ifrs 4 / ind as 104 as applicable to general insurance ... mukherjee.pdf · 1 1-1 ifrs 4 / ind as...

TRANSCRIPT

1 1- 1 -

IFRS 4 / IND AS 104 – As applicable to

General Insurance Companies

TATA AIG GENERAL INSURANCE

COMPANY LTD

MIRANJIT MUKHERJEE

2

AGENDA

1. Background of IFRS 4

2. Background of IND AS 104

3. What is IFRS 4 / IND AS 104

4. Recognition and measurement under IND-AS 104

5. Insurance Contracts

6. Examples of Insurance Contracts

7. Liability Adequacy test and examples

8. Disclosures principles and summary

9. Comparison of IND AS 104 vs current requirements

10. Balance Sheet – IND AS 104

11. Additional disclosures under IND AS 104

12. Key issues for implementation

13. Impact of IND AS 104 / IFRS on general insurers

14. Terms Used

3

IFRS 4 – Phase I – BACKGROUND

Comprehensive insurance contracts project carried over

from IASC to new IASB

Short-term insurance contracts project split off from

comprehensive project

Exposure Draft ED 5 Insurance Contracts

April 2001

May 2002

July 2003

IFRS 4 Insurance Contracts31st Mar 2004

Effective date of IFRS 41st Jan 2005

4

IND AS 104 – BACKGROUND

IRDA issues exposure draft on IFRS Compliance

Exposure Draft AS 39 on Insurance Contracts

2009

2010

MCA notifies 35 IFRS (IND AS) incl IND AS 10425 Feb 2010

Insurance cos prepare opening bal sheet as per IND AS1 April 2012

Date - ? Preparation of opening bal sheet as per IND AS

5

WHAT IS IFRS 4 – PHASE I – IND AS 104

Interim standard - focused primarily on disclosures and classification of

insurance contracts.

Introduces a definition for an insurance contract based on the contract

containing significant insurance risk.

Required only limited changes to existing accounting practices for insurance

contracts and extensive disclosures.

IFRS 4 does not affect the business fundamentals since there is

No change in the underlying transactions

No change in real cash flow

6

RECOGNITION AND MEASUREMENT UNDER IND AS 104

In most respects, IND AS 104 allows an entity to continue to account for insurance contracts

under its previous accounting policies.

However, the standard makes some limited improvements to accounting for insurance

contracts

Liabilities only on existing contracts : Catastrophe provisions and equalization provisions are

not permitted. They are not liabilities.

Liability Adequacy Test : The adequacy of insurance liabilities must be tested at the end of

each reporting period. The liability adequacy test is based on current estimates of future cash

flows. Any deficiency is recognized in profit or loss.

Impairment testing : Furthermore, reinsurance assets are tested for impairment.

No offsetting : Insurance liabilities are presented without offsetting them against related

reinsurance assets.

No offsetting : Insurance expense or income against related reinsurance income or expense.

7

INSURANCE CONTRACTS

IND AS 104 covers insurance contracts

It applies to insurance contracts where policy holders pass insurance risk to insurance companies

OR where insurers pass insurance risk to re-insurers

What is an insurance contract

In the contract one party accepts significant insurance risk from another party

The party accepting insurance risk agrees to compensate the policy holder

If a specified uncertain future event affects the policyholder

What is an insurance risk

The risk in the contract must be insurance risk, which is any risk except for financial risk

This specified uncertain future event is known as the “insured event” while the uncertain future event

that is covered by an insurance contract creates “insurance risk”.

Uncertainty

Uncertainty is the essence of an insurance contract . At least one of the following is uncertain at the

inception of the contract :

Whether an insured event will happen

When will it occur

How much the insurer needs to pay

8

INSURANCE CONTRACTS

Insurance Contract

Insurer accepts Insurance Risk

Significant Risk

Insurer accepts Significant Risk

No numerical range fixed for what is significant risk

Meaning of significant : Payment of significant additional benefit

Another Party

Insurer must accept risk from another party .

Insurer must be separate from the policy holder .

Accordingly self insurance is not an insurance contract as per IND AS 104

9

SIGNIFICANT INSURANCE RISKS

The underlying tenet behind insurance transactions.

