iii cfa - cfa.awardspace.comcfa.awardspace.com/level_3/1998_cfa_level3_exam... · cfa chartered...

TRANSCRIPT

CFA Chartered Financial Analysts

III

Exams1998

ASSOCIATION FOR INVESTMENT MANAGEMENT AND RESEARCH

_______________________________1998 Level III Guideline Answers

Morning Section – Page 1

LEVEL III: QUESTION 1

Topic: Portfolio ManagementMinutes: 46

Reading References:“Determination of Portfolio Policies: Institutional Investors,” Ch. 4, Keith P. Ambachtsheer, JohnL. Maginn, and Jay Vawter, Managing Investment Portfolios: A Dynamic Process, 2nd edition,John L. Maginn and Donald L. Tuttle, eds. (Warren, Gorham & Lamont, 1990). “PensionInvesting and Corporate Risk Management,” Roger A. Haugen, Managing Institutional Assets,Frank J. Fabozzi, ed. (HarperCollins, 1990). Cases in Portfolio Management, John W. Peavy IIIand Katrina F. Sherrerd, eds. (AIMR, 1990). “Structured Portfolio Strategies II: LiabilityFunding,” Ch. 22 (Ch.19 in 3rd ed.), Bond Markets, Analysis and Strategies, 2nd or 3rd edition,Frank J. Fabozzi (Prentice–Hall, 1993 or 1996).

Purpose:To test candidates’ ability to identify and integrate the major objectives of pension funds in settinginvestment policy and creating an appropriate asset allocation.

LOS: The candidate should be able to:

“Determination of Portfolio Policies: Institutional Investors” (Session 13)• construct appropriate investment policy statements based on an evaluation of the

characteristics of the assets and liabilities of these institutions.

Pension Investing and Corporate Risk Management” (Session 13)• discuss the relationship between the balance sheet of a corporation’s pension fund and

the corporation itself;• evaluate the effect a corporate pension fund investment policy may have on plan

surplus and the company’s net worth;• appraise the effect that the correlation between a pension plan’s assets and liabilities

• compare the effect of the correlation structure of a company plan’s asset returns with acompany’s operating asset returns on the company’s ability to meet minimum annualpension fund contributions.

_______________________________1998 Level III Guideline Answers

Morning Section – Page 2

Cases in Portfolio Management (Session 21)• discuss the overall portfolio management process leading to the asset allocation

decision, including the information requirements of the objectives/constraints and thecapital market expectation stages of that process;

• contrast the investment objectives and constraints for investors in several differenteconomic circumstances;

• create a formal investment policy statement for a given investor;• recommend and justify a broad asset allocation that would be appropriate for that

investor.

“Structured Portfolio Strategies II: Liability Funding” (Session 8)• design a bond immunization strategy that will ensure the funding of a predetermined

liability or liabilities and determine why and how the portfolio should be adjusted;• construct an immunized portfolio, addressing immunization risk, credit risk, and call

risk.

Guideline Answer

A. Investment Policy Statement Elements and Justification

i. Return requirements. The primary requirement for the active-lives portion of ApexSailboat Corporation’s (ASC’s) pension plan is to achieve a total return sufficient toavoid a long-term shortfall and to meet projected pension liabilities. A long-termgrowth orientation is appropriate. Capital gains are likely to be more important thanincome. Inflation protection is necessary.

Justification. The plan’s return objective should focus on real total returns that willfund its long-term obligations on an inflation-adjusted basis. Because the plan cantake above-average risk and has little need for immediate liquidity, the plan can adoptan aggressive investment course and focus on the higher return potential of capitalgrowth. The board’s objective of a 9 percent return for the active-lives portion of theplan over the long term appears reasonable.

ii. Risk Tolerance. The active-lives pension plan’s risk tolerance indicates an ability toaccept above-average or relatively high portfolio risk to achieve its return objective.

_______________________________1998 Level III Guideline Answers

Morning Section – Page 3

Justification. The recommended above-average risk tolerance for this portion of theplan is justified because• the plan has a small surplus (5 percent of plan assets); that is, the plan is

overfunded by $5 million;• the fund can invest in less liquid assets because of limited near-term payout

requirements and its young workforce;• the company’s balance sheet is strong;• the company has been able to overfund the plan despite operating in a cyclical

industry;• the plan has a long time horizon;• separation has been maintained between the plan and ASC in terms of respective

exposures to the effects of economic fluctuations; the cyclicality of ASC’searnings has not materially affected ASC’s ability to fund the active-lives pensionplan.

iii. Time Horizon. The active-lives portion of ASC’s pension plan has a relatively longtime horizon.

Justification. On average, the plan participants are 39 years old and the duration ofplan liabilities is 20 years. The “time to maturity” of the corporate workforce is akey strategic element for any defined-benefit pension plan. Having a youngerworkforce often means that the plan has a longer investment horizon and moretime available for wealth compounding to occur. These factors justify a relativelylong time horizon as long as ASC remains a viable, going concern.

B. Asset AllocationJustification exists for recommending either Asset Allocation C or Asset Allocation B asbest achieving the three objectives simultaneously.

Justification:

i. Improved risk-adjusted performance. The Sharpe ratio is a common barometer ofrisk-adjusted performance. The Sharpe ratio is an estimate of an investment’s orportfolio’s expected return per unit of risk. Asset Allocation C has a higher Sharperatio than that of the original portfolio (0.35 versus 0.31) and the highest Sharpe ratioof any of the asset allocation choices. This superior risk-adjusted return potentialprobably results from improved diversification in international developed marketequities and emerging market equities. Asset Allocation B is the only other alternativethat has a higher Sharpe ratio than the original asset allocation. The differencebetween the Sharpe ratio for Asset Allocations B and C is small.

_______________________________1998 Level III Guideline Answers

Morning Section – Page 4

ii. Reduced surplus volatility. Asset Allocations A and C include long-term U.S. bondswhich may make these allocations more closely match the stated duration of ACS’sliabilities than do the other allocations. Because long-term bonds are interest sensitive,this type of investment may reduce the volatility of the pension surplus. ASC’sliabilities have a stated duration of 20 years. Therefore, some may view a strategy ofmatching bonds with a 20-year duration to the 20-year-duration liabilities as reducingsurplus volatility. Ongoing pension liabilities, however, are of a type for whichuncertainty exists as to both the amount and timing of the cash outlay because offactors such as varying future inflation and interest rates. In this context, AllocationA, which consists of 100 percent bonds, is not diversified and does not provideprotection against the risk that inflation will increase plan liabilities through inflation-related wage and benefit increases. Allocation C, which consists of 40 percent in 20-year duration bonds and 60 percent in equities, is a better choice than Allocation A.

Some may contend that the asset types that closely mirror economic cycle dependent,going-concern pension liabilities, such as ASC’s, are short-term government bonds orinflation-indexed debt. The apparent match between long-term bonds and 20-year-duration liabilities can disappear if inflation erodes the purchasing power of the fixed-coupon bonds and the company’s competitive position. In this context, long-termbonds can become risky when used to match pension liabilities. From this perspective,Allocation B can be justified because it uses short- and intermediate-term bondscombined with a larger stock component to provide inflation protection for this.

Although Asset Allocation D could be considered for reasons similar to those forAsset Allocation B, it does not meet the board’s return objective and does not improveon the risk-adjusted performance of the original portfolio.

iii. Meeting the return objective. The board’s return objective is 9 percent. AssetAllocations B and C both achieve this long-term return objective as well as orbetter than the original asset allocation and Asset Allocations A and D. Shortfallrisk may be higher for Asset Allocation B than for Asset Allocation C in the shortrun because of its higher projected standard deviation. The long time horizon forthe plan coupled with Asset Allocation B’s greater diversification and better abilityto cope with potential inflation-based liability increases may result in smallershortfall risk for Asset Allocation B over time.

_______________________________1998 Level III Guideline Answers

Morning Section – Page 5

C. Managing Corporate Risk ExposureManaging corporate risk exposure involves incorporating the operational, economic, orfinancial risk characteristics and exposures of the corporation into the pension fundinvestment policy equation. A company might want its pension fund to adopt aninvestment policy that seeks to manage corporate risk exposure for several reasons. Onereason is to increase the probability that the company will be in a comfortable position toincrease its support for the plan if called upon to do so. The strategy for achieving thisobjective focuses on managing plan assets to maintain funded returns while reducing theprobability that adverse developments in the company’s basic business will accompany arequirement to greatly increase corporate contributions to the plan. Implementing thisstrategy requires selecting pension fund investment assets that have a low or negativecorrelation with the company’s basic business.

