ile' philippines agricultural credit sector...

TRANSCRIPT

Report No. 4117-PH ILE' COy

PhilippinesAgricultural Credit Sector Review

May 12, 1983

Projects DepartmentEast Asia and Pacific Regional Office

FOR OFFICIAL USE ONLY

(N&H

Document of the World Bank

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. Its contents may not otherwisebe disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Currency Unit = Peso (P)IF 1.00 = US$ 0.12US$1.00 = P 8.3P 1,000,000 = US$120,000

WEIGHTS AND MEASURES

1 hectare (ha) = 2.47 acres1 kilometer (km) = 0.62 miles1 metric ton (m ton) = 2,204.6 pounds1 kilogram (kg) = 2.2 pounds1 cavan rice = 50 kg20 cavans rice = 1 m ton

ABBREVIATIONS AND ACRONYMS

ACA - Agricultural Credit AdministrationACCFA - Agricultural Credit and Cooperative Financing AdministrationALF - Agricultural Loan FundAMC - Area Marketing CooperativeBOCD - Bureau of Cooperative DevelopmentCB - Central Bank of the PhilippinesCF - Compact FarmCFC - Compact Farm ClustersCRB - Cooperative Rural BankDBP - Development Bank of the PhilippinesDRBSLA - Department of Rural Banks and Savings and Loan AssociationsFMG - Farm Management GroupFSDC - Farm Systems Development CorporationGSIS - Government Service Insurance SystemIEDP - Integrated Estate Development ProgramKB - Commercial BankLBP - Land Bank of the PhilippinesM-99 - Masagana 99MAR - Ministry of Agrarian ReformMLG - Ministry of Local GovernmentMOA - Ministry of AgricultureMNR - Ministry of Natural ResourcesMPWH - Ministry of Public Works and HighwaysNEDA - National Economic and Development AuthorityNFA - National Food AuthorityNIA - National Irrigation AdministrationNIDC - National Investment and Development CorporationPAB - Philippine Amanah BankPCA - Philippine Coconut AuthorityPCAC - Presidential Committee on Agricultural CreditPCI - Philippine Commercial and Industrial BankPDB - Private Development BankPFMG - Professional Farm Management GroupPHILSUCOM - Philippine Sugar CommissionPNB - Philippine National BankRB - Rural BankRDC - Regional Development CouncilRPB - Republic Planters BankSLA - Savings and Loan AssociationSMB - Savings and Mortgage BankSN - Samahang Nayon (Village Cooperatives)SSS - Social Security SystemTBAC - Technical Board for Agricultural CreditUCPB - United Coconut Planters' Bank

FOR OFFICIAL USE ONLY

PHILIPPINES

AGRICULTURAL CREDIT SECTOR REVIEW

PREFACE

This report, based on the findings of a mission which visited the

Philippines in March 1982, reviews the major issues affecting agricultural

credit and makes recommendations on policy and institutional changes to

address these problems. The review was undertaken in view of the serious

problems of arrearages that have emerged in the Bank-assisted credit

projects and Government-financed agricultural credit programs, and the weak

financial condition of many banks engaged in agricultural credit activities.

A major concern was to identify the causes which make agricultural financial

intermediaries excessively reliant on government resources and subsidies for

continued agricultural lending. The draft of this report was discussed with

the Technical Board for Agricultural Credit and the Presidential Committee

on Agricultural Credit during November and December 1982. The comments

received have been appropriately incorporated in the final report. The

report is intended to provide the basis for a continuing Bank-Government

dialogue on appropriate action to strengthen the country-s agricultural

credit system and policies.

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

PHILIPPINES

AGRICULTURAL CREDIT SECTOR REVIEW

Table of Contents

Page No.PREFACE

SUMMARY AND RECOMMENDATIONS ....... ........... i-v

1. THE RURAL SECTOR .1.. . . . . . . . . . . . . . . . . . . . . I

A. Dimensions .1... . . . . . . . . . . . . . . . . . . IB. Composition of the Rural Economy ... . . . . . . . . . . 2C. Agricultural Performance . . . . . . . . . . . . . . . . . 3

2. THE RURAL FINANCIAL MARKET: INSTITUTIONAL ANDNONINSTITUTIONAL ARRANGEMENTS. 6

A. Introduction. 6B. Organization of the Rural Institutional Financial Market . 6C. Noninstitutional Credit Arrangements ... . . . . . . . . 17

3. MAJOR TRENDS IN AGRICULTURAL CREDIT ... . . .... . . . . . 24

A. Introduction .... . . . . . . . . . . . . . . . . . . . 24B. Trends . .. . . . . . . . . . . . . . . . . . . . . . . . 25

- Increased Use of Noninstitutional Credit .25- Trends in Institutional Credit . . . . . . . . . . . . . 25- Mediur- and Long-term Credit ... . . . . . . . . . . . 29- Resource Mobilization ... . . . . . . . . . . . . . . 29

4. GOVERNMENT POLICIES AND PROGRAMS FOR AGRICULTURALCREDIT .... . . . . . . . . . . . . . . . . . . . . . . . 33

A. Introduction .... . . . . . . . . . . . . . . . . . . . 33B. Credit and Extension Programs for Commodity Production . 33C. Agricultural Credit Quota Policy ... . . . . . . . . . . 37D. Agricultural Loan Guarantee Scheme and Crop Insurance . . 38E. Low Interest Rates ... . . . . . . . . . . . . . . . . . 42F. Government Subsidies ... . . . . . . . . . . . . . . . . 45

5. GOVERNMENT AGRICULTURAL POLICIES, PROGRAMS AND INSTI-TUTIONS: THEIR EFFECTS ON AGRICULTURAL INVESTMENT . . . . . 47

A. Introduction .47B. Tenurial Reforms .47

This report was prepared by a review mission which visited the Philippinesin March 1982. The mission consisted of Ramesh Deshpande, J.D. Von Pischke,Robert Hindle, John Macgregor (Bank), and Parviz Maleki and Loretta Sonn(FAO/CP). P. Brereton (Bank) assisted in preparing the report.

2-

Page No.

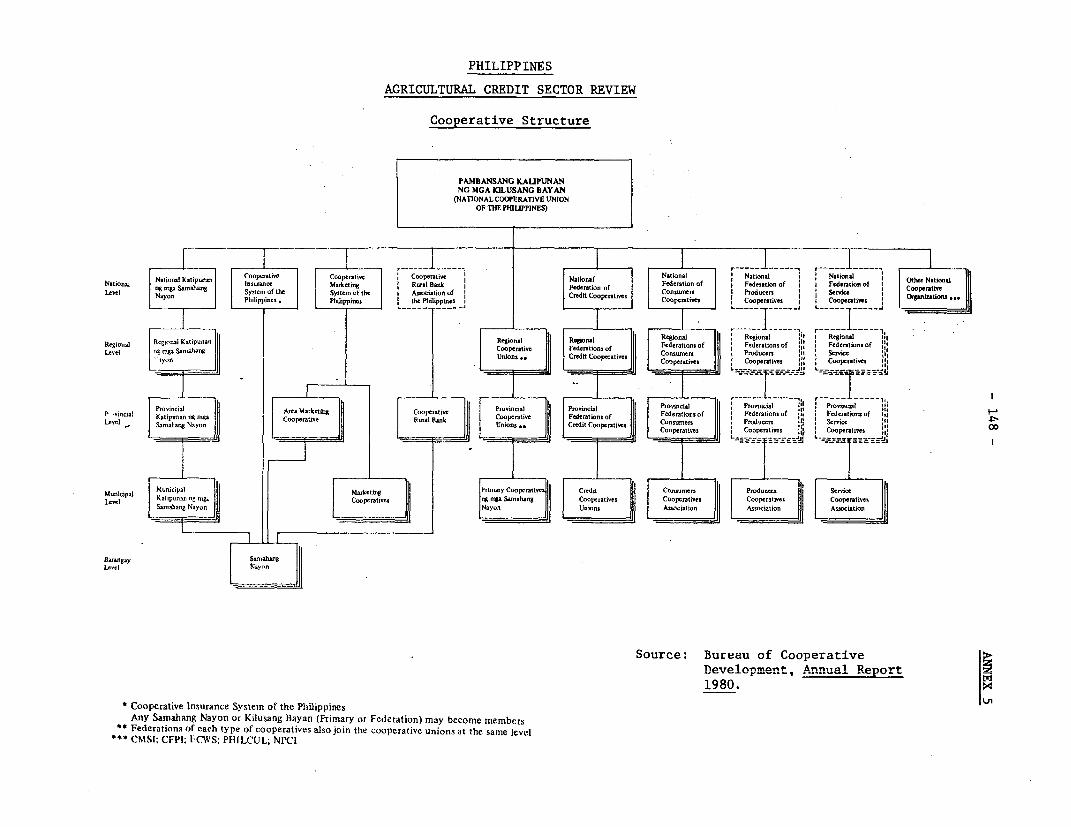

C. Support Services . . . . . . . . . . . . . . . . . . . . . 49D. Marketing and Pricing Policies . . . . . . . . . . . . . . 52E. Cooperatives . . . . . . . . . . . . . . . . . . . . . . . 54F. Administrative Organization . . . . . . . . . . . . . . . . 57

6. THE STATUS OF MAJOR INSTITUTIONS IN THE RURAL FINANCIALSECTOR . . . . . . . . 6 . . . . . . . . . . . . . . . . . . 62

A. Philippine National Bank . . . . . . . . . . . . . . . . . 62B. Land Bank of the Philippines . . . . . . . . . . . . . . 65C. Agricultural Credit Administration . . . . . . . . . . . . 69D. Development Bank of the Philippines . . . . . . . . . . . . 71E. Private Commercial Banks . . . . . . . . . . . . . . . . . 77F. The Rural Banking System.. . . . . . 78G. Thrift Banks . . . . . . . . . . . . . . . . . . . 84H. Cooperative Rural Banks .. . . . . . ....... 85I. Institutional Performance in World Bank-assisted Credit

Projects . . . . . . . . . . . . . . . . . . . . . . . 86

7. SUMMARY OVERVIEW, AND A SUGGESTED ACTION PROGRAM . . . . . . . 89

A. Overview . . . . . . . . . . . . . . . . . . . . . . . . . 89B. Problems in Agricultural Credit . . . . . . . . . 91C. An Action Program . . . . . . . . . . . . . . . . . . . . . 98

STATISTICAL ANNEXES . . . . . . . . . . . . . . . . . . . . . . . . 113

TABLES IN TEXT

Table 2.1: Structure of Financial System, 1980 . . . . . . 8Table 2.2: Number of Financial Institutions in

Operation, 1975-80 . . . . . . . . . . . . . 9Table 2.3: Formal Institutions in Rural Financial

Market . .. . . . . . . . . . . . . . 12Table 2.4: Agricultural Loans Granted, by Bank . . . . . . 14Table 2.5: Agricultural Loans as a Percent of

Total Loans, by Bank . . . . . .. . . . . . 15Table 3.1: Composition of Institutional and

Noninstitutional Credit to Agriculture . 25Table 3.2: Agricultural Loans Granted

by Activity, 1972-75 . . . . . . . . . . . . 26Table 3.3: Agricultural Loans Granted, 1975-80 . .27

Table 3.4: Agricultural Loans Granted by Activity,1975-80 . .. . . . . . . . . . . . . . . . 28

Table 4.1: Coverage and Payments of Loan Guarantee Funds . 39Table 4.2: Crop Insurance Premium Rates . . . . . . . . . 40Table 6.1: Agricultural Production Loans Granted by

PNB, 1975-81 . . . . . . . . . . . . . . . . 63Table 6.2: LBP: Agricultural Loans Granted . . . . . . . 66Table 6.3: DBP: Agricultural Loan Approvals . . . . .. 72Table 6.4: DBP: Agricualtural Loan Approvals by Activity 74Table 6.5: DBP's Margin on Agricultural Lending . . . 76Table 6.6: Rural Banks Arrearages under Central

Bank Loans, Septemer/December 1981 .81

- i-

SUMMARY AND RECOMMENDATIONS

1. During the past decade or so, the Philippines- agricultural sectorhas made impressive gains. Overall output has grown at an average rate of4.9% p.a. and the country has achieved self-sufficiency in rice production.The Government has introduced a number of new credit policies and programs tosupport its production objectives, and these have made important contributionsto the sector-s production achievements. As a result of greatly expandedcrop-specific credit programs, made available through a growing network ofgovernment and private banks, many more farmers found themselves able to takeadvantage of the greater opportunities provided by the Government's owninfrastructure investments and by improved extension services. Althoughcredit for medium and longer-term purposes did not expand much, productioncredit grew rapidly throughout the 1970s. Continued growth of theagricultural sector remains crucial for the future of the economy and for the46% of the population who are farmers. The growing availability of credit,for various terms and purposes will be essential to agricultural growth.

