implementation of accrual accounting over indian · pdf fileimplementation of accrual...

TRANSCRIPT

Implementation of Accrual Accounting over Indian Railways

ByIndian Railways and ICAI Accounting Research Foundation

As part of broader administrative reforms, Ministry of Railways decided

to bring transparency in its accounting system by preparing additional

set of Financial Statements on accrual principles in addition to cash

based accounts so as to achieve convergence with Generally Accepted

A ti P i i l (GAAP) F thi t il t P j tAccounting Principles (GAAP). For this purpose two pilot Projects were

started, one in North Western Railway (NWR) and another one in Rail

Coach Factory (RCF)Coach Factory (RCF).

Now, MOR has resolved to scale up Accrual Accounting in whole Indian

Railways in collaboration with Institute of Chartered Accountant of India–Railways in collaboration with Institute of Chartered Accountant of India

Accounting Research Foundation (ICAI ARF).

The entire Accounting Reforms project has a March 2019deadline for the Indian Railways. As elaborated in the 2017-18 Budget speech of Hon’ble Finance Minister, the projectunderscores the need for the state-owned transporter totake “transformative measures” in the way it conducts itsbusiness.

Indian Railways, being a department of Government of India, maintains

its Finance Accounts under hybrid system of accounting in the form and

format mandated by CGA and C&AG.

In August 2002, Government of India formed GASAB to formulate

A ti St d d f b th C h A ti d A l A ti iAccounting Standards for both Cash Accounting and Accrual Accounting in

Government Departments. This was followed with the setting up of

Accounting Reforms Directorate in the Railway BoardAccounting Reforms Directorate in the Railway Board.

In 2016 Board set up AR project organization in NR headed by CPM/AR to

implement Accounting Reforms on all Indian Railways The organization isimplement Accounting Reforms on all Indian Railways. The organization is

working under administrative control of FA&CAO & GM, NR and overall

guidance of AR Directorate /Railway Board.

Accounting Reforms on IR comprise :Accrual AccountAccrual AccountBeing implemented in association with ICAI-ARFPerformance Costing Performance Costing Being implemented in association with ICWAI-MARF

Outcome BudgetingConcept development stage.

The Institute of Chartered Accountants of India, set up under an Act of

P li (Th Ch d A A 1949) h ICAIParliament (The Chartered Accountants Act, 1949), has set up ICAI

Accounting Research Foundation (ICAI ARF) in January, 1999 as a

Section 8 company ICAI ARF is a core research body in the areas ofSection 8 company. ICAI ARF is a core research body in the areas of

accounting, auditing, capital market, fiscal policies, monetary policies

and other related disciplines.p

Indian Railways is presently following Cash based system of Accountingalong with some elements of accrual accounting. e.g. Demand Payable,D d R i bl t F ll i g th k f t f h b dDemand Receivable, etc. Following are the key features of cash basedsystem of accounting:

Mandated by extant Rules;Th iti t i i b d fl f h The recognition trigger is based on flow of cash;

The focus presently is to report earnings and expenditure onreceipt/expenditure basis; and

Budgetary and legislative compliances assume equal importanceunder this system.

Existing Accounting

Indian Railways has following sources of earnings1. Coaching earnings (Passenger/Other than Passenger);g g ( g g );2. Goods earnings;3. Sundry Other earnings; and4. Miscellaneous ReceiptsPresently earning is recognized as and when it is receivedPresently, earning is recognized as and when it is received.

Let us understand the present accounting system with the following example:Mr A booked a ticked on 30th March 2017 whose travel date is 5th April 2017punder present accounting system the earning will be booked in the previousfinancial year i.e., 2016-17.

However, in accrual accounting system amount received from Mr A should be, g ytreated as liability till 4th April and when the journey takes place, i.e., on 5thApril, the amount will be transferred to relevant income head.

Accounting on Accrual Basis As per the accounting policy finalized for revenue, passenger earning will

be recognized on accrual basis.

Goods earning should also be recognized when the goods are actuallydelivered;delivered;

Sundry other earning1. Rental Income in respect of land/property will be recognized on1. Rental Income in respect of land/property will be recognized on

accrual basis in accordance with the terms and conditions of thecontract with licensee/lessee, etc.

2. Income from sale of un-serviceable revenue scrap, not creditable toDevelopment Fund Depreciation Reserve Fund etc will be accountedDevelopment Fund, Depreciation Reserve Fund, etc. will be accountedfor on realization basis.

Currently, Expenditure is booked based on their demand as prescribed in Finance Code – II. Following two types of demands are mentioned in Finance Code II. Following two types of demands are mentioned in Finance Code – II:Revenue Demands1. Policy Formulation and Railway Board Expenditure (Demand 01 and 02) y y p ( )2. Working Expenses (Demand 03 to 13); 3. Appropriation to various funds like DF, DRF, etc., (Demand 14);4. Suspense (Demand 15); andp ( );Capital Demand1. Capital Expenditure (Demand 16).Expenditure is booked based on their demand allocation rather than itspnature.

Long term liabilities relating to employee benefit are not recognized such as pension leave encashment etcsuch as pension, leave encashment, etc.

Long term liabilities in respect of leased assets taken from IRFC is also not recognizedalso not recognized.

It is imperative for Indian Railways that all such liabilities h ld b i d i th b k should be recognized in the books.

Only payments actually made are reflected in accounts andy p y ypayables are not shown in accounts;

A t d li biliti t fl t d tl Assets and liabilities are not reflected; consequently,financial strength (net worth) not known;

Deficient liability management and weak MIS; Inadequateinternal control procedures;

Inadequate disclosure and audit mechanism.

No disclosure is made about provision of contingentliabilities;

No disclosures are made about accounting policies on thebasis of which Financial Statements are prepared.

No charging of Depreciation on Fixed Assets.

Accrual-based accounting is a method by which, revenues, costs,assets & liabilities are reflected in the period in which they accrueand arise;

Accrual basis attempts to record financial effects of transactions inthe period in which they occur, rather than recording them in theperiod in which cash is received/paid;

The transactions are recognised as soon as a right to receive revenueand/or an obligation to pay a liability is created;

The expenses are recognised when incurred and incomes arerecognized when earned;recognized when earned;

Adjustments are made at the end of the year ensuring incomes andexpenses are recognized in the relevant period;expenses are recognized in the relevant period;

Accrual matches the expenditure incurred with the income earnedduring the period;during the period;

It helps in the assessment of financial performance i.e. profit andloss correctly;loss correctly;

It gives comprehensive information on the Financial Position i.e.assets and liabilities;

It gives information on whether income streams are adequate tomeet short and long term liabilities;

It provides comprehensive information on expenses which helps inknowing the cost consequences of policies and enables comparisonwith alternative policies;

Liquidity position can be better assessed;

It bridges the gap leftover by cash accounting by inclusion ofd d ( i bl d bl ) taccrued expenses and revenues (receivables and payables), assets,

liabilities and provisions, depreciation on fixed assets, etc. in theaccounting system.

It discloses the Accounting Policies used in the preparation ofFinancial Statements for better understanding leading to HigherTransparency and Accountability;

Value-addition to Strategic Financial Decision-making;

Value-added Disclosures;

Analyzability/Comparability of Financial Statements;

Increased value of Management Discussion and Analysis (MD&A); and

Increased effectiveness of internal control systems.

Cash Basis Accrual Basis

Income

On receipt When due

Expense

On payment On crystallization

Asset

Transactions

A Few fixed assets are Considered as revenue exp., and

written off

Capitalized & depreciated

Liabilities

Not recognized recognized

19

Th K Diff Id tifi d The Key Differences Identified during the Pilot Study at during the Pilot Study at North Western Railway

S.No.

Particular Accrual Basis Existing system Remarks

1. Gross Assets includingCWIP (of Rs.

14,789 13,258 • Represent Assets identified from assets charged to revenue. However, several Assets

2102crores)charged to revenue. However, several Assets which were decommissioned were notremoved from Block Account.

• CWIP was identified, which was earlier included in Block Accountincluded in Block Account.

2. AccumulatedDepreciation

3,845 NIL No Depreciation is charged under existingsystem of Accounting based on actualwear/tear. However, an ad-hoc amount istransferred to DRF to compensate thedepreciation.

3. Net Fixed Assets 10,944 13,258 Shows difference between Gross Assets and Accumulated Depreciationp

4 Lease Assets* 2,270 NIL Not recognized in existing system of accounting

.*There is a corresponding liability of Rs. 2270 Crore on Lease Assets.

S.No.

Particular Accrual Basis Cash Basis Remarks

1. Depreciation for the year

499 NIL No Depreciation ischarged under existingsystem of Accountingy gbased on actualwear/tear. However,an ad-hoc amount istransferred to DRF to

2. Appropriation to Depreciation Reserve Fund

291 291

transferred to DRF tocompensate thedepreciation.

Reserve Fund

3. Appropriation to 1,246 1246pp pPension Fund

,

4. Net Profit after Depreciation and

59 565p

Appropriation

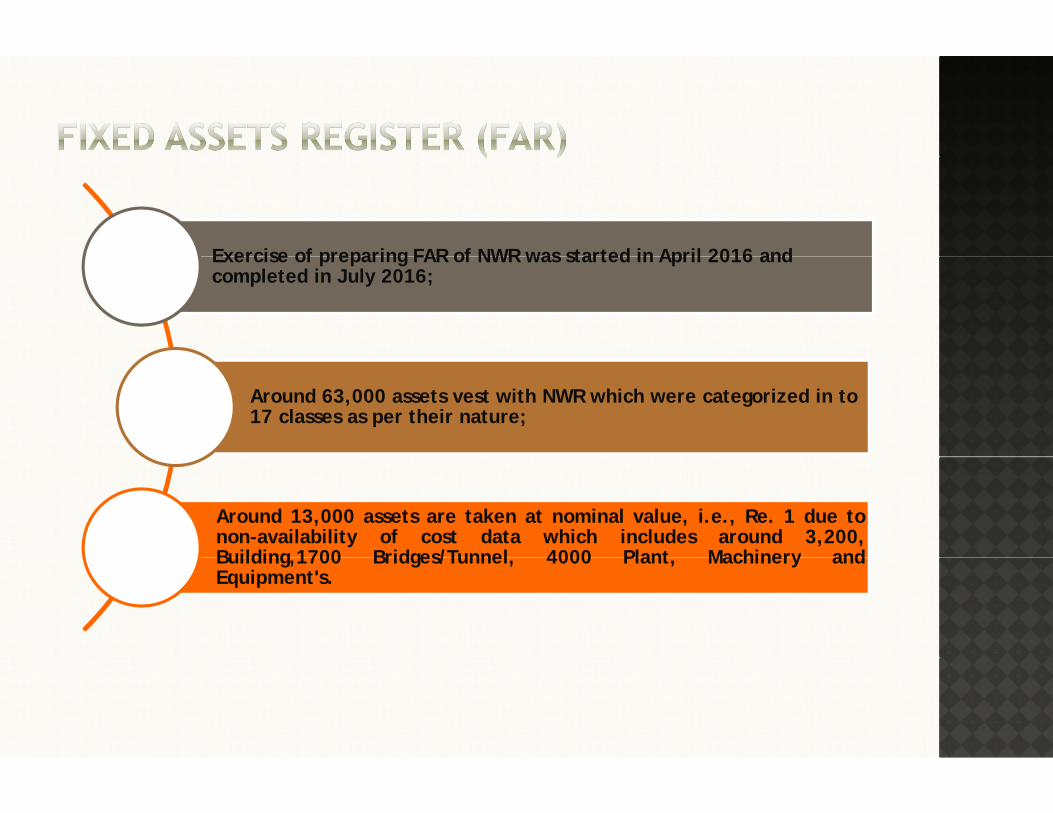

Exercise of preparing FAR of NWR was started in April 2016 and Exercise of preparing FAR of NWR was started in April 2016 and completed in July 2016;

