ifrs - transformation agenda for saudi corporates€¦ · · 2014-06-04ifrs - transformation...

TRANSCRIPT

IFRS - Transformation Agenda for Saudi Corporates 3rd Saudi-Pak Accountancy Symposium – Riyadh May 15, 2014 Organized by ICAP KSA Chapter

www.pwc.com

PwC

Here today

Gavin Steel PwC ME

Conversion Leader

2

PwC

Origin of IFRS

IASC (International Accounting Standard Committee)

IASB (International Accounting Standard Board)

• Introduced in 1973 • Issued the IAS’s (International Accounting

Standards)

• Introduced in April 2001 • Succeeded IASC • Introduced IFRSs( International Financial

Reporting Standards) • Introduced IFRIC (International Financial

Reporting Interpretation Committee)

IFRS is now widely applied around the world. Today over 140 countries either require or permit the use of IFRS for public company reporting

PwC

What are International Financial Reporting Standards (“IFRS”)?

IFRS is a single set of high quality, understandable and enforceable global accounting standards that require transparent and comparable information to be disclosed in general purpose financial statements.

They comprise:

IAS’s (Standards issued prior to the formation of the IASB)

IFRS‘s (Standards issued post the formation of the IASB)

IFRIC’s (Interpretations)

SIC (Standing Interpretations Committee)

There are

28 IASs (part of them were superseded by IFRSs. Or withrawn)

14 IFRSs

16 IFRICs

13 SIC

Where do they come from?

The International Accounting Standards Board (“IASB”) establishes the standards through a consultative process

The IASB has 16 full time members

The IASB is the independent standard-setting body of the IFRS Foundation – a not for profit organisation

The IFRS Foundation is an independent, not-for-profit private sector organisation working in the public interest.

The Foundation is run by a board of Trustees

The IFRS Interpretations Committee has 14 members appointed by the Board of Trustees

International Financial Reporting Standards

PwC

SOCPA

5

• The Saudi Organisation for Certified Public Accountants (SOCPA) was established under Royal Decree No. M12 in 1991

• SOCPA’s responsibilities include development and approval of accounting and auditing standards . It operates

under the supervision of the Ministry of Commerce. • All banks and insurance companies are required to adopt IFRS (SAMA requirement),

• In 2013, SOCPA approved an IFRS convergence plan by which listed entities other than banks and

insurance companies would be required to report under SOCPA standards that will be IFRSs with some modifications – “ IFRS as adopted in Saudi Arabia”

• Listed entities are required to adopt in 2017; and • Remaining entities are required to adopt in 2018

• IFRS in Saudi Arabia will be similar to the standards issued by the IASB with possible modifications in three

respects:

• Adding more disclosure requirements • Removing optional treatments; and • Amending the requirements that contradict Shariah or local law, taking in consideration level of

technical and professional preparedness in the Kingdom • The IFRS transition is part of a project called “SOCPA project for transition to International

Accounting and Auditing Standards”

PwC

The Global Move to IFRS

6

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

IASB Formed in

2001

Previously referred to as International Accounting Standards

(“IAS”)

EU announces adoption of

IFRS for listed entities

EU listed entities adopt

IFRS

First “IFRS” issued

19 Countries using IFRS

the reporting framework

KSA Adopts IFRS for

listed entities

KSA announces adoption of

IFRS

70 countries adopted IFRS

for listed companies

141 countries have adopted

IFRS for listed

companies Continued adoption of

IFRS expected

• Saudi Arabia is the only country of the G20 that has not adopted IFR

PwC

Why IFRS?