2. Despite the strong performance of agriculture during the 1970s, andthe support provided by rural credit institutions over many of those years,the present condition of the rural credit markets is far from healthy. Alarge number of the loans made by both government and private banks havefallen into arrears, disqualifying many borrowers from further loans anddisqualifying the banks from use of discount privileges at the Central Bank(CB). These twin constraints have caused the proportion of institutionalcredit, which rose to 68% in the mid-seventies when the government-sponsoredsupervised credit programs were in full swing (1975), to fall back to only 32%in late 1970s. Currently about two-thirds of all agricultural credit is beingprovided by informal or non-institutional sources -- relatives, friends,traders, landlords, and professional moneylenders. Noninstitutional creditusually costs more than institutional credit, and is generally not availablefor medium- and longer-term loans. In 1980, 98% of bank credit was forshort-term use, i.e., for loans that had to be repaid within 12 months.

3. The unhealthy state into which rural credit institutions have fallenhas not only reduced credit availability but has threatened the viability ofmany of the institutions, both public and private. The Government's majorterm lending institution, the Development Bank of the Philippines (DBP), hasarrears of + 1.1 billion or 65% of the amount due for repayment (para.6.39). The Philippine National Bank (PNB), a government commercial bank, hasarrears of nearly P 200 million (para. 6.06). The privately owned ruralbanks have arrears of over P 1 billion owed to the CB, disqualifying aboutone half of 1,041 banks from further access to rediscounting facilities. Muchof the serious arrearage problem has arisen in the Government-sponsoredsupervised credit programs designed to achieve production targets for specificcrops. Supervised credit does not require collateral, and the drying up ofit has caused a shift towards nonsupervised credit, which almost always

- fi -

requires collateral. However, even the performance of non-supervised creditprograms, which provide collateralized loans to farmers and commercialentrepreneurs in relatively high income groups, has not been satisfactorybecause of low subloan collections. A large proportion of small farmers haveno collateral to offer, partly because the land reform program has movedslowly and has not yet given many farmers clear land titles. Thesedevelopments also underlie the return to much greater reliance onnoninstitutional credit.

4. Apart from arrearages the rural credit system has many otherweaknesses that need attention. Some of the more important weaknesses arenoted below:

(a) Rural financial institutions have typically specializedtheir functions, and this has inhibited efficient financialintermediation, led to high transaction costs and a limitedspread of risk, and restricted the range of banking servicesavailable to farmers. Examples of functional specializationrelate to the type of clientele served (small vs. largerfarmers), length of loan (short vs. long-term), type of commodityfinanced (coconut, sugar, etc.) and activity financed(production, marketing or processing). Rural banks, PNB, theLand Bank of the Philippines (LBP), and the Agricultural CreditAdministration (ACA) support smallholder rice and corn productionwhile private commercial banks, DBP and PDBs finance only aselective clientele, usually medium- and large-scale borrowers.

(b) Although there has been a considerable expansion of ruralbanking facilities during the past decade, the country'sbanking system is still highly urban-oriented, leavingmany rural areas seriously "under-banked."

(c) The banking system has not been fully successful in tapping therural savings potential. Although the limited network of ruralcredit institutions partly explains the low mobilization rate, amore important reason has been the government's low interestrate policy which was not adequate to attract larger savings.With inadequate deposits to finance their lending, and lowinterest rates on agricultural loans, rural credit institutionshave had to rely heavily on low-cost funds provided byGovernment.

- iii -

(d) The transaction costs of banks handling supervised credithave been high, despite access to low-cost funds throughCB rediscounting. The transaction costs include not onlyadministrative costs (4.5-6.0%) but compulsory insurancepremiums (3%) and the cost of carrying past due loans (4%for rural banks, 12% for PNB). With lending rates regulatedat 12% (15% for corn), many banks found supervised creditlending unprofitable. From the farmers viewpoint, a 12-15%interest cost was not in fact their full borrowing cost: tothis had to be added a 2% service charge, a 3% charge forcompulsory deposits in the Barrio Saving Fund (sincediscontinued), plus a transaction charge of 3%. For manyfarmers, these and other costs have pushed the cost ofinstitutional credit close to that of informal credit, whichis often easier to arrange.

5. A 1980 joint IMF/World Bank review of the Philippine financialsector led the Government to introduce a set of reforms that had two mainobjectives, (a) increased competition among financial institutions to achievegreater efficiency and (b) the greater availability of longer-term credit.One major change designed to help achieve these aims was the deregulation ofinterest rates on both deposits and loans, excluding agricultural loansrefinanced by CB. The benefits of liberalization are unlikely to be felt inagriculture until remedial measures are taken to overcome the difficultiesthat are now preventing rural credit institutions from giving farmers the helpthey need.

Recommendations

6. Chapter 7 of the report suggests an Action Program to nurse therural credit markets back to health. There are three broad sets of problemsthat need to be addressed: (a) limitations on the supply of formal credit tofarmers; (b) institutional weaknesses; and (c) deficiencies in governmentpolicies affecting agricultural credit. The principal means proposed foraddressing these problems are:

(a) Fostering greater competition between formal and informallenders;

(b) Completing the deregulation of interest rates in order topromote greater deposit mobilization in rural areas and theuse of deposit resources for agricultural lending;

(c) Rationalizing and, in phases, eliminating credit subsidies;

- iv -

(d) Increasing the efficiency of the rural financial marketsthrough functional de-specialization and the financialrehabilitation of DBP and the private and cooperativerural banks; increased participation of commercial banksand savings and mortgage banks in agricultural lending,especially for medium- and long-term credit; and animproved field-level credit-delivery mechanism, includingthe strengthening of village cooperatives; and

(e) Establishing an agency or mechanism to support retaillending agencies and to coordinate their agriculturalcredit activities.

Implementation of these objectives will require a number of initiatives by theGovernment, including agreement on flexible interest rate policies for thesector, changes in the corporate policies of some banks, a realistic resolu-tion of the problem concerning the large volume of uncollectable debts, andthe creation of a new central mechanism to support retail lending institu-tions. Equally important will be agricultural pricing policies which will, asearly as feasible, turn the terms of trade in favor of agriculture, withemphasis on benefiting the productive activities of small farmers. Some ofthese steps must be taken promptly, but the creation of a sound system ofrural credit will require various actions extending over several years.

1. THE RURAL SECTOR

A. Dimensions

1.01 Agriculture, including forestry and fisheries, plays a dominantrole in the Philippine economy. The country's population is predominantlyrural, with about 70% (34 million people) living in rural areas, two thirdsof whom depend on farming for their livelihood. Over all, more than half ofthe labor force are engaged in agricultural activities. Agricultureproduces about 26% of gross domestic product (GDP) and 60% of aggregateexport receipts.

1.02 Of the total land area of 30 million ha, about 28% is cultivated./INearly three fourths of this is devoted to grains, essentially rice andcorn. Other important crops are coconut, sugarcane, fiber crops, pineapple,banana and tobacco. Almost all of the irrigated area, estimated at 1.2million ha, is planted to rice; rainfed agriculture, which sustains 60% ofthe total farm population, is dominated by mixed farming systems where rice,corn and coconut are grown together with livestock raising.

1.03 The rural scene is characterized by small units farmed by tenantfamilies. The Agricultural Census of 1971 estimated the total number offarm holdings at 2.35 million, 85% of which were less than 5 ha. Theaverage farm size was 3.6 ha for all commodities, 2.7 ha for palay and13.6 ha for sugar. Due to population growth and inheritance customs, theaverage farm may now be even smaller, probably about 2.7 ha, and fragmented.

1.04 Farm productivity is generally low and, combined with landscarcity and the fact that most of the non-marginal lands are already undercultivation, results in low incomes. In 1971, the average family income inrural areas was about P 4,400 (US$580), representing 75% of the nationalaverage. According to the World Bank's 1980 Poverty Report,/2 aboutthree quarters of the poorest 40% of all Filipino families in the 1970slived in rural areas, with per capita incomes equivalent to the 1975 povertyline of P 827 (US$110) /3 or less. While farm size was the most

/1 Effective harvested area is larger due to multiple cropping.

/2 World Bank, "Aspects of Poverty in the Philippines: A Review andAssessment," Report No. 2984-PH, December 1, 1980.

/3 P 1,103 (US$147) for urban areas.

- 2 -

important variable explaining disparities in income level, poverty incidencevaries considerably among the 13 regions in the country. Together withrelatively poor access to services and social infrastructure, low farmincomes have encouraged migration from the rural to the urban areas,particularly in the Manila region where population grew by more than amillion in the period 1975-1980.

