 23

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

India has a relatively low level of urbanisation compared with most other developing countries in Asia: almost 60% of Indians live in villages with a population of less than 5,000. However, the rate of migration from rural to urban areas is increasing. The urban population constituted 28% of the total in 2001, up from just over 25% in the mid-1990s, and is likely to reach 36% around 2025. In 2001 there were 35 cities with a population above 1m; the number of such cities is likely to rise to 70 by 2025, when they will contain about one-half of the country's urban inhabitants. The urban population is growing fastest in states such as Bihar and Uttar Pradesh, which have comparatively low levels of urbanisation. More developed states such as Maharashtra and Tamil Nadu, whose populations are growing less rapidly, experience lower urban growth. The largest urban agglomerations are Mumbai (16.4m in 2001), Kolkata (13.2m), Delhi (12.8m), Chennai (6.4m), Bangalore (5.7m) and Hyderabad (5.5m).

India's population is extremely diverse, differentiated by language, religion, caste and class. A significant political divide exists between Hindus (81% of the population) and other religious groups, including Muslims (13%), Sikhs and Christians. However, Hinduism is itself a highly stratified religion, and a large number of Hindus, particularly among the lower castes, do not have a political affinity with Hindu-nationalist movements. Another important distinction exists between the primarily Hindi-speaking north and the south, where a number of vernacular languages are in use, together with English. English is a lingua franca throughout the country, however, and competence in the language is more a function of class than region.

Income and consumption differentials are significant, but not high by develop-ing-country standards: the top one-fifth of India's population accounts for around 46% of income or consumption, whereas the bottom one-fifth accounts for around 8%. About 25% of the population, or 260m people, were below the poverty line in 2000, as measured by an income level of less than one US dollar a day.

Education

Literacy rates among the population aged seven years and over have risen considerably during the 1990s. The 2001 census recorded literacy rates of 65.2%, up from 52.2% in 1991—the highest rise ever in a single decade. The male literacy rate was 75.6% in 2001 (up from 56% in 1981 and 27% in 1951), compared with 54% for women (30% in 1981 and 9% in 1951). The 2001 census indicated a decline in the total number of illiterate people for the first time since independence, with 21.5m fewer illiterate males and 10.5m fewer illiterate females in 2001 than in 1991. In spite of recent progress, India still lags behind in educational standards, both absolutely and compared with other developing countries: it has 17% of the world's population, but some 40% of the world's illiterates. India also possesses a large pool of highly educated and vocationally qualified people, although they make up a small fraction of the population. There are considerable regional variations in literacy rates: Kerala has a rate of 91%, whereas Bihar has a rate of only 49%.

The picture is mixed

Migration is shifting from rural to urban

The population is diverse

24 India

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Literacy and school attendance have improved markedly since the early 1990s, as poverty has declined and educational aspirations have surged. In fiscal year 2002/03 (April-March) an estimated 82% of children in the 6-14 age group were enrolled in school. Attendance in primary schools has risen notably, but the rates for girls are significantly lower than for boys. Overall attendance in secondary schools rose from 20% in 1960 to 44% in 1991 (with the female rate rising from 13% to 32%). In higher education (science, math and engineering) the rate was 20% for both males and females in 1998-2003, the highest rate by far for a low-income developing country, and up from single digits in 1960.