impact of demand uncertainty for automotive powertrains ... · mckinsey & company 2 bulk...

TRANSCRIPT

Nancy, France | 27th – 29th June 2018

Impact of Demand Uncertainty for Automotive Powertrains and Body on Bulk Materials

CONFIDENTIAL AND PROPRIETARY Any use of this material without specific permission of McKinsey & Company is strictly prohibited

2 McKinsey & Company

Bulk materials such as aluminum, steel and copper are impacted by increasing adaptation of electromobility which leads to changes in powertrain technology, the car body and chassis

2 McKinsey & Company SOURCE: McKinsey

Car body – continuous battle for Aluminum and steel lightweight solutions, especially for ICEs

Chassis – BEVs with different long steel product requirements compared to ICEs due to heavy batteries

Powertrain – BEVs with a higher Copper intensity per car and different long steel product requirements compared to ICEs

Cu 63.546 Copper

29

3 McKinsey & Company

Iron ore availability will not be an issue

3 McKinsey & Company SOURCE: McKinsey 3 McKinsey & Company

Uncertainty of supply

Vulnerability to the absence of substitution

Fe 26

55.845 Iron

55 years of iron ore reserves (83 bn t) at current production volume

Sufficient mine capacity (2.5 bn tons) already today to meet future demand

Uncertainty of demand Decline of iron ore demand by 350 Mt due to increase of scrap supply

Political exposure of supply

Low political exposure supply risk (Australia, Brazil, China)

Supply chain recycling Further increase of steel scrap supply (~100 Mt in China, another ~100 Mt in Rest of World)

Years of known reserves

No supply disruptions resulting in vulnerability expected

Years of known reserves

Uncertainty of supply

Political exposure of

supply

Supply chain recycling

Uncertainty of demand

Vulnerability to absence of substitution

4 McKinsey & Company

Global steel demand is expected to grow slowly at ~0.5-1.0% p.a. and automotive end uses account for 10-12% of finished steel demand

4 McKinsey & Company

11%

1,499

40%

18%

10%

12%

2017 2015

1,587

11% 7%

11%

40%

11%

19%

8%

12%

10%

12%

12% 1,647

39%

12%

Construction

7% 12%

10%

10%

21%

2025 2020

1,614

8%

Others

39%

20%

+0.5% p.a.

Other transport

40%

Engineering

7% Oil and Gas

Automotive 1,702

20%

11%

2030 SOURCE: Worldsteel; McKinsey integrated steel demand model 2018Q1; JFK

Million tons

§ Continuous growth at low level for automotive steel

§ Shift to high-value ultra-high strength flat steel due to continuation of light-weight trend

§ Shift in long steel portfolio due EV adaptation

1.4

CAGR 2017-30, % p.a.

5 McKinsey & Company

Research suggests a strong decline for the share of steel in the automotive BIW and a shift towards higher value AHSS and UHSS at the same time

5 McKinsey & Company SOURCE: CAR - Center of Automotive Research, June 2017

42%

20% 18%

20%

16% 14%

10%

15%14%

10%12%

6% 8%

9% 9%8%

5%

2025

Aluminum (5000/6000 Alloys)

Magnesium

2020

Carbon Fiber Reinforced Plastic/ Composites

Aluminum High Strength Alloys

2015

Mild steel

High Strength Low Alloy

High Strength Steel

2%

Advanced High Strength Steel Ultra High Strength Steel Boron/Martensite (UHSS)

Material distribution Body-in-White1 Global Demand AHSS steel In million tons

1 Body-in-White plus closures in the US fleet

22

16

12

2025 2016 2020

6 McKinsey & Company

Iron ore demand is expected to decline by 350 Mt due to increasing scrap availability

6 McKinsey & Company

400

800

2,400

2,000

1,600

1,200

0

~350

Rest of World

China

2030 25 20 15 10

SOURCE: Global steel and raw materials model 2018Q1; McKinsey iron ore team analysis

