iia atlanta chapter cae appreciation day michalisin - presentation.pdfiia atlanta chapter cae...

TRANSCRIPT

IIA Atlanta Chapter

CAE Appreciation

Day

Insights & Updates

from The IIA

15 April 2016

Bill Michalisin

EVP & COO, North America

• Trends & Insights

• 2016 Priorities &

Investments

• Questions

Overview

TRENDS & INSIGHTS

Practitioner

Insights

Stakeholder

Insights

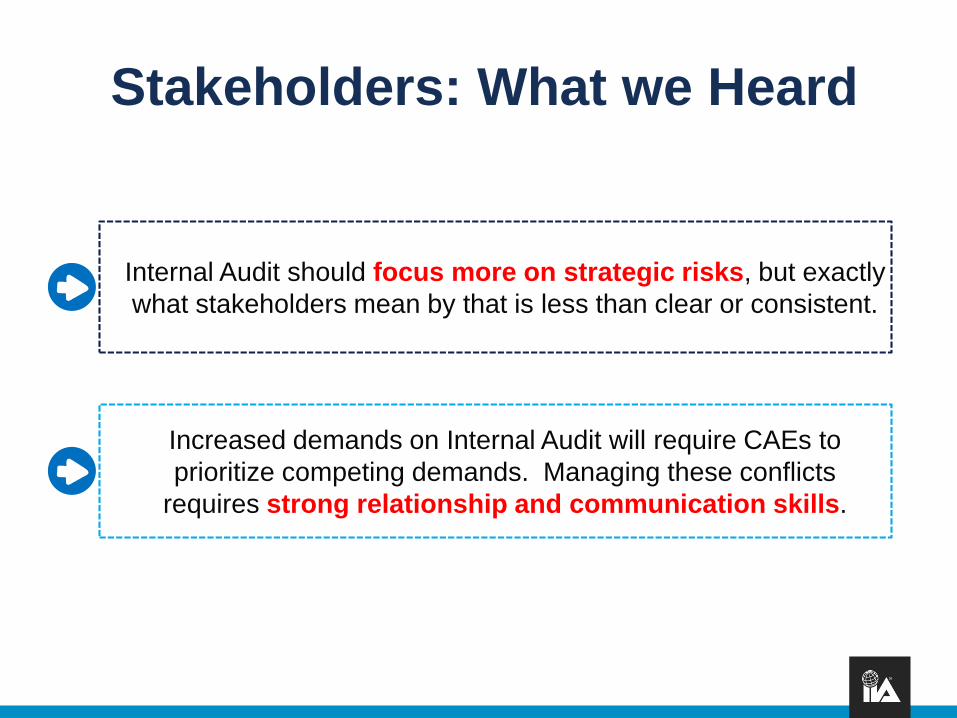

Stakeholders: What we Heard

Internal Audit does many things well that could be considered

foundational elements of assurance work.

There are opportunities for Internal Audit to add value to their

organization by spending more time focusing on risk

identification and management, in addition to assurance work.

5

Internal Audit should focus more on strategic risks, but exactly

what stakeholders mean by that is less than clear or consistent.

Increased demands on Internal Audit will require CAEs to

prioritize competing demands. Managing these conflicts

requires strong relationship and communication skills.

6

Stakeholders: What we Heard

Foundational Elements, High

Ratings

More than 80% of stakeholders agree or strongly agree that Internal Auditors:

More

than

80%

• Assess areas or topics that are

significant.

• Keep up to date with changes in the

business.

• Sufficiently communicate audit plans.

7

Foundational Elements, High

Ratings

Top three criteria (supported by 70% of respondents) used to evaluate the performance of Internal Auditors:

Top

three

criteria

• Quality of audit work/reliable results.

• Usefulness of recommendations made.

• Timely communication of risks.

8

Beyond Basics: Assurance vs.

Advisory

Many respondents note that they see value in advisory services. What should this non-assurance work cover?

Top

3

areas

• Identifying known/emerging risk areas.

• Facilitating/monitoring risk

management.

• Identifying appropriate risk

management frameworks.

9

Offense vs. Defense

71%

74%

76%

78%

78%

85%

Assurance on compliance with legal & regulatoryrequirements

Alert operational management to emerging issues& changing regulatory & risk scenarios

Consult on business process improvements

Identify appropriate risk management frameworks,practices & processes

Facilitate & monitor effective risk managementpractices by operational management

Identify known & emerging risk areas

Source: CBOK Stakeholder Report: Relationships and

Risk, Insights from Stakeholders in North America

Risk Is A Broad Term

Stakeholders say they want Internal Audit to add value by being engaged in risk-related activities. Which ones?

58%

• More than half of our respondents want

Internal Audit to be more active in

assessing and evaluating strategic

risks.

• Only 1 in 4 disagree.