A second reason for adopting a policy that considers corporate risk exposure is the beliefthat the investment policy should recognize the financial interdependence of the pensionfund’s and the company’s financial affairs. Financial interdependence results from thepension fund’s effect on the company’s balance sheet and earnings. If plan asset growthexceeds liability growth, the sponsor’s required contributions are eventually reduced as abalance sheet surplus builds. Higher reported earnings result from a reduction in requiredcontributions. If liabilities grow faster than assets, the eventual result is a balance sheetdeficiency, a rising contribution rate, and a negative impact on reported earnings. Thisperspective shows that corporate management is correct in controlling pension fund risk atthe corporate level instead of considering risk at the pension fund level separately.

Alternatively, the company might view its pension fund from the perspective of a whollyowned subsidiary of the plan sponsor. Constituents thus are not only plan beneficiariesbut also customers, employees, and suppliers (including creditors). These constituents arejointly concerned about maintaining a prolonged, stable relationship with a healthycompany. They are interested in the company’s survival. Also, their welfare is enhancedby optimal risk management in the pension plan in the same way that their welfare isenhanced by insuring the main plant against fire. Having a pension plan investment policythat considers corporate risk exposure may provide, among other things, an increasedlevel of product demand from customers, lessened wage pressures from employees, betterprices or service from suppliers, and more favorable financing terms from creditors.

D. Reducing Corporate Risk ExposureAn asset allocation strategy that takes into account the risk exposures of the corporationwould avoid assets that are expected to underperform when the company isunderperforming. ASC is a leading producer of luxury sailboats, and all of its revenuescome from the United States. Therefore, ASC would be vulnerable if a U.S. recessionwere to occur.

_______________________________1998 Level III Guideline Answers

Morning Section – Page 6

i. International emerging market equities. Investing in the securities of emerging foreignmarkets could be justified as potentially reducing the corporate risk exposure of theactive-lives portion of ASC’s pension plan. International emerging markets have had alow correlation with the U.S. market. Thus, increasing pension fund investment ininternational emerging markets could reduce the probability that adversity in thecompany’s basic business (because of a weak domestic economy) would coincide withdeterioration in funded status requiring increases in contributions.

Using international emerging market equities could reduce risk within the pension fundand could provide potentially higher returns. The risk reduction reduces surplusvolatility and the potentially higher returns reduce the probability of future fundingshortfalls.

ii. U.S. long-term bonds. Long-term U.S. bonds could also be used to reduce the riskexposures of ASC. Lower long-term interest rates often characterize times ofeconomic weakness. Lower rates are favorable for interest-sensitive long-term fixed-income investments. Therefore, high-quality U.S. long-term bonds could provide aneffective means of diversifying the threat posed to ASC during a recession. Thepension plan’s bond exposure would increase in value relative to a decrease in thegeneral level of interest rates.

ACS could also use U.S. long-term bonds to implement a duration-matching strategyfor the active-lives plan liabilities. This strategy might minimize surplus volatility andreduce the correlation between plan contribution requirements and the ability of thecompany’s basic business to fund future pension contributions.

U.S. long-term bond returns also have a low correlation with equity returns. Addingbonds would thus reduce the portfolio’s risk and the probability that the company willhave to increase plan contributions if the company’s business falters.

E. Duration-Matched Strategies for the Retired-Lives PortionThe objective in constructing a duration-matched portfolio is to match the duration of theasset portfolio to the duration of the plan liabilities, which minimizes the risk of notachieving the target yield. Weaknesses in duration-matched strategies could affect theability of the retired-lives pension plan to meet its cash flow requirements. The followingare weaknesses in the asset allocations suggested by each of the managers:

Common Weakness of All Three StrategiesEach strategy is duration matched but not cash matched. (1) Therefore, over time, cashsurpluses or cash deficits will occur. These surpluses (deficits) will force the plan toreinvest surpluses (sell bonds) and expose the plan to reinvestment risk (price risk). (2)Also, if a nonparallel shift in the yield curve occurs, simple duration-matched strategiesmay not effectively immunize against losses.

Common Weaknesses of Managers B’s and C’s Strategies

_______________________________1998 Level III Guideline Answers

Morning Section – Page 7

(1) Corporate bonds have default risk. By investing in corporate bonds, the plan isexposing itself to the possibility of capital loss from default. This loss would seriouslyimpair the plan’s ability to meet cash flow requirements.

(2) Corporate bonds have credit risk. By investing in corporate bonds, the plan is

exposing itself to the possibility of credit-rating downgrades. A downgrade wouldreduce the plan’s ability to achieve the target rate of return if the fund needed torebalance by selling bonds.

(3) The government bonds have reinvestment risk because they are coupon bearing. A

reduction in the reinvestment rate would impair the plan’s ability to achieve its targetrate of return.

Weaknesses of Manager A’s Strategy

(1) George Fletcher intends that the portfolio fund the retired-lives portion of thecompany’s pension plan. Because zero-coupon government bonds do not provide anincome return, the zero-coupon bond strategy is poorly suited to funding the ongoingliabilities. This strategy requires constant rebalancing as the fund sells zeros toproduce cash flow and exposes the plan to price risk that might affect the plan’s abilityto achieve its target rate of return.

(2) The yield on zero-coupon bonds is typically lower than the yield on coupon bonds.

For example, Manager A has the lowest target yield of the three strategies. ManagerA’s strategy is expensive to construct.

Weaknesses of Manager B’s Strategy

Manager B has no unique weaknesses.

Weaknesses of Manager C’s Strategy

Manager C’s strategy is exposed to call risk. Call risk can impair the plan’s ability toachieve the target return in several ways:

• Callable bonds have limited upside potential when interest rates fall.• Callable bonds have reinvestment risk if they are called.• Callable bonds have an effective duration that may differ from the reported

duration.

_______________________________1998 Level III Guideline Answers

Morning Section – Page 8

Note to candidates on Question 1: In this question, candidates were told that each manager’sduration-matched strategy had a 10-year duration. Candidates should be aware that portfolioduration is calculated using the market value weighted average duration of the asset classescomposing the portfolio. If the managers’ portfolio allocations were interpreted as marketvalue weights, only Manager A’s portfolio would have a duration of 10 years and the portfolioduration for Managers B and C would be less than 10 years.

_______________________________1998 Level III Guideline Answers

Morning Section – Page 9

LEVEL III: QUESTION 2

Topic: Global/Asset Valuation: EquityMinutes: 38

Reading References:“Disentangling Equity Return Regularities,” Bruce I. Jacobs and Kenneth N. Levy, andEngineered Investment Strategies: Problems and Solutions,” Robert L. Hagin, Equity Marketsand Valuation Methods (AIMR, 1988). The New Finance: The Case Against Efficient Markets,Robert A. Haugen (Prentice-Hall, 1995).

Purpose:• To test candidates’ understanding of the various explanations that have been advanced to

explain the occurrence and persistence of the value-versus-growth effect.• To test candidates’ understanding of the difference between naive and pure or independent

effects.• To test candidates’ understanding of the potential problems relating to the design and

implementation of quantitative investment strategies.

LOS: The candidate should be able to:

“Disentangling Equity Return Regularities” (Session 7)• describe various stock market anomalies (return regularities) and demonstrate an

understanding of how the interrelationships of anomaly-based models can be“disentangled” to produce a “pure return effect”;

• evaluate the implications of this research for the efficient market hypothesis and asset-pricing models.

“Engineered Investment Strategies: Problems and Solutions” (Session 7)• describe the characteristics of an engineered investment strategy;• illustrate the potential problems with the design or implementation of engineered

investment strategies;• compare the assumption that companies with high returns on equity are "good" with

the assertion that value stocks outperform growth stocks (refer to Reading 3).

The New Finance: The Case Against Efficient Markets (Session 7)• evaluate the concept of efficient markets and discuss how recent empirical research has

led many to question its validity;• appraise the premise that value stocks provide higher returns than growth stocks;• construct a portfolio that attempts to exploit the contention that markets tend to be

overreactive and inefficient.

_______________________________1998 Level III Guideline Answers

Morning Section – Page 10

Guideline Answer

A. Discussion of ExplanationsThe first explanation of the value-versus-growth effect is that the empirically observedpositive return spread between value and growth stocks represents a risk premium. Thatis, investors expect the positive return spread as a reward for taking on higher risk. Thisexplanation is consistent with the efficient market hypothesis. According to someresearchers, a characteristic of low price-to-book (P/B) or low price-to-earnings (P/E)stocks is that they have poor earnings growth prospects. Also, investors do not highlyregard low-expectation firms. Therefore, investing in such stocks represents a risk(distress) and presents discomfort for some investors. Consequently, investors require ahigher expected return to entice them to invest in these securities. The ex post positivereturn spread between value and growth stocks represents nothing more than therealization of an expected risk premium.