Around 63,000 assets vest with NWR which were categorized in to 17 classes as per their nature;

Around 13,000 assets are taken at nominal value, i.e., Re. 1 due tonon-availability of cost data which includes around 3,200,Building 1700 Bridges/Tunnel 4000 Plant Machinery andBuilding,1700 Bridges/Tunnel, 4000 Plant, Machinery andEquipment's.

Actuarial Liability as on 31.03.2015 Net Worth of North Western Railway (NWR) as on 31.03.2015

S.No.

Particular Amount (in Crores)

1 Gratuity 1 707

S.No.

Particular Amount (in Crores)

1. Gratuity 1,707

2. Earned Leave 1,250

3. Medical 1,277

1. Total Assets 23,648

2. Current Liabilities (9,961)

4. Pension 23,907

5. Composite Transfer Grant

111

3. Non-Current Liabilities

(3,912)

4. Net Worth 9,775

Total 28253

*Actuarial Liability is not provided in the Financial Statements as on 31st March 2015

Non Current

AssetsAssets

Current Assets

Balance Sheet

Assets

Current Liabilities

Financial Statements

LiabilitiesNon Current Liabilities

Income Profit & Loss

Account

Income

ExpenditureC h Fl Cash Flow Statement

Financial statements are intended to meet the needs of users.Users of financial statements include stake holders like taxpayers,p y ,members of Legislature, Government entities, the media and thepublic.

The objective of financial statements is primarily to provide ‘trueand fair’ view of the financial position, financial performance andcash flow of the entity which is useful to a wide range of users inmaking and evaluating decisions about allocation of resources andto demonstrate the accountability of the entity for the resourcesentrusted to it.

A complete set of financial statement comprises :A complete set of financial statement comprises :

A statement of financial position; A statement of financial performance; A statement of financial performance; A statement of changes in net assets/equity; A cash flow statement; and Notes to Accounts.

While preparing financial statements on accrual basis, first major task isto prepare an assets register of the organization for all assets held byto prepare an assets register of the organization for all assets held bythem.Fixed Assets, being a significant portion of the total assets of anyorganization, the accounting thereof involves proper classification,organization, the accounting thereof involves proper classification,segregation, recording and presentation for the purpose of reflecting thecorrect financial status and determining the level of efficiency of theorganization in relation to the cost incurred on the assets.

ICAI ARF team compiled the FAR of NWR and RCF in the pilotstudy. Now, FAR for whole Indian Railway is to be preparedstudy. Now, FAR for whole Indian Railway is to be preparedto ascertain the value of assets held by Indian Railways.

• “Property plant and equipments are tangible assets th tthat:• are held by an entity for use in the production or

supply of goods or services, for rental to others, or for administrative purpose; and are expected to be used during more than one

Indian Government Financial Reporting

Standard -2• are expected to be used during more than one

reporting period.

• “Fixed Assets is an asset held with the intention of being used for the purpose of producing or providing goods or services and is not held for sale in the normal Accounting goods or services and is not held for sale in the normal course of business.”

Accounting Standard -10

An asset should be recognized in books of accounts when:

It i t ti. It is put to use;ii. Future economic benefits associated with the asset will flow to

the organization; andiii. Cost of the asset can be measured reliably.

All the fixed assets that are in existence as at the end of the year,i.e., before switching over to the accrual system of accounting shallhave to be brought to the Fixed Assets Register.

Concept of control is an important tool to recognize assets in thebooks of accounts.

The concept of control of an asset’s economic benefit is the key issuein determining whether that asset should be reported in the financialin determining whether that asset should be reported in the financialstatement of the Organisation or not.

According to AS-26, ‘Control’ is identified when the enterprise has According to AS 26, Control is identified when the enterprise hasthe power to obtain future economic benefits flowing from theunderlying resources and also can restrict the access of others tothose benefits;

However, legal enforceability of a right is not a necessary conditionfor control since an enterprise may be able to control the futurep yeconomic benefits in some other way.

In Indian Railways, Assets are classified into two parts:

Fixed Assets

Tangible Intangible Tangible Assets

Intangible Assets

Immovable Assets

Movable AssetsAssets Assets

Roads/ Street

Immovable Assets

Bridges/Flyover/Subway/ TunnelsLand

Railway TracksBuilding

Furniture & Fixture

Loco/Coach/Wagon

Computers & Peripherals

Medical EquipmentVehicles

Electric Equipment & Fittings Plant, Machinery

& Equipment

Movable Assets

& Equipment (Signal)

Other Equipments (OHE)

Plant, Machinery & EquipmentMast/Portal

Structure

Transformer Office Equipment

Plant, Machinery & Equipment

Conductors (Wire) Equipment

(Telecom)(Wire)

Para 1720 of Engineering Code as applicable on Indian Railwaysprescribes an Asset Register Format (depicted on next slide) toprescribes an Asset Register Format (depicted on next slide) torecord the details of fixed assets. Investment of more than Rs. 20lakhs in fixed assets is included in this Register.

As we all know that Indian Railways prepare Block account for theamount expended from Capital demand i.e. Demand 16.

Presently, Fixed Asset Register is not maintained properly asrequired by accrual based accounting, i.e., fixed asset register foreach and every assets along with all details like Cost date ofeach and every assets along with all details like Cost, date ofacquisition, etc.

Assets Register (Form E, 1720)1.Name of Work2 Date of Commencement2.Date of Commencement3.Date of Completion4.Completion report no. and date5 Authority sanctioning the completion report

Y A t f I t t

5.Authority sanctioning the completion report6.Completion Cost7. Investment Schedule

Year Amount of Investment

Capital DRF DF Revenue

Total

Format provided under Para 1720 of engineering Code is not sufficient torecord the Fixed Assets to be shown under accrual accountingrecord the Fixed Assets to be shown under accrual accounting.

Now, One of the most important tasks is to prepare an assets register forll th fi d t h ld b th I di R ilall the fixed assets held by the Indian Railways.

We would like to apprise that The Fixed Asset Register formats haveb f l d f id i h i i d f dbeen formulated after considering the inputs received from concernedBranch officers at Ajmer Division and Workshop to capture the assets dataand to prepare FAR during pilot study.

37

Following table shows the formats finalized for the collection of Fixed Assets Data:

S. No Name of Fixed Assets Prescribed Format

1 Land FA-1

2 Buildings FA-2

3 Bridge/Flyover/Subways/Tunnel FA-3g y y

4 Roads/Streets FA-4

5 Rails FA-5A5 Rails FA-5A

6 Sleeper FA-5B

7 B ll t FA 5C7 Ballast FA-5C

S. No Name of Fixed Assets Prescribed Format

8 Track Fittings FA 5D8 Track Fittings FA-5D

9 Furniture and Fixtures FA-6

10 Details of Office Equipments FA-7

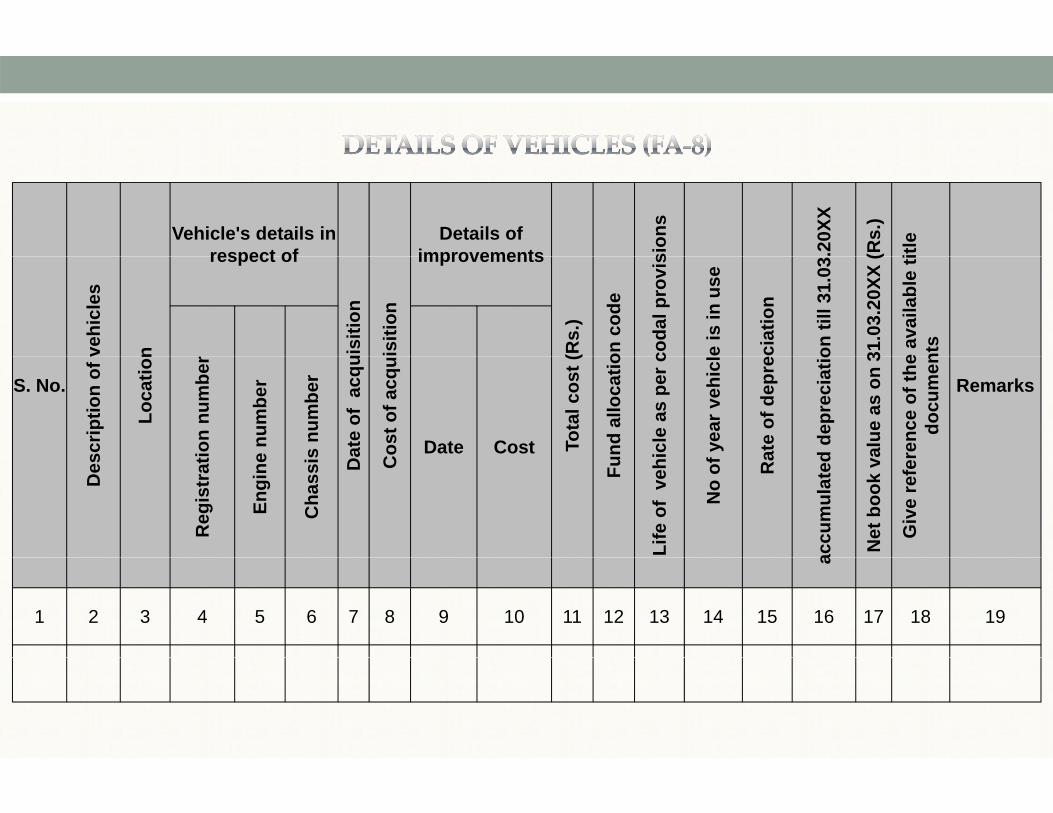

11 Details of Vehicles FA 811 Details of Vehicles FA-8

12 Details of Plant, Machinery and Equipments

FA-9Equipments

13 Details of Computer and Peripherals FA-10

14 M di l E i t FA 1114 Medical Equipments FA-11

S. No Name of Fixed Assets Prescribed Format

15 Loco/Coach/Wagon FA 1215 Loco/Coach/Wagon FA-12

16 Capital Work in Progress FA-13

17 Plant, Machinery and Equipment (Signal)

FA-14

18 Plant, Machinery and Equipment (Telecom)

FA-15

19 Electrical Equipment and Fittings FA-16q p g

20 Intangible Assets FA-17

S. No Name of Fixed Assets Prescribed Format

21 Details of Conductors (Wire) FA-18A

22 Details of Transformers FA-18B

23 Details of Mast/Portal Structure FA-18C

24 Details of Other Equipments (OHE) FA-18D

Plot

s

tions

)