7

There are numerous reasons as to why countries (and businesses) are supporting the move to IFRS: • Access and movement of global capital:

• Investor confidence • Access to broader investment base • Better supplier / payment terms for businesses • Lower costs of capital • Improved liquidity in the market

• Regulatory

• Better comparability of financial reporting • Improved transparency

• Business

• Improves the skills of workforce • Standardises processes / procedures and policies across a group • Lowers costs

The support for IFRS adoption is broad:

• International Organization of Securities Commissions (IOSCO); • International Federation of Accountants (IFAC); • Securities and Exchange Commissions (SEC); • Basel Committee; • The World Bank; • International Monetary Fund (IMF); and • The European Commission /all support the adoption of IFRS

PwC

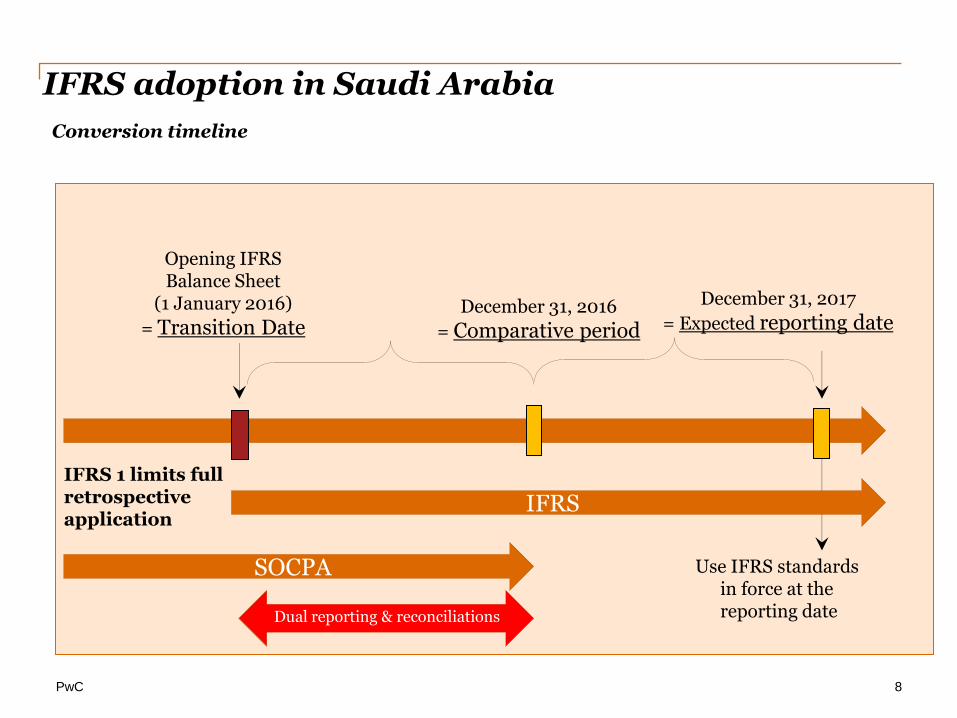

December 31, 2017

= Expected reporting date

Opening IFRS Balance Sheet

(1 January 2016)

