in association with integrating esg into portfolios · in association with-integrating esg into...

TRANSCRIPT

in association with

-

Integrating ESG into Portfolios

From Europe to the US: best practice in achieving responsible returns

Sponsors

Media Partners

The Corporate Social Responsibility Newsw

-

Welcome to Integrating ESG into Portfolios, the third in a series of ‘Responsible In-vestor Events’, which aim to bring top-level speakers from asset owners, asset man-agers and advisers together for targeted, practical discussion on pertinent themes

of sustainable and responsible investment.This latest conference, subtitled: ‘From Europe to the US: best practice in achieving respon-

sible returns’, is our second ESG integration event after a highly successful first outing in Am-sterdam in November 2008. At that time, a number of investors told us they thought the same kind of focused event and exchange of investor experience would be extremely useful in the US, where take up of the United Nations Principles for Responsible Investment (PRI) has been somewhat slower than in Europe, but where interest in the what, why and how of ESG integration incarnated by the PRI has been equally strong. This is especially true since the opening of a New York hub for the PRI secretariat, led by our opening speaker, Jerome Tag-gart, the PRI’s chief operating officer.

Among a wealth of hugely experienced speakers, we are particularly delighted to hear at this event from three of the world’s biggest pension funds and advocates of ESG in investment. Rob Lake, head of sustainability at APG Asset Management, the wholly-owned fund manager of the giant €173bn ($231bn) ABP pension fund for Dutch civil servants, now runs a team of eight ESG spe-cialists looking at, among others, equities, bonds, real estate and emerging markets investments.

Christina Kusoffsky Hillesöy, chair of the ethical council at Sweden’s €80bn AP1-4 gov-ernment buffer pension funds, oversees one of the most comprehensive investor engagement projects in the world and recently announced that they had successfully lobbied three major international companies, Spain’s Grupo Ferrovial, PetroChina and France’s Thales to abandon projects that flouted international conventions ratified by the country.

Hye-Won Choi, senior vice president and head of corporate governance at TIAA-CREF, the giant $400bn US pension plan and investment fund group for US teachers and researchers, not only leads one of the most active corporate governance departments in the US, but was also recently invited by US Securities and Exchange Commission chairman Mary Schapiro to join the Investor Advisory Committee to give investors a greater voice in the SEC’s work.

Signatories to the PRI in the three-plus years since it launched are estimated to super-vise upwards of $19trn in assets, making it one of the world’s biggest investor initiatives.

The six ‘principles’ aim gradually to mainstream the broad theme of ‘responsible’ investment by giving targets for integrating ESG issues into strategy and investment decisions. These range from drawing up responsible investment manifestos to industry promotion of the PRI and the inclusion of ESG criteria in investment mandate requests for proposal (RFPs).

The US has traditionally been the home of socially responsible investment (SRI) based on the screening out of unfavourable companies or the best-in-class positive weighting approach to investment. ESG integration, however, is a more holistic look at where environmental, social and governance factors can add value or mitigate risk across an entire institutional investment portfolio. Yet, the UN PRI Report on Progress includes the key finding that: “Principle 1 of the PRI, which focuses on incorporating ESG issues into investment analysis and decision

making, was ranked the most difficult to implement.” As a result, there is much that investors can learn from each other. Responsible Investor Events aim to translate this discussion into practical solutions.

Hugh Wheelan, Editor and co-founder, Responsible Investor (www.responsible-investor.com)

From Europe to the US: learning from each other

Contents2/3 Conference programme

4/5 Institutional investors’ adoption of the UN PRI is bringing ESG issues into the investment mainstream. By Hugh Wheelan

6/7 Good performance on ESG issues is often an indicator of a com-pany’s overall management quality and ability to deal with long-term strategic risks. By Christopher Greenwald, ASSET4

8/9 Business approaches that inte-grate responsible behaviour into a company’s strategy contribute to competitiveness as well as to sustainable development. By Erik Breen, Robeco

10/11 Can financial performance be en-hanced by investing in sustainable companies? First, it is necessary to identify the sustainability lead-ers. By Christophe Churet, Sus-tainable Asset Management

Response Global Media Ltd30 Spalding Road, London SW17 9BW, UKTel: +44 (0)20 8682 3638www.responsible-investor.comEditorial: Hugh Wheelan, [email protected]: Tony Hay, [email protected]

© 2009 Response Global Media Ltd/

June 2009

-

Integrating ESG into PortfoliosFrom Europe to the US: best practice in achieving responsible returns

25th June 2009, The Harvard Club, New York

in association with

Sponsors

www.Responsible-Investor.com

ProgrammeThe US has traditionally been the home of socially responsible investment (SRI) based on the screening out of

unfavourable companies or the best-in-class positive weighting approach to investment.More recently, however, new SRI terminology has entered the lexicon: ESG integration, a holistic look at where environmental, social and governance factors can add value or mitigate risk across an entire institutional investment portfolio. The trend has been taken up strongly in Europe and the same is happening in the US.With more than 500 institutional investors (both asset owners and investment managers) signed up to the UN Principles for Responsible Investment (UN PRI) – of which the number of US signatories is 78 and rising fast – there is now a wall of institutional money lined up to evaluate ESG integration. Yet, the UN PRI Report on Progress includes the key finding that: “Principle 1 of the PRI, which focuses on incorporating ESG issues into investment analysis and decision making, was ranked the most difficult to implement.”As a result, there is much that investors can learn from each other. Responsible Investor Events aim to translate discussion into practical solutions.Integrating ESG into Portfolios is a one-day seminar examining how institutional investors and portfolio managers can integrate environmental, social and corporate governance issues into mainstream investment analysis and decision-making, including the wider portfolio impacts.Delegates will hear from practitioners who will deliver knowledge and insights gained via their first-hand experience. The entire event will focus on best practice.