The second explanation of the value-versus-growth effect is that the ex post positivereturn spread between value and growth stocks represents a surprise caused by mispricingof securities. This explanation is inconsistent with the efficient market hypothesis.According to some researchers, the mispricing occurs because stock markets are initiallyslow to react and then overreact to information about earnings. Inertia and positivemomentum characterize short-run price behavior. The market seems to price growthstocks as if their above-average relative earnings growth will continue for a very long timein the future and price value stocks as if their earnings will continue to be depressed for along time. Earnings have a tendency to revert to the mean, however, in a short time span(four to five years). When the reversion happens, the market is surprised and returns fromgrowth (value) stocks tend to be low (high).

B. Support of Julia Smith’s StatementSmith's assertion is correct. Single-factor models have not demonstrated an ability toisolate the pure or independent effect of one variable. Some studies have examined onlyone factor and used the findings to support the notion that markets are inefficient. Othershave shown that single-variable effects are not distinguishable; a web of interrelationshipsappears to exist among various anomalies. For example, Jacobs and Levy showed thatlow price/cash flow is a significant anomaly in its naive form but it tends to becomeinsignificant in its pure form. Other studies have showed that size and low-P/E effects areindependent. That is, after controlling for size, the low-P/E effect still prevails and viceversa. These results highlight the importance of determining whether an anomaly is a pureone or simply a naive proxy for some other variable(s) before using the anomaly in anactive investment strategy. If the model does not incorporate the variable driving theanomaly, a strategy based on the model is unlikely to produce the promised results.

_______________________________1998 Level III Guideline Answers

Morning Section – Page 11

According to the data appearing in Table 4, the lowest-P/B stocks (Portfolios 1 and 2)appear to provide a higher return than the market over the study period. Whether thisresult is a pure effect is unclear. For example, average size and average stock price arealso lowest for stocks in Portfolios 1 and 2. Both average market capitalization andaverage price per share increase steadily when moving from Portfolio 1 to Portfolio 10.Thus, the results could capture a small-capitalization effect, a low-price-per-share effect,or both. Therefore, Joe Brown should determine whether the P/B effect is a pure one or aproxy for either a size effect or a low-price-per-share effect or both before recommendingthat Smith use this stock selection strategy.

C. Biases in Brown’s Research Design

i. Survivorship bias. A test design is subject to survivorship bias if it fails to accountfor companies that have gone bankrupt, merged, or are otherwise “dead.” In thisexample, Brown used the current list of FTSE 900 stocks rather than the actual listof stocks that existed at the start of each test year. To the extent that thecomputation of returns excluded dead companies, the performance of Portfolios 1and 2 is subject to survivorship bias and may be overstated.

ii. Look-ahead bias. A test design is subject to look-ahead bias if it uses informationthat was unavailable on the test date. In this example, Brown conducted the testassuming that the necessary accounting information was available at the end of thefiscal year. For example, Brown assumed that book value per share for fiscal 1987was available on December 31, 1986. Because this information is not released forseveral months after the close of a fiscal year, the test may have contained look-ahead bias. This bias favors a strategy based on the information because itassumes perfect forecasting ability.

iii. Time-period bias. A test design is subject to time-period bias if it is based on ashort time period, which may make the results time-period specific. Although thetest covered a period extending over the past 10 years, the test had only 10 datapoints because the investment horizon was 1 year. This period may be too shortfor testing an anomaly. Also, this period may not have included a completebusiness cycle. Ideally, Brown should test market anomalies over several businesscycles to ensure that results are not period specific. This bias can favor a proposedstrategy if the time period chosen is favorable.

_______________________________1998 Level III Guideline Answers

Morning Section – Page 12

iv. Portfolio-weighting bias. A test design is subject to portfolio-weighting bias if thetest results are compared with a benchmark that uses a different weighting scheme.In this example, the test results are shown in terms of excess returns (portfolioreturns minus FTSE All Share Index returns). Because the portfolio returns wereequally weighted and the FTSE returns are capitalization weighted, the two returnseries are not directly comparable. Brown’s equal weighting scheme exaggeratedthe influence of small-cap stock performance on the model results. This bias couldfavor the value strategy because of a small-firm effect. Brown should compare thecap-weighted return on the portfolios with FTSE returns to compute excessreturns.

D. Implementing Brown’s Strategy

i. Benchmark and performance evaluation issues. The existing equity portfoliosmanaged by Global Alpha Investors (GAI) use FTSE 100 as the benchmark, butthe test results are shown relative to the FTSE All Share index. Thus, the resultsare not directly applicable to the GAI portfolios. Also, existing U.K. equitymandates require GAI to outperform the benchmark over rolling three-yearperiods. The test results present the average annual excess return only over the1987–97 period. These results do not clearly show, therefore, whether thestrategy would have outperformed the market over rolling three-year periods.Brown needs to conduct more research in this area before recommending astrategy.

An inappropriate reference portfolio also raises risk management and equity styleissues. For instance, the proposed strategy requires investing in Portfolio 1 stocksonly. Based on data in Table 4, these stocks appear to be small-cap stocks withaverage market capitalization of only £200 million. Most of these stocks areunlikely to be in the FTSE 100 index. Investing solely in these stocks would meaninvesting in many stocks that are not in the benchmark and would result in largeportfolio tracking errors relative to the FTSE 100 benchmark. These trackingerrors would be inconsistent with the aggressive excess return requirement of 200basis points (bps) a year. Because current U.K. equity mandates managed by GAIspecify the FTSE 100 as the benchmark, GAI manages large-cap U.K. equityportfolios for their clients. The proposed strategy, however, would requireinvesting in small-cap issues, which may violate existing mandates and may beunacceptable to GAI's clients.

_______________________________1998 Level III Guideline Answers

Morning Section – Page 13

ii. Turnover, trade size, and transaction costs. The test results do not indicate howmuch turnover the proposed strategy would generate. Furthermore, the excessreturns for the various portfolios in Table 4 are not shown net of transaction costs.These costs are critical in the case of the proposed strategy because it involvesbuying small-cap stocks, which have high transaction costs. Once Brown factorsin these costs, the proposed strategy may be unable to deliver returns 200 bps ayear above the benchmark returns. GAI currently has £5 billion in U.K. equitiesunder management. Because of the large size of funds under management, theproposed strategy of investing solely in the lowest-P/B stocks (Portfolio 1) couldbe difficult to implement. The average market capitalization of stocks appearing inPortfolio 1 is only £200 million. To implement the proposed strategy, GAI wouldhave to take substantial ownership positions in many of these stocks, which GAIand/or its institutional clients may not want to do for various reasons. The lack ofliquidity, coupled with substantial equity ownership stakes, suggests high market-impact costs.

_______________________________1998 Level III Guideline Answers

Morning Section – Page 14

LEVEL III: QUESTION 3

Topic: Asset Valuation: Fixed IncomeMinutes: 12

Reading References:“International Bond Portfolio Management,” Ch. 26, Christopher B. Steward and J. Hank Lynch,Managing Fixed Income Portfolios, Frank J. Fabozzi, ed. (Frank J. Fabozzi Associates, 1997).“Using International Economic Inputs,” Jeffrey J. Diermeier, Improving the Investment DecisionProcess—Better Use of Economic Inputs in Securities Analysis and Portfolio Management(AIMR, 1992).

Purpose:To test candidates’ ability to disentangle currency from asset returns and to differentiate betweensuccessful domestic and global investment strategies.

LOS: The candidate should be able to:

“International Bond Portfolio Management” (Session 9)• discriminate between the challenges faced by a domestic bond portfolio manager and

an international bond portfolio manager by citing specific common responsibilities andresponsibilities that differ;

• support the assertion that market dynamics and noncorrelation properties makeinternational bond investments behave more like domestic equity investments than likedomestic bond investments;

• determine why—of five broad strategies that include currency selection, bondselection, duration management, sector/credit/security selection, and outsidebenchmark investing—currency and bond selection provide the majority of returns (orlosses) to international portfolios (i.e., describe limits to duration management ininternational markets).

“Using International Economic Inputs” (Session 5)• demonstrate a method of integrating the risky-asset decision (i.e., country and asset

selection) with the currency decision in a global portfolio.

Guideline Answer

A. Effect of Changes in U.S. DollarThe difference between the hedged and unhedged returns is a function of fluctuations inthe currency return over the time period studied. Over the five-year period, the U.S.dollar was relatively weak against other currencies, causing the unhedged index tooutperform the hedged by 8.7 percentage points. For the recent one-year period, the U.S.dollar strengthened against other currencies. The index returns hedged into U.S. dollarsincreased by 5.5 percentage points because of the relative dollar strength.

