img technology & corp template - amazon web … · based on increased backlog and active...

TRANSCRIPT

www.imgtec.com

Hossein Yassaie, CEO and Richard Smith, CFO

18th September 2015

AGM 2015

© Imagination Technologies FY15 AGM 18th September 2015 2

FY15 highlights Group

Strong licensing across all IP families

Significant increase in committed SoCs

Operating costs lower than previously guided

Technology

Significant new tier-one deals for PowerVR graphics & MIPS

Encouraging year-on-year MIPS volume growth

Growing momentum for Ensigma

Significant design wins secured for Platform offerings

Pure

Narrower focus in product lines & geographical presence

Improving performance in key markets

Business well positioned for future growth

www.imgtec.com

Richard Smith

CFO

Financial Overview

© Imagination Technologies FY15 AGM 18th September 2015 4

Financial highlights - 1 Technology revenues growing

Licensing: up 2% to £39.0m (FY14: £38.3m)

Royalties: up 9% to £118.9m (FY14: £109m)

Licensing: increased activity across all IP families

121 licenses (FY14: 115) signed across more than 40 partners

52 PowerVR multimedia

47 MIPS processor

15 Ensigma communications

7 System level/support IP (including FlowCloud, VoIP and Caskeid)

Platform IP capability gaining traction and fuelling momentum

© Imagination Technologies FY15 AGM 18th September 2015 5

Financial highlights - 2 Shipments: 1,327m units (FY14: 1,259m)

Non-MIPS: 530m (FY14: 530m)

MIPS: up 9% to 797m (FY14: 729m)

Stronger average royalty rate on both non-MIPS and MIPS unit shipments due to mix