Ms ld Location ec

ords

Dimension of Land on

ear

lier

aila

ble)

e) (A

ny

stru

ctio

n

(Are

a)

Rat

e

C ra

te

d

o. der C

ode

tion

of L

and

P

ence

No.

wee

n tw

o St

at

in K

ms)

ncre

asin

g K

M

ehol

d/Fr

eeho

l

per r

even

ue re Land

now

n),

men

tiot k

now

n)an

No.

enue

Rec

ord

of L

and

(if A

va

t (If

Avai

labl

ela

nd li

ke c

ons

wal

l/fen

cing

e of

Lan

d

for o

ther

use

mitt

ee (D

LC)

renc

e to

DLC

LC R

ate

Cos

t of L

and

arks

S.n

Stoc

k H

old

ular

/Des

crip

t

Plot

Ref

ere

Sect

ion

(Bet

w

Cha

inag

e

S or

LH

S in

in

ecify

if L

ease

e vi

llage

as

p

quis

ition

(if k

nth

an (i

f no

Land

Pla

Stat

us in

Rev

e

acqu

isiti

on o

Impr

ovem

enin

curr

ed o

n l

of b

ound

ary

w

Cur

rent

Us

rt S

epar

able

f

ct L

evel

Com

m

n un

it in

refe

r

Year

of D

rese

nt /a

ctua

l

Rem

a

Stat

e

Dis

tric

t

wn/

villa

ge

Length Area

Part

ic

Blo

ck S

RH

S

Spe

Rev

enue

year

of a

cq S

Cos

t of a

Cos

t of

expe

nses

o

Any

par

Dis

tric

Are

a i Pr

D

Tow

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26

Location reco

rds

Dimension of building s

loca

ted

f kno

wn)

, ) tio

n

Improveme isio

ns

se .03.

20XX

.03.

20XX

20XX

men

t

no.

olde

r Cod

e

riptio

n

per r

even

ue of building

f flo

ors

ch B

uild

ing

is

ld U

p ar

ea

onst

ruct

ion(

if(if

not

kno

wn

ion/

cons

truc

t

nt (If any)

l cos

t

er c

odal

pro

v

sset

s is

in u

s

sets

as

on 3

1

epre

ciat

ion

ciat

ion

till 3

1.

as o

n 31

.03.

2

e of

Bui

ldin

g

of ti

tle D

ocum

mar

ks

ent

ent

S.

Stoc

k H

o

Des

cr

ue v

illag

e as

No.

of

land

on

whi

c

Tota

l bui

l

acqu

isiti

on/c

oEa

rlier

than

(

st o

f acq

uisi

t

Tota

of a

sset

as

pe

No.

of y

ear a

s

ing

life

of a

ss

Rat

e of

De

ulat

ed D

epre

c

t Boo

k Va

lue

a

Cur

rent

Use

ve re

fere

nce

o

Rem

Stat

e

Dis

tric

t

Tow

n/Vi

llage

Leng

th

Bre

adth

of Im

prov

eme

of Im

prov

eme

Rev

enu

Are

a of

year

of a co

s

Life

o N

Rem

ain

Acc

umu

Net GivT

Year

o

Cos

t

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 261 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26

RC

C

C) ed I XX

de OB

/RU

B)

RO

B/R

UB

no.

)

wo

stat

ions

)

)

Location

r/PSC

gird

er/R Dimension of structure

MB

G/R

BG

/GC

e is

con

stru

ct

ion

ion

Improvement (If

any)

ode

visi

ons

in u

se

ion

date

31.

03.2

0X

3.20

XX(R

s.)

o.

S.no

.

ock

hold

er c

od

pe (B

ridge

/RO

ridge

no.

Or R

n (B

etw

een

tw

hain

age

(KM

s)

ch/s

teel

gird

erbo

x et

c.

sanc

tion

for (

whi

ch s

truc

ture

e of

con

stru

cti

t of c

onst

ruct

i

Tota

l cos

t

d al

loca

tion

cope

r cod

al p

rov

year

ass

ets

is

e of

dep

reci

ati

prec

iatio

n til

l d

ue a

s on

31.

03pr

oved

Drg

. N

Rem

arks

te rict

Villa

ge

gth

Of s

pans

span

-1-1 sp

an-2

-2 span

-3

-3 rove

men

t

rove

men

t

Sto

Brid

ge ty

Des

crip

tion(

B

Blo

ck s

ectio C

h

of b

ridge

(Arc

oadi

ng b

ridge

a of

land

on

w

Dat

e

Cos

t

Fund

Life

as

p

No.

of y

Rat

e

cum

ulat

ed d

ep

Net

boo

k va

luA

pp

Stat

Dis

trTo

wn

/ V

Leng

Tota

l no.

ON

o. O

f s SP-

No.

Of s SP

-N

o. O

f s SP-

Year

of i

mpr

Cos

t of i

mp

D

Type

Lo Are Ac c

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33

age

road

age)

Location s s lo

cate

d

Dimension of roads

improvement (If 3.

20XX

r Cod

eci

pal r

oad/

villa

inin

g to

wn/

vill

n e ro

ad/s

tree

t is

/kut

cha/

WB

M

re s

truc

ture

is

n of roads

(Sq.

M.)

truc

tion

truc

tion

uenc

y

ment (If any)

ost

on c

ode

l pro

visi

ons

in u

se

ecia

tion

n til

l dat

e 31

.03

.03.

20XX

itle

docu

men

t

ks

S.no

.

Stoc

k H

olde

(NH

/SH

/mun

icet

c.

on o

f roa

d (jo

i

Stat

ion

fy w

heth

er th

ecr

ete/

bitu

men

/

the

land

whe

r

Are

a of

road

Dat

e of

con

s t

Cos

t of c

onst

Rep

air F

req

Tota

l co

Fund

allo

catio

e a

s pe

r cod

al

No.

of y

ear

Rat

e of

dep

re

d de

prec

iatio

n

WD

V as

on

31

refe

renc

e of

ti

Rem

ark

Stat

e

Dis

tric

t

wn/

villa

ge

Leng

th

Bre

adth

impr

ovem

ent

impr

ovem

ent

Type

of r

oad

(

Des

crip

tio

Spec

ifco

nc

Surv

ey n

o. o

f

Lif e

Acc

umul

ated W

Giv

e rD

Tow L B

Year

of i

Cos

t of

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27

e) XX

Rai

lway

s

on n K

Ms)

nth

iod

Per K

M)

t mou

nt

sidu

al V

alue

nth in u

se

e Rat

e

on n 31

.03.

XXX

S. N

o.

on/Z

onal

R

Rai

l Sec

tio

l Len

gth

(in

Rol

ling

Mon

Rol

ling

Peri

t of R

ails

(P

Tota

l Cos

prec

iabl

e A

mst

–5%

Res

Layi

ng M

on

of y

ears

is

Cod

al L

ife

epre

ciat

ion

Dep

reci

atio

Valu

e as

on

Div

isi

Tota

l R R

Cos

t

Dep

(Tot

al C

os

L

No.

De

Net

Boo

k V

1 2 3 4 5 6 7 8 9 1011 12 13 14 15

ue)

X

o. LY Type

and

Yea

r

ensi

ty

h (K

Ms)

rs (N

o's)

leep

er)

Slee

pers

Am

ount

R

esid

ual V

al

Life s in

use

reci

atio

n

atio

n

31.0

3.XX

X X

S. N

o

DIV

/RL

Slee

per T

ying

Mon

th

Slee

per D

e

Tota

l Len

gth

otal

Sle

eper

Cos

t (pe

r S

otal

Cos

t of

epre

ciab

le

Cos

t –5%

R

Cod

al L

No.

of y

ear i

ate

of D

epr

Dep

reci

a

book

Val

ue

Lay T To C

To D(T

otal

C N R

Net

b

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

st –

5%

XX

No. Rai

lway

ion

h (i

n K

Ms)

ng D

ate

Bal

last

Cos

t

nt (T

otal

Cos

l Val

ue)

s is

in u

se

Life

ion

Rat

e

iatio

n

e 31

.03.

XXX

S. N

Div

isio

n/R

Sect

i

Tota

l Len

gth

Scre

enin

Rat

e of

B

Tota

l C

able

Am

oun

Res

idua

l

No.

of y

ears

Cod

al

Dep

reci

ati

Dep

rec

Boo

kVa

lue

T

Dep

reci

a N

Net

1 2 3 4 5 6 7 8 9 1011 12 13

st –

5%

se XX

o. Rai

lway

ular

s

te sum

ed

M. er K

M.

Cos

t

nt (T

otal

Cos

l Val

ue)

l Life

sset

is in

us

prec

iatio

n

iatio

n

e 31

.03.

XXX

S.N

Div

isio

n/R

Part

icu

Dat

Dat

e A

ss KM

Rat

e Pe

Tota

l C

able

Am

oun

Res

idua

l

Use

ful

of Y

ears

as

Rat

e of

Dep

Dep

rec

book

Val

ue

Dep

reci

a

No.

R

Net

1 2 3 4 5 6 7 8 9 10 11 12 13 141 2 3 4 5 6 7 8 9 10 11 12 13 14

If an

y)

uctio

n

ts uctio

n

r cod

al

in u

se

tion

atio

n til

l

s on

.)

S.N

O.

escr

iptio

n

Loca

tion

ce n

umbe

r (

Dat

e of

io

n/co

nstr

u

al n

o of

uni

t

ost p

er u

nit

otal

Cos

t of

ion/

cons

tru

sets

as

per

rovi

sion

s

ar a

sset

s is

of d

epre

ciat

ted

depr

ecia

1.03

.20X

X

ok v

alue

as

3.20

XX (R

s

Rem

arks

De L

Ref

eren

c

acqu

isiti

Tota Co To

acqu

isiti

Life

of a

s p

No

of y

e a

Rat

e o

Acc

umul

at 31

Net

bo

31.0 R

1 2 3 4 5 6 7 8 9 10 11 12 13 14

mbe

r

on tion

coda

l

n us

e

on tion

till

.03.