_______________________________1998 Level III Guideline Answers

Morning Section – Page 15

B. Transferability of Duration and Sector ManagementDuration Management is more difficult in international fixed-income investing becausefew non U.S. bond markets have liquid issues with maturities greater than 10 years. Mostnon U.S. bond markets also lack the broad range of instruments, such as strips and repos,that allow low-cost duration management in the U.S. market. Although interest ratefutures are available in most non U.S. markets and offer a low-cost vehicle, they arelimited typically to the short end of the term structure. Swap markets are liquid andgenerally available but pose challenges in counterparty credit and technical and operationalbarriers. A U.S. bond portfolio’s duration, benchmarked to the U.S. yield curve, ismanaged in the aggregate. Managing the durations of international portfolios against anaggregate benchmark can be difficult because of the differing volatility and correlationcharacteristics among the markets composing the index.

Sector management is also difficult outside the United States. A scarcity of corporatebonds often exists outside the United States because of policies favoring the raising ofcapital through bank financing and equity issuance. Market anomalies can arise fromdiffering tax treatments among markets. Implementing some sector managementstrategies may be difficult because mortgage markets and the derivative instrumentsproduced by that sector may not exist to the extent available in the United States.

_______________________________1998 Level III Guideline Answers

Morning Section – Page 16

LEVEL III: QUESTION 4

Topic: EconomicsMinutes: 22

Reading Reference:“The Effects of Budget Deficit Reduction on the Exchange Rate,” Craig S. Hakkio, EconomicReview (Federal Reserve Bank of Kansas City, Third Quarter 1996).

Purpose:To test candidates’ understanding of the immediate, (direct) effects and the long-term, (indirect)effects of budget reduction on the foreign exchange rate; understanding of the different effects ofdifferent fiscal policies on the exchange rate, and ability to identify the conditions necessary for astrengthening in an exchange rate.

LOS: The candidate should be able to:

"The Effects of Budget Deficit Reduction on the Exchange Rate” (Session 5)• compare and contrast the direct and indirect effects of a country’s budget deficit

reduction on the domestic demand for funds and the resultant effects on the country’sexchange rate;

• evaluate the effects of a country’s fiscal and monetary policies on domestic budgetdeficit reduction and explain how they affect the country’s exchange rate;

• discuss the conditions that are necessary for budget deficit reduction to strengthen acountry’s exchange rate.

Guideline Answer

A. Direct Effects of a Reduction in Budget Deficit on:

i. Demand for loanable funds. The immediate (direct) effect of reducing the budget deficit isto reduce the demand for loanable funds because the government needs to borrow less tobridge the gap between spending and taxes.

ii. Nominal interest rates. The reduced public-sector demand for loanable funds has thedirect effect of lowering nominal interest rates because lower demand leads to a lowercost of borrowing.

iii. Exchange rates. The immediate (direct) effect of the budget deficit reduction is adepreciation of the domestic currency and the exchange rate. As investors sell lower-yielding Country M securities to buy the securities of other countries, Country M’scurrency will come under pressure and Country M’s currency will depreciate.

_______________________________1998 Level III Guideline Answers

Morning Section – Page 17

B. Support for Helga Wu’s PositionCountry M’s foreign exchange rate will strengthen because of the changes the budgetdeficit reduction will cause in:

i. Expected inflation rates. In the case of a credible, sustainable, and large reductionin the budget deficit, reduced inflationary expectations are likely because thecentral bank is less likely to “monetize” the debt by printing money. Theseexpectations should reduce the inflation premium in the bond markets, resulting inlower nominal interest rates. Lower nominal interest rates, combined with lowerinflation expectations, typically lead initially to an increase in the real interest rate.That is, the decline in nominal interest rates is less than the decline in inflation. Ifconfidence exists in the monetary authorities, the deficit reduction will tend tostrengthen the exchange rate.

Purchasing power parity and international Fisher relationships suggest that acurrency should strengthen against other currencies when expected inflation in thecountry declines relative to inflation in other countries. That is, higher relative realinterest rates in Country M should lead to a rise in demand for Country M’ssecurities and its currency.

ii. Expected rates of return on domestic securities. The effect would be to increase

the expected return on domestic securities. A reduction in government spendingwould tend to shift resources into private-sector investments, where productivity isgenerally assumed to be higher. A reduction in the budget deficit could also resultin a lower future tax rate and reduced economic inefficiencies, both of whichshould result in higher returns for financial securities. The net effect would be tostrengthen the foreign exchange rate.

Both effects of a reduction in the budget deficit would lead to a stronger currency as aresult of stronger private-sector demand for domestic securities. In a country where thereduction is viewed as credible, long term, and sustainable, reduced public-sector demandfor resources and improved prospects for private-sector real investment will encourageprivate investors. The favorable changes in inflation expectations, after-tax returns ondomestic securities, public-sector versus private-sector allocation, and other issues thatwould typically accompany a government budget deficit reduction will increase the relativedemand for domestic securities and will strengthen the foreign exchange rate.

_______________________________1998 Level III Guideline Answers

Morning Section – Page 18

LEVEL III: QUESTION 5

Topic: Portfolio ManagementMinutes: 16

Reading References:Performance Presentation Standards, 1st edition, including appendixes (AIMR, 1993) and theDescription of Change included in the CFA Level III Candidate Readings OR AIMR PerformancePresentation Standards Handbook, 2nd edition, including appendixes (AIMR, 1997).“Moosehead Investment Management,” Jonathan J. Stokes, Standards of Practice Casebook(AIMR, 1996).

Purpose:To test candidates’ understanding of the requirements of the AIMR Performance PresentationStandards.

LOS: The candidate should be able to:

Performance Presentation Standards, including appendixes (Session 19)• evaluate a sample performance presentation to determine whether the presentation

complies with the AIMR-PPS standards;• describe and explain deviations from the AIMR-PPS standards.

“Moosehead Investment Management” (Session 19)• evaluate a performance presentation to determine violations of the AIMR-PPS

standards and the AIMR Standards of Professional Conduct (see Sessions 2–4);• evaluate the responsibilities of multiple supervisors in accordance with AIMR’s

Standards of Professional Conduct (see Sessions 2–4).

Guideline Answer

Any four of the following six answers would constitute a complete answer:

The AIMR-PPS standards require firms to:

• present annual returns for 10 years (or since inception of the firm). The Everleigh AssetManagement (EAM) presentation includes return calculations for 10 years, but thepresentation does not provide annual returns for the 10-year history of the composites.

• provide the number of portfolios in each composite. EAM does not disclose this informationin the presentation.

• provide the amount of assets in a composite. EAM does not disclose this information in thepresentation.

_______________________________1998 Level III Guideline Answers

Morning Section – Page 19

• provide the percentage of the firm’s total assets that each composite represents. EAMdiscloses total firm assets but does not disclose the percentage of firm assets that eachcomposite represents.

• disclose composite dispersion for each composite. EAM does not disclose this information inthe presentation.

• disclose whether performance results are calculated gross or net of fees, what the firm’s feeschedule is, and for net results, the weighted average management fee. EAM does notdisclose this information in the presentation.

_______________________________1998 Level III Guideline Answers

Morning Section – Page 20

LEVEL III: QUESTION 6

Topic: Ethical and Professional StandardsMinutes: 12

Reading Reference:Standards of Practice Handbook, 7th edition (AIMR, 1996), pp. 11–18, 83–93, 139–146.

Purpose:To test candidates’ understanding of the requirements of the AIMR Standards of ProfessionalConduct concerning knowledge of and compliance with governing laws and regulations, and thefollowing standards: Use of Material Nonpublic Information, Fiduciary Duty (Soft Dollars),Priority of Transactions, and Disclosure of Referral Fees.

LOS: The candidate should be able to:

Standards of Practice Handbook (Session 2)• appraise behavior that could lead to potential or actual violations of the Code and

Standards;• determine actions that should be taken to correct or avoid violations of the Code and

Standards.