In association with the US Social Investment Forum (US SIF)

8.00 Registration8.45 Chairman’s introduction – What is ESG integration and why is it growing in importance? Why ESG is important for restoring market confidence.

What are the main differences/similarities in ESG between Europe and the US? Hugh Wheelan, editor and co-founder, Responsible Investor9.00 United Nations Principles for Responsible Investment – What is working well for investors

regarding ESG integration and what can we now expect from the PRI? What is proving more difficult to achieve and why?

Jerome Tagger, chief operating officer, UN PRI9.20 How and why are leading US and European investors integrating ESG into their mainstream

portfolios? Moderator – Hugh Wheelan, editor, Responsible Investor Equities and bonds – Rob Lake, head of sustainability, APG Asset Management, Netherlands Alternatives and property – David Wood, Boston College Institute for Responsible Investing Domestic emerging markets – Betsy Zeidman, director, Center for Emerging Domestic Markets, Milken Institute10.10 Refreshment break10.40 The future of corporate ESG data/information Delivering and using ESG data and information in investment. Moderator – Gary Turkel, head of equity product and ESG, Bloomberg Hugo Steensma, managing director, Sustainable Asset Management, USA Christopher Greenwald, director of data content, ASSET4, Switzerland

Programme is provisional and speakers and topics may change before the event

-

Integrating ESG into PortfoliosFrom Europe to the US: best practice in achieving responsible returns

25th June 2009, The Harvard Club, New York

in association with

Media Partners

www.Responsible-Investor.com

11.20 Trends in ESG reporting internationally in emerging markets Moderator – Hugh Wheelan, editor, Responsible Investor Lauren Compere, director of shareholder advocacy, Boston Common Asset Management Sonia Wildash, senior research analyst, Eiris Euan Marshall, program manager, Environment and Social Development Department, International

Finance Corporation12.00 How are investors assessing climate change risk and opportunities in their

investment portfolios? Moderator – Stephen Viederman David Blitzer, managing director and chairman of index committees, Standard & Poor’s Mark Fulton, global head of climate change research, Deutsche Asset Management 12.40 Lunch1.45 Keynote Address Stuart L Berman, partner, Barroway Topaz Kessler Meltzer & Check, LLP

2.00 What are the latest US/European trends in terms of corporate engagement? How can engagement be measured in terms of success?

Moderator – Hugh Wheelan, editor, Responsible Investor Christina Kussofsky Hillesoy, chair of ethical council for AP Government buffer funds, Sweden Hye-Won Chon, head of corporate governance, TIAA-CREF Laura Shaffer, director of shareholder activities, Nathan Cummings Foundation Hanna Roberts, engagement manager, GES Investment Services, Sweden2.50 How serious are money managers about integrating ESG issues into their investment and

what are they doing? Moderator – Hugh Wheelan, editor, Responsible Investor Erik Breen, head of responsible investing, Robeco, Netherlands Mike Musuraca, managing director, Blue Wolf Capital Tim Smith, senior vice president, ESG group, Walden Asset Management3.40 Refreshment break4.00 Corporate reporting, fiduciary duty and the US regulatory environment under the

Obama administration Moderator – Meg Voorhes, deputy director and research director, Social Investment Forum Adam Kanzer, managing director and general counsel, Domini Social Investments Sanford Lewis, counsel, Investor Environmental Health Network4.50 How do you incorporate ESG criteria into asset managers requests for proposals (RFPs)? Moderator – Hugh Wheelan, editor, Responsible Investor Craig Metrick, US head of responsible investment team, Mercer Sarah Cleveland, senior consultant, Watson Wyatt5.30 Chairman’s closing remarks5.40 Drinks reception in the Biddle Room of the Harvard Club

The Corporate Social Responsibility Newsw

4 Responsible-Investor.com

Integrating ESG into Portfolios

Prior to the full launch of the United Na-tions Principles for Responsible Invest-ment (UNPRI) in April 2006, the inte-

gration of environmental, social and governance (ESG) factors into investment was a niche area advocated by a handful of asset owners and fund managers. They argued that socially responsible investment meant little if confined to relatively small specialist SRI or ethical funds or mandates, rather than aggregated into overall investment de-cisions should it be material (ie, performance or risk sensitive), in breach of agreed international standards or against the long-term interests of scheme members.

The adoption of ESG integration as the cor-nerstone of the UN principles took the concept above ground in a big way in a short time and is now its principle driver. Signatories to the PRI in the three-plus years since it launched are estimat-ed to supervise upwards of $19trn in assets, mak-ing it one of the world’s biggest investor initiatives.

The six ‘principles’ aim gradually to mainstream the broad theme of ‘responsible’ investment by giving targets for integrating ESG issues into strategy and investment decisions. These range from drawing up responsible investment mani-

festos to industry promotion of the PRI and the inclusion of ESG criteria in investment mandate requests for proposal (RFPs).

This latter point is key: put simply, if enough asset owners want their investments managed ac-cording to certain ESG criteria, then fund man-agers and advisers that want the business will fol-low. This gives the PRI a classic push/pull mecha-nism that has been in place since it was founded, with the support of a group of the world’s biggest pension funds, and will undoubtedly spread. As a result, some of the world’s biggest fund man-agement chiefs have stood up to say they believe responsible investment could be the norm within a decade.