Million tons

Global Iron Ore Demand Global Scrap Availability and Supply

+100

~85

~275

~400

~215

~315

2017 ~60

2030

Unused scrap

Scrap supplied

+100

~450

~225

~200

~550 ~775

~650 2017

2030

75-80%

75-80%

~70%

~70%

Recycling rate

7 McKinsey & Company

Aluminum won't be an issue either

7 McKinsey & Company SOURCE: McKinsey 7 McKinsey & Company

Al 13

26.9815386 Aluminum

Years of known reserves

Uncertainty of supply

Vulnerability to the absence of substitution

~100 years of bauxite reserves (30 bn tons) at current production volume

Sufficient future mine capacity (~700 Mt) expected to meet future demand

Uncertainty of demand Continuous growth at slower rates than over the last decade, ~25% of demand for automotive, strong competition with steel

Political exposure of supply

Medium political exposure supply risk (Australia, China, Guinea)

No supply disruptions resulting in vulnerability expected

Supply chain recycling Further increase of scrap recycling rates expected (Ø 40% globally; automotive and construction Europe >90%)

Years of known reserves

Uncertainty of supply

Political exposure of

supply

Supply chain recycling

Uncertainty of demand

Vulnerability to absence of substitution

8 McKinsey & Company

Global aluminum demand is expected to grow steady at ~3% p.a., share of automotive end uses in demand expected to increase from 25% to 30% until 2030

8 McKinsey & Company SOURCE: Worldsteel; McKinsey integrated steel demand model 2018Q1; JFK

85

16%

28%

93

26%

10%

28%

10%

11% 16%

10% 10%

15%

2017 2020

119

2030

Automotive

23%

27%

+2.7% p.a.

Consumer durables

Engineering Packaging

25%

ABC

11% 11%

10%

30% 106

Others 15%

10%

2025

12% 10%

10%

25%

Million tons

§ Strong growth in automotive, mainly driven by flat rolled products

4.1

CAGR 2017-30, % p.a.

9 McKinsey & Company

Automotive body sheet (ABS) shows strong demand growth, however, mainly driven by the use in standard ICE's – further investments in new capacity required to meet future demand

9 McKinsey & Company

Capacity 2025

3.2

2025 2020

1.9

3.3

2017

1.2

Mt Global ABS Demand What would it take to increase ABS penetration?

§ ABS will represent <3% of global aluminum demand in 2025 with focus on premium car segment

§ Global ABS nameplate capacity 2025 will grow to ~3.2 Mt based on installed and announced capacity expansions; further investments required to meet the growing demand

§ Use of aluminum body sheet has clear advantages - Much higher weight reduction potential than AHSS - Longer life-cycle for aluminum processing machines - Lower scrap price discount for aluminum than steel

§ Potential drivers to increase ABS penetration - Set up sufficient large scale production capacity to reduce

cost gap to steel, e.g., continuous CRM instead of reversing - Improve relationships to automotive OEMs - Get involved early on in model development and assembly

plant planning (e.g., F150 example)

SOURCE: McKinsey Integrated Aluminum Model v1.27 2018Q1

10 McKinsey & Company

A detailed analysis from a teardown reveals a 5-10% p. larger share of aluminum in BEVs vs. ICEs today and a lower share of HSS

10 McKinsey & Company

47% 41% 36%

22%22%

19%

12% 18%

24%22%22%3%

Gasoline Diesel

3% 100%

BEV

6%

3% 100% 100%

Split of total vehicle weight (excl. powertrain) by material1

Standard steel and cast iron Others

HSS

Aluminum

Plastics

Breakdown of material type by powertrain ▪ In line with expectations,

BEVs with largest share of aluminum in structural components (mainly BiW)

▪ BEVs also with lowest share of HSS and significantly lower share of standard steel