B. Composition of the Rural Economy

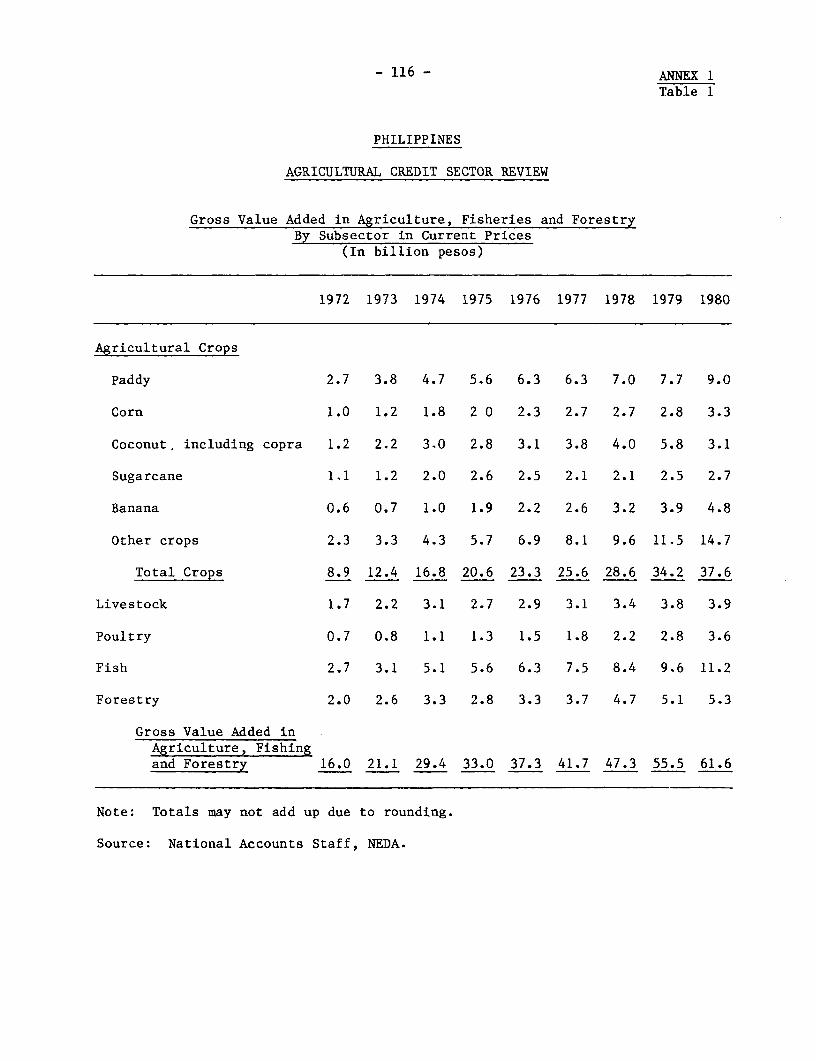

1.05 Crop production is the predominant subsector, contributing 61%of gross value added in agriculture./l Livestock and poultry accounted for12%, fisheries 18% and forestry 8% (Annex 1, Table 1)./2

1.06 Food crops are more important than commercial crops in both areaand value of production, occupying some 69% of the planted area and yielding64% of the value of production. Rice is grown on 3.5 million ha, providingthe staple of both urban and rural populations in the lowlands and plains.Corn, the other major food crop, is grown on a subsistence basis on about3.3 million ha, mainly in the uplands where it is complemented by upland riceand root crops. Corn also provides livestock feed. Yields are typicallylow (0.8-0.9 tons per ha).

1.07 The commercial crops area is largely planted to coconut /3(about 3 million ha), followed by sugar, abaca and coffee. Sugarcane andcoconut products account for about 83% of the total value of commercialcrops. Exports of copra have fluctuated widely but those of both dessicatedcoconut and coconut oil have registered steady increases. Despite a muchsmaller magnitude, the two most successful commercial crops in recent yearshave been pineapple and bananas, both developed efficiently as plantationcrops. Cotton production has also increased.

1.08 In livestock, commercial pig and poultry farming has expandedrapidly, while beef production has been lagging behind fast-growing demand.Forty percent of the beef consumed is imported, mainly in the form of cornedbeef. About three quarters of the nearly 2 million farms with cattle -mainly carabao for power - are in rainfed areas, concentrated in the drierand upland zones.

/1 1975 figures.

/2 Gross value added at 1972 constant prices in Annex 1, Table 2.

/3 One third of the population is in one way or another involved inthe coconut industry.

1.09 The country's vast inland fishery resources are estimated toinclude 900,000 ha of freshwater areas, mainly suited for fishpond purposes;about 20% of this potential has been developed. Marine fishing groundscovering about 170 million ha of coastlines have a potential maximum sustain-able yield of 1.95 million tons, of which about 1.25 million tons areexploited. However, some traditional fishing grounds are already overfished,and this has become a major economic and social problem, particularly for the200,000 or so "municipal fishermen" who constitute part of the rural poor.

1.10 Forest resources occupy some 65% of the total land area, or13.7 million ha, most of which is public forest lands. Although commercialforests are estimated to contain 1.9 billion cubic meters of sound woodresources, exploitation has greatly reduced timber stands. Strictersupervision of fellings, planting of fast growing species, and squattercontrol are among new approaches that should enable sustainable exploitationof the forests.

C. Agricultural Performance

1.11 Self-sufficiency in food production, especially in rice, hasconsistently received highest government priority. This objective wasachieved in 1977 through a two-pronged strategy which envisaged: expansionand rehabilitation of irrigation systems to remove the constraint ofinadequate water supplies; and increased use of high-yielding varieties(HYVs), fertilizers and pesticides through the Masagana-99 (M-99) credit-cum-extension program. During the last decade the Philippines also madesignificant progress toward other objectives which included expansion ofagriculture-s share in exports, land reform and land distribution, andconservation of natural resources. Since the early 1970s, the Governmenthas accorded increasing importance to raising income levels of small farmersand fishermen, and reducing income disparities between the rich and the poor,between rural and urban areas and among the rural regions.

1.12 Although in proportion to other sectors of the economy, the contri-bution of agriculture has been declining slowly, from 28.9% of GDP in 1970to 25.5% /1 in 1980, the agricultural sector grew at an annual rate of about4.9% during 1970-80 which was comparable to the performance of other EastAsian countries (Annex 1, Table 3). Increased grain production was associ-ated with the Philippines' shift from being a major importer of rice up to

/1 Preliminary estimate of NEDA.

- 4 -

1977 to having small exportable surpluses (currently estimated at about200,000 tons a year). Corn production, however, continues to be below thetotal estimated corn consumption for food, feeds and other uses. Output ofvegetables, peas and beans, fruits and nuts, roots and tubers has markedlyand steadily increased. Vegetable and fruit production, however, isconstrained by problems related to post-harvest facilities, marketing anddistribution.

1.13 From a small base, coffee and rubber production have increased bymore than 10a annually, and export potentials are good. Among other exportcrops, results have varied: output of cocoa is estimated to have fallen,while that of abaca and tobacco has essentially remained at the same level.Production of sugar has risen at less than 2.5% p.a. Exports of bananas andpineapple have notably increased, but coconut, still the country's majorforeign exchange earner, has suffered from low world market prices andfluctuating yields due to weather conditions, diseases and the age of thetrees.

1.14 While production of fish, pigs and poultry has expandedsignificantly, value added in the traditional livestock (cattle) subsectorstagnated during the 1970s. However, Government has intensified itsactivities to promote livestock production, in particular through BakahangBarangay and other credit programs.

1.15 Continued agricultural growth will remain crucial for thePhilippines to grapple with its major economic problems. First, althoughthe total population is growing by 2.5% annually, the labor force isprojected to increase by 3.7% annually due to very high fertility rates pre-vailing in the 1960s, before the introduction of family planning programs,and an expected increase in the proportion of working women. Between L980and 1987, the economy will have to find jobs for 5 million people, or700,000 persons annually, if an increase in unemployment is to be prevented.While the manufacturing sector will promote more rapid growth of employment,the labor force is expected to grow so rapidly that most of the incrementwill have to be absorbed by the agricultural sector./l Second, despitesignificant increases in output, the Philippines' agricultural productivitycontinues to be low by international standards. Reaching higher levels; ofproductivity. both in irrigated and rainfed areas, is important for generaleconomic growth and for increased rural incomes. Third, during the lastdecade average rural incomes increased in real terms as the rate of growth

/1 World Bank, "The Philippines - Selected Issues for the 1983-87 Plan.Period," Report No. 3861-PH, June 1, 1982.

- 5 -

of agricultural production exceeded that of the population by a substantialmargin. But while employment increased by more than 20%, the gains in bothincome and employment were not evenly produced. Fourth, agriculturalstrategies will also have to respond to ongoing efforts to reduce dependenceon imported energy, promote larger domestic resource mobilization and, inthe context of deteriorating terms of trade, reduce dependence on foreignborrowings and promote exports.

1.16 The Government's proposed development plan (1983-87) thereforeenvisages more efficient exploitation of agricultural potential, sustainedself-sufficiency in rice, fish, poultry, pork and fruits and vegetables andexpanded production of export crops, import substitutes and agro-industrycrops. The development of infrastructure, particularly small-scale irriga-tion systems, mini hydro projects, and farm-to-market roads, will receivehigh priority. Agrarian reform is proposed to be intensified. Crop insur-ance will be expanded. Incremental resources are intended to be generatedfrom greater reliance on domestic savings through financial innovations andmore efficient intermediation, development of long-term capital markets,expanded commercial banking, greater reliance on resource mobilizationthrough issue of government securities, and floating interest rates. Thenew plan emphasizes significant improvement in access by a larger section ofthe population to facilities and resources such as infrastructure, credit,raw materials, technology and markets. Formal credit-facilitated agricul-tural development and efficient financial intermediation, particularlyresource mobilization and credit, should support Government's developmentobjectives in agriculture. It is against this background that this reportreviews Philippine agricultural credit.

- 6 -

2. THE RURAL FINANCIAL MARKET: INSTITUTIONALAND NONINSTITUTIONAL ARRANGEMENTS

A. Introduction

2.01 The Philippine rural financial market consists of a formalinstitutional sector and an informal noninstitutional sector. Institu--tional credit for agriculture is offered by a variety of government- andprivately-owned entities whose lending operations often have rather welldefined emphasis in terms of loan amount (large vs. small loans), duration(long vs. short-term), recipients (commercial operations, agrarian reformbeneficiaries, etc.), commodities (sugar, coconut, etc.) and activity(production, marketing or processing). Noninstitutional credit is offeredby private moneylenders, traders, relatives, friends and landlords. Ittends to be short-term, often requiring no collateral but at interest rateswhich are substantially above those used for institutional credit.

B. Organization of the Rural Institutional Financial Market

2.02 A clear demarcation between the Philippines' rural and nonruralfinancial markets is not feasible /1 since the Manila offices of rural creditinstitutions participate in the rural financial market through resourcemobilization and the extension of credit for agricultural activities. Infact, the Metro Manila area has a sizable share in institutional credit foragriculture. The national financial structure is therefore described belowin order to provide a context for the operations of the rural sector.

Structure of the National Financial System

2.03 The financial sector in the Philippines is relatively well-developed. The sector grew rapidly during the 1960s, and total resources

/1 In the Philippines, rural areas are defined as those with a populationdensity of less than 1,000 persons per sq km and where at least 50% ofthe population is engaged in agricultural activities. By thisdefinition, 99.4% of the total land area of the country is classified asrural, and 84% of the 1970 population are rural dwellers. In thisreport, however, "rural" refers to areas outside Metro Manila, whichrepresent 99.8% of the country's total land area, where 89% of the 1970population reside. Systematic data on financial institutions'activities in "rural" areas and "nonrural" areas are not available.

