india chindia chindiafrica - touteconomie · 2000/01* 2001/02* 2002/03* 2003/04* 2004/05 2005/06...

TRANSCRIPT

ChIndiAfrica - © J.J. Boillot 1

IndiaChindia

Chindiafrica

Jean-Joseph Boillot� Economist, club CEPII - EIEBG

ChIndiAfrica - © J.J. Boillot 2

I- The End of Shinning India?1- The 3 scenarios of 2006

0

2

4

6

8

10

12

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

%

Bolly World Pahale India Atakta Bharat

3 stylized Scenarios for India 2025*

* from WEF-CII 2006

ChIndiAfrica - © J.J. Boillot 3

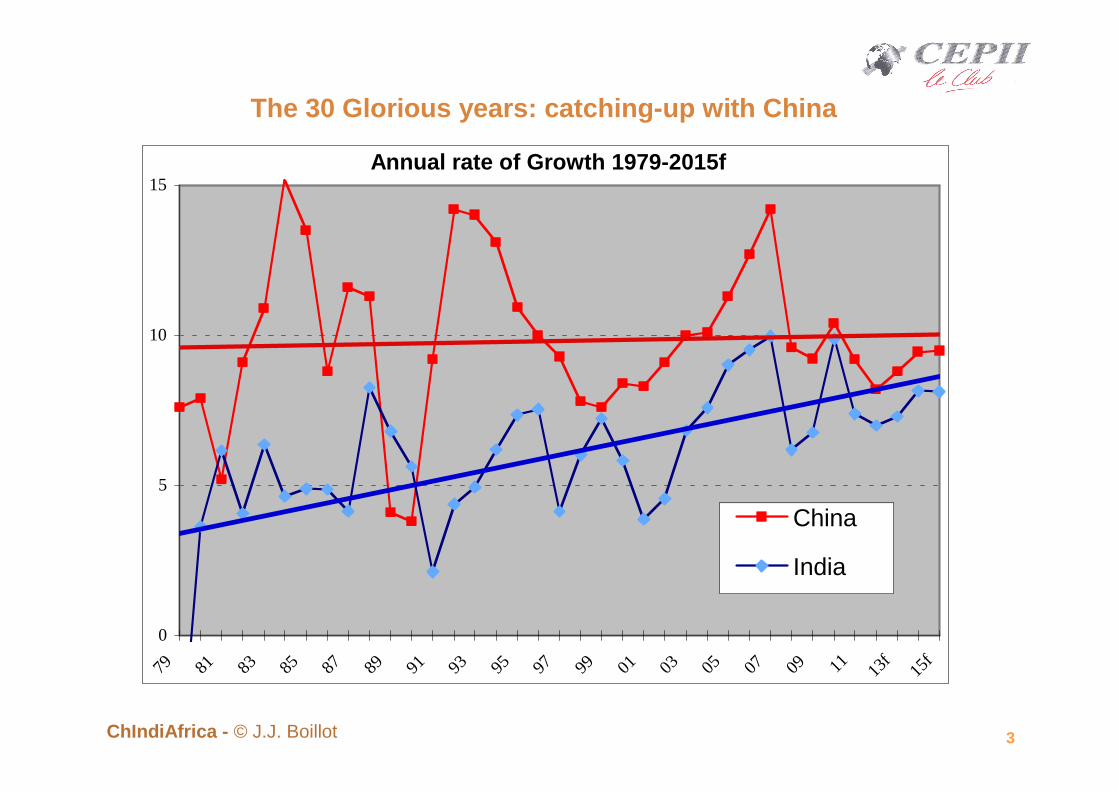

The 30 Glorious years: catching-up with China

Annual rate of Growth 1979-2015f

0

5

10

15

79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13f

15f

China

India

ChIndiAfrica - © J.J. Boillot 4

The driving forces of Growth: domestic…

0

10

20

30

40

50

60

7020

00/0

1*

2001

/02*

2002

/03*

2003

/04*

2004

/05

2005

/06

2006

/07

2007

/08

2008

/09

2009

/10

2010

/11e

2011

/12e

st

Conso priv Conso Pub Invest Saving

GDP distribution (%)