_______________________________1998 Level III Guideline Answers

Morning Section – Page 21

Guideline Answer

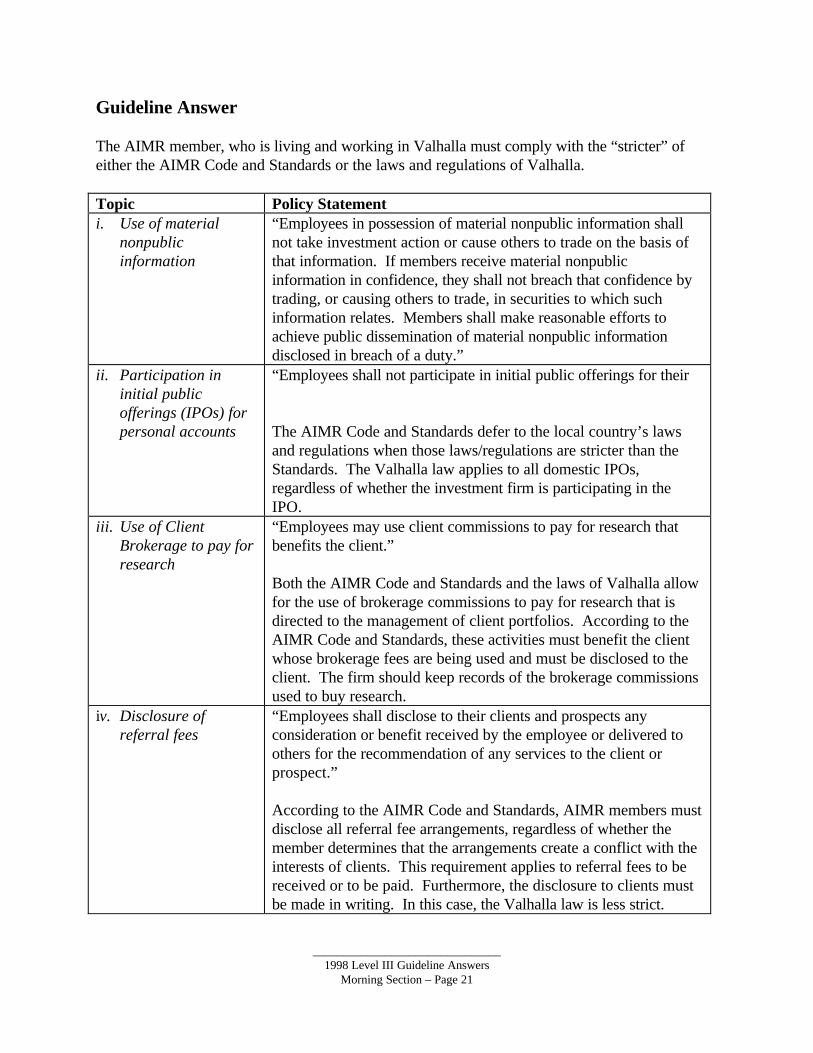

The AIMR member, who is living and working in Valhalla must comply with the “stricter” ofeither the AIMR Code and Standards or the laws and regulations of Valhalla.

Topic Policy Statementi. Use of material

nonpublicinformation

“Employees in possession of material nonpublic information shallnot take investment action or cause others to trade on the basis ofthat information. If members receive material nonpublicinformation in confidence, they shall not breach that confidence bytrading, or causing others to trade, in securities to which suchinformation relates. Members shall make reasonable efforts toachieve public dissemination of material nonpublic informationdisclosed in breach of a duty.”

ii. Participation ininitial publicofferings (IPOs) forpersonal accounts

“Employees shall not participate in initial public offerings for their

The AIMR Code and Standards defer to the local country’s lawsand regulations when those laws/regulations are stricter than theStandards. The Valhalla law applies to all domestic IPOs,regardless of whether the investment firm is participating in theIPO.

iii. Use of ClientBrokerage to pay forresearch

“Employees may use client commissions to pay for research thatbenefits the client.”

Both the AIMR Code and Standards and the laws of Valhalla allowfor the use of brokerage commissions to pay for research that isdirected to the management of client portfolios. According to theAIMR Code and Standards, these activities must benefit the clientwhose brokerage fees are being used and must be disclosed to theclient. The firm should keep records of the brokerage commissionsused to buy research.

iv. Disclosure ofreferral fees

“Employees shall disclose to their clients and prospects anyconsideration or benefit received by the employee or delivered toothers for the recommendation of any services to the client orprospect.”

According to the AIMR Code and Standards, AIMR members mustdisclose all referral fee arrangements, regardless of whether themember determines that the arrangements create a conflict with theinterests of clients. This requirement applies to referral fees to bereceived or to be paid. Furthermore, the disclosure to clients mustbe made in writing. In this case, the Valhalla law is less strict.

_______________________________1998 Level III Guideline Answers

Morning Section – Page 22

LEVEL III: QUESTION 7

Topic: Portfolio ManagementMinutes: 22

Reading References:“Determination of Portfolio Policies: Institutional Investors,” Ch. 4, pp. 26–38, Keith P.Ambachtsheer, John L. Maginn, and Jay Vawter, Managing Investment Portfolios: A DynamicProcess, 2nd edition, John L. Maginn and Donald L. Tuttle eds. (Warren, Gorham, & Lamont,1990). “Endowment Management,” David F. Swenson, Investment Policy (AIMR, 1994).

Purpose:To test candidates’ knowledge of issues relating to endowment fund management.

LOS: The candidate should be able to:

“Determination of Portfolio Policies: Institutional Investors” (Session 13)• identify the return objectives and risk tolerances of endowment funds, including

spending rate and inflation rate considerations.

“Endowment Management” (Session 13)• identify the elements of the investment process for an endowment fund, beginning with

goals and philosophy and ending with portfolio construction and policy revision;• construct a set of investment policies and a compatible asset allocation intended to

cope with competing needs, such as cash flow to supplement an operating budget andpreservation of the purchasing power of assets.

Guideline Answer

A. Implications of Conflicting Objectives

Endowments have conflicting objectives between current beneficiaries and futurebeneficiaries. Conflicting objectives lead to different perspectives on optimal assetallocations. The spending policy and asset allocation should be used to balance the needsof the different beneficiaries.

i. Spending policy. Current beneficiaries prefer to maximize current payout at theexpense of the future. They have minimal interests in preserving an inflation-adjustedincome stream over the long run.

Future beneficiaries prefer to maximize future payout at the expense of currentbeneficiaries. Therefore, future beneficiaries desire a payout that not only preservesthe real income stream but also provides real growth in the income stream. Futurebeneficiaries want to limit the current payout to provide the maximum future payout.

_______________________________1998 Level III Guideline Answers

Morning Section – Page 23

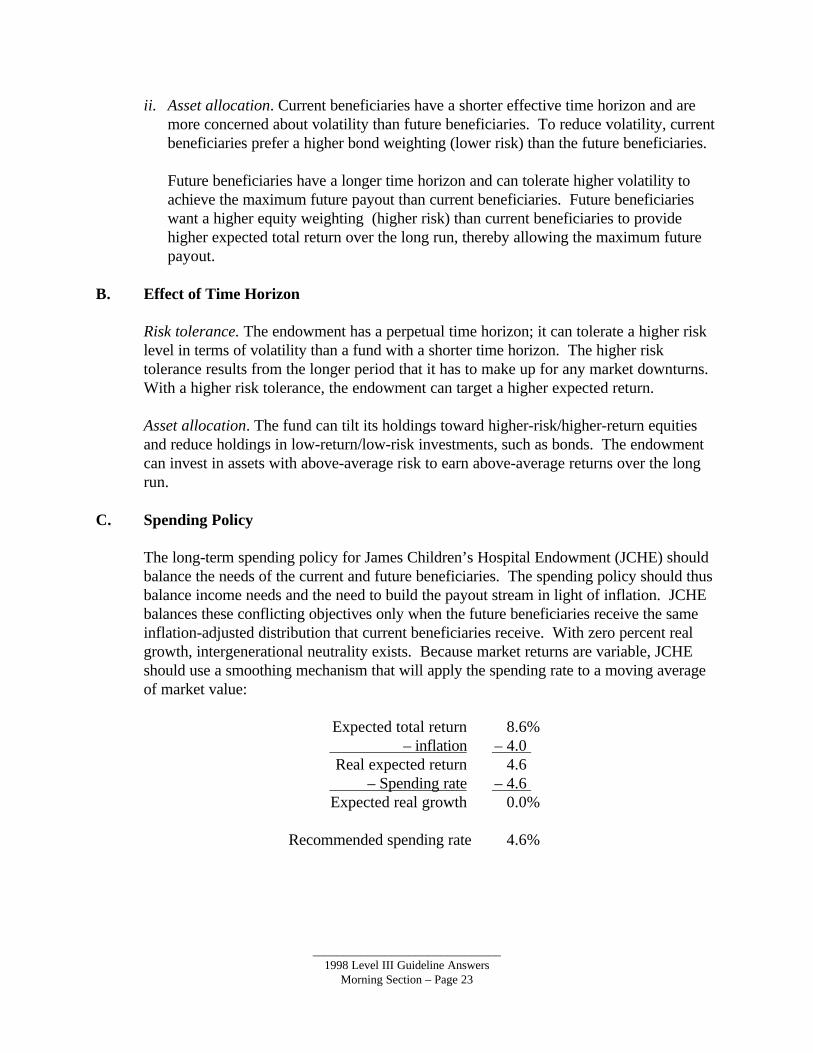

ii. Asset allocation. Current beneficiaries have a shorter effective time horizon and aremore concerned about volatility than future beneficiaries. To reduce volatility, currentbeneficiaries prefer a higher bond weighting (lower risk) than the future beneficiaries.