The market incentive has been strengthened by the proactive approach of PRI signatories. Some pension plans, such as the UK Environ-ment Agency fund, have terminated investment contracts with managers and cited their non-adherence to the PRI as an important part of the decision. Other large European pension funds including France’s €34bn ($54bn) French pen-sions reserve fund (FRR), include PRI member-ship as an integral part of their manager selection process. Asset managers say they increasingly

see mandate RFPs in the market that are precise about the commitment of the manager to the PRI and ask for evidence of engagement, voting and research as outlined in the principles.

The investment rationale for ESG integra-tion is that some so-called ‘extra-financial’ factors, taken over a medium- to long-term time horizon are ‘material’ to corporate performance, but be-ing ignored by many asset owners and manag-ers that purport to be duration investors. The argument has received strong research backing. A 2007 report by the United Nations Environ-ment Programme Finance Initiative (UNEP FI), concluded that a majority of academic and broker papers it selected showed that integrating ESG factors into investment decisions could match or improve current performance.

In a review of the major research available in the market, UNEP FI and Mercer, the investment consultant, found that out of

20 academic studies, 10 found a positive rela-tionship between ESG factors and performance, seven were broadly neutral and three negative. The report, Demystifying Responsible Investment Performance, found 10 similar studies by broker-age houses gave three positive reviews and seven neutral indicators. None concluded that perform-ance could be negative as a result of ESG integra-tion. UNEP FI said the research would reassure investors that introducing ESG criteria into their investments was not a barrier to good returns.

Critics of the report claim a selection bias in the research chosen. Others argue that mainstream portfolio managers are well aware of ESG issues such as carbon pricing or brand reputation con-cerns if they are deemed a risk to the near-term share price. The real problem, they say, is that in-stitutional investment has become short-termist, with mandates based on quarterly performance and stocks traded regularly rather than held for the long term. If investors believe greater action is warranted from companies on these issues,

From Europe to the US: best practice in achieving responsible returns

The success of the UN PRI in signing up in-vestors with around $19trn in assets worldwide is just one indicator of the ex-tent to which consid-eration of ESG issues is moving into the mainstream. By Hugh Wheelan

5Responsible-Investor.com

they say, then they either need to assign a greater importance to social and environmental issues in their investment process (ie, to broaden the defi-nition of materiality beyond financial metrics) or to press for government intervention to require higher standards.

Some commentators believe a better focus by institutional investors on corporate governance, executive pay and engagement could have gone a long way towards preventing the credit crunch by reining in dubious mortgage lending practices and preventing a short-term misalignment of bank-ing pay with shareholder value. Certainly, many governments have taken the view that investor activism is the only way to safeguard against fu-ture excesses and are promoting firm shareholder governance accordingly. Other SRI investors ar-gue that ESG issues are still wilfully ignored by mainstream investment analysts, despite a wealth of research that they say proves the correlation be-tween corporate social performance and financial performance.

The publication of the Freshfields legal opin-ion on ESG in the UK in late 2005 gave some indication to investors that it might no longer be considered a breach of fiduciary duty to look at ESG concerns if they are material. Indeed, Fresh-fields argued that the opposite could be true, that if ESG factors are material it could be deemed to be fiduciary to make sure they are considered. European investors may have been quicker to latch on to the PRI as the body for building in-vestor consensus on ESG issues, but after a slow start US investors are now also joining in greater numbers, notably since the introduction of a New York hub for the PRI secretariat.

Importantly, the PRI is voluntary and aspira-tional. It doesn’t set firm standards. Instead, it opts for an annual assessment programme

where signatories indicate progress in moving to-wards the principles. After two years, discernible and verifiable change is expected.

What does this really mean to US investors in the country where SRI became a major force on the back of the South Africa boycott cam-paigns of the 1980s. Isn’t it all just semantics? Yes and no. ESG integration should not be entirely confused with SRI or ethical investing – despite bearing hallmarks of both. Some US investors have weighed up materiality factors in stock selec-tion for many years, as well as offering screened portfolios and best-in-class portfolios. They may not have flagged it as such, though, and indeed a

growing number of US ethical fund managers are making a notable strategy and branding switch to become ‘sustainable’ investment managers rather than maintain the somewhat negative connota-tion of being corporate screeners.

US pension funds have also been caught up in their own fiduciary struggle on responsible investment, particularly since the release of modi-fied guidance on fiduciary duty in October 2008 by the US Department of Labor that obliges

trustees to demonstrate that investment returns are ‘optimised’ by ESG or ethical criteria; a proof that many in the RI industry believe is difficult to make.

The US Social Investment Forum (SIF) has called on the Obama administration to provide pension plans with “clear, consistent and unam-biguous guidance” that adheres to a more contem-porary and principled understanding of fiduciary duties. The SIF has said it also hopes that the administration will push the US Securities & Ex-change Commission (SEC) to enforce corporate

disclosure of financially material environmental and social issues, which it believes could reinforce the argument on materiality.

To some extent, ESG is a way to look at sus-tainability across all the companies investors buy, and then for investors to decide what time-frame they believe is important to them and their mem-bers. As a result, it is directly related to ‘extra-fi-nancial’ investment (EFI) analysis, also known as ‘enhanced analytics’, which is broker research that has included ESG factors. While some invest-ment banks have been reducing their commit-ment to ESG research, others such as Goldman Sachs have been investing in initiatives, such as GS Sustain, to identify long-term investment trends based on ESG and financial data. Nota-bly, the PRI recently announced a merger with the Enhanced Analytics Initiative (EAI), the as-sociation of investors and brokers that promotes the inclusion of EFIs into company and sector research. The amalgamation, they said, will “inter-nationalise” the call for better investment research. It also goes some way to revealing how the PRI could prompt members to further actively inte-grate ESG factors into investment after making the initial commitment to sign up.

