impact of the recession theories analysis

TRANSCRIPT

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 1/25

Impact of the Recession on Eating OutHabits - UK - October 2010previous section next section

* Operating Costs

Operating Costs

bookmark | export

Key points The recession has prompted operators to streamline their operations as margins

have been increasingly squeezed. However, issues such as rising staff costs havealways been a constant factor for operators to balance.

Menu engineering has become increasingly important during the recession both inorder to protect operators’ bottom lines and to ensure that consumers ar epresented with a tiered pricing structure offering value for money dish options aswell as more expensive items to provide the opportunity to upsell to those lessaffected by the economic downturn.

However, some cost rises are inevitable and difficult to counteract, for example, inOctober 2010 the National Minimum Wage was increased and a VAT rise is plannedfor January 2011.

bookmark | export

Food inflation Food inflation has been and will continue to be an ongoing issue in the eating out market:

in broad terms, in 2008 it rocketed, falling in 2009/10 and beginning to increase again inthe second quarter of 2010. For example, the Office for National Statistics reported thatfood prices jumped 0.7% between June and July 2010, representing the biggest monthlyrise for two years and according to the British Retail Consortium (BRC), food inflation hit a15-month high of 4% for September 2010, with sharp price rises in wheat, oil and corncontributing to the increase.

In an article for Caterer & Hotelkeeper in September 2010, Raymond Blanc stated thatfood costs at Le Manoir aux Quat‟Saisons had increased significantly since 2009: theprice of blueberries increased by 16% since 2009, butter 4.5%, flour nearly 12%, Jabugoham 15%, Manuka honey 11.5% and milk by more than 8%. Blanc stated that his aim in

2009 had been to increase his restaurant‟s use of organic produce from 31.4% to 80% by2014 but that food cost increases had meant that he had been „wrong- footed’ and thatfigures of 50% were more realistic.

Protecting the brand when trying to balance rising costs can be undertaken in a number ofways, eg trading down and maintaining lower price points by using more affordableproducts and ingredients, such as lesser-known cuts of meat, or increasing the prices andthus passing some of the cost increases from food inflation etc onto consumers. The latteris often inevitable, particularly with high-end restaurants that don‟t want to damage their overall business model. These price rises are already evident, for example, in July 2009Heston Blumenthal‟s Fat Duck restaurant increased the price of its tasting menu from£130 to £140 and by October 2010 this has reached a price of £160.

bookmark | export

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 2/25

Menu engineering Whilst some costs inevitably have to be absorbed or passed onto consumers, operators

who are on the ball in terms of menu engineering have been implementing variousstrategies to limit the effect of food inflation on their bottom lines, eg substituting potatoesfor rice and vice versa depending on price levels.

Kasavana and Smith‟s concept of dish ratings was established decades ago, but hasexperienced a resurgence in popularity recently, as the significance of detailed menuengineering was brought to the fore once again: Star (popular and high margins), PlowHorse (popular and low margins), Puzzle (low popularity and high margins) and Dogs (lowpopularity and low margins).

Examples of menu engineering techniques that have been employed include:

Taking more expensive choices off of the menu. For example, in Summer2009 Antony Worrall Thompson reopened his Oxfordshire pub, The Greyhound, whichwas originally closed at the start of 2009 as the recession hit. The modernized venue was

reported to be offering a more flexible menu after redevelopment, for example, more „pubfavourites‟ such as ham, egg and chips for £9.50.

Substituting ingredients, such as using cheaper cuts of meat or breeds of fish.

Using central ingredients a number of times across a menu (eg using a whole chickenor half a pig carcass). This helps with wastage as well as reducing the ingredients costs,however it does require a higher skill set and knowledge base and often greatercollaboration with providers such as butchers. An example of this in practice wasdiscussed in an article in The Publican in December 2009 which outlined how GeronimoInns was beginning to source whole Dexter cow carcasses, with special menus designedwhich used all the different cuts of the animal. As well as a costs saving exercise, this

strategy was also used in an attempt to promote quality and provenance at the chain.

Negotiating with suppliers and purchasing surplus seasonal produce.

Reigning in the portion size of the plate‟s main ingredient and tighter portion controlgenerally to avoid increasing the price of the dish. In practical terms operators rarely drawattention to this and instead reprint similar menus, this time omitting the weight of theproduct – which is particularly relevant to steaks.

Alternatively, other operators have expanded the range of choices in this area to keepprice pointing flexible therefore accommodating those harder hit by the recession whilstalso allowing for upselling to those that haven‟t been. For example, The Cowper Arms in

Cole Green, Hertfordshire, offers consumers the more expensive choice of fillet steak withchicken pate on toasted brioche with Madeira sauce (£16.95) on its „seasonal dishes‟menu, or rib eye steak with baked tomato, peppercorn sauce and home-cut chunky chips(£14.50) on its „pub classics‟ menu.

In an article for Caterer & Hotelkeeper in September 2010, Raymond Blanc also notedthat his restaurant Le Manoir aux Quat‟Saisons was looking to balance its food costs byincreasing the size of its vegetable garden from 1.5 acres to three acres. He also statedthat the restaurant would be relying less on animal protein and instead would be creatingimaginative vegetarian dishes using interesting herbs, fungi and other vegetables.

Key analysis: The key motivator here is looking at cost-saving measures to ensure

that price rises aren’t passed on to the already price-sensitive diners in order to stabilise footfall both during and following the recession. However, these best

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 3/25

business practices can also help operators generally going forward to ensure their procurement processes are streamlined and margins maximized. Also, whilst many of these initiatives have helped appeal to recession-hit diners by offering cheaper dishes, menus should still offer a range of price points: diners can’t spend more unless restaurants give them the option to do so.

Centralised kitchens are frequently used within the eating out industry as a way ofensuring consistency of food production amongst other benefits such as relieving thepressure on restaurants themselves which may have limited kitchen space.However, Gordon Ramsay was widely criticised in the national press in 2009 for using acentralised kitchen to prepare food for a number of the pub restaurants in his portfolio,with many press articles referring to the dishes served there as „ready meals‟. In summer 2010, Gordon Ramsay Holdings announced its intention to close its central productionkitchen in favour of keeping the cooking all in-house.

Key analysis: Centralised kitchens are frequently used within the eating out industry,the difference here being that consumers expected more from venues carrying the upmarket ‘Ramsay’ branding.

bookmark | export

Menu flavour trend issues

Although classic British dishes never really fall out of fashion, they did experience aresurgence during the recession in particular for a number of reasons. For example,substituting steak dishes for steak pies enabled consumers to purchase a cheaper versionof a much-loved dish.

Trust was another motivator behind classic British dishes/comfort food resurgence:consumers became more cautious and less adventurous with their menu choices duringthe recession as they were increasingly looking for „guaranteed‟ good choices. This wasalso reflected in the food retail market: rather than automatically switching to the cheapestsupermarket products, consumers tended to stick to brands they already knew and trustedto ensure that they were getting good value for money.

Carveries also seem to be gaining pace in recent years: this option adds a sense oftheatre to venues as well as providing consumers with a seemingly clear-cut value formoney option.

Subsequently, however, it has become increasingly difficult for operators to make theirmenus stand out as many are employing the same strategy or chasing the same marketwith these classic British dishes. As a result, some chefs have experimented with the ideaof „classics with a twist‟. This has generally received mixed reviews, with some consumers

appreciating the points of difference and others seeing the new twists as somewhatsuperfluous.