The purpose of this action is to take a specific risk, which is detailed in the insurance

contract, and pass it from one party who does not wish to have this risk (the insured) to a party

who is willing to take on the risk for a premium (the insurer).

Risk transfer Conditions

Underwriting risk

Timing Risk

RISK TRANSFER

INSURANCE RISK

Amount Risk

10

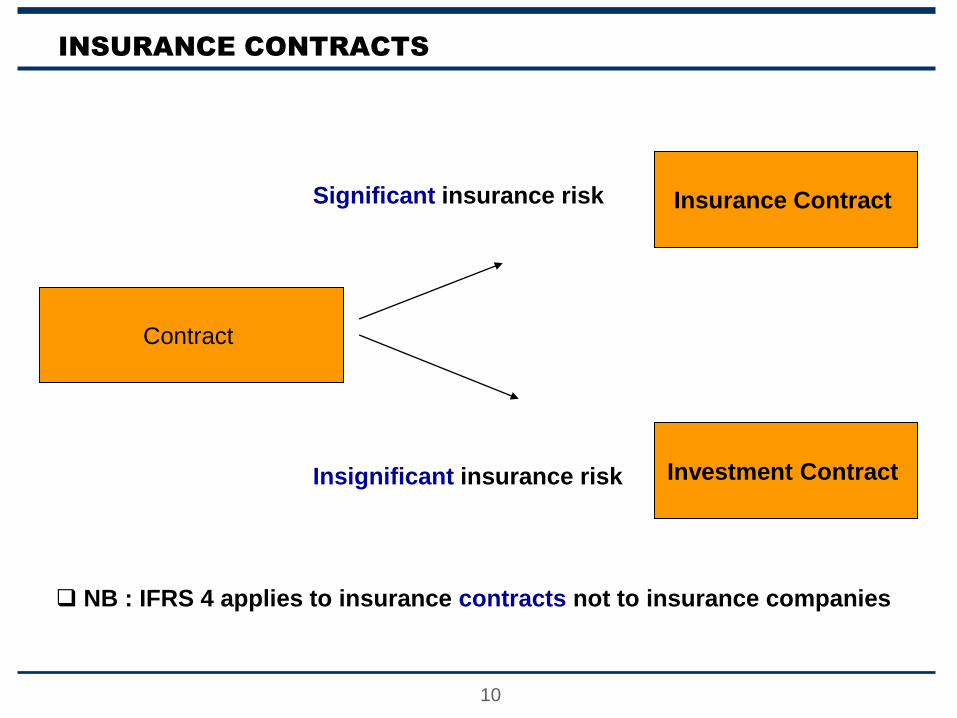

INSURANCE CONTRACTS

Contract

Significant insurance risk Insurance Contract

Insignificant insurance risk Investment Contract

NB : IFRS 4 applies to insurance contracts not to insurance companies

11

EXAMPLES OF INSURANCE CONTRACTS - IND AS 104

Insurance contracts covered

Theft / Damage to property

Product / Professional Liability

Accident and Health

Marine

Engineering

Product Warranty ( excl issued

by manufacturer / dealer / retailer )

Title Insurance

Travel Insurance

Reinsurance Contracts

Contracts to be excluded

Self Insurance

Credit related guarantee

Weather derivative

Catastrophic Bonds

12

LIABILITY ADEQUACY TEST

If existing accounting policies include an assessment that meets

the specified minimum requirements, no further action required.

If not ?

If no sufficient assessment, the carrying amount of the liability must

be tested and, if necessary increased

Must assess at each reporting date whether recognised insurance liabilities are adequate

based on current estimates of future cash flows under insurance contracts.

The assessment must use current assumptions and consider all contractual cash flows.

13

HOW DO YOU CARRY OUT LIABILITY ADEQUACY TEST

If the present value of the expected cash flows arising out of future claims exceeds the

unearned premium liability then the unearned premium liability is deficient . The recognized

deficiency has to be recorded in the income statement .

This should not be an issue in India as insurers are already required to create a

premium deficiency in their accounts in the current accounting principles .