ChIndiAfrica - © J.J. Boillot 5

… and external

0

20

40

60

80

100

120

2004

/05

2005

/06

2006

/07

2007

/08

2008

/09

2009

/10

2010

/11e

2011

/12p

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

7,0%

8,0%

9,0%

10,0%

Capital Financing bnUSD % GDP

ChIndiAfrica - © J.J. Boillot 6

2- Structural crisis or Cyclical turnaroundWorld cycle and the (de)coupling issue

GDP/PIB 1980-2011e

-5

0

5

10

15

20

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10

taux

de

croi

ssan

ce %

USA China India

ChIndiAfrica - © J.J. Boillot 7

Agriculture: stagnation vs Income per capita Growth

Agriculture and GDP

-2,0%

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11e 2011-12p 2012-13p

%

GDP Agriculture

ChIndiAfrica - © J.J. Boillot 8

Mass poverty still prevalent (unicef 2012)

Malnutrition is more common in India than in Sub-Saharan Africa. One in every three malnourished children in the world lives in India.

Malnutrition limits development and the capacity to learn. It also costs lives: about 50 per cent of all childhood deaths are attributed to malnutrition.

In India, around 46 per cent of all children below the age of three are too small for their age, 47 per cent are underweight and at least 16 per cent are wasted. Many of these children are severely malnourished.

The prevalence of malnutrition varies across states, with Madhya Pradesh recording the highest rate (55 per cent) and Kerala among the lowest (27 per cent).

ChIndiAfrica - © J.J. Boillot 9

And growing Inequalities

6

1310

18

1413

25

2119

37

4853

7 7

9

0%

20%

40%

60%

80%

100%

1993-94 2004-05 2009-10

Q5 (Top)

Q4

Q3

Q2

Q1 (Bottom)

ChIndiAfrica - © J.J. Boillot 10

II- Scenario for the future: 2012-2020The Inclusive Growth Regime at stake

ChIndiAfrica - © J.J. Boillot 11

A- Rising Regionalism: political crisis & “Atakta India”1- Political factors

�Les vert-bleu

�Contre les Safran

�Et les Rouge

ChIndiAfrica - © J.J. Boillot 12

2- Regional inequalities and the political factor The demographic shift

P r o je c t io n d ˇ m o g r a p h iq u e d e s E t a t s In d ie n s * e n 2 0 5 1 e t 2 1 0 1S ta te s M illio n s % a ll In d iaS ta te s 1 9 9 1 2 0 5 1 2 1 0 1 1 9 9 1 2 0 5 1 2 1 0 1

K e r a la 2 9 ,1 3 6 2 5 ,2 3 ,5 % 2 ,2 % 1 ,4 %T a m il N a d u 5 5 ,9 7 2 5 7 6 ,6 % 4 ,4 % 3 ,1 %A n d h ra P ra d e s h 6 6 ,5 1 1 9 ,9 1 3 0 ,5 7 ,9 % 7 ,4 % 7 ,2 %

H im a c h a l P ra d e s h 5 ,2 9 ,5 1 0 ,3 0 ,6 % 0 ,6 % 0 ,6 %K a r n a ta k a 4 5 7 8 8 5 5 ,3 % 4 ,8 % 4 ,7 %

M a h ra s tra 7 8 ,9 1 4 7 ,4 1 5 9 ,6 9 ,4 % 9 ,1 % 8 ,8 %S u b to ta l 2 8 0 ,6 4 6 2 ,8 4 6 7 ,6 3 3 ,3 % 2 8 ,6 % 2 5 ,8 %

P u n ja b 2 0 ,3 3 5 ,7 3 7 ,9 2 ,4 % 2 ,2 % 2 ,1 %W e s t B e n g a l 6 8 ,1 1 2 1 ,9 1 3 2 8 ,1 % 7 ,5 % 7 ,3 %