- 7 -

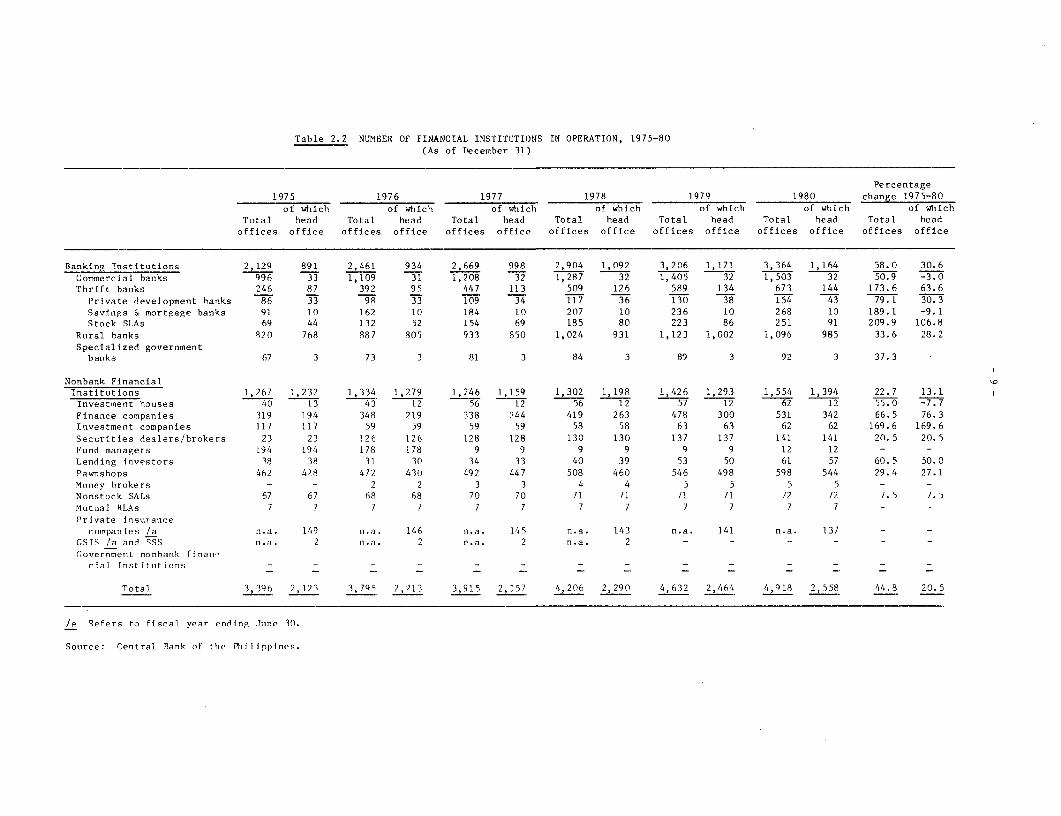

of the financial system as a percentage of GNP increased from 48% in 1960 to115% in 1980. During 1975-80, growth in total assets averaged 8% p.a. inreal terms while real GNP grew at 6% (Table 2.1). This growth was accom-panied with and made possible by a significant expansion in the network ofoffices, which increased from 3,396 in 1975 to 4,918 in 1980 (Table 2.2).Exclusive of the Central Bank portfolio, ownership of the sector is aboutequally divided between private and government entities.

2.04 Within the financial sector, the banking system is predominant andcontrols about 60% of total assets, mainly through the commercial banks.Non-banking financial institutions account for a relatively small share oftotal assets, but perform specialized functions not handled by the commer-cial banks, and thus broaden the sector's geographical coverage and range ofservices. Insurance companies and investment houses, for example, areimportant by undertaking resource mobilization and capital formation.

2.05 The Banking Sector. The banking system comprises commercialbanks, rural banks, thrift banks ard specialized government-owned banks.The Central Bank (CB) is responsible for monetary stability and creditregulation. It also ensures availability of credit for agricultural produc-tion and related activities, as far as is consistent with conventionalcentral banking functions.

2.06 Commercial Banks. At the end of World War II, there were 4domestic banks and 4 foreign banks. However, at the end of 1980, thecommercial banking sector included a total of 32 banks, comprising 26 privatedomestic banks, 2 government or semi-government banks and 4 branches offoreign commercial banks. A large number of banks were established between1955-65, in response to government efforts to rehabilitate the bankingindustry and to meet the growing demand for financial services. Thegovernment-owned Philippine National Bank (PNB), established in 1916, is thelargest commercial bank in the country with 175 offices and 25% of the totalassets of the banking system. The five largest private domestic banks have23% of total assets and 616 offices./1 Foreign banks own about 12% of totalassets and operate mainly in Metro Manila.

2.07 Commercial banks operate through 1,503 offices, more than half ofwhich are in Metro Manila (651), Central Luzon (121) and Southern Tagalog(106). Other regions, particularly Ilocos, Cagayan, Visayas and Mindanao

/1 Bank of the Philippine Islands, Allied Bank, Metropolitan Bank, UnitedPlanters Bank and Far East Bank & Trust Co.

- 8 -

Table 2.1: PHILIPPINES: STRUCTURE OF FINANCIAL SYSTEM, 1980(Billion pesos and percentages)

Asset size Real rates of growth p.a.Compo- 1960- 1965- 1970- 1975-

Amount sition 65 70 75 80(Pesos) - …---------- (%) --------------

Central Bank 65.4 21.1 4.0 6.3 16.8 8.0

Banking SystemCommercial Banks 138.4 44.5 17.2 7.9 12.3 8.8

Private 85.1 = T17T.0 T 8.8 14r.0 73Government 34.6 11.1 17.5 6.3 8.6 2.3Foreign 18.7 6.0 - - - -

Thrift Banks 10.6 3.4 28.2 15.0 -2.9 24.2Savings & Mortgage 7.4 2.4 25.3 14.7 -5.5 25.3Private development banks 1.6 0.5 46.5 9.2 -0.8 18.3Savings & loan associations 1.6 0.5 - - 17.3 25.3

Rural Banks 5.6 1.8 23.0 10.5 14.0 3.2

Other Banks 34.2 11.0 10.0 10.7 7.4 11.4Development Bank of the Phil. 28.9 9.3 10.0 10.7 3.4 72.1Land Bank 5.2 1.7 - 128.0 7.6

Philippine Amanah Bank 0.1 0.0 - - - --8.4

Total Banking System 188.8 60.7 16.4 8.8 10.9 9.6

Nonbank Financial IntermediariesInsurance Companies 27.5 8.9 7.0 4.7 -4.5 6.3Government /a 18.5 6.0 4.8 4.1 -3.0 7.1Private 9.0 2.9 13.3 6.2 -8.0 5.0

Investment Institutions 25.6 8.2 - 16.6 11.2 7.8Finance companies 11.9 3.8 - 9.3 -3.5 14.9Investment companies /b 5.0 1.6 - - - 7.2

Others /c 8.7 2.8 - 37.1 25.8 0.9

Trust Operations 1.7 0.5 - 23.7 18.8 -10.1

Other Financial Intermediaries 2.1 0.6 -8.4 22.3 13.9 -6.8Security dealers & brokers 1.0 0.3 - 111.8 29.7 -8.1Nonbank savings & loan assn. 0.3 0.0 - - -5.3 11.8Agricultural credit admin. 0.5 0.2 -23.3 12.0 -9.0 -9.5Pawnbrokers 0.3 0.0 - - - 11.8

Total Nonbank FinancialIntermediaries 56.9 18.2 11.5 8.5 2.7 9.5

Total Financial System 311.1 100.0 12.0 8.3 10.1 8.2

/a Includes GSIS and SSS.7b Includes mutual funds./c Includes investment houses.

Note: (-) = insignificantn.a. = not availablep = preliminary

Source: Central Bank of the Philippines.

Table 2.2 NUMBER OF FINANCIAL INSTITUTIONS IN OPERATION, 1975-80(As of December 31)

Percentage1975 1976 1977 1978 1979 1980 change 1975-80

of which of which of which of which of which of which of whichTotal head Total head Total head Total head Total head Total head Total head

offices office offices office offices office offices office offices office offices office offices office

Banking Institutions 2,129 891 2,461 934 2,669 998 2,904 1,092 3,206 1,171 3,364 1,164 58.0 30.6Commercial hanks 996 33 1,109 31 1,208 32 1,287 32 1,405 32 1,503 32 50.9 -3.0Thrift banks 246 87 392 95 447 113 509 126 589 134 673 144 173.6 63.6

Private development hanks 86 33 98 33 109 34 117 36 130 38 154 43 79.1 30.3Savings & mortgage banks 91 10 162 10 184 10 207 10 236 10 268 10 189.1 -9.1Stock SLAs 69 44 132 52 154 69 185 80 223 86 251 91 209.9 106.8

Rural banks 820 768 887 805 933 850 1,024 931 1,123 1,002 1,096 985 33.6 28.2Specialized government

banks 67 3 73 3 81 3 84 3 89 3 92 3 37.3 -

Nonbank FinancialInstitutions 1,267 1,232 1,334 1,279 1,246 1,159 1,302 1,198 1,426 1,293 1,554 1,394 22.7 13.1

Investment houses 40 13 43 12 56 12 56 12 57 12 62 12 15.0 7.7Finance companies 319 194 348 219 338 244 419 263 478 300 531 342 66.5 76.3Investment companies 117 117 59 59 59 59 58 58 63 63 62 62 169.6 169.6Securities dealers/brokers 23 23 126 126 128 128 130 130 137 137 141 141 20.5 20.5Fund managers 194 194 178 178 9 9 9 9 9 9 12 12 - -

Lending investors 38 38 31 30 34 33 40 39 53 50 61 57 60.5 50.0Pawnshops 462 428 472 430 492 447 508 460 546 498 598 544 29.4 27.1Money brokers - - 2 2 3 3 4 4 5 5 5 5 - -Nonstock SALs 67 67 68 68 70 70 71 71 71 71 72 72 7. 5 7. 5Mutual RLAs 7 7 7 7 7 7 7 7 7 7 7 7 - -

Private insuranicecompanies /a n.a. 149 n.a. 146 n.a. 145 n.a. 143 n.a. 141 n.a. 137

GSIS /a and SSS n.a. 2 n.a. 2 n.a. 2 n.a. 2 - - - - - -

Covernment nonhank finan-cial institutions - - - - - -

Total 3, 396 2,123 3,795 2,213 3,915 2,1 57 4,206 2,290 4,632 2,464 4,918 2,558 44.8 20.5

/I Refers to fiscal year endiing June 30.

Source: Central Bank of the Philippines.

- 10 -

are less well served in terms of the ratio of number of offices to thenumber of municipalities and cities in the regions (Annex 2, Tables 1 and2). The commercial banks' offices outside Metro Manila (852 offices) aresecond in network only to that of the rural banks (1,125 offices).

2.08 Commercial bank credit is apportioned over a wide range ofactivities, comprising manufacturing and industry (35.1%); trade, insuranceand mining (34.3%); and agriculture (10-15%). The agricultural lending ofprivate commercial banks is mainly for large commercial plantations,processing and marketing. PNB does however lend to smallholders, particu-larly to finance agricultural production under government-sponsoredcommodity credit programs.

2.09 Thrift Banks. The thrift banks comprise 10 savings and mortgagebanks (SMBs), 91 stock savings and loan associations (SLAs) and 43 develop-ment banks. Together, they recorded the highest growth rate in total bankingassets during 1975-80, at about 24% p.a. in real terms, compared with 8.2%for the entire financial sector. The thrift banks account for about 9% ofthe total deposits of the banking system. SMBs and SLAs specialize inpersonal loans for consumer goods, housing and real estate, while thedevelopment banks provide medium- and long-term credit for agriculture andindustry, especially to small and medium enterprises. The development banksare specialized institutions which, though predominantly private, are partlyowned by the Government-owned Development Bank of the Philippines throughits purchase of shares in these institutions which helps them to extendmedium-and long-term credit to industry and agriculture.

2.10 Rural Banks. The more than 1,000 rural banks, generally unitbanks, constitute an important component of the rural financial market inview of their wide geographical coverage, proximity to rural areas andaccessibility to the farming community. Rural banks are generally family-owned although partially capitalized by government shares. In addition,25 cooperative rural banks have been organized, primarily by farmerorganizations (samahang nayons), to provide financial services to theirmembers. The rural banks' share in the total assets of the financial systemis less than 2%, although in 1975 they provided about 50% of the totalinstitutional production credit for cereals, the absolute amount of whichhas steadily declined as has the number of loans. Rural bank lending ismostly short-term for production of cereals, livestock and poultry, and to alesser extent for export crops like sugar and coconut. Rural banks alsoextend credit to small industries and enterprises. The rural banks' depositliabilities constitute about 2% of the total deposit liabilities of thebanking system.

