india economic update - world banksiteresources.worldbank.org/indiaextn/resources/... · india...

TRANSCRIPT

December, 2010

Economic Policy and Poverty Team

South Asia Region

The World Bank

India Economic Update

Overview

A Robust Recovery

The Indian economy recovered from the slowdown at the time of the global financial crisis with strong

GDP growth, in particular over the first half of FY2010-11. The agricultural sector bounced back strongly

after the 2010 monsoon brought normal levels of rainfall, and the industrial sector registered double-digit

growth for three consecutive quarters. Inflation came down to 7.5 percent in November but then

accelerated again to 8.4 percent in December because of a renewed food supply shock. The current

account deficit in FY2009-10 was the largest ever (in US$ terms) and the monthly deficit widened further

during the first half of FY2010-11, but the trend then reversed with import growth slowing and export

growth accelerating in September-December 2010. With the significant inflation differential between

India and its trading partners, the rupee‟s real effective exchange rate (REER) strengthened. On the fiscal

side, massive windfall revenue from wireless spectrum auctions and buoyant tax revenue are likely to be

offset by two supplementary spending bills. Monetary policy tightening continued with increases in

policy rates.

Looking forward, GDP growth looks set to regain the pre-crisis trend of around 8.5-9 percent in this year

and the next (FY2011-12). Assuming that the December resurgence in food inflation is temporary, overall

wholesale price inflation is likely to decelerate to 7 percent by end-March 2011 and further during the

coming fiscal year, although uncertainty over international commodity prices persists. The widening trade

deficit during the first half of the year could result in a current account deficit around 3.5 percent of GDP

in FY2010-11, although the recent decline in the trade deficit augurs well for the coming year. Capital

inflows are expected to cover this gap in the current year.

The RBI is likely to continue its policy of cautious rate hikes in a highly uncertain environment. While

inflation has become more broad based, capacity utilization, industrial production, import, and credit

indicators do not point to overheating. The signals are therefore not clear whether core inflation is caused

by more general demand pressures, which would best be addressed with more aggressive policy

tightening, or by second round effects of earlier food and commodity price shocks, for which the current

monetary policy stance is likely to be adequate.

This update also discusses several medium-term issues: the link between the real exchange rate and

growth, a long-term look at education, demographics and growth, the challenges facing the introduction

of the GST, and the mid-term evaluation of the Eleventh Development Plan. On the real exchange rate,

economists have pointed out that the most successful emerging market economies have maintained an

undervalued exchange rate to promote exports. In India, the real exchange rate has been broadly stable

since the early 1990s, and the IMF judges it fairly valued with respect to different measures of

equilibrium. However, the growing trade deficit and a large fiscal deficit do not quite fit this picture.

Discussing policies, we argue that it would be best to focus on policies that increase productivity and

competitiveness.

Education is a strong factor influencing the demographic transition, and it also has direct effects on

economic growth. We present an outlook on India‟s population over the next three decades focusing on

educational attainment. A database for 120 countries allows us to estimate the average relationship

1 Prepared by Ulrich Bartsch, Abhijit Sen Gupta, and Monika Sharma. Helpful comments from Roberto Zagha, Miria Pigato,

Martin Rama, Ivailo Izvorski, Kalpana Kochhar, and Ravi Kanbur are gratefully acknowledged.

India Economic Update1 December, 2010

between education and growth. Applying this to different education scenarios in India highlights the

increase in economic growth that could be expected from a major push for education.

While preparations for the implementation of a Goods and Services Tax are well advanced, political

agreement on the modalities is elusive. The introduction of the GST is intended to broaden the revenue

base and boost growth by removing distortions and increasing integration within India. Discussions are

ongoing about tax rates and which state and local taxes to discontinue, with some of India‟s states fearing

erosion of fiscal autonomy and higher dependence on central transfers.

Lastly, we highlight the Planning Commission‟s Mid-term Assessment of the Eleventh Plan. The most

interesting are its optimism that major goals of the plan, particularly with regard to infrastructure

investment, could be met despite the negative impact of the global financial crisis, and the preview of a

massive step-up in infrastructure spending under the Twelfth Plan.

1

I. Recent Economic Developments

Strong headline GDP growth and quarter-on-

quarter results indicate that the recovery of the

Indian economy is robust. Backed by strong growth

of 8.9 percent y-o-y in the first half of FY2010-11, the

economy is estimated to grow by 8.6 percent during

the fiscal year, as compared with a revised estimate of

8 percent growth for FY2009-10.2 The first and

second quarter growth rates of 8.9 percent were the

highest achieved since Q3 FY2007-08. The quarter-

on-quarter seasonally adjusted annual rate (q-o-q

SAAR) of GDP growth reached 9.0 and 9.3 percent

for the same two quarters.

A low base helped agriculture record a strong

growth rate, but food production is well below

peak levels achieved in earlier years. Agriculture is

expected to grow at 5.4 percent spurred by a low base

in the drought year FY2009-10. The first advance

estimates of kharif (summer) crop production peg

output around 114.6 million tons, a rise of 10.4

percent compared with FY2009-10. The rise in output

was driven by pulses (39.4 percent), jowar (17.2

percent), maize (19.5 percent) and rice (5.9 percent).

However, production in FY2010-11 is estimated to be

well below the levels achieved in FY2007-08 (121

million tons) and FY2008-09 (118 million tons).

The industrial sector registered double digit

growth for three consecutive quarters but slowed

significantly in the October-December quarter. Industrial production (IIP) registered an average

growth of 10.2 percent between April and November

2010. The robust growth was driven by strong

performance of the capital goods and consumer

durables, which grew by 25.8 percent and 22.3 percent

respectively. The manufacturing sector had slowed

down in August and September 2010, but recovered to

register growth of 11.3 percent in October 2010. The

industrial sector is estimated to grow at 8.1 percent in

the fiscal year due to slowing down of the industrial

production in the second half of the year.

On the expenditure side, a resurgence of investment led the recovery, but private consumption

growth is now also picking up. Overall consumption is estimated to grow by 7.3 percent in FY2010-11,

lower than 8.7 percent in FY2009-10. While private consumption growth is set to increase from 7.3 to 8.2

percent, government consumption growth declined from 16.4 percent to 2.6 percent as a result of slowing

2 GDP growth estimate was raised to 8 percent from 7.4 percent for FY2009-10. Advance estimates by CSO for

FY2010-11.

-4.0%-2.0%0.0%2.0%4.0%6.0%8.0%10.0%12.0%14.0%16.0%

-4.0%-2.0%0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%16.0%

07-0

8 Q

1

07-0

8 Q

2

07

-08

Q3

07-0

8 Q

4

08-0

9 Q

1

08

-09

Q2

08-0

9 Q

3

08-0

9 Q

4

09-1

0 Q

1

09

-10

Q2

09-1

0 Q

3

09-1

0 Q

4

10

-11

Q1

10-1

1 Q

2

Agriculture Services GDP Industry

The Rebound in the Agricultural Sector Strengthened.(y-o-y change, in percent)

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

05-

06

Q1

05-

06

Q2

05-

06

Q3

05-

06

Q4

06-

07

Q1

06-

07

Q2

06-

07

Q3

06

-07

Q4

07

-08

Q1

07

-08

Q2

07

-08

Q3

07-

08

Q4

08-

09

Q1

08-

09

Q2

08-

09

Q3

08-

09

Q4

09-

10

Q1

09-

10

Q2

09-

10

Q3

09-

10

Q4

10-

11

Q1

10-

11

Q2

Private Demand Growth Remained Strong. (Components of GDP, y-o-y, change in percent)

GDP Excl. Gov. Cons.

GDP

Source: CSO. Note: Expenditure GDP growth not always same as production.

