implied interest rates in a market with frictions

TRANSCRIPT

Implied Interest Rates in a Market with Frictions∗

Lorenzo Naranjo†

New York University

This Version: March 2009

Abstract

There are many proxies for the short-term interest rate that are used in asset pricing. Yet,they behave differently, especially in periods of economic stress. Derivatives markets offer aunique laboratory to extract a short-term borrowing and lending rate available to all investorsthat is relatively free from liquidity and credit effects. Interestingly, implied interest rates do notresemble benchmark interest rates such as the three-month T-bill rate or LIBOR, but insteadare much more volatile. I argue that the volatility in the implied short-term rate in futuresand option markets is due to frictions arising from borrowing and short-selling costs. I derivean equilibrium model of the futures market where demand imbalances from traders affect theimplied interest rate. In the model, the implied interest rate depends on the “true” risk-freerate and a latent demand factor. I estimate the model based on S&P 500 index futures usingthe Kalman filter. The risk-free rate that results from this estimation has time-series propertiessimilar to Treasury and LIBOR rates, and anticipates interest rate changes. The spread betweenthe risk-free and the T-bill rate correlates with liquidity proxies of the Treasury market, whilethe spread between LIBOR and the risk-free rate is related to economic distress. The latentdemand factor is closely related to proxies for demand pressure in the futures market, such aslarge speculator positions as well as investor sentiment. The demand factor is positive (negative)when buying (selling) pressure is high and is difficult to borrow (to short-sell the underlying).I also find that demand imbalances are correlated across different indexes, for both futures andoptions.

JEL Classification: E43, G12, G13Keywords: Implied Interest Rates, Derivatives, Borrowing Costs, Demand Pressure, Limited Arbitrage

∗I owe my gratitude to my advisor, Marti Subrahmanyam, for his invaluable guidance and unconditional support. I alsowould like to thank the other members of my committee –Menachem Brenner, Stephen Brown, Joel Hasbrouck and Stijn VanNieuwerburgh– for their feedback and encouragement, and Ashwini Agrawal, Yakov Amihud, Jennifer Carpenter, FarhangFarazmand, Stephen Figlewski, Xavier Gabaix, JongSub Lee, Marcin Kacperczyk, Bryan Kelly, Rik Sen, Dimitri Vayanos andseminar participants at Cornell University, ESSEC Business School, London School of Economics, New York University, OxfordUniversity, and University of Illinois at Urbana-Champaign for helpful suggestions. All errors are mine.†Department of Finance, Stern School of Business, New York University, 44 West Fourth Street, New York, NY 10012,

Email: [email protected], Web: http://www.stern.nyu.edu/˜lnaranjo.

1

1 Introduction

Measuring and understanding the risk-free rate is a fundamental question in financial economics.

The risk-free rate is a required input in many theories that are extensively used by academics and

practitioners in finance, like the CAPM, the APT and the no-arbitrage valuation of derivatives

products. The valuation of real and financial assets depends crucially on using the correct risk-free

rate.

There are many proxies for the short-term interest rate that are used in asset pricing. On the

one hand, it is common for empirical researchers in finance to use the yield on three-month T-bills

as a proxy for the risk-free rate. The intuition for this practice is simple: T-bills are backed by

the full faith and credit of the U.S. government. As such, they are the safest investment available

for an investor whose consumption is denominated in U.S. dollars. One problem with using T-bill

yields as a proxy of the risk-free rate is that only the U.S. government can borrow at this rate.

Also, Treasury rates can exhibit periods of flight-to-liquidity during which investors are willing

to pay more for the benefit of holding a liquid security (Longstaff, 2004). On the other hand, it

is common for practitioners to use LIBOR rates as a proxy for the risk-free rate when valuing

derivatives contracts. The intuition for this practice is also simple: practitioners regard LIBOR

as their opportunity cost of capital. However, LIBOR represents the interest rate charged on an

uncollateralized loan between banks and hence is subject to credit risk1.

As a result, these interest rates behave differently, especially in periods of economic stress. For

example, Figure 1 shows how Treasury and LIBOR rates have being drifting apart during the 2007-

08 credit and liquidity crisis. The so-called TED spread, defined as the difference between LIBOR

and Treasury rates, was at an all time high (461 bp) during October 2008.

Fortunately, there are other markets that investors can use to lend or borrow from which it is

possible to infer short-term interest rates. For example, an investor can borrow by entering into a

long position in a forward contract and selling the underlying asset. Similarly, an investor can lend

by shorting a forward and buying the underlying asset. If this transaction is performed through an

organized exchange, standard features such as margin requirements and the existence of a clearing

corporation significantly reduce the credit risk of the transaction. Also, since derivatives contracts

1These two interest rates also carry inflation risk since they are both nominal rates.

2

Figure 1: Interest Rates During the 2007-08 Credit Crisis

are in zero net-supply, flight-to-liquidity problems are mitigated. Thus, derivatives markets offer

a unique laboratory to extract a short-term borrowing and lending rate available to all investors

that is free from liquidity and credit risks.

In perfect markets, it is well-known that the cost of carrying a forward position should be equal

to the risk-free rate minus the underlying asset’s dividend yield. Thus, in frictionless markets it is

possible to use forward and futures contracts as substitutes for risk-free bonds to derive risk-free

rate estimates. In reality, though, there are costs faced by agents when they want to borrow funds or

short-sell the risky asset. As a result, if a group of agents borrow funds using the derivatives market,

the equilibrium derivative price should reflect the costs associated with borrowing to preclude

arbitrage opportunities. Here the assumption is that agents borrowing through the derivatives

market generate demand pressure for the derivative, affecting its price because of the borrowing

costs. A similar effect follows if a group of agents generate demand pressure in the derivatives

market to short-sell the risky asset. Thus, in the presence of borrowing and short-selling costs, the

implied interest rate obtained by inverting the cost-of-carry formula is not equal to the risk-free

rate.

In Section 2 I study implied risk-free rates from futures and put-call parity relations written

on major indexes: S&P 500, Nasdaq 100 and Dow Jones Industrial Average (DJIA). I find that

3

on average implied interest rates from both futures and options lie between Treasury and LIBOR

rates. From January 1998 to December 2007, three-month rates implied from futures prices are on

average 48 bp above Treasury and 5 bp below LIBOR, whereas implied interest rates from options

are on average 50 bp above Treasury and 3 bp below LIBOR. Thus, implied interest rates are very

similar regardless of whether they are extracted from futures or options, and are on average much

closer to borrowing (LIBOR) rather than lending (Treasury) rates. This result is consistent with

the common industry practice of using LIBOR rates as a proxy for the risk-free rate when valuing

derivatives contracts, and also with previous findings in the literature (Brenner and Galai, 1986).

Interestingly, the time-series of implied interest rates do not resemble that of benchmark interest

rates such as the three-month T-bill rate or LIBOR, but instead is much more volatile. I argue

that the volatility in the implied short-term rate in futures and option markets is due to frictions

arising from borrowing and short-selling costs. In the presence of such costs, an arbitrageur that

provides liquidity in a particular derivatives market will be unable to hedge the derivative perfectly

if she is exposed to exogenous demand shocks. In this case demand imbalances for the derivative

will affect prices, in a similar manner as in the model originally studied by Garleanu, Pedersen, and

Poteshman (2007) for option markets and Vayanos and Vila (2007) for the fixed-income market.

Thus, implied interest rates are correlated with demand increasing their volatility and affecting

their level.

In Section 3 I formalize this argument and derive a continuous-time equilibrium model of the

futures market where demand imbalances from traders affect the implied interest rate2. There

are two types of agents: arbitrageurs and traders. Arbitrageurs operate in a competitive market

in which there are no-arbitrage opportunities. Traders can be speculators or hedgers, although

I do not distinguish between them and assume that all traders have an exogenous demand for

the derivative. In order to derive a closed-form solution for the model, I make the simplifying

assumption that borrowing costs increase linearly with demand. The assumption is consistent with

the fact that borrowing rates may differ from lending rates, and that it is more expensive to borrow

larger amounts of the riskless or risky asset.

If traders’ demand is positive, then arbitrageurs short the derivative, buy the risky asset and

2Even though I specialize the model to price futures contracts, it can be extended to price other derivatives aswell.