G u ja ra t 4 1 ,3 7 3 8 0 ,2 4 ,9 % 4 ,5 % 4 ,4 %O r is s a 3 1 ,7 5 3 ,9 5 9 ,5 3 ,8 % 3 ,3 % 3 ,3 %

A s s a m 2 2 ,4 4 2 4 7 2 ,7 % 2 ,6 % 2 ,6 %S u b to ta l 1 8 3 ,8 3 2 6 ,5 3 5 6 ,6 2 1 ,8 % 2 0 ,2 % 1 9 ,7 %

H a ry a n a 1 6 ,5 4 1 ,1 4 8 ,8 2 ,0 % 2 ,5 % 2 ,7 %M a d h y a P ra d e s h 6 6 ,2 1 4 8 1 7 5 ,3 7 ,9 % 9 ,1 % 9 ,7 %

B ih a r 8 6 ,4 1 8 8 2 1 6 ,7 1 0 ,2 % 1 1 ,6 % 1 2 ,0 %R a ja s th a n 4 4 1 0 6 ,1 1 2 5 ,9 5 ,2 % 6 ,6 % 6 ,9 %

U tta r P ra d e s h 1 3 9 ,1 3 3 7 4 0 5 1 6 ,5 % 2 0 ,8 % 2 2 ,3 %S u b to ta l 3 5 2 ,2 8 2 0 ,2 9 7 1 ,7 4 1 ,8 % 5 0 ,6 % 5 3 ,6 %

A ll In d ia 8 4 3 ,3 1 6 1 9 ,5 1 8 1 2 ,2 1 0 0 ,0 % 1 0 0 ,0 % 1 0 0 ,0 %

ChIndiAfrica - © J.J. Boillot 13

One indicator of inequality : Life Expectancy

Source : National Human Development Report 2001, Pl anning Commission/ Inde Etats données+travail /2026