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

05-0

6 Q

105

-06

Q2

05-0

6 Q

30

5-0

6 Q

406

-07

Q1

06-0

7 Q

206

-07

Q3

06-0

7 Q

407

-08

Q1

07-0

8 Q

207

-08

Q3

07-0

8 Q

408

-09

Q1

08-0

9 Q

20

8-0

9 Q

308

-09

Q4

09-1

0 Q

109

-10

Q2

09

-10

Q3

09-1

0 Q

410

-11

Q1

10-1

1 Q

2

Investment Slowed.(Components of GDP, y-o-y change, in percent)

Total Consumption

Private Consumption

Investment

Government Consumption

2

fiscal stimulus spending. Investment (net of stocks) is expected to grow by 8.4 percent in FY 2010-11 as

opposed to 7.3 percent in the previous year.

Food prices renewed their steep climb after a brief slow-down in inflation in the second half of

2010. The WPI inflation rate rose to 8.4 percent in December 2010 from 7.4 percent a month ago,

averaging at 9.4 percent for the period April to December 2010. The recent uptick in inflation can be

attributed to a surge in prices of food articles, which grew by 13.5 percent in December. While food grain

prices have dropped by 2.6 percent in December 2010, the recent surge is due to a spike in fruits and

vegetable prices, which increased by 22.8 percent. Milk, eggs, meat, fish and spices also experienced

double digit inflation rates.

A new wholesale price index was introduced in September 2010 with an updated product basket

and FY2004-05 as base year. While the weights of major product groups have changed little, the new

index has broader coverage (676 items as compared with 435 previously) and nearly three times the

number of price quotations. The new index track the old closely, although the moderation of inflation in

August is more pronounced in the new index than in the old.

The rising merchandise trade deficit pushed the current account deficit to its largest value ever (in

US$ terms). The current account deficit widened to $38.4 billion (2.9 percent of GDP) in FY2009-10.

Nevertheless, strong capital inflows more than compensated for the current account deficit.

Merchandise exports grew by 29.5 percent between

April and December 2010 to reach $164.7 billion.

Over the same period rising oil price and increased

domestic activity pushed imports to $246.7 billion,

increasing by 19 percent from the previous year. The

trade deficit reached US$13bn in August 2010 but has

come down to US$9.5bn in September-October. At the

same time, services exports reacted with a lag to the

global crisis and fell strongly since Q2FY2008-09,

while remittances stabilized. The invisibles‟ surplus

witnessed a slowdown to $79 billion from $90 billion

on account of a deficit in business, financial and

communication services in the first half of FY2010-11.

Capital inflows remained buoyant. Portfolio

investment has been strong for most of the period with

net inflows of $52.6 billion, during April to October

2010. However, November 2010 witnessed a net

outflow of $19.8 billion. There has been a relative

slowdown in FDI flows to $14.0 billion from $19.3

billion during the Apr.-Oct. periods in FY2010-11 and

FY2009-10, respectively. After refraining from

intervention in the foreign exchange market through

most of the first half of FY2010-11, the RBI purchased

$1.3 billion in October and December 2010.

With the significant inflation differential between

India and its trading partners, the rupee’s real

effective exchange rate (REER) strengthened. From

its trough in the wake of the global financial crisis and

-50

-40

-30

-20

-10

0

10

20

1981

-82

1983

-84

1985

-86

1987

-88

1989

-90

1991

-92

1993

-94

1995

-96

1997

-98

1999

-00

2001

-02

2003

-04

2005

-06

2007

-08

2009

-10

The Current Account Deficit Widened(in US$ billion)

60

65

70

75

80

85

90

95

100

105

110

1/20

06

4/20

06

7/20

06

10/2

006

1/20

07

4/20

07

7/20

07

10/2

007

1/20

08

4/20

08

7/20

08

10/2

008

1/20

09

4/20

09

7/20

09

10/2

009

1/20

10

4/20

10

7/20

10

10/2

010

The Real Exchange Rate Appreciated(1993=100)

3

ahead of the May 2009 elections, the REER appreciated

by about 13.6 percent till November 2010 but is still

well below the level it had reached around mid-2007.

Business sentiment is strong, but capacity utilization

is below previous peaks. The RBI‟s industrial outlook

surveys show that companies‟ perceptions of financial

situation and profit margins have recovered to levels

last seen in mid-2007, while selling prices are perceived

to be still lower than at the peak at end-2008. On the

other hand, the RBI‟s Order Books, Inventories and

Capacity Utilization Survey (OBICUS) indicates that

capacity utilization increased during the second quarter

of FY2010-11, but remained below the previous peak.

Capacity utilization in core infrastructure sectors was

largely unchanged from the same period in FY2009-10.

India’s growth resilience and fiscal consolidation

strategy prompted upwards revisions of credit

ratings. Both Moody‟s and Fitch upgraded their local

currency ratings. While Moody‟s upgraded its rating

from Ba2 to Ba1 with a positive outlook, Fitch revised

its rating from negative to stable. These revisions are

likely to encourage FII inflows and strengthening of the

rupee.

Fiscal Developments

Both revenue and expenditure are likely to be higher

than envisaged at the time of the budget. The

government received a massive windfall revenue of

close to Rs.1 trillion (US$20bn, equivalent to 1.8

percent of GDP) from auctions of wireless spectrum.

On the other hand, additional spending was authorized

through adoption by parliament of a first and second

supplementary demand for grants. The supplementary

demands for grants tabled by the government involve an

additional expenditure of Rs.1.1 trillion (1.8 percent of

GDP). A large part of this expenditure, Rs.744 billion

(1.1 percent of GDP) would compensate losses by oil

marketing companies, finance food and fertilizer

subsidy, build roads and houses under centrally

sponsored schemes, and finance transfers to states.

Furthermore, the linking of wages with the CPI would

result in potential higher outgo on NREGA

Tax revenue collections during the first half of

FY2010-11 are promising. Gross tax revenue during

the April-December 2010 stood at Rs.5.28 trillion, up

26.8 percent from the same period last year. Improving

merchandise trade and economic activity as well as reversal of some of the earlier cutbacks in tax rates

resulted in an increase in customs and excise duties of 65.7 percent and 36.5 percent, respectively, over

Oil Under recoveries

19%

PMGSY & Rural Housing

10%

Transfers to State and UTs

8%

Fertilizer Subsidy7%

Food Subsidy

7%Education5%

Rural Development for North East

4%

IMF Quota4%

Defence6%

Police2%

Others28%

Supplementary Spending Bills(Share of total in percent)

-30

-20

-10

0

10

20

30

40

50

3/2

00

5

9/2

00

5

3/2

00

6

9/2

00

6

3/2

00

7

9/2

00

7

3/2

00

8

9/2

00

8

3/2

00

9

9/2

00

9

3/2

01

0

9/2

01

0

3/2

01

1

Industrial Outlook Survey(Perception Indices)

Fin. Situation Selling Prices Profit Margin

Source: RBI

2009-10 2010-11

Finished Steel

(SAIL + VSP + Tata Steel) 87.7 88.9

Cement 80 75

Fertilizer 94.1 94.2

Refinery Production-Petroleum 101.3 102.7

Thermal Power* 72.9 76.2

* Data represent plant load factor for April-December.

Apr.-Oct.

Source: Capsule Report on Infrastructure Sector

Performance (April 2010-October 2010), Ministry of

Statistics and Program Implementation, and Central

Electricity Authority.

Capacity Utilization in Infrastructure Sectors

4

the previous year. Direct tax collection also witnessed

a steady increase with corporate tax revenue

increasing by 20.4 percent and income tax rising by

13.1 percent.

The central government is likely to overperform

on its deficit target under the government’s

accounting rules. However, license fees should be

counted as a financing item because they arose from

the sale of a non-renewable asset much like

privatization revenue. Under this treatment, the

central government deficit is likely to reach 6-6.5

percent of GDP and fiscal consolidation during

FY2010-11 looks feeble.

Monetary Developments

Credit growth and liquidity developments were

largely driven by the result of the telecom

spectrum auctions concluded in June 2010.