4

borrow. In equilibrium, arbitrageurs borrow when traders’ demand is positive, which is precisely

when borrowing costs are high. In a competitive market, arbitrageurs set the price of the derivative

such that they are indifferent between taking the opposite side of the trade or do nothing. This

equilibrium price will be higher than the price obtained in an otherwise equivalent frictionless

economy. A similar logic applies if traders want to short the derivative. In that case, arbitrageurs

buy the derivative, short the underlying asset and pay short-selling costs. In equilibrium, the price

of the derivative should be set lower than in an otherwise equivalent frictionless economy in order

to motivate arbitrageurs to take the long position. Thus, the implied interest rate depends on the

“true” risk-free rate and a latent demand factor. The idea that the “true” risk-free rate is a latent

variable that cannot be observed but that can nevertheless be estimated from traded assets goes

back at least to Black (1972).

I estimate the model using S&P 500 index futures and the Kalman filter in Section 4. This

is possible because the model delivers a closed-form solution for the valuation of futures contracts

and the state-variables follow a system of Gaussian processes. I estimate sixteen parameters by

maximizing the likelihood function of price innovations. An interesting result that follows from the

estimation is that the demand factor is significantly priced. Thus, borrowing cheap by using the

futures market is risky.

In Section 5 I show that the risk-free rate that results from this estimation has similar time-

series properties as Treasury and LIBOR rates. The estimated spot risk-free rate is on average

15 bp above the fed funds rate, and estimated short-term rates are on average lower than implied

rates computed in Section 2. Most interestingly, it seems to be forecasting the Federal funds rate,

suggesting that futures markets anticipate changes in short-term interest rates. Also, the spread

between LIBOR and the risk-free rate is high in periods of market stress, as proxied by the VIX

and the credit spread between AAA and BAA bonds. The spread between the risk-free rate and

three-month T-bill rates is high in periods of market illiquidity. These results suggest that the

estimated risk-free rate is less affected by liquidity and credit risk than Treasury rates and LIBOR,

respectively. On the other hand, the latent demand factor is priced, which is in line with previous

findings in the literature (Figlewski, 1984). Hence, arbitrageurs are exposed to an additional source

of risk when taking a position in the futures market, i.e. “index arbitrage” is risky.

I finalize the paper by verifying that the latent demand factor is related to proxies for demand

5

pressure in the futures market, such as large speculator positions in S&P 500 futures and investor

sentiment (Han, 2008). Also, I find that the latent demand factor is positive (negative) when

buying (selling) pressure is high and it is difficult to borrow (short-sell the underlying). Despite

the fact that these two empirical results are interesting on their own right, they put the model on

solid ground. Finally, I look at whether latent demand imbalances co-move across instruments and

markets. Since the demand factor is essentially capturing the difference between the no-arbitrage

price in a market without frictions and observed prices, it is possible to obtain estimates of this

factor for other indexes and also put-call parity relations. I find that mispricings in futures and

put-call parity relations in the three indexes studied in Section 2 are significantly correlated between

each other and also with the sentiment proxy, suggesting co-movement in demand imbalances across

instruments and markets.

1.1 Related Literature and Discussion

While there is a huge literature on dynamic term structure modeling3 using Treasury bonds and

LIBOR rates, the use of derivatives for extracting information about the risk-free rate has been

mostly ignored by financial economists. A notable exception is Brenner and Galai (1986), who are

probably the first to estimate implied risk-free rates from put-call parity relations on stock option

prices. In related work, Brenner, Subrahmanyam, and Uno (1990) also look at implied risk-free

rates using Nikkei index futures data. Liu, Longstaff, and Mandell (2006) obtain implied risk-free

rates from plain-vanilla swap contracts, but they use the three-month General Collateral (GC) repo

rate as a proxy for the three-month risk-free rate. I make no initial assumptions about what the

risk-free rate should be. Feldhutter and Lando (2008) also use swap data to estimate the risk-free

rate. However, I use a much larger time-series and I cross-validate my implied rate with different

assets. I also account for the fact that demand pressure can affect derivatives prices, distorting

implied risk-free rate estimates in significant ways.

This study also contributes to the literature that studies index futures arbitrage4. The main

3This literature is too large to put all the references here. Two recent surveys of the field are Dai and Singleton(2003) and Piazzesi (2003).

4See, for example, Modest and Sundaresan (1983), Kawaller, Koch, and Koch (1987), Brenner, Subrahmanyam,and Uno (1989), Brenner et al. (1990), Yadav and Pope (1990), Chung (1991), Klemkosky and Lee (1991), Subrah-manyam (1991), Bessembinder and Seguin (1992), Chan (1992), Sofianos (1993), Miller, Muthuswamy, and Whaley(1994), Neal (1996), Roll, Schwartz, and Subrahmanyam (2007).

6

focus of this literature has been to understand absolute mispricings, whereas this paper contributes

understanding the sign and magnitude of mispricings.

Finally, this paper fits into a broader literature that looks at how market frictions prevent

arbitrageurs in some circumstances from profiting of arbitrage opportunities5. Effectively, I show

that borrowing costs open a channel through which demand imbalances in the derivatives market

can affect no-arbitrage prices, even when the payoff is linear in the underlying asset.

2 Implied Interest Rates

I start this section by analyzing the problems of two interest rates commonly used by academics and

practitioners, which serves as a motivation for the study of implied interest rates from derivative

contracts. I then present summary statistics on implied interest rates computed from futures

contracts and synthetic forwards derived from put-call parity relations for three major indexes. In

a frictionless market, the implied interest rate from these contracts should correspond exactly to

the risk-free rate in order to prevent arbitrage opportunities. However, the time-series of implied

interest rates do not resemble that of benchmark interest rates such as the three-month T-bill

rate or LIBOR, but instead is much more volatile, which I argue is due to frictions arising from

borrowing and short-selling costs.

2.1 Market Rates

It is common for empirical researchers in finance to use the yield on Treasury bills as a proxy for the

short-term risk-free rate. The intuition for this practice is simple: Treasury bills are backed by the

full faith and credit of the U.S. government. As such, they are the safest investment available for an

investor whose consumption is denominated in U.S. dollars. However, there is now a large literature

documenting discrepancies between Treasury and other interest rates. Some authors suggest that

these discrepancies might be due to transaction costs and taxes6, while other authors argue that

investors perceive a convenience yield from owning a treasury security7. A major implication of

5See, for example, Shleifer and Vishny (1997), Xiong (2001), Gromb and Vayanos (2002), Duffie, Garleanu, andPedersen (2002), Liu and Longstaff (2004), Kondor (2007).

6See, for example, Amihud and Mendelson (1991), Kamara (1994), Elton and Green (1998), Strebulaev (2002)7See, for example, Jarrow and Turnbull (1997), Longstaff (2004), Krishnamurthy and Vissing-Jorgensen (2008)

7

this literature is that using Treasury rates to price real and financial assets might introduce pricing

errors.

On the other hand, it is common for practitioners to use LIBOR rates as a proxy for the risk-free

rate when valuing derivative contracts. Indeed, as noted by Hull (2002, p. 94),

“[...] banks and other large financial institutions tend to use the LIBOR rate rather

than the Treasury rate as the “risk-free rate” when they evaluate derivatives trans-

actions. The reason is that financial institutions invest surplus funds in the LIBOR

market and borrow to meet their short-term funding requirements in this market. They

regard LIBOR as their opportunity cost of capital.”

Even though LIBOR is an interest rate charged on uncollateralized loans between banks, and

hence is subject to credit risk, there are several authors that argue that LIBOR carries very low

credit risk. For example, Collin-Dufresne and Solnik (2001) and Grinblatt (2001) indicate that

LIBOR rates are almost risk-free since they are refreshed top-credit-quality rates. Feldhutter and

Lando (2008) find that the default-risk embedded in LIBOR rates does not contribute significantly

to the long-term swap spreads.

However, during the 2007-08 credit crisis LIBOR rates have increased above “normal” levels.

Figure 1 in the introduction shows the evolution over time of Treasury and LIBOR rates from

January 2006 until October 2008. The two traditional benchmarks that academics and practitioners

generally use, Treasury and LIBOR rates, respectively, have being drifting apart during this period.

The so-called TED spread, defined as the difference between LIBOR and Treasury rates was during

October 2008 at an all time high (461 bp).

Moreover, the TED spread has varied significantly during the time of this study. Figure 2 plots

the TED spread from January 1989 to December 2007. Even though this spread has never been as

high as during the 2007-08 credit crisis, it has been higher than 100 bp during several periods.

Moreover, using only Treasury or LIBOR rates can be misleading. Treasury bills are issued by

the U.S. government and might be considered closer to a lending rate to a representative investor.

Even though it is easy for an investor to buy Treasury securities, frictions prevent them from

borrowing at that rate. Similarly, LIBOR rates are usually used to measure the cost of borrowing

for banks and other financial institutions which makes them closer to a borrowing rate.