20XX

S.N

O.

scrip

tion

ocat

ion

fere

nce

Nu

f ac

quis

itio

no o

f uni

ts

st p

er u

nit

al c

ost o

f on

/inst

alla

t

ets

as p

er c

ovis

ions

asse

ts is

i n

depr

ecia

tio

d de

prec

iat

.03.

20XX

ue a

s on

31.

(Rs.

)

emar

ks

S

Des Lo

Ass

ets

Ref

Dat

e of

Tota

l

Cos To

taac

quis

iti

Life

of a

ss pro

No

of y

ear

Rat

e of

Acc

umul

ate

31.

t boo

k va

lu Re

A

Ne

1 2 3 4 5 6 7 8 9 10 11 12 13 14

Vehicle's details in respect of

Details of improvements si

ons

.20X

X

(Rs.

)

itle

vehi

cles

n

respect of

uisi

tion

isiti

on

improvements

(Rs.

)

on c

ode

coda

l pro

vis

e is

in u

se

ecia

tion

on ti

ll 31

.03

31.0

3.20

XX (

e av

aila

ble

tint

s

r

S. No.

scrip

tion

of v

Loca

tion

ate

of a

cqu

Cos

t of a

cqu

Tota

l cos

t (

und

allo

catio

icle

as

per c

fyea

r veh

icl

ate

of d

epre

d de

prec

iatio

alue

as

on 3

renc

e of

the

docu

men

Remarks

ion

num

ber

e nu

mbe

r

s nu

mbe

r

Date Cost

Des D C Fu

Life

of

veh

No

of

Ra

accu

mul

ated

Net

boo

k v

Giv

e re

fer

Reg

istr

at

Engi

ne

Cha

ssis

a

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19

n on atio

n

Details of isio

ns

se

l (Rs.

)

title

ble)

r Cod

e

n n Mac

hine

Mac

hine

y o. &

dat

e

pplie

r

n/in

stal

latio

n/in

stal

latio

ent o

f ope

ra

in u

se

improvements

st on c

ode

coda

l pro

vi

nery

is in

us

ciat

ion

reci

atio

n til

XX 31.0

3.20

XX

e av

aila

ble

tnt

se

(if A

vaila

b

on rplu

ss

S. N

o.to

ck H

olde

rU

nit

Stat

ion

Loca

tion

tego

ry o

f Mcr

iptio

n of

MC

apac

ity

MO

W P

O n

o

Nam

e of

Sup

acqu

isiti

on

acqu

isiti

on

mm

ence

me

o of

shi

fts i

Tota

l cos

nd a

lloca

tiohi

ne a

s pe

r

ars

mac

hin

te o

f dep

reul

ated

dep

r31

.03.

20X

alue

as

on 3

ence

of t

hedo

cum

enm

arke

t val

ue

Con

ditio

Whe

ther

Su

Rem

ark s

ate

ost

St Cat

Des

c

CO

FM N

Cos

t of

Dat

e of

Dat

e of

co m N

o

Fun

fe o

f m

ach

No

of y

e Ra

Acc

umu

Net

boo

k va

Giv

e re

fer

Cur

rent

m WDa

Co

Li N

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28

r on ion

odal

use

n on ti

ll

on

S. N

o.

crip

tion

ocat

ion

nce

num

ber

ate

of

on/in

stal

latio

no o

f uni

ts

t per

uni

t

of a

cqui

sit

ets

as p

er c

ovi

sion

s

asse

ts is

in

depr

ecia

tio

d de

prec

iati

1.03

.20X

X

k va

lue

as o

20XX

(Rs.

)

Remarks

S

Des Lo

Ref

eren D

aac

quis

itio

Tota

l n

Cos

t

Tota

l cos

t

Life

of a

sse

prov

No

of y

ear a

Rat

e of

d

ccum

ulat

edda

te 3

Net

boo

k31

.03.

2

L N

Ac

1 2 3 4 5 6 7 8 9 10 11 12 13 14

mbe

r

tion/

its t uisi

tion

er c

odal

s in

use

atio

n

ecia

tion

X as o

n s.

)

S.N

O.

Des

crip

tion

Loca

tion

eren

ce n

um

of a

cqui

sit

inst

alla

tion

tal n

o of

un

Cos

t per

uni

ost o

f acq

u

sset

s as

pe

prov

isio

ns

ear a

sset

s is

of D

epre

cia

ulat

ed d

epre

l 31.

03.2

0XX

ook

valu

e a

03.2

0XX

(R

Remarks

D

Ref

e

Dat

e i

Tot C

Tota

l Co

Life

of a

p

No

of y

e

Rat

e

Acc

umu til

Net

bo

31.

1 2 3 4 5 6 7 8 9 10 11 12 13 14

n on er

Details of e Rs.

)

code

t e ode

e no

.

ach/

loco

n onst

ruct

ion

t of o

pera

tio

ty stru

ctio

n p

oach

Details of improvem

ent

code

rovi

sion

s

s in

use

atio

ntio

n til

l dat

eX .0

3.20

XX (R

S.N

o.

ck h

olde

r c

Dep

artm

ent

Gro

up c

ode

b G

roup

co

et re

fere

nce

wag

on/c

oa

Des

crip

tion

Loca

tion

quis

ition

/co

men

cem

ent

otal

qua

ntit

uisi

tion/

cons

gon/

loco

/co

Tota

l Cos

t

d al

loca

tion

per c

odal

pr

ear a

sset

s i

of D

epre

cia

ed d

epre

cia

31.0

3.20

X X

ue a

s on

31.

Rem

arks

Stoc D G

Su

Ass

e

Type

of D

Dat

e of

acq

ate

of c

omm To

ost o

f acq

uw

ag

Fund

Life

as

p

No

of y

e

Rat

e A

ccum

ulat

e

et b

ook

valu

Dat

e

Cos

t

Da Co A

Ne

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23

S D i ti f Estimated C t i d Fund Estimated dateS. No.

Description of Work Location

Estimated Cost of work

Cost incurred till 31.03.20XX

Fund allocation

code

Estimated date of completion

of the workRemarks

1 2 3 4 5 6 7 8

y hine

tion

of

dal

use

till

able

O. f M

achi

nery

ure

of m

ach

/Sta

tion

city

hifts

in u

se

ion/

inst

alla

t

ence

men

t otio

n

ost o

f ns

talla

tion

atio

n co

dee

as p

er c

odio

ns

hine

ry is

in

prec

iatio

n

epre

ciat

ion

20XX

alue

as

on

XX (R

s.)

of th

e av

aila

umen

tske

t val

ue (i

f ab

le)

arks

S.N

O

scrip

tion

of

ficat

ion/

natu

Loca

tion/

Cap

ac

umbe

r of s

h

of a

cqui

siti

e of

com

me

oper

at

Tota

l Co

cqui

sitio

n/in

Fund

allo

caof

mac

hine

prov

is

year

s m

ach

Rat

e of

dep

umul

ated

de

31.0

3.2

Net

boo

k va

31.0

3.20

X

refe

renc

e o

title

doc

uur

rent

mar

kAv

aila

Rem

a

Des

Spec

if Nu

Dat

e o

Dat a c F

Life

o

No

of y R

Acc

u N

Giv

e r

Cu

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 181 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

y hine

wo

e atio

n

of

dal

use

till

20XX

able

labl

e)

O.

of M

achi

nery

ture

of m

ac

(Bet

wee

n tw

ons)

city

hifts

in u

se

ion/

inst

alla

ence

men

t oat

ion

ost o

f ns

talla

tion

atio

n co

dee

as p

er c

odsi

ons

hine

ry is

in

prec

iatio

n

epre

ciat

ion

20XX

s on

31.

03.2

s.)

of th

e av

aila

umen

ts

alue

(if A

vai

arks

S.N

O

escr

iptio

n o

ficat

ion/

nat

ck S

ectio

n(st

atio

Cap

a

umbe

r of s

h

of a

cqui

sit

te o

f com

mop

era

Tota

l Co

cqui

sitio

n/i

Fund

allo

caof

mac

hine

prov

is

year

s m

ach

Rat

e of

dep

umul

ated

de

31.0

3.2

ook

valu

e as

(Rs

refe

renc

e o

title

doc

u

t mar

ket v

a

Rem

a

De

Spec

if

Blo

c N

Dat

e o

Dat ac F

Life

No

of

Acc

u

Net

bo

Giv

e

Cur

ren

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

n on X

on der

no. (

if an

y) Chainage (in Km)

units

/inst

alla

tion

nit

Details of Improvement

on/in

stal

lati

per c

odal

s is

in u

se

ciat

ion

ecia

tion

till

X n 31

.03.

20XX

s

S.N

o.

Des

crip

ti o

Stoc

k H

old

refe

renc

e n

Loca

tion

ngth

/No

of

acqu

isiti

on/

Cos

t per

un

of a

cqui

sitio

asse

ts a

s p

prov

isio

ns

year

ass

ets

e of

dep

rec

late

d de

pre

31.0

3.20

XX

valu

e as

on

(Rs.

)

Rem

arks

m e t

Ass

ets Le

n

Dat

e of

a

Tota

l cos

t oLi

fe o

f

No

of y

Rat

e

Acc

umu

Net

boo

k v

From To Dat

e

cost

T

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19

S. D i ti

Date of acquisition/

Cost of acquisition/ L ti

No of year for which Amortization/di ti

Accumulated depreciation/

ti ti

Net Book Value

R kNo. Descriptionq

development/installation

qdevelopment/ installation

Location license is obtained

epreciation Rate

amortization value till 31.03.20XX

as on 31.03.20XX (Rs.)

Remarks

1 2 3 4 5 6 7 8 9 10

Chainage n Details of visi

ons

.20X

X

(Rs.

)

der

ondu

ctor

s

no. (

if an

y)

nChainage (in KMs)

able

/inst

alla

tion

.)

Details of Improvement

Rs.

)

n C

ode

r cod

al p

rov

s is

in u

se

ciat

ion

on ti

ll 31

.03

1.03

.20X

X (

s

S.N

o.

Stoc

k H

old

ptio

n of

Co

refe

renc

e n

Loca

tion

Leng

th o

f Ca

acqu

isiti

on/

Cos

t (R

s.

