impacts of macroeconomic indicators on inward fdi in

TRANSCRIPT

Impacts of Macroeconomic Indicators on Inward FDI in Nigeria:

1981 2016

Abstract

Introduction

–

Dr. Ochuko Benedict Emudainohwo

Government's macroeconomic intervention policy are designed to attainingfull

employment (low unemployment), stable prices (low inflation rate), high and sustainable rate of economic growth, rise in average living standards, just

distribution of income and keeping the balance of payment in equilibrium (Abata,

Kehinde & Bolarinwa 2012; Adefeso & Mobolaji, 2010). An economy that achieved

macroeconomic policy objective has an advantage of attracting inward FDI. Macroeconomic policy management is aggregating macro-economic variables

having some common features to improve the performance of an economy as a

whole.

economy as a whole.

This paper examines the impact of macroeconomic indicators on FDI inflows in

Nigeria using secondary data extracted from Central Bank of Nigeria, World Bank

World Development Indicator and UNCTAD. The study adopted Fully Modified

Ordinary Least-Square Regression Model. The study finds long-run relation among the

variables. Over the period examined, total government expenditure, trade openness

and marker sizeproxy with GDP have positive impact on FDI inflow into Nigeriawhile

real effective exchange rate has negative and insignificant bearing with FDI inflows

into Nigeria. However, only total government expenditure and trade openness are

statistically significant to explain FDI inflows into Nigeria over the period examined.

The study suggests dedicating part of government expenditure for building

infrastructural facility and strong institutions that will minimise transaction cost to

foreign investors, and adopt policy that will appreciate exchange rate in Nigeria.

Key words:macro-economic, fully modified ordinary Least-square regression,

foreign direct investment, government expenditure, exchange rate, trade

openness, and market size.

JEL Classification:C32, E70, F23, F62.

,

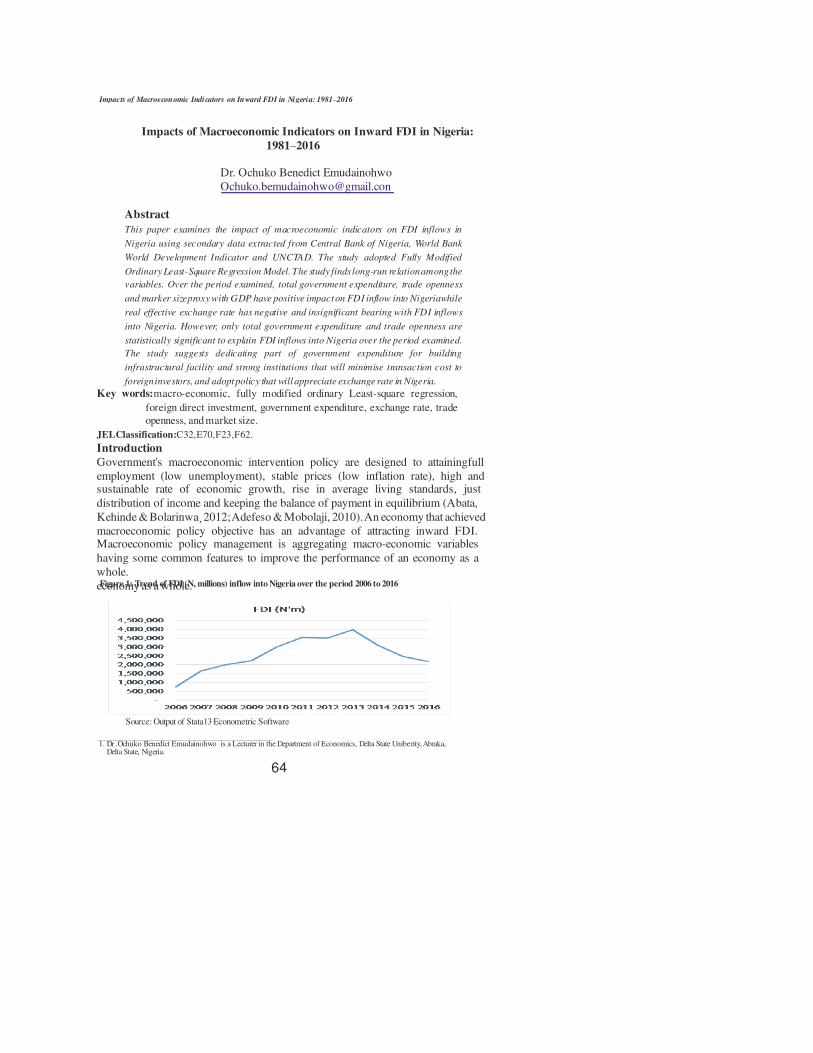

Figure 1: Trend of FDI (N, millions) inflow into Nigeria over the period 2006 to 2016

Source: Output of Stata13 Econometric Software

64

1. Dr .Ochuko Benedict Emudainohwo is a Lecturer in the Department of Economics, Delta State Uniberity, Abraka, Delta State, Nigeria.