8

The previous analysis highlights the difficulty in determining which interest rate is the best

proxy for the risk-free rate. This is problematic because the risk-free rate is a required input in

the valuation of real and financial assets, and in many standard financial theories like the CAPM,

APT, and the option pricing model.

2.2 Implied Interest Rates in a Market without Frictions

Fortunately, there are other markets that investors can use to lend or borrow from which it is

possible to infer short-term interest rates. For example, an investor can borrow by entering into a

long position in a forward contract and selling the underlying asset. Similarly, an investor can lend

by shorting the forward and buying the underlying. If this transaction is performed through an

organized exchange, standard features such as margin requirements and the existence of a clearing

corporation significantly reduces the credit risk of the transaction. Also, since derivative contracts

are in zero net-supply, flight-to-liquidity or flight-to-quality problems are avoided. Thus, derivative

markets offer a unique laboratory to extract a short-term borrowing and lending rate available to

all investors that is free from liquidity and credit risks.

It is a well-known fact that in a frictionless market the futures8 price is given by the so-called

cost-of-carry formula:

Ft(τ) = St exp((Rt(τ)− δt(τ))τ), (1)

where τ is the maturity of the contract, Ft(τ) is the futures price, St is the spot price, δt(τ) is the

annualized dividend yield from time t up to time t+ τ , and Rt(τ) is the risk-free rate. Thus, if the

futures and the spot prices are known, it is possible to compute an implied interest rate as:

Rt(τ) =1τ

log(Ft(τ)St

)+ δt(τ). (2)

The absence of arbitrage opportunities in perfect markets requires that Rt(τ) is the current risk-free

zero-rate for maturity τ . Any deviation from equation (2) would represent an arbitrage opportunity,

the existence of a friction, or a combination of both.

A similar procedure can be applied to synthetic forward contracts derived from option prices.

8For simplicity, in this section I do not consider any convexity adjustment on futures prices due to stochasticinterest rates.

9

An implied interest rate from options can be obtained by inverting the put-call parity relation:

Rt(τ) = −1τ

log

(Ste−δt(τ) − Ct(K, τ) + Pt(K, τ)

K

), (3)

where Ct(K, τ) and Pt(K, τ) are the prices of a call and a put option with maturity τ and strike

K, respectively. It is important to note that this relation is exact only if the options are European,

which is the case for options on the indexes that I include in the analysis. Also, the implied rate is

independent of the moneyness of the options.

2.3 Data

In this paper I use futures and options on three major indexes: S&P 500, Nasdaq 100 and Dow

Jones Industrial Average (DJIA). The period I study in this section is from January 1998 to June

2007, because DJIA futures and options only start trading after January 1998, and options data is

available until the end of June 2007. In a subsequent section, I present results that span a longer

time period (January 1989 to December 2007) in which I only use S&P 500 futures contracts.

Ideally, it would be interesting to look at a wide array of underlying assets and different deriva-

tives to obtain more precise estimates of implied interest rates. However, there are some restrictions

on the array of instruments or underlying assets available. First, if the underlying pays a dividend,

it is necessary to estimate that dividend with precision. Second, in the case of options, the put-call

parity relationship only holds exactly for European options. Third, it is important for the deriva-

tives used in the analysis to be liquid and actively traded. For these reasons I study futures and

options written on those three major indexes. Dividends on these indexes are observed and can be

easily forecasted. Also, options on these indexes are European and put-call parity relations hold

exactly. Finally, futures and options on these indexes, specially on the S&P 500, are very liquid

and trade for a wide arrange of maturities and, in the case of options, strike prices.

2.3.1 Dividends

Dividend data for each index is obtained from Bloomberg, and is available starting January 1988

for the S&P 500, and January 1993 for Nasdaq and DJIA indexes, respectively. The top panel

of Figure 3 displays the average dividend yield per year and per index. The dividend yield has

10

been on average increasing slowly for all indexes during the time period. Also, it is highest for the

DJIA, followed very closely by the S&P 500. Nasdaq 100 has very low dividend yields as would

be expected from technology stocks, although its dividend yield has increased significantly in the

last years. Nevertheless, year to year variations are small indicating that dividends are highly

predictable, at least for up to 12 months.

Despite year to year predictability, dividend payments are highly seasonal within the year.

The bottom panel of Figure 3 shows that dividend payments peak in February, May, August and

November for all indexes. The difference between a high dividend yield month and a low dividend

yield month can be significant, specially for the DJIA and the S&P 500.

In order to take into account the seasonality of dividend payments I compute the dividend yield

at time t for each contract expiring at time t+ τ as:

δt(τ) =1τ

(t+τ−1∑n=t−1

dnSn

),

where dn is the ex-dividend payment in dollars at day n and St is the index cash price at time t.

Since variation in dividend payments from year to year is small, this estimate of the dividend yield

is likely to (Roll et al., 2007), at least for up to one year. It is important to note, however, that

market participants might have better information of future dividend yields at the time they trade

index futures and option contracts. This is turn can have an impact on implied interest-rates.

2.3.2 Futures and Options

Data on S&P 500, Nasdaq 100 and DJIA futures starts in January 1983, May 1996 and January

1998, respectively, and is obtained from Bloomberg. There are several contracts available for trading

on each index with maturities ranging from 3 to 24 months. All contracts expire the third Friday

of March, June, September, and December of each year. Thus, every three months a new contract

is issued. Despite the fact that there are eight maturities available for trading in S&P 500 futures,

trading concentrates heavily in the first three contracts with the shortest maturity. Among all

indexes, S&P 500 futures are by far the most traded and hence the most liquid contract.

Table 1, Panel A presents summary statistics of the percentage of open interest by maturity in

S&P 500, Nasdaq 100 and DJIA futures contracts from January 1998 to December 2007. For each

11

index the table summarizes the proportion of open interest for three, six, nine, and twelve-month

contracts, respectively, with respect to the total open interest on that day for a given contract. On

average, a very large proportion of the total open interest concentrates in the closest-to-maturity

contract. The twelve-month contract contributes to less than 1% of the total open interest for all

indexes. For this reason I follow Roll et al. (2007) and include in my analysis only the three, six,

and nine-month contracts.

Data on S&P 500 and Nasdaq 100 options starts in January 1996, while for DJIA it starts in

January 1998, and is obtained from OptionMetrics. Options on indexes also follow the issuance

cycle of futures contracts. The main difference in terms of data availability with respect to futures

is that for each maturity there are several options with different strike prices. Table 1, Panel B

presents summary statistics of the percentage of open interest by maturity in S&P 500, Nasdaq

100 and DJIA options contracts from January 1998 to December 2007. For each stock index the

table summarizes the proportion of open interest for three, six, nine, and twelve-month options,

respectively, with respect to the total open interest on that day for a given contract. As with futures,

on average a very large proportion of the total open interest concentrates in the closest-to-maturity

option contracts. However, more open interest is observed in the longer maturity contracts than

for futures. For options, the twelve-month contract contributes on average to approximately 5% of

the total open interest for all indexes.

2.4 Results

Table 2 presents summary statistics for implied interest rates obtained from stock index (S&P 500,

Nasdaq 100, and DJIA) futures and put-call parity relations, for the period January 1998 to June

2007. I also compare these results with Treasury and LIBOR interest rates. In the table all rates are

continuously compounded. Treasury and LIBOR rates are presented for three, six and twelve-month

maturities. Treasury rates are Constant Maturity Treasuries (CMTs) rates obtained from the U.S.

Department of the Treasury. Implied rates from futures are computed using equation (2) and are

presented for three, six and nine-month contracts, and also for the daily cross-sectional average of

all three indexes. Implied rates from put-call parity relations are computed using equation (3) and

are averaged across strikes for each index for maturities ranging from 30 to 90 days, 90 to 180 days,

180 to 270 days, and 270 to 365 days. For options, only contracts with a volume greater than 10

12

contracts for calls and puts at the same strike and on the same day are included. Also, I discard

all calls and puts for a given strike for which the absolute put-call parity violation defined as

∣∣∣∣∣Ct(K, τ)− Pt(K, τ)− Ste−δt(τ) +Ke−rt(τ)

0.5 (Ct(K, τ) + Pt(K, τ))

∣∣∣∣∣ ,and computed using either Treasury or LIBOR, is more than 50%. This filteris used to avoid some

extreme observations affecting the results.

As can be seen from Table 2, average implied rates from futures and options are very similar.