Tota

l cos

t (R

d A

lloca

tion

sset

s as

pe

year

ass

ets

te o

f dep

rec

depr

ecia

tio

lue

as o

n 3

Rem

arks

m e Rs.

)

Des

cri

Ass

ets L

Dat

e of

a T

Fun

ful l

ife o

f as

No

of y

Rat

cum

ulat

ed

Net

boo

k va

From To Dat

e

Cos

t (

Use

f

Ac N

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

on Details of dal

3.20

XX

(Rs.

)

der

rans

form

er

nsfo

rmer

no. (

if an

y)

n n/in

stal

latio

nits Uni

t

s.)

Details of Improvement

(Rs.

)

on C

ode

s as

per

cod

ns s is

in u

se

ecia

tion

on ti

ll 31

.03

31.0

3.20

XX

ks

S.N

o.St

ock

Hol

riptio

n of

Tr

acity

of T

ran

s re

fere

nce

Loca

tioac

quis

ition

No.

of u

n

Cos

t per

U

Cos

t (R

s

Tota

l cos

t (

nd A

lloca

tio

fe o

f ass

ets

prov

isio

n

year

ass

ets

ate

of d

epre

d de

prec

iati

alue

as

on 3

Rem

ark

ate (R

s.)

Des

cr

Cap

a

Ass

ets

Dat

e of

Fun

Use

ful l

if

No

of

Ra

ccum

ulat

ed

Net

boo

k vaDa

Cos

t

Ac N

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

re n Details of l 20XX

Rs.

)

er rtal

Str

uctu

o. (i

f any

)

/inst

alla

tion Details of

Improvement

s.) Cod

e

s pe

r cod

a ls is

in u

se

atio

n

n til

l 31.

03.2

.03.

20XX

(R

S.N

o.

Stoc

k H

olde

of M

ast/P

or

efer

ence

no

Loca

tion

onst

ruct

ion/

Cos

t (R

s.)

otal

cos

t (R

s

Allo

catio

n

of a

sset

s a

prov

isio

n s

ear a

sset

s i

e of

dep

reci

depr

ecia

tion

ue a

s on

31

Rem

arks

Rs.

)

S

escr

iptio

n o

Ass

ets

r

Dat

e of

Co To

Fund

Use

ful l

ife

No

of y

e

Rat

e

umul

ated

d

et b

ook

valu

Dat

e

Cos

t (R

D

Acc N

e

1 2 3 5 6 7 10 11 12 13 14 15 16 17 18 19 20

ts n Details of al

.20X

X

(Rs.

)

der Eq

uipm

ent

no. (

if an

y)

n /inst

alla

tion

ts nit

.)

Details of Improvement

Rs.

)

n C

ode

as p

er C

oda

s s is

in u

se

ciat

ion

on ti

ll 31

.03.

1.03

.20X

X (

s

S.N

o

Stoc

k H

old

on o

f Oth

er

refe

renc

e n

Loca

tion

Acq

uisi

tion/

No.

of u

nit

Cos

t per

U

Cos

t (R

s.

Tota

l cos

t (R

d A

lloca

tion

e of

ass

ets

apr

ovis

ion

year

ass

ets

te o

f dep

rec

depr

ecia

tio

lue

as o

n 31

Rem

arks

e Rs.

)

Des

crip

tio

Ass

ets

Dat

e of

A T

Fund

Use

ful l

ife

No

of y

Rat

cum

ulat

ed

Net

boo

k va

l

Dat

e

Cos

t (

Acc N

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19

During the pilot study, following major challenges were faced in compilationf FARof FAR:

Non availability of Cost;

Non availability of Date/Year of acquisition;

Non availability of Codal life; and

Other miscellaneous issues. Other miscellaneous issues.

Cost was not available in most of cases; specially for Land, Building, Tracks, Bridge, etc.;

Unless the Fixed Assets are shown properly, we will not be able to know the true picture of financial position of any Organization;

Some of the assets are more than 50 years old, assessment of cost of such assets is also a major issue.

67

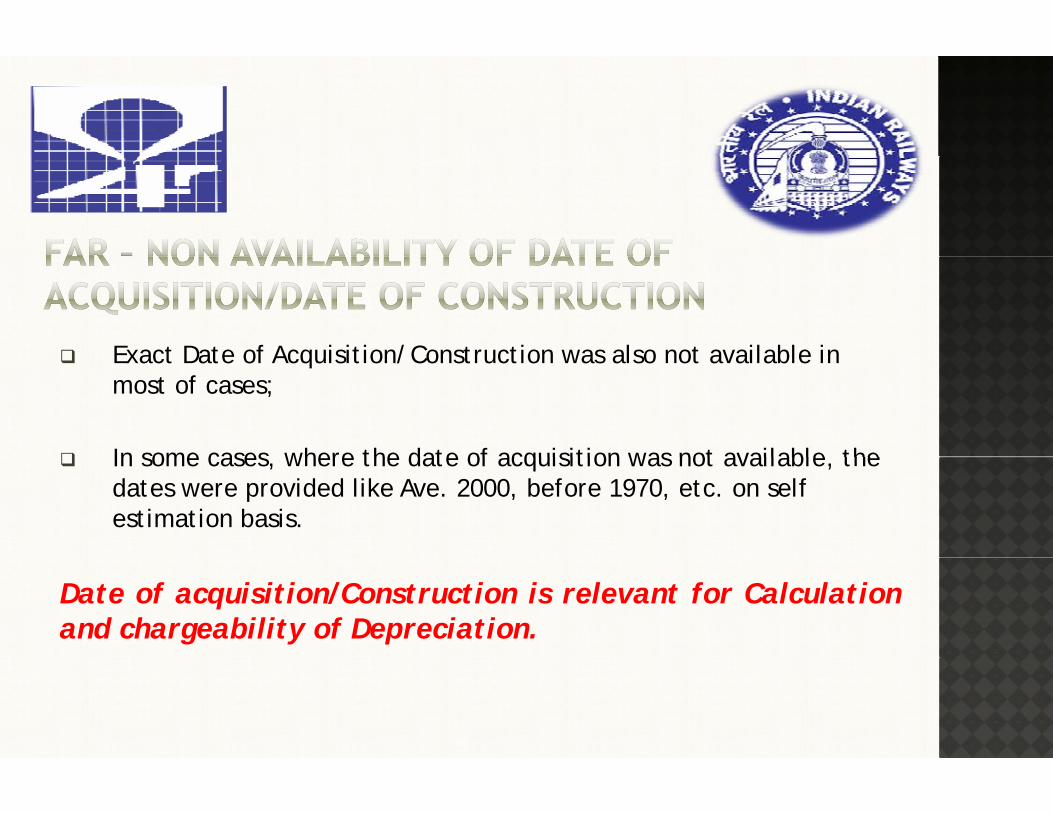

Exact Date of Acquisition/Construction was also not available in Exact Date of Acquisition/Construction was also not available in most of cases;

In some cases where the date of acquisition was not available the In some cases, where the date of acquisition was not available, the dates were provided like Ave. 2000, before 1970, etc. on self estimation basis.

Date of acquisition/Construction is relevant for Calculationand chargeability of Depreciation.

68

A Fixed asset is required to be depreciated/amortized over itsuseful life;

Para 219 of the Finance code volume- I of Indian railwaysprescribe the useful life of assets. However, in case of somepassets it prescribes the codal life in range.

For examplep

1. Codal Life of Microwave Equipment is provided as 12-15years;years;

2. Codal Life of Walkie-Talkie/VHF is provided as 5-8 years.

69

‘Assets purchased /received from’ was mentioned in the column ofReference Number instead of reference numberReference Number, instead of reference number.

In some cases classification of fixed assets were not proper and detailsof the followings are given in the format of Furniture & Fixtures:of the followings are given in the format of Furniture & Fixtures:

Tea Set; Water bottle; Thermos; Table glass; Calculator;Door curtain; etc.

Likewise, the details of followings were given in the format of Officeequipment instead of providing it in the format prescribed:

Micro Wave; UPS; Aqua guard; Refrigerator; etcMicro Wave; UPS; Aqua guard; Refrigerator; etc.

All the details of Fixed assets were provided in only one format However All the details of Fixed assets were provided in only one format. However,it should be provided in their respective format of fixed assets (FA - 1 toFA - 17).

In the format of intangible assets following details were provided duringthe NWR project:

a. Insurance premium paid;b. Renewable fees paid, etc.Basically, these are expenditures not an intangible asset.

Any item which qualifies for recognition for the purpose of fixed assets,valuation need to be made as per following:

If both the cost and date of construction/purchase are available thenasset should be valued at original cost, i.e., historical cost;

As per IGFRS- 2 “Historical cost/cost of acquisition is the amount ofcash or cash equivalent paid or the fair value of the other considerationgiven to acquire an asset at the time of its acquisition or construction”.

Where an asset is acquired through a non-exchange transaction, itscost shall be measured at its fair value as at the date of acquisition;

Where cost of any assets is not ascertainable because of inadequateor non-existent record; Such assets need to be valued at nominal

l i R 1 t th ti f g iti d ig ti t lvalue, i.e., Re.1 at the time of recognition under migration to accrualaccounting; (as per the Guidelines prepared by ICAI ARF duly approved byRailway Board)

Interest on direct borrowing in relation to any assets will also become the part of cost; and

Repairs, renovations and replacements can be capitalized, only ifsuch expenditure increases the capacity or operating efficiency orextend the useful economic life of the assetextend the useful economic life of the asset.

Land is to be recorded at the purchase price paid/payable and otherincidental costs such as registration charges incurred to bring theasset to its present location and condition;

All the land under the ownership or permissive possession of theIndian Railways (like land taken on perpetual lease), received fromother Government agencies, shall form part of the opening BalanceSheet;

If original documents are not available, valuation can be done on thebasis of value mentioned in the records of Land Revenue Department

th b i f t ti l f i il l t i th i ilor on the basis of transaction value of a similar plot in the similar areaaround the estimated year of transaction;

Any land acquired free of cost or received as gift will be recorded at

nominal value of Re.1/- for the purpose of control. However, costnominal value of Re.1/ for the purpose of control. However, cost

of any developmental work may be capitalized; and

If any land is acquired through compulsory acquisition, land isy q g p y q ,

recorded at the total compensation paid/payable.

It is pertinent to note that “As per the valuation methodology

finalized by Railway Board, consolidated value of Land will be taken

from the appropriation accounts of concerned Zonal

Railway/Production units”.

