impact assessment report - danish refugee … assessment report nusaf2 - northern uganda social...

TRANSCRIPT

IMPACT ASSESSMENT REPORT NUSAF2 - Northern Uganda Social Action Fund

2012-2013 Project in Moroto Municipality and Nadunget Sub-County

Karamoja, Uganda

2

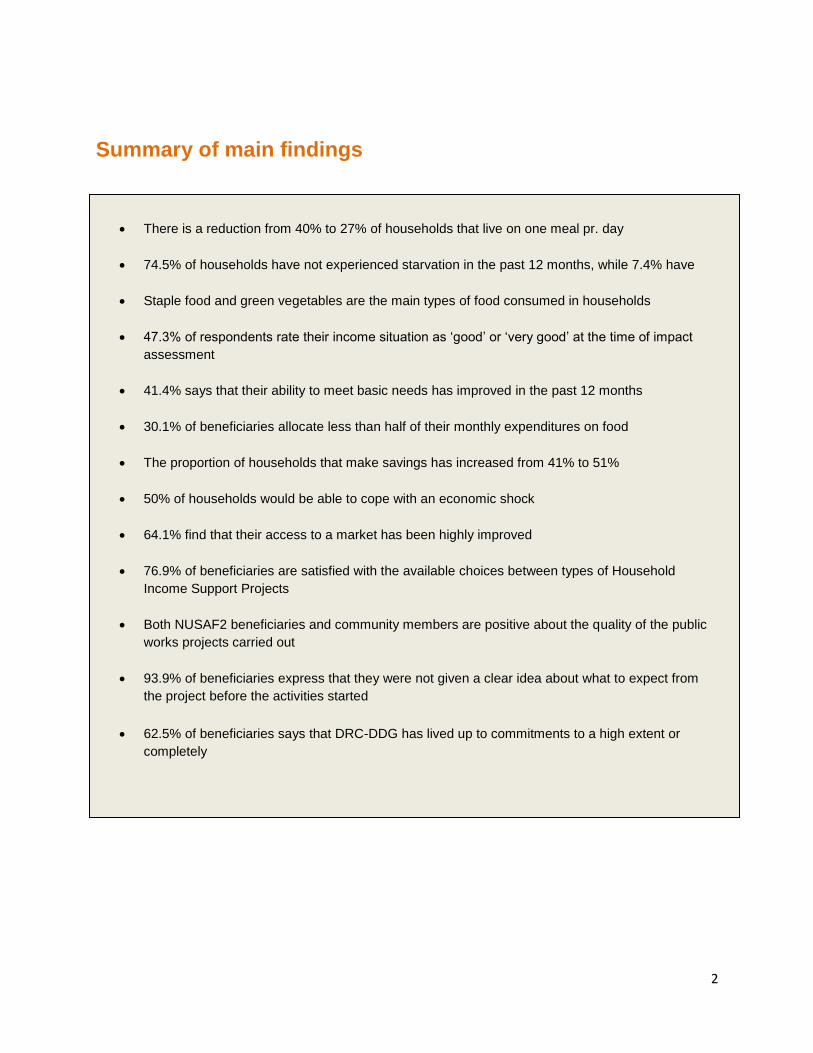

Summary of main findings

There is a reduction from 40% to 27% of households that live on one meal pr. day

74.5% of households have not experienced starvation in the past 12 months, while 7.4% have

Staple food and green vegetables are the main types of food consumed in households

47.3% of respondents rate their income situation as ‘good’ or ‘very good’ at the time of impact

assessment

41.4% says that their ability to meet basic needs has improved in the past 12 months

30.1% of beneficiaries allocate less than half of their monthly expenditures on food

The proportion of households that make savings has increased from 41% to 51%

50% of households would be able to cope with an economic shock

64.1% find that their access to a market has been highly improved

76.9% of beneficiaries are satisfied with the available choices between types of Household

Income Support Projects

Both NUSAF2 beneficiaries and community members are positive about the quality of the public

works projects carried out

93.9% of beneficiaries express that they were not given a clear idea about what to expect from

the project before the activities started

62.5% of beneficiaries says that DRC-DDG has lived up to commitments to a high extent or

completely

3

Table of contents

Executive summary

1. Introduction

a. DRC-DDG Program in Uganda

b. Description of project and working context

2. Methodology

a. Data collection methods

b. Sampling and characteristics of respondents

c. Data handling and analysis

d. MitHISPtion of methodological challenges

3. Findings

a. Indicator I: Food Security

b. Indicator II: Income and economic resilience

c. Indictator III: Market access

4. Quality assessment: Project relevance and accountability in delivery

5. Conclusion

4

1. Introduction

Description of project and work context

DRC-DDG has been an implementing partner to the WFP-funded Northern Uganda Social Action Fund 2

program in Karamoja from March 2012. DDG has been responsible for Public Works projects and

Household Income Support Projects (HISP) in Moroto and Nadunget, and has administered the

distribution of cash and food for work.