= Transition Date

Use IFRS standards in force at the reporting date

Conversion timeline

IFRS

IFRS 1 limits full retrospective application

SOCPA

December 31, 2016

= Comparative period

8

IFRS adoption in Saudi Arabia

Dual reporting & reconciliations

PwC

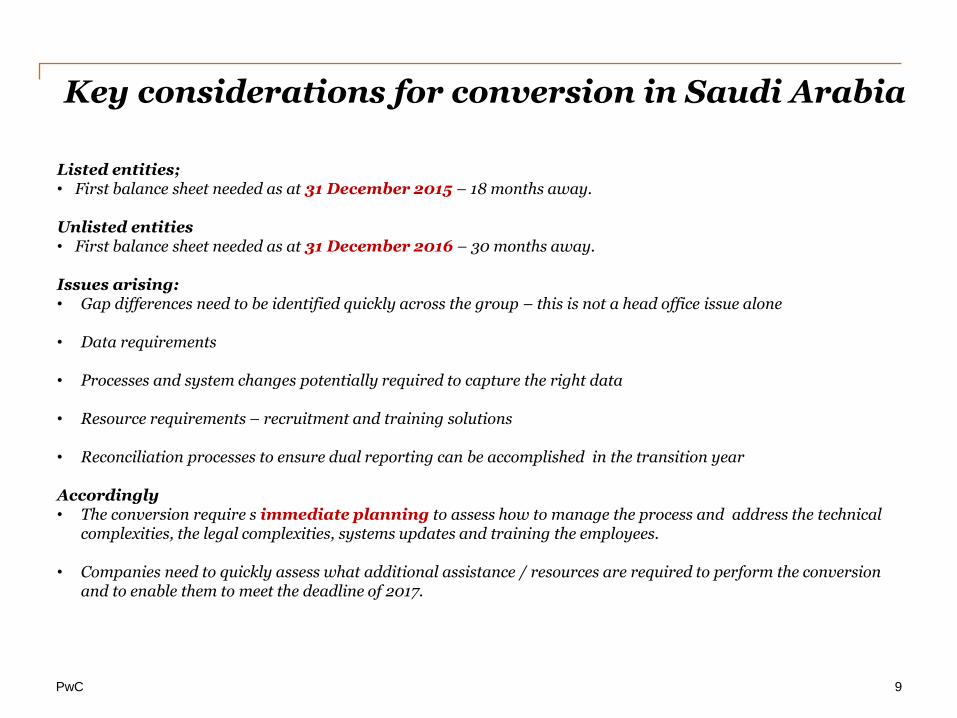

Key considerations for conversion in Saudi Arabia

9

Listed entities; • First balance sheet needed as at 31 December 2015 – 18 months away.

Unlisted entities • First balance sheet needed as at 31 December 2016 – 30 months away. Issues arising: • Gap differences need to be identified quickly across the group – this is not a head office issue alone

• Data requirements

• Processes and system changes potentially required to capture the right data

• Resource requirements – recruitment and training solutions

• Reconciliation processes to ensure dual reporting can be accomplished in the transition year

Accordingly • The conversion require s immediate planning to assess how to manage the process and address the technical

complexities, the legal complexities, systems updates and training the employees.

• Companies need to quickly assess what additional assistance / resources are required to perform the conversion and to enable them to meet the deadline of 2017.