In addition what has been stated in the general norms of valuationmentioned earlier the following specific norms with respect to valuationmentioned earlier, the following specific norms with respect to valuationof buildings should be followed:

If it i h d th it i t b l d t h i d ll If it is purchased then it is to be valued at purchase price and allother incidental costs incurred to bring the asset to its presentlocation and condition;

If the building has been constructed, then the cost of the buildingwill be taken as the cost of construction. However, if any amount isreceived as grant than same shall be deducted from the cost;received as grant than same shall be deducted from the cost;

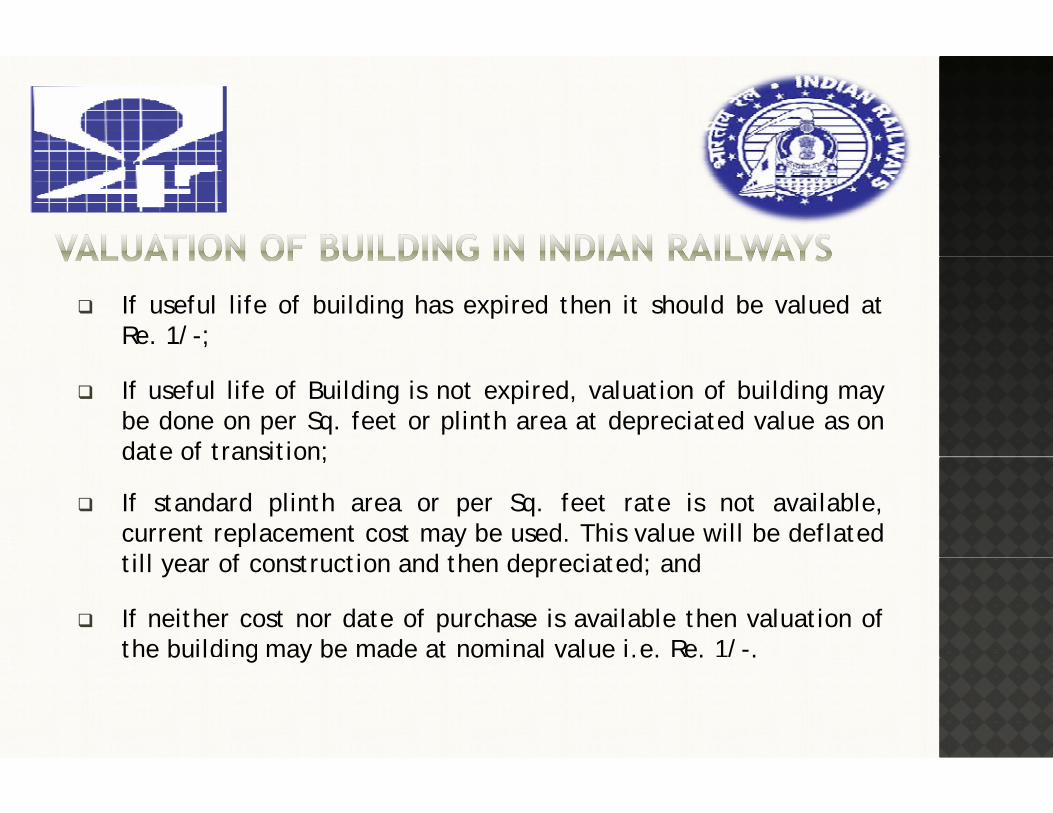

If useful life of building has expired then it should be valued atRe. 1/-;

If useful life of Building is not expired, valuation of building maybe done on per Sq. feet or plinth area at depreciated value as ondate of transition;date of transition;

If standard plinth area or per Sq. feet rate is not available,current replacement cost may be used. This value will be deflatedtill f t ti d th d i t d dtill year of construction and then depreciated; and

If neither cost nor date of purchase is available then valuation ofthe building may be made at nominal value i.e. Re. 1/-.t e bu l g ay be a e at o al value .e. e. .

Capital work-in-progress (CWIP) is a main category of Fixed Assets.CWIP is not recorded in any of the asset register. However, ay g ,separate CWIP register is maintained to record progressive bills forconstruction;

CWIP is valued at the amount of money spent and paid plus the CWIP is valued at the amount of money spent and paid plus theamount of bills passed but not yet paid;

No depreciation is charged on CWIP since the asset has not been putp g pto use; and

Asset should be transferred from CWIP to fixed asset register, onceasset got complete and put to useasset got complete and put to use.

AS 26 describes “ An intangible asset is an identifiable non-monetary assets, without physical substance, held for use in the production or supply of goods or services, for rentals to others, or for administrative purposes”.

If an intangible asset is purchased/constructed then cost ofintangible assets comprises all expenditure directly attributed or costincurred to make the assets ready for its intended use;

If an intangible asset is acquired in exchange for shares/securities ofreporting enterprise, the asset is recorded at its fair value, or thefair value of securities issued, whichever is more clearly evident.

S. No. Scenario Basis of Valuation

1 If both the cost and date of purchase/construction is

Original Cost, i.e., historical costp

available/ascertainable

2 If cost is not available/unascertainable but

• If normal useful life of assets is expired, then it will be

the date of construction/purchase is available

p ,valued at Re.1/-; and

• For assets that have not li d h i f l lif outlived their useful life,

valuation shall be done based on current standard costcost.

S. No Scenario Basis of Valuation

3 If date of purchase is not ascertainable

The assets valuation is to be done on case by case basis.y

4 In case neither the cost nor the date of

Valuation will be at Re.1/-, the same being considered as the

purchase/construction is available

gresidual value.

5 If assets received as a If evidence exists, or it is known gift

,that an asset was received by IR as a gift, i.e., without any consideration being paid, it h ld b i d R 1/ should be recognized at Re.1/-.

Start

YesWas the assets received as a

gift?

Yes

Value at Re.1/-

No

Is the cost of the assets available?

Yes

Use Historical Costassets available?

No

Is the year of purchase

Yes

Is it beyond useful life?

Yes

Value at pavailable?

No

useful life?Re.1/-

N

NoNo

No

Does it appear to be beyond useful

life?

Current standard cost

YesYes

Deflated till the year of purchase

Value at Re.1/-

To prepare financial statements data of respective Financial year To prepare financial statements, data of respective Financial yearis required to be captured which is not considered in cash basedfinancial statements;

ICAI ARF team designed various formats in pilot project to capturesuch data;

Now, these formats will be circulated in all Zonal Railways andProduction Units to capture all such data which is not considered inthe cash based financial statements;the cash based financial statements;

Following table shows the formats finalized for the Current Assets Data:

S. No Name of Current Assets PrescribedFormat

1 Investments CA-1

2 Advance to Employees CA-2

3 Misc Advances other than employees CA-33 Misc. Advances other than employees CA-3

4 Earnest Money and Deposits CA-4

5 Transfer Certificate (TC) Debit CA-5

6 Transfer Certificate (TC) Credit CA-66 Transfer Certificate (TC) Credit CA 6

7 Demand Recoverable/Siding Charges CA-7

8 Bank Balances CA-8

S. No Name of Current Assets PrescribedFormatFormat

9 Cash & Cash Equivalents CA-9

l k10 Inventory/Closing Stock CA-10

11 Diesel stock in Railway Diesel Installation (RDI) CA-10A

12 Imprest CA-11

13 R i bl CA 1213 Receivables CA-12

14 Foreign Service Contribution CA-13

15 Advance against State Railway Provident Fund CA-14

16 Warranty Charges CA-1516 Warranty Charges CA 15

Details of InvestmentsForm :- CA-1

S No Description Specify the fund Nature of Date of Duration of Amount Accrued Closing BalS.No. Description Specify the fund from which

Investment made

Nature of Deposit

Date of Investment/

Deposit

Duration of Investment

Amount Invested

(Rs.)

Accrued Interest up to 31.03.20XX

(Rs.)

Closing Bal. as on

31.03.20XX (Rs.)

1 2 3 4 5 6 7 8 9

Details of Advance to EmployeesForm :- CA-2

S.No. Name of Employee Nature of Advance

Amount Advanced

(Rs.)

Principal outstanding as on 31.03.20XX

(Rs )

Interest receivable as on

31.03.20XX (Rs )

Total amount outstanding as on 31.03.20XX

(Rs )(Rs.) (Rs.) (Rs.)

1 2 3 4 5 6 7

Details of Misc. Advance other than EmployeesForm:- CA-3

S.No. Name of Supplier/Contractors

Nature of Advance

Date of Advance

(DD/MM/YY)

Amount Advanced

(Rs.)

Interest receivable as on 31.03.20XX (if

any) (Rs.)

Total amount outstanding as on 31.03.20XX

(Rs.)

1 2 3 4 5 6 7

Details of Earnest money and DepositForm -CA-4

S.No. Particulars Nature of Deposit Amount of Deposit as on 31.03.20XX (Rs.)

Remark(s)

1 2 3 4 5

Details of Transfer Certificate (TC) DebitForm:- CA-5

S. No. Name of Accounting Unit

Particulars of TC Specify whether inward or outward

Date of TC TC reference

no. (if Any)

Total amount outstanding as on 31.03.20XX (Rs.)

1 2 3 4 5 6 7

Details of Transfer Certificate (TC) CreditForm:- CA-6

S No Name of Particulars of Specify whether Date of TC reference Total amountS. No. Name of Accounting Unit

Particulars of TC

Specify whether inward or outward

Date of TC

TC reference no. (if Any)

Total amount outstanding as on 31.03.20XX (Rs.)

1 2 3 4 5 6 7

Details of Demand Recoverable/Siding ChargesForm:- CA-7

S. No. Name of Parties Nature of Demand Due date of Payment

Total amount outstanding as on 31.03.20XX (Rs)

1 2 3 4 5

Details of Bank BalancesForm: CA-8

S. No. Name of Account(s) Name of the Bank Branch Balance as on 31.03.20XX (Rs.)

1 2 3 4 51 2 3 4 5

Details of Cash and Cash Equivalents Form: CA-9

S N P ti l Cl i B lS. No. Particulars Closing Balance as on 31.03.20XX (Rs.)

1 2 3

Details of Inventory/Closing Stock Form: CA-10

S.No. Name of Item/ Material Specification (if any)

Unit of Measuremen

t

Qty./No. of units of item in

stock as on 31 03 20XX

Unit Cost (Rs.)

Total Value as on 31.03.20XX

(Rs.)31.03.20XX

1 2 3 4 5 6 7

Details of Diesel stock in Railway Diesel Institution

Form: CA-10A

S.No. Tank No. Capacity Quantity as on 31st March 20XX

Rate of purchase

Unit of Measurement (UOM) Total Amount (Rs.)p ( )

Details of ImprestForm: CA-11

S. No. Particular of employees Purpose of Imprest

Amount of Imprest Given

Closing Balance as on 31.03.20XX

(Rs.)