Operating expenses

Underlying operating expenses tightly controlled

Better than guidance, with growth of only 9% for the full year

Foreign exchange

The average USD foreign exchange rate has been broadly neutral from FY14 to FY15

© Imagination Technologies FY15 AGM 18th September 2015 6

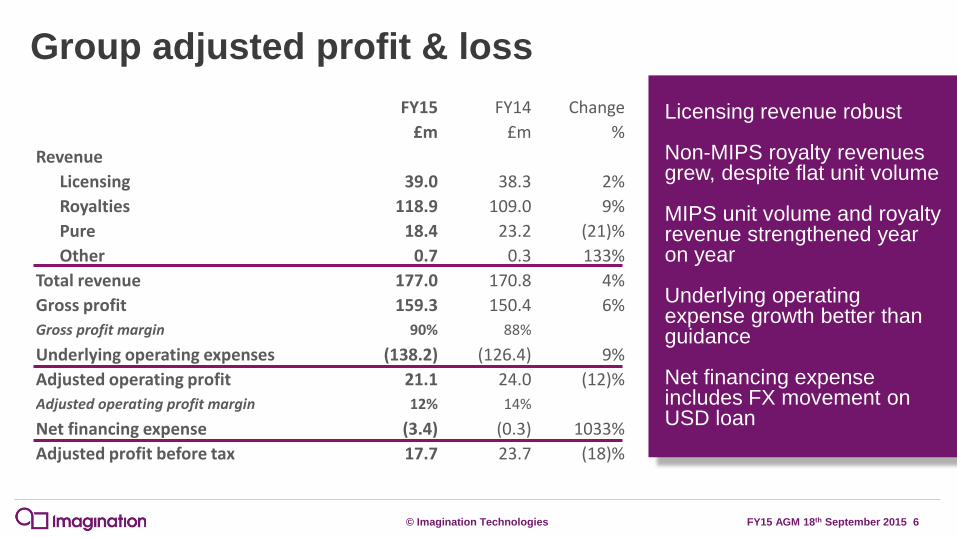

Group adjusted profit & loss

FY15 FY14 Change

£m £m %

Revenue

Licensing 39.0 38.3 2%

Royalties 118.9 109.0 9%

Pure 18.4 23.2 (21)%

Other 0.7 0.3 133%

Total revenue 177.0 170.8 4%

Gross profit 159.3 150.4 6%

Gross profit margin 90% 88%

Underlying operating expenses (138.2) (126.4) 9%

Adjusted operating profit 21.1 24.0 (12)%

Adjusted operating profit margin 12% 14%

Net financing expense (3.4) (0.3) 1033%

Adjusted profit before tax 17.7 23.7 (18)%

Licensing revenue robust Non-MIPS royalty revenues grew, despite flat unit volume MIPS unit volume and royalty revenue strengthened year on year Underlying operating expense growth better than guidance Net financing expense includes FX movement on USD loan

© Imagination Technologies FY15 AGM 18th September 2015 7

Technology business

£m

£5m

£10m

£15m

£20m

£25m

£30m

£35m

£40m

£45m

FY11 FY12 FY13 FY14 FY15

Licensing

£m

£20m

£40m

£60m

£80m

£100m

£120m

£140m

FY11 FY12 FY13 FY14 FY15

Royalties

£m

£50m

£100m

£150m

£200m

FY11 FY12 FY13 FY14 FY15

Revenue

Royalties Licensing Other

0

200

400

600

800

1000

1200

1400

FY11 FY12 FY13 FY14 FY15

Unit v

olu

me

in

mill

ion

s

Units

Non-MIPS MIPS

Licensing: strongest

year despite lower

growth than expected

Units: strong growth

in MIPS; stable

non-MIPS

Royalties: solid

growth in royalty

revenues driven by

volume and mix

© Imagination Technologies FY15 AGM 18th September 2015 8

Pure

FY15 FY14 Change

£m £m %

Revenue 18.4 23.2 (21)%

Adjusted operating loss (6.0) (7.4) (19)%

Improved focus:

Areas of strategic interest

Products & geographical

regions

Markets & products with

better returns

Revenue reduced but

improved profitability

© Imagination Technologies FY15 AGM 18th September 2015 9

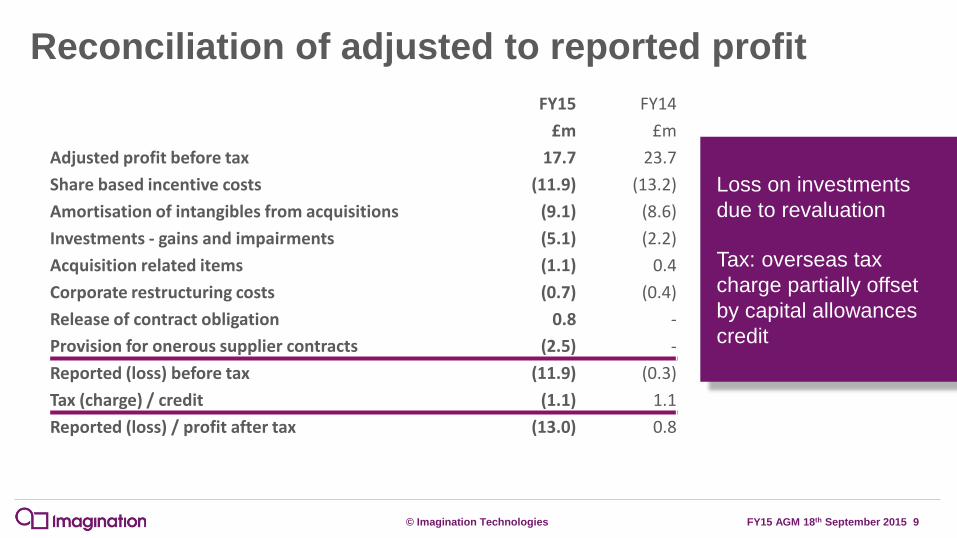

Reconciliation of adjusted to reported profit

FY15 FY14

£m £m

Adjusted profit before tax 17.7 23.7

Share based incentive costs (11.9) (13.2)