14

EXAMPLES OF LIABILITY ADEQUACY TESTS

At each balance sheet date an assessment is made of whether the provisions for unearned premiums are adequate.

A separate provision is made, based on information available at the balance sheet date, for any estimated future

underwriting losses relating to unexpired risks. The provision is calculated after taking into account future investment

income that is expected to be earned from the assets backing the provisions for unearned premiums (net of deferred

acquisition costs). The unexpired risk provision is assessed in aggregate for business classes which, in the opinion

of the directors, are managed together.

Royal Sun Alliance

A provision should be made for unexpired risks where the expected value of claims and expenses attributable to the

unexpired periods of policies in force at the balance sheet date exceeds the unearned premiums provision in relation

to such policies after the deduction of any deferred acquisition costs. The need for an unexpired risk provision has

been considered separately by reference to classes of business that are managed together, after taking into account

the relevant investment returns. An unexpired risk provision was not found necessary for any business classes and

therefore a provision is not raised in the accounts.

Zurich

For the Non Life segment the test is performed in the event the ultimate underwriting combined ratio is in excess of

100% to the unearned premium reserve net of deferred acquisition costs . The liability adequacy test is performed on

the level of the actuarial segment and then aggregated at the entity level .

SCOR RE

15

PRINCIPLES OF DISCLOSURES UNDER IFRS 4

Disclosure is particularly important for information relating to insurance

contracts, as entities can continue to use local GAAP accounting policies for

measurement.

IFRS 4 has two main principles for disclosure.

Entities should disclose information that identifies and explains the

amounts in its financial statements arising from insurance contracts.

Information that enables users of its financial statements to evaluate the

nature and extent of risks arising from insurance contracts.

16

SUMMARY OF DISCLOSURES REQUIRED UNDER IFRS 4

Accounting policies for insurance contracts

Recognized Assets , Liabilities , Income, Expenses and

Cash Flows arising from these contracts

Assumptions that impact value of Assets , Liabilities , Income

and Expenses

Historic claims development ( loss development triangle )