1 2 3 4 5

Details of ReceivablesForm - CA 12

S. No. Particulars Opening Balance as on 01.04.20XX

(R )

Amount of Bill raised during the

Y

Amount Received during the Year

Total amount outstanding as on 31 03 20XX (R )(Rs.) Year 31.03.20XX (Rs)

Details of Foreign Service ContributionForm: CA 13Form: CA - 13

S. No. Name of Employee Date of Deputation Amount to be

receivedAmount

RecoveredOutstanding

Balance

Details of Advance Against State Railway Provident FundForm:- CA-14

S. No. Name of Employee Total amount outstanding as on 31.03.20XX (Rs.)

Total amount outstanding as on 31.03.20XX (Rs.)

Details of Warranty ChargesForm:- CA-15

Period of warranty Amount h d

Amount to be i d f dS. No. Particular of Warranty charged

exclusively for warranty

carried forward for following FY

From To

S. Name of Current Liabilities Prescribed

Following table shows the formats finalized for the Current Liabilities Data:

S. No

Na e o Cu e t ab l t es esc bedFormat

1 TDS payable U/s 192 (Salary Payment) CL-1

2 TDS payable U/s 194C (Payment to Contractors) CL-2

3 TDS payable U/s 194J (Payment for ProfessionalServices)

CL-3

4 Service Tax payable CL-4

5 Sales Tax/VAT payable CL-5

6 Wages Payable CL-6

7 Salary Payable CL-7

8 Provident Fund CL-8

9 Other Employee Benefit Payable CL-9

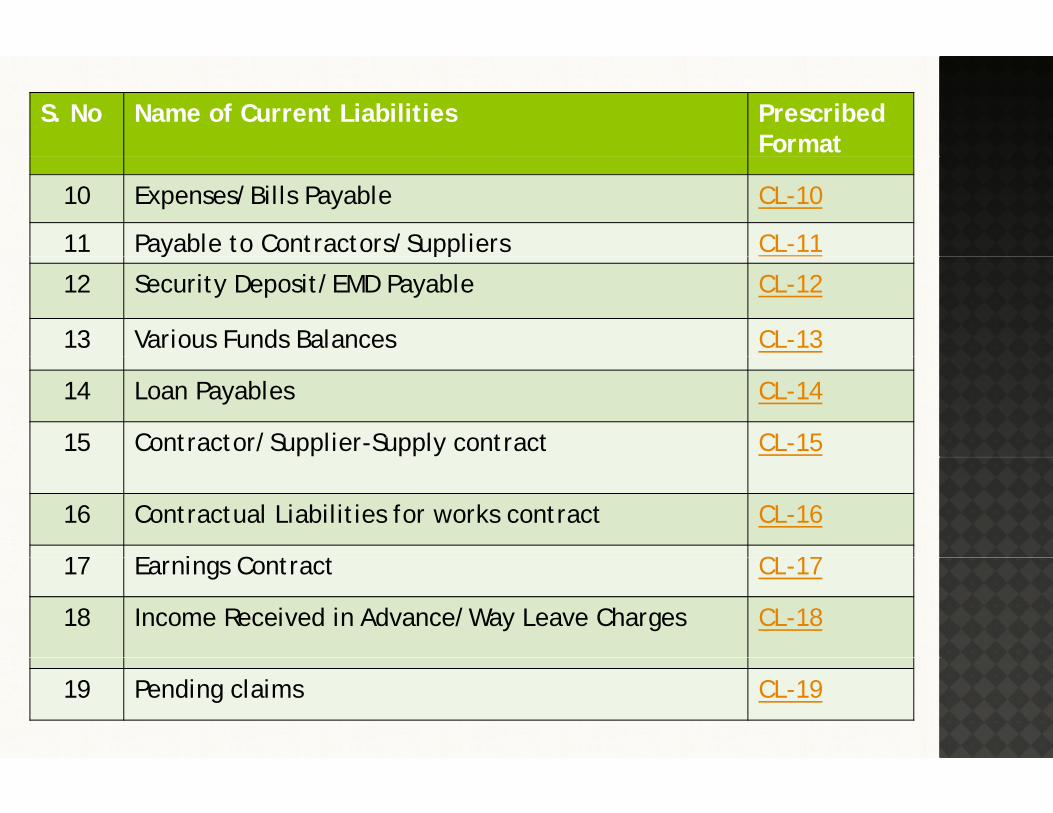

S. No Name of Current Liabilities PrescribedFormat

10 Expenses/Bills Payable CL-10

11 Payable to Contractors/Suppliers CL-11y pp

12 Security Deposit/EMD Payable CL-12

13 Various Funds Balances CL-13

14 Loan Payables CL-14

15 Contractor/Supplier-Supply contract CL-15

16 Contractual Liabilities for works contract CL-16

17 E i C CL 1717 Earnings Contract CL-17

18 Income Received in Advance/Way Leave Charges CL-18

19 Pending claims CL-19

Detail of TDS payable Under Section 192 (Salary Payment)Form:- CL-1

S.No. Particulars TDS payable as on 31.03.20XX (Rs.) Remarks

1 2 3 4

Detail of TDS payable Under Section 194C (Payment to Contractors)Form:- CL-2

S.No. Name of Contractor Nature of Expenditure TDS Payable as on 31.03.20XX (Rs.)

Remarks

1 2 3 4 5

Detail of TDS payable Under Section 194J (Payment for Professional Services)

Form:- CL-3

S.No. Particular of Services Name of Service Provider

TDS Payable as on 31.03.20XX (Rs.)

Remarks

1 2 3 4 5

Detail of Service Tax Payable Form:- CL-4

S.No. Particulars Balance Outstanding on 31.03.20XX (Rs.)

Remarks

1 2 3 4

Detail of Sales Tax/ VAT Payable

Form:- CL-5

S.No. Particulars Balance Outstanding on 31.03.20XX (Rs.)

Remarks

1 2 3 4

Detail of Wages Payable Form:- CL-6

S.No. Particular of Wages Balance Outstanding on 31.03.20XX (Rs.)

Remarks

1 2 3 4

Detail of Salary PayableForm:- CL-7

S.No. Particulars of Salary Balance Outstanding on 31.03.20XX (Rs.)

Remarks (If any)

1 2 3 4

Detail of Provident Fund (PF)Form:- CL-8

S. No. Opening Balance as on 01.04.20XX

Subscription received during the

year

Interest earned during the year

Withdrawal/ Payment to

subscriber made during the year

Closing Balance as on 31.03.20XX

g y

1 2 3 4 5 6

Detail of other Employee Benefits PayableForm:- CL-9

S.No. Particulars Balance Outstanding as on 31.03.20XX (Rs.)

Remarks

1 2 3 4

Detail of Expenses/Bills PayableForm:- CL-10Form: CL 10

S.No. Particulars of Expenditure Balance Outstanding as on 31.03.20XX (Rs.)

1 2 3

Detail of amount payable to Contractors/SuppliersForm:- CL-11

S.No. Name of Contractors/Suppliers Nature of Expenditure Balance Outstanding as on 31.03.20XX (Rs.)

Remarks

1 2 3 4 5

Detail of Security Deposits/EMD payablesForm:- CL-12

S.No. Name of Contractors Nature of work Specify whether Security deposit

or EMD

Balance Outstanding as on 31.03.20XX

(Rs.)

1 2 3 4 5

Details of Various Funds BalancesForm:- CL-13

S.No. Particulars of Fund Opening Balance as on 01.04.20XX

(Rs.)

Contribution to During

FY

Deduction from Funds During

FY

Balance Outstanding

as on

Remarks

31.03.20XX (Rs.)

1 2 3 4 5 6 7

Details of Loans Payable

Form:- CL-14

S.No. Name of Financial

Nature of Loan

Whether secured or

Purpose of Loan

Amount of loan outstanding as

Amount of interest

Amount of penal interest

RemarksFinancial Institution/Bank

Loan secured or unsecured

Loan outstanding as on 31.03.20XX

interest payable as on 31.03.20XX

penal interest payable (If any) as on

31.03.20XX

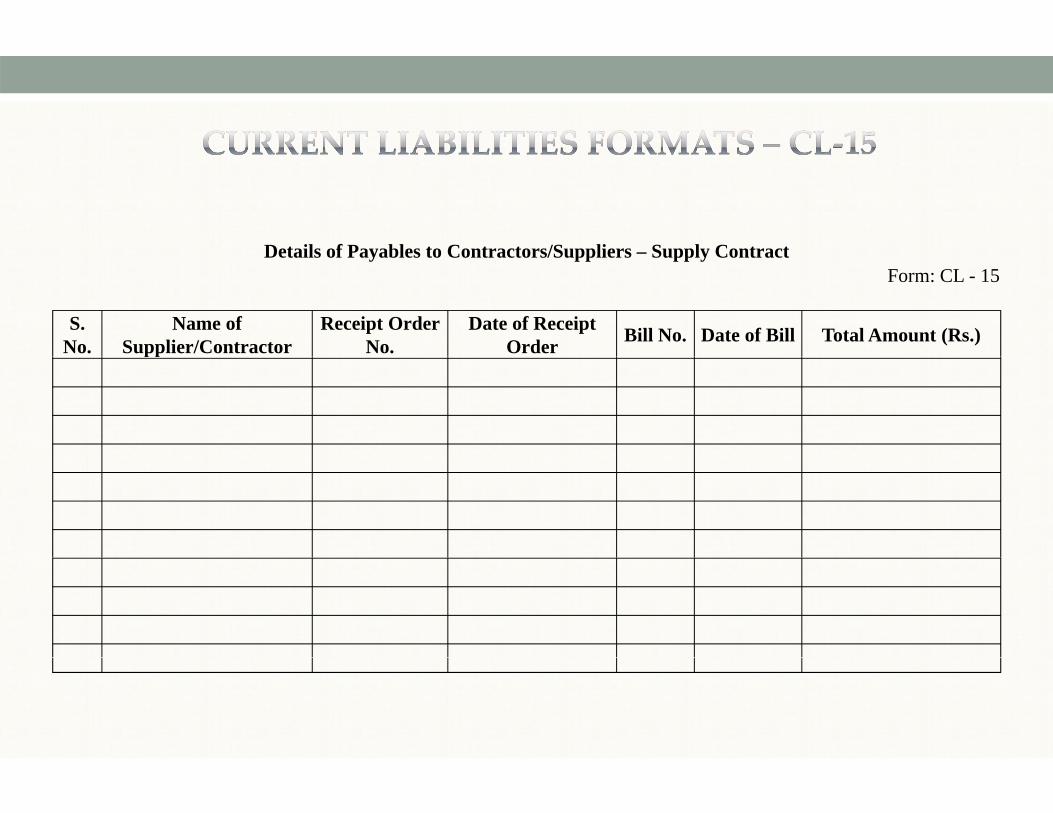

Details of Payables to Contractors/Suppliers – Supply ContractDetails of Payables to Contractors/Suppliers Supply ContractForm: CL - 15

S. No.

Name of Supplier/Contractor

Receipt Order No.