INDIA 60,7

1 Kerala 73,1

2 Punjab 67,4

3 Maharastra 65,2

4 Haryana 63,8

5 Tamil Nadu 63,7

6 Karnataka 62,9

7 West Bengal 62,4

8 Andhra Pradesh 62

9 Gujarat 61,4

10 Rajasthan 59,5

11 Bihar 59,4

12 Uttar Pradesh 57,2

13 Orissa 56,9

14 Assam 56,2

15 Madhya Pradesh 55,2

ChIndiAfrica - © J.J. Boillot 14

The Fertile crescent of the “Shinning India” decade…

ChIndiAfrica - © J.J. Boillot 15

… and the Political economy of Regionalism

Relation GDP per capital and Growth 2004- y = 0,2793x + 2,0859

R2 = 0,1806

100%

150%

200%

250%

300%

350%

0% 50% 100% 150% 200% 250% 300%

PIB/h India=100

ChIndiAfrica - © J.J. Boillot 16

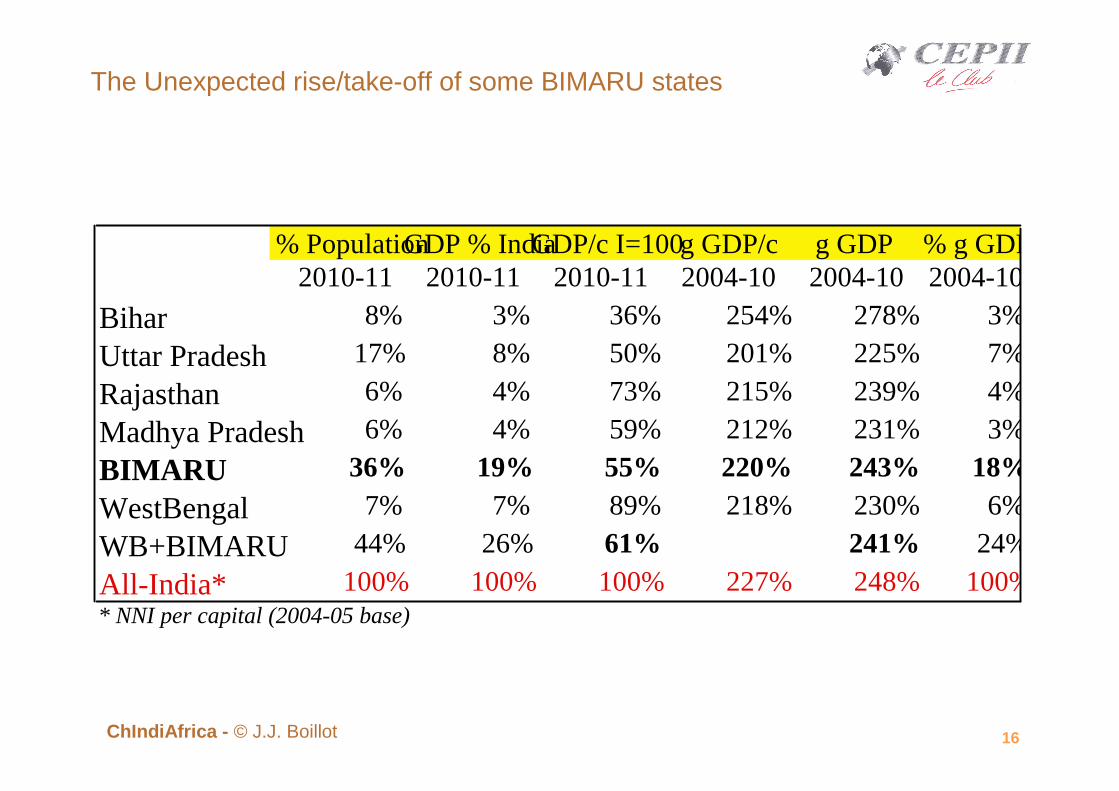

The Unexpected rise/take-off of some BIMARU states

% PopulationGDP % IndiaGDP/c I=100g GDP/c g GDP% g GDP2010-11 2010-11 2010-11 2004-10 2004-102004-10

Bihar 8% 3% 36% 254% 278% 3%

Uttar Pradesh 17% 8% 50% 201% 225% 7%

Rajasthan 6% 4% 73% 215% 239% 4%

Madhya Pradesh 6% 4% 59% 212% 231% 3%

BIMARU 36% 19% 55% 220% 243% 18%

WestBengal 7% 7% 89% 218% 230% 6%

WB+BIMARU 44% 26% 61% 241% 24%

All-India* 100% 100% 100% 227% 248% 100%* NNI per capital (2004-05 base)

ChIndiAfrica - © J.J. Boillot 17

B- The Inclusive Business Models1- The strengh of the Indian Business Culture

rang Sociˇtˇs Rˇgion d'origine

Communautˇ

1 RELIANCE INDUSTRIES (1) Gujarat Vaishnava gujarati3 TATA Gujarat (Iran) Parsi4 BHARTI TELE-VENTURES Punjab Baniya punjabi6 INFOSYS TECHNOLOGIES Tamil Nadu Brahmane Iyer/Iyengar7 WIPRO Gujarat Bora (musulman)8 AV Birla Rajasthan Baniya marwari13 RANBAXY LABORATORIES Punjab Shatriya sikh15 HCL TECHNOLOGIES Tamil Nadu Nadar16 BAJAJ Auto Rajasthan Baniya marwari24 LARSEN & TOUBRO Maharastra Brahmane marathi25 SATYAM COMPUTER SERVICES Tamil Nadu Brahmane Iyer/Iyengar27 HERO HONDA MOTORS Punjab Baniya punjabi29 United Breweries (UB) Karnataka Brahmane Chetia Naga30 CIPLA Gujarat Bora (musulman)31 SUN PHARMACEUTICAL INDS. Rajasthan Baniya marwari32 LM THAPAR Punjab Shatriya punjabi34 NICHOLAS PIRAMAL INDIA Rajasthan Baniya marwari