The difference between the three-month rate obtained from futures contracts differs only 2 bp from

the same rate obtained from all options, while the same difference is 10 and 5 bp for the six and

nine-month implied rate. Also, both implied rates are on average between Treasury and LIBOR

rates, although the implied rate is closer to LIBOR (borrowing) than Treasury (lending). This fact

is consistent with the original finding in Brenner and Galai (1986) using a different time period

and contracts.

Interestingly, the time-series of implied interest rates do not resemble that of benchmark interest

rates such as the three-month T-bill rate or LIBOR, but instead is much more volatile, specially at

short maturities. For example, the standard deviation of three-month implied interest rates from

futures and options is 2.78% and 2.36%, respectively, whereas for three-month T-bill and LIBOR

is 1.66% and 1.88%, respectively. If this is just serially uncorrelated measurement error, it should

be possible to avoid part of it by taking averages during a longer period of time. Figure 4 shows

monthly averages from January 1998 to December 2007 for the interest rates described in Table 2.

The figure displays three-month interest rates and shows that implied interest rates follow closely

the other two market rates, as is expected by the results presented in Table 2. However, there are

periods of time during which bothrates move in the same direction away from Treasury or LIBOR

rates. This is surprising since both implied rates are obtained from different sources (futures and

option prices).

2.5 Discussion

I argue that the volatility in the implied short-term rate in futures and option markets is due to

frictions arising from borrowing and short-selling costs. In the presence of such costs, an arbitrageur

13

that provides liquidity in a particular derivatives market will be unable to hedge the derivative

perfectly if she is exposed to exogenous demand shocks.

In perfect markets, the risk-free rate measures the price of borrowing and lending unlimited

units of the numeraire at any given point in time. In real markets, however, agents face borrowing

costs that prevent them from borrowing unlimited amounts of funds (see e.g. Black, 1972) or other

securities (see e.g. D’Avolio, 2002). Therefore, in real markets the risk-free rate represents a latent

variable over which borrowing costs have to be incorporated to obtain the final cost of a trading

strategy.

An agent that enters into a large short position in a futures contract will hedge it by buying

the risky asset and shorting the riskless asset. If there are borrowing costs, the futures price should

be higher than in an otherwise equivalent frictionless economy to incentive the agent to hold the

position. Similarly, an agent who enters into a long position in a futures contract will hedge it

by shorting the risky asset and buying the riskless asset. If there are short-selling costs, she will

require the futures to be priced lower relative to the price in an otherwise equivalent frictionless

economy.

In equilibrium, however, the impact of borrowing costs on the price of the derivative will depend

on the aggregate demand. For example, if an agent wants to long a futures contract because of

hedging purposes, and another agent wants to short the same contract for a similar reason, the

equilibrium futures price might actually be equal to the no-arbitrage price in a frictionless economy.

On the other hand, if an agent wants to long a futures but there are no other counterparts with

the same need, she might be willing to pay more for the long position than the cost-of-carry price

presented in equation (1). Therefore, the presence of borrowing costs for either the risk-free or the

risky asset will have an impact on the implied interest rate if there are demand imbalances for long

or short positions.

3 A Model with Borrowing and Short-Selling Costs

In this section I derive a continuous-time equilibrium model of the futures market where demand

imbalances from traders affect the implied interest rate. I derive a closed-form solution of the

futures price that depends on the “true” risk-free rate and a latent demand factor. This valuation

14

formula will prove useful when estimating the model and extracting the latent factors from the data.

I specialize the model to futures contracts because I use S&P 500 futures prices in the estimation.

However, the model can be adapted to price other derivatives as well.

3.1 Economic Environment

3.1.1 Economy

I consider a continuous-time economy with a finite horizon T in which is defined a probability space

(Ω,F ,P), and a filtration FtTt=0 satisfying the usual conditions (see e.g. Karatzas and Shreve,

1998, Section 2.7). There is a single consumption good that acts as the numeraire. The economy

is populated by a continuum of two types of agents: arbitrageurs and traders. The economy is

competitive, all agents are price takers and there exists a representative agent of each type.

The arbitrageur can buy or sell in any amount a risky asset St, a locally risk-free asset Mt

which can be thought as a money-market account, and futures contracts Ft(τ) written on the risky

asset for a continuum of maturities τ ∈ (0, T ]. The prices of the risk-free and the risky asset are

exogenously given.

Futures contracts are financial instruments that are traded in organized exchanges. A particular

feature of these contracts is that they are continuously marked-to-market9, so any profit or loss

accrues immediately to the owner of the contract.

Another feature of futures contracts is that market participants are required to keep a margin

account at the exchange. An initial margin is required to start trading and traders receive margin

calls whenever their margin account drops below a certain predetermined level. In this model,

however, I abstract from margin requirements because the arbitrageur is constrained to maintain

a strictly positive wealth at all times, as will be studied in the next subsection.

Traders are investors who have an exogenous demand for futures contracts which might be

driven by hedging or speculative reasons. They are similar to option’s “end users” in Garleanu

et al. (2007) or “clientele investors” in Vayanos and Vila (2007). While it is possible to motivate

why investors might want to hold call and put options, or risk-free bonds of a certain maturity,

it is more difficult to motivate the demand for futures contracts since their payoffs are essentially

9See, for example, Cox, Ingersoll, and Ross (1981), Jarrow and Oldfield (1981), Duffie and Stanton (1992).

15

linear in the risky asset. Therefore, in this model traders do not have specific reasons to trade in

the futures market. I show later that for S&P 500 index futures the empirical evidence suggests

that “traders” in that market are large speculators that trade because of “sentiment reasons” , i.e.

they take long positions when they are bullish and short positions when they are bearish.

3.1.2 Arbitrageurs

The arbitrageur is a fully rational risk-averse agent that derives utility from consumption and

is compensated for the risks and costs associated with providing liquidity to other investors. In

contrast with traders that might want to speculate or hedge only part of their exposure to the

risky asset, the arbitrageur holds an optimal portfolio that allows her to hedge her position in the

futures market.

In the model, the arbitrageur also has the role of a liquidity provider. The reason I call this

agent an arbitrageur is that in equilibrium she is the only agent that “arbitrages away” any price

discrepancy by either increasing or decreasing her demand for futures contracts. However, the

arbitrageur does not make abnormal profits since by construction the market is competitive and

there are no arbitrage opportunities. Therefore, the arbitrageur will price the futures contracts at

the marginal cost of carrying forward her position.

The arbitrageur is endowed with a strictly positive wealth W0 and consumes continuously at

a rate Ct up to an arbitrary time T . At each point in time the arbitrageur holds a self-financing

portfolio consisting of Zft (τ)τ∈(0,T ] futures contracts for each maturity τ , Zmt units of the riskless

asset, and Zst units of the risky asset. Since futures contracts are continuously marked-to-market

and the gains or losses are credited to the arbitrageur’s money-market account, the futures position

is not included in the arbitrageur’s wealth computation. The market value of the arbitrageur’s

wealth at time t is given by:

Wt = Zmt Mt + Zst St. (4)

Since the arbitrageur’s portfolio is self-financing, the wealth evolution equation of the arbitrageur

satisfies:

dWt =∫ T

0Zft (τ)dFt(τ)dτ + Zmt dMt + Zst dSt + ZstDtdt− Ctdt. (5)

The first term in (5) describes the mark-to-market feature of futures contracts. After entering into

16

a futures position of Zft (τ) contracts for each maturity, all gains or loses dFt(τ) over the next time

interval are credited to the arbitrageur’s account, resulting in a total cash-flow of Zft (τ)dFt(τ) for

all τ ∈ (0, T ]. The other terms are standard.

In order to rule out arbitrage opportunities, some restrictions need to be imposed on the array

of trading strategies available to the arbitrageur (Harrison and Kreps, 1979). One way to rule

out arbitrage opportunities is to directly impose constraints on the trading strategies, as shown

by Harrison and Kreps (1979) and Harrison and Pliska (1981). An alternative way to achieve the

same goal, which is the one I follow in this paper, is to require the arbitrageur to keep her wealth

strictly positive at all times, i.e. Wt > 0 for all t ∈ [0, T ] (Dybvig and Huang, 1988). This positivity

constraint on wealth rules out arbitrage opportunities by indirectly limiting the array of trading

strategies available to the arbitrageur. It also rules out the possibility of bankruptcy, which is

consistent with the fact that the arbitrageur is not required to maintain a margin account in the

futures exchange. Finally, it simplifies the portfolio choice analysis because it is then possible to

work with returns on wealth rather than the level of wealth itself.