Date of Receipt Order Bill No. Date of Bill Total Amount (Rs.)pp

Details of Contractual Liabilities for Works contractDetails of Contractual Liabilities for Works contract

Form: CL - 16

P i d f Measurement of work Bill b i d

S. No.

Particulars of Contract

Work Order

No.

Name of Contract

orLocation

Period of Contract Total

Contract Value

Measurement of work done but bill not

submitted

Bill submitted but not Paid

Remarks

From To Date of Measurement

Amount for Bill

Date of Bill

Amount of BillMeasurement for Bill of Bill of Bill

Details of Earning Contract Form: CL - 17

S.No.Name of

Contractor Nature of Contract LocationLicense

Fees Cycle of

License Fees

Period of Contract

RemarksFrom To

Details of Income Received in Advance/Way leave Charges

Form - CL-18

S. No. Particulars Amount Received d i th Y

Date of Advance R i d

Period of Ad

Remarkduring the Year Received Advance

Detail of pending claim

Form: CL – 19

S. No. Particulars of C i

Amount of Claim Whether claim Amount of Claim Whether claim i i RemarksS. No. Claimant Lodge accepted accepted accepted is paid Remarks

Statement of Financial PositionAs on 31st March 20XX

(Fi i R )(Figure in Rs.)

Liabilities Schedule As on 31st March 20XX

As on 1st April 20XX

EquityCapital at Charge (Loan in perpetuity) 1Safety Funds 2

Designated Funds (Internally Generated Funds) 3Investment Financed from Designated Fund (Internally Generated Funds) 4Reserves and Surplus 5p

Non‐current liabilitiesFinance Lease ObligationsDeposits 6Provident Fund and Other Funds 7

Current LiabilitiesFinance Lease ObligationsE l B fit P bl 8Employee Benefits Payable 8Other Liabilities 9

Total Liabilities

Statement of Financial PositionAs on 31st March 20XX

(Fi i R )(Figure in Rs.)

Assets Schedule As on 31st March 20XX

As on 1st April 20XX

Non Current assetsFixed AssetsFixed AssetsTangible Assets 10Gross BlockLess: Accumulated DepreciationNet BlockNet Block

Intangible Assets 11Gross BlockLess: Accumulated AmortizationNet Block

Capital work in progress (CWIP) 12Loans and advances 13Current AssetsCash and cash equivalents 14Receivables 15Inventories 16Other assets 17Adjustment Accounts (Annexure C)

North Western Railways Fund

Total Assets

Statement of Financial Performance

For the year ended 31st March 20XX

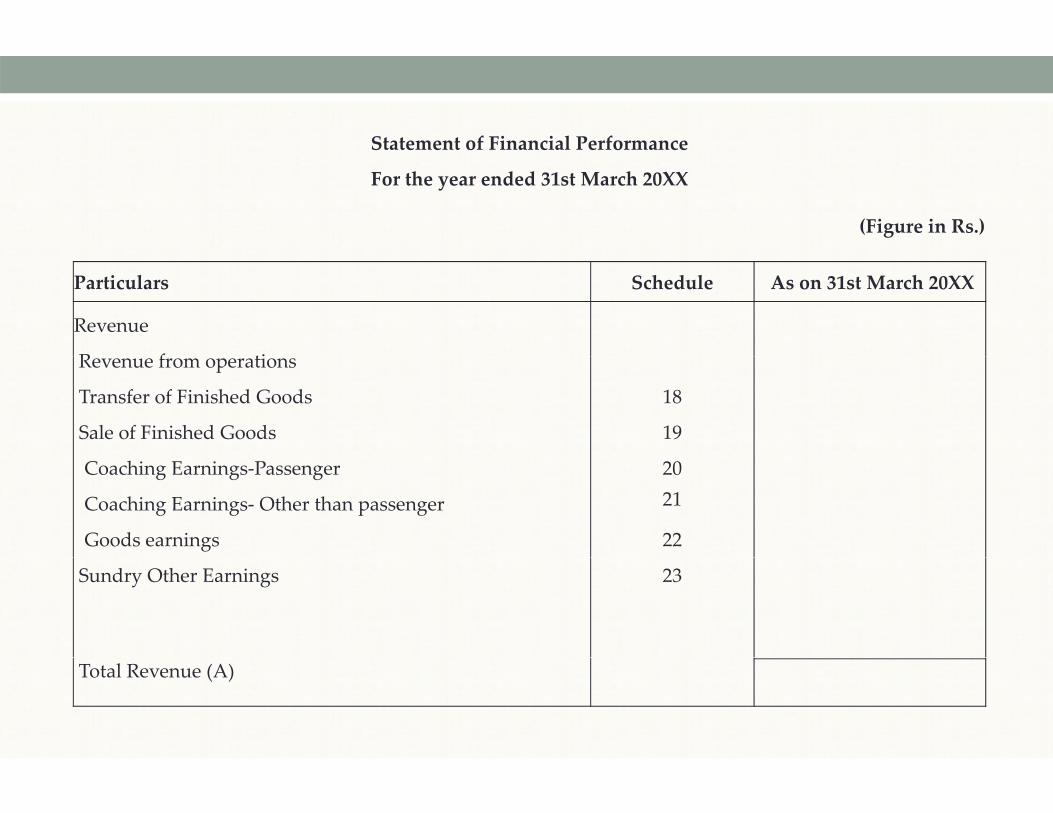

(Figure in Rs.)

Particulars Schedule As on 31st March 20XX

Revenue

R f tiRevenue from operations

Transfer of Finished Goods 18

Sale of Finished Goods 19

Coaching Earnings‐Passenger 20

Coaching Earnings‐ Other than passenger 21

Goods earnings 22

Sundry Other Earnings 23

Total Revenue (A)

Statement of Financial PerformanceFor the year ended 31st March 20XX

(Figure in Rs.)(Figure in Rs.) Particulars Schedule As on 31st March 20XXExpensesCost of Material Consumed 24Establishment Expenses 25P d F l 26Power and Fuel 26Repair & Maintenance ‐ other than Stores 27Repair & Maintenance ‐ Stores 27Finance Lease ChargesOperational Expenses 28p pOther expenses 29Changes in Inventories of Finished Goods, Stock in Process & Stock in Trade 30Statutory AuditExpenditure on SurveyExpenditure on Survey

Profit before Depreciation and Appropriation to Funds and payment of DividendDepreciation and Amortization 10, 11

Profit after Depreciation and before Appropriation to FundsAppropriation to Pension FundAppropriation to Depreciation Reserve Fund

Dividend Paid

Surplus/(Deficit) After contribution to Reserve Fund

Cash Flow StatementFor the year ended 31st March 20XX

(Fi i R )(Figure in Rs.) Particulars AmountA. Cash Flow from Operating Activities

Net Profit as per Profit & Loss AccountNet Profit as per Profit & Loss AccountAdjustment for: Depreciation and Amortization Appropriation to Pension FundAppropriation to Depreciation Reserve FundAppropriation to Depreciation Reserve FundDividend PaidPayment of Finance Lease ChargesOperating Profit before working capital changesAdjustment for change in working capital:j g g pIncrease/(Decrease) in Employees Benefit PayableIncrease/(Decrease) in other current liabilitiesIncrease/(Decrease) in Receivable(Increase)/(Decrease) in Inventories

Increase/(Decrease) in Current Finance Lease ObligationIncrease/(Decrease) in other current assetsIncrease/(Decrease) in Adjustment Accounts

Net Cash Flow from Operating Activities

Cash Flow StatementFor the year ended 31st March 20XX

(Fi i R )(Figure in Rs.) Particulars AmountB. Cash Flow from Investing ActivitiesAddition in Fixed AssetsAddition in Capital Work in ProgressAddition in Capital Work in ProgressAddition in Loans and AdvancesIncrease/(Decrease) in Provident Fund and other FundsIncrease/(Decrease) in DepositsNet Cash Flow from Investing ActivitiesNet Cash Flow from Investing Activities

C. Cash Flow from Financing ActivitiesIncrease/(Decrease) in Capital In ChargeIncrease/(Decrease) in Safety Fund( ) yIncrease/(Decrease) in Designated Funds (Internally Generated)Increase/(Decrease) in Finance Lease ObligationDividend PaidPayment of Finance Lease ChargesAppropriation to Pension FundAppropriation to Depreciation Reserve FundIncrease/(Decrease in Investment Financed from Designated FundNet Cash Flow from Financing Activities

Cash and Cash Equivalents (Opening Balance)Net Increase/ (Decrease) in Cash and Cash Equivalents Cash and Cash Equivalents (Closing Balance)

Schedules forming part of Financial Statements

Schedule 1 Capital at Charge (Loan in Perpetuity) (Figure in Rs.)Schedule 1 Capital at Charge (Loan in Perpetuity) (Figure in Rs.)

Particulars

Opening Balance as on 1st April

Addition During the Year

Adjustment during the Year on account of Transfer without Financial Adjustment

Closing Balance as on 31st

March 20XXp20XX Financial Adjustment

(TWFA)March 20XX

Loan Capital

Total

Schedule 2 Safety Fund (Figure in Rs )Schedule 2 Safety Fund (Figure in Rs.)

Particulars Opening Balance as on 1st April 20XX

Addition during the year

Closing Balance as on 31st

March 20XX

Special Railway Safety FundRailway Safety Fund

‐Total

Schedule 3 Designated Funds (Internally Generated Fund)(Figure in Rs.)(Figure in Rs.)

Particulars

Opening Balance as on 1st April

20XX

Additions during the year

Interest earned during

the year

Deduction during the year

Closing Balance as on 31st

March 20XX

Depreciation Reserve FundPension Fund

Total

Schedule 4 Investment Financed from Designated Fund (Internally Generated Funds)(Figure in Rs.)

AdditiAdjustment during

th t fParticulars Opening Balance

as on 1st April 20XX

Additions during the

year

the year on account of Transfer without

Financial Adjustment (TWFA)

Closing Balance as on 31st

March 20XX

Railway Capital FundDepreciation Reserve FundDevelopment FundOpen Line WorksOpen Line Works Revenue

‐Total

Schedule 5 Reserves and Surplus (Figure in Rs.)

ParticularsOpening

Balance as on 1st April 20XX

Additions during the

year

Interest earned

during the year

Deduction during the year

Closing Balance as on 31st March

20XX

Surplus carried forward from P & L account

TotalTotal

Schedule 6 Deposits (Figure in Rs.)

Particulars As on 31st March 20XX