PwC

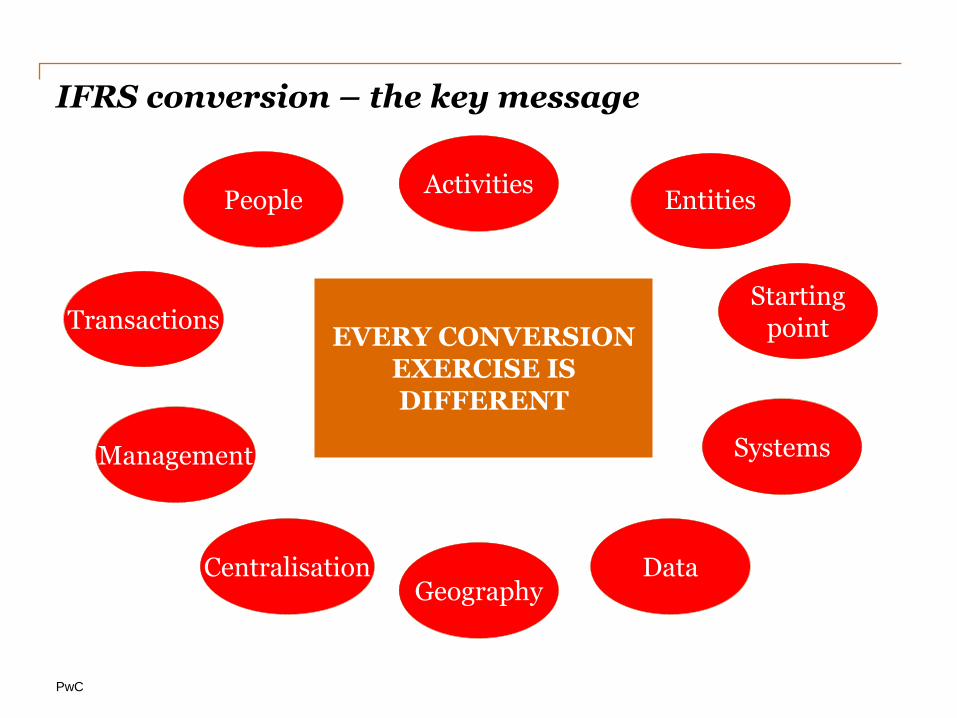

IFRS conversion – the key message

EVERY CONVERSION EXERCISE IS DIFFERENT

People Activities

Entities

Starting point

Systems

Data Geography

Centralisation

Management

Transactions

PwC

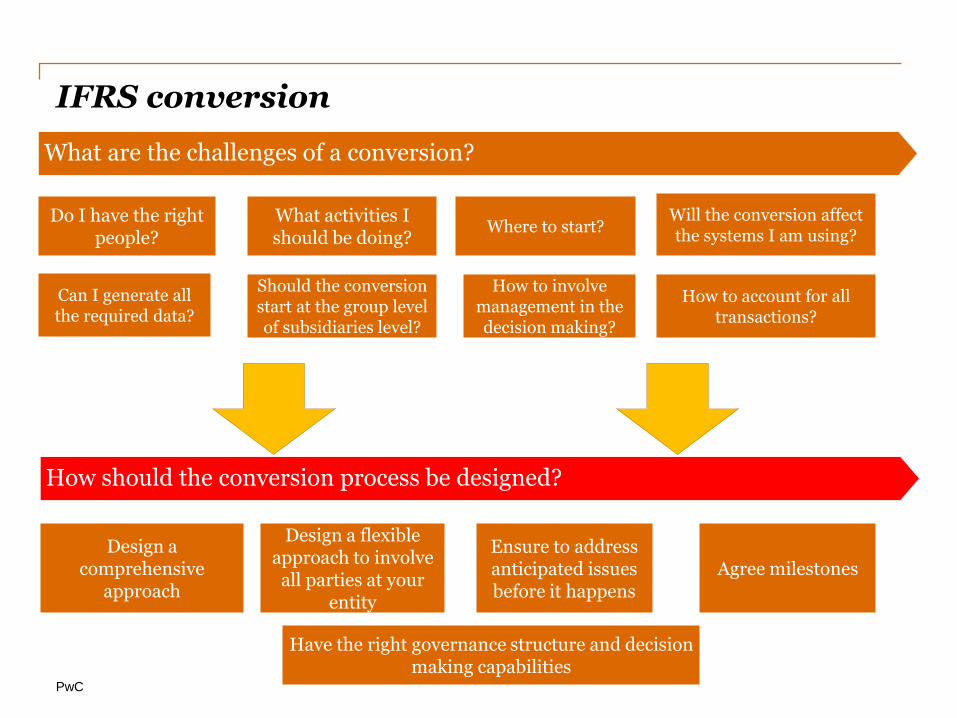

IFRS conversion

What are the challenges of a conversion?

Do I have the right people?

What activities I should be doing?

Where to start?

Will the conversion affect the systems I am using?

Can I generate all the required data?

Should the conversion start at the group level of subsidiaries level?

How to involve management in the decision making?

How to account for all transactions?

How should the conversion process be designed?

Design a comprehensive

approach

Design a flexible approach to involve

all parties at your entity

Ensure to address anticipated issues before it happens

Agree milestones

Have the right governance structure and decision making capabilities

PwC

The Conversion Approach

Project and change

management

Gap analysis and

roadmap

Conversion Embedding

People Processes

Systems Financial manage-ment and reporting

Policies

The PwC IFRS (or equivalent) conversion methodology typically follows a three-phase approach as illustrated opposite:

GAP Analysis and Roadmap: involves a detailed gap analysis, which produces a roadmap for successful conversion; Conversion: results in the production of the first IFRS financial statements; Embedding: ensures that systems, processes, policies and behaviours are adopted to report efficiently under IFRS (or equivalent) on an ongoing basis.