Information that helps

users understand the

amounts in the financial

statements arising from

Insurance contracts

Nature and extent of risks

arising from Insurance

contracts

Risk management policies and objectives

Information about insurance risk sensitivity and

concentration

Information about credit risk, liquidity risk and market risk

17

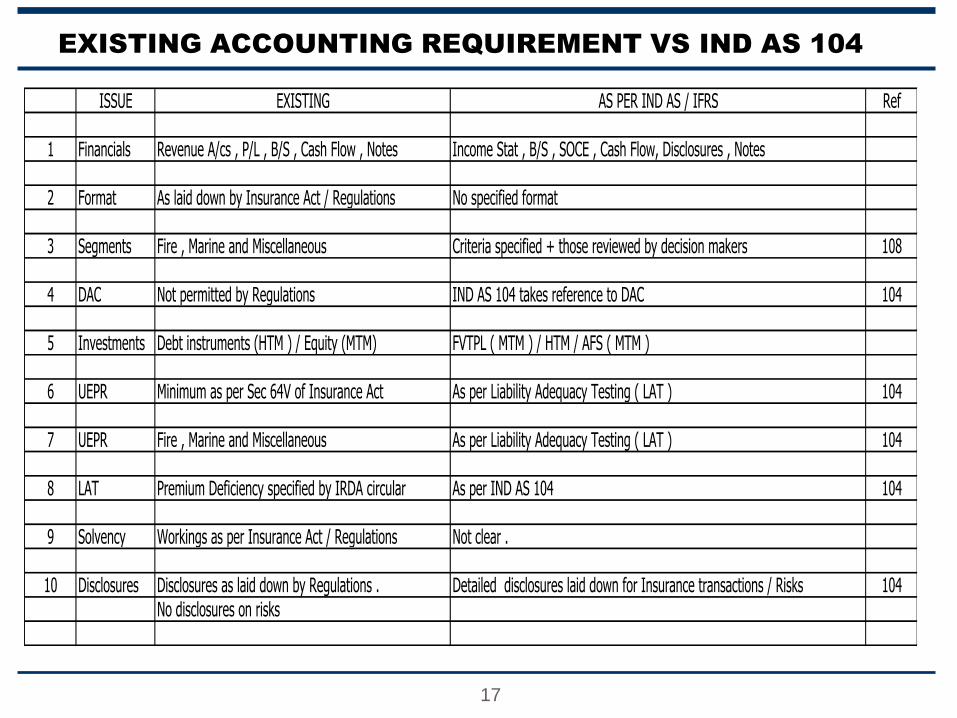

EXISTING ACCOUNTING REQUIREMENT VS IND AS 104

ISSUE EXISTING AS PER IND AS / IFRS Ref

1 Financials Revenue A/cs , P/L , B/S , Cash Flow , Notes Income Stat , B/S , SOCE , Cash Flow, Disclosures , Notes

2 Format As laid down by Insurance Act / Regulations No specified format

3 Segments Fire , Marine and Miscellaneous Criteria specified + those reviewed by decision makers 108

4 DAC Not permitted by Regulations IND AS 104 takes reference to DAC 104

5 Investments Debt instruments (HTM ) / Equity (MTM) FVTPL ( MTM ) / HTM / AFS ( MTM )

6 UEPR Minimum as per Sec 64V of Insurance Act As per Liability Adequacy Testing ( LAT ) 104

7 UEPR Fire , Marine and Miscellaneous As per Liability Adequacy Testing ( LAT ) 104

8 LAT Premium Deficiency specified by IRDA circular As per IND AS 104 104

9 Solvency Workings as per Insurance Act / Regulations Not clear .

10 Disclosures Disclosures as laid down by Regulations . Detailed disclosures laid down for Insurance transactions / Risks 104No disclosures on risks

18

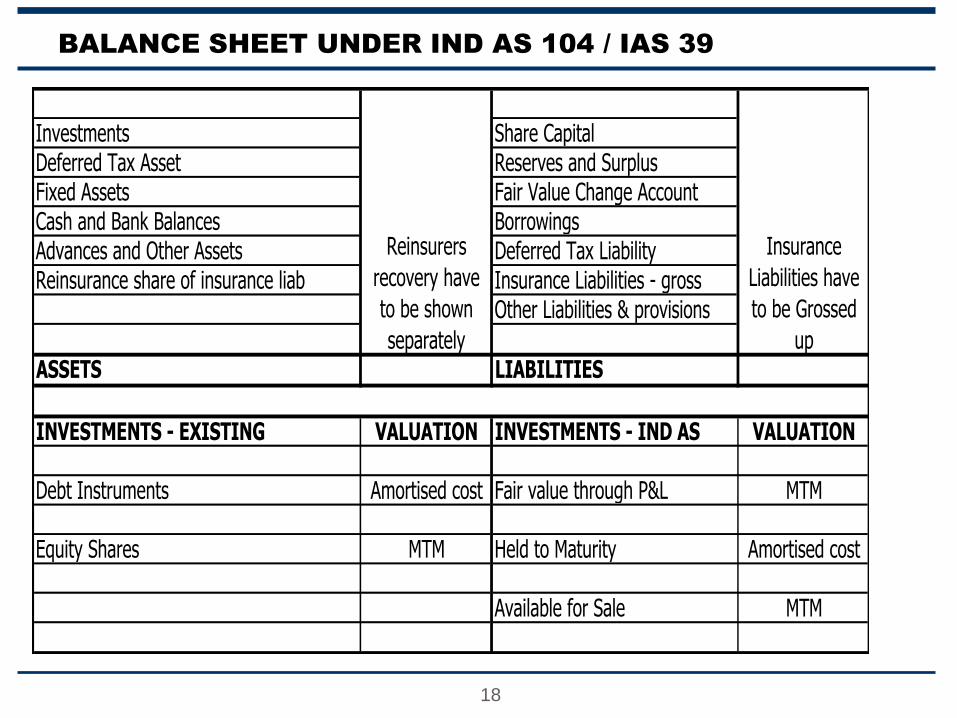

BALANCE SHEET UNDER IND AS 104 / IAS 39

Investments Share CapitalDeferred Tax Asset Reserves and SurplusFixed Assets Fair Value Change AccountCash and Bank Balances BorrowingsAdvances and Other Assets Deferred Tax LiabilityReinsurance share of insurance liab Insurance Liabilities - gross