2.11 The rural banking system has actively supported the Government'scommodity production programs, particularly for rice. In view of theircrucial role in the rural economy, rural banks receive financial incentivesand subloan guarantees from the Government as well as low-cost rediscountingfacilities from the Central Bank. At present, the rural banking system

- 11 -

faces major financial problems such as low capital, poor liquidity onaccount of high arrearages, ineligibility for access to Central Bank fundsdue to high subloan arrearage levels, an inadequate number of field staff,and nonviability due to low turnover.

2.12 Specialized Government Banks. The government-owned DevelopmentBank of the Philippines (DBP), the Land Bank of the Philippines (LBP), andthe Philippine Amanah Bank (PAB) provide long-term resources to industry andagriculture and perform specialized functions important to the Government'spolitical, socioeconomic and development objectives. Altogether, they havea total of 92 offices. DBP was established in 1958, with a mandate tosupply credit for industry, housing, and agriculture. In 1964, it was givenresponsibility for assisting in the establishment of smaller privatedevelopment banks (PDBs) in order to provide decentralized credit facilitiesto small enterprises. DBP's current lending is largely for industry (69%),followed by real estate (19%) and agriculture (12%). DBP-s resources comefrom equity contributions by the Government, borrowings from CB, foreignborrowings, deposits from the Government, sale of DBP bonds and internalcash generation. LBP, established in 1963, functions as the financial armof the Government's land reform program, although it has recently begun toaccept and undertake all functions performed by a commercial bank. PABprovides banking services including credit to Muslim areas in Mindanao.

2.13 Nonbank Financial Intermediaries. Nonbank financial institutionsare widely diverse, comprising insurance and finance companies, investmenthouses, trusts and specialized government institutions. The insurancecompanies primarily support industrial and commercial activities throughshort-term investments and loans, besides policy loans to customers. TheGovernment Service Insurance System (GSIS) and the Social Security System(SSS), also government-owned, provide benefits to government employees andprivate sector employees, respectively. While both GSIS and SSS extendloans to policy holders, GSIS allocates about 33% of its resources forpurchase of stocks and bonds, and private and government securities, SSSinvests about 45% of its resources in notes receivable issued by PNB andDBP. The government insurance and social security systems are alsoimportant sources of longer-term funds for government institutions otherthan DBP and PNB.

2.14 Investment houses engage in underwriting corporate securities,equity investments, stockbroking and quasi-banking functions. Majorinvestment houses provide long-term credit to industry and, in a very smallway, to agriculture. Finance companies, on the other hand, specialize inextending credit through discounting of commercial paper on accountsreceivable for individuals and enterprises.

- 12 -

2.15 The government-owned Agricultural Credit Administration (ACA) andPNB's subsidiary, the National Investment and Development Corporation(NIDC), were established to perform specialized functions. ACA supportsagricultural production through the provision of credit to farmers and toagricultural projects. The government has since merged ACA with LBP. NIDCpromotes a wide variety of industrial, agricultural and commercialenterprises and also acts as a holding company.

The Rural Financial Market

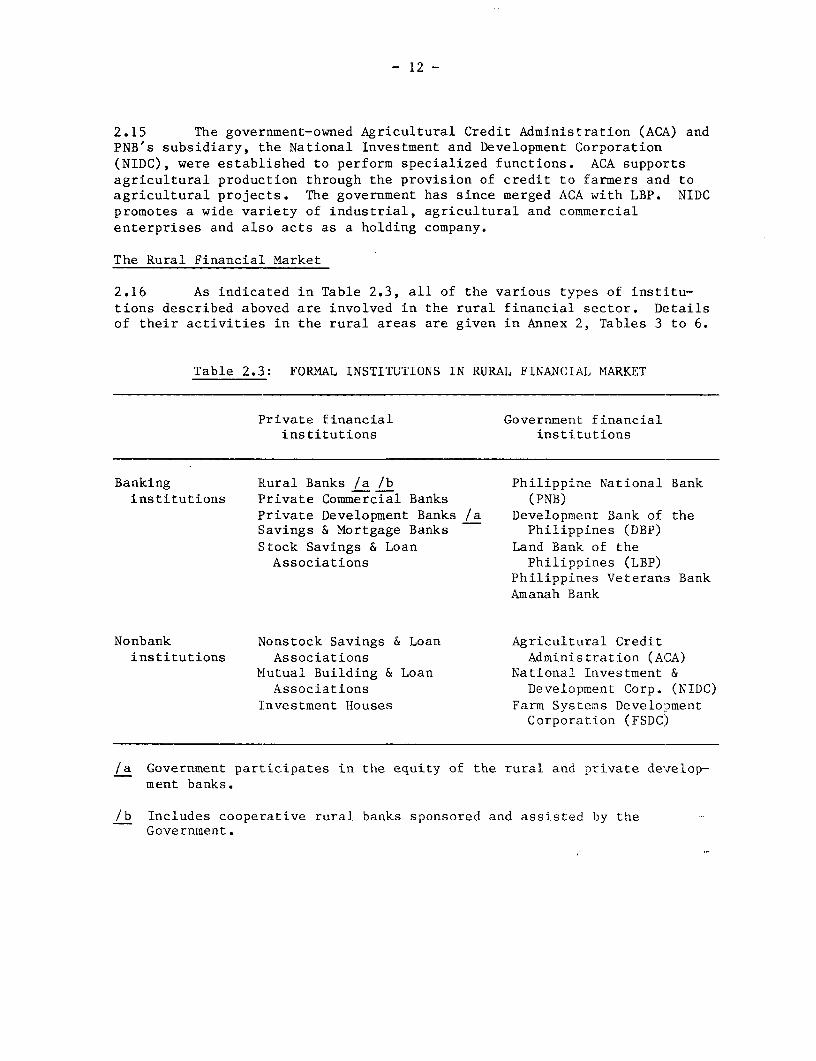

2.16 As indicated in Table 2.3, all of the various types of institu-tions described aboved are involved in the rural financial sector. Detailsof their activities in the rural areas are given in Annex 2, Tables 3 to 6.

Table 2.3: FORMAL INSTITUTIONS IN RURAL FINANCIAL MARKET

Private financial Government financialinstitutions institutions

Banking Rural Banks /a /b Philippine National Bankinstitutions Private Commercial Banks (PNB)

Private Development Banks /a Development Bank of theSavings & Mortgage Banks Philippines (DBP)Stock Savings & Loan Land Bank of theAssociations Philippines (LBP)

Philippines Veterans BankAmanah Bank

Nonbank Nonstock Savings & Loan Agricultural Creditinstitutions Associations Administration (ACA)

Mutual Building & Loan National Investment &Associations Development Corp. (NIDC)

Investment Houses Farm Systems Develo?mentCorporation (FSDC)

/a Government participates in the equity of the rural and private develop-ment banks.

/b Includes cooperative rural banks sponsored and assisted by theGovernment.

- 13 -

Evolution of Formal Rural Financial System

2.17 Since early in this century, the Philippine rural financial markethas been characterized by Government intervention. The Government first usedthe Bank of the Philippine Islands to channel its funds to the sugarindustry. Later, to broaden the credit system, the Government establishedthe Agriculture Bank, but this too became wholly involved in the sugarindustry to the neglect of other subsectors. In 1916 the Government estab-lished the Philippine National Bank (PNB) to take over the by then defunctAgriculture Bank. Like its predecessors, PNB paid little attention tosmallholders and instead supported commercial crops and general banking.However, with the establishment of the Central Bank in 1946, rural financialmarkets and credit mechanisms received greater government attention. TheRural Banks Act was passed in 1950 to establish a viable rural credit systemwith the intention of providing credit on reasonable terms at locationseasily accessible to the rural population.

2.18 Since a nationwide private rural banking system would take sometime to become established, in 1952 the Government organized a fullygovernment-owned nonbank agency, the Agricultural Credit and CooperativeFinancing Administration (ACCFA), to assist small farmers through liberalcredit and cooperative marketing. ACCFA, however, went bankrupt in 1960 dueto poor management and low collections. ACCFA was reorganized into the ACAto expand finance for agrarian land reform. ACA has recently been mergedwith LBP.

2.19 The institutions currently most active in lending for agricultureper se are the Government-owned PNB, DBP and LBP, as well as the privatecommercial and rural banks, the PDBs and savings and mortgage banks. Theirrelative importance in the sector is shown in Table 2.4, which highlightsthe greatly increased activity of the commercial banks and the decline inPNB lending. The share of government-owned banks in agricultural loans fellfrom 35.2% in 1975 to 18.6% in 1980, while the private commercial banksexpanded agricultural lending from 56.8% to 74.5% during the same period.

- 14 -

Table 2.4; AGRICULTURAL LOANS GRANTED, BY BANK(Annual Disbursements)

(? billion)

1980Amount

1975 1980 (at 1L975% of % of constant

Source Amount total Amount total price)/a

Government BanksPNB (Gov-t commercial bank) 8 84 31.7 8.43 15.9 4.88DBP 0.86 3.1 0.65 1.2 0.38LBP 0.05 0.2 0.80 1.5 0.46ACA 0.06 0.2 0.03 - 0.02

Subtotal 9.81 35.2 9.91 18.6 5.74

Private BanksCommercial banks 15.84 56.8 39 .50 74.5 22.88Rural banks/SLAs /b /c 2.12 7.6 3.26 6.2 1.89Private development banks /c 0.09 0.3 0.16 0.3 0.09Savings & mortgage banks 0.04 0.1 0.20 0.4 0.12

Subtotal 18.09 64.8 43.12 81.4 24.98

Total 27.90 100.0 53.03 100.0 30.72

/a Deflated by consumer price index at 193.00 (1975=100).

/b Includes cooperative rural banks.

/c Private development and rural banks are partially capitalized by theGove rnment.

Source: TBAC.

2.20 The relative importance of agricultural lending to the totallending of each institution is shown in Table 2.5.

- 15 -

Table 2.5: AGRICULTURAL LOANS AS A PERCENT OFTOTAL LOANS, BY BANK

1975 1978 1979

GovernmentpNB 48 39 37DBP 36 23 17LBP 21 60 71ACA 100 100 100

PrivateCommercial banks 23 19 20Rural banks /a 89 87 86PDBs /a 46 40 31SMBs 10 2 4

/a Mixed ownership.

Source: TBAC.

Banking Reforms of 1980

2.21 The evolution and growth of the financial system in the Philippines,though impressive and innovative, was not without its problems. In 1979, ajoint IMF/IBRD review of the Philippines financial sector noted thatfragmentation among institutions reduced competition in the system and, inturn, its responsiveness to changing opportunities and demands. Thesystem also appeared to have done little to promote longer-term lending andborrowing.

2.22 Following the recommendations of the IMF/World Bank mission,/l thePhilippines introduced a set of financial reforms with two principal objec-tives: (a) increased competition in the financial sector to achieve greaterefficiency, and (b) increased availability of longer-term credit. Towardthe latter objective, a certain proportion of the nominally short-term fundsof deposit banks will be used for longer-term lending. Toward the goal ofincreasing competition, the functional distinctions between bank and nonbank

/1 The Philippines: Aspects of the Financial Sector, World Bank Country,Study, May 1980.