Government revenue from auctions of telecoms

licenses was close to Rs.1 trillion. Absorption of

liquidity through payments of the license fee and tax

payments led to a sharp switch in the interbank

market interest rate from the bottom to the top of the

RBI‟s policy rate band (100 basis points between

reverse repo and repo) as banks went from excess

liquidity to liquidity shortage and cash accumulated

in government accounts at the RBI. Broad money expanded by 16.9 percent while reserve money

expanded by 23.6 percent in November 2010 (y-o-y). Credit growth picked up to 18 percent in December

2010 and 20 percent in January 2011, after remaining around 15-16 percent during most of 2010.

Monetary policy tightening continued. With the inflation rate persisting at high levels, the RBI

increased the repo and reverse repo rate in six steps between January 2010 and January 2011 by 150 and

225 basis points, to 6.5 percent and 5.5 percent, respectively.

In a major step to clarify loan pricing, the RBI ruled that commercial banks adopt a Base Rate in

the place of the benchmark prime lending rate (BPLR). The reform is expected to increase the

transparency in lending rates, improve the transmission of monetary policy, and discourage cross-

subsidization of loans. In contrast to the earlier BPLR, banks are now disbarred from lending below the

base rate. It is calculated on the basis of the cost of funds, overhead costs, adjustment for the negative

carry of statutory reserve requirements, and average return on net worth. The banks retain the flexibility

of determining their own lending rates by incorporating customer specific charges as deemed appropriate.

The base rate can be decided on a quarterly basis.

0

5

10

15

20

25

Ap

r-0

5

Jul-

05

Oct

-05

Jan

-06

Ap

r-0

6

Jul-

06

Oct

-06

Jan

-07

Ap

r-0

7

Jul-

07

Oct

-07

Jan

-08

Ap

r-0

8

Jul-

08

Oct

-08

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Reverse RepoCRRRepoCall Money Rate

Monetary Policy Tightening Continued(Policy Rates and Bombay Interbank Call-Money Rates, in percent)

-1,500

-1,000

-500

0

500

1,000

1,500

2,000

5/3

/20

04

9/3

/20

04

1/3

/20

05

5/3

/20

05

9/3

/20

05

1/3

/20

06

5/3

/20

06

9/3

/20

06

1/3

/20

07

5/3

/20

07

9/3

/20

07

1/3

/20

08

5/3

/20

08

9/3

/20

08

1/3

/20

09

5/3

/20

09

9/3

/20

09

1/3

/20

10

5/3

/20

10

9/3

/20

10

1/3

/20

11

A Liquidity Shortage has Developed(- = injection, in billions of rupees)

Note: RBI Liquidity Adjustment Facility, net bids accepted.Source: RBI.

5

II. Outlook

Global Prospects and Capital Flows

The first half of 2010 witnessed a robust recovery in global GDP growth to 5.25 percent. However,

this benign global picture hides significant heterogeneity among both advanced economies and emerging

markets. Asian economies outside Japan have witnessed rapid growth rates, and the United States has

managed to regain output growth similar to pre-crisis levels, but the output is still well below its pre-crisis

level and unemployment remains uncomfortably large. Germany, on the other hand, has benefited from

an export boom which reduced unemployment to an 18-year low. Despite the German success, the euro

area still contends with an output gap larger than the US‟s. Among the developing countries, both Asian

and Latin American countries have experienced strong growth driven by fixed investment and private

demand. In contrast, developing countries like Mexico, the CIS, and others that had strong trade and

financial linkages with the advanced economies and were therefore more strongly affected by the crisis

are experiencing a more subdued recovery.

Capital Flows to Emerging Markets

(in US$ billions)

2004 2005 2006 2007 2008 2009 2010f 2010f

Private Inflows 426.6 641.7 798.0 1,284.5 594.4 581.4 825.0 833.5

Equity Investment 275.1 359.8 409.9 596.7 422.3 490.4 553.0 549.5

Direct Investment 216.3 288.7 328.6 499.5 508.5 341.8 366.5 406.5

Portfolio Investment 58.8 71.1 81.3 97.2 -86.2 148.7 186.5 143.0

Private Creditors 151.6 281.9 388.1 687.9 172.1 91.0 272.0 283.9

Commercial Banks 65.0 189.2 235.4 451.3 29.1 -44.3 84.9 111.6

Non-banks 86.6 92.7 152.6 236.6 143.0 135.3 187.1 172.3

Source: IIF (2010)

The continuing high unemployment und sluggish growth in most advanced economies has

prevented them from unwinding some of the exceptional liquidity injections undertaken during the

crisis. In fact, the US embarked on a second round of quantitative easing (QE2), thereby again pushing

down yields of US and other securities. While this move was initially expected to lead to a further

significant devaluation of the U.S. dollar, it has so far remained stable against major currencies. Critics

point out, however, that the extra liquidity is likely to exacerbate the surge of capital flows to emerging

economies, which started in the first quarter of 2010. Concerns over exchange rate appreciation, asset

bubbles, and a renewed surge in commodity prices have therefore increased.

Emerging markets are expected to have received

near-record capital inflows. An estimated

US$825billion flowed into emerging economies in

2010, which was nearly 42 percent higher than in 2009

due to relatively high interest rates, strong growth and

improved terms of trade.3 Most of the inflow was in

the form of portfolio equity investments by non-

residents into emerging markets, which rose to

US$186 billion, compared to an annual average of

US$77 billion during 2004 to 2007. In contrast,

commercial bank inflows are estimated to be

3 See IIF (2010).

0

200

400

600

800

1000

Jan

-09

Mar-

09

May-0

9

Ju

l-09

Se

p-0

9

No

v-0

9

Jan

-10

Mar-

10

May-1

0

Ju

l-10

Se

p-1

0

No

v-1

0

Sovereign Bond Interest Spreads

BRACHNIDNMYSPHL

6

significantly lower at US$84.9 billion as opposed to an

average of US$235 billion during 2004-07.

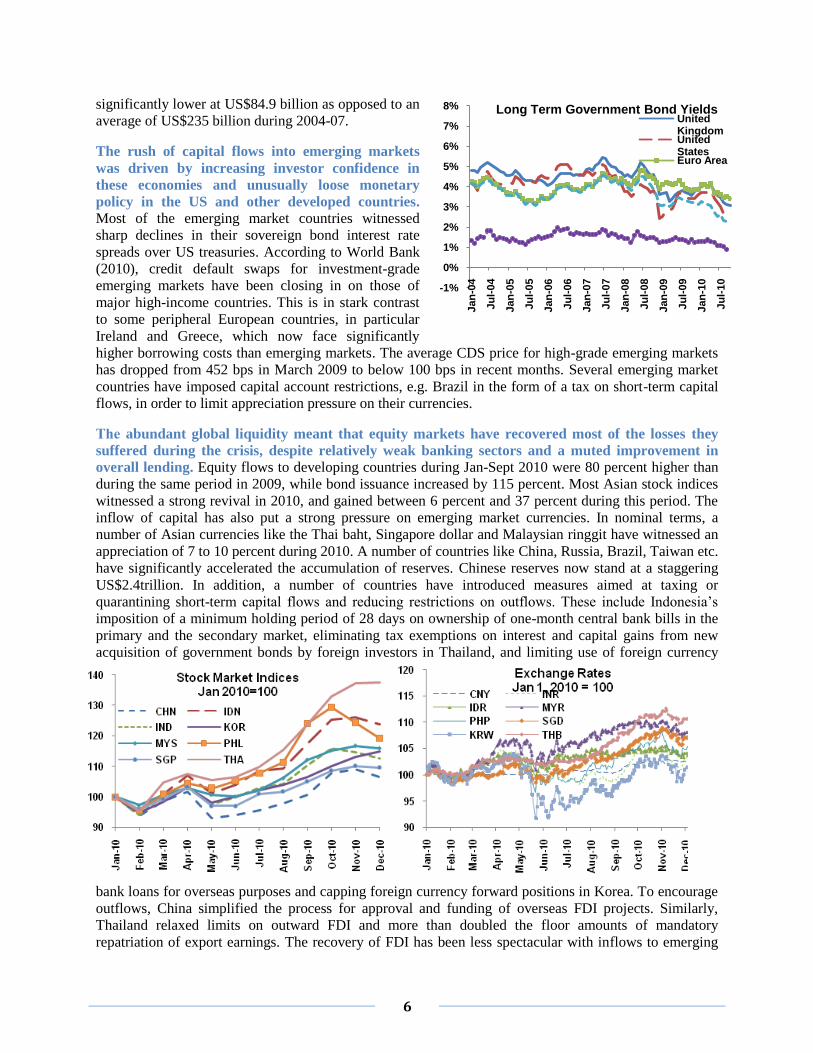

The rush of capital flows into emerging markets

was driven by increasing investor confidence in

these economies and unusually loose monetary

policy in the US and other developed countries. Most of the emerging market countries witnessed