Future beneficiaries have a longer time horizon and can tolerate higher volatility toachieve the maximum future payout than current beneficiaries. Future beneficiarieswant a higher equity weighting (higher risk) than current beneficiaries to providehigher expected total return over the long run, thereby allowing the maximum futurepayout.

B. Effect of Time Horizon

Risk tolerance. The endowment has a perpetual time horizon; it can tolerate a higher risklevel in terms of volatility than a fund with a shorter time horizon. The higher risktolerance results from the longer period that it has to make up for any market downturns.With a higher risk tolerance, the endowment can target a higher expected return.

Asset allocation. The fund can tilt its holdings toward higher-risk/higher-return equitiesand reduce holdings in low-return/low-risk investments, such as bonds. The endowmentcan invest in assets with above-average risk to earn above-average returns over the longrun.

C. Spending Policy

The long-term spending policy for James Children’s Hospital Endowment (JCHE) shouldbalance the needs of the current and future beneficiaries. The spending policy should thusbalance income needs and the need to build the payout stream in light of inflation. JCHEbalances these conflicting objectives only when the future beneficiaries receive the sameinflation-adjusted distribution that current beneficiaries receive. With zero percent realgrowth, intergenerational neutrality exists. Because market returns are variable, JCHEshould use a smoothing mechanism that will apply the spending rate to a moving averageof market value:

Expected total return 8.6% – inflation – 4.0 Real expected return 4.6

– Spending rate – 4.6 Expected real growth 0.0%

Recommended spending rate 4.6%

_______________________________1998 Level III Guideline Answers

Morning Section – Page 24

The optimal spending rate is 4.6 percent of assets. At this payout, the payout plusinflation equals the expected return on the portfolio. Spending above this level will lead toa declining real value of the assets because the spending rates plus inflation will be abovethe actual return on the portfolio. Spending rates below 4.6 percent indicate that the fundis allowing real growth and not maintaining intergenerational neutrality.

_______________________________1998 Level III Guideline Answers

Morning Section – Page 25

LEVEL III: QUESTION 8

Topic: Global Markets and InstrumentsMinutes: 6

Reading References:“ Emerging Markets: A Quantitative Perspective,” Arjun B. Divecha, Jaime Drach, and DanStefek, Journal of Portfolio Management (Institutional Investor, Fall 1992). “Industry versusCountry Correlations,” Andrew Rudd, Investing Worldwide IV (AIMR, 1994).

Purpose:• To test candidates’ understanding of multifactor models, country models, and industry

models• To test candidates’ understanding of the importance of country factors in generating excess

returns in emerging markets and developed markets.

LOS: The candidate should be able to:

“Emerging Markets: A Quantitative Perspective” (Session 6)• determine the implications of country selection vs. industry or stock selection in

portfolio management.

“Industry versus Country Correlations” (Session 14)• contrast the relative importance of country factors and industry factors in stock market

returns, citing examples in which the country factor is likely to be more important andexamples in which the industry factor is likely to be more important;

• demonstrate the effect on portfolio management of the more segmented vs. the moreintegrated country markets.

_______________________________1998 Level III Guideline Answers

Morning Section – Page 26

Guideline Answer

Usefulness of Two Models

i. Country factor model. An industry factor model looks at only the proportion of excessreturns explained by the industry in which a company operates, regardless of the countryand risk factors. The country factor model looks at the proportion of excess returnsexplained by the country factors alone without considering the industry and risk factors.A country factor model would be more useful than an industry factor model for valuingemerging market stocks because emerging markets are generally homogeneous. That is,individual emerging market securities tend to have a high correlation with that country’smarket. The cause may be that emerging markets are concentrated, which means that fewindustries or several large companies dominate the market. Emerging markets also havehigher volatility and are less well developed and integrated than developed markets.Empirical studies show that country factor models are better than industry factor modelsat explaining excess returns in emerging markets for several reasons. First, a few largecompanies tend to dominate emerging markets. Second, market forces tend to unify thesemarkets. Third, emerging markets exhibit a strong positive relationship between R2 andmarket volatility. In the data presented in Table 6, the country factor model has a higherR2 than the industry factor model.

ii. Multifactor model. Multifactor models are more useful than industry factor models for

valuing emerging market stocks. Adding more factors to a model typically increases itsexplanatory power. In the data presented in Table 6, the multifactor model has a higheradjusted R2 than the industry factor model. The data also show that the multifactor modelfor emerging markets explains more than three times as much of the variation in excesslocal returns than the industry factor model alone.

For most emerging market stocks, the country factor is more important than the industryfactor. Therefore, any model incorporating a country factor has more explanatory powerthan one that does not. In those few cases—where industries are integrated acrosscountries, such as banking, oil, mining, and forest products—models with a country factormay not work as well as industry models.

_______________________________1998 Level III Guideline Answers

Afternoon Section – Page 27

LEVEL III: QUESTION 9

Topic: Global Markets and InstrumentsMinutes: 12

Reading References:“Investing in Emerging Markets,” Ch.1 and “Risks of Investing in Emerging Markets,” Ch. 2, TheIrwin Guide to Investing in Emerging Markets, Marjorie T. Stanley (Richard D. Irwin, 1995).“Valuation Techniques for Emerging Markets,” Donald M. Krueger, Managing EmergingMarket Portfolios (AIMR, 1994).

Purpose:To test candidates’ understanding of the risks of investing in emerging markets.

LOS: The candidate should be able to:

“Investing in Emerging Markets” (Session 6)• summarize the problems or constraints facing the emerging market investor.

“Risks of Investing in Emerging Markets” (Session 6)• discuss the risks involved in investing in emerging markets.

Valuation Techniques for Emerging Markets (Session 6)• discuss the problems that can arise when investing in emerging markets.

Guideline Answer

i. Accounting conventions. Accounting conventions, standards, and systems in emergingmarkets may differ markedly from those in developed markets. Accounting standards maybe nonexistent in some countries. Financial reporting by emerging market companies maybe unreliable or inadequate. Although locally prepared financial statements may refer to“GAAP”, the reference may be to local generally accepted accounting principles, not U.S.GAAP.

When working with companies in emerging markets, investors should be careful ininterpreting financial statements and in performing comparative financial ratio analysis.Financial ratios such as price-to-book, earnings-to-price, and cash flow ratios may differdepending on the convention used. Data may not be comparable, and financial statementsmay not be audited. Inflation adjustments may also vary among countries.

_______________________________1998 Level III Guideline Answers

Afternoon Section – Page 28

ii. Settlement risk. Investors are more likely to encounter settlement problems in emergingmarkets than in developed markets. Settlement risk is the risk that a trade may not besettled accurately or in a timely manner because of inadequate settlement procedures, poormanagement, or other factors. In some emerging markets, settlement may not occur at all.In addition, costs of settlement can be higher than in developed markets. In someemerging markets, settlement procedures may look reasonable but may not work asplanned. Local laws and regulations may also cause difficulties.

iii. Information barriers. Major problems revolve around the quantity and quality ofinformation about certain emerging markets and the companies in those markets.Information barriers include:

• Language barriers. Even in emerging markets where extensive and reliableinvestment information is available, information may not be available in the languageof the analyst. Translation costs are thus a factor that investors must consider.

• Lack of disclosure. Investors in emerging markets are usually operating with muchless information than is the case in developed markets. The disclosure of relevantfinancial information on companies is often lacking. Disclosure laws are sometimesinadequate or unenforced. If such information is available to insiders but not toinvestors, investors are at a disadvantage. Many companies do not provide balancesheets but, instead, concentrate on providing income statements.

• Reliability of information. Finding reliable information is often difficult. Localanalysts in emerging markets are sometimes inexperienced and unskilled at securitiesanalysis. Companies operating in emerging markets frequently do not understand theneeds and interests of sophisticated institutional investors.

• Other informational barriers. Politics, local laws, and taxes may add toinformational barriers. Governmental economic data may be unavailable, withheld, orinaccurate. Local laws may make data difficult to obtain or add to its unreliability.

iv. Custodial facilities. Some emerging markets do not have satisfactory custodial facilities.The facilities may not be adequate, trustworthy, or reputable. Institutional investors whoenter emerging markets should make sure that custodial facilities meet their needs andadequate safeguards exist to prevent fraud and abuse. Problems may include corruption,counterfeit securities, unauthorized (“under the table”) activities, and poor management.Unsatisfactory custodial facilities create concerns about handling proxies and repatriatingfunds and may lead to high fees.

_______________________________1998 Level III Guideline Answers

Afternoon Section – Page 29

LEVEL III: QUESTION 10

Topic: Portfolio ManagementMinutes: 8

Reading Reference:“Individual Investors,” Ch. 3, Ronald W. Kaiser, Managing Investment Portfolios: A DynamicProcess, 2nd edition, John L. Maginn and Donald L. Tuttle, eds. (Warren, Gorham & Lamont,1990).