“Guiding you through the conversion”

12

PwC

Illustrative effort and impact of selected IFRS to SOCPA differences

13

IFRS adoption in Saudi Arabia

Implementation effort/complexity high

high

Fin

an

cia

l s

tate

me

nts

eff

ec

ts

Consolidation, JV’s &

associates Financial instruments

Business combination OCI

Disclosures

Derivatives and hedging

Investments

Fixed assets

Intangible assets

Borrowing costs

Leases

Zakat/ Taxes

Impairment

Inventory

Investment properties

Related parties

Employee benefits

PwC

Finance Systems Architecture and Data Flows

Fin

an

ce

& A

cco

un

ting

Lo

gic

al D

ata

Flo

w

Financial Applications - differences between business units / subsidiaries (Oracle, SAP, Microsoft)

Workflow

Master

Data

Management

P2P

Other

Financial Applications – Consolidation, Planning / Budgeting and Reporting

Management

Reports Planning /

Budgeitng Consolidation

Integration

Reporting Delivery

Web Reports Fin Reporting Bridge

Business

Intelligence

E-mail Standard Reports

Integration

Output Requirements

- External Applications XBRL filing / IFRS / SOCPA

Reporting Zakat / Tax Reporting

PO AP

GA

PO AP

AR CM

O2C

Projects

Financial

Reports

14

PwC

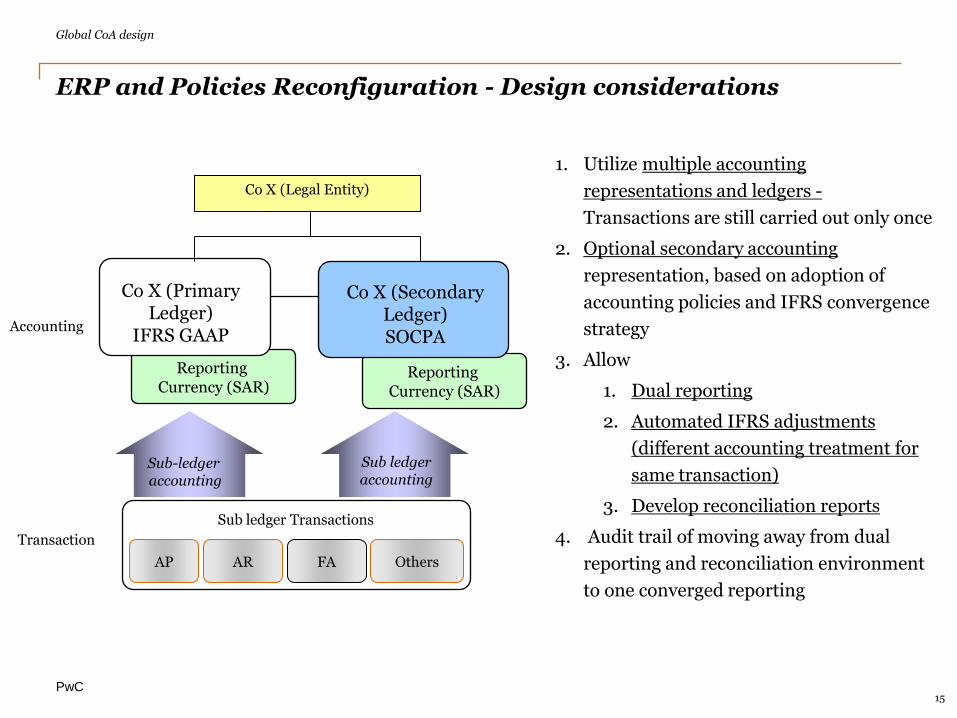

ERP and Policies Reconfiguration - Design considerations

Global CoA design

15

Reporting Currency (SAR)

Reporting Currency (SAR)

Sub-ledger accounting

Sub ledger Transactions

Sub ledger accounting

Co X (Primary Ledger)

IFRS GAAP

Co X (Secondary Ledger) SOCPA

AP AR FA Others

Co X (Legal Entity)

Accounting

Transaction

1. Utilize multiple accounting

representations and ledgers -

Transactions are still carried out only once

2. Optional secondary accounting

representation, based on adoption of

accounting policies and IFRS convergence

strategy

3. Allow

1. Dual reporting

2. Automated IFRS adjustments

(different accounting treatment for

same transaction)