sharp declines in their sovereign bond interest rate

spreads over US treasuries. According to World Bank

(2010), credit default swaps for investment-grade

emerging markets have been closing in on those of

major high-income countries. This is in stark contrast

to some peripheral European countries, in particular

Ireland and Greece, which now face significantly

higher borrowing costs than emerging markets. The average CDS price for high-grade emerging markets

has dropped from 452 bps in March 2009 to below 100 bps in recent months. Several emerging market

countries have imposed capital account restrictions, e.g. Brazil in the form of a tax on short-term capital

flows, in order to limit appreciation pressure on their currencies.

The abundant global liquidity meant that equity markets have recovered most of the losses they

suffered during the crisis, despite relatively weak banking sectors and a muted improvement in

overall lending. Equity flows to developing countries during Jan-Sept 2010 were 80 percent higher than

during the same period in 2009, while bond issuance increased by 115 percent. Most Asian stock indices

witnessed a strong revival in 2010, and gained between 6 percent and 37 percent during this period. The

inflow of capital has also put a strong pressure on emerging market currencies. In nominal terms, a

number of Asian currencies like the Thai baht, Singapore dollar and Malaysian ringgit have witnessed an

appreciation of 7 to 10 percent during 2010. A number of countries like China, Russia, Brazil, Taiwan etc.

have significantly accelerated the accumulation of reserves. Chinese reserves now stand at a staggering

US$2.4trillion. In addition, a number of countries have introduced measures aimed at taxing or

quarantining short-term capital flows and reducing restrictions on outflows. These include Indonesia‟s

imposition of a minimum holding period of 28 days on ownership of one-month central bank bills in the

primary and the secondary market, eliminating tax exemptions on interest and capital gains from new

acquisition of government bonds by foreign investors in Thailand, and limiting use of foreign currency

bank loans for overseas purposes and capping foreign currency forward positions in Korea. To encourage

outflows, China simplified the process for approval and funding of overseas FDI projects. Similarly,

Thailand relaxed limits on outward FDI and more than doubled the floor amounts of mandatory

repatriation of export earnings. The recovery of FDI has been less spectacular with inflows to emerging

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

Jan

-04

Ju

l-04

Jan

-05

Ju

l-05

Jan

-06

Ju

l-06

Jan

-07

Ju

l-07

Jan

-08

Ju

l-08

Jan

-09

Ju

l-09

Jan

-10

Ju

l-10

Long Term Government Bond YieldsUnited KingdomUnited StatesEuro Area

7

markets expected to have increased by only 7.2 percent in 2010, compared to a decline of 32 percent in

2009. Much of this rise in FDI is due to an increase in South-South FDI, with the BRIC countries

accounting for 60 percent.

Is India Making Development more Sustainable

through Effective Enforcement of Environmental Compliance?

The challenge of environmental management and regulation is immense, but India has a credible

legislative and policy base to foster environmental sustainability. However, gaps are evident in the

institutional mechanisms for enforcement and compliance, as well as the implementation and

mainstreaming of environmental issues across various sectors of the economy. During recent years, the

Ministry of Environment and Forest (MoEF) has clearly raised the profile of environmental concerns

and inclusive growth in the Government of India‟s development agenda, and Prime Minister Singh

pointed out that disregard of environmental and social issues would lead to “perpetuating poverty”.1

Four recent decisions by the MoEF have made headlines: the cancellation of the “in principle”

environmental clearance provided two years ago to an alumina refinery in Orissa‟s Kalahandi District

and a Bauxite mine in the Niyamgiri Hills, the scrapping of three hydro-electric projects in the

Bhagirathi basin, the withholding of environmental clearance to any other of the hydro-electric projects

planned in the Bhagirathi and Alaknanda basins (tributaries of the Ganges) till the completion of

cumulative impact analyses for the basins, and the stay order on construction of the new city Lavasa in

Maharashtra. There have been determined efforts to bring greater transparency and professionalism to

the granting of environmental and forestry clearances, further facilitated through the Right to

Information Act. New initiatives also aim at addressing institutional and compliance gaps: a National

Environmental Protection Agency (NEPA) will focus on enforcement and monitoring of

environmental laws in the country, and „Green Tribunals„ will rule on environmental disputes of a civil

nature including the provision of compensation for damage to persons and property.

Major boosts to the sustainable development agenda are also expected from linking central grants to

India‟s states to environmental performance. A „Green Index‟ to be developed by the Planning

Commission based on a review of the air and water quality, forest cover, size of national parks, and

climate change gas emissions will rule over the disbursement of around Rs.19 billion (US$400 million)

to the states in FY2010-11.1

The recent legal actions and responses from communities and NGOs are a clear indication that

sustainable development of infrastructure rests on transparency and meaningful participation of all

stakeholders, especially the marginalized sections of society affected by the project. At the same time,

effective implementation and enforcement of the regulatory framework and its underlying provisions is

required to ensure that environmental and social issues do not become a constraint to economic

development.

Contributors: Pyush Dogra and Sonia Chand Sandhu

8

India Outlook

Strong growth is likely to be sustained. GDP growth

for FY2010-11 and FY2011-12 is likely to reach 8.5-9

percent. The high growth of the two last quarters (Q1

and Q2 of FY2010-11) surprised analysts. In

particular, the strong Q2 growth came on the back of a

relatively strong performance in the same period a year

earlier and therefore did not benefit from a positive

„base effect‟. However, growth would still partially be

a rebound from the slowdown in the wake of the global

financial crisis, and could therefore appear somewhat

weaker in subsequent quarters. Slower IIP growth and a

slowdown in imports points into the same direction.

The current account deficit is likely to widen

significantly from the record deficit of FY2009-10.

Initially, imports recovered more strongly than exports

from the slowdown and the “great trade collapse”

during the global financial crisis. Growing services

surpluses and net transfers have compensated for rising

trade deficits in the past. However, the picture now

looks less benign. Extrapolating from the trends in

merchandise trade, services and transfers, the

remainder of the current fiscal year would produce a

current account deficit of around US$40 billion for

FY2010-11, an increase from the record deficit

recorded in FY2009-10.

Capital inflows are expected to continue to be strong

and pose risks in both directions. While FDI held up

well during the global crisis, recent numbers have

disappointed. Portfolio investments are likely to

continue at levels similar to those observed recently,

although volatility could be high. Loans have recovered

strongly and now constitute the biggest item in the

capital account. At current levels of inflows, the capital

account surplus would be sufficient to cover the current

account gap. However, renewed shocks to the global

financial system could quickly change investor

perceptions and lead to another “flight to safety”. The

risk for such shocks occurring is high in light of the

unsettled debt issues in some European countries. On

the other hand, global liquidity remains unusually high

with little prospects for monetary policy tightening in

major developed countries in 2011. High liquidity

could lead to sudden FII surges in emerging markets.

The RBI has demonstrated its ability to react quickly to

short-term capital flows and its reserves remain

sufficient to prevent unwanted volatility of the rupee.