Other Liabilities & provisions

ASSETS LIABILITIES

INVESTMENTS - EXISTING VALUATION INVESTMENTS - IND AS VALUATION

Debt Instruments Amortised cost Fair value through P&L MTM

Equity Shares MTM Held to Maturity Amortised cost

Available for Sale MTM

Insurance

Liabilities have

to be Grossed

up

Reinsurers

recovery have

to be shown

separately

19

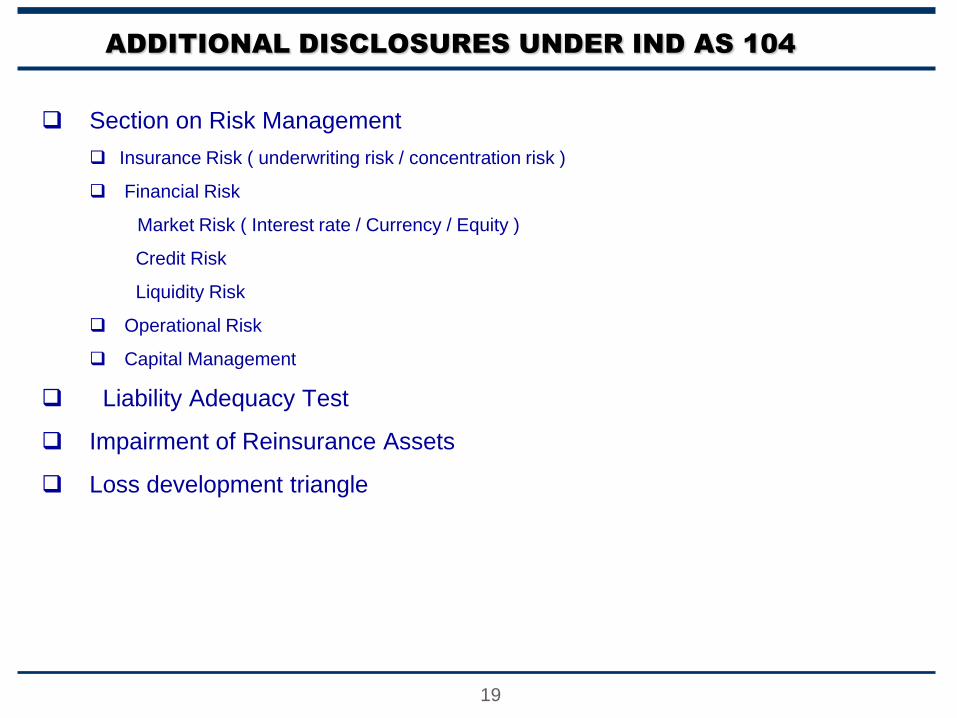

ADDITIONAL DISCLOSURES UNDER IND AS 104

Section on Risk Management

Insurance Risk ( underwriting risk / concentration risk )

Financial Risk

Market Risk ( Interest rate / Currency / Equity )

Credit Risk

Liquidity Risk

Operational Risk

Capital Management

Liability Adequacy Test

Impairment of Reinsurance Assets

Loss development triangle

20

KEY ISSUES THAT NEEDS TO BE ADDRESSED

Start date Date for the opening balance sheet needs to be fixed

Amendment Amendment required to the Insurance Act / Regulations

F. Statements As per IND AS or existing basis or both

Solvency Based on existing regulations or IND AS

21

IMPACT OF IND AS 104 / IFRS ON INDIAN GEN INSURERS

Ins Contracts Not very significant

Disclosures Significant effort during the earlier years of implementation

Investments Accounting and measurement would have a big impact

LAT Segment wise LAT would impact solvency

Op Segments Companies monitor performance on their chosen segments

Solvency Would be impacted by Investments measurement / LAT

22

TERMS USED

MCA : Ministry of Corporate Affairs

DAC : Deferring of acquisition costs

LAT : Liability Adequacy Test

URR : Unexpired Risk Reserve

HTM : Held to Maturity

MTM : Mark to Market

AFS : Available for Sale

SOCE : Statement of Change in Equity

B/S : Balance Sheet