If the continuing debate reveals anything, it is that institutional investors are beginning to take the principle of ESG as being both important fi-nancially and socially for their long-term benefici-ary scheme members, and coalescing around the PRI to determine the best way do so. RI

Responsible Investor’s recent coverage

3 June 2009: US pension shareholder activism has no economic value, may breach fid duty: Chamber of Commerce www.responsible-investor.com/home/article/us_pension/

3 June 2009: US carbon cap and trade could wipe out some US companies’ future earningswww.responsible-investor.com/home/article/trucost1/

23 April 2009: OECD – Better governance and risk tools could have limited $5 tril-lion global pension fund losseswww.responsible-investor.com/home/article/oecd/

22 January 2009: US SIF puts proxy vote and fiduciary duty on Obama agenda www.responsible-investor.com/home/article/us_sif1/

3 November 2008: US SRI managers shift from ethical to sustainablewww.responsible-investor.com/home/article/sustainability_managers/

7 September 2007: Can enhanced analysis deliver environmental and social benefits?www.responsible-investor.com/home/article/can_enhanced_analysis_de-liver_social_and_environmental_benefits/

‘Some of the world’s big-gest fund management chiefs say they believe responsible investment could be the norm within a decade’

6 Responsible-Investor.com

Integrating ESG into Portfolios

An increasing number of investors and financial professionals have come to recognise the usefulness of environ-

mental, social and governance (ESG) data as a means for measuring the quality of a com-pany’s management. In the spring issue of McKinsey Quarterly, 80% of CFOs and CIOs responding to a McKinsey survey agreed with the claim that ESG data can serve as a proxy for management quality. Indeed, those compa-nies that are able to manage and benchmark their ESG performance tend to be those that are able to manage all aspects of their business effectively.

While the central importance of manage-ment quality for long-term valuations has be-come all too apparent to investors during the financial crisis, it nonetheless remains one of the most difficult factors to determine on the basis of financial reporting alone. Investors have become increasingly aware of the useful-ness of ESG performance data in providing a more concrete basis for assessing manage-ment quality that can aid traditional financial

ESG data and management quality: lessons from the investment banks

analysis in determining the long-term valua-tions of companies.

The credit crisis: a window into management qualityWhile this recognition of the usefulness of ESG data has emerged, the details of the spe-cific links between ESG data and manage-ment quality have not yet been fully explored. The credit crisis provides a unique opportu-nity to study this link in greater depth, given the stark differences between companies’ risk management practices prior to the crisis that were revealed so starkly by the radically dif-fering performances of companies once the crisis began.

The investment banking industry in the US represents the most dramatic example of such differences. Goldman Sachs, Morgan Stanley, Merrill Lynch, Lehman Brothers and Bear Stearns were all involved to differing degrees in the securitisation of mortgage financing, which was the epicentre of the financial crisis. The stark differences in the fates of Goldman

Sachs, Morgan Stanley and Merrill Lynch, which survived or were acquired during the crisis, and Lehman Brothers and Bear Stearns, which failed, provide a unique opportunity to examine what, if any, ESG variables differed among these companies. Which of these vari-ables might have provided some signal of the quality of management decisions before the crisis began?

Any such study must focus on the reports of these companies for fiscal year 2006, which were published prior to the onset of the crisis. An examination of some of the key differences leads to two initial observations.

First, prior to the financial crisis, many of the most important financial indicators of these companies were very similar. The five-year average returns on equity as well as the credit ratings of the investment banks were virtually identical at the beginning of 2007. Moreover, any considerations of either sub-prime lending or mortgage-backed securities as risk factors were completely absent from the 2006 10-K filings by the investment banks. This was despite the increasing importance of these assets on their balance sheets, as well as the dominance of these topics in their 2007 10-K filings after the crisis began.

Second, while a number of the ESG vari-ables for these companies were similar for fis-cal year 2006, there were nonetheless several key and notable differences in the reporting of Morgan Stanley, Goldman Sachs and Merrill Lynch, on the one hand, and Lehman Broth-ers and Bear Stearns on the other. With the exception of two key indicators, the corporate governance data of the five investment banks were quite similar in 2006, both in terms of policies and actual performance measures such as committee independence and compensa-tion ratios. Similarly, in the social area, many similarities existed among the investment banks’ performance.

The US investment banks that survived the credit crisis performed better on ESG issues than those that didn’t. This perhaps surpris-ing correlation suggests a strong indicator of manage-ment quality: managements able to assess and mitigate longer-term strategic risks to their business are also better equipped to cope with a crisis. By Christopher Greenwald

7Responsible-Investor.com

Environmental reporting reveals key differences

Surprisingly, the clearest differences between the banks that survived and those that failed were in the area of environmental data. Mor-gan Stanley, Goldman Sachs and Merrill Lynch all provided much better information on policies and initiatives to improve envi-ronmental efficiency and reduce emissions. Interestingly, and more specifically, in contrast to Lehman Brothers and Bear Stearns, these companies also reported on the importance of climate change as a risk to their future busi-ness performance, and they identified the overall strategic importance of extra-financial factors more generally.

The table shows the 10 factors for which the performance of Morgan Stanley, Goldman Sachs and Merrill Lynch was clearly better than Lehman Brothers and Bear Stearns for FY 2006.

While out-performance on these factors correlated with the investment banks that sur-vived the financial crisis, it is important also to examine these factors and their relationship to the financial performance of other capital mar-kets companies. By combining these 10 ESG criteria into a unique rating framework using the ASSET4 system, it is possible to exam-ine the correlation of these factors with price performance over time. Doing so reveals quite interesting parallels.