- 16 -

financial intermediaries have been reduced and the range of financialservices provided by these institutions has been broadened through thefollowing measures:

(a) the commercial banks can combine domestic and internationalbanking and engage in the functions of an investment house, suchas underwriting, equity investments and security dealing. Theminimum capital requirement of P 500 million for expanded(universal) commercial banks will encourage consolidation of thesystem into larger units. Further, commercial banks can now ownrural and thrift banks to take advantage of economies of scale.They can also form subsidiaries for specific financial services.Expanded commercial banking authority should result in benefitssuch as economies of scale in operations, flexibility inarranging financial packages, stronger competitive capacity andability to service broader markets;

(b) all functional distinctions among thrift banks (privatedevelopment banks, savings and mortgage banks, and stock andsavings and loan associations) have been abolished. Upon meetingminimum capital requirements, thrift banks can qualify for fulldomestic banking powers;

(c) rural banks have been given broader domestic banking powers. Tostimulate growth and profitability, restrictions have been liftedon rural banks' lending coverage which had fonnerly been limitedto farm families cultivating less than 50 ha of land and tomerchants and cooperatives with less than P 10,000 in capital.Rural banks, which were established as unit banks, may nowestablish chain banking or group banking arrangements, directlyor through a holding corporation including a commercial bank.Minimum capital requirements have been enhanced and will beconformed to by existing banks over about a three year period;

(d) a former requirement that PDBs invest 75% of their loanable fundsin medium- and long-term loans has been changed to a requireraentof 75% of the aggregate par value of DBP's subscribed shares, andonly as long as such counterpart capital exists. This willpromote diversification of PDB operations into short term lendingand will also give PDBs greater access to DBP's long-term funds;and

(e) nonbank financial intermediaries can now undertake quasi-bankingactivities authorized by the Central Bank, which will also allowthem access to Central Bank credit facilities to enhance theirintermediation in longer-tera capital flows. I

- 17 -

2.23 Another major change in the financial sector was the deregulationof interest rates on savings deposits and all types of deposits and loanshaving an original maturity of more than 720 days (subsequently lowered to365 days)./l The limited floating of interest rates was an important steptowards achieving the universal banking concept by fostering greater competi-tion among the banking institutions. This should eventually lead to greaterefficiency in the use of capital, the cost of which will be determined bymarket forces. The elimination of ceilings on interest rates is also intendedto give financial institutions greater flexibility in financial intermedia-tion, especially for longer-term funds, and to allow the system to respondmore promptly to domestic and external developments.

2.24 While it is too early to judge how the banking system would respondto these reforms, these have paved the way for initiating measures whichwould go a long way in resolving the Philippines- current institutional andfinancial issues in agricultural credit, especially with regard to thefollowing: (a) greater mobilization of domestic long-term resources; (b)expansion in medium- and long-term lending by the government-owned PNB andprivate commercial banks; (c) introduction of structural and operationalchanges in DBP and LBP; and (d) facilitation of an increased agriculturalcredit and resource mobilization effort by thrift banks.

C. Noninstitutional Credit Arrangements

2.25 Informal financial arrangements are especially important to theagricultural sector. For most farmers, the informal financial system mustbe seen as the natural provider of financial services since transaction costsand other costs of access to formal finance are not appropriate for thesefarmers. The informal financial sources seem to serve them effectively.Recent estimates indicate that the informal sector now provides between 64%and 78% of the total credit received by the agricultural sector./2 Informalcredit may be classified as land based, commodity based, or socially based.

Major Sources of Informal Credit

2.26 Land-based Credit Arrangements. These are made either within oroutside of the traditional landlord-tenant relationship. Landlord credit totenants takes the form of landlords providing inputs and other workingcapital to tenants between harvests. This arrangement may be expected todiminish over time as land reform continues, and also to the extent that

/1 Effective January 1, 1983, the interest rate ceiling on loans withmaturities of less than 365 days was also lifted.

/2 Source: TBAC, "A Study of the Informal Rural Financial Markets in ThreeSelected Provinces of the Philippines."

I-- 18 -

tenants become able to enter the formal financial market through thriftinstitutions, rural banks and pawnshops. Transactions outside of thelandlord-tenant relationship primarily involve a redeemable pledge, underwhich an owner of a plot of land permits another farmer to operate the landin exchange for an advance. The lender has access to the land and enjoysthe fruits of its production so long as the advance remains unpaid. Theredeemable pledge is not permitted by regulations applied to land reformareas, but unregistered transactions of this type frequently occur.

2.27 Commodity-based Credit Arrangements. Commodity-based credit isfundamentally commercial in nature, always involving interest payments inkind or cash, directly or hidden. The most common type of commodity-basedcredit arrangement is "five-six" credit which in its most basic forminvolves the borrowing of five units of rice and repayment of six units ofrice. Five-six arrangements are common in food marketing. Vegetablehawkers, for example, might borrow e 50 worth of produce each morning froma stallholder in a vegetable market and return e 60 in cash to thestallholder each evening. The five-six rate of interest in the daily caseis 20% per day and in annual terms is astronomical. The high rates seem tobe acceptable, apparently because they are more closely related to theopportunity costs of small vendors' labor than to the scarcity of capital.Rates of interest specified in percentage terms can be a very abstractnotion when applied to informal finance.

2.28 Another common form of commodity-based credit is a salesarrangement under which a farmer obtains a loan after promising to sell hisproduce to the lender at a below-market price. Commodity-based credit isalso found in relationships between small-scale "integrators" and producersin the livestock sector. Integrators, often landlords, traders andranchers, place animals with backyard or other small-scale commercialproducers, and take them back when they are ready for slaughter.

2.29 Socially-based Credit Arrangements. These may be defined as thosein which the relationship between lender and borrower is primarily of asocial rather than a commercial nature. This would cover friends, neighborsand relatives. Disbursements and repayments may be in cash or in kind. Theloans frequently carry no specified interest rate, but generally involveobligations of reciprocity on the part of the borrower.

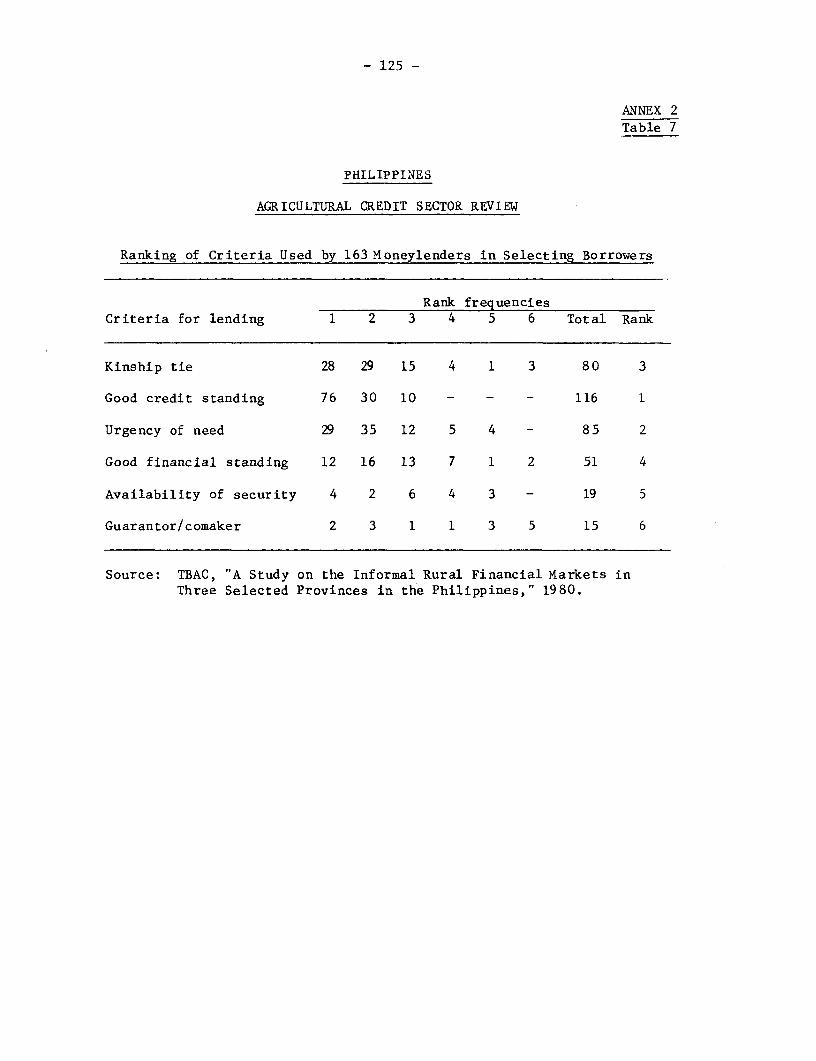

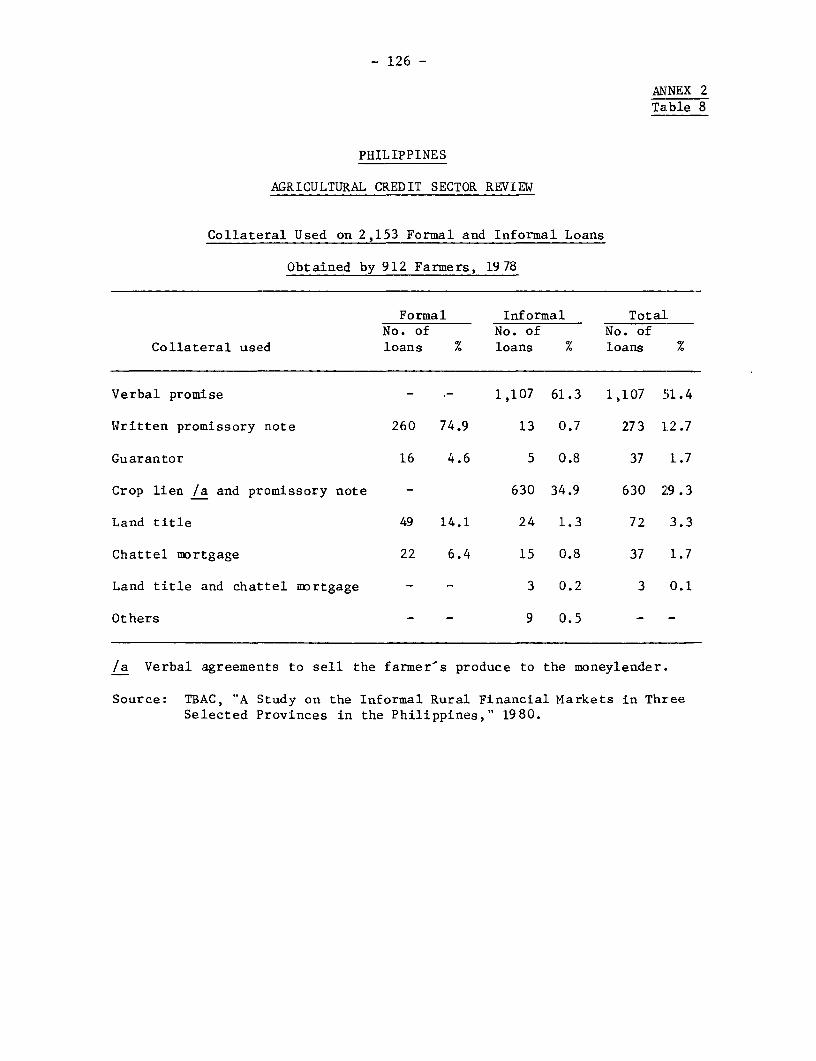

Terms and Conditions of Informal Credit

2.30 A survey made by TBAC found that the informal sector issues creditprincipally on the basis of the good credit standing of the borrower and averbal promise to pay (Annex 2, Table 7). Only 35% of the loans surveyedwere secured by a written promissory note and a verbal agreement to sellfarmer produce, and only 2.8% were secured with land title (Annex 2, Table8). Private lenders, particularly those engaged in palay trading, require