11

Moving Out of the Comfort Zone

CultureCyber risk

Data Interpersonal skills

55% 71%

52% 58%

Source: Pulse of Internal Audit report, 2016

TEXT

TEXT

TOP

ANSWERS

AUDIT

FOCUS

KEY

RISKS

Role In Responding To

Strategic Risks

Stakeholders were asked to choose the best avenue for Internal Audit to improve its role in responding to risks.

Focus on strategic risks as well as

operational, financial, and compliance risks during audit projects.

Periodically evaluating and communicating key risks to the Board and

Executive Management.

13

Internal Auditors Cannot Do

Everything

The survey asked stakeholders about the best way for Internal Audit to prioritize competing demands.

77%

said…

• The most popular option: CAE to build

strong relationships with management.

• Expect strong relationships with board

members also.

14Focus on Relationships

Interpersonal Skills are Critical

9%

19%

21%

23%

28%

37%

40%

42%

44%

65%

83%

97%

98%

Quality controls

Investigations

Fraud auditing

Finance

Cybersecurity

Data mining & analytics

Risk management…

Accounting

IT

Industry-specific

Business Acumen

Analytical/critical thinking

Communication skills

Source: Pulse of Internal Audit report, 2016

Invest in yourself and your

team

Key Takeaways

Demonstrate understanding

of strategic risks.

Focus on risk activities.

Explore adding more

advisory work.

Preserve the foundational

elements.

Build your soft skills.

16

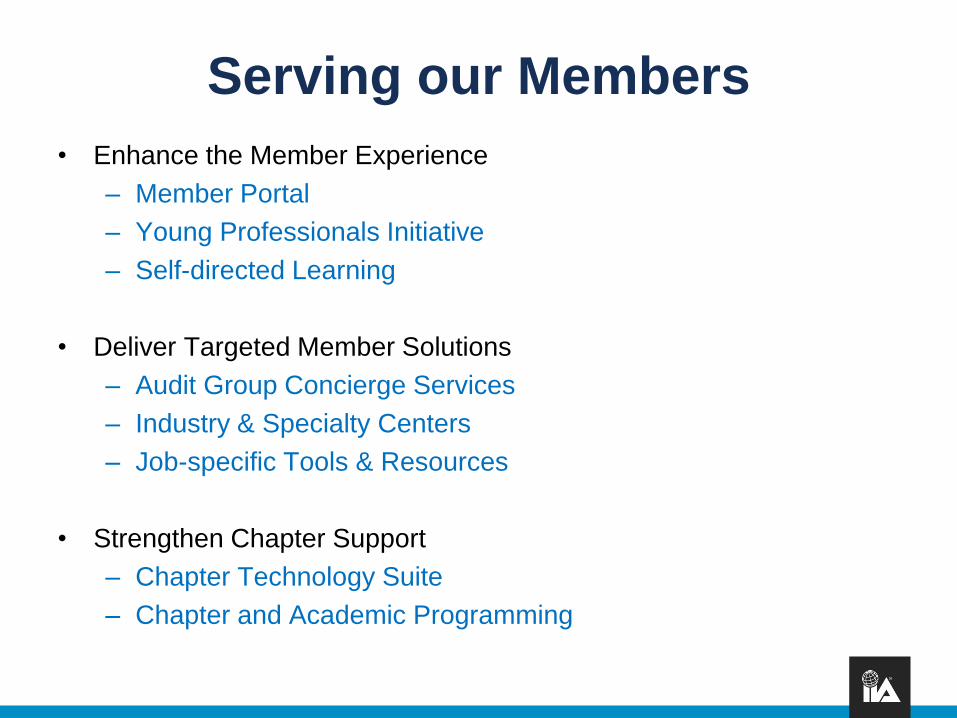

IIA 2016 PRIORITIES

• Enhance the Member Experience

– Member Portal

– Young Professionals Initiative

– Self-directed Learning

• Deliver Targeted Member Solutions

– Audit Group Concierge Services

– Industry & Specialty Centers

– Job-specific Tools & Resources

• Strengthen Chapter Support

– Chapter Technology Suite

– Chapter and Academic Programming

Serving our Members

INVESTING IN YOU

Member Empowerment

Omni-channel Learning

22

Exis

tin

g C

en

ters

Exch

an

ges

Fu

ture

Information Technology

Colleges & Universities

Health Services

Gaming & Hospitality

CANADIAN

Public SectorAUDITING CENTRE

Specialty Resources

Digital & Social Engagement

55%

45%

BY GENDER

Male Female

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

18 – 34 25 – 34 35 – 44 45 – 54 55 – 64 65+

14%

33%

24%

18%

9%

2%

BY AGE

1%

37%

41%

13%

4%1.40% 2.60%

13-17 18-24 25-34 35-44 45-54 55-64 65+

73%

27%

47%

71%

80%93%

27%

Come Celebrate the 75th

Anniversary in New York City

Registration is open

24

Questions?

www.theiia.org | www.globaliia.org

The Institute of Internal Auditors

Bill Michalisin

EVP & COO, North America

Thank You

© 2016 The Institute of Internal Auditors. All Rights Reserved.