Insights

SOURCE: A2Mac1, McKinsey

1 Results based on Honda Civic, Honda CR-V, Mazda 2, Peugeot 208, Renault Kwid ,Toyota Camry, VW Golf, Ford Ranger, Mercedes S-Class, Nissan Qashqai, BMW X5, Toyota Prius, Nissan Leaf, Opel Ampera-e, Tesla Model S, VW e-Golf, Toyota Mirai as available in US market

11 McKinsey & Company

Costs to be considered when thinking about aluminum vs. steel substitution in automotive

SOURCE: McKinsey 11 McKinsey & Company

Disposal Usage Manufacturing

▪ Scrap credit discount vs. virgin material

▪ Fuel costs ▪ CO2 emissions ▪ Body repair costs

– Equipment and processing cost for repair shops

– Material costs

▪ Raw material cost – Material needs – Material price – CO2 emissions

▪ Manufacturing cost – Manufacturing/quality yield – Other costs

▪ Capex – For ABS production lines – For OEM assembling lines

12 McKinsey & Company

Tesla Model 3

Potentially investment into lightweight no longer outweighs the investment into larger and better battery packs in the future

12 McKinsey & Company SOURCE: A2Mac1, McKinsey

Tesla Model S

Aluminum body in white

(Mostly) steel body in white

Weight Kg ~275 ~320

Volume adjusted weight1

Kg ~244 ~320

1 Tesla Model S weight adjusted to dimensions of smaller Tesla Model 3

Material cost

EUR ~928 ~608

Model 3 frame is ~76 kg heavier than the Model S but saves ~EUR 320 in material cost In future, OEMs are likely to pay less for lightweight in BEVs as battery prices are