35 DR. REDDY'S LABORATORIES Andhra Pradesh Brahmanes

36 ASIAN PAINTS (INDIA Gujarat Choksi gujarati37 WOCKHARDT Gujarat Bora (musulman)38 Murugappa Tamil Nadu Chettiar39 ZEE TELEFILMS Rajasthan Baniya marwari40 ESSAR Rajasthan Ruia marwari42 GUJARAT AMBUJA CEMENTS Rajasthan Baniya marwari43 BIOCON Gujarat Gujarati44 jaiPrakash Maharastra Baniya mahrati45 Jindal Rajasthan Marwari46 BK BIRLA Rajasthan Baniya marwari47 Wadia Gujarat (Iran) Parsi48 Godrej Consumers products Gujarat (Iran) Parsi49 VSNL (VIDESH SANCHAR NIGAM) Gujarat (Iran) Parsi50 RP GONEKA Rajasthan Jain marwari

ChIndiAfrica - © J.J. Boillot 18

Managerial excellence, a key assetclassement des 25 meilleurs CEO 2012

1 Naveen Jindal JSPL steel & power2 A.M.Naik Larsen & Toubro3 Y.C. Deveshwar ITC4 Bhaskar Bhat TITAN5 Sunil Mittal Bharti6 R. Sridhar Shriram Capital7 Mukesh Ambani Reliance Industries8 Vijay Jindal Zee Entertainment Enterprises9 Pankaj R. Patel Cadila Healthcare10 Pangal Jayendra Nayak Axis Bank11 Subir Raha ONGC Oil & Natural Gas Corporation12 Kalyan Ganguly United Breweries President UB Group13 Madhukar B. Parekh Pidilite Industries14 Sunil Duggal Dabur India15 V.K. Rekhi United Spirits UB group16 V.S. Jain Steel Authority of India17 Prakash Kulkarni Thermax18 L.A. Dean Sesa Goa19 A.K. Puri Bharat Heavy Electricals BHEL20 Ashok Soni Voltas21 B. Muthuraman Tata Steel22 S.S. Kohli Punjab National Bank23 Anand Mahindra Mahindra & Mahindra24 R. Seshasayee Ashok Leyland25 Kamal K. Sharma Lupin

ChIndiAfrica - © J.J. Boillot 19

FDI in and outbound

Why Indian firms invest abroad? Dual explanation

0,0

10,0

20,0

30,0

40,0

50,0

60,0

2004

/05

2005

/06

2006

/07

2007

/08

2008

/09

2009

/10

2010

/11

2011

/12e

2012

/13f

Inbound FDI

Outbound FDI

ChIndiAfrica - © J.J. Boillot 20

True challenge: Nano Capitalism & Emergence of new bu siness Models(a) The « Reverse Innovation »

1) Vijay Govindarajan*, and the concept of "Reverse innovation", overtaking the « glocalisation » model of post-fordist capitalism.

* The product and process innovation took essentially its source in the advanced economies, then adapted locally;

* this time, innovation starts at the local level, and at first in the emerging countries especially China and India with processes and products adapted to their constraints (resources & incomes) and abundances (labor & consumers).

*Read in the Harvard Review of Management 2009 his article co-signed by the

CEO of GE himself, Jeffrey R. Immelt.

ChIndiAfrica - © J.J. Boillot 21

(b) The « Bottom of the Pyramid » market target

2) C.K. Prahalad, from the university of Michigan, with his concept of " base of the pyramid " (BoP or Bottom of the Pyramid), aims at the 4-5 billion human beings living with less than 2 dollars a day.

*A Whole range of products, including housing & infrastructures (water or electricity) are emerging under the push of new innovations and retain more and more the attention of international agencies as the World Bank or UNDP.

* Due to its consumption-led-growth and democratic structure, India looms more incline to the BoP approach than China who has followed the typical set of western patterns due to its export-led-growth including inequalities.