Purpose:To test candidates’ ability to distinguish between two investors in the context of a theoreticalpersonality profile model.

LOS: The candidate should be able to:

“Individual Investors” (Session 12)

• analyze the objectives and constraints of a particular individual investor and use thisinformation to formulate an appropriate set of investment policies by taking intoconsideration the investor’s psychological characteristics, position in the life cycle,long-term goals, and particular constraints, such as liquidity, taxes, gifts, and estateplanning.

Guideline Answer

The Bailard, Biehl and Kaiser personality classification model, shown below, focuses on twoaspects of investor personality. The first deals with how confidently the investor approaches life.The second deals with whether the investor is methodical, careful, and analytical or whether theinvestor is emotional, intuitive, and impetuous. These two elements constitute the two axes ofindividual psychology: the confident–anxious axis and the careful–impetuous axis.

confident

Individualist Adventurer

careful Straight Arrow impetuous

Guardian Celebrity

anxious

_______________________________1998 Level III Guideline Answers

Afternoon Section – Page 30

The Adventurer is characterized by a combination of confidence and impetuosity. VincenzoDonadoni’s personality traits place him in this classification. He exhibits confidence because he isentrepreneurial, strong willed, impulsive, and willing to take risks. Donadoni has a history ofmaking large “bets” on short-term business opportunities. He also has preconceived notionsabout investments that he intends to impose on Alpine.

The Guardian represents a combination of care and anxiety in investment decision making.Maria Barda falls into this classification. She is anxious about her financial situation and worriesabout whether her assets will last for her lifetime. She prefers to focus on preserving her assets,realizing consistent returns, and avoiding losses. She plans to allow others to manage her fundswithout providing any input herself.

Celebrities are anxious and impetuous in their decision making. As investors, they like to bewhere the action is and are afraid of being excluded. They do not have their own ideas aboutinvestments. Individualists combine caution and confidence in their decision making. They tendto go their own way and try to make their own decisions in life by going about things carefully ina methodical and analytical way. Straight Arrow investors are so well balanced in their emotionalmake-up that they cannot be placed in any specific category. They fall near the center. None ofthese three personalities fully describes either Donadoni or Barda.

_______________________________1998 Level III Guideline Answers

Afternoon Section – Page 31

LEVEL III: QUESTION 11

Topic: Portfolio ManagementMinutes: 6

Reading References:“Behavioral Risk: Anecdotes and Disturbing Evidence,” Arnold S. Wood, Investing Worldwide VI(AIMR, 1996). “The Psychology of Risk,” Amos Tversky, Quantifying the Market Risk PremiumPhenomenon for Investment Decision Making (AIMR, 1990).

Purpose:To test candidates’ ability to distinguish between a stated risk tolerance and a theoretical risktolerance.

LOS: The candidate should be able to:

“Behavioral Risk: Anecdotes and Disturbing Evidence” (Session 18)• explain how the frame or context in which investors see a situation influences their

investment decisions.

“The Psychology of Risk” (Session 18)• discriminate between accepted theories of economic rationality and observed behavior

with respect to loss aversion, reference dependence, asset segregation, mentalaccounting, and biased expectations;

• describe how such observed behavior might be applied to investment management.

Guideline Answer

Maria Barda worries that her assets will be insufficient to support her in her remaining years. Shedoes not want to incur a loss in any of her individual securities. This aversion to losses is acharacteristic shared by many investors and differs from the “rational choice” concept ofinvestment decision making as outlined by Alpine’s portfolio manager.

The rational choice decision making of modern portfolio theory indicates that investors should

• consider investments on a portfolio basis;• have expected returns (probability-weighted returns of all possible outcomes) of an investment

or a portfolio as their primary return consideration;• focus on maximizing expected returns for their risk level; and• assess portfolio gains and losses in an unbiased manner.

_______________________________1998 Level III Guideline Answers

Afternoon Section – Page 32

In contrast, Barda prefers to

• consider her investments individually instead of as part of a portfolio;• concentrate on the extreme negative outcomes of an investment rather than the expected

return; and• focus on avoiding any losses.

Barda’s attitude toward investments is closer to loss aversion than risk aversion. Her preferencescause her to favor a more conservative investment policy than might be warranted by the purelyrational perspective of modern portfolio theory.

_______________________________1998 Level III Guideline Answers

Afternoon Section – Page 33

LEVEL III: QUESTION 12

Topic: Portfolio ManagementMinutes: 10

Reading References:“Individual Investors,” Ch. 3, Ronald W. Kaiser, Managing Investment Portfolios: A DynamicProcess, 2nd edition, John L. Maginn and Donald L. Tuttle, eds. (Warren, Gorham & Lamont,1990). Investment Policy: How to Win the Loser’s Game, 2nd edition, Charles D. Ellis (Irwin,1993).

Purpose:To test candidates’ ability to contrast two non-U.S. investors in order to draw distinctions indetermining and writing selected elements of investment policy statements.

LOS: The candidate should be able to:

“Individual Investors” (Session 12)• analyze the objectives and constraints of a particular individual investor and use this

information to formulate an appropriate set of investment policies by taking intoconsideration the investor’s psychological characteristics, position in the life cycle,long-term goals, and particular constraints, such as liquidity, taxes, gifts, and estateplanning.

Investment Policy: How to Win the Loser’s Game (Session 11)• formulate an investment policy that considers the following dimensions: the investor’s

objectives and risk tolerance, the level of market risk the investor is willing to take, theamount of nonsystematic risk the investor is willing to take, and whether the level ofrisk is to be varied as market conditions change.

Guideline Answer

Vincenzo Donadoni and Maria Barda differ in each of the following areas of their investmentpolicies.

i. Current income requirement.

Donadoni. Donadoni has a minimal need for income. He believes that his current CHF250,000 a year will rise with inflation. He can use his consulting income of CHF 125,000a year for the next two years to satisfy a portion of his needs. Donadoni now has a lowneed for income [CHF 125,000 /(CHF 13 million – CHF 1.5 million home renovation) =1.1 percent] from his portfolio. At the end of two years, his estimated expenses of CHF250,000 (adjusted for inflation) still represent a modest need for current income [CHF250,000 / (CHF 13 million – CHF 2 million tax payment – CHF 1.5 million homerenovation) = 2.6 percent].

_______________________________1998 Level III Guideline Answers

Afternoon Section – Page 34

Barda. Barda has a much greater income requirement than Donadoni. She also expressesconcern about the effects of inflation. Her lack of other income sources means that hercurrent income needs from her investment portfolio represent a reasonably largepercentage of her asset base (LIT 175 million income needs / LIT 2.86 billion asset base =6.1 percent requirement).

ii. Total return requirement.

Donadoni. Donadoni wants to leave a sizable trust (CHF 15 million) for his children.Reaching this goal will require considerable growth of his current financial assets over hisremaining lifetime. Donadoni must realize a return above his income needs to meet hislong-term financial goals. He should adopt a total-return approach to the portfolio withlong-term capital appreciation as the primary objective.

Barda. Barda’s key objective is to preserve the real purchasing power of her assets for herlifetime. Therefore, an appropriate investment strategy for Barda would be to accentuatereal current income.

iii. Willingness to assume risk.

Donadoni. Donadoni is a risk taker. Considering his history of taking large bets on short-term opportunities and preferring to take the initiative in financial matters, he has anabove-average willingness to assume risk.

Barda. Barda is cautious. Based on her concern that her assets will be insufficient tosupport her in her remaining years, she has a below-average willingness to take on risk.She prefers to avoid risk and minimize the chance of loss in any individual security.

iv. Ability to assume risk.

Donadoni. Donadoni’s long time horizon, relatively low income needs, and large assetbase relative to his needs suggest an above-average ability to assume risk.

Barda. Barda’s age and higher income needs relative to her smaller asset base suggest lowfinancial ability to withstand losses in her portfolio.

_______________________________1998 Level III Guideline Answers

Afternoon Section – Page 35

v. Time horizon.

Donadoni. Donadoni’s long time horizon consists of three major intervals. The firstinterval is the next two years. At the end of this period, his income circumstances willchange because of the expiration of his consulting contract. He will also experience alarge outflow of funds because of large tax payments. This change will create a liquidityconstraint on the portion of the portfolio needed for the tax payment. Alpine shouldevaluate both events for their potential effect on Donadoni’s current income requirementand risk tolerance. The second interval encompasses the remainder of his lifetime, whichis an estimated 20–30 years (based on his life expectancy). The third interval includes thetime period when the trust will exist for his children. This interval assumes that Donadonihas achieved his goal of leaving a large trust for his children at his death.