Using equation (4) and because of the positivity constraint on wealth, it is possible to rewrite

(5) asdWt

Wt=∫ T

0zft (τ)

dFt(τ)Ft(τ)

dτ + (1− zst )dMt

Mt+ zst

(dStSt

+ δdt

)− ctdt, (6)

where zft (τ) =Zft (τ)Ft(τ)

Wtis the total value of the futures position per dollar of wealth, zst =

Zst StWt

is the percentage of wealth invested in the risky asset, and ct =CtWt

is the proportion of wealth

that is continuously consumed.

The arbitrageur’s problem is to dynamically choose a consumption rate ct and a portfolio

φt = zft (τ)τ∈(0,T ], zst , for all t ∈ [0, T ], so as to maximize

E0

(∫ T

0e−ρt log(Ct)dt

). (7)

The choice of this preference structure in dynamic portfolio choice problems is standard (see e.g.

Xiong, 2001, Liu and Longstaff, 2004, Vayanos and Vila, 2007). It is important to note that the

problem is well-defined because the wealth is required to be strictly positive at all times. If this

was not the case, the arbitrageur could borrow funds to finance any desired consumption stream

17

and pay her debt by using a doubling strategy. This would allow her to achieve any desired level

of wealth in a finite amount of time10.

3.1.3 Traders

In this economy, each trader has a demand for futures contracts at one or several maturities. The

demand for each contract can be either positive or negative, depending on weather she wants to

take a long or a short position, respectively. Therefore, the aggregate demand from traders includes

the netting out of opposite positions.

Traders’ demand for futures contracts is given by:

H(Xt, τ) = λ(τ)Xt, (8)

where λ(τ) is a deterministic function of maturity and Xt is an unobserved factor. The function

λ(τ) can be thought as the term structure of the demand for futures contracts. This demand

function is general enough to accommodate for different demand term-structures, although the

demand is driven by a single factor, implying that demand shocks at all maturities are perfectly

correlated. This restriction, however, can be easily relaxed by allowing for more factors in equation

(8).

The demand factor Xt is stochastically cointegrated with arbitrageurs wealth Wt such that

Xt = xtWt,

where xt is an unobserved factor that follows a mean-reverting process

dxt = −κxxtdt+ σxdwxt , (9)

and wxt is a Brownian motion under P .

This cointegrating relationship is necessary to obtain a stationary equilibrium. If the demand for

10It can be shown that if the problem admits a solution, the arbitrageur’s risk aversion is inversely related to thelevel of wealth. As the wealth approaches zero, the absolute risk aversion goes to infinity. In this case, one might beinclined to conclude that whenever the wealth of the arbitrageur approaches zero, she will trade so as to keep herwealth positive at all times. However, the positivity of wealth is actually necessary to solve the problem in the firstplace, and not a consequence of the arbitrageur having a concave utility.

18

futures contracts is too high, futures prices will increase so as to accommodate the excess demand,

making it profitable for other arbitrageurs to enter the market. This will have the long-run effect of

increasing the arbitrageur’s wealth, keeping the ratio Xt/Wt stationary. Similarly, if the demand is

too low, it might be profitable for some arbitrageurs to leave the market, decreasing the wealth of

the arbitrageur. Because by construction the arbitrageur’s wealth is strictly positive, the demand

factor xt is well-defined.

3.1.4 Assets

The price St of the risky asset follows a geometric Brownian motion

dStSt

= µsdt+ σsdwst , (10)

where wst is a Brownian motion under P correlated with wxt such that (dwst )(dwxt ) = ρsxdt. In order

to simplify the results I denote by vij = ρijσiσj ,∀i, j ∈ s, x, and uij = [Σ−1]ij , ∀i, j ∈ s, x,

where Σ = (vij)i,j∈s,x is a covariance matrix.

The risky asset pays a continuous dividend Dt = Stδ, where the dividend yield δ is a constant.

Even though in many cases the assumption of a constant dividend yield might not seem adequate,

it greatly simplifies the results. Nevertheless, the model could easily be modified to incorporate a

stochastic dividend yield process.

The value Mt of the risk-free asset at time t solves, for a strictly positive initial investment M0,

dMt

Mt= rtdt. (11)

where rt is the arbitrageur’s net funding cost. The risk-free asset is a bank account where the

arbitrageur can make deposits or borrow funds as needed.

If the risky asset is an index, there are costs associated with selling short the index constituents

(D’Avolio, 2002) and borrowing funds11 (Black, 1972). The funding cost faced by the arbitrageur

11There might be other costs associated with either borrowing funds or selling short the risk asset, like informationasymmetry, reputation or liquidity.

19

is included in the return on the money-market account such that

rt = r + ϑxt, (12)

where r is the risk-free rate. The intuition behind this modeling choice is as follows. If traders take

a long position in futures contracts, the arbitrageur will take a short position in the futures market.

In order to hedge the additional risk carried by the futures, the arbitrageur will simultaneously

take a long position in the risky asset. If this position is sufficiently large, she will have to borrow

inducing borrowing costs. Equivalently, if traders short the futures, the arbitrageur will have to

take the opposite position in the futures market and hedge it by selling the risky asset. If the

shorting demand by traders is sufficiently large, the arbitrageur will have to sell short the risky

asset, incurring in short-selling costs. If there are no frictions, i.e. if ϑ = 0, then the return on the

money market account should be the risk-free rate to prevent arbitrage opportunities.

In this model borrowing costs depend on the traders’ demand xt and not on the arbitrageur’s

own demand for the risky asset zst . The reason for this is that I consider a fully competitive market

and do not allow for strategic behavior from the part of the arbitrageur. The analysis, however,

could be modified to account for strategic behavior.

3.2 Equilibrium

3.2.1 Portfolio Choice Problem

The optimal consumption and portfolio choice is solved using standard dynamic programming

methods. The value function J(Wt, xt, t) depends current wealth Wt and the demand factor xt.

The Bellman equation for the arbitrageur’s problem is

maxct,φt

e−ρt log(Ct)dt+ EtdJt = 0, (13)

such that J(WT , xT , T ) = 0. It is a well known fact (e.g. Merton, 1971) that under logarithmic

utility the consumption and portfolio choice is independent of other state variables. The following

lemma just makes explicit this fact in the context of this particular application.

20

Lemma 1 If the arbitrageur’s problem is given by (13), then her portfolio choice problem φt for

t ∈ [0, T ] is equivalent to solving

maxφt

1dtEt

(dWt

Wt− 1

2

(dWt

Wt

)2). (14)

Proof. See the appendix.

Under logarithmic utility, the arbitrageur’s value function is separable12. This means that the

optimal consumption and portfolio choice depend only on the evolution of wealth. The arbitrageur’s

problem is then equivalent to maximizing a simple quadratic utility function over instantaneous

returns on wealth. A similar result is obtained if the arbitrageur only consumes at time T (Liu and

Longstaff, 2004).

As shown in the appendix, by solving equation (14) and imposing the equilibrium condition

that the aggregate demand for futures contracts for all maturities should be zero, it is possible to

derive the equilibrium futures price, as stated in the following proposition.

Proposition 1 If the function λ(τ) is such that β is the unique solution to

β =∫ T

0λ(τ)ξ(κx, τ)dτ, (15)

where κx = κx + ϑ

(uxs − βuxx

), and ξ(κ, τ) =

1− e−κτ

κ, then the economy admits a unique equilib-

rium futures price given by

F (St, xt, τ) = St exp (a(τ) + ϑξ(κx, τ)xt) , (16)

where

a(τ) = (r − δ)τ +(vsx + κxθx

)( ϑ

κx

)(τ − ξ(κx, τ)) +

12vxx

(ϑ

κx

)2

(τ − 2ξ(κx, τ) + ξ(2κx, τ)) ,

and θx =(

1κx

)(uxsuxx

)(µs + δ).

Proof. See the appendix.

12This is shown in equation (A.1) in the appendix.

21

The existence and uniqueness of the equilibrium futures price relies on the assumption that there

exists a unique solution β for the equation β =∫ T

0 λ(τ)ξ(κx, τ)dτ . Even though this assumption

may seem arbitrary, the function λ(τ) is given exogenously and many functional forms for this

function will generate a unique solution for this equation.

It is easy to see that if ϑ = 0 then the equilibrium futures prices reduces to the well-known

cost-of-carry formula. In a competitive market the cost of carrying forward this position is just

r − δ. I state this observation in the following corollary.

Corollary 1 If there are no frictions, i.e. if ϑ = 0, then the futures price is given by F (St, τ) =

Ste(r−δ)τ .