Among all US capital markets and commer-cial banks, companies with relatively higher scores (greater than 50 percentile) on these 10 ESG factors out-performed those with lower scores between 2006 to 2008 by 14.4% on average. Consequently, the 10 ESG criteria that differed markedly among the five leading investment banks in 2006 may reveal impor-tant variables that can be used as a signal for measuring management quality across other companies in similar industries.

This conclusion may initially appear to be counter-intuitive, given that environmental factors do not have a significant material link to the financial performance of capital markets companies in the short term. However, these subtle differences in company reporting may nonetheless provide important signals con-cerning the seriousness with which ESG fac-tors are taken by management. Specifically, the ability of management to foresee the impact of climate change on its business reflects its abil-

ity to understand its business activities in the light of longer-term and systematic risks.

Similarly, the ability of such companies to report and benchmark their environmental performance can serve as a strong reflection of the extent of effective measurement tools and management practices throughout these com-panies’ activities.

In short, these variables provide a meas-urement of management’s ability to adopt a long-term view of its business strategy. Those

capital markets companies that are able to make short-term decisions in the light of such a longer-term view are much more likely to be cognisant of the systematic risks that they face. They are therefore better prepared to face the challenges that unforeseen circumstances such as the financial crisis may present.

Combining extra-financial and traditional analysisESG data does not hold a set of answers that can explain all or even most of the many com-plex factors that determined companies’ radi-cally differing financial performance during

the credit crisis. However, when combined with traditional financial analysis, ESG data can provide a useful means for measuring management quality and understanding the long-term orientation of companies more generally. Such assessments are most effec-tive when grounded in objective ESG criteria that are filtered through sector- or industry-specific frameworks, given the differences in company reporting across industries as well as the various degrees of importance of ESG variables in different sectors.

As the provider of the world’s largest da-tabase on objective, ESG data, ASSET4 is uniquely positioned to allow investors to ex-plore the link between ESG data and man-agement quality in greater detail. With 278 key performance indicators and over 900 in-dividual data points as well as three to seven years of historical data on over 2,600 publicly traded companies, ASSET4’s database allows investors to conduct in-depth qualitative or quantitative analyses on the impacts of specific ESG factors on performance at the level of the company, industry or sector.

ASSET4 is convinced that additional re-search in this area will reveal many new and important links between ESG data and the quality of a company’s management. Doing so will help the larger financial community to un-derstand better the significance of ESG data as providing a means to identify those com-panies which have a longer-term orientation toward managing extra-financial and financial risks that will be reflected in their valuations over time. RI

Christopher Greenwald is director of data content at ASSET4

10 key extra-financial performance indicators

l Overall strategic policy on extra-financial indicators

l Commercial risks and opportunities due to climate change

l Emissions reduction policy

l Total reported carbon dioxide emissions

l Energy efficiency initiatives

l Environmental partnerships

l Environmental citizenship initiatives

l Environmental project financing

l Percentage of strictly independent board members

l Ratio of non-audit to audit fees

‘The ability of companies to report and bench-mark their environmen-tal activities can serves as a strong reflection of the extent of effec-tive measurement and management practices’

8 Responsible-Investor.com

Integrating ESG into Portfolios

With a financial crisis as the backdrop, both consum-ers and the media have committed themselves to

increasingly public discussion on the topic of sustainability, notably in finance and invest-ment. However, sustainability as a concept is broad in its nature and covers a wide, complex and relatively new part of the financial services industry. As a result, we believe it needs some markers to chart the path ahead.

Sustainable development is a way to meet the needs of the present without compromis-ing the ability for future generations to meet their own needs. This is the classical and glo-bally accepted definition of sustainable devel-opment formulated by the Brundtland Com-mission in its report for the United Nations in 1987.

Sustainable development is not a prohibi-tion for economic growth, the market econo-my or globalisation. It does, however, seek to define boundaries, given the consequences of this growth. For Robeco, the following defini-

tions with respect to sustainable development are relevant.

Vision on corporate responsibilityCorporate responsibility (CR) is a balance of economic performance with social develop-ment and respect for the environment. Re-sponsibilities are prioritised by a company’s identity and delineated by its sphere of influ-ence.1

Robeco believes in the growing necessity for companies to act responsibly. Several long-term trends are the basis of this notion:n The growing scarcity of natural resources as a consequence of growing population and increasing wealth globally.n The faster spread and broader reach of in-formation on external effects of business ac-tivities.n The growing impact of international NGOs that act as corporate responsibility watchdogs.n Rising awareness and demands from indi-viduals and consumers on global sustainability issues.

n Increasing globalisation and the shift of power from governments to companies.n Greater transparency and accountability of companies on the subject of corporate respon-sibility.

Acting responsibly as a company makes commercial business sense, while also meet-ing a moral duty. Business approaches where responsible behaviour is integrated into the company’s strategy and core business are likely to contribute to competitiveness as well as to sustainable development.2

Vision on responsible investment Responsible investing (RI) is the active con-sideration of environmental, social and gov-ernance issues in decision-making and owner-ship of investments.3

Sustainable corporate business strategies lead directly to responsible investment via the integration of these relevant environmental, social and governance (ESG) issues into the selection of those companies taking them seri-ously and performing better than their peers.

For Robeco, responsible investing is also the most important part of our own corporate responsibility as it refers directly to our core process and product: asset management. It is a growing theme.