3. Develop reconciliation reports

4. Audit trail of moving away from dual

reporting and reconciliation environment

to one converged reporting

PwC

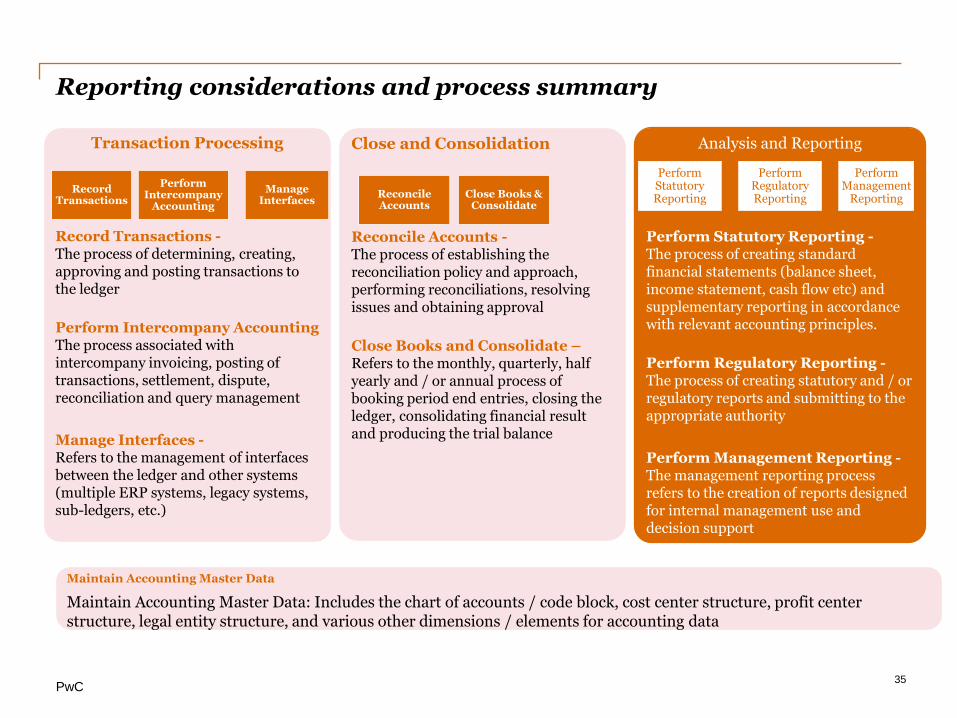

Transaction Processing Record Transactions - The process of determining, creating, approving and posting transactions to the ledger

Perform Intercompany Accounting The process associated with intercompany invoicing, posting of transactions, settlement, dispute, reconciliation and query management

Manage Interfaces - Refers to the management of interfaces between the ledger and other systems (multiple ERP systems, legacy systems, sub-ledgers, etc.)

Record Transactions

Manage Interfaces

Perform Intercompany

Accounting

Close and Consolidation Reconcile Accounts - The process of establishing the reconciliation policy and approach, performing reconciliations, resolving issues and obtaining approval

Close Books and Consolidate – Refers to the monthly, quarterly, half yearly and / or annual process of booking period end entries, closing the ledger, consolidating financial result and producing the trial balance

Close Books & Consolidate

Reconcile Accounts

Analysis and Reporting Perform Statutory Reporting - The process of creating standard financial statements (balance sheet, income statement, cash flow etc) and supplementary reporting in accordance with relevant accounting principles.

Perform Regulatory Reporting - The process of creating statutory and / or regulatory reports and submitting to the appropriate authority

Perform Management Reporting - The management reporting process refers to the creation of reports designed for internal management use and decision support

Perform Statutory Reporting

Perform Management

Reporting

Perform Regulatory Reporting

Maintain Accounting Master Data

Maintain Accounting Master Data: Includes the chart of accounts / code block, cost center structure, profit center structure, legal entity structure, and various other dimensions / elements for accounting data

35

Reporting considerations and process summary

PwC

In a Nutshell..

17

PwC

What questions should you be asking now? Considerations for management and audit committees

1. Planning Are you aware of what needs to be done?

2. Applying IFRS 1

3. Accounting policies

4. Stakeholders

5. Embedding IFRS

Have you considered the implications of the relevant exemptions?

