impact of shg-bank linkage programme of rural poor

TRANSCRIPT

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 1/33

Presented by:

Anil Ratnu (1761)

Muzaffar Hussain (1778)

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 2/33

SHG - A group of 10-20 people from ahomogeneous class, who come together foraddressing the common problems.

Ideal number of members would be between

15 -20.

They are encouraged to make voluntary thrifton a regular basis.

Trust among members in the group.

The Group Maintains books of accounts.

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 3/33

S Saving

E Earning

L Learning

F Friendship

G Growth

R Resources

O Opportunities

U Unity

P Progress

H Honesty

E Economy

L Leadership

P Productivity

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 4/33

To assess the impact of SHG-bank linkage programme onincome generation of the SHG households.

To find problems of SHPI for promotion and maintenance of

SHGs.

To know the utilization of credit.

To find out the change in access to nutrition, children’s

education and health care.

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 5/33

•DescriptiveResearch

Research

Type

•Area sampling

Sampling

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 6/33

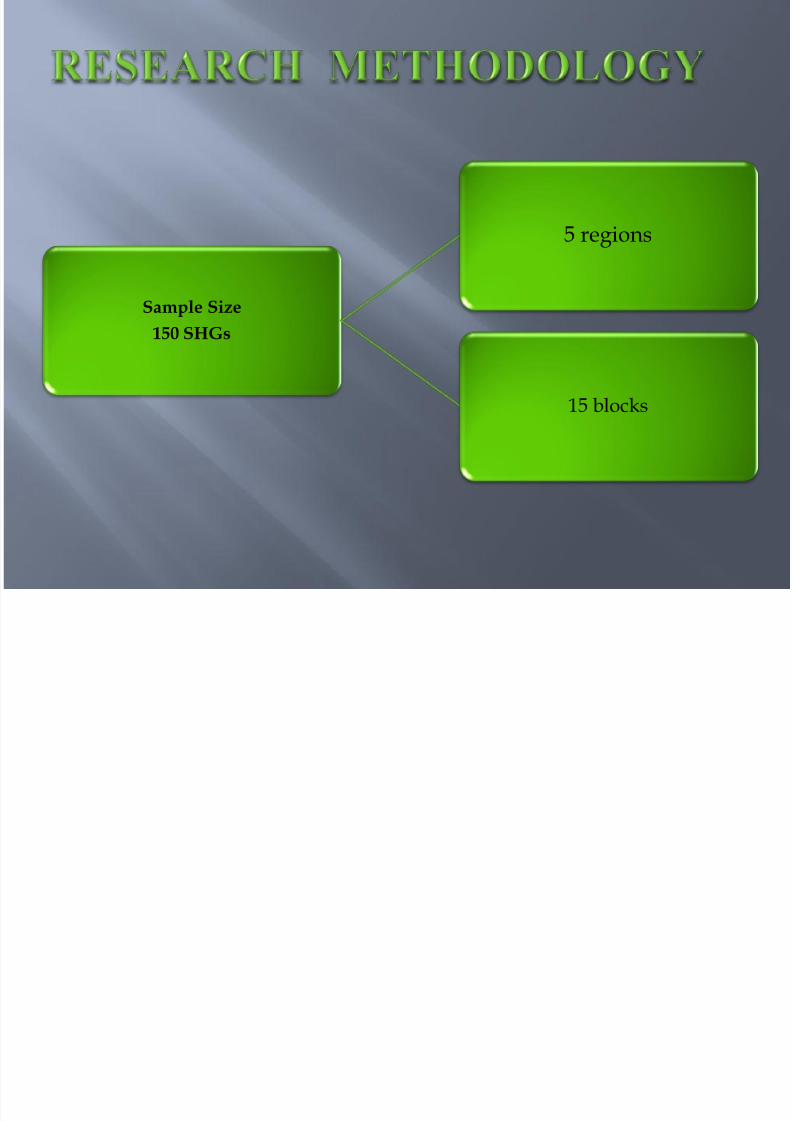

Sample Size

150 SHGs

5 regions

15 blocks

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 7/33

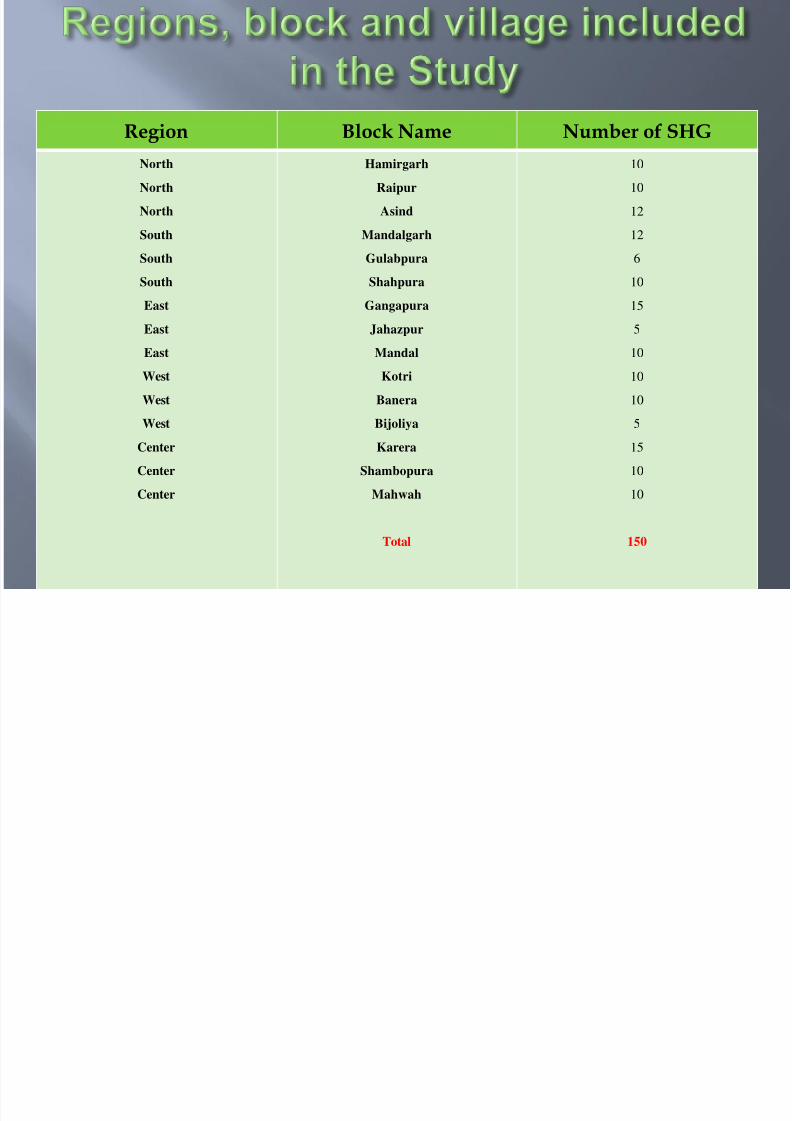

Region

Block Name

Number of SHG

North North North South South South East East East West West West Center Center Center

Hamirgarh Raipur Asind

Mandalgarh Gulabpura Shahpura Gangapura Jahazpur Mandal Kotri Banera Bijoliya Karera