3.2.2 Risk-Neutral Pricing

It is a well-known fact that, at least in the finite probability case (Harrison and Pliska, 1981), that

the absence of arbitrage opportunities implies the existence of a pricing kernel. In a setting in

which the arbitrageur can borrow and short the risky asset without incurring in any costs, Cox

et al. (1981) show that the futures price is equal to the expected value of the spot price under a

risk-neutral measure Q in which the risky asset drifts at r − δ. It turns out that a similar result

can be obtained in this economy since the positivity of wealth rules out arbitrage opportunities.

The following proposition shows that there exists an equivalent measure Qx such that the futures

price is equal the expected spot price under Qx.

Proposition 2 Let ηst =1σs

[(µs + δ − r)− ϑxt] and ηxt =1σx

[−κxθx + (κx − κx)xt

]be the market

prices of risk of wst and wxt , respectively. Define the measure Qx by its Radon-Nikodym derivative

such thatdQx

dP= exp

(−∫ T

0ηtdwt −

12

∫ T

0ηt · ηtdt

), where ηt = (ηst , η

xt )′ and wt = (wst , w

xt )′.

Then, the futures price in this economy is given by the expectation of the spot price under Qx, i.e.

F (St, xt, τ) = EQx

t (St+τ ),

22

where

dStSt

= (rt − δ)dt+ σsdwst ,

dxt = κx(θx − xt)dt+ σxdwxt ,

rt is defined in equation (12), κx and θx are defined in Proposition 1, and wt = (wst , wxt )′ is a

Brownian motion under Qx.

Proof. See the appendix.

Thus, it is possible to recover a similar result to the traditional frictionless economy in which

ηst and ηxt are the arbitrageur’s local market prices of risk of wst and wxt , respectively.

3.2.3 Stochastic Interest Rates

A natural extension of the model that is relevant in empirical applications is when interest rates

are stochastic. In this case, the arbitrageur faces an additional source of risk that can be hedged if

she is allowed to trade in risk-free bonds, Eurodollar futures or any other claim that is contingent

on the risk-free rate.

In order to keep the model tractable, I consider the case where the risk-free rate follows a

Gaussian one-factor mean-reverting process as in Vasicek (1977). The general model under the

historical measure P is defined as

dst =(µs −

12σ2s

)dt+ σsdw

st , (17)

dxt = −κxxtdt+ σxdwxt , (18)

drt = κr(θr − rt)dt+ σrdwrt , (19)

where st = log(St), wst , wxt and wrt are Brownian motions such that (dwit)(dw

jt ) = ρijdt,∀i, j ∈

s, x, r and ρii = 1, ∀i ∈ s, x, r. I denote by vij = ρijσiσj , ∀i, j ∈ s, x, r, and uij =

[Σ−1]ij ,∀i, j ∈ s, x, r, where Σ = (vij)i,j∈s,x,r is a covariance matrix. The arbitrageur’s funding

cost rt now depends on rt and xt such that rt = rt + ϑxt.

A small modification of the argument used in the proof of Lemma 1 shows that in this case the ar-

23

bitrageur’s portfolio choice problem is to dynamically choose a portfolio φt = zft (τ)τ∈(0,T ], zst , z

rt

so as to solve (14).

In order to allow for additional flexibility in the risk premia induced by the model, I assume

that traders’ demand for futures is given by:

H(Xt, τ) = (λc(τ) + λx(τ)xt + λr(τ)rt)Wt.

Under this setup, it is possible to find the equilibrium futures price as stated in the following

proposition.

Proposition 3 If the function λi(τ) is such that βi is the unique solution to

βi =∫ T

0λi(τ)ξ(κx, τ)dτ, i ∈ c, x, r

where κx = κx + ϑ

(uxs − βxuxx

), and ξ(κ, τ) =

1− e−κτ

κ, then the economy admits a unique equi-

librium futures price given by

F (St, xt, rt, τ) = St exp(a(τ) + ϑξ(κx, τ)xt +

((1 + φ) ξ(κr, τ)− φe−κxτξ(κr − κx, τ)

)rt

),

where φ =(ϑ

κx

)(βr − uxs + uxrψ

r2σr

uxx

), κr = κr + ηr1σr and a(τ) is defined in equation (A.23) in

the appendix.

Proof. See the appendix.

The existence and uniqueness of the equilibrium relies on the fact that βi is a unique solution

to βi =∫ T

0λi(τ)ξ(κx, τ)dτ , for each i ∈ c, x, r. If ϑ = 0, the futures price is equivalent to the

frictionless case like in Schwartz (1997). There is also an analog result for Proposition 2.

Proposition 4 Let ηst =1σs

[(µs + δ)− ϑxt − rt], ηxt =1σx

[−κxθx+ (κx− κx)xt− κxφrt], and ηrt =

1σr

[(κrθr−κrθr)+(κr−κr)rt] be the market prices of risk of wst , wxt and wrt , respectively. Define the

measure Qx by its Radon-Nikodym derivative such thatdQx

dP= exp

(−∫ T

0ηtdwt −

12

∫ T

0ηt · ηtdt

),

where ηt = (ηst , ηxt , η

rt )′ and wt = (wst , w

xt , w

rt )′. Then, the futures price in this economy is given by

24

the expectation of the spot price under Qx, i.e.

F (St, xt, τ) = EQx

t (St+τ ),

where

dStSt

= (rt − δ)dt+ σsdwst , (20)

dxt = κx(θx − xt + φrt)dt+ σxdwxt , (21)

drt = κr(θr − rt)dt+ σrdwrt , (22)

κx, φ, κr and θr are defined as in Proposition 3, θx =(

1κx

)(βc + uxs(µs + δ) + uxrψ

r0σr

uxx

), and

wt = (wst , wxt , w

rt )′ is a Brownian motion under Qx.

Proof. See the appendix.

The market prices of risk are time-varying, and can be expressed in terms of reduced-form

parameters. I estimate this reduced-form version of the model later and extract the latent risk-free

rate and demand factor.

The last result of this section relates the term-structure of the implied interest rate rt with the

term-structure of the risk-free factor rt and the latent demand factor xt.

Proposition 5 The term-structure of implied interest-rates Rt(τ) is given by

Rt(xt, rt, τ) = α(τ) + ϑζ(κx, τ)xt + ((1− φ) ζ(κr, τ) + φe−κxτζ(κr − κx, τ))rt, (23)

where ζ(κ, τ) =1− e−κτ

κτ, α(τ) is defined in equation (A.24) in the appendix, and all the other

parameters are defined in Proposition 4. This term-structure can in turn be decomposed into two

components: the term-structure of the latent risk-free rate Rt(τ)

Rt(τ) =

(θr (1− ζ(κr, τ))− 1

2

(σrκr

)2

(1− 2ζ(κr, τ) + ζ(2κr, τ))

)+ ζ(κr, τ)rt, (24)

and the term-structure of the latent demand factor Xt(τ) ≡ Rt(τ)−Rt(τ).

Proof. See the appendix.

25

The decomposition of implied interest rates is useful, however, only if we can implement it

through the data. In the following section I describe how both factors can be estimated from the

term-structure of futures prices using the Kalman filter.

4 Estimation

I estimate the model defined by equations (17), (18), (19), (20), (21) and (22) using daily S&P 500

index futures prices from January 1989 to December 2007. I choose to estimate the model using

this contract because it has the longest time-series of prices among all index futures and options,

and also because it is the most liquid index futures contract.

Data on the S&P 500 cash index, futures prices, and dividends are obtained at a daily frequency

from Bloomberg. Dividends are computed as described in section 2.3.1. I start my estimation in

January 1989 because detailed daily data on S&P 500 dividends starts only in January 1988. I use

a total of 4788 time-series observations.

There is an important reason to use daily data in the estimation. The no-arbitrage relation

between futures and spot prices could be violated from purely mechanical reasons, like asynchronous

trading between the underlying cash index and futures contracts. For example, Miller et al. (1994)

show that asynchronous trading in the constituents of an index can produce mean-reversion of the

basis, generating the illusion of futures mispricing. Also, the closing futures price is measured at

4:15pm, whereas the closing index price is measured at 4:00pm13. Part of these problems should

be mitigated by the use of daily data since state variable estimates using the Kalman filter are

essentially weighted-averages of current and past observations, and as such behave like moving

averages.

The model is cast in state-space form and estimated using the Kalman filter14. I use the

observed spot price (Sobst ), and the three (F 3M

t ), six (F 6Mt ), and nine-month futures (F 9M

t ) in my

13In a recent paper, Richie, Daigler, and Gleason (2008) show that price discrepancies exist even when the S&P 500Exchange Traded Fund (ETF) is used as the underlying index. The ETF should mitigate staleness and transactioncosts problems, as well as the effects of volatility associated with the staleness of the index.