Where twists on classics really seem to be gaining ground are cocktail and dessertmenus. For example, the ice cream manufacturer Mövenpick produces a variety ofunusual flavours (eg balsamic vinegar or double cream and meringue ice cream) andreported that it had seen a 43% rise in year-on-year menu sales between January andMay 2010. (For more information on this subject regarding cocktail menus please seeMintel‟s Wine, Cocktail and Champagne Bars – UK, July 2010 .)

Key analysis: The question now is how to increase menu prices without alienating consumers and weakening footfall once again – taking the emphasis away from price

and instead focusing on menu innovation can provide a potential route for achieving this. See Also

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 4/25

Eating Out Review - UK

bookmark | export

Menu psychology As well as menu engineering in the kitchen, menu psychology front-of-house has been

given increased prominence during the recession. For example, tips such as removing £signs from menus and/or adding „decoys‟ (eg highlighting more profitable dishes in boxes)onto menus has become more significant in recent years.

Key analysis: Small operators and independents such as takeaway outlets also need to pay heed to this trend and introduce some of the ideas to their own menu design in order to gain a competitive edge. For example, using more evocative and emotive descriptions to ‘romance’ the dishes, particularly signature and in-house specials,should help restaurants on a number of levels.

bookmark | export

Non-food cost saving areasThe recession has also prompted firms to streamline operational procedures such asprocurement contracts, utility suppliers etc to protect margins by lowering their bottom lines.

For example, in August 2009 a survey conducted by BDO Stoy Hayward on behalf ofthe British Hospitality Association (BHA) stated that over two thirds of the majorcompanies (24 brands were surveyed) had cut back on staff and frozen the salaries ofthose that remained in 2008 in response to the recession.

In its preliminary results for 2009/10 released in April 2010, Whitbread stated that it hadachieved ongoing savings by strategies such as simplifying systems and outsourcing rolessuch as logistics, payroll and back office accounting.

In its half-year results for the 28 weeks ending 10 April 2010, M&B stated that itsefficiency and productivity improvements had delivered a cost saving of £25 million for theyear, which was £5 million better than expected. The company stated that it had looked atsavings in a number of areas such as menu engineering, stock wastage, energyefficiency, overhead reduction and purchasing.

Sometimes these cost saving measures are tied into environmentally friendly initiativeswhich can also provide a marketing opportunity in terms of being community-minded andsocially responsible.

For example, in July 2010 Costa Coffee reported that it had introduced a new systemwhich enabled the chain to recycle the steam from its dishwashers to preheat fresh water.As well as being eco-friendly, this initiative was said to have resulted in a 30% reduction inenergy usage and reduction of 15,000 litres of water per year. The chain also introducedFutura coffee machines, which are marketed as being 30% more energy efficient.

However, some rising costs are inevitable and difficult to avoid, for example: In October 2010 the National Minimum Wage was increased and a VAT rise is planned

for January 2011.

Price-led Trends

bookmark | export

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 5/25

Key points The eating out market was arguably over-reliant on the discount culture during the

recession. As operators look to regain a grip on margins, the broad approach todiscounting has been replaced with a more restrictive and selective strategy.

Such prolonged and widescale discounting in some sectors of the market doessuggest that operators need to take another look at their value positioning

Market Developments

Ernst & Young Item Club: 'Tough retail conditions will last for a decade'

bookmark | export

DiscountingPrice promotions were increasingly relied upon by some operators to drive footfall during therecession and beyond, particularly for those with heavy debt structures which relied oncontinuing sales figures in order to meet debt repayment requirements.

Heavy discounting has also been more evident in some sectors than others, for example,price-led promotions have been particularly evident in the pizza/pasta restaurant sector.

PizzaExpress vouchers constitute a third of the online restaurant deals market accordingto a survey by restaurant voucher website Crunchlunch, released in June 2010. Zizzi wasthe second largest distributor of vouchers at 15% of the online restaurant deals market,with chains such asGourmet Burger Kitchen, Ask and La Tasca following.

Michelin-starred credit crunch lunches: During the recession many high-endrestaurants introduced lunchtime set menus with prices that rival many mid-market menus(eg £20 a head for two courses) or at least increased accessibility for other consumerswho might otherwise not be able to afford to eat in these type of restaurants. This waslargely in response to the significant downturn in corporate expenditure.

In Greggs‟ interim results for the 26 weeks ended 3 July 2010, the company stated that ithad sold more than 2 million meal deals in the first half of the year, up 167% from theprevious year. The company also said that it had received a „good response ‟ to itsseasonal promotion of two soft drinks for £1.80.

See Also

Business and Industry Catering - UK

Eating Out Review - UK

bookmark | export

Have the operators trained consumers to buy on promotion?

However, the eating out market‟s reliance on the discount culture in recent years hasinevitably changed consumers purchasing behaviour and damaged the value of the marketin the sense that consumers have become used to paying less.

Recently, although the approach to discounting from operators has altered, many venuesare struggling to wean both themselves and their consumers off of price promotions.

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 6/25

Offers have become more targeted and operators are ditching the „scattergun‟ approach asthey recognize that heavy blanket discounting was unnecessarily damaging margins (andbrand reputations) in some instances. This has been done in a number of ways, for example:

Offers that are particularly targeted at driving mid-week trade – however, arepromotions such as theme nights now so common that they lack the point of differentiationthat they were originally designed to provide? Mintel‟s Pub Catering – UK, September 2010 shows that only one in ten admit to being drawn to theme night menus (eg curryclubs).

Pre-booking requirements – the majority of Corney & Barrow‟s offers require consumersto pre-book a table for lunch in order to redeem a voucher for a free drink, for example.

Special offers limited to social media/newsletter members.

Research for this report shows that few diners rank promotional deals as the main reasonwhy theyeat out. However, of the diners who have cut back on eating out in the last 12months, a quarter state that they often use money-off vouchers, which illustrates that

discounting does affect their venue and dish choices. The downside of discounting thereforeis that it has promoted venue promiscuity amongst consumers, as they have been taught tobuy on promotion.See Also

Eating Out Review - UK

bookmark | export

Vouchers

Vouchers tend to be limited to use amongst younger consumers; older consumers aremore likely to attach a certain amount of stigma to using vouchers.

Technological innovations are slowly helping operators negotiate the problem ofconsumers forgetting to bring hardcopy print outs of vouchers out with them, eg mobileapps for Vouchercloud. (See section Brand Communication and Promotion ).

bookmark | export

Value rangesAn alternative price-led strategy used heavily during the recession was the introduction orexpansion of value ranges which created an added dimension to menus. By creating theseadditional menu sections, operators were seen to be responding to changing consumerspending behaviour without damaging the value of their core menu or their brand image.

Between Autumn 2009 and Spring 2010, JD Wetherspoon ran what it described as asuccessful „value meals‟ menu offering consumers a selection of meals at a £2.99 pricepoint. Although the company does still offer a few products around this low price point,they are no longer marketed as a specific and separate menu.

As well as value menus there was also growth in the number of individual „value‟ productsduring the recession eg filter coffees. For example, at the start of 2009 Pret a Mangerlaunched a 99p filter coffee offering.

Key analysis: It is worth noting that the trend towards flat white/filter coffees was also prompted by changing market conditions within the specific coffee shop sector, and was not just influenced by the recession alone. For example,JD Wetherspoon has

been pursuing the all day dining market for many years and has extended its reach in this area in 2010 with the addition of a 79p espresso to its hot drinks range.Furthermore, McDonald’s has seen the number of cups sold climb by 39% over the

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 7/25

last two years since re-launching its coffee range in 2007. McDonald’s is arguably now the biggest seller of coffee on UK high streets.