The overall objective for DRC-DDG’s work has been: To support livelihoods of poverty-stricken

households in Nadunget Subcounty and Moroto Municipality.

DRC-DDG has sought to contribute to this overall objective, by pursuing the immediate objective:

Improved access to income earning opportunities and basic social services of food insecure households

in Nadunget Subcounty and Moroto Municipality

The project has targeted a total of 6,492 households with an estimated 38,900 direct and indirect

individual beneficiaries.1 The beneficiaries have been organized into 135 clustered, each carrying out one

Public Works project, and one HISP. In total, the following activities have been carried out under NUSAF

2 in the period March 2012 to March 2013.

135 Public works projects:

Community Access Road 48

Cattle Crush 7

Tree Planting 80

135 Household Income Support Projects:

Vegetable garden 45

Grinding mill 16

Cereal banking 4

Field crop cultivation 30

Bee keeping 10

Mushroom growing 8

Orchards 5

Tree nursery 10

Groundnuts grinding mill 6

Poultry 1

In addition, beneficiaries have been encouraged to establish Village Savings and Loans Associations

(VSLA), and the clusters who took interest have been given training in VSLA and saving-boxes with

record books.

1 A direct beneficiary is defined as a household member who actively takes part in public works and HISP. An indirect

beneficiary is a household member of a direct beneficiary. Number of indirect beneficiaries is estimated based on an average household size of 6 persons.

5

2. Methodology

Data collection methods This impact assessment aims to explore impact of the NUSAF2 implementation phase that started in

March 2012. It is based on a mixed methodology comprising a quantitative household survey and

qualitative focus group discussions. The household survey has been carried out in August 2013, six

months after the completion of the implementation phase, and the qualitative data in October 2013 with

the purpose of leaving enough time for project outcomes and impact to materialize. A second phase has

continued after March 2013, whereby this assessment also serves as a mid-term assessment for the two-

year program phase. Data has been collected by a team of external enumerators under the management

of DRC-DDGs M&E Unit. Enumerators have undergone a one-day training prior to data collection, and

the tools have been pilot-tested prior to usage. All data collection tools have been translated into

Ngakarimojong, and respondents have been interviewed in their mother tongue.

Sampling and characteristics of respondents

The household survey is based on responses from 599 randomly sampled NUSAF2 beneficiaries in all

locations and clusters of the project. Sampling has been made proportional to number of cluster members

to ensure that all clusters have relatively equal representation in the sample, and gender and age has

been made to reflect the distribution among the beneficiary population. In consequence, 62.5% of

respondents are female and 37.5% are male, while the age distribution is as follows:

Mitigation of methodological challenges

Prior to data collection in 2013, the data collection tools have been revised and specified with a further

level of detail than the baseline data collection in 2012. The end-line data thus introduces additional

measurements that were not included in the baseline, and to enable tracking of change in the

implementation period, such new questions have been accompanied by a question assessing

respondent’s perception of change in comparison with one year earlier. Therefore, this impact

assessment comprise a combination of direct comparisons between respondents answers to questions in

2012 and 2013 respectively, and perception-based assessments of change. This will be clearly indicated

with a label of when data was collected (2012 or 2013) in all tables in the report.

Age distribution of survey respondents

25 years andbelow

26-45 years

46 years andabove

6

3. Findings

Indicator 1: Food Security

Description of the indicator:

This indicator seeks to map food beneficiaries’ food security by assessing number of meals pr. day, level

of food sufficiency and diversity of food intake.

Impact assessment:

In 2012, 40% of beneficiary households stated to rely on one meal pr. day. In 2013, this proportion is

reduced to 27%, while 55.6% of respondents in 2013 live on two meals pr. day and 16.2% on three meals

pr. day. In the end-line survey, respondents have in addition been asked whether they in comparison to

the time before the project have experienced any change in the amount of food available in the

household. To this, 45.3% have indicated that there has been an increase in amount of food available in

the household, while 30.7% says the amount has remained the same and 9.6% that the amount has

decreased.