- 19 -

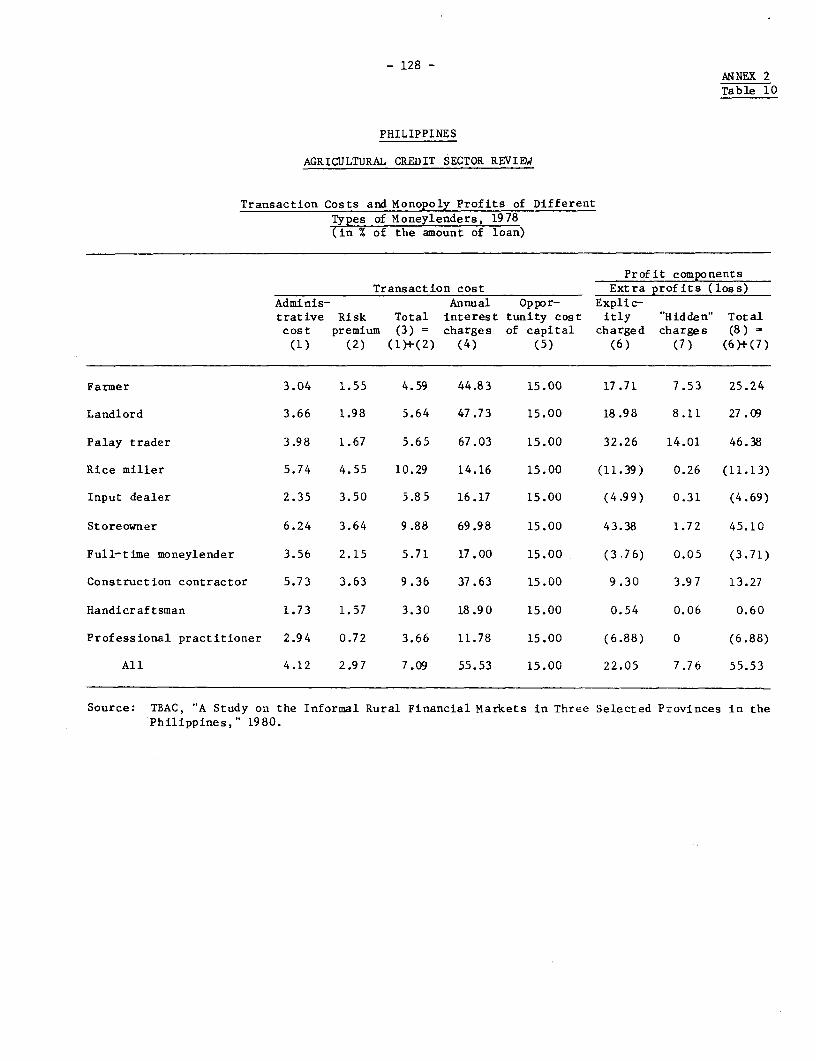

their borrowers to pay in kind (Annex 2, Table 8). In cases of default,private lenders impose strict measures. Any additional loans are secured byland title or chattle mortgage, and have interest rates double those of thedefaulted loan. Repayment rates on informal loans are, however, relativelyhigher than in the formal sector (Annex 2, Table 9). The incidence ofdefault in aggregate terms is significant in informal lending, as it is informal lending. However, the overall interest rates charged by privatemoneylenders include a risk premium of 1-5% and are designed to leave anadequate profit margin, explicit or hidden in commodity transactions (Annex2, Table 10).

Other Characteristics of Informal Credit in the Philippines

2.31 A selective study of informal rural financial markets in thePhilippines carried out by the Technical Board for Agricultural Credit (TBAC)in 1978 provides glimpses of vitality, competitiveness and flexibility whichare quite at variance with the traditional view of informal lenders as mono-polistic, and exploitive./l Some moneylenders, for instance, were found tocharge interest rates below those of commercial banks while others chargedhigher rates. Moreover, high rates prove somewhat illusory in terms ofreturns to lenders because of default risks and repayment experience.

2.32 The Changing Structure of Rural Moneylending. Competitivebehavior in moneylending is seen in the emergence of a new class of lendersduring the 1960s and 1970s, consisting of farmer moneylenders and inputdealers. The input dealers included in the TBAC sample accounted for twothirds of the loans made by sample moneylenders, which is indicative oftheir prominence. The survey results indicate that the new class ofmoneylenders has to a large extent displaced landlords as the traditionalsource of funds for share tenants and small operators, although landlordsstill constitute about 15% of the sample. Annex 2, Table 11 shows aclassification of the sample moneylenders by type of business.

2.33 According to the TBAC study, the new class of lenders arose inresponse to the profitable opportunities in product and credit marketscreated by the revolution in seeds, fertilizer and related technologies aswell as the expansion of irrigation and the infusion of low-cost officialcredit into the rural economy. These developments may have particularlyfavored increased lending by input dealers in that their administrativeexpenses per peso loaned are lower than those of any other type of informal

/1 TBAC, "A Study of Informal Rural Financial Markets in Three SelectedProvinces in the Philippines, 1978." The study surveyed 163 privatemoneylenders and 912 farmer borrowers in the provinces of Bulacan,Camarines Sur and Isabela.

- 20 -

lender included in the sample (see Annex 2, Table 12). This suggests thatthe change in market structure reflects the effects of cost-reducingfinancial innovation in the provision of service to clients. Input dealersentering moneylending were in many cases also new entrants into farm inputsupply. iialf of the sample had been moneylenders for less than six years,suggesting competition in the market. Another suggestion of competition isthe survey finding that moneylenders who were buyers of rice were reportedby half the farmers to offer higher prices for rice than other buyers.

2.34 The presence of competition within the informal sector also seemsindicated in a survey carried out by TBAC and the University of thePhilippines Business Research Foundation. The survey found that the averageannual interest rates (in 1978) on all fully paid informal loans were 33%,51%, and 83% p.a. in the three provinces surveyed (Annex 2, Table 13).Interest rates were lower in two of the provinces where input dealers, whoare generally sources of low-cost informal credit, tended to predominate andcompete with one another. In one of the provinces surveyed, input dealerscontributed around 90% of the total volume of loans issued to all borrowersby sample private lenders (Annex 2, Table 14).

2.35 Loan Size. The average loan amount obtained from informal lendersin the TBAC survey was smaller than that from formal sources. This isindicated by the fact that informal lenders provided two thirds of thevolume of funds borrowed by sample borrowers, but about 83% of the number ofloans (Annex 2, Table 15). As is generally observed, formal lenders avoidsmall-scale lending in an effort to economize on administrative costs.

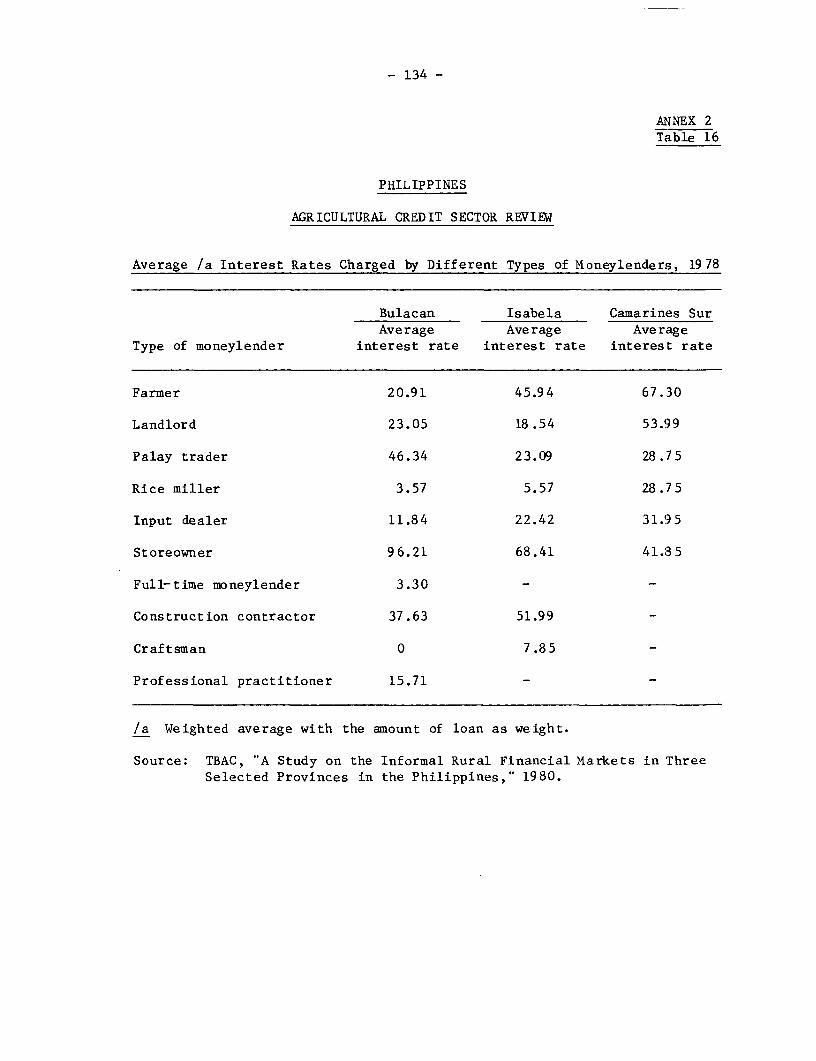

2.36 Lending Rates. Average annual informal lending rates in theTBAC sample ranged between 25% and 96% (Annex 2, Table 16). The highestaverage annual rate reported was 163% on 2% of the total loan volume, while26% of all informal loans surveyed carried no contractual rate of interest.Interest rates on informal loans tend to be lower in areas where officialcredit and other formal lending is relatively widespread. The extent towhich this reflects the impact of formal credit on the overall supply ofcredit, or is simply the result of formal lenders' preference for low riskareas, has not been ascertained. Presumably, both effects apply.

2.37 The Justification for Informal Credit. The TBAC study finds aneconomic justification for the activities of small-scale private money-lenders in their comparative advantage arising from economies of scale.These economies are realized through their integration of product and creditmarkets based on face-to-face arrangements. The study concluded that themethod of operation of informal lenders tended to result in repayment rateswhich were superior to those which can be achieved by formal institutions.Portfolio diversification and risk minimization were also possible becauseprivate lenders tailor their interest rates to specific borrowers and

- 21 -

transactions, while rural banks and other lenders tend to have fixedinterest rates. Administrative expenses are also relatively low, averaging5.7% of amounts lent by sample moneylenders.

2.38 The study proposes that more flexibility for bankers, in the formof removal of interest rate ceilings (a step since partially taken), and useof informal lenders as conduits for official funds, would improve theefficiency of the rural credit system. In other words, TBAC urged that theformal sector become less so.