Impacts of Macroeconomic Indicators on Inward FDI in Nigeria: 1981 2016–

Source: Output of Stata13 Econometric Software

Figure 1 shows that value of FDI rise from 2006 to 2013 and thereafter, it has been experiencing a downward trend. In the same vein, the macro-economic factors have

also experienced varied movement partly due to government policy to stabilise and

or improve the economy for attracting inward FDI. Given that

(OECD, 2002)

The remaining section is organised as follows: Section2 is literature review and

hypotheses formulation. Section 3 is source of data and methodology. Section 4 presents empirical re port, and section 5 is conclusion and summary.

This section review extant literatures and formulates hypotheses with important

macro-economic determinants of FDI discussed in previous literature. Among these

determinants are: government expenditure, real effective exchange rate, trade openness, market size and GDP growth potential of the host economy(Walsh & Yu,

2010). From the reviewed literatures, the specific independent variables that will be

adopted for this study are discussed as follows:

Traditional Keynesian macroeconomic predict that public expenditure contributes to positive economic growth through multiplier effects on aggregate demand,

increase in government consumption, increase in employment and investment

(Alimi, 2014).Oladipo (2013) examines the relation between government recurrent

expenditure and FDI using time series data for the period 1985-2010 in Generalised

Method of Moment (GMM) estimates, and showed that government recurrent expenditure has strong and positive im pact on FDI.Muhammad, Khan, Hunjra,

Ahmad &Chani (2011) studied the link among public spending, FDI and economic

growth in Pakistan for the period 1975 to 2008 based on simple accounting

framework. They showed that public expenditure slowdown economic growth while FDI is positively associated with growth and this remains strengthens until

public spending grow less than 6 per cent per annum and beyond this level positive

effects of FDI become fragile and becoming uninteresting to attracting FDI i nflows.

H : Government expenditure have positive relation with FDI inflow in Nigeria.

Exchange rate play a key significant role in trades and flows of FDI particularly due

to its rate of fluctuation (Ullah, Haider& Azim 2012; Chakrabarti, 2001) and it has a

major effect on macroeconomics performance of country's (

2014; Cushman,

1985). The exchange rate makes it possible to convert domestic currencies into foreign currencies and vice versa. Exchange rate is, therefore, the price of one

currency in terms of another currency. The exchange rate assumes relevance because

of cross-border flows of goods, services, financial assets and funds transfer.

FDI enhances

growth and economic development of the host countries, while economic

growth is directly related to attracting FDI inflows , this study intends to add to existing literature, the macro-economic drivers of FDI in

Nigeria, a developing economy.

Literature Review and Hypotheses Formulation

Government expenditure

Exchange Rate

Muhammad,

Muhammad, Amjad, Muhammad, Mansoor, Iltaf&Tehreem

1

,

,

65

Impacts of Macroeconomic Indicators on Inward FDI in Nigeria: 1981 2016–

Theoretically, depreciation of the host country currency decreases the relative total

cost of production in terms of a higher valued foreign currency and increases return on capital, and hence induces inward FDI (Seo, Tarumun& Suh 2002). Where there

is depreciation of host country currency, some assets will cost less to foreign

investors: the depreciation of the host economy currency increase the relative wealth

position of foreigners and hence lower the relative cost of capital (Froot& Stein,

1989).Similarly, weak exchange rate is assumed to make host economy currency to be

cheaper to foreign investors and thus has a systematic effect on attracting inward

FDI. Froot& Stein (1989) show that an economy with weaker currency tends to

attract inward FDI within an imperfect capital market model and thus, a stronger real

currency exchange rate of the host economy will encourage investing at

home.Sharifi-Renani&Mirfatah (2012) in their evaluation of the determinants of inward FDI in Iran using Johansen and Juseliu's co-integration system approach

model for the period 1980Q2 to 2006Q2, find that in Iran, exchange rate has positive

relationship with inward FDI. Consistent positive influence of exchange rate level

on FDI was also reported by Seo, (2002) who examined the link between

exchange rate with FDI flows to Korea over the period 1985 to 2000, using OLS. Ullah (2012) studied the relationship between FDI with exchange rate using

time series data for the periods 1980 – 2010 for Pa kistan. It was reported that FDI is

positively associated with Rupee depreciation and exchange rate volatility dissuades

FDI.Ehimare (2011) also show that exchange rate has positive effect on FDI in

Nigeria. Edwards (1990) support a significant and positive correlation between exchange rate and FDI. Oladipo (2013) also showed that exchange rates have

significant and positive correlation with FDI in Nigeria.

On another hand, it is argued that the weaker the currency of a country the less likely

for foreigners to invest in that location because, the income stream from a country

with a weak currency is associated with an exchange rate risk (Chakrabarti, 2001; Aliber, 1970).The researcher is of the view that using earnings from an economy

with a weak currency for investment in an economy with a strong currency may

result in higher cost of investment to the foreign investors. In an examining the

impact of changes in exchange rate in China on FDI, Jin&Zang (2013) used monthly

FDI data in China and index of real exchange rate of RMB for the period January

1997 to September 2012. They showed that appreciation in RMB promotes FDI after the reforms in the exchange rate regime in 2005. Strong negative correlation

between exchange rates and FDI is supported by Blonigen&Feenstra (1996).