When this is coupled whether beneficiary households have experienced starvation in the past 12 months,

it is found that a fairly small fraction of 7.4% says this has been the case, and 74.5% says that their

household has not suffered from starvation in the past 12 months. In the qualitative data, it is a frequent

statement that they are “now able to feed the family”, and respondents have stated that their main usage

of additional income from NUSAF 2- related activities goes into food, medical treatment and school fees.

Respondents to the household questionnaire have, however, indicated that there are issues of food

insufficiency in relation to having food for all household members in the meals served. Less than 10% of

respondents says that there ‘always’ or ‘most often’ are food for all household members, while 48.5%

indicate this to be the case ‘sometimes’. As much as 25.5% says that there is ‘rarely’ food for all

household members in the meals in the home.

40 48.2

11

27

55.6

16.2

0

10

20

30

40

50

60

70

80

90

100

1 2 3

Pe

rce

nt

Number of meals pr. day

Number of meals pr. day

2012

2013

7

In a focus group discussion in Motoro town, a lady of a group that had a grinding mill as their HISP,

responded to a question on food diversity. She stated “those days [before joining the NUSAF project] the

only thing me and my children were eating was the residuals from brewing. Now, we eat posho”. In the

household questionnaire, it has been assessed whether this statement reflects a general trend. 34.8% of

respondents indicate that they today consume more varied types of food than one year ago, which

indicates a positive trend for food diversity. At the same time, 31% of beneficiaries says that the diversity

of their food consumption is at the same level as one year ago, and 21.2% says that they eat less varied

food. It thereby appears, that there are different trends of food security among different groups of

beneficiaries. Overall, the distribution of frequency of consuming various food items indicates that the

main sources of food today comprises carbohydrate-based staple foods (referred to by beneficiaries as

“bread”) and green vegetables.

7.4

74.5

17.4

0

20

40

60

80

100

Yes No No answer

Pe

rce

nt

Have you in the past 12 months experienced starvation in the household?

2013

18

1.3 3 0.7

7.59 5

0.89

21

0

5

10

15

20

25

30

Nu

mb

er

of

day

s in

mo

nth

Food item

Frequency of consuming various food items in a month

2013

8

28.4 29.5

41.4

0

10

20

30

40

50

Worsened Same Improved

Pe

rce

nt

Change in ability to meet basic needs

Endline: Do you think there in the past 12 months has been any change in your ability to meet basic needs?

2013

Indicator 2: Income and economic resilience

Description of the indicator:

In this section, beneficiaries’ level of income, savings and assets in the form of livestock is assessed to

explore trends in self-reliance and ability to cope with economic shocks.

Impact assessment:

Respondents in the household survey have made a subjective rating of their income situation. In the

baseline survey, the rating is made numerically on a scale from 1 to 5, and in the end-line the scale has

had five categories from ‘very bad’ to ‘very good’. Due to difference in the scales across the two surveys,

they cannot be directly compared, but the findings presented in the table below do indicate that there has

been a positive trend in the period from 2012 to 2013. In the end-line assessment, 47.3% of respondents

have rated their income situation as ‘good’ or ‘very good’.

Due to the difference in the scales, this measurement is in the end-line survey triangulated with a

question regarding beneficiaries’ perception of change in their ability to meet basic needs. In these

answers there is a similarity with the self-assessments of change in food security above as answers are

spread across the answer categories in a manner that indicates that there has been varied impact among

different groups of beneficiaries. The most significant trend among the answers is, however, that 41.4%

find that their ability to meet basic needs has been improved in the past 12 months.

5.3

15.2 18.4

23.6 23.7

0.7

26.8

46.6

18.5

8.1

0 0.8 0

10

20

30

40

50

Very bad Bad Fair Good Very good Don't know

Pe

rce

nt

How do you perceive the income situation for your household?

2013

2012

9

Additionally, respondents have answered an open-ended question about whether they think that being

part of the project has been of any benefit to their daily life, and if so in which way. The responses have

been mapped into a visual overview, with the size of the text indicating the frequency by which something

is mentioned:

The responses point at that the main benefits experienced by beneficiaries relate to improved access to

food and ability to feed the family, better possibilities of paying school fees and providing scholastic

materials to children, improved ability to buy subsidiary food, better and more balanced diet and improved

medical care and health. During focus group discussions, a number of beneficiaries highlighted that they

had found the project to motivate them to work, and that they had learnt how to engage in productive

activities that had otherwise been outside reach. This relates both to practical skills, but also to the

attitude to work. A man in Nadunget expressed the latter in the following way: “Let me say this like we

pastoralists do. If you want a cow to give milk, you first have to make the effort and take her grazing.