Barda. Barda faces a single time horizon encompassing the remainder of her life. Thistime horizon represents an intermediate time frame of 15–20 years (based on her lifeexpectancy). Thus, the time horizon of her portfolio is shorter than that of Donadoni’s.Also, her portfolio’s time horizon does not extend beyond her death.

_______________________________1998 Level III Guideline Answers

Afternoon Section – Page 36

LEVEL III: QUESTION 13

Topic: Portfolio ManagementMinutes: 18

Reading References:“Individual Investors,” Ch. 3, Ronald W. Kaiser, Managing Investment Portfolios: A DynamicProcess, 2nd edition, John L. Maginn and Donald L. Tuttle, eds. (Warren, Gorham & Lamont,1990). Investment Policy: How to Win the Loser’s Game, 2nd edition, Charles D. Ellis (Irwin,1993). “Asset Allocation for Private Clients,” Jean L.P. Brunel, Investment Counsel for PrivateClients (AIMR, 1993).

Purpose:To test candidates’ ability to recommend an asset allocation that takes into account returnrequirements, risk tolerance, and currency issues.

LOS: The candidate should be able to:

“Individual Investors” (Session 12)• create a set of portfolio policies that is based on a multi-asset, total-return approach to

individual investing.

Investment Policy: How to Win the Loser’s Game (Session 11)• formulate an investment policy statement that considers the following dimensions: the

investor’s objectives and risk tolerance, the level of market risk the investor is willingto take, the amount of nonsystematic risk the investor is willing to take, and whetherthe level of risk is to be varied as market conditions change;

• explain the importance of defining (1) investor objectives and constraints, (2) what isrelevant in terms of return and risk for major asset classes, and (3) the process fordeveloping relatively time-insensitive investment policies.

“Asset Allocation for Private Clients” (Session 12)• discuss the factors that influence asset allocation for individual investors.

_______________________________1998 Level III Guideline Answers

Afternoon Section – Page 37

Guideline Answer

Recommendation. A case can be made for Portfolio C or Portfolio D, but Portfolio C is themore justifiable recommendation. From solely an expected return standpoint, Portfolio D is moreattractive (2.8 percent versus 2.7 percent for Portfolio C). On an ex ante basis, however, a 0.1percent difference in expected return is probably not meaningful. Despite long-term growth ofcapital being one of Vincenzo Donadoni’s primary objectives, other factors argue for Portfolio C.Portfolio C has two key advantages. First, it maintains cash reserves in Italian lira rather thanSwiss francs. Therefore, this portfolio does not expose cash reserves to currency exchange riskbefore the tax payment is made in two years. Second, the geographical diversification of theportfolio’s assets is superior to Portfolio D, which should help minimize investment risks overtime.

Justification: The proposed portfolios differ in terms of expected real return, asset allocation,currency denomination of cash holdings, and geographical diversification.

i. Expected return. The expected return of the four portfolios ranges from a low of 2.3percent for Portfolio A to a high of 2.8 percent for Portfolio D. Given Donadoni’s abilityand willingness to tolerate risk, the portfolio manager should strive for the highest returnavailable that is compatible with other relevant criteria. Based only on expected realreturn, the best portfolio is Portfolio D.

ii. Allocation among asset classes. Donadoni’s primary objective is long-term capitalappreciation. Portfolios C and D, given their allocations among asset classes, are the mostappropriate vehicles for him to achieve this objective. Portfolios C and D have highexposure to equities (60 percent and 70 percent, respectively). Donadoni should targetthis kind of exposure if he wants to achieve his long-term investment objectives.Portfolios A and B, with only 40 percent each in equities, appear incompatible withDonadoni’s return objectives and his higher-than-average risk tolerance. Portfolio A isunsuitable because this portfolio has a 40 percent allocation to cash reserves.

iii. Currency denomination of cash holdings. The currency denomination of cash holdingsfavors Portfolios A and C, because Donadoni has ruled out currency hedging. Bothportfolios propose holding the cash reserves in Italian lira, which is the same currency asthe large tax payment that is due in two years. Portfolios A and C thus offer a currencymatch of assets and liabilities; Portfolios B and D do not because Portfolios B and D holdtheir cash reserves in Swiss francs, which exposes the investor to potential currencyexchange risk.

_______________________________1998 Level III Guideline Answers

Afternoon Section – Page 38

iv. Geographical diversification. Investors may gain important advantages by diversifyingtheir portfolios internationally among different markets, not solely among different sectorswithin individual markets. The size of international markets compared with an investor’sdomestic market generally justifies substantial international investments. This case appliesto Donadoni, who should not restrict his investments to the relatively small markets ofSwitzerland or Italy. Another reason for geographical diversification lies in the lowcorrelation displayed by markets around the world. Subject to different economic cycles,national markets are unlikely to move in lockstep over time. Their relative independenceleaves ample room for investors to diversify their risk among foreign markets. Addinginternational holdings to a domestic portfolio reduces the total risk of the portfoliobecause foreign markets and the domestic market are not perfectly correlated. Bydiversifying a portfolio internationally, investors can improve the portfolio’s risk-adjustedperformance.

The criterion of geographical diversification favors Portfolio C. This portfolio is the leastconcentrated in Switzerland and Italy (total of 57 percent). Portfolio A has more than 70percent of its allocation in Switzerland and Italy, and both Portfolios B and D have morethan 80 percent. Because Portfolio C spreads 43 percent of its allocations among the restof Europe and the rest of the world, it offers the best global balance.

_______________________________1998 Level III Guideline Answers

Afternoon Section – Page 39

LEVEL III: QUESTION 14

Topic: Portfolio ManagementMinutes: 10

Reading References:Investment Policy: How to Win the Loser’s Game, 2nd edition, Charles D. Ellis (Irwin, 1993). “Individual Investors,” Ch. 3, Ronald W. Kaiser, Managing Investment Portfolios: A DynamicProcess, 2nd edition, John L. Maginn and Donald L. Tuttle, eds. (Warren, Gorham & Lamont,1990). “Asset Allocation for Private Clients,” Jean L.P. Brunel, Investment Counsel for PrivateClients (AIMR, 1993).

Purpose:To test candidates’ ability to explain how an investor’s change in circumstances affects his/herreturn requirement, risk tolerance, and time horizon.

LOS: The candidate should be able to:

“Investment Policy: How to Win the Loser’s Game (Session 11)• formulate an investment policy statement that considers the following dimensions: the

investor’s objectives and risk tolerance, the level of market risk the investor is willingto take, the amount of nonsystematic risk the investor is willing to take, and whetherthe level of risk is to be varied as market conditions change;

• explain the importance of defining (1) investor objectives and constraints, (2) what isrelevant in terms of return and risk for major asset classes, and (3) the process fordeveloping relatively time-insensitive investment policies.

“Individual Investors” (Session 12)• create a set of portfolio policies that is based on a multi-asset, total-return approach to

individual investing.

“Asset Allocation for Private Clients” (Session 12)• discuss the factors that influence asset allocation for individual investors.

_______________________________1998 Level III Guideline Answers

Afternoon Section – Page 40

Guideline Answer

In the past three years, Vincenzo Donadoni’s financial situation has changed in the followingways:

• the large outflow of funds for the tax payment has occurred;• his cash flow needs have increased significantly;• his expenses are now denominated in U.S. dollars because he has moved to the United

States;• his willingness to assume risk in his portfolio has diminished; and• his asset base has shrunk, so his ability to assume risk has diminished.

Each of these changes will affect the way his portfolio is structured.

i. Current income requirements. Donadoni’s portfolio has diminished considerably in size,yet his annual living expenses have increased. Thus, the portfolio’s income requirementhas grown greatly relative to his asset base (it is now 6.0 percent, for a CHF 300,000income need from a CHF 5 million asset base).

ii. Total return requirements. Donadoni has abandoned the idea of building up his assets toprovide a CHF 15 million trust fund. His long-term objective is now to preserve a portionof his assets for his children. Therefore, the investment strategy should shift from onegeared to long-term capital appreciation to one that emphasizes generating income andpreserving capital.

These factors suggest that a more conservative asset allocation is now appropriate. Suchan allocation would include a lower equity allocation than previously.

iii. Ability to withstand losses. Donadoni’s ability to assume risk has decreased because ofchanges to his asset base and his income needs. His annual needs now amount to a muchlarger percentage (6 percent) of his asset base than previously. Despite his still long timehorizon, these changes have put Donadoni in a position where he is less able to withstandshortfalls in investment earnings from year to year or over a period of years. Any furthererosion of his asset base (either from market losses or because of annual earnings belowthe 6 percent requirement) or increase in annual needs will increase the difficulty ofachieving any growth of his portfolio’s principal over time. Such changes could alsoreduce Donadoni’s chances of preserving his current asset base.