-20.0

-16.0

-12.0

-8.0

-4.0

0.0

4.0

8.0

12.0

16.0

20.0

-20.0

-16.0

-12.0

-8.0

-4.0

0.0

4.0

8.0

12.0

16.0

20.0

20

05

Q4

20

06

Q3

20

07

Q2

200

8Q

1

20

08

Q4

20

09

Q3

201

0Q

2

20

11

Q1

20

11

Q4

20

12

Q3

201

3Q

2

20

14

Q1

20

14

Q4

20

15

Q3

Macroeconomic Indicators

Actual CY2006-10Q2, Forecast CY2010Q2-15

(in %)

Output Gap Y-o-y Inflation Real Interest Rate

Nom. Int. Rate Exchange Rate Gap

Forecast

0.00

5,000.00

10,000.00

15,000.00

20,000.00

25,000.00

30,000.00

35,000.00

40,000.00

45,000.00

Sep

-03

Mar

-04

Sep

-04

Mar

-05

Sep

-05

Mar

-06

Sep

-06

Mar

-07

Sep

-07

Mar

-08

Sep

-08

Mar

-09

Sep

-09

Mar

-10

Sep

-10

Mar

-11

The Current Account Deficit Could Fall Further.(in US$ million)

Merchandise Trade Balance (-)

Services Balance

Net Transfers

Proj.

-10,000.00

-5,000.00

0.00

5,000.00

10,000.00

15,000.00

20,000.00

25,000.00

Sep

-03

Dec

-03

Mar

-04

Jun

-04

Sep

-04

Dec

-04

Mar

-05

Jun

-05

Sep

-05

Dec

-05

Mar

-06

Jun

-06

Sep

-06

Dec

-06

Mar

-07

Jun

-07

Sep

-07

Dec

-07

Mar

-08

Jun

-08

Sep

-08

Dec

-08

Mar

-09

Jun

-09

Sep

-09

Dec

-09

Mar

-10

Jun

-10

Sep

-10

Dec

-10

Mar

-11

Capital Inflows Remained Robust(in US$ millions)

FDI FII Loans

Proj.

Sources: RBI, WB, and author's calculations.

0

5000

10000

15000

20000

25000

30000

35000

Jan

-00

Au

g-00

Mar

-01

Oct

-01

May

-02

Dec

-02

Jul-

03

Feb

-04

Sep

-04

Ap

r-0

5

No

v-05

Jun

-06

Jan

-07

Au

g-07

Mar

-08

Oct

-08

May

-09

Dec

-09

Jul-

10

Feb

-11

Sep

-11

Imports

Exports

Imports and Exports, actual to December 2010, forecasts to October 2011(in US$ millions)

Note: Seasonally adjusted.

Proj.

9

The current and capital account movements make the direction of the rupee hard to forecast. When

the current account deficit was high in the first three quarters of 2010, capital inflows were strong. When

the current account deficit narrowed during the last quarter of the year, portfolio flows reversed. The

result was a relatively stable rupee during much of the year. In the near term, this stability is likely to

hold, while towards the second half of 2011 appreciation pressure is likely to return. Because of the

inflation differential between India and its trading partners, the real effective exchange rate is projected to

appreciate further.

Monetary policy is walking a tightrope between supporting growth and fighting inflation. The RBI

is likely to continue tightening its policy rates in the first two quarters of 2011, although rate increases are

likely to be limited. Real interest rates are currently below historical averages, but falling inflation and

further rate hikes would allow them to normalize in the next few months. With progress in disinflation,

policy rates should peak in the second half of FY2011-12 and then fall, in line with falling inflation. The

environment for monetary policy decisions is highly uncertain. Food inflation is expected to moderate

(see next section) and monetary policy instruments are in any case ill suited to address it. External and

temporary supply shocks are best accommodated, i.e. the central bank should raise rates to prevent real

interest rates from falling but should not raise them aggressively. RBI‟s recent step-wise, cautious rate

hikes seem to have followed this concept. Apart from the inflation indices, other signals about the demand

and supply balance in the Indian economy are mixed: capacity utilization indicators are stable, while the

recent industrial production and imports data point to a slowdown rather than overheating. On the other

hand, credit growth has picked up in December 2010 and January 2011, although it can hardly be seen as

excessive. The signals are therefore mixed as to whether inflation is caused by more general demand

pressures, which would call for more aggressive monetary policy tightening, or by second round effects

of earlier food and commodity price shocks, for which the current policy stance would be adequate.

A Look at Inflation

Global commodity prices have started to rise after a period of some stability in the wake of the

global financial crisis. The last months of 2010 saw a pronounced increase in international prices, in

particular those of food commodities. The increase in U.S. dollar prices is moderated somewhat by the

U.S. dollar depreciation against major currencies, but the trajectory is worrying. Rice prices retreated to

about twice their historic levels from the peak of 3.5 times and have fallen again since March 2010.

Wheat prices declined through June 2010, but have since shot up by more than 60 percent. The supply

and demand balance cannot entirely explain the sudden rise. Disruptions in Russia reduced wheat

production there by 40 percent, but global production is only about 5 percent below last year‟s. This still

leaves it 8 percent higher than in 2008. On the other hand, oil prices recovered to around US$75 per

barrel in early 2009 and have since inched up to $90 per barrel in December 2010. The real price index on

the other hand is fairly stable since October 2009.

While the supply and demand balance does not

present cause for worries, global liquidity remains

exceptionally high, and interest rates in major

economies low – two factors that could contribute

to a renewed speculative commodity price rally.

India’s inflation trajectory is similar to that of

other emerging markets, but India’s level of

inflation is relatively high. Inflation accelerated in

the run-up to the global financial crises, dropped

into negative territory as global commodity prices

collapsed during the crisis, and accelerated again in

early-mid-2010. India‟s inflation was comparable to

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

M1

20

06

M3

20

06

M5

20

06

M7

20

06

M9

20

06

M1

1 2

00

6

M1

20

07

M3

20

07

M5

20

07

M7

20

07

M9

20

07

M1

1 2

00

7

M1

20

08

M3

20

08

M5

20

08

M7

20

08

M9

20

08

M1

1 2

00

8

M1

20

09

M3

20

09

M5

20

09

M7

20

09

M9

20

09

M1

1 2

00

9

M1

20

10

M3

20

10

M5

20

10

M7

20

10

M9

20

10

M1

1 2

01

0WPI Inflation in Major Emerging Market Economies

(y-o-y change in percent)

India Brazil China Thailand Philippines Malaysia Korea

10

that of major Asian EMEs and Brazil in the 2008 rally, dropped less than the mean during the global

crisis, and recovered to somewhat above the mean in 2010. In the chart, Thai inflation is higher than

Indian except in the very end of the year when Brazilian inflation overtakes both. In the group shown

except in Brazil, inflation seems to have passed a peak and dropped in recent months, which is partly a

result of the fading base effect of low prices in 2009.

In India, food inflation is remaining stubbornly high, while core inflation is now also high. Core

inflation is driven by second-round effects of the food price pressure, high commodity prices, and

possibly rising capacity utilization. Core inflation

(non-food, non-fuel) began to accelerate in the early

months of 2010 and reached 8.5 percent in

November 2010, but fell back to 7.5 percent in

January 2011. Support for the argument that this

reflects to some extent second-round effect of the

food price shocks comes from data collected for the

CPI on personal services. These show a significant

increase in non-tradable prices and wages. Higher

core inflation has been cited by the RBI as a

worrying sign that inflation is becoming entrenched.

In fact, long-term inflationary expectations in the

RBI‟s survey data recently shifted upward by 0.5

percentage points. A renewed increase in

international food and energy commodity prices

could also lead to a renewed price spiral in India, similar to what was observed in FY2007-08. Current

projections of the global demand and supply balances for commodities do not point to another price

boom, but the outlook is highly uncertain. WPI inflation is projected to fall to around 7 percent by end-

March 2011, and 4-5 percent by the end of FY2011-12.