What we have learnt is that it is the same for earning money, you first have to work”.

In the household survey in 2013, household’s economic situation has been explored. There does not exist

equivalently detailed information in the baseline study, but these figures can be used for future reference,

and can be compared to other livelihoods studies among the target group in Karamoja.The figures will be

reported firstly in averages for the entire group of respondents followed by a detailed break-down that

describes the variance among beneficiaries. In 2013, NUSAF2 beneficiaries in Moroto and Nadunget

reportedly had the following average economic details:

Household monthly income 49,000 UGX

Household monthly expenditures 81,300 UGX

Monthly spending on food 47,900 UGX

Estimation of value of household savings 15,700 UGX

10

This indicates that beneficiaries on average spend almost all earnings on food, and that they are faced

with expenditures that exceed their income. When the numbers are broken further down, it is found that

there is a significant degree of variance across beneficiaries behind these average findings.

In relation to the distribution of the proportion of expenditure allocated to food, it is found that 30.1%

spend less than half of their monthly earnings on food, and that the remaining 69.9% of beneficiaries are

spread between spending between the ranges of 50% to 100% of their expenditures.

As a measurement of economic resilience, respondents have been asked about their saving habits and

ability to cope with an economic shock. Regarding savings, there has from 2012 to 2013 been an

increase from 41% to 51% of beneficiaries who state to make savings in the household. In 2013,

respondents have additionally been asked whether they make savings in a group, which 57.6% state to

do.

8.5 21.6

33.3 36.6

0

20

40

60

80

100

1-25% 26-50% 51-75% 76-100%

Pe

rce

nt

ho

use

ho

lds

Percentage of expenditure spent on food

Endline: Distribution of proportion of expenditure spent on food

2013

41 51

57.6

0

20

40

60

80

100

2012 2013 - inhousehold

2013 - in a group

Pe

rce

nt

Proportion of households making savings

11

Among the beneficiaries who make savings, the value of household savings has been broken down in

categories:

Here it is found that a greater percentage of 39.6% of respondents have less than 5,000 UGX saved, and

thus a quite limited liquidity available for crisis situations. 50.2% of beneficiaries have between 5,000 and

40,000 UGX, and 10.3 % have more than 40,000 UGX. Respondents have in addition been asked directly

whether they, in the event that member of the household urgently needed 20.000 UGX for medical care,

would be able to raise the money. To this, 50% of respondents have said yes – divided between 29.2%

who claimed to be able to get the money from household funds and 20.8% who claims they would be able

to borrow the money. It thus appears that there is a social economic resilience among the beneficiaries

that enables a larger fraction than the ones who have liquidity at hand to cope with an economic shock.

During focus group discussions, it has frequently been mentioned that beneficiaries seek to multiply

income that has been earned under NUSAF2, and that many beneficiaries succeed in setting up small

businesses. When inquiring about the types of business vested in, a common answer is brewing of local

brew. While this is a rational choice in a setting where there is a market for it, it may be considered if this

is the most constructive outcome of NUSAF activities – taken the challenges with alcohol addiction and

violence related to alcohol-intake into account.

One more measurement regarding the household’s economic situation has been made in relation to

number of livestock lost and gained in the previous 12 months. These findings indicate that 10% of

households have increased the number of livestock with 1 head, and 4% with 2 heads or more. 14.9%

state to have the same number as earlier, and 11% that they have lost livestock in the period. These

figures are at a background of a significant number of beneficiaries indicating that they neither at the time

of baseline nor end-line were in possession of livestock.

39.6

20.8 15.8 13.6

7.2 3.1

05

101520253035404550

Pe

rce

nt

Amount saved

Endline: Distribution of value of savings among households who make savings

2013

12

Indicator 3: Market Access

Description of indicator:

The measurements under this indicator are made with the purpose of exploring whether there is any

change in beneficiaries’ access to market places and thereby improved access to economic activities.