A report by Booz & Company, the man-agement consultancy, which we sponsored last year, suggested that RI will be a main-stream part of the asset management market by 2015, running assets of 15–20% of the global total. The report suggested total rev-enues for the RI sector could reach $50bn a year within the same timeframe, meaning that RI funds become a major source of in-come for asset managers. It said that factors driving the growth of the RI market included increased social awareness, greater media at-tention and external pressure on investors, increasing prices of energy and raw materials and changing legislation such as mandatory carbon dioxide reductions.

Other contributory growth factors, the re-port said, included the increasingly established

1 Partly based on the UN Global Compact2 Among others, Michael E Porter and Mark R �ramer, ‘Strategy and Society: the �ink Between Com-Among others, Michael E Porter and Mark R �ramer, ‘Strategy and Society: the �ink Between Com-

petitive Advantage and Corporate Social Responsibility’, Harvard Business Review, December 2006.3 Definition from UNEP Finance Initiative4 See also www.unpri.org.

Robeco embraces responsible investing

Acting responsibly as a company makes commer-cial business sense, while also meeting a moral duty. Business approaches where responsible behaviour is integrated into the com-pany’s strategy and core business are likely to con-tribute to competitiveness as well as to sustainable development. By Erik Breen

9Responsible-Investor.com

track record for RI performance as well as fur-ther technological innovations.

The report said that Europe – particularly the UK and Switzerland – would drive much of the RI growth, with the institutional mar-ket growing faster than retail fund sales. As a result, the report claimed that the shape of the asset management landscape will change con-siderably over the next few years: “Today, the RI market is heavily fragmented. Larger play-ers have not yet actively pursued RI or are only just beginning to position themselves in the

market. By 2015, niche players are either likely to be taken over by global players or will grow themselves to become sizeable specialists; the current leading players might become laggards if they do not follow this trend.”

Charles Teschner, partner of Booz & Com-pany, said: “RI is becoming more and more sig-nificant in the investment world, with raised social awareness and improved performance factors, as well as the fact that pension funds and other institutional investors are increas-ingly required to disclose their policies and positions.”

Investment approaches that integrate ESG factors into the investment process are more likely to gain enhanced insights into potential risk and return rewards leading to better deci-sions. The declaration by the United Nations Principles for Responsible Investment (UN PRI)4 provides a framework for action as an involved owner and actively promotes respon-sibility in investments. Robeco has been an ac-tive signatory of the UN PRI since December 2006.

External codes of conductRobeco’s ambition on responsible investing cannot be seen apart from our wide range of products and specialist investment teams in Europe and the US serving a diverse client base. Among Robeco’s clients are private inves-tors, wealthy clients and institutional inves-tors of all sizes and from all regions across the world with a diverse set of values. For this rea-son, Robeco chooses broadly accepted, exter-nally verified codes of conduct, many of which are signed by Robeco and/or Robeco’s parent company Rabobank.

Dispersed ownership and collaborationFrom the perspective of client focus and coop-eration, Robeco recognises the similar position that asset owners and asset managers have as financial participants in companies around the world. We believe in the responsibility of shared ownership despite the dispersed share register of today’s companies. Active owner-ship by shareholders can enhance the long-term value of a company.

In pursuing active ownership, Robeco aims to collaborate with other asset own-ers and asset managers for more effective corporate oversight. Companies can also benefit as a result through the efficiency of communication via one point of contact for a group of like-minded investors. As as-set owners and asset managers tend to buy and sell shares regularly, ownership is not a continuous process per se. Collaboration with other investors raises the chances of a continued dialogue that is important in the long-term relationship we believe investors and companies should build. Such collabo-ration can occur for instance in executing votes at meetings of shareholders, in con-structive dialogues with companies and in supporting general stances towards policy makers, legislators and regulators.

Robeco has chosen to focus its contribu-tion based on the expected value creation for its clients. This can depend on factors such as

the size of the holding in our clients’ portfo-lios. Collaboration on a case-by-case basis means a greater diversity – and balance – of discussions can be worked through by asset owners, asset managers and companies. Shar-ing this workload can improve the efficiency of resources that asset managers allocate to responsible ownership on behalf of their asset owner clients.

In actively exercising voting rights and in conducting active dialogues with companies, Robeco aims to improve the governance and

sustainability of companies held. It is our be-lief that good governance and sustainability contribute to the creation of long-term share-holder value. The degree of governance and sustainability within a company is increasingly becoming a driver in the allocation of capital. In valuing – and in buying and selling – finan-cial securities, an important part of the current estimated value lies in the expected value of future cash flow.

We believe that the expected value of future cash flow improves if a company improves its governance and sustainability. Such improve-ment is beneficial to the company’s stake-holders overall. Although the results of these efforts may materialise only over time, it is expected that current valuation can reflect the expected results more momentarily. The valu-ation horizon of financial markets in general is therefore the key element, regardless of the average holding period of securities. RI

Erik Breen is head of responsible investing at Robeco.

Responsible investing will be a mainstream part of the asset management market by 2015, running assets of 15–20% of the global total

‘It is our belief that good governance and sustain-ability contribute to the creation of long-term shareholder value’

10 Responsible-Investor.com

Integrating ESG into Portfolios

Sustainability investing is one of the major topics in finance today, generating increas-ing interest among a wide range of inves-

tors. And the numbers speak for themselves: the UN Principles for Responsible Investment (UN PRI), an initiative that promotes the integration of sustainability factors into investment decisions, now has signatories representing assets worth more than $15trn globally. Institutional investors can no longer ignore the importance of sustain-ability factors. But why does it make sense to con-sider sustainability? Can financial performance be enhanced by investing in sustainable companies? These are the questions to be answered in this article, which introduces SAM’s research philoso-phy and assessment process before presenting the results of our latest empirical study, carried out by Robeco’s Quantitative Strategies Department.