A near-normal monsoon should put downward pressure on food prices in India. The monsoon in

India is important, not only for the largely rain-fed kharif (summer) crop, but also for replenishing

reservoirs for the irrigated rabi (winter) crop. The near-normal summer 2010 monsoon is expected to lead

to further easing of price pressures on primary food articles with the upcoming winter harvest, although

transportation disruptions and local flooding led to some renewed price pressures in late August-early

September 2010 and again in November 2010. Production of rice, wheat and pulses is expected to

increase significantly over last year. Wheat production is projected to be 80.7 million metric tons (mt)

while consumption is projected to be 82.4 million mt (USDA). Rice production is projected to increase to

99.0 million mt with consumption projected to be around 98.0 million mt.

The government’s handling of food grain has come under increased pressure. The Food Corporation

of India (FCI) buys food grains from India‟s farmers at prices set by the government (Minimum Support

Prices, MSP) to hold precautionary stocks and release grains to stores to be sold at subsidized prices to

poor households (the public distribution system, PDS). Buffer stocks of wheat and rice held by the FCI

reached 50 million Mt in July as against the norm of 27 million Mt. The simultaneous occurrence of high

food inflation and large food-grain stocks has become a matter of widespread concern.

-15

-10

-5

0

5

10

15

20

25

-15

-10

-5

0

5

10

15

20

25

Jan

-08

Ap

r-0

8

Jul-

08

Oct

-08

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

WPI-AllWPI- CoreWPI - FoodWPI- Energy

Indian Food Inflation is Lingering, Overall Inflation Will Fall Very Slowly...(Components of WPI, y-o-y change, in percent)

Note: Extrapolation of average of past 6 monthly increases.Sources: CSO and authors' calculations.

Forecast

11

III. Real Exchange Rate and Growth

Developments in the exchange rate are at the heart of discussions of economic policies in India

because of the increasing openness of the economy to current and capital account transactions. The

rupee has shown considerable volatility in the last two years – first appreciating strongly against the U.S.

dollar on the back of massive foreign capital inflows in late 2007 – early 2008, then depreciating by more

than 20 percent during the global financial crisis, and now appreciating again since May 2009. There is

therefore a concern that appreciation of the rupee against the U.S. dollar would be detrimental for exports

which, in turn, would be detrimental for growth. This section discusses the rationale and empirical

evidence regarding the link between the exchange rate, exports, and long-run economic growth, as well as

policy implications. This is necessarily a very short summary of a complex subject.

A Perspective on Rising Minimum Support Prices (MSP)

A recent paper studies the relationship between cost of production (CoP), support prices, prices realized and

wholesale prices.1 It argues that the shift in agricultural policy since the 1990s emphasized price intervention over

non-price interventions, which resulted in a decline in the growth rate of yields and a rise in the costs of production.

Support prices were raised repeatedly to sustain the long-run margin over total costs.

Years Rice Wheat

CoP MSP

MSP over

cost (%) CoP MSP

MSP over

cost (%)

2005-06 557.6 600 7.6 541.5 700 29.3

2006-07 569.5 650 14.1 573.6 850 48.2

2007-08 595 775 30.3 624.5 1000 60.1

2008-09 619 930 50.2 648.6 1080 66.5

2009-10 644.9 1030 59.7 741.0 1100 48.4 Note: Cost of production includes transportation, insurance premium and marketing charges.

The MSPs declined in the 1980s in real terms but returns to farming remained adequate because costs of production

fell during the period as productivity improved at more than 2.5 percent per annum. On the other hand, the costs of

production rose at the rate of nearly 1.5 percent per annum in both crops during the 1990s and beyond as yield

growth slowed. MSPs were raised to help farmers maintain their incomes. The authors blame the slowdown in yield

growth on dwindling non-price interventions such as public investments. The second major factor driving higher

support prices is the operation of market forces in a liberal and open trade regime. When the international market

prices are higher and rising as a result of a supply shock, domestic prices of the respective commodity shoot up and

procurement of sufficient quantities to the required levels to ensure food security becomes difficult. Therefore, the

government will have to offer higher prices, as happened in 2007 and 2008 in the case of wheat, making the gross

margin more than 50 percent. The pulls and pressures of democracy and farmer lobbies make it impossible to roll

back these prices, even if global prices recede considerably.

A related influential paper proposes an overhaul of the entire system of government intervention in food production,

procurement and distribution by the FCI.2 In particular, a new set of rules would be needed on when and how to

release food grains from the public stocks to stabilize prices. With the current policy, releasing stocks is hampered

by an attempt to sell grain at prices higher than the procurement prices, which results in low or no off-take when

prices are above market, and stringent controls are imposed on buyers. Grain released through open market

operations by the FCI is sold to millers in bulk, and only rarely to traders. The millers are then prohibited from

onward selling to traders. It is not clear why grain cannot be released in small quantities to large numbers of traders

and millers to allow competition between them to keep prices low.

1 Dev and Rao (2010).

2 Basu (2010).

12

Export-led growth strategies have been credited with the resounding success of several economies,

especially in East Asia in achieving rapid improvements in living standards. In fact, studies show that

nearly all developing countries that experience sustained growth also show an increase in the share of

manufacturing exports in GDP.4 Some economists propose that the production of tradables provides

greater opportunities for productivity increases than the production of non-tradables. Some of the

dynamic effects of tradables are thought to be externalities – learning by doing, investment in search for

opportunities which are then available to everyone – and a market-based equilibrium would leave

production below the social optimum. Another argument is that the size of the domestic market in poorer

countries is not sufficient to provide the employment opportunities needed to absorb the surplus labor.

There are indications that at least some of the fast-growing countries relied, and still rely, on measures

aimed at undervaluing the real exchange rate to reduce the consumption of tradables but improve the

profitability of their production for exports.5 Undervaluation means that non-tradables are somehow made

cheaper relative to tradables than what they would be without policy intervention, which allows

consumption to switch to non-tradables while the production of tradables for export receives a boost.6

Some cross-country studies support the view that the level of the real exchange rate is correlated

with economic growth but the direction of causality is hotly debated.7 It is very difficult to

disentangle the direct effects on growth of policies that also move the real exchange rate from the effects

on growth of the exchange rate itself. For example, the policies that lead to and maintain overvaluation –

rationing of foreign exchange, foreign exchange controls – have direct effects on investment in the

tradables sector, which are possibly more damaging than the loss of competitiveness of the tradables

sector from overvaluation. Those who see a causal link between undervaluation and growth argue that

undervaluation is needed because (potential) producers of tradables suffer disproportionately from the

institutional weaknesses and market failures that characterize low-income countries. Undervaluation is

akin to a blanket subsidy aimed at helping tradables to overcome these barriers. Critics argue that the

studies used to support the undervaluation-high growth causal chain suffer from omitted variables. For

example, an increase in domestic savings and investment simultaneously depreciates the real exchange

rate and boosts growth.8

The evidence for the existence of externalities and spillovers from exports is mixed. There are several

studies which support the thesis that increasing the share of manufacturing exports is good for growth.9

The evidence on positive spillovers from exporting, however, is less than conclusive. A number of studies

report that proximity to other exporting firms increases the likelihood that a subject firm will itself

4 Johnson, Ostry and Subramaniam (2007). 5 See for example Krueger, A.O. (1998). Real exchange rate undervaluation was not the only enabling factor: abundant cheap

labor, subsidized credit, energy, infrastructure, supportive tax and tariff rates are also described in the literature. 6 Non-tradables in low-income countries are necessarily cheaper than in high-income countries, and real exchange rates therefore

appreciate when countries grow richer – so so-called Balassa-Samuelson effect. The focus here is on lowering the relative price

of non-tradables beyond what the market would produce. 7 Rodrik (2008) and Haddad and Pancaro (2010). The latter shows that the effect seems to fade over time and may actually

reverse – i.e., undervaluation may be detrimental to growth in the long run. Real exchange-rate volatility is detrimental to growth

and the difficulties in maintaining real exchange-rate undervaluation over time may lead to volatility which could explain the

long-run reversal of its effects on growth. Eichengreen (2008) is another proponent, while Woodford (2009) provides a strong

critique of Rodrik‟s methodology and argumentation. 8 Bernanke (2005) argues that while a relationship between depreciated real exchange rate and high savings rate exists the

causality goes from a depreciated real exchange rate to a high saving rate to a high growth rate driven by capital accumulation.