Impact assessment:

In order to establish information about changes in beneficiaries’ access to markets, a direct and an

indirect question has been included in the survey. In 2013, respondents have directly been asked,

whether their access to a market place has improved in the past 12 months. In this matter, there is a very

clear trend that beneficiaries do experience to have improved market access, as indicated in the following

table.

Also, respondents have been asked where they buy items to cover their daily basic needs, e.g. food and

other essentials. In both baseline and end-line, it is by far the majority of respondents who indicate that

they get this from a town or trading centre. The table above should thus be interpreted in the way that the

access to these trading centers is perceived to be improved in the period. At the same time, there is a

change in the proportion of respondents who indicate to purchase essential items in the village itself. At

the time of baseline it was as few as 1.7% of respondents that stated this as the main avenue for

household purchases, while it by the time of the end-line is 5.3%. This could reflect an emerging level of

economic activities in the villages, while still at a very modest level.

8.4 7.8 6.9

26

38.1

12.8

0

10

20

30

40

50

Pe

rce

nt

Level of change in access to market place

Has your access to a market place been improved in the past 12 months?

2013

13

4. Quality Assessment: Project relevance and accountability in delivery

As a result of DRC-DDG’s commitment to Humanitarian Accountability Partnership (HAP), an assessment

of beneficiaries’ rating of project relevance, delivery on commitments and rating of how accessible it is for

beneficiaries to raise complaints. In relation to project relevance, beneficiaries have rated the choices

available to them for different types of HISPs. A significantly positive trend is found here, with 76.7%

saying ‘satisfied’ or ‘very satisfied, and less than 6% expressing dissatisfaction with the available types of

HISPs.

Subsequently, beneficiaries and a sample of other community members have been asked how satisfied

they are with the quality of the public works project that has been carried out in their area. There appears

to be a high level of satisfaction with the results of public works, and community members who has not

taken part in the public works process are slightly more positive than sampled NUSAF2 beneficiaries.

0.4 5.5 4.6

13.9

62.8

12.8

0102030405060708090

100

Verydissatisfied

Dissatisfied Neitherdissatisfied

norsatisfied

Satisfied Verysatisfied

No answer

Pe

rce

nt

How satisfied have you been with the choices available to your group between different types of IGAs?

2013

2.8 3.7 5.2

15.9

59.4

12.8

1.8 3.6 7.1

23.3

64.3

0

10

20

30

40

50

60

70

Not at all Low extent Someextent

High extent Comletely No answer

Pe

rce

nt

Level of satisfaction with quality

How satisfied are you with the quality of the public works project that has been implemented under NUSAF2 in your parish?

NUSAF2Beneficiaries

Othercommunitymembers

14

On the matter of level of information to beneficiaries and clarity about project details prior to

implementation, the findings are much less positive. In fact, 93.9% of respondents state that they did not

get a clear idea about what to expect from the project before activities started in 2011. This could point at

that there have been weaknesses in the community liaison and community entry process during project

inception.2

In the end-line assessment, beneficiaries have been asked to rate the quality of DRC-DDG’s service

delivery, by answering to what extent DRC-DDG has lived up to commitments. Findings are generally

positive with 69.7% of respondents stating either to a ‘high extent’ or ‘completely’, while 6% say to a ‘low

extent’ or ‘not at all’.

2 DRC-DDG became an implementing partner for NUSAF2 in 2012

93.9

6.1

0

20

40

60

80

100

No Yes

Pe

rce

nt

Did NUSAF staff give you a clear idea of what to expect from the project before activities started?

2013

0.4

5.6

11.2

34.2 35.5

13

0

5

10

15

20

25

30

35

40

45

50

Not at all Lowextent

Someextent

Highextent

Comletely Noanswer

Pe

rce

nt

To what extent has DRC-DDG lived up to commitments?