Amortisation of intangibles from acquisitions (9.1) (8.6)

Investments - gains and impairments (5.1) (2.2)

Acquisition related items (1.1) 0.4

Corporate restructuring costs (0.7) (0.4)

Release of contract obligation 0.8 -

Provision for onerous supplier contracts (2.5) -

Reported (loss) before tax (11.9) (0.3)

Tax (charge) / credit (1.1) 1.1

Reported (loss) / profit after tax (13.0) 0.8

Loss on investments

due to revaluation

Tax: overseas tax

charge partially offset

by capital allowances

credit

© Imagination Technologies FY15 AGM 18th September 2015 10

Group cash flow

FY15 FY14

£m £m

Adjusted profit before tax 17.7 23.7

Depreciation 8.2 5.8

Other (1.2) (1.6)

Operating cashflows before working capital 24.7 27.9

Working capital (28.8) 6.0

Cash generated by operations (4.1) 33.9

Interest (0.5) (0.6)

Tax (1.2) (58.4)

Net cashflows from operating activities (5.8) (25.1)

Cash flows from Investing activities (15.0) (27.2)

Cash flows from Financing activities 3.4 (5.3)

Net (decrease)/increase in cash (17.4) (57.6)

Effect of exchange rate fluctuation 0.9 0.2

Opening cash position 19.2 76.6

Closing cash position 2.7 19.2

£25m operating cashflow Working capital movements due to timing of royalty receipts – reflected in debtors at year end Capital expenditure primarily related to the redevelopment of property Over £60m of property assets (offices and data centre) Short term utilisation of RCF over period end to cover timing of royalty receipts

© Imagination Technologies FY15 AGM 18th September 2015 11

FY16 outlook as at 30th June Licensing

Based on increased backlog and active pipeline of prospects,

target of 10% growth in licensing revenue in FY16

As usual dependent on timing of partners’ activities

Royalties

Expect growth in unit shipments and royalty revenue

Pure

Expect continued improvement in financial performance from refocus and operational

changes already implemented

Operating margin & expenses

Expansion of operating margins in medium-term with longer-term target of 30% - 40%,

with a rise in profitability in FY16

Full year operating expenses growth target in the range of 5% - 10%

© Imagination Technologies FY15 AGM 18th September 2015 12

Summary of Interim Update Licensing:

Steady start to the year

Increase in overall pipeline

Holding guidance at this stage

Royalties:

June quarter impacted by overall slowdown in semi industry and customer-

specific ramp down timing

Strong recent and ongoing design wins expected to create significant added

momentum in mid-term unit shipments

Pure:

In line with expectations

Operating costs:

Tightly managed; marginally lower than expectations

Overall H1 looking weaker, but H2 expected to be stronger than previously expected