Montiel and Serven (2008) find that exchange rate policy in general, or a depreciated real exchange rate has not been identified as

an important factor in explaining differences in savings rate. Even in the high saving, high-growth countries key determinants of

saving rates have been identified as demographics, financial sector policies, mandated saving schemes, and fiscal policies, rather

than exchange rate policies. 9 Jones and Olken (2005) find significant reallocation of resources toward manufacturing during growth upturns. Johnson et al.

(2007) find that nearly all developing countries that experience sustained growth also witness a rapid increase in their shares of

manufacturing exports. Similarly, Rodrik (2006) argues that rapidly growing developing countries tend to have unusually large

manufacturing sectors and that growth accelerations are associated with structural shifts in the direction of manufacturing.

13

export.10

However, there are other studies showing that the tendency of firms to export is not affected by

their proximity to other exporters.11

Fairly robust evidence shows that there is indeed a productivity

differential between exporters and domestic firms.12

However, there do not seem to be any learning-by-

doing effects from exporting. Rather, firms self-select into exports, i.e. they go into export markets after

they have somehow managed to establish a productivity premium. The empirical evidence therefore does

not show greater dynamism for improving TFP in exports relative to home production.

India’s Exchange Rate Management

Nominal and real exchange rate indices show that

India maintained a fair degree of stability

throughout the liberalization period after 1991. The nominal effective exchange rate depreciated by

about 10 percent in the early 1990s and stabilized

thereafter, until it experienced a pronounced

appreciation during the capital inflow boom in 2007.

The real effective exchange rate, calculated by RBI

on the basis of trade weights, also showed a

depreciating trend in the 1990s, but returned to the

1993 level in the 2000s. Exchange rate volatility

increased markedly from 2007 as the RBI intervened

less in foreign exchange markets. The capital inflow

boom brought appreciation in 2007, which was followed by a significant depreciation in the wake of the

global financial crisis. In the aftermath of the crisis, both the nominal and the real exchange rate bounced

back strongly but in October 2010, the real exchange rate index reached 99.7, which was well below the

peak it had reached in 2007.

While it is common to observe the rate of change of the real exchange rate, indirect methods are

needed to evaluate its level. Economists compare the developments of domestic and foreign prices

(converted at market exchange rates).13

The resulting index numbers give an indication of the change in

the real exchange rate over time, but they do not in themselves enable us to judge whether the real

exchange rate is over- or undervalued. A methodology used to judge the level of the real exchange rate

rather than its direction of change involves estimating whether or not the economy is in external and

internal equilibrium. This Equilibrium Method is used by the IMF‟s Consultative Group on Exchange

Rate issues (CGER).14

The IMF judges the Indian rupee to be fairly valued relative to different concepts

of medium-term equilibrium. Another method compares market exchange rates with purchasing power

parity exchange rates (the PPP method used by Rodrik and others). The difficulty in using this

methodology is to make an appropriate adjustment for the fact that the relative price of non-tradable

goods is higher in countries with higher income per capita (the Balassa-Samuelson effect).15

10 Lin (2004) finds that the propensity for Taiwanese firms to export is positively affected by the propensity to export of other

firms in the same industry in its geographic vicinity. Koenig (2005) reports similar results for a sample of French firms, while

Alvarez and Lopez (2006) report evidence of horizontal productivity spillovers from exporting for a sample of Chilean firms. 11 Aitken et al. (1997), Barrios et al. (2003), Bernard and Jensen (2004), and Lawless (2005). 12 International Study Group on Exports and Productivity (2008). 13

The rationale is that tradable prices are determined in the international market while non-tradable prices are determined in the

domestic market. Comparing price indices between two or more countries therefore is a proxy for the real exchange rate as long

as the „law of one price‟ holds, i.e. tradables cost the same (adjusted for transport and other costs) in different countries. 14

IMF (2006). 15 The undervaluation index (UNDERVAL) is computed as the residual of a regression of the real exchange rate (RER) on real

GDP per capita (RGDPCH), where RERit is defined as the ratio between the nominal exchange rate (XRAT) and the purchasing

6065707580859095

100105110

Ap

r-9

3

Jul-

94

Oct

-95

Jan

-97

Ap

r-9

8

Jul-

99

Oct

-00

Jan

-02

Ap

r-0

3

Jul-

04

Oct

-05

Jan

-07

Ap

r-0

8

Jul-

09

Oct

-10

REER

NEER

Real and Nominal Exchange Rate Indices(1993=100)

14

India’s current account and fiscal deficits are not pointing to undervaluation of the exchange rate. India has never been able to achieve a trade surplus and the current account has recorded a deficit during

most years post independence. The current account deficit hovered around 2 percent of GDP during much

of the 1970s and 1980s, and improved after the balance of payments crisis in 1991 to reach a brief surplus

of 2 percent in 2003. Since then, the current account has deteriorated again to probably reach a deficit of

3.5 percent of GDP in FY2010-11. Large inflows of remittances mask the widening trade deficit,

especially in recent years. More recently, imports actually grew faster than exports. The trade deficit

reached a record 6 percent of GDP in FY2008-09 and narrowed a little in FY2009-10, but is again

widening in FY2010-11. In fact, trade made a negative contribution to growth in a national accounting

sense in most years of the 2000s. India‟s government accounts were also in deficit over recent decades, a

situation usually associated with exchange rate overvaluation. In fact, India‟s fast growth, particularly in

the 2000s, seems to have been fueled by a growing domestic market with imports of capital and consumer

goods financed to a large degree by remittances and foreign savings.

India’s Trade and Domestic Production

India may differ from other emerging markets because of its size. If the domestic market is

sufficiently attractive, domestic entrepreneurs and foreign investors set up sophisticated production

capacity for the domestic market, rather than for export. They compete with imported products, thereby

importing skills and technologies. The car industry is an interesting example of capacity being created to

compete with imports, and learning-by-doing improvements in productivity that eventually produce an

exportable surplus.

There is–admittedly weak–evidence that home production in India is as ‘sophisticated’ as exports. This result is obtained by comparing the share of

„sophisticated‟ goods in exports, as shown in UN trade

statistics, with their share in domestic production, as

shown in India‟s Annual Survey of Industry (ASI).16

Import data show the competitiveness of India’s

human capital and the increasing use of technology-

intensive goods in production, but unskilled labor is

falling behind. Over the last four decades, the share of

human capital-intensive goods in imports has fallen,

while the share of technology-intensive imports has risen

significantly. Somewhat surprisingly, the share of

unskilled labor-intensive imports has also risen strongly.

This indicates that India‟s unskilled labor-intensive

products have lost international competitiveness,

power parity (PPP) conversion factor for country i at time t. RER equal to 1 implies that the nominal exchange rate provides the

same price level as in the USA.

ittitit fRGDPCHRER lnln (1)

ititit RERRERUNDERVAL ˆlnlnln (2)

The regression in equation (1) includes time-fixed effects, denoted as ft . Rodrick‟s paper shows that India‟s real exchange rate

was mildly overvalued in the early decades after independence, when India was pursuing import substitution policies, but

significant devaluation took place after the mid-1970s. In the mid-2000s, the real exchange rate was undervalued by about 60

percent according to this measure, which means that a U.S. dollar would buy 60 percent more in India than in the average country

of the rest of the world. Woodford (2009), however, strongly criticizes the methodology used by Rodrik. In particular, he

discounts Rodrik‟s purported adjustment for the Balassa-Samuelson effect and proposes to compare PPP exchange rates directly.