Have you considered all the relevant options and new standards?

Are you managing stakeholders’ expectations?

How will the entity conduct business as usual?

18

PwC

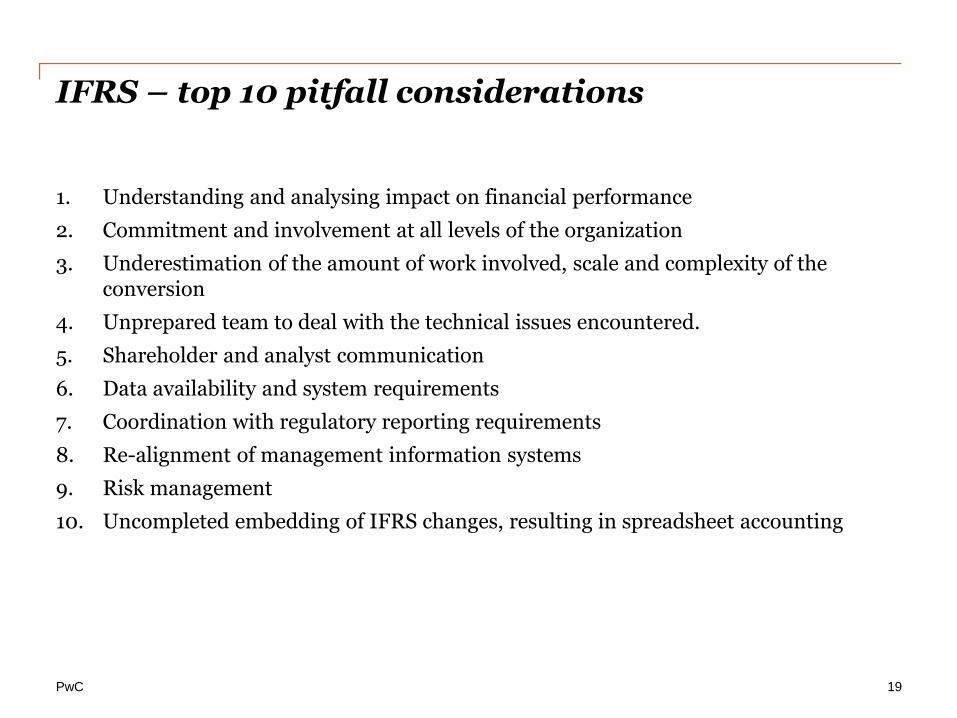

IFRS – top 10 pitfall considerations

1. Understanding and analysing impact on financial performance

2. Commitment and involvement at all levels of the organization

3. Underestimation of the amount of work involved, scale and complexity of the conversion

4. Unprepared team to deal with the technical issues encountered.

5. Shareholder and analyst communication

6. Data availability and system requirements

7. Coordination with regulatory reporting requirements

8. Re-alignment of management information systems

9. Risk management

10. Uncompleted embedding of IFRS changes, resulting in spreadsheet accounting

19

PwC

Our experience says

• Do not delay the process – act now!

• Have the FD as the Project Sponsor

• Define clear project and governance structures

• Implementation plan should have clear milestones and timelines

• Educate stakeholders early in the process

• Align IFRS conversion with entity’s strategic objectives

• Financial reporting solutions should be sustainable

• Make sure your advisors do not do it too for you, but do it with you

• Understand where IFRS is going

20

PwC Slide 21

The information contained in this presentation is for general guidance on matters of interest only. The application and impact of laws can vary widely based on the specific facts involved. Before taking any action, please ensure that you obtain advice specific to your circumstances from your usual PricewaterhouseCoopers client service team or your other tax advisers. The materials contained in this presentation were assembled in September 2013 and are based on the law enforceable and information available at that time. © PricewaterhouseCoopers, May 2014. All rights reserved. PricewaterhouseCoopers refers to the network of member firms of PricewaterhouseCoopers International Limited, each of which is a separate and independent legal entity.