14The Kalman filter has been used extensively in the finance literature. See, for example, Schwartz (1997), Babbsand Nowman (1999), Duffee (1999) for applications of the Kalman filter to the estimation of commodity, term-structure, and corporate bond models, respectively. For a detailed discussion of state-space models and the Kalmanfilter see, for example, Harvey (1990, Chap. 3).

26

estimation. The measurement equations are given by

log(Sobst ) = st + υobs

t

for the spot price, and

log(F 3Mt

)= a(τ3M ) + st + b(τ3M )xt + c(τ3M )rt + υ3M

t ,

log(F 6Mt

)= a(τ6M ) + st + b(τ6M )xt + c(τ6M )rt + υ6M

t ,

log(F 9Mt

)= a(τ9M ) + st + b(τ9M )xt + c(τ9M )rt + υ9M

t ,

for the futures prices, where st = log(St), a(τ) is defined in equation (A.23), b(τ) = ϑξ(κx, τ),

c(τ) = (1 + φ) ξ(κr, τ)+φe−κxτξ(κr− κx, τ), and τ3M , τ6M , and τ9M are the exact maturities of the

three, six, and nine-month futures, respectively. All the other variables and parameters are defined

in propositions 3 and 4. Since the model only have three state variables but there are four prices,

the estimation is over-identified and I assume that all prices are estimated with some uncorrelated

measurement error υit, i ∈ obs, 3M, 6M, 9M with standard deviation σm. In order to identify the

model, I set the parameter ϑ = 1. Thus, the demand factor xt is a scaled version of the futures

demand as defined in the model.

The transition equations are the Euler time-discretized versions of equations (17), (18), (19):

st+∆t

xt+∆t

rt+∆t

=

(µs − 1

2σ2s

)∆t

0

κrθr∆t

+

1 0 0

0 1− κx∆t 0

0 0 1− κr∆t

st

xt

rt

+

εst

εxt

εrt

,

where εst , εxt and εrt are standardized normal innovations such that Eεitε

jt = ρijσiσj∆t,∀i, j ∈

s, x, r. Since the sampling frequency is daily, this approximation should work well with the

continuous-time model defined by equations (17), (18), and (19).

Parameter estimates are obtained by maximizing the likelihood function of log-price innovations.

The reduced-form of the model has 16 parameters: µs, σs, κx, σx, θr, κr, σr, ρsx, ρxr, ρrs, κx, θx, φ,

κr, θr, and σm. Since the measurement equation is linear in the state-variables and the transition

equations follow a Gaussian process, the estimation is efficient. Standard errors of all parameters are

27

computed by inverting the information matrix. An estimate of the information matrix is obtained

by computing the outer-product of the gradient (see, for example, Hamilton, 1994, p. 143).

Table 3 shows parameter estimates. There are two important results to notice from the table.

The first is that there exists a strong correlation between the demand factor and innovations in

returns. Thus, there is a diversification effect between the demand factor and the underlying cash

index. This positive correlation suggests that the demand factor is high (low) when market returns

are positive (negative), which is consistent with the fact that the demand factor is correlated

with actual demand by large speculators, as shown in Section 5. Also, the correlation between

the demand factor and interest rate innovations is negative, reinforcing the interpretation that

the latent demand factor is high (low) when the market is bullish (bearish). Second, the mean

reverting parameter of the demand factor is different under the P and the Qx–measure, suggesting

the existence of a risk premium. I test for this difference and find that it is statistically significant

at the 1% level. Thus, index futures arbitrage is risky.

5 Risk-Free Rate Analysis

In this section I analyze the risk-free rate that results from the estimation performed in Section 4

and compare it to LIBOR and Treasury rates.

Table 4 presents summary statistics for Treasury, LIBOR, and estimated risk-free interest rates.

Risk-free rates for a specific maturity are computed using equation (24). For comparison, I also

present results for implied interest rates estimated by inverting the cost-of-carry formula. There

are several results from the table. First, the overnight risk-free rate is on average 15 bp higher than

the federal funds rate. Second, implied interest rates have higher means than model estimated

risk-free rates. Third, estimated risk-free rates are on average between Treasury and LIBOR rates,

for all maturities.

The top panel of Figure 5 shows the estimated risk-free spot-rate and the target overnight fed

funds rate from January 1989 to December 2007. Note that this period is different from the one

analyzed in Section 2 since I have nine more years of data. The figure shows that these two rates

are very closely related, implying that the model works well in extracting a meaningful short-term

rate from the futures data.

28

However, the estimated risk-free rate seems to lead the fed target rate, suggesting that futures

markets anticipate changes in short-term interest rates. I test for this predictability in Table 5.

I run a VAR on the estimated risk-free rate and the Fed Target from January 1989 to December

2007. All rates are sampled at the end of each month, and the VAR is run on differences using

three lags. The lag selection is based on the Schwarz information criterion. In order to test for

the predictability, the table also presents the chi-squared value on Granger causality tests. It is

clear from the VAR that changes in the estimated risk-free rate predicts a similar change in the fed

target rate.

The bottom panel of the same figure shows that the three-month risk-free rate also follows very

closely Treasury and LIBOR rates. In general, the estimated risk-free rate is between Treasury

and LIBOR, specially in periods when the TED spread widens. However, during other periods of

time this rate is either below Treasury or above LIBOR. These are usually times when the TED

spread is low and interest rates are changing. During those periods, if the latent risk-free rate is

forecasting large changes in interest rates, it might be either higher than LIBOR or below Treasury

rates depending on the direction of the change.

A related question that provides additional support for the model concerns the analysis of

the spread between Treasury yields and the estimated risk-free rate for a particular maturity. It

has been argued in the literature that Treasury yields contain a convenience yield due to flight-

to-liquidity episodes (Longstaff, 2004). In order to proxy for times in which Treasury securities

become more valuable to local investors, I use two proxies that are similar to some of the variables

used by Longstaff (2004). The first proxy is the log-change in Treasury Bill holdings by foreign

investors. A decrease in the Treasury holdings by foreign investors might proxy for an increase

in the popularity among U.S. investors of Treasury securities, who benefit more of their liquidity.

The second proxy is the percentage change in Treasury securities outstanding. A decrease in the

amount of Treasury securities outstanding proxies for times in which Treasury securities are scarcer

and hence more valuable to local investors. These two proxies should be negatively correlated with

the spread between the three-month risk-free rate and T-bill yield.

Also, the estimated risk-free can help analyzing whether the spread with respect to LIBOR is

related to credit risk. Again, I use two proxies for credit risk in the economy. The first one is the

VIX and should proxy for times in which market volatility is high, increasing the probability of

29

default by banks and financial institutions. The second proxy is the difference between the yield of

BAA and AAA corporate bonds. This spread should widen in times of economic distress.

Table 6 presents results for two regressions. All variables but the VIX are sampled at the end

of the month. A monthly version of the VIX is obtained by taking the squared-root of the average

of squared daily VIX values. The sample period is February 1990 to December 2007. The data

source is Datastream.

In the first regression, which corresponds to models (1) to (4), the dependent variable is the

difference between the three-month estimated risk-free rate and the three-month T-bill (rt − tsyt).

In the second regression, which corresponds to models (5) to (8), the dependent variable is the

difference between the three-month LIBOR and the three-month estimated risk-free rate (libt−rt).

In models (1) to (3) the regressors are the lagged dependent variable (rt−1 − tsyt−1), the log-

change in seasonal adjusted T-bill holdings by foreign investors (∆ log(TbillFgnt)), and the log-

change in seasonal adjusted marketable Treasury securities outstanding (∆ log(TsyOutt)). The

regression shows that the spread between the risk-free and T-bill rates is negatively correlated

with the two regressors, which is consistent with the flight-to-liquidity interpretation of lower T-bill

yields. Both coefficients in the regression are statistically significant.

In model (5) to (7) the regressors are the lagged dependent variable (libt−1−rt−1), the change in

the VIX (∆V IXt), and the change in the spread between the redemption yield of AAA and BAA

Lehman corporate bonds indexes(∆CredSprdt). The regression shows that the spread between

LIBOR and the risk-free rate is positively correlated with both credit risk proxies, and that this

correlation is also statistically significant. Thus, the risk-free rate estimated from S&P 500 futures

seems to be less affected by both liquidity and credit risk than Treasury rates and LIBOR.