For India, the unadjusted ratio of PPP over market exchange rates indicates an undervaluation of 466 percent in the five-year

period 2003-07. See Heston et al. (2009) for PPP exchange rates (version 6.3). 16 World Bank (2010a) for a more detailed description. The analysis is based on a methodology used by Krause (1987).

Factor Intensities of Exports, Imports, and Domestic Production

(in share of total)

Shares by Factor Intensity

Year

Natural

Resources

Unskilled

Labor

Human

Capital

Intensive

Technology

Intensive

2006-08 50.4 10.9 18.9 19.8

1996-2000 44.4 22.2 17.1 16.3

1986-90 56.9 19.1 11.5 12.4

1976-80 55.8 20.3 15.9 8.0

1966-70 49.8 36.8 9.8 3.6

2006-08 40.7 5.0 13.6 40.7

1996-2000 48.2 4.1 11.8 35.9

1986-90 47.1 2.7 13.5 36.6

1976-80 46.3 1.1 16.1 36.5

1966-70 30.5 1.2 20.7 47.7

2008 49.6 9.0 25.3 16.0

2004 47.1 9.8 25.9 17.2Domestic Production

Sources : UN Comtrade and Centra l Statis tics Office, Annual Survey of Industry.

Exports

Imports

15

although India is still far from converting surplus unskilled agricultural labor into more productive

employment. This loss of competitiveness would also explain some of the decline in unskilled labor-

intensive exports.

How Could Policies Aim at Boosting the Competitiveness of Exports?

Policies aimed at boosting the production of tradables and exports would aim at changing the level

of the real exchange rate. The central bank can influence the nominal and with it also the real exchange

rate at least in the short term. It is not clear, however, how this will affect the real exchange rate over a

longer time frame: unsterilized intervention can lead to inflation if the domestic money supply rises faster

than money demand, which may not be the case in a fast growing economy with financial deepening. If

inflation results, however, the price ratio of non-tradables over tradables increases and therefore the real

exchange rate appreciates into the direction of the level it held before the nominal devaluation. Sterilized

intervention on the other hand increases interest rates which in turn risks leading to more capital inflow

and appreciation of the nominal rate as suggested by interest parity models of the exchange rate.

Lasting real devaluation can be achieved through a surplus of savings over investment, or

structural reforms. Lower aggregate demand depresses the prices of non-tradables while the prices of

tradables remain unchanged because they are determined internationally. A real exchange rate

undervaluation therefore can be brought about through a contraction of aggregate demand relative to

supply, which results in an increase of savings over investment. Fiscal contraction or an increase in public

savings together with an increase in private savings can do the trick. If household savings are not high and

cannot be increased, targeting a decline in real wages can increase profits and corporate savings. Both

these options are politically very difficult and may be incompatible with social objectives. The price of

non-tradables can also be targeted directly, rather than through aggregate demand: lowering the costs of

doing business (red tape, infrastructure) lowers the prices of non-tradables and increases the profitability

of producing tradables. A surplus of savings over investment implies a trade surplus, which means a

strategy of real exchange rate undervaluation to promote growth can only succeed if there is an elastic

market for the country‟s surplus production of ‟sophisticated‟ products.

In conclusion, the most promising avenue for India to promote exports and growth more generally

would be structural reforms and investment in infrastructure to reduce the costs of doing business

and increase competitiveness. Lowering the costs of doing business as a way to lower the costs of non-

tradables and improve the competitiveness of tradables would boost growth by making the production of

sophisticated goods for exports more profitable for domestic firms. At the same time, the RBI‟s approach

to the management of the nominal exchange rate provides the enabling environment for businesses to plan

0

10

20

30

40

50

60

70

80

90

100

19

66

19

68

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

Technology Human Capital Unskilled Lab. Natural Res.

Relative Factor Intensities in Exports(Shares in percent)

Source: UN Comtrade.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

Technology Human Cap. Unskilled Lab. Natural Res.

Relative Factor Intensities in Imports(Shares in percent)

16

ahead: a market-based approach safeguarding against volatility associated with short-term capital flows

and some „leaning against the wind‟ to avoid undue appreciation.

IV. Education and Long-term Growth17

One of the variables influencing India’s long-term prospects is the education of its young and

growing population. Mean years of schooling for the population ages 15 and above increased from

around 3.5 in 1990 to 5.1 in 2010. Notwithstanding this obvious progress, overall schooling has been

relatively low especially compared with some fast growing Asian countries. In addition to relatively low

levels of schooling, India has high educational inequality between sexes. Mean years of schooling for

women is roughly 4, while the male population has over 6 years of education on average in 2010.

Interactions between education and most dimensions of development have been documented.18

For

example, fundamental components of demography (fertility, mortality, and migration) are strongly

affected by education. Using a new database combining information on years of schooling, age and

gender characteristics of the population of 120 countries around the world, we show the impact of various

scenarios for future educational expansion on India‟s per capita income. The difference between a

„business-as-usual‟ (slow) educational expansion, and a major push to achieve Korea‟s 2000 enrolment

levels in India by 2040 can be substantial: based on a production function cross-country regression, we

estimate that per capita incomes in India could be 16 percent higher in the Korea scenario compared with

„business-as-usual‟.

The Database: Educational Attainment for Age Cohorts

A new database documents educational attainment around the world. Using the demographic method

of multistate back projection, a group of researchers at the International Institute for Applied Systems

Analysis (IIASA) and the Vienna Institute of

Demography (VID) has recently completed a full

reconstruction of educational attainment

distributions by age and sex for 120 countries for

the years 1970–2000.19

Taking into account the

interactions between education, demography, and

development the database also provides

projections of population pyramids forward to

2050 for these countries. The age and education

composition details in this database also allow for

statistical analyses of the relation between

education and economic growth. Using this

database, a significant relation has been found

contradicting previous cross-country economic

growth regressions, which – in contradiction to

theory and microeconometric evidence – tended to show that changes in educational attainment are

largely unrelated to economic growth.20

Based on this work, we first show the distribution of educational attainment levels across age

groups and sexes for India.21

The projections are based on the assumption that educational attainment in

17

This section is based on a background paper provided by Jesus Crespo Cuaresma of Vienna University of Economics and

Business. 18 Sen (1999), Collier and Hoeffler (2000). 19 Lutz et al. (2007). 20 J. Benhabib, M. Spiegel, J. Monet. Econ. 34, 143 (1994), and L. Pritchett, World Bank Econ. Rev. 15, 367 (2001).

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1970 1980 1990 2000 2010 2020 2030 2040 2050

No Education Primary Secondary Tertiary

Indian Population by Educational Attainment(Population 15 years and older, 1970-2010 and projections for 2010-2050)

17

India will follow the average global enrolment trend (GET) in the next thirty years (one of the scenarios

described in more detail below). The proportion of individuals aged 15-19 with some secondary schooling

in 1990 was about 37 percent, which rose to over 51 percent in 2000.

Total fertility rates in India and elsewhere are strongly influenced by improvements in education. In line with the expansion of education described above, we expect a decrease in children per woman

from 2.76 in 2005-2010 to 1.85 in 2040.22

These changes bring about a slowdown in the trend of

population growth and dramatic changes in the age structure of the Indian population: a strong decrease in

the youth dependency ratio and a potentially sizable demographic dividend in the coming decades.

21 The projections are based on the methods described in KC et al. (2010). They assume that the attainment dynamics in India

will follow the pattern observed in a global panel of historical data. In particular, the global panel is used to provide gender-

specific and attainment level-specific convergence trends to universal attainment levels. These trends are modeled using cubic

splines and the estimated specifications are used to create projections for India. It should be noted that this model uses the

average speed of convergence to universal attainment and as such is reasonably realistic, but not particularly optimistic: it takes

approximately 40 years to raise female participation in primary schooling from 50% to 90%, and 30 years more to reach 99%.