expected to drop which will influence the choice of materials used

-320

13 McKinsey & Company

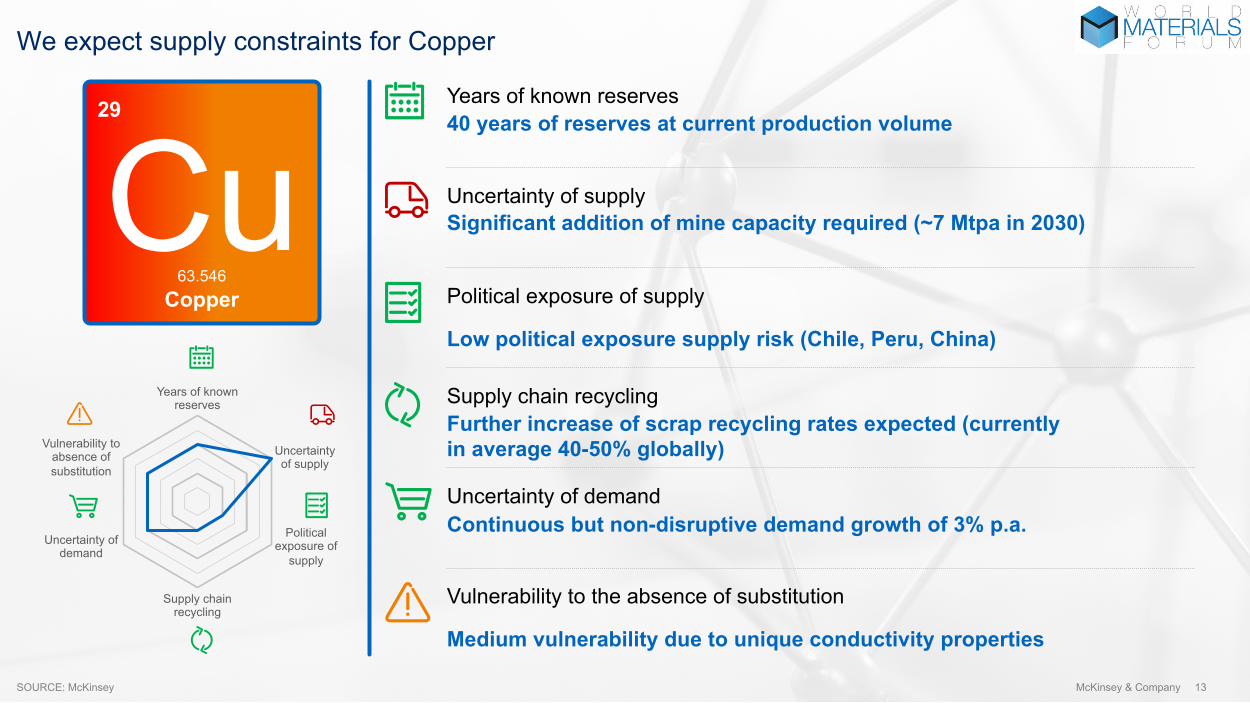

We expect supply constraints for Copper

13 McKinsey & Company SOURCE: McKinsey

Cu 29

63.546 Copper

Years of known reserves

Uncertainty of supply

Uncertainty of demand

Political exposure of supply

Supply chain recycling

Vulnerability to the absence of substitution

40 years of reserves at current production volume

Significant addition of mine capacity required (~7 Mtpa in 2030)

Continuous but non-disruptive demand growth of 3% p.a.

Low political exposure supply risk (Chile, Peru, China)

Further increase of scrap recycling rates expected (currently in average 40-50% globally)

Medium vulnerability due to unique conductivity properties

Years of known reserves

Uncertainty of supply

Political exposure of

supply

Supply chain recycling

Uncertainty of demand

Vulnerability to absence of substitution

14 McKinsey & Company

Demand growth mainly driven by electrical and industrial applications as well as EVs and EV-infrastructure – additional upside of 1.1 Mt in our high case demand scenario

SOURCE: McKinsey 14 McKinsey & Company

+40%

High case demand

33.3 34.4

Upside Base case demand

1.1

2.7

0

Electric vehicles

Transpor- tation

1.3

2.9

Building and construction

0.9 1.7

Consumer and general products

Electrical/ electronic

2017

23.8

Industrial machinery and equip.

Change of refined copper usage by end-use, in million tons

▪ Adoption of electric vehicles will be a major contributor of growth to the copper demand ▪ Copper intensity in EVs is ~3-4x higher than conventional

propulsion cars ▪ Charging infrastructure to add ~0.8 kg of copper per unit

15 McKinsey & Company

The continuous copper demand growth accelerated by EVs puts even more pressure on suppliers to add primary production capacity

SOURCE: MineSpans by McKinsey, McKinsey copper scrap model

Copper primary and secondary supply Kt, 2017-30

Likelihood of higher copper prices going forward

▪ Greenfield price regime needed to incentivize capacity additions, i.e. premium of 50-70% over C90 to recover greenfield investment costs

▪ Accelerating cost inflation due to lower grade deposits and more challenging geological conditions

Primary Secondary Induced additions to meet demand

29.7

7.2

25

33.3

2030 20 2017

23.6 1.5

25.9

15 McKinsey & Company

16 McKinsey & Company

Conclusions for the impact of demand uncertainty for automotive powertrains and body on bulk materials

16 McKinsey & Company

§ Automotive body sheet (ABS) will see further strong demand growth driven by the need for lightweight solutions for standard ICE's – further investments in new capacity required to meet future demand

§ Iron ore and aluminum availability won't be an issue going forward. Iron ore demand will decline due to increase scrap availability, especially in China

§ OEMs likely to pay less for lightweight in BEVs in future as battery prices are expected to drop. Choice of materials likely to shift towards high strength steels, similar to the trend observed in 2nd generation mass market BEVs (Nissan Leaf, Tesla Model 3)

§ BEVs contribute to the copper demand growth. Absolute demand volume for EVs and infrastructure expected to reach ~1.8Mt. This contribution puts more pressure on suppliers to add primary production capacity and we expect a greenfield price regime for copper in future to incentivize further supply capacity additions

SOURCE: McKinsey