Informal Credit and the Formal Financial Market

2.39 Interaction between formal and informal financial markets is tosome extent competitive and to some extent facilitating and complementary.As development occurs, financial markets expand, and formal markets expandfaster than informal markets, taking over part of the latter's functions.

2.40 The advantages of informal finance include: a willingness to dealwith transactions that are small in absolute amounts, absence of burdensomedocumentation and bookkeeping requirements, confidence engendered by face-to-face relationships between creditor and debtor, flexibility of loanterms, rapidity with which informal lenders can respond to the applicants-requests, and access costs which are generally low as a result of all thesefeatures. The advantages of formal finance include: the confidentiality ofinstitutional finance, the ability to deal in relatively large amounts ofmoney, the confidence provided by documentation and established legalpractice within the formal sector, specialization and the resultingeconomies of scale and expansion of markets, and the convenience oftranscending face-to-face relationships through communication systems whichcan transfer financial claims through space cheaply and quickly.

2.41 An interesting aspect of the interaction between formal andinformal credit is the extent to which informal credit appears to havereplaced formal credit as a source of funds for farmers who defaulted ongovernment-backed loans and thus became ineligible for further officialcredit. This is best exemplified by the use of credit by rice farmersunder the Masagana 99 program (M-99) introduced in 1972 (paras. 4.03-4.06).At its peak, approximately 800,000 small farmers used M-99 credit forseasonal inputs. This number has fallen to fewer than 100,000 becauseborrowers failed to repay the loans as specified and were subsequentlydenied further access to M-99 credit. Remarkably, the decreased use offormal credit was accompanied by significant increases in rice production.It must be presumed that the gap in institutional credit was filled by acombination of informal credit and self-financing.

- 22 -

Government Policies Toward Informal Finance

2.42 The Government has no articulated policy concerning informalfinance. However, many officials in government and in government-ownedfinancial institutions express concern that informal finance ischaracterized by exorbitant rates of interest, and these perceptions arefactors in decisions which result in government intervention in ruralfinancial markets. Although the informal sector does not seem to be asusurious as some officials believe, a fruitful area for consideration bypolicy makers is how to motivate the formal financial sector to providesmall-scale services which could compete with informal financial inter--mediaries and expand access to formal finance. Historically, attempts todisplace informal finance with formal credit arrangements by utilizinglow-cost government resources have tended to develop into high-costfailures (except when subloan collection is linked with captive marketingarrangements for the produce financed). But despite this lack of success,continued efforts should be made to encourage the growth of the formalsector which has an advantage over the informal sector in that the latterdoes not offer two other services provided by the formal sector, namely:deposit mobilization and provision of medium-and long-term credit. Growthof the formal sector is, therefore, important to promote resource mobiliza-tion, especially through innovations that attract rural savings and offer abroader range of banking services, including investment credit.

2.43 Deregulation of short-term lending rates by the Central Bank couldincrease the developmental potential of informal credit by stimulatingcompetition between formal and informal lenders and by eliminating thepre-emptive activities of those having access to low rate, regulated loans.Loans having an original maturity of less than 365 days are the only loanssubject to lending rate ceilings at present, and it is in providing thistype of financial contract that formal and informal credit would be mostcompetitive, given the short-term emphasis of commercial lenders, especiallyinformal ones.

2.44 Changes in other Central Bank regulations that create barriers toentry into innovative finance would also increase the scope for competitiionbetween formal and informal finance. The money shop innovation of thePhilippine Commercial and Industrial Bank (PCI), for example, is a demon-stration of how new, small-scale financial services can be provided by formallenders in market segments where informal lending has a large market share.Regulations that prohibit pawnshops, the formal lending institutions withprobably the highest concentration of clients among the poor, from acceptingdeposits should be re-examined./l The merger of pawning with deposit taking,

/1 CB believes that this is not feasible in view of formidable difficul-ties in monitoring the financial operations and stability of numerouspawn shops.

- 23 -

including rural banks and rural branches of commercial banks, would permitthe poor to enjoy expanded options in liquidity management and would providethe means for introducing them to services that would increase theirwillingness to invest in financial assets, such as deposit accounts.

2.45 It may also appear attractive to promote informal lending throughprograms designed to permit greater access to funds by informal lenders suchas input dealers and rice traders and millers. This approach is exemplifiedin the following ongoing arrangements: Planters Products Inc. currently useslocal input dealers as distribution channels for fertilizer and pesticidecredit; the CB grain-financing program provides funds to rice traders toaugment their working capital; and DBP, LBP and commercial banks extend loansto integrators who in turn provide credit, in cash or kind, to participatinglivestock producers. An evaluation of these programs is important to promotea wider use of similar arrangements and to establish effective monitoringarrangements for ensuring that the greater access given to informal lenders isreflected in their increased lending to clients. Through this strategy, itshould be possible to provide larger resources to the private sector toestablish a network of depots to supply inputs to farmers, either on credit orfor cash, as the retail supplier may consider appropriate. A condition forthe success of this facility would require a means of directing credit towardthose informal lenders currently uneconomically constrained by inadequatecredit. It would also have to be demonstrated that input dealers and othertargeted lenders could increase their net income from lending if more creditwere available to them, and also that the financial institutions passing ongovernment funds could increase their net incomes by participating in such aprogram. Attempts to gather evidence that informal lenders are uneconomicallyconstrained by lack of credit could be difficult, and no research methodologyis readily available that would precisely determine the existence or extent ofthe credit shortage. However, CB through its proposed credit budgetingmechanism should be able to monitor subsectoral and commodity-specific creditflows and, through selective credit measures, regulate the flow of formalsector funds to the private sector intermediaries which use informal lendingarrangements to support agricultural activities. Obviously, any innovationsin expanding the formal sector into the informal credit market should beapplied only after careful consideration.

- 24 -

3. MAJOR TRENDS IN AGRICULTURAL CREDIT /1

A. Introduction

3.01 Production credit for cereal crops is currently provided by theformal credit sector on a limited scale, and the informal credit sectorseems to have replaced formal credit. Financial institutions have becomemore restrictive in defining creditworthy borrowers, with the result thatentrepreneurs of small means tend to be excluded from credit programs.Although credit availability would normally not be a constraint for commer-cial enterprises in view of their capacity to provide collateral, resourceavailability, high arrearage levels and high transaction costs seem to havecontributed to significant credit gaps especially in medium- and long-termcredit and difficulties in mobilizing deposits. Institutional constraintsand a consequent erosion in the sector's capabilities to undertake efficientfinancial intermediation now appear to be a major handicap to the growthobjectives of the country.

/1 Agricultural data in the Philippines include all loan-financing activi-ties relating to agriculture, fisheries and forestry as well as theprocessing, storage and distribution of the resulting products. Thedata are not classified by maturity; thus, for the purpose of analysis,all loans disbursed by the commercial banks including PNB and LBP areconsidered as short-term credit, while those of DBP and thrift banks aremedium-term. Furthermore, the time series on agricultural credit wasmodified as of 1975 to include activities which are agriculture-basedbut classified under industry, e.g., manufacturing and marketing ofinputs like fertilizers, feeds, chemicals, farm implements, andconstruction of warehouses and irrigation systems. For this reason,Tables 3.3 and 3.4 show both the old and new time series. Some data,especially that relating to credit issued by private commercial banksand thrift banks, are based on TBAC estimates.

- 25 -

B. Trends

Increased Use of Noninstitutional Credit

3.02 As noted in para. 2.25, the informal sector currently providesabout 64-78% of the total credit received by the agricultural sector.Informal sources provided an even larger volume of credit, ranging between75-80% of the total, prior to the mid-1970s when formal credit increaseddramatically, largely as part of Government-sponsored supervised creditprograms which made funds available to rural banks under a rediscountingfacility from the Central Bank. In the late 1970s the flow of credit undersupervised credit decelerated because of high default rates on loans, whichcaused a majority of banks to become ineligible for further rediscounting.

Table 3.1: COMPOSITION OF INSTITUTIONAL AND NONINSTITUTIONALCREDIT TO AGRICULTURE /a

(In percent)

Source 1950s Mid-1970s Late 1970s

Institutional 20-25 64-67 22-36Noninstitutional 75-80 31-33 64-78

/a TBAC, "A Study on the Informal Rural Financial Markets in ThreeSelected Provinces in the Philippines," 1980.

Trends in Institutional Credit

3.03 Constraints. The Philippine rural financial sector has beenremarkably responsive to Government's development strategies related tocredit programs and savings mobilization. However, these strategies have ledto a situation in which the performance of the rural financial sector withregard to credit has become increasingly constrained by major institutionalproblems, most notably high levels of arrearages and high transaction costs.The high arrearage levels are in part a product of high default rates onloans made under Government-backed supervised credit programs for farmers, but

- 26 -

also reflect problems specific to the individual institutions. The banksmost affected by this are the PNB, LBP, DBP and, in particular, the ruralbanks. High transaction costs are a problem for banks like PNB and DBPwhich have a comparatively small branch network and a wide operating areafor each outlet. In view of these difficulties, the affected banks havelimited the availability of credit for agricultural development, and havebeen particularly cautious about lending to small farmers and ruralentrepreneurs who lack collateral.

3.04 Credit Trends, 1972-75. The availability of institutional creditfor agriculture expanded rapidly during 1972-75, when lending increased fromabout P 6 billion to P 17.8 billion. At 1975 prices, the increase wasat an average annual rate of 27% (Table 3.2). Production credit increasedduring the period primarily because of a large number of loans for sugarproduction, for which the export market was then buoyant, and sizeabledisbursements under the Government-sponsored Masagana 99 (M-99) programwhich channelled low-interest credit for rice production through PNB, ACAand the RBs. Processing activities in rice, sugar and coconut also receiveda larger share in total credit as did the livestock and fisheriessub sectors.

Table 3.2: AGRICULTURAL LOANS GRANTED BY ACTIVITY, 1972-75(P billion)

1972/a %(at 1975 prices) 1975 increase

Production 4.8 7.3 52Processing 0.9 1.5 66Marketing 4.1 8.9 117

9.8 17.7 81

/a Data base for 1972 is not consistent with that for1975 and should be regarded as indicative.

3.05 The performance of the formal credit system in expanding credit tosmall farmers was notable. The percentage share of total production creditextended to farmers cultivating less than 3 ha increased from 1.6% in 1965 to

- 27 -

19.4% in 1974. This increase was due primarily to loan operations underM-99 (average farm size 1.4 ha) and to ACA and LBP lending to agrarianreform beneficiaries.

3.06 Credit Trends, 1975-80. After 1975, however, the growth ininstitutional credit for agriculture slowed to an annual average of 2.1%(Table 3.3).

Table 3.3: AGRICULTURAL LOANS GRANTED, 1975-80(P billion)

Old series /a New seriesAnnual Annual

At At growth At At growthcurrent 1975 rate current 1975 rate

Year prices prices (%) prices prices (%)

1975 17.8 17.8 - 27.9 27.91976 22.0 20.7 16.0 29.0 27.3 (2.1)1977 22.5 19.6 (5.3)/b 29.2 25.5 (8.0)1978 28.6 23.2 18.3 36.7 29.8 16.91979 36.0 24.6 6.0 45.5 31.0 4.01980 37.8 21.9 (10.9) 53.4 30.9 -

Average annualgrowth rate(1976-80) 4.8 2.1

/a Reflects old time series data base prior to redefinition affect-ing data from 1975 on.

/b Parenthesis indicates negative growth.