www.imgtec.com

Business and Market Environment

Hossein Yassaie, CEO

© Imagination Technologies FY15 AGM 18th September 2015 14

Market opportunities evolving & emerging Existing markets growing & changing

Mobile phones and computing => maturity, low-end shifting up

Home consumer => connected devices, connected consumers

Enterprise and networking => ubiquitous connectivity,

heterogeneous compute

Automotive => connected, advanced automotive

New markets emerging – no established players

Wearables

IoT: health, energy, agriculture; transport; retail; security; toys

Automation & robotics

VR (Virtual Reality) & AR (Augmented Reality) becoming significant

Real-time and big data analytics SoCs remain the key enablers

System know-how the key differentiator

Products + cloud services are disruptive combinations

© Imagination Technologies FY15 AGM 18th September 2015 15

Mega societal changes underway The arrival of the emerging world

China, India, Brazil - size matters

More consumers but also more competitors

The connected and accessible world => one market

Accelerating technological possibilities in many fields

IoT, robotics/automation, biomedical etc - even bigger than Internet

Global warming and the need for efficiency and conservation

Manufacturing returning to local markets in many sectors

The rise of the middle-class world and people’s expectations

Towards 100+ year human life spans and changing demographics

Today’s infrastructure cannot cope with tomorrow’s population’s needs

© Imagination Technologies FY15 AGM 18th September 2015 16

The semiconductor world is changing

Consolidation in established markets

Mostly in West and Japan

Largely driven by mobile market consolidation

Rapid rise of players in emerging economies

Western companies investing in eastern partners

Trend towards OEM verticalisation in several markets

Driven by SoC-level differentiation

New semis even closer to applications

Have to become much more than just a semi

Picture of change

Flags of China, TW

© Imagination Technologies FY15 AGM 18th September 2015 17

The developing landscape: four types of “semi” players

1. The super-high volume (SoC) semi Supporting large mainstream segments, driven by mobile

SoC capability and/or proprietary architecture driven

2. The market focused, specialised semi Smaller and operating closer to more specialised applications

Auto, Health, Home Automation, Industrial/Enterprise, …

3. The vertical major OEM brand with internal semi SoCs + Cloud are key enablers & differentiators

Branded products covering multiple segments

4. The “partnership” vertical OEM, Service Provider, Brand Replicating vertical model (category 3) but through partnership

Custom SoC => an enabler and a differentiator

Medium to large scale

© Imagination Technologies FY15 AGM 18th September 2015 18

IoT - very large but fragmented

The breadth of applications means no one

player will dominate

Tier-one “walled garden” communities will be

first to develop and service adjacent markets

Service level interoperability and security will

be real growth enablers

Ecosystems of many different skills will be

essential to create solutions that really work

Still early stage - too much re-branding of

existing technologies and products as “IoT”

Both open communities and walled gardens

IoT - in reality not one market

© Imagination Technologies FY15 AGM 18th September 2015 19

Security is another fundamental hurdle Every application has security demands

Fundamental to all connected devices (including IoT)

Today’s solutions simply don’t meet users and

application needs

Simplistic “binary in/out” model no longer good enough

Since so many don’t understand it, most copy others

who claim they do

We need universal solutions to security

Heterogeneous - goes across every processing element

in the SoC

Multi-domain for multiple co-existing apps

Multi-domain, system-wide security will become a must

www.imgtec.com

Business update

© Imagination Technologies FY15 AGM 18th September 2015 21

IoT – where we can make a real difference

We see three main levels:

Sensor hubs (application specific)

Sensor hubs + audio/voice

Sensor hubs + audio/voice + smart vision

Biggest impact where solutions address major societal issues

Health

Energy Transport

Infrastructure Security

&Safety

Retail

Agriculture

Our silicon IP portfolio addresses the

needs of all of these key markets

Connected processors central to all hubs

Smart cameras & audio demand

complex local processing

GPU

Video

Camera ISP

+ S

ma

rt v

isio

n

Audio + A

ud

io/v

oic

e

RPU

CPU

Co

nn

ec

ted

P

roc

es

so

r

© Imagination Technologies FY15 AGM 18th September 2015 22

Enabling IoT solutions

SensorHub

Flo

wR

adio

Flo

wTalk

3rd P

arty

FlowCloud

M2M Services

• Registration

• Device Mgt

• Device History

• Event History

• Device App logs

• Authentication

• Authorisation

• Storage

• Device Messaging

PaaS using open source framework

Software as a Service

Service Market place

Built in metering

Subscription plans

Devices IoT Applications (SaaS)