Shambopura Mahwah

Total

10 10 12 12 6 10 15 5 10 10 10 5 15 10 10

150

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 8/33

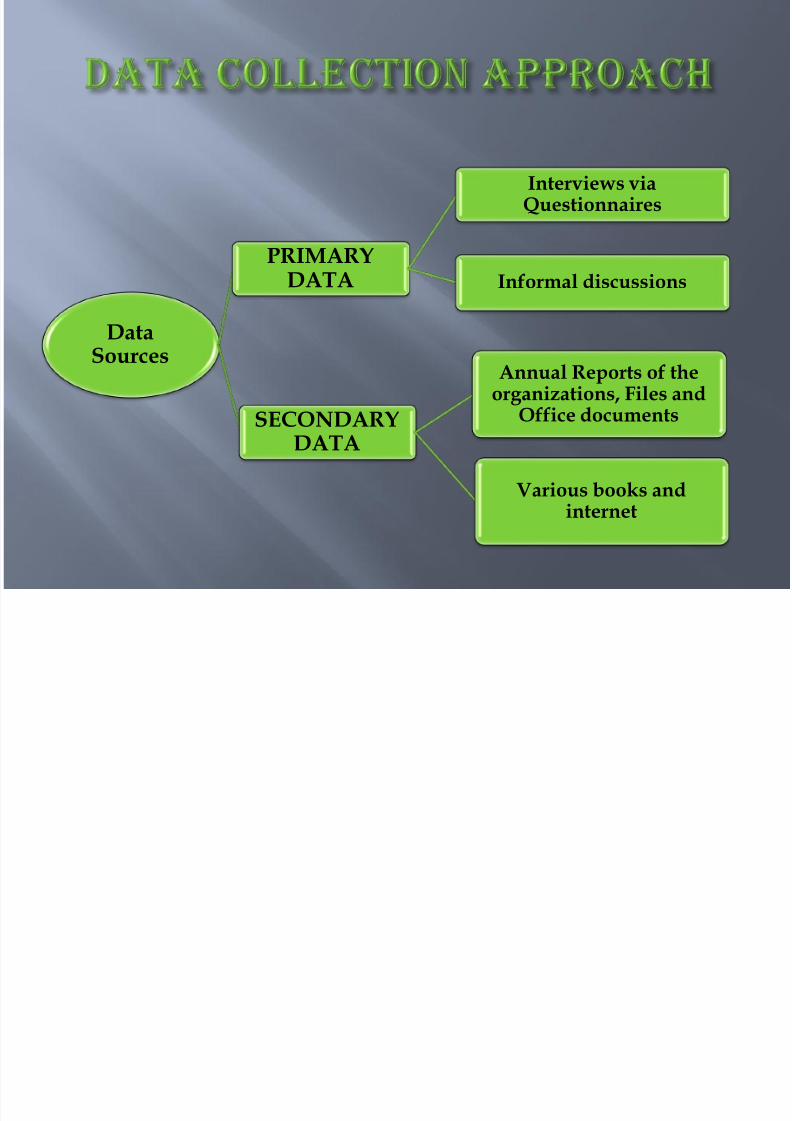

DataSources

SECONDARYDATA

Annual Reports of theorganizations, Files and

Office documents

Various books andinternet

PRIMARY

DATA

Interviews viaQuestionnaires

Informal discussions

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 9/33

Illiterate respondents(SHGs).

Time constraintsdue to wide scopeof study

Transportationproblems in

villages

Inaccessibility ofSHG members

Busy schedule ofofficers inorganizations

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 10/33

S.no

Banks No. of SHGs % Total Loan givento SHGs (Rs inlakhs)

%

1 CommericalBank

9597 32.32 7697.98 46.00

2 RRBs 8843 29.79 3912.22 23.38

3 CCBs 11247 37.89 5123.93 30.62

Total 29687 100.0 16734.13 100.0

Source :Apex Bank Report

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 11/33

DATA

ANALYSIS

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 12/33

Financialsupport

28%

Shortage of fieldstaffs32%

Illiteracy/ignorance of people

40%

Problems faced in promotion of SHGs (%)(by SHPI)