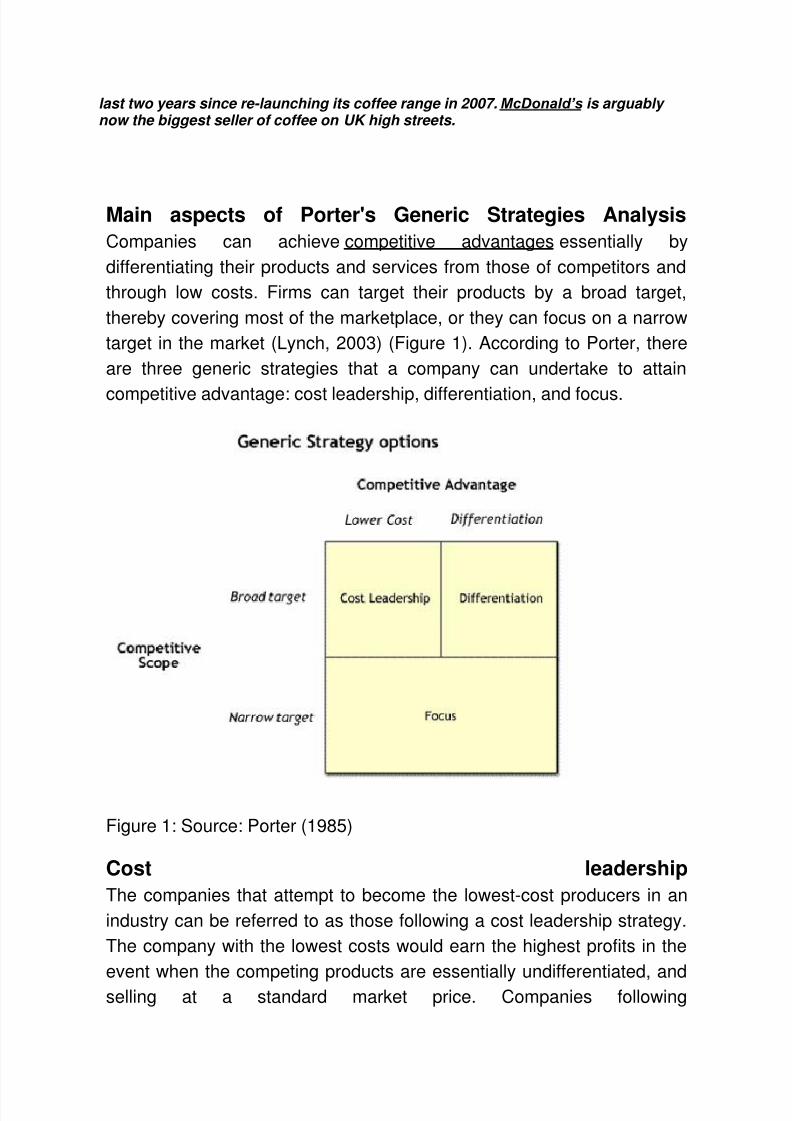

Main aspects of Porter's Generic Strategies Analysis

Companies can achieve competitive advantages essentially by

differentiating their products and services from those of competitors and

through low costs. Firms can target their products by a broad target,

thereby covering most of the marketplace, or they can focus on a narrow

target in the market (Lynch, 2003) (Figure 1). According to Porter, there

are three generic strategies that a company can undertake to attain

competitive advantage: cost leadership, differentiation, and focus.

Figure 1: Source: Porter (1985)

Cost leadership

The companies that attempt to become the lowest-cost producers in an

industry can be referred to as those following a cost leadership strategy.

The company with the lowest costs would earn the highest profits in the

event when the competing products are essentially undifferentiated, and

selling at a standard market price. Companies following

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 8/25

this strategy place emphasis on cost reduction in every activity in the

value chain. It is important to note that a company might be a cost leader

but that does not necessarily imply that the company's products would

have a low price. In certain instances, the company can for instance

charge an average price while following the low cost leadership strategy

and reinvest the extra profits into the business (Lynch, 2003). Examples

of companies following a cost leadership strategy include RyanAir,

and easyJet, in airlines, and ASDA and Tesco, in superstores.

The risk of following the cost leadership strategy is that the company's

focus on reducing costs, even sometimes at the expense of other vital

factors, may become so dominant that the company loses vision of why it

embarked on one such strategy in the first place.

Differentiation

When a company differentiates its products, it is often able to charge a

premium price for its products or services in the market. Some general

examples of differentiation include better service levels to customers,

better product performance etc. in comparison with the existing

competitors. Porter (1980) has argued that for a company employing a

differentiation strategy, there would be extra costs that the company

would have to incur. Such extra costs may include

high advertising spending to promote a differentiated brand image for the

product, which in fact can be considered as a cost and an

investment.McDonalds , for example, is differentiated by its very brand

name and brand images of Big Mac and Ronald McDonald.

Differentiation has many advantages for the firm which makes use of the

strategy. Some problematic areas include the difficulty on part of the firm

to estimate if the extra costs entailed in differentiation can actually be

recovered from the customer through premium pricing. Moreover,

successful differentiation strategy of a firm may attract competitors to

enter the company's market segment and copy the differentiated product

(Lynch, 2003).

Focus

Porter initially presented focus as one of the three generic strategies, but

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 9/25

later identified focus as a moderator of the two strategies. Companies

employ this strategy by focusing on the areas in a market where there is

the least amount of competition (Pearson, 1999). Organisations can

make use of the focus strategy by focusing on a specific niche in the

market and offering specialised products for that niche. This is why the

focus strategy is also sometimes referred to as the niche strategy (Lynch,

2003). Therefore, competitive advantage can be achieved only in the

company's target segments by employing the focus strategy. The

company can make use of the cost leadership or differentiation approach

with regard to the focus strategy. In that, a company using the cost focus

approach would aim for a cost advantage in its target segment only. If a

company is using the differentiation focus approach, it would aim fordifferentiation in its target segment only, and not the overall market.

This strategy provides the company the possibility to charge a premium

price for superior quality (differentiation focus) or by offering a low price

product to a small and specialised group of buyers (cost

focus). Ferrari and Rolls-Royce are classic examples of niche players in

the automobile industry. Both these companies have a niche of premium

products available at a premium price. Moreover, they have a smallpercentage of the worldwide market, which is a trait characteristic of

niche players. The downside of the focus strategy, however, is that the

niche characteristically is small and may not be significant or large

enough to justify a company's attention. The focus on costs can be

difficult in industries where economies of scale play an important role.

There is the evident danger that the niche may disappear over time, as

the business environment and customer preferences change over time

Mc Kinsey 7s Model

The McKinsey 7S model was named after a consulting company, McKinsey and Company, which has

conducted applied research in business and industry (Pascale & Athos, 1981; Peters & Waterman, 1982). All of

the authors worked as consultants at McKinsey and Company; in the 1980s, they used the model to analyse

over 70 large organisations. The McKinsey 7S Framework was created as a recognisable and easily

remembered model in business. The seven variables, which the authors term "levers", all begin with the letter

"S":

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 10/25

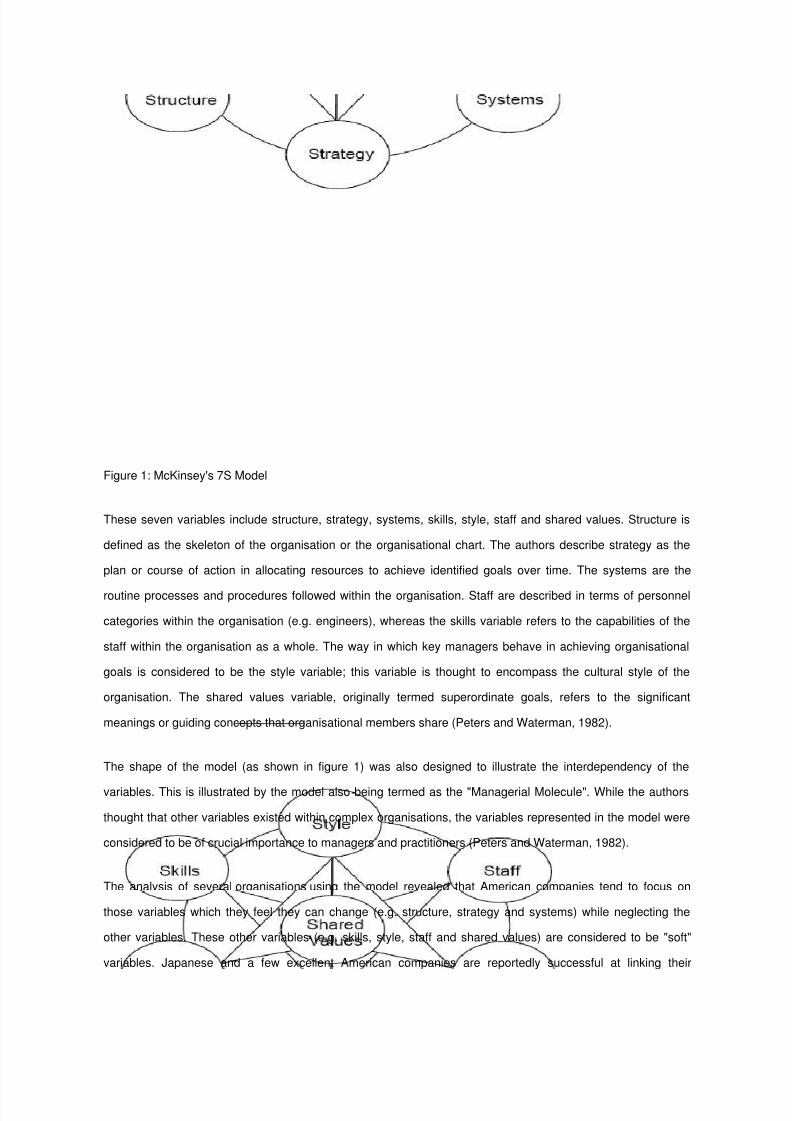

Figure 1: McKinsey's 7S Model

These seven variables include structure, strategy, systems, skills, style, staff and shared values. Structure is

defined as the skeleton of the organisation or the organisational chart. The authors describe strategy as the

plan or course of action in allocating resources to achieve identified goals over time. The systems are the

routine processes and procedures followed within the organisation. Staff are described in terms of personnel

categories within the organisation (e.g. engineers), whereas the skills variable refers to the capabilities of the

staff within the organisation as a whole. The way in which key managers behave in achieving organisational

goals is considered to be the style variable; this variable is thought to encompass the cultural style of the

organisation. The shared values variable, originally termed superordinate goals, refers to the significant

meanings or guiding concepts that organisational members share (Peters and Waterman, 1982).

The shape of the model (as shown in figure 1) was also designed to illustrate the interdependency of the

variables. This is illustrated by the model also being termed as the "Managerial Molecule". While the authors

thought that other variables existed within complex organisations, the variables represented in the model were

considered to be of crucial importance to managers and practitioners (Peters and Waterman, 1982).

The analysis of several organisations using the model revealed that American companies tend to focus on

those variables which they feel they can change (e.g. structure, strategy and systems) while neglecting the

other variables. These other variables (e.g. skills, style, staff and shared values) are considered to be "soft"

variables. Japanese and a few excellent American companies are reportedly successful at linking their

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 11/25

structure, strategy and systems with the soft variables. The authors have concluded that a company cannot

merely change one or two variables to change the whole organisation.

For long-term benefit, they feel that the variables should be changed to become more congruent as a system.

The external environment is not mentioned in the McKinsey 7S Framework, although the authors do

acknowledge that other variables exist and that they depict only the most crucial variables in the model. While

alluded to in their discussion of the model, the notion of performance or effectiveness is not made explicit in the

model.

Description of 7 Ss

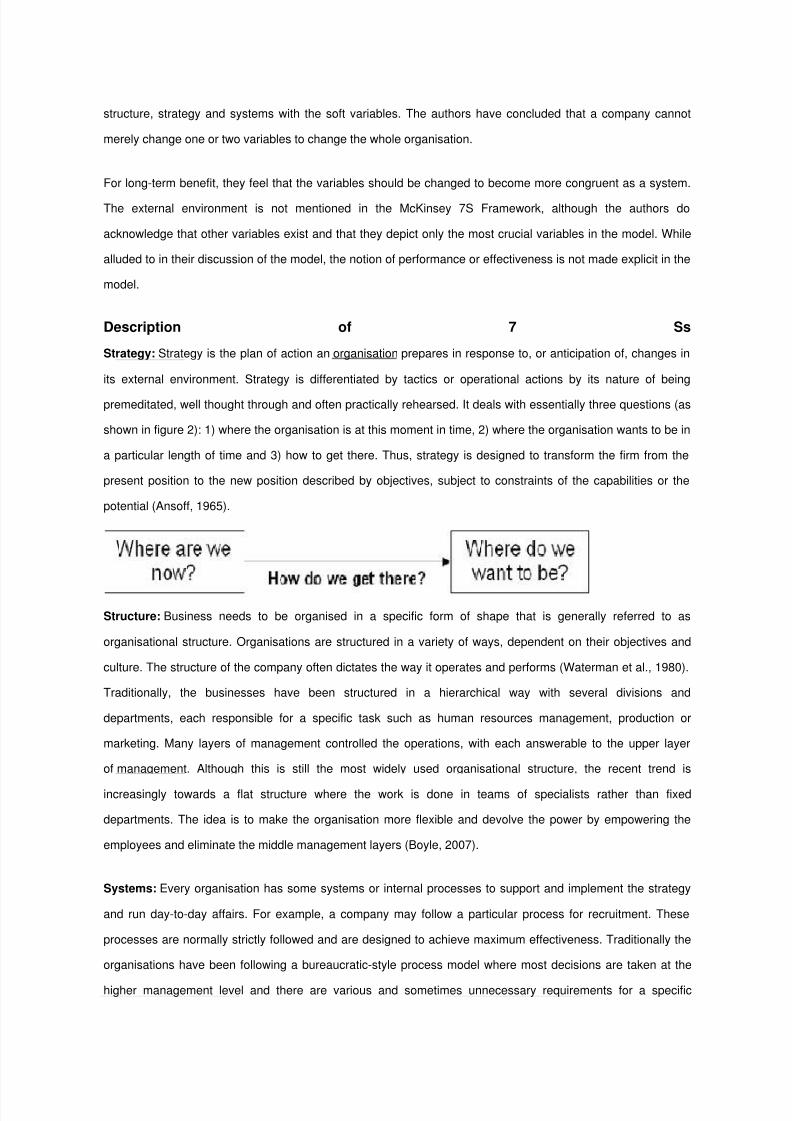

Strategy: Strategy is the plan of action an organisation prepares in response to, or anticipation of, changes in

its external environment. Strategy is differentiated by tactics or operational actions by its nature of being

premeditated, well thought through and often practically rehearsed. It deals with essentially three questions (as

shown in figure 2): 1) where the organisation is at this moment in time, 2) where the organisation wants to be in

a particular length of time and 3) how to get there. Thus, strategy is designed to transform the firm from the

present position to the new position described by objectives, subject to constraints of the capabilities or the

potential (Ansoff, 1965).

Structure: Business needs to be organised in a specific form of shape that is generally referred to as

organisational structure. Organisations are structured in a variety of ways, dependent on their objectives and

culture. The structure of the company often dictates the way it operates and performs (Waterman et al., 1980).

Traditionally, the businesses have been structured in a hierarchical way with several divisions and

departments, each responsible for a specific task such as human resources management, production or

marketing. Many layers of management controlled the operations, with each answerable to the upper layer

of management. Although this is still the most widely used organisational structure, the recent trend is

increasingly towards a flat structure where the work is done in teams of specialists rather than fixed

departments. The idea is to make the organisation more flexible and devolve the power by empowering the

employees and eliminate the middle management layers (Boyle, 2007).

Systems: Every organisation has some systems or internal processes to support and implement the strategy

and run day-to-day affairs. For example, a company may follow a particular process for recruitment. These

processes are normally strictly followed and are designed to achieve maximum effectiveness. Traditionally the

organisations have been following a bureaucratic-style process model where most decisions are taken at the

higher management level and there are various and sometimes unnecessary requirements for a specific

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 12/25

decision (e.g. procurement of daily use goods) to be taken. Increasingly, the organisations are simplifying and

modernising their process by innovation and use of new technology to make the decision-making process

quicker. Special emphasis is on the customers with the intention to make the processes that involve customers

as user friendly as possible (Lynch, 2005).

Style/Culture: All organisations have their own distinct culture and management style. It includes the dominant

values, beliefs and norms which develop over time and become relatively enduring features of the

organisational life. It also entails the way managers interact with the employees and the way they spend their

time. The businesses have traditionally been influenced by the military style of management and culture where

strict adherence to the upper management and procedures was expected from the lower-rank employees.

However, there have been extensive efforts in the past couple of decades to change to culture to a more open,

innovative and friendly environment with fewer hierarchies and smaller chain of command. Culture remains an

important consideration in the implementation of any strategy in the organisation (Martins and Terblanche,

2003).

Staff: Organisations are made up of humans and it's the people who make the real difference to the success of

the organisation in the increasingly knowledge-based society. The importance of human resources has thus got

the central position in the strategy of the organisation, away from the traditional model of capital and land. All

leading organisations such as IBM, Microsoft, Cisco, etc put extraordinary emphasis on hiring the best staff,

providing them with rigorous training and mentoring support, and pushing their staff to limits in achieving

professional excellence, and this forms the basis of these organisations' strategy and competitive

advantage over their competitors. It is also important for the organisation to instil confidence among the

employees about their future in the organisation and future career growth as an incentive for hard work (Purcell

and Boxal, 2003).

Shared Values/Superordinate Goals: All members of the organisation share some common fundamental

ideas or guiding concepts around which the business is built. This may be to make money or to achieve

excellence in a particular field. These values and common goals keep the employees working towards a

common destination as a coherent team and are important to keep the team spirit alive. The organisations with

weak values and common goals often find their employees following their own personal goals that may be

different or even in conflict with those of the organisation or their fellow colleagues (Martins and Terblanche,

2003).

Main aspects of Value Chain Analysis

Value chain analysis is a powerful tool for managers to identify the key

activities within the firm which form the value chain for that organisation,

and have the potential of a sustainable competitive advantage for a

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 13/25

company. Therein, competitive advantage of an organisation lies in its

ability to perform crucial activities along the value chain better than its

competitors.

The value chain framework of Porter (1990) is “an interdependent system

or network of activities, connected by linkages” (p. 41). When the system

is managed carefully, the linkages can be a vital source of competitive

advantage (Pathania-Jain, 2001). The value chain analysis essentially

entails the linkage of two areas. Firstly, the value chain links the value of

the organisations‟ activities with its main functional parts. Then the

assessment of the contribution of each part in the overall added value of

the business is made (Lynch, 2003). In order to conduct the value chain

analysis, the company is split into primary and support activities (Figure

1). Primary activities are those that are related with production, while

support activities are those that provide the background necessary for the

effectiveness and efficiency of the firm, such as human resource

management. The primary and secondary activities of the firm are

discussed in detail below.

Primary activities

The primary activities (Porter, 1985) of the company include the following:

Inbound logistics

These are the activities concerned with receiving the materials

from suppliers, storing these externally sourced materials, and

handling them within the firm.

Operations

These are the activities related to the production of products andservices. This area can be split into more departments in certain

companies. For example, the operations in case of a hotel would

include reception, room service etc.

Outbound logistics

These are all the activities concerned with distributing the final

product and/or service to the customers. For example, in case of a

hotel this activity would entail the ways of bringing customers tothe hotel.

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 14/25

Marketing and sales

This functional area essentially analyses the needs and wants of

customers and is responsible for creating awareness among the

target audience of the company about the firm‟s products andservices. Companies make use of marketing

communications tools like advertising, sales promotions etc. to

attract customers to their products.

Service

There is often a need to provide services like pre-installation or

after-sales service before or after the sale of the product or

service.

Support activities

The support activities of a company include the following:

Procurement

This function is responsible for purchasing the materials that are

necessary for the company‟s operations. An efficient procurement

department should be able to obtain the highest quality goods at

the lowest prices.

Human Resource Management

This is a function concerned with recruiting, training, motivating

and rewarding the workforce of the company. Human resources

are increasingly becoming an important way of attaining

sustainable competitive advantage.

Technology Development

This is an area that is concerned with technological innovation,

training and knowledge that is crucial for most companies today in

order to survive.

Firm Infrastructure

This includes planning and control systems, such as finance,

accounting, and corporate strategy etc. (Lynch, 2003).

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 15/25

Figure 1: The Value Chain: Source: Porter (1985)

Porter used the word „margin‟ for the difference between the total value

and the cost of performing the value activities (Figure 1). Here, value is

referred to as the price that the customer is willing to pay for a certain

offering (Macmillan et al, 2000). Other scholars have used the word

„added value‟ instead of margin in order to describe the same (Lynch,

2003). The analysis entails a thorough examination of how each part

might contribute towards added value in the company and how this may

differ from the competition. In a study of Saudi companies, Ghamdi

(2005) found that 22% of the companies in the study used value chain

frequently, while 17% reported that they somewhat used it, and 42% did

not use the tool at all. An interesting finding of the study was that the

manufacturing firms were frequent users of the tool compared to their

service counterparts (Ghamdi, 2005).

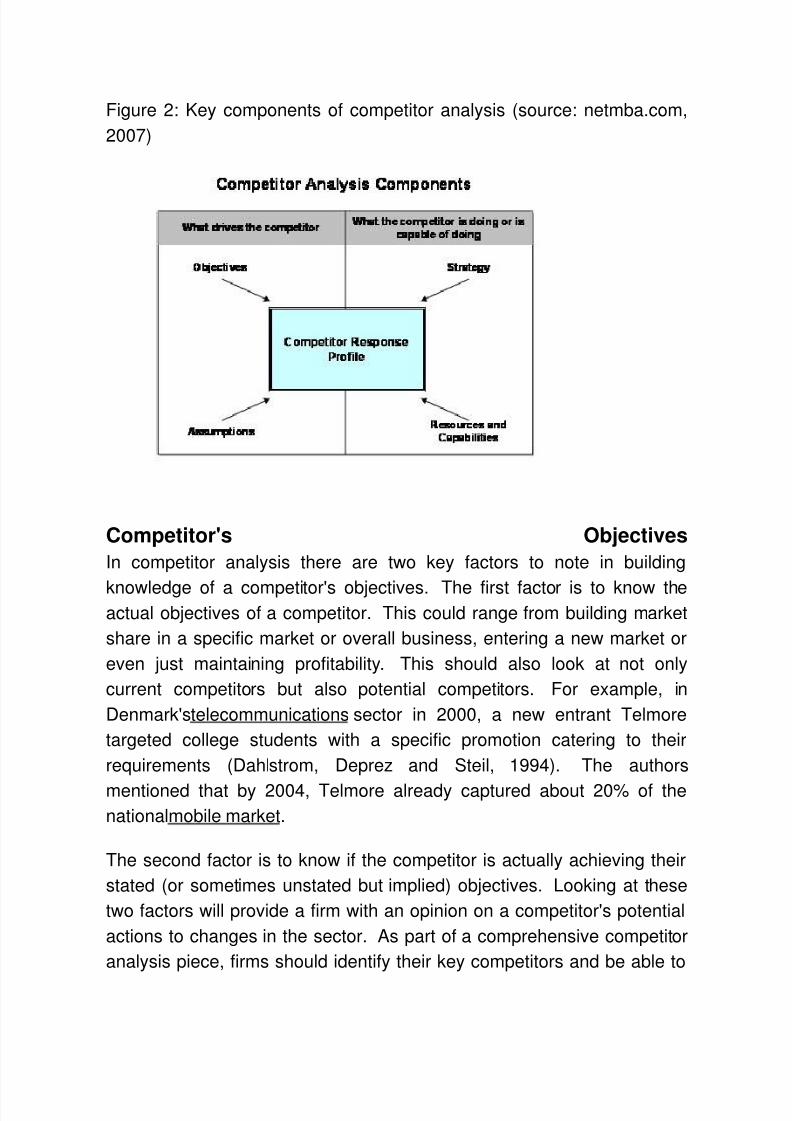

Competitor analysis is a critical part of a firm's activities. It is an

assessment of thestrengths and weaknesses of current and potential

competitors, which may encompass firms not only in their own sectors

but also in other sectors. Directly or indirectly, competitor analysis is a

driver of a firm's strategy and impacts on how firms act or react in their

sectors. Gluck, Kaufman and Walleck (2000) showed that competitor

analysis is one of two components that give a firm a strong marketunderstanding (see figure 1). This drives the formulation of

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 16/25

a strategy and it applies whether a firm formulates a strategythrough

strategic thinking, formal strategic planning, or opportunistic

strategic decision making. Competitor analysis, together with an

understanding of major environmental trends, is a key input in strategy

formulation and should be developed properly.

In utilising competitor analysis as part of strategy formulation, firms are

able to adapt or build their own strategies and be able to compete

effectively, improve performance and gain market share in their

businesses. In a large number of instances, firms are able to tap new

markets or build new niches. For example, after European air travel was

deregulated in the mid-1990s, Ryanair and Easyjet focused on the no-

frills market and provided low-cost travel across Europe after figuring outthrough competitor analysis, where the opportunities were emerging

(Binggeli and Pompeo, 2002). The authors showed that, at the point in

time, Ryanair and Easyjet were performing better than their competitors

with operating margins of 26% and 9.5% respectively, which were

significantly better than the operating margins achieved by the

traditional airlines.

MAIN ASPECTS OF COMPETITOR ANALYSIS The key objectives in competitor analysis are to develop a greater

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 17/25

understanding of what competitors have in place in terms of resources

and capabilities, what they plan to do in their businesses, and how the

competitors may react to various situations in reaction to what the firm

does. Michael Porter has defined a competitor analysis framework that

focused on four key aspects (Porter, 1980 cited in

netmba.com): competitor's objectives, competitor's assumptions,

competitor's strategy, and competitor's resources and capabilities.

These four aspects of competitor analysis are the areas critical for a firm

to understand and they should pursue this knowledge not only for current

competitors but also for other potential competitors in the business.

There are other competitor analysis frameworks that firms can utilise. An

example is an international competitor analysis framework presented byGarsombke (1989) but the foundations follow Porter's framework with

additional components relating to the understanding of the "international"

marketplace. Others focus on specific components and thus become a

subset of the framework. For example, Slater and Narver (1994) looked

at this through the value to customers and identified three components in

the analysis: customer orientation, competitor focus and cross-functional

coordination.

Rather than compare various competitor analysis frameworks, the focusfrom hereon is Porter's framework (see figure 2) for competitor analysis.

This framework is broken into two parts. The competitor's objectives and

assumptions drive the competitor while the competitor's strategy and

resources and capabilities define what the competitor is doing or is

capable of doing. Together, these four aspects define a competitor

response profile which gives the firm an understanding of what actions a

competitor may take. Taking this analysis across a firm's key competitors

will give the firm a viewpoint on where the sector is heading, and provides

the firm with a basis for developing their strategy and actions. The key

aspects of competitor analysis and the resulting competitor response

profile are defined further below.

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 18/25

Figure 2: Key components of competitor analysis (source: netmba.com,

2007)

Competitor's Objectives

In competitor analysis there are two key factors to note in building

knowledge of a competitor's objectives. The first factor is to know theactual objectives of a competitor. This could range from building market

share in a specific market or overall business, entering a new market or

even just maintaining profitability. This should also look at not only

current competitors but also potential competitors. For example, in

Denmark'stelecommunications sector in 2000, a new entrant Telmore

targeted college students with a specific promotion catering to their

requirements (Dahlstrom, Deprez and Steil, 1994). The authors

mentioned that by 2004, Telmore already captured about 20% of the

nationalmobile market.

The second factor is to know if the competitor is actually achieving their

stated (or sometimes unstated but implied) objectives. Looking at these

two factors will provide a firm with an opinion on a competitor's potential

actions to changes in the sector. As part of a comprehensive competitor

analysis piece, firms should identify their key competitors and be able to

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 19/25

define the objectives of each competitor and their likelihood of achieving

their objectives.

An example we can look at is Apple which recently launched

its iPhone product. Knowing the innovation in Apple, one could sense

that the eventual goal of Apple would be to have a product that combines

the iPhone capabilities and the iPod features, or have an iPhonewith

other capabilities such as a global positioning system (Baig, 2007). With

the recent success of Apple in various markets, there would be no doubt

that Apple would be able to achieve this.

Some of the questions to ask for the competitor's strategic objectives are:

What are the short-term and long-term objectives? What are the financial

objectives? Where is the competitor investing?

Competitor's Assumptions

Another key aspect in competitor analysis is an understanding of

competitors' assumptions about the overall market (trends in the market,

products, and consumers). For example, competitors could define their

actions based on what their assumptions are on the growth of the

market. In a cyclical industry (say pulp and paper or shipping sectors),

investments decided by players in the industry should be driven by when

competitors expect the industry to be at their peak, as timing is critical for

players in the industry to meet demand. However, this is not what usually

happens. Typically, shipping companies such as China Cosco (largest

shipping line in China) tends to invest and order new ships when the

industry is at its peak, and financing is not an issue (Stanley, 2006). As

shipbuilding takes a number of years, by the time the ships are ready, the

industry is at the other end of the cycle or in decline already. For aproper competitor analysis work, the assumptions made by competitors

on the industry and other players should be indicated, but as seen in the

example, the validity of these assumptions should be challenged.

Federal Express is a good example to highlight. When FedEx considered

overnight delivery, they assumed that demand would reach high levels

and that it would change the mail-and-package delivery industry

(Courtney, Kirkland and Viguerie, 2000). FedEx turned out to be correctand this changed the industry with other competitors following suit to offer

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 20/25

the same service. In this example, FedEx made a strong assumption on

the industry behaviour and was able to establish a presence in overnight

delivery quickly.

Some questions to address for this aspect include: What is the

competitor's viewpoint on the market and development? Who are the key

consumers or clients who the competitor feels will be most profitable?

Competitor's Strategy

A third aspect in competitor analysis is the understanding of a

competitor's strategy. In most cases, this strategy will be defined and

stated, particularly for public firms. In other cases, it may not be openly

stated what competitors' strategies are but these can be understood by

utilising a number of sources available to firms from analysing a

competitor's behaviour in certain situations to discussing with industry

experts to get their viewpoints.

For example, bookmaker Ladbrokes has clearly been expanding their

international presence through joint ventures in other markets. This

strategy was pursued after the firm split from the Hilton Group in 2006

(Attwood, 2007). By observing Ladbrokes' activities, one can determine

what the firm's strategy has been since the split. Another example is

Southwest Airlines, which pursued a "no-frills, point-to-point service and

which turned out to be a highly innovative, industry-changing and value-

creating strategy" (Courtney, Kirkland and Vihuerie, 2000). These two

examples indicate the value of having an understanding of competitors'

strategies and their focus.

A number of questions that need to be addressed are: What are the

strategy and plans of competitors in their key markets? Which markets

and products will the competitor focus on?

Competitor's Resources and Capabilities

Finally, a competitor analysis should also include an understanding of a

competitor's resources and capabilities as these would give a firm an idea

of how a competitor can achieve its strategy and objectives, and also give

a firm a timeline for when it would expect competitors to pursue certain

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 21/25

activities. For this aspect, a large part of information can be gleaned from

press articles and news. An example is the increase in orders of

the Airbus A380, the largest commercial aircraft in the world, by Dubai-

based Emirates Airlines from the current 55 to double the number (Dow

Jones, 2007). This indicates several thoughts: (1) Emirates Airlines has

large funding capability, and (2) Emirates Airlines will be expanding its

international business and presence once these aircraft are received.

Another example is Lanier Business Products. A leading manufacturer of

dictating machines, the firm leveraged its marketing strength to

successfully expand into another product, word processors, which they

sourced from another firm (Bales et al., 2000). This shows how important

it is to understand a competitor's resources and capabilities, and theirstrengths.

Several questions that can be raised in this respect are: What is the level

of resources available to the competitor for their investments? What are

the areas of strength for the competitor?

Competitor Response Profile

The results of the analysis from the four aspects of competitor analysis,

as defined above, lead to a competitor response profile. In this profile, afirm can define its thoughts on what actions competitors may purse

depending on the understanding given by the competitor analysis. This

provides a firm with a better grounding and preparation to react to

competitor actions.

RATER Model to Improve the Customer Service

RATER model is invented by Leonard Berry. He identified this five quality customer service dimensions.

Reliability, Assurance, Tangibles, Empathy, and Responsiveness. Nowadays, B2C businesses are taking care ofthis model. But, this will work out for all businesses such as B2B, B2C etc.

The quality customer service is the foundation for long run businesses. RATER model will regulate the business

process, solutions and services.

Reliability – Which means that the service providers ability to identify and provide business solutions to their

customers to achieve their goals and objectives.

Assurance – Providing trust and confidence to the buyers with good quality solutions.

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 22/25

Tangibility – Making customers happy with business environment, internal processes, corporate structure,

meeting schedule and everything

Empathy – Understanding the customer‟s business, goals, objectives and providing solutions with good quality

and helping them to overcome their problems

Responsiveness – Reveals the service providers awareness in problem solving with viable business solutions.

This process will refine the quality of business solutions and customer support.

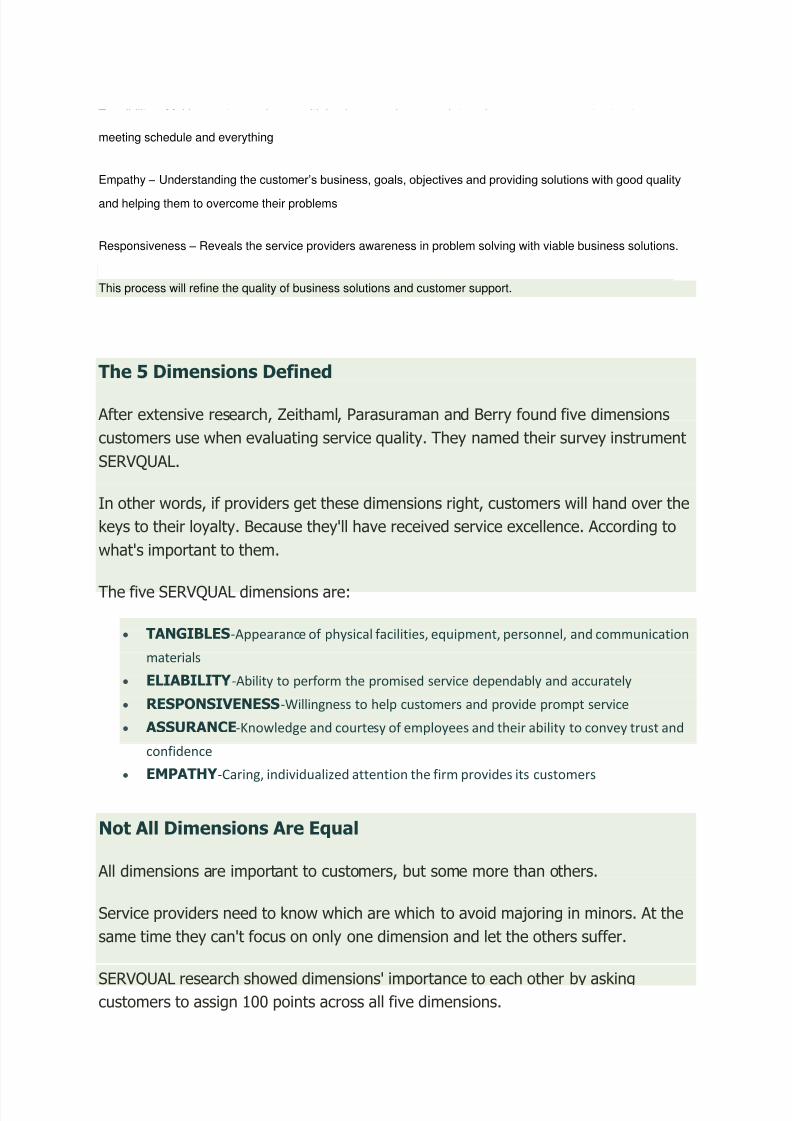

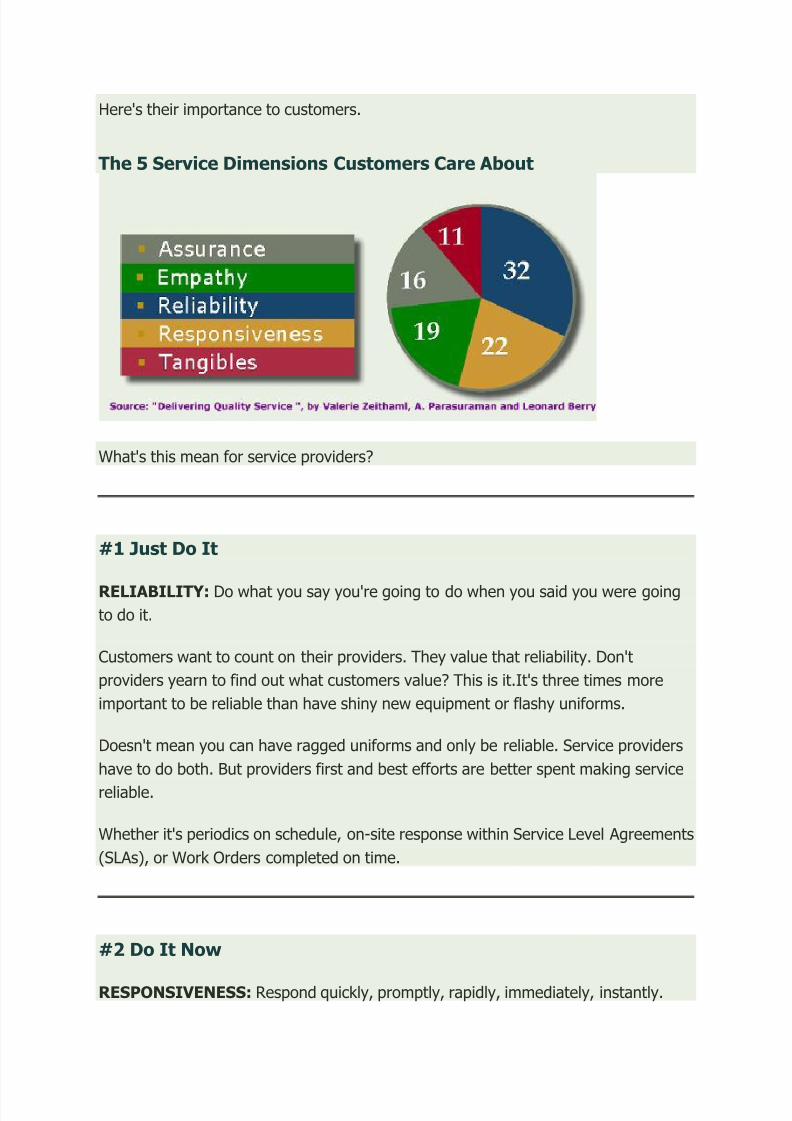

The 5 Dimensions Defined

After extensive research, Zeithaml, Parasuraman and Berry found five dimensions

customers use when evaluating service quality. They named their survey instrument

SERVQUAL.

In other words, if providers get these dimensions right, customers will hand over the

keys to their loyalty. Because they'll have received service excellence. According to

what's important to them.

The five SERVQUAL dimensions are:

TANGIBLES-Appearance of physical facilities, equipment, personnel, and communication

materials

ELIABILITY -Ability to perform the promised service dependably and accurately

RESPONSIVENESS-Willingness to help customers and provide prompt service

ASSURANCE-Knowledge and courtesy of employees and their ability to convey trust and

confidence

EMPATHY -Caring, individualized attention the firm provides its customers

Not All Dimensions Are Equal

All dimensions are important to customers, but some more than others.

Service providers need to know which are which to avoid majoring in minors. At the

same time they can't focus on only one dimension and let the others suffer.

SERVQUAL research showed dimensions' importance to each other by askingcustomers to assign 100 points across all five dimensions.

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 23/25

Here's their importance to customers.

The 5 Service Dimensions Customers Care About

What's this mean for service providers?

#1 Just Do It

RELIABILITY: Do what you say you're going to do when you said you were goingto do it.

Customers want to count on their providers. They value that reliability. Don't

providers yearn to find out what customers value? This is it.It's three times more

important to be reliable than have shiny new equipment or flashy uniforms.

Doesn't mean you can have ragged uniforms and only be reliable. Service providers

have to do both. But providers first and best efforts are better spent making service

reliable.

Whether it's periodics on schedule, on-site response within Service Level Agreements

(SLAs), or Work Orders completed on time.

#2 Do It Now

RESPONSIVENESS: Respond quickly, promptly, rapidly, immediately, instantly.

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 24/25

Waiting a day to return a call or email doesn't make it. Even if customers are

chronically slow in getting back to providers, responsiveness is more than 1/5th of

their service quality assessment.

Service providers benefit by establishing internal SLAs for things like returning phonecalls, emails and responding on-site. Whether it's 30 minutes, 4 hours, or 24 hours,

it's important customers feel providers are responsive to their requests. Not just

emergencies, but everyday responses too.

REPORTING RESPONSIVENESS

Call centers typically track caller wait times. Service providers can track response

times. And their attainment of SLAs or other Key Performance Indicators (KPIs) of

responsiveness. This is great performance data to present to customers in

Departmental Performance Reviews.

#3 Know What Your Doing

ASSURANCE: Service providers are expected to be the experts of the service

they're delivering. It's a given.

SERVQUAL research showed it's important to communicate that expertise to

customers. If a service provider is highly skilled, but customers don't see that, their

confidence in that provider will be lower. And their assessment of that provider's

service quality will be lower.

RAISE CUSTOMER AWARENESS OF YOUR COMPETENCIES

Service providers must communicate their expertise and competencies - before they

do the work. This can be done in many ways that are repeatedly seen by customers,

such as:

Display industry certifications on patches, badges or buttons worn by employees

Include certification logos on emails, letters & reports

Put certifications into posters, newsletters & handouts

By communicating competencies, providers can help manage customer expectations.

And influence their service quality assessment in advance.

8/3/2019 Impact of the Recession Theories Analysis

http://slidepdf.com/reader/full/impact-of-the-recession-theories-analysis 25/25

#4 Care about Customers as much as the Service

EMPATHY: Services can be performed completely to specifications. Yet customers

may not feel provider employees care about them during delivery. And this hurts

customers' assessments of providers' service quality.

For example, a day porter efficiently cleans up a spill in a lobby. However, during the

clean up doesn't smile, make eye contact, or ask the customer if there is anything

else they could do for them. In this hypothetical the provider's service was

performed fully. But the customer didn't feel the provider employee cared. And it's

not necessarily the employees fault. They may not know how they're being judged.They may be overwhelmed, inadequately trained, or disinterested.

SERVICE DELIVERY MATTERS

Providers' service delivery can be as important as how it was done. Provider

employees should be trained how to interact with customers and their end-users.

Even a brief session during initial orientation helps. Anything to help them

understand their impact on customers' assessment of service quality.

#5 Look Sharp

TANGIBLES: Even though this is the least important dimension, appearance

matters. Just not as much as the other dimensions.

Service providers will still want to make certain their employees appearance,

uniforms, equipment, and work areas on-site (closets, service offices, etc.) look good. The danger is for providers to make everything look sharp, and then fall short

on RELIABILITY or RESPONSIVENESS.