• Wi-Fi

• BT / BTLE

• 6LowPan

• Thread

• Brillo

• OpenWRT

Sensors 3rd P

arty

3rd Party

© Imagination Technologies FY15 AGM 18th September 2015 23

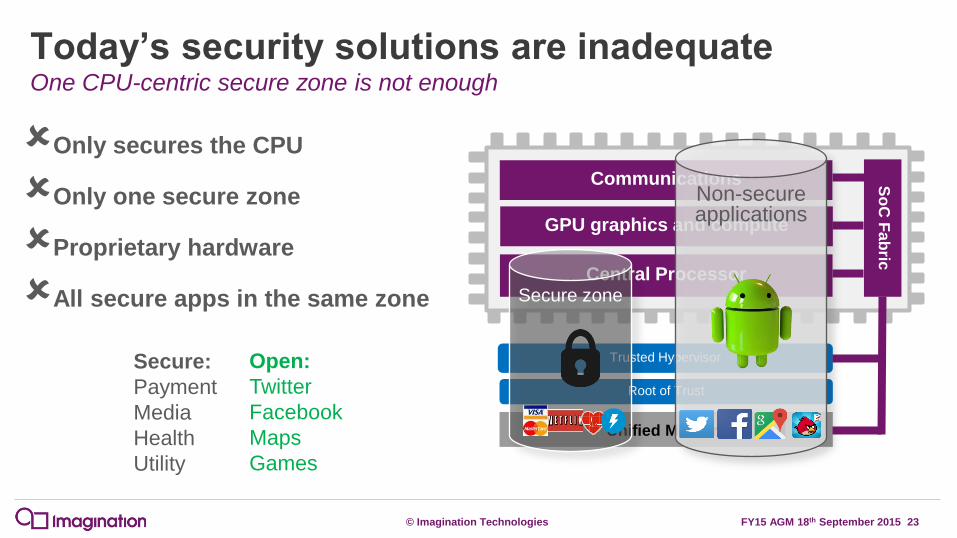

Today’s security solutions are inadequate

Only secures the CPU

Only one secure zone

Proprietary hardware

All secure apps in the same zone

One CPU-centric secure zone is not enough

Trusted Hypervisor

Unified Memory

Root of Trust

Communications

GPU graphics and compute

Central Processor

So

C F

ab

ric

Secure:

Payment

Media

Health

Utility

Secure zone

Open:

Maps

Games

Non-secure applications

© Imagination Technologies FY15 AGM 18th September 2015 24

OmniShield™ redefines the future

Multi-domain: up to 255 containers

Heterogeneous: CPU GPU, RPU

Hardware separation: virtualisation

Open: prpl Security PEG

Multi-domain, heterogeneous, hardware separation

Trusted Hypervisor

Unified Memory

Root of Trust

Communications

GPU graphics and compute

Central Processor

So

C F

ab

ric

Secure:

Payment

Media

Health

Utility

Open:

Maps

Games

Non-secure applications

© Imagination Technologies FY15 AGM 18th September 2015 25

Helping our customers leverage their know-how

Domain Solutions Customer

technologies & know-how

Customizable IP platforms Ecosystems

software, tools, apps, middleware, hardware

Scalable IP

PowerVR Multimedia

Networking Enterprise IoT Smart Home

Connected Cars

Wearables Mobile

© Imagination Technologies FY15 AGM 18th September 2015 26

PowerVR multimedia Graphics, Video & Vision Processor IP families

Significant & growing market

1bn+ growing to >5bn

Clear leadership in mobile graphics for mid-high end;

growing in the low end

Series7: starting volume production

Series8: in an advanced development stage; strong customer interest

No 1 supplier for automotive dashboard display

Significant and growing volume in TV/STB

Strong volume in video including 4K

Continuing to innovate

GPU compute, VR, AR, ray tracing, computer vision

Ray Tracing reference chip in the lab; initial tests promising

Vision IP Platform: strategic and significant

Acknowledged technology &

industry leaders

© Imagination Technologies FY15 AGM 18th September 2015 27

MIPS processors Strategy since acquisition:

Existing customers: networking & digital home

Reassured and relationships strengthening

Mobile: new market wins

Secured strategic design win for embedded processing in mobile SoCs

App processing opening up as ISA dependency a non-issue medium-term

Automotive: MobilEye leading ADAS supplier – MIPS-based

Embedded: Microchip key player in IoT, 32-bit MCUs

Customers acknowledging commitment of Imagination

Tier-ones see MIPS as strategic; new key multi-year design win

Shipment strength continues across markets

Strong technology with compelling roadmap

Strong line-up from micro-controllers to 64-bit => real choice

Multi-threading & OmniShield => differentiation in many markets

The industry’s much-needed

& welcomed choice

© Imagination Technologies FY15 AGM 18th September 2015 28

Promoting MIPS in Silicon Valley

© Imagination Technologies FY15 AGM 18th September 2015 29

Ensigma communications

Efficient & scalable comms IP family

Explorer RPUs for highest performance Wi-Fi & BT

Wi-Fi 2x2ac now in production in partner’s products

New Whisper RPU cores targeting ultra-low power for

IoT and wearables

Uniquely positioned for the industry’s

transition to integrated comms IP

Similar transition to that we saw in graphics

Complete end-to-end solution

Software to antenna

Industry’s largest centre of excellence

~ 200 engineers focussed on connectivity IP

10+ licensees & growing

Several entering production in 2015

A massive opportunity as

connectivity transitions to IP

© Imagination Technologies FY15 AGM 18th September 2015 30

IP platforms: addressing the emerging demand Pre-verified solutions - enabling the next wave of innovation

Customisable

IP Platforms

Differentiated

Customer SoC

Optimal OEM

products Scalable IP

PowerVR graphics

MIPS processors

Ensigma communications

PowerVR video

PowerVR vision

Scala

ble

& S

ecure

Fabric

Graphics & GPU Compute

Video decode & encode

Wi-Fi, BT TV, Radio

CPU processors

Camera ISP

Peripheral IP

Pre-verified baseline SW

Unique SoC

Domain know-how

Fa

bric

VDE

CPU VPU

Peripherals

Baseline SW

Customer IP

RPU GPU

3rd party SW

Partner SW

© Imagination Technologies FY15 AGM 18th September 2015 31

Focusing on the essentials Significant operational changes; improving financials

Losses reduced and key trends look encouraging

Using DAB line-up and brand to drive adoption

Extensive new product line-up announced at IFA:

- Evoke F3 with BT and Spotify; new One range; Siesta Rise

bedside radio; Evoke C-series all-in-one home audio systems

Targeting international consumer & automotive markets

Driving connectivity (Wi-Fi for internet radio, BT for streaming)

Strategic support for key technologies and partnerships

E.g. wireless speakers including multi-channel and IoT

Have revised partnership model for music service to optimise cost

Engineering supporting technology ecosystem growth

Supporting IP business for Creator Ci20, Caskeid, …

© Imagination Technologies FY15 AGM 18th September 2015 32

Leverage & profitability

Imagination’s operating margin expansion

Planned strategic investment in complementary

technologies =>impacted short-term margin

All planned product lines are now in place

=> we’re at the end of major new investments

All business units either already in or entering revenue

generation

Ongoing tight & systematic control of Opex

– now sub 10%

Margin expansion => longer term goal 30%-40% FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20

Time

Develop-ment

Market Entry

Maturity Research Phase

£m

PowerVR

Ensigma

MIPS

IP product profitability profile

Long investment cycle

Slow initial revenue ramp (licensing only)

Accelerated later royalty + licensing ramp

© Imagination Technologies FY15 AGM 18th September 2015 33

Summary Technology

Strong and comprehensive range of IP addressing all target applications

Solution-centric IP platforms that efficiently address the needs of all customers

Well aligned with the trends in the market and opportunities

Pure

Business rationalised and focussed on areas of strategic & financial significance

Group

Many opportunities and active licensing engagements across all IP families

Some short-term softness in customer unit shipments but expect growing momentum for

mid-term

Leverage within the business model will enable expansion of operating margins with a

long-term steady state of 30%-40%

Business well positioned for future growth

www.imgtec.com

Q&A