ChIndiAfrica - © J.J. Boillot 22

(c) The « Jugaad Innovation » experience

3) Navi Radjou, Jaideep Prabhu and Simone Ahuja in their book « Jugaad Innovation » have theorised the experiences of many entrepreneurs from India and other developping countries.

* Seek opportunity in adversity* Do more with less (frugality)* Think and Act flexibily

• * Keep it simple• * Include the margin

* Follow your Heart

ChIndiAfrica - © J.J. Boillot 23

Will India succeed in the modernisation of its business culture: the « Indian Way of Management » versus the old bania predatory culture?

1- PRINCIPLES1) Managing People: holistic engagement of employees- the

« Employee First » of Vineet Nayar (HCL);2) Leading the Entreprise: improvisation and adaptability (jugaad)3) Competitive Advantage: delivering the Creative Value

Proposition (Infosys/Wipro)4) Company Governance: fulfilling broad mission and purpose

2- INNOVATIONS1) Scaling-Out : the Bharti paradigm (mobile phone Airtel);2) Frugal Innovations: the GM ECG or Tata water filter;3) Inclusive innovation: the Microfinance paradigm (SHGs);4) Opportunistic solutions : the Tulsi Tanti strategic shift in

Windpower

ChIndiAfrica - © J.J. Boillot 24

III- Neither China, nor Chindia but ChindiafricaThe demographic trends

Evolution de la population du monde par grandes rˇg ions 1950-2050

0,0

0,5

1,0

1,5

2,0

2,5

1950

1960

1970

1980

1990

2000

2010

2020

2030

2040

2050

Millions

en m

illia

rd

Afrique

Inde

Chine

ASudhors Inde

ASud-est

A. Latine

Europe

Am.Nord 0

50

100

150

200

250

300

350

400

1950

1960

1970

1980

1990

2000

2010

2020

2030

2040

2050

USA Europe Inde Chine Afrique

ChIndiAfrica - © J.J. Boillot 25

The Demographic window of opportunity

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

54 57 60 63 66 69 72 75 78 81 84 87 90 93 96 99 02 05 08 11

40,0

45,0

50,0

55,0

60,0

65,0

70,0

75,0

80,0

Transition dˇmographique (% Pop active-ech droite) et Dˇcollage ˇconomique (croissance- ˇch gauche)

Chine

Inde

Afrique

ChIndiAfrica - © J.J. Boillot 26

And the shifting Human Capital

0%

10%

20%

30%

40%

50%

60%

70%

1980 2010 2030 2050

AFRIQUE

INDE

CHINE

EU

USA

4

6

8

10

12

14

16

2010 2020 2030 2040 2050

US

Ch

In

LA

Nafr

Afr

ChIndiAfrica - © J.J. Boillot 27

Towards a Multipolar World with three giants

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1980 2010 2020 2030 2040 2050

Ru

EU

TotAFR

India

China

Jap

LA

Bz

US

Share World GDP current USD %

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1980 2010 2020 2030 2040 2050

Ru

EU

TotAFR

India

China

Jap

LA

Bz

US

Share World GDP USD PPP %

ChIndiAfrica - © J.J. Boillot 28

And the same challenge: Sustainability

ChIndiAfrica - © J.J. Boillot 29

One example of the CIA triangle:Technologies and Business Models

Mapping of Country Capability Rating to Top 16 Technology Applications

Needed Capability Technology Applications

Low Cheap solar energy

lagging Rural wireless communications

(South Africa…) GM crops

Filters and catalysts

Cheap autonomous housing

Medium Rapid bioassays

developing Green manufacturing

(China, India…) Ubiquitous RFID tagging

Hybrid vehicles

High Targeted drug delivery

proficient Improved diagnostic and surgical methods

(Europe, ….) Quantum cryptography

Very High Ubiquitous information access

advanced Tissue engineering

(US, Japan, top Europe…)Pervasive sensors

Wearable computers

Source: Rand Corporation2006, Richard Silberglitt ... et al., The Global technology revolution 2020