Long-term approachSustainability investing is a long-term invest-ment approach that integrates economic, en-vironmental and social considerations into the selection and retention of investments.

So, why consider sustainability in the first place? In a market economy, the competitive position of a company ultimately determines its potential to create value. Our conviction is that sustainability trends such as climate change, resource efficiency or demographics have an impact on the environment in which companies

compete. Moreover, capital markets are increas-ingly aware of the value of intangible assets to the firm.

As shown in Figure 1, the average ratio of book value to overall market value has dropped significantly over the past decades; this implies that a firm’s ability to grow earnings increasingly depends on intangible assets such as the quality of management, branding power, human capital de-velopment and intellectual capital. In view of this, investment professionals can no longer afford to overlook the value of intangibles when perform-ing fundamental analysis. SAM’s sustainability criteria act as a suitable proxy for quantifying the value of a firm’s intangible assets, leading to bet-ter-informed investment decisions.

By analysing the sustainability profile of companies, SAM gains additional insights that facilitate the selection of stocks offering the po-tential for attractive long-term returns, while investing in responsible corporate citizens.

Sustainability assessmentSAM seeks to identify companies that both:n demonstrate a core ability to manage sustain-ability issues, andn represent attractive investment opportunities.

The first step in achieving this goal is to iden-tify the sustainability trends that are likely to have an impact on the creation of shareholder value in the future. Together with its profes-sional network of industry experts and NGOs, SAM then develops a number of criteria de-signed to assess a company’s ability to manage these trends and challenges (see Figure 2).

In terms of competitiveness, sustainability per-formance is of greatest relevance to shareholder value creation when assessed in relative terms. As a result, SAM opts for a best-in-class approach targeted at identifying the leading companies in each sector. Our screening methodology is based on an assessment questionnaire, with information coming directly from companies.

SAM’s screening processEvery year, SAM invites the 2,500 largest com-panies worldwide, based on free-float market capitalisation, to take part in the assessment. The number of companies completing this annual survey has been growing steadily since 1999. This assessment is complemented by a media and stakeholder analysis that enables analysts to consider additional information from NGOs and the media. Lastly, our screen-

Finding alpha in sustainablility

Can financial performance be enhanced by investing in sustainable companies? By investing in the sustain-ability leaders, investors are enhancing their returns while also making a posi-tive contribution on issues affecting us all. By Christophe Churet

2. General sustainability criteria

Source: SAM

SAMCORPORATE

SUSTAINABILITYASSESSMENT

ECONOMICDIMENSION

Codes of conductCompliance

Corruption & briberyCorporate governance

Risk & crisis management

SOCIAL DIMENSION

Corporate citizenship

Labour practice indicators Human capital development

Social reporting Talent attraction

& retention

ENVIRONMENTAL DIMENSION Eco-efficiencyEnvironmental reporting

0

20

40

60

80

100

1. The rise of the intangibles

%

1978 2005

FTSE 250 Index market capitalisation

Intangibles Tangibles

Source: Interbrand: Brand Value Management (2006)