2013

15

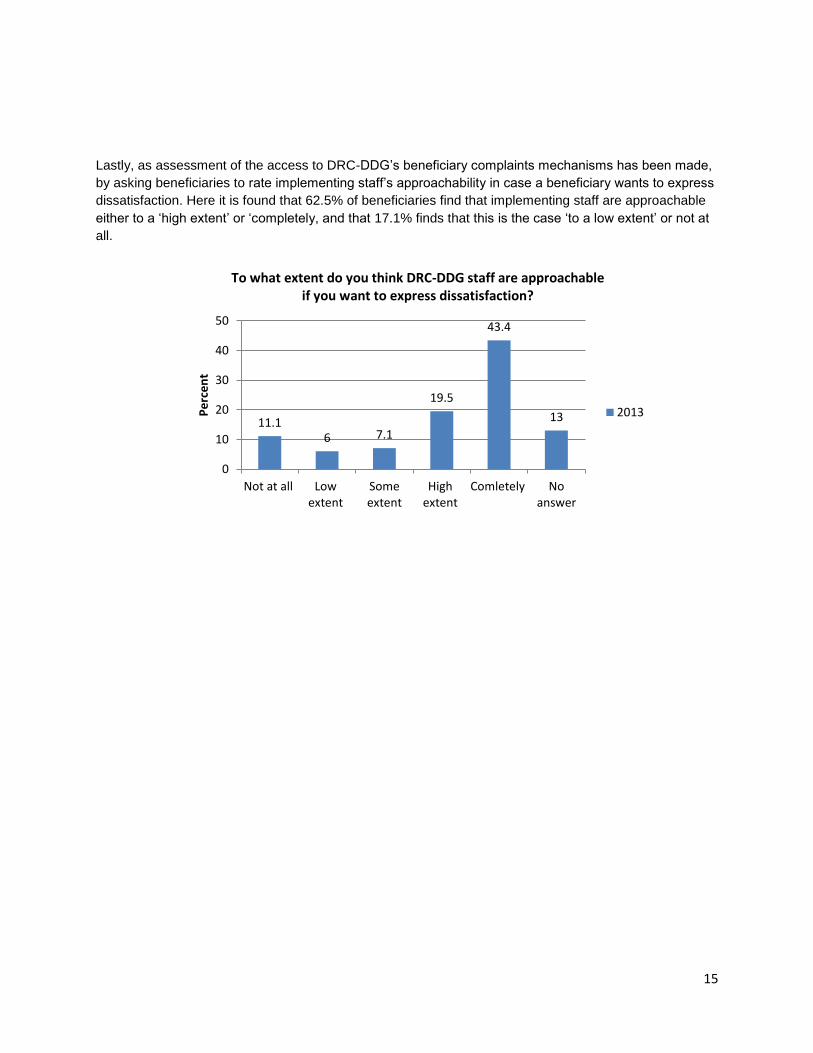

Lastly, as assessment of the access to DRC-DDG’s beneficiary complaints mechanisms has been made,

by asking beneficiaries to rate implementing staff’s approachability in case a beneficiary wants to express

dissatisfaction. Here it is found that 62.5% of beneficiaries find that implementing staff are approachable

either to a ‘high extent’ or ‘completely, and that 17.1% finds that this is the case ‘to a low extent’ or not at

all.

11.1 6 7.1

19.5

43.4

13

0

10

20

30

40

50

Not at all Lowextent

Someextent

Highextent

Comletely Noanswer

Pe

rce

nt

To what extent do you think DRC-DDG staff are approachable if you want to express dissatisfaction?

2013

16

5. Conclusion

In relation to food security, a reduction has been found in the number of people who live on one meal pr.

day. Only a very limited number of households have been faced with starvation in the past 12 months,

and the amount of food available in the households has increased. There has been found increased

dietary diversity and beneficiaries have indicated to experience improved nutrition and health among their

family members. There are, however, still a significant portion of beneficiaries who point at challenges in

ensuring food for all members of the household in the number of meals prepared pr. day.

In relation to household income and economic resilience, there has been found a positive trend in

beneficiaries’ self-assessment of their income situation. In 2013, 47.3% of beneficiaries rate their income

situation as ‘good’ or ‘very good’ There is also a trend towards improved ability to meet basic needs, as it

has been found that 41.4% of beneficiaries state a positive development in this regard. In focus group

discussions, beneficiaries have emphasized that the households are able to access medical care, school

enrollment and purchase of subsidiary food which had been out of reach before.

There has been an increase in the number of persons making savings, and 50% of respondents indicate

to be able to cope with an economic shock for the household.

There has been a significant improvement in market access, and beneficiaries are found to utilize

earnings from Household Income Support Projects (HISP) for investments in small scale business.

Beneficiaries express a high level of satisfaction with the available choices of HISPs, and the quality of

the public works projects has been rated highly by NUSAF2 beneficiaries as well as by other community

members.

There have been identified weaknesses in the information provided to beneficiaries prior to launching of

the project, which DRC-DDG will take into account in the event of leading a community entry process in

the future. Lastly, the majority of beneficiaries find that DRC-DDG has lived out to its commitments in

service delivery in the implementation period.