Models (4) and (8) present further evidence in favor of the model. It may be argued that even

though rt − tsyt and libt−1 − rt−1 are correlated with proxies for flight-to-liquidity and credit risk,

respectively, the estimate for rt could still contain a premium for either flight-to-liquidity or credit

risk. Model (4) shows that rt − tsyt contains only information about flight-to-liquidity but not

credit risk. Similarly, model (8) shows that libt−1 − rt−1 is correlated only with proxies for credit

risk but not for flight-to-liquidity in the Treasury market.

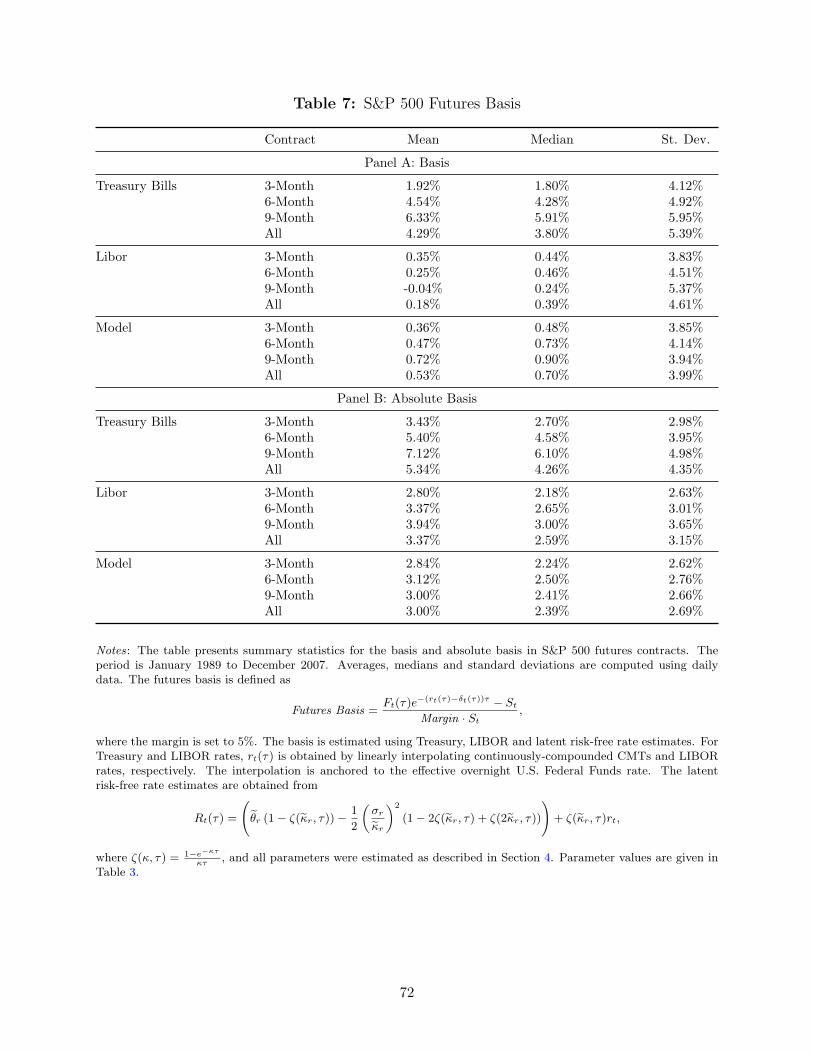

I also check if deviations from the cost-of-carry formula, or “futures mispricing”, are smaller

30

using the estimated risk-free rate. I define “futures mispricing”, or “basis”, as

Futures Basis =Ft(τ)e−(rt(τ)−δt(τ))τ − St

Margin · St. (25)

This definition is standard although I scale the usual “basis” by a margin requirement to reflect the

fact that a futures position is in fact a leveraged transaction. If the futures price is mispriced, this

would be the total return per unit of capital deployed by an arbitrageur. I set the margin equal

to 5% which is consistent with historical margin information for S&P 500 futures (Brunnermeier

and Pedersen, 2008, Figure 1). Note, however, that the margin is just a constant scaling factor and

does not affect the results of the paper. In the absence of frictions and arbitrage opportunities, the

basis should be zero.

Table 7 presents summary statistics for the basis and the absolute basis computed using Trea-

sury, LIBOR, and model estimated risk-free rates. Interest rates for each maturity are obtained

by linearly interpolating continuously-compounded Constant Maturity Treasury rates (CMTs) and

LIBOR rates, respectively. The interpolation is anchored to the effective overnight U.S. Federal

Funds rate. The use of Treasury rates in computing the basis is standard in the finance literature

(see e.g. Roll et al., 2007), while it is common practice in industry to use LIBOR rates Hull (2002,

p. 94). Dividends are computed following the procedure described in section 2.3.1.

It can be seen from the table that the absolute basis is smallest when computed using the

estimated risk-free. The difference is economically important when compared with Treasury rates.

6 Prices and Demand

In this section I show that the demand factor computed from futures prices is related to two proxies

of demand imbalances. The first proxy is the net demand of S&P 500 futures contracts by large

speculators, obtained from the Commitments of Traders (COT) reports provided by the Commodity

Futures Trading Commission (CFTC). These reports contain information on open interest in long

positions by large speculators, large hedgers and non-reportable positions. The data is described

in detail in Appendix B. The second proxy is the difference in the percentage of bullish minus

bearish investment newsletter writers provided by Investors Intelligence. I use this proxy because

31

it has been documented (e.g. Han, 2008) that demand by large speculators is correlated with this

sentiment measure. The measure is a weekly survey of approximately 150 investment newsletter

writers. Each newsletter is read and marked bullish, neutral or bearish. The “bullbear spread” is

defined as the difference between the fraction of bullish and bearish investors, and is usually seen

as a proxy of sentiment for large investors.

The model predicts that the demand factor estimated in Section 4 is positively correlated with

these two proxies for demand pressure. Casual examination of the time series of these two variables

suggests that this is indeed the case. Figure 6 shows the monthly average of the demand factor

implied from the model using S&P 500 futures and the net demand of S&P 500 futures contracts by

large speculators monthly from January 1989 to December 2007. The bottom panel shows for the

same period the monthly average of the demand factor implied from the model and the difference

in the percentage of bullish minus bearish investment newsletter writers. It is apparent from these

two pictures, specially from the one with the sentiment measure, that the series are positively

correlated.

In the model presented in Section 3 I abstract from transaction costs, which can be an impor-

tant friction affecting arbitrageurs’ ability to hedge futures prices. The main difference between

transaction costs, and borrowing and short-selling costs, is that the former are approximately insen-

sitive to the sign of the demand factor. This is why previous literature on index futures mispricing

has focused on analyzing the absolute basis and not the basis (see e.g. Roll et al., 2007). Thus,

illiquidity should be positively related to the volatility of the mispricing and a possible “control” for

this problem is to run a regression in which the variance of the residuals depends on an illiquidity

proxy. When illiquidity is high, deviations from the cost-of-carry model (positive or negative) will

be given less weight in the regression. I combine several illiquidity proxies that I describe in detail

in Appendix C to generate a single time-series that I call the illiquidity factor, which is just the

principal component of the individual illiquidity measures. I also control on the variance equation

for mismeasurement of the underlying index by including the VIX in the variance equation.

Table 8 presents results from GLS regressions of the latent demand factor xt (DemandFactor)

on the lagged demand factor, the innovation in net demand of S&P 500 futures contracts by large

speculators (LongShort) and the innovation of the difference in the percentage of bullish minus

32

bearish investment newsletter writers (BullBear):

DemandFactor t = β0 + β1DemandFactor t−1 + β2LongShort t + β3BullBear t + εt.

I use innovations in demand proxies because these variables are highly persistent. The variance

equation is described by an exponential process that includes the VIX and the illiquidity factor:

log(σ2t ) = γ0 + γ1VIX t + γ2IlliqFactor t. (26)

The choice of the exponential process guarantees that the variance is positive even if the illiquidity

factor is negative. The period is January 1990 to December 2007 because the VIX series starts in

January 1990. All variables are monthly averages. The table shows that both proxies for demand

are significantly and positively correlated with the demand factor, as predicted by the model. Also,

both the VIX and illiquidity are significantly and positively correlated with the demand factor

volatility.

Table 9 presents additional evidence in support of the model. The fact that demand proxies

are positively related to the demand factor could be the result of some other friction different from

borrowing and short-selling costs. Thus, it would be interesting to see whether the demand factor

is positive when buying pressure is high and is difficult to borrow, and if the demand factor is

negative when selling pressure is high and is difficult to short-sell the underlying. To test this,

the table presents results from GLS regressions of the latent demand factor xt (DemandFactor) on

the lagged latent demand factor, an indicator function (Buy) that is equal to one if LongShort is