5%

95%

72%

28%

11Responsible-Investor.com

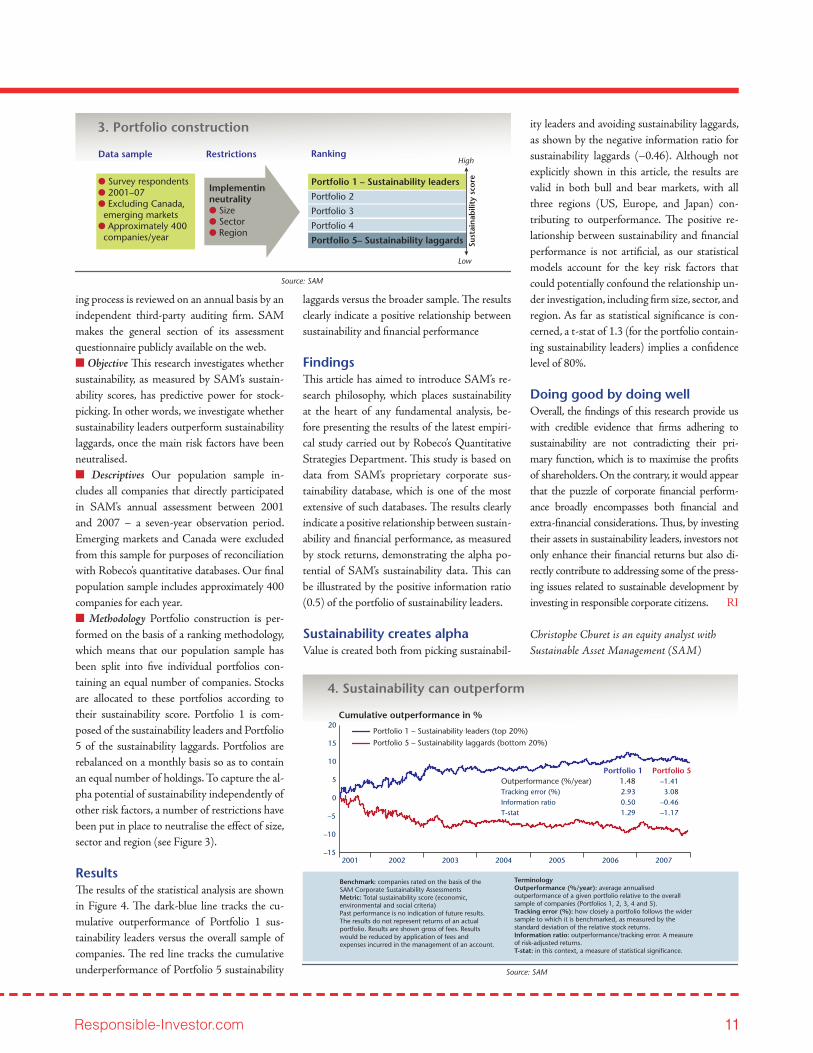

ing process is reviewed on an annual basis by an independent third-party auditing firm. SAM makes the general section of its assessment questionnaire publicly available on the web.n Objective This research investigates whether sustainability, as measured by SAM’s sustain-ability scores, has predictive power for stock-picking. In other words, we investigate whether sustainability leaders outperform sustainability laggards, once the main risk factors have been neutralised.n Descriptives Our population sample in-cludes all companies that directly participated in SAM’s annual assessment between 2001 and 2007 – a seven-year observation period. Emerging markets and Canada were excluded from this sample for purposes of reconciliation with Robeco’s quantitative databases. Our final population sample includes approximately 400 companies for each year.n Methodology Portfolio construction is per-formed on the basis of a ranking methodology, which means that our population sample has been split into five individual portfolios con-taining an equal number of companies. Stocks are allocated to these portfolios according to their sustainability score. Portfolio 1 is com-posed of the sustainability leaders and Portfolio 5 of the sustainability laggards. Portfolios are rebalanced on a monthly basis so as to contain an equal number of holdings. To capture the al-pha potential of sustainability independently of other risk factors, a number of restrictions have been put in place to neutralise the effect of size, sector and region (see Figure 3).

ResultsThe results of the statistical analysis are shown in Figure 4. The dark-blue line tracks the cu-mulative outperformance of Portfolio 1 sus-tainability leaders versus the overall sample of companies. The red line tracks the cumulative underperformance of Portfolio 5 sustainability

laggards versus the broader sample. The results clearly indicate a positive relationship between sustainability and financial performance

FindingsThis article has aimed to introduce SAM’s re-search philosophy, which places sustainability at the heart of any fundamental analysis, be-fore presenting the results of the latest empiri-cal study carried out by Robeco’s Quantitative Strategies Department. This study is based on data from SAM’s proprietary corporate sus-tainability database, which is one of the most extensive of such databases. The results clearly indicate a positive relationship between sustain-ability and financial performance, as measured by stock returns, demonstrating the alpha po-tential of SAM’s sustainability data. This can be illustrated by the positive information ratio (0.5) of the portfolio of sustainability leaders.

Sustainability creates alphaValue is created both from picking sustainabil-

ity leaders and avoiding sustainability laggards, as shown by the negative information ratio for sustainability laggards (–0.46). Although not explicitly shown in this article, the results are valid in both bull and bear markets, with all three regions (US, Europe, and Japan) con-tributing to outperformance. The positive re-lationship between sustainability and financial performance is not artificial, as our statistical models account for the key risk factors that could potentially confound the relationship un-der investigation, including firm size, sector, and region. As far as statistical significance is con-cerned, a t-stat of 1.3 (for the portfolio contain-ing sustainability leaders) implies a confidence level of 80%.

Doing good by doing wellOverall, the findings of this research provide us with credible evidence that firms adhering to sustainability are not contradicting their pri-mary function, which is to maximise the profits of shareholders. On the contrary, it would appear that the puzzle of corporate financial perform-ance broadly encompasses both financial and extra-financial considerations. Thus, by investing their assets in sustainability leaders, investors not only enhance their financial returns but also di-rectly contribute to addressing some of the press-ing issues related to sustainable development by investing in responsible corporate citizens. RI

Christophe Churet is an equity analyst with Sustainable Asset Management (SAM)

3. Portfolio construction

Source: SAM

Data sample Restrictions Ranking

� Survey respondents� 2001–07� Excluding Canada, emerging markets� Approximately 400 companies/year

Implementingneutrality� Size� Sector� Region

Portfolio 1 – Sustainability leaders

Portfolio 2

Portfolio 3

Portfolio 4

Portfolio 5– Sustainability laggards Sust

ain

abili

ty s

core

High

Low

4. Sustainability can outperform

Source: SAM

200720062005200420032002 2001

20

15

10

5

0

–5

–10

–15

Portfolio 1 – Sustainability leaders (top 20%)

Portfolio 5 – Sustainability laggards (bottom 20%)

Portfolio 1 Portfolio 5Outperformance (%/year) 1.48 –1.41Tracking error (%) 2.93 3.08Information ratio 0.50 –0.46T-stat 1.29 –1.17

TerminologyOutperformance (%/year): average annualised outperformance of a given portfolio relative to the overall sample of companies (Portfolios 1, 2, 3, 4 and 5).Tracking error (%): how closely a portfolio follows the wider sample to which it is benchmarked, as measured by the standard deviation of the relative stock returns.Information ratio: outperformance/tracking error. A measure of risk-adjusted returns.T-stat: in this context, a measure of statistical significance.

Cumulative outperformance in %

Benchmark: companies rated on the basis of the SAM Corporate Sustainability AssessmentsMetric: Total sustainability score (economic, environmental and social criteria)Past performance is no indication of future results.The results do not represent returns of an actual portfolio. Results are shown gross of fees. Results would be reduced by application of fees and expenses incurred in the management of an account.

risk or opportunity?

news, features and resourceswww.responsible-investor.com

climate change

risk or opportunity?

news, features and resourceswww.responsible-investor.com

climate change

risk or opportunity?

news, features and resourceswww.responsible-investor.com

climate change

risk or opportunity?

news, features and resourceswww.responsible-investor.com

climate change

risk or opportunity?

news, features and resourceswww.responsible-investor.com

climate change