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 13/33

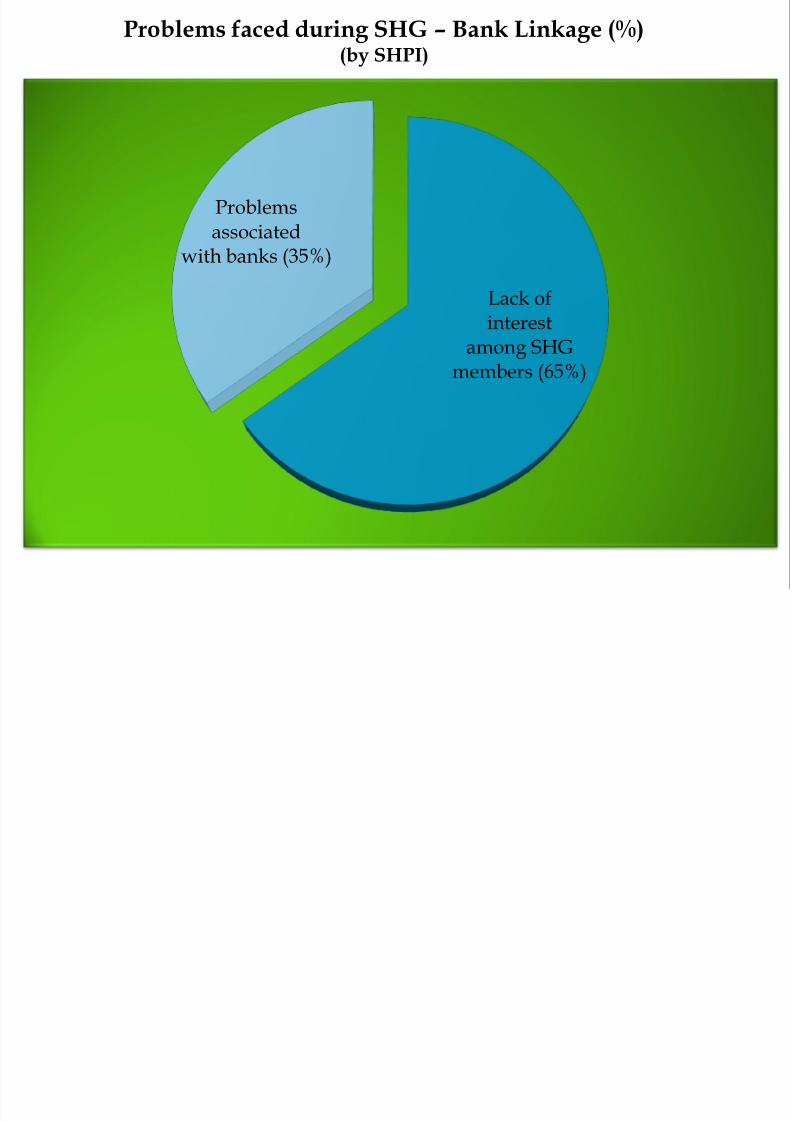

Lack ofinterest

among SHGmembers (65%)

Problemsassociated

with banks (35%)

Problems faced during SHG – Bank Linkage (%)(by SHPI)

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 14/33

81.33%

8.67%

10%

Distribution of SHGs bysex of members (%)

All female All male Mixed

22%

36%22%

20%

Distribution of SHGs bycaste of members (%)

Only SC/ST

Only OBC

SC/ST & OBC

SC/ST, OBC and General

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 15/33

52%

48%

Distribution of SHGs byeconomic status of

members (%)

All/majority BPLAll/ majority APL

34%

2%10%

8%26%

20%

Total distribution ofmembers by occupation

(%)

FarmersArtisans

Traders

Agro processors

Agriculture labour

Non agriculture labour

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 16/33

80%

4% 6%

2% 2% 2%

4%

Distribution of SHGs by percentage of loanrecovery (%)

100% 95-99% 90-94% 85-90% 75-84% 50-74% <50%

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 17/33

41381

43950

40000

40500

41000

41500

42000

42500

43000

43500

44000

44500

Pre SHGs Post SHGs

CHANGES IN ANNUAL NET HOUSEHOLDINCOME (Rs)

CHANGES INANNUAL NETHOUSEHOLDINCOME

Growthrate6.1%

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 18/33

4187

4401

4050

4100

4150

4200

4250

4300

4350

4400

4450

Pre SHGs Post SHGs

Annual per household consumption expenditure offood (Rs)

Annual per householdconsumption expenditureof food

Growthrate5.1%

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 19/33

1283

1352

1240

1260

1280

1300

1320

1340

1360

Pre SHGs Post SHGs

Annual per household consumption expenditure ofnon food

Annual per householdconsumptionexpenditure of non food

1283

1352

1240

1260

1280

1300

1320

1340

1360

Pre SHGs Post SHGs

Annual per household consumption expenditure of non-food (Rs)

Annual per householdconsumption expenditureof non-food

Growthrate5.4%

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 20/33

297

314

285

290

295

300

305

310

315

320

Pre SHGs Post SHGs

Changes in expenditure on health (Rs)

Changes in expenditure onhealth

Growthrate6.6%

h ld b f ( )

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 21/33

0

5

10

15

20

25

30

3534

6

24

12

18

6

28

8

26

14

20

4

Household income by sources of earnings (%)

Pre- SHGs Post-SHGs

h i i i hild ’ d i d

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 22/33

0

10

20

30

40

50

60

70

80

90

Nutrition Children’s education Health care

7882

76

2016 18

2 2 2

change in access to nutrition, children’s education and

health care (%)

Increase No change Decrease

Di ib i f i i b h h ld

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 23/33

0

20

40

60

80

100

120

140

160

SHG Bank Co-operative

society

0

33

3

150

42

6

N o . o f M e m b e

r s

Distribution of saving instruments by households

Pre-SHG Post-SHG

P t di t ib ti f b b f l

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 24/33

0

10

20

30

40

50

60

SHG Banks Moneylenders Relatives/friends

0

16

60

24

48

22

1614

Percentage distribution of borrowers by source of loan(%)