Among the main objectives of exchange rate policy in Nigeria are to preserve the

value of the domestic currency (Naira), and the overall goal is of macroeconomic

stability. Nigeria has operated several exch ange rate regimes which can be sub-divided in to 2: fixed exchange rate regime from whence Central Bank of Nigeria

(CBN) started operation in 1959 to June 1986 when structural adjustment

programmes was introduced; and flexible exchange rate regime from June 1986

with the exchange rate liberalisation policy under SAP to date (CBN, 2016). As

noted earlier, part of exchange rate regime is to create friendly business environment that will attract foreign investors to bring their capital into an econ omy. Given the

,

et al

et al.,

66

Impacts of Macroeconomic Indicators on Inward FDI in Nigeria: 1981 2016–

volume of studies that supported positive exchange rate, this study hypothesis as

follows:H : Exchange rate have positive relation with FDI inflow in Nigeria.

Trade openness measures the international competitiveness of a country in the

global market (Ehinomen & Da'silva, 2014). It is argued theoreticallythat openness

to trade and FDI are important for enhancing industrial sector growth, attracting

foreign technology and possible spill-over, and creatingopportunities for

technology advancements ( Umer&Alam, 2013; Chakrabarti, 2001; Solow, 1957).

Trade openness is expected to minimise hurdles to trade, improves total factor

production, reduces costs of production, increase efficiencies through competition,

facilitates the flow of international capital and redirects factor of production to more

productive sectors (Romer, 1990). Trade openness suggests limited controls in

taxes, quotas or state monopolies on businesses rather than to improve business

environment competitiveness for attracti ng inward FDIs (Boateng, Hua, &Wud

2015).

Trade openness is expected to positively attract inward FDI (Asiedu, 2002).

Empirical studies support positive and significant relation between openness and

inward FDI (Boateng 2015; Chakrabarti, 2001; Edwards, 1990). Pradhan

(2010) also showed that in India, trade openness had positive and statistically

significant impact on FDI inflows in the post-globalisation-era (1991-2007) but not

statistically significant during the pre-globalisation-era (1980-1990 ). However,

insignificant bearings from trade openness on FDI inflows have also been reported

from an empirical examination (Pradhan &Kelkar, 2014; Wheeler &Mody, 1992).

The opposing argument is that trade openness leads to macroeconomic imbalance in

the host country (Levine &Renelt, 1992). Since equilibrium rate of growth differs

among countries and regions, it is argued that trade openness perceived benefits may

not always hold (Edwards, 1998). Empirical study has found that the bearing

between openness and inward FDI is negative and s tatis tically

significant(Umer&Alam, 2013).

As part of measure to improve business environment, Nigeria liberalised trade and

investment to support development and also to attract FDI inflows. Liberal policies

are expected to minimise transaction costs (Walsh & Yu, 2010; Edwards, 1990), it

portrays open and secured markets for trade and investing partners (Klasra, 2011)

and it eased extreme controls that minimised bureaucratic barriers for foreign

2

Trade openness

,

et al.,

67

Impacts of Macroeconomic Indicators on Inward FDI in Nigeria: 1981 2016–

investors. Other than liberalisation policy from SAP of 1986, NIPC Decree and

Foreign exchange (monitoring and miscellaneous provision) Decree both of 1995, brings trade openness with it, further liberalisation of the foreign exchange market in

2006 (CBN, 2006) and adoption in October 2005 of the Economic Community of

West African States tariff (UNCTAD, 2009) have greatly improved trade openness

in Nigeria. Though, World Economic Forum (2014, p. 24) remarked that 'Nigeria's

market is very open, yet many non-tariff barriers are hindering trade development'.

Oladipo (2013) used (GMM) estimates to show that

trade openness is significant and positively correlate to FDI in Nigeria.Following

theoretical arguments for liberal trade policy (Umer&Alam, 2013;Chakrabarti,

2001; Edwards, 1990; Solow, 195) and empirical findings (Boateng 2015;

Chakrabarti, 2001; Edwards, 1990), trade openness was expected to attract higher

level of FDI activity (Uwubanmwen&Ajao, 2012; Kyrkilis&Pantelidis, 2003).

Thus, the study hypothesis that:

H : Trade openness is positively related to FDI inflows in Nigeria.

The market size hypothesis contends that a large market is necessary for efficient

utilisation of resources and exploitation of economies of scale (Chakrabarti, 2001).

It is argued that increasing market size will attract inward FDI (Sahoo, 2006;

Chakrabarti, 2001; Wang & Swain, 1995). The above argument is supported by

Dunning's (1993) eclectic paradigm which asserted that access to large market size

in the host country is one of the primary motives for internalisation. The above

assertions are empirical supported that market size havepositive and statistically

significant influence on inward FDI (Jadhav, 2012; Buckley, Forsans&Munjal

2012; Grosse & Trevino, 2005; Dunning, 1980).

Market size have been shown to be the most robust and positively traditional

determinant of FDI (Chakrabarti, 2001; Fedderke&Romm, 2006;

, 2012). Boateng (2015) and Boateng (2011)

remarked that the larger the market size of a host country, in terms of the country's

GDP, the higher the FDI inflows into the host country. Notwithstanding, market size

had also been reported to have insignificant influence on inward FDI

(Villaverde&Maza, 2015; Uwubanmwen&Ajao, 2012;

, 2010;Asiedu, 2002; Edwards, 1990).

Generalised Method of Moment

et al.,

,

et al., et al.,

3

Market size

Buchanan,

Quan&Meenakshi

Ramakrishnan,

Kushwah&Kateja

68

Impacts of Macroeconomic Indicators on Inward FDI in Nigeria: 1981 2016–

In spite large market size (proxy with GDP per capita) in Nigeria, poor infrastructure

and weak institutions may likely limit the potential from market size in Nigeria as they may increase transaction costs of doing business (see:Modrego, Mccann,

Foster &Olfert 2014; Ma, 2013). The market size role in triggering cross-border

acquisitions may be limited even with free trade (Fikru&Lahiri, 2014). Nego (2010,

p. 1401) captured this fact by saying that 'the efficacy of market is significantly

affected by the institutional environment in which economic operate.' WEF (2014) noted that many non-tariff barriers are hindering trade development and the

advantages of market size in Nigeria. We expect poor infrastructure (see:Modrego

2014; Ma, 2013) and weak institutional environment (Fikru&Lahiri, 2014;

Nego, 2010) to limit market size in Nigeria, due to their effects on total transaction

costs on FDI. Hence, the study hypothesis that:H : There is a negative association between market size and FDI inflows in Nigeria

Secondary time series data are gathered from several sources are used for the

analysis of this study. These sources of secondary data have been severally used by researchers in FDI. The sources of the data and the adopted measurement of the

variables used in this study are as listed in table 1.

,

et

al.,

4

Sources of Data and measurement

69

Impacts of Macroeconomic Indicators on Inward FDI in Nigeria: 1981 2016–

Analytical Method

Model Specification

Results Presentation

Summary statistics of the time series data

Using ordinary least squares (OLS) regression on time series variables may produce spurious regression, with very high R even though there is no meaningful

relationship among the variables (Gujarati and Porter, 2010). Thus, the study will

empirical analysis the data for the study's objective in a co-integration model after

testing for the data's stationarity.Fully modified ordinary least-squared regression

(FMOLS) models will be employed for the study's analysis (Wang and Wu, 2012).The FMOLS analytical approaches includes firstly, investigating the unit root of

variables, by assuming the null hypothesis of the series has a unit root (non-

stationary) which is tested against the alternative of no unit root (stationary). The

FMOLS was first used in a study by Phillips & Hansen (1990) to provide optimal estimates of co-integrating regressions (see: Saboori, Maimunah&Maizan 2014).

FMOLS model modifies least squares (standard OLS) to account for serial

correlation effects and eradicates the endogeneity problems in the regressors that

results from the existence of a co-integration regression relationship (Saboori .,

2014). FMOLS produces estimates of a unit root in time series regression that are hyper-consistent in the sense that their rate of convergence exceeds that of the OLS

estimator (Phillip, 1995). Thus, FMOLS approach eliminates the problems caused

by the long-run correlation between the co-integrating equation and stochastic

regressors changes (Saboori ., 2014; Phillips, 1995).

The construct estimates from FMOLS have no nuisance parameters in their asymptotic distribution and it allows practitioners to use standard normal

asymptotic inference when investigating the properties of co-integrating space

(Gregoir, 2010). Because FMOLS is asymptotically unbiased, it is then possible to

construct Wald test statistics that are asymptotically distributed as Chi-square

statistical inference (Saboori ., 2014; Gregoir, 2010). It has also been credited to deliver the best results in terms of bias, efficiency and Type I errors of asymptotic

tests (Di Iorio&Fachin, 2012). Thus, only variables stationary at first level will be

employed for the analysis and the model will be run after first using information

criteria to select the maximum lag that will be included in the regression.

Following Wang and Wu(2012), this study's specific model is as follows:

FDI TGE ExcR Trop MktSize + e

Where: FDI is foreign direct investment, TGE is total government expenditure,

Trop is trade openness, MktSize is market size proxy with gross domestic product at current basic price, is constant term, to are the coefficient of the regressors,

eis the stochastic term and t is time. The variables value is annually.

Table 2 shows the summary of the time series data for the study: it shows the mean, range, standard deviation, minimum and maximum statistics.The dependent

variable, Foreigndirect investment (FDI) is in millions of Naira and this study use

the log of value of FDI. The maximum val ue of FDI is about 15.2 while the

minimum is about 5.6. FDI has a standard deviation of about 3 and mean of about 11

for FDI inflow into Nigeria, over the period 1981 – 2016. Total government

2

,

et al

et al

et al

t 1 t 2 t 3 t 4 t t

1 4

= β + β + β + β + β

β β β

˳

˳

70

Impacts of Macroeconomic Indicators on Inward FDI in Nigeria: 1981 2016–

expenditure is in millions of Naira. It has a maximum value of N5,185,319 million

and minimum of N9,636.5 million, given rise to a great disparity in range of N5,175,682 million and a standard deviation of N1,857,414 million. The real

effective exchange rate has 2010 as base year.Its minimum is about 50 % and

maximum is about 546 %. It has a mean value of about 153 % and a standard

deviation from mean of about 125 %. Lastly is market size proxy with real GDP in

millions of Naira. The study uses the log of the value of real GDP. The minimum value in log is about 16, maximum about 18, mean about 17 while the standard

deviation is about 0.54.

Table 3 show the results of the augmented Dickey-Fuller unit root test for

stationarity. The result shows that the variables are non-stationary at level but were

stationary at first difference. The result suggests that the variables may be co-integrated at order 1, i.e. I (1). (Gujarati and Porter, 2010).

Unit Root Test

71

Impacts of Macroeconomic Indicators on Inward FDI in Nigeria: 1981 2016–

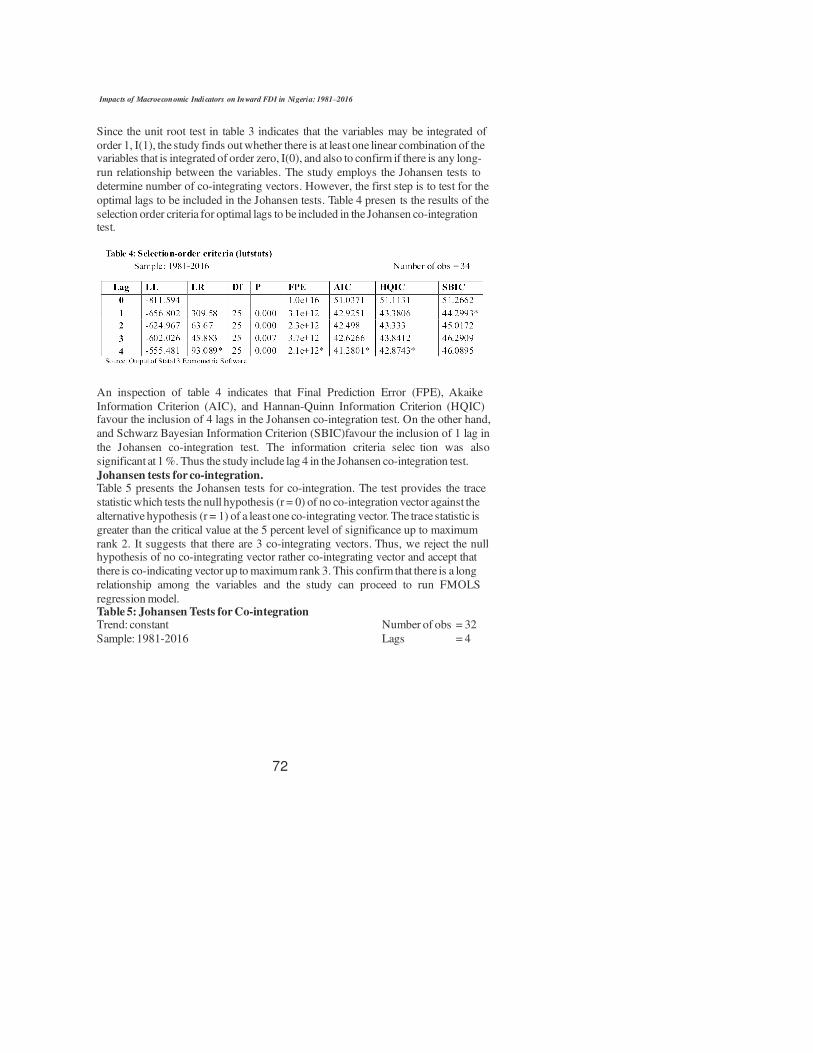

Since the unit root test in table 3 indicates that the variables may be integrated of

order 1, I(1), the study finds out whether there is at least one linear combination of the variables that is integrated of order zero, I(0), and also to confirm if there is any long-

run relationship between the variables. The study employs the Johansen tests to

determine number of co-integrating vectors. However, the first step is to test for the

optimal lags to be included in the Johansen tests. Table 4 presen ts the results of the

selection order criteria for optimal lags to be included in the Johansen co-integration test.

An inspection of table 4 indicates that Final Prediction Error (FPE), Akaike

Information Criterion (AIC), and Hannan-Quinn Information Criterion (HQIC) favour the inclusion of 4 lags in the Johansen co-integration test. On the other hand,

and Schwarz Bayesian Information Criterion (SBIC)favour the inclusion of 1 lag in

the Johansen co-integration test. The information criteria selec tion was also

significant at 1 %. Thus the study include lag 4 in the Johansen co-integration test.

Table 5 presents the Johansen tests for co-integration. The test provides the trace

statistic which tests the null hypothesis (r = 0) of no co-integration vector against the

alternative hypothesis (r = 1) of a least one co-integrating vector. The trace statistic is

greater than the critical value at the 5 percent level of significance up to maximum

rank 2. It suggests that there are 3 co-integrating vectors. Thus, we reject the null hypothesis of no co-integrating vector rather co-integrating vector and accept that

there is co-indicating vector up to maximum rank 3. This confirm that there is a long

relationship among the variables and the study can proceed to run FMOLS

regression model.

Trend: constant Number of obs = 32

Sample: 1981-2016 Lags = 4

Johansen tests for co-integration.

Table 5: Johansen Tests for Co-integration

72

Impacts of Macroeconomic Indicators on Inward FDI in Nigeria: 1981 2016–

An inspection of theFMOLS regression model(table 6) shows that the model fits the

data. The model has an adjusted R of about 77 percent. The results show that the regressors(total government expenditure, real effective exchange rate, trade

openness and market size proxy with real GDP) explain about 77 percent of the

variation in the regressand (changes in FDI).

The results indicate that total government expenditure has a positive and statistically

significant (p = 0.019) influence on FDI inflow in Nigeria on the examined period. The result supports the study's hypothesis that says 'total government expenditure impact positively on FDI inflow into Nigeria', and it is sufficient to explain

movement of FDI inflows into Nigeria over the period 1981 to 2016.The result

supports the Keynesian macroeconomic prediction that public expenditure will spur further economic activities and this include the activities of foreign investors' that

will bring their private capital activities. The result su pports Emudainohwo (2015)

and Oladipo (2013) that show government expenditure have positive and strong influence on movement of FDI inflows in Nigeria. This study also confirmed that

government expenditure has the strongest impact on attracting inward FDI into Nigeria over the period examined. The study suggests that increased government

expenditure particularly when channelled to facilities that will reduce cost to foreign

investors, will attract foreign direct investment in Nigeria.

2

73

Impacts of Macroeconomic Indicators on Inward FDI in Nigeria: 1981 2016–

Table 6 shows that exchange rate has negative and insignificant impact on inward

FDI in Nigeria over the period examined. However, it is not sufficient to explain inward FDI in Nigeria over the period 1981-2016. Table 6 shows that trade openness

has positive and statistically significant influence on FDI inflows in Nigeria over the

examined period. The result supports the study's hypothesis that 'trade openness has

positive bearing on inward FDI in Nigeria' and also collaborate Edwards (1990),

Chakrabarti (2001), Boateng et al. (2015) and Emudainohwo (2015) that found positive and significant influence of trade openness on inward FDI. It however,

negated Wheeler &Mody (1992), Pradhan and Kelker (2014) that reported negative

and insignificant bearing of trade openness on inward FDI and Umer&Alam (2014)

that showed trade openness has negative and significant influence on inward FDI.

Perhaps, on the general side, trade openness that have been implemented in Nigeria can be said to have att racted inward FDI I Nigeria over the examined period.

Notwithstanding, some of the macro-economic variables are either weak or not

stable such as interest rate, exchange rate and institutions (bribery and bureaucracy).

The study thus, suggests that efforts should be made to improve on the weak and unstable macro-economic factors and the weak institutions.

Lastly, table 6 shows that market size proxy with GDP has positive and insignificant

influence on inward FDIs in Nigeria. The result did not su pport the study's

hypothesis that expects 'negative association between market size and FDI inflows in

Nigeria over the examined period. Thus, the result is not sufficient to explain inward FDI in Nigeria over the period 1981-2016

The study used times series data to examine the macro-economic determinants of

inward FDI in Nigeria over the period 1981 to 2016. The study confirmed the

existence of co-movement among the dependent and independent variables using Johansen co-integration test. The FMOLS regression model showed that total

government expenditure, real effective exchange rate and market size proxy with

real GDP has positive and strong impact on inward FDI in Nigeria.And, real effective

exchange rate has negative and insignificant impact on inward FDIs in Nigeria over

the examined period. Total government expenditure and trade openness have a statistically significant effect on inward FDI. The study suggests that government

should undertake macro-economic policies that will impro ve the weak and unstable

macroeconomic variables and strengthen the existing weak institutions. In addition,

government expenditure should be dedicated to building infrastructure that will help

reduce transaction cost to investors in Nigeria. Thus, the study has contributed to literature on the drivers of inward FDI in an economy.

Summary and Conclusion

74

Impacts of Macroeconomic Indicators on Inward FDI in Nigeria: 1981 2016–

References

1

7

Asiedu E. 2002. On the Determinants of Foreign Direct Investment to Developing Countries: Is Africa Different?

107 119.

22

47Buchanan B.G., Quan V.L. &Meenakshi R. 2012. Foreign direct investment and

institutional quality: Some empirical evidence. , 21: 81 89.

21

54

67

6

Pre 1986

Abata M.A., Kehinde J.S. &Bolarinwa S.A. 2012. Fiscal/Monetary policy and economic growth in Nigeria: A theoretical exploration.

(5): 75–88.

Adefeso H.A. &Mobolaji H.I. 2010. The fiscal-monetary policy and economic

growth in Nigeria: Further empirical evidence.

(2): 137–142.Aliber R. 1970. A Theory of direct foreign investment [in C. P. Kindleberger (Ed),

The international corporation] AssymposiumCombrite MA. MIT. Press.

Alimi R. S. 2014. A time series and panel analysis of government spending an d

national income. .

–Blonigen B.A. &Feenstra F.C. 1996. Effect of US trade protection and promotion

policies. (Cambridge, M. A.) Working

Paper No 5285.Boateng A. Naraidoo R. & Uddin M. 2011. An analysis of the inward cross-border

mergers and acquisitions in the UK: A macroeconomic perspective. (2): 91–113.

Boateng A., Hua X., Nisar S. &Wud J. 2015. Examining the determinants of inward

FDI: Evidence from Norway. , : 118–127.

–

Buckley P.J., Forsans N. &Munjal S. 2012. Host-home country linkages an d host-home country specific advantages as determinants of foreign acquisitions by Indian firms. , : 878–890.

Chakrabarti A. 2001. The determinants of foreign direct investment: Sensitivity

analyses of cross-country regressions. (1): 89–114.

Cushman D.O. 1985. Real exchange rate risk, expectations, and the level of direct

investment. , (2): 297–308.

Di Iorio F. &Fachin S. 2012. A note on the estimation of long-run relationships in panel equations with cross-section linkages. (2012-19 | June 6, 2012): 1–16.

Dunning H.J. 1980. Toward an eclectic theory of international production: Some

empirical tests. (

): 9–31.

Dunning H.J. 1993. The globalisation of business. The challenge of the 1990s. Routledge, London, UK; ,

Chatham, Kent, UK.

Edwards S. 1990. Capital flows, foreign direct investment, and debt equity swaps in

developing countries. (Cambridge,

M. A.) Working Paper No. 3497.Ehimare O.

International Journal

of Academic Research in economics and Management Sciences,

Pakistan Journal of social

Sciences,

Munich Personal RePEc Archive

National Bureau of Economic Research

Journal of International Financial Management and Accounting,

Economic Modelling

International Business Review

KYKLOS,

The Review of Economics and Statistics

Journal of International Business Studies, Spring

1980

Reprinted 1995 Mackays of Chatham PLC

National Bureau of Economic Research,

World Development,30 (1):

International Review of Financial Analysis

Central Bank of Nigeria. 2006. CBN Statistical Bulletin, 17: December, 2006.

A. 2011. Foreign direct investment and its effect on the Nigerian economy.

(2): 253–261.Business Intelligence Journal, 4

75

Impacts of Macroeconomic Indicators on Inward FDI in Nigeria: 1981 2016–

Ehinomen C. &Da'silva D. 2014. Impact of Trade Openness on the Output

Growth in the Nigerian Economy.

106

Gregoir S. 2010. Fully modified estimation of seasonally co-integrated processes. , 26: 1491 1528.

Gujarati D.N. & Porter D.C. 2010. Essentials of econometrics, 4 Ed. McGraw-Hill International Edition, Singapore.

Jadhav P. 2012. Determinants of foreign direct investment in BRICS

economies: Analysis of economic, institutional and political factor. 37: 5 14.

Kyrkilis D. &Pantelidis P. 2003. Macroeco nomic determinants of outward

foreign direct investment. 30 (7/8): 827 836.

Levine R. &Renelt D. 1992. A sensitivity analysis of cross-country growth

regressions. , 82: 942 963.

9

British Journal of Economics, Management and Trade, 4 (5): 755 768.

Impact of government policy, institutions and macroeconomic factors on FDI in Nigeria. PhD Thesis, Department of Accountancy, Glasgow School for Business and Society Glasgow Caledonian University, Glasgow, UK.

23

34

Econometric TheoryGrosse R. & Trevino L.J. 2005. New institutional economics and FDI location in

Central and Eastern Europe. Management International Review, 45 (2): 123 145.

Procedia-Social and Behavioral Sciences,

Jin W. &Zang Q. 2013. Impact of change in exchange rate on foreign direct

Investment: Evidence from China. Lingnan Journal of Banking, Finance and Economics, 4 (1): 1 17.

Klasra M.A. 2011. Foreign direct investment, trade openness and economic growth in Pakistan and Turkey: an investigation using bounds test. Quality Quantity, 45 (1): 223-231.

International Journal of Social Economics,

American Economics ReviewMarket size, local sourcing and policy competition for foreign direct

investment. Review of International Economics,21 (5): 984 995.

–

Emudainohwo O.B. 2015.

–

–

Froot K.A. & Stein J.C. 1991. Exchange rates and foreign direct investment: An

imperfect capital markets approach. (4):

1191–1217.

–

–

–

–

–

–

–Modrego F., Mccann P, Foster W.E. &Olfert M.R. 2014. Regional market potential

and the number and size of firms: observations and evidence from Chile. , (3): 327–348.

Muhammad A., Khan H., Hunjra A.I, Ahmad H.M. &Chani M.I. 2011. Institutions,

macroeconomic policy and foreign direct investment: South Asian countries case. Munich Personal RePEc Archive.

Fedderke J.W. &Romm A.T. 2006. Growth impact and determinants of foreign direct investment into South Africa, 1956–2003. Economic Modelling, (2): 738 760

Fikru M.G. &Lahiri S. 2014.Cross-border mergers with flexible policy regime: The role of efficiency and market size. Journal of the Japanese and International Economies, : 58 70.

Quarterly Journal of Economics,

Ma J. 2013.

Spatial Economic Analysis

th

76

Impacts of Macroeconomic Indicators on Inward FDI in Nigeria: 1981 2016–

Muhammad B., Muhammad I., Amjad A., Muhammad S., Mansoor A., Iltaf H.

&Tehreem F. 2014. Impact of exchange rate on foreign direct investment in Pakistan. , 2 (6): 223 231.

2

Phillips P.C.B. & Hansen B.E. 1990. Statistical inference in instrumental variables regression with I(1) processes. 57: 99 125.

Phillips P.C.B. 1995. Fully modified least squares and vector autoregression. 63 (5): 1023 1078

Pradhan A.K. &Kelkar S. 2014. Macroeconomic determinants of foreign direct

investment in India: An empirical investigation (1991 2012). 5 (4): 530 544.

Pradhan R.P. 2010. Trade openness and foreign direct investment in India: The globalisation experience. 16 (3):

26 43.Ramakrishnan S., Kushwah S.V. &Kateja A. 2010. Determinants of foreign

direct investment: an empirical analysis. ,

3 (1 & 2): 12 16.Romer P.M. 1990. Endogenous technological change.

s71 s103.

66

Sahoo P. 2006. Foreign direct investment in South Asia: Policy, trends, impact and determinants. .

l

Solow R.M. 1957. Technical change and aggregate pro duction function. , 39: 12 20.

Advances in Economics and Business

77

Oni L.B., Aninkan O.O. &Akinsanya T.A. 2014. Joint effects of capital and

recurrent expenditures in Nigeria's economic growth. European Journal of Globalization and Development Research,9 (1): 529–543.

Review of Economics Studies,

Econometrica,

Journal of Commerce and Management Thought,

The IUP Journal of Applied Finance,

ASBM Journal of Managements

Journal of Political Economy, 98 (5/2):

ADB Institute Discussion Paper No. 56

Review of Economics and Statistics

–

–

Oladipo S.O. 2013. Macroeconomic determinant of foreign direct investment in

Nigeria (1985-2010): a GMM approach.

(4): 801–817.

–

–

––

–

–

–Saboori B., Maimunah S.I. Maizan B.B. 2014. Economic growth, energy

consumption and CO2 emissions in OECD (Organization for Economic Co-operation and Development)'s transport sector: A fully modified bi-directional relationship approach. , : 150–161.

Seo J., Tarumun S. & Suh C. 2002. Do exchange rates have any impact on FDI flows in the Asia: Experiences of Kore a. Paper presented at Korea and the world

economy. First Annual Conference of the AKES, a Joint Conference of AKES,

KDI and RCIE, Yonsei University, Seoul, Korea.

Sharifi-Renani H. &Mirfatah M. 2012. The impact of exchange rate volatility on

foreign direct investment in Iran. , (1): 365–373.

–

Nego B. 2010. No shortcut to stability: Democratic accountability and sustainable development in Ethiopia. Social Research, (4): 1401 1446.

Journal of Emerging issues in Economics, Finance and Banking: An Online International Monthly Journal,

Organisation for Economic Corporation and Development (OECD). 2002. Foreign

direct investment for development: maximising benefits, minimising costs.

Energy

Procedia Economics and Finance

77

Impacts of Macroeconomic Indicators on Inward FDI in Nigeria: 1981 2016–

Ullah S., Haider S.Z. & Azim P. 2012.

–

–

2009. World

investment report 2009: Transnational corporations, agricultural production and development.

–

–

–

–

–

World Economic Forum. 2014. Global Competitiveness Index Data Platform

Impact of exchange rate volatility on

foreign direct investment: A case study of Pakistan. 50 (2): 121 138.

Umer F. &Alam S. 2013. Effect of openness to trade and FDI on industrial sector growth: A case study for Pakistan. , 16 (48): 179 198.

Uwubanmwen A.E. &Ajao G.I. 2012. The determinants and impacts of foreign direct investment in Nigeria.

, 7 (24): 67 77.

Walsh J.P. & Yu J. 2010. Determinants of foreign direct investment: A sectoral

and institutional approach. : WP/10/187.Wang Q. & Wu N. 2012. Long-run covariance and its applications in co-

integration regression. , 12 (3): 515 542.Wang Z. & Swain N. 1995. The determinants of foreign direct investment in

transforming economies: Empirical evidence from Hungary and China.

, 129: 359 381.Wheeler D. &Mody A. 1992. International investment location decisions.

, 33: 57 76.

Pakistan Economic and Social Review,

The Romanian Economic Journal

United Nations Conference On Trade and Development (UNCTAD). 2009.

Assessing the impact of the current financial and economic crisis on global FDI flows.

United Nations Conference On Trade and Development (UNCTAD).

International Journal of Business and

ManagementVillaverde J. &Maza A. 2015. The determinants of inward foreign direct

investment: Evidence from the European regions. International Business

Review, 24: 209 223.

IMF Working Paper

The Stata Journal

Weltwirtschaftiches

Journal of International Economics

78

Impacts of Macroeconomic Indicators on Inward FDI in Nigeria: 1981 2016–