Pre-SHG Post-SHG

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 25/33

0

10

20

30

40

50

60

70

80

90100

Loans not taken Loans taken

54

46

8

92

Changes in household availing loan (%)

Pre-SHG Post-SHG

P t di t ib ti f l b

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 26/33

0

10

20

30

40

50

60

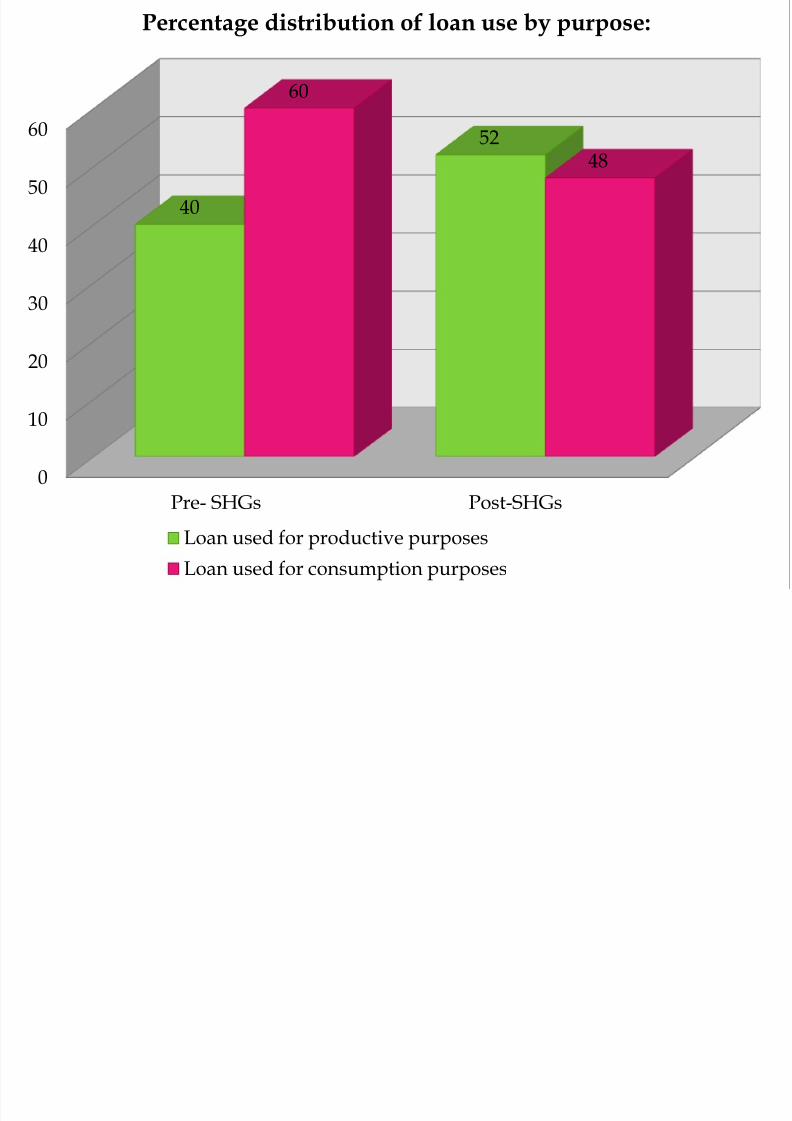

Pre- SHGs Post-SHGs

40

52

60

48

Percentage distribution of loan use by purpose:

Loan used for productive purposes

Loan used for consumption purposes

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 27/33

Strengths Weaknesses

Linkages

Regular savings

Inter-lending

Unity

Faith in each other

Lack of interest

Lack of confidence

Lack of time

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 28/33

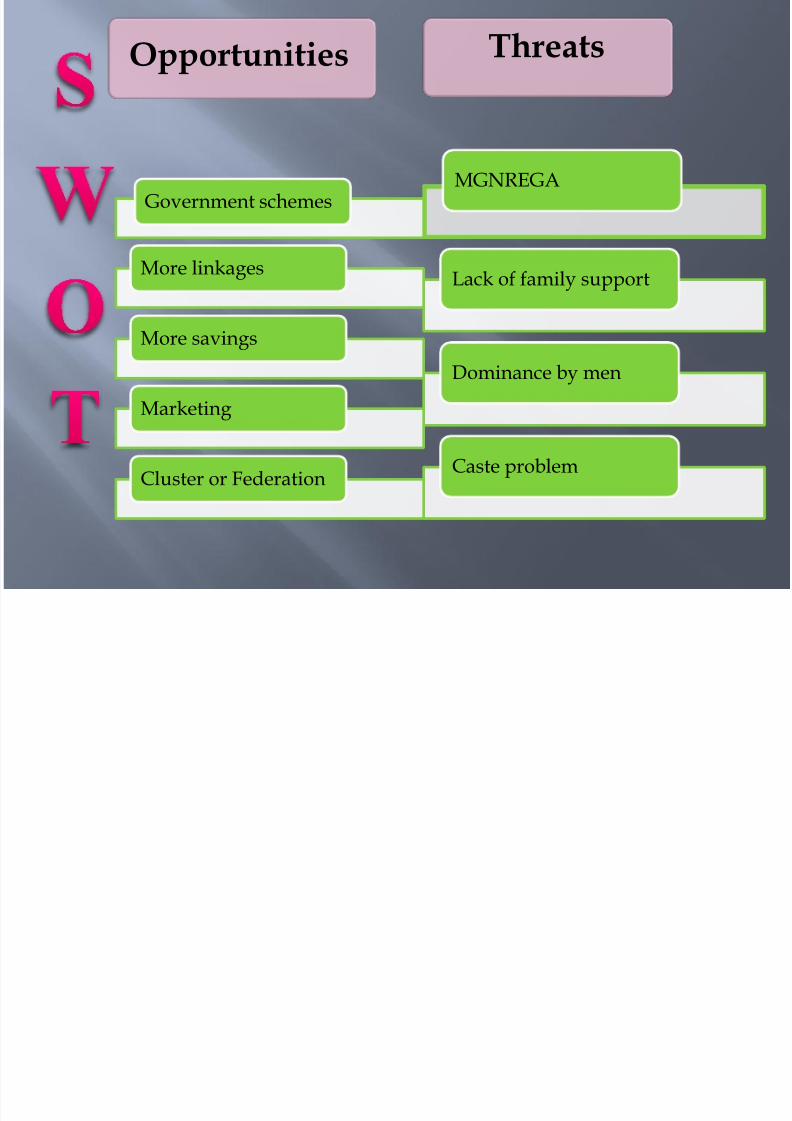

ThreatsOpportunities

Government schemes

More linkages

More savings

Marketing

Cluster or Federation

MGNREGA

Lack of family support

Dominance by men

Caste problem

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 29/33

80 per cent of SHGs have only women members.

More than 52 per cent of SHGs consist of membersbelonging to BPL families.

Changes in net household income between pre-SHGand post-SHG registered a significant growth per yearat 6.1 per cent.

The annual growth rate of per household consumptionexpenditure on food and non-food items recorded 5.1per cent and 5.4 percent respectively.

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 30/33

Per household annual expenditure on education andhealth recorded 6.6 per cent and 5.7 per cent growthrespectively.

On the issue of repayment of loan by SHG members,the findings show 90 per cent of households reportedregularity in repayments of loans.

About 92 per cent of households reported that thesocial empowerment of women had increased afterattaining membership in SHGs over a period of time.

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 31/33

More than 60 per cent of the households indicated thatthere is an increase in the ownership of productiveassets in post-SHG situation as compared pre-SHGssituation.

The major problems in promoting new SHGs asreported by SHPIs were mainly illiteracy andignorance of people (40 per cent), shortage of field

staffs (32 per cent) and financial support (28 per cent).

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 32/33

Let project be continued and also started in thosevillages where it has not started yet.

Further formation of SHGs should be directed towardsparticipation of BPL families.

Employee from the linked bank should regularlyattend the SHG meeting.

Still 30% of total loan consumption comes frommoneylenders and relatives so there is still scope forfurther loan disbursement.

SHG members should be given proper training andguidelines to utilize the loan amount for incomegenerating purpose.

8/3/2019 Impact of Shg-bank Linkage Programme of Rural Poor

http://slidepdf.com/reader/full/impact-of-shg-bank-linkage